Embed Size (px)

Citation preview

THE ARTICLED

ISSUE 15 September 2016

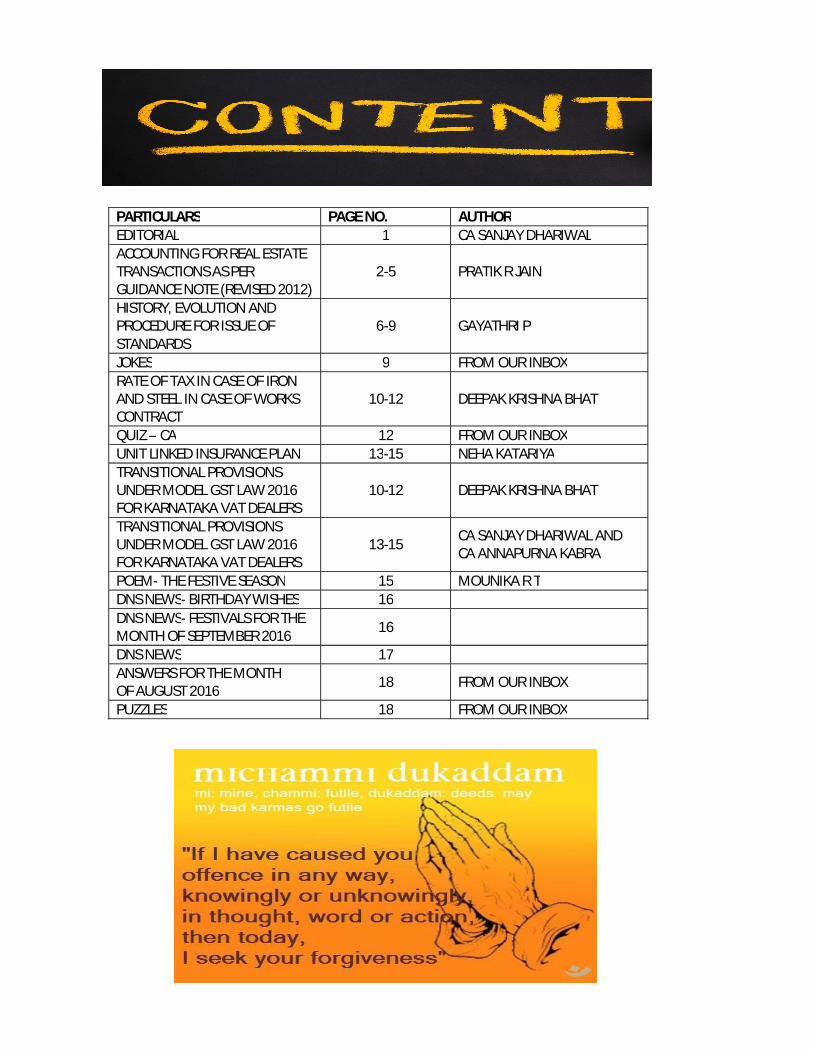

PARTICULARS PAGE NO. AUTHOR EDITORIAL 1 CA SANJAY DHARIWAL ACCOUNTING FOR REAL ESTATE TRANSACTIONS AS PER GUIDANCE NOTE (REVISED 2012)

2-5 PRATIK R JAIN

HISTORY, EVOLUTION AND PROCEDURE FOR ISSUE OF STANDARDS

6-9 GAYATHRI P

JOKES 9 FROM OUR INBOX RATE OF TAX IN CASE OF IRON AND STEEL IN CASE OF WORKS CONTRACT

10-12 DEEPAK KRISHNA BHAT

QUIZ – CA 12 FROM OUR INBOX UNIT LINKED INSURANCE PLAN 13-15 NEHA KATARIYA TRANSITIONAL PROVISIONS UNDER MODEL GST LAW 2016 FOR KARNATAKA VAT DEALERS

10-12 DEEPAK KRISHNA BHAT

TRANSITIONAL PROVISIONS UNDER MODEL GST LAW 2016 FOR KARNATAKA VAT DEALERS

13-15 CA SANJAY DHARIWAL AND CA ANNAPURNA KABRA

POEM- THE FESTIVE SEASON 15 MOUNIKA R T DNS NEWS- BIRTHDAY WISHES 16 DNS NEWS- FESTIVALS FOR THE MONTH OF SEPTEMBER 2016 16

DNS NEWS 17 ANSWERS FOR THE MONTH OF AUGUST 2016 18 FROM OUR INBOX

PUZZLES 18 FROM OUR INBOX

Ganesha Chaturthi (also known as Vināyaka Chaturthi, Ganēśa Chaturthī or Vināyaka Chaviti) is a Hindu

festival celebrated in honour of Ganesha, son of Shiva & Parvathy, the God with elephant-head. This day is considered to be a very auspicious day to pray to the god so that every new activity that is started is successfully completed without any obstacles

Samvatsarī (International Forgiveness Day) is the last day of Paryushana —the eight days festival of Jain.

It is the holiest day in the Jain calendar. Many Jains observe a complete fast on this day. The whole day is spent in prayers and contemplation. A yearly, elaborate penitential retreat called samvatsarī pratikramana is performed on this day. After the pratikramana Jains seek forgiveness from all the creatures of the world whom they may have harmed knowingly or unknowingly by uttering the phrase—Micchami Dukkadam, "Khamau Sa", or "Khamat Khamna". As integral part of ritual, Jains personally greet their friends, relatives and other near and dear ones Micchami Dukkadam, especially to those with whom one has day today interaction. No private quarrel or dispute may be carried beyond Samvatsarī. Messages and telephone calls are made even to the outstation friends and relatives asking their forgiveness. This gives a great internal peace and satisfaction to one’s soul.

Teachers' Day is a special day for the appreciation of teachers, and may include celebrations to honour

them for their special contributions in a particular field area, or the community in general. Children (Students) show their respect to their teachers by organizing various programs in their schools. We remember and celebrate the birthday of Dr. S Radhakrishnan, as teacher’s day on 5th of September every year.

Regards, CA Sanjay Dhariwal Editor- in- chief

EDITOR BOARD Editor-in- Chief CA Sanjay Dhariwal [email protected] Editor Smruti Shah [email protected]

Coordinators Coordinators S. Sophia [email protected] Coordinators Deepak Shrimali [email protected]

ACCOUNTING FOR REAL ESTATE TRANSACTIONS AS PER GUIDANCE NOTE (REVISED 2012)

- By: PRATIK R JAIN The growth of real estate sector has always contributed towards increase in Indian economy. In recent past, various real estate developers have followed different practices in recognizing their revenue. Considering this, ICAI felt the necessity of revision in this guidance note for recognition of revenue in a uniform manner by all the real estate developers.

This guidance note recommends accounting treatment by enterprises dealing in ‘Real Estate’ as sellers or developers. The term ‘real estate’ refers to land as well as buildings and rights in relation thereto. Enterprises who undertake such activity are generally referred to by different terms such as ‘real estate developers’, ‘builders’ or ‘property developers’.

SCOPE

This Guidance Note covers all forms of transactions in real estate. An illustrative list of transactions which are covered by this Guidance Note is as under:

1. Sale of plot of land (including long term sale type leases) without any development.

2. Sale of plot of land (including long term sale type leases) with development in the form of common facilities like laying of roads, drainage lines and water pipelines, electrical lines, sewage tanks, water storage tanks, sports facilities, gymnasium, club house, landscaping, etc.

3. Development and sale of residential and commercial units, row houses, independent houses, with or without an undivided share in land.

4. Acquisition, utilization and transfer of development rights.

5. Redevelopment of existing buildings and structures.

6. Joint development agreements for any of the above facilities.

This guidance note is based on application of Percentage of Completion Method. It draws upon principles enunciated in Accounting Standard 7, Construction Contracts and Accounting Standard 9, Revenue Recognition.

ACCOUNTING FOR REAL ESTATE TRANSACTION

The nature of Real estate transactions are such that the date of commencement and the date of completion are spread over two or more accounting periods. For recognition of revenue in case of real estate sales, the conditions mentioned in Paragraphs 10 and 11 of AS-9, Revenue Recognition must be satisfied, i.e., all significant risks and rewards of ownership has been transferred to the buyer along with possession of the unit and the seller retains no control of the unit.

In case of real estate sales, the seller usually enters into an agreement with the buyer at initial stages of construction. This agreement is also considered having transferred all risks and rewards of ownership to the buyer provided the agreement is legally enforceable and subject to satisfaction of conditions which signify transferring all significant risks and rewards even though the legal title is not transferred or possession is not given to the buyer. Once, all risks and rewards are transferred to the buyer, any act done by the seller is considered to be performed on behalf of the buyer. Accordingly, revenue in such cases is recognized by applying the Percentage of Completion Method.

Where individual contracts are a part of a single project, even after signing of a legally enforceable individual contract and transferring all the risks and reward revenue in respect of such individual contract cannot be recognized until the performance on the remaining components of the project is pending. Revenue will be recognized only when performance on the remaining components of the project is considered to be complete.

When development right are sold or transferred, revenue should be recognized when both the following conditions are satisfied:

1. Title to the development rights is transferred to the buyer; and

2. It is not unreasonable to expect ultimate realization of revenue

APPLICATION OF PERCENTAGE COMPLETION METHOD

The percentage completion method should be applied in the accounting of all real estate transactions/ activities where the economic substance is similar to construction contracts.

