Embed Size (px)

Citation preview

Treaty Series

Treaties and international agreements

registeredor filed and recorded

with the Secretariat of the United Nations

Recueil des Traitis

Traitds et accords internationaux

enregistrsou classes et inscrits au ripertoire

au Secritariat de l'Organisation des Nations Unies

Copyright © United Nations 2001All rights reserved

Manufactured in the United States of America

Copyright © Nations Unies 2001Tous droits r6serv6s

Imprim6 aux Etats-Unis d'Am6rique

Treaty Series

Treaties and international agreements

registeredor filed and recorded

with the Secretariat of the United Nations

VOLUME 1908

Recueil des Traitis

Traitis et accords internationaux

enregistrisou classis et inscrits au repertoire

au Secritariat de l'Organisation des Nations Unies

United Nations * Nations UniesNew York, 2001

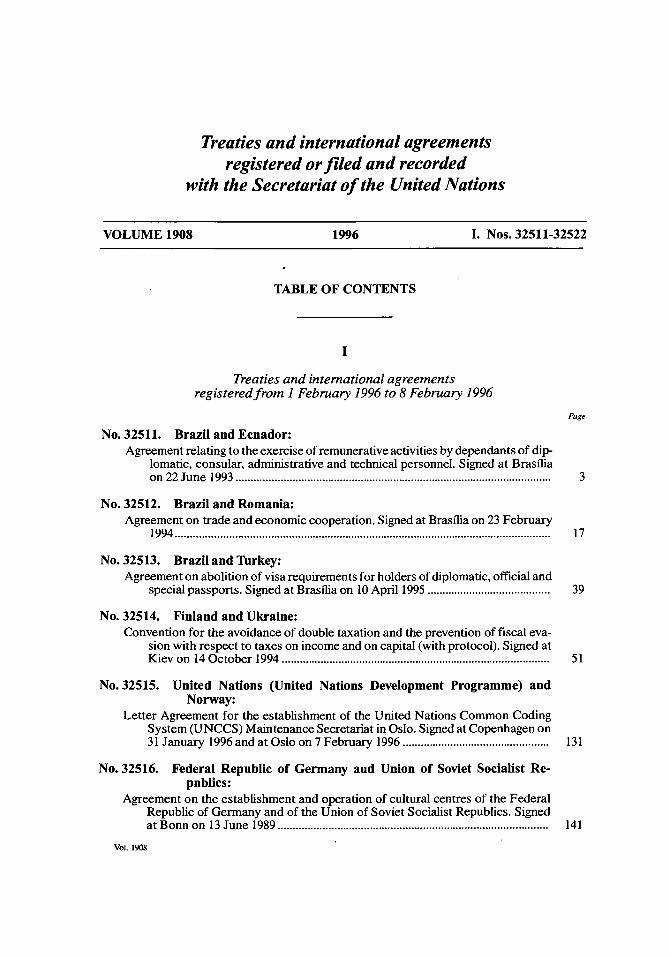

Treaties and international agreementsregistered or filed and recorded

with the Secretariat of the United Nations

VOLUME 1908 1996 I. Nos. 32511-32522

TABLE OF CONTENTS

I

Treaties and international agreements

registered from 1 February 1996 to 8 February 1996

Page

No. 32511. Brazil and Ecuador:Agreement relating to the exercise of remunerative activities by dependants of dip-

lomatic, consular, administrative and technical personnel. Signed at Brasiliaon 22 June 1993 ..................................................................................................... ..... 3

No. 32512. Brazil and Romania:Agreement on trade and economic cooperation. Signed at Brasilia on 23 February

1994 .............................................................................................................................. 17

No. 32513. Brazil and Turkey:Agreement on abolition of visa requirements for holders of diplomatic, official and

special passports. Signed at Brasilia on 10 April 1995 .................... 39

No. 32514. Finland and Ukraine:Convention for the avoidance of double taxation and the prevention of fiscal eva-

sion with respect to taxes on income and on capital (with protocol). Signed atK iev on 14 O ctober 1994 ......................................................................................... 51

No. 32515. United Nations (United Nations Development Programme) andNorway:

Letter Agreement for the establishment of the United Nations Common CodingSystem (UNCCS) Maintenance Secretariat in Oslo. Signed at Copenhagen on31 January 1996 and at Oslo on 7 February 1996 ................................................. 131

No. 32516. Federal Republic of Germany and Union of Soviet Socialist Re-publics:

Agreement on the establishment and operation of cultural centres of the FederalRepublic of Germany and of the Union of Soviet Socialist Republics. Signedat B onn on 13 June 1989 ........................................................................................... 141

Vol. 1908

Traitis et accords internationauxenregistris ou classes et inscrits au re'pertoire

au Secrjtariat de l'Organisation des Nations Unies

VOLUME 1908 1996 I. NOS 32511-32522

TABLE DES MATIERES

I

Trait&s et accords internationaux

enregistrds du lerfivrier 1996 au 8fivrier 1996

Pages

N0 32511. Br~sil et ltquateur:Accord relatif A l'exercice d'activit6s r6mun6r6es par des personnes A charge du

personnel diplomatique, consulaire, administratif et technique. Signd A Bra-sflia le 22 juin 1993 ..................................................................................................... 3

NO 32512. Brisil et Roumanie :Accord de commerce et de coop6ration 6conomique. Sign6 A Brasilia le 23 f6vrier

1994 .............................................................................................................................. 17

NO 32513. Brksil et Turquie :Accord relatif A la suppression des formalit6s de visa pour les titulaires de passe-

ports diplomatiques, officiels et de service. Sign6 ? Brasilia le 10 avril 1995 ... 39

N0 32514. Finlande et Ukraine:Convention tendant A 6viter la double imposition et A pr6venir l'6vasion fiscale en

mati~re d'imp6ts sur le revenu et sur la fortune (avec protocole). Sign6e AK iev le 14 octobre 1994 ............................................................................................. 51

NO 32515. Organisation des Nations Unies (Programme des Nations Unies pourle d6veloppement) et Norvge :

Lettre d'accord relative A la cr6ation du Secr6tariat de gestion du syst~me com-mun de codification de l'Organisation des Nations Unies (SCCONU) A Oslo.Sign6e A Copenhague le 31 janvier 1996 et i Oslo le 7 fWvrier 1996 .................... 131

NO 32516. Ripublique fidirale d'Allemagne et Union des Ripubliques socia-listes sovi6tiques :

Accord concernant I'6tablissement et les activit6s de centres culturels de la R6pu-blique f6d6rale d'Allemagne et de l'Union des R6publiques socialistes sovi6-tiques. Sign6 A Bonn le 13 juin 1989 ........................................................................ 141

Vol. 1908

VI United Nations - Treaty Series * Nations Unies - Recueil des Traitis 1996

Page

No. 32517. Germany and Union of Soviet Socialist Republics:

Agreement on maritime shipping (with exchange of notes). Signed at Bonn on7 Jan uary 1991 ............................................................................................................ 173

