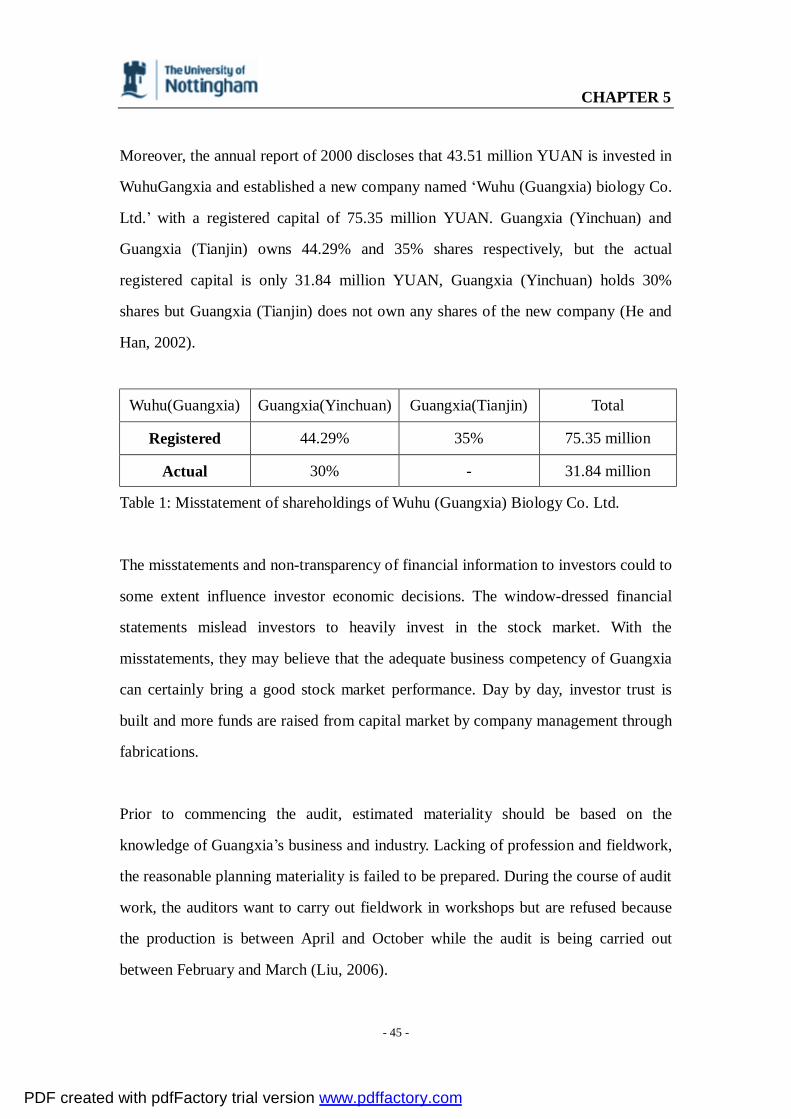

Embed Size (px)

Citation preview

UNIVERSITY OF NOTTINGHAM

The Audit Risk Associated with Fraudulent Accounting of Listed

Companies in China : A Case Study

By

Lei Lei

MA Finance and Investment

PDF created with pdfFactory trial version www.pdffactory.com

Acknowledgement

Acknowledgement

Taking this opportunity, first of all, I would like to thank my supervisor Mark Billings,

for his invaluable comments and suggestions in guiding me finishing the dissertation.

Without his well-organized schedule, I would never finish the dissertation on time.

I am also appreciated with the help from my good friends, Luping Sun, Chunhui Lian,

Xiaoqi Zhu, Lerui Guo etc. Thanks for being with me for this wonderful year and

supports given during my gloomy days. Especially, I would like to thank my

boyfriend, Zhigang Zhao, who always supports and helps me whenever I am needed.

Lastly, I must express my sincere love to my parents, who encourage and support me

all the way. Without their faithful trust and enduring love, I would not finish my

degree and scholastic life in the University of Nottingham.

PDF created with pdfFactory trial version www.pdffactory.com

Abstract

Abstract

This dissertation studies the discipline of auditing and fraudulent accounting. The

investigation of literature review initially concerns about the basic concepts of

auditing and audit risk, and then followed by fraudulent accounting which has direct

impact on audit risk. The literature tries to discuss audit risk and fraudulent

accounting separately and then presents the relationship between the two.

Based upon this, firstly, backgrounds of Chinese auditing environment are analyzed to

have a preview of the conditions in the case, and then a case study is employed as the

methodology to find the gap between literature review and the truth in case study.

From the analysis, it can be concluded that literature can explain most of the truth in

the case except some particular points that are of Chinese characteristics.

Finally, conclusion is derived from comparisons and contrast between Guangxia and

Enron to stress the culture difference in terms of corporate scandals. Possible

suggestions are given from the inspiration of U.S. Sabanes-Oxley Act to solve

Chinese corporate scandal problems and improve business performance in stock

market. Limitations are also given to state the constraints to this dissertation and any

improvements that maybe needed.

PDF created with pdfFactory trial version www.pdffactory.com

Abbreviations

Abbreviations

APC: Auditing Practices Committee

CFO: Chief Financial Officer

CPA: Chartered Public Accountant

CICPA: Chinese Institute of Certified Public Accountants

CSRC: China Securities Regulatory Commission

EPS: Earnings per share

FASB: Financial Accounting Standards Board

GAAP: Generally Accepted Accounting Principles

IAS: International Accounting Standards

IASB: The International Accounting Standards Board

IASC: The International Accounting Standards Committee

IIA: Institute of Internal Auditors

IOD: The Institute of Directors

IFRS: International Financial Reporting Standards

MOF: The Ministry of Finance

OECD: Organization for Economic Cooperation and Development

PCAOB: Public Company Accounting Oversight Board

PRC: People’s Republic of China

SAS: Statement on Accounting Standards

SEC: Securities and Exchange Commission

SOE: State-owned Enterprises

SOX: Sarbanes-Oxley

SPE: Special Purpose Entities

PDF created with pdfFactory trial version www.pdffactory.com

CONTENTS

i

CONTENTS

Acknowledgement

Abstract

Abbreviations

Chapter 1 Introduction.............................................................................................1

1.1. Backgrounds and motivations…………………………………………………….1

1.2. Aims and objectives………………………………………………………………2

1.3. Methodology……………………………………………………………………...2

1.4. Structures of the dissertation……………………………………………………...3

Chapter 2 Literature Review....................................................................................4

