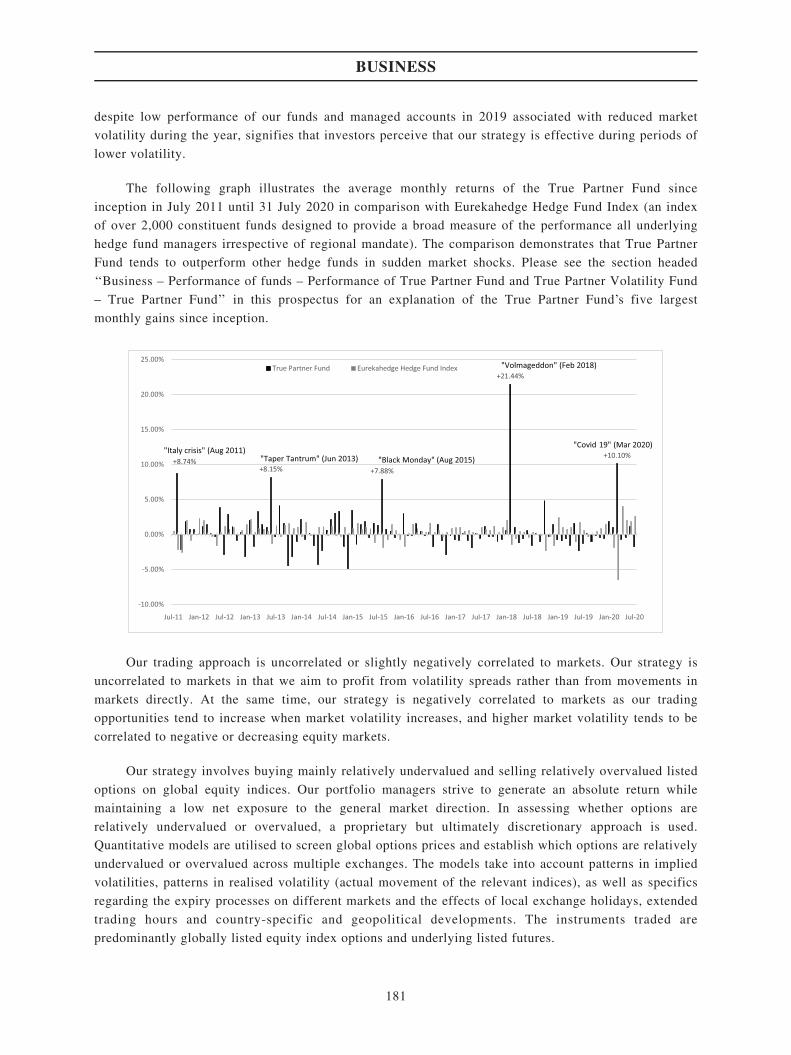

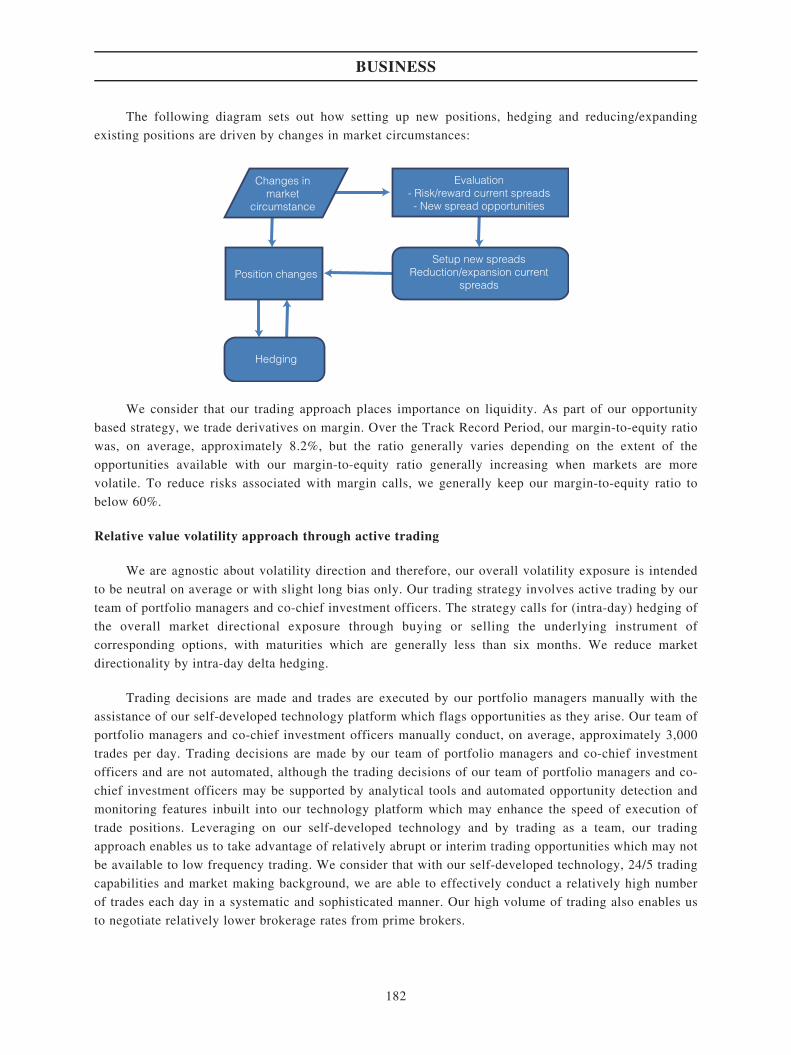

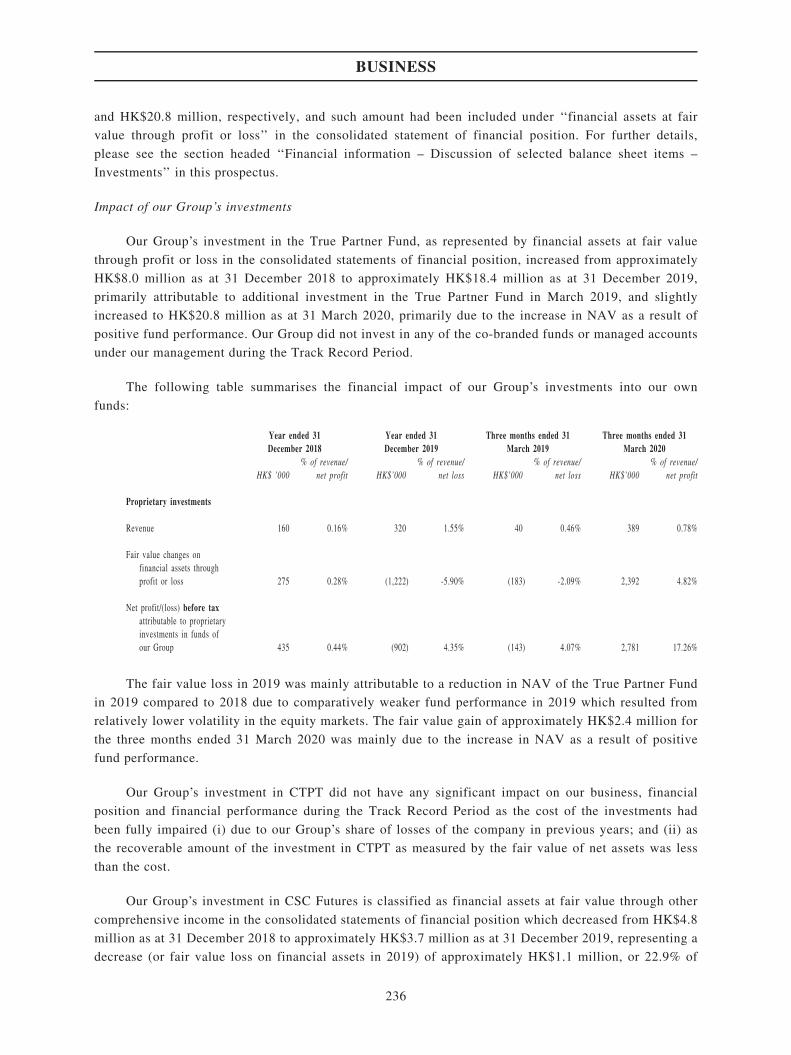

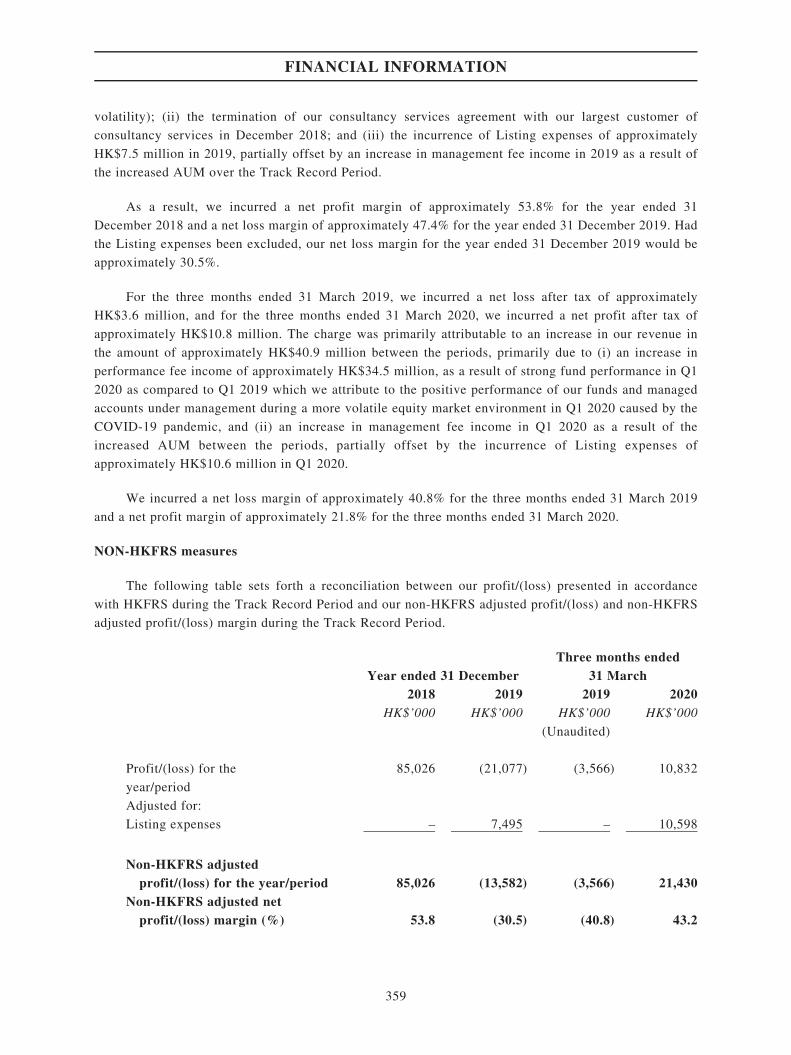

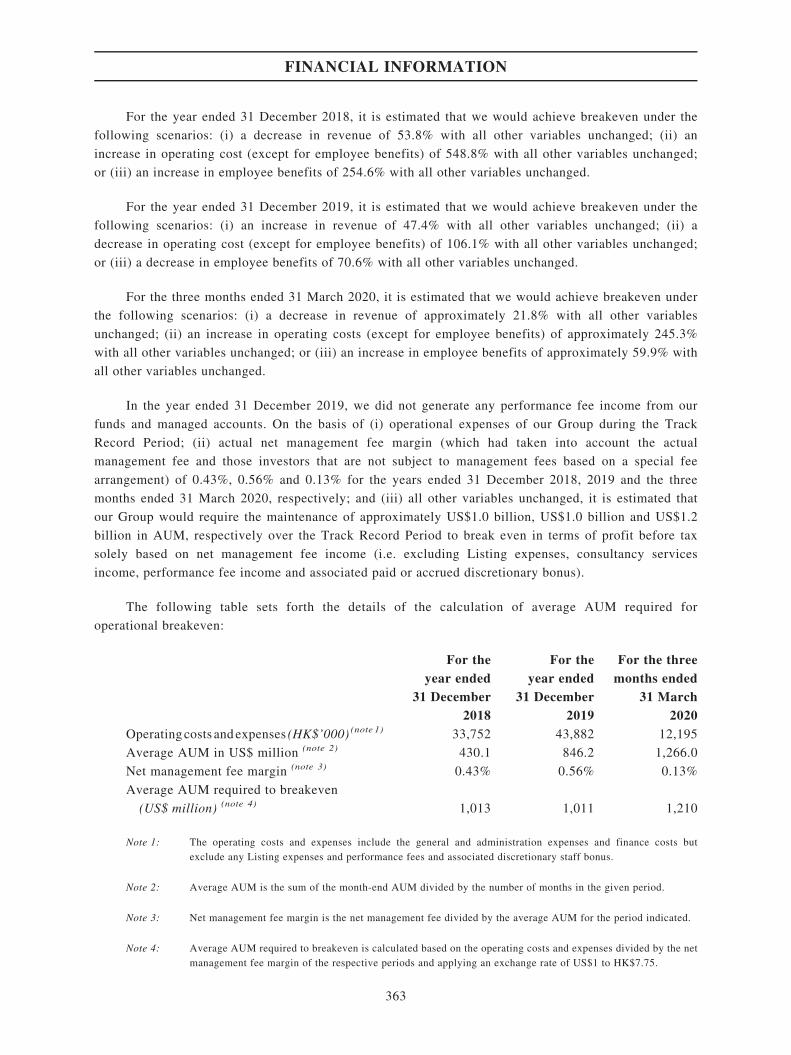

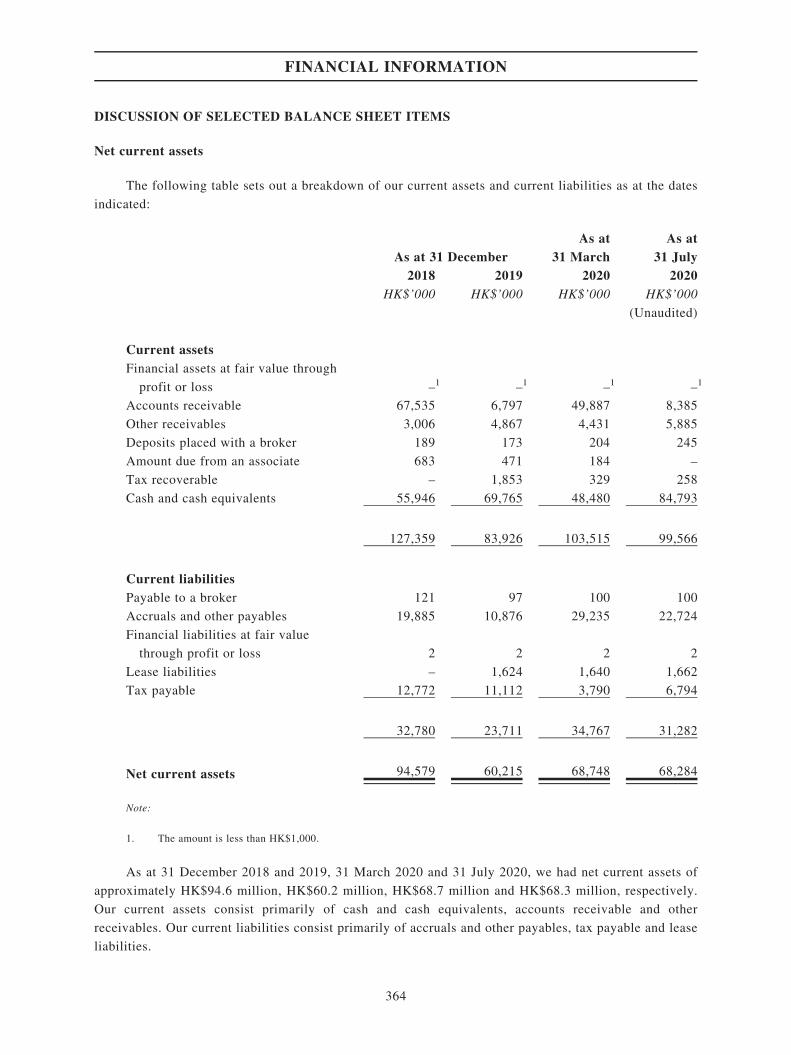

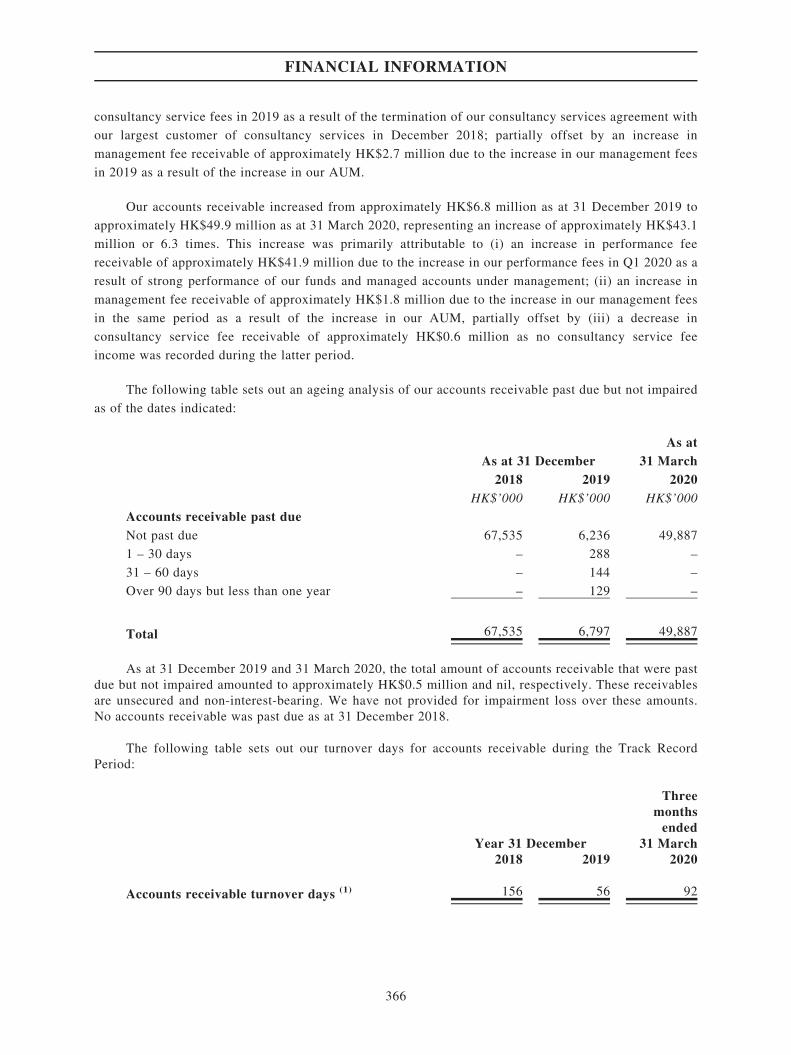

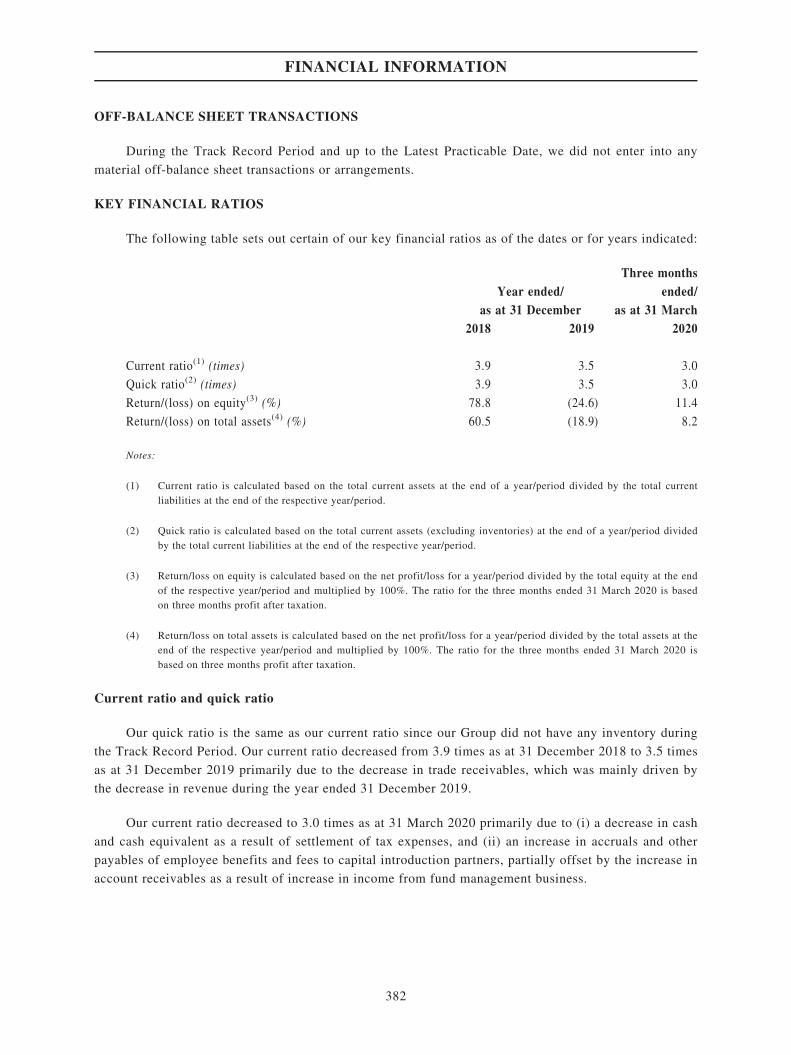

Embed Size (px)

Citation preview

(Incorporated under the laws of the Cayman Islands with limited liability)

Stock code : 8657

SHARE OFFER

TRUE PARTNER CAPITAL HOLDING LIMITED

Sole Sponsor

Joint Bookrunners

Joint Lead Managers

Securities Ltd.佳富達證券

IMPORTANT: If you are in any doubt about any of the contents of this prospectus, you should obtain independent professionaladvice.