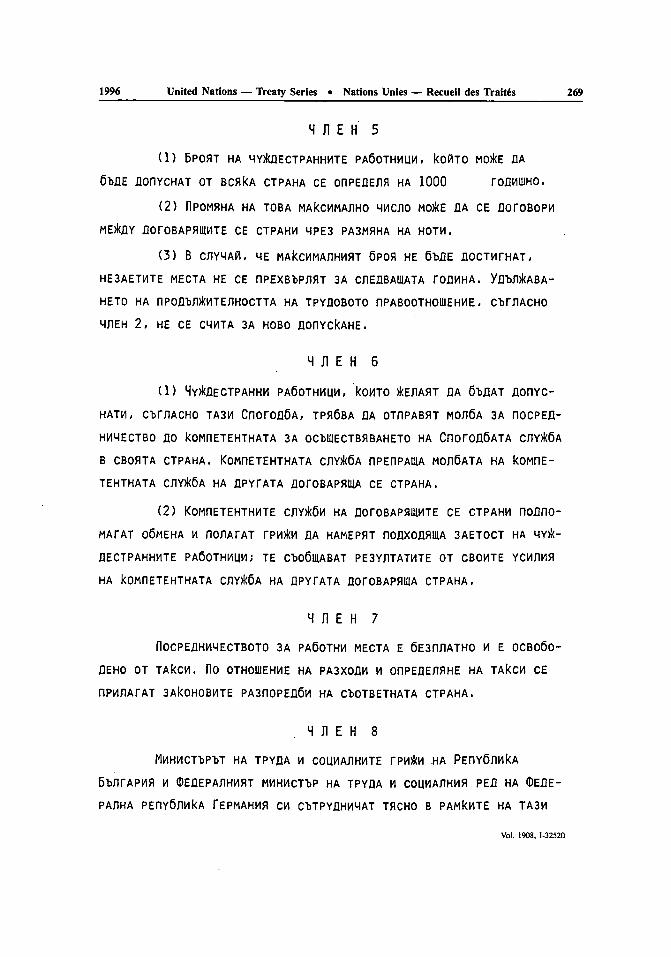

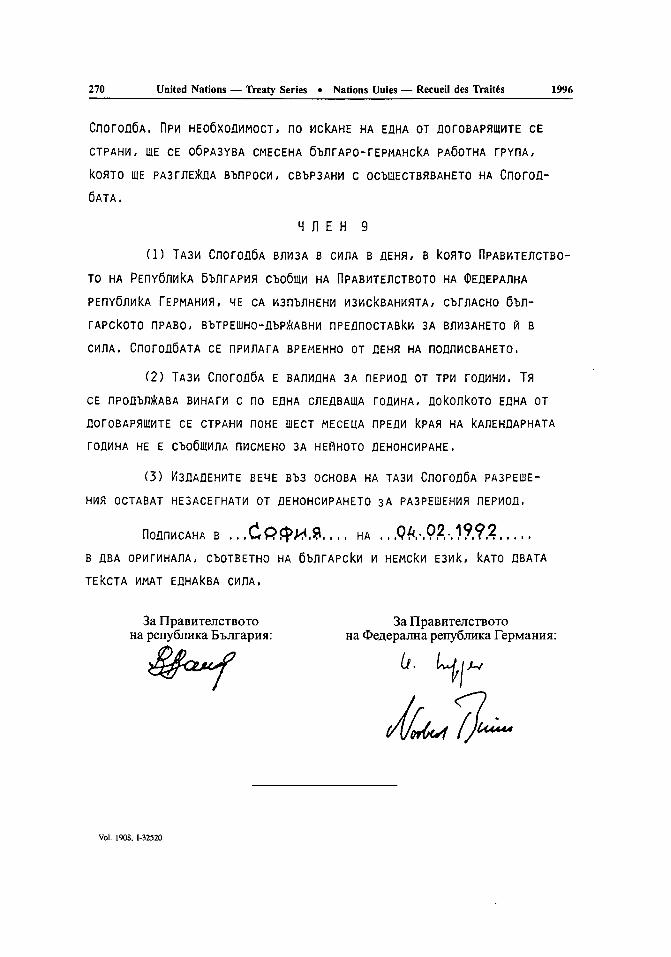

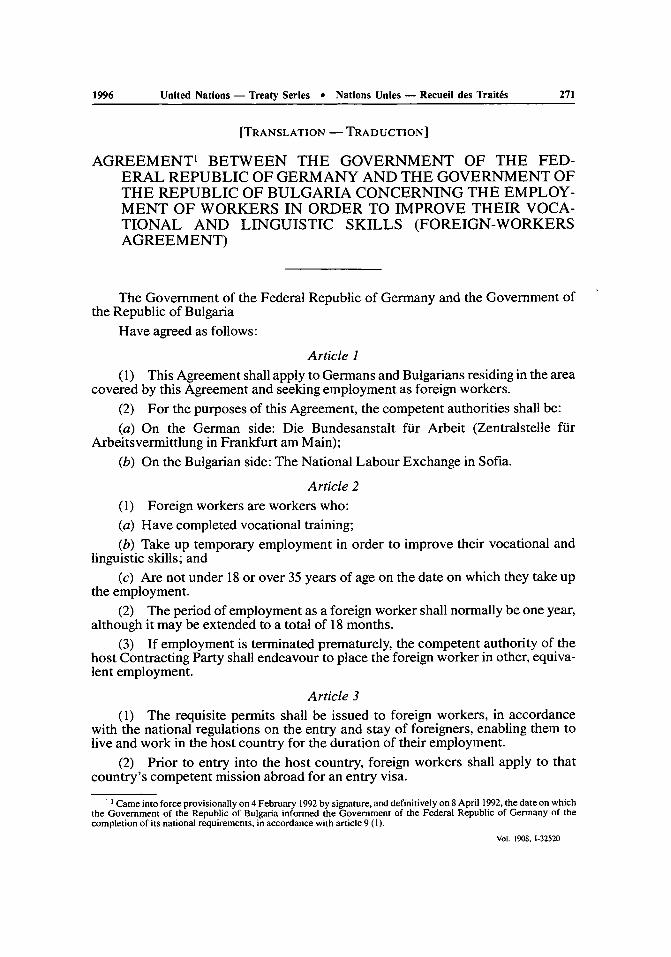

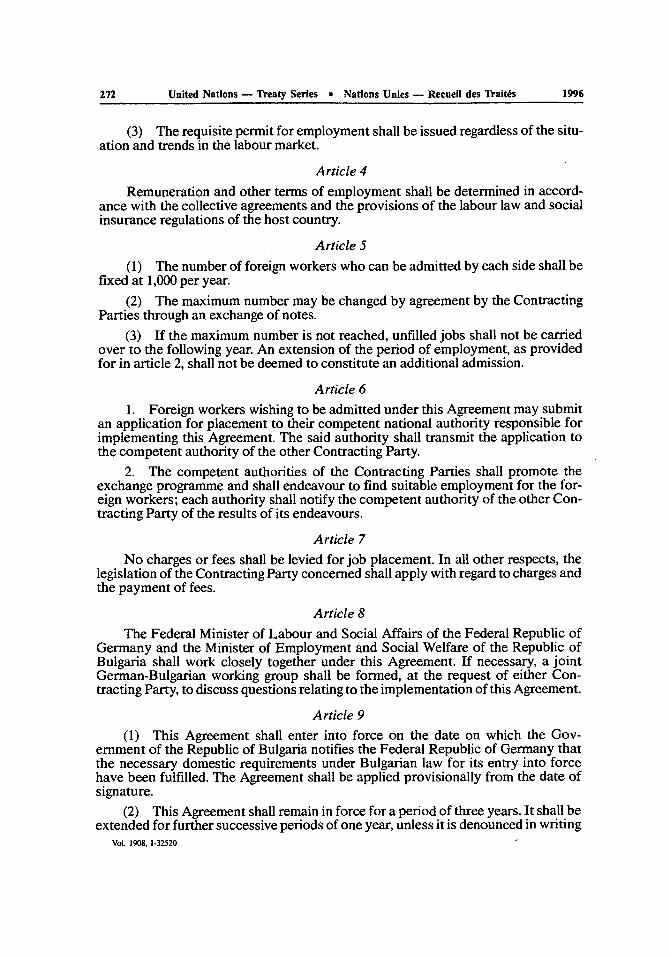

No. 32518. Germany and Bulgaria:

Agreement on navigation on inland waterways (with protocol dated at Sofia on15 July 1988). Signed at Bonn on 4 July 1989 ........................................................ 211

No. 32519. Germany and Bulgaria:Agreement concerning cooperation in the field of labour and social policy. Signed

at Sofia on 7 July 1991 .............................................................................................. 251

No. 32520. Germany and Bulgaria:Arrangement concerning the employment of workers in order to improve their

vocational and linguistic skills (Foreign-workers Agreement). Signed at Sofiaon 4 F ebruary 1992 .................................................................................................... 263

No. 32521. Germany and United Republic of Tanzania:Agreement concerning cultural cooperation (with exchange of letters). Signed at

Dares Salaam on 16 October 1989 ......................................................................... 277

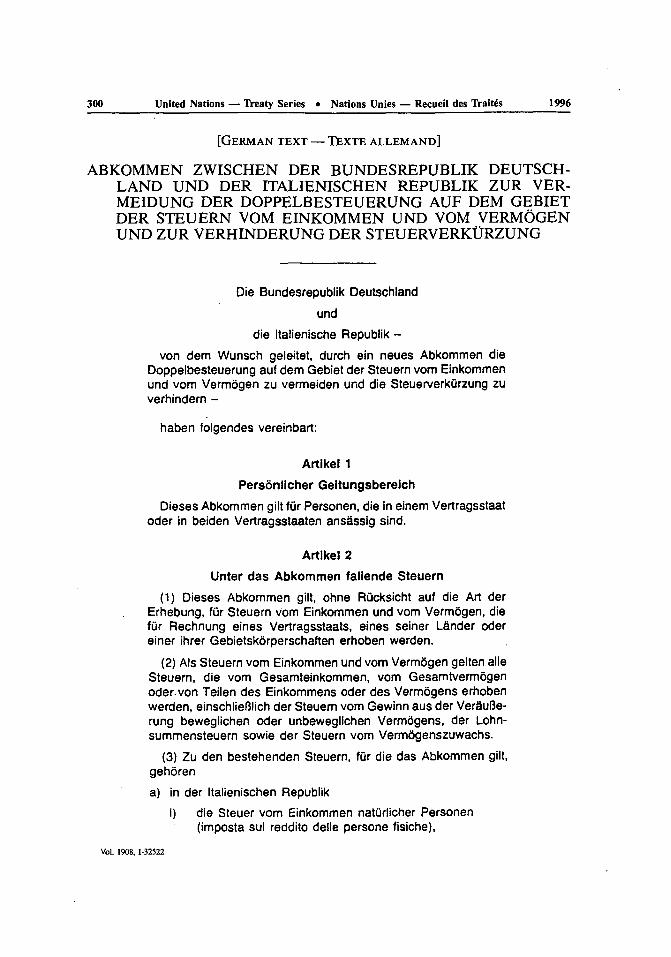

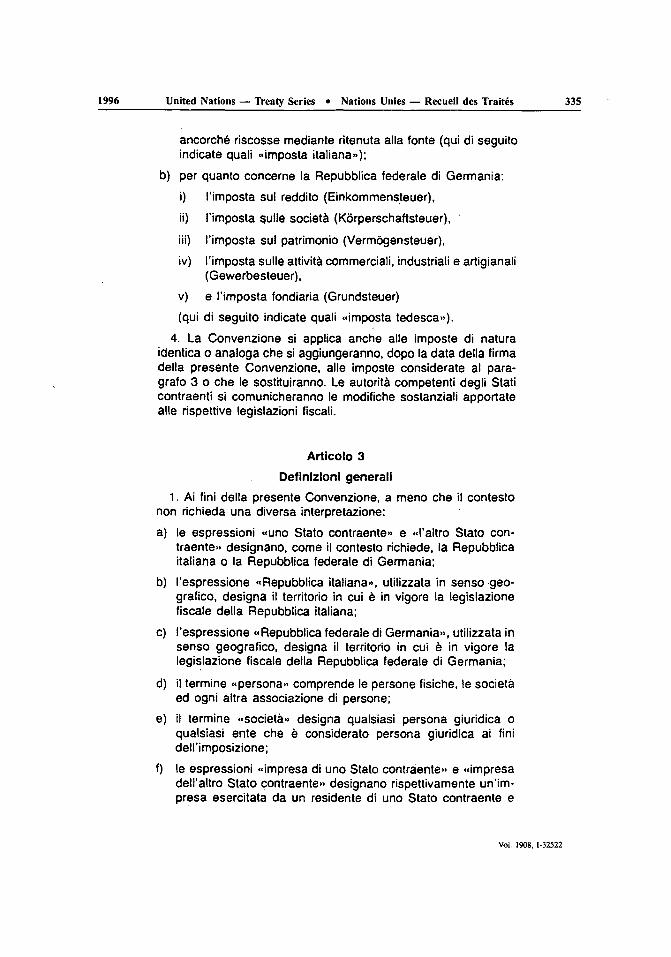

No. 32522. Germany and Italy:Agreement concerning the avoidance of double taxation with respect to taxes

on income and capital and the prevention of fiscal evasion (with protocol).Signed at Bonn on 18 October 1989 ........................................................................ 299

ANNEX A. Ratifications, accessions, subsequent agreements, etc., con-cerning treaties and international agreements registered with theSecretariat of the United Nations

No. 4739. Convention on the Recognition and Enforcement of Foreign ArbitralAwards. Done at New York, on 10 June 1958:

A ccession by U zbekistan ................................................................................................. 418

No. 4789. Agreement concerning the adoption of uniform conditions of ap-proval and reciprocal recognition of approval for motor vehicleequipment and parts. Done at Geneva, on 20 March 1958:

Application by Spain of Regulation No. 44 annexed to the above-mentionedA greem ent ................................................................................................................... 4 19

No. 6262. Agreement between Finland, Denmark, Iceland, Norway and Swedenconcerning co-operation. Signed at Helsinki, on 23 March 1962:

Agreement amending the above-mentioned Agreement, as amended. Signed atCopenhagen on 29 September 1995 ........................................................................ 420

Vol. 1908

1996 United Nations - Treaty Series 9 Nations Unies - Recueil des Traitis VII

Pages

NO 32517. Allemagne et Union des Rkpubliques socialistes soviktiques:Accord relatif aux transports maritimes (avec 6change de notes). Signd A Bonn le

7 jan vier 199 1 .............................................................................................................. 173

NO 32518. Allemagne et Bulgarie :Accord relatif A la navigation sur les eaux intdrieures (avec protocole en date A

Sofia du 15 juillet 1988). Signd A Bonn le 4 juillet 1989 ........................................ 211

NO 32519. Allemagne et Bulgarie :Accord relatif A la coopdration dans le domaine de la politique du travail et de la

politique sociale. Signd A Sofia le 7 juillet 1991 ..................................................... 251

N0 32520. Allemagne et Bulgarie :Convention relative h l'emploi de travailleurs en vue d'approfondir leurs connais-

sances professionnelles et linguistiques (Convention relative aux travailleursmigrants). Sign6 A Sofia le 4 fWvrier 1992 ............................................................... 263

