Embed Size (px)

Citation preview

University of Potsdam Department of Economic and Social Sciences

Termpaper

Regulating the International Financial System: Regulators Afoul in a Complex Network

Jana K. Ollmann M.A. Verwaltungswissenschaft, 2nd term

Matr.-Nr.: 761654

Course: The G20, the IMF and Reforms of

the International Financial Architecture Lecturer: PD Dr. Heribert Dieter Term: Summer term 2012 Date: 31. August 2012

Content

1! Introduction ..........................................................................................................................2!2! The financial system as a complex network.........................................................................3!

2.1! Network analysis ...........................................................................................................3!2.2! Networks of financial institutions .................................................................................5!2.3! Networks of national financial systems.........................................................................6!

3! Regulating the global financial system.................................................................................7!3.1! Defining ‘regulation’ .....................................................................................................7!3.2! Past and present developments in international financial regulation ............................8!3.3! Discussion of developments in the light of findings from network analysis ..............11!

4! Conclusion..........................................................................................................................13!5! Bibliography .......................................................................................................................14!

2

1 Introduction

In his widely recognized speech to the Financial Students Association, Andrew G.

Haldane, Executive Director of the Bank of England, characterized the global financial

system as a complex, adaptive network (Haldane 2009). National financial markets and

institutions are strongly interconnected. Turmoil in one region of the network quickly affects

other regions. The global financial crisis, which started in 2007 as a US subprime mortgage

crisis, but rapidly turned into the worst financial crisis since the Great Depression of the

1930s, provides impressive evidence. Difficulties on the US subprime mortgage market

spread to debt markets. A number of financial institutions were rescued by US government

support, but in September 2008 Lehman Brothers collapsed. Panic seized financial markets.

World wide capital flows came to a sudden standstill. The capital market freeze in turn

amplified the global economy’s decline and contributed to the European sovereign debt crisis.

In the wake of the crisis, there have been many calls for a fundamental reform of

international financial regulation. Haldane’s characterization of the financial system

highlights that this reform should include a paradigmatic shift from micro- to macro-

prudential regulation. In order to stabilize the system as a whole, regulators have to consider

not only the stability of singular financial institutions but also the structure of the institutions’

interconnectedness. In this paper, I review the findings of hitherto network analyses of the

financial system and discuss their policy implications. I consider two strands of literature:

Studies belonging to the first strand predominantly use mathematical modeling to examine the

relation between the interconnectedness of financial institutions and the risk of contagion.

Studies belonging to the second strand are based on empirical data from the BIS International

Banking Statistics and describe the structural developments of the global network of national

financial sectors (these are interconnected through cross-border bank exposures) from the

1980s onward. On the basis of these studies’ findings, I discuss past and present

developments in international financial regulation.

Structure

In chapter two I will firstly give a concise introduction to network analysis (2.1) and then

review hitherto network analyses in the field of finance – those that model the relation

between the interconnectedness of financial institutions and the risk of contagion (2.2) as well

as those which describe the empirical development of the interconnectedness between

national financial sectors (2.3). The goal of the second chapter is to identify the structural

properties of the financial network and the dynamics that result from these properties. The

3

implications that these characteristics have for the regulation of the global financial system

then are discussed in chapter three. The chapter first defines regulation (3.1) and then sketches

past and present developments in international regulation (3.2), which finally are evaluated in

the light of the network studies’ findings (3.3). Chapter four resumes the main findings and

points out questions for future research.

