Embed Size (px)

Citation preview

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

Recent Developments in Transfer Pricing

Wednesday, 30th April, 2014 CA. (Prof.) Tarun Chaturvedi

6.00 pm to 8.00 pm h#p://icaitv.com/live/icaicitax300414/

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

Rulings Discussed in this webcast

• The following recent Judicial rulings on TP are discussed in this webcast: – Transfer Pricing & 10A benefits – Mo7f India – Corporate Guarantee & Imputed interest on Share ApplicaEon money – Bhara7 Cellular

– Special Bench on ITES Comparables – Maersk Global

– Internal CUP vs TNMM – J.P. Morgan

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

No TP adjustment if profit less than arm’s length profit

resulEng in a lower tax holiday claim

M/S MoEf India Infotech Pvt. Ltd. v. ACIT for AY 2006-‐07, ITA No.3043-‐Ahd-‐2010 dated 25 March 2014

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

ExecuEve Summary • The Tribunal held that where internaEonal transacEons give rise to

exempt income under secEon 10A of the Income tax Act, 1961 (Act), the Transfer Pricing (TP) analysis of such internaEonal transacEons needs to be carried out only to ensure that the taxpayer does not claim excessive tax exempEons.

• Such exempEons will only be allowed on the profits determined based on

Transfer pricing provisions and any excess profit would not be eligible for a tax holiday.

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

Facts • The taxpayer, renders data support services to its Associated Enterprises

(AEs). The Company’s enEre income was eligible for tax holiday u/s 10A of the Act.

• The taxpayer contended that TP provisions were not applicable to it since it was covered by s10A and there was no incenEve / intenEon to shi` profits.

• The TPO did not accept the submissions of the taxpayer.

• The TPO carried out a fresh search for comparables and determined an arm’s length margin of 34.26% against the margin of 17.89 % earned by the taxpayer and made a TP adjustment for the difference.

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

Main issue before the Tribunal

• Whether transfer pricing provisions are applicable in cases where the enEre income of the taxpayer from the internaEonal transacEon is eligible for a tax holiday benefit u/s 10A of the Act?

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

ObservaEons & Ruling of the Tribunal

• The Tribunal, relying on CBDT Circular No.14 of 2001 and the ruling in case of Philips So`ware held that the intenEon of introducing TP provisions in the Act was to ensure that the taxable income in India is not reduced due to any arrangement between a taxpayer and its overseas AEs.

• However, at the same Eme, there is no provision in the Act that excludes applicaEon of TP provisions to internaEonal transacEons where a taxpayer’s enEre income is exempt under secEon 10A of the Act.

• Based on a harmonious reading of the provisions of SecEon 92C(4) of the Act and the object and purpose of inserEon of Transfer Pricing provisions as explained by the CBDT Circular, the Tribunal held that when internaEonal transacEons give rise to exempt income, TP provisions apply to such internaEonal transacEons only to ensure that no excess exempEon is claimed by the taxpayer.

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

ObservaEons & Ruling of the Tribunal

• The exempEon will be available only to the income determined under TP provisions and excess profits (if any) would not be eligible for exempEon.

• The Tribunal made a specific observaEon that the ruling in case of Gharda Chemicals would not be applicable in the present case since the quesEon regarding the applicability of TP provisions to a tax holiday unit was neither raised nor analysed by the Tribunal.

• In view of the above, the Tribunal held that no adjustment was required to be made to the exempt income earned by the taxpayer and therefore deleted the enEre TP adjustment.

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

Conclusion • The ruling aims to provide a harmonious interpretaEon between

the intent of TP provisions and the statutory provision under the Act on applicability of TP provisions to tax holiday units.

• However, it is interesEng to note that the relevant TP provision dealing with tax holiday units states that no exempEon/deducEon would be allowed in respect of the shoriall between the income determined based on arm’s length price versus the taxpayer’s actual/ reported income.