N0 32521. Allemagne et Rkpublique-Unie de Tanzanie:Accord concemant la cooperation culturelle (avec 6change de lettres). Sign6 A Dar

es-Salaam le 16 octobre 1989 ................................................................................... 277

NO 32522. Allemagne et Italic :Convention tendant A 6viter la double imposition en mati~re d'imp6ts sur le revenu

et sur la fortune et "i pr6venir '6vasion fiscale (avec protocole). Sign6e A Bonnle 18 octobre 1989 ...................................................................................................... 299

ANNEXE A. Ratifications, adhesions, accords ultirieurs, etc., concernantdes traits et accords internationaux enregistrs au Secretariat del'Organisation des Nations Unies

NO 4739. Convention pour la reconnaissance et I'exkcution des sentences arbi-trales ktrangires. Faite A New-York, le 10 juin 1958 :

A dh6sion de l'O uzb6kistan .............................................................................................. 418

N0 4789. Accord concernant I'adoption de conditions uniformes d'homologa-tion et la reconnaissance rkciproque de l'homologation des kquipe-ments et pi~ces de vhicules A moteur. Fait i Genive, le 20 mars1958 :

Application par I'Espagne du R~glement n° 44 annex6 l'Accord susmentionnd.. 419

N0 6262. Accord de coopkration entre la Finlande, le Danemark, i'Islande, laNorv~ge et la Suide. Signi A Helsinki, le 23 mars 1962 :

Accord modifiant 'Accord susmentionn6, tel que modifi6. Sign6 bt Copenhague le29 septem bre 1995 ..................................................................................................... 420

Vol. 1908

VIII United Nations - Treaty Series * Nations Unies - Recueil des Trait6s 1996

Page

No. 8641. Convention on Transit Trade of Land-locked States. Done at NewYork, on 8 July 1965:

A ccession by U zbekistan ................................................................................................. 446

No. 12330. Agreement between the Government of the Republic of Finland andthe Government of the Union of Soviet Socialist Republics on thereciprocal exemption of the airlines and their personnel fromtaxes and social security payments. Signed at Helsinki on 5 May1972:

Termination with respect to Finland and Ukraine (Note by the Secretariat) ....... 447

No. 14403. Statutes of the World Tourism Organization (WTO). Adopted atMexico City on 27 September 1970:

Approval by Costa Rica of the Statutes and acceptance of the obligations of mem-bership in the W orld Tourism Organisation ........................................................... 448

No. 15511. Convention for the protection of the world cultural and naturalheritage. Adopted by the General Conference of the UnitedNations Educational, Scientific and Cultural Organization at itsseventeenth session, Paris, 16 November 1972:

R atification by Iceland ...................................................................................................... 449

No. 15935. Agreement on trade and payments between the Government of theFederative Republic of Brazil and the Government of the Social-ist Republic of Romania. Signed at Brasilia on 5 June 1975:

Termination (N ote by the Secretariat)... ........................................................................ 450

No. 17119. Convention on the prohibition of military or any other hostile use ofenvironmental modification techniques. Adopted by the GeneralAssembly of the United Nations on 10 December 1976:

A ccession by C osta R ica .................................................................................................. 451

No. 26171. Convention between Finland and the Union of Soviet Socialist Re-publics for the avoidance of double taxation with respect to taxeson income. Signed at Moscow on 6 October 1987:

Termination with respect to Finland and Ukraine (Note by the Secretariat) .......... 452

No. 28911. Basel Convention on the control of transboundary movements ofhazardous wastes and their disposal. Concluded at Basel on22 March 1989:

A ccession by U zbekistan ........................ ........................................................................ 453

No. 29215. United Nations Convention on the carriage of goods by sea, 1978.Concluded at Hamburg on 31 March 1978:

A ccession by G am bia ....................................................................................................... 454

Vol. 1908

1996 United Nations - Treaty Series * Nations Unies - Recueil des Traitis IX

Pages

NO 8641. Convention relative au commerce de transit des Etats sans littoral.Faite A New York, le 8 juillet 1965 :

A dhdsion de l'O uzbdkistan .............................................................................................. 446

NO 12330. Accord entre le Gouvernement de la R~publique de Finlande et ieGouvernement de I'Union des Ripubliques socialistes soviktiquesvisant i exonkrer rkciproquement d'impfts et de cotisations A laskcuritk sociale leurs compagnies aeriennes et le personnel decelles-ci. Signi i Helsinki le 5 mai 1972 :

Abrogation A l'6gard de la Finlande et l'Ukraine (Note du Secritariat) ................... 447

NO 14403. Statuts de I'Organisation mondiale du tourisme (OMT). Adopt~s iMexico le 27 septembre 1970:

Approbation par Costa Rica des Statuts et acceptation des obligations inhdrentesb la qualit6 de membre de 'Organisation mondiale du Tourisme ....................... 448

N0 15511. Convention pour la protection du patrimoine mondial, culturel etnaturel. Adopt6e par la Confirence g6n6rale de r'Organisationdes Nations Unies pour i'ducation, la science et la culture A sadix-septikme session, Paris, 16 novembre 1972 :

R atification de l'Islande .................................................................................................... 44 9

NO 15935. Accord de commerce et de paiements entre le Gouvernement de laRepublique fidrative du Brisil et le Gouvernement de la Rkpu-blique socialiste de Roumanie. Signe i Brasilia le 5 juin 1975:

A brogation (N ote du Secrdtariat) ................................................................................... 450

NO 17119. Convention sur I'interdiction d'utiliser des techniques de modifica-tion de renvironnement i des fins militaires on toutes autres f'mshostiles. Adoptie par l'Assemble g~nirale de l'Organisation desNations Unies le 10 d~cembre 1976 :

A dhdsion du C osta R ica ................................................................................................... 451

N0 26171. Convention entre la Finlande et l'Union des Ripubliques socialistessoviitiques tendant i 6viter la double imposition en mati~re d'im-p6ts sur le revenu. Signke A Moscou le 6 octobre 1987 :

Abrogation A I'dgard de la Finlande et 'Ukraine (Note du Secretariat) ................... 452

NO 28911. Convention de Bile sur le contr6le des mouvements transfronti resde d~chets dangereux et de leur klimination. Conclue i Bile le22 mars 1989 :

A dh6sion de l'O uzb~kistan .............................................................................................. 453

NO 29215. Convention des Nations Unies sur le transport de marchandises parmer, 1978. Conclue A Hambourg le 31 mars 1978:

Adh6sion de la Gambie ................................................................................ 454

Vol. 1908

United Nations - Treaty Series * Nations Unies - Recueil des Traitis

Page

No. 31771. Agreement between the United Nations and the Government of theRepublic of Croatia on the United Nations forces and operationsin Croatia. Signed at Zagreb on 15 May 1995:

Exchange of letters constituting an agreement supplementing the above-men-tioned Agreement. Zagreb, 26 January and 2 February 1996 .............................. 455

No. 31775. Agreement between the Federal Republic of Germany and Tunisiaconcerning financial cooperation. Signed at Tunis on 22 March1989:

Exchange of letters constituting an agreement amending the Agreement of22 March 1989 concerning financial cooperation. Tunis, 20 April 1990 and31 A ugust 1990 ........................................................................................................... 461

No. 32022. International Grains Agreement, 1995:(b) Food Aid Convention, 1995. Concluded at London on 5 December 1994:

R atification by Spain ......................................................................................................... 462Ratification by G erm any .................................................................................................. 463

International Labour Organisation

No. 606. Convention (No. 23) concerning the repatriation of seamen, adoptedby the General Conference of the International Labour Organisa-tion at its ninth session, Geneva, 23 June 1926, as modified by theFinal Articles Revision Convention, 1946:

R atification by C yprus ...................................................................................................... 464

No. 612. Convention (No. 29) concerning forced or compulsory labour, adoptedby the General Conference of the International Labour Organisa-tion at its fourteenth session, Geneva, 28 June 1930, as modified bythe Final Articles Revision Convention, 1946:

Ratification by U ruguay ................................................................................................... 466

No. 638. Convention (No. 63) concerning statistics of wages and hours of workin the principal mining and manufacturing industries, includingbuilding and construction, and in agriculture, adopted by the Gen-eral Conference of the International Labour Organisation at itstwenty-fourth session, Geneva, 20 June 1938, as modified by theFinal Articles Revision Convention, 1946:

D enunciation by Ireland ................................................................................................... 468

Vol. 1908

United Nations - Treaty Series a Nations Unies - Recueil des Traitis

Pages

NO 31771. Accord entre 'Organisation des Nations Unies et le Gouvernementde la Ripublique de Croatie relatif aux forces et aux operationsdes Nations Unies en Croatie. Signi A Zagreb le 15 mai 1995:

tchange de lettres constituant un accord compl~tant I'Accord susmentionn6.Zagreb, 26janvier et 2 f~vrier 1996 ......................................................................... 458

N0 31775. Accord de cooperation financire entre la R~publique f~dkraled'Allemagne et la Tunisie. Sign6 A Tunis le 22 mars 1989:

]change de lettres constituant un accord modifiant l'Accord de coop6ration finan-ci~re du 22 mars 1989. Tunis, 20 avril 1990 et 31 aoOt 1990 ................................. 461

NO 32022. Accord international sur les ckrkales de 1995:

b) Convention relative A l'aide alimentaire de 1995. Conclue A Londres le 5 d&cembre 1994 :

R atification de l'E spagne .................................................................................................. 462

Ratification de l'A llem agne .............................................................................................. 463

Organisation internationale du Travail

N0 606. Convention (no 23) concernant le rapatriement des marins, adoptke parla Conference ginrale de 'Organisation internationale du Travail Asa neuvi6me session, Genve, 23 juin 1926, telle qu'elle a 60 modifikepar la Convention portant rkvision des articles finals, 1946 :

R atification de Chypre ...................................................................................................... 46 5

NO 612. Convention (no 29) concernant le travail forck on obligatoire, adoptkepar la Conference gknkrale de l'Organisation internationale du Tra-vail A sa quatorzi~me session, Gen~ve, 28 juin 1930, telle qu'elle a6 t modifike par la Convention portant rkvision des articles finals,1946 :

R atification de r'U ruguay ................................................................................................. 467

NO 638. Convention (n0 63) concernant les statistiques des salaires et des heuresde travail dans les principales industries mini~res et manufactu-ri~res, y compris le bfitiment et la construction, et dans ragriculture,adopt~e par la Conference gknkrale de I'Organisation internationaledu Travail A sa vingt-quatriime session, Gen~ve, 20 juin 1938, tellequ'elle a ktk modifike par ia Convention portant revision des articlesfinals, 1946:

D dnonciation de l'Irlande ................................................................................................. 469

Vol. 1908

XII United Nations - Treaty Series * Nations Unies - Recueil des Traitis 1996

Page

No. 792. Convention (No. 81) concerning labour inspection in industry andcommerce. Adopted by the General Conference of the InternationalLabour Organisation at its thirtieth session, Geneva, 11 July 1947:

Ratification by Belarus ..................................................................................................... 470

No. 881. Convention (No. 87) concerning freedom of association and protectionof the right to organise. Adopted by the General Conference of theInternational Labour Organisation at its thirty-first session, SanFrancisco, 9 July 1948:

R atification by Sri L anka ................................................................................................. 472

No. 898. Convention (No. 88) concerning the organisation of the employ-ment service. Adopted by the General Conference of the Interna-tional Labour Organisation at its thirty-first session, San Fran-cisco, 9 July 1948:

R atification by B elarus ..................................................................................................... 474

No. 2109. Convention (No. 92) concerning crew accommodation on board ship(revised 1949). Adopted by the General Conference of the Interna-tional Labour Organisation at its thirty-second session, Geneva,18 June 1949:

R atification by C yprus ...................................................................................................... 476

No. 4648. Convention (No. 105) concerning the abolition of forced labour.Adopted by the General Conference of the International LabourOrganisation at its fortieth session, Geneva, 25 June 1957:

R atification by B elarus ..................................................................................................... 478

No. 8175. Convention (No. 120) concerning hygiene in commerce and offices,adopted by the General Conference of the International LabourOrganisation at its forty-eighth session, Geneva, 8 July 1964:

R atification by U ruguay ................................................................................................... 480

No. 14862. Convention (No. 138) concerning minimum age for admission toemployment. Adopted by the General Conference of the Interna-tional Labour Organisation at its fifty-eighth session, Geneva,26 June 1973:

Ratification by San M arino .............................................................................................. 482

No. 16705. Convention (No. 144) concerning tripartite consultations to pro-mote the implementation of international labour standards.Adopted by the General Conference of the International LabourOrganisation at its sixty-first session, Geneva, 21 June 1976:

R atification by G uinea ..................................................................................................... 484

Vol. 1908

1996 United Nations - Treaty Series 9 Nations Unies - Recueil des Traitis Xlll

Pages

NO 792. Convention (n0 81) concernant l'inspection du travail dans l'industrieet le commerce. Adoptke par la Conffrence gkn6rale de I'Organisa-tion internationale du Travail A sa trenti me session, Gen~ve, 1H juil-let 1947 :

R atification du B 61arus ..................................................................................................... 471

NO 881. Convention (n° 87) concernant la libert6 syndicale et la protection dudroit syndical. Adopt6e par ia Conference ginkrale de I'Organisationinternationale du Travail A sa trente et uni me session, San Fran-cisco, 9 juillet 1948 :

R atification de Sri L anka .................................................................................................. 473

N° 898. Convention (n0 88) concernant l'organisation du service de I'em-ploi. Adoptke par la Conffrence gkn6rale de l'Organisation interna-tionale du Travail A sa trente et uni6me session, San Francisco, 9 juil-let 1948 :

R atification du B 61arus ..................................................................................................... 475

NO 2109. Convention (n° 92) concernant le logement de l'iquipage A bord(riviske en 1949). Adoptie par la Conf6rence g6nirale de I'Orga-nisation internationale du Travail A sa trente-deuxi~me session,Genive, 18 juin 1949 :

R atification de C hypre ...................................................................................................... 477

NO 4648. Convention (no 105) concernant 'abolition du travail forck. Adoptkepar la Conf6rence ginkrale de I'Organisation internationale du Tra-vail i sa quarantime session, Genive, 25 juin 1957 :

R atification du BW 1arus ..................................................................................................... 479

NO 8175. Convention (no 120) concernant l'hygiine dans le commerce et lesbureaux, adoptke par la Conf6rence gknkrale de l'Organisationinternationale du Travail A sa quarante-huitiime session, Geneve,8 juillet 1964 :

R atification de l'U ruguay ................................................................................................. 481

NO 14862. Convention (n° 138) concernant l'ige minimum d'admission il i'em-ploi. Adoptke par la Confirence gkn6rale de l'Organisation inter-nationale du Travail A sa cinquante-huiti me session, Gen~ve,26 juin 1973 :

R atification de Saint-M arin .............................................................................................. 483

NO 16705. Convention (n° 144) concernant les consultations tripartitesdestinies A promouvoir la mise en ceuvre des normes internatio-nales du travail. Adoptie par la Conference g~n~rale de l'Organi-sation internationale du Travail A sa soixante et uni6me session,Gen~ve, 21 juin 1976:

R atification de la G uin e .................................................................................................. 485

Vol. 1908

XIV United Nations - Treaty Series * Nations Unies - Recueil des Traitis 1996

Page

No. 20690. Convention (No. 147) concerning minimum standards in merchantships. Adopted by the General Conference of the InternationalLabour Organisation at its sixty-second session, Geneva, 29 Oc-tober 1976:

R atification by C yprus ...................................................................................................... 486

No. 22346. Convention (No. 156) concerning equal opportunities and equaltreatment for men and women workers: workers with family re-sponsibilities. Adopted by the General Conference of the Interna-tional Labour Organisation at its sixty-seventh session, Geneva,23 June 1981:

R atification by Ireland ...................................................................................................... 488

No. 23439. Convention (No. 159) concerning vocational rehabilitation and em-ployment (disabled persons). Adopted by the General Conferenceof the International Labour Organisation at its sixty-ninth ses-sion, Geneva, 20 June 1983:

R atification by G uinea ...................................................................................................... 490

No. 25944. Convention (No. 160) concerning labour statistics. Adopted by theGeneral Conference of the International Labour Organisation atits seventy-first session, Geneva, 25 June 1985:

R atification by Ireland ...................................................................................................... 492

No. 26705. Convention (No. 162) concerning safety in the use of asbestos.Adopted by the General Conference of the International LabourOrganisation at its seventy-second session, Geneva, 24 June 1986:

R atification by U ruguay ................................................................................................... 494

No. 31173. Convention (No. 172) concerning working conditions in hotels,restaurants and similar establishments. Adopted by the Gen-eral Conference of the International Labour Organisation at itsseventy-eighth session, Geneva, 25 June 1991:

R atification by U ruguay ................................................................................................... 496

No. 32088. Convention (No. 173) concerning the protection of workers' claimsin the event of the insolvency of their employer. Adopted by theGeneral Conference of the International Labour Organisation atits seventy-ninth session, Geneva, 23 June 1992:

Ratification by Sw itzerland ............................................................................................. 498

Vol. 1908

1996 United Nations - Treaty Series * Nations Unies - Recueil des Trait~s XV

Pages

NO 20690. Convention (no 147) concernant les normes minima A observer surles navires marchands. Adoptke par la Confirence g6nkrale del'Organisation internationale du Travail A sa soixante-deuxi~mesession, Genive, 29 octobre 1976 :

R atification de Chypre ...................................................................................................... 487

NO 22346. Convention (n0 156) concernant l'kgalit6 de chances et de traitementpour les travailleurs des deux sexes : travailleurs ayant des res-ponsabilitis familiales. Adoptke par la Conference g~n~rale del'Organisation internationale du Travail A sa soixante-septi~mesession, Gen~ve, 23 juin 1981 :

R atification de rIrlande .................................................................................................... 489

N0 23439. Convention (n0 159) concernant la rkadaptation professionnelle etl'emploi des personnes handicap~es. Adopt~e par la Conferenceg~nkrale de l'Organisation internationale du Travail Ai sa soixante-neuviime session, Gen~ve, 20 juin 1983 :

Ratification de la G uin~e .................................................................................................. 491

NO 25944. Convention (n0 160) concernant les statistiques du travail. Adopt~epar la Confirence gknirale de I'Organisation internationale duTravail A sa soixante et onziime session, Gen~ve, 25 juin 1985 :

R atification de I'Irlande .................................................................................................... 493

NO 26705. Convention (n° 162) concernant la s~curiti dans l'utilisation del'amiante. Adoptke par la Conference g6nirale de l'Organisationinternationale du Travail A sa soixante-douziime session, Gen~ve,24 juin 1986:

R atification de l'U ruguay ................................................................................................. 495

NO 31173. Convention (n0 172) concernant les conditions de travail dans lesh6tels, restaurants et ktablissements similaires. Adoptke par laConfirence gin~rale de l'Organisation internationale du Travail Asa soixante-dix-huitiime session, Genive, 25 juin 1991 :

R atification de l'U ruguay ................................................................................................. 497

NO 32088. Convention (no 173) concernant ia protection des crkances des tra-vailleurs en cas d'insolvabilit6 de leur employeur. Adopt~e par iaConference gkn~rale de l'Organisation internationale du Travail Asa soixante-dix-neuvi~me session, Gen~ve, 23 juin 1992 :

R atification de la Suisse .................................................................................................... 499

Vol. 1908

XVI United Nations - Treaty Series e Nations Unies - Recuei des Traitis 1996

Page

ANNEX C. Ratifications, accessions, etc., concerning treaties and interna-tional agreements registered with the Secretariat of the League ofNations

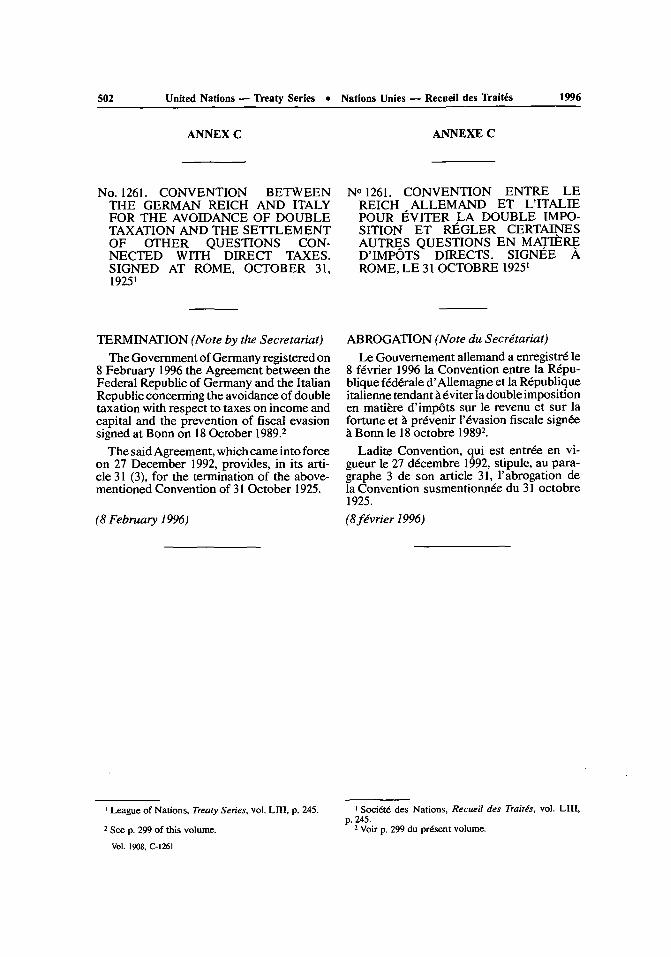

No. 1261. Convention between the German Reich and Italy for the avoidance ofdouble taxation and the settlement of other questions connectedwith direct taxes. Signed at Rome, October 31, 1925:

Termination (N ote by the Secretariat) ........................................................................... 502

Vol. 1908

United Nations - Treaty Series * Nations Unies - Recueil des Trait~s

Pages

ANNEXE C. Ratifications, adhesions, etc., concernant des traits et accordsinternationaux enregistrs au Secritariat de la Societg des Nations

NO 1261. Convention entre le Reich allemand et l'Italie pour 6viter la doubleimposition et r~gler certaines autres questions en mati~re d'imp6tsdirects. Signke A Rome, le 31 octobre 1925 :

A brogation (N ote du Secrftariat) ................................................................................... 502

Vol. 1908

XVII

NOTE BY THE SECRETARIAT

Under Article 102 of the Charter of the United Nations every treaty and every international agree-ment entered into by any Member of the United Nations after the coming into force of the Charter shall,as soon as possible, be registered with the Secretariat and published by it. Furthermore, no party to atreaty or international agreement subject to registration which has not been registered may invoke thattreaty or agreement before any organ of the United Nations. The General Assembly, by resolution 97 (I),established regulations to give effect to Article 102 of the Charter (see text of the regulations, vol. 859,p. vI).