TRUE PARTNER CAPITAL HOLDING LIMITED(Incorporated under the laws of the Cayman Islands with limited liability)

LISTING ON THE GEM OF THE STOCK EXCHANGE OFHONG KONG LIMITED BY WAY OF

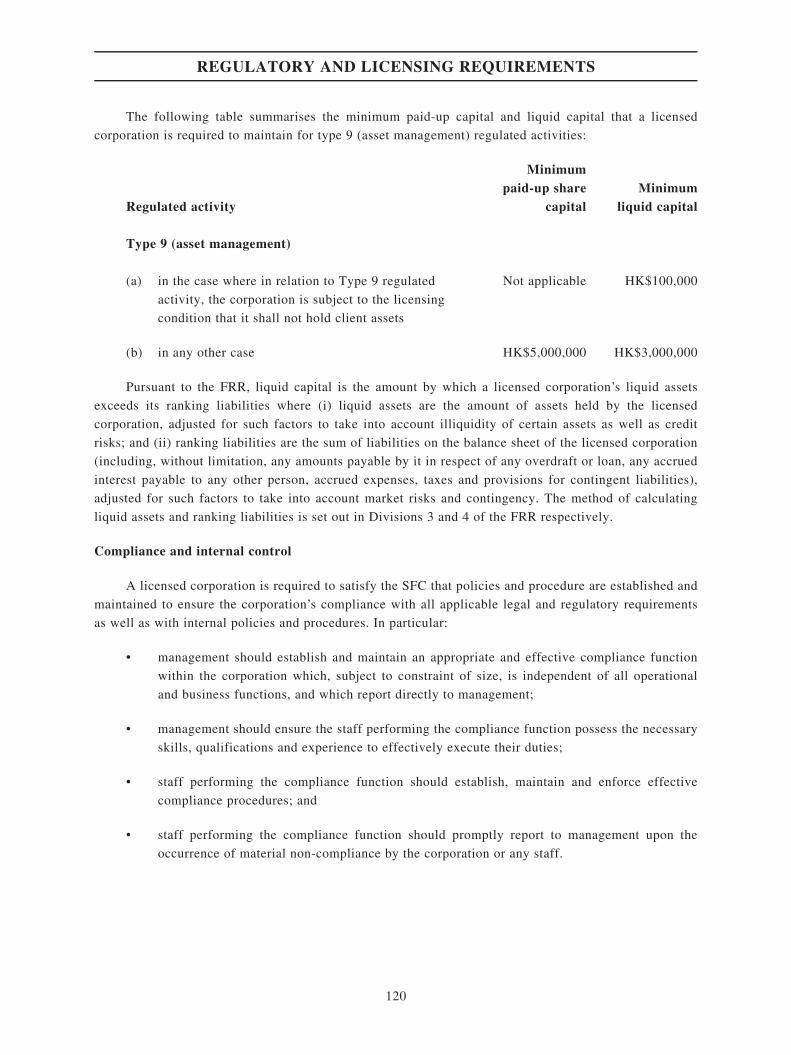

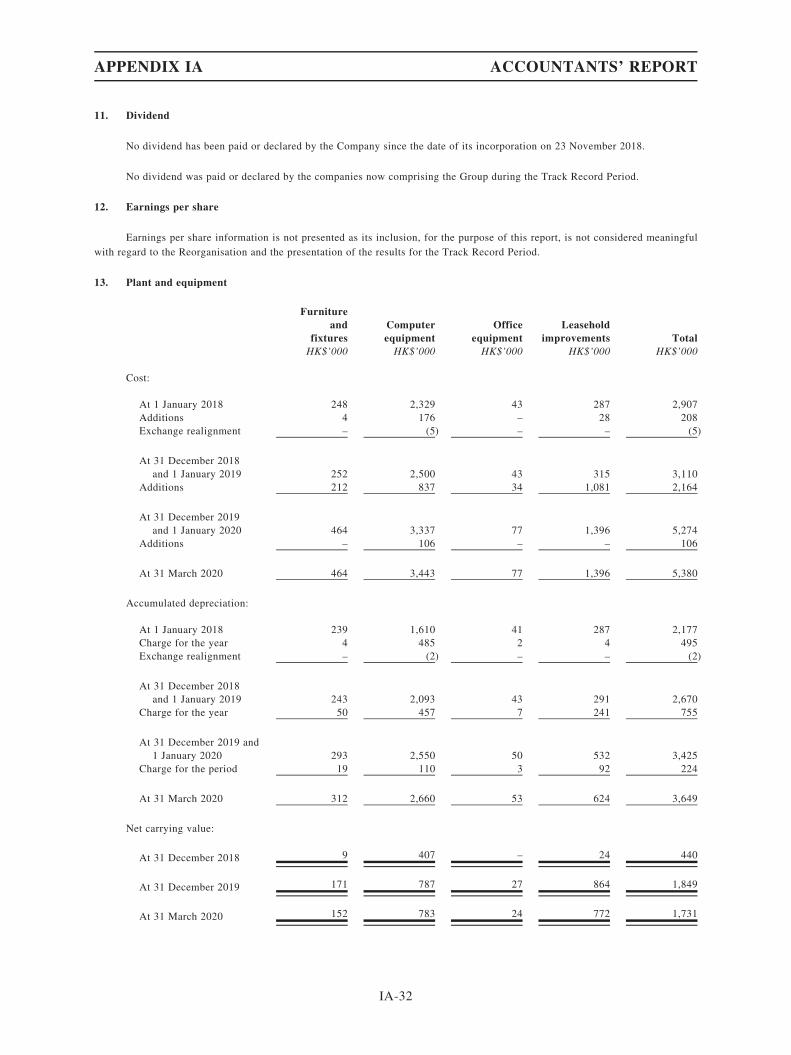

SHARE OFFERNumber of Offer Shares : 100,000,000 Shares (subject to the Offer Size Adjustment

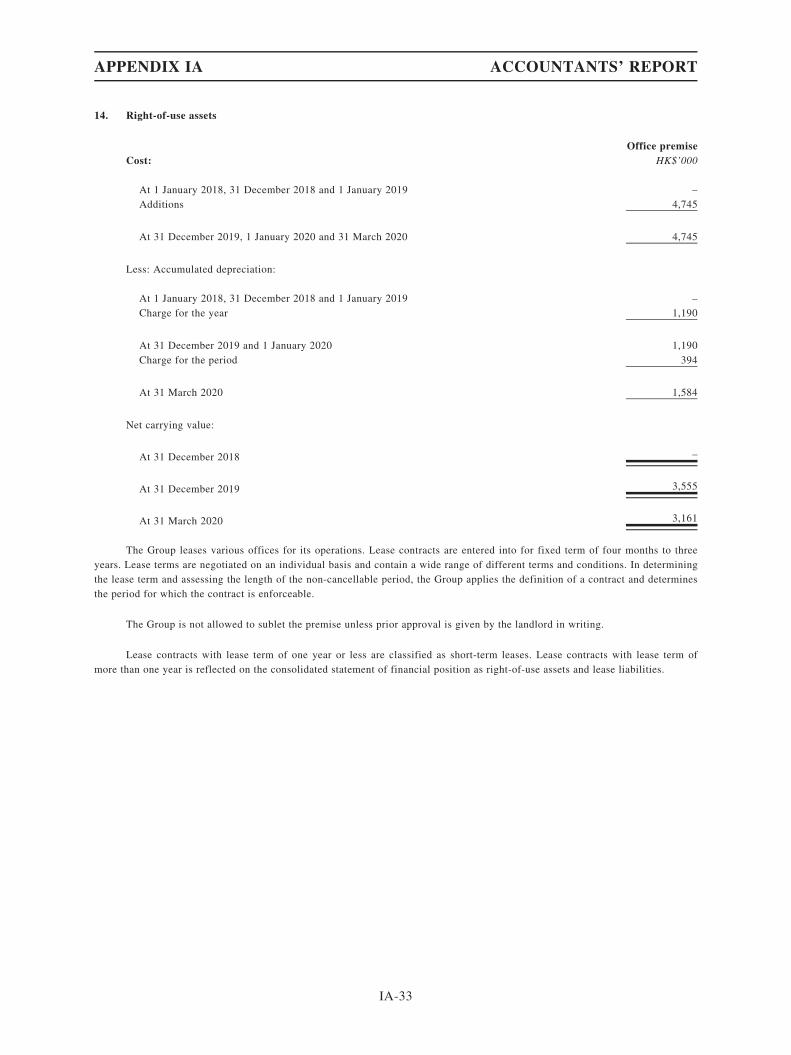

Option)Number of Public Offer Shares : 10,000,000 Shares (subject to re-allocation)

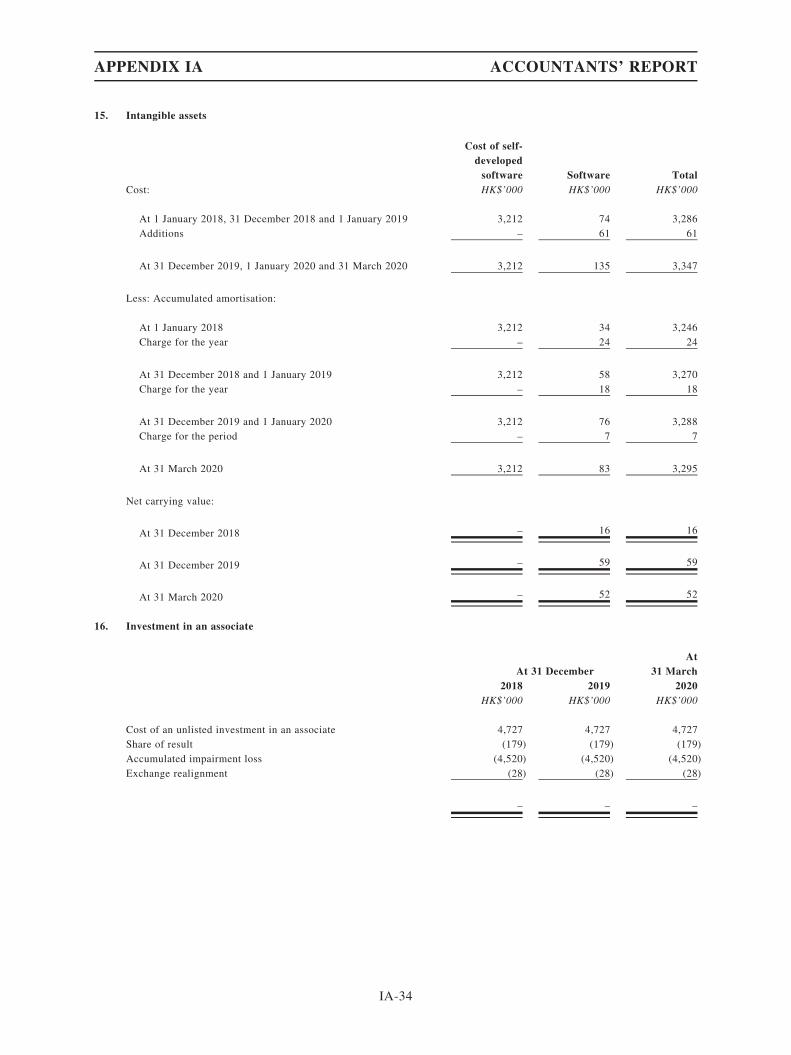

Number of Placing Shares : 90,000,000 Shares (subject to re-allocation and Offer SizeAdjustment Option)

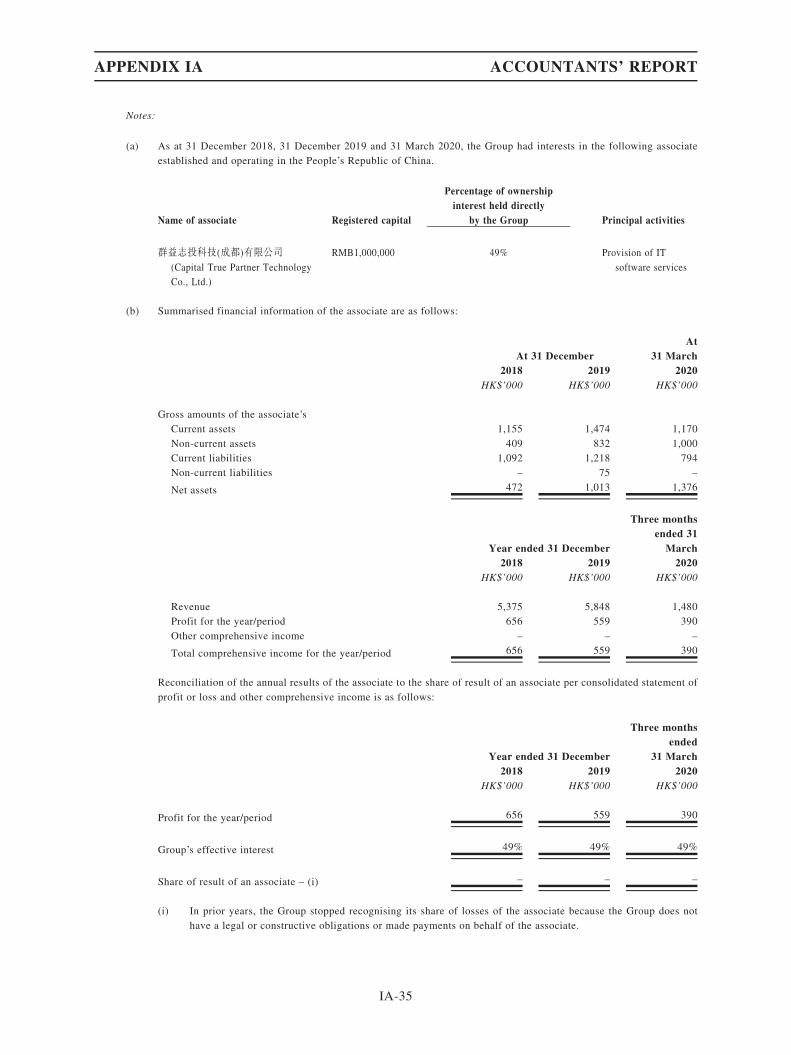

Offer Price(subject to the DownwardOffer Price Adjustment)

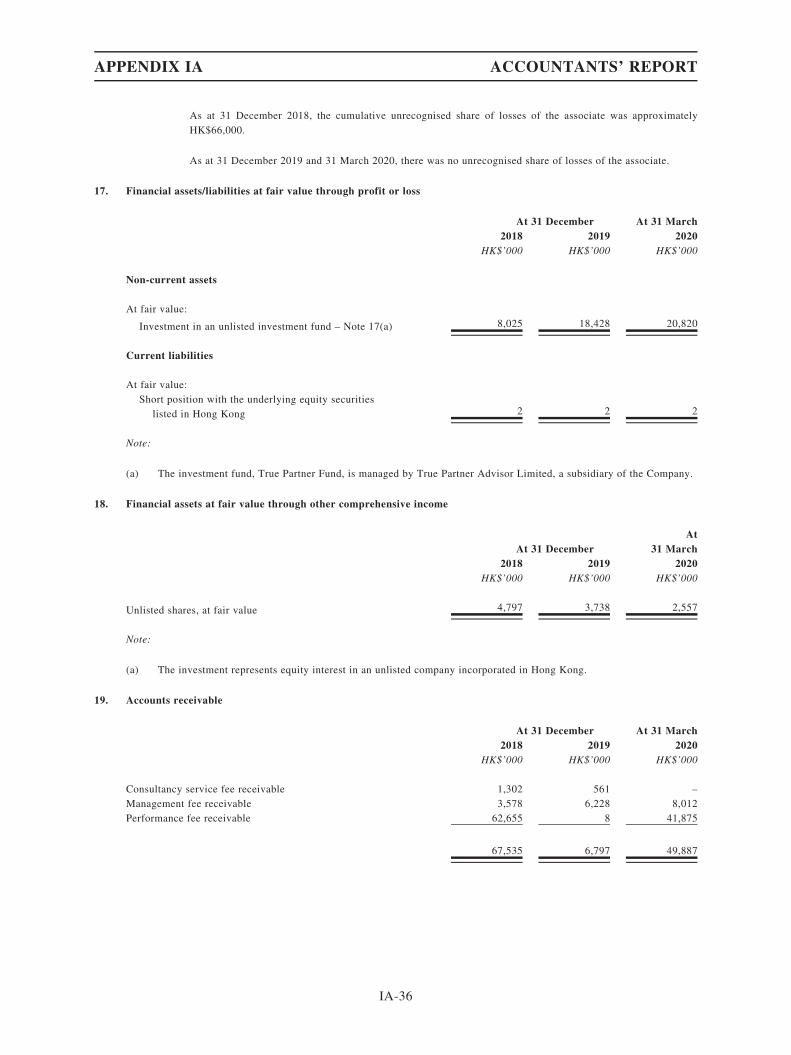

: Not more than HK$1.95 per Offer Share and expected to benot less than HK$1.55 per Offer Share, plus brokerage of1.0%, SFC transaction levy of 0.0027% and Hong KongStock Exchange trading fee of 0.005% (payable in full onapplication in Hong Kong dollars, subject to refund on finalpricing)(If the Offer Price is set at 10% below the bottom end of theindicative Offer Price range after making the Downward OfferPrice Adjustment, the Offer Price will be HK$1.40 per OfferShare)

Nominal value : HK$0.01 per ShareGEM Stock code : 8657

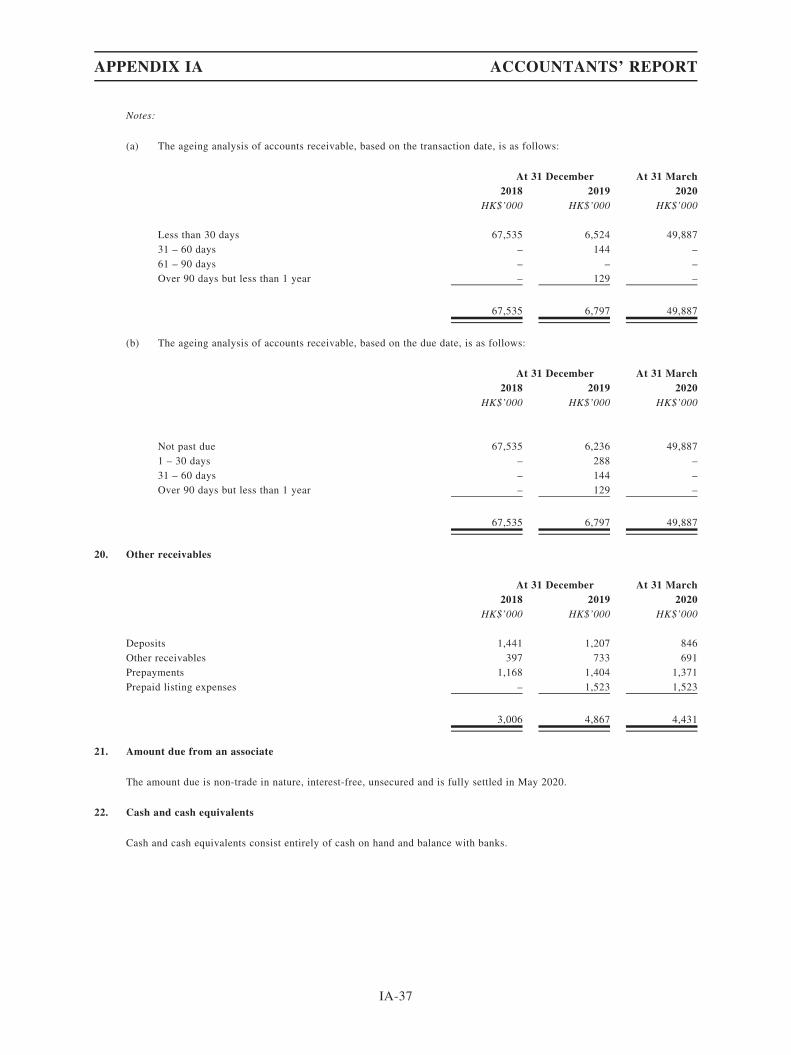

Sole Sponsor

Alliance Capital Partners Limited同 人 融 資 有 限 公 司

Joint Bookrunners

Joint Lead Managers

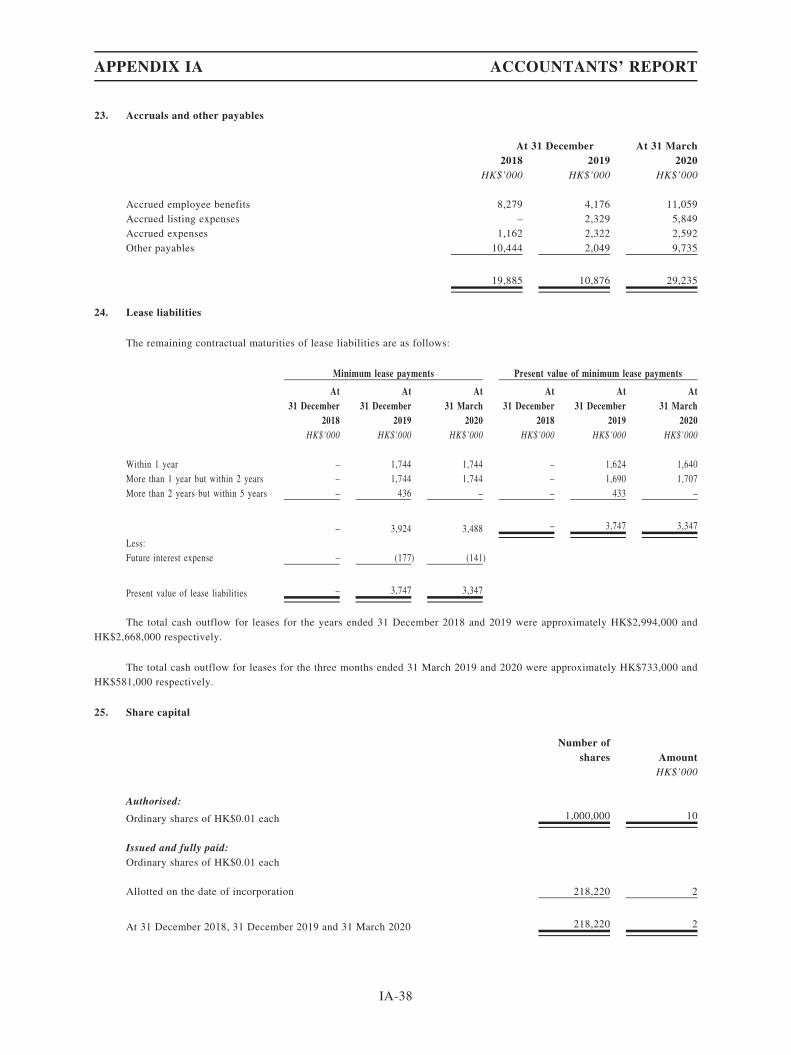

Securities Ltd.佳富達證券

Hong Kong Exchanges and Clearing Limited, The Stock Exchange of Hong Kong Limited and Hong Kong Securities Clearing Company Limited take no responsibility for the contents of thisprospectus, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or anypart of the contents of this prospectus.A copy of this prospectus, having attached thereto the documents specified in the section headed ‘‘Documents Delivered to the Registrar of Companies and Available for Inspection’’ inAppendix V to this prospectus, has been registered by the Registrar of Companies in Hong Kong as required by Section 342C of the Companies (Winding Up and Miscellaneous Provisions)Ordinance (Chapter 32 of the Laws of Hong Kong). The Securities and Futures Commission of Hong Kong and the Registrar of Companies in Hong Kong take no responsibility for the contentsof this prospectus or any of the other documents referred to above.The Offer Price is expected to be fixed by an agreement between our Company and the Joint Bookrunners (for themselves and on behalf of the Underwriters) on the Price Determination Date.The Price Determination Date is expected to be on or around Friday, 9 October 2020 and, in any event, not later than 5:00 p.m. on Saturday, 10 October 2020. The Offer Price will be not morethan HK$1.95 and is currently expected to be not less than HK$1.55 per Offer Share (subject to the Downward Offer Price Adjustment) unless otherwise announced. Applicants for OfferShares are required to pay, on application, the maximum Offer Price of HK$1.95 for each Share together with a brokerage fee of 1%, SFC transaction levy of 0.0027% and Stock Exchangetrading fee of 0.005% subject to refund if the Offer Price as finally determined should be lower than HK$1.95. If, for any reason, the Offer Price is not agreed by Saturday, 10 October 2020between the Company and the Sole Lead Manager (for themselves and on behalf of the Underwriters), the Share Offer will not proceed and will lapse. In the case of such event, a notice will bepublished on the website of the Stock Exchange at www.hkexnews.hk and our Company’s website at www.truepartnercapital.com.The Sole Lead Manager (for itself and on behalf of the Underwriters), may, with our consent, extend or reduce the indicative Offer Price range and/or the number of Offer Shares stated in thisprospectus at any time prior to the morning of the last day for lodging applications under the Public Offer. If this occurs, a notice of the extension or reduction in the indicative Offer Pricerange and/or the number of Offer Shares will be published on the Stock Exchange website at www.hkexnews.hk and the Company’s website at www.truepartnercapital.com not later than themorning of the last day for lodging applications under the Public Offer. Further details are set out in the section headed ‘‘Structure of the Share Offer’’ and ‘‘How to apply for Public OfferShares’’ of this prospectus.Prior to making an investment decision, prospective investors should consider carefully all of the information set out in this prospectus, including but not limited to the risk factors set out inthe section headed ‘‘Risk factors’’ of this prospectus. Prospective investors of the Offer Shares should note that the Joint Bookrunners (for themselves and on behalf of the Underwriters) isentitled to terminate the obligations under the Underwriting Agreements if certain grounds arise prior to 8:00 a.m. on the day that trading in the Offer Shares commences on the StockExchange. Such grounds are set out in the section headed ‘‘Underwriting – Underwriting arrangements and expenses – Grounds for termination’’ in this prospectus. It is important thatprospective investors refer to that section of this prospectus for further details.The Offer Shares have not been and will not be registered under the U.S. Securities Act or any state securities law of the United States and may not be offered, sold, pledged or transferredwithin the United States except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the U.S. Securities Act and the applicable laws of eachjurisdiction where those offers and sales occurs.

