Embed Size (px)

Citation preview

Report No. 10079-CE

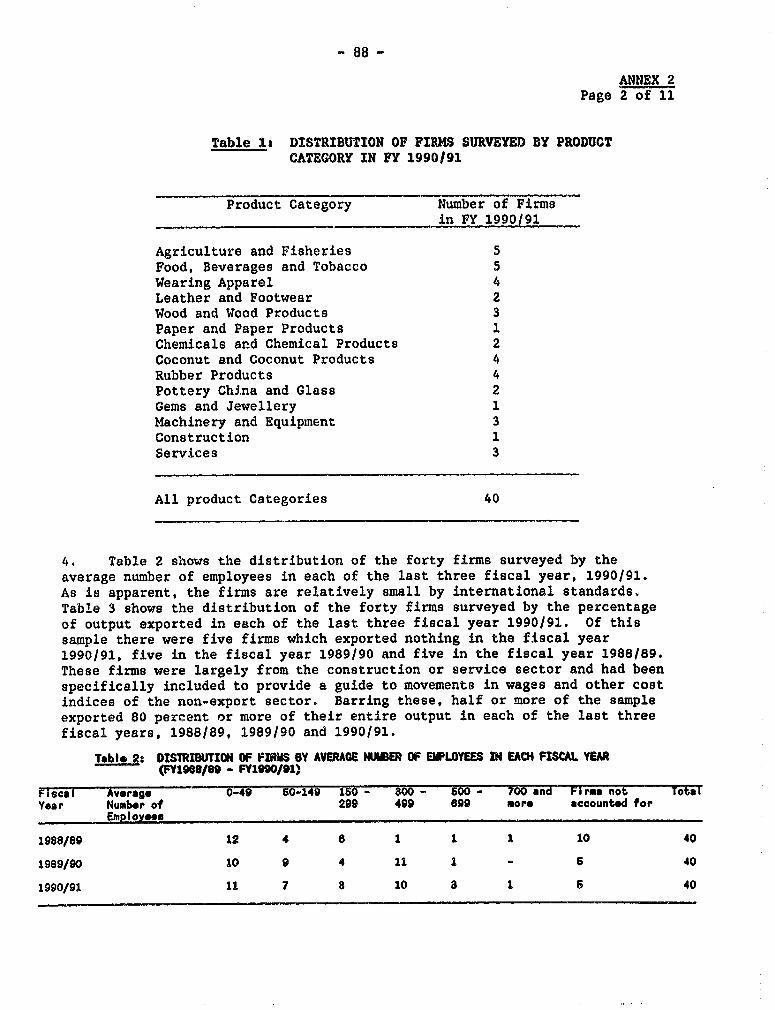

Sri LankaStrengthened Adjustment for Growthand Poverty ReductionJanuary 8, 1992

Country Operations, Industry & Finance Division MICROFICHE COPY

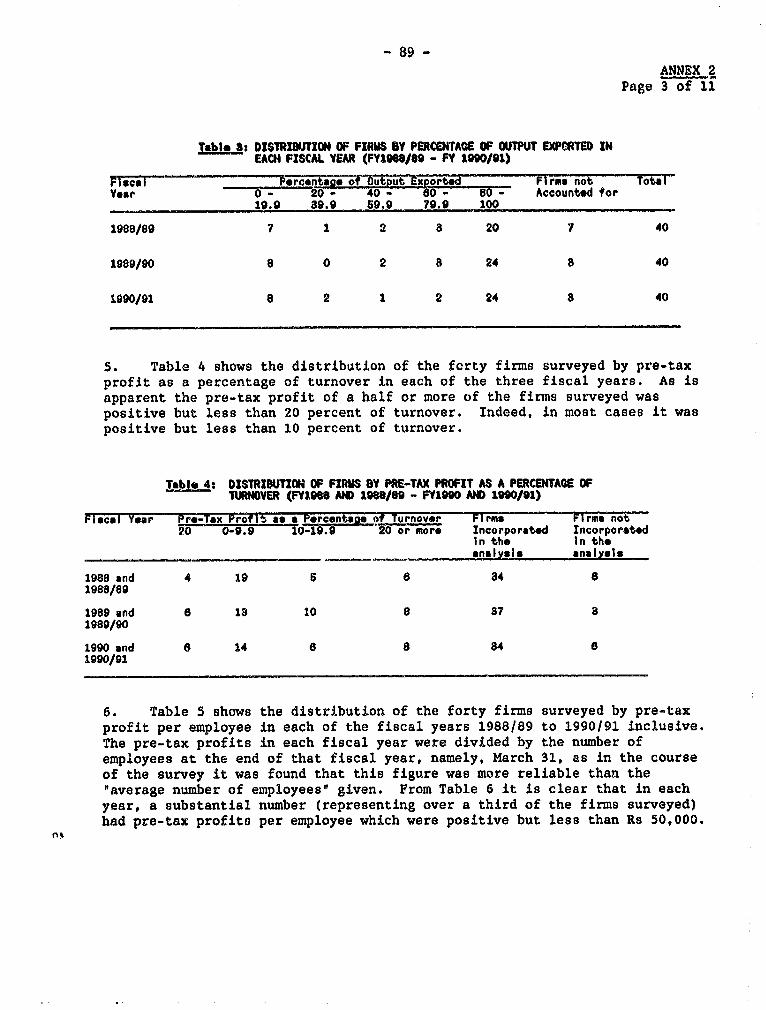

South Asia Country Department IIIReport No. 10079-CE Type: (ECO)

FOR OFFICIAL USE ONLY SHISHIDO, / X80429 / D9091/ ASICO

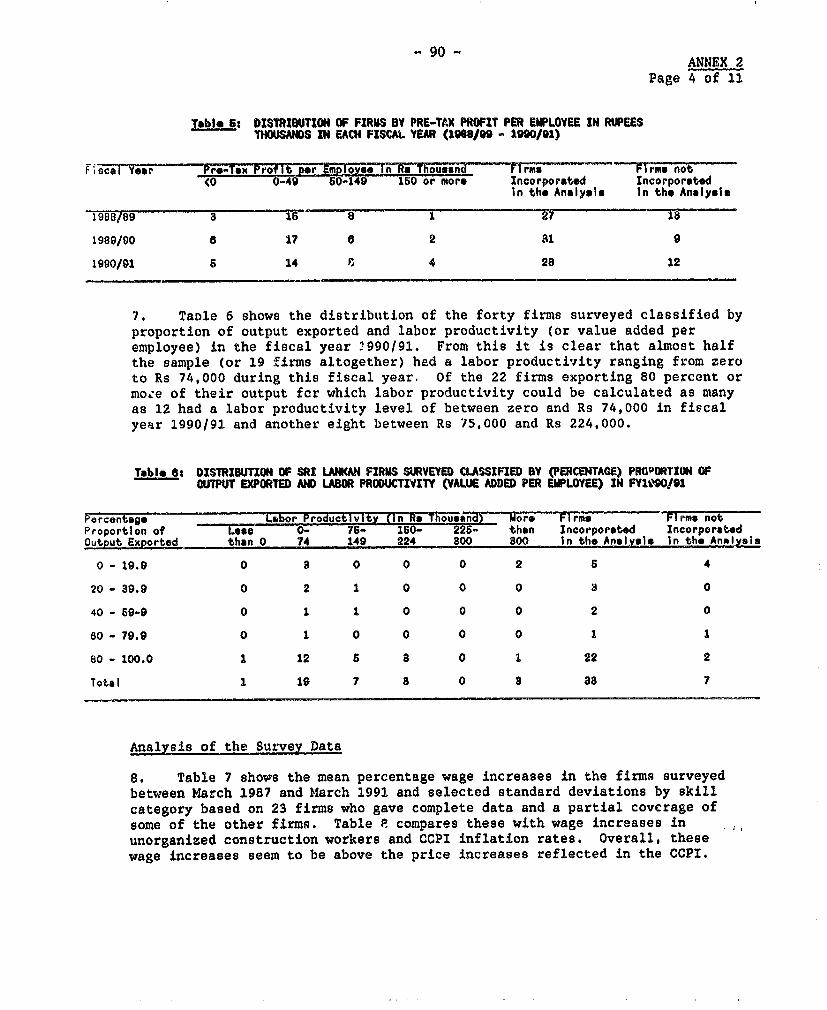

6~

Document~ of the World Ban'k

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. Its contents may nototherwise

be disclosed without World Bank Authorizati,n.

19>,9 ,, J . .. '~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~4

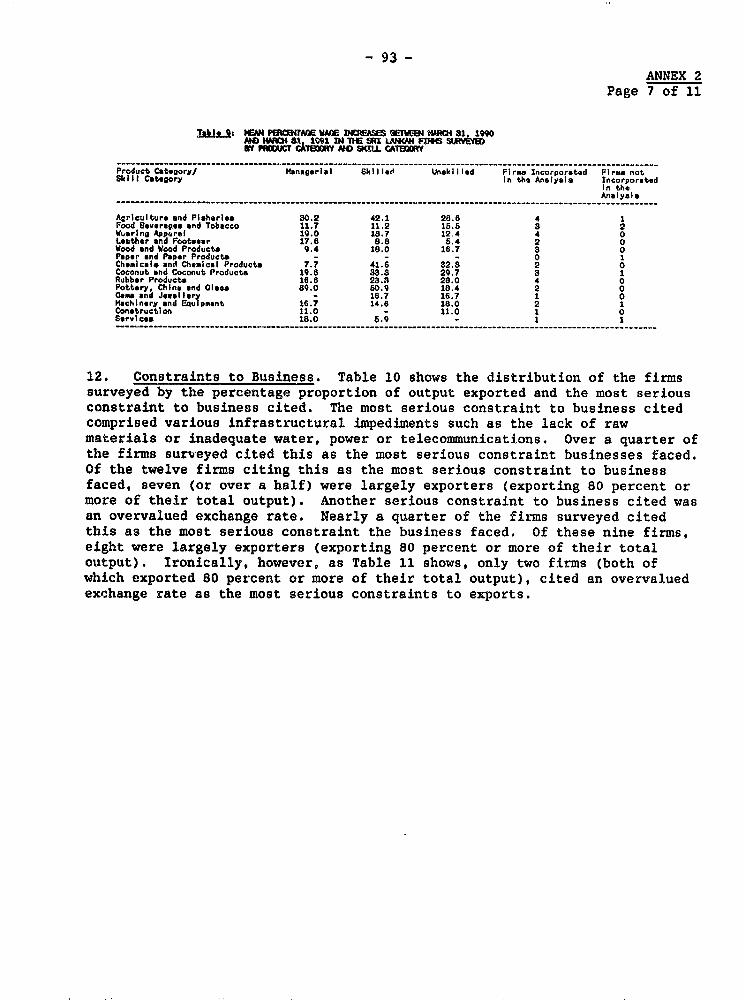

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

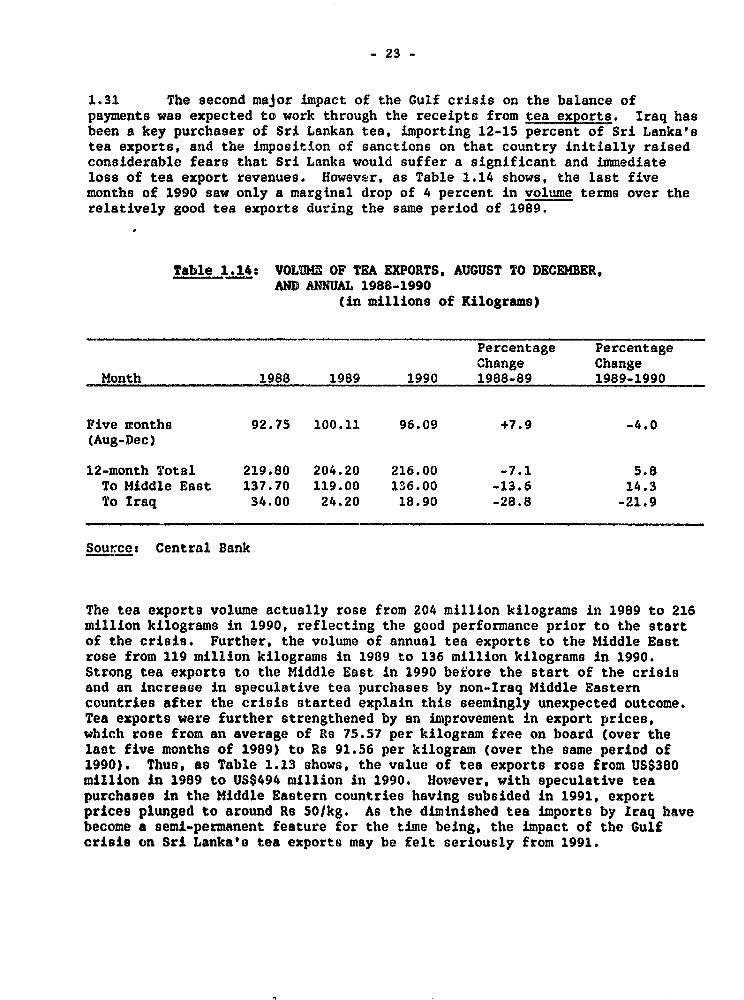

utho

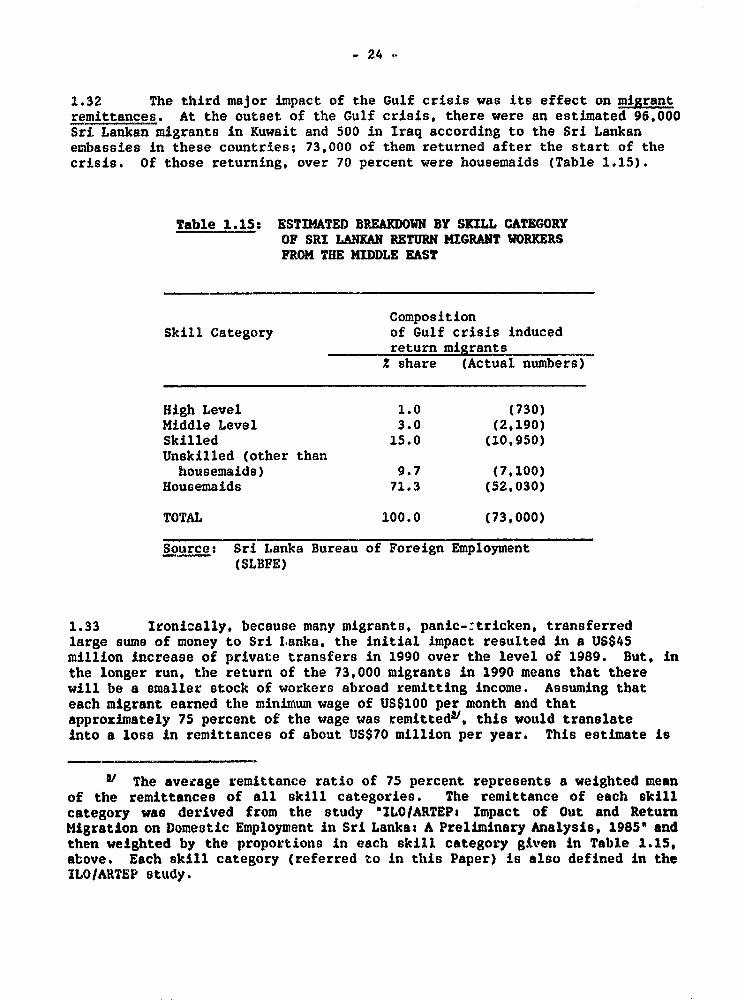

rized

Pub

lic D

iscl

osur

e A

utho

rized

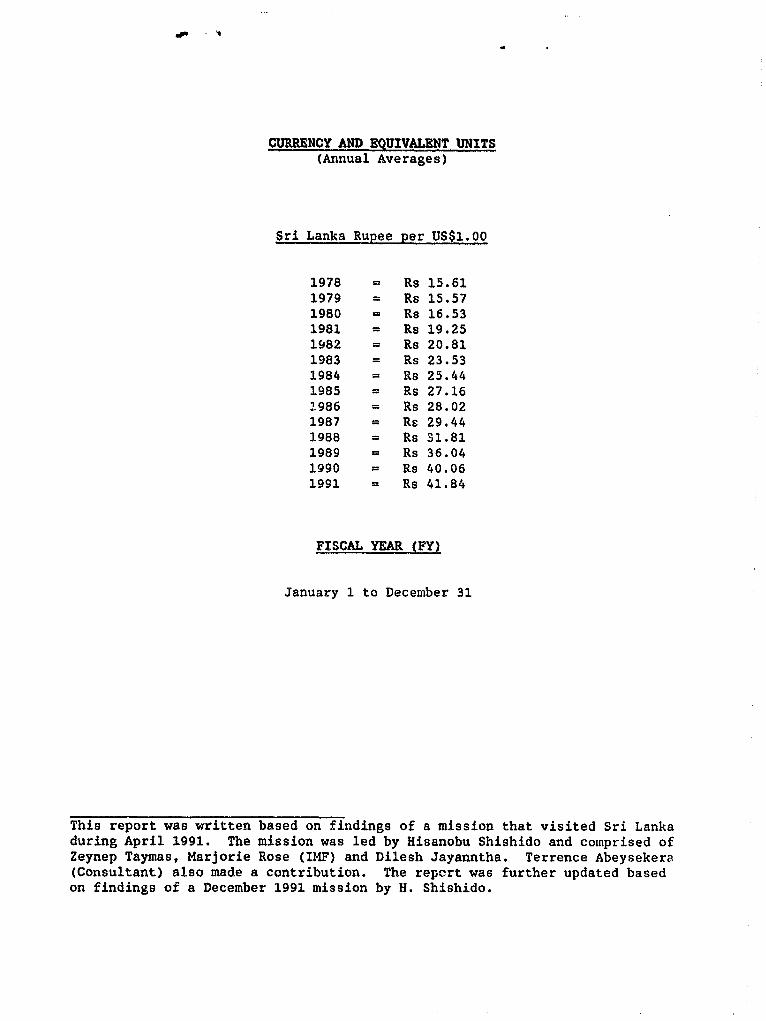

CURRENCY AND EQUIVALENT UNITS(Annual Averages)

Sri Lanka Rupee per US$1.00

1978 = Rs 15.611979 = Rs 15.571980 = Rs 16.531981 = Rs 19.251982 = Rs 20.811983 = Rs 23.531984 - Rs 25.441985 Rs 27.161986 = Rs 28.021987 - Rs 29.441988 = Rs 31.811989 = Rs 36.041990 Rs 40.061991 = Rs 41.84

FISCAL YEAR (FY)

January 1 to December 31

This report was written based on findings of a mission that visited Sri Lankaduring April 1991. The mission was led by Hisanobu Shishido and comprised ofZeynep Taymas, Marjorie Rose (IMF) and Dilesh Jayanntha. Terrence Abeysekera(Consultant) also made a contribution. The repert was further updated basedon findings of a December 1991 mission by H. Shishido.

FOR OFFICIAL USE ONLY

List of Abbreviations and Acronyms Used

ADB - Asian Development BankAGA - Assistant Government AgentARC - Administrative Reforms Commission

BOC - Bank of Ceylon

CBSL - Central Bank of Sri LankaCCPI - Colombo Consumer Price IndexCPC - Ceylon Petroleum CorporationCTB - Central Transport BoardCWE - Cooperative Wholesale Establishment

EEC - European Economic CommunityEPZ - Export Processing Zones

FCD - Food Commissioner's DepartmentFIAC - Foreign Investment Advisory C;mmitteeFIAS - Foreign Investment Advisor:, ServiceFSP - Food Stamp Program

GCEO - Greater Colombo Economic CommissionGDP - Gross Domestic ProductGNP - Gross National ProductGOBUs - Government Owned Business Undertakings

HYV - High Yielding Varieties

IDA - International Development AssociationILO - International Labor OrganisationIMF - International Monetary Fund

JEDB - Janatha Estates Development BoardJSP - Jana Saviya ProgramJVP - Janatha Vimukthi Peramuna (Peoples' Liberation Front)

MDMP - Mid-Day Meal ProgramMPA - Ministry of Public AdministrationMPCS - Multi-Purpose Cooperative Societies

NGOs - Non-Governmental OrganizationsNIC - Newly Industrialized CountriesNSB - National Savings BankNTC - National Transportation Commission

O&M - Operation & Maintenance

PAC - Poverty Alleviation CreditPB - Peoples' BankPEs - Public Enterprises

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

- 2-

PMB - Paddy Marketing BoardPSC - Public Service Commission

RACA - Restructuring and Collection AgencyRTB - Regional Transport Board

SLBFE - Sri Lanka Bureau of Foreign EmploymentSLSPC - Sri Lanka State Plantations Corporation

/

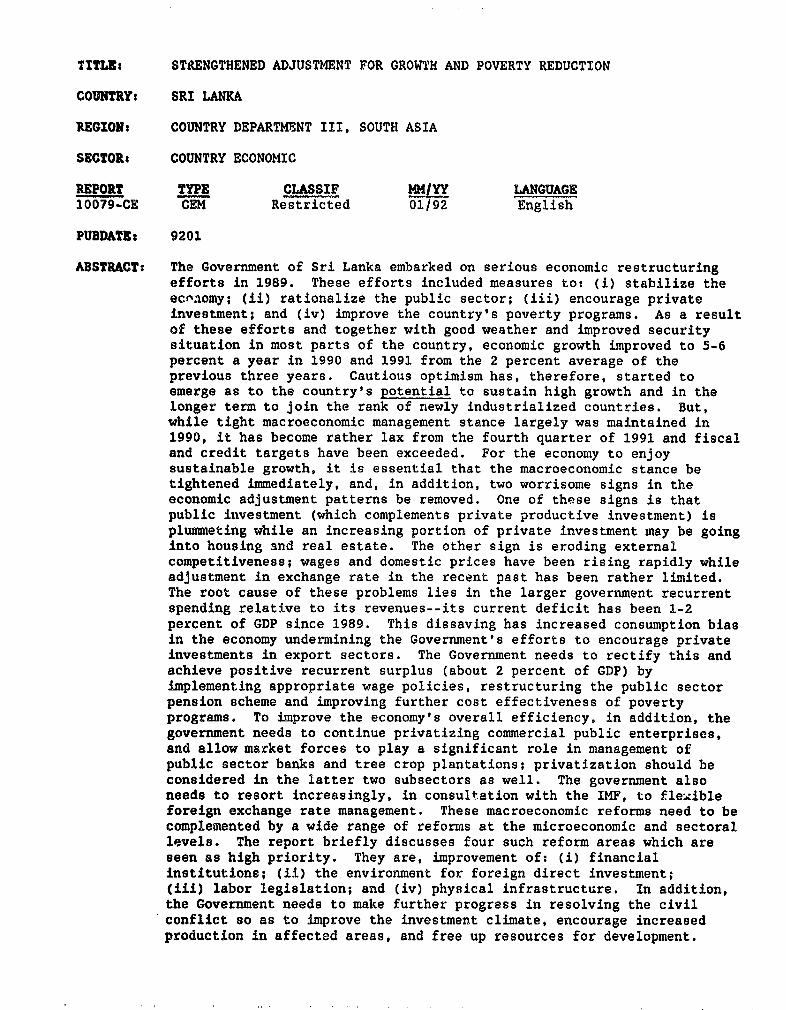

TITLE: STRENGTHENED ADJUSTMENT FOR GROWTH AND POVERTY REDUCTION

COUNTRYs SRI LANKA

REGION: COUNTRY DEPARTMENT III, SOUTH ASIA

SECTOR: COUNTRY ECONOMIC

REPORT TYPE CLASSIF MM1YX LANGUAGE10079-CE CEM Restricted 01/92 English

PUBDATE: 9201

ABSTRACT: The Government of Sri Lanka embarked on serious economic restructuringefforts in 1989. These efforts included measures to: (i) stabilize theecoaomy; (ii) rationalize the public sector; (iii) encourage privateinvestment; and (iv) improve the country's poverty programs. As a resultof these efforts and together with good weather and improved securitysituation in most parts of the country, economic growth improved to 5-6percent a year in 1990 and 1991 from the 2 percent average of theprevious three years. Cautious optimism has, therefore, started toemerge as to the country's potential to sustain high growth and in thelonger term to join the rank of newly industrialized countries. But,while tight macroeconomic management stance largely was maintained in1990, it has become rather lax from the fourth quarter of 1991 and fiscaland credit targets have been exceeded. For the economy to enjoysustainable growth, it is essential that the macroeconomic stance betightened immediately, and, in addition, two worrisome signs in theeconomic adjustment patterns be removed. One of these signs is thatpublic investment (which complements private productive investment) isplummeting while an increasing portion of private investment may be goinginto housing and real estate. The other sign is eroding externalcompetitiveness; wages and domestic prices have been rising rapidly whileadjustment in exchange rate in the recent past has been rather limited.The root cause of these problems lies in the larger government recurrentspending relative to its revenues--its current deficit has been 1-2percent of GDP since 1989. This dissaving has increased consumption biasin the economy undermining the Government's efforts to encourage privateinvestments in export sectors. The Government needs to rectify this andachieve positive recurrent surplus (about 2 percent of GDP) byimplementing appropriate wage policies, restructuring the public sectorpension scheme and improving further cost effectiveness of povertyprograms. To improve the economy's overall efficiency, in addition, thegovernment needs to continue privatizing commercial public enterprises,and allow market forces to play a significant role in management ofpublic sector banks and tree crop plantations; privatization should beconsidered in the latter two subsectors as well. The government alsoneeds to resort increasingly, in consultation with the IMF, to fle.ibleforeign exchange rate management. These macroeconomic reforms need to becomplemented by a wide range of reforms at the microeconomic and sectorallevels. The report briefly discusses four such reform areas which areseen as high priority. They are, improvement of: (i) financialinstitutions; (ii) the environment for foreign direct investment;(iii) labor legislation; and (iv) physical infrastructure. In addition,the Government needs to make further progress in resolving the civilconflict so as to improve the investment climate, encourage increasedproduction in affected areas, and free up resources for development.