The terms "treaty" and "international agreement" have not been defined either in the Charter or inthe regulations, and the Secretariat follows the principle that it acts in accordance with the position of theMember State submitting an instrument for registration that so far as that party is concerned the instru-ment is a treaty or an international agreement within the meaning of Article 102. Registration of aninstrument submitted by a Member State, therefore, does not imply ajudgement by the Secretariat on thenature of the instrument, the status of a party or any similar question. It is the understanding of theSecretariat that its action does not confer on the instrument the status of a treaty or an internationalagreement if it does not already have that status and does not confer on a party a status which it wouldnot otherwise have.

Unless otherwise indicated, the translations of the original texts of treaties, etc., published in thisSeries have been made by the Secretariat of the United Nations.

NOTE DU SECRP-TARIAT

Aux termes de l'Article 102 de la Charte des Nations Unies, tout trait6 ou accord internationalconclu par un Membre des Nations Unies apr~s l'entr6e en vigueur de la Charte sera, le plus t6t possible,enregistr6 au Secretariat et publi6 par lui. De plus, aucune partie h un trait6 ou accord international quiaurait dO Ptre enregistr6 mais ne l'a pas W ne pourra invoquer ledit trait6 ou accord devant un organe desNations Unies. Par sa r6solution 97 (1), I'Assembl(e g6n~rale a adopt6 un r glement destin6 A mettre enapplication ]'Article 102 de la Charte (voir texte du r glement, vol. 859, p. IX).

Le terme <( traitd >> et l'expression « accord international o n'ont W d6finis ni dans la Charte ni dansle r~glement, et le Secretariat a pris comme principe de s'en tenir A la position adoptie A cet 6gard parl'Etat Membre qui a pr6sent6 l'instrument A l'enregistrement, A savoir que pour autant qu'il s'agit de cetEtat comme partie contractante l'instrument constitue un trait6 ou un accord international au sens del'Article 102. I1 s'ensuit que l'enregistrement d'un instrument prdsent6 par un Etat Membre n'implique,de la part du Secretariat, aucun jugement sur la nature de l'instrument, le statut d'une partie ou touteautre question similaire. Le Secretariat considare donc que les actes qu'il pourrait 8tre amen6 h accomplirne confirent pas A un instrument la qualit6 de <, traits ou d'<< accord international , si cet instrumentn'a pas d6jA cette qualit6, et qu'ils ne conferent pas A une partie un statut que, par ailleurs, elle neposs&lerait pas.

Sauf indication contraire, les traductions des textes originaux des trait6s, etc., publids dans ce Re-cueil ont 6td 6tablies par le Secretariat de l'Organisation des Nations Unies.

Treaties and international agreements

registered

from 1 February 1996 to 8 February 1996

Nos. 32511 to 32522

Traitis et accords internationaux

enregistris

du ler fivrier 1996 au 8 fivrier 1996

NOs 32511 4 32522

Vol. 1908

No. 32511

BRAZILand

ECUADOR

Agreement relating to the exercise of remunerative activitiesby dependants of diplomatic, consular, administrativeand technical personnel. Signed at Brasilia on 22 June1993

Authentic texts: Portuguese and Spanish.

Registered by Brazil on 1 February 1996.

BRESILet

EQUATEUR

Accord relatif ' 'exercice d'activites rkmun6rees par despersonnes a charge du personnel diplomatique, con-sulaire, administratif et technique. Signe ' Brasilia le22 juin 1993

Textes authentiques : portugais et espagnol.

Enregistr. par le Brsil le lerfgvrier 1996.

Vol. 1908, 1-32511

4 United Nations - Treaty Series * Nations Unies - Recueil des Traitis 1996

[PORTUGUESE TEXT - TEXTE PORTUGAIS]

ACORDO ENTRE 0 GOVERNO DA REP(JBLICA FEDERATIVA DOBRASIL E 0 GOVERNO DA REPOBLICA DO EQUADOR SOBRE0 EXERCICIO DE ATIVIDADES REMUNERADAS POR PARTEDE DEPENDENTES DO PESSOAL DIPLOMATICO, CONSU-LAR, ADMINISTRATIVO E T1tCNICO

0 Governo da Repblica Federativa do Brasil

e

O Governo da Rep6blica do Equador(doravante denominados "Partes Contratantes"),

Considerando a estigio particularmente elevado de

entendimento e compreensio existentes entre os dois palses; e

Com o intuito de estabelecer novos mecanismos para a

fortalecimento das suas relaCies diplomiticas,

Acordam o seguinte:

ARTIGO I

Os dependentes do pessoal diplomitico, consular,

administrativo e ticnico de uma das Partes Contratantes, designado para

exercer missgo oficial na outra, como membro de Missio diplomitica,

Repartigio consular ou Missiao junto a Organismo Internacional com sede

em qualquer dos dois palses, poderao receber autorizacio para exercer

atividade remunerada no Estado receptor, respeitados os interesses

nacionais. A autorizagco em aprego poderg ser negada nos casos em que:

a) o empregador for o Estado receptor, inclusive por meio de

sues autarquias, fundagves, empresas p5blican a sociedades

de economia mista;

b) afetem a seguranCa nactonal.

Vol. 1908. 1-32511

1996 United Nations - Treaty Series * Nations Unies - Recueil des Traitis 5

ARTIGO II

Para fins deste Acordo, sao considerados "dependentes":

a) conjuge;

b) filhos ou filhas solteiros menores de 21 anos;

c) filhos ou filhas solteiros menores de 25 anos que estejam

estudando, em horrio integral, nas universidades ou

centros de ensino superior reconhecidos por cada Estado;

d) filhos ou filhas solteiros com deficiincias fisicas ou

mentais.

ARTIGO III

1. 0 exercicio de atividade remunerada por dependente, no Estado

receptor, dependerS de pr~via autorizac~o de trabalho do Governo local,

por intermidio de pedido formulado pela Embaixada junto ao Cerimonial

do Ministgrio Cas Relag6es Exteriores. Ap6s verificar se a pessoa em

questgo se enquadra nas categorias defLnidas no presente Acordo e ap6s

observar os dispositivos internos aplic~veis, o Cerimonial informara

oficialmente i Embaixada que a pessoa tem permiss~o para exercer

atividade remunerada, sujeita A legislacio aplic~vel no Estado

receptor.

2. Nos casos de profiss5es que requeiram qualificag6es

especiais, o dependente nio estarS isento de preenchi-las. As

disposigces do presente Acordo nio poderiao ser interpretadas como

implicando o reconhecimento, pela o6tra Parte Contratante, de t~tulos

para os efeitos do exercicio de uma profisso.

3. Para os dependentes que exercam atividade remunerada nos

termos deste Acordo, fica suspensa, em carter irrevoggvel, a imunidade

de jurisdigio civil e administrativa relativa a todas as quest6es

decorrentes da referida atividade. Nos casos em que um dependente, nos

termos do presente Acordo, que gozar de imunidade de jurisdigio penal,

de conformidade com a Conven~io de Viena sobre RelaC~es Diplomiticas,

seja acusado de um delito cometido em relagio a tal atividade, o Estado

acreditante considerarl seriamente qualquer solicitaqio escrita de

renincia daquela imunidade.

VOL. 1908, 1-32511

6 United Nations - Treaty Series - Nations Unies - Recueil des Traitks 1996

4. Os dependentes que exergam atividade remunerada nos termos

deste Acordo perderio a isenao de cumprimento das obrigac5es

tributgrias e previdencifrias decorrentes da referida atividade,

ficando, em conseqincia, sujeitos a legislaqao de referincia aplicivel

5s pessoas fisicas residentes ou domiciliadas no Estado receptor.

5. A autorizacao para exercer atividade remunerada por parte de

um dependente cessari quando o agente diplomitico, funcionirio ou

empregado consular ou membro do pessoal administrativo e ticnico do

qual emana a dependencia termine suas funGoes perante o Governo onde

esteja acreditado.

ARTIGO IV

1. Cada Parte Contratante notificarg i outra o cumprimento dos

respectivos requisitos legais internos necessairios a entrada em vigor

deste Acordo, a qual se dari na data da 61tima notificagao.

2. 0 presente Acordo ter validade de 6 (seis) anos, sendo

tacitamente renovado por sucessivos periodos de urn ano, salvo se uma

das Partes manifestar, por via diplomitica, sua intengao de

denuncii-lo. Nesse caso, a den~ncia surtiri efeito 6 (seis) meses ap6s

o recebimento da notificacio.

Feito em Brasilia, em c9-L de junho de 1993, em dois

exemplares originais, nos idiomas portugu~s e espanhol, sendo ambos os

textos igualmente autgnticos.

Pelo Governo Pelo Governoda Rep6blica do Brasil: da Repdiblica do Equador:

Luiz FELIPE PALMEIRA LAMPREIA JUAN MANUEL AGUIRREMinistro de Estado, interino, Embaixador Extraordinirio e Plenipo-

das Relaq6es Exteriores tencidrio junto ao Governo da Repd-blica Federativa do Brasil

Vol. 1908, 1-32511

United Nations - Treaty Series * Nations Unies - Recueil des Traitks

[SPANISH TEXT - TEXTE ESPAGNOL]

ACUERDO ENTRE EL GOBIERNO DE LA REPJBLICA FEDE-RATIVA DEL BRASIL Y EL GOBIERNO DE LA REPUBLICADEL ECUADOR SOBRE EL EJERCICIO DE ACTIVIDADESREMUNERADAS POR PARTE DE LOS DEPENDIENTES DELPERSONAL DIPLOMATICO, CONSULAR, ADMINISTRATIVO YTECNICO

El Gobierno da la Repfblica Federativa del Brasil

y

El Gobierno de la Rep~blica del Ecuador

(en adelante denominados "Partes Contratantes"),

Considerando el nivel particularmente elevado de

entendimiento y comprensi6n existente entre los dos palses; y

Con el prop6sito de establecer nuevos mecanismos para el

fortalecimiento de sus relaciones diplomiticas,

Acuerdan 1o siguiente:

ARTICULO I

Los dependientes del personal diplomitico, consular,

administrativo y t~cnico de una de las Partes Contratantes, designado

para ejercer misi6n oficial en la otra, como miembro de la Misi6n

Diplomitica, Repartici6n Consular o Misi6n ante Organismo Internacional

con sede en cualquiera de los dos palses, podrin recibir autorizaci6n

para ejercer actividad remunerada en el Estado receptor, respetando los

intereses nacionales.