2.1. Overview of Auditing……………………………………………………………..4

2.1.1. Introduction…………………………………………………………………4

2.1.2. The principles of true and fair view………………………………………...4

2.1.3. Accounting policy…………………………………………………………..6

2.1.4. Materiality…………………………………………………………………..7

2.1.5. Audit failure………………………………………………………………..9

2.2. Audit Risk………………………………………………………………………..11

2.2.1. Concept of audit risk………………………………………………………11

2.2.2. Identifying and assessing audit risk……………………………………….13

2.2.3. Relationship between materiality, audit risk and audit planning…………..14

2.2.4. Corporate governance……………………………………………………...15

2.2.5. Internal audit………………………………………………………………17

2.2.6. Auditor independence……………………………………………………..18

2.3. Fraudulent Accounting…………………………………………………………..20

2.3.1. Introduction………………………………………………………………..20

PDF created with pdfFactory trial version www.pdffactory.com

CONTENTS

ii

2.3.2. Concept of fraudulent accounting…………………………………………21

2.3.3. Causes of fraudulent accounting…………………………………………..24

2.3.4. Fraud techniques…………………………………………………………..26

2.3.4.1. Overstatement of revenues…………………………………………26

2.3.4.2. Cultivate current assets and concealment of losses or liabilities…...27

2.3.4.3. Tamper with taxation……………………………………………….27

2.3.5. Consequences of fraudulent accounting…………………………………..28

Chapter 3 Methodology…………………………………………………………..30

Chapter 4 Overview of Chinese Auditing Environment………………………..33

4.1. Inherent pitfalls of equity structure and company management………………...33

4.2. Auditor profession……………………………………………………………….34

4.2.1. Due-risks…………………………………………………………………..34

4.2.2. Agency problems…………………………………………………………..36

4.3. Traits of domestic audit environment……………………………………………37

Chapter 5 Case Study……………………………………………………………39

5.1. Introduction……………………………………………………………………..39

5.2. Backgrounds of Guangxia fabrication case……………………………………..40

5.3. Case analysis…………………………………………………………………….42

5.3.1. The true and fair view……………………………………………………..42

5.3.2. Materiality…………………………………………………………………43

5.3.3. Audit failure……………………………………………………………….46

5.3.4. Audit risk…………………………………………………………………..47

5.3.5. Internal control…………………………………………………………….52

5.3.6. Auditor independence……………………………………………………..53

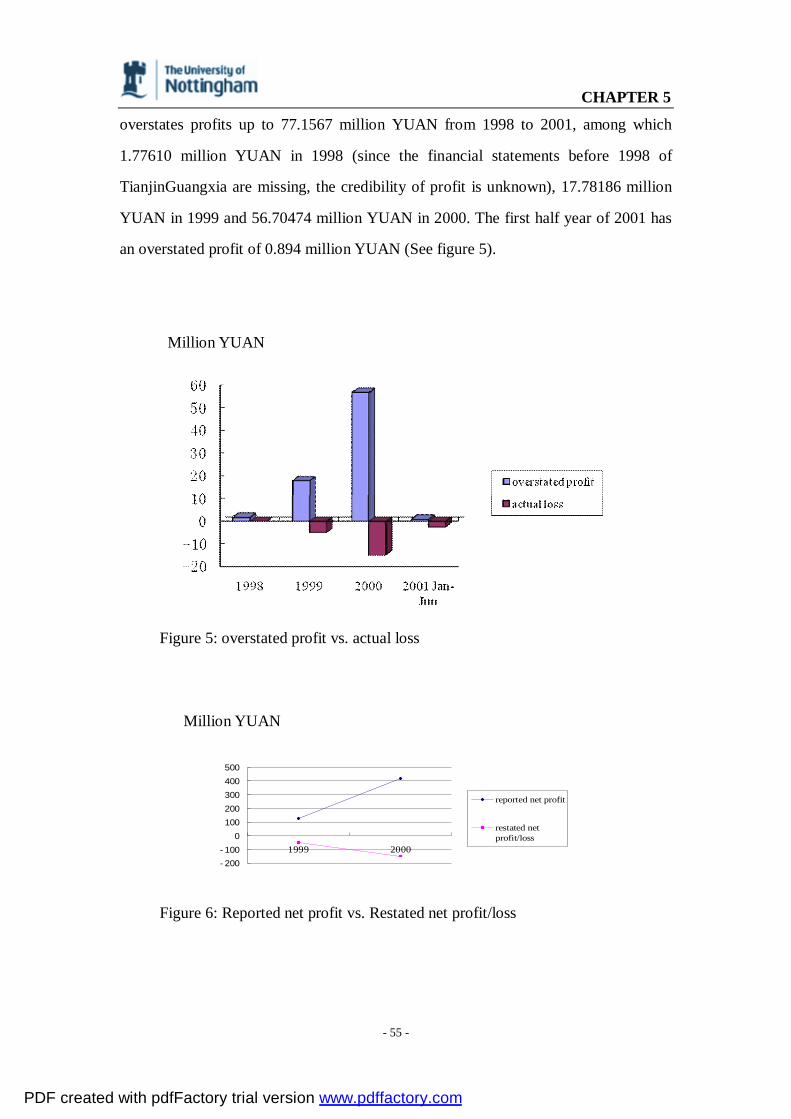

5.3.7. Accounting fraud…………………………………………………………..54