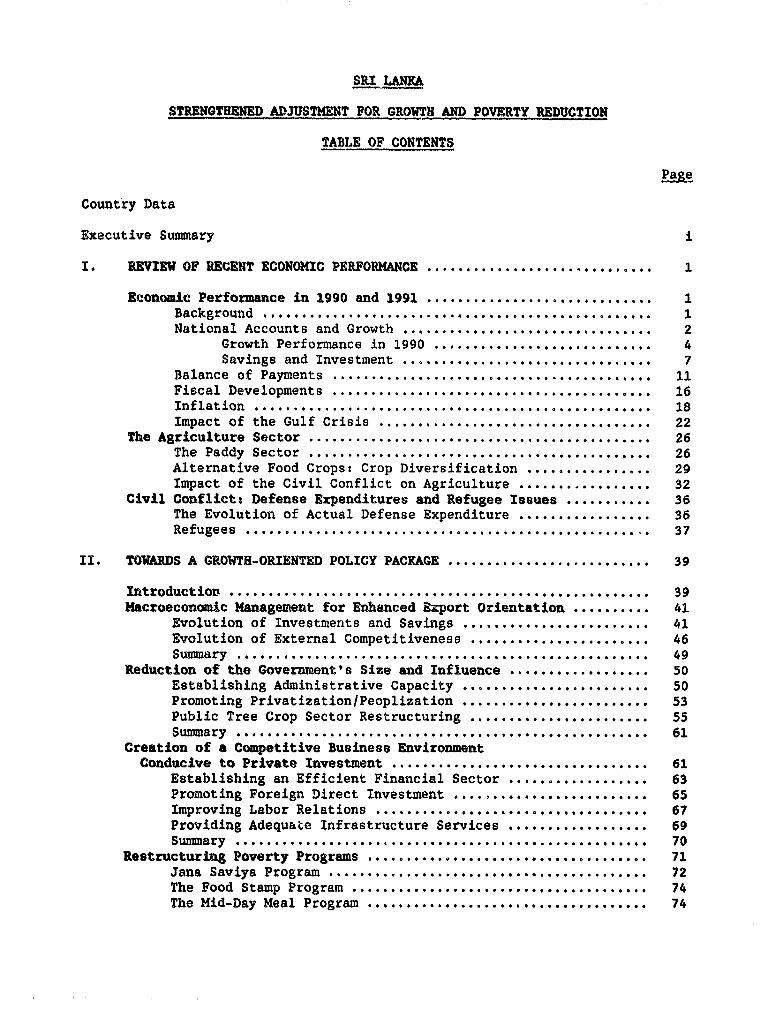

SRI LANKA

STRENGTHENED ADJUSTMENT FOR GROWTH AND POVERTY REDUCTION

TABLE OF CONTENTS

Page

Country Data

Executive Summary i

I. REVIEW OF RECENT ECONOMIC PERFORMANCE ............................. 1

Economic Performance in 1990 and 1991 .......................... 1

Background ....... ...................... 1National Accounts and Growth ................................ 2

Growth Performance in 1990 ..... ............. 4Savings and Investment ................................ 7

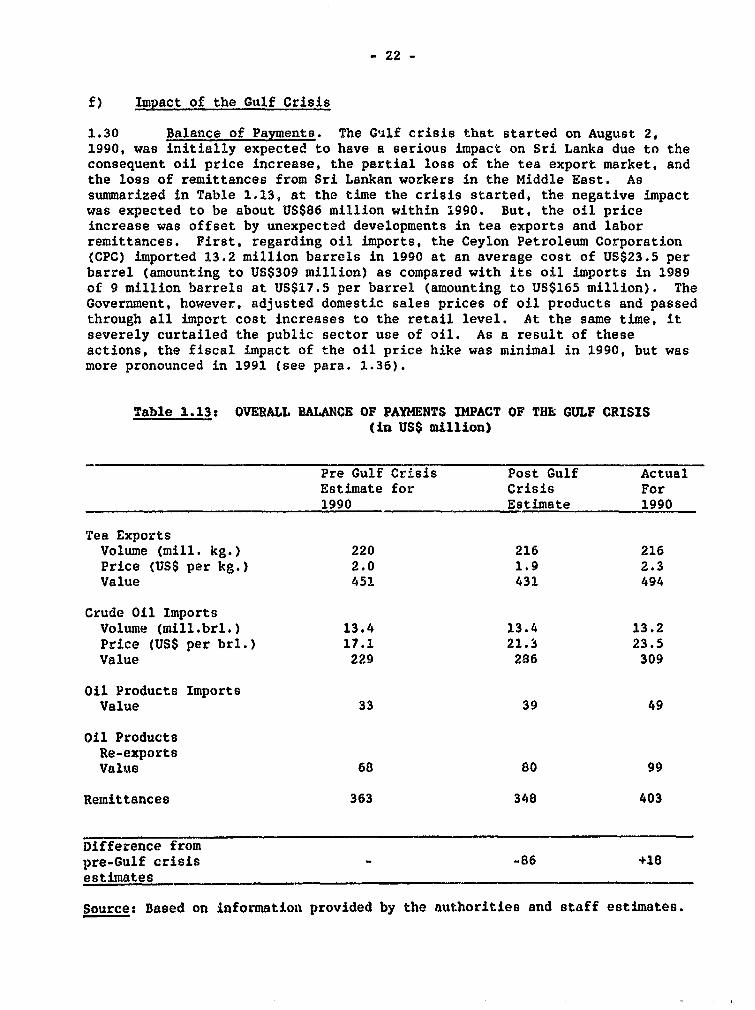

Balance of Payments ......................................... 11Fiscal Developments .................... ..................... 16Inflation ......................... .......................... 18Impact of the Gulf Crisis ................................... 22

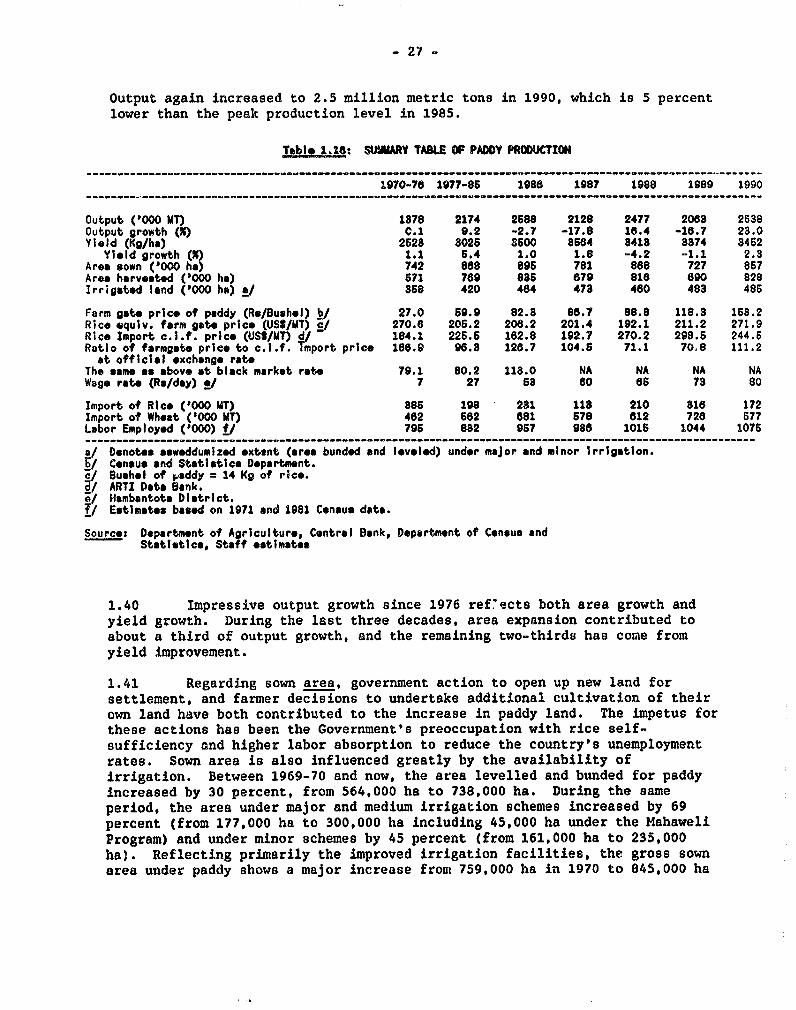

The Agriculture Sector ..................... ....................... 26The Paddy Sector ..................... ....................... 26Alternative Food Crops: Crop Diversification ....... ......... 29Impact of the Civil Conflict on Agriculture ........ ......... 32

Civil Conflicts Defense Expenditures and Refugee Issues ........... 36The Evolution of Actual Defense Expenditure ........ ......... 36Refugees ......................... ........................... 37

II. TOWARDS A GROWTH-ORIENTED POLICY PACK&GE .......................... 39

Introduction ........... 39

Macroeconomic Management for Enhanced Export Orientation ........ .. 41Evolution of Investments and Savings ......... .. ............. 41Evolution of External Competitiveness ......... .. ............ 46Summary ..... 49

Reduction of the Government's Size and Influence .. ................ 50Establishing Administrative Capacity ........... ............. 50Promoting Privatization/Peoplization ...... .................. 53Public Tree Crop Sector Restructuring ...... ................. 55Summary ................................................. 61

Creation of a Competitive Business EnvironmentConducive to Private Ilvestment ................ ................. 61

Establishing an Efficient Financial Sector ........ .......... 63Promoting Foreign Direct Investment .. ....................... 65Improving Labor Relations ................. .................. 67Providing Adequate Infrastructure Services .................. 69Summary ............................... . 70

Restructuring Poverty Programs .. ............................ 71Jana Saviya Program ............... ............... 72The Food Stamp Program .............................. 74The Mid-Day Meal Program .............................. 74

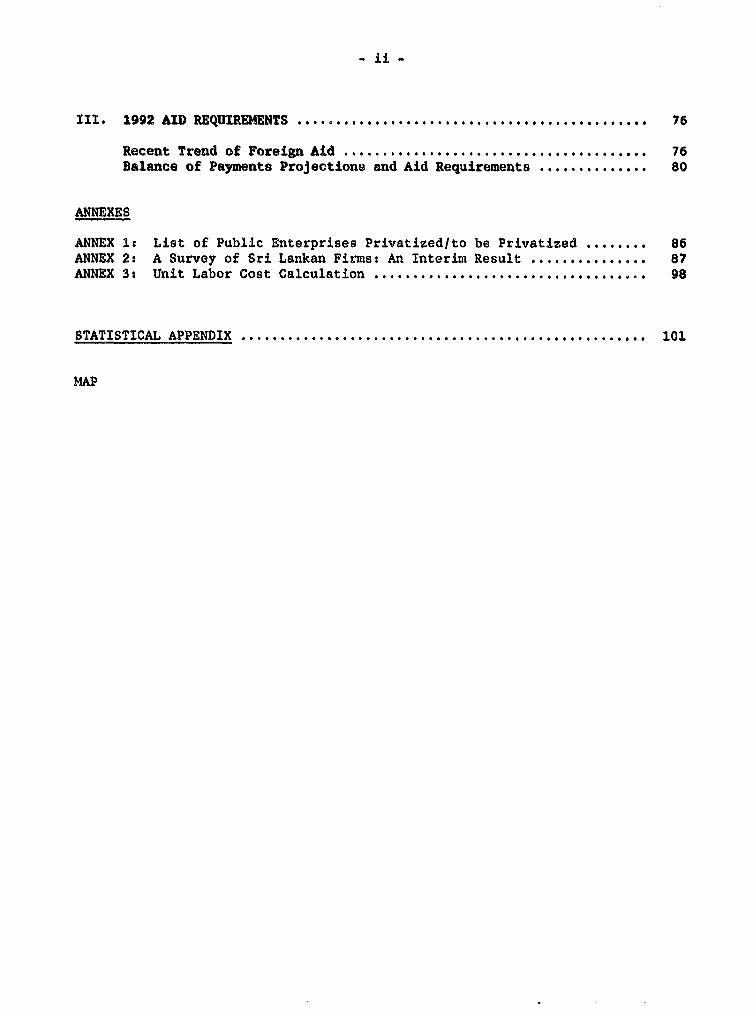

- ii -

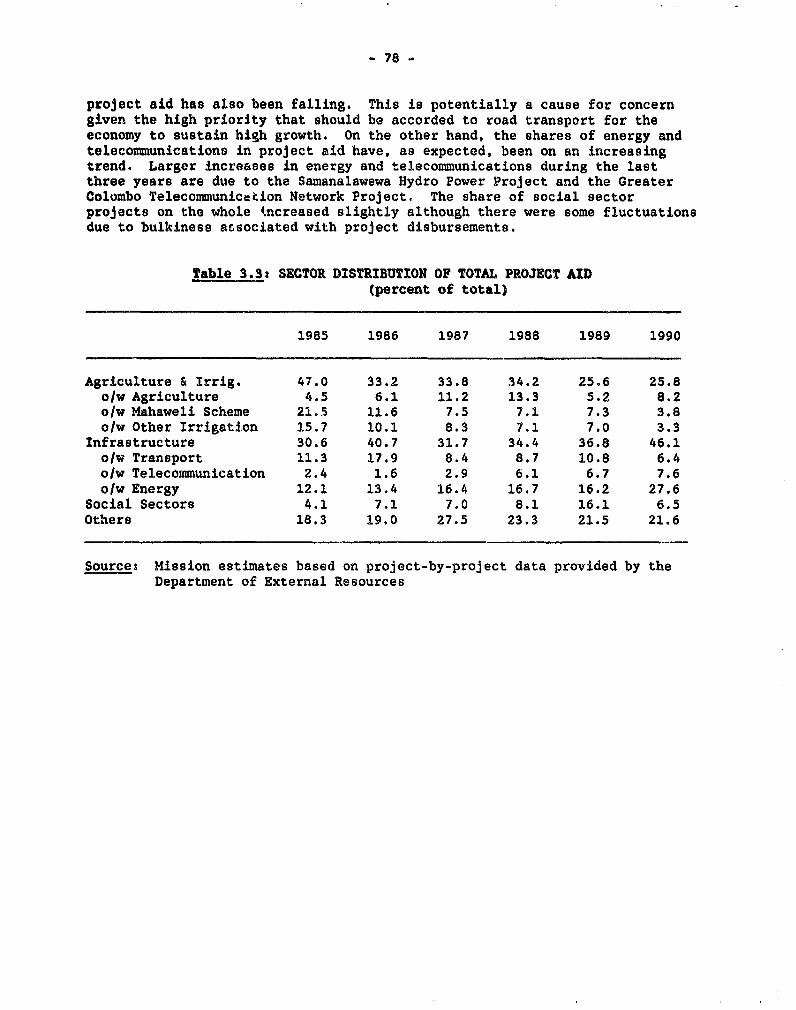

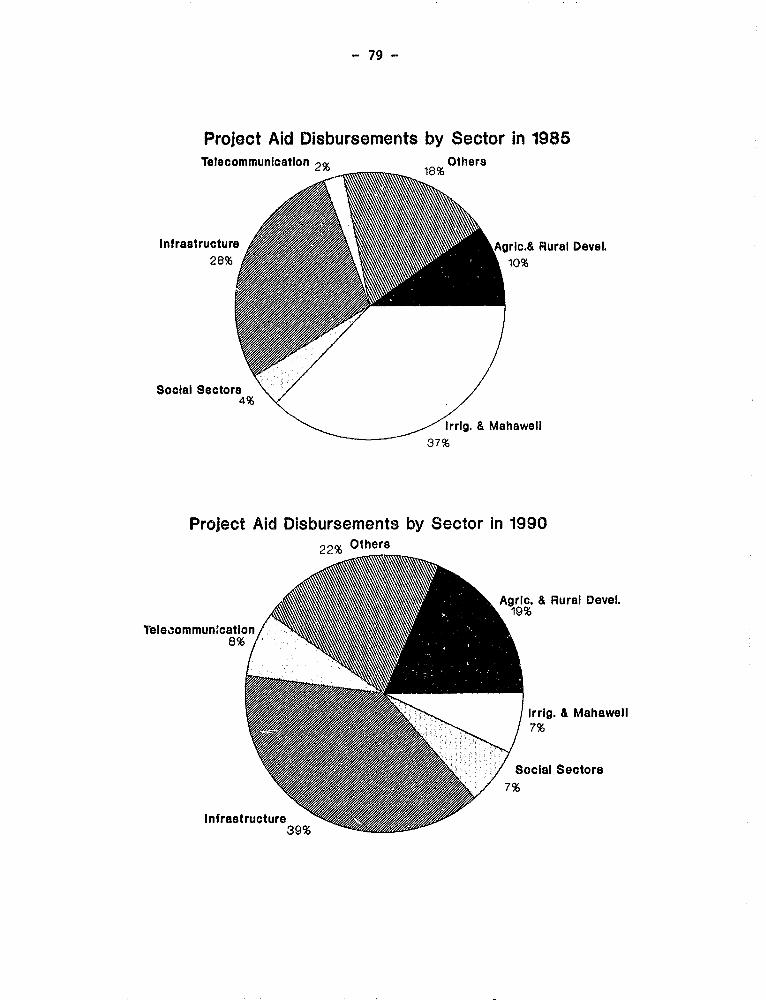

III. 1992 AID REQUIREMENTS . ..... ............................................ 76

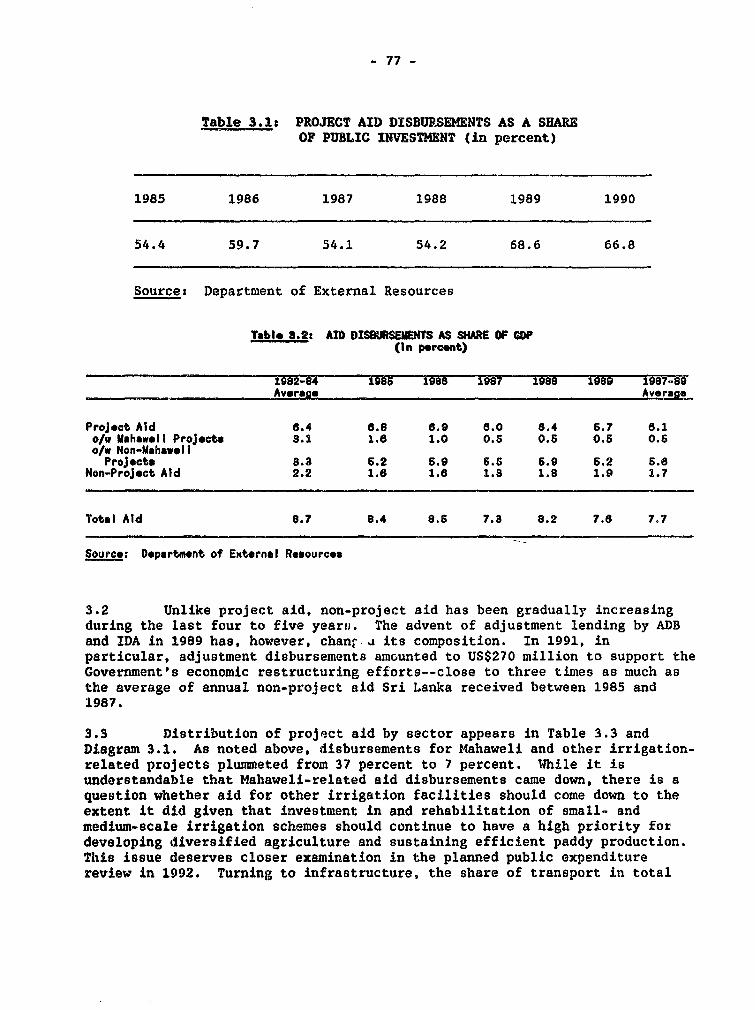

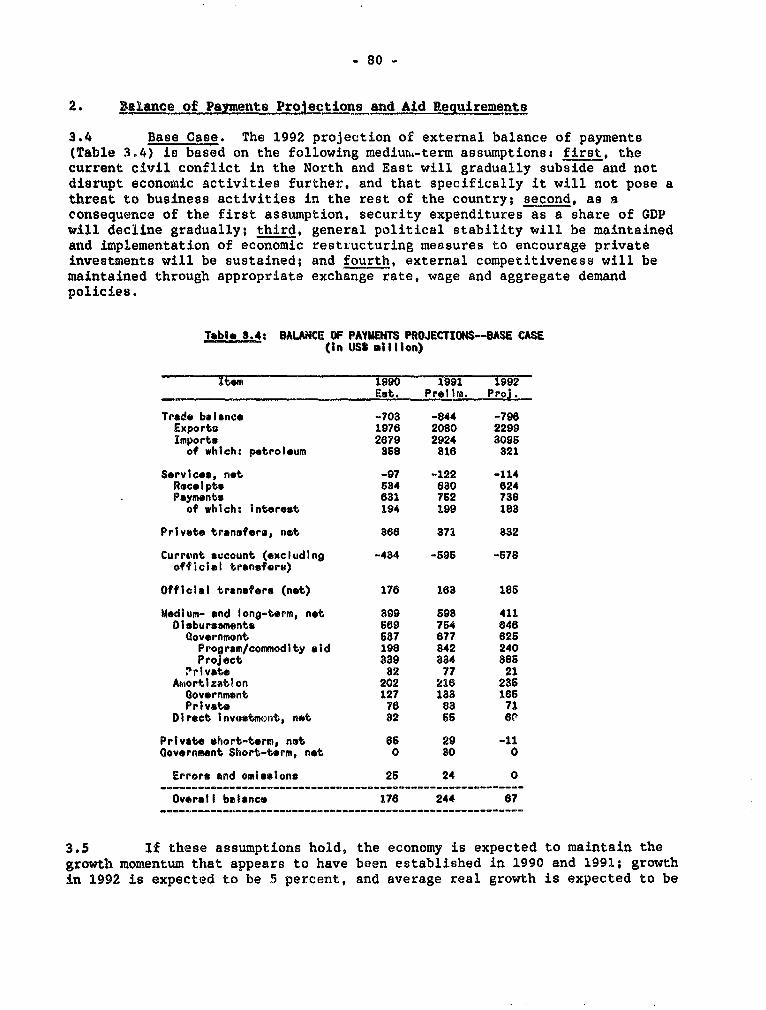

Recent Trend of Foreign Aid ....... ................................ 76Balance of Payments Projections and Aid Requirements .............. 80

