Embed Size (px)

Citation preview

Accounting approaches in the 1990soften enabled aggressively priced trans-actions to be immediately accretive tothe buyer’s earnings, but subsequentlyrequiring a continuing stream of futuretransactions to keep earnings increasing.The high prices paid in these transac-tions eventually came home to roost in anumber of companies, as the underlyingeconomic value realities of the acquiredbusiness emerged.

Many experienced insurance companybuyers have become more conservative inpricing potential insurance companytargets. In a number of recent cases, sellerobjectives have not reduced commensu-rately, which in turn resulted in an unusualnumber of aborted sale attempts.

The pace of insurance M&A transactionshas slowed considerably over the pastcouple of years. This decline can beattributed to a number of factors,including emerging new risks anduncertainties (e.g., terrorism),weak equitymarkets

and a general decision malaise. Mostexperts predict that, once the economyand related consumer confidence pickup, the pace of deals will surge again.Although I agree that the activity levelwill likely pick up in the future, the char-acter of future insurance M&A deals willchange in several fundamental ways.

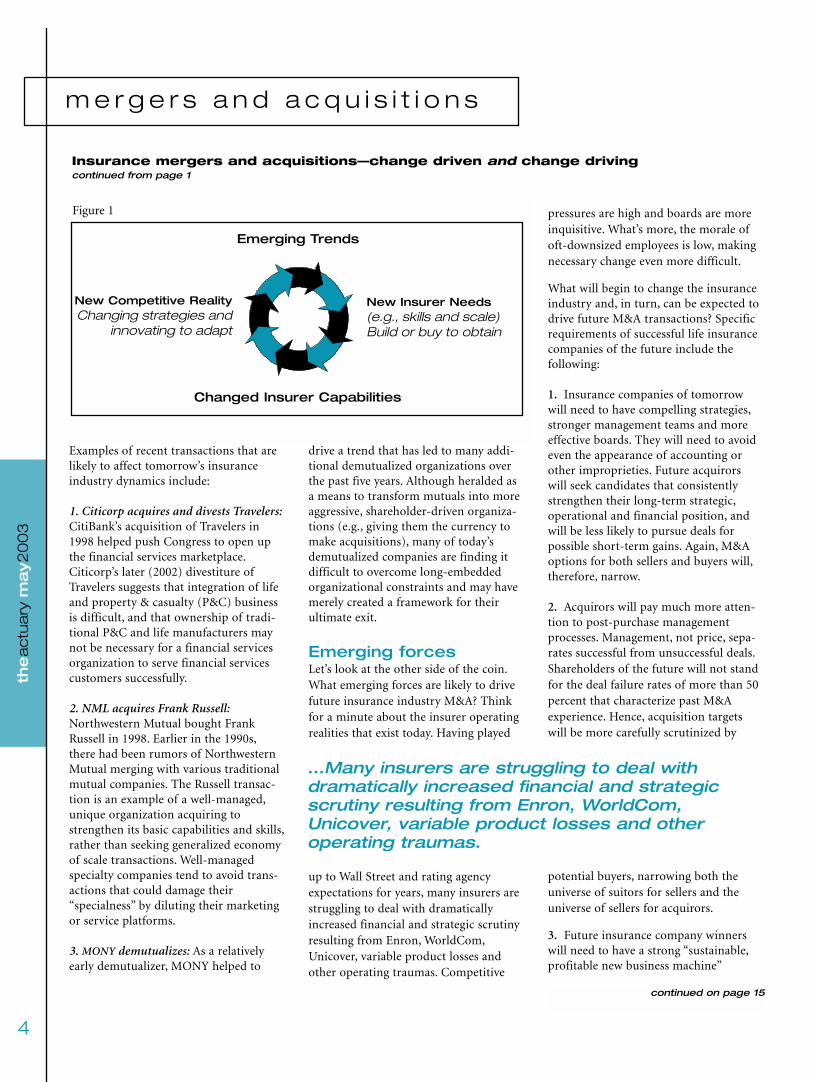

M&A as a function anddriver of changeM&A both drives and is driven bymarketplace change. There is a continu-ally evolving relationship between thechanging needs and wants of insurerstakeholders (e.g., customers, employeesand agents) and insurer M&A activity.For example, as distributors havebecome increasingly scarce and highlyvalued, there has been an escalation ininsurance distribution deals—for exam-ple, insurer and bank acquisitions ofmarketing companies (e.g., Essex andPlanco) and the proliferation of distri-

bution rollups (e.g., USI and NFS).What do recent insurance M&A

transactions portend for theinsurance industry? What emerg-ing marketplace, economic andinsurance industry trends willshape future insurance M&A?As a starting point in address-

ing these questions,consider the simplepicture in Figure 1 onpage 4 of how M&Aboth reflects and

creates change.

The 1990s were characterized byan active, often frenetic, insur-ance mergers and acquisitions

(M&A) market. Many transactionsclosed at prices that were high relativeto historical standards. This aggressivetransaction activity and pricing wasdriven by a number of factors, includ-ing the limited organic growth capacityof many insurers, high valuationsplaced on companies by European andother strategic buyers and aggressiveaccounting tactics that, in part,reflected the increasing prevalence ofstock option incentives.

vol.

37

, no

. 5

inside

the newsletter of theSociety of Actuaries

theactuarymay 2003

Insurance mergers and acquisitions—changedriven and change drivingby Robert D. Shapiro

continued on page 4

Editorial: Oh, what a hangover!by Morris Fishman .....................2

Letters to the editor......................3

Who owns your intellectual property?by Tom Bakos ...............................5

Regulators and insureds also have a stake in mergers and acquisitionsby Robert Wilcox and Carl Harris......................................7

SOA Board of Governors endorsesE&E redesign direction..................11

CE corner......................................14

Executive director news .................18

Presidential musings.......................19

Puzzle.........................................20

Mer

ger

s

Acq

uis

itio

ns

EditorJay A. Novik, FSA

Associate EditorsMorris Fishman, FSA

[email protected] S. Kalman, FSA

[email protected] N. Parikh, FSA

[email protected] Perrott, FSA

[email protected]. Steven Prince, FSA

Assistant EditorLoretta J. Jacobs, FSA

Contributing EditorsAnna M. Rappaport, FSA

[email protected] D. Shapiro, FSA

Puzzle EditorsLouise Thiessen, FSA

[email protected] Kinsky, FSA

[email protected] Dreher, ASA, [email protected]

Society Staff Contacts: 847.706.3500Clay Baznik, Publishing Director

[email protected] G. Coleman, Associate Editor

The Actuary welcomes articles and letters.Send correspondence to:

The Actuary

475 North Martingale Road, Suite 800Schaumburg, IL 60173-2226

Web site: www.soa.org

The Actuary is published monthly (except July and August).

Harry H. Panjer, FSA, PresidentBoard Advisory Group on Publications

Shirley Hwei-Chung Shao, FSATom Bakos, FSA

R. Thomas Herget, FSA

Nonmember subscriptions: students, $15; others, $30.Send subscriptions to: Society of Actuaries, P.O. Box

95668, Chicago, IL 60694.

2

the

ac

tua

ry m

ay

20

03

the newsletter of the Society of Actuaries

Vol. 37, No. 5 • May 2003

theactuary

Morris Fishman

Editor responsible

for this issue

Copyright © 2003, Society of Actuaries.The Society of Actuaries is not responsible for statements made or opinions expressed herein.All contributions are subject to editing. Submissionsmust be signed.

e d i t o r i a l

Did you ever wake up in the morningand say to yourself: “I made a bigmistake”? Did you ever pat yourself

on the back for coming up with a creativeidea to make a product more salable, onlyto realize later that your idea was stupid?Have you ever had an assumption comeback to haunt you, like assuming that inter-est rate or stock market guarantees carryno cost? And, if you have, did things workout much differently than you projected?

Honestly, most of us would answer yes toone or more of these questions—or, at thevery least, we’ve observed it in the market-place. As the saying goes: “To err is human,to forgive divine.” As we have seen, thestock market is not divine; neither are stockanalysts.

The real question is: What are we going todo about it? If experience is the bestteacher, what will the student in all of us dodifferently?

This month, our theme is mergers, acquisi-tions and creativity. Some would argue thatfinancial (and actuarial) creativity helpedfuel the insurance merger and acquisitionboom of the 1990s. In some situations,criminal activity was involved (see the arti-cle on page 7 by Bob Wilcox and CarlHarris). In others, “irrational exuberance”was the culprit. It is sometimes difficult toknow where to draw the line.