5.3.7.1. Overview…………………………………………………………..54

PDF created with pdfFactory trial version www.pdffactory.com

CONTENTS

iii

5.3.7.2. Fraud techniques…………………………………………………..59

5.3.7.2.1. Overstatement of revenue………………………………...59

5.3.7.2.2. Cultivate account receivables and concealment of losses..60

5.3.7.2.3. Tax………………………………………………………..61

5.3.7.3. Consequences of accounting fraud…………………………………62

5.3.7. Implications……………………………………………………………….63

5.3.7.1. Generalize Accounting Standards……………………………….....63

5.3.7.2. Auditor independence………………………………………………64

5.3.7.3. Rationality of investment…………………………………………..65

5.3.7.4. Corporate governance………………………………………………66

5.3.7.5. Lacking of comprehensive statue…………………………………..67

Chapter 6 Conclusion…………………………………………………………….69

6.1. Problems…………………………………………………………………………69

6.2. Guangxia vs. Enron……………………………………………………………...70

6.2.1. Similarities………………………………………………………………...70

6.2.2. Differences………………………………………………………………..72

6.2.3. Summary…………………………………………………………………..73

6.3. Post-Guangxia thinking………………………………………………………….74

6.4. Solutions to fraudulent accounting………………………………………………75

6.4.1. Tenure of audit firm………………………………………………………..75

6.4.2. Non-audit services…………………………………………………………75

6.4.3. Supervision………………………………………………………………..76

6.4.4. Internal control……………………………………………………………77

6.5. Limitations………………………………………………………………………78

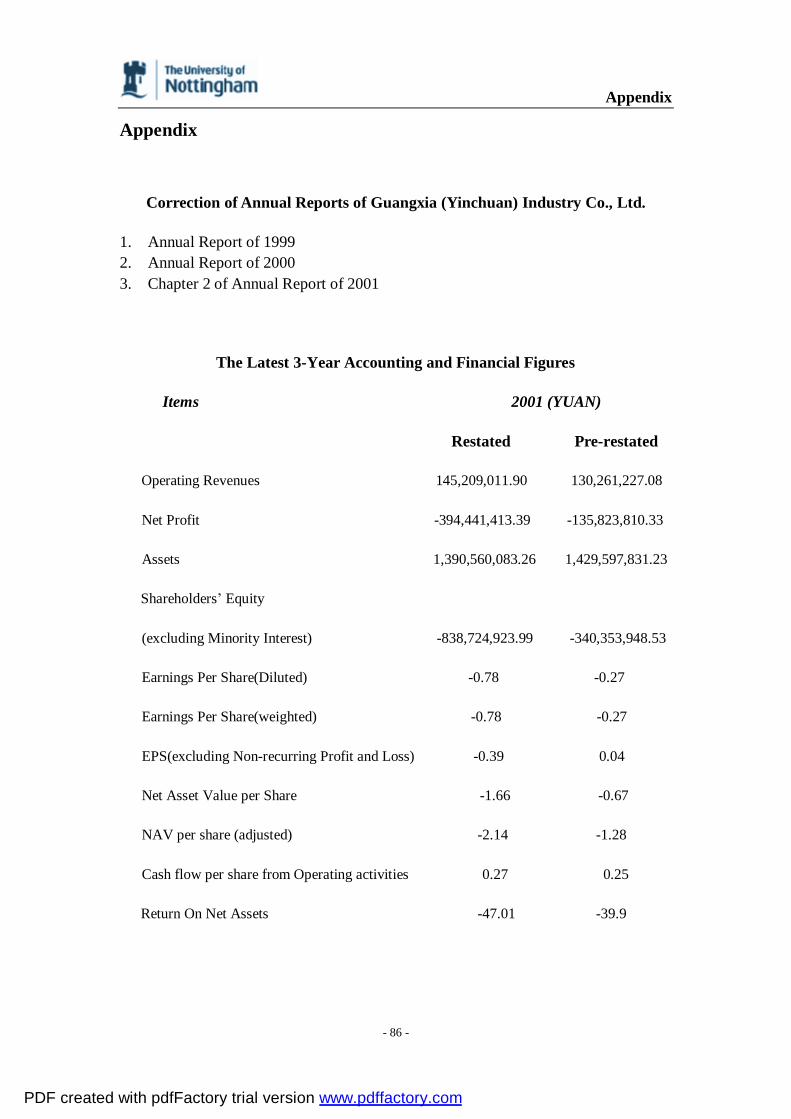

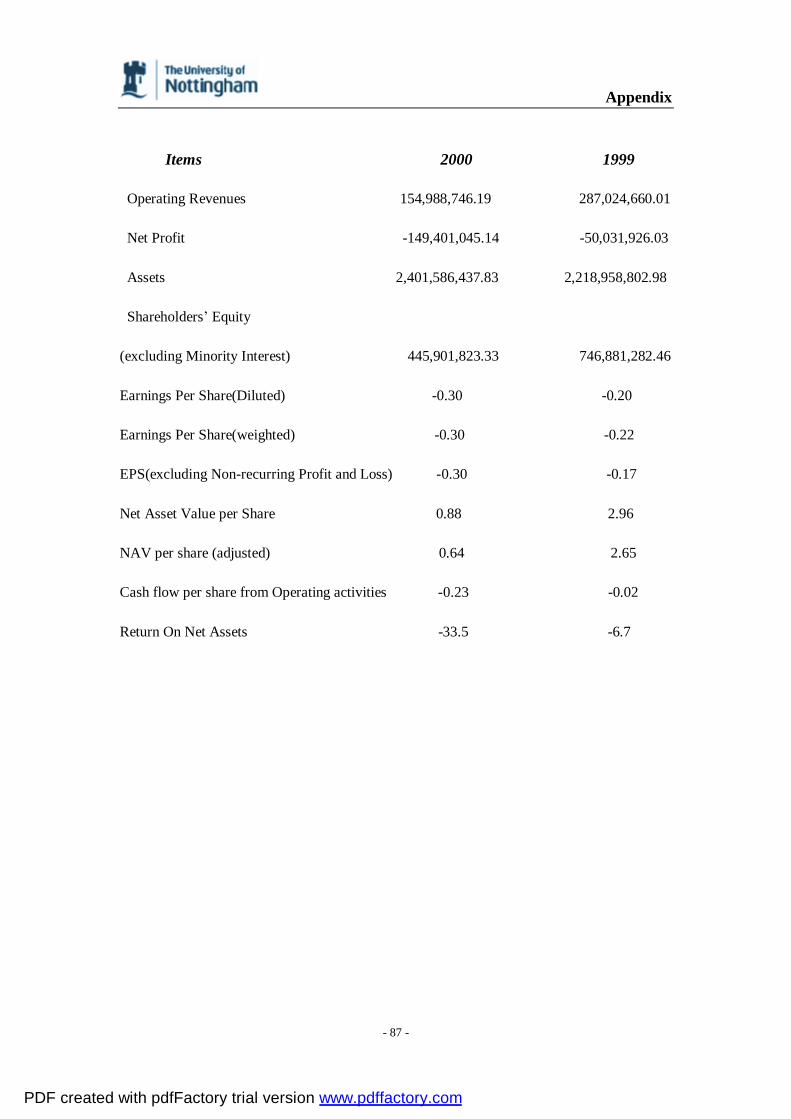

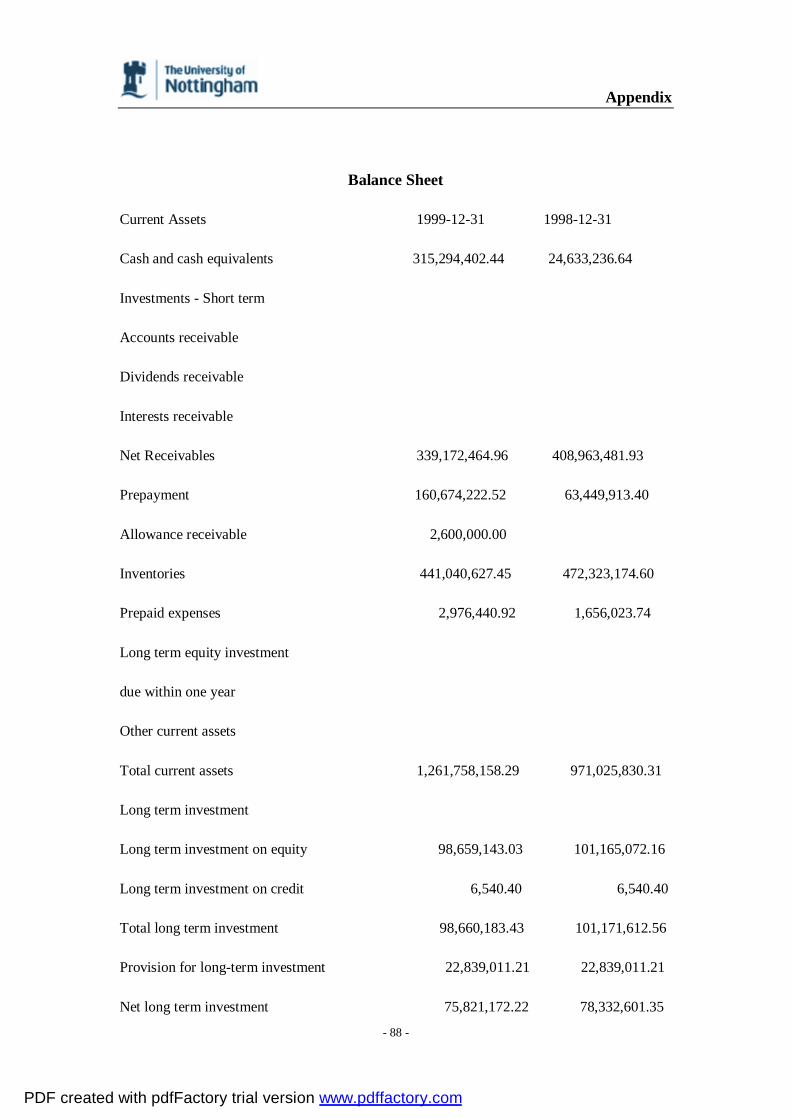

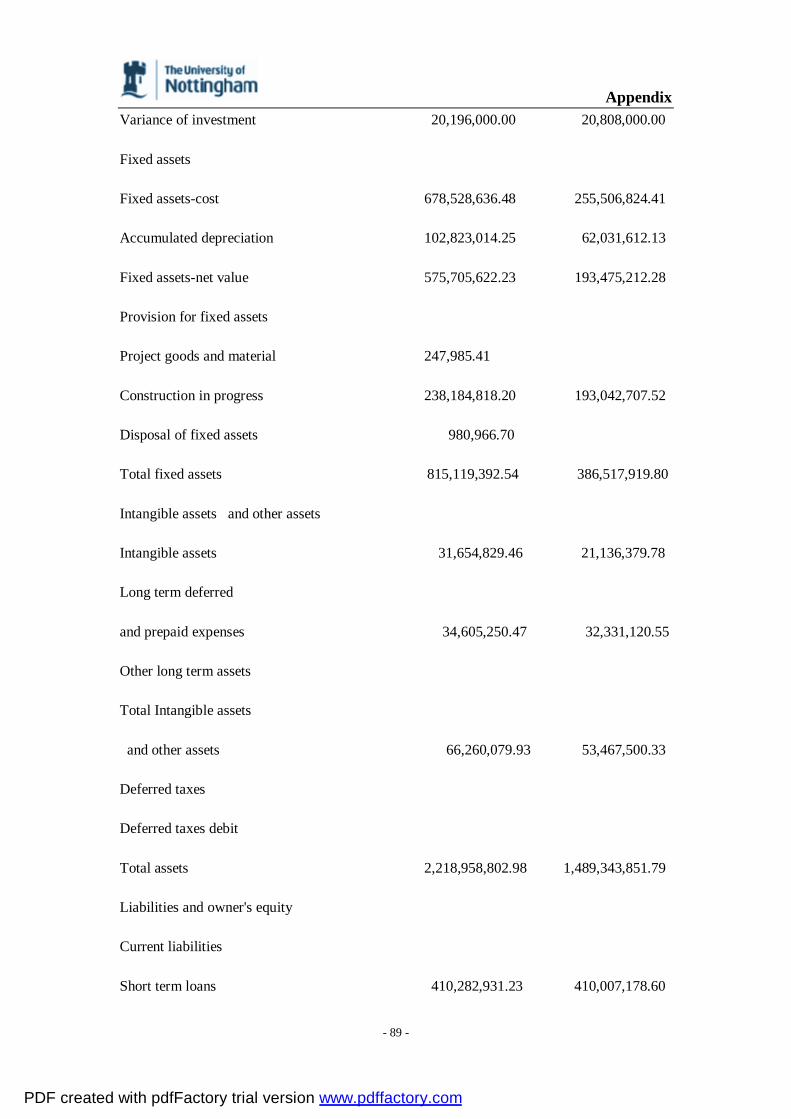

Bibliography………………………………………………………………………...79 Appendix……………………………………………………………………………86

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 1

- 1 -

CHAPTER 1

Introduction

1.1. Backgrounds and Motivations

Financial statements, as the mirror of a company’s performance, require a

fundamental and appropriate financial analysis. The validity and accuracy of financial

statements is an issue extensively stressed due to its high significance. As companies

have grown in size, the management has passed from shareholder-owners to small

groups of professional managers. Thus, a need has arisen for company managers to

report to the organization’s owners and other providers of funds such as banks and

other lenders, on the financial aspects of their activities (Porter et al. 2003, p. 9).