This method is applied when the outcome of a real estate project can be estimated reliably and when all the following conditions are satisfied:

1. Total project revenue can be estimated reliably; 2. It is probable that economic benefits associated with the project will flow to the

enterprise; 3. The project cost and stage of project completion at the reporting date can be measured

reliably; and 4. The project cost attributable to the project can be clearly identified and measured

reliably so that actual project cost incurred can be compared with prior estimates

Further, revenue should be recognized under the percentage completion method only when the following conditions are satisfied:

1. All approvals for commencement of project have been obtained like Environmental and other clearances, Title to land or other rights to development, Approval of plan, design, etc.

2. The stage of completion of the project reaches a reasonable level of development, i.e., expenditure incurred on construction and development cost should be 25% or more than 25% of estimated construction and development cost.

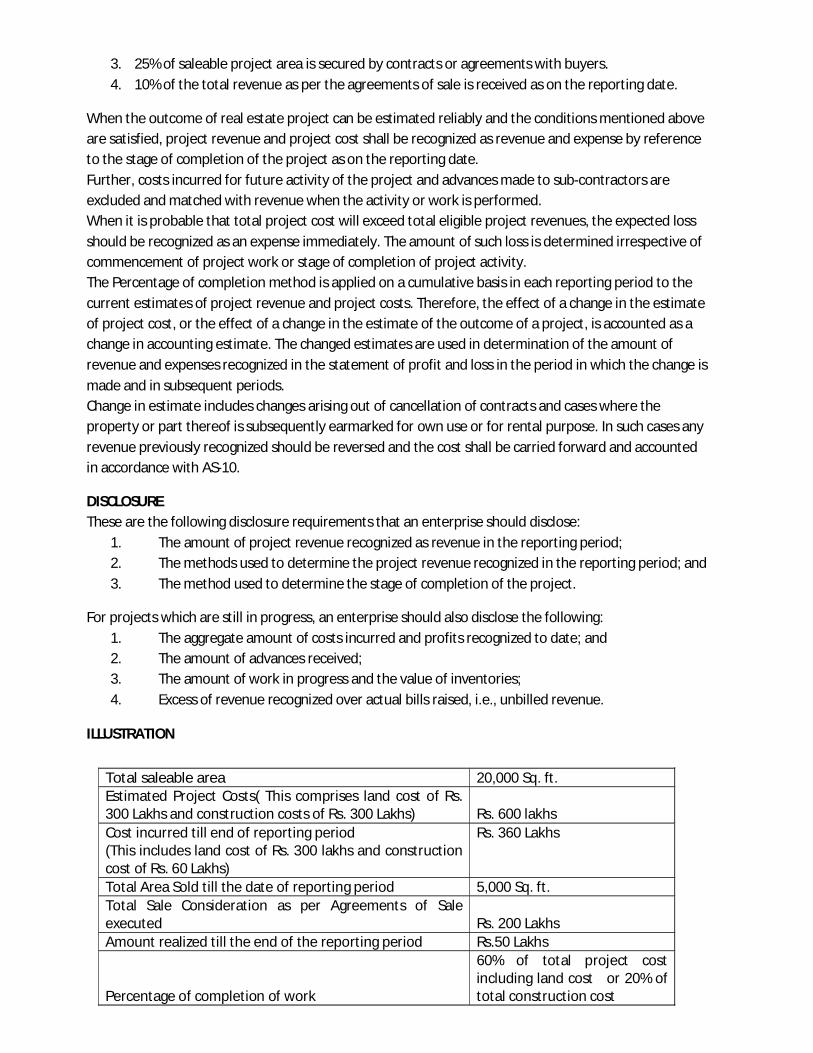

Total saleable area 20,000 Sq. ft. Estimated Project Costs( This comprises land cost of Rs. 300 Lakhs and construction costs of Rs. 300 Lakhs) Rs. 600 lakhs Cost incurred till end of reporting period Rs. 360 Lakhs (This includes land cost of Rs. 300 lakhs and construction cost of Rs. 60 Lakhs) Total Area Sold till the date of reporting period 5,000 Sq. ft. Total Sale Consideration as per Agreements of Sale executed Rs. 200 Lakhs Amount realized till the end of the reporting period Rs.50 Lakhs

Percentage of completion of work

60% of total project cost including land cost or 20% of total construction cost

3. 25% of saleable project area is secured by contracts or agreements with buyers. 4. 10% of the total revenue as per the agreements of sale is received as on the reporting date.

When the outcome of real estate project can be estimated reliably and the conditions mentioned above are satisfied, project revenue and project cost shall be recognized as revenue and expense by reference to the stage of completion of the project as on the reporting date. Further, costs incurred for future activity of the project and advances made to sub-contractors are excluded and matched with revenue when the activity or work is performed. When it is probable that total project cost will exceed total eligible project revenues, the expected loss should be recognized as an expense immediately. The amount of such loss is determined irrespective of commencement of project work or stage of completion of project activity. The Percentage of completion method is applied on a cumulative basis in each reporting period to the current estimates of project revenue and project costs. Therefore, the effect of a change in the estimate of project cost, or the effect of a change in the estimate of the outcome of a project, is accounted as a change in accounting estimate. The changed estimates are used in determination of the amount of revenue and expenses recognized in the statement of profit and loss in the period in which the change is made and in subsequent periods. Change in estimate includes changes arising out of cancellation of contracts and cases where the property or part thereof is subsequently earmarked for own use or for rental purpose. In such cases any revenue previously recognized should be reversed and the cost shall be carried forward and accounted in accordance with AS-10.

DISCLOSURE These are the following disclosure requirements that an enterprise should disclose:

1. The amount of project revenue recognized as revenue in the reporting period; 2. The methods used to determine the project revenue recognized in the reporting period; and 3. The method used to determine the stage of completion of the project.

For projects which are still in progress, an enterprise should also disclose the following: 1. The aggregate amount of costs incurred and profits recognized to date; and 2. The amount of advances received; 3. The amount of work in progress and the value of inventories; 4. Excess of revenue recognized over actual bills raised, i.e., unbilled revenue.

ILLUSTRATION

JOKES

1. Knock knock Somebody knocks on door: - Who is there? - Police? - What do you want? - We want to talk. - How many of you are there? - Two. - So talk with each other.

2. 100 dollar bill A: Why are you late? B: There was a man who lost a hundred dollar bill. A: That's nice. Were you helping him look for it? B: No, I was standing on it.

3. Teacher vs Student Two boys were arguing when the teacher entered the room. The teacher says, "Why are you arguing?" One boy answers, "We found a ten dollarbill and decided to give it to whoever tells the biggest lie." "You should be ashamed of yourselves," said the teacher, "When I was your age I didn't even know what a lie was." The boys gave the ten dollars to the teacher.

FROM OUR INBOX

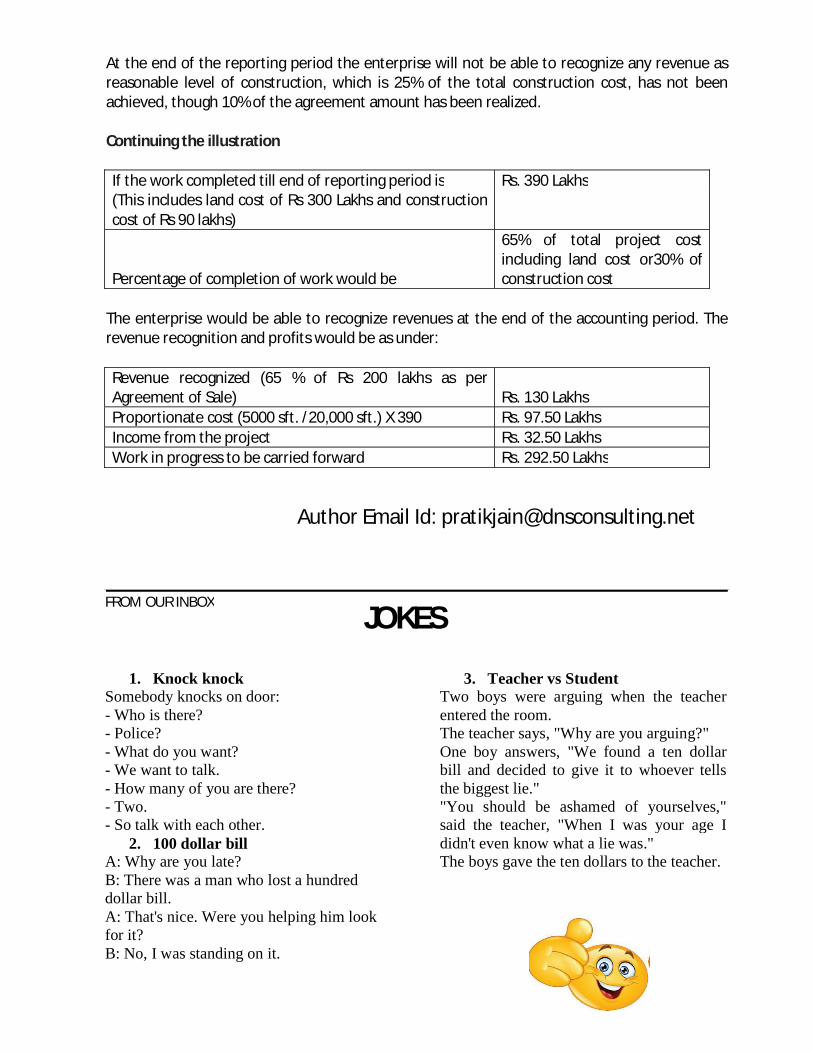

At the end of the reporting period the enterprise will not be able to recognize any revenue as reasonable level of construction, which is 25% of the total construction cost, has not been achieved, though 10% of the agreement amount has been realized. Continuing the illustration If the work completed till end of reporting period is Rs. 390 Lakhs (This includes land cost of Rs 300 Lakhs and construction cost of Rs 90 lakhs)

Percentage of completion of work would be

65% of total project cost including land cost or30% of construction cost

The enterprise would be able to recognize revenues at the end of the accounting period. The revenue recognition and profits would be as under: Revenue recognized (65 % of Rs 200 lakhs as per Agreement of Sale) Rs. 130 Lakhs Proportionate cost (5000 sft. /20,000 sft.) X 390 Rs. 97.50 Lakhs Income from the project Rs. 32.50 Lakhs Work in progress to be carried forward Rs. 292.50 Lakhs

Author Email Id: [email protected]

HISTORY, EVOLUTION AND PROCEDURE FOR ISSUE OF STANDARDS

- By: GAYATHRI P

Overview

The expanded use of technology in both the operating and financial systems of companies has significantly affected the audit environment, forcing audit firms to recruit, train and deploy a large number of information technology specialists to support their audit efforts.