The two words, “mergers” and “acquisi-tions” (M&As), evoke extreme emotions inthe hearts and minds of actuaries involvedin these efforts (assuming actuaries haveextreme emotions.) Actuaries of the acquir-ing company see mounds of work ahead.Actuaries of the target company polishtheir resumes and prepare for major lifechanges. Consulting actuaries for bothsides salivate at the fees they can generate;with so much at stake, competition forthese projects can get very intense. It’s notjust the stockholders whose fortunes can bemade or lost in the process, and there isoften tremendous pressure on the actuary.Let’s make sure that our actuarial opinionsdo not get clouded by the numbers.

The 1990s saw quite a binge. But for manyinsurance consolidators, the morning after

has arrived—and, with it, the hangover ofcollapsed stock prices. For those compa-nies, let’s hope that the answers flow asfreely as the questions.

While actuaries in their role as actuaries arenot the ultimate decision makers, they havea responsibility to educate the decisionmakers on the consequences of theiractions. When an actuary provides a rangeof potential values, he or she must assurethat the reader of the report understandsthe pluses and minuses, the facts versusassumptions—and the limits of manage-ment to change the likelihood of each. Ifcreative actuarial science places today’searnings in a good light, it is not creatingearnings but merely borrowing fromtomorrow.

In product development, the focus on newbusiness growth appears to have overtakenthe more appropriate focus on sustainabil-ity. We must recognize that the products wedevelop create a lifelong commitment toour policyholders.

I tried, but just cannot close without bring-ing up something “About Schmidt.”Leaving his personality out of the discus-sion (every actuary is cool—just ask one),how would someone like Schmidt fare inthe M&A world? How creative was he?Conscientious to a fault, Schmidt wouldprobably fit the role of the acquired actu-ary, and his beautiful work would end upwhere it did (I won’t mention where forthose who haven’t yet seen the movie.) Hisreplacement might fit one of the otherroles. If you were a stockholder, whichactuary would you want to have protectingyour interests? If you were managementwith stock options, would your decisiondiffer?

As actuaries, let’s do our part to make surethat the insurance marketplace returns to amore fundamentally sound foundation.Let’s make sure that our creativity is in thebest interests of our customers. As actuar-ies, let’s be agents of this change, whetheras decision makers or their vocal advisors.Maybe then we will all respect ourselves inthe morning.�

Oh, what a hangover!by Morris Fishman

�Printed on recycled paper in the U.S.A.

the

ac

tua

ry may

20

03

33

U.K. par business under pressureI was interested to see the article on parbusiness (we call it “with profits” in theUnited Kingdom) in the February 2003issue (“Participating life insurance—R.I.P.?” by Kevin Wark). In the UnitedKingdom, par business is under pressure;in particular, solvency margins of insur-ers have declined (guaranteed benefitsare more expensive in an era of lowinterest rates and many insurers havemismatched with equities; fine whenthere was a large surplus, but equityvalues have fallen sharply).

We have a concept of smoothing—bonuses (dividends) are declared atintervals so the payout does not go upand down daily with asset values, but thedecline in equities has been such thatbonuses have dropped markedly (to zeroin some cases).

The regulator is very concerned aboutthe discretion in with-profit funds, andthe rules are getting more onerous.Perhaps you have lower guarantees (ornone) or better asset-liability matching?And perhaps insurers’ practices in declar-ing dividends are more transparent,hence, meaning that regulators andconsumers are not so worried? Anycomments on the above would be ofinterest.

Christopher O’Brien Centre for Risk and Insurance Studies

Nottingham University Business SchoolNottingham, England

christopher.obrien @nottingham.ac.uk

Fuzzy illustrations boosting par sales“Participating life insurance—R.I.P.?”(February 2003) [was] a nice summary. Iagree that there are advantages anddisadvantages to both UL and par.Unfortunately, I feel the recent bigincrease in sales of par plans has a lotmore to do with improper illustrationwars; i.e., agents run a par illustrationbased on current dividends and see thevalues are better than a UL done at 4-6percent. They, thus, automatically

promote the par without truly under-standing it, especially the fact thatdividend yields are based on a rollingaverage of mainly book rates.

This means the declared dividend yield(currently 7-9 percent) lags behindactual yields available in the market. Thedividend yields will eventually drop by1-2 percent, unless long-term bondyields quickly increase by 2 percent andstay there.

Most agents and marketing staff do notrealize this. In my experience, expecta-tions are not being properly set forclients. In fact, I encountered a large salerecently where brokers and agents from alarge national distributor were very vocalin stating that dividends were going toincrease in the next year! This type of saleneed not happen. When I market wholelife, I use at least 1 percent lower divi-dends, and often lower, in order to betterset client expectations. This still showshigher values than a comparable UL.

Ashley CrozierCrozier Consultants

Toronto, Canadaacrozier @yorkfunds.com

Author’s replyI agree that the current 7-8 percentreturns are driving much of the salesincrease for the par product. Conversely,the negative returns on many ULcontracts are causing brokers to look formore "stable" options. I also share yourconcerns if brokers are representingpotential increases to dividend scales. Infact, Standard Life just withdrew its lineof par products because it is anticipatinga large decline in its dividend scale anddid not want the products being soldbased on the current dividend scale. Thebottom line is the ongoing need forbroker training and consumer disclosureso everyone understands the risks as wellas potential rewards. — Kevin Wark

Moral justification of insuranceThe November/December 2002 issue ofthe “Navigator” has an excellent article—

“The Inherent Individualism ofInsurance,” by Stephen Moses—thatmakes a moral defense of a free marketin insurance. I encourage all actuaries toread the article, which is available free onthe Objectivist Center’s Web site atwww.objectivistcenter.org.

Harvey SobelPrincipal and Consulting Actuary

Buck ConsultantsSecaucus, N.J.

hsobel @buckconsultants.com

Social security solutionRecently, I had the opportunity to workon a consulting project for a governmentsocial security program in China.Besides doing actuarial analysis andprojections, I was also asked to findsolutions to resolve the various chal-lenges facing the system.

My idea is to require every citizen to gothrough a period of compulsory commu-nity service (CCS) before they canreceive the retirement pension providedby the government. This service will startwith some formal education about theaging process and training on how totake care of our aged.

I believe everyone should learn how totake care of our aged. In the process, welearn more about best practices fortaking care of ourselves when webecome old. Everyone also shouldcontribute toward society to help resolvethe old age challenge.

I would compare the training for CCSbefore retirement to the educationsystem for our children. The purpose ofa compulsory education system is tobetter prepare them to continue thefurther development of our society. Asimilar argument applies to retirement.As our life expectancy increases, theretirement period is becoming a biggerand bigger portion of our life, yet manycitizens are financially and psychologi-cally unprepared for old age and have

l e t t e r s

continued on page 12

Examples of recent transactions that arelikely to affect tomorrow’s insuranceindustry dynamics include:

1. Citicorp acquires and divests Travelers:CitiBank’s acquisition of Travelers in1998 helped push Congress to open upthe financial services marketplace.Citicorp’s later (2002) divestiture ofTravelers suggests that integration of lifeand property & casualty (P&C) businessis difficult, and that ownership of tradi-tional P&C and life manufacturers maynot be necessary for a financial servicesorganization to serve financial servicescustomers successfully.

2. NML acquires Frank Russell:Northwestern Mutual bought FrankRussell in 1998. Earlier in the 1990s,there had been rumors of NorthwesternMutual merging with various traditionalmutual companies. The Russell transac-tion is an example of a well-managed,unique organization acquiring tostrengthen its basic capabilities and skills,rather than seeking generalized economyof scale transactions. Well-managedspecialty companies tend to avoid trans-actions that could damage their“specialness” by diluting their marketingor service platforms.

3. MONY demutualizes: As a relativelyearly demutualizer, MONY helped to

drive a trend that has led to many addi-tional demutualized organizations overthe past five years. Although heralded asa means to transform mutuals into moreaggressive, shareholder-driven organiza-tions (e.g., giving them the currency tomake acquisitions), many of today’sdemutualized companies are finding itdifficult to overcome long-embeddedorganizational constraints and may havemerely created a framework for theirultimate exit.

Emerging forcesLet’s look at the other side of the coin.What emerging forces are likely to drive future insurance industry M&A? Thinkfor a minute about the insurer operatingrealities that exist today. Having played

up to Wall Street and rating agencyexpectations for years, many insurers arestruggling to deal with dramaticallyincreased financial and strategic scrutinyresulting from Enron, WorldCom,Unicover, variable product losses andother operating traumas. Competitive

pressures are high and boards are moreinquisitive. What’s more, the morale ofoft-downsized employees is low, makingnecessary change even more difficult.

What will begin to change the insuranceindustry and, in turn, can be expected todrive future M&A transactions? Specificrequirements of successful life insurancecompanies of the future include thefollowing:

1. Insurance companies of tomorrowwill need to have compelling strategies,stronger management teams and moreeffective boards. They will need to avoideven the appearance of accounting orother improprieties. Future acquirorswill seek candidates that consistentlystrengthen their long-term strategic,operational and financial position, andwill be less likely to pursue deals forpossible short-term gains. Again, M&Aoptions for both sellers and buyers will,therefore, narrow.