Those receiving external financial reports wish to have the information “checked out”

or audited in the reports to assure reliability.

The external use of financial statements and high public importance are main driving

forces of creative actions. The gravity and credit given by the public for an

outstanding performance and the obsession for high profits and earnings, lead to

creativity (Griffiths, 1987). Nowadays more and more companies use fraudulent

accounting1 to make company economic performance attractive to investors, which

on the other hand provides more difficulties for external auditing and affects audit

quality.

The fraudulent accounting deliberately used by management may mislead

stakeholders and shareholders and result in investment loss ultimately. Therefore,

there is an increasing concern on the audit risk of fraudulent accounting used by listed

companies. The reason for choosing listed company is because the separation of 1 From 1994 to 2004, 117 out of about 1260 listed companies in China were exposed for fraudulent accounting by media (Han, 2005).

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 1

- 2 -

ownership and management control in listed companies makes the independent

external audit especially important with respect to corporate governance and the

oversight of such companies (Nicholls, 2005).

1.2. Aims and Objectives

This dissertation is built up to review the literature in the field of audit risk associated

with fraudulent accounting. The most important task for this dissertation is to

compare the theories and the truth in case study of “Guangxia Ltd.” so as to interpret

whether those theories are good to explain the same evidences in the company.

The literature review generally focuses on following aspects:

1. Overview of auditing

2. Factors affect audit risk.

3. Causes of accounting scandals.

4. Techniques and consequences of fraudulent accounting.

5. The relationship between audit risk and fraudulent accounting.

With the literature review, a case study of “Guangxia Ltd.” will be provided to

examine whether those aspects have been consistent with the truth in the company.

From the comparison, an implication of possible solutions to fraudulent accounting

can be concluded.

1.3. Methodology

Qualitative research methodology will be adopted according to the nature of the

dissertation topic. Qualitative research is concerned with developing explanations of

social phenomenon, it is concerned with the questions about “how”, “why” but not

“how much” or “how often” (Bryman, 1993). In this dissertation, a case study named

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 1

- 3 -

“Guangxia Ltd.” is concluded as an approach to the research. Case study is one of the

forms of qualitative research design, which offers a richness and depth of information

not usually offered by other methods. By attempting to capture as many variables as

possible, case studies can identify how a complex set of circumstances come together

to produce a particular manifestation.

Besides, both primary and secondary research will be carried out to obtain more

information. The primary data collection will be face-to-face and telephone interviews.

Unfortunately, the author failed to get in touch with the staff who had worked in

“Guangxia”, because it is difficult to get the truth from an old staff according to the

nature of accounting scandal. The secondary research will be conducted to collect and

organize data through an examination of an array of books, journals, articles,

newspapers, reports, professional bodies and government agencies.

1.4. Structures of the Dissertation

The dissertation is divided into six parts. The first part states the backgrounds,

motivations and objectives for doing this dissertation. At the second part, literature

review will be given to provide the theoretical basis for further research. The third

part will summarize the methodology used in the research. The forth part provides the

backgrounds of the Chinese auditing environment, which will offer a clear context for

better understanding in the future case study. As the most important segment of the

dissertation, the fifth part will focus on the audit risk associated with “Guangxia Ltd.”.

In this part, case and effects of fraudulent accounting will be introduced in order

based on the literature review. Further, the comparison between the theory and the

truth will be explained to support or argue against those literatures mentioned. The

conclusion in the last part will stress comparisons between “Guangxia” and another

well-known accounting scandal, “Enron” and then offer final opinions on possible

solutions to fraudulent accounting based on Sarbanes-Oxley Act.

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 4 -

CHAPTER 2

Literature Review

This section is divided into three parts. In the first part will generally overview the

concept of auditing. In the second part, audit risk will be introduced from different

areas to aid understanding the audit risk in case study that discussed in chapter 5.

Then the relevant concept of fraudulent accounting which is another key element of

literature review will be addressed in part 3.

2.1. Overview of Auditing

2.1.1. Introduction

Financial statements are the primary source in discovering a company’s performance

and likewise companies are fully aware of the implications of this. There is a broad

range of parties use this financial information although their information needs vary,

such as investors, lenders, customers, employees, governments, the public, etc. The

audited financial statements may be perceived to be reliable by investors and the

public. However, when fraudulent accounting is used by companies, audit risk is

increased and consequently result in investment loss. By then, is accounting as Goethe

says the fairest invention of the human mind?

2.1.2. The Principle of True and Fair Financial Statements

The vision of promoting transparency, shareholder activism and finally, accountability,

is the purpose of a new co-regulatory regime (Dean and Clarke, 2004). Phrases such

as ‘a true and fair view’ and ‘presenting a fair view’ are expressions refer to the value

and validility of financial statements, which bring to the attention the issue of

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 5 -

principle versus rules based accounting and the varying notions applied between

different countries. Dean and Clarke (2004) stated that the ‘true and fair’ criterion has

long been a cornerstone of British-based accounting whereas the U.S. standards in

contrast are categorized as the archetypal rules-based system of reporting.

The International Accounting Standards Board (IASB) and the newly formed

International Financial Reporting Standards (IFRS) used within the U.K. are

perceived to represent the closest thing to a principles-based regime (Vinten, 2003).

This can be defined as a ‘true and fair state of affairs and the need for current value

information to inform investors – reliable, relevant, understandable and comparable

data – proxied by fair value reporting’ (Dean and Clarke, 2004, p. 2)

The standards applied by the U.S. notably the Financial Accounting Standards Board

(FASB) and Securities and Exchange Commission (SEC) are significantly more

detailed and prescriptive than either the United Kingdoms IASB standards or IFRS

(Vinten, 2003). FASB standards are more prescriptive and rule based because the

litigious environment in the United States calls for this, and there is no such ‘true and

fair view’ concept in the U.S. with a comparable equivalent being ‘fairly presented in

conformity with generally accepted accounting principles (GAAP)’.

China has the continental law system and thus adopts the rule-based accounting,

which clearly identifies accounting policy, standards and regulations. It is difficult to

accurately define true and fair view as different people have different opinions toward

it. It is impractical to take true and fair view as the sole guideline in dealing with

financial reporting issues in China, there might be chaos and disorder in practice

(Wang, 2006). However, it is unreasonable to completely reject it; after all it is the

best representation of financial reporting objectives.

Wang (2006) suggests that the notion of true and fair view should be applied in

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 6 -

enactions of regulations, standards and policies. Chinese accounting standards are

government-driven and concern more about governmental supervision and revenue

collection, whereas the true and fair view is information user-driven and focuses on

information credibility and preparation of financial reporting. Therefore, it is

necessary to put the emphasis on enaction of accounting standards and swift to

user-driven objectives.

2.1.3. Accounting Policy

China has long time been using its own accounting standards, which are different

from the well-known U.S. GAAP and European IAS (International Accounting

Standards: previous name of IFRS). On 15 February 2006, the Ministry of Finance

(MOF) issued a series of new and revised Accounting Standards for Business

Enterprises. Referring to the New Accounting Standards, David Sun, Chairman and

Country Managing Partner of Ernst & Young China says, ‘The issuance of the New

Accounting Standards marks the beginning of a new era for the alignment with

international accounting practices in China.’