Vol. 1908, 1-32511

8 United Nations - Treaty Series * Nations Unies - Recueil des Traitis 1996

La referida autorizaci6n podri ser negada en los casos en

que:

a) el empleador sea el Estado receptor, inclusive por medio

de sus entidades aut6nomas, fundaciones, empresas p~blicas

y sociedades de economa mixta;

b) afectan a la seguridad nacional.

ARTICULO II

Para fines de este Acuerdo, se consideran "dependientes":

a) El c6nyuge;

b) Los hijos o hijas solteros menores de 21 anos;

c) Los hijos o hijas solteros menores de 25 afos que se

encuentren estudiando, en horario completo, en las

universidades o centros de ensefianza superior reconocidos

por cada Estado; y

d) Los hijos o hijas solteros con deficiencias fisicas o

mentales.

ARTICULO III

1. El ejercicio de la actividad remunerada por un dependiente,

en el Estado receptor, dependeri de autorizaci6n de trabajo del

Gobierno local, por intermedio de pedido formulado por la Embajada ante

el Departamento de Protocolo del Ministerio de Relaciones Exteriores.

Luego de comprobar que la persona en cuesti6n se encuadra en las

categorlas definidas en el presente Acuerdo y despugs de observar las

disposiciones internas aplicables, el Departamento de Protocolo

informari oficialmente a la Embajada que el dependiente esti autorizado

para ejercer actividad remunerada, sujeta a la legislaci6n aplicable en

el Estado receptor.

2. En los casos de profesionales que requieran requisitos

especiales, el dependiente no estarg exonerado de cumplirlos. Las

disposiciones del presente Acuerdo no podrin ser interpretadas en el

Vol. 1908, 1-32511

1996 United Nations - Treaty Series e Nations Unies - Recueil des Traitis 9

sentido de que obligan el reconocimiento, por la otra Parte, de t1tulos

para el ejercicio de una profesi6n.

3. Para los dependientes que ejerzan actividad remunerada, de

conformidad con este Acuerdo, queda suspendida, con caricter

irrevocable, la inmunidad de la jurisdicci6n civil y administrativa

relacionada con todas las cuestiones consecuentes de la aludida

actividad. En los casos en que un dependiente, dentro de los tirminos

del presente Acuerdo, y que goce de inmunidad de jurisdicci6n penal de

acuerdo con la Convenci6n de Viena sobre Relaciones Diplomiticas, sea

acusado de un delito cometido en relaci6n con tal actividad, el Estado

acreditante considerari seriamente cualquier solicitud por escrito de

renuncia de dicha inmunidad.

4. Los dependientes que ejerzan actividad remunerada, de

conformidad con este Acuerdo, perderin la exenci6n de cumplir las

obligaciones tributarias y de seguridad social, decurrentes de la

mencionada actividad, quedando, en consecuencia, sujetos a la

legislaci6n de referencia aplicable a las personas fisicas residentes y

domiciliadas en el Estado receptor.

5. La autorizaci6n para ejercer actividad remunerada por parte

de un dependiente, cesari cuando el agente diplomitico, funcionario oempleado consular o miembro del personal administrativo y ticnico del

cual emana la dependencia, termine sus funciones ante el Gobierno donde

se encuentre acreditado.

ARTICULO IV

1. Cada Parte Contratante notificari a la otra el cumplimiento

de los respectivos requisitos legales internos necesarios para la

entrada en vigencia de este Acuerdo. La fecha de entrada en vigor seri

la de la 5itima notificaci6n.

2. El presente Acuerdo tendrg validez de seis afios, siendo

t~citamente renovado por sucesivos perfodos de un afo, salvo si una delas Parte manifieste, pOr vla diplomitica, su intenci6n de denunciarlo.

En este caso, la denuncia surtiri efecto seis meses denpu6s de recibida

la notificaci6n.

Vol. 1908.1-32511

10 United Nations - Teaty Series * Nations Unies - Recueil des Trait6s 1996

Celebrado en Brasilia, a los Q-Xdfas del mes de junio de

mil novecientos noventa y tres en dos ejemplares originales, en idiomas

portugugs y espaiiol, igualmente id6nticos.

Por el Gobiemode la Repdblica Federativa del Brasil:

Por el Gobiemode la Reptblica del Ecuador:

Vol. 1908, 1-32511

1996 United Nations - Treaty Series * Nations Unies - Recueil des Traitks 11

[TRANSLATION - TRADUCTION]

AGREEMENT' BETWEEN THE GOVERNMENT OF THE FEDER-ATIVE REPUBLIC OF BRAZIL AND THE GOVERNMENT OFTHE REPUBLIC OF ECUADOR RELATING TO THE EXERCISEOF REMUNERATIVE ACTIVITIES BY DEPENDANTS OF DIP-LOMATIC, CONSULAR, ADMINISTRATIVE AND TECHNICALPERSONNEL

The Government of the Federative Republic of Brazil and the Government ofthe Republic of Ecuador (hereinafter referred to as the "Contracting Parties"),

Considering the very high level of agreement and understanding that existsbetween the two countries, and

With a view to establishing new mechanisms for strengthening their diplomaticrelations,

Have agreed as follows:

Article IThe dependants of diplomatic, consular, administrative and technical personnel

of one Contracting Party appointed to carry out, in the other Party, official duties asa member of a diplomatic mission, consular office or mission to an internationalorganization based in either of the two countries may receive permission to exercisea remunerative activity in the receiving State, provided that national interests arerespected.

The permission in question may be refused in cases in which:

(a) The employer is the receiving State, including instances where the Statewould be acting as an employer through its quasi-independent organizations, foun-dations, public enterprises and mixed-economy companies; or

(b) National security might be affected.

Article IIFor the purposes of this Agreement, "dependant" means:

(a) Spouses;

(b) Unmarried children under 21;

(c) Unmarried children under 25 in full-time attendance at a university or post-secondary educational institution recognized by each State;

(d) Unmarried children who are physically or mentally disabled.

Article III1. A dependant who wishes to exercise a remunerative activity in the re-

ceiving State will need authorization from the local Government. Such permissionshall be sought by means of a request made by the Embassy to the Department of

I Came into force on 19 June 1995, the date of the last of the notifications by which the Contracting Parties informed

each other of the completion of their respective internal legal requirements, in accordance with article IV (1).

Vol. 1908, 1-32511

12 United Nations - Treaty Series * Nations Unies - Recueil des Traitis 1996

Protocol of the Ministry of Foreign Affairs. After establishing that the person inquestion comes within the categories defined in this Agreement, and after observingthe applicable internal provisions, the Department of Protocol shall officially informthe Embassy that the dependant has permission to exercise a remunerative activity,subject to the legislation applicable in the receiving State.

2. In the case of professions which require special qualifications, the depen-dant shall not be exempt from the requirement to comply with these conditions. Theprovisions of this Agreement may not be construed to require the recognition, by theother Party, of academic qualifications for the purpose of practising a profession.

3. Immunity from civil and administrative jurisdiction relating to all mattersstemming from employment shall be suspended irrevocably in respect of those de-pendants who exercise a remunerative activity in accordance with this Agreement.In the event that a dependant who, within the terms of this Agreement, has immunityfrom criminal jurisdiction in accordance with the Vienna Convention on DiplomaticRelations' is accused of a criminal offence in relation to his or her employment, thesending State shall give serious consideration to any written request for the waivingof such immunity.

4. Dependants who exercise a remunerative activity in the receiving State inaccordance with this Agreement shall cease to be exempt from tax and social secu-rity obligations stemming from the above-mentioned activity. They shall, in conse-quence, become subject to the relevant legislation which is applicable to physicalpersons resident or domiciled in the receiving State.

5. The authorization of a dependant to exercise a remunerative activity shallterminate when the functions of the diplomatic agent, consular official or employeeor administrative or technical staff member on whom that person is dependent haveended in relation to the Government to which he or she was accredited.

Article IV

1. The Contracting Parties shall notify each other of the completion of theirrespective internal legal procedures required for the entry into force of this Agree-ment. The date of entry into force shall be that of the second notification.

2. This Agreement shall be valid for six years and shall be renewed by tacitagreement for successive one-year periods unless either Party indicates through thediplomatic channel that it wishes to terminate the Agreement. In such case, thetermination shall be effective six months from the receipt of the notification.

DONE at Brasilia on 22 June 1993, in two originals in the Portuguese and Span-ish languages, both texts being equally authentic.

For the Government For the Governmentof the Federative Republic of Brazil: of the Republic of Ecuador:Luiz FELIPE PALMEIRA LAMPREIA JUAN MANUEL AGUIRRE

Minister of State, Interior Ambassador Extraordinary and Pleni-and Exterior Relations potentiary to Government of the Fed-

erative Republic of Brazil

'United Nations, Treaty Series, vol. 500, p. 95.

Vol. 1908, 1-32511

1996 United Nations - Treaty Series * Nations Unies - Recueil des Traitks 13

[TRADUCTION - TRANSLATION]

ACCORD' ENTRE LE GOUVERNEMENT DE LA REPUBLIQUE Ft-DERATIVE DU BR1tSIL ET LE GOUVERNEMENT DE LA Rit-PUBLIQUE DE L'.QUATEUR RELATIF A L'EXERCICE D'AC-TIVITItS R1tMUNItRES PAR DES PERSONNES A CHARGE DUPERSONNEL DIPLOMATIQUE, CONSULAIRE, ADMINISTRA-TIF ET TECHNIQUE

Le Gouvernement de la Rdpublique f6ddrative du Br6sil et le Gouvemement dela R6publique de l'Equateur (ci-apris : les << Parties contractantes >>),

Consid6rant les liens particuli~rement 6troits d'entente et de compr6hensionexistant entre les deux pays,

Entendant 6tablir de nouveaux m6canismes pour renforcer leurs relationsdiplomatiques,

Conviennent de ce qui suit:

Article er

Les personnes A charge des membres du personnel diplomatique, consulaire,administratif et technique de l'une des Parties contractantes ddsign6s pour accom-plir une mission officielle aupris de l'autre Partie contractante en tant que membresd'une mission diplomatique, d'un poste consulaire ou d'une mission aupr~s d'uneorganisation intemationale ayant son si6ge dans l'un quelconque des deux payspourront recevoir l'autorisation d'exercer une activit6 r6mun6r6e dans l'Etat d'ac-cueil sous r6serve du respect des int6rts nationaux. Cette autorisation pourra 8trerefusde dans les cas suivants :

a) L'employeur est l'Etat d'accueil, y compris par le canal de ses organismesautonomes, de ses fondations, de ses entreprises publiques et de ses soci6t6s d'6co-nomie mixte;

b) Les activit6s touchent A la sdcurit6 nationale.

Article II

Aux fins du pr6sent Accord, sont consid6r6es << personnes A charge >:

a) Le conjoint;

b) Les fils et filles c61ibataires mineurs de 21 ans;

c) Les fils et filles c61ibataires mineurs de 25 ans qui poursuivent des 6tudes, Atemps complet, dans des universit6s ou centres d'enseignement sup6rieur reconnuspar chacun des deux Etats;

d) Les fils et filles c6libataires atteints de d6ficiences physiques ou mentales.