2. Acquirors will pay much more atten-tion to post-purchase management processes. Management, not price, sepa-rates successful from unsuccessful deals.Shareholders of the future will not standfor the deal failure rates of more than 50percent that characterize past M&Aexperience. Hence, acquisition targetswill be more carefully scrutinized by

potential buyers, narrowing both theuniverse of suitors for sellers and theuniverse of sellers for acquirors.

3. Future insurance company winnerswill need to have a strong “sustainable,profitable new business machine”

4

the

ac

tua

ry m

ay

20

03

m e r g e r s a n d a c q u i s i t i o n s

Insurance mergers and acquisitions—change driven and change drivingcontinued from page 1

...Many insurers are struggling to deal withdramatically increased financial and strategicscrutiny resulting from Enron, WorldCom,Unicover, variable product losses and other operating traumas.

Emerging Trends

Changed Insurer Capabilities

New Insurer Needs(e.g., skills and scale)Build or buy to obtain

New Competitive RealityChanging strategies and

innovating to adapt

Figure 1

continued on page 15

5

the

ac

tua

ry may

20

03

Who owns your intellectual property?by Tom Bakos

Early in my actuarial career I recallparticipating in a psychologicalstudy that was supposed to measure

individual creativity. My recollection isthat the results of the study showed thatactuaries, as a group, were very creativepeople. I was pleased to be a member ofsuch a group and, of course, suspected theresult all along.

Certainly, in my career since then, I haveseen nothing but support for the conclu-sion that study reached over 30 years ago.Actuaries are highly creative. Critics maycomplain that this creativity dwells on thedark side to the extent that actuaries aidand support—through their creativeproduct designs and processes—attackson the supposed integrity of valuation,illustration or taxation systems. All of this,they say, in apparent condemnation ofcreativity, is done to the ultimate detri-ment of our company’s policyholders orstakeholders and the insurance industry’sreputation.

Well, I think we need to take a morebalanced look at this. After all, you can’thave animals without insects or seasonswithout winter. So, too, one must be will-ing to accept all kinds of creativity inorder to have creativity at all.

Let’s focus on the creative efforts weactuaries exhibit that most of us can beproud of. These creative efforts arereflected in new product designs, systemsand processes, many of which supportvaluation, illustration or taxation systemsand provide lasting value to ourcompany’s policyowners, customers andstakeholders.

Measuring creative valueThe “value” element raises an interestingquestion: What is the measure of creativ-ity’s value?

Our forefathers recognized that individu-als could be creative and provided in theconstitution they drafted a way for indi-vidual citizens to protect the value ofwhat they create. In particular,

Congress (in Article 1, Section 8, Clause8 of the U.S. Constitution) was givenand exercised the power to allow indi-vidual inventors the right to exclusiveuse of their discoveries for a limitedperiod of time.

The granting of exclusive use wasintended to encourage creative people toshare their ideas with the general public,which, in turn, was expected to encourageadditional creativity. “Exclusive use” isrecognized by a patent issued by the U.S.Patent and Trademark Office (USPTO).The value in creativity protected by apatent, therefore, is the right to exclusiveuse for a limited period of time—typi-cally, 20 years.

Who owns creativity?The creativity embodied in the patent isgenerally characterized as intellectualproperty, and this characterization as“property” begs the next question: Whoowns it?

Well, the insurance industry, in whichmost of us practice, has never placedmuch value on creativity in general, eventhough it has been an important andnecessary element in the success of manyinsurance companies.

In large insurance organizations, therehas never been much acknowledg-ment, encouragement or rewardfor inventiveness. Creativeideas, new products, illustra-tion concepts andmarketing techniques havebeen freely shared in theinsurance industry as ifthey had no value. Theyare copied and plagia-rized by competitors inways that wouldconfound practitioners inalmost every other type ofbusiness. One might evensuggest that creativitywithin our insurance organizations is not evenexpected.

Contrast this with the electronics indus-try, for example, where innovation is partof the culture. Product designers areexpected to produce patentable inventionson a regular basis. That is what they werehired to do. The employment agreementthey sign clearly spells this out and clearlystates that the inventions they produce arethe property of their employers. It isimportant to note that only individualscan patent an invention. A corporationcannot be an inventor. However, theinvention can be owned by the corporateemployer through an assignment made bythe inventor employee.

So, in industries where intellectual prop-erty, as reflected in patents, is considered athing of value, the ownership issue isfairly well resolved. You are specificallyhired to invent things. You are paid to dothat. You are given all the tools and train-ing you need to make it easy to inventthings and the company pays all expensesassociated with your work, including thecosts associated with actually getting thepatent. In exchange for that, youremployer owns the intellectual propertyyou create. In fact, you’d be paid even ifyou didn’t invent anything—althoughprobably not for long.

Creative free for-allIn the insurance industry, the question

of who owns your intellectual

i n s u r a n c e

Intellect

continued on page 6

6

the

ac

tua

ry m

ay

20

03

i n s u r a n c e

property is not so clear. I have neversigned an employment contract. Whilethere may be some rare exceptions, Iimagine most of you haven’t either. So, isthe ownership of anything you mightinvent on or off the job some kind of free-for-all?

Of course, if you adopted the existingfree-for-all view now practiced, you wouldsimply publish your idea either in theform of an insurance product, illustrationcalculation, marketing material, newsletterarticle or something like that, and meas-ure your advantage only in terms of thehead start you could get over your compe-tition because you thought of it first.Indeed, that is probably what youremployers expect of you. They probablyconsider your invention to be no morethan a beneficial by-product of someother process you are involved in.

However, let’s assume that you are a rebel(as, perhaps, you would have to be inorder to be creative in the first place). Youthink you have a pretty good idea thatcould be worth a lot of money, and you’renot willing just to give it away.

First, recognize that I am not an attorneyand I am not intending to provide legaladvice. Now assume that you know a littleabout patents, and that is the directionyou start to go.

An idea might come to you during yourlong commute to work or in the showerthat clearly has nothing at all to do withinsurance or your job. It might be somegreat new idea for novel, cheap CrackerJack prizes that your employer could notpossibly claim they hired or paid you toinvent. In this case, the invention is prob-ably all yours, assuming it would qualifyfor a patent at all, and, unless you couldfind some other backer, the costs and therisks of proceeding would be all yours.

Insurance inventionscenariosHowever, if it’s an insurance invention,you could approach your employer andsuggest that you would assign your inven-tion to the company for some payment tobe negotiated if it absorbed the costs of a

patent application. My best guess is that you would be involved in one of thefollowing scenarios:

1. The company managers might surpriseyou. They may recognize that you are avaluable employee whom they want toretain and also recognize that they havenever placed any value on or had anyconcern or expectation that your jobinvolved inventing things. They mightnote that, although they do not have anemployment contract with you:

• They have provided you with a job description.

• Your file contains many job evalua-tions.

• No where in this material is there anyindication that your job requires you to invent things or that it is even expected that you might.

Because of this, they might recognize thattheir compensation arrangement with youdid not contemplate their assumption ofownership of any intellectual propertyyou create, and they would, therefore,have no hesitation about rewarding youfor your additional effort in bringingvalue to the company above and beyondthe scope of what you were hired to do.

2. More realistically, they would probablyreact with wonder and amazement at youraudacity. They would probably insist thatyou were specifically hired to solve thetypes of problems for the company that

your “invention” solves, and that you, infact, were paid to come up with the solu-tion you came up with and owe it to thecompany.

They might not be so much arguing thatyou have an obligation to assign anypatent issued on your invention to thecompany as they are arguing for the statusquo, the free-for-all environment. Theyare arguing that, whether or not you havedeveloped a patentable invention, it isnevertheless a work product of youremployment with the company and theyhave a right to use it. They may not seethe need for a patent.

3. They may recognize the value in apatent but claim, as above, that the idea isa work product of your employment withthem and that the intellectual propertyhas already been bought and paid for as aresult of your employment. They mayinsist that you patent the invention, sinceonly the inventor can seek a patent. Thecompany would pay for the patentexpenses and you would be required toassign it to the company. The continua-tion of your employment would probablydepend on it.

Contingency planClearly, if faced with one of the lattertwo situations, you would need to have aplan B. You could either be a meek capit-ulator and play the game the old way orbe a daring go-getter and step out onyour own.

Some people, familiar with invention inthe insurance industry, might suggestthat it would be rather rare to findinventive minds in a large insuranceorganization. That environment, they’dobserve, is not currently well suited toindependent inventors who think beyondthe box. So, I suspect, there has been alot of stepping out.