The rapid development of China’s economy calls for more accurate and objective

accounting information to reflect the increasingly complex business environment. In

line with the globalization of the worldwide economy and international capital

markets, there is an increasingly strong need from the participants of capital markets

and users of accounting information for financial information that exhibits a greater

level of quality, transparency and comparability (Ernst & Young, 2006).

The New Accounting Standards represent convergence with IFRS. Most of them

make reference to the equivalent IFRS and adopt the principles and treatments similar

to its international counterpart. They have specified accounting treatments for

important accounting issues such as business combinations and consolidated financial

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 7 -

statements, providing comprehensive and more authoritative provisions and

guidelines (Ernst & Young, 2006).

The IFRS provides the implicit framework used in accounting. As guideline to the

accounting practioners, they define the accepted accounting practices at a particular

time, concerning the accounting techniques and financial statements preparations

(Belkaoui, 1992; Lehman, 1995). The concepts of fairness, justice, equity and truth

are the basic core elements for the ethical validity of financial statements. There are

three concepts are needed for supporting accounting theory, concerning justice with

equitable treatment of all interested parties, fairness with fair, unbiased and impartial

presentation and truth with true and accurate accounting statements without

misrepresentation (Scott, 1941, in Belkaoui, 1992, p. 62).

2.1.4. Materiality

The auditors are required ‘to determine with reasonable confidence whether the

financial statements are free of material misstatement’ (Statement on Accounting

Standards: SAS 100, para 2,) and that a ‘matter is material if its omission… [or]

misstatement… would reasonably influence the decisions of an addressee of the

auditors’ report (SAS 220, para 3). Likewise, the International Accounting Standards

Committee (IASC) stresses the importance of materiality to financial statement users’

decisions. Therefore, auditors need to form a judgment with regard to what is

‘material’ in the context of a particular audit when planning their audits.

SAS 220 states that:

“The assessment of what is material is a matter of professional judgment and

includes consideration of both the amount (quantity) and nature (quality) of

misstatements” (para. 4).

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 8 -

For instance, remuneration of an executive manager may be immaterial itself but may

be material as a whole to the financial statements. Thus, the sensitivity of an item

nature is important in deciding materiality, even a small inaccuracy can be material. A

user of the financial statements could be misled by inadequate or inaccurate

description of an accounting policy, this description can be perceived to be material

misstatement as well (Porter et al. 2003).

Moreover, different audit types have different understanding on materiality. For

example, a $10M fraud in General Motors was treated as an immaterial financial

event, because it was immaterial2. To some of the general public, and probably the

majority of GM stockholders would perceive such a fraud as a significant financial

event, but to fraud audit it is immaterial, since a fraud audit does not consider

materiality in the processes or in the analysis of the audit evidence (Singleton and

Singleton, 2007).

The overall materiality means the amount of error that the auditor is prepared to

accept as a whole but still concludes they provide a true and fair view of the affairs

and profit/loss of the reporting company. The auditor needs to estimate materiality

level before commencing an audit based on his understanding of the client, its

business and industry and on his assessment of the decision needs of users of the

auditee’s financial statements (Porter et al., 2003).

The lower the level of planning materiality, the greater the amount and/or the more

appropriate the evidence that needs to be collected to make sure that the combined

errors in the financial statements do not exceed it. However, “it must not be viewed as

a fixed monetary amount which, if exceeded even by a small margin, will necessarily

cause the auditor to conclude that the financial statements do not give a true and fair

view, but which, if not exceeded, will lead to the contrary conclusion” (Porter et al.,

2 In the early 1990s, General Motors suffered a lease fraud of over $10M by a Long Island dealer.

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 9 -

2003).

2.1.5. Audit Failure

Audit quality can be viewed as a theoretical continuum ranging from low to high audit

quality, while audit failures occur on the lower end of the quality continuum (Porter et

al., 2003). It occurs when there is a serious distortion of the financial statements

which is not reflected in the audit report, and the auditor has made a serious error in

the conduct of the audit (Arens et al., 2002). A properly done audit does not guarantee

serious distortions have not occurred, but a properly done audit unlikely make serious

distortions. Thus, audit failure cannot occur unless there is serious auditor error or

misjudgment (Tackett et al., 2004).

The nature of this auditor error has only four systematic causes:

n “The auditor can blunder by misapplying or misinterpreting accounting

standards” (Tackett et al. 2004; Wang and Liu, 2004), and such a blunder is

unintentional that can be caused by fatigue or human error. n The auditor can be inappropriately influenced by having a direct or indirect

financial interest with the client (Tackett et al., 2004; Wang and Liu, 2004). For

instance, an auditor who is in consulting engagements for an audit client may be

reluctant to insist on accounting adjustments due to the fear of losing the client to

its competitors. In addition, when an auditor is not performing any consulting service in an audit

client, he is still reluctant to stand up to the client on accounting issues for fear of

being fired. Thus, the auditor perpetrate fraud by intentionally issuing a more

favorable report than is warranted (Tackett et al., 2004), especially at the time

when he accepts a bribe or bows to client pressure.

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 10 -

n “The auditor can be unduly influenced because of having some personal

relationship with the client beyond what is expected in a normal audit between

independent parties” (Tackett et al., 2004). For example, it is common for a staff

member of a CPA firm to leave the firm if he was employed by a previously

audited client, because it is likely that personal relationships with his previous

employer may have some unfavorable impact on his audit opinions.

Further, Wang and Liu (2004) add that audit quality is influenced by two determinants:

the competency of collecting audit evidence and efforts made in achieving it; and

auditor independence, among which the latter is affected by pressures of litigation and

requirements of auditee company. Pressures of litigation derive from the potential

losses once audit fails, and requirements from auditee company may make auditors

conceal truth to financial statement users. Audit quality is inverse of audit failure, the

higher the failure rate, the lower the audit quality. Outright audit failures are difficult

to determine with certainty but can be obtained from some sources such as auditor

litigation and business failures, investigations by SEC, and earnings restatements

(Francis, 2004).

“Audit firms (especially large firms) have reviewed the causes of audit failure and

concluded that the failure does not generally come from auditor’s failure in detection

of accounting data recording or error processing” (Porter et al. 2003). On the contrary,

it tends to result from the matters associated with how the business is managed.

Lemon et al. (2000, p. 10) state that factors such as the business environment,

governance issues and the nature of managerial control will ultimately have

significance for the financial statements – their accuracy, issues of fraud and going

concern. They also add that effective auditing requires greater attention to be paid to

understanding the risks of the business (p. 12).

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 11 -

A broader definition of auditor failure could be based on business failure rates. When

audited report has inappropriate presentation on financial statements, auditors may be

litigated by external users. Audit failure is inevitable as a result of Chartered

Accountants’ negligence or fraud. A recent study shows that nearly 50% audit

litigation is associated with business failure, and this is borne out by the fact of Enron

and other recent domestic fabrication cases of listed companies, but this does not

certainly mean all business failures are audit failures, rather, business failures are

more possible of audit problems.

2.2. Audit Risk

2.2.1. Concept of Audit Risk

Porter et al. (2003) define audit risk as:

“the risk that auditors may give an inappropriate opinion on financial

statements” (p. 56).

The audit risk has two forms, they are:

n “α risk: the risk that the auditor may express a qualified opinion (say something

is amiss) on financial statements that are not materially misstated; and

n β risk: the risk that the auditor may express an unqualified (‘clean’) opinion on

financial statements that are materially misstated” (p. 57).

In practice, α risk is very rare; therefore, the term “audit risk” is generally mean β risk.

Audit risk arises when auditors have legal liability due to an issue of a “clean” audit

report on financial statements which are materially misstated; therefore users of the

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 12 -

financial statements are misled and suffer great loss as a consequence. Arens and

Loebbecke (1980) suggest that it is impossible to get absolute assurance of accuracy

of the financial statements, because auditors cannot guarantee the complete absence of

material errors and irregularities (Arens and Loebbecke, 1980). They only need to

express an opinion on financial statements rather than certifying the truth and fairness

on them.