In this changing environment, it is obvious that a professional accountant should adhere to standards and procedures laid down by the professional accountancy bodies of which he is a member while discharging his duties in a responsible manner. Hence The Institute of Chartered Accountants of India (ICAI) has formulated auditing and accounting standards for the guidance of its member.

Auditing

Auditing is a systematic examination of data, records, operations & performance. Auditing is nothing but Checking, Examining and reporting of Financial statements. However in practical life Auditing is extremely different where a number of questions arise in our mind and which cannot be reconciled or revalued easily as explained by the client.

Example: You had gone for an audit of manufacturing unit and there is a chemical of 10000 litres in the tank which is valuing to Rs.5 Crore. As an auditor you may get different types of questions and you ask an employee to explain about the same. Later you may be confused as which of the following would give better assurance,. Like

An Oral Explanation from the client Production head written letter Expert Opinion Appointment of expert by an auditor etc.

Necessity for standards

Hence for the purpose of getting clarity on these aspects the Principles & guidance are required which guide us in an audit. In the absence of these principles and guidance even an auditor shall be in an ambiguity of how to proceed with an audit and what the major areas to be covered are.

Therefore the standards are required for the following purposes: To assist professionals to provide assurance & related services. To improve efficiency & effectiveness To bring consistency in professional work To maintain quality (Reliability) To improve trust of society on professionals

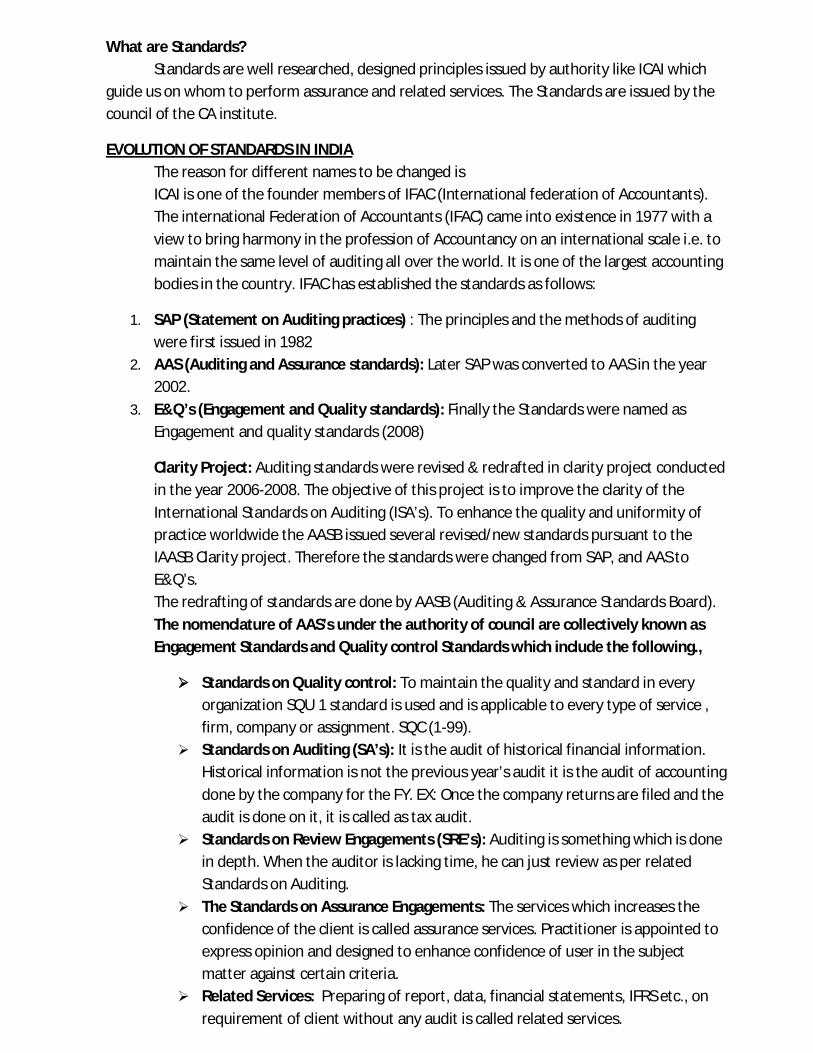

What are Standards? Standards are well researched, designed principles issued by authority like ICAI which guide us on whom to perform assurance and related services. The Standards are issued by the council of the CA institute.

EVOLUTION OF STANDARDS IN INDIA The reason for different names to be changed is ICAI is one of the founder members of IFAC (International federation of Accountants). The international Federation of Accountants (IFAC) came into existence in 1977 with a view to bring harmony in the profession of Accountancy on an international scale i.e. to maintain the same level of auditing all over the world. It is one of the largest accounting bodies in the country. IFAC has established the standards as follows:

1. SAP (Statement on Auditing practices) : The principles and the methods of auditing were first issued in 1982

2. AAS (Auditing and Assurance standards): Later SAP was converted to AAS in the year 2002.

3. E&Q’s (Engagement and Quality standards): Finally the Standards were named as Engagement and quality standards (2008)

Clarity Project: Auditing standards were revised & redrafted in clarity project conducted in the year 2006-2008. The objective of this project is to improve the clarity of the International Standards on Auditing (ISA’s). To enhance the quality and uniformity of practice worldwide the AASB issued several revised/new standards pursuant to the IAASB Clarity project. Therefore the standards were changed from SAP, and AAS to E&Q’s. The redrafting of standards are done by AASB (Auditing & Assurance Standards Board). The nomenclature of AAS’s under the authority of council are collectively known as Engagement Standards and Quality control Standards which include the following.,

Standards on Quality control: To maintain the quality and standard in every organization SQU 1 standard is used and is applicable to every type of service , firm, company or assignment. SQC (1-99).

Standards on Auditing (SA’s): It is the audit of historical financial information. Historical information is not the previous year’s audit it is the audit of accounting done by the company for the FY. EX: Once the company returns are filed and the audit is done on it, it is called as tax audit.

Standards on Review Engagements (SRE’s): Auditing is something which is done in depth. When the auditor is lacking time, he can just review as per related Standards on Auditing.

The Standards on Assurance Engagements: The services which increases the confidence of the client is called assurance services. Practitioner is appointed to express opinion and designed to enhance confidence of user in the subject matter against certain criteria.

Related Services: Preparing of report, data, financial statements, IFRS etc., on requirement of client without any audit is called related services.

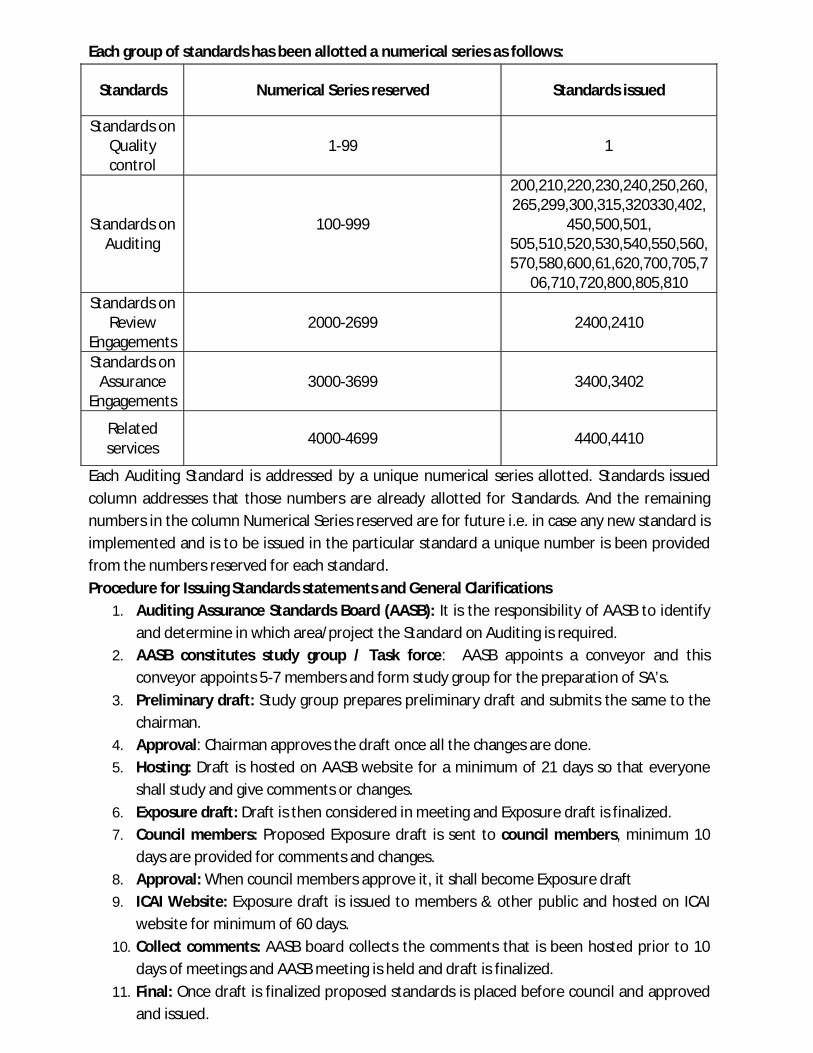

Each group of standards has been allotted a numerical series as follows:

Standards Numerical Series reserved Standards issued

Standards on Quality control

1-99 1

Standards on Auditing

100-999

200,210,220,230,240,250,260,265,299,300,315,320330,402,

450,500,501, 505,510,520,530,540,550,560,570,580,600,61,620,700,705,7

06,710,720,800,805,810 Standards on

Review Engagements

2000-2699 2400,2410

Standards on Assurance

Engagements 3000-3699 3400,3402

Related services 4000-4699 4400,4410

Each Auditing Standard is addressed by a unique numerical series allotted. Standards issued column addresses that those numbers are already allotted for Standards. And the remaining numbers in the column Numerical Series reserved are for future i.e. in case any new standard is implemented and is to be issued in the particular standard a unique number is been provided from the numbers reserved for each standard. Procedure for Issuing Standards statements and General Clarifications

1. Auditing Assurance Standards Board (AASB): It is the responsibility of AASB to identify and determine in which area/project the Standard on Auditing is required.

2. AASB constitutes study group / Task force: AASB appoints a conveyor and this conveyor appoints 5-7 members and form study group for the preparation of SA’s.

3. Preliminary draft: Study group prepares preliminary draft and submits the same to the chairman.

4. Approval: Chairman approves the draft once all the changes are done. 5. Hosting: Draft is hosted on AASB website for a minimum of 21 days so that everyone

shall study and give comments or changes. 6. Exposure draft: Draft is then considered in meeting and Exposure draft is finalized. 7. Council members: Proposed Exposure draft is sent to council members, minimum 10

days are provided for comments and changes. 8. Approval: When council members approve it, it shall become Exposure draft 9. ICAI Website: Exposure draft is issued to members & other public and hosted on ICAI

website for minimum of 60 days. 10. Collect comments: AASB board collects the comments that is been hosted prior to 10

days of meetings and AASB meeting is held and draft is finalized. 11. Final: Once draft is finalized proposed standards is placed before council and approved

and issued.

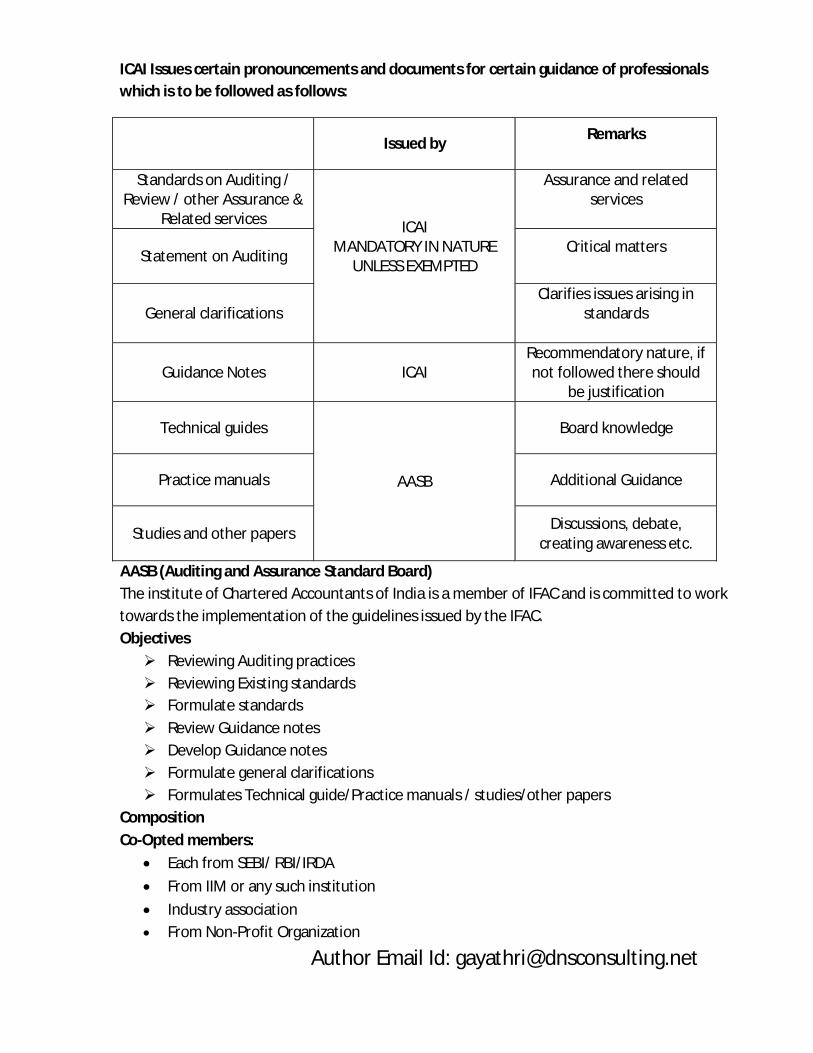

ICAI Issues certain pronouncements and documents for certain guidance of professionals which is to be followed as follows:

Issued by Remarks

Standards on Auditing / Review / other Assurance &

Related services ICAI MANDATORY IN NATURE

UNLESS EXEMPTED

Assurance and related services

Statement on Auditing Critical matters

General clarifications Clarifies issues arising in

standards

Guidance Notes ICAI Recommendatory nature, if not followed there should

be justification

Technical guides

AASB

Board knowledge

Practice manuals Additional Guidance

Studies and other papers Discussions, debate, creating awareness etc.

AASB (Auditing and Assurance Standard Board) The institute of Chartered Accountants of India is a member of IFAC and is committed to work towards the implementation of the guidelines issued by the IFAC. Objectives Reviewing Auditing practices Reviewing Existing standards Formulate standards Review Guidance notes Develop Guidance notes Formulate general clarifications Formulates Technical guide/Practice manuals / studies/other papers

Composition Co-Opted members:

Each from SEBI/ RBI/IRDA From IIM or any such institution Industry association From Non-Profit Organization

Author Email Id: [email protected]

RATE OF TAX IN CASE OF IRON AND STEEL IN CASE OF WORKS CONTRACT

- By: DEEPAK KRISHNA BHAT

A Long standing Dispute In the above subject has been resolved in the recent Supreme Court Decision (ref:-Smt B Narasamma Vs Deputy Commercial Taxes)

Applicable Provisions of Central Sales tax and constitution

Article 286(3), Restrictions as to imposition of tax on the sale or purchase of goods (3) Any law of a State shall, in so far as it imposes, or authorizes the imposition of,

(a) a tax on the sale or purchase of goods declared by Parliament by law to be of special importance in inter State trade or commerce; or

(b) a tax on the sale or purchase of goods, being a tax of the nature referred to in sub clause (b), sub clause

(c) or sub clause (d) of clause 29 A of Article 366, be subject to such restrictions and conditions in regard to the system of levy, rates and other incidents of the tax as Parliament may by law specify.”

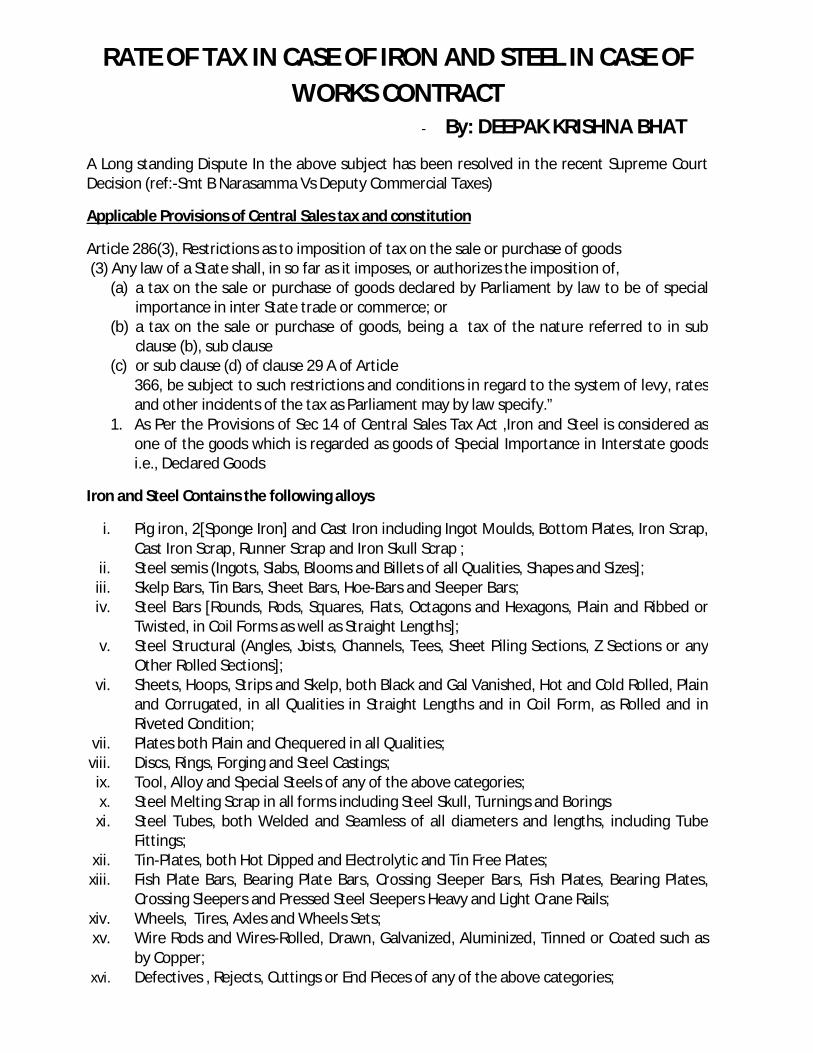

1. As Per the Provisions of Sec 14 of Central Sales Tax Act ,Iron and Steel is considered as one of the goods which is regarded as goods of Special Importance in Interstate goods i.e., Declared Goods