I believe that most invention in the insur-ance industry is done in small shops

...Is the ownership of anything you might invent on or off the job some kind of free-for-all?

Who owns your intellectual property?continued from page 5

continued on page 16

When one hears the expression“mergers and acquisitions,” theusual conclusion is that there

are two parties: the “willing” buyer andthe “willing” seller. In truth, when insur-ance companies are involved, there aretwo additional parties: the policyholdersand the regulators.

The latter two parties are sometimesforgotten because they usually are notdirectly involved in the transaction, eventhough they are directly affected by it.

Over the past 10 years, we have seen aconsolidation of the insurance industry,brought about not by financial insolvency,but through merger activity. The reasonsfor this include:

• Large international companies seek entrance to the U.S. market by buying existing insurance companies,viewing this as a cheaper way to penetrate the market than starting from scratch.

• Existing companies are looking for increased market share.

• Companies want to take advantage ofsynergies within certain market-places.

• Insurance companies desire expense savings through increased volume.

The main result of these activities hasbeen the reduction of the total number ofinsurance companies. According to A.M.Best, in 1996, there were 1,748 life

insurance companies in the United States.In 2002, this number decreased to 1,445.This article will deal with mergers andacquisitions (M&A) from the perspectiveof the regulator and the insured.

Some basics In the insurance world, for the most part,there are two types of insurance compa-nies: stocks and mutuals. A stockinsurance company is owned by its share-holders, similar to any other stockcompany. Anyone wishing to gain controlmerely has to purchase enough stock. The

customers, or policyholders—despitebeing the sole reason for the company’sexistence—have no rights other thanthose contained in the insurance policiesthey have purchased. If policyholder inter-ests are to receive attention, it will bethrough the efforts of regulators.

A mutual insurance company isowned by its policyholders. Assuch, there are no stockholders.These policyholders have boththe contract rights andownership rights. Twomutual insurancecompanies can merge;however, one will ceaseto exist after the trans-action. The remainingcompany continueson as the survivor.

For a mutual insur-ance company to beacquired, it must firstgo through a process

called “demutualization,” whereupon itsstructure changes from that of a mutualcompany to that of a stock company. Thepolicyholders are compensated for givingup their “ownership” rights. At this point,the stock company can be acquired in thesame way as any other stock company.

The regulator’s viewIn each of these cases, the regulator is inti-mately involved in the process This rest ofthis section provides coauthor and formerinsurance regulator Robert Wilcox’sperspective on some of the problems hehas seen and how the Insurance HoldingCompany Act (IHA) has been and shouldbe used to prevent such problems.

The most serious abuses that I have seenwithin the insurance business involvedchange of control or restructuring, some-times including reinsurance in the mix.My observations span four decades and include a variety of companies. Many ofthese abusive situations have resulted inrehabilitations or liquidations. All have

had a negative effect on policyholders.

M & A r e g u l a t i o n

7

the

ac

tua

ry may

20

03

Regulators and insureds also have astake in mergers and acquisitionsby Robert Wilcox and Carl Harris

Over the past 10 years, we have seen a consolidation of the insurance industry, broughtabout not by financial insolvency, but throughmerger activity.

continued on page 8

8

the

ac

tua

ry m

ay

20

03

M & A r e g u l a t i o n

That is not to say that all acquisitions orrestructurings are bad; most are positiveand benefit both policyholders as well asstockholders. The boards of directorshave, for the most part, carried out theirresponsibilities to review each transactioncarefully for compliance with the law andultimate soundness. Thus, they have madefar more good decisions than bad. Reg-ulators have provided oversight that bene-fited all involved.

However, there are some cases that havenot had positive outcomes:

• Many years ago (before the IHA was adopted), a small life insurance company that was owned by a larger life insurance company was sold to an individual. As soon as the new owner had control, he proceeded to sell most of the listed securities in thecompany’s vault and reportedly replace them with residential mort-gages. An alert insurance examiner,after pressing the investigation,discovered the agreement in the drawer that pledged the mortgages ascollateral for their purchase. Some ofthe cash from the sale of the securi-ties went into the pocket of the broker who facilitated the sale; most went into the pocket of the new owner to cover the purchase of the company. The purchaser ultimately went to jail for this. The policyhold-ers had their values frozen while the company went through reha-bilitation.

• One day while I was commissioner ofinsurance, I received a phone call from the U.S. Attorney’s office in another state. “Could you come to

my office to discuss some matters with regard to one of our companies?” he asked. There I listened to details of an FBI sting operation involving money laun-dering, a suitcase full of cash and reinsurance. A few years previously,the company had been acquired by new owners and redomesticated fromanother state. In the acquisition, the controlling person, and his prior record of foul deeds, had been concealed from the regulator.Because of the complex holding

company structure that had been created, the obfuscation was not that difficult. By the time of the call from the U.S. Attorney, the company had already been put into receivership for a variety of reasons,most of which did not relate to solvency.

• A property and casualty company was for sale. Several prospective buyers, after proper due diligence,had walked away. Another prospec-tive buyer with no insurance experi-ence, after less than half a day ofinvestigation, made an offer. The prior owners allowed the new owner the opportunity to take control of thecompany’s funds prior to closure so that the bulk of the purchase price could be withdrawn from the company’s own surplus. After the company was subsequently put into receivership, it was discovered that there were large numbers of long-tailed liability risks that had never been reserved. Even if the new owner had not absconded with the signifi-cant amounts of funds that he did,

the company would have eventually failed because of these unreserved obligations, but the damage to policyholders could have been a bit less.

What is the protection against these sortsof corporate misdeeds? The first line ofdefense is the responsibility of the respec-tive boards of directors. They certainlyhad some responsibility for the actionsthat took place, but not always sufficient information or control over management.

Regulators also have a role, and theygenerally look to the IHA for authorityand to the Acquisition of Control-Statement Filing (Form A) forinformation.

The IHA was adopted by the NAIC in1969 with material amendments in 1980,1985 and 1995. There were a variety oftechnical amendments over the years and,in 1994, the act was made applicable to

Many of these abusive situations have resulted in rehabilitations or liquidations. All have had anegative effect on policyholders.

Regulators and insureds also have a stake in mergers and acquisitionscontinued from page 7

nonprofit medical and hospital serviceplans. All jurisdictions have adopted themodel act or legislation that is essentiallysimilar.

The model act provides that a tenderoffer—or other agreement to exchangesecurities that would result in a change ofcontrol of an insurer—may not take placeuntil approved by the commissioner. Theact requires the filing of information to beused in the approval process and thegrounds for disapproval. In some cases,the grounds for disapproval point toother statutes.

For example, if, after the change ofcontrol, the insurer could not satisfy therequirements for the issuance of a licenseto write the same lines of insurance, thatconstitutes grounds for disapproval.Other requirements depend on the regu-latory judgment of the regulator, such as

a finding that the acquisition islikely to be hazardous or

prejudicial to the insur-ance-buying public.

In most of the casesdescribed above, theacquisition mighthave been blockedunder paragraphD(e) of Section 3

of the IHA,which provides

that the acquisi-tion may be

disapproved if thecommissioner finds

that:

“The competence, experienceand integrity of those persons whowould control the operation of theinsurer are such that it would not be inthe interest of the policyholders of theinsurer and the public to permit themerger or other acquisition of control.”

It has been my experience, however, thatbiographical affidavits tend to gild thefavorable attributes and obscure or omitthe negative. Criminal convictions, abuseof fiduciary responsibility, involvementwith failed enterprises and unresolved

indictments will often be left to the regu-lator to discover. Efforts to discover these“character flaws” may still be insufficient,but regulators must try. I recall the inci-dent involving a person who had givenno indication of lack of fiscal integrityuntil the day he took several milliondollars out of the insurance companyaccounts in cash. He left his family and

the United States for a tropical countrywithout an extradition treaty with theUnited States. It happens.

Despite the success of Frank W. AbagnaleJr., as depicted in the movie “Catch Me IfYou Can,” in most instances, carefulinvestigation will reveal false representa-tions and disclose a history of previousactions that cast doubt on the future.Some insurance regulators do not havedirect access to criminal databases thatwill reveal information not disclosed byan individual, but the research can beperformed on their behalf by anotherstate agency that has the required access.

You may have noticed in the casesdescribed here that the funds used toacquire control might provide some indi-cation of future problems. Section 3B ofthe IHA provides the authority for thecontent of Form A, and paragraph (3) iscritically important. This paragraphrequires disclosure of “the source, natureand amount of the consideration used orto be used in effecting the merger or otheracquisition of control … .”