2 The financial system as a complex network

2.1 Network analysis

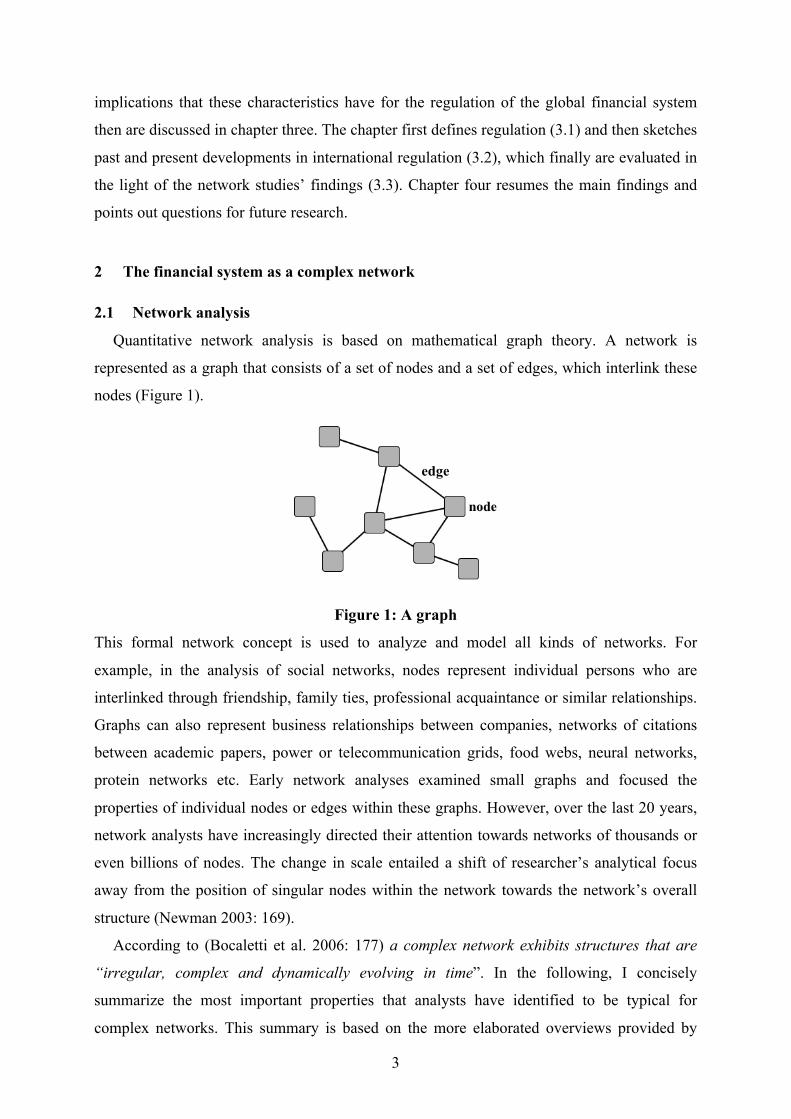

Quantitative network analysis is based on mathematical graph theory. A network is

represented as a graph that consists of a set of nodes and a set of edges, which interlink these

nodes (Figure 1).

Figure 1: A graph

This formal network concept is used to analyze and model all kinds of networks. For

example, in the analysis of social networks, nodes represent individual persons who are

interlinked through friendship, family ties, professional acquaintance or similar relationships.

Graphs can also represent business relationships between companies, networks of citations

between academic papers, power or telecommunication grids, food webs, neural networks,

protein networks etc. Early network analyses examined small graphs and focused the

properties of individual nodes or edges within these graphs. However, over the last 20 years,

network analysts have increasingly directed their attention towards networks of thousands or

even billions of nodes. The change in scale entailed a shift of researcher’s analytical focus

away from the position of singular nodes within the network towards the network’s overall

structure (Newman 2003: 169).

According to (Bocaletti et al. 2006: 177) a complex network exhibits structures that are

“irregular, complex and dynamically evolving in time”. In the following, I concisely

summarize the most important properties that analysts have identified to be typical for

complex networks. This summary is based on the more elaborated overviews provided by

edge

4

Newman (2003) and Bocaletti et al. (2006). A key structural property of a network is its

degree distribution. The degree of a node is defined as the number of its direct connections to

other nodes. The degree distribution P(k) of a network designates “the probability that a node

chosen uniformly at random has degree k” (Newman 2003: 165). Classical mathematical

models of random networks, which dominated the analysis of large networks until 1998, are

based on the assumption that the degree of nodes is distributed according to a binominal or

Poisson distribution. Meanwhile, a number of empirical studies of large-scale networks have

shown that real world networks significantly deviate from this expectation. Empirical large-

scale networks are usually characterized by hierarchical structures and often exhibit power

law tails. The degree distribution is highly inhomogeneous. A few nodes (the hubs) are linked

to many other nodes, while the majority of nodes are only poorly connected. Moreover, the

node degrees in most real world networks are strongly correlated. Most social networks for

example are assortative, i.e. the higher a node’s degree, the higher is the average degree of its

neighbors. Typically, the paths between any two nodes are relatively short (small world

property). Nodes cluster, i.e. where two nodes are connected to the same third node, they are

likely to also be connected to each other (transitivity). Furthermore, nodes form communities,

sub-groups within which the density of edges is higher than between them. These properties

affect the networks’ functional robustness and responses to external perturbations such as

random failures or targeted attacks. For example, the destructive effects of targeted deletions

of nodes are much greater in scale-free networks than in networks exhibiting a Poisson-

shaped degree distribution, while the effects of random breakdowns are less harmful.

Structural properties furthermore affect the internal dynamics of a network’s emergence and

evolution.