Iron and Steel Contains the following alloys

i. Pig iron, 2[Sponge Iron] and Cast Iron including Ingot Moulds, Bottom Plates, Iron Scrap, Cast Iron Scrap, Runner Scrap and Iron Skull Scrap ;

ii. Steel semis (Ingots, Slabs, Blooms and Billets of all Qualities, Shapes and Sizes]; iii. Skelp Bars, Tin Bars, Sheet Bars, Hoe-Bars and Sleeper Bars; iv. Steel Bars [Rounds, Rods, Squares, Flats, Octagons and Hexagons, Plain and Ribbed or

Twisted, in Coil Forms as well as Straight Lengths]; v. Steel Structural (Angles, Joists, Channels, Tees, Sheet Piling Sections, Z Sections or any

Other Rolled Sections]; vi. Sheets, Hoops, Strips and Skelp, both Black and Gal Vanished, Hot and Cold Rolled, Plain

and Corrugated, in all Qualities in Straight Lengths and in Coil Form, as Rolled and in Riveted Condition;

vii. Plates both Plain and Chequered in all Qualities; viii. Discs, Rings, Forging and Steel Castings;

ix. Tool, Alloy and Special Steels of any of the above categories; x. Steel Melting Scrap in all forms including Steel Skull, Turnings and Borings xi. Steel Tubes, both Welded and Seamless of all diameters and lengths, including Tube

Fittings; xii. Tin-Plates, both Hot Dipped and Electrolytic and Tin Free Plates; xiii. Fish Plate Bars, Bearing Plate Bars, Crossing Sleeper Bars, Fish Plates, Bearing Plates,

Crossing Sleepers and Pressed Steel Sleepers Heavy and Light Crane Rails; xiv. Wheels, Tires, Axles and Wheels Sets; xv. Wire Rods and Wires-Rolled, Drawn, Galvanized, Aluminized, Tinned or Coated such as

by Copper; xvi. Defectives , Rejects, Cuttings or End Pieces of any of the above categories;

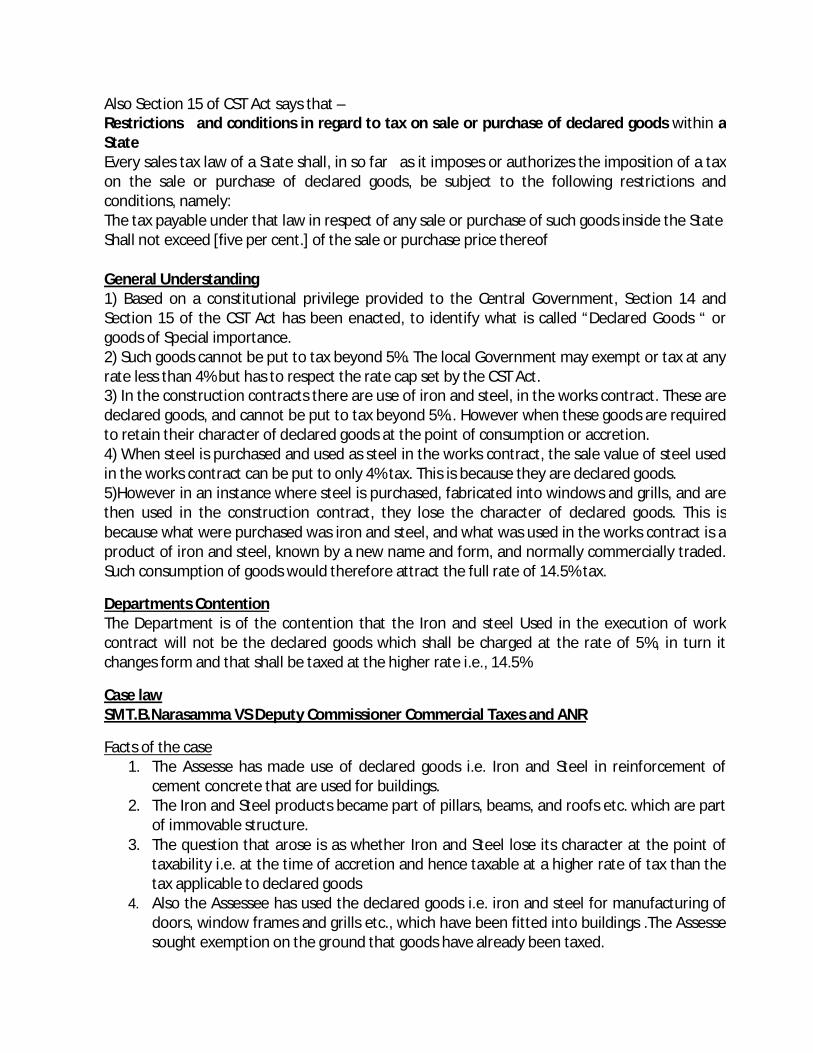

Also Section 15 of CST Act says that – Restrictions and conditions in regard to tax on sale or purchase of declared goods within a State Every sales tax law of a State shall, in so far as it imposes or authorizes the imposition of a tax on the sale or purchase of declared goods, be subject to the following restrictions and conditions, namely: The tax payable under that law in respect of any sale or purchase of such goods inside the State Shall not exceed [five per cent.] of the sale or purchase price thereof General Understanding 1) Based on a constitutional privilege provided to the Central Government, Section 14 and Section 15 of the CST Act has been enacted, to identify what is called “Declared Goods “ or goods of Special importance. 2) Such goods cannot be put to tax beyond 5%. The local Government may exempt or tax at any rate less than 4% but has to respect the rate cap set by the CST Act. 3) In the construction contracts there are use of iron and steel, in the works contract. These are declared goods, and cannot be put to tax beyond 5%.. However when these goods are required to retain their character of declared goods at the point of consumption or accretion. 4) When steel is purchased and used as steel in the works contract, the sale value of steel used in the works contract can be put to only 4% tax. This is because they are declared goods. 5)However in an instance where steel is purchased, fabricated into windows and grills, and are then used in the construction contract, they lose the character of declared goods. This is because what were purchased was iron and steel, and what was used in the works contract is a product of iron and steel, known by a new name and form, and normally commercially traded. Such consumption of goods would therefore attract the full rate of 14.5% tax.

Departments Contention The Department is of the contention that the Iron and steel Used in the execution of work contract will not be the declared goods which shall be charged at the rate of 5%, in turn it changes form and that shall be taxed at the higher rate i.e., 14.5%

Case law SMT.B.Narasamma VS Deputy Commissioner Commercial Taxes and ANR

Facts of the case 1. The Assesse has made use of declared goods i.e. Iron and Steel in reinforcement of

cement concrete that are used for buildings. 2. The Iron and Steel products became part of pillars, beams, and roofs etc. which are part

of immovable structure. 3. The question that arose is as whether Iron and Steel lose its character at the point of

taxability i.e. at the time of accretion and hence taxable at a higher rate of tax than the tax applicable to declared goods

4. Also the Assessee has used the declared goods i.e. iron and steel for manufacturing of doors, window frames and grills etc., which have been fitted into buildings .The Assesse sought exemption on the ground that goods have already been taxed.