ANNEXES

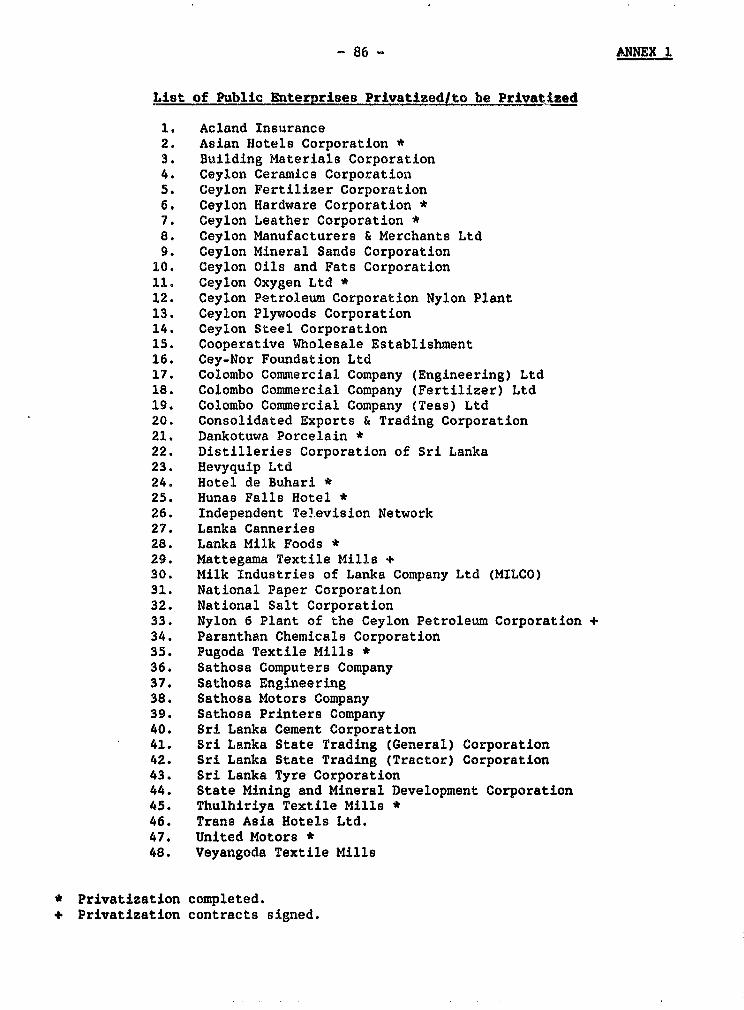

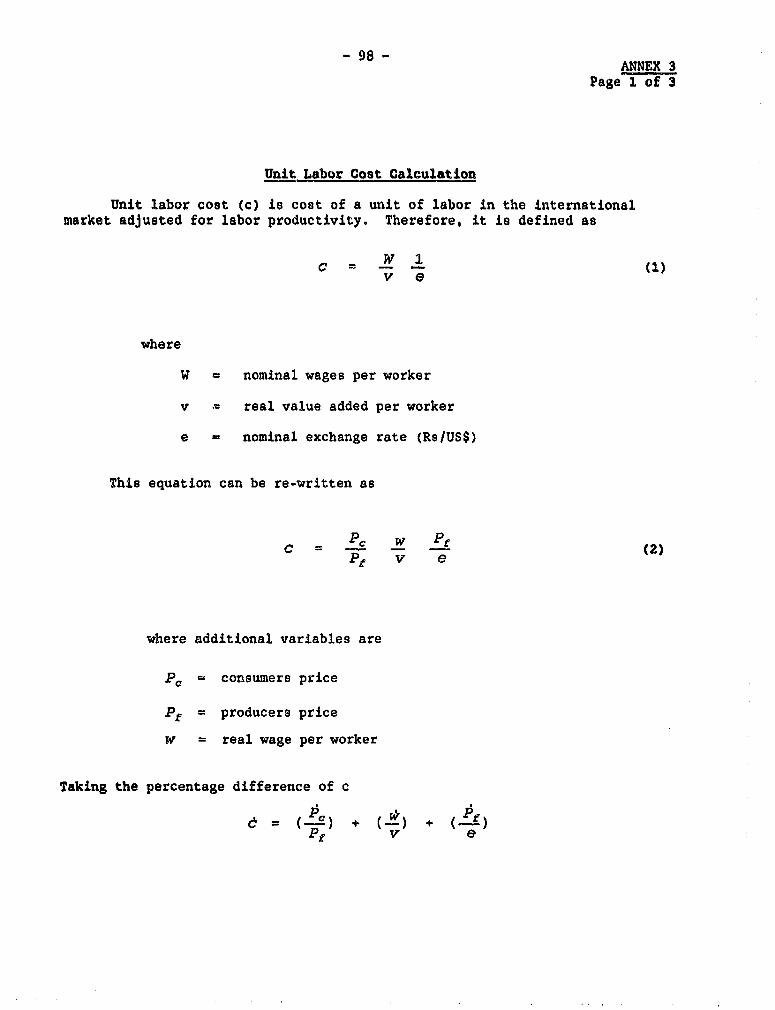

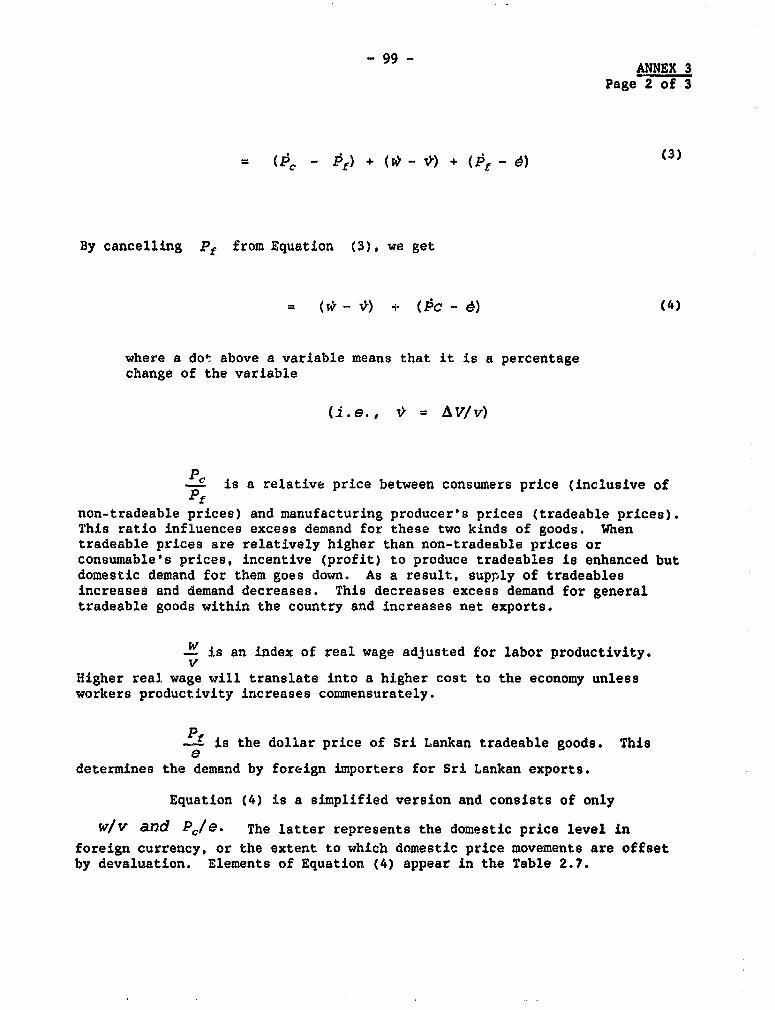

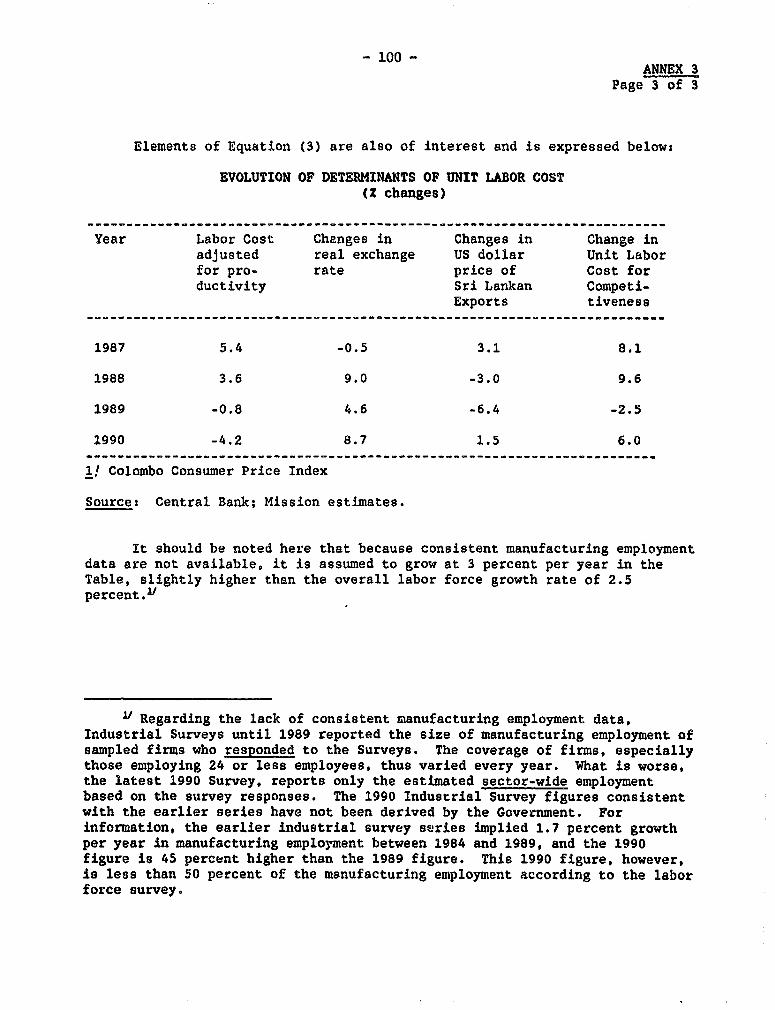

ANNEX 1: List of Public Enterprises Privatized/to be Privatized ........ 86ANNEX 2: A Survey of Sri Lankan Firms: An Interim Result ............... 87ANNEX 3: Unit Labor Cost Calculation .................................. . 98

STATISTICAL APPENDIX ...................................... 101

MAP

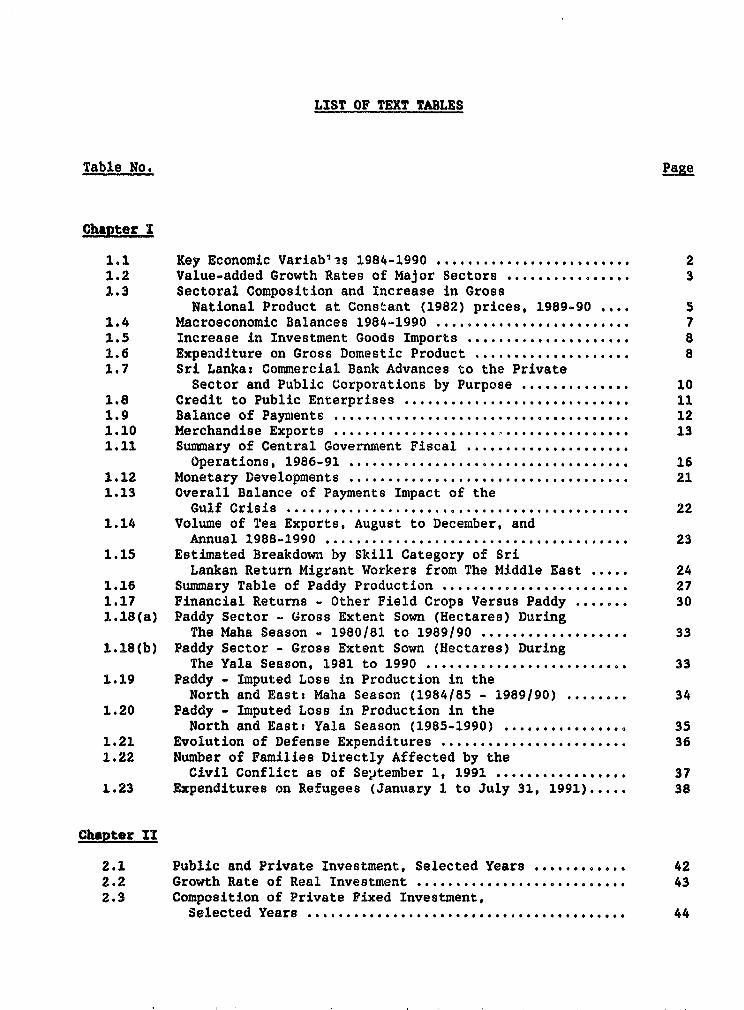

LIST OF TEXT TABLES

Table No. PaRe

Chater 1I

1.1 Key Economic Variab1 -s 1984-1990 ........... 21.2 Value-added Growth Rates of Major Sectors ............... 31.3 Sectoral Composition and Increase in Gross

National Product at Constant (1982) prices, 1989-90 .... 51.4 Macroeconomic Balances 1984-1990 .......... * .............. 71.5 Increase in Investment Goods Imports .................... . 81.6 Expenditure on Gross Domestic Product .. .................. 81.7 Sri Lanka: Commercial Bank Advances to the Private

Sector and Public Corporations by Purpose .............. 101.8 Credit to Public Enterprises ............................. 111.9 Balance of Payments ...................................... 121.10 Merchandise Exports ................. 131.11 Summary of Central Government Fiscal .

Operations, 1986-91 ........ ............................ 161.12 Monetary Developments ........ ............................ 211.13 Overall Balance of Payments Impact of the

Gulf Crisis .221.14 Volume of Tea Exports, August to December, and

Annual 1988-1990. 231.15 Estimated Breakdown by Skill Category of Sri

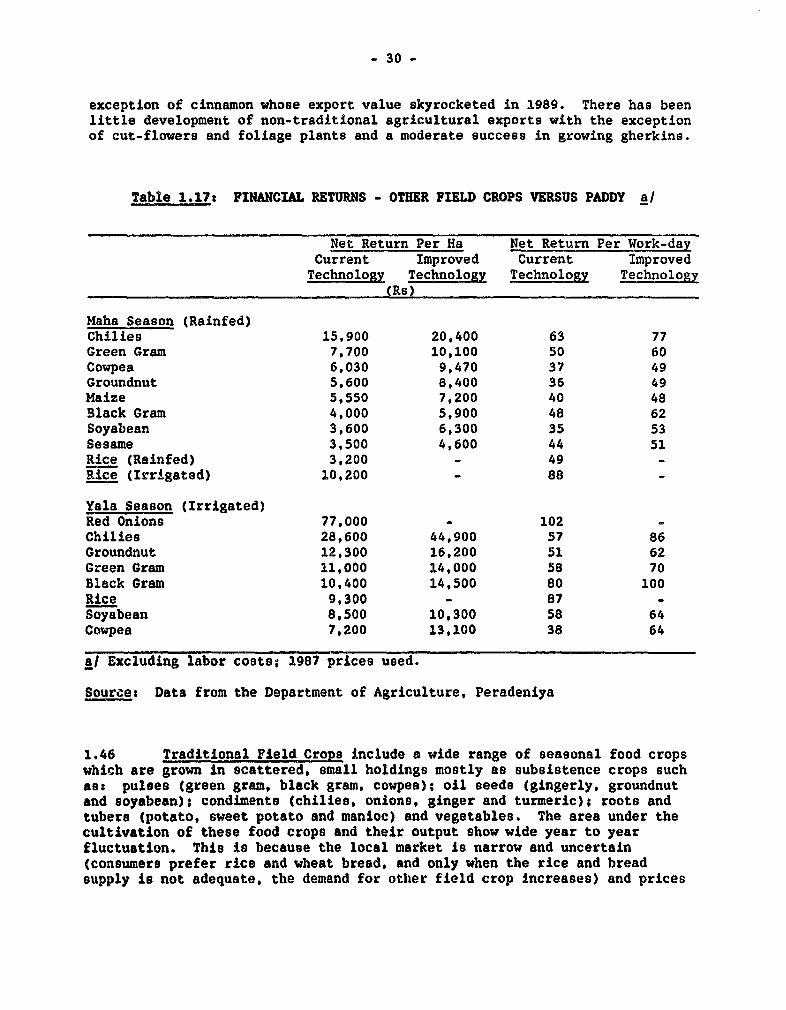

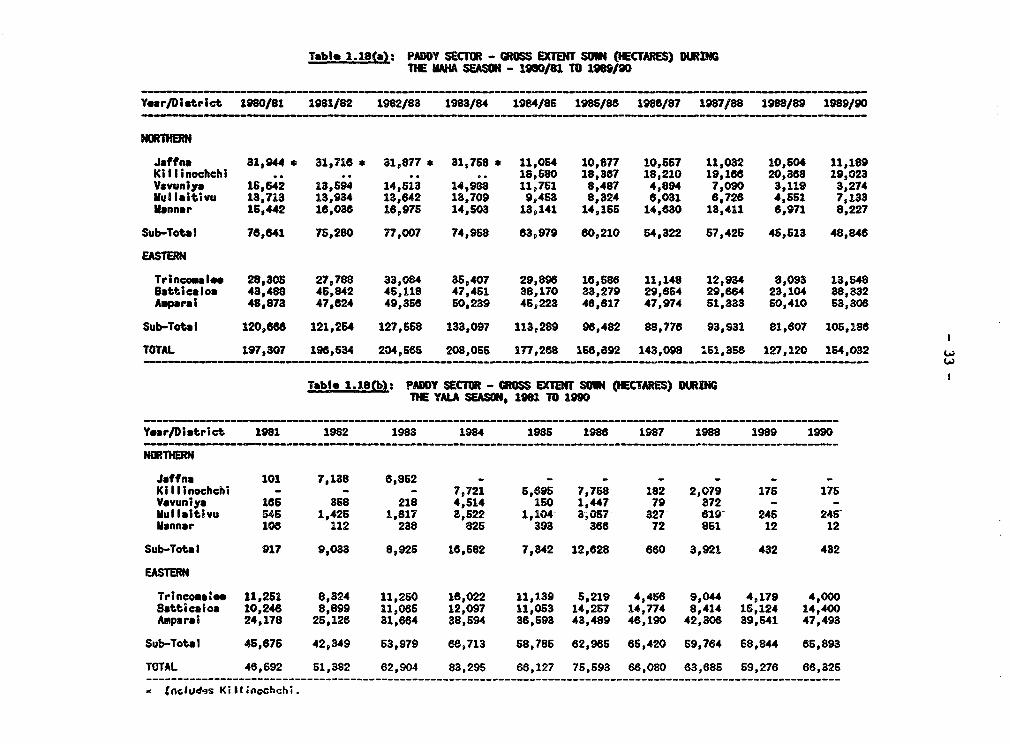

Lankan Return Migrant Workers from The Middle East ..... 241.16 Summary Table of Paddy Production ........ ................ 271.17 Financial Returns - Other Field Crops Versus Paddy ....... 301.18(a) Paddy Sector - Gross Extent Sown (Hectares) During

The Maha Season - 1980/81 to 1989/90 ................... 331.18(b) Paddy Sector - Gross Extent Sown (Hectares) During

The Yala Season, 1981 to 1990 ............ 331.19 Paddy - Imputed Loss in Production in the

North and East: Maha Season (1984/85 - 1989/90). 341.20 Paddy - Imputed Loss in Production in the

North and East: Yala Season (1985-1990) ............... . 351.21 Evolution of Defense Expenditures ........................ 361.22 Number of Families Directly Affected by the