In a previous, broader review of network analyses in the field of economics and finance,

Allen and Babus (2009) pointed out that models of complex networks are more mechanical

than those models, which take a micro perspective and focus the position of singular nodes

within small networks. The latter models in general are based on game theory and assume that

the formation of a link between two agents (e.g. financial institutions) is the result of the

agents’ rational decision. This requires agents to know how the network they belong to is

structured and how this affects their individual gains. Models of complex networks take a

macro perspective. They examine complex processes on which individual agents may have

only limited influence.

5

2.2 Networks of financial institutions

There have been several attempts to conceptualize financial systems as networks and to

identify the financial networks’ structural characteristics. This subchapter reviews studies that

model how the interconnectedness between financial institutions relates to the risk of financial

contagion in the case that one bank or a few banks fail. One of the first and best known

network analyses in the field is that of Allen and Gale (2000) who construct a network of four

hypothetical banks, which exchange deposits on the interbank market in order to insure

against liquidity shocks. They demonstrate that within complete networks, with each bank

having exposures to all other banks, the shock hitting one bank affects all the other banks, but

evenly and modestly so that the shock can be absorbed. Incomplete networks are less resilient.

Freixas et al. (2000) model the case that one bank within a network of banks becomes

insolvent and come to similar conclusion. Leitner (2005) reemphasizes the stability-enhancing

effect of interconnectivity, arguing that interconnected private agents may be willing to bail

out other agents in order to prevent the network’s collapse.

The model of Allen and Gale (2000) has been refined and enhanced. Lagunoff and Schreft

(2001) as well as Cifuentes et al. (2005) point to indirect financial relationships through

similar portfolios as a further channel of contagion. Nier et al. (2008) examine financial

contagion as a function of bank capitalization, the size of cross-exposures, and

interconnectedness. They detect an M-shaped relationship between interconnectedness and

financial stability: If connectivity is very low, an increase raises the likelihood of contagion.

In more interconnected networks, additional links may increase or decrease risk, but if

connectivity is sufficiently high, further increase in connectivity is associated with

strengthened system resilience. Gai and Kapadia (2010) adopt more complex techniques from

the literature on complex epidemic networks. They find that greater connectivity reduces the

risk of contagion, but also that financial networks, which exhibit a Poisson-shaped degree

distribution, have a robust-yet-fragile tendency, i.e. the probability of contagion is low, but

the effect of contagion if it occurs is devastating.

However, these models may underestimate negative externalities of interconnectedness.

Dasgupta (2004) as well as Iyer and Peydro-Alcalde (2007)1 highlight that depositors base

their decision whether to store or to withdraw funds on information about banks, which are

interlinked with their bank. Thus, turmoil at one bank may lead to bank runs at other banks.

Caballero and Simsek (2009) demonstrate that complexity raises the cost of information 1 The study of Iyer and Peydro-Alcalde (2007) is the only study within this section, which is based on empirical data. The authors analyze the behavior of depositors in the case of a large Indian banks failure.

6

gathering, especially if the system is under stress. Banks therefore become increasingly

reluctant to buy assets, withdraw from loan commitments and illiquid positions as tensions

rise. According to the model provided by Battiston et al. (2009) an increase in connectivity

only stabilizes the system if initial connectivity is low, because high connectivity is associated

with bankruptcy cascades (the system may absorb the bankruptcy of one bank, but in the

aftermath a second bankruptcy may trigger the collapse of the already weakened system) as

well as financial accelerators (pro-cyclicality of leverage and the hardening of credit

conditions in the case of financial stress).

Overall, the findings on whether an increase of interconnectedness enhances the stability of

the financial system are mixed. The answer depends on the initial level of interconnectedness,

the distribution of edges as well as on negative side effects that are associated with an

increase in interconnectedness.

2.3 Networks of national financial systems

This subchapter reviews analyses, which describe the structural properties of the global

network between national financial systems as well as how these properties have changed

since the 1980s. These analyses are based on data from the BIS International Banking

Statistics. Links represent cross-border bank exposures. The BIS International Banking

Statistics do not contain data on financial institutions other than banks such as hedge funds or

security companies. One important factor that contributed to the global financial crisis –

complex channels of securitization thus is not traced by the studies presented in this chapter.

Since 1985 cross-border bank exposures have augmented. Previous to the global crisis, the

network of national financial systems experienced an increase in connectivity and a decrease

in average path length. It became more clustered and centralized (Hattori and Suda 2007,

Kubelec and Sá 2010). New banks entered the global network, but existing banks were the

main drivers of the increase in interconnectedness (Hale 2011). The interconnectedness

rankings, especially those of borrower countries, were relatively volatile. Minoiu and Reyes

(2011) state that the financial network’s connectivity tends to fall during and after systemic

banking crises and sovereign debt crises. This is confirmed by the findings of Chinazzi et al.