ATTENTIONWe have adopted a fully electronic application process for the Public Offer. We will not provide printed copies of this prospectus or printed copies of any application forms tothe public in relation to the Public Offer.

This prospectus is available at the website of the Hong Kong Stock Exchange at www.hkexnews.hk and our website at www.truepartnercapital.com. If you require a printedcopy of this prospectus, you may download and print from the website addresses above.

30 September 2020

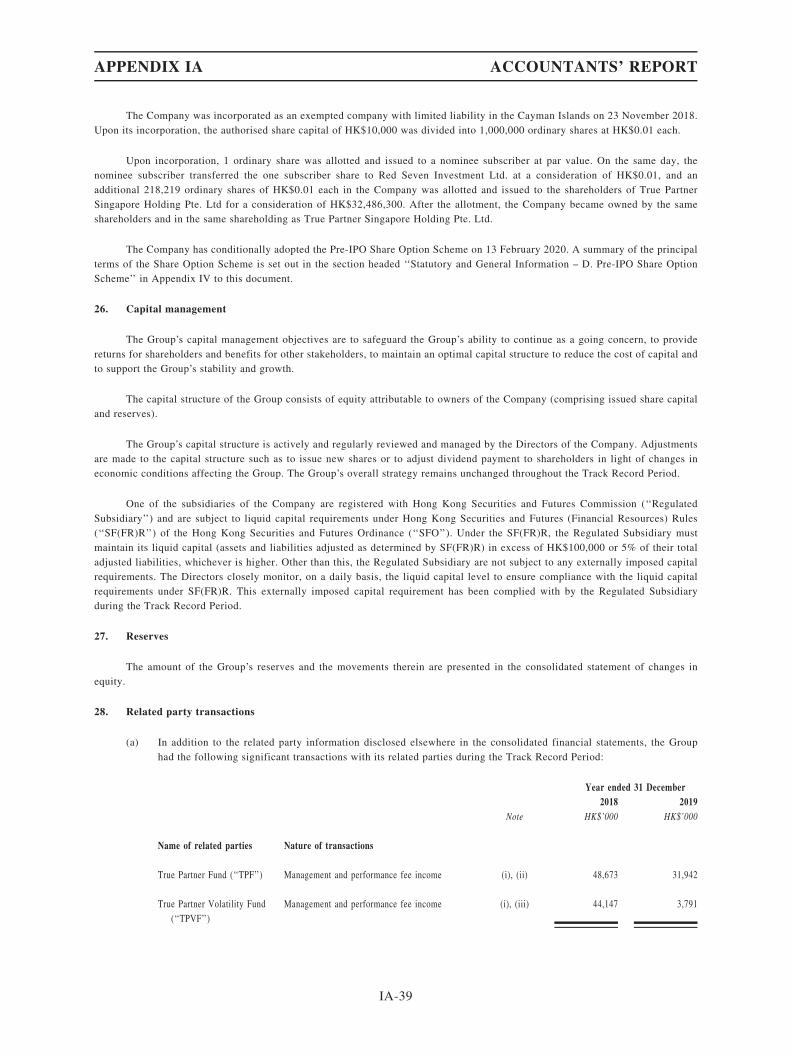

IMPORTANT

IMPORTANT NOTICE TO INVESTORS:FULLY ELECTRONIC APPLICATION PROCESS

We have adopted a fully electronic application process for the Public Offer. We will not provideprinted copies of this document or printed copies of any application forms to the public inrelation to the Public Offer.

This prospectus is available at the website of the Hong Kong Stock Exchange atwww.hkexnews.hk under the ‘‘HKEXnews > New Listings > New Listing Information’’ section andour website at www.truepartnercapital.com. If you require a printed copy of this prospectus, youmay download and print from the website addresses above.

To apply for the Public Offer Shares, you may:

(1) apply online through the HK eIPO White Form service through the IPO App or atwww.hkeipo.hk;

(2) apply through the CCASS EIPO service to electronically cause HKSCC Nominees to apply onyour behalf, including by:

(i) instructing your broker or custodian who is a CCASS Clearing Participant or a CCASSCustodian Participant to give electronic application instructions via CCASS terminals toapply for the Public Offer Shares on your behalf; or

(ii) (if you are an existing CCASS Investor Participant) giving electronic applicationinstructions through the CCASS Internet System (https://ip.ccass.com) or through theCCASS Phone System by calling +852 2979 7888 (using the procedures in HKSCC’s ‘‘AnOperating Guide for Investor Participants’’ in effect from time to time). HKSCC can alsoinput electronic application instructions for CCASS Investor Participants throughHKSCC’s Customer Service Centre at 1/F, One & Two Exchange Square, 8 ConnaughtPlace, Central, Hong Kong by completing an input request.

If you have any question about the application for the Public Offer Shares, you may call the enquiryhotline of our Hong Kong Branch Share Registrar and HK eIPO White Form Service Provider, TricorInvestor Services Limited, both at +852 3907-7333 on the following dates:

Wednesday, 30 September 2020 – 9:00 a.m. to 5:00 p.m.Saturday, 3 October 2020 – 9:00 a.m. to 1:00 p.m.Monday, 5 October 2020 – 9:00 a.m. to 5:00 p.m.Tuesday, 6 October 2020 – 9:00 a.m. to 5:00 p.m.

Wednesday, 7 October 2020 – 9:00 a.m. to 5:00 p.m.Thursday, 8 October 2020 – 9:00 a.m. to 5:00 p.m.

Friday, 9 October 2020 – 9:00 a.m. to 12:00 noon

We will not provide any physical channels to accept any application for the Public Offer Shares by thepublic. The contents of the electronic version of this prospectus are identical to the printed documentas registered with the Registrar of Companies in Hong Kong pursuant to Section 342C of theCompanies (Winding Up and Miscellaneous Provisions) Ordinance.

If you are an intermediary, broker or agent, please remind your customers, clients or principals, asapplicable, that this prospectus is available online at the website addresses above.

Please refer to the section headed ‘‘How to Apply for Public Offer Shares’’ in this prospectus forfurther details on the procedures through which you can apply for the Public Offer Shareselectronically.

IMPORTANT

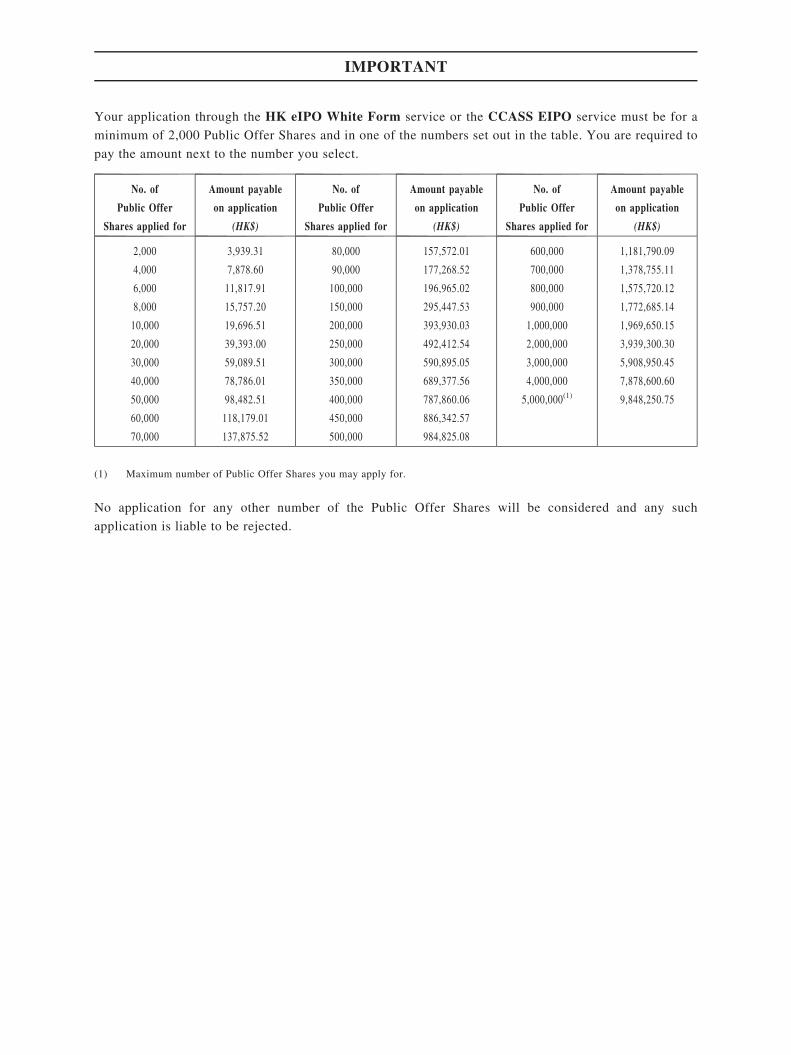

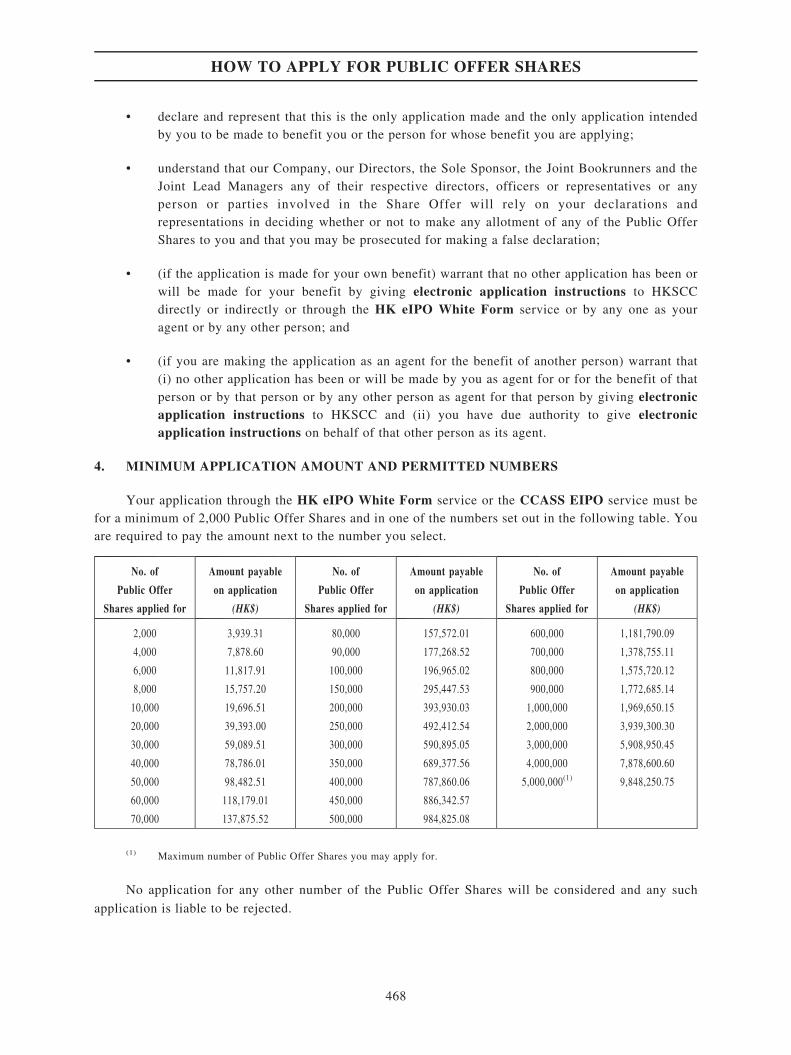

Your application through the HK eIPO White Form service or the CCASS EIPO service must be for a

minimum of 2,000 Public Offer Shares and in one of the numbers set out in the table. You are required to

pay the amount next to the number you select.

No. of

Public Offer

Shares applied for

Amount payable

on application

(HK$)

No. of

Public Offer

Shares applied for

Amount payable

on application

(HK$)

No. of

Public Offer

Shares applied for

Amount payable

on application

(HK$)

2,000

4,000

6,000

8,000

10,000

20,000

30,000

40,000

50,000

60,000

70,000

3,939.31

7,878.60

11,817.91

15,757.20

19,696.51

39,393.00

59,089.51

78,786.01

98,482.51

118,179.01

137,875.52

80,000

90,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

157,572.01

177,268.52

196,965.02

295,447.53

393,930.03

492,412.54

590,895.05

689,377.56

787,860.06

886,342.57

984,825.08

600,000

700,000

800,000

900,000

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000(1)

1,181,790.09

1,378,755.11

1,575,720.12

1,772,685.14

1,969,650.15

3,939,300.30

5,908,950.45

7,878,600.60

9,848,250.75

(1) Maximum number of Public Offer Shares you may apply for.

No application for any other number of the Public Offer Shares will be considered and any such

application is liable to be rejected.

IMPORTANT

GEM has been positioned as a market designed to accommodate companies to which ahigher investment risk may be attached than other companies listed on the Stock Exchange.Prospective investors should be aware of the potential risks of investing in such companies andshould make the decision to invest only after due and careful consideration. The greater riskprofile and other characteristics of GEM mean that it is a market more suited to professionaland other sophisticated investors.

Given the emerging nature of companies listed on GEM, there is a risk that securitiestraded on GEM may be more susceptible to high market volatility than securities traded on theMain Board and no assurance is given that there will be a liquid market in the securities tradedon GEM.

The principal means of information dissemination on GEM is by publication on the Internetwebsite operated by the Stock Exchange. Listed companies are not generally required to issuepaid announcements in gazetted newspaper. Accordingly, prospective investors should note thatthey need to have access to the Stock Exchange’s website at www.hkexnews.hk in order to obtainup-to-date information on companies listed on GEM.

CHARACTERISTICS OF GEM

i

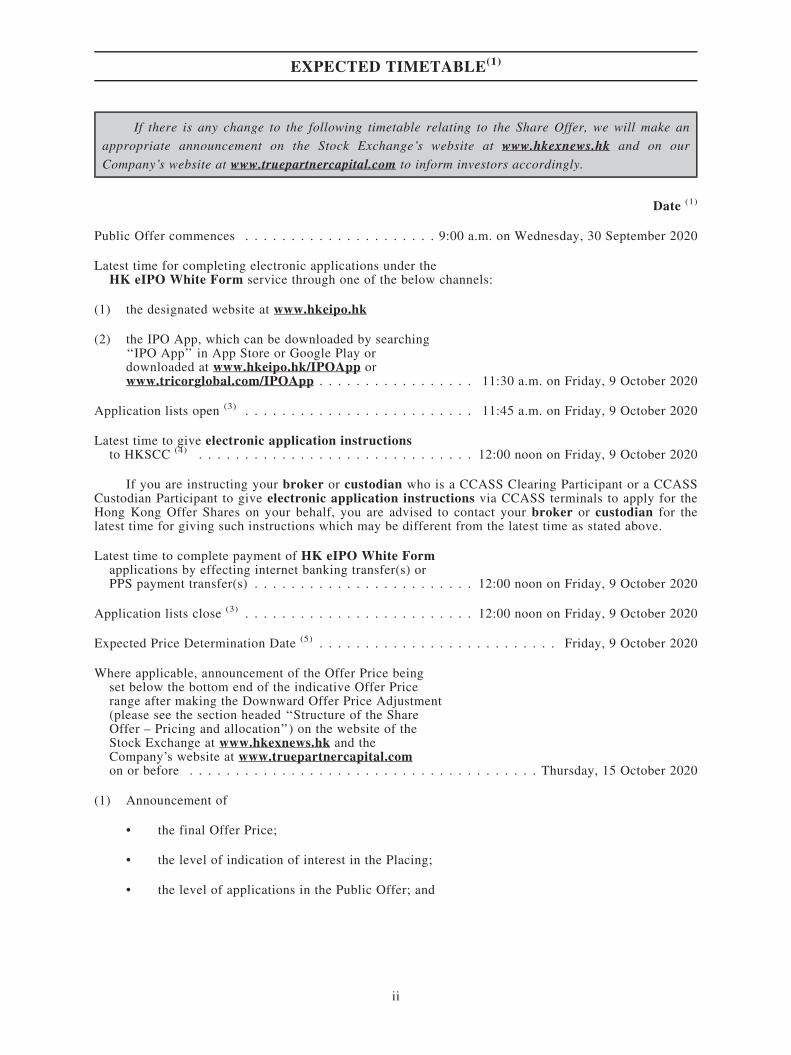

If there is any change to the following timetable relating to the Share Offer, we will make an

appropriate announcement on the Stock Exchange’s website at www.hkexnews.hk and on our

Company’s website at www.truepartnercapital.com to inform investors accordingly.

Date (1)

Public Offer commences . . . . . . . . . . . . . . . . . . . . . 9:00 a.m. on Wednesday, 30 September 2020

Latest time for completing electronic applications under theHK eIPO White Form service through one of the below channels:

(1) the designated website at www.hkeipo.hk

(2) the IPO App, which can be downloaded by searching‘‘IPO App’’ in App Store or Google Play ordownloaded at www.hkeipo.hk/IPOApp orwww.tricorglobal.com/IPOApp . . . . . . . . . . . . . . . . . 11:30 a.m. on Friday, 9 October 2020

Application lists open (3) . . . . . . . . . . . . . . . . . . . . . . . . . 11:45 a.m. on Friday, 9 October 2020

Latest time to give electronic application instructionsto HKSCC (4) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12:00 noon on Friday, 9 October 2020

If you are instructing your broker or custodian who is a CCASS Clearing Participant or a CCASSCustodian Participant to give electronic application instructions via CCASS terminals to apply for theHong Kong Offer Shares on your behalf, you are advised to contact your broker or custodian for thelatest time for giving such instructions which may be different from the latest time as stated above.