It isn’t enough to know that the moneyexists; the regulator needs to know thesource of the money. If you want to knowwho really has ultimate control, follow the money. The source of funds is a far betterindicator of control than any organizationchart. Just as with biographical affidavits,the disclosure of the source of funds isnot likely to tell all, if the informationmight be viewed unfavorably. A carefulinvestigation might find that the money

doesn’t exist at all and that the onlysource will be the company’s own surplus.

Despite the best efforts of the regulator,bad deals still occur. What happens afterthe deal when the bad guys are in control?The IHA still provides tools to the regula-tors who will use them. Section 4 requiresan insurance holding company to file a

registration statement annually and toupdate the statement within 15 days afterthe end of a month in which any materialchange occurs. This is Form B, containingdetailed information about the insuranceholding company system, all significanttransactions and arrangements within thesystem and material transactions outsidethe system.

Section 5 of the IHA requires advancenotice of certain kinds of transactions,such as sales or purchases of assets thatexceed 3 percent of the insurer’s assets orreinsurance agreements with a premiumof more than 5 percent of surplus.Extraordinary dividends or other distri-butions to shareholders also are subject tothe advance notice requirement, and thecommissioner has 30 days in which thetransaction can be disapproved.

This section also has requirements thatat least one-third of the directors of theinsurer shall be persons who are notofficers or employees of the insurer orits affiliates. Committees made up ofthese nonaffiliated directors areexpected to control independent andinternal audits and the compensation ofprincipal officers.

I have just touched on the authoritygranted by the IHA and the informationthat it requires, but it should be notedthat Section 10 provides for severe penal-ties for willful violation of the act. These

M & A r e g u l a t i o n

9

the

ac

tua

ry may

20

03

continued on page 10

Criminal convictions, abuse of fiduciary responsibility, involvement with failed enterprisesand unresolved indictments will often be left tothe regulator to discover.

the

ac

tua

ry m

ay

20

03

M & A r e g u l a t i o n

include fines to be paid by the individual,not the company, and up to three yearsimprisonment.

As stated earlier, at the very heart of theM&A process is the Form A filing. Theacquiring company must file with thepotentially acquired insurance company’sdomestic state appropriate documentsoutlining the process by which it will gaincontrol. When the documentation iscomplete, the commissioner will review itand hold a hearing to determine whetherthe transaction will be approved. In most cases, this is a formality, as enough discus-sions will have taken place prior to thehearing so that there are no problemsremaining.

Part of the regulator’s function is to deter-mine not only whether policyholder rightswill continue, but also whether the surviv-ing company will be strong enough to paythe promised policy benefits uponcompletion of the transaction. In otherwords, will the surviving company be asstrong as the individual companies priorto the transaction? Over the past severalyears, we have all seen some outrageousprices paid for acquisitions, usually in the

name of expense consolidation. Not all ofthese acquisitions have been successstories.

The hearing process should not be takenas perfunctory to the approval process. Onthe contrary, regulators take great pride inensuring that the interests of the policy-holders are not compromised by theproposed transaction. However, it shouldnot be taken to mean that the regulator isinvolved in obtaining the “best or fairest”price for each party either. The regulator’srole in this process is not as a financialanalyst. That is the responsibility of the “willing” buyer and the “willing” seller.One would like to hope that issuers of

“fairness opinions” are “god-like” andprotectors of the policyholders. However,with the high prices paid for these instru-ments, sometimes good judgment can beclouded with dollar signs.

The insured’s viewLet’s turn our focus to the policyholder.Where do they stand, or better yet, dothey stand? Clearly, unless they own sharesin the company being acquired, the onlyrights they have are those contained intheir policies. This does not mean thatthey have no voice. Policies are bought formany reasons, including price, featuresand the perception of company strength.However, paramount to the process ofpurchasing insurance is that thecompany will pay the promised benefitswhen policy conditions are met.Sometimes these are shortly after thepolicy is purchased, and other timesthere is a long lag until benefits are paid.In either case, the policyholder has tobelieve that the company will be aroundto pay these benefits.

One of the biggest precepts of the M&Aprocess is that it is in the “best interests ofall parties” for the transaction to be

approved. Included in the definition of“all parties” are both the shareholders andthe policyholders. While this is true mostof the time, it is not true all of the time.I think we can all think of at least oneexample where insurance companies havebeen acquired and, sometime afterward,the acquiring company runs into somefinancial trouble. To work through thefinancially troubling times, policy benefitsare sacrificed for survival to levels belowwhat would have probably been paid topolicyholders had the transaction not been approved. Sure, the shareholders also usually suffer during these times; however,policyholders suffer as much, if not more.

How is this possible? While benefits maynot be specifically lost:

• Premiums may be required to increase,

• Premium periods may require exten-sion just to keep them alive,

• There may be an inability to with-draw funds or

• Buildup of policy values may be deferred.

So what are policyholders to do? Clearly, ifthey have concerns regarding the transac-tion, they should voice them to theinsurance commissioner. If they areunhappy with the new owners, they cancancel their policy and purchase it fromanother company. This is sometimesdifficult if the policyholder has had achange in health status. Beyond thesesteps, there is probably little else a policy-holder can do other than enter thequagmire of litigation.

In conclusion, in order for any transactionto take place, all four of these partiesshould be heard prior to making a finaldetermination. The insurance commis-sioner should take all “interests” intoconsideration when making the final acqui-sition determination. In the end, the solereason for approving the transactionshould not be that the sellers received agreat deal.�

Robert Wilcox, ASA, MAAA, FCA, is aconsulting actuary with Wilcox & CompanyInc., Alpine, Utah. He can be reached [email protected]. Carl Harris,FSA, MAAA, FCA, is a consultant withInsurance Strategies Consulting LLC, WestDes Moines, Iowa. He can be reached at [email protected].

Regulators and insureds also have a stake in mergers and acquisitionscontinued from page 9

10

...With the high prices paid for these instruments,sometimes good judgment can be clouded withdollar signs.

This is the second in a series of articlesaddressing potential changes to the educa-tion and examination (E&E) system. Lookfor follow-up articles in future issues of“The Actuary.”

The SOA Board of Governorscontinued strategic discussion ofE&E redesign issues at its March

13-14 meeting. The discussions focusedon key parameters of the revised system.The subsequent Board action indicatedtheir commitment and clarified furtherdirection for the working groups. Withthis direction, the working groups arecontinuing their efforts and plan to

present a refined and more detailed designto the Board in June.

The Board endorsed five statements thatare intended to shape the E&E redesign.In addition to providing direction to theworking groups, this action representsBoard commitment to resolving issues ofimportance to SOA candidates, membersand employers of actuaries.

1. All Fellowship tracks should be ofapproximately the same scope with regardto the number of exams/experiences and theexpected travel time through thoseexams/experiences. That scope should beequivalent to three or four (to be recom-mended by the working groups) traditionalFellowship exams.

Board endorsement of this statement rein-forces the working groups’ thinking thatthe qualification process should be essen-tially equal for each of the traditionalspecialty tracks (finance/investment,health, life and retirement) in terms ofamount of material, number of exams anddepth of treatment. The Board’s action alsosets an upper limit for the working groups.

The working groups are in the process ofdefining instructional objectives andlearning outcomes for each of the practiceareas. With practice-area-specific objec-tives defined, the working groups are alsoidentifying common elements importantto all Fellows, regardless of specialty area.Central to the redesign is the understand-ing that, while a new Fellow hasdemonstrated attainment of a certain levelof knowledge and expertise, the attain-ment of the FSA should not be regardedas the end of an actuary’s education.Once the complete scope of desired learn-ing is defined and articulated, the workinggroups will prioritize learning objectives toassure that the scope falls within the threeor four exams/experiences upper limit.

Content not included in the three or fourexams will be retained for continuingeducation.

2. With the exception of a possible track inenterprise risk management, no additionalFellowship tracks should be investigated orproposed at this time.

The Board discussed the opportunity/demand for a specialty focus on enterpriserisk management (ERM). Although a RiskManagement Task Force is already in place,the Board discussed opportunities to movequickly to an ERM section or practice area.An informal group consisting of key Boardvolunteers and SOA staff will explore thepossibilities. Members of this informalgroup include Mike McLaughlin, ShirleyShao, Peter Tilley, Kathy Wong, ValentinaIsakina and Mike Kaster. That group willreport to the Board and involve the work-ing groups as appropriate.

3. The ASA Course should provide an intro-duction to financial security systems,utilizing the control cycle context whereapplicable. Development of learning objec-tives is more critical at this time than aredelivery and evaluation mechanisms.Creation and implementation of the ASACourse should not delay the implementa-tion date of the new education system.

The overarching goal of the ASA Course isto introduce candidates to financial secu-rity systems and common actuarialtechniques. Additionally, the course willfocus on commonly practiced techniques,with an introduction to more specializedpractices and methods, enable skill devel-opment in common applications andreinforce understanding of the ActuarialControl Cycle.