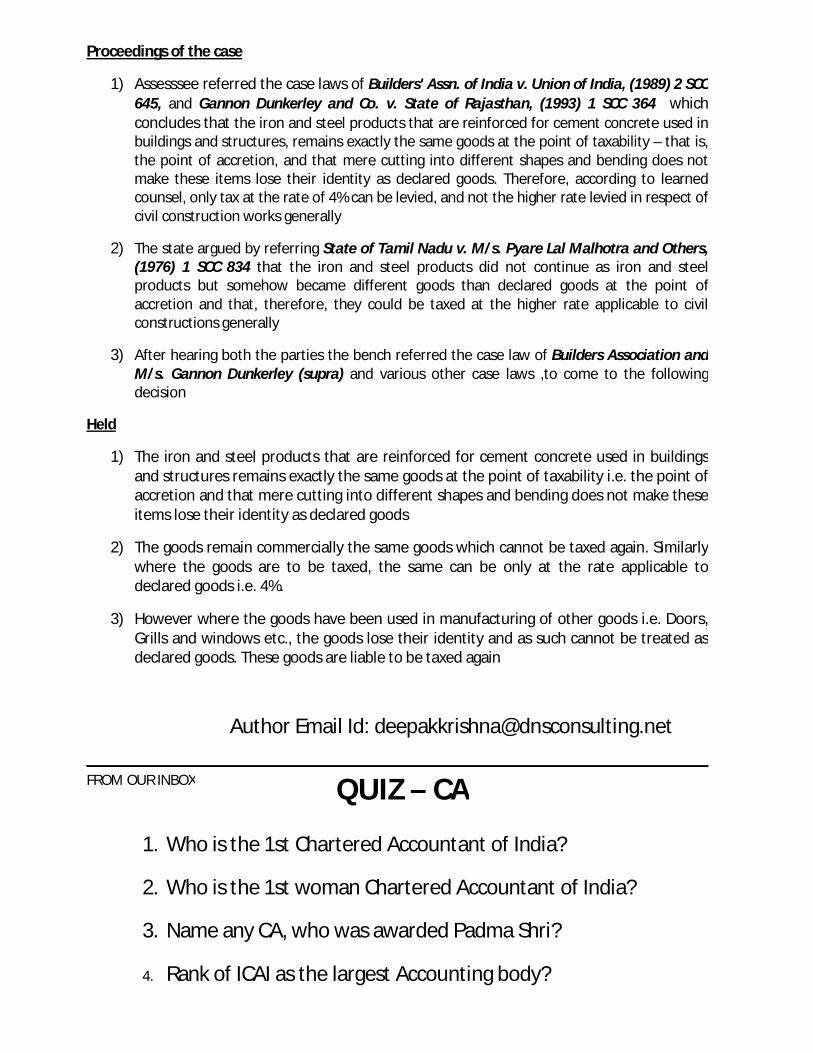

Proceedings of the case

1) Assesssee referred the case laws of Builders' Assn. of India v. Union of India, (1989) 2 SCC 645, and Gannon Dunkerley and Co. v. State of Rajasthan, (1993) 1 SCC 364 which concludes that the iron and steel products that are reinforced for cement concrete used in buildings and structures, remains exactly the same goods at the point of taxability – that is, the point of accretion, and that mere cutting into different shapes and bending does not make these items lose their identity as declared goods. Therefore, according to learned counsel, only tax at the rate of 4% can be levied, and not the higher rate levied in respect of civil construction works generally

2) The state argued by referring State of Tamil Nadu v. M/s. Pyare Lal Malhotra and Others, (1976) 1 SCC 834 that the iron and steel products did not continue as iron and steel products but somehow became different goods than declared goods at the point of accretion and that, therefore, they could be taxed at the higher rate applicable to civil constructions generally

3) After hearing both the parties the bench referred the case law of Builders Association and M/s. Gannon Dunkerley (supra) and various other case laws ,to come to the following decision

Held

1) The iron and steel products that are reinforced for cement concrete used in buildings and structures remains exactly the same goods at the point of taxability i.e. the point of accretion and that mere cutting into different shapes and bending does not make these items lose their identity as declared goods

2) The goods remain commercially the same goods which cannot be taxed again. Similarly where the goods are to be taxed, the same can be only at the rate applicable todeclared goods i.e. 4%.

3) However where the goods have been used in manufacturing of other goods i.e. Doors, Grills and windows etc., the goods lose their identity and as such cannot be treated as declared goods. These goods are liable to be taxed again

Author Email Id: [email protected]

QUIZ – CA

1. Who is the 1st Chartered Accountant of India?

2. Who is the 1st woman Chartered Accountant of India?

3. Name any CA, who was awarded Padma Shri?

4. Rank of ICAI as the largest Accounting body?

FROM OUR INBOX

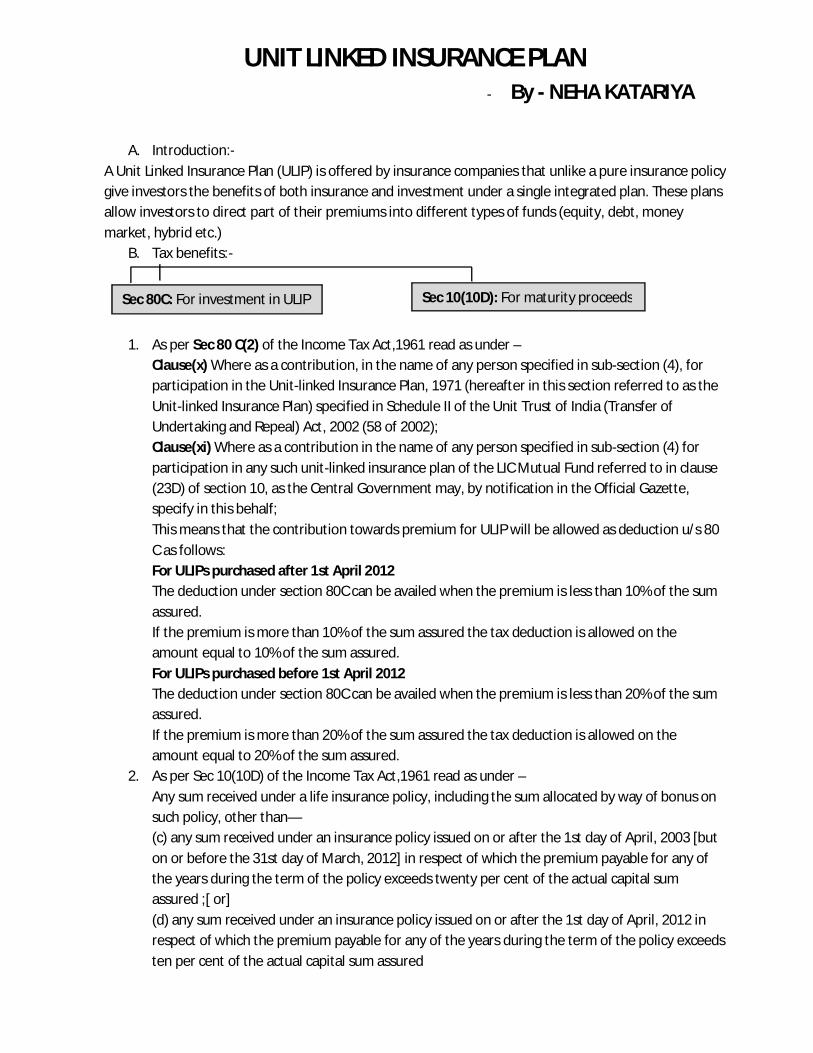

UNIT LINKED INSURANCE PLAN - By - NEHA KATARIYA

A. Introduction:- A Unit Linked Insurance Plan (ULIP) is offered by insurance companies that unlike a pure insurance policy give investors the benefits of both insurance and investment under a single integrated plan. These plans allow investors to direct part of their premiums into different types of funds (equity, debt, money market, hybrid etc.)

B. Tax benefits:-

1. As per Sec 80 C(2) of the Income Tax Act,1961 read as under –

Clause(x) Where as a contribution, in the name of any person specified in sub-section (4), for participation in the Unit-linked Insurance Plan, 1971 (hereafter in this section referred to as the Unit-linked Insurance Plan) specified in Schedule II of the Unit Trust of India (Transfer of Undertaking and Repeal) Act, 2002 (58 of 2002); Clause(xi) Where as a contribution in the name of any person specified in sub-section (4) for participation in any such unit-linked insurance plan of the LIC Mutual Fund referred to in clause (23D) of section 10, as the Central Government may, by notification in the Official Gazette, specify in this behalf; This means that the contribution towards premium for ULIP will be allowed as deduction u/s 80 C as follows: For ULIPs purchased after 1st April 2012 The deduction under section 80C can be availed when the premium is less than 10% of the sum assured. If the premium is more than 10% of the sum assured the tax deduction is allowed on the amount equal to 10% of the sum assured. For ULIPs purchased before 1st April 2012 The deduction under section 80C can be availed when the premium is less than 20% of the sum assured. If the premium is more than 20% of the sum assured the tax deduction is allowed on the amount equal to 20% of the sum assured.

2. As per Sec 10(10D) of the Income Tax Act,1961 read as under – Any sum received under a life insurance policy, including the sum allocated by way of bonus on such policy, other than— (c) any sum received under an insurance policy issued on or after the 1st day of April, 2003 [but on or before the 31st day of March, 2012] in respect of which the premium payable for any of the years during the term of the policy exceeds twenty per cent of the actual capital sum assured ;[ or] (d) any sum received under an insurance policy issued on or after the 1st day of April, 2012 in respect of which the premium payable for any of the years during the term of the policy exceeds ten per cent of the actual capital sum assured