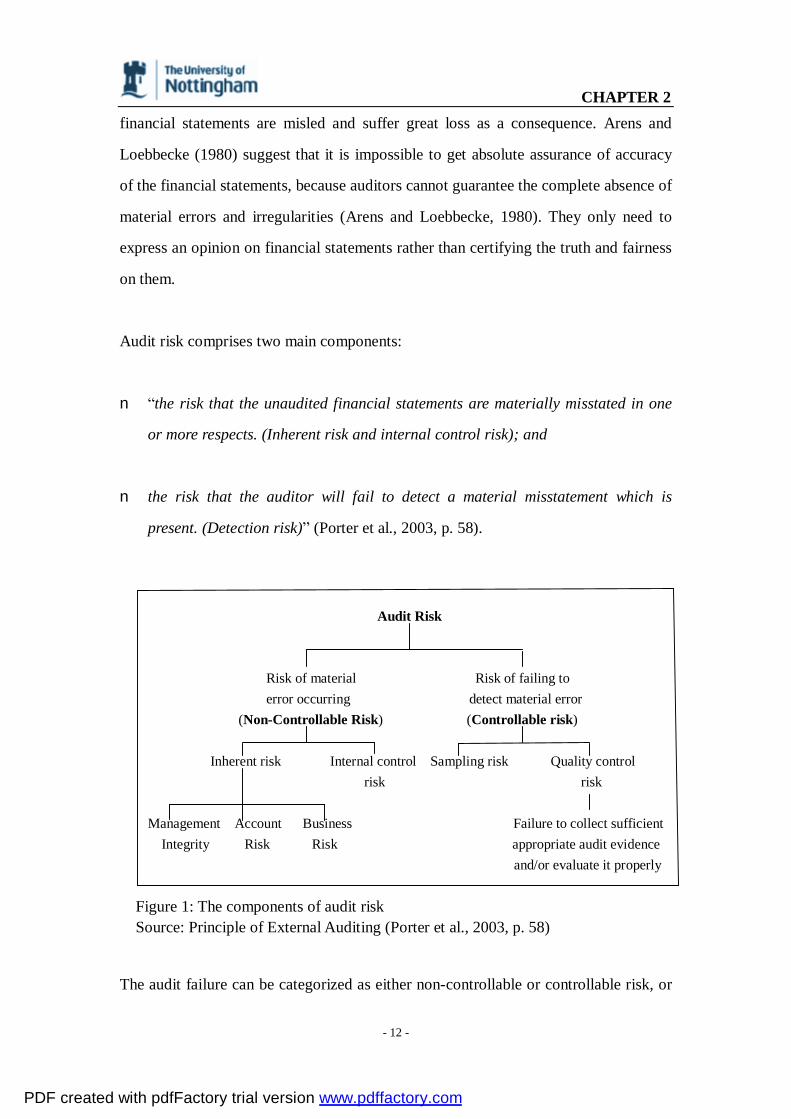

Audit risk comprises two main components:

n “the risk that the unaudited financial statements are materially misstated in one

or more respects. (Inherent risk and internal control risk); and

n the risk that the auditor will fail to detect a material misstatement which is

present. (Detection risk)” (Porter et al., 2003, p. 58).

Audit Risk

Risk of material Risk of failing to error occurring detect material error

(Non-Controllable Risk) (Controllable risk)

Inherent risk Internal control Sampling risk Quality control risk risk

Management Account Business Failure to collect sufficient

Integrity Risk Risk appropriate audit evidence and/or evaluate it properly

Figure 1: The components of audit risk Source: Principle of External Auditing (Porter et al., 2003, p. 58)

The audit failure can be categorized as either non-controllable or controllable risk, or

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 13 -

a combination of both. Corporate accounting fraudulence always has internal

fabrication which greatly increases the inherent risk and internal control risk. With the

existence of fraud, auditors fail to collect sufficient audit evidence or evaluate

properly, thus controllable risk is therein.

2.2.2. Identifying and Assessing Audit Risk

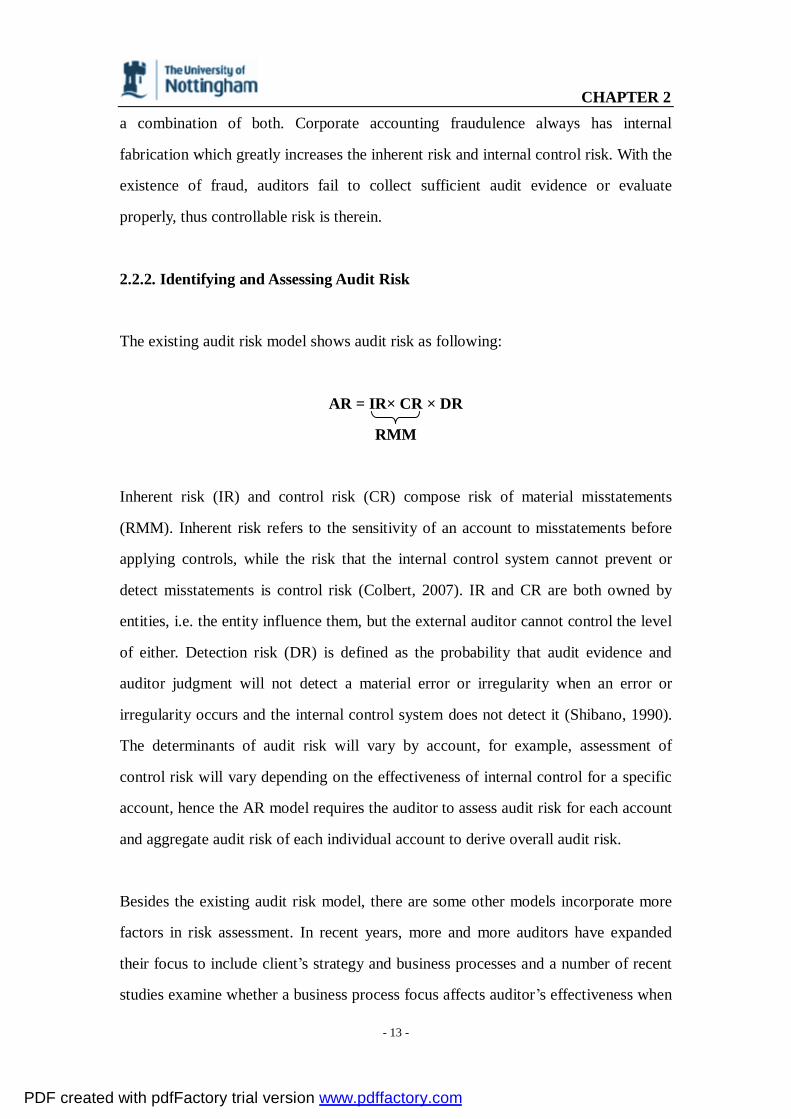

The existing audit risk model shows audit risk as following:

AR = IR× CR × DR

RMM

Inherent risk (IR) and control risk (CR) compose risk of material misstatements

(RMM). Inherent risk refers to the sensitivity of an account to misstatements before

applying controls, while the risk that the internal control system cannot prevent or

detect misstatements is control risk (Colbert, 2007). IR and CR are both owned by

entities, i.e. the entity influence them, but the external auditor cannot control the level

of either. Detection risk (DR) is defined as the probability that audit evidence and

auditor judgment will not detect a material error or irregularity when an error or

irregularity occurs and the internal control system does not detect it (Shibano, 1990).

The determinants of audit risk will vary by account, for example, assessment of

control risk will vary depending on the effectiveness of internal control for a specific

account, hence the AR model requires the auditor to assess audit risk for each account

and aggregate audit risk of each individual account to derive overall audit risk.

Besides the existing audit risk model, there are some other models incorporate more

factors in risk assessment. In recent years, more and more auditors have expanded

their focus to include client’s strategy and business processes and a number of recent

studies examine whether a business process focus affects auditor’s effectiveness when

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 14 -

identifying risks. Bell et al. (1997) describe how this approach drives auditors from a

balance sheet orientation to a broader focus on the overall organization, environment,

and its key processes. Lemon et al. (2000) describe the extent to which firms are

adopting this focus in their audit methodology, and Eilifsen et al. (2001) describe how

this approach is applied to an individual audit.