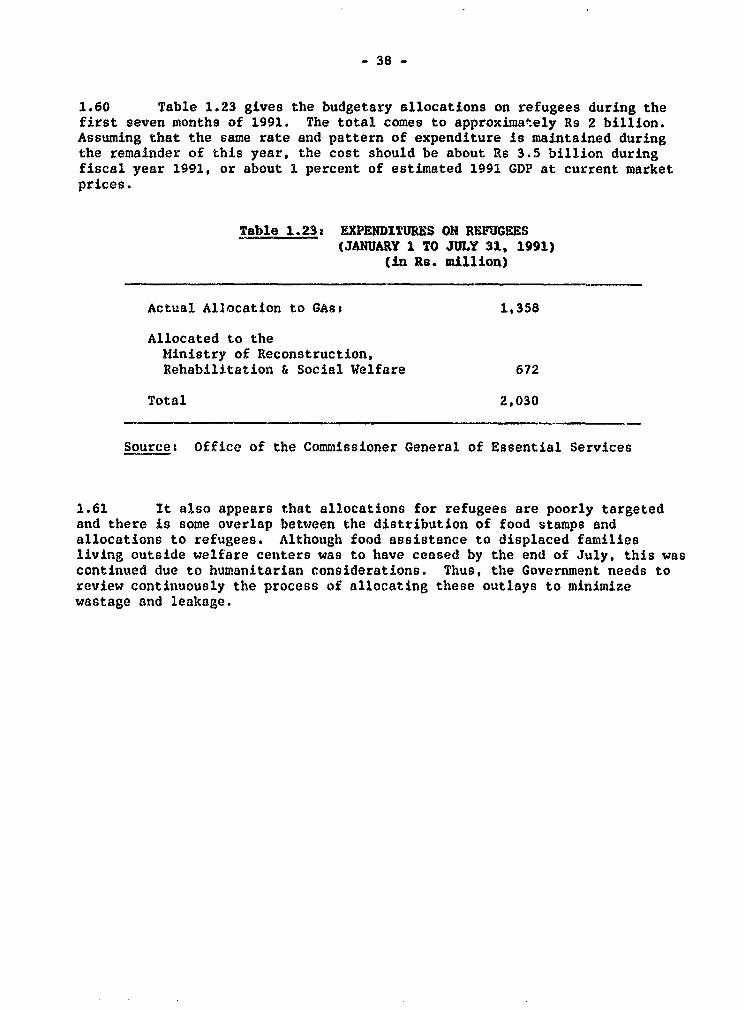

Civil Conflict as of September 1, 1991 ................ . 371.23 Expenditures on Refugees (January 1 to July 31, 1991) ..... 38

Chapter It

2.1 Public and Private Investment, Selected Years ....... , 422.2 Growth Rate of Real Investment ........................... 432.3 Composition of Private Fixed Investment,

Selected Years......... . ...... 44

2-

2.4 Domestic Savings, Selected Years ................... .... 442.5 Percentage Wage and Price Changes ....... ......... 482.6 Evolution of Determinants of Unit Labor Cost ............. 492.7 Tea Production ................. .......................... 57

Chapter III

3.1 Project Aid Disbursements as a Share ofPublic Investment ...................................... 77

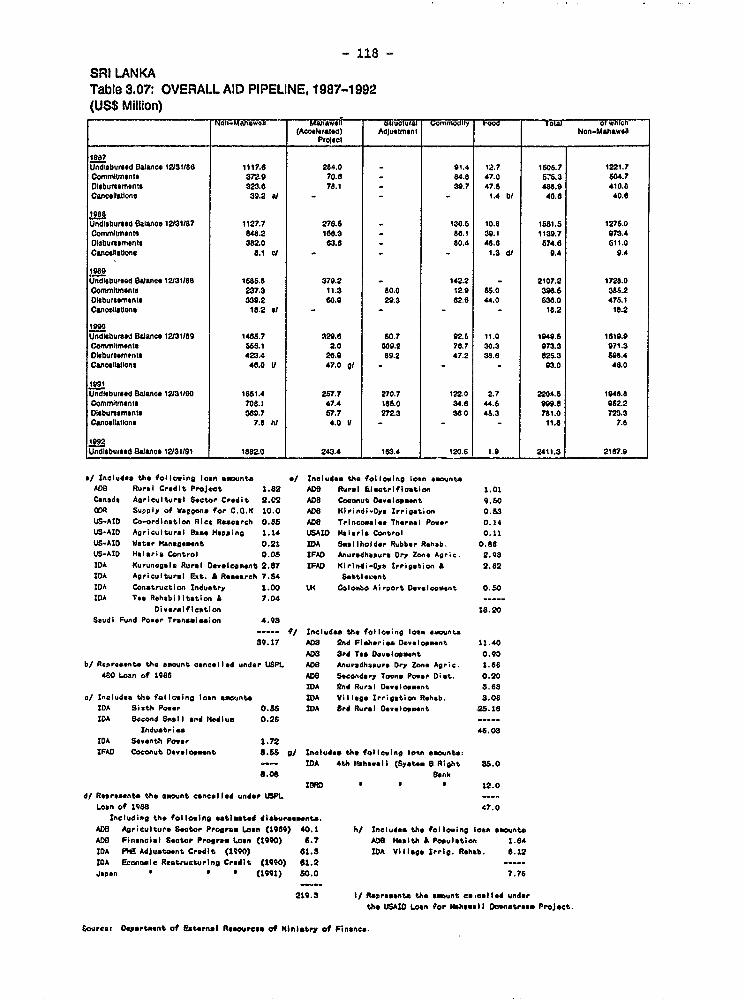

3.2 Aid Disbursements as Share of GDP ..... ................... 773.3 Sector Distribution of Total Project Aid ............... . . 783.4 Balance of Payments Projections--Base Case . .............. 803.5 External Financing Requirements .......................... 833.6 Overall Aid Pipeline, 1987-1992 ...... .................... 84

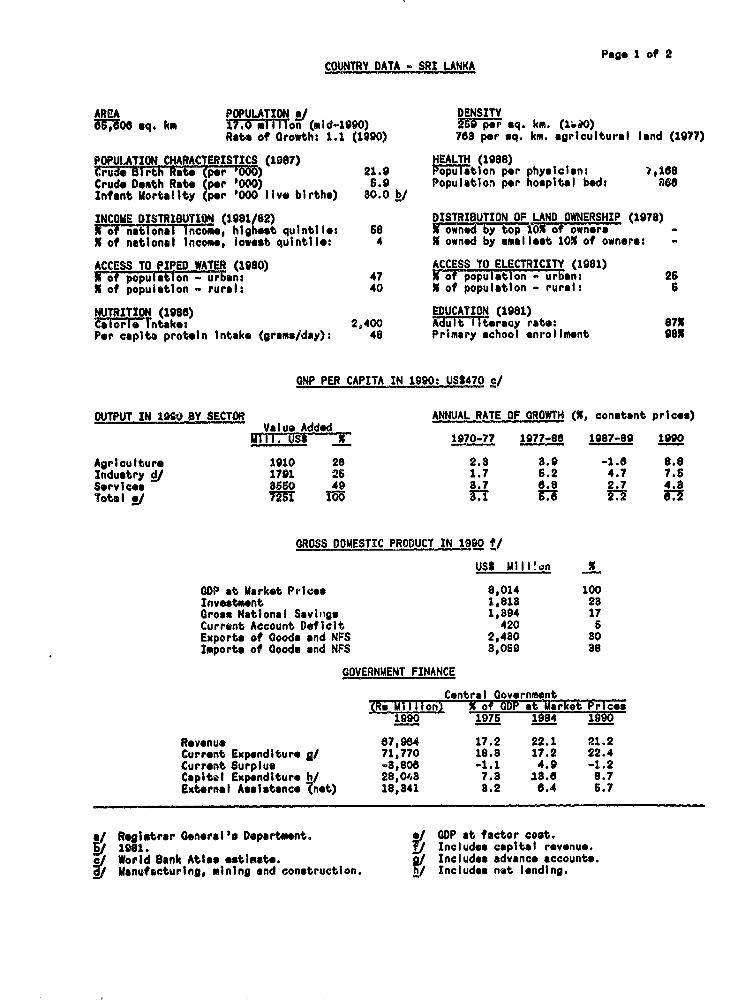

Pago 1 of 2CONTRY DATA SRI LANKA

AREA POPULATION ^/ DENSITYMU;OO sq. km X77rTTITon (mid-1990) 25W per sq. km. (l.i0)

Rate of Growth: 1.1 (1990) 703 per sq. km. agricultural land (1977)

POPULATION CHARACTERISTICS (1987) HEALTH (1988)Crude Birtn Rate (per '000) 21.9 Population per physician: ),168Crud. Death Rat. (per '000) 6.9 Population per ho.pit.l bed: 6seInfant Mortality (per '000 live births) 80.0 b/

INCOME DISTR18UTION (1081/82) DISTRIBUTION OF LAND OWNERSHIP (1978)X of natlonal i come, highest quintilI: 58 X owned by top lox of owners -X of national income, lowest quintile: 4 X owned by smalloot 10 of owners: -

ACCESS TO PIPED WATER (1980) ACCESS TO ELECTRICITY (1981)X-of population - urban: 47 X of population - urban: 26X of populatlon - rural: 40 X of population - rural: 6

NUTRITION (1988) EDUCATION (1981)Calo;-reTntako: 2,400 Adult lteracy rate: 87XPer capita protein Intake (grams/day): 48 Primary school enrollmont 98x

GNP PER CAPITA IN 1990: USU470 c/

OUTPUT IN 1990 BY SECTOR ANNUAL RATE OF GROWTH (X, constant prices)Value Added

Mill. Us$ U 1970-77 1977-86 1987-89 1990

Agriculturo 1910 26 2.8 8.9 -1.8 8.6Industry j/ 1791 26 1.7 6.2 4.7 7.6Services a850 49 3.7 6.8 2.7 4.3Total !/ m .T

GROSS DOMESTIC PRODUCT IN 1990 f/

US$ Mill!,on U

GDP at Market Prices 8,014 100Investment 1,818 23Gross National Savings 1,894 17Current Account Deficit 420 5Exports of Goods and NFS 2,48o 8oImports of Goods and NFS 8,069 38

GOVERNMENT FINANCE

Contral Government(Ru Million) X of GDP at MarketE Pricos

1990 1975 1984 1990

Revenue 67,984 17.2 22.1 21.2Current Expenditure g/ 71,770 18.8 17.2 22.4Current Surplus -3,806 -1.1 4.9 -1.2Capltl Expenditure hl 28,04S 7.3 13.6 8.7External Assist nco (not) 18,841 8.2 6.4 6.7

a Rogistrar General's Department. */ GDP at factor cost./, 1961. / Includes capital revenue.

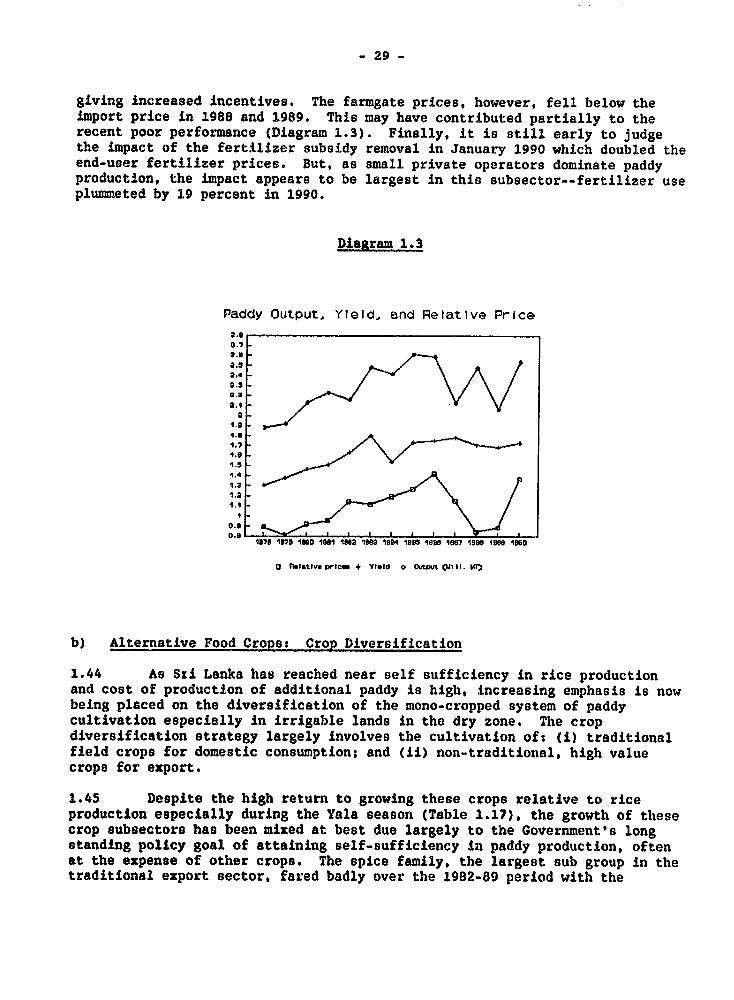

cl World Bank Atlas estite. / Includes advance accounts.Manufacturlng, mlning and construction. f/ Includes not lending.

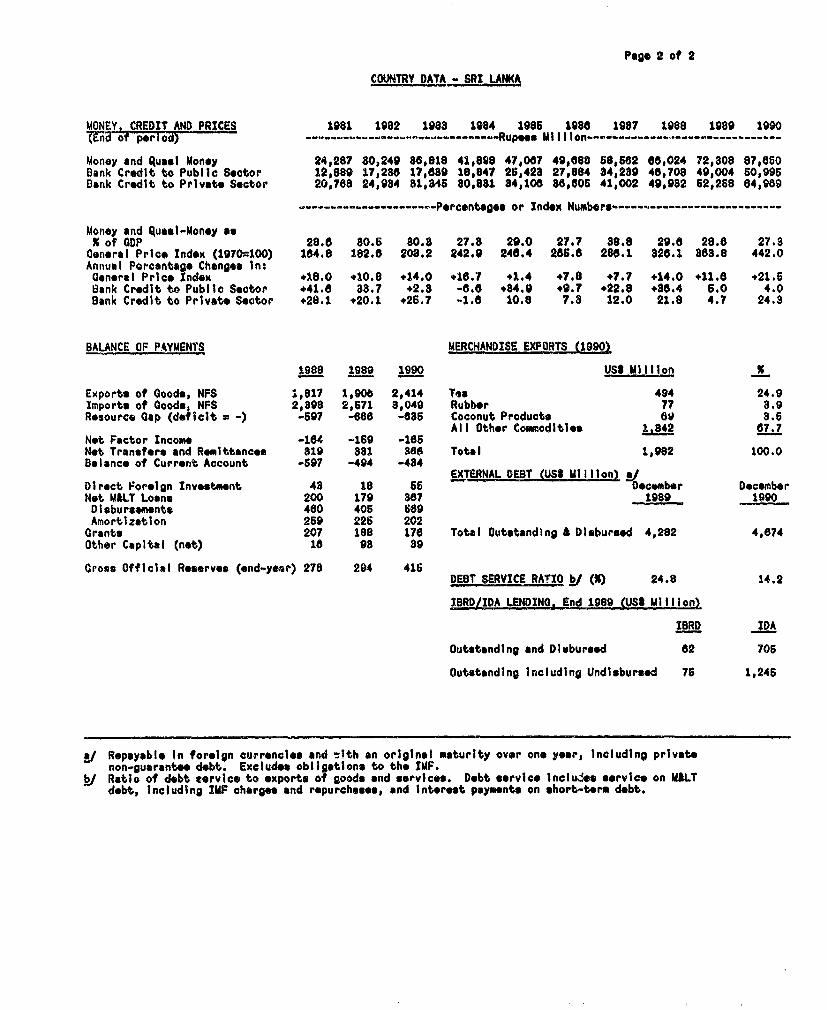

Page 2 of 2

COUNTRY DATA SRI LANKA

MONEY. CREDIT AND PRICES 1981 1982 1983 1984 1986 198a 1987 1988 1989 1990(End of perioa) - …-- Rupsee Million…------

Money and Qusl Money 24,287 80,249 88,818 41,898 47,087 49,680 68,662 66,024 72,808 87,850Bank Credit to Public Sector 12,889 17,288 17,889 18,847 25,423 27,684 a4,289 48,708 49,004 60,995Dank Credit to Private Sector 20,768 24,934 81,346 80,881 34,108 8a,605 41,002 49,982 62,268 84,989

-Percentage* or Index Numbers-----------------------

Money and Quasi-Money as% of GDP 28.6 80.5 80.3 27.3 29.0 27.7 88.8 29.8 28.6 27.8Oeneral Price Index (1970-100) 164.8 182.6 208.2 242.9 246.4 256.8 288.1 328.1 863.8 442.0Annual Pereantago Changes In:General Price Index .18.0 +10.8 +14.0 e18.7 +1.4 +7.8 +7.7 +14.0 +11.8 +21.5Bank Credit to Public Sector e41.0 38.7 +2.8 -6.8 .84.9 .9.7 +22.8 +86.4 6.0 4.0Bank Credit to Private Soctor +28.1 +20.1 +26.7 -1.8 10.8 7.8 12.0 21.8 4.7 24.3

BALANCE OF PAYMENTS MERCHANDISE EXPORTS (19901

1988 1989 1990 USt Million U

Exports of Goods, NFS 1,817 1,906 2,414 Toa 494 24.9Import. of Goods, NFS 2,898 2,671 3,049 Rubber 77 3.9Resource Gap (deficit m -) -597 -6e8 -685 Coconut Products 68 3.6

All Other Commodities 1.S42 67.7Net Factor Income -164 -169 -1B6Net Transfer* and Romittancos 819 881 386 Total 1,982 100.0Balance of Current. Account -697 -494 -434

EXTERNAL DEBT (US$ Million) /Direct Foreign Invostment 43 18 65 December DecomberNot MALT Loan. 200 179 387 1989 1990Disbursements 460 405 669Amortization 269 225 202Grants 207 188 176 Total Outstanding £ Disbursed 4,282 4,674Other Capital (net) 16 98 89

Gross Official Resorves (end-year) 278 294 416DEBT SERVICE RATIO ki (U) 24.8 14.2

IBRD/IDA LENDING. End 1989 QUS2 Million)

IBRD IDA

Outstanding and Diabursed 82 705

Outstanding Including Undisbursed 76 1,246

ki Repayable in foreign currencles and tith an original maturity over one year, Including privatenon-guarante debt. Excludes obligations to the IMF.

b Ratio of debt tervice to exports of goods and services. Debt service lncludos service on MALTdebt, Including IMF charges and repurchases, and Interest paymnts on short-term debt.

EXECUTIVtI' SMARY

The Setting

1. Sri Lanka is characterized by levels of literacy, infant mortality, andlife expectancy that are comparable to those of more developed countries. Butits success in generating economic growth has not been commensurate with itssocial progress. Economic growth during the early 1970s was limited by aninefficient public sector and by efforts to protect domestic industry fromforeign competition. The celebrated 1977 reform that introduced market forcesinto the process of resource allocation resulted in only a one-time increasein efficiency gains, and growth startea to slow down by the mid-1980s. Alarge and inefficient public sector had been left intact and large publicinvestment projects financed primarily by donors and foreign commerciallenders yielded low returns and unsustainable macroeconomic gaps. Togetherwith the negative impact of the civil conflict in the North and East thatstarted in 1983 and the JVP (leftist) terrorist insurgency in the South in1988 and 1989, the growth rate in 1987-89 came down to a mere 2 percent ayear, and the economy was on the verge of a balance of payments crisis by mid-1989.

2. The new Government that came .o power in 1989 decided to stabilize theeconomy and to restructure it in the direction of private sector-leddevelopment. The Government's reform efforts addressed issues in four areas:stabilization; public sector rationalization; poverty program restructuring;and private sector development. A strong stabilization program was institutedto arrest the rapid economic deterioration. Economic performance began toimprove rapidly by early 1990 in the wake of a significant devaluation, anacross-the-board cut in budgetary outlays, and removal of major subsidies onwheat flour, rice, and fertilizers. This was aided throughout 1990 by goodweather and the return of civil normalcy in most of the country. The fiscalburden !,as however been increased by about 2 percent of GDP with renewal ofhostilicies since June 1990. The conflict in the North and East has notjeopardized implementation of the economic restructuring program in 1990.It has, however, not only reduced output in affected areas but has hurt SriLanka's efforts to attract more domestic and foreign investment and hasdiverted substantial public and private resources from development.

3. In the fourth quarter of 1991, however, the Government appears to haveweakened its grip on the tight macroeconomic management of the previous year.While the economy is estimated to have grown by about 5 percent and thuscontinued to follow the trend of robust growth established in 1990, bothfiscal and balance of payments deficits are expected to exceed targets bynearly one percentage point of GDP. This was partially caused by high defenseexpenditures, with inadequate countervailing expenditure cuts or revenuemobilization to maintain the overall macroeconomic tightness. If this trendwere allowed to continue, it would nullify most of the progress so far of therecent economic stabilization efforts. Much tighter economic managen.ant in1992 is thus called for to keep the economic restructuring on track andmaintain the economy on a sustainable high growth path.

- ii -

Economic Performance in 1990 and 1991

4. A significant part of the improvement in economic growth to 6 percent in1990 should be attributed to good weather, the improving civil conflictsituation and a low 1989 base as a result of the low growth that averaged at 2percent a year over the previous three years. Paddy and tea productionincreased, respectively, by 23 percent and 13 percent over the low 1989 base.While private manufacturing continued to grow, non-oil public manufacturingsector output declined. Investment stayed at around 22-23 percent of GDP, butits composition changed significantly: while public investment continued todecline from 10 percent of GDP in 1989 to 8.7 percent, private sectorinvestment as a share of GDP is reported as having increased rapidly, afeature that is however, not fully consistent with che pattern of -reditallocation observed for 1990. The current account deficit of the balance ofpayments improved from 7.1 percent in 1989 to 5.2 percent of GDP in 1990.This was due to an 11 percent volume growth in merchandise exports.Furthermore, the impact of high price oE imported oil due to the Gulf crisiswas moderated by two unexpected developments: (i) many migrant workers in theMiddle East, panic-stricken, remitted their savings home thereby raisingonetime private transfers; and (ii) notwithstanding the loss of Iraqi markets,which had accounted for 12-15 percent of Sri Lanka's total tea exports, thelatter total improved both with respect to price and volume, in part due togood export perfoLnance prior to the start of the crisis as well as totemporary speculative purchases by non-Iraq Middle Eastern countries. Thesedevelopments, together with increased disbursements of balance of paymentsaid, led to an overall balance surplus and increased gross official reservecoverage to two months of imports. The balance of payments performance in1991 shows some weakening because of a drop in tea prices, (a delayed effectof the Gulf crisis), and an increase in imports, especially in consumerdurable (cars and motor cycles), reflecting a liberalized import environmentand, probably, worsening public transport conditions. Together with apurchase of an aircraft by Air Lanka, these factors increased the currentaccount of the balance of payments to about 6.6 percent of GDP, as compared tothe targeted 5.8 percent.