• However, the Tribunal has interpreted the secEon to mean no exempEon would be allowed in respect of the taxpayer’s reported income over and above the arm’s length income. The judgment could further impact exempEon claims of taxpayers earning excess profits over and above arm’s length profit.

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

Corporate Guarantees and

Share ApplicaEon Money TP ImplicaEons

BharE Airtel Limited. Vs. ACIT, I.T.A. No.: 5816/Del/2012, dated 11 March, 2014

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

ExecuEve Summary

• Corporate Guarantees with no cost implicaEons to the taxpayer and which have no impact on the profits, income, losses or assets of the taxpayer are not considered internaEonal transacEons and hence do not fall within the ambit of Indian Transfer Pricing (TP) Regulatons.

• The Tribunal also provided guidance on the determinaEon of arm’s length interest rates on outbound foreign currency loans to Associated Enterpeises (AEs) and ruled against the recharacterisaEon of any taxpayer transacEon unless proven to be a sham.

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

Facts • The taxpayer entered into certain financial transacEons with its AEs viz.

– Issuance of corporate guarantee to a third party bank on behalf of its AE

– loans extended to its AEs and – Payment of share applica7on money.

• Guarantee given on behalf of AE: The taxpayer did not charge any guarantee fee However, considering market quotaEons, the taxpayer determined a guarantee fee of 0.65% per annum (p.a.) and made a voluntary adjustment in its tax return.

• Loans extended to AEs: The taxpayer applied LIBOR on such loans • Payment of share applica@on money to AEs: the taxpayer did not carry

out any TP analysis for such a transacEon, as it was a transacEon on capital account.

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

Facts • With respect to Guarantee commission, the Transfer Pricing Officer

(TPO), based on informaEon obtained from various Indian banks under SecEon 133(6) of the Income Tax Act, 1961 (the Act), computed an arm’s length guarantee fee of 4.68% p.a. and made a TP adjustment for the shoriall in the guarantee fee offered to tax by the taxpayer.

• With respect to the loans, the TPO relied on the informaEon obtained under secEon 133(6) of the Act on Indian corporate bond rates to compute an arm’s length interest rate at 17.26% p.a.

• With respect to the share applicaEon money, the TPO held the share applicaEon transacEon to be an interest free loan given to the AEs and imputed noEonal interest on such amount.

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

QuesEons for consideraEon before the Tribunal

• Whether the issuance of corporate guarantees on behalf of AE which does not involve any cost to the taxpayer falls within the ambit of the definiEon of ‘InternaEonal TransacEon’ under the Act ?

• Whether interest rates charged on foreign currency loans should be compared with interest rates charged on Indian borrowings for the purpose of determining the arm’s length interest rate?

• Whether payments of share appplicaEon money can be recharacterised as interest free loans?

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

ObservaEons and Ruling of the Tribunal

Issuance of guarantee • The Tribunal analysed secEon 92B of the Act alongwith the ExplanaEon to the

definiEon of ‘InternaEonal TransacEon” as amended by Finance Act, 2012.

• The Tribunal observed that since the ExplanaEon is clarificatory in nature, the retrospecEve amendment does not alter the basic character of the definiEon of internaEonal transacEon.

• The Tribunal observed that under the scheme of the Act, any transacEon including capital financing, guarantees, business restructuring/ reorganisaEon can be regarded as an ‘internaEonal transacEon’ only if such a transacEon has a bearing on the profits, income, losses or assets of an enterprise (either immediately or in future).

• Tribunal further noted that such an impact in the future has to be certain (and not conEngent) for covering a transacEon in the definiEon of internaEonal transacEon.

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

ObservaEons and Ruling of the Tribunal

• The corporate guarantees issued by the taxpayer to the bank on behalf of its AE did not have any implicaEon on the profits, income, losses or assets of the taxpayer. It also observed that the AE had not taken any borrowing from the bank based on the taxpayer’s guarantee.

• Since TP provisions are anE-‐avoidance measures, enhancement in their scope can generally not be done with retrospecEve effect .