Sec 80C: For investment in ULIP Sec 10(10D): For maturity proceeds

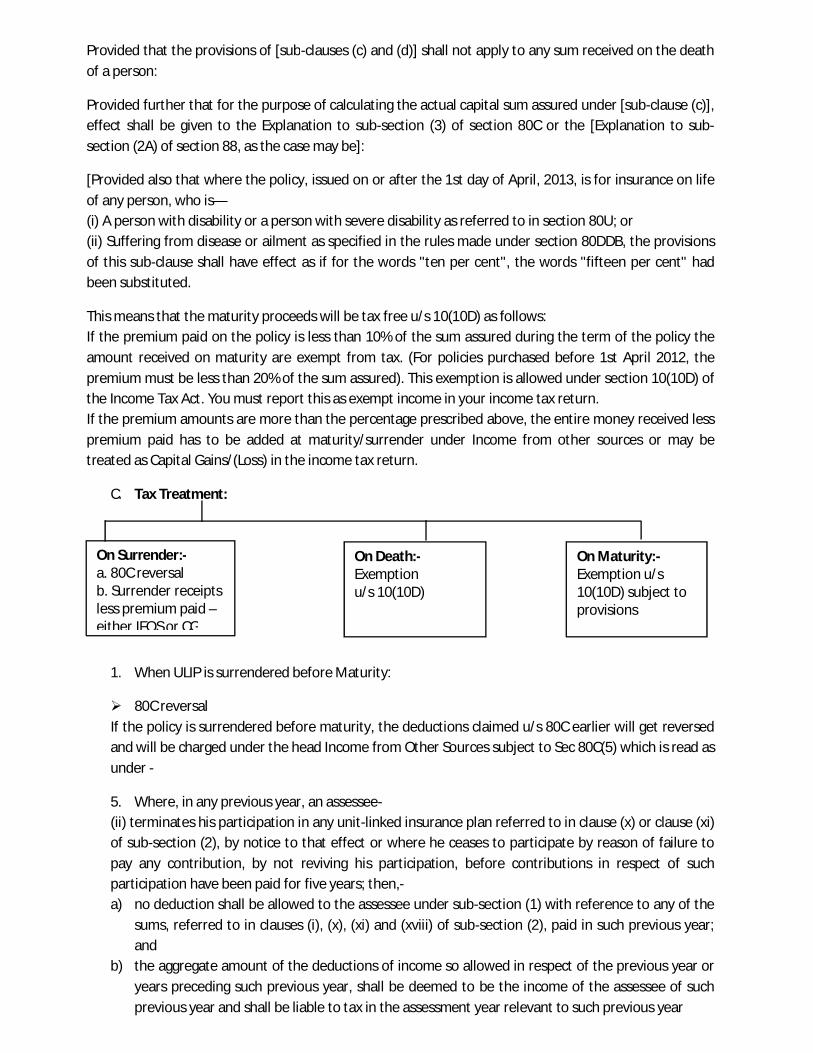

Provided that the provisions of [sub-clauses (c) and (d)] shall not apply to any sum received on the death of a person:

Provided further that for the purpose of calculating the actual capital sum assured under [sub-clause (c)], effect shall be given to the Explanation to sub-section (3) of section 80C or the [Explanation to sub-section (2A) of section 88, as the case may be]:

[Provided also that where the policy, issued on or after the 1st day of April, 2013, is for insurance on life of any person, who is— (i) A person with disability or a person with severe disability as referred to in section 80U; or (ii) Suffering from disease or ailment as specified in the rules made under section 80DDB, the provisions of this sub-clause shall have effect as if for the words "ten per cent", the words "fifteen per cent" had been substituted.

This means that the maturity proceeds will be tax free u/s 10(10D) as follows: If the premium paid on the policy is less than 10% of the sum assured during the term of the policy the amount received on maturity are exempt from tax. (For policies purchased before 1st April 2012, the premium must be less than 20% of the sum assured). This exemption is allowed under section 10(10D) of the Income Tax Act. You must report this as exempt income in your income tax return. If the premium amounts are more than the percentage prescribed above, the entire money received less premium paid has to be added at maturity/surrender under Income from other sources or may be treated as Capital Gains/(Loss) in the income tax return.

C. Tax Treatment:

1. When ULIP is surrendered before Maturity:

80C reversal If the policy is surrendered before maturity, the deductions claimed u/s 80C earlier will get reversed and will be charged under the head Income from Other Sources subject to Sec 80C(5) which is read as under -

5. Where, in any previous year, an assessee- (ii) terminates his participation in any unit-linked insurance plan referred to in clause (x) or clause (xi) of sub-section (2), by notice to that effect or where he ceases to participate by reason of failure to pay any contribution, by not reviving his participation, before contributions in respect of such participation have been paid for five years; then,- a) no deduction shall be allowed to the assessee under sub-section (1) with reference to any of the

sums, referred to in clauses (i), (x), (xi) and (xviii) of sub-section (2), paid in such previous year; and

b) the aggregate amount of the deductions of income so allowed in respect of the previous year or years preceding such previous year, shall be deemed to be the income of the assessee of such previous year and shall be liable to tax in the assessment year relevant to such previous year

On Surrender:- a. 80C reversal b. Surrender receipts less premium paid –either IFOS or CG

On Death:- Exemption u/s 10(10D)

On Maturity:- Exemption u/s 10(10D) subject to provisions

Surrender Receipts less Premium paid Thus the assessee will have to pay tax by treating the policy proceeds less premium paid either as Income from Other Sources or as Capital Gains/(Loss).It was also as held in the case of The ACIT, Ahemdabad V/s Girish Haribhai Trivedi (this case law is discussed at the end of this article)“. TDS u/s 194DA When the conditions of Section 10(10D) on surrender are not met, tax is deducted by the Insurance companies as per the new section 194DA (TDS on Maturity of Life Insurance Policy) of Income Tax Act, 1961 read as under - Any person responsible for paying to a resident any sum under a life insurance policy, including the sum allocated by way of bonus on such policy, other than the amount not includible in the total income under clause (10D) of section 10, shall, at the time of payment thereof, deduct income-tax thereon at the rate of 1[one] per cent: Provided that no deduction under this section shall be made where the amount of such payment or, as the case may be, the aggregate amount of such payments to the payee during the financial year is less than one hundred thousand rupees. 2. When ULIP is surrendered due to Death: It is tax free under Section 10(10D) of Income Tax Act. (as discussed above) 3. When ULIP is matured: The amount received at maturity will be tax free subject to provisions of Sec 10(10D) If the premium paid is more than 10 percent of sum assured, the maturity benefit less premium paid will be added to insured's income. Insurance company will also deduct tax from such policies as per newly inserted section mentioned below. Remaining tax has to be paid by insured at time of filing ITR either under the head Capital Gains/Losses or Income from Other Sources. As per the new section 194DA of IT Act (effective from 1st October 2014), if premium paid is more than 10 percent of sum assured and policy proceeds for a year exceeds R. 1 lakhs, then the tax deductions by insurer will be as under: At 1% (for valid Pan registered) At 20% (for valid Pan not registered or invalid pan) as per Sec 206AA D. Case Law The ACIT, Ahemdabad V/s Girish Haribhai Trivedi (AY 2008-09) The Revenue filed an appeal before Ahemdabad Tribunal The assessee had invested in ICICI ULIP policy on 31.7.2003 by paying Rs.18,00,000/- within 2 years from purchase of policy and received Rs. 32,74,493/- on 22.08.2007 as the surrender amount ,the assessee treated this amount as Long Term Capital Gain and the paid the tax thereon taking Rs.18,00,000/- as cost and maturity proceeds of Rs.32,74,493/- as sale proceeds while the differential of Rs. 14,72,493/- as Long Term Capital Gain ,the same was rejected by the Assessing Officer since the A.O was of the opinion that the fund is controlled by ICICI Pru Life Insurance Company, the amount received on that account would be treated as ‘surrender value’ of the policy and the entire amount of Rs.32,74,493/- will be taxable ,due to which the assessee filed an appeal ,the Tribunal looking at facts and circumstances of the case arrived at the conclusion that the assessee will be allowed to treat the proceeds as capital gain and the A.O is therefore directed to take the sale consideration of units as amount received on maturity of the policy and the cost of investment as amount invested by assessee during the span of 2-3 years i.e. Rs.18,00,000/- and accordingly work out the long term capital gain and tax payable thereon ,if any.

Author Email Id: [email protected]

TRANSITIONAL PROVISIONS UNDER MODEL GST LAW 2016 FOR KARNATAKA VAT DEALERS

- By CA SANJAY DHARIWAL AND CA ANNAPURNA KABRA

The Draft GST law which has come on public domain on 14th June 2014 discusses each component in detail. We have to understand why we need GST, why we all want to know about GST, how it is transforming the manufacturing, sale, provision of services to supply of goods and services. The introduction of GST will be one of the biggest reform in the country and will be one of the most significant tax reforms in the fiscal history of India to consolidate present multiple layers of Indirect taxation. The Model law also includes the draft of Integrated GST as well as Draft Valuation Rules. The GST law covers various aspects relating to supply of goods and services, time and place of such supply, Input tax credit, Valuation Rules, tax administration and the transition provisions. The GST model law is provided to understand the framework of GST and accordingly the transitional provisions are discussed in below Para as may be applicable to VAT dealers in Karnataka.

VAT Credit on Inputs: The registered taxable person will be entitled to take credit of the amount of VAT availed under the existing law subject to the following that amount is reflected as carry forward in the return and such credit is admissible under the earlier law and GST law. The VAT Credit can be availed as SGST Credit. Input tax credit as per the return furnished for the period ending will be carried forward as SGST under GST law

VAT Credit on Capital Goods : A registered taxable person shall be entitled to unavailed Input tax credit in respect of capital goods not carried forward in a return will be allowed in certain situations. Under the KVAT law the input tax credit can be availed on capital goods only after the commencement of commercial production. The GST law specifically allows unavailed Input Tax credit in respect of only capital goods and not inputs and input services. The VAT Credit should have been admissible under both the earlier law and GST.

VAT Credit on Exempted Goods: The Taxable person has not been registered under the earlier law. The person must be a registered taxable person under the GST laws. The goods must have been exempted under the State level VAT / CST laws but those goods must be liable to tax under GST law. The inputs should be intended for use in making taxable supplies under the GST law. Such inputs should be held in stock on the date of introduction of GST.