5. The Government's fiscal deficit improved from 16 percent of GDP in 1988to 10 percent in 1990, despite increased security-related spending and thehigh cost of severance packages for workers retrenched as part of publicsector rest:'ucturing. This improvement was hor.ever accomplished largely bysuppressing public investment in, among other areas, infrastructure withpotentially negative effects on private investment. Fiscal management appearsto have deteriorated substantially in 1991 reflecting intensified fighting inthe North and East, increasing cost to accommodate refugees, and laborretrenchment cost associated with public sector restructuring. Efforts tooffset this increase in current expenditures (by cutting other expenditures ormobilizing additional resources) were inadequate, and the current deficit,which was 1.2 percent of GDP in 1990 worsened to 1.5 percent of GDP in 1991.Thus, despitd the continued suppression of public investment (8.7 percent ofGDP), the overall deficit appears to have increased to 10.8 percent of GDP asopposed to the targeted 10.1 percent.

iii -

6. Inflation, at 21.5 percent was high in 1990 and was caused mainly by:(i) removal of distortions in prices, such as devaluation and elimination ofsubsidies; (ii) higher import costs induced partly by the Gulf crisis-relatedoil price increase; and (iii) and localized sporadic problems in productionand transportation of agricultural goods, in particular, vegetables.Inflation had come down to about 10 percent by October 1991 because thesefactors had worked themselves through the system. But, inflationaryexpectations remain strong reflecting the fact that net domestic bankborrowing by the Government was larger than projected and that anaccommodating private credit policy has been followed; the demand for creditshows no sign of abatement despite the real interest rate increasing from anegative 4 percent in 1990 to a positive 4-6 percent in 1991.

Developments in Agriculture

7. Agriculture, which provides income to 70 percent of the population inSri Lanka, has not fared well in the 1980s, growing at 2.4 percent a yearbet,reen 1982 and 1990--a period when GDP grew at 4 percent a year in realterms. Outputs of tea and paddy grew at 2.8 percent and 2.1 percent a year,while non-tea tree crops suffered a decline. This unsatisfactory performancecan be explained by the following three factors. First, paddy production hasnot been expanding since the mid-1980s because (i) weather and civilconditions have been unfavorable; and (ii) high yielding varieties andadequate fertilizers are already used in most of the irrigated areas and,thus, increasing production further implies the need for additional investmentand research to enhance productivity in areas with less favorable conditions--which is costly. This has reinforced the Government's decision to de-emphasize paddy production. Second, inefficiency of the two publiccorporations managing the vast majority of tree crop plantations led to a fallin public sector production, which led to the Government's decision torestructure the subsector to increase the role of the private sector. Third,policies that have traditionally favored paddy production have militatedagainst crop diversification. In addition, the ongoing civil conflict isestimated to have reduced paddy production in the North and East by as much asone million tons over the last seven years (or 3 percent of 1990 GDP valued at1990 prices).

A Growth-Oriented Policy Package

8. Sustaining growth based on exports requires that the Governmentcontinues to carry out the following: (i) t %vht macroeconomic managementespecially fiscal management through better control of recurrent expenditure;(ii) continued rationalization of the public sector; (iii) continuedrationalization of the poverty programs; and (iv) provision of an enablingframework for the private sector. Revenue mobilization efforts shouldcontinue based on improved tax administration and tax reforms that broaden thetax base and increase the system's efficiency. (Any temporary loss of revenueresulting from the changes in the tax rate structure should be off-set byefforts to raise additional revenues through, for example, more excises.) Itis also important that the Government consult closely with the IMF on exchangerate management to as,ure and maintain export competitiveness.

- iv -

Resumption of Tight Macroeconomic Management

9. The favorable economic outturn in 1990 and 1991 has allowed cautiousoptimism to emerge regarding the future of Sri Lanka's growth prospects.However, given, that most factors supporting this performance were external toeconomic management, viz., good weather, a relatively stable securitysituation and unexpected positive, albeit temporary, effects of the Gulfcrisis, it is important that optimism not give way to complacency. Indeed thestill good 1991 output performance has been accompanied by weakening effortstowards tight macroeconomic management as both fiscal deficit and balance-of-payments deficit are projected to be higher than targeted; a trend that needsto be reversed as soon as possible. Moreover, the pattern of growth ischaracterized by a number of undesirable features. First, real investment hasstagnated. Public investment has fallen sharply. While private investmenthas been on the rise, there is some evidence to suggest that an increasingshare of it is going towards residential buildings rather than into directlyproductive sectors of the economy. Second, the real effective exchange ratehas appreciated by 20 percent from the fourth quarter of 1989 till July 1991.The erosion of competitiveness during this period reflects a rapid increase inproductivity-adjusted unit labor costs and exchange rate depreciation thatfalls short of domestic inflation. This reinforces the need for coordinatedaction to contain these labor costs as well as, in close consultation with theIMF, on exchange rate management.

10. The low public investment and erosion of external competitiveness maybe traced at least in part, to a shortfall of revenues over currentexpenditures amounving to 1-2 percent of GDP, a situation caused in part byintroduction of additional welfare programs (which need better targeting) andof the substantial wage and salary component of security-related spending.These outlays increased demands for consumption goods, mostly food and somese-:ices. This set of circumstances has weakened incentives for investmentsin the production of exports goods and redirected resources towardsconsumption or investments in activities such as real estate. This phenomenonis borne out by the fact that private sector credits for residential buildingsand consumption increased rapidly in 1990 at 37 percent and 42 percent,respectively. The situation needs to be redressed through changes in policy.To prevent such a tendency from gaining momentum, the Government should aim atattaining a current budget surplus of about 2 percent of GDP within two tothree years through control of current expenditure items such as the publicsector wage bill, transfers to public corporations, the government pensionscheme and leakages from welfare programs to those not truly in need.Somewhat lax macroeconomic management in 2991 must be reversed in 1992 to puteconomic restructuring back on track. In addition, given the difficulty inachieving immediate and adequate fiscal retrenchment, an appropriate mix ofwage policy, aggregate demand policy, and exchange rate policy, should beemployed. At the same time, public resources should be shifted towardinvestment in efficient infrastructure (see para. 18 below).

Public Sector Rationallation

11. The Government has taken various measures to rationalize public sectoractivities to make more room for the private sector and improve overallefficiency. First, the public sector bus company was converted into about 80privatized companies through employee share ownership, (or "peoplization").While this is a step in the right direction, experiences in other countriesshow that this method of privatization often ended up inhibiting the infusioninto the ccmpanies of managerial, financial and technological resources theyneed to compete in the private market. More direct divestiture should beencouraged in the future. Second, an action plan has been prepared toincrease the role of the private sector in managing the important (andcurrently loss-making) state-owned tree-crop plantations through privatemanagement contracts based on fees-for-services and profit sharing. To ensurethe success of this measure, however, it is crucial that there be moreincentive to maximize longer-run profits. Privatization is the preferable wayto accomplish this. Third, the Government has also committed itself toprivatizing all commercially oriented public enterprises and corporations, andso far has divested eleven firms. Fourth, in an effort to achieve the targetof retrenching 25 percent or 80,000-90,000 staff over a four-to-five yearperiod based on the recommendations made by the Administrative ReformCommittee, the Government retrenched about 10 percent or about 40,000 ofcentral and provincial staff in 1990. Lastly, the Government has made theprocess of recruitment and promotion purely merit-based. There are recentindications, however, that the Government's commitment to furtherrationalization of the civil service is weakening; they have difficulties incommitting to further reduction in civil service size.

Poverty Program Restructuring

12. The Government has made considerable efforts to improve the nation'sthree major poverty p.:ograms. They are: the Jana Saviya (poverty alleviation)program (JSP), the fo'd stamp program (FSP), and the Mid-Day Meal Program(HDMP) for school children. All three suffered from inadequate targeting;many more people than the truly poor or those at risk were receiving benefits,causing a drain on the budget and diluting the effectiveness of the programs.While the truly poor in Sri Lanka are estimated at about 20-25 percent of thepopulation, the JSP was initially envisaged to provide substantial incometransfers (close to semi-skilled labor wages) and, in the aggregate, amountingto 20 percent of GDP, to half of the nation's population for two years duringwhich period recipients were supposed to learn skills for employment or self-employment. There was however no mechanism established to monitor whetherthose conditions were being met. The FSP provided food stamps to half thepopulation as well. The MDMP is designed to provide additional food stamps toall school children in the country to supplement children's nutritionalintake.

13. As part of rationalization, the JSP has been staggered over 11 rounds tolessen its fiscal cost, with the beneficiaries screened at the community levelto ensure that only the truly needy get the benefits. In addition, it hasbeen made mandatory that a person from each beneficiary household participate

- vi -

in rural civil works. There is, however, substantial difficulty in monitoringthe progress. For the FSP, restructuring mainly consisted of improvedtargeting: about one million families currently receive stamps as compared to1.9 million families until October 1991. The MDMP is being administered in away that reduces program cost by 20 percent. Nutritional interventions wouldhowever be much more effective if they were targeted towards needy pre-schoolers who are truly nutritionally at risk as well as lactating mothers.While these measures discussed above represent significant improvements of theimplementation design of the three programs, there continue to be strongpolitical pressures in Sri Lanka for welfare programs comprising primarilyconsumption-oriented income transfers.

An Enabling Framework for Privat Investment

14. The macroeconomic policy reforms and public sector restructuringdiscussed above provide a framework within which private investment may bepromoted. They however need to be complemented by a wide range of reforms atthe microeconomic and sectoral levels, four areas of high priority arementioned here although the list is not meant to be exhaustive.

15. An efficiently functioning financial sector is a prerequisite forprivate sector-led growth. Among various policy measures to improve thefinancial sector, highest priority should be attached to addressinginefficiencies in the finiancial institutions, especially the state-ownedentities. The two state-owned banks, Bank of Ceylon and People's Bank, whichown more than 60 percent of the commercial bank assets, but are insolvent wheninternationally accepted provisioning for bad debts is taken, need to berestructured after appropriate provisioning and recapitalization is completed.In particular, the two state-owned banks need to be commercialized to improvethe competitive environment of the sector. Furthermore, the Bank of Ceylonneeds to be privatized in the future. In addition, major functions of theNational Savings Bank, such as supply of funds to the Government, are lessrelevant with the expansion of treasury bill sales and investment by pensionfunds. It is thus recommended that its rural branch structure berationalized, and that if it cannot break even by investing in treasury bills,consideration should be given to its phasing out. In addition, improvedprocedures for classifying and provisioning for bad debts should beeffectively implemented. Debt recovery should be improved through amendingand enforcing the country's debt recovery laws, and establishing a debtrecovery agency.

16. Despite low wages and a strategic location, Sri Lanka remains a marginalrecipient of foreign direct investment: the figure was about US$32 million in1990. While part of this is clearly due to the unsettled civil situation inthe country, uncoordinated policies and the discretionary nature of approvalprocedures have also played their part. The Government has therefore recentlyannounced measures that will open up most of the economy to foreign investmentand allow free remittances to be made even during balance-of-payments crises.At the same time, the institution that approves and assists foreign investorsshould be improved to handle efficiently all kinds of applications whether ornot the investments take place in the Export Processing Zones. In addition,

- vii -

the list of activities that would not get "automatic approval" shouldeventually be limited to only those that relate to national security andhealth hazards. While this approach represents a significant step forward, itis important that the new policies be implemented expeditiously and thatremaining obstacles to foreign investment--such as limited access to domesticcredit--be removed.

17. The Termination of Workmen Act, which effectively takes away theemployer's right to decide on lay-offs and firings of workers, by making ithighly costly to do so is a controversial piece of labor legislation. ThisAct, originally established with the intention of protecting labor, is nowdamaging workers interests in general by giving incentives to employers toreplace labor with capital. Its repeal or, transitionally, announcement of aprocedure for receiving a waiver from its effects is recommended. TheIndustrial Dispute Act already offers an acceptable alternative to theTermination Act. The rest of the economy's complex labor legislation shouldbe reviewed and streamlined.

18. Appropriate infrastructural services lower the cost of private businessand induce private investment. To promote industrial development for exports,a further concentration of production activities in the Greater ColomboMetropolitan Area may be unavoidable, and an appropriate infrastructurestrategy should be built on this assumption. For diversified agriculture withexport orientation, the crucial factors, beyond incentives, will be access tomarkets and market information. Priority areas in this latter regard shouldbe: establishing a well-maintained intercity road network; developingcommercial refrigerated transportation and storage systems; and improvingquality and coverage of the domestic and international telecommunicationsnetwork.

1992 Aid Requirements

19. If the measures discussed above are substantially implemented in thenear future including reversing the deteriorating macroeconomic managementwitnessed in the second half of 1991, and if the civil conflict situationgradually improves, the country is expected to grow at around 5-6 percent ayear in the medium-term future, with a current account deficit of around 5.8-5.9 percent of GDP. This current account deficit, together with amortizationand other foreign exchange needs, would bring total foreign financingrequirements to about US$1 billion a year. Taking into consideration netprivate flows and net purchases from the IMF, annual foreign aid flows wouldneed to be about US$790 million in 1992. Project aid requirements in 1992 areexpected to be about US$530 million, of which US$500 million is expected to bedisbursed from the existing project pipeline. Furthermore, disbursements ofnon-project aid from the existing pipeline would be US$190 million. Theremaining gap of US$100 million needs therefore to be filled by commitments ofproject aid amounting to about US$630 million and quick-disbursing balance-of-payment assistance of approximately US$170 million in 1992. Again, it isimportant to emphasize that if the momentum for policy reforms is notmaintained, the rationale for this level of high donor assistance will besubstantially weakened. In particular, without the re-establishment of

- viii -

disciplined and tight fiscal management within 1992, balance-of-paymentssupport could allow maintenance of unsustainable external current account andfiscal deficits.

CHAPTER IR REVIEW OF RECENT ECONOMIC PERFORMANCE

1. Economic Performance in 1990 and 1991

a) Background

1.1 Sri Lanka has had a long tradition of emphasizing socialdevelopment and has enjoyed levels of literacy, infant mortality and lifeexpectancy comparable to more developed economies. But its success ingenerating growth in income and employment has been limited by theinefficiencies in the public sector and the insulation of the domestic marketfrom foreign competition. In 1977, therefore, the Government reversed itslong-standing policy and started to encourage market forces to play anincreased role in the allocation of resources. This resulted in a one timeincrease in efficiency gains--paddy production increased substantially as wellas exports. Growth was further accelerated by a concurrent start of largepublic investment programs, most notably the Mahaweli River Irrigation andHydropower Scheme. Thus growth, which averaged 3 percent per year in the19709, increased to close to 7 percent in 1978-80 and remained at around 5percent during the first half of the 19809.

1.2 This growth momentum, however, would not be sustained. By the mid-1980s, slow growth and high unemployment emerged once again as seriousproblems. This was mainly because the 1977 reforms did not address thefundamental problem of a large and inefficient public sector which employedover 20 percent of the labor force. Furthermore, ambitious public investmentprograms (whose returns turned out to be disappointingly low) exacerbated thesituation by increasing further the role of the public sector in the economyand creating excessive macroeconomic imbalances. The Government's reluctancein adjusting the exchange rate adequately after 1977 also aggravatedmacroeconomic imbalances and worsened export competitiveness. The continuedcivil conflict in the North and resurgence of leftist (JVP) terrorism in theSouth in 1987, put additional pressures on macroeconomic management. As aresult growth slowed down to a mere 2 percent a year during 1987-89, and bymid-1989, the economy was on the verge of a balance of payments crisis.

1.3 The new Government formed in early 1989, therefore, initiatedstructural reforms to stabilize the economy and to get it on to a sustainedhigh growth path. The reform process was broad-based, and focussed on (i)achieving macroeconomic stabilization; (ii) improving effectiveness of thecountry's welfare programs through better targeting; and (iii) creating anenabling environment for private sector and export-led development. Followingthe introduction of this reform process in mid-1989, overall economicmanagement and performance improved markedly (see Table 1.1 for keyindicators).

-2-

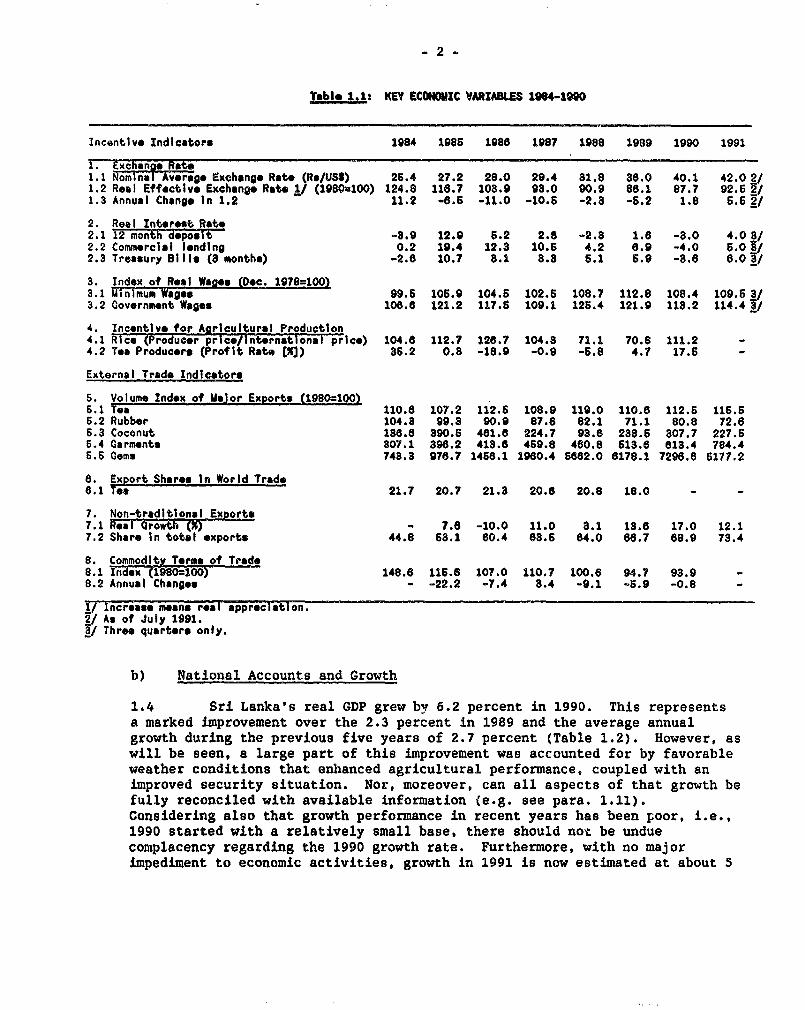

Table 1.1: KEY ECONOMIC VARIABES 1904-990

Incentive Indlcators 1984 1986 1988 1987 1988 1989 1990 1991

1 Exchance Rot;1.1 NominI-A crig h Exchnge Rate (R/US$) 26.4 27.2 28.0 29.4 81.8 88.0 40.1 42 0 2/1.2 Real Effecive Exchange Rote h (1980=100) 124.8 118.7 108.9 93.0 90.9 88.1 87.7 92.6 R/1.3 Annual Change In 1.2 11.2 -8.5 -11.0 -10.6 -2.3 -5.2 1.8 6.6 2/

2. Real Interest Rat.2.1 12 month deposlt -3.9 12.9 6.2 2.6 -2.3 1.6 -3.0 4.0 9/2.2 Commercial lending 0.2 19.4 12.3 10.5 4.2 6.9 -4.0 6.0 3/2.3 Treasury Bills (3 months) -2.8 10.7 3.1 3.8 6.1 5.9 -8.6 e.o I/

3. Index of Real Wage* (D*c. 1978=100)3.1 Minimum Wages 99.5 105.9 104.5 102.6 108.7 112.8 108.4 109.5 3/3.2 Government Wage. 108.8 121.2 117.6 109.1 125.4 121.9 113.2 114.4 3/

4. Incentive for Agricultural Production4.1 Rice (Produc*r price/international price) 104.8 112.7 126.7 104.3 71.1 70.8 111.2 -4.2 Tea Producers (Profit Rate [%]) 85.2 0.3 -18.9 -0.9 -6.8 4.7 17.5 -

External Trade Indicators

S. Volume Index of Major Exports (1980-100)5.1 Tea 110.6 107.2 112.6 108.9 119.0 110.6 112.6 115.55.2 Rubber 104.3 99.3 90.9 87.6 82.1 71.1 80.8 72.65.3 Coconut 138.8 390.5 481.6 224.7 93.6 238.6 307.7 227.65.4 Gorments 807.1 396.2 413.6 459.8 480.8 513.6 613.4 784.46.5 Goms 743.8 976.7 1456.1 1960.4 e882.0 6178.1 7298.8 6177.2

8 Export Shares In World Trade8.1 Tea 21.7 20.7 21.3 20.6 20.8 18.0 - -

7. Non-traditlonal ExDortt7.1 RlF roWth (Xy-- - 7.6 -10.0 11.0 3.1 13.6 17.0 12.17.2 Share In total exports 44.8 63.1 60.4 68.5 64.0 66.7 68.9 73.4

8 Commodity Terms of Trad.8.1 Index (I980=7100) 148.6 116.6 107.0 110.7 100.6 94.7 93.9 -8.2 Annual Changes - -22.2 -7.4 3.4 -9.1 -5.9 -0.8 -

1/ Increase meane real appreclaElon.2/ As of July 1991.3/ Three quarters only.

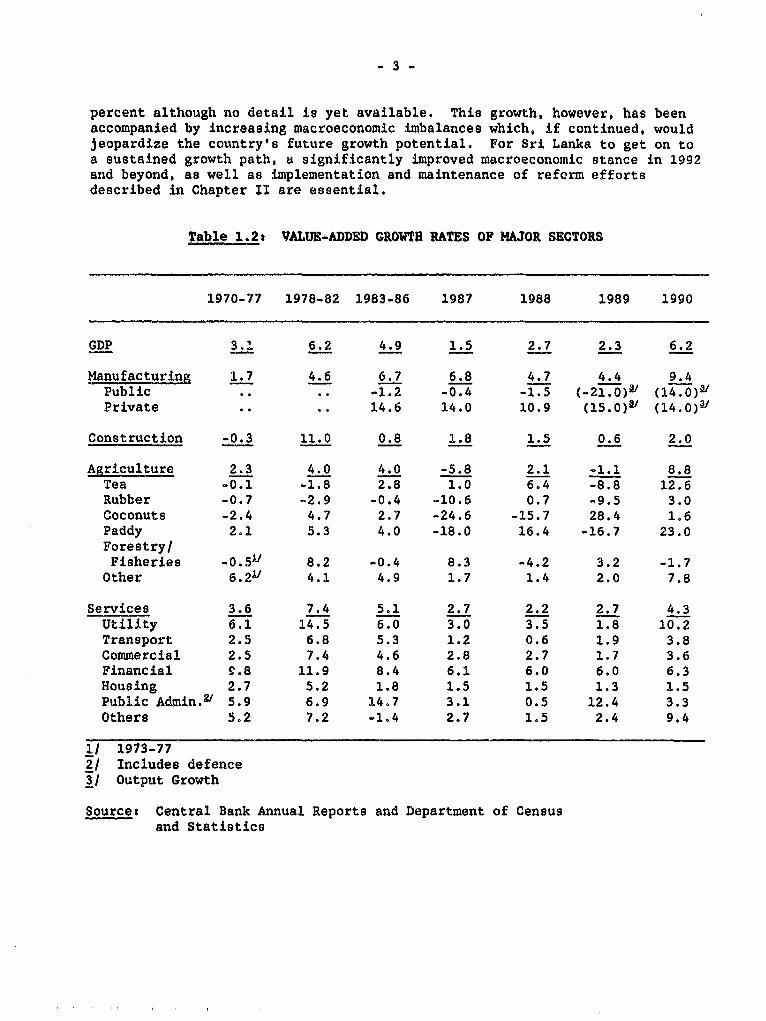

b) National Accounts and Growth

1.4 Sri Lanka's real GDP grew by 6.2 percent in 1990. This representsa marked improvement over the 2.3 percent in 1989 and the average annualgrowth during the previous five years of 2.7 percent (Table 1.2). However, aswill be seen, a large part of this improvement was accounted for by favorableweather conditions that enhanced agricultural performance, coupled with animproved security situation. Nor, moreover, can all aspects of that growth befully reconciled with available information (e.g. see para. 1.11).Considering also that growth performance in recent years has been poor, i.e.,1990 started with a relatively small base, there should not be unduecomplacency regarding the 1990 growth rate. Furthermore, with no majorimpediment to economic activities, growth in 1991 is now estimated at about 5

-3-

percent although no detail is yet available. This growth, however, has beenaccompanied by increasing macroeconomic imbalances which, if continued, wouldjeopardize the country's future growth potential. For Sri Lanka to get on toa sustained growth path, a significantly improved macroeconomic stance in 1992and beyond, as well as implementation and maintenance of referm effortsdescribed in Chapter II are essential.