(2012) according to which the networks’ density decreased after 2008.

Kubelec and Sá (2010) find that the global financial network is characterized by a power

law structure: It consists of a small number of global financial centers (hubs) and a large

periphery that includes not only developing countries but also most advanced industrialized

countries. The financial hubs form rich clubs, i.e. they are more linked among themselves

than to periphery-countries (Chinazzi et al. 2012). Chinazzi et al. (2012) explain that the

7

decrease of interconnectedness after the financial crisis’ outbreak resulted from creditor

countries reducing their number of links – especially the number of links to periphery

countries. This implies that the network became even more asymmetric after the crisis.

Garratt et al. (2011) apply the model of Battiston et al. (2009) and find that since the 1980s

the risk of contagion within the international financial system has steadily increased and that

this trend is set to continue (similarly Chan-Lau 2010). Simulations show that if the US or the

UK were hit by a banking crisis, this crisis would spread to all other countries. Most countries

would also be affected, if Germany, Turkey or Russia experienced a banking crisis (Degrysen

et al. 2009). All in all, contagion is more widespread in geographical proximity (Degrysen et

al. 2009) and more devastating when it originates in creditor countries and flows upstream via

borrowing countries’ funding channels (Cihak et al. 2011). Cihak et al. (2011) as well as

Chinazzi et al. (2012) construct models on the basis of BIS data, which confirm an M-shaped

relationship between interconnectedness and financial-stability (compare to Nier et al. 2007,

Gai and Kapdia 2010 in the previous subchapter).

3 Regulating the global financial system

Chapter two reviews hitherto network analyses in the field of finance and thereby

conveys a picture of the financial network’s structures and dynamics. This chapter discusses

the implications that these structures and dynamics have for the regulation of the financial

system. But first, subchapter 3.1 defines the term of regulation, which has been used in many

different ways (for an overview see Levi-Faur 2010). Subchapter 3.2 sketches how the modes

of financial regulation have changed since the Bretton Woods conference of 1944. The

historical development of regulation also relates to the evolvement of those network

structures, which are described in chapter 2.3, and therefore has to be taken into account when

discussing the policy implications of these structures. This discussion takes place in

subchapter 3.3.

3.1 Defining ‘regulation’

The pre-crisis literature on international financial regulation has focused on explaining the

creation and strengthening of international prudential standards in the context of rapidly

globalizing financial markets (Helleiner and Pagliari 2011: 179). In the current policy

discourse as well, the term ‘regulation’ is often used as a synonym for the setting of formal

standards. This definition excludes more informal mechanisms of (self-)regulation, which are

essential to systemic thinking. Within this paper, I therefore adopt a multi-tired definition of

regulation from (Baldwin et al. 2012: 3). Regulation as a specific set of commands (1) refers

8

to authoritative rule-setting, which is often accompanied by the establishment of some

administrative agency for monitoring and enforcing compliance. For example capital

requirements, which are enforced through European Banking Authority (EBA), belong to this

form of regulation. In a more broad sense, regulation as deliberate state influence (2)

designates all state activities that are designed to steer social or business behavior. Under this

definition, economic incentives (e.g. taxes or subsidies) or the strategic supply of information

through government authorities are deemed regulatory. In its widest sense regulation denotes

all forms of social or economic influence (3), which may be exercised by the state, but also by

private actors. According to the latter definition, e.g. the gate-keeping practices of scientific

journals constitute regulation.

The distinction between micro- and macro-prudential regulation has already been

mentioned in the introduction. Micro-prudential regulation focuses the stability of individual

financial institutions. Macro-prudential regulation seeks to stabilize the financial system as a

whole. Thus, while macro-prudential regulation “recognizes the importance of general

equilibrium effects”, micro-prudential regulation is “partial equilibrium in its conception”

(Hanson et al. 2011: 3).

Different mechanisms of convergence may lead to the international harmonization of

financial regulation. Regulatory harmonization may result from formal agreements between

national governments or majority decisions within international organizations. Alternatively,

market pressures or soft power coercion may force countries to adopt or abandon specific

regulatory measures. Finally, regulators may engage in a transnational process of policy

learning and best practice exchange (Holzinger and Knill 2005).