• When a taxpayer extends any assistance to its AE without incurring any expenditure and for which the taxpayer otherwise also could have not realized any income by giving it to any third party, such assistance has no bearing on profits, income, losses or assets of the taxpayer. Hence, it cannot be regarded as an internaEonal transacEon.

• The Tribunal also disEnguished the current case from the preceding Tribunal cases (on quanEficaEon of arm’s length guarantee fee) by holding that none of the earlier cases dealt with the issue of coverage of the guarantee transacEon in the scope of internaEonal transacEon as defined in the Act. The Tribunal did not consider the Canadian ruling in the case of GE Capital on the basis that Indian TP regulaEons differ from Canadian TP provisions.

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

Receipt of interest on loans • Interest is Eme value of money, it depends on the strength of the currency in which the loan

is extended. If a loan is given in a FC, the interest rate on rupee bonds is irrelevant. • TPO had adopted a mark up on LIBOR based on informaEon gathered from some websites

and also determined the credit raEng of AEs based on various arbitrary presumpEons. On the other hand, the taxpayer had determined the arm’s length interest rate based on specific comparable agreements of foreign currency loans.

• The Tribunal also observed that the adjustment in interest rate by the TPO to factor in the hedging cost is applicable to a domesEc borrower obtaining a loan from overseas. Such a borrower’s transacEon cost is not relevant while analysing the lender’s perspecEve in a foreign currency loan extended to an overseas enEty.

• With respect to the increase in the interest rate for factoring in the addiEonal risks inter-‐alia on account of lack of security provided by the AE, the Tribunal held that the taxpayer had advanced loans to its subsidiaries that are under its management and control which reduces the risk rather than increasing it. Hence, no such adjustment in the interest rate is warranted.

• The Tribunal also noted that the taxpayer had obtained foreign currency loans from third parEes at much lower rates.

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

Recharaterisa@on of the share applica@on transac@on • The TPO did not challenge the fundamental character of the capital

subscripEon transacEon and that there is no provision in the Act that enables deeming of a capital transacEon as a loan.

• The TPO had imputed interest on the grounds that there was an inordinate delay in the issue of equity shares but did not provide any basis for determining the reasonable period for issue of shares.

• Moreover, in case interest was to be imputed, it should have been determined only for the period of inordinate delay and a`er considering whether interest would have been payable to an unrelated share applicant in a similar situaEon.

• In view of the above, the Tribunal held that the TPO cannot recharacterise a transacEon unless it is a sham or the transacEon is substanEally at variance from the stated form.

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

Conclusion • The observaEons of the Tribunal regarding the coverage of guarantee transacEon

in the definiEon of internaEonal transacEon depends on the facts and circumstances of the case and cannot be applied generally. A noteworthy fact in the present case was that the AE had not taken any loans from the third party bank based on the taxpayer’s guarantee. The Transfer pricing analysis of guarantees given by a taxpayer to its AEs depends on a number of factors including the purpose of borrowing, the cost incurred by the taxpayer, the underlying risk of the taxpayer etc.

• This ruling sets an important precedent in case of taxpayers lending funds to overseas AEs in a foreign currency. The ruling upholds the applicaEon of the CUP method and the use of foreign currency comparable agreements as external comparables for benchmarking such loans.

• In the wake of numerous ongoing transfer pricing disputes on share valuaEon and deeming of the shoriall in funds received for such share issuances as interest free loans for impuEng noEonal interest, this ruling gives guidance from the judiciary that the revenue authoriEes cannot recharacterise a transacEon and deem a capital transacEon as loan.

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

Special Bench strikes down sub-‐classificaEon

of ITES into BPO and KPO, upholds strict funcEonal comparability; negates outright

rejecEon of high margin companies

Maersk Global Centres (I) Private Ltd . vs ACIT, ITA Nos. 7466 /Mum/2012, dated 7thMarch, 2014

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

ExecuEve Summary

• In its ruling pronounced recently, the SB has – denied strict sub-‐classificaEon of InformaEon Technology Enabled Service (ITeS) companies into BPO and KPO but

– has held that the arm’s length margin under TransacEonal Net Margin Method (TNMM) needs to be determined through a two-‐step close funcEonal comparability process.