Latest time to complete payment of HK eIPO White Formapplications by effecting internet banking transfer(s) orPPS payment transfer(s) . . . . . . . . . . . . . . . . . . . . . . . . 12:00 noon on Friday, 9 October 2020

Application lists close (3) . . . . . . . . . . . . . . . . . . . . . . . . . 12:00 noon on Friday, 9 October 2020

Expected Price Determination Date (5) . . . . . . . . . . . . . . . . . . . . . . . . . . Friday, 9 October 2020

Where applicable, announcement of the Offer Price beingset below the bottom end of the indicative Offer Pricerange after making the Downward Offer Price Adjustment(please see the section headed ‘‘Structure of the ShareOffer – Pricing and allocation’’) on the website of theStock Exchange at www.hkexnews.hk and theCompany’s website at www.truepartnercapital.comon or before . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Thursday, 15 October 2020

(1) Announcement of

• the final Offer Price;

• the level of indication of interest in the Placing;

• the level of applications in the Public Offer; and

EXPECTED TIMETABLE(1)

ii

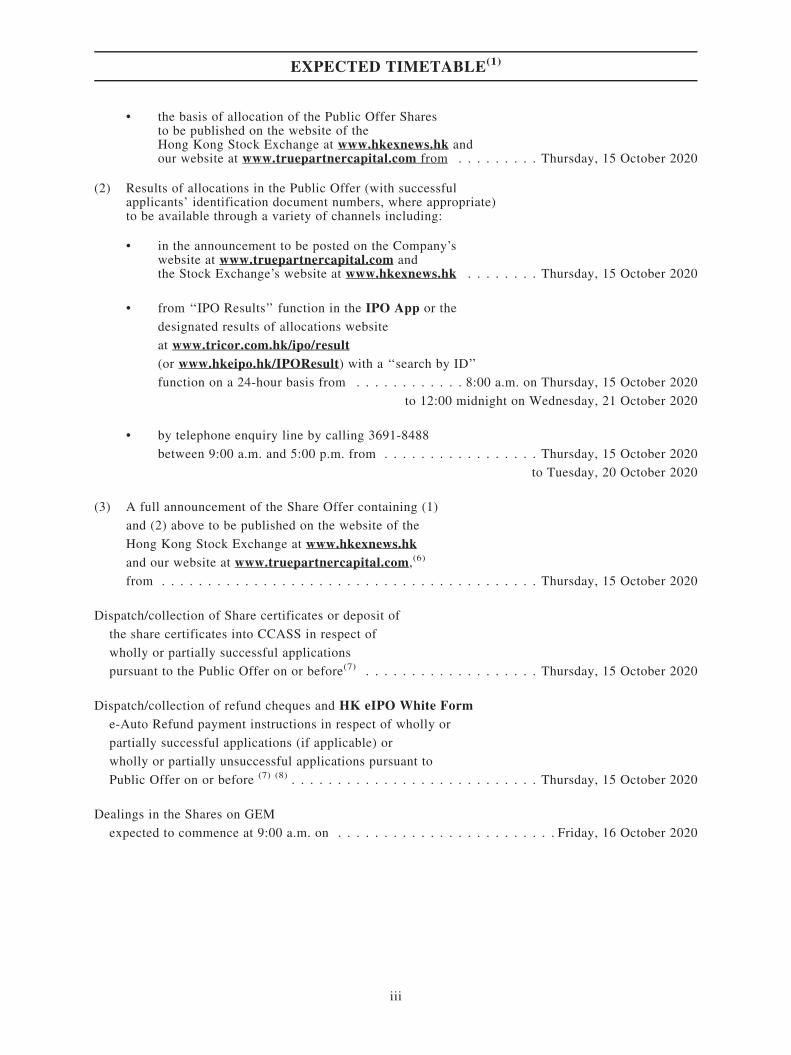

• the basis of allocation of the Public Offer Sharesto be published on the website of theHong Kong Stock Exchange at www.hkexnews.hk andour website at www.truepartnercapital.com from . . . . . . . . . Thursday, 15 October 2020

(2) Results of allocations in the Public Offer (with successfulapplicants’ identification document numbers, where appropriate)to be available through a variety of channels including:

• in the announcement to be posted on the Company’swebsite at www.truepartnercapital.com andthe Stock Exchange’s website at www.hkexnews.hk . . . . . . . . Thursday, 15 October 2020

• from ‘‘IPO Results’’ function in the IPO App or the

designated results of allocations website

at www.tricor.com.hk/ipo/result(or www.hkeipo.hk/IPOResult) with a ‘‘search by ID’’

function on a 24-hour basis from . . . . . . . . . . . . 8:00 a.m. on Thursday, 15 October 2020

to 12:00 midnight on Wednesday, 21 October 2020

• by telephone enquiry line by calling 3691-8488

between 9:00 a.m. and 5:00 p.m. from . . . . . . . . . . . . . . . . . Thursday, 15 October 2020

to Tuesday, 20 October 2020

(3) A full announcement of the Share Offer containing (1)

and (2) above to be published on the website of the

Hong Kong Stock Exchange at www.hkexnews.hkand our website at www.truepartnercapital.com,(6)

from . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Thursday, 15 October 2020

Dispatch/collection of Share certificates or deposit of

the share certificates into CCASS in respect of

wholly or partially successful applications

pursuant to the Public Offer on or before(7) . . . . . . . . . . . . . . . . . . . Thursday, 15 October 2020

Dispatch/collection of refund cheques and HK eIPO White Forme-Auto Refund payment instructions in respect of wholly or

partially successful applications (if applicable) or

wholly or partially unsuccessful applications pursuant to

Public Offer on or before (7) (8) . . . . . . . . . . . . . . . . . . . . . . . . . . . Thursday, 15 October 2020

Dealings in the Shares on GEM

expected to commence at 9:00 a.m. on . . . . . . . . . . . . . . . . . . . . . . . . Friday, 16 October 2020

EXPECTED TIMETABLE(1)

iii

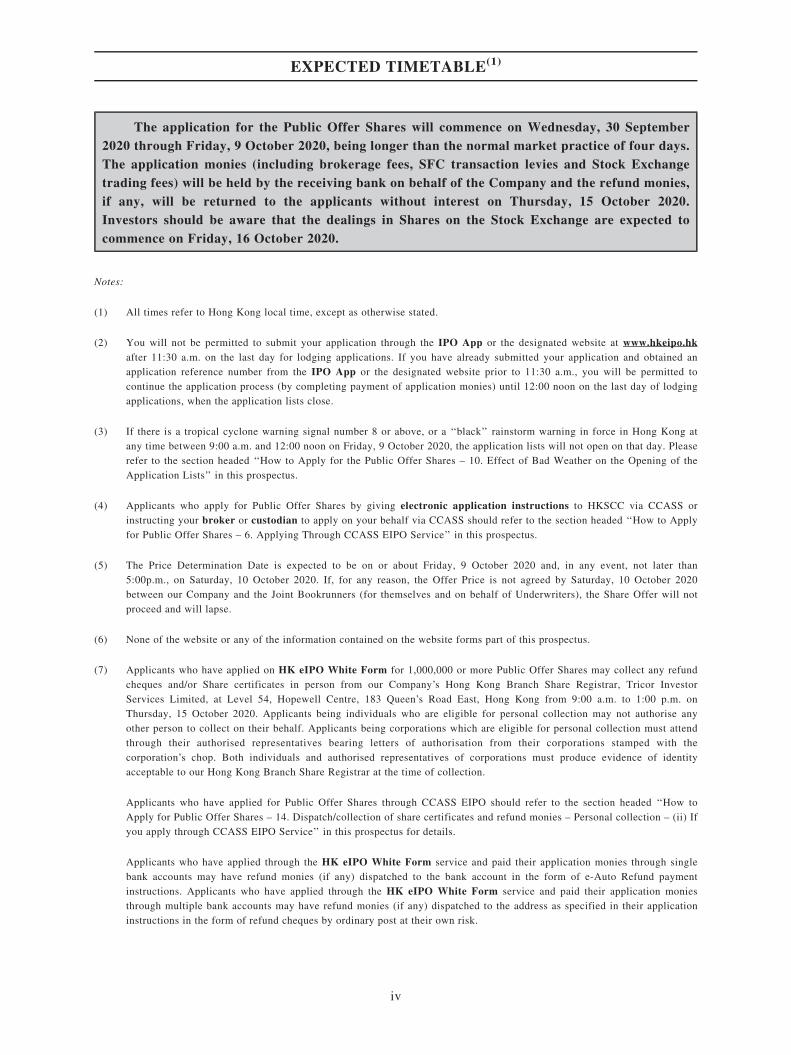

The application for the Public Offer Shares will commence on Wednesday, 30 September2020 through Friday, 9 October 2020, being longer than the normal market practice of four days.The application monies (including brokerage fees, SFC transaction levies and Stock Exchangetrading fees) will be held by the receiving bank on behalf of the Company and the refund monies,if any, will be returned to the applicants without interest on Thursday, 15 October 2020.Investors should be aware that the dealings in Shares on the Stock Exchange are expected tocommence on Friday, 16 October 2020.

Notes:

(1) All times refer to Hong Kong local time, except as otherwise stated.

(2) You will not be permitted to submit your application through the IPO App or the designated website at www.hkeipo.hkafter 11:30 a.m. on the last day for lodging applications. If you have already submitted your application and obtained anapplication reference number from the IPO App or the designated website prior to 11:30 a.m., you will be permitted tocontinue the application process (by completing payment of application monies) until 12:00 noon on the last day of lodgingapplications, when the application lists close.

(3) If there is a tropical cyclone warning signal number 8 or above, or a ‘‘black’’ rainstorm warning in force in Hong Kong atany time between 9:00 a.m. and 12:00 noon on Friday, 9 October 2020, the application lists will not open on that day. Pleaserefer to the section headed ‘‘How to Apply for the Public Offer Shares – 10. Effect of Bad Weather on the Opening of theApplication Lists’’ in this prospectus.

(4) Applicants who apply for Public Offer Shares by giving electronic application instructions to HKSCC via CCASS orinstructing your broker or custodian to apply on your behalf via CCASS should refer to the section headed ‘‘How to Applyfor Public Offer Shares – 6. Applying Through CCASS EIPO Service’’ in this prospectus.

(5) The Price Determination Date is expected to be on or about Friday, 9 October 2020 and, in any event, not later than5:00p.m., on Saturday, 10 October 2020. If, for any reason, the Offer Price is not agreed by Saturday, 10 October 2020between our Company and the Joint Bookrunners (for themselves and on behalf of Underwriters), the Share Offer will notproceed and will lapse.

(6) None of the website or any of the information contained on the website forms part of this prospectus.

(7) Applicants who have applied on HK eIPO White Form for 1,000,000 or more Public Offer Shares may collect any refundcheques and/or Share certificates in person from our Company’s Hong Kong Branch Share Registrar, Tricor InvestorServices Limited, at Level 54, Hopewell Centre, 183 Queen’s Road East, Hong Kong from 9:00 a.m. to 1:00 p.m. onThursday, 15 October 2020. Applicants being individuals who are eligible for personal collection may not authorise anyother person to collect on their behalf. Applicants being corporations which are eligible for personal collection must attendthrough their authorised representatives bearing letters of authorisation from their corporations stamped with thecorporation’s chop. Both individuals and authorised representatives of corporations must produce evidence of identityacceptable to our Hong Kong Branch Share Registrar at the time of collection.

Applicants who have applied for Public Offer Shares through CCASS EIPO should refer to the section headed ‘‘How toApply for Public Offer Shares – 14. Dispatch/collection of share certificates and refund monies – Personal collection – (ii) Ifyou apply through CCASS EIPO Service’’ in this prospectus for details.

Applicants who have applied through the HK eIPO White Form service and paid their application monies through singlebank accounts may have refund monies (if any) dispatched to the bank account in the form of e-Auto Refund paymentinstructions. Applicants who have applied through the HK eIPO White Form service and paid their application moniesthrough multiple bank accounts may have refund monies (if any) dispatched to the address as specified in their applicationinstructions in the form of refund cheques by ordinary post at their own risk.

EXPECTED TIMETABLE(1)

iv

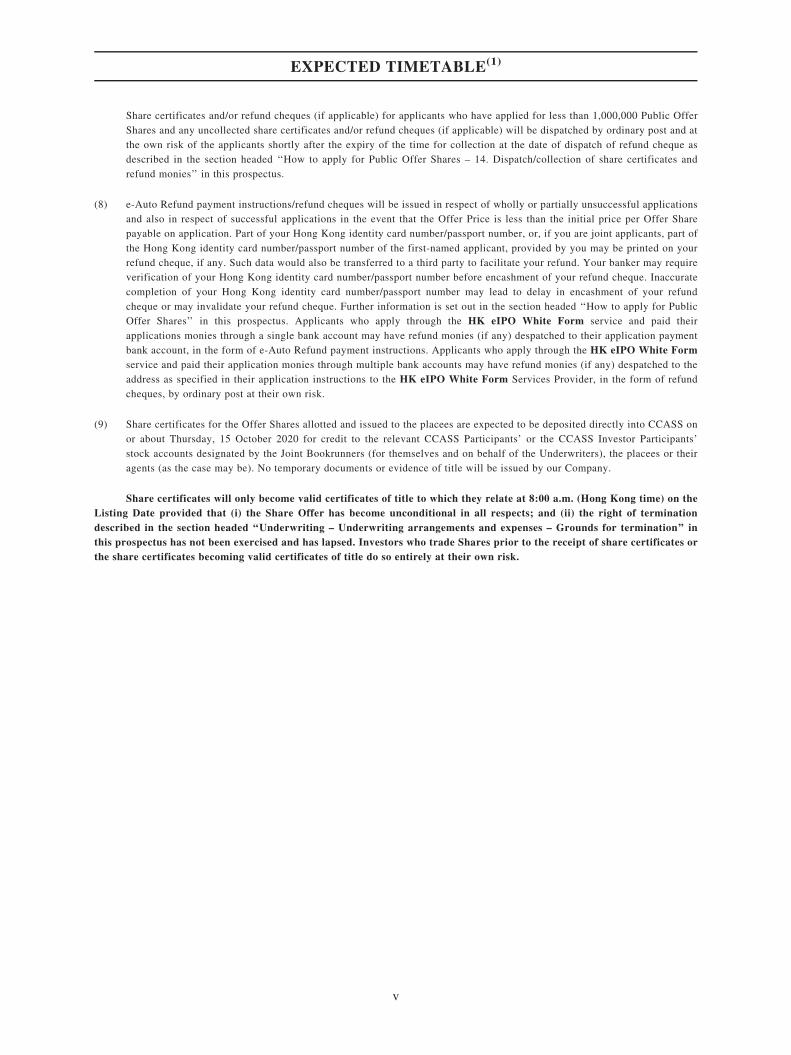

Share certificates and/or refund cheques (if applicable) for applicants who have applied for less than 1,000,000 Public OfferShares and any uncollected share certificates and/or refund cheques (if applicable) will be dispatched by ordinary post and atthe own risk of the applicants shortly after the expiry of the time for collection at the date of dispatch of refund cheque asdescribed in the section headed ‘‘How to apply for Public Offer Shares – 14. Dispatch/collection of share certificates andrefund monies’’ in this prospectus.

(8) e-Auto Refund payment instructions/refund cheques will be issued in respect of wholly or partially unsuccessful applicationsand also in respect of successful applications in the event that the Offer Price is less than the initial price per Offer Sharepayable on application. Part of your Hong Kong identity card number/passport number, or, if you are joint applicants, part ofthe Hong Kong identity card number/passport number of the first-named applicant, provided by you may be printed on yourrefund cheque, if any. Such data would also be transferred to a third party to facilitate your refund. Your banker may requireverification of your Hong Kong identity card number/passport number before encashment of your refund cheque. Inaccuratecompletion of your Hong Kong identity card number/passport number may lead to delay in encashment of your refundcheque or may invalidate your refund cheque. Further information is set out in the section headed ‘‘How to apply for PublicOffer Shares’’ in this prospectus. Applicants who apply through the HK eIPO White Form service and paid theirapplications monies through a single bank account may have refund monies (if any) despatched to their application paymentbank account, in the form of e-Auto Refund payment instructions. Applicants who apply through the HK eIPO White Formservice and paid their application monies through multiple bank accounts may have refund monies (if any) despatched to theaddress as specified in their application instructions to the HK eIPO White Form Services Provider, in the form of refundcheques, by ordinary post at their own risk.

(9) Share certificates for the Offer Shares allotted and issued to the placees are expected to be deposited directly into CCASS onor about Thursday, 15 October 2020 for credit to the relevant CCASS Participants’ or the CCASS Investor Participants’stock accounts designated by the Joint Bookrunners (for themselves and on behalf of the Underwriters), the placees or theiragents (as the case may be). No temporary documents or evidence of title will be issued by our Company.

Share certificates will only become valid certificates of title to which they relate at 8:00 a.m. (Hong Kong time) on theListing Date provided that (i) the Share Offer has become unconditional in all respects; and (ii) the right of terminationdescribed in the section headed ‘‘Underwriting – Underwriting arrangements and expenses – Grounds for termination’’ inthis prospectus has not been exercised and has lapsed. Investors who trade Shares prior to the receipt of share certificates orthe share certificates becoming valid certificates of title do so entirely at their own risk.

EXPECTED TIMETABLE(1)

v

IMPORTANT NOTICE TO INVESTORS

This prospectus is issued by our Company solely in connection with the Share Offers and does

not constitute an offer to sell or a solicitation of an offer to buy any securities other than the Offer

Shares offered by this prospectus pursuant to the Share Offer. This prospectus may not be used for the

purpose of, and does not constitute, an offer to sell or a solicitation of an offer in any other

jurisdiction or in any other circumstances. No action has been taken to permit a public offer of the

Offer Shares or the distribution of this prospectus in any jurisdiction other than Hong Kong.

You should rely only on the information contained in this prospectus to make your investment

decision. Our Company, the Sole Sponsor, the Joint Bookrunners, the Joint Lead Managers and the

Underwriters have not authorised anyone to provide you with information that is different from what

is contained in this prospectus. Any information or representation not contained in this prospectus

must not be relied on by you as having been authorised by our Company, the Sole Sponsor, the Joint

Bookrunners, the Joint Lead Managers, the Underwriters, any of their respective directors, officers,

employees, agents, affiliates or representatives, or any other person or party involved in the Share

Offer.

The contents of our Company’s website at www.truepartnercapital.com do not form part of this

prospectus.

Page

Characteristics of GEM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . i

Expected timetable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ii

Contents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . vi

Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Definitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Glossary of technical terms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

Forward-looking statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

Risk factors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

Information about this prospectus and the Share Offer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

Waiver from compliance with the GEM Listing Rules . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78

Directors and parties involved in the Share Offer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82

Corporate information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 86

Industry overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88

CONTENTS

vi

Page

Regulatory and licensing requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 112

History, Reorganisation and corporate structure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 149

Business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 161

Relative value volatility strategy and illustration of trade process and execution . . . . . . . . . . . 293

Relationship with the Capital Group . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 310

The Cornerstone Placing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 316

Financial information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 320

Directors and senior management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 392

Share capital . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 405

Substantial Shareholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 409

Future plans and use of proceeds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 414

Underwriting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 438

Structure of the Share Offer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 451

How to apply for Public Offer Shares . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 460

Appendix IA – Accountants’ report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . IA-1

Appendix IB – Unaudited condensed consolidated financial informationof the Group as of and for the three andsix months ended 30 June 2020 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . IB-1

Appendix II – Unaudited pro forma financial information . . . . . . . . . . . . . . . . . . . . . . . . . . II-1

Appendix III – Summary of the constitution of our Company andCayman Companies Law . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . III-1

Appendix IV – Statutory and general information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . IV-1

Appendix V – Documents delivered to the Registrar of Companiesand available for inspection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . V-1

CONTENTS

vii

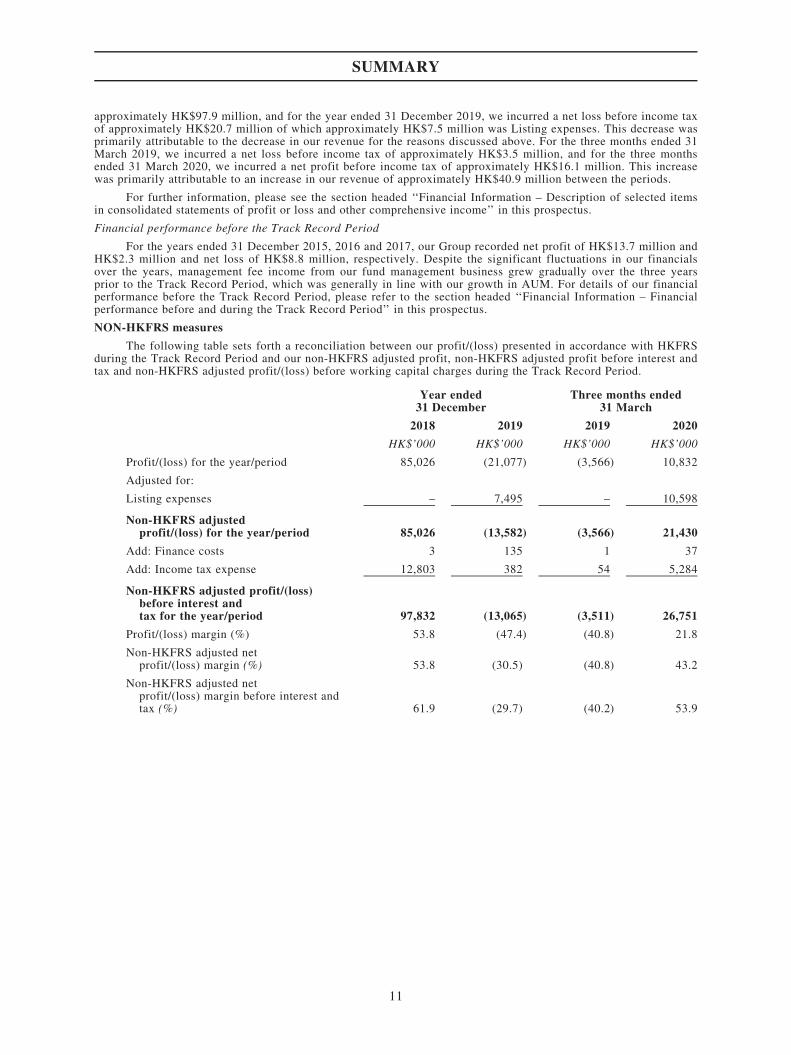

This summary aims to give you an overview of the information contained in this prospectus. As this is asummary, it does not contain all of the information that may be important to you and is qualified in its entirety by,and should be read in conjunction with, the full text of this prospectus. You should read the whole prospectusbefore you decide to invest in the Offer Shares.

There are risks associated with any investment in the Offer Shares. Some of the particular risks associatedwith an investment in the Offer Shares are set out in the section headed ‘‘Risk Factors’’ in this prospectus. Youshould read that section carefully before you decide to invest in the Offer Shares.

OVERVIEW

We are a Hong Kong and U.S. based fund management group which manages funds and managed accounts ona discretionary basis using a global volatility relative value trading strategy supported by our in-house proprietarytrading platform. Such strategy involves the identification and exploitation of market inefficiencies in exchangelisted options (through the purchase of relatively undervalued options and sale of relatively overvalued options)whilst hedging resulting options positions through the adoption of active portfolio management. This involves active24/5 trading of liquid exchange listed derivatives (including equity index options with less than six months maturity,large cap single stock options, as well as futures, exchange traded funds and equities) across major markets(including the U.S., Europe and Asia) and different time zones using a single book, which enables us to promptlyreact to trading opportunities and arbitrage across major markets. Our trading decisions are supported by our in-house proprietary trading platform (embedded with option pricing and volatility surface models) designed for ourspecific way of trading and which enables real-time pricing of implied volatilities, quantitative comparisons, riskmanagement as well as speedy execution of trades. The collective expertise and specialised knowledge in options andvolatility trading of our team (including senior management team members with market making and softwaredevelopment background and who have worked together for over a decade) are the foundation of our proprietarytrading technology and are material to our success.