3.2 Past and present developments in international financial regulation

The Bretton Woods system

In July 1944, representatives of 44 nations gathered in Bretton Woods, New Hampshire, to

establish a monetary and fiscal order for the post-war era. Under what became known as the

Bretton Woods system, international financial regulation had a macro-prudential character

and was based on formal agreements that set out broad principles for monetary and fiscal

steering: Governments committed to ensure currency convertibility for current account

payments and to keep exchange rates stable. The International Monetary Fund (IMF) and the

World Bank were created to supervise member state compliance with the core principles and

to provide international lending. The Bretton Woods agreements explicitly permitted national

capital controls. Thus, national governments strengthened restrictions on capital flows and

implemented a number of further regulatory measures such as interest rate caps and banking

9

standards (type 1 and 2 regulation). Although, the techniques and patterns of regulation varied

among countries, reflecting differences in state structure as well as traditional state-society

relations (Lütz 2004), national governments in general made use of the whole spectrum of

regulatory instruments and adopted rather interventionist policies (Eichengreen 2007).

The post-Bretton Woods era

In 1973, the adjustable pegg exchange rate system of Bretton Woods was replaced by a

system of floating exchange rates. National governments deregulated financial markets and

abolished capital controls. The UK and the US were leading this liberalization movement, but

other countries soon followed more or less voluntarily. Economic pressure and soft power

coercion, e.g. through the conditionality of IMF lending, often left economically weak

countries no other choice but to liberalize their economic and financial policies. Neo-liberal

thinking became dominant among scientists and national regulators as well as IMF officials

(type 3 regulation).

An increase in the frequency of financial crises forced governments to consider a

reregulation of the financial sector. In reaction to the collapse of the German Herstatt Bank in

1974, which caused losses at many other banks around the word, central bank governors of

the G10 created the Basel Committee on Banking Supervision (BCBS). The BCBS’ aim was

to foster cooperation on bank-supervisory measures as well as to develop supervisory

standards and guidelines (type 1 and 3 regulation). However, central bank governors did not

produce any significant agreement until 1988 when they adopted the Basel Accord. The Basel

Accord defines capital requirements for banks, which serve as an assurance for the case that

borrowers default on loans. The Basel Accord is non-binding, but has been implemented into

binding national laws. It was revised for the first time in 2004. While the calculation of capital

requirements was based on simple standardized risk categories under Basel I, it is based on

the risk assessments of the banks themselves or of private rating agencies under Basel II.

Supervisory bodies similar to the BCBS were also established for the securities and

insurance sector, the International Organization of Securities Commissions (IOSCO) in 1983

and the International Association of Insurance Supervisors (IAIS) in 1994. These bodies have

formulated principles, guidelines and standards, but these have not gained the same legal

status as the Basel Accords. In 1999, G7 financial ministers and central bank governors

founded the Financial Stability Forum (FSF) as a venue that would bring together regulators

from the different sector-specific international groupings of regulators and committees of

central bank experts. Furthermore, a variety of standards emerged from private, professional

associations such as the International Accounting Standard Board or expert committees like

10

the Committee on Payment and Settlement Systems. Monitoring reports and research papers

were regularly published by the IMF, the World Bank, the Bank for International Settlements

(BIS) and the Organization for Economic Cooperation and Development (OECD) (for an

overview see Brummer 2012: chapter 2 or Baxter 2010). All in all, international financial

regulation in the post-Bretton Woods era typically took place within transnational networks of

regulators as well as practitioners and consisted of informal policy coordination and standard-

setting (type 1 and 3 regulation). It had a micro-prudential focus and neglected possible side

effects on the financial system as a whole.

Present developments

In reaction to the outbreak of the global financial crisis in 2008, politicians declared the

reform of the financial regulatory framework to be the top priority on the global policy

agenda. Then President of the European Council Nicolas Sarkozy even called for a second

Bretton Woods conference. Soon thereafter, the leaders of G20 countries assembled in

Washington DC to outline a reform agenda. They agreed to strengthen international financial

standards and to foster cooperation between national regulators (type 1 and 3 regulation), to

widen the membership of the FSF and international standard-setting bodies such as the BCBS.

The expansion of these bodies was quickly implemented, but soon conflict arose about

standard-setting. As no agreement was found at the international level, the EU announced to

implement stricter rules on hedge funds, derivatives and rating agencies unilaterally and to

make them obligatory for foreign firms entering the European market (host-country

regulation). This marked a turn in the European approach to financial regulation, which

previously had been an authority-sharing arrangement according to which the EU permitted

the entrance of US companies if they complied with US standards (home-country regulation)

(Pagliari 2012). By now, other countries have followed the European example (IOSCO 2011)

and the outrage of US government officials that followed the announcement has calmed

down. The US has adopted unilateral rules (Dodd Frank Act), which in some areas such as the

regulation of derivatives are more stringent than current EU regulations, and is now planning

to add the so-called Volcker Rule that prohibits commercial banks to engage in proprietary

trading or to invest in private equity funds.