– Further, the SB also ruled against the outright rejecEon of comparable companies solely on the ground of their abnormally high margins.

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

Facts • The taxpayer was engaged in the provision of IT enabled services like

transacEon processing, data entry, accounEng and other support services as well as certain InformaEon Technology (IT) services like process support, process opEmizaEon and technical support services to its Associated Enterprises (AEs).

• The Transfer Pricing Officer (TPO) rejected the benchmarking analysis of the taxpayer and accepted only one out of the 13 ITeS comparable companies selected in the Transfer pricing (TP) documentaEon. The TPO determined the arm’s length margin for both IT and ITeS segments of the taxpayer by undertaking a fresh search of comparables

• Aggrieved by the addiEons proposed by the TPO, the taxpayer filed

objecEons before the Dispute ResoluEon Panel (DRP).

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

Facts • The DRP partly accepted the taxpayer’s contenEons and upheld re-‐

instatement of some of the taxpayer’s comparables and ruled against inclusion of some of the comparables sought to be introduced by the TPO. However, the DRP did not accept the rejecEon of certain comparables (introduced by the TPO) on the ground that such companies were engaged in high-‐end KPO services and/or earned abnormally high margins.

• Aggrieved by the DRP’s order, the taxpayer preferred an appeal before the

Tribunal. The taxpayer, inter-‐alia, appealed against the inclusion of two abnormally high profit earning comparables that were engaged in KPO services, viz. Mold-‐Tek and eClerx Services Ltd (eClerx).

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

QuesEons for consideraEon before the Special Bench

• Whether for the purpose of determining arm’s length price of internaEonal transacEons of the taxpayer providing back office support services to its overseas AEs, companies performing KPO acEviEes should be considered as comparables?

• Whether, in the facts and circumstances of the taxpayer’s case, companies earning abnormally high profit margin should be included as comparables for the purpose of determining the arm’s length price of internaEonal transacEons?

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

Arguments before the Special Bench Whether BPO companies can be compared with KPO en@@es • The taxpayer submised that there is a basic disEncEon between BPO and KPO acEviEes in

terms of the differences in the skill set/ experience of employees and the level of domain experEse required to render the services. The company inter-‐alia relied on the report of NaEonal Skill development CorporaEon (NSDC) which pointed out that BPO is a low end provision of service that primarily involves informaEon collaEon and populaEng the same into various systems and processes. On the other hand, KPO services are significantly high on the value chain and involve processes that require advanced informaEon analysis, research, experience as well as decision making judgment.

• The taxpayer argued that a similar disEncEon (between BPO and KPO) has been recognized in the recently introduced Safe Harbour Rules by the Indian Government, as well as various Tribunal Judgments.

• The taxpayer also relied on the (OECD) Guidelines on comparability and submised that determinaEon of arm’s length outcomes requires flexibility and good judgment. In case some uncontrolled transacEons have a lesser degree of comparability, such uncontrolled transacEons should be eliminated to achieve a reasonable outcome under TNMM.

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

Arguments before the Special Bench

• The Company also submised detailed funcEonal profiles of Mold-‐Tek and eClerx from their annual reports and websites and contended that both the enEEes are engaged in KPO acEviEes and hence should be excluded from the comparables set.

• The Departmental RepresentaEve (DR) inter-‐alia argued that based on perusal of various services rendered by the taxpayer, it is neither a pure BPO nor KPO, but lies somewhere in between. The taxpayer itself had considered some comparables engaged in providing KPO services in its TP documentaEon and the Safe Harbour Rules had no applicability whatsoever in the present case.