The Board approved flexibility in courseselection to satisfy the educational require-ments of the ASA in the current system

the

ac

tua

ry may

20

03

11

SOA Board of Governors endorses E&Eredesign direction

E & E s e r i e s

continued on page 17

Working GroupPrinciplesThe following eight principles reflect thecompleted work and the continuingdirection for the working groups indefining the framework for an E&Esystem redesign. These underlying princi-ples support the overarching goals ofenhancing the value of the E&E systemand preserving and enhancing the valueof the FSA.

1. Improve education for actuaries.2. Maintain suitable standards of

accreditation.3. Use appropriate assessment methods.4. Meet the needs of our stakeholders.5. Use appropriate education delivery

tools.6. Make best use of volunteer expertise.7. Effect a sound balance between the

practical and the theoretical.8. Provide flexibility so that the system

may evolve.

The initial report of the working groupsis available on the SOA Web site atwww.soa.org/eande/report_member-ship02.pdf.

12

the

ac

tua

ry m

ay

20

03

unrealistic expectations about their retire-ment life. This knowledge gap can be filledby a compulsory formal education onaging just before we retire.

As the baby boomers retire, the demandfor resources to service the aged willincrease at an increasing rate. More moneyalone is not sufficient to resolve the agingchallenge. We need more workers, espe-cially knowledgeable workers. Theprovision of CCS will greatly increase thesupply of workers serving the aged. Onebig source is those who are newly retiredor about to retire. Many are still in perfecthealth, fit and ready to work.

I would compare the provision of CCS tothe aged to the compulsory military servicein some countries for national defense.The same argument applies to the agingchallenge facing us.

There is another big advantage from thearrangement—it will discourage peoplefrom retiring early. The CCS before retire-ment will make it more difficult, if notimpossible, to carry on with one’s usualtrade after retirement. And, of course, weall know that a reduction in the earlyretirement pattern will have big costsavings to our social security systems.

Before this idea can be applied, a numberof issues must be dealt with: the age of

normal retirement, the length of the learn-ing period, the length of the CCS period,exemptions, transitions, legalities, humanrights, administration and compliance.

The purpose of my note is to generatediscussions, comments and thoughts onthe idea from other members. Hopefully,we can all work together and contributetoward our profession’s continued effort tofind a good solution for the aging chal-lenge facing us.�

C. K. Cheung Hewitt Associates LLC

Hong [email protected]

Letters to the editorcontinued from page 3

l e t t e r s

The Society of Actuaries has published a first-of-its-kindchart that summarizes many potential hazards that canjeopardize an individual’s retirement dreams. The

Post-Retirement Risk Chart (PRRC) was created specifically tohelp people face down potential pitfalls in retirement plan-ning.

“While most Americans understand the importance of savingfor retirement, many might not understand the risks afterretirement—but that doesn’t mean they aren’t there,” saidAnna Rappaport, one of the creators of the PRRC. “Just asone wouldn’t own a home without fire insurance, we mustalso look realistically at the risks that might face us in retire-ment.”

With factors such as increased longevity, the vulnerability ofmarkets and the large numbers of baby boomers rapidlyapproaching retirement age, the importance of knowing—andbeing able to deal with—the real risks to retirement is morecritical than ever.

“There are two major parts of the retirement planningprocess: accumulating retirement funds and managing thosefunds during retirement. We’re concerned that most of thefocus to date has been on the accumulation and too little onthe post-retirement management,” said Rappaport. “The

PRRC goes a long way in breaking down all the various threatsto an individual’s retirement in clear, everyday languageanyone can understand.”

To that end, the PRRC reviews the reality of increasedlongevity and how traditional government programs andretirement planning tend not to adjust for that increased life-span and use of resources. It also examines the variouseconomic unknowns, including inflation, interest rates andstock market returns, and then cross-references that informa-tion with business and public policy conditions that may playa large part in an individual’s retirement plans. The PRRCeven examines how a person needs to plan for the day whenhe or she will need assisted-living services.

“This chart is very important as a compliment to other,already-existing retirement planning materials on topics suchas how much to save or how to invest funds. It is our hopethat people will use this chart to make smart, informedchoices,” said Rappaport.

The PRRC also has been posted on the SOA Web site atwww.soa.org/sections/retirement/PRRD_chart.pdf. Indeed, it ishoped that as many people as possible will utilize this newresource. Any questions regarding the PRRC can be directedto the SOA at 847.706.3528.�

SOA unveils revolutionary new tool to help peoplesuccessfully plan for retirementby Bill Breedlove, SOA communications specialist

13

the

ac

tua

ry may

20

03

Does the financial economics’ perspective apply to theliabilities and risks faced by employer-sponsoredpension plans? Is it appropriate for funding, measur-

ing plan solvency and determining pension expense?

These questions are considered in the article “ReinventingPension Actuarial Science,” by Lawrence N. Bader and JeremyGold (“Pension Forum,” January 2003). The authors contendthat the actuarial pension model, used in compliance withERISA and FAS87, does not reflect the teachings of financialeconomics. In fact, the authors feel that the traditionalpension valuation model is not an accurate reflection of theprice of the risk, both in selection of assumptions and thesmoothing of assets and gains and losses.

Of course, many would disagree, feeling that our currentmodel supplies a true present value of pension liability and an appropriate level of contributions/expense. Smoothing has been seen as an important tool for protecting the sponsorfrom volatility in a way that’s fair and safe for an ongoingplan. Anticipating future market gains in the actuarialassumptions would also be considered appropriate.

To address these issues, the SOA’s Pension Section, theActuarial Foundation and the AAA have joined forces to pres-ent the symposium, “Great Controversy: Current PensionActuarial Practice in Light of Financial Economics,” to be heldJune 24-25 in Vancouver. The 23 papers that will be presentedat the symposium were written in response to a call for paperson the possible intersection of the financial economics modelwith pension liability measurement, accounting models andfunding models.

The symposium will be held in conjunction with the SOA’sVancouver Spring Meeting. You can register for the sympo-sium alone or for the entire Spring Meeting at the SOA Website www.soa.org/section/pension_financial_econ.html or by calling 847.706.3581.

Consider the appropriateness of new and older ways to look atpension finances. Find out where you stand and discuss theissues with all sides of the debate. Attend the symposium.�

“Great Controversy: Current Pension Actuarial Practice in Light of Financial Economics” symposium to be held June 24-25 in Vancouver

by Judy Anderson, staff actuary, actuarial education

LOMA is sponsoring a new study to provide clear customerfeedback to life insurance providers. The study, conductedby J.D. Power and Associates, is expected to provide a

comprehensive source of information about the expectations,needs and desires of today’s insurance customers.

Using surveys of companies’ insurance clients, a consortium willidentify the key elements of the customer experience and providecompanies with actionable feedback. Specifically, the consortiumwill explore the following:

• Reasons for selecting a life insurance provider.

• Overall customer satisfaction, including attributes that have the greatest impact on customer satisfaction.

• Individual provider profiles with competitive comparisons.

• Recommendations and repurchase intentions.

• Provider loyalty, customer retention.

• Identification of cross-selling opportunities.

LOMA was accepting commitments from life insurance compa-nies to participate in the consortium early this spring. If there area sufficient number of participants and respondents in the study,some of the results will be made available to the public at the J.D.Power Consumer Center at www.jdpower.com. For additionalinformation about the consortium, visit www.loma.org or call770.984.6446.�

LOMA embarks on life insurance consortium study

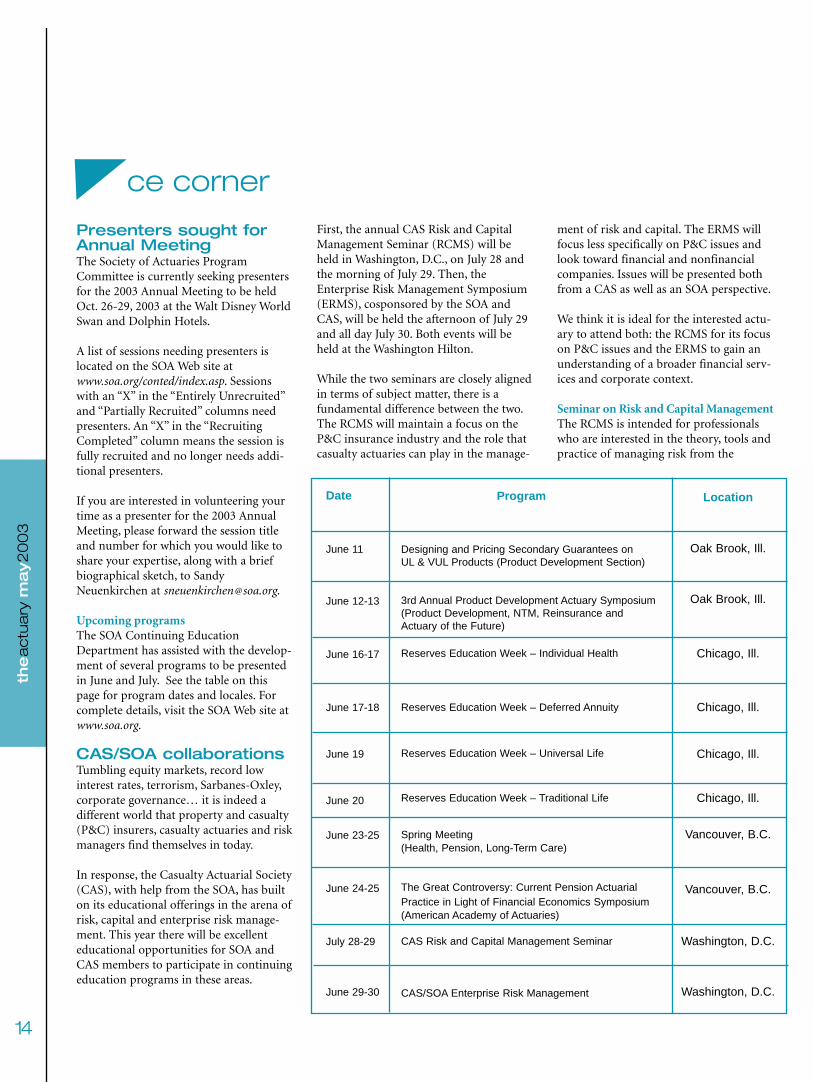

Presenters sought for Annual MeetingThe Society of Actuaries ProgramCommittee is currently seeking presentersfor the 2003 Annual Meeting to be heldOct. 26-29, 2003 at the Walt Disney WorldSwan and Dolphin Hotels.

A list of sessions needing presenters islocated on the SOA Web site atwww.soa.org/conted/index.asp. Sessionswith an “X” in the “Entirely Unrecruited”and “Partially Recruited” columns needpresenters. An “X” in the “RecruitingCompleted” column means the session isfully recruited and no longer needs addi-tional presenters.

If you are interested in volunteering yourtime as a presenter for the 2003 AnnualMeeting, please forward the session titleand number for which you would like toshare your expertise, along with a briefbiographical sketch, to SandyNeuenkirchen at [email protected].

Upcoming programsThe SOA Continuing EducationDepartment has assisted with the develop-ment of several programs to be presentedin June and July. See the table on thispage for program dates and locales. Forcomplete details, visit the SOA Web site atwww.soa.org.

CAS/SOA collaborationsTumbling equity markets, record lowinterest rates, terrorism, Sarbanes-Oxley,corporate governance… it is indeed adifferent world that property and casualty(P&C) insurers, casualty actuaries and riskmanagers find themselves in today.

In response, the Casualty Actuarial Society(CAS), with help from the SOA, has builton its educational offerings in the arena ofrisk, capital and enterprise risk manage-ment. This year there will be excellenteducational opportunities for SOA andCAS members to participate in continuingeducation programs in these areas.

First, the annual CAS Risk and CapitalManagement Seminar (RCMS) will beheld in Washington, D.C., on July 28 andthe morning of July 29. Then, theEnterprise Risk Management Symposium(ERMS), cosponsored by the SOA andCAS, will be held the afternoon of July 29and all day July 30. Both events will beheld at the Washington Hilton.

While the two seminars are closely alignedin terms of subject matter, there is afundamental difference between the two.The RCMS will maintain a focus on theP&C insurance industry and the role thatcasualty actuaries can play in the manage-

ment of risk and capital. The ERMS willfocus less specifically on P&C issues andlook toward financial and nonfinancialcompanies. Issues will be presented bothfrom a CAS as well as an SOA perspective.

We think it is ideal for the interested actu-ary to attend both: the RCMS for its focuson P&C issues and the ERMS to gain anunderstanding of a broader financial serv-ices and corporate context.

Seminar on Risk and Capital ManagementThe RCMS is intended for professionalswho are interested in the theory, tools andpractice of managing risk from the

14

the

ac

tua

ry m

ay

20

03

ce corner

Date

June 11

June 12-13

June 16-17

June 17-18

June 19

June 20

June 23-25

June 24-25

July 28-29

June 29-30

Program

Designing and Pricing Secondary Guarantees on UL & VUL Products (Product Development Section)

3rd Annual Product Development Actuary Symposium (Product Development, NTM, Reinsurance and Actuary of the Future)

Reserves Education Week – Individual Health

Reserves Education Week – Deferred Annuity

Reserves Education Week – Universal Life

Reserves Education Week – Traditional Life

Spring Meeting (Health, Pension, Long-Term Care)

The Great Controversy: Current Pension Actuarial Practice in Light of Financial Economics Symposium(American Academy of Actuaries)

CAS Risk and Capital Management Seminar

CAS/SOA Enterprise Risk Management

Location

Oak Brook, Ill.

Oak Brook, Ill.

Chicago, Ill.

Chicago, Ill.

Chicago, Ill.

Chicago, Ill.

Vancouver, B.C.

Vancouver, B.C.

Washington, D.C.

Washington, D.C.

15

the

ac

tua

ry may

20

03

perspective of a P&C insurance enter-prise. Sessions at this year’s seminar willinclude:

• A look back at industry results with adiscussion of the role that risk management could, and should, haveplayed in this recent history.

• A candid discussion of the state ofdynamic financial analysis (DFA) modeling today, both in terms of the technology as well as its acceptance throughout the industry.

• New approaches to capital allocation.

• Educational sessions on the basics ofcapital management and the cost ofcapital.

As always, there will continue to bespecific topics for the practitioner ofdynamic financial analysis.

Enterprise Risk Management SymposiumThis joint symposium came about from arealization that both the SOA and CASare increasingly involved in risk manage-ment issues—each specializing in uniquerisks but using common techniques andboth asked to demonstrate how their activities add corporate value.

The two societies realized it would bebeneficial to share knowledge, broadenperspectives and enable actuaries to play alarger role in ERM, which, broadlydefined, is the identification, measure-ment, prioritization and management ofrisks that face an organization. ERM is

not unique to the insurance industry. Infact, both societies have benefited fromlearning about ERM issues and practicesin the broader financial services industry.Actuaries’ training and specializationmake them uniquely qualified to play arole in this area.

The joint ERMS will include sessions onmodeling, risk metrics and capitalmanagement, among others. One high-light will be a general session featuringchief risk officers who will give theirperspective on key risk issues facingorganizations.

Look for information on the CAS Website, www.casact.org, and in the mail inlate May. �

(SPNBM). It won’t be sufficient merelyto continue adding more and more massthrough deals, as some of the aggressiveacquirors of the 1990s did. As insurersstruggle to refine their SPNBMs, theywill need to be much more careful intheir M&A approaches to assure thatthey don’t impair the new businessmachines. Hence, future sellers oftenwon’t fit the need of many future buyers.There will be fewer buyers for messy or

troubled companies, at least at pricelevels that such transactions sold for inthe past. As the power in financial serv-ices in sales situations continues to movefrom agent/company to customer,historic simplistic integration and post-purchase management protocols thatcharacterized much of the M&A environ-ment of the 1990s will be replaced byprinciples and processes that are much

more sensitive to the nuances of thebuyer’s SPNBM and the customer it serves.

The future of insurance M&AEventually, insurance M&A will increase.It appears that the marketplace will landon a more fundamentally sound transac-tion foundation. In the end, as actuariesknow, real economic value is the key.

This fundamental is appreciated by moreacquirors today. So, although the M&Amarketplace is changing, transactionactivity will pick up—but likely at pricesthat are more closely related to realeconomic value.

Every time an insurance company sells adivision, buys another organization,merges or establishes a joint venture

with another entity, it is both acting onits perceived need to compete in thechanging marketplace and disrupting theinsurance universe by sending messagesthat will change the future behavior ofother executives inside and outside ofthe insurance industry.

An analogy is the butterfly flapping itswings and creating air currents that lateraffect life halfway across the globe. Thesum of all insurance company events, intotal and over time, has a significanteffect on the future environment inwhich we will operate and the companiesthat we will manage.�

Robert D. Shapiro is president of TheShapiro Network Inc. in Milwaukee. Hecan be reached at shapironetwork@

ameritech.net.

Insurance mergers and acquisitions—change driven and change drivingcontinued from page 4

It won’t be sufficient merely to continue addingmore and more mass through deals, as some ofthe aggressive acquirors of the 1990s did.