Table 1.2: VALUE-ADDED GRO'WTH RATES OF MAJOR SECTORS

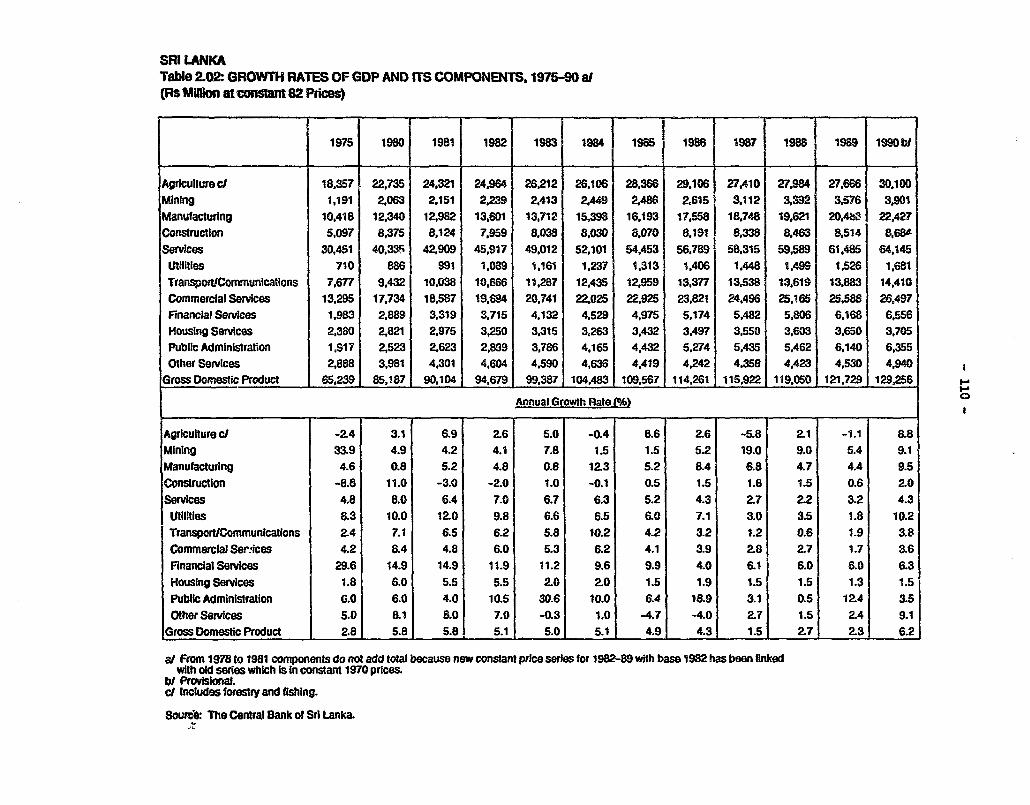

1970-77 1978-82 1983-86 1987 1988 1989 1990

GDP 3.1 6.2 4.9 1.5 2.7 2.3 6.2

Manufacturing 1.7 4.6 6.7 6.8 4.7 4.4 9.4Public .. .. -1.2 -0.4 -1.5 (-21.0)9/ (14.0)?JPrivate .. .. 14.6 14.0 10.9 (15 .0 )v (14.0)2

Construction -0.3 11.0 0.8 1.8 1.5 0.6 2.0

Agriculture 2.3 4.0 4.0 -5.8 2.1 -1.1 8.8Tea -0.1 -1.8 2.8 1.0 6.4 -8.8 12.6Rubber -0.7 -2.9 -0.4 -10.6 0.7 -9.5 3.0Coconuts -2.4 4.7 2.7 -24.6 -15.7 28.4 1.6Paddy 2.1 5.3 4.0 -18.0 16.4 -16.7 23.0Forestry/Fisheries -0.51 8.2 -0.4 8.3 -4.2 3.2 -1.7

Other 6.211 4.1 4.9 1.7 1.4 2.0 7.8

Services 3.6 7.4 5.1 2.7 2.2 2.7 4.3Utility 6.1 14.5 6.0 3.0 3.5 1.8 10.2Transport 2.5 6.8 5.3 1.2 0.6 1.9 3.8Commercial 2.5 7.4 4.6 2.8 2.7 1.7 3.6Financial S.8 11.9 8.4 6.1 6.0 6.0 6.3Housing 2.7 5.2 1.8 1.5 1.5 1.3 1.5Public Admin.V 5.9 6.9 14.7 3.1 0.5 12.4 3.3Others 5.2 7.2 -1.4 2.7 1.5 2.4 9.4

1/ 1973-772/ Includes defence3/ Output Growth

Source: Central Bank Annual Reports and Department of Censusand Statistics

-4-

1. Growth Performance in 1990

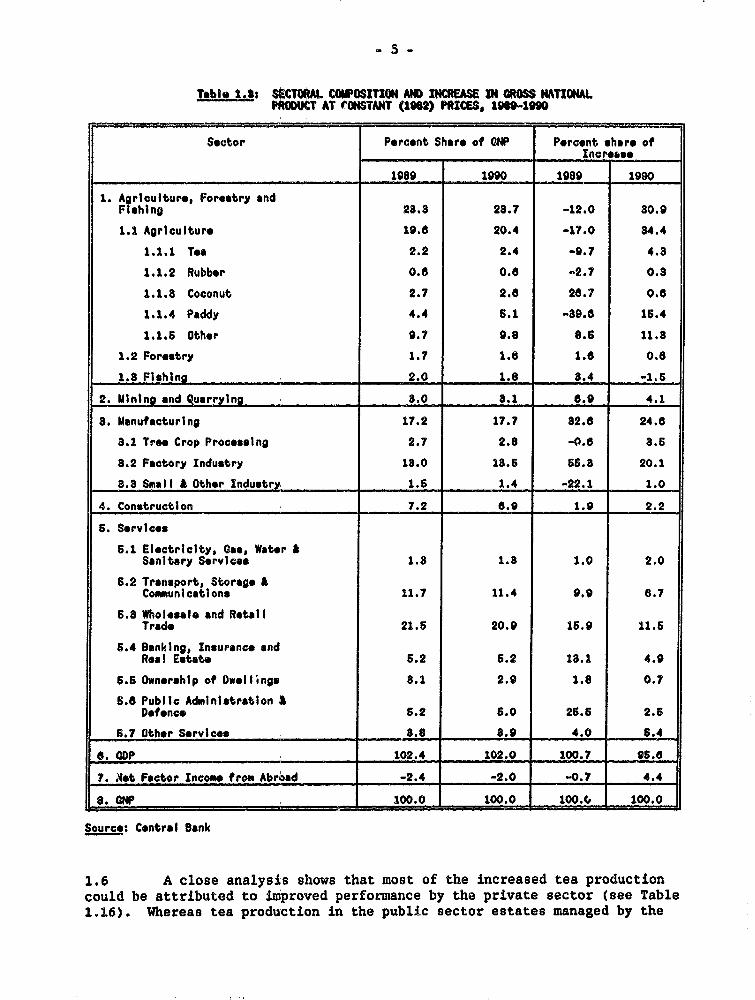

1.5 Agriculture. Agriculture accounts for a significant part of theaccelerated growth in 1990. As Table 1.3 illustrates, over a third of theincrease in GNP in 1990 could be accounted for by increased agriculturalproduction, and about half of this can be attributed to the 23 percent growthin paddy output over a poor 1989 base. This high paddy growth was due to asubstantial expansion in the area sown and harvested. The average yield,however, increased only marginally. Minor food crop production alsocontributed to the high sector growth by recording an increase of 8 percentover its 1989 level. In addition, tea production in 1990 reached its highestrecorded level and its value added in real terms increased by 12.6 percentover its 1989 level. The other two tree crops, namely, rubber and coconut,grew marginally in 1990 (3.0 percent and 1.6 percent, respectively).

able1-.3Ss SECTORAL COMPOSITION Am INCREASE IN GROSS NATIONALPRODUCT AT EONSTANT (1OU) PRICES, 1999-bO

Sector Percent Share of ONP Percent share of____________ _________ Increse,

1989 1990 1989 1990

1. A riculture, Forestry andFishing 23.8 28.7 -12.0 30.9

1.1 Agriculture 19.6 20.4 -17.0 84.4

1.1.1 Tea 2.2 2.4 -9.7 4.8

1.1.2 Rubber 0.6 0.6 -2.7 0.3

1.1.8 Coconut 2.7 2.8 28.7 0.6

1.1.4 Paddy 4.4 S 1 -39.8 16.4

1.1.6 Other 9.7 9.8 8.6 11.3

1.2 Forestry 1.7 1.6 1.6 0.6

1.8 Fishing 2.0 1.8 3.4 -1l5

2. Mining and Quarrying 8.0 8. 1 8.9 4.1

a. Manufacturing 17.2 17.7 82.6 24.6

3.1 Tre Crop Processlng 2.7 2.8 -0.6 3.6

8.2 Factory Industry 13.0 13.5 65.3 20.1

3.8 Small A Other Industry 1.5 1.4 -22.1 1.0

4. Construction 7.2 8.9 1.9 2.2

5 Services

5.1 Electricity, Gas, Water ASanitary Serviceo 1.3 1.3 1.0 2.0

6.2 Transport, Storage ACommunications 11.7 11.4 9.9 6.7

6.8 Wholesale and RetallTrade 21.5 20.9 16.9 11.5

6.4 Banking, Insurance andReal Estate 6.2 5.2 18.1 4.9

6.5 Ownership of Dwellings 3.1 2.9 1.8 0.7

5.8 Public Administrstlon ADefence 5.2 5.0 26.5 2.6

6.? Other Services 8.8 8.9 4.0 5.4

6. CDP 102.4 102.0 100.7 95.6

7. Ut Factor Income from Abroad -2.4 -2.0 -0.7 4.4

8. OMP 100.0 100.0 100.C 100.0

Soure: Central Bank

1.6 A close analysis shows that most of the increased tea productioncould be attributed to improved performance by the private sector (see Table1.16). Whereas tea production in the public sector estates managed by the

-6-

Janatha Estates Development Board (JEDB) and the Sri Lanka State PlantationsCorporation (SLSPC) grew by 4 percent and 5 percent respectively, teaproduction in the private sector rose by 27 percent. This was partly due tothe fact that 1989 was a particularly bad year for private sector teaproducers, many of whom are in the Southern Province and cultivate low grownvarieties; the South was especially affected by the JVP insurgency in 1989(paras. 1.52-1.53) and by adverse weather conditions that damaged mostly low-grown varieties in the same year.

1.7 The Manufacturing and Other Industrial Sectors. Another sectorthat contributed to enhanced 1990 growth was manufacturing which grew by 9.4percent. As Table 1.3 illustrates, a quarter of the increase in GNP in 1990could be accounted for by this sector. The industrial sub-categories whichrecorded the largest increases in value added during the year were chemicals,petroleum and plastic products (25 percent), fabricated metal products,machinery and transport equipment (12 percent), textiles, apparel and leatherproducts (10 percent) and food, beverages and tobacco (8 percent). Accordingto the Central Bank, both public and private sector industrial output grew by14 percent. However, a large part of this was due to increased output ofpetroleum products (especially that of the Ceylon Petroleum Corporation due tothe high output to build up oil reserves amidst the Gulf crisis and to a lowbase of 1989 when the refinery had to stop operation for five weeks formaintenance purposes). When the value of petroleum products output isexcluded, overall industrial production increased by only 7 percent, andproduction in the public manufacturing sector declined by 21 percent in 1990.Part of this decline is due to the transfer if ownership of two large publicsector textile mills to the private sector which resulted in a 45 percentreduction in the output of Textile Corporation.

1.8 The construction sector expanded by a modest 2 percent in 1990,(compared to a growth of 0.6 percent in the preceding year) reflectingsluggish construction-intensive public investment (which declined in realterms by close to 30 percent) although the sector received some boost fromincreasing residential housing investment. Value added in the mining andquarrying sector rose by 9.1 percent in 1990 largely due to an expansion ofgem mining. Some other mining activities, however, suffered a decline inoutput due to the renewed fighting in the North and East.

1.9 The Services Sector. Like the agriculture sector, the servicessector accounted for one third of the total increase in GDP during 1990.Increased production in the agricultural and manufacturing sectors stimulatedgrowth in the transport, trade, banking, insurance and real estate services.Underlying this was the improved security situation in the country, a majorfactor in the recovery in tourism (covered in the "other services"sub-category). Tourist arrivals in 1990 recorded an increase of 62 percentover those of 1989.

-7-

2. Savings and Investment

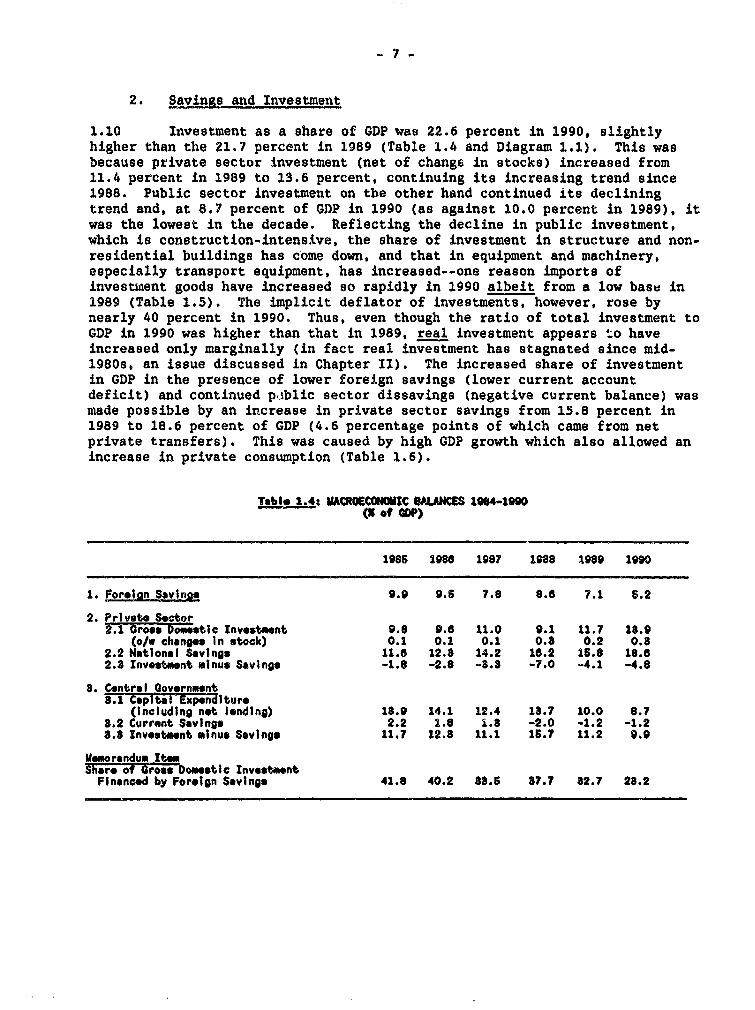

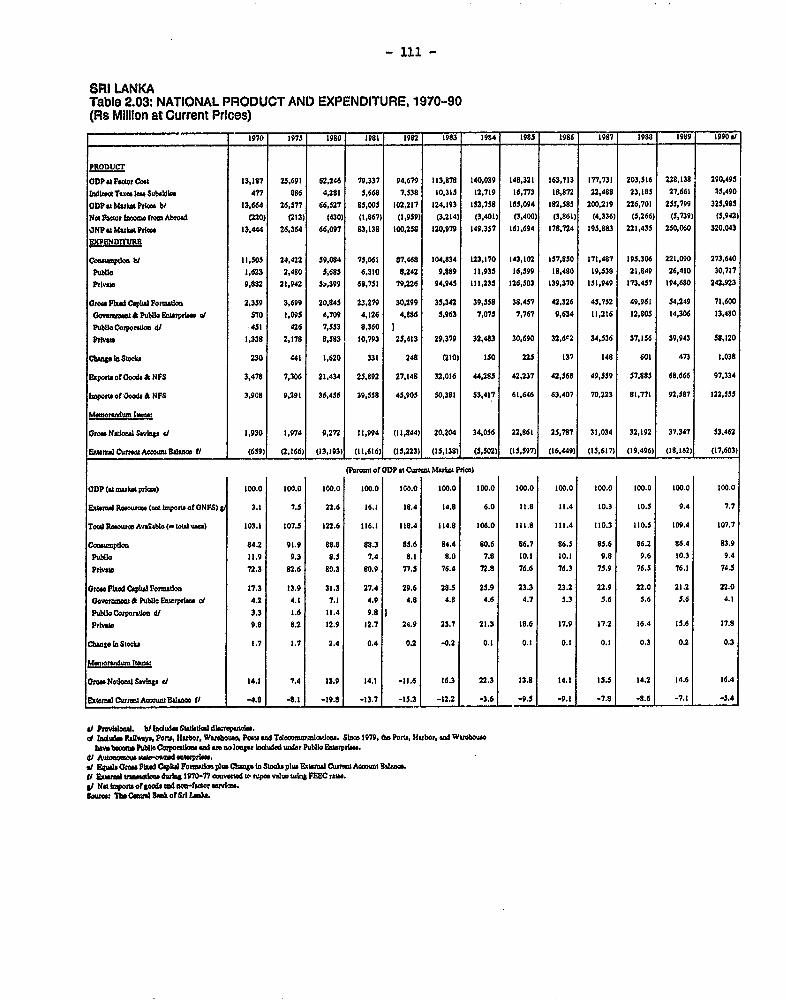

1.10 Investment as a share of GDP was 22.6 percent in 1990, slightlyhigher than the 21.7 percent in 1989 (Table 1.4 and Diagram 1.1). This wasbecause private sector investment (net of change in stocks) increased from11.4 percent in 1989 to 13.6 percent, continuing its increasing trend since1988. Public sector investment on the other hand continued its decliningtrend and, at 8.7 percent of GDP in 1990 (as against 10.0 percent in 1989), itwas the lowest in the decade. Reflecting the decline in public investment,which is construction-intensive, the share of investment in structure and non-residential buildings has come down, and that in equipment and machinery,especially transport equipment, has increased--one reason imports ofinvestinent goods have increased so rapidly in 1990 albeit from a low base in1989 (Table 1.5). The implicit deflator of investments, however, rose bynearly 40 percent in 1990. Thus, even though the ratio of total investment toGDP in 1990 was higher than that in 1989, real investment appears to haveincreased only marginally (in fact real investment has stagnated since mid-1980s, an issue discussed in Chapter II). The increased share of investmentin GDP in the presence of lower foreign savings (lower current accountdeficit) and continued p.Ablic sector dissavings (negative current balance) wasmade possible by an increase in private sector savings from 15.8 percent in1989 to 18.6 percent of GDP (4.6 percentage points of which came from netprivate transfers). This was caused by high GDP growth which also allowed anincrease in private consumption (Table 1.6).

Table 1.4s MACROENOMC 8ALANCOS 1864-1990-- ( of GDP)

19o5 1986 1987 1988 1989 1990

1. Forgian Savings 9.9 9.5 7.8 8.6 7.1 6.2

2. Private Sector2.1 Grove Doss tIc Investment 9.8 9.6 11.0 9.1 11.7 1.9

(o/w changes In stock) 0.1 0.1 0.1 0.8 0.2 0.82.2 National Savings 11.6 12.8 14.2 16.2 15. 8 18.62.8 Investment minus Saving. -1.8 -2.8 -3.8 -7.0 -4.1 -4.8

8. Central Government8.1 Capital Expenditure

(including not lending) 18.9 14.1 12.4 18.7 10.0 8.78.2 Current Savings 2.2 1.8 1.8 -2.0 -1.2 -1.28.8 Investment minus Savings 11.7 12.8 11.1 16.7 11.2 9.9

Memorandum ItemShare of arose Doometic investmentFinanced by Foreign Savings 41.8 40.2 38.6 87.7 82.7 28.2

-8-

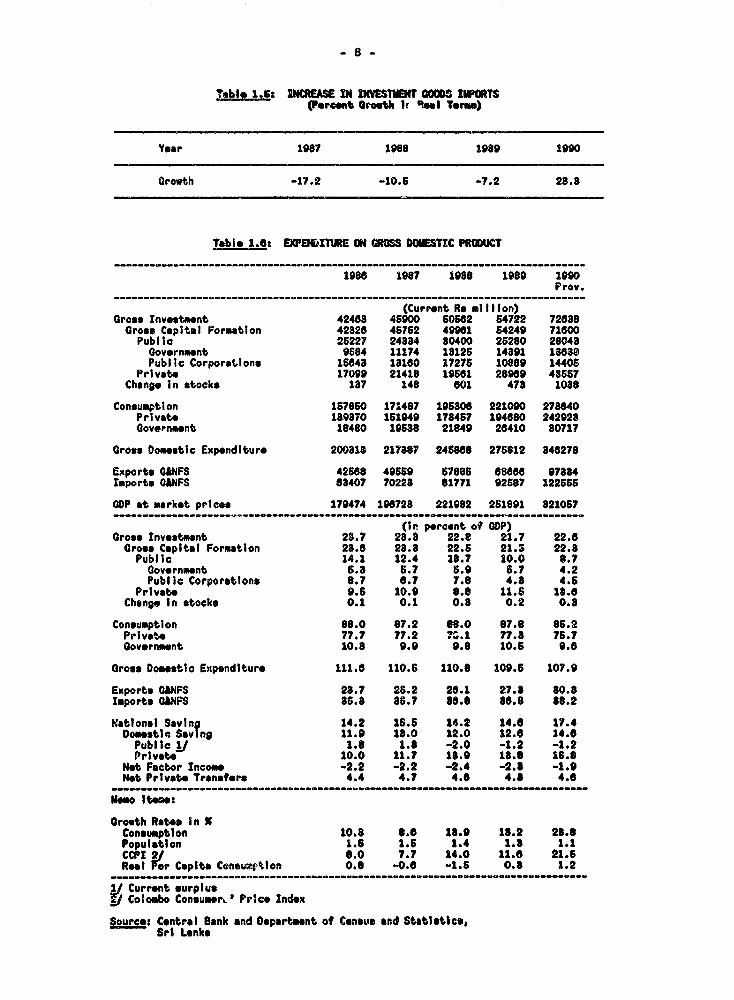

Table 1.5S INCREASE IN DINESTMFI C00WS0 IPORTS(Percent Growth Ir R l Term)

Year 1987 1988 1989 1990

Growth -17.2 -10.6 -7.2 28.8

Table 1.6: EXPENDZTURE ON OSS DCIESTIC PRODUCT

------------------------------------------------------------ __---------------__-

1986 1987 1988 1989 1990Prov.