• Relying on the OECD Guidelines, the DR submised that only a broad level of funcEonal comparability and not strict product/ service characterisEcs comparability is required for applicaEon of TNMM and hence companies engaged in ITES should be broadly considered as comparable without dissecEon into BPO and KPO.

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

Arguments before the Special Bench

Companies earning abnormally high profit margins • The taxpayer inter-‐alia placed reliance on earlier judicial precedents on

the issue and pleaded for rejecEon of comparable companies having abnormally high profit margins.

• The DR brought out the difference in OECD guidelines and the Indian TP regulaEons and emphaEcally put forward that if outliers were to be removed, the interquarEle range (as specified in the OECD guidelines) would have been considered under the Indian TP regulaEons, instead of adopEng the arithmeEc mean. Further, the arithmeEc mean being a measure of central tendency is adopted to ease out distorEons due to both high and low margins and thus outright rejecEon of high margin companies is not permissible.

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

ObservaEons and Ruling of the Tribunal

Whether BPO companies can be compared with KPO en@@es • The Tribunal held that IT enabled services cannot be further dissected into BPO

and KPO services for the purposes of comparability analysis inter-‐alia in view of the following: – Due to a broad range of acEviEes in the ITeS sector and significant overlap between

such services, no strict line of disEncEon can be drawn between low end BPO or high end KPO acEviEes;

– The upward shi` of BPO industry in the value chain has resulted in emergence of KPOs and due to the mixed nature of both services, the arEficial segregaEon or creaEon of a third ‘in-‐between’ category is not possible.

• However, the Tribunal menEoned that its intenEon is not to dilute the standards of comparability just because the TNMM was being used.

• The Tribunal suggested a ‘two-‐step’ approach for benchmarking of ITeS acEviEes. – The first step involves selecEon of all potenEal comparables engaged in the broad realm

of ITeS, thus applying a broad-‐based funcEonality test. – Step two entails dissecEng the broad ITeS set and selecEng comparables from such set

which undertake the same ‘principal funcEons’ as carried out by the tested party, for ensuring close comparability.

•

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

ObservaEons and Ruling of the Tribunal

Whether BPO companies can be compared with KPO en@@es • The Tribunal noted that the principal funcEon of the taxpayer was provision of low

end data collaEon and processing services. It also provided some technical IT services but such services were about 10% of the taxpayer’s total revenue. Further, although the taxpayer rendered certain other IT enabled services which required some degree of specialized knowledge and experEse, the Tribunal pragmaEcally categorized such services as incidental to the main low end services. Accordingly, the taxpayer was categorized as a capEve contract service provider mainly engaged in the provision of back office support services to its AEs.

• The Tribunal then evaluated in detail the funcEonal profile of Mold-‐Tek (mainly engaged in structural engineering design services) and eClerx (mainly engaged in data analysis and data process soluEons) and concluded that both these companies were providing high-‐end services involving higher specialised knowledge and domain experEse. Therefore, the Tribunal concluded that both Mold-‐Tek and eClerx could not be considered as appropriate comparables of the taxpayer.

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

ObservaEons and Ruling of the Tribunal

Companies earning abnormally high profit margins as comparable companies • The Tribunal noted that in view of the exclusion of Mold-‐Tek

and eClerx from the comparables set on account of funcEonal dissimilarity, in the present case, this issue had become infructuous and did not require consideraEon. In general, the Tribunal held that: – Indian TP regulaEons deviate from the OECD guidelines by adopEng the

arithmeEc mean instead of quarEle range suggested by the OECD, which excludes outliers.

– PotenEal comparables cannot be excluded merely on the ground of abnormally high profits.

– Such abnormal margins should trigger further invesEgaEon and analysis to inter-‐alia ascertain whether such high profits reflect a normal business condiEon or arise from some abnormal condiEons during the year; are there any differences in funcEons and if all comparability condiEons are met by such potenEal comparables.