The second revision of the Basel Accord (Basel III) has been the only notable

advancement of international standards since the crisis. It tightens the previous capital

definition, strengthens capital requirements and introduces counter-cyclical capital buffers,

leverage as well as liquidity requirements. Especially stringent capital requirements apply to

“systemically important institutions” – a concept which has been introduced to give the

11

accord a more macro-prudential orientation. But, the implementation of Basel III has already

evoked new tensions between EU and US regulators (Véron 2012).

In sum, international efforts to reform the system of financial regulation after the recent

crisis did not result in a comprehensive new financial order like the Bretton Woods

agreements did in the 1940s (compare Helleiner 2010). Nonetheless, some important

developments can be observed: Emerging economies are now better represented within

international forums of financial regulation. However, the shift towards more unilateral, host-

country regulation indicates that the international level is losing importance in comparison

with the national level. So far national governments have focused type 1 regulation, but type 2

regulation has been discussed as well (e.g. the EU as well as the US are considering the

introduction of a transaction tax). Policy-makers agree that there is a need for more macro-

prudential regulation, but this has so far only resulted in a lot of talk about “systemic

relevance”.

3.3 Discussion of developments in the light of findings from network analysis

The liberalization of financial regulation after the breakdown of the Bretton Wood system

enabled the increase of financial cross-border transactions and thus the evolvement of an

increasingly dense global financial network exhibiting those characteristics described in

chapter 2.3. Those countries, which were leading the liberalization movement, are the core

centers of today’s financial network. A number of scholars have argued that the US

dominance in financial markets is declining and that this decline has been accelerated through

the financial crisis. Helleiner and Pagliari (2011) argue that by introducing host-country

regulation unilaterally the EU demonstrated its “power-as-autonomy”. The EU proved that it

is able to act independently from US influence. Oatley et al. (forthcoming) however argue that

the US is likely to remain the dominant power in financial markets and in financial regulation

because of its “network power”. The US experienced net capital inflows during the crisis and

its borrowing costs remained low despite its large deficit. Oatley et al. (forthcoming: 17)

reason: “Positive feedback might keep a prior hegemon at the center of the global financial

network even as its initial advantage in terms of capabilities diminishes”. The findings of

Chinazzi et al. (2012) provide strong evidence for the existence of positive feedback

mechanisms in financial networks. This means that those countries, which have been financial

centers in the post-Bretton Woods era, are likely to also dominate financial markets after the

global crisis. It furthermore implies that the financial network will continue to be asymmetric.

The greatest risk of contagion emanates from few financial centers. If these centers

experience a financial crisis, the shock will damage the whole system. In the same time, the

12

centers are less vulnerable to shocks that emanate from peripheral countries (Cihak et a. 2011,

Degrysen 2009). Financial centers – especially the US and the UK – therefore have little

incentive to decrease their interconnectedness, which would reduce the global system’s

asymmetry. This might explain the US’ outrage in reaction to the EU’s move towards a host-

country principle in financial regulation and its reluctance to global regulatory efforts (even

though it is adopting national measures directed at the internal stabilization of its national

financial system).

Peripheral countries face the question whether it is best for the stability of their respective

national system to increase or decrease its interconnectedness. The studies reviewed in

chapter 2.2 provide no clear answer on whether interconnectedness increases or decreases

stability. Cihak et al. (2011) argue that banking systems, which are not very connected to the

global banking network, could reduce their vulnerability if they got engaged in more financial

cross-border relations. In any case, they have to become less dependent on links to financial

centers. Therefore it is sensible for them to adopt policies independently from central

countries.

Instead of edges, regulatory measures in the post-Bretton Woods era focused singular

nodes. Through the setting of prudential standards, regulators tried to stabilize individual

banks. A number of the reviewed models confirm that capital and especially liquidity buffers

are essential for the stability of financial networks (Cifuentes et al. 2005, Nier et al. 2008,

Caballero and Simsek 2009, Gai and Kapadia 2010). However, the first Basel Accord

provides an example of how standards may increase the risk of contagion. A number of

scholars (e.g. Levinson 2010) have pointed to the fact that the risk assessment scheme under

Basel I underestimated the risk of government bonds as well as the risk of mortgages. Many

banks thus hold too little capital to cover losses from mortgages when the bubble on the real

estate market burst. The findings of Lagunoff and Schreft (2001) as well as Cifuentes et al.

(2005) point out that if the harmonization of risk assessments leads to the harmonization of

portfolios, the number of channels of contagion increases. Therefore greater diversity in risk

assessment enhances system stability.