Key performance indicators can be understood by understanding the client’s business

processes, meanwhile, it also aids in developing expectations for financial statement

accounts (Allen et al, 2006). By using this approach, auditors integrate assessments of

strategic business risks to some extent (O’Donnell et al. 2005). This approach helps

auditors to document more business risks of clients so that they can assess the strength

of control environment and inherent risk differently.

2.2.3. Relationship between Materiality, Audit risk and Audit planning

In order to reduce audit risk to desired level, auditors must plan the nature, timing and

extent of audit procedures carefully (Porter et al., 2003). When planning an audit,

“auditors consider the likelihood of error in the light of inherent risk and the system of

internal control in order to determine the extent of work required to satisfy themselves

that the risk of error in the financial statements is sufficiently low” (SAS 300, para 12).

The materiality limits (planning materiality and tolerable error) should be set at which

they affect the nature of audit procedures planning and the amount or appropriateness

of the evidence that the auditor must collect.

The lower the materiality limits, the greater the likelihood that errors or omissions

will occur in the financial statements that will exceed those limits and thus qualify as

material misstatements, therefore, the more (or more relevant and reliable) evidence

that auditors must collect to make sure they are not exceeded (Porter et al., 2003). In

addition, the lower the materiality limits, the more “careful” the auditor will be to

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 15 -

determine whether those limits are exceeded. The inverse relationship between

materiality and the level of audit risk shows that the higher the materiality level, the

lower the audit risk and vice versa.

2.2.4. Corporate Governance

Davidson et al. (2005) comment that recent accounting scandals have focused

attention on the need for strong corporate governance mechanisms. The Institute of

Directors (IOD) defines corporate governance as:

“rigorous supervision of the management of a company…ensuring that business

is done competently, with integrity and with due regard for the interests of all

stakeholders (IOD, 2004)”

Balancing corporate performance with an appropriate level of monitoring can give

rise to strong governance (Cadbury, 1992). The board of directors plays a very

important role in corporate governance, which manages the strategic direction of the

company, evaluates the performance and determines the remuneration of management

(including executive directors). It also ensures the integrity of internal controls and

financial reporting. In U.S., only 9% of S&P 500 companies have a chairman

genuinely independent of chief executive, and in 70% of these companies the roles are

combined.

There are some other alternative board structures. The one-tier, also known as

Anglo-Saxon boards consist of a mix of executive and non-executive directors, while

the two-tier, known as German boards are separate executive and supervisory,

typically with employee representatives on the latter. However, neither system has

been entirely satisfactory, because scandals have arisen in both systems, and it is

difficult to ensure director independence in practice.

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 16 -

The countries, including China, under continental law system employ the two-tier

board structure (Pi, 2006) and nowadays begin to construct the system of independent

director as the Anglo-American law system has (Ma and Cai, 2002). The number of

independent directors required by Company Law of China is one third of the total

number of directors to ensure independence.

From January 2002, Chinese corporations can constitute audit committees, thus there

are some corporations have a combination of both two. Since the functions of

supervisory board and audit committee overlap each other, some conflicts rise in

practice (Pi, 2006). Therefore, supervisory board should supervise the board of

directors on behalf of shareholders because it comes into being from general meetings,

whereas audit committee supervises managers on behalf of the board and is

supervised by supervisory board.

The preparation and disclosure of true and fair financial information is core of

corporate governance, because it enables stakeholders to exercise their rights so as to

protect their interests (OECD, 1999). However, audit committees in Chinese

companies fail to prevent various high profile corporate failures because the board is

controlled by a minority of directors (Pi, 2006).

Thus, the disclosure of financial frauds is difficult with the fact that they are typically

done by executive management. Auditors are normally constrained in detecting frauds,

because executives are in a good position to hide the fraud or misdirect auditors’

efforts (Singleton and Singleton, 2007). Similarly, an empirical study carried out in

the U.S. finds that the presence of audit committee does not affect the likelihood of

financial statement fraud significantly and no-fraud firms have higher percentages of

outside members in boards than fraud firms (Beasley, 1996).

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 17 -

In addition, another study provides insight into financial statement fraud instances

investigated during late 1980s through 1990s within three volatile industries,

technology, health care, and financial services. It highlights corporate governance

differences between fraud companies and no-fraud companies on an

industry-by-industry basis. “The fraud techniques used vary substantially across

industries, with revenue frauds most common in technology companies and asset

frauds and misappropriations in financial-services firms” (Beasley et al., 2000).

From the research, fraud companies have very weak governance mechanisms

comparing with no-fraud industry companies. Consistent with prior research, fraud

companies in the technology and financial-services industries have fewer audit

committees, but fraud companies in all three industries have less independent audit

committees and boards (Beasley et al., 2000).

2.2.5. Internal Audit

The accounting system of an entity is designed to capture accounting data, convert

and output the data as useful financial information (Porter et al., 2003). It must be

reliable in order to ensure financial information is useful. Thus, the underlying

accounting data must be valid, complete and accurate. To ensure that the data meets

these criteria, internal controls are required to be built into the accounting system. The

internal control mechanisms within a system form the central point of an audit

(Hawks and Pitts, 1990), and the quality of internal control system usually has a

significant impact on audit.

Although internal audit function is internal to a company, it is not a part of the control

environment; “instead it is a mechanism for conducting an independent review of that

environment on behalf of the directors and senior executives” (Porter et al., 2003).

Ideally, the value of an internal control mechanism is its ability to prevent errors or

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 18 -

frauds rather than to merely detect them (Hawks and Pitts, 1990). A fundamental

contributor to audit failure is a weak or ineffective internal audit function (Hamilton

and Micklethwait, 2006, because management always believe that it is expensive and

unnecessary.

If the internal control system is well designed and if it operates effectively to meet the

internal accounting control objectives, auditor will have a higher level of assurance

that any material errors or irregularities in the accounting data will be eliminated

when data passes through the accounting system (Porter et al., 2003). Thus, the

auditor will feel fairly confident when the financial statements are free of material

misstatement. In terms of audit risk, if an entity has a well designed and effective

internal control system, then the risk of material errors in the accounting data that not

being eliminated will be low.

However, if an entity’s internal control system is poor and /or is ineffective in meeting

the objectives of internal accounting control; the auditor will have less assurance that

the financial statements are free of material error. As a consequence, before issuing a

“clean” audit report, the auditor will need to conduct substantive tests in order to gain

sufficient assurance that the financial statements are free of material errors.

2.2.6. Auditor Independence

“Auditors being independent of their audit clients, their clients’ managements, and

any other influences which might impair their objectivity and impartiality, are of

critical importance to the audit function” (Porter et al., 2003). If auditors are not

perceived to be independent by those who use or rely on audited financial statements,

then their opinion on those the financial statements will lack of credibility and thus

the audit will have little use or no value.

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 19 -

Auditors are hired, fired and paid by clients’ managements, they work closely with

them as they conduct their audits and, after a number of years of acting as auditor for

the client they become very familiar with them (Porter et al., 2003). Further, the long

and incestuous relationship between audit firms and their clients can weaken the

ability of audit firms to provide rigorous scrutiny of their client’s accounts, the

distorted incentives of providing non-audit services with their client companies can

also weaken the ability. Hence, if the auditors issue an audit report with a conclusion

that the financial statements do not show a true and fair view, they know that it is

possible to be fired or having their fee reduced (Moizer, 1997). In addition, a sense of

loyalty built up between an auditor and the managers will also threaten auditor

opinion, for example, an auditor may not want to jeopardize the career of a manager

who is a personal friend.

There are two types of ethical reasoning, consequentialism and deontology. In

consequentialism, actions are judged based on the consequences that it results,

whereas in deontology some acts are morally obligatory in spite of their consequences

(Moizer, 1997). The ethical position that an auditor has will influence his/her decision

in terms of auditor independence and honest reporting. Thus an auditor could adopt

the deonological stance because it is wrong to be dishonest. This sort of person

therefore would not give an audit opinion that he/she knows to be wrong, even though

the consequences of issuing an honest opinion are expected to be terrible for a number

of people.