We are a growing business with a trading strategy that has attracted material investments to our funds andmanaged accounts in recent years, with a large portion of our AUM invested in funds which were only launched, orotherwise in respect of investment mandates which were only entered, during the Track Record Period. Given therelatively short track record of most of our funds, we have relatively few investors (with our top 5 investorscontributing to approximately 67.9%, 76.8% and 77.6% of our total AUM as at 31 December 2018, 31 December2019 and 31 March 2020 respectively) at present and rely materially on our top investors in terms of our revenuegeneration. Notwithstanding this, our investors are typically not subject to lock-up on their investments (with only4.3% of AUM subject to a lock-up period of 12 months, with one investor’s lock-up being released for 25% after thefirst calendar quarter and gradually released in full in a staggered manner after 12 months) and they (including twolarge institutional investors who accounted for 36% of our revenue for the three months ended 31 March 2020) mayredeem their investments at any time by providing 20 business days or less prior notice (with some investors entitledto redeem their investments by giving as short as one to three days’ prior notice, despite this being within theindustry norm). Notwithstanding net increase of our AUM over the years, material redemption decisions by our topinvestors (due to their assessment of the effectiveness of our trading strategy vis-à-vis other trading or investmentstrategies of other fund managers, or otherwise) may materially and adversely affect our fee income, potentially leadto the closure of the relevant fund(s) or managed account(s) (if all investments by investors are redeemed in full)which may lead to material reduction in our fee income and consequently possibly net loss being incurred by ourGroup, and may adversely affect our ability to attract new investments and our business prospects. Further, atpresent, the Group is materially reliant on the continued services of our senior management team and key personnel(in particular, our co-chief investment officers from the perspective of executing our trading strategy as well as ourchief technology officer and global head of research and development for carrying out technology and softwaredevelopment functions), most of which have worked together for many years prior to joining our Group. Most ofsuch senior management team members and key personnel may terminate their employment with us by providingshort prior notices (generally ranging from one to three months, which is similar to the length of prior notice we arerequired to give to terminate their employement) and the departure of one or more of them may potentially impair ouroperations, business development or implementation of our business strategies. However, despite the crucial role ofthese members of staff to our operations, we do not maintain key man insurance because we have implementedvarious mitigating measures to ensure sustainability of our business including, without limitation (i) ensuring thatthere is considerable overlap in competencies and functions among our senior management and key personnel; (ii)ensuring that they are sufficiently incentivised through their shareholding (many of our senior management membershas worked together for many years prior joining our Group and are Substantial Shareholders) as well as optionswhich may be granted pursuant to the Pre-IPO Share Option Scheme and the Share Option Scheme); and (iii)additional hiring and training of staff to increase redundancies. Please refer to the paragraphs headed ‘‘We are agrowing business with a limited number of products and investors (who do not have a long business relationship withour Group) and our business and prospectus may be materially and adversely affected by the withdrawal ofinvestments due to loss in confidence in our trading strategy or otherwise, or the departure of senior management andkey personnel whom we materially rely on to grow our business. The business nature of our Group during thisgrowth stage as we continue to mature may be considered to be relatively high risk’’ and other related risk factors inthe ‘‘Risk factor’’ section of this prospectus for further details of the relevant risks generally described above.Trading from our offices in Hong Kong and Chicago and supported by our technology centre in the Netherlands, wecurrently manage two flagship funds launched by us, namely, the True Partner Fund (launched in July 2011, whichapplies a volatility exposure which is intended to be viewed on an average) and the True Partner Volatility Fund

SUMMARY

1

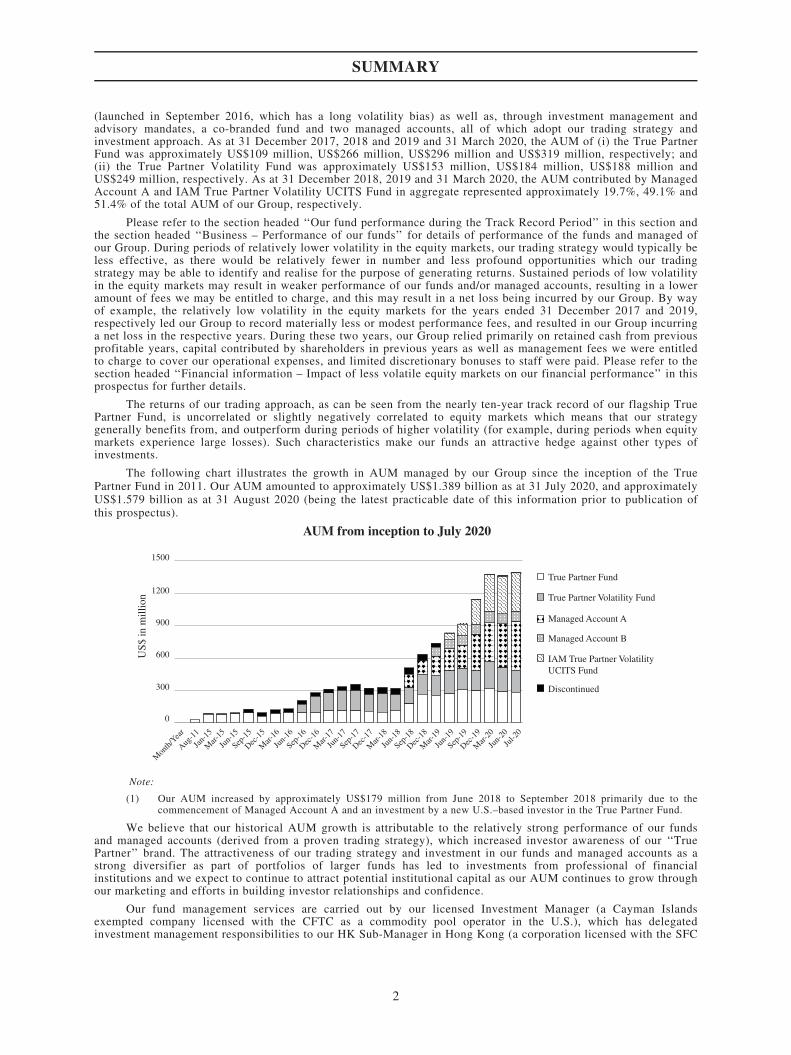

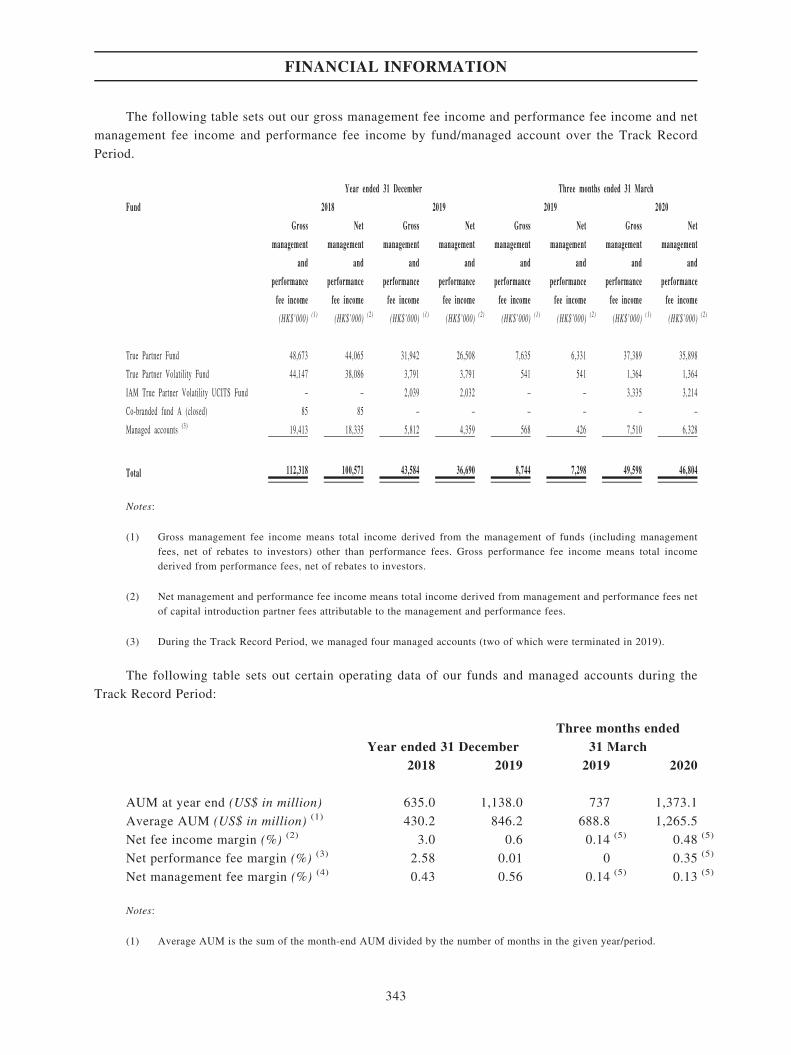

(launched in September 2016, which has a long volatility bias) as well as, through investment management andadvisory mandates, a co-branded fund and two managed accounts, all of which adopt our trading strategy andinvestment approach. As at 31 December 2017, 2018 and 2019 and 31 March 2020, the AUM of (i) the True PartnerFund was approximately US$109 million, US$266 million, US$296 million and US$319 million, respectively; and(ii) the True Partner Volatility Fund was approximately US$153 million, US$184 million, US$188 million andUS$249 million, respectively. As at 31 December 2018, 2019 and 31 March 2020, the AUM contributed by ManagedAccount A and IAM True Partner Volatility UCITS Fund in aggregate represented approximately 19.7%, 49.1% and51.4% of the total AUM of our Group, respectively.

Please refer to the section headed ‘‘Our fund performance during the Track Record Period’’ in this section andthe section headed ‘‘Business – Performance of our funds’’ for details of performance of the funds and managed ofour Group. During periods of relatively lower volatility in the equity markets, our trading strategy would typically beless effective, as there would be relatively fewer in number and less profound opportunities which our tradingstrategy may be able to identify and realise for the purpose of generating returns. Sustained periods of low volatilityin the equity markets may result in weaker performance of our funds and/or managed accounts, resulting in a loweramount of fees we may be entitled to charge, and this may result in a net loss being incurred by our Group. By wayof example, the relatively low volatility in the equity markets for the years ended 31 December 2017 and 2019,respectively led our Group to record materially less or modest performance fees, and resulted in our Group incurringa net loss in the respective years. During these two years, our Group relied primarily on retained cash from previousprofitable years, capital contributed by shareholders in previous years as well as management fees we were entitledto charge to cover our operational expenses, and limited discretionary bonuses to staff were paid. Please refer to thesection headed ‘‘Financial information – Impact of less volatile equity markets on our financial performance’’ in thisprospectus for further details.

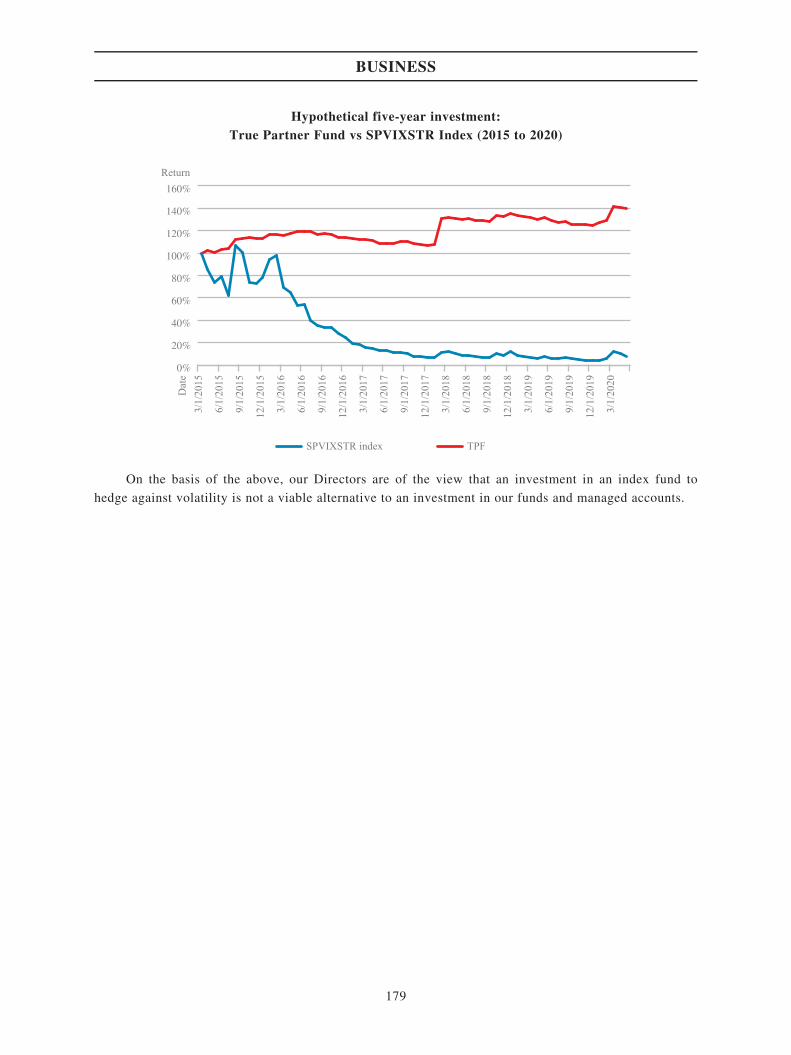

The returns of our trading approach, as can be seen from the nearly ten-year track record of our flagship TruePartner Fund, is uncorrelated or slightly negatively correlated to equity markets which means that our strategygenerally benefits from, and outperform during periods of higher volatility (for example, during periods when equitymarkets experience large losses). Such characteristics make our funds an attractive hedge against other types ofinvestments.

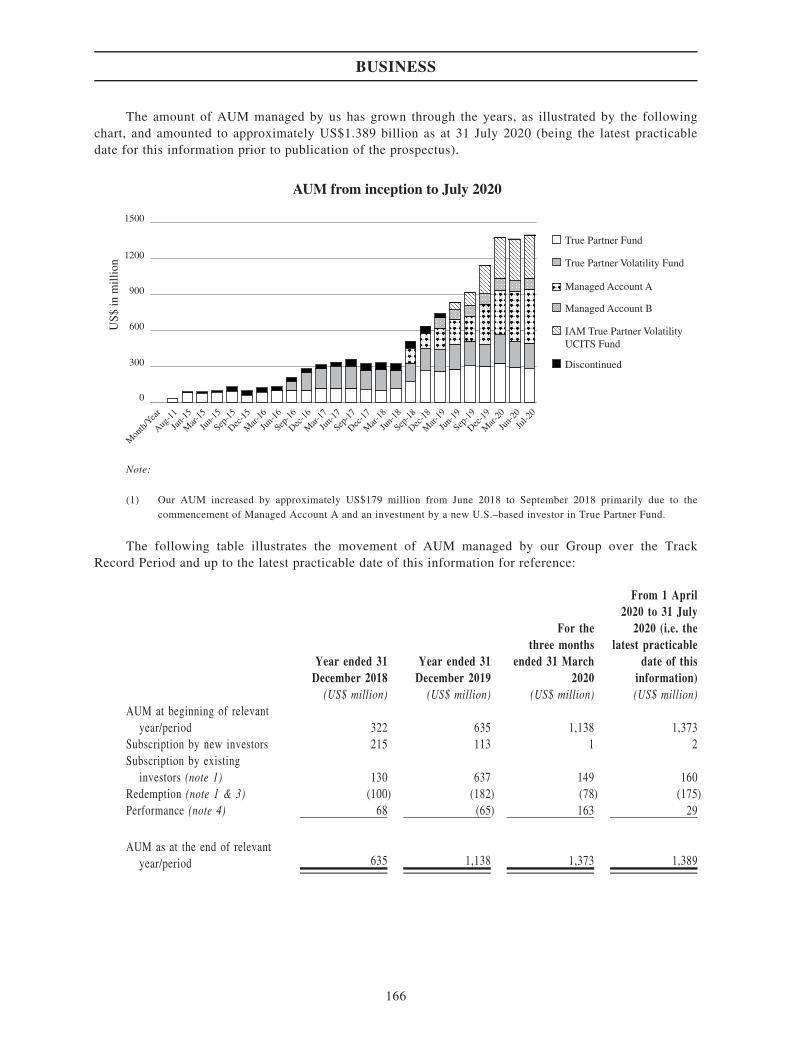

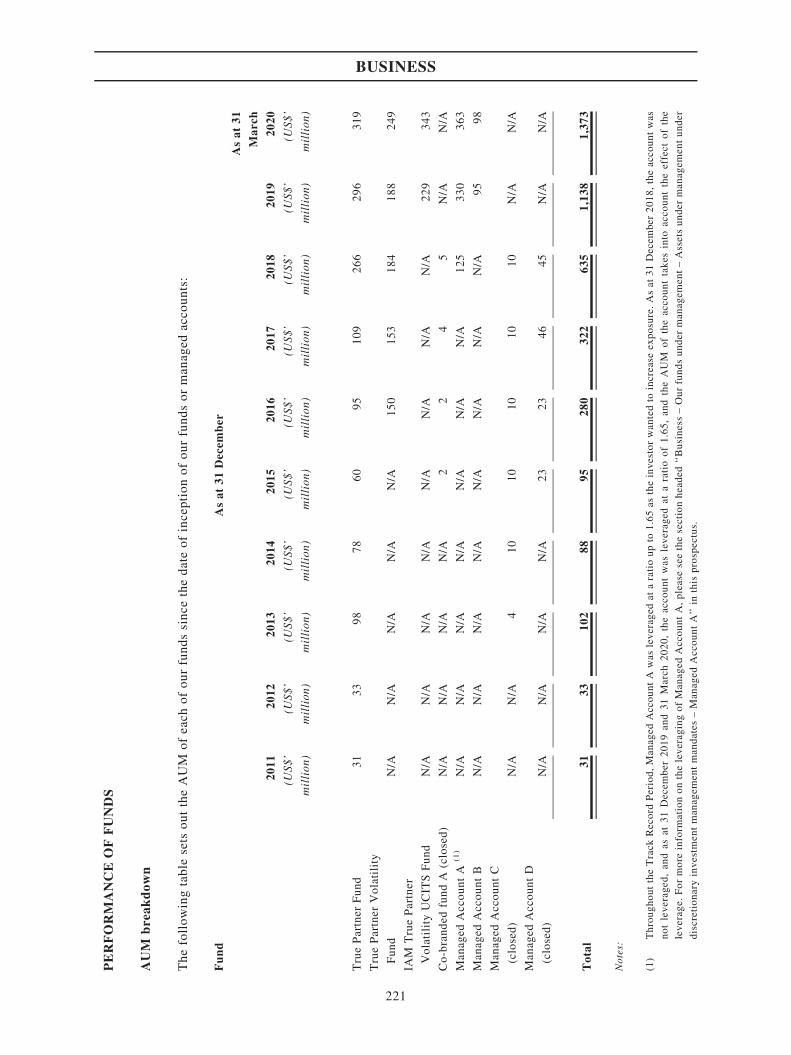

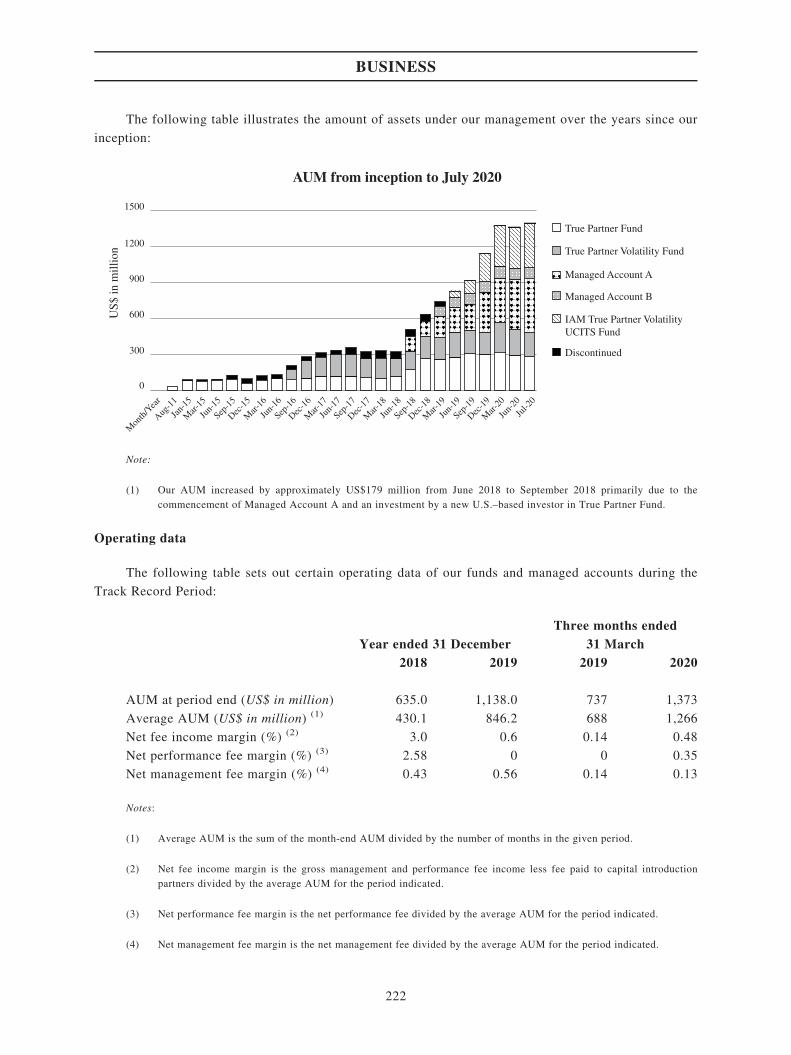

The following chart illustrates the growth in AUM managed by our Group since the inception of the TruePartner Fund in 2011. Our AUM amounted to approximately US$1.389 billion as at 31 July 2020, and approximatelyUS$1.579 billion as at 31 August 2020 (being the latest practicable date of this information prior to publication ofthis prospectus).

0

300

600

900

1200

1500

AUM from inception to July 2020

US

$ i

n m

illi

on

Mon

th/Y

ear

Aug

-11

Jan-

15

Mar

-15

Jun-

15

Sep-1

5

Dec

-15

Mar

-16

Jun-

16

Sep-1

6

Dec

-16

Mar

-17

Jun-

17

Sep-1

7

Dec

-17

Mar

-18

Jun-

18

Sep-1

8

Dec

-18

Mar

-19

Jun-

19

Sep-1

9

Mar

-20

Jun-

20

Jul-2

0

Dec

-19

True Partner Fund

True Partner Volatility Fund

Managed Account B

IAM True Partner Volatility

UCITS Fund

Managed Account A

Discontinued

Note:

(1) Our AUM increased by approximately US$179 million from June 2018 to September 2018 primarily due to thecommencement of Managed Account A and an investment by a new U.S.–based investor in the True Partner Fund.

We believe that our historical AUM growth is attributable to the relatively strong performance of our fundsand managed accounts (derived from a proven trading strategy), which increased investor awareness of our ‘‘TruePartner’’ brand. The attractiveness of our trading strategy and investment in our funds and managed accounts as astrong diversifier as part of portfolios of larger funds has led to investments from professional of financialinstitutions and we expect to continue to attract potential institutional capital as our AUM continues to grow throughour marketing and efforts in building investor relationships and confidence.

Our fund management services are carried out by our licensed Investment Manager (a Cayman Islandsexempted company licensed with the CFTC as a commodity pool operator in the U.S.), which has delegatedinvestment management responsibilities to our HK Sub-Manager in Hong Kong (a corporation licensed with the SFC

SUMMARY

2

to carry out type 9 (asset management) regulated activity) and our U.S. Sub-Manager (registered with the SEC as aninvestment advisor). The investors in our funds and managed accounts are primarily professional investors. We donot hold client assets.

Whether our Group is suitable for listing given that only 4.3% of our AUM is subject to lock-up and the noticeperiod of redemption is only generally 20 business days or less

Our investors are typically not subject to lock-up on their investments (with only 4.3% of AUM subject to alock-up period of 12 months, with one investor’s lock-up being released gradually in a staggered manner) and they(including two large institutional investors who accounted for 48% of our revenue for the year ended 31 December2018) may redeem their investments at any time by providing short prior notice (generally 20 business days or lessprior notice, with some investors entitled to redeem their investments by giving as short as one to three days’ priornotice, despite this being within the industry norm). During the Track Record Period, other than in respect ofManaged Account C (closed) where no redemption notice period was mutually agreed in writing, approximately7.7%, 4.7% and 18.0% of our revenue was generated from investors with redemption notice periods of less than 20days. As at 31 March 2020, 51.4% of AUM was attributable to investors with redemption notice periods of less than20 days. Material redemption decisions by our top investors (which may result from such considerations as change ininvestment appetite or preference or other factors beyond our control) may materially and adversely affect our feeincome, potentially lead to net losses being incurred, and may adversely affect our ability to attract new investmentsand our business prospects. The redemption amounts of our top 5 investors during the Track Record Periodrepresented in aggregate approximately 13.2%, 19.8% and 7.1% of our AUM at 31 December 2018, 2019 and 31March 2020, respectively.