------------------------------------------------------------------ __---------__-

(Current Re mlillon)Gross Invostment 42463 45900 50582 64722 72638

Gross Capital Formation 42826 4S762 49961 54249 71600Public 25227 24384 80400 26280 28048

Government 9684 11174 18126 14391 13688Public Corporations 16848 1816o 17276 10889 14406

Private 17099 21418 19681 28989 48657Change In stocks 137 148 601 478 1038

Consumption 157860 171487 195306 221090 273840Private 189370 161949 178457 194680 242928Government 18480 19388 21849 26410 80717

Grosv Domestic Expenditure 200818 217387 245868 276812 346278

Exports CO4FS 42688 49569 67885 6886s 97884Imports G1NFS 63407 70228 81771 92587 122565

GDP at market prices 179474 190728 221982 261891 821057

(in percent ot GDP)Gross Investment 28.7 28.8 22.e 21.7 22.6Gross Capital Formation 28.6 28.8 22.5 21.S 22.8Public 14.1 12.4 18.7 10.0 8.7Governmnt 5.8 6.7 6.9 5.7 4.2Public Corporatlons 8.7 6.7 7.8 4.8 4.6

Private 9.6 10.9 8.8 11.6 18.6Change In stocks 0.1 0.1 0.8 0.2 0.8

Consumption 88.0 67.2 68.0 87.8 85.2PrIvate 77.7 77.2 7v.1 77.8 76.7Government 10.8 9.9 9.8 10.6 9.6

Gross Domstlc Expenditure 111.6 110.6 110.8 109.6 107.9

Exports QihFS 28.7 26.2 26.1 27.8 80.8Imports GMNFS 86.8 86.7 #8.6 88.8 88.2

Natlonal Saving 14.2 1656 14.2 14.6 17.4Domestl Saving 11.9 18.0 12.0 12.6 14.6Public 1/ 1.6 1.8 -2.0 -1.2 -1.2Privat 10.0 11.7 18.0 18.8 16.8

Net Factor Income -2.2 -2.2 -2.4 -2.8 -1.9Not Private Transter* 4.4 4.7 4.6 4.8 4.6

Memo Iteo:

Orowth Rates In XConsumption 10.8 8.6 18.9 18.2 28.8Population 1.6 1.5 1.4 1.8 1.1CCPI 2/ 6.0 7.7 14.0 11.6 21.6Real For Capita Con**ition 0.8 -0.6 -1.6 0.8 1.2

1 Current surplusV Colombo ConsumerO Price Index

Source: Central fank and Doparteent ot Census and Statistics,Sri Lanka

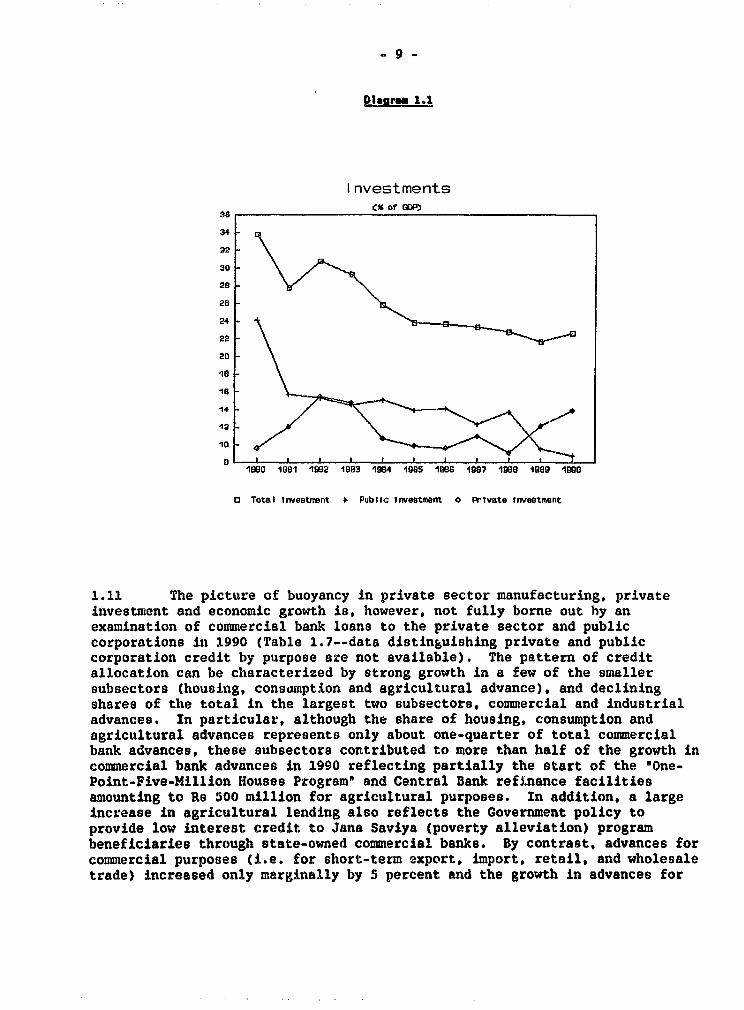

-9-

Diagram 1.1

I nvestmentsCM of GD3

S8_

34

32

30

28

28

24

22

20

la

14

12

10

1980 1981 1982 1983 1984 1G9S 1986 1987 1988 1989 1W90

a Toteai tnvesetrert 1 Pubitc Investment o PrTvate Investment

1.11 The picture of buoyancy in private sector manufacturing, privateinvestment and economic growth is, however, not fully borne out by anexamination of commercial bank loans to the private sector and publiccorporations in 1990 (Table 1.7--data distinguishing private and publiccorporation credit by purpose are not available). The pattern of creditallocation can be characterized by strong growth in a few of the smallersubsectors (housing, consamption and agricultural advance), and decliningshares of the total in the largest two subsectors, commercial and industrialadvances. In particular, although the share of housing, consumption andagricultural advances represents only about one-quarter of total commercialbank advances, these subsectors contributed to more than half of the growth incommercial bank advances in 1990 reflecting partially the start of the "One-Point-Five-Million Houses Program" and Central Bank refinance facilitiesamounting to Re 500 million for agricultural purposes. In addition, a largeincrease in agricultural lending also reflects the Government policy toprovide low interest credit to Jana Saviya (poverty alleviation) programbeneficiaries through state-owned commercial banks. By contrast, advances forcommercial purposes (i.e. for short-tenm export, import, retail, and wholesaletrade) increased only marginally by 5 percent and the growth in advances for

- 10

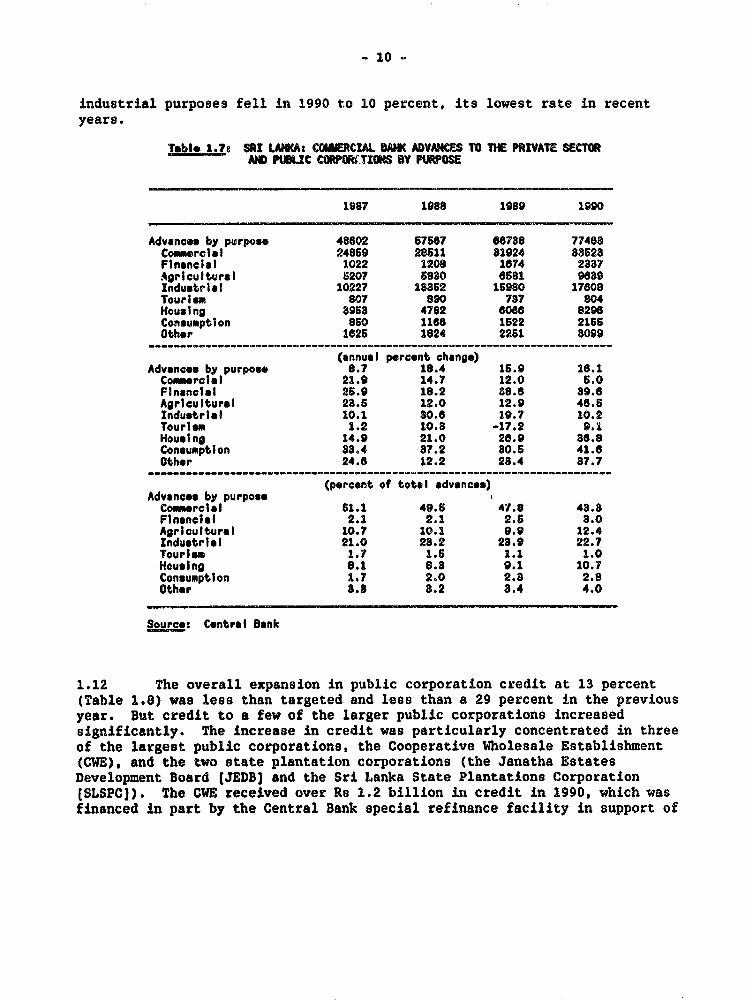

industrial purposes fell in 1990 to 10 percent, its lowest rate in recentyears.

Table 1.7s SRI LACA: COMMERCIAL BMI ADVANCES TOTHE PRIVATE SECTORAND PUBLC CORPTXONS BY PURPOSE

1987 1988 1989 1990

Advances by purpose 48602 67687 68788 77408Coomrcial 24859 28511 81924 33628Financial 1022 1208 1874 2337Agricultural 6207 5830 8s81 9839Industrial 10227 13562 16980 17808Tourism 807 890 737 804Housing 3968 4782 6068 8298Consumption 860 1186 1522 2166Other 1625 1824 2251 3099

(annual percent change)Advanco by purpose 8.7 18.4 15.9 16.1Commercial 21.9 14.7 12.0 6.0Financial 25.9 18.2 88.6 39.6Agricultural 23.6 12.0 12.9 46.5Industrial 10.1 80.8 19.7 10.2Tourism 1.2 10.8 -17.2 9.1Housing 14.9 21.0 28.9 86.8Consumption 83.4 37.2 30.6 41.6Other 24.6 12.2 23.4 37.7

(percent of total advances)Advances by purposeCowmrclal 61.1 49.6 47.8 43.8Financial 2.1 2.1 2.5 3.0Agricultural 10.7 10.1 9.9 12.4Industrlsl 21.0 23.2 23.9 22.7Tourism 1.7 1.5 1.1 1.0Housing 8.1 8.8 9.1 10.7Consumption 1.7 2.0 2.3 2.8Other 8.8 8.2 3.4 4.0

Source: Central Bank

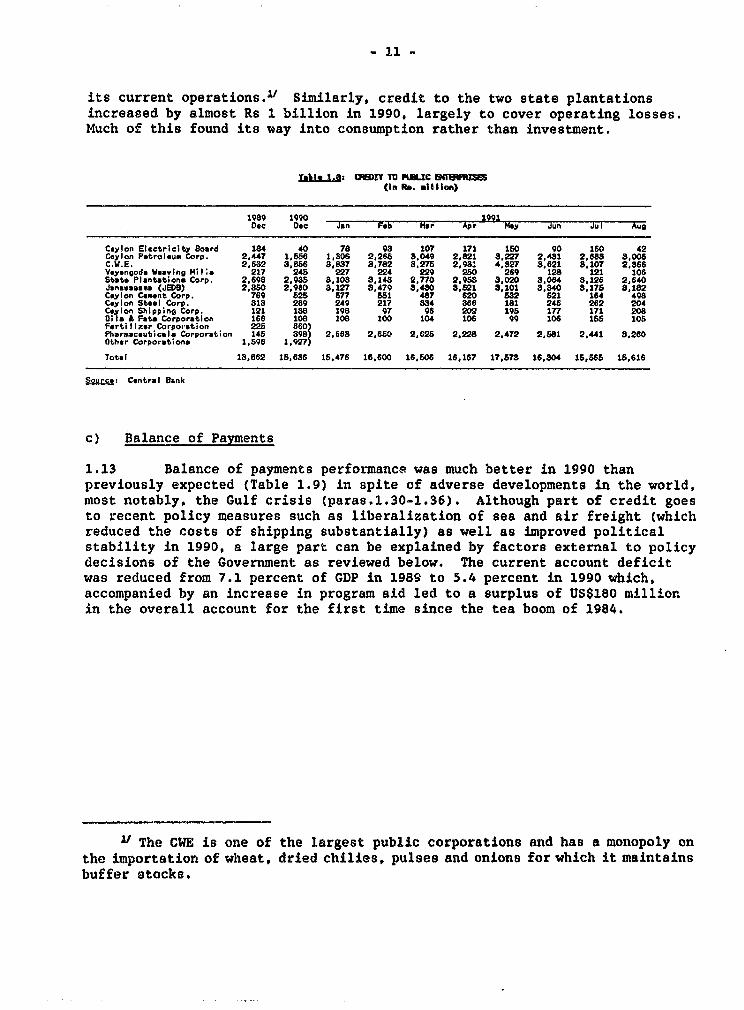

1.12 The overall expansion in public corporation credit at 13 percent(Table 1.8) was lees than targeted and less than a 29 percent in the previousyear. But credit to a few of the larger public corporations increasedsignificantly. The increase in credit was particularly concentrated in threeof the largest public corporations, the Cooperative Wholesale Establishment(CWE), and the two state plantation corporations (the Janatha EstatesDevelopment Board (JEDBJ and the Sri Lanka State Plantations Corporation(SLSPC]). The CWE received over Re 1.2 billion in credit in 1990, which wasfinanced in part by the Central Bank special refinance facility in support of

- 11 -

its current operations. Similarly, credit to the two state plantationsincreased by almost Rs 1 billion in 1990, largely to cover operating losses.Much of this found its way into consumption rather than investment.

ZIkLt-.I: aRr2T TO PWUC 8lWRl_(I n Rs. l I I ton)

1989 1090 1991Dtec Oc Jan F b Mar Apr May Jun Jul Aug

Ceylon Electricity Board 184 40 78 98 107 171 180 90 160 42Ceylon Petroleum Corp. 2,447 1,580 1,306 2,265 8.049 2,821 9.227 2,481 2,S88 8,008C.W.' 2,682 3,856 8,837 8,782 8.278 2,981 4,827 8,621 8,107 2,866Veyangod Weaing ;1; 217 24S 227 224 229 280 269 128 121 108st.et Plent,tion- Corp. 2,698 2,938 8,108 8,148 2,770 2,9S8 3,020 3S064 8,126 2,640Janaweamas (JED8) 2,80 2,O90 8,127 3,479 8,430 3.821 3.101 a.340 S,17S 8,182Ceylon Cemnt. Corp. 769 525 877 551 487 620 532 821 164 498Ceylon Steel Corp. S31 289 240 217 334 856 181 246 262 204Ceylon Shipping Corp. 121 188 198 97 98 202 19S 177 171 208Bil& & Fats Corporation 166 108 108 100 104 106 99 10 185 108Fertilizer Corporation 225 660)Pharamaceuticale Corporation 148 898) 2,668 2,6t0 2,628 2,228 2,472 2,581 2,441 8.260Other Corporationa 1,596 1,927)

Total 18,862 15,686 15,476 16,600 16,606 16,167 17,678 16,804 16,865 15,616

5ource: Central Bank

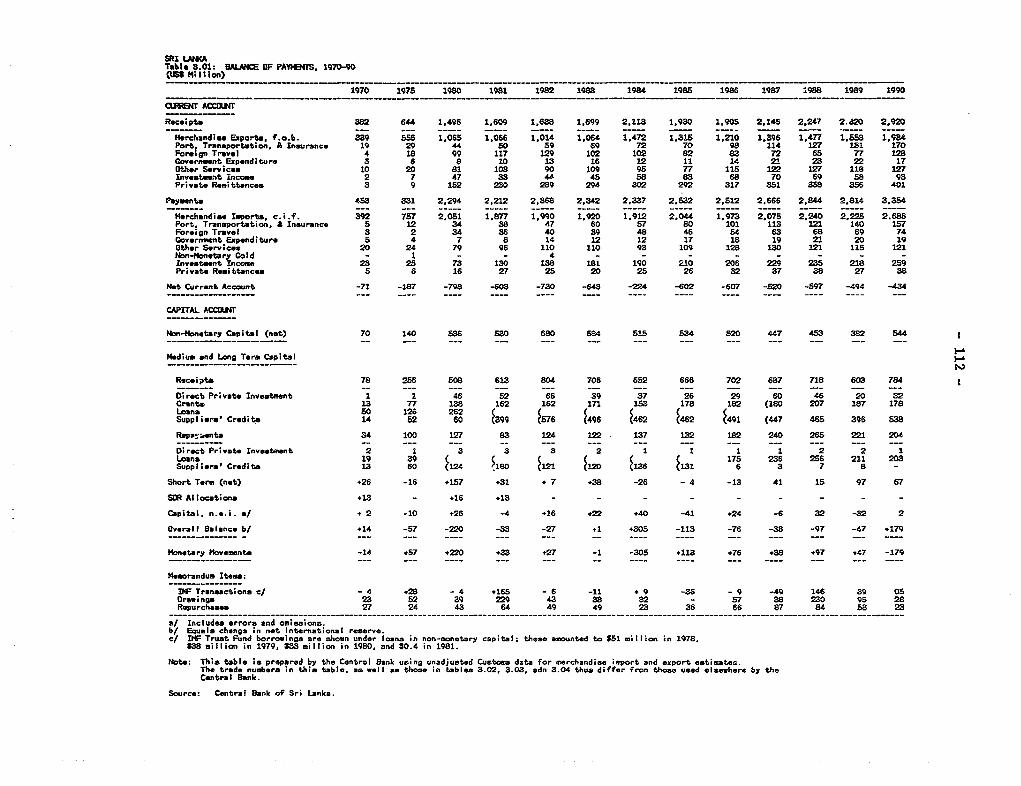

c) Balance of Payments

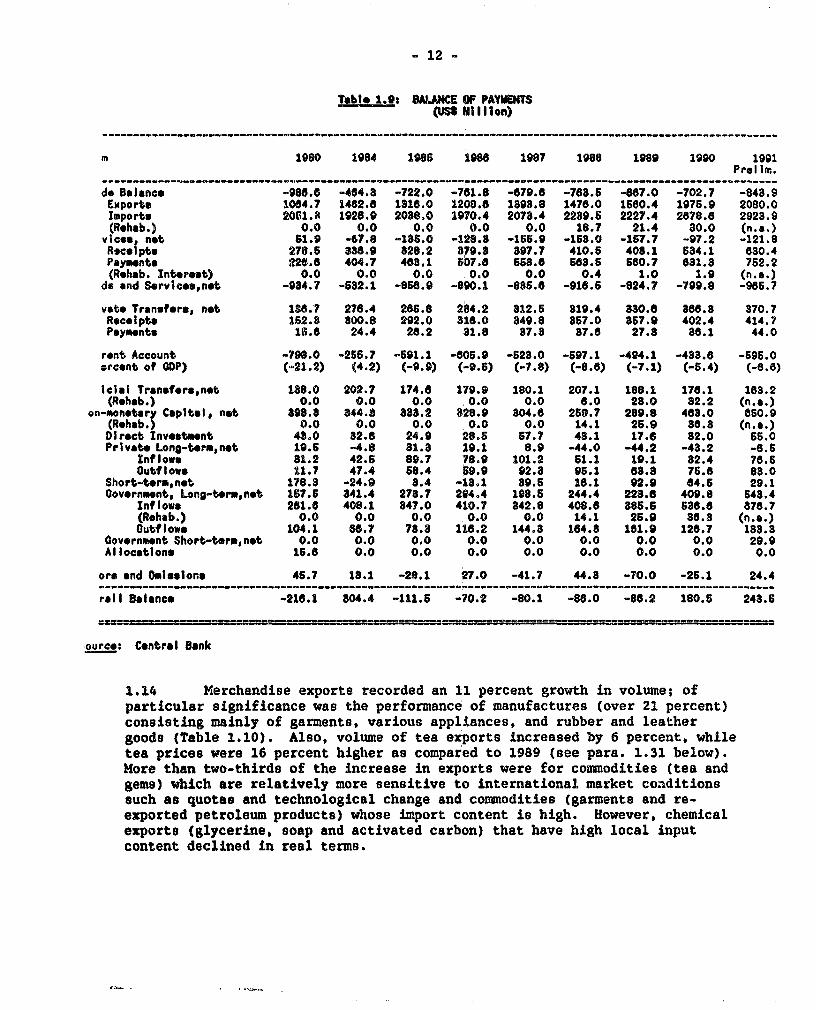

1.13 Balance of payments performance was much better in 1990 thanpreviously expected (Table 1.9) in spite of adverse developments in the world,most notably, the Gulf crisis (paras.1.30-1.36). Although part of credit goesto recent policy measures such as liberalization of sea and air freight (whichreduced the costs of shipping substantially) as well as improved politicalstability in 1990, a large part can be explained by factors external to policydecisions of the Government as reviewed below. The current account deficitwas reduced from 7.1 percent of GDP in 1989 to 5.4 percent in 1990 which,accompanied by an increase in program aid led to a surplus of US$180 millior.in the overall account for the first time since the tea boom of 1984.

l/ The CWE is one of the largest public corporations and has a monopoly onthe importation of wlheat, dried chilies, pulses and onions for which it maintainsbuffer stocks.