Credit of eligible taxes on inputs held in stock to be allowed to a taxable person switching over from composition scheme under the existing law to regular scheme in GST Scheme: The person must be a registered taxable person under the GST Laws. The taxable person must have also been registered under the earlier law and should have opted for payment of tax at a fixed rate or fixed amount under the composition scheme under the earlier law. Specified taxes / duties paid on ‘inputs’ would be allowed as transitional credit. The taxable person should opt for payment of tax under the regular scheme under the GST law (cannot be a composition taxpayer u/s 8 of GST Laws).

The relevant inputs should be held in stock on the date of introduction of GST. Inputs may take any of the following forms – (i) inputs as such (in the same form as it was procured / received –may be raw materials, consumables, packing materials, traded goods etc.), (ii) may be contained in WIP or semi- finished goods or (iii) may be contained in the finished goods. Such inputs must be used or intended to be used for making taxable supplies under the GST Laws. Such goods should qualify as eligible inputs under the GST law. The taxable person should be in possession of the invoice and such other documents (as may be prescribed). The invoice / other document should evidence the payment of duty / tax on such goods. The invoice should not be more than 12 months prior to the date of introduction of GST.

Amount payable in the event of a taxable person switching over to the composition scheme under GST regime:

The person working under the composition scheme under the GST law does not carry forward credit from the old regime. The taxable person should be registered under the regular scheme in the old law. The taxable person should have an unutilized portion of input credit under the old law. He must have opted for composition scheme under the GST law in terms of section 8. He should pay an amount by way of debit in the electronic credit ledger or electronic cash ledger equivalent to input tax credit in respect of stock held on the day immediately preceding the date of such switch over. The balance of Input tax credit lying in electronic credit ledger shall lapse

Exempted goods returned to the place of business on or after the appointed day:

It provides for non-payment of GST on return of exempted goods sold under the earlier law and the return of such goods is under the GST law. Exempted or duty paid goods returned within six months from appointed day to any place of business then no tax payable under GST law and If not returned within six months of appointed day to any place of business then tax payable by person returning the goods if such goods are liable to tax under GST.

Duty paid goods returned to the place of business on or after the appointed day:

In case the duty paid goods sold six months prior to the appointed date of GST should be returned to the place of business within six months of the appointed date. In case the duty paid goods returned to the place of business after six months of the appointed date then it shall become taxable. If the goods are returned by the buyer to the seller within 6 months from the date of GST coming into effect, the seller can take credit of tax paid under the earlier law.

Issue of supplementary invoices, debit or credit notes where price is revised in pursuance of a contract:

In case of upward price revision in contract a supplementary Invoice or debit note is required to be issued within thirty days of revision and tax is required to be paid to the extent revision under GST regime. And in case of downward revision a supplementary Invoice or Credit Note is required to be issued within thirty days of revision. The tax liability will be reduced to the extent of revision under GST regime.

Summer, Winter and Rainy In fact we have many. Do you know that the Indian season lasts throughout the year for a reason Binding people together inculcates feeling of longing for one another we put up with bright colors just like the varied Flowers We either chant mantras or pray but we also find soldiers walking in the 'Gateway' music and beats of drums Which is the ceremonial welcome Not just Diwali or Dhashera We have Republic and Independence day as our parampara However Friday turned out to be Good Friday Whereas Roza done for a month and not a day We end up eating chocolates and cakes praying to forgive our mistakes immediately succeeds the New year and this is the Indian atmosphere.

POEM: THE FESTIVE SEASON

By: MOUNIKA R T ([email protected])

FROM OUR INBOX

Claim of credit to be disposed of under the earlier law: Where any matter in respect of input credit is pending in an appeal or revision or review or reference under any of the earlier laws and if the input credits are finally allowed then in such instance refund would accrue in cash. And if the input credit is disallowed then it would become recoverable as an arrear of tax under the GST law. The amount so recovered would not be allowed as input tax credit under the GST laws. The recovery of taxes will be conducted under the GST law

Finalization of proceedings relating to output duty Liability: The Section applies where any matter in respect of output tax / duty liabilities are pending in appeal, review, revision or reference proceedings under any of the earlier law. If the output liability is finally payable then it should be recovered as an arrear of tax under relevant GST Act. The amount so recovered would not be allowed as input tax credit under the GST laws.

The GST law will change the tax incidence, tax computation, tax structure, credit utilization, Input tax credit mechanism etc. which will completely transform the current indirect taxation system and accordingly the dealers should gear up from the current indirect taxation to the impending Goods and Service Tax law.

Author Email Id: [email protected]

DNS NEWS BIRTHDAYS FOR THE MONTH OF SEPTEMBER-2016

DNS FAMILY WISHES YOU A VERY “HAPPY BIRTHDAY”

DATE FESTIVAL 05th September 2016 Ganesh Chaturthi, Teacher’s Day 13th September 2016 Onam, Bakrid

FESTIVALS FOR THE MONTH OF

SEPTEMBER 2016

PARTICULARS DATE EMAIL ID Siva Teja 01st September 2016 [email protected] Subramanyam 06th September 2016 [email protected] Praveen 06th September 2016 [email protected] Ranjita (Gala) 08th September 2016 [email protected] Mohammed Jameel 10th September 2016 [email protected] Arun (Gala) 11th September 2016 [email protected] Chirag 11th September 2016 [email protected] Pratik Jain 14th September 2016 [email protected] Kamala 23rd September 2016 [email protected] Anjan 23rd September 2016 [email protected] Ashwini 25th September 2016 [email protected] Lokesh 28th September 2016 [email protected] Smruti 29th September 2016 [email protected]

DNS NEWS

Man of the Match Paresh S Shah on Sunday 21st August 2016 at St Joseph College of Commerce between Old Students Ranging from 1973 batch to 2016 batch

CA Annapurna Kabra gave a presentation on GST at the 30th

Annual Conference “YUNAKTI-Navigating the Change” of ICAI Hubbali on 4th August 2016.

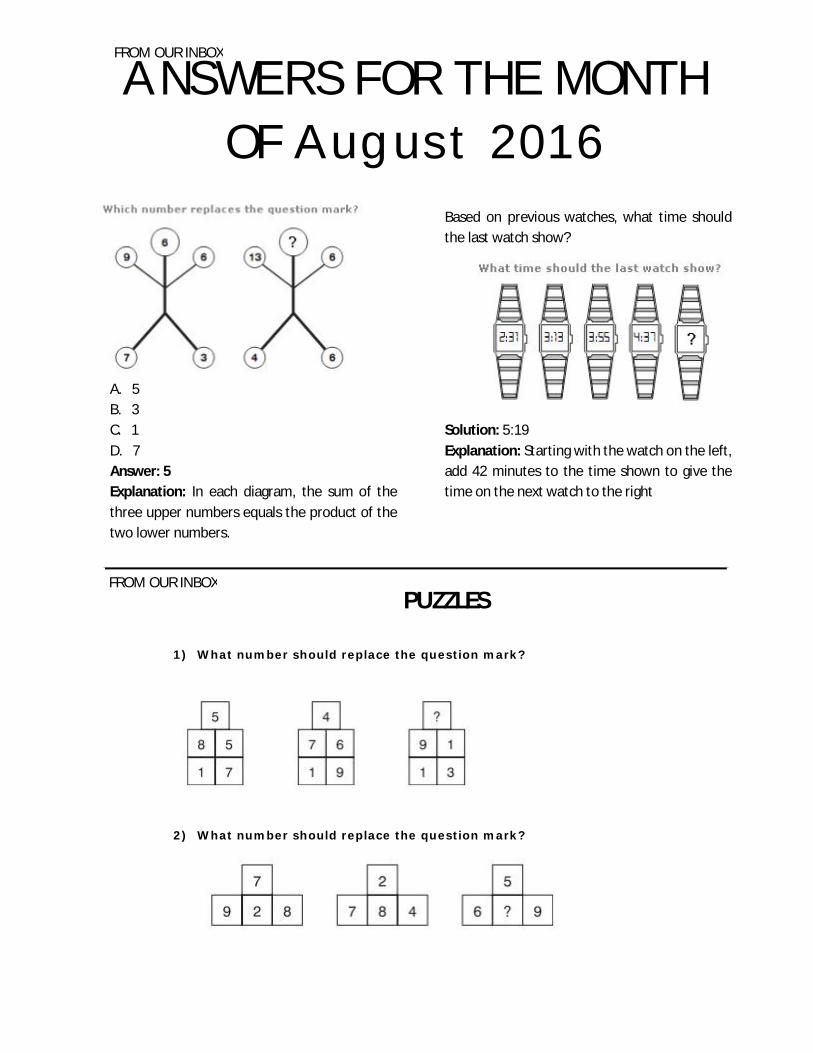

ANSWERS FOR THE MONTH OF August 2016

A. 5 B. 3 C. 1 D. 7 Answer: 5 Explanation: In each diagram, the sum of the three upper numbers equals the product of the two lower numbers.

Based on previous watches, what time should the last watch show?

Solution: 5:19 Explanation: Starting with the watch on the left, add 42 minutes to the time shown to give the time on the next watch to the right

PUZZLES

1) What number should replace the question mark?

2) What number should replace the question mark?

FROM OUR INBOX

FROM OUR INBOX

“DNS Consulting Pvt Ltd” Head Office: No 10, South Park Road, Nehru Nagar, Bangalore - 20 Tel/Fax: 42479333 / 42479301 Branch Office: #36, Ground Floor and Third Floor, 2nd Cross, Kumara Park West, Bangalore – 560020

Disclaimer: The information contained herein is subject to change without prior notice. Whileevery effort has been made to ensure the accuracy and Completeness ofinformation contained in this newsletter, the Editorial makes no guarantee &assumes no responsibility for any errors or omissions of information.