Notwithstanding the above important redemption risk, our Directors believe that our Company is neverthelesssuitable for Listing as the amount of AUM managed by our Group has continued to grow over the years since theinception of our first flagship fund, the True Partner Fund, in 2011. This is because, notwithstanding redemptionsfrom investors from time to time as described in the section "Business - Overview" of this prospectus, there has beennet subscriptions (i.e. taking into account redemptions) in our funds and managed accounts. For illustration,notwithstanding the material redemption amounts from our top 5 investors during the Track Record Period asdescribed above, the net subscriptions (taking into account redemptions) of our top 5 investors were approximatelyUS$190.5 million; US$530.1 million and US$64.5 million for each of the years ended 31 December 2018 and 2019and the three months ended 31 March 2020;

OUR BUSINESS MODEL

Investment management services

We generate revenue through charging the funds and managed accounts under our management: (i)management fees, calculated as a percentage of NAV of shares of the relevant fund or managed account; and (ii)performance fees, calculated based on the absolute performance of the relevant fund or managed account, generallycalculated on a high watermark basis by reference to the NAV of the relevant fund or managed account at a particulartime. Further to our provision of fund management services, we also derived revenue from providing consultancyservices.

Our flagship fund is the True Partner Fund which we launched in July 2011 as a stand-alone fund, but whichwas later restructured into a master-feeder structure to facilitate investments from U.S. taxable investors. We furtherlaunched an additional fund, the True Partner Volatility Fund, which is similarly structured, but with a tradingstrategy which has a long volatility bias which means that the trading strategy is tailored to have slight negativecorrelation to equities (i.e. deliver higher payoff during periods when equity markets experience losses). In additionto the funds launched by us, we also enter into investment management mandates with third parties who allocate asub-fund of their umbrella fund or a portion of their assets to be managed by us. During the Track Record Period andup to the Latest Practicable Date, we managed two co-branded funds (being funds which include the ‘‘True Partner’’name in the name of the fund) and four managed accounts in addition to the two funds launched by us of which, twomanaged accounts and one co-branded fund have been terminated as at the Latest Practicable Date. Please see thesection headed ‘‘Business – Our funds under management’’ in this prospectus for more details on our funds andmanaged accounts.

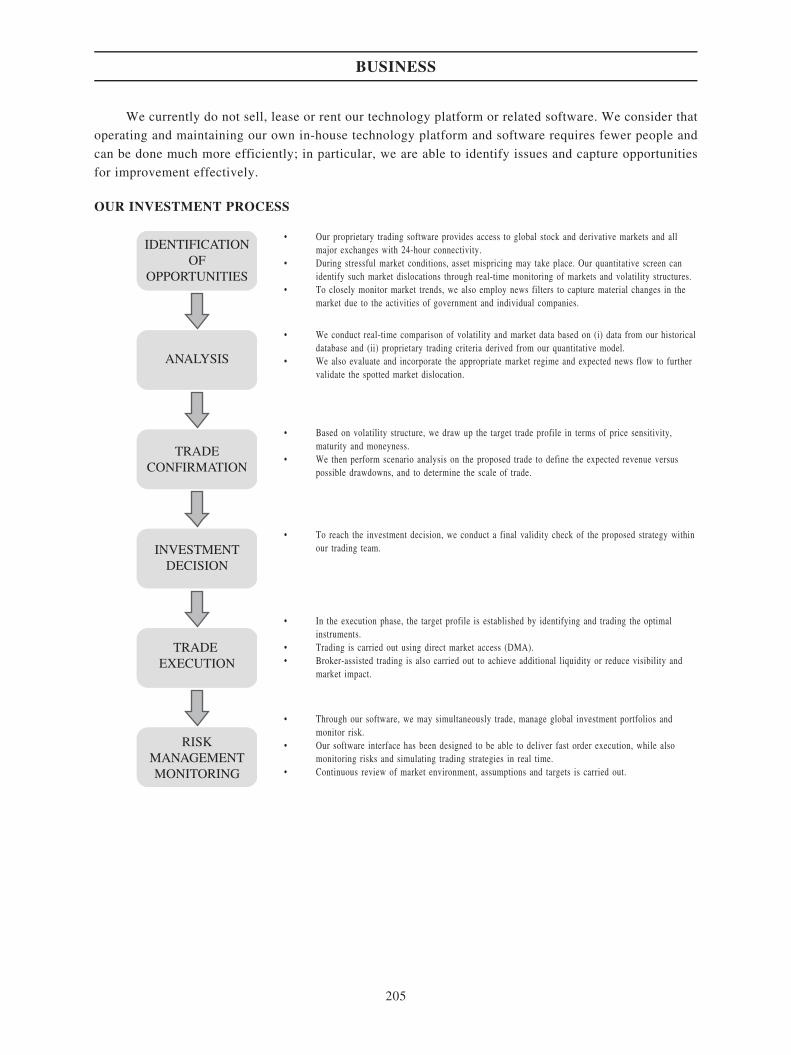

We manage funds and managed accounts on a discretionary basis using a global volatility relative valuetrading strategy. Our trading strategy involves identifying market inefficiencies and dislocation in terms of impliedvolatility arising from events affecting equity markets, which results in options being overpriced or undervalued, andthen setting up positions to capture potential benefits. During less volatile markets, our trading strategy would remainthe same although there may be less volatility spread opportunities which we may capitalise, which may negativelyaffect the performance of our funds and managed accounts. During such periods, we may need to rely on retainedcash from previous profitable years, capital contributed by shareholders as well as management fees to coveroperational expenses, and no or very limited discretionary bonuses to staff would be paid. We did not have to resortto corporate restructuring, material equity or debt financing, liquidation or disposal of material assets, or the layingoff of staff due to accumulated losses caused by lack of performance in such environment. We consider that ouractive trading strategy involving highly-liquid derivatives and use of our proprietary technology enhances our abilityto react quickly to (abrupt) changes in market circumstances on an intra-day basis. For further information on ourstrategy, please see the sections headed ‘‘Business – Our investment approach’’ and ‘‘Relative value volatilitystrategy and illustration of trade process and execution’’ in this prospectus.

SUMMARY

3

The following table sets out certain operating data of our funds and managed accounts during the Track RecordPeriod:

Year ended 31 December Three months ended 31 March2018 2019 2019 2020

AUM at period end (US$ in million) 635.0 1,138.0 737 1,373Average AUM (US$ in million) 430.1 846.2 688 1,266Net fee income margin (%) 3.0 0.6 0.14 0.48Net performance fee margin (%) 2.58 0 0 0.35Net management fee margin (%) 0.43 0.56 0.14 0.13

The net fee income margin and net performance fee margin dropped significantly in the year ended 31December 2019 as our Group’s fee income was materially affected by a material decrease in the amount ofperformance fees generated as the relatively lower volatility in the equity markets during the year presented lessopportunities to us and limited the performance of our funds and managed accounts. For further information on theperformance and operating data of our funds and managed accounts, please see the sections headed ‘‘Business –Performance of funds’’ and ‘‘Financial Information – Revenue’’ in this prospectus.

The terms on which our fees are charged on our funds and managed accounts are negotiated with our investorson an arm’s length basis, and for certain early and significant investors, we may negotiate specific terms with respectto management fees and performance fees (pursuant to which these investors may be given special/preferential feetreatments through subscriptions to special share classes and/or the entering into of side letters which shall continuefor the duration of their investments). Generally, we would strive to negotiate, with those institutional investorswhich are charged lower management fees, a higher performance fee to compensate. However, we may notnecessarily succeed in negotiating a higher performance fee in each case where we agree on a lower management fee.For the financial years ended 31 December 2018 and 2019 and the three months ended 31 March 2020,approximately 44%, 60% and 61% of the total AUM of our Group was chargeable with management fees, whereasthe remainder of AUM was not chargeable with management fees, respectively. Where an investor has negotiated nilmanagement fees, the relevant increase in AUM may not necessarily result in an increase in our fee income. As at 31December 2018 and 2019 and 31 March 2020, 48.4%, 75.7% and 62.5%, respectively, of the increase in our Group’sAUM during the respective year/period were chargeable with a lower management fee, while 44.8%, 20.7% and33.5%, respectively, of the increase in our Group’s AUM during the respective years/period were chargeable with nilmanagement fee rate. In respect of those investors in our flagship funds (i.e. the True Partner Fund and the TruePartner Volatility Fund) and managed accounts which were offered preferential fee treatment (i.e. charged a lowermanagement fee than 2% at the time), we were able to negotiate a higher performance fee (above 20%) in respect offour investors (out of 18 of such investors with preferential fee treatment), and the investment percentages inaggregate attributable to these investors were (i) approximately 15.9%, 7.3% and 7.5% of our total AUM as at 31December 2018, 31 December 2019 and 31 March 2020, respectively; and (ii) approximately 12.0%, 12.9% and 3.7%of our total revenue contribution over the years ended 31 December 2018 and 2019 and three months ended 31 March2020, respectively.

Such preferential fee arrangements may be offered to seed and early investors as well as more significantreputable investors willing to make meaningful investments as it is considered that the attraction of investments,especially during the initial launch stage of our funds, would be important for growing the relevant funds’ AUM intoa decent size which is crucial for attracting and facilitating prospective investments (due to minimum investment sizerequirements and concentration criteria that are commonly applied by asset allocators – please refer to the sectionheaded ‘‘Industry Overview – Concentration criteria and minimum investment amount requirements of assetallocators’’ in this prospectus for further details).

Given that our Group has built a demonstrable track record over the years, our Directors believe that our Groupis at a relatively matured stage whereby we could gradually reduce our reliance on seed capital and/or grantingpreferential fee arrangements in the future.

During the Track Record Period, for those investors to which we charged management fees, the fee ratecharged ranged from 0.9% to 2%, with the majority between 1.5% and 2%, and our performance fees ranged from 5%to 50%. Performance fees are calculated based on the absolute performance of the relevant fund or managed accountover the relevant performance period. Performance fees only become realised upon crystallisation which occurs uponthe earlier of (i) redemption of investment by an investor; and (ii) at the end of the relevant performance period,which may be 31 March, 30 June, 30 September or 31 December, depending on the terms of the relevant fund ormanaged account.

Our Hong Kong and Chicago offices house our investment management teams, and our third office inAmsterdam mainly provides IT and software development support. As at the Latest Practicable Date, four responsibleofficers and seven licensed representatives are accredited to our HK Sub-Manager, and we employed in total 26 staff.

SUMMARY

4

Consultancy services

From time to time, we may provide consultancy services to complement our fund management business. Ourlargest customer of consultancy services over the Track Record Period was Capital Futures Corp., a company listedon the Taiwan Stock Exchange (stock code: 6024) and a subsidiary of CSC. Pursuant to an agreement dated 1 July2015, we provided Capital Futures Corp. with consultancy services in relation to trading analysis, market researchand derivatives related information technology. The consultancy services agreement was terminated on 31 December2018 upon completion of our services. Additionally, our consultancy services may include serving as expert witnessto market regulators with regards to cases involving suspected market manipulation as well as our personnel makingcontributions to university courses.

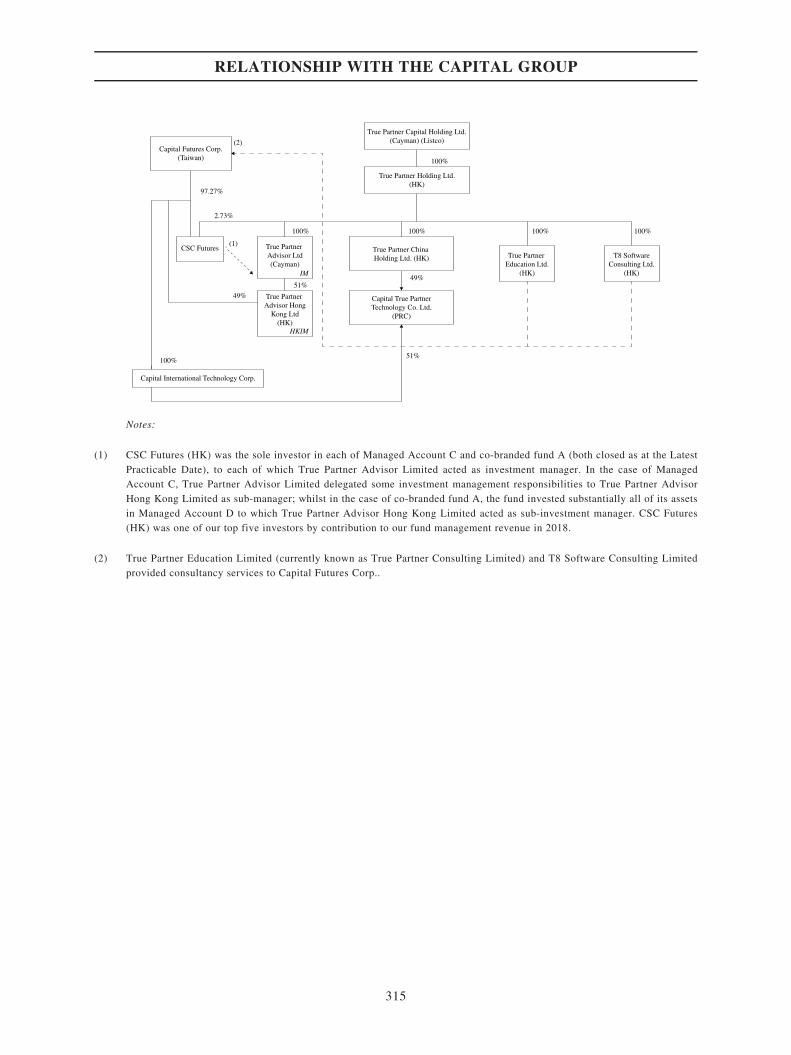

For information on our consultancy services provided to and our relationship with Capital Futures Corp.,please see the section headed ‘‘Relationship with the Capital Group’’ in this prospectus, respectively.

Our investors

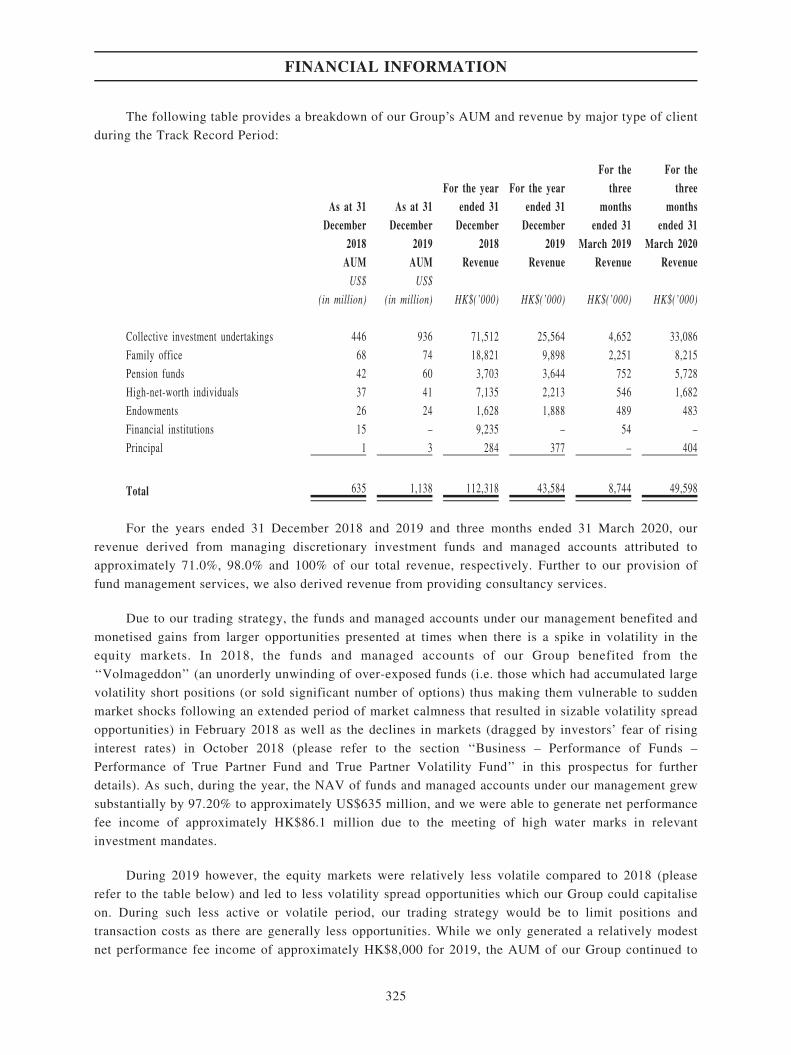

The investors of our funds and managed accounts are mainly professional investors, including collectiveinvestment undertakings, family offices, pension funds, high-net-worth individuals, endowments/foundations andfinancial institutions.

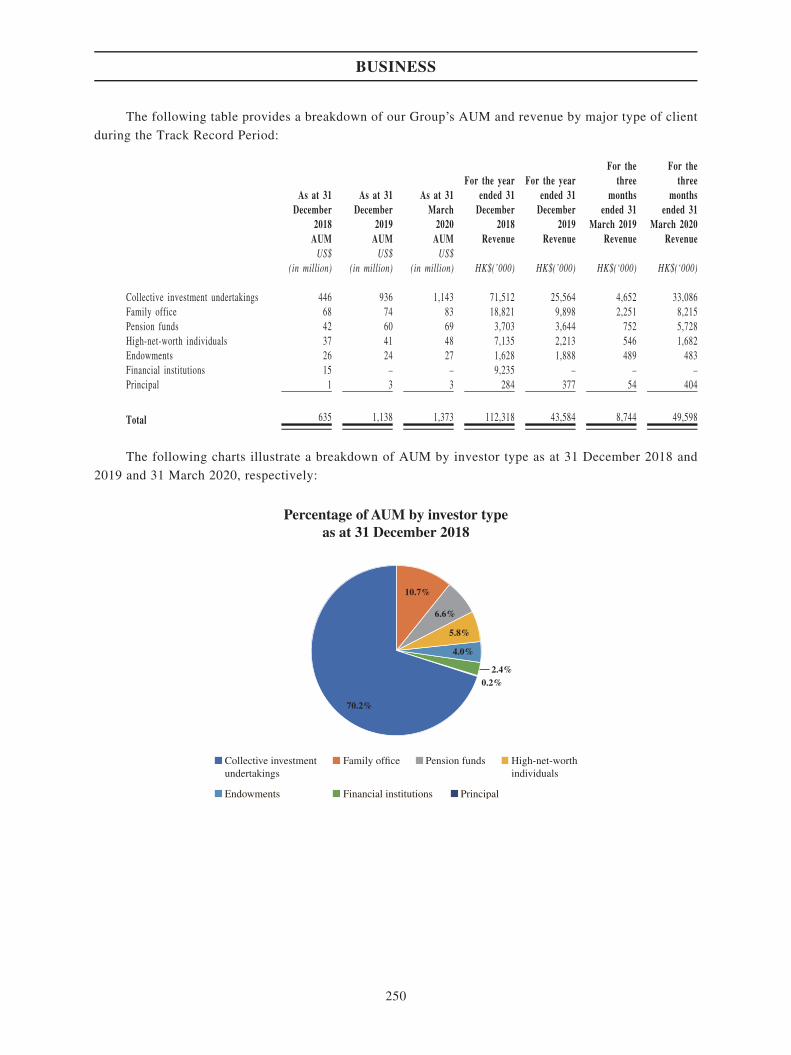

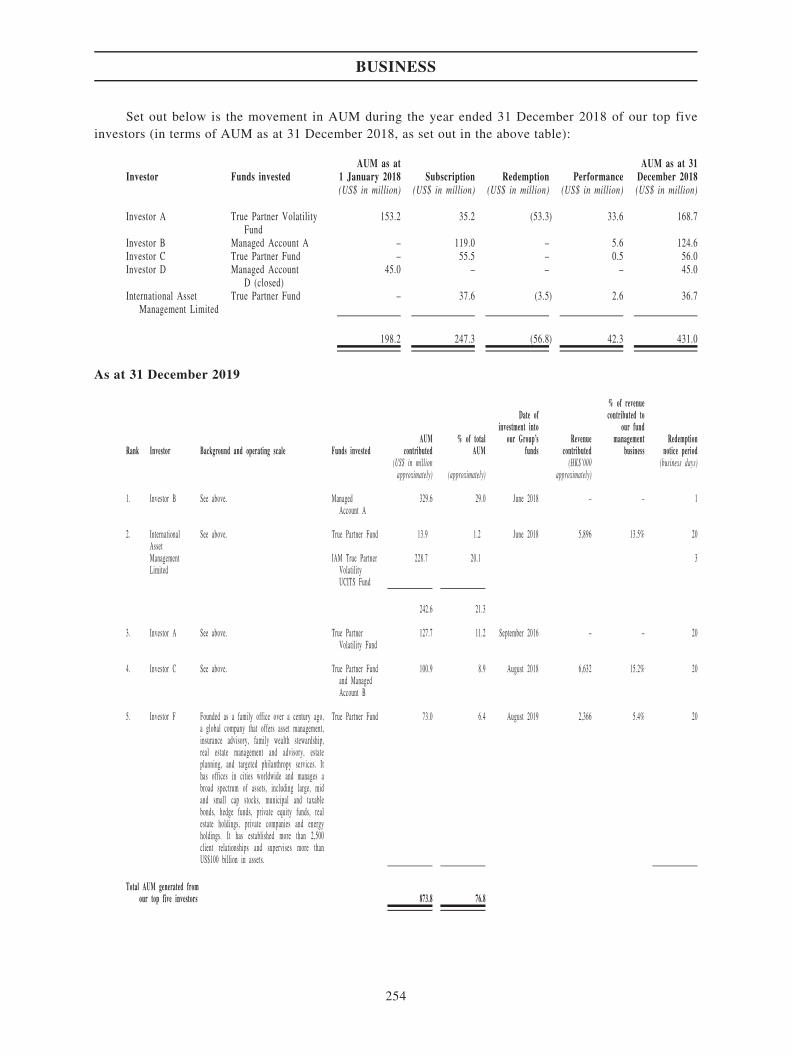

For a breakdown of our Group’s AUM and revenue by major type of customers during the Track RecordPeriod, please see the section headed ‘‘Business – Our investors’’ in this prospectus. In particular, our AUMcontributed by collective investment undertakings increased significantly from US$446 million as at 31 December2018 to US$936 million as at 31 December 2019, which was mainly attributable to the capital contributed byInvestor B and International Asset Management Limited. Revenue from collective investment undertakings, familyoffices, high-net-worth individuals and financial institutions decreased significantly between the years ended 31December 2018 and 2019, which was mainly due to the decrease in performance fee income during 2019. From thethree months ended 31 March 2019 to the same period in 2020, revenue generated across the different major types ofcustomers (apart from endowments) significantly increased. Further, the amount of AUM also increased across thedifferent major customer types from the end of 2019 to 31 March 2020. Throughout the Track Record Period, over 30investors invested in our funds and managed accounts.

Geographical information of our revenue for the years ended 31 December 2018 and 2019 and the three monthsended 31 March 2019 and 2020 is set out in note 4 of the Accountants Report at Appendix IA to the prospectus.