- 12 -

Tblei 1.9: WAKUCE OF PAYiS(US$ MllIIIon)

mn 1980 1984 1985 1988 1987 1988 1989 1990 1991Prol mn.

do Balance -986.8 -464.8 -722.0 -761.8 -679.8 -7683.6 -687.0 -702.7 -843.9Exports 1064.7 1462.6 1318.0 1208.6 1893.8 1478.0 1680.4 1976.9 2080.0Imports 2061.R 1926.9 2038.0 1970.4 2078.4 2239.5 2227.4 2678.6 2923.9(R*hab.) 0.0 0.0 0.0 0.0 0.0 18.7 21.4 30.0 (n.a.)

vico, not 61.9 -67.8 -136.0 -128.8 -165.9 -168.0 -167.7 -97.2 -121.8Recelpts 278.6 336.9 828.2 379.8 397.7 410.6 403.1 534.1 e60.4Payments 226.8 404.7 468.1 607.8 563.6 683.6 680.7 631.3 762.2(Rohab. Interest) 0.0 0.0 0.0 00 0.0 0.4 1.0 1.9 (n.e.)

de and Servicoo,n.t -934.7 -632.1 -856.9 -890.1 -835.6 -916.5 -824.7 -799.8 -985.7

vet, Transfere, net 186.7 276.4 285.8 284.2 312.6 319.4 830.6 866.3 370.7Receipts 152.3 800.8 292.0 316.0 849.8 367.0 367.9 402.4 414.7Payments 16.8 24.4 28.2 31.8 37.8 37.6 27.8 36.1 44.0

rent Account -798.0 -256.7 -691.1 -605.9 -523.0 -597.1 -494.1 -433.6 -696.0ercent of ODP) (.21.2) (4.2) (-9.9) (-9.5) (-7.8) (-8.6) (-7.1) (-5.4) (-8.6)

icial Transfers,not 138.0 202.7 174.6 179.9 180.1 207.1 188.1 176.1 163.2(Rehab.) 0°0 0.0 0.0 0.0 0.0 6.0 23.0 82.2 (n.o.)

on-monetary Capital, not 390.3 344.8 388.2 828.9 804.6 259.7 289.8 468.0 650.9(Reheb.) 0.0 0.0 0.0 0.0 0.0 14.1 25.9 36.8 (n.e.)Direct Investment 48.0 82.6 24.9 28.6 67.7 48.1 17.6 32.0 66.0Private Long-term,not 19.6 -4.8 31.3 19.1 8.9 -44.0 -44.2 -43.2 -6.6

Inflows 81.2 42.5 89.7 78.9 101.2 51.1 19.1 32.4 76.6Outflows 11.7 47.4 S8.4 t9.9 92.8 95.1 68.8 76.6 83.0

Short-term,not 178.3 -24.9 3.4 -13.1 89.6 16.1 92.9 64.6 29.1Governmnt, Long-teru,net 167.6 841.4 273.7 294.4 198.5 244.4 223.6 409.8 643.4

Inflows 261.6 408.1 347.0 410.? 842.8 408.6 386.6 658.6 876.7(Rehab.) 0.0 0.0 0.0 0.0 0.0 14.1 26.9 38.8 (n.a.)Outflows 104.1 o6.7 73.3 118.2 144.3 164.8 161.9 126.7 183.3

Government Short-term,not 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 29.9Allocations 16.6 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

or and Omissions 46.7 18.1 -28.1 27.0 -41.7 44.3 -70.0 -26.1 24.4

roil Balance -216.1 804.4 -111.6 -70.2 -80.1 -88.0 -88.2 180.5 243.6

ource: Central Bank

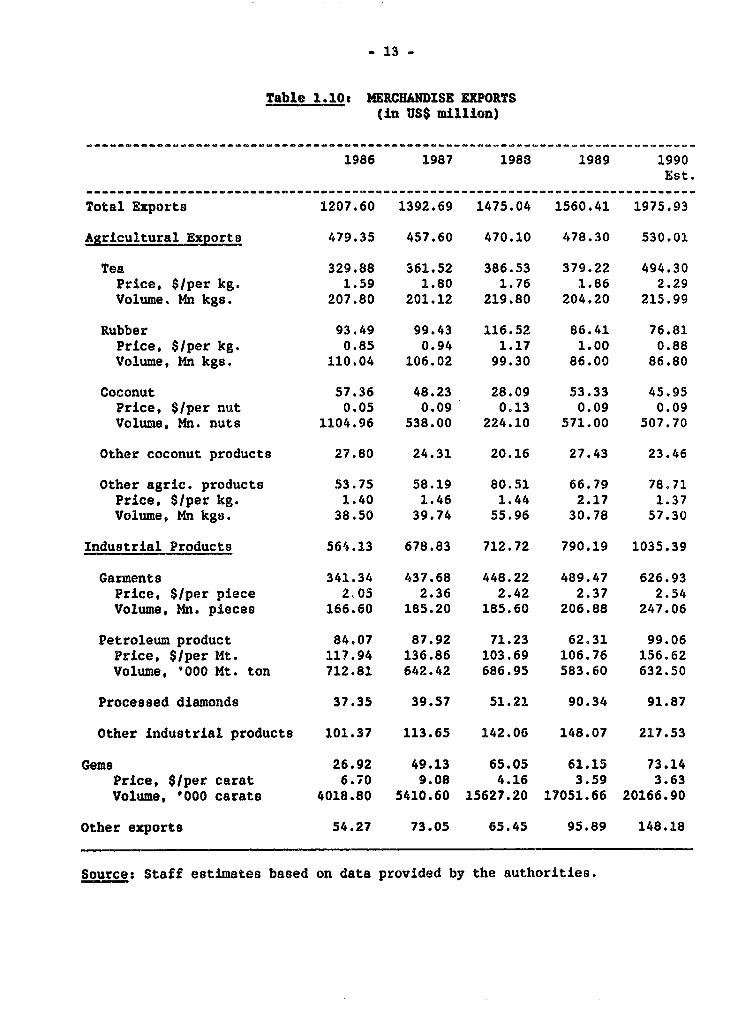

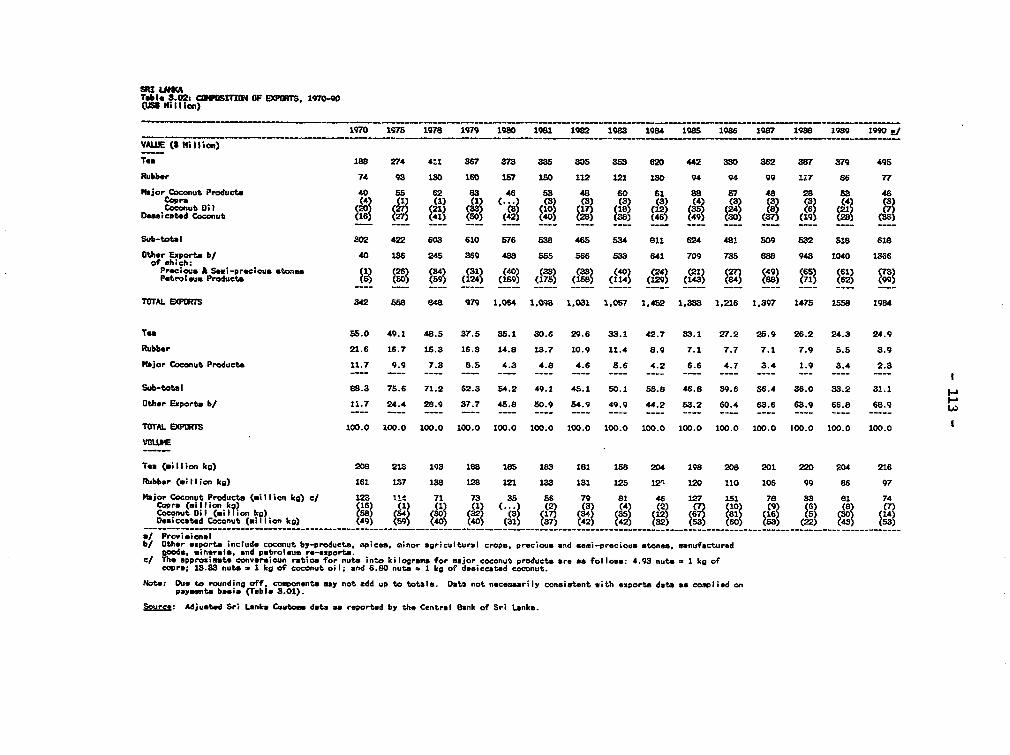

1.14 Merchandise exports recorded an 11 percent growth in volume; ofparticular significance was the performance of manufactures (over 21 percent)consisting mainly of garments, various appliances, and rubber and leathergoods (Table 1.10). Also, volume of tea exports increased by 6 percent, whiletea prices were 16 percent higher as compared to 1989 (see para. 1.31 below).More than two-thirds of the increase in exports were for comiodities (tea andgems) which are relatively more sensitive to international market conditionssuch as quotas and technological change and commodities (garments and re-exported petroleum products) whose import content is high. However, chemicalexports (glycerine, soap and activated carbon) that have high local inputcontent declined in real terms.

_ 13 -

Table 1.10: MERCHANDISE EXPORTS(in USS million)

1986 1987 1988 1989 1990Est.

Total Exports 1207.60 1392.69 1475.04 1560.41 1975.93

Agricultural Exports 479.35 457.60 470.10 478.30 530.01

Tea 329.88 361.52 386.53 379.22 494.30Price, $/per kg. 1.59 1.80 1.76 1.86 2.29Volume. Mn kgs. 207.80 201.12 219.80 204.20 215.99

Rubber 93.49 99.43 116.52 86.41 76.81Price, S/per kg. 0.85 0.94 1.17 1.00 0.88Volume, Mn kgs. 110.04 106.02 99.30 86.00 86.80

Coconut 57.36 48.23 28.09 53.33 45.95Price, $/per nut 0.05 0.09 0.13 0.09 0.09Volume, Mn. nuts 1104.96 538.00 224.10 571.00 507.70

Other coconut products 27.80 24.31 20.16 27.43 23.46

Other agric. products 53.75 58.19 80.51 66.79 78.71Price, $/per kg. 1.40 1.46 1.44 2.17 1.37Volume, Mn kgs. 38.50 39.74 55.96 30.78 57.30

Industrial Products 564.13 678.83 712.72 790.19 1035.39

Garments 341.34 437.68 448.22 489.47 626.93Price, $/per piece 2.05 2.36 2.42 2.37 2.54Volume, Mn. pieces 166.60 185.20 185.60 206.88 247.06

Petroleum product 84.07 87.92 71.23 62.31 99.06Price, $/per Mt. 117.94 136.86 103.69 106.76 156.62Volume, '000 Mt. ton 712.81 642.42 686.95 583.60 632.50

Processed diamonds 37.35 39.57 51.21 90.34 91.87

Other industrial products 101.37 113.65 142.06 148.07 217.53

Gems 26.92 49.13 65.05 61.15 73.14Price, S/per carat 6.70 9.08 4.16 3.59 3.63Volume, '000 carats 4018.80 5410.60 15627.20 17051.66 20166.90

Other exports 54.27 73.05 65.45 95.89 148.18

Source: Staff estimates based on data provided by the authorities.

- 14 -

1.15 These latter developments occurred in a situation where the nominalexchange rate had remained virtually fixed at around Rs 40 to the US dollarfrom September 1989 till the end of 1990 despite inflation in excess of 20percent (Diagram 1.2)V. Real appreciation during 1990 was limited to 6-7percent due to the substantial real depreciation of the US dollar (theintervention currency) vis-a-vis other major world currencies in the secondhalf of 1990. But, in 1991, as the dollar started to appreciate, the rupeeappreciated an additional 12 percent in real terms. Although the rate movedfrom about Rs 40 in early 1991 to Rs 42 to the US dollar in November 1991,this did not offset the real appreciation of the currency. The introductionof a more market-oriented system of exchange rate determination in August 1990(based on weighted average of the previous day's interbank transaction rates)has not provided enough flexibility to encourage exports with substantiallocal input or value added content because the Central Bank is also a majorplayer in the interbank market.

Diagram 1.2

PRe&I Effective Exchange Pate 1989-1991

40

07

94

4340

40

.011

0,~~~~W,

(1980=100, an i ncrss means mal a pproci tlon)

1.16 The tourism industry which had been seriously affected by the civildisturbances showed a remarkable recovery in 1990, as arrivals increased by 62percent. Contrary to expectations at the start of the Gulf crisis,

,v The real effective exchange rate is calibrated taking into considerationboth trade-weightLed effective rate and movement of exchange rates of countriescompeting with Sri Lanka for export markets.

- 15 -

remittances of workers from Gulf countries showed a robust increase of 11percer. in US dollar terms, as many panic-stricken workers remitted to SriLanka their savings (see paras.l.32-1.33). On the import side, favorableweather conditions and the resulting good paddy production allowed riceimports to be almost halved as compared to 1989. Imports of petroleum,however, increased reflecting higher prices and the felt need to holdstrategic reserves. Terms of trade declined only marginally by about 1percent.

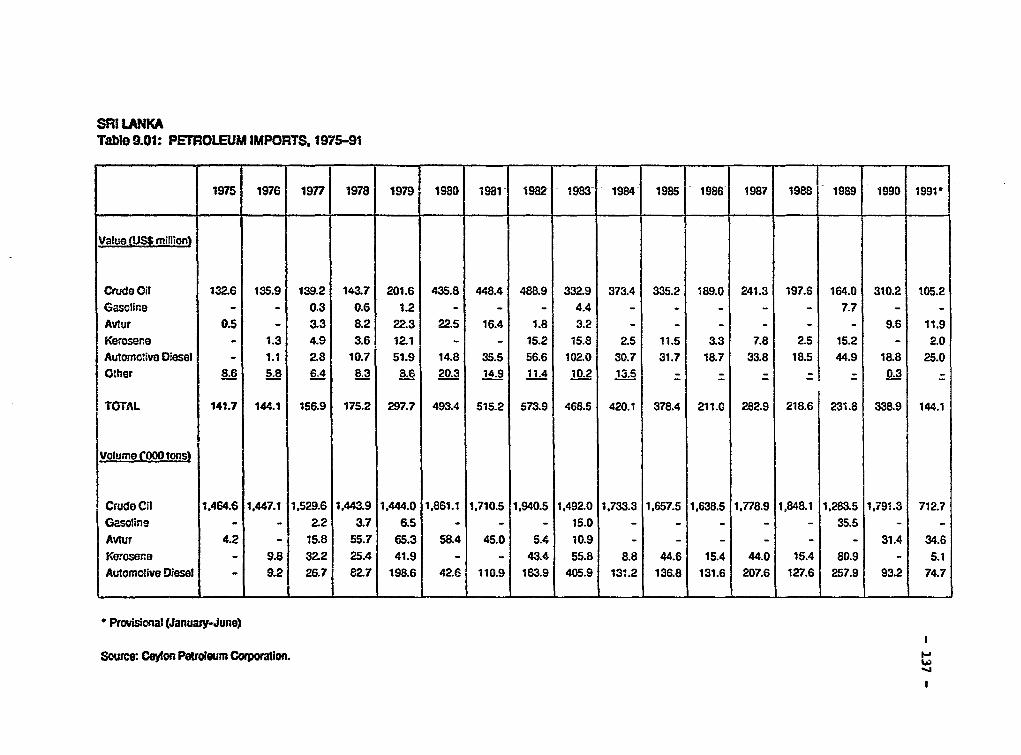

1.17 In 1990 a new pattern of external assistance seems to be emergingwhereby external resource transfers to Sri Lanka are achieved through arelatively high contribution of balance-of-payments support rather thanproject-related aid. Not only did official grants decline due to a large dropin commodity aid, but project-related disbursements in nominal US dollar termsstayed at the level of 1989. This was rather disappointing becausedisbursements in 1989 were already low on account of slow projectimplementation. These shortfalls, however, were more than offset bydisbursements of program loans by IDA and ADB which amounted to about US$90million in 1990 (as compared to US$29 million in 1989). The level of foreigndirect investment grew rapidly form the small base in 1989 but still remainedrelatively low at about US$32 million in 1990, underscoring the difficulty ofpromoting Sri Lanka's image abroad as a "foreign investment haven" in the faceof ongoing civil conflict. There was also a 20 percent reduction inamortization payments, as a result of the government paying off the bulk ofshort-term nonconcessional loans in 1989. The debt service ratio improvedfurther and remained relatively low at 14 percent of exports and non factorservices. Notwithstanding these favorable developments, gross officialforeign exchange reserves still cover only about 2 months of merchandiseimports.

1.18 Preliminary data for 1991 indicate an increase in current accountdeficit to 6.6 percent of GDP from the 5.4 percent achieved in 1990--primarilybecause of higher than projected imports of "non-grain food", "non-foodconsumer goods" and "textile as intermediate inputs". Most of the increase in"non-food consumer goods" imports was due to cars and motor cycles while hightextile imports reflect adjustment of input stocks. The increased imports ofconsumer goods in general were probably a result of an increased degree ofimport liberalization in an environment where bias toward consumption wasstrong as discussed in Chapter II. The amount of nominal exports at slightlyabove US$2 billion (real growth of 4.8 percent over 1990) was largely asexpected. There are, however, some worrisome signs. Real growth of exportsof "other" agricultural and industrial goods (which are presumably the engineof export-led growth) has been much less than anticipated, with the formersuffering negative growth implying that the Government could do much more toencourage non-traditional exports including in the areas of exchange ratemanagement. Private transfers on the other hand recorded modest but positivenominal growth despite the expectation that this would decline due to anexpected loss in remittances/transfers from migrant workers abroad as a resultof the Gulf crisis-induced return of a substantial number in 1990. In fact,the expected decline in workers' remittances in 1991 appears to have occurred.But, as the economy has been doing rather well in 1990 and 1991, there appears

- 16

to have been a reverse flow of earlier capital flight, probably amounting toat least about US$40 million. This latter helped realize the overall increasein private transfers. On the capital account, foreign investment increasedsubstantially to US$55 million reflecting the relative stability in theeconomic and political environment. Most of the increase in foreigninvestment, however, was due to investment in existing shares rather thanfixed capital formation. Finally aid disbursements increased by about US$80million over the level in 1990. But, because disbursements of balance-of-payments support increased by almost US$ 200 million, nominal project aiddisbursements appear to have been below the 1990 level.

d) Fiscal Developments

1.19 Fiscal operations in 1990 also showed progress irn terms ofadjustment of macroeconomic aggregates; the overall deficit was contained to9.9 percent of GDP, (Table 1.11). This is because revenues were enhanced byreceipts from domestic turn-over taxes (38 percent above the 1989 level) andincome taxes (43 percent increase). These improvements derive fromaccelerated economic activity and increased efficiency in tax collection.Total expenditures on the other hand were contained to 31.1 percent of GDPcompar,I with the budgeted 31.7 percent or the 1989 actual of 32.6 percent.This expenditure level was, however, achieved primarily because publicinvestment (capital expenditures and net lending) was further reduced to 8.7percent of GDP from 10 percent in 1989.

Imbls..L1: 5.SItf OF CETARL CO^V844E FISCA OPERATIONS, 19691(Percent of GP)

---------------------------------------------------------------------- ___-----__----------------------

Budget Preli. Budget1986 1987 1988 1989 1Q90 1991 1991 1992

Total Revenue und Grant- 22.8 28.8 21.8 24.0 23.3 20.0 21.8 21.2

Total Revenue 20.7 21.4 18.8 21.4 21.2 18.7 19.7 19.2Ta.r 17.4 17.9 16.2 18.9 19.1 17.0 17.8 17.3Nontex 3.3 3.6 2.6 2.6 2.1 1.7 2.2 1.9

Grants 2.1 2.4 3.0 2.5 2.1 2.1 2.1 2.0

Toat; &ip. Not Lend;ng 3.0 32.6 34.8 82.6 S3.1 28.1 so.8 28.0Current 18.9 20.1 20.8 22.6 22.4 19.1 21.2 19.0Capital A Net Lending 14.1 12.4 13.7 10.0 8.7 9.0 9.2 1/ 10.1

Current Account Sur/Dof(-) 1.8 1.3 -2.0 -1.2 -1.2 -0.4 -1.5 0.2

Deficit (before grants) -12.2 -11.1 -15.7 -11.2 -9.9 -9.4 -10.8 -8.0

Deficit (after grants) -10.1 -8.7 -12.7 -8.6 -7.8 -7.3 -8.6 -6.8

Financing 10.1 8.7 12.7 8.6 7.8 7.3 8.6 6.8

Foreign iorrouine 8.0 2.9 3.2 2.4 3.6 6.2 5.0 4.9Dlebureoment. 6.7 5.3 5.6 4.6 8.2 6.5 -Amortizatione 1.7 2.4 2.8 2.8 1.5 1.8 -

Net Domestic 8.1 5.8 9.6 4.9 4.9 2.1 3.7 2.1Bank financing 1.7 1.9 4.8 -1.8 0.1 -1.2 -0.8 0.0Nonbank financing 8.4 4.0 4.9 6.2 4.7 3.8 4.0 2.1

Arrear 0.0 0.0 0.0 1.4 --. 7 0.0 - -

I/ 0.5 percentage pointo of this is due to privatization. Capital epPeiditure and traditional netlending sount to 8.7 percent of DP.

Source: Central Bunk ond the Trenaury

1.20 The pressure for increased recurrent expenditures was strong during1990 because of, among others: the civil conflict in the North and East (an

- 17

additional Rs 4.5 billion was allocated for this purpose in a mid-yearsupplementary budget); severance payments for continued public sector laborretrenchment (Rs 2.3 billion); and the revived mid-day meal program (Rs 1.5billion although Rs 1.1 billion was actually disbursed for this program). Inaddition, probably because of the tight control on fund releases in 1989 aspart of the stabilization efforts started in mid-1989, many of the claimsaccrued to the Government during the second half of 1989 had not been paidwithin the same year; the authorities found that they had to pay in 1990accumulated arrears amounting to Rs 3.5 billion.

1.21 In 1991, the strong pressure for increased recurrent expendituresremained due to the civil conflict in the North and East while the refugeesfrom the affected areas needed to be taken care of. Supplementaryexpenditures for these two purposes have been at Rs 5 billion and Rs 1.9billion, respectively. Together with the public sector restructuring cost(additional pension of Rs 2.2 billion, and unpaid transport staff severancepayments of Rs 3.8 billion), expenditures for 1991 over and above theoriginally budgeted figures are currently expected to be Rs 13.5 billion (3.6percent of projected 1991 GDP). Although increased savings and revenuesattenuated the situation somewhat, more of these efforts could have been made,e.g., making the defense levy and additional excises effective as of November1991 rather than a later date in 1992 announced in the budget. As a result,it is estimated that the current deficit was 1.5 percent of GDP in 1991 andthe overall deficit 10.8 percent exceeding the Government's target of 10.1percent by a significant margin. In addition to the insufficient efforts madeto offset increased military and other expenditures, the Government morerecently appears to be making ad hoc decisions that are intended to tackledifferent problems piecemeal rather than in a consistent policy framework. (Acase in point is a government-sponsored training program for unemployedgraduates with provision of substantial stipend so that they become employableby the private sector.) It is also noteworthy that, as stated above, theproject disbursements in 1991 declined nominally in US dollar terms over 1990disbursements implying further slow down of implementation of major projects.The increased disbursements of balance-of-payments aid has more than offsetthis decline in financing the budget deficit.