I EntrA en vigueurle 19juin 1995, date de la dernire des notifications par lesquelles les Parties contractantes se sontinform6es de I'accomplissement de leurs formalitds 16gales internes respectives, conformdment au paragraphe I de1'article IV.

Vol. 1908, 1-32511

United Nations - Treaty Series o Nations Unies - Recueil des Traitis

Article III

1. L'exercice de l'activit6 r6mun6rde par une personne A charge, dans l'Etatd'accueil, d6pendra d'une autorisation pr6alable de travail d61ivr6e par le gouverne-ment local sur demande prdsent6e par l'Ambassade au Service du protocole duMinist~re des relations ext6rieures. Apr~s avoir v6rifi6 si l'int6ress6 relive de l'unedes cat6gories d6finies dans le pr6sent Accord et apr~s avoir satisfait aux disposi-tions internes applicables, le Service du protocole informera officiellement l'Ambas-sade que l'int6ress6 est autoris6 A exercer une activit6 r6mun6r6e, sous r6serve de la16gislation applicable dans l'Etat d'accueil.

2. Dans le cas de professions qui exigent des qualifications sp6ciales, la per-sonne A charge ne sera pas dispensde de ces qualifications. Les dispositions dupr6sent Accord ne pourront pas 8tre interpr6t6es comme impliquant reconnaissancepar l'autre Partie contractante de titres aux fins de l'exercice d'une profession.

3. En ce qui concerne les personnes A charge qui exercent une activit6 r6mu-n6r6e au sens du pr6sent Accord, est levde A titre irr6vocable l'immunit6 de juridic-tion civile et administrative pour toutes les questions d6coulant de l'activitd con-sid6rde. Au cas oii une personne charge entendue au sens du pr6sent Accord et quib6n6ficierait de l'immunit6 de juridiction p6nale conform6ment A la Convention deVienne sur les relations diplomatiques' serait accus6e d'une infraction commise enrapport avec son activit6, l'Etat accr6ditant examinera attentivement toute demande6crite de renonciation A cette immunit6.

4. Les personnes A charge qui exercent une activit6 r6munre au sens dupr6sent Accord cesseront d'8tre exemptdes des obligations fiscales et des obliga-tions de pr6voyance sociale d6coulant de l'activit6 consid6r6e et seront, en con-s6quence, assujetties A la l6gislation applicable aux personnes physiques r6sidant oudomicili6es dans l'Etat d'accueil.

5. L'autorisation donn6e A une personne A charge d'exercer une activit6 r6mu-n6r6e cessera lorsque l'agent diplomatique, fonctionnaire ou employ6 consulaire oumembre du personnel administratif et technique qui est A la source de la qualifica-tion de personne A charge cesse ses fonctions aupr~s du gouvernement accr6ditaire.

Article IV

1. Chaque Partie contractante notifiera A l'autre Partie contractante l'accom-plissement des formalit6s 16gales internes requises aux fins de 1'entr6e en vigueur duprdsent Accord, laquelle interviendra A la date de la derni~re notification.

2. Le pr6sent Accord restera en vigueur pendant six ans et sera renouvelablepar tacite reconduction pour une dur6e d'un an A la fois, A moins que l'une desParties manifeste, par la voie diplomatique, son intention de le d6noncer. En pareilcas, la d6nonciation prendra effet six mois apr~s la r6ception de la notification cor-respondante.

I Nations Unies, Recueji des Traitds, vol. 500, p. 95.

Vol. 1908, 1-32511

1996 United Nations - Treaty Series * Nations Unies - Recueil des Traitis 15

FAIT A Brasflia le 22 juin 1993, en deux originaux, en langues portugaise etespagnole, les deux textes faisant 6galement foi.

Pour le Gouvemementde la Rpublique f6d6rative du Br6sil:

Le Ministre d'Etataux relations int6rieures et ext6rieures,

Luiz FELIPE PALMEIRA LAMPREIA

Pour le Gouvemementde la R6publique de l'Equateur:

L'Ambassadeur extraordinaire et pl6ni-potentiaire aupr~s du Gouvemementde la R6publique f6d6rative du Br6sil,

JUAN MANUEL AGUIRRE

Vol. 1908. 1-32511

No. 32512

BRAZIL

andROMANIA

Agreement on trade and economic cooperation. Signed atBrasilia on 23 February 1994

Authentic texts: Portuguese and Romanian.

Registered by Brazil on 1 February 1996.

BRESILet

ROUMANIE

Accord de commerce et de cooperation economique. Signe iBrasflia le 23 fkvrier 1994

Textes authentiques : portugais et roumain.

Enregistri par le Brsil le lerf~vrier 1996.

Vol. 1908, 1-32512

18 United Nations - Treaty Series * Nations Unies - Recueil des Traitis 1996

[PORTUGUESE TEXT - TEXTE PORTUGAIS]

ACORDO DE COMtRCIO E COOPERACAO ECONOMICA ENTRE0 GOVERNO DA REPfJBLICA FEDERATIVA DO BRASIL E 0GOVERNO DA ROMtNIA

O (overno da Repblica Federativa do Brasil

O Governo da RomCnia(doravante denominados "Partes Contratantes"),

Desejando expandir e fortalecer os vinculos comercials e acooperac¢o r'conSmica entre os dois paises, com base nos principios daigualdade soberana dos Estados e da reciprocidade;

Considerando nas relaC es comerciais bilaterais os principiose as regras do GATT do qual ambos os paises s~o Partes Contratantes;

Corn o objetivo primordial de intensificar as rela;6esbilaterais cm bases mutuamente vantajosas,

Acordam o sequinte:

ArTIGO 1

] As Partes Contratantes fomentargo e facilitarao adesenvo]vimento do intercrmbio comercial e da cooperac o econamica

bilateral em conformidade corn o presente Acordo e corn as disposicves

legais internas em vigor em ambos os paises.

2. Os setores nos quais a cooperaggo econ6mica bilateral podergser desenvolvida sao, entre outros: indistria alimenticia, m5quinas eequipamentos, ind6stria de madeira e construg5es, ind(istria quimlca,siderurgia, mineraco, transportes e comunicag6es, eletrrnica e

eletrot~cnica, energia, bens de consumo, finanqas e bancos.

Vol. 1908, 1-32512

1996 United Nations - Treaty Series & Nations Unies - Recueil des Trait6s 19

ARTIGO II

1. As Partes Contratantes conceder-se-Ro reciprocamente otratamento de nac7o mais favorecida segundo as regras do GATT, em todos

os assuntos concernentes ao interc5mbio comercial.

2. Quaisquer vantagens, facilidades, franqulas e privilgios

concedidos pelas Partes Contratantes com relaqio 5 importaco ou

exportac5o de produtos procedentes ou enviados ao territ6rio de um

terceiro pais ser5o imediata e incondicionalmente aplicados a produto

anilogo procedente do, ou enviado ao territ6rio de qualquer da Partes

Contratantes.

ARTIGO III

As disposiq6es do Artigo II n5o serio aplicadas 5s vantagens,

facilidades, privilgios e franquias que uma das Partes Contratantes

concede ou venha a conceder:

a) aos palses limitrofes, com vistas a facilitar o trinsito

flas fronteiras e/ou a cooperaco com as zonas

fronteiriqas;

b) a terceiros paises, em raz~o de sua participaq o em zonade livre comrrcio, uni5o aduaneira ou acordo de integracio

ncon8mica do qual seja membro;

c) a terceiros paises, com base em acordos para evitar a

dupla tributaC5o, em acordos multilaterais de que a outra

Parte Contratante n~o participe, em acordos de cooperaqio

que, segundo a IegislaCio nacional da Parte Contratante

prevejam isenq6es s6 concedidas em decorrincia de atosinternacionais que contiverem clausulas expressas

conteinplando esses beneficios;

d) A importacao de mercadorias em virtude de programas de

ajuda em favor de uma das Partes Contratantes, fornecida

por terceiros paises ou por instituic6es, organismos ou

qucilquer outra organizacio internacional.

Vol. 1908, 1-32512

20 United Nations - Treaty Series * Nations Unies - Recuei des Traitis 1996

ARTiGO IV

No Smbito do intercimbio bilateral, as Partes Contratantes

procurar~o aplicar as preferencias alfandeggrias acordadas no quadro do

Sistema Global de Prefer~ncias Comerciais entre Palses em

Desenvolvimento e do Protocolo Relativo 5s Negociac6es Comerciais entre

Palses cm |)eenvolvimento do GATT.

ARTIGO V

Os contratos especificos de irnportaC5o e exportavao

concluidos ao amparo do presente Acordo serio negociados diretamente

entre emprosas dos dois palses com base nos preqos mundiais dos

respectivos; produtos.

ARTIGO VI

Os pagamentos resultantes dos contratos concluldos ao amparo

do presente Acordo serio efetuados em divisas livremente conversiveis e

em conformidade com o regime cambial vigente em cada pals.

ARTIGO VII

Os produtos comercializados com base em contratos concluldos

ao amparo do presente Acordo somente poder~o ser reexportados para

terceiros palsos coin o consentimento expresso da empresa exportadora.

ARTIGO VIII

Com o prop6sito de promover e implementar os objetivos do

presente Acordo, as Partes Contratantes apoiar5o e facilitarao:

a) o fortalecimento dos contatos e dos lagos entre os agentes

econ8micos, especialistas e t6cnicos em variados setores

(In atividade de ambos os paises, inclusive com a criacio

d-" cmaras de comrcio brasileiro-romenas, de forma a

estimular o crescimento do comnrcio bilateral; com tal

Vol. 1908, 1-32512

1996 United Nations - Treaty Series * Nations Unies - Recueil des Traitis 21

objetivo, as autoridades competentes de ambos os paises

divulgar~o o presente Acordo e garantirio que o mesmo seja

posto A disposiqvo de todos os agentes econ~mncos

interessados;

b) a organizacqo de promoC6es de car~ter comercial, tais como

fciras, exposiqFes, miss~es comerciais, semingrios e

confer ,cias, e outras, no terr t6rio de ambos os paises,

bem como a participacio dos agentes econ6micos nessas

promoc6es;

c) a instalaq3o no territ6rio de ambos os palses de

representac~es comerciais dos agentes econ6micos da outra

Parte Contratante e a concessio de tratamento

ti5o-discriminat6rio em relacgo 5s representacqes de

agentes econ~micos de terceiros paises no que diz respeito

as suas atividades;

d) a troca de informacbes de caterer nio-confidencial entre

as autoridades competentes e os agentes econrmicos de

ambos os palses a respeito das leis, regulamentos e

procedimentos administrativos relacionados com o comfircio

exterior, investimentos, impostos e taxas, atividade

hancfirla, seguros e demals serviqos financeiros e de

transporte, bem como referentes aos programas e diretrizes

de desenvolvimento econimico, as possibilidades de

inportaqio e exportaqio entre ambos os paises, inclusive

as concorrincias e licitaq8es a serem organizadas em ambos

ns paises;

) a participacio mais intensa das pequenas e midias empresas

na troca de mercadorias e servicos entre ambos os palses,

tio ambito do presente Acordo.