Please refer to the sections headed ‘‘Business – Our Investors’’ and ‘‘Financial Information – Overview’’ formore details.

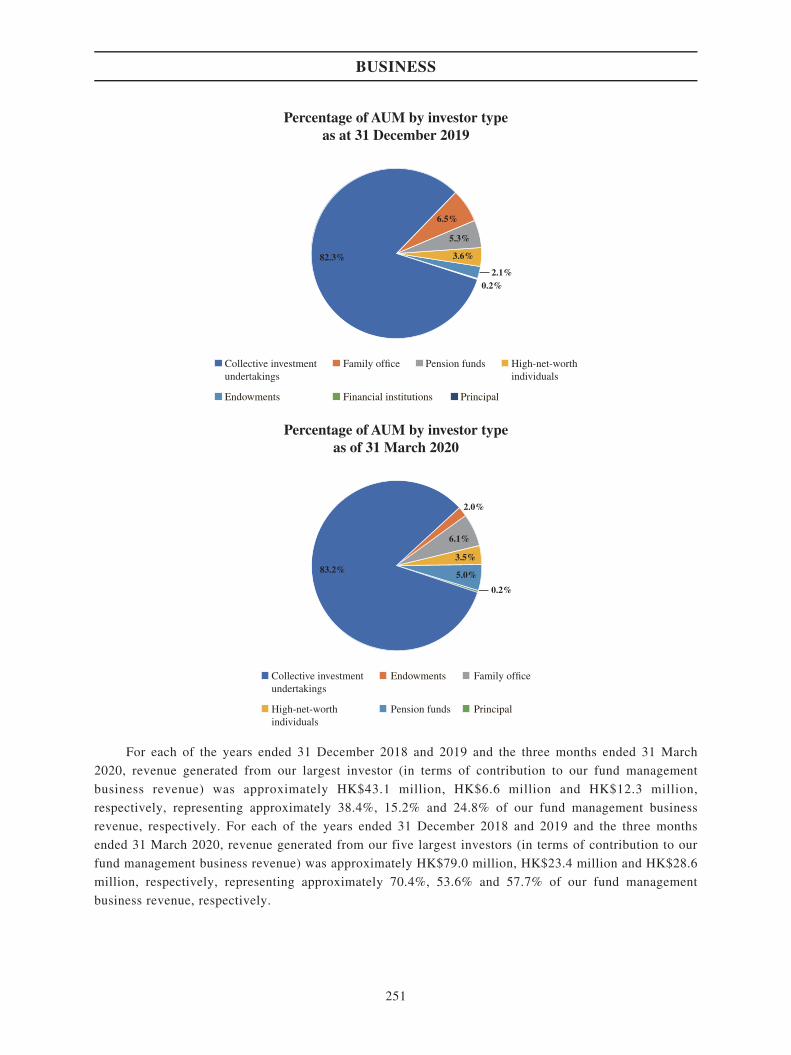

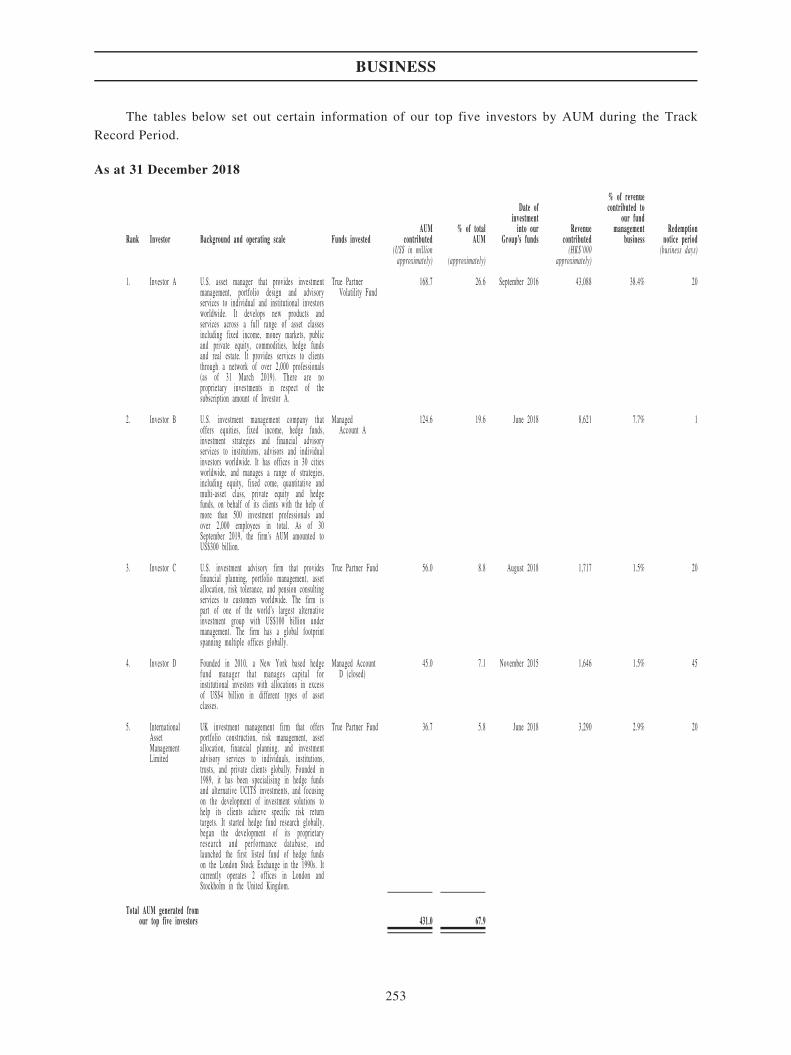

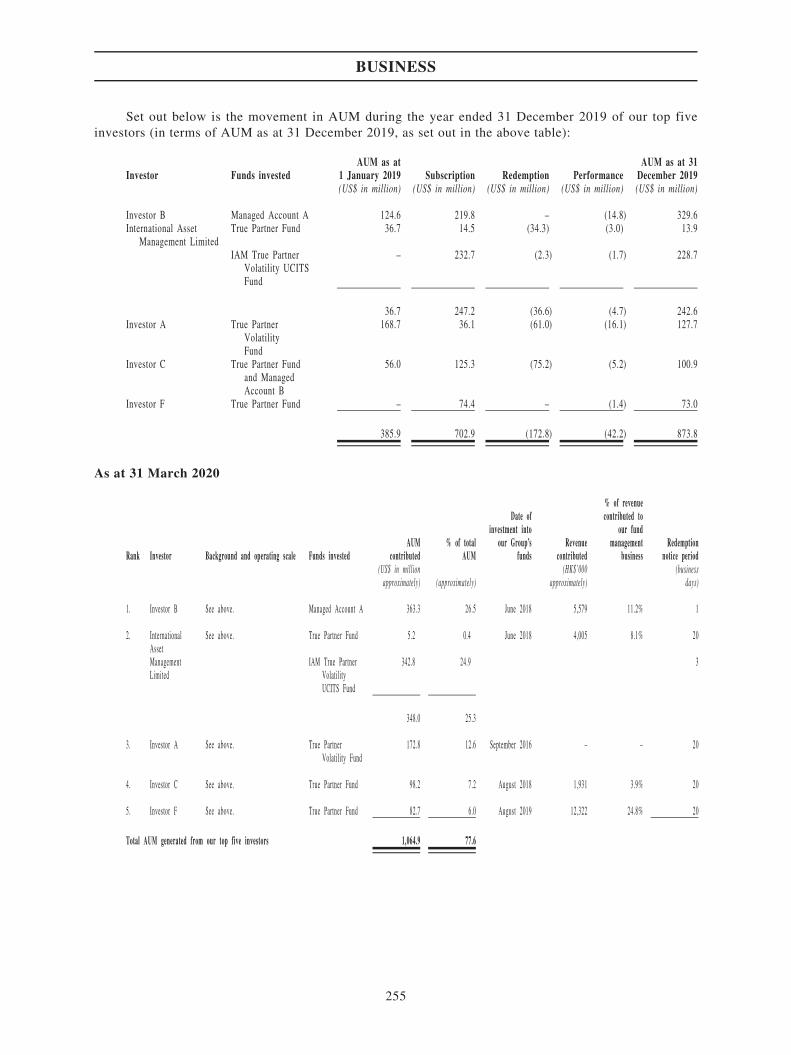

For each of the years ended 31 December 2018 and 2019 and the three months ended 31 March 2020, revenuegenerated from our five largest investors (in terms of contribution to our fund management business revenue)accounted for approximately 70.40%, 53.6% and 57.7% of our fund management business revenue, respectively, andrevenue generated from our largest investor (in terms of contribution to our fund management business revenue)accounted for approximately 38.4%, 15.2% and 24.8% of our fund management business revenue, respectively. Oursubsidiary True Partner Holding Limited holds a 2.73% equity interest in CSC Futures which was our third largestinvestor by contribution to our fund management business revenue in 2018 and third largest investor by AUM as at31 December 2018. For more information on our relationship with CSC Futures and its investments in our funds,please see the sections headed ‘‘Business – Our Investments’’, ‘‘Business – Our investors – Clients and investors whoare related persons of our Group’’ and ‘‘Relationship with the Capital Group’’ in this prospectus.

In order to demonstrate alignment of interests between our funds’ investors and our Group, our subsidiary TruePartner Advisor Limited has invested in True Partner Fund. Please see the section headed ‘‘Business – OurInvestments’’ in this prospectus for further information.

Our service providers

Our major service providers over the Track Record Period included (i) capital introduction partners who assistus in sourcing investors; (ii) providers of office space in Hong Kong; (iii) a consultant who provided services relatingto, without limitation, market research and business development as well as providing guidance and advisory (withsuch consultancy ceasing in 2019, subsequent to which the consultant became a connected person); (iv) a softwareconsultancy service provider in respect of the provision of remote support, internet and consultancy services; and (v)a contractor to provide administrative support in connection with the Listing.

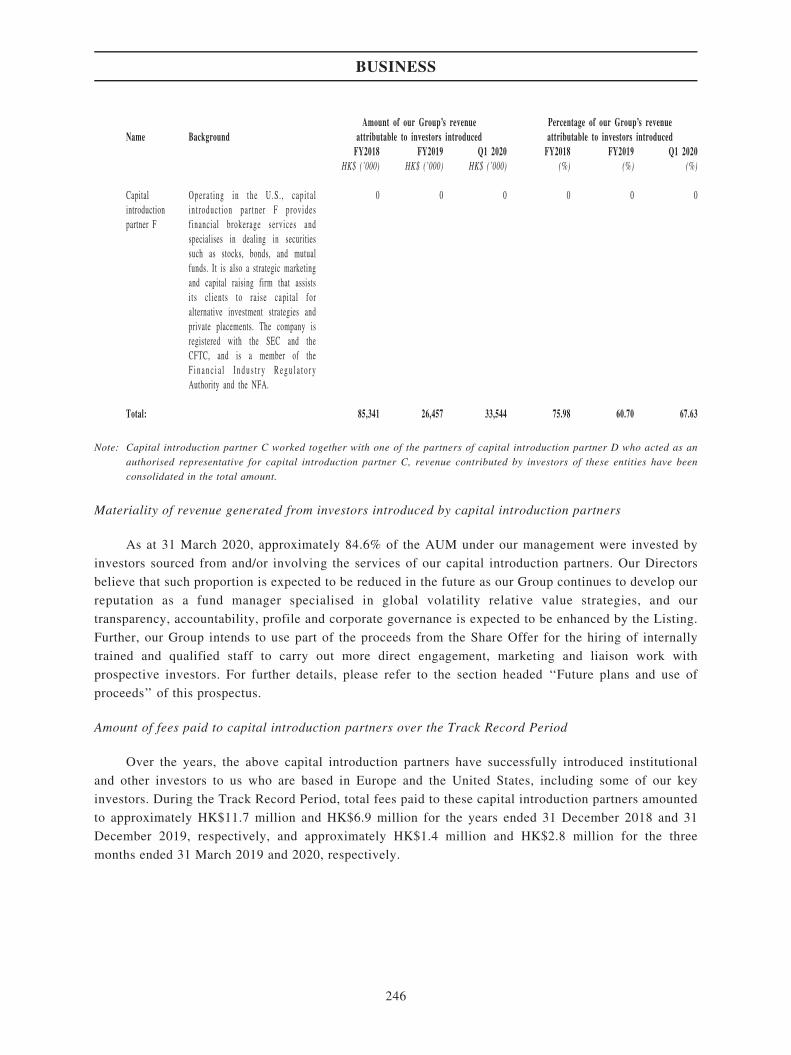

We engage capital introduction partners to assist us in sourcing institutional investors and certain high-net-worth individuals for our funds. The amount of fees paid to such capital introduction partners amounted toapproximately 18.9%, 15.8% and 13.4% of our gross management fee income in 2018 and 2019 and the three monthsended 31 March 2020, respectively, and 8.9% and 2.5% of our gross performance fee income in 2018 and the threemonths ended 31 March 2020, respectively. As we continue to grow our brand and reputation as a fund managerspecialised in global volatility relative value strategies, an increasing number of potential investors have contacted usdirectly with a view to considering investing in our funds. As such, we expect to reduce our use of capitalintroduction partners in the future and to use part of the net proceeds from the Share Offer for hiring staff to carryout more direct engagement, marketing and liaison work with prospective investors. Please refer to the sectionheaded ‘‘Future plans and use of proceeds’’ in this prospectus for further details.

In addition, various professional parties, including administrators, prime brokers, custodian and legal counsels,provide services to the funds under our management.

SUMMARY

5

Risks relating to our business operations

Due to the nature of our operations, our Group faces various risks (in additional to legal and compliance risks)including, without limitation:

(i) redemption risk: we are subject to redemption risk, with only a small portion of our invetors in ourfunds/managed accounts (only approximately 4.3% of our AUM) is subject to a lock-up period of 12months, with one investor’s lock-up being released gradually in a staggered manner) and most of ourinvestors may redeem their investments with short notice (generally 20 business days or less priornotice, with some investors entitled to redeem their investments by giving as short as one to three days’prior notice, despite this being within the industry norm); and

(ii) key man risk: we depend on on our senior management and key personnel for our business andoperations; most of them may terminate their employment with us by providing short prior notices andthe departure of one or more of them may potentially impair our operations, business development orimplementation of our business strategies.

For further details of risks relevant to our operations including, inter alia, trading risks, counterparty risks,liquidity risk and market risks, plese refer to the section ‘‘Business – Risk management and internal control – Riskmanagement’’ of this prospectus.

PRINCIPAL RISK FACTORS

Our business faces risks including those set out in the section headed ‘‘Risk Factors’’ in this prospectus. Someof the major risks are summarised below:

• we are a growing business with a limited number of products and investors (most of them do not havelong business relationships with our Group) and our business and prospects and may materially andadversely affected by the withdrawal of investments due to loss of confidence in our trading strategy orotherwise, or the departure of senior management and key personnel whom we materially rely on for ourbusiness operations. However, our investors are typically not subject to lock-up on their investments(with only 4.3% of AUM subject to a lock-up period of 12 months, with one investor’s lock-up beingreleased gradually in a staggered manner) and they (including two large institutional investors whoaccounted for 48% of our revenue for the year ended 31 December 2018) may redeem their investmentsat any time by providing short prior notice (generally 20 business days or less prior notice, with someinvestors entitled to redeem their investments by giving as short as one to three days’ prior notice,despite this being within the industry norm). Material redemption decisions by our top investors (whichmay result in considerations, such as change in investment appetites or preference or other factorsbeyond our control) may materially and adversely affect our fee income, potentially lead to net lossesbeing incurred, and may adversely affect our ability to attract new investments and our businessprospects. Furthermore, our profitability may be adversely impacted by potential increases in our costsincurred after the Listing, as we have to hire additional staff under our business expansion plan and tooffer higher base salaries to attract the necessary qualified staff and we may offer better remunerationpackages (including higher base salaries and/or higher bonuses) to our staff to recognise the contributionthat our staff have made to our Group over the years and the degree of experience and seniority that theyhave attained after working with our Group for a period of time.

• we depend on our senior management and key personnel (in particular, our co-chief investment officersfrom the perspective of executing our trading strategy as well as our chief technology officer and globalhead of research and development for carrying out technology and software development functions) forour business and operations and most of them may terminate their employment with us by providingshort prior notices (generally ranging from one to three months, which is similar to the length of priornotice we are required to give to terminate their employment). Whilst the departure of one or more ofthem may potentially impair our operations, business development or implementation of our businessstrategies, we do not maintain key man insurance.

• our revenue decreased between 2018 and 2019, and we suffered a net loss after tax for the year ended 31December 2019. There is no assurance that our revenue and net profit/loss after tax position will notmaterially deteriorate in the future;

• our volatility trading strategy is relatively less effective during low market volatility periods which mayimpact investor appetite for our funds and managed accounts;

• our Group’s results of operations and financial condition may be materially and adversely affected by theinvestment performance of our funds and managed accounts, as unsatisfactory performance would affectour ability to generate fees and may lead to reduced purchases, subscriptions, redemptions and/orwithdrawals from our funds and managed accounts; in particular, where the amount of management andperformance fees we are entitled to charge is not sufficient to cover our operating costs we may incur aloss (for reference, we had an accumulated loss of approximately HK$19.8 million as at 1 January 2018due to loss-making periods over the start-up stages of our funds);

• we depend on our senior management and key personnel (including our co-chief investment officers, Mr.Godefriedus Jelte Heijboer and Mr. Tobias Benjamin Hekster, who are Shareholders in our Company, inleading execution of our trading strategy) who possess extensive experience, knowledge and expertise intrading, market making and technology development; nevertheless, we do not maintain key man

SUMMARY

6

insurance for such senior management or key personnel and their engagement may be terminated withoutrestrictions in their terms of employment at any time. The loss of members of our senior managementteam and/or key personnel and/or the inability to find suitable replacements may significantly disrupt ourbusiness and adversely impair our business prospects and the implementation of our business objectivesand strategies;

• our growth in profits substantially depends on increasing our AUM, and there may be a decline in ourAUM as investors may withdraw and/or redeem their investments in our funds and managed accounts,and we may fail to attract new AUM in the future if investors are not attracted to our global equityrelative value volatility strategy;

• our top investors may reduce, withdraw or redeem their investments in our funds by giving very shortnotice (generally 20 business days or less prior notice, with some investors entitled to redeem theirinvestments by giving as short as one to three days’ prior notice) due to changes in their investmentappetite and preference as well as other factors beyond our or their control; and

• a significant portion of our fee income is derived from performance fees which are subject to thefluctuations in our funds’ investment performance and thus increase the volatility of our Group’searnings.