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

Conclusion • The ruling seeks to sesle the long drawn contenEous issue between

taxpayers and revenue authoriEes on selecEon of comparables for the ITES sector. Based on the suggested two steps approach for selecEon of comparables, the Tribunal has placed significant emphasis on the need for detailed analysis and close comparability of the funcEons of the taxpayer and comparables for determining the arm’s length margin.

• The Tribunal has also provided guidance on the selecEon of comparables having abnormally high margins. The ruling emphasizes that there is no straight jacket formula and selecEon (or otherwise) of such companies as comparables requires detailed invesEgaEon. The ruling makes it criEcal for taxpayers to undertake much more in-‐depth and detailed funcEonal analysis of potenEal comparables, since outright rejecEon of comparables based on the BPO vs KPO argument or abnormal margins would now not be an opEon.

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

Internal CUP with adjustments

preferred over TNMM J.P.Morgan India Private Limited Vs. ACIT, Mumbai for AY 2002-‐03, ITA No. 670/MUM/2006 and ACIT Vs. J.P.Morgan India Private

Limited, Mumbai for AY 2002-‐03, ITA No. 618/MUM/2006, dated 12 February 2014

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

ExecuEve Summary

• The Mumbai bench of the Income Tax Appellate Tribunal (the Tribunal) recently pronounced its ruling in the case of JP Morgan India Private Limited (the taxpayer/ the company). The Tribunal held that if comparable price data is available and differences in funcEons, assets and risks (FAR) profile of taxpayer’s transacEons with Associated Enterprises (AEs) versus its transacEons with third parEes can be quanEfied, the Comparable Uncontrolled Price (CUP) method should be preferred over the TransacEonal Net Margin Method (TNMM).

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

Facts

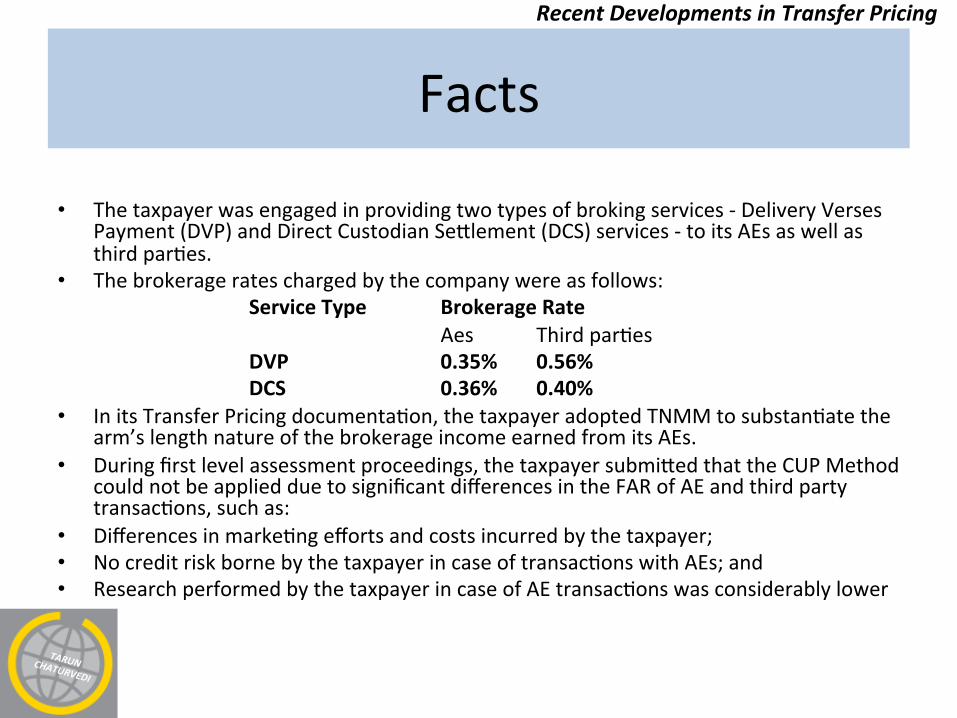

• The taxpayer was engaged in providing two types of broking services -‐ Delivery Verses Payment (DVP) and Direct Custodian Seslement (DCS) services -‐ to its AEs as well as third parEes.