16

the

ac

tua

ry m

ay

20

03

i n s u r a n c e

where constraints are not imposed on theway people think and where inventionmay even be rewarded. Or, the patentsare for data processing systems or othersimilar support processes utilized in theinsurance industry but owned by compa-nies in these support industries.

For example, IBM has five of the 175 U.S.patents issued between 1978 and 2002 inthe insurance business method patentsdesignation (class 705, subclass 4). This ismore than any other company. In fact,very few insurance companies have insur-ance-related business method patentsassigned to them.

Hidden R&D resourceOf course, not all insurance companiesare ignoring the talent of their people orthe value of the intellectual property theycreate. Some insurance companies arebeginning to realize that they have a largeresearch and development (R&D) budget;they just had not recognized it as such.Clearly, many actuaries, underwriters,advanced marketing and systems peoplewho work for insurance companies andare involved in product developmentoften find themselves doing R&D. Theneed for insurance companies to recog-nize and claim this individual creativeeffort in a more formal way is going to

become critical to the future success ofinsurance companies that want to protecttheir investment in R&D.

Why is the value and ownership of intel-lectual property important? It’s importantbecause things are changing. “Businessmethod patents,” the category that mosteasily includes insurance product design,marketing, underwriting and salesconcepts, were given a tremendous boost

when the U.S. Supreme Court, in July1998, upheld the U.S. Federal CircuitCourt of Appeals affirmation (in StateStreet v. Signature Financial) that “busi-ness methods” were proper subjectmatter for patents.

From 1998 through 2002, 128 businessmethod patents were issued in the class705/4 insurance category. Only 47 wereissued from 1985 to 1998, and none at allwere issued from 1978 through 1984!

Currently, there are over 200 insurancebusiness method patents pending, andthe count grows daily. The insurancesegment is not big in the whole schemeof things. The USPTO issues over180,000 patents and gets over 350,000new applications each year. However, youmay be getting the idea that you could bemissing out on something.

Recognizing and rewarding creative talentThe answer to the question, “Who ownsyour intellectual property?” begins with arecognition that you might have some. Ifyou are an employer, you may want toconsider what your employees’ expecta-tions are regarding this question, becausea difference in expectations can create aproblem.

Clearly, it would be difficult to impose anemployment contract that makesdemands on creative talent on an unsus-pecting employee population. My belief isthat a requirement to sign such an agree-ment cannot be made a condition ofcontinued employment. Rather, an insur-ance company that wakes up to the patentrevolution would probably have to beselective in which of its existing employ-ees it asks to sign an employment

agreement and provide some reward orcompensation if it expects those employees to assign their intellectualproperty to the company.

And, of course, appropriate job descrip-tion modifications and employmentcontracts that clearly provide for inven-tion will become a necessity for newhires in positions like actuarial productdesign and development, or in any otherposition in which problem solving is ajob requirement.

Even if your employer doesn’t suggest anemployment agreement, you may find itadvantageous to address this issue andarrive at some agreement relative toinvention prior to accepting employment.For example, this may be particularlyimportant if the reason you left yourprevious employer was because of adispute regarding an invention.

Basically, you, the individual inventor, arethe initial owner of your intellectualproperty. You can retain and use it foryour own profit if you have carefullyavoided any outside claims others mayhave on your work. Or, you can license itto others or sell it outright and reap therewards of your invention that way.

If your employer is enlightened, you mayfind yourself working in an environmentthat encourages and rewards your inven-tive efforts, but this is probably a little bitinto the future yet. Any way you go,however, recognize that your inventive-ness has value.�

Tom Bakos, FSA, MAAA, is president ofTom Bakos Consulting Inc., Ridgway, Colo.He can be reached at tbakos@

BakosEnterprises.com.

Who owns your intellectual property?continued from page 6

...Most invention in the insurance industry is donein small shops where constraints are not imposedon the way people think and where invention mayeven be rewarded.

(see Board Bulletins in the February 2003issue) and has explicitly directed the work-ing groups to set the ASA at approximatelyhalfway to FSA in the redesign.

The ASA Course will be module-based andconcentrate on integrating generalconcepts and functions across all practiceareas and using current practice-areaapplications of the concepts and functions.Material will be developed so that the ASACourse will be equivalent to one course inthe current system.

To accomplish these goals, the workinggroups’ current and primary activity, asendorsed by the Board, is to continue todefine instructional and learning objectivesfor the ASA Course and the practice areas.This includes objectives that are commonto all practice areas, practice-area-specificobjectives required of all candidates, andfundamental and practical functionsexpected of candidates planning to prac-tice in a given practice area.

With specific objectives in hand, the work-ing groups will be exploring innovativepresentation, delivery and assessmentoptions for the modularized, integratedASA course. Delivery and evaluationmechanisms will be considered to create amore engaging and useful learning experience for candidates and to capitalizeon available technologies and resources.The Board and the working groups will look to SOA staff to research and recom-mend mechanisms. One anticipatedbenefit of a more innovative approach todelivery mechanisms is an expected reduc-tion in travel time.

4. Preliminary education as conceived inthe September 2002 report is acceptable asis. The working groups should continue torefine learning objectives and define “vali-dation by experience.”

The working groups submitted a report tothe Board in September 2002. Subjects

addressed in the preliminary (pre-ASA)education will be categorized as prerequi-site (with no validation required),validated by experiences, or validated byexamination. The SOA will directly test thesubjects in the “validation by examination”category. Alternative means of acquiringand demonstrating mastery, such ascompletion of an approved set of collegecourses with acceptable grades and/or thecompletion of an approved learning/test-ing experience, will be acceptable forsubjects in the “prerequisite” or “validatedby experience” categories.

The working groups have recommendedthat calculus, linear algebra and accountingbe prerequisite subjects. Subjects to be vali-dated by experiences include economics,corporate finance and applied statistics.Subjects to be validated by examination(formally examined by the SOA) includemathematical probability, financial mathe-matics (theory of interest), contingenciesand actuarial modeling. The placement ofmathematical statistics is yet to be deter-mined.

With the Board’s March action, the work-ing groups will finalize the preliminaryeducation proposal, including the meaningof “validation by experience,” in advance ofthe June Board meeting.

5. Implementation of the new structureshould be preceded by the assurance thathigh-quality study materials are in place.

Commitment to developing high-qualitymaterials prior to implementation iscrucial to providing effective education forcandidates and creating a successfulsystem. The Board strongly endorsed thisstatement and will look to the working groups and staff to define a process foridentifying needs. The working groups andstaff plan to review what currently workswell, what needs to be adapted or is yet tobe developed and what resources will beused to create new materials.

The Board has contributed substantiallyto the process to date. The workinggroups very much appreciate the Board’scommitment, support and direction andwill be working diligently via a system-atic and multidisciplinary approach todesign, develop, deliver, implement, eval-uate and maintain the new system. Theworking groups consider their efforts asworks in progress and will continue tobalance market forces with the E&Esystem’s purpose.�

SOA Board of Governors endorses E&E redesign directioncontinued from page 11

the

ac

tua

ry may

20

03

17

E & E s e r i e s

Second ballot votingkicks off in July

The Society of Actuaries will holdthe second ballot election for offi-cers and board members beginningJuly 8. Board member candidatescan be found at www.soa.org/second_ballot03.html.

Since SOA elections materials aresent via e-mail, please check yourcontact information on the onlinedirectory to make sure it lists yourcurrent e-mail address. Fellows whodo not have an e-mail address onthe SOA database will receive paperelection materials in the mail. Allvoters will have 30 days to cast theirballots.

If you have any questions about theelection, please contact LoisChinnock at the SOA office at 847.706.3524 or [email protected].

18

the

ac

tua

ry m

ay

20

03

executivedirectornews

Board of Governorsreviews 2002 organizational results

At its March 13-14, 2003, meeting, the SOABoard of Governors reviewed the results ofan extremely successful year for the SOA.The year 2002 started off with some specialand significant challenges. In the aftermathof the September 11 tragedy and the widelyacknowledged slashes in industry supportfor professional education and businesstravel, the pressure on financial performancein all aspects of the organization was evengreater than usual.

However, 2002 was the third consecutiveyear of strong financial performance for theSOA. Currently, the member equity/reservefund balance is at the high end of the desig-nated range. This will allow the SOA to fundplanned initiatives.

The strategic focus of the organizationremains strong, and every strategic initiativeoutlined in the Strategic Plan was addressed.Here are some of the strategic highlights of2002:

• Offered 25 percent more seminars than last year.

• Generated record levels of participa-tion and revenue from continuing education.

• Attracted record attendance at the multidisciplinary Long-Term Care Conference; held successful critical illness and underwriting multidiscipli-nary seminars. All brought significant numbers of actuaries and nonactuaries together.

• Established inclusive dialogue with employers and practitioners regarding education and examinations (E&E) programs.