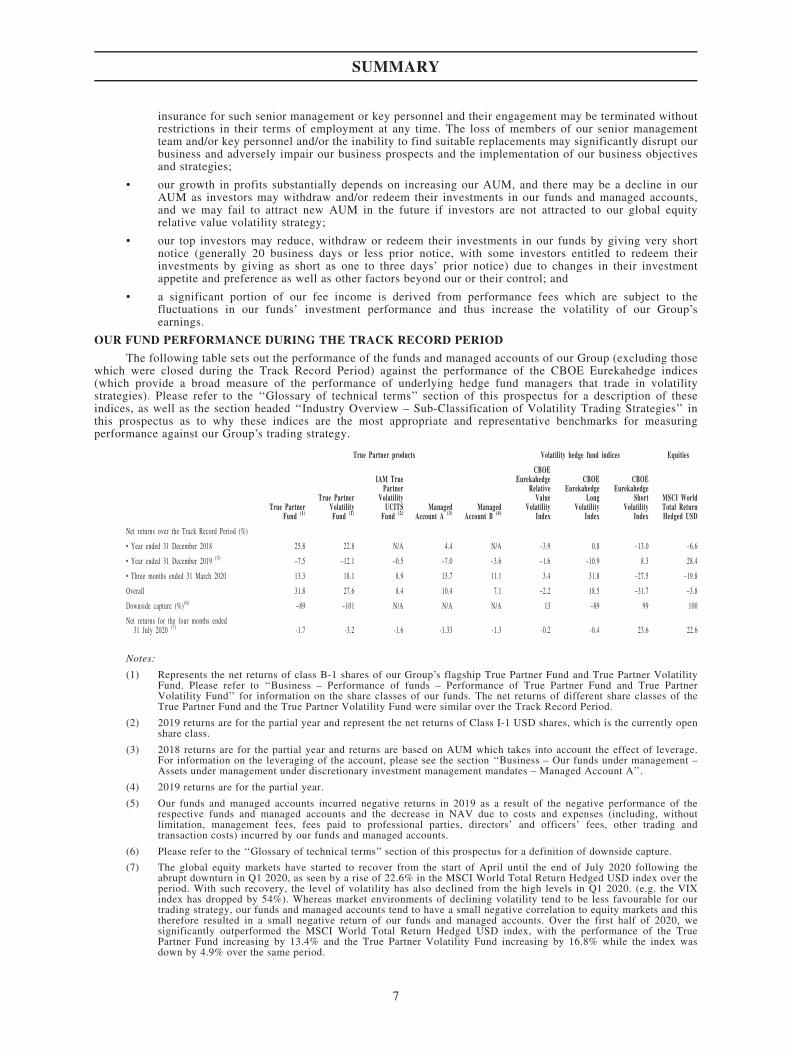

OUR FUND PERFORMANCE DURING THE TRACK RECORD PERIOD

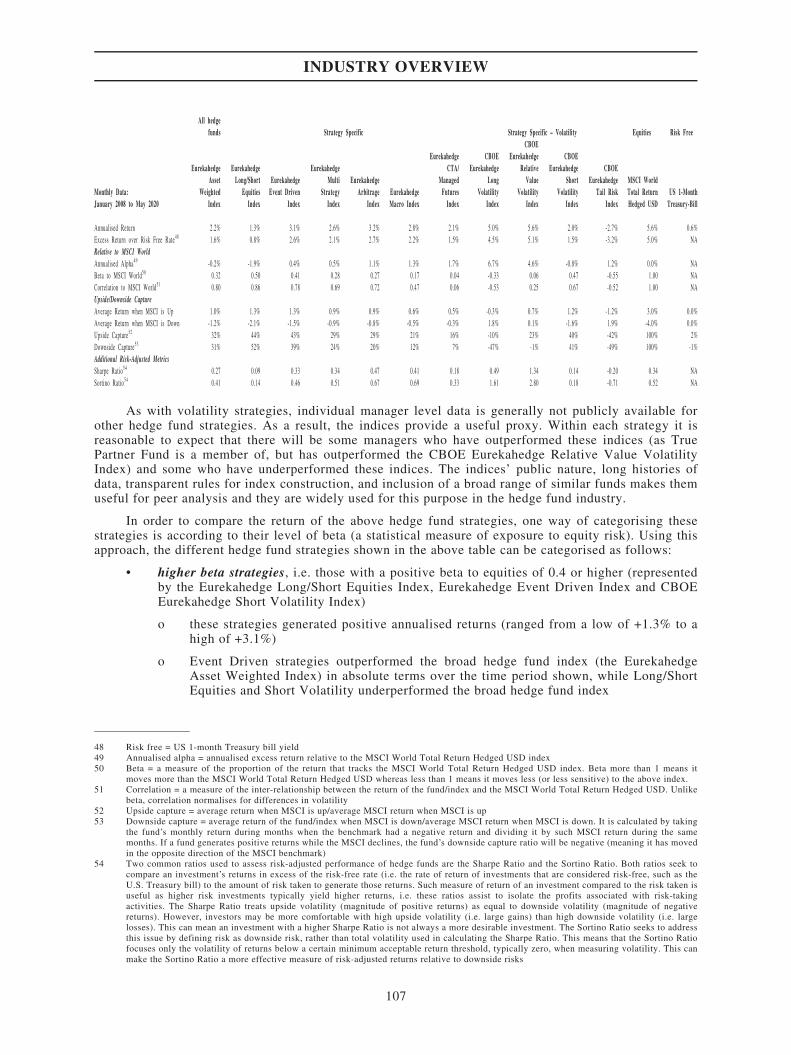

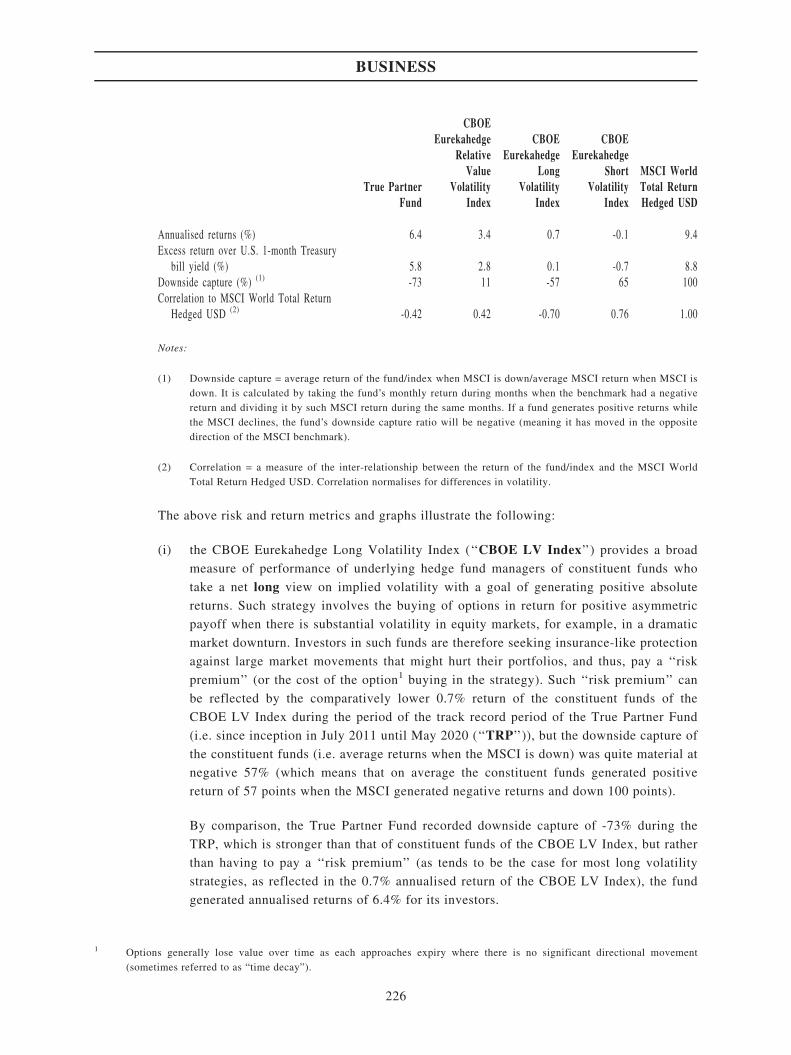

The following table sets out the performance of the funds and managed accounts of our Group (excluding thosewhich were closed during the Track Record Period) against the performance of the CBOE Eurekahedge indices(which provide a broad measure of the performance of underlying hedge fund managers that trade in volatilitystrategies). Please refer to the ‘‘Glossary of technical terms’’ section of this prospectus for a description of theseindices, as well as the section headed ‘‘Industry Overview – Sub-Classification of Volatility Trading Strategies’’ inthis prospectus as to why these indices are the most appropriate and representative benchmarks for measuringperformance against our Group’s trading strategy.

True Partner products Volatility hedge fund indices Equities

True PartnerFund (1)

True PartnerVolatilityFund (1)

IAM TruePartner

VolatilityUCITS

Fund (2)Managed

Account A (3)Managed

Account B (4)

CBOEEurekahedge

RelativeValue

VolatilityIndex

CBOEEurekahedge

LongVolatility

Index

CBOEEurekahedge

ShortVolatility

Index

MSCI WorldTotal ReturnHedged USD

Net returns over the Track Record Period (%)

• Year ended 31 December 2018 25.8 22.8 N/A 4.4 N/A –3.9 0.8 –13.0 –6.6

• Year ended 31 December 2019 (5)–7.5 –12.1 –0.5 –7.0 –3.6 –1.6 –10.9 8.3 28.4

• Three months ended 31 March 2020 13.3 18.1 8.9 13.7 11.1 3.4 31.8 –27.5 –19.8

Overall 31.8 27.6 8.4 10.4 7.1 –2.2 18.5 –31.7 –3.8

Downside capture (%)(6) –89 –101 N/A N/A N/A 13 –89 99 100

Net returns for the four months ended31 July 2020 (7) -1.7 -3.2 -1.6 -1.33 -1.3 -0.2 -0.4 23.6 22.6

Notes:

(1) Represents the net returns of class B-1 shares of our Group’s flagship True Partner Fund and True Partner VolatilityFund. Please refer to ‘‘Business – Performance of funds – Performance of True Partner Fund and True PartnerVolatility Fund’’ for information on the share classes of our funds. The net returns of different share classes of theTrue Partner Fund and the True Partner Volatility Fund were similar over the Track Record Period.

(2) 2019 returns are for the partial year and represent the net returns of Class I-1 USD shares, which is the currently openshare class.

(3) 2018 returns are for the partial year and returns are based on AUM which takes into account the effect of leverage.For information on the leveraging of the account, please see the section ‘‘Business – Our funds under management –Assets under management under discretionary investment management mandates – Managed Account A’’.

(4) 2019 returns are for the partial year.

(5) Our funds and managed accounts incurred negative returns in 2019 as a result of the negative performance of therespective funds and managed accounts and the decrease in NAV due to costs and expenses (including, withoutlimitation, management fees, fees paid to professional parties, directors’ and officers’ fees, other trading andtransaction costs) incurred by our funds and managed accounts.

(6) Please refer to the ‘‘Glossary of technical terms’’ section of this prospectus for a definition of downside capture.

(7) The global equity markets have started to recover from the start of April until the end of July 2020 following theabrupt downturn in Q1 2020, as seen by a rise of 22.6% in the MSCI World Total Return Hedged USD index over theperiod. With such recovery, the level of volatility has also declined from the high levels in Q1 2020. (e.g. the VIXindex has dropped by 54%). Whereas market environments of declining volatility tend to be less favourable for ourtrading strategy, our funds and managed accounts tend to have a small negative correlation to equity markets and thistherefore resulted in a small negative return of our funds and managed accounts. Over the first half of 2020, wesignificantly outperformed the MSCI World Total Return Hedged USD index, with the performance of the TruePartner Fund increasing by 13.4% and the True Partner Volatility Fund increasing by 16.8% while the index wasdown by 4.9% over the same period.

SUMMARY

7

In respect of the performance of funds and managed accounts which were closed during the Track RecordPeriod, the performance of (i) Managed Account C was +14% in 2018 and 0% in 2019; (ii) Managed Account D was+3% in 2018 and 0% in 2019; and (iii) co-branded fund A was +14% in 2018 and -2% in 2019.

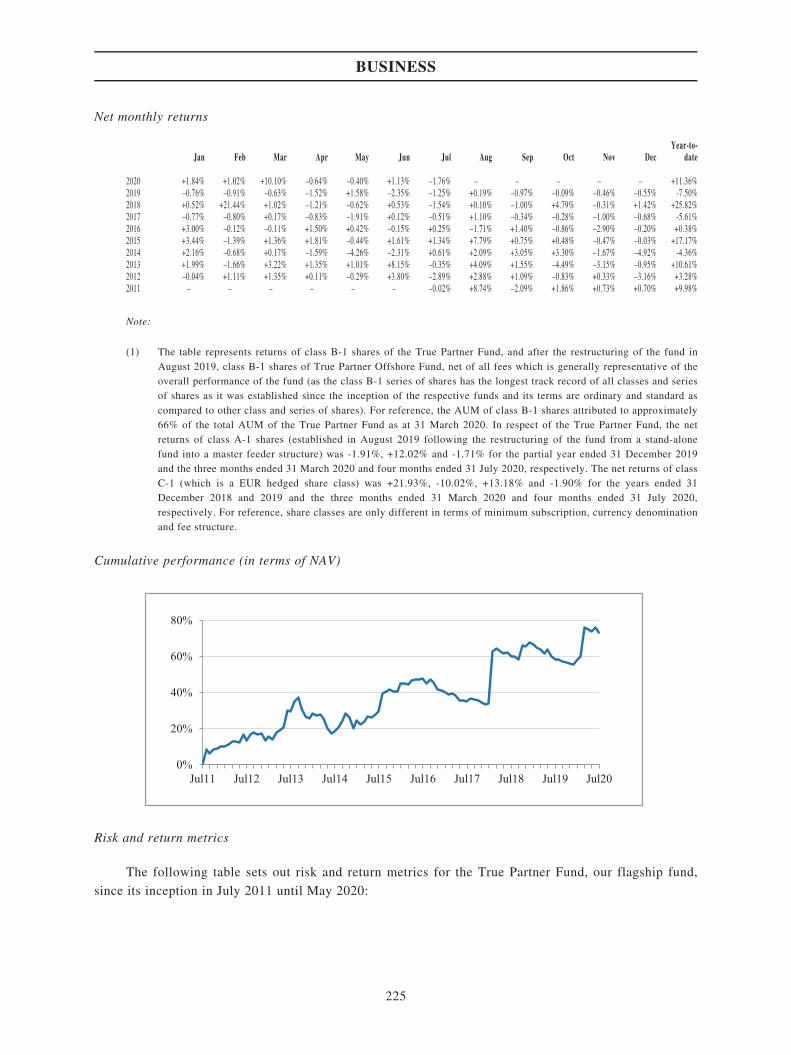

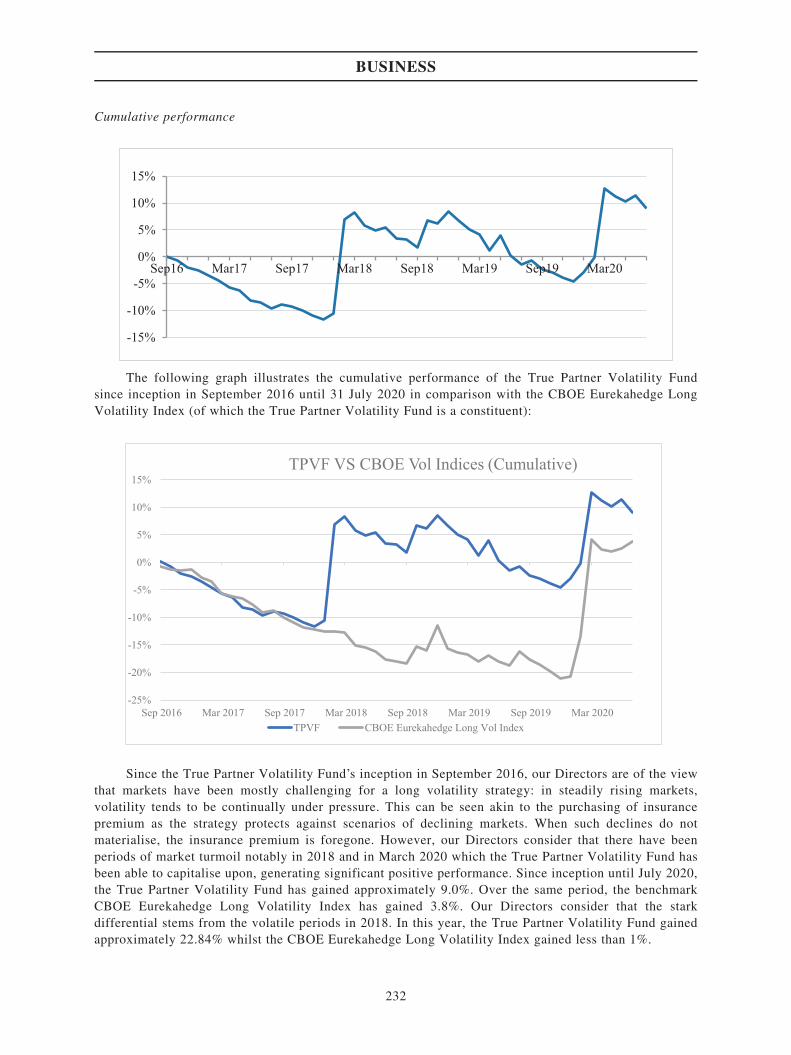

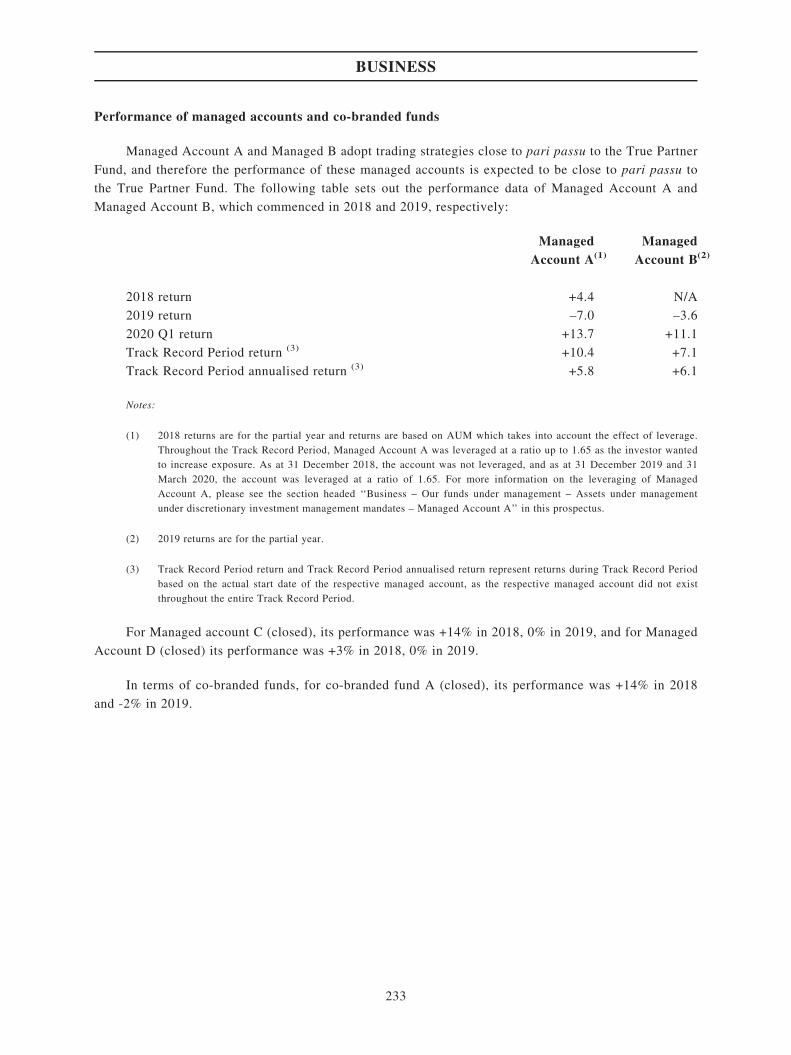

Our True Partner Fund, our flagship fund with the longest track record of our managed funds, generatedannualised returns from inception in 2011 until 31 July 2020 (being the latest practicable date of this information) ofapproximately +6.25%.

True Partner Volatility Fund, our other flagship fund, generated annualised returns from inception inSeptember 2016 until 31 July 2020 (being the latest practicable date of this information) of +2.23%.

For further details on the performance of our funds and managed accounts (including net monthly returns ofour flagship funds, True Partner Fund and True Partner Volatility Fund), please refer to the sections headed‘‘Business – Performance of funds’’ in this prospectus.

PERFORMANCE OVER THE TRACK RECORD PERIOD

Due to our trading strategy, the funds and managed accounts under our management benefited and monetisedgains from opportunities presented at times when there was a spike in volatility in equity markets. In 2018, the fundsand managed accounts of our Group benefited from ‘‘Volmageddon’’ (an unorderly unwinding of positions by over-exposed funds (i.e. those which had accumulated large volatility short positions (or sold significant number ofoptions) which made them vulnerable to sudden market shocks) by buying back short positions in options contractswhich they had sold following an extended period of market calmness that resulted in sizable volatility spreadopportunities) in February as well as the declines in markets (dragged by investors’ fear of rising interest rates) inOctober (please refer to the section ‘‘Business – Performance of Funds – Performance of True Partner Fund and TruePartner Volatility Fund’’ in this prospectus for further details). As such, during the year, the NAV of funds andmanaged accounts under our management grew substantially by 97.20% to approximately US$635 million, and wegenerated gross management fees and performance fees of approximately HK$17.8 million and HK$94.5 millionpursuant to the relevant investment mandates respectively.

During 2019 however, the equity markets were relatively less volatile compared to 2018 and this led to lessvolatility spread opportunities which our Group could capitalise on. During such less active or volatile period, ourtrading strategy would be to limit positions and transaction costs as there would be generally less opportunities.During the year, we generated gross management fees of approximately HK$43.6 million while our grossperformance fee was only approximately HK$8,000 due to less market volatility opportunities, but the AUM of ourGroup continued to grow during the period by 79.21% to approximately US$1.14 billion, and as explained in theIndustry Report, such AUM growth was attributable to our strong performance during volatile periods or marketdownturns due to the strong downside capture of our funds and managed accounts.

For quantitative information regarding historical volatility of equity markets in 2018 and 2019 and the firsthalf of 2020 as well as details of the impact of less or more volatile equity markets on our financial performance,please refer to the section ‘‘Financial information – Overview’’ of this prospectus.

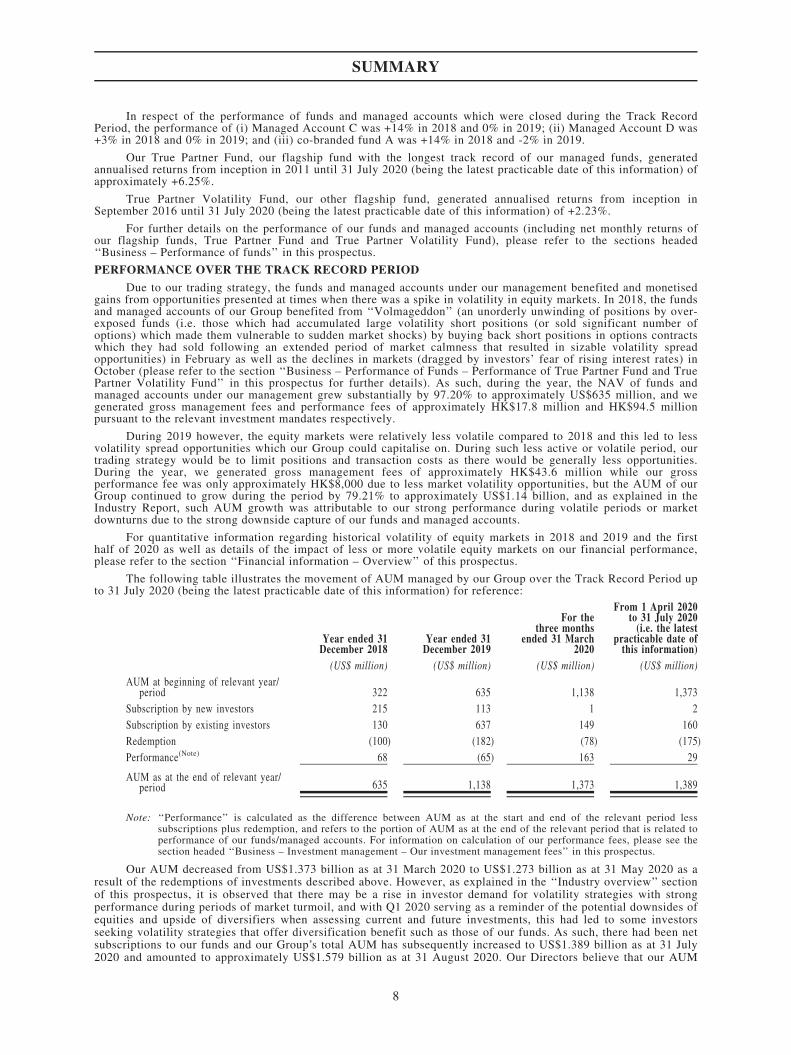

The following table illustrates the movement of AUM managed by our Group over the Track Record Period upto 31 July 2020 (being the latest practicable date of this information) for reference:

Year ended 31December 2018

Year ended 31December 2019

For thethree months

ended 31 March2020

From 1 April 2020to 31 July 2020(i.e. the latest

practicable date ofthis information)

(US$ million) (US$ million) (US$ million) (US$ million)AUM at beginning of relevant year/

period 322 635 1,138 1,373Subscription by new investors 215 113 1 2Subscription by existing investors 130 637 149 160Redemption (100) (182) (78) (175)Performance(Note) 68 (65) 163 29

AUM as at the end of relevant year/period 635 1,138 1,373 1,389

Note: ‘‘Performance’’ is calculated as the difference between AUM as at the start and end of the relevant period lesssubscriptions plus redemption, and refers to the portion of AUM as at the end of the relevant period that is related toperformance of our funds/managed accounts. For information on calculation of our performance fees, please see thesection headed ‘‘Business – Investment management – Our investment management fees’’ in this prospectus.

Our AUM decreased from US$1.373 billion as at 31 March 2020 to US$1.273 billion as at 31 May 2020 as aresult of the redemptions of investments described above. However, as explained in the ‘‘Industry overview’’ sectionof this prospectus, it is observed that there may be a rise in investor demand for volatility strategies with strongperformance during periods of market turmoil, and with Q1 2020 serving as a reminder of the potential downsides ofequities and upside of diversifiers when assessing current and future investments, this had led to some investorsseeking volatility strategies that offer diversification benefit such as those of our funds. As such, there had been netsubscriptions to our funds and our Group’s total AUM has subsequently increased to US$1.389 billion as at 31 July2020 and amounted to approximately US$1.579 billion as at 31 August 2020. Our Directors believe that our AUM

SUMMARY

8

will continue to increase as the equity markets are expected to remain volatile for the remainder of 2020. For detailsof the movement in AUM during the Track Record Period of our top five investors (in terms of AUM as at 31December 2018, 2019 and 31 March 2020), please see the section headed ‘‘Business – Our Investors – Our top fiveinvestors during the Track Record Period’’ in this prospectus.