• The brokerage rates charged by the company were as follows: Service Type Brokerage Rate Aes Third parEes DVP 0.35% 0.56% DCS 0.36% 0.40%

• In its Transfer Pricing documentaEon, the taxpayer adopted TNMM to substanEate the arm’s length nature of the brokerage income earned from its AEs.

• During first level assessment proceedings, the taxpayer submised that the CUP Method could not be applied due to significant differences in the FAR of AE and third party transacEons, such as:

• Differences in markeEng efforts and costs incurred by the taxpayer; • No credit risk borne by the taxpayer in case of transacEons with AEs; and • Research performed by the taxpayer in case of AE transacEons was considerably lower

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

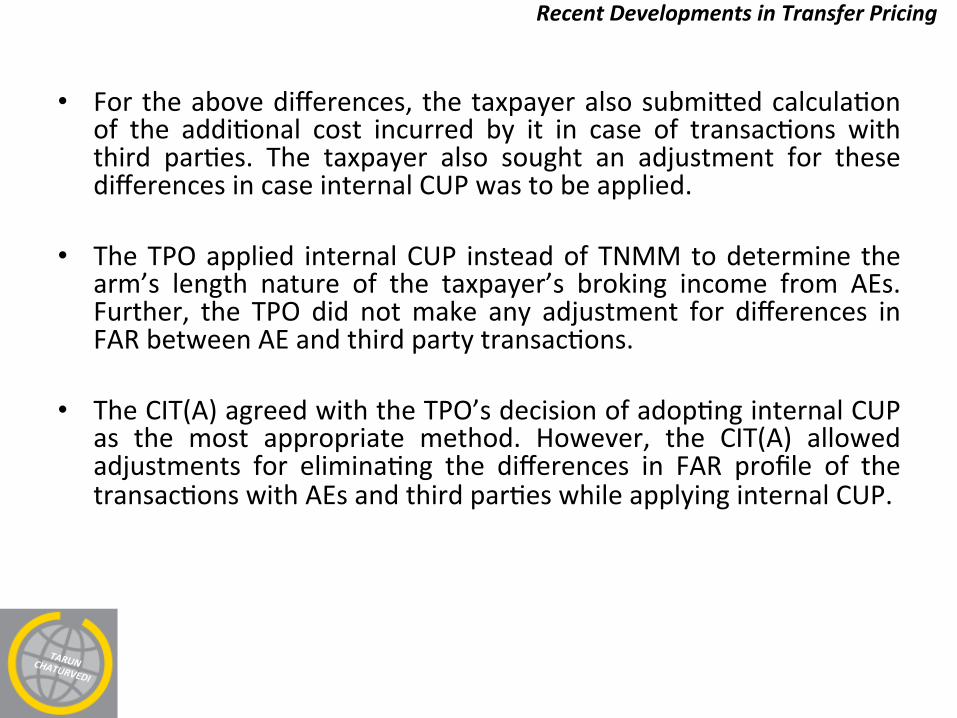

• For the above differences, the taxpayer also submised calculaEon of the addiEonal cost incurred by it in case of transacEons with third parEes. The taxpayer also sought an adjustment for these differences in case internal CUP was to be applied.

• The TPO applied internal CUP instead of TNMM to determine the

arm’s length nature of the taxpayer’s broking income from AEs. Further, the TPO did not make any adjustment for differences in FAR between AE and third party transacEons.

• The CIT(A) agreed with the TPO’s decision of adopEng internal CUP

as the most appropriate method. However, the CIT(A) allowed adjustments for eliminaEng the differences in FAR profile of the transacEons with AEs and third parEes while applying internal CUP.