The findings of Gai and Kapadia (2010) highlight the problem of long-tails. If a large

percentage of the network’s edges are concentrated with a few nodes, the banks, which are

represented by these nodes, constitute a threat to the whole network. With the concept of

“systemically important banks”, regulators intend to address this problem. But Basel III again

is focused on nodes, while the problem of long-tails lies with the distribution of edges. The

13

network can only be stabilized if its asymmetry is reduced. It is stable, when systemically

important banks do not exist.

The authors of those studies presented in chapter 2.2 also address the issue of bailouts.

However, their opinions in this respect differ. Freixas et al. (2000) favor an orderly

liquidation, Iyer and Peydro-Alcalde (2009) stress that it might be necessary to bailout a bank

to save the whole system. Leitner’s (2005) perspective that if governments function as

mediators, banks will rescue each other, is especially optimistic. From a network-perspective

whether a bailout is necessary or not certainly depends on the bank’s centrality within the

network. The problems of moral hazard that come along with bailouts are not an issue of

network analyses and have been discussed elsewhere. But, what can be learned e.g. from the

analysis of Iyer and Peydro-Alcalde (2009) is that in some cases, it might be necessary to

close down weak banks even if they are liquid in order to cut channels of contagion. Freixas

et al. (2000) make a similar argument. They emphasize that such a close down enhances

market discipline. In any case, as Caballero and Simsek (2009) argue, an increase in the

system’s transparency is crucial in order to reduce the risk of contagion.

4 Conclusion

Network analyses point out the need to focus regulatory efforts more on edges than on

nodes. This aspect has not yet been fully recognized in policy discourses even though the

notion of macro-prudential regulation has gained prominence. While there is no definite

answer to the question which level of interconnectedness is ideal, hitherto network analyses

demonstrate that the asymmetry of the financial system threatens its stability. For peripheral

countries it is important to gain independence from central countries. A diversification of

regulation might reduce the asymmetry within the network. However, at this point crucial

questions remain unanswered: How does the degree of policy convergence relate to the

interconnectedness of financial systems? How does the position of a countries’ financial

sector within the global financial network affect the countries’ power-as-influence and its

power-as-autonomy? How strong are informal mechanisms of policy convergence?

Analyses of complex networks taking a macro perspective can inform researchers and

policy makers about weaknesses in the network structure. Once policy makers have that

information, they have to decide on how to use it. Their decision will depend on their own

position within the network. At this point researchers have to switch from the macro- to the

micro-perspective, which models games on networks. Building the bridge between these two

14

perspectives is one of the main challenges for researchers who are concerned with the

governance of complex networks.

5 Bibliography

Allen, B., and A. Babus. 2009. "Networks in Finance." In The network challenge: strategy, profit, and risk in an interlinked world, eds. P. Kleindorf, Y. Wind and R. Gunther. Philadelphia: Wharton School Publishing. Allen, F., and D. Gale. 2000. Financial Contagion. Journal of Political Economy 108 (1): 1-33. Baldwin, R., M. Cave, and M. Lodge. 2012. Understanding Regulation. Theory, Strategy, and Practice. 2 ed. Oxford, New York: Oxford University Press. Battiston, S., D.D. Gatti, M. Gallegati, B.C. Greenwald, and J.E. Stiglitz. 2009. Liaisons Dangereuses: Increasing Connectivity, Risk Sharing, and Systemic Risk. NBER Research Papers 15611.

Baxter, L.G. 2010. "Internationalization of Law: The „Compex“ Case of Bank Regulation." In The Internationalization of Law: Legistlature, Decision-Making. Practice and Education, eds. W. Van Caenegem and M. Hiscock. Chaltenham: Edward Elgar. Bocaletti, S., V. Latora, Y. Moreno, M. Chavez, and D.U. Hwang. 2006. Complex networks: Structure and dynamics. Physicy Report 424: 175-308. Brummer, C. 2012. Soft Law and the Global Financial System: Rule-Making in the Twenty-First Century. Cambridge: Cambridge University Press. Caballero, R., and A. Simsek. 2009. Complexity and Financial Panics. NBER Research Papers 14997. Chan-Lau, J.A. 2010. Balance Sheet Network Analysis of Too-Connected-to-Fail Risk in Global and Domestic Banking Systems. International Monetary Fund. Chinazzi, M., DG. Fagiolo, J.A: Reyes, and S. Schiavo. 2012. Post-Mortem Examination of the International Financial Network. URL: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1995499 (Accessed 16 August 2012).