Vol. 1908. 1-32512

22 United Nations - Treaty Series * Nations Unies - Recueil des Traitks 1996

ARTIGO IX

1. As Partes Contratantes, em conformidade com suas leis e

regulamentos internos, isentar5o de direitos aduaneiros os seguintes

bens:

i) material para teste ou pesquisa;

ii) amostras sem valor comercial e material publicitirio;

iii) bens que foram objeto de reparo ou que foram

substituldos, assim como suas pecas sobressalentes,

dentro do seu periodo de garantia;

iv) donativos de cariter humanit~rio, cultural e esportivo.

2. Os bens e produtos acima mencionados n~o podergo ser

coniercializados, nem aproveitados por terceiros com fins lucrativos.

ARTIGO X

Cada Parte Contratante concedera, em conformidade com suas

leis e regulamentos, facilidades de tr~nsito em seu terrlt6rio ismercadorias origin5rias do territ6rio do outro pals e destinadas aterceiros paises, assim como As mercadorias origin~rias de terceiros

paises coin d.stino A outra Parte Contratante.

ARTIGO XI

1. Con o prop6sito de assegurar a implementaco do presente

Acordo, as Partes Contratantes concordam em dar continuidade 5 Comissio

Mista bilateral, a reunir-se alternadamente em Brasilia e Bucareste,

por solicitacSo de uma das Partes, em datas a serem mutuamente

acordadas.

2. A Comiss5o Mista procurari abordar sobretudo temas que

conduzam ao fortalecimento e ao aprofundamento das relac5es bilaterais,

especialmente no 5mbito da coopera~go comercial e econ~mica.

3. An Partes Contratantes estimular~o a participacio derepresetoitter governamentais e de agentes econ~micos de ambos os

paises na Comissio Mista, cuja chefia serS fle nivel condizente.

Vol. 1908, 1-32512

1996 United Nations - Treaty Series * Nations Unies - Recueil des Traitks 23

ARTIGO XII

As Partes Contratantes designam como 6rg~os encarregados da

exectic5o do prosente Acordo, pela Rep6blica Federativa do Brasil, 0f inistrio das Relac5es Exteriores e, pela Romnia, o Ministgrio do

Com6rcio.

ARTIGO XIII

1. As controversias que possam surgir a respeito dainterpretac~o ou aplicac~o do presente Acordo ser~o solucionadas

mediant- consultas diretas entre os 6rg~os mencionados no Artigo XII,por via ,Iiplor,, tica ou no 5mbito da Comiss~o Mista, mencionada no

Artiqo XI do presente Acordo.

2. As controv~rsias que possam surgir a respeito do cumprimentodos contratos, concluidos ao amparo do presente Acordo, serao

solucionadas segundo as disposiC6es contratuais especificas previstasnos respectivos contratos e/ou conforme a legislaCAo aplicivel.

AWI'IGO XIV

As disposic~es do presente Acordo tamb~m serio aplicaveis aoscontratos concluidos durante sua vig6ncia e cumpridos ap6s sua

expiracio.

ARTIGO XV

O presente Acordo ser vilido por um periodo de 5 Icinco)anos e serg automaticamente prorrogado por perlodos sucessivos de 3(tris) anos, a menos que uma das Partes Contratantes comunique A outra,por escrito e por via diplomitica, sua intenqio de denunciA-lo, comantecedgncia de 90 (noventa) dias em relaqio 5 data prevista para sua

expiragio.

ARTIGO XVI

O presente Acordo entrarS em vigor 30 (trinta) dias ap6s a

data do recebimento da 61tima notificacio a respeito do cumprimento dasformalidades internas para sua aprovaCio.

Vol. 1908, 1-32512

24 United Nations - Treaty Series e Nations Unies - Recueil des Trait6s 1996

ARIIGO XVII

1. Ao entrar em vigor, 0 presente Acordo substituirS o Acordo de

Com~rcio e Pagamentos assinado entre os Governos dos dois paises em

Brasilia, em 05 de julhol de 1975.

2. 0 Banco Central do Brasil e as autoridades financeiras e

banc5rias da Romania adotar~o as provid~ncias clue se fizerem

necess5rias para o t~rmino da conta em moeda-convenio prevista no acina

referido Acordo de Comnrcio e Pagamentos.

Feito em Brasilia, em

exemplares originais, nas linguas

textos igualmente autgnticos.

Pelo Govemoda Repdblica Federativa do Brasil:

ROBERTO ABDENURMinistro de Estado, interino,

das Relaq6es Exteriores

23 de fevereiro de 1994, em dois

portuguesa e romena, sendo ambos os

Pelo Govemoda Romania:

CRISTIAN IONESCUMinistro de Com6rcio

I Should read June - Debrait se lire juin.

Vol. 1908, 1-32512

1996 United Nations - Treaty Series * Nations Unies - Recueil des Traits 25

[ROMANIAN TEXT - TEXTE ROUMAIN]

ACORD DE COMERT SI COOPERARE ECONOMICA NITRE GUVER-NUL REPUBLICII FEDERATIVE A BRAZILIEI SI GUVERNULROMANIEI

Guvernul Republicli Federative a BrazillelsiGuvernul Rominlel( In continuare denumite" PArti Contractante ')

Dorind sa lrgeascA si sA tntareasca legaturile comerciale si de cooperareeconomica ITnte cele doua tai, pe baza pnncipiilor egalitabi suverane a statelor si alreciprocitatbi,

LuAnd In considerare, In relatiile comerciale bilaterale, principiile si regulileGATT, la care ambele tai sunt pirti contractante,

Cu obiectivul primordial de a iniensifica relaliile bilaterale pe baze reciprocavantajoase,

Au convenit urmatoarele:

ARTICOLUL I1. Partile Contractante vor Incuraja si facilita dezvoltarea schimburilor

comerciale si a cooperarii economice bilaterale In conformitate cu prezentul Acord sicu reglementaile legale In vigoare In cele doua tai.

2- Sectoarele In care cooperarea economica bilaterali s-ar putea dezvoltasunt, Intre altele, urmtoarele : industria alimentara, masini si echipamente, industrialemnului si a constructiilor, industria chimicA si petrochimica, siderurgia, minerit,transport si comunicali, electronica si electrotehnica, energie, bunuri de consum,finante si bnci.

ARTICOLUL II1. PArtlle Contractante Isi vor acorda reciproc tratamentul natiunii celei mai

favorizate, potrivit regulilor GATT, In toate problemele care privesc schimburilecomerciale.

2. Once fel de avantaje, facilitti, scutiri si pdivilegii acordate de catre PartileContractante cu privire la importul sau exportul de produse provenind din sau livrateIn teritonul unei terte tari vor fi apilcate imediat si neconditionat produselor analoageprovenind din sau livrate In tentoriul oricireia din Pirtlie Contractante.

Vol. 1908, 1-32512

26 United Nations - Treaty Series e Nations Unies - Recueil des Trait6s 1996

ARTICOLUL III1. Prevederile Articolului I nu vor fi aplicate la avanlajele, facilitatile, privilegiile

si scutirile pe care una din Partile Contractante le acorda sau le va acorda:a) tarilor limitrofe, cu scopul de a facilita tranzitul de frontiera si/sau

cooperarea In zonele de frontiera ;b) tarilor terte, ca urmare a participarii sale la o zona de comert liber, uniune

vamala sau [a un acord de integrare economica la care este membru;c) tarilor terte, potrivit acordurilor pentru evitarea dublei impuneri, acordunlor

multilaterale [a care cealalta Parte ContractantA nu participa, acordurilor decooperare care, conform legislafiei interne a Pirtil Contractante, prevad scutriacordate numai ca urmare a actelor intemationale care contin clauze exprese cupnvire la aceste avantaje ;

d) la importul marfurilor in cadrul programelor de ajutor In favoarea uneia dinPirtlle Contractante, fumizate de terte tri sau de insttutii, organisme sau once altaorganizatie intemationali.

ARTICOLUL IVIn schimburile comerciale bilaterale, Partlle Contractante vor aplica

prefedintele vamale convenite Tn cadrul Sistemului Global de Preferinte ComercialeIntre Tgrile In Curs de Dezvoltare si a Prolocolului privind negocieiie comerciale intretaile In curs de dezvoltare din GATT.

ARTICOLUL VContractele specifice de import si export ncheiate In baza prezentului Acord

vor fi negociate direct Intre firmele din cele doui taid pe baza preturilor mondiale laprodusele respective.

ARTICOLUL VIPlatile Tn cadrul contractelor ncheiate In baza prezentului Acord se vor

efectua In devize liber convertibile si In conformitate cu regimul valutar in vigoare infiecare tarn.

ARTICOLUL VIIProdusele comercializate Tn baza contractelor Tncheiate In cadrul prezentului

Acord vor putea fi reexportate In terte tai numai cu consimtamantul expres alTntreprinderii exportatoare.

ARTICOLUL VIiiIn scopul promovdrii si implementrii obiectivelor prezentuiui Acord, P.rtile

Contractante vor sprijini si facilita :

Vol. 1908, 1-32512

1996 United Nations - Treaty Series * Nations Unies - Recueil des Trait6s 27

a) intensificarea contactelor si legaturilor intre agentii economici, specialisti sitehnicieni din diverse sectoare de activitate din cele doua tad, inclusiv prin lnfiintareade Camere de comert braziliano-romane, astfel Incat sa fie stimulat comertul bilateral ;avand In vedere acest obiectiv, autoritatile competente din cele doua tari vor facecunoscut prezentul Acord si vor garanta punerea lui la dispozilia tuturor agentiloreconomici interesati ;

b) organizarea de actiuni promotionale cum sunt targurile, expozitiile, misiunilecomerciale, seminarii, conferinte si altele, In ambele tad, ca si paruciparea agentiloreconomici la astfel de actiuni ;

c) instalarea, pe teritoriul celor doua tari, de reprezentante comerciale aleagentilor economlci al celeilalte Partl Contractante si acordarea unui tratamentnediscriminatoru fata de reprezentantele agentilor economici din terte tarl In cepriveste activitatile lor;

d) schimbul de informai cu caracter neconfidential inlre autoritatilecompetente si agentii economici din ambele tar! cu privire [a legile, reglementarile siprocedurile administrative legate de comertul exterior, investitii, impozite sitaxe,activitate bancara, asigurari si alte servicii financiare si de transport, ca si celereferitoare la programele si orientanle de dezvoltare economica, la posibilitatile deimport si export Intre ambele tari, inclusiv la licitatiile internationale ce se vor organiza Incele doua tari;

e) participarea mai intensd a Tntreprinderilor mici si rnijlocii la schimbul demarfuri si servicii Intre cele doua tari, In cadrul prezentului Acord.

ARTICOLUL IX1. PArtlle Contractante, In confonnitate cu legile si reglernentarile lor

interne, vor scuti de taxe vamale urmatoarele bunuri :

I) materiale pentru Incercad sau cercetare;II) mostre fara valoare comerciala si material publicitar;iii) bunui care au facut obiectul unor reparatii sau care au fost