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

Issues raised before the Tribunal

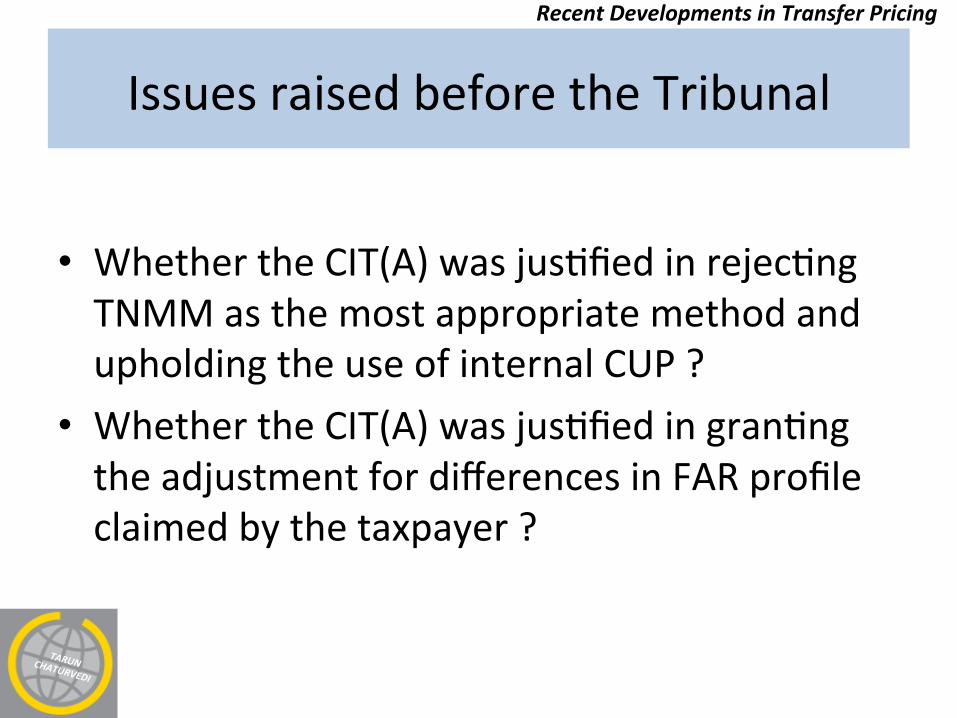

• Whether the CIT(A) was jusEfied in rejecEng TNMM as the most appropriate method and upholding the use of internal CUP ?

• Whether the CIT(A) was jusEfied in granEng the adjustment for differences in FAR profile claimed by the taxpayer ?

TARUN CHATURVEDI

Recent Developments in Transfer Pricing ObservaEons and Ruling of the

Tribunal

• The Tribunal upheld the decision of the lower authoriEes that TNMM is not the most appropriate method in cases where appropriate internal CUP data is available.

• The Tribunal also observed that the TPO had not pointed out any flaws in the computaEon of adjustment sought by the taxpayer for differences in FAR profile of its transacEons with AEs and third parEes.

• In view of the above, the Tribunal upheld the decision of the CIT(A) allowing appropriate adjustments between the transacEon prices of AEs and third parEes for applying the internal CUP method in order to determine the arm’s length nature of internaEonal transacEons of the taxpayer.

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

Conclusion • Although, the Indian Transfer Pricing RegulaEons do not

provide for any preference/hierarchy of methods, the applicaEon of direct methods to determine prices is generally preferred over indirect (profit based) methods. The OrganizaEon for Economic CooperaEon and Development (OECD) guidelines also lay down that the CUP method should be preferred over TNMM, in case, reliable and appropriate data is available and differences (if any) can be appropriately quanEfied and adjusted. Taxpayers therefore, need to closely analyze and evaluate their potenEal internal CUPs before resorEng to other/profit based methods for substanEaEng the arm’s length nature of their internaEonal transacEons.

TARUN CHATURVEDI

Recent Developments in Transfer Pricing

Recent Developments in Transfer Pricing

Wednesday, 30th April, 2014 CA. (Prof.) Tarun Chaturvedi

6.00 pm to 8.00 pm h#p://icaitv.com/live/icaicitax300414/