Cifuentes, R., G. Ferrucci, and H.S. Shin. 2005. Liquidity Risk and Contagion. Journal of European Economic Association 3 (2-3): 556-566.

Cihak, M., S. Munoz, and R. Scuzzarella. 2011. The Bright and the Dark Side of Cross-Border Banking Linkages. International Monetary Fund Working Paper 11 (86).

Dasgupta, A. 2004. Financial Contagion through Capital Connections: A Model of the Origin and Spread of Bank Panics. Journal of European Economic Association 2 (6): 1049-1084.

Degrysen, H., M. Ather Elahu, and M.F. Penas. 2009. Cross-border exposure and financial contagion. European Banking Center Discussion Paper 2009-2.

Eichengreen, B. 2007. Globalizing Capital. Princeton: Princeton University Press. Freixas, X., B. Parigi, and J.C. Rochet. 2000. Systemic Risk, Interbank Relations and Liquidity Provision by the Central Bank. Journal of Money, Credit and Banking 32 (3): 611-638.

Gai, P., and S. Kapadia. 2010. Contagion in Financial Networks. Bank of England Working Paper 383.

15

Garratt, R.J., L. Mahadeva, and K. Svirydzenka. 2011. The contagious capacity of the international banking network: 1985-2009. UCSB Working Paper (submitted to Elsevier). Haldane, A.G. 2009. Rethinking the financial network. Speech delivered at the Financial Student Association in Amsterdam on 28 April 2009. Bank of England. Hale, G. 2011. Bank Relationships, Business Cycles, and Financial Crises. NBER Working Paper 17356. Hanson, S.G., A.K. Kashypa, and J.C. Stein. 2011. A Macroprudential Approach to Financial Regulation. Journal of Economic Perspectives 25 (1): 3-28. Hattori, M., and Y. Suda. 2007. Developments in a Cross-Border Bank Exposure "Network". Bank of Japan Working Paper Series 07-E-21. Helleiner, E. 2010. A Bretton Woods moment? The 2007-2008 crisis and the future of globale finance. International Affairs 86 (3): 619-636. Helleiner, E., and S. Pagliari. 2011. The End of an Era in International Financial Regulation? A Postcrisis Research Agenda. International Organization 65: 169-200. Holzinger, K., and C. Knill. 2005. Causes and conditions of cross-national policy convergence. Journal of European Public Policy 12 (5): 775-796. IOSCO. 2011. Regulatory Implementation of the Statement of Principles Regarding the Activities of Credit Rating Agencies. Technical Committee of the International Organization of Securities Commissions.

Iyer, R., and J.L. Peydro-Alcalde. 2007. The Achilles’ Hell of Interbank Markets: Financial Contagion Due to Interbank Linkages. University of Amsterdam Working Paper.

Kubelec, C., and F. Sá. 2010. The Geographical Composition of National External Balance Sheets: 1980-2005. Bank of England.

Lagunoff, R., and L. Schreft. 2001. A Model of Financial Fragility. Journal of Economic Theory 99: 220-264.

Leitner, Y. 2005. Financial Networks: Contagion, Commitment, and Private Sector Bailouts. Journal of Finance 60 (6): 2925-2953.

Levi-Faur, D. 2010. Regulation & Regulatory Governance. Jerusalem Papers in Regulation & Governance Working Paper No.1 (February 2010).

Levinson, M. 2010. Faulty Basel. Foreign Affairs 89 (2): 76-88. Lütz, S. 2004. Convergence within National Diversity: The Regulatory State in Finance. Journal of Public Policy 24 (2): 169-197. Minoiu, C., and J.A. Reyes. 2011. A network analysis of global banking:1978-2009. International Monetary Fund Working Paper 11(74). Newman, M.E.J. 2003. The Structure and Function of Complex Networks. SIAM Review 45 (2): 167-256. Nier, E., J. Yang, T. Yorulmazer, and A. Alentorn. 2008. Network models and financial stability. Journal of Economic Dynamics and Control 31: 2033-2060. Oatley, T., W.K. Winecoff, A. Pennock, and S. Bauerle Danzmann. forthcoming. The Political Economy of Global Finance: A Complex Network Model. Perspectives on Politics. Pagliari, S. 2012. A Wall Around Europe? The European Regulatory Response to the Global Financial Crisis and the Turn in Transatlantic Relations. Journal of European Integration. DOI: 10. 1080/ 07036337.2012.689830.

16

Véron, N. 2012. "The European debate on bank capital is not just about Europe," VOX Research-based policy analysis and commentary from leading economists. URL: http://voxeu.org/article/european-debate-bank-capital-not-just-about-europe (Accessed 16 August 2012).