Independent Auditors, like Chartered Public Accountants (CPAs) perform financial

statement audit to gain reasonable assurance that financial statements are free of

material errors or misstatements. Failed financial statement audits arise when auditor

fails to detect or detects but fails to report misstatements. Misstatements can be either

errors (unintentional) or frauds (intentional). The most dangerous fraud is

management fraud, intentional fraudulent financial reporting by management.

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 20 -

Comparing with the incentives of deliberate fraudulent financial reporting by

management, ethical considerations relating to an auditor’s failure to report a

misstatement are obvious too.

Fellingham and Newman (1985) suggested that the auditor and client were competing

(playing a game) against each other in a way that “allow(s) the auditor to influence

the behavior of the auditee” (p. 635). This certainly implies the auditee (client) will

influence the behavior of the auditor too. In this game, the client chooses high or low

effort to eliminate the misstatements from financial statements; whereas the auditor

exerts high or low audit effort to detect misstatements and then issues an audit report

either qualified or unqualifited.

Shibano (1990) allows misstatements to be derived from both errors and irregularities

and tied his model to the three components of audit risk. Thus, he provides game

theory framework that distinguishes between test of controls and substantive testing.

This theory provides an insight into a client auditor relationship that may result in a

failure in audit. The literature stream of game theory was begun by DeAngelo (1981)

and resumed and extended by a number of authors, but a common characteristic of

these authors’ models is the creation of low-balling and potential loss of auditor

independence.

2.3. Fraudulent Accounting

2.3.1. Introduction

The late 1990s and early years of the 21st century, misreporting by public companies

had a relatively big scale. In the U.S. the number of companies that restate their

financial results more than doubled from 1998 to 2004, despite of a decline in total

number of public corporations. An increasing number of restatements were by large

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 21 -

companies and a significant number were disastrous – they were accompanied by

losses in shareholder wealth of more than $1 billion and bankruptcy in some cases

(Grant and Visconti, 2006). Enron and WorldCom stood out as landmarks in recent

corporate scandal history. There are also some Chinese corporate scandals that stress

the issue of fraudulent accounting, for example, “Guangxia”, “Zhengzhou Baiwen”,

“Lantian” etc.

2.3.2. Concept of Fraudulent Accounting

Corporate accounting scandals are “political and business scandals which arise with

the disclosure of misdeeds by trusted executives of large public corporations”

(Wikipedia). They typically include complex methods for misusing or misdirecting

funds, overstating revenues, assets value, understating expenses or underreporting

liabilities, sometimes with the cooperation of officials in other corporations or

affiliates (Wikipedia).

The term corporate scandal lends itself to be a legal term and thus may be considered

as a form of corporate crime. Such example of corporate crime, defined as the

“deliberate steps by one or more individuals to deceive or mislead with the objective

of misappropriating assets of business, distorting an organization’s apparent financial

performance or strength, or otherwise obtaining an unjust or illegal financial

advantage” (Robarts, 1978, p. 46), as recognized by the APC (Auditing Practices

Committee), Guideline 418, and “encompasses white-collar crime, defalculation,

irregularities and embezzlement” (Hemraj, 2004, p. 268).

However, Levy (1985) asserts that in a corporate sense, fraud is “an intentional

deception, misappropriation of a company’s assets or the manipulation of its financial

data to the advantage of the prioritor” (p. 78). Therefore, it can be argued that a

corporate accounting scandal may have been the result of justifiable actions in view of

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 22 -

period’s legislation rather than an intentional misrepresentation, concealment, or

omission of the truth, which always exist in fraud.

Fraudulent accounting is a major application of corporate scandals, which typically

involves various account manipulations. Fraudulent financial reporting is sometimes

called creative accounting, aggressive accounting, income smoothing, window

dressing and earnings management, etc. However, some literature states that creative

accounting is a broader term covering not only earnings management but other

practices such as deliberate misclassification in the balance sheet. Arthur Levitt

(1998), former chairman of U.S. SEC, defined fraudulent financial reporting as

practices by which “earnings reports reflect the desires of management rather than the

underlying financial performance of the company”. Recent reports of the demise of

high-profile giants such as Enron, WorldCom and Arthur Andersen have cast the

spotlight on this ‘numbers game’ (Levitt, 1998).

Dechow and Skinner (2000) state that appropriate accrual accounting may make

reported earnings smoother than underlying cash flows and the earnings can provide

better information about economic performance than cash flows to investors. But

when there is “too much” smoothing, it becomes earnings management. It occurs

when managers use judgment in financial reporting and in structuring transactions to

make changes on financial reports to mislead some stakeholders about company

economic performance or to influence contractual outcomes that rely on reported

accounting numbers (Healy and Wahlen, 1999).

The distinction between fraudulent accounting and earnings management, but

acceptable, that managers can exercise their accounting choices is illustrated in figure

2. There is a clear distinction between fraudulent accounting and the judgments and

estimates falling within GAAP that may comprise earnings management relying on

managerial intent (Dechow and Skinner, 2000).

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 23 -

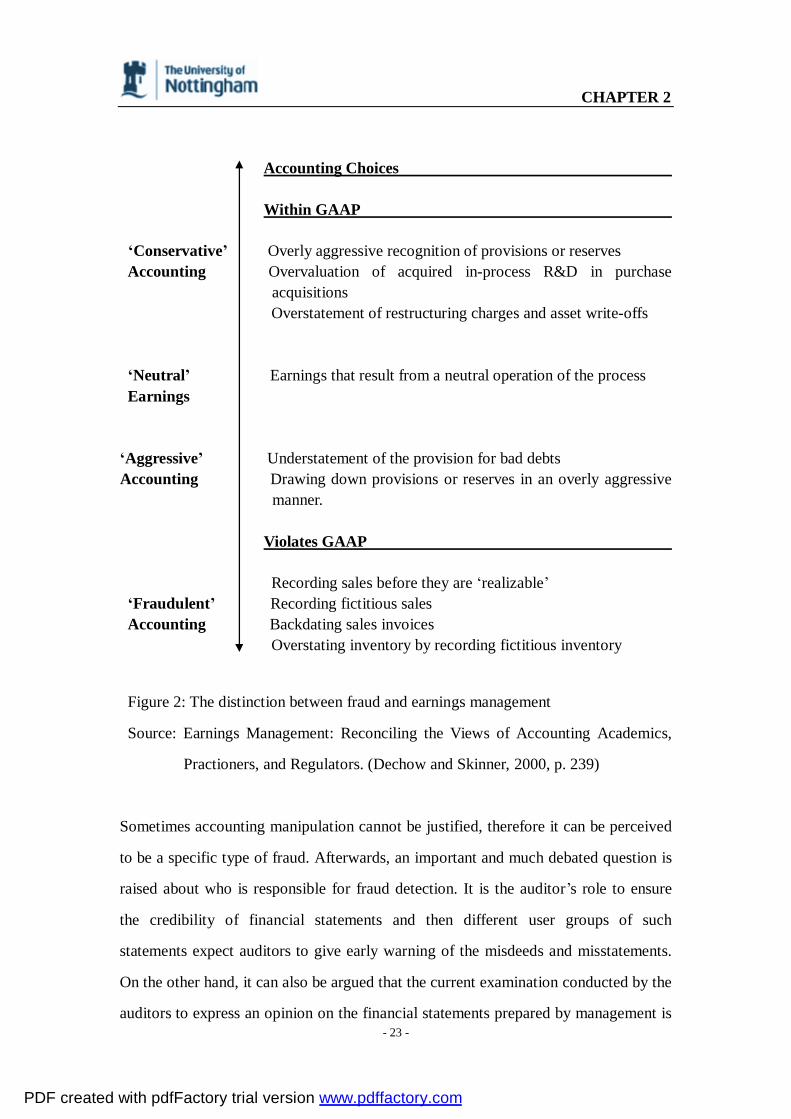

Accounting Choices Within GAAP ‘Conservative’ Overly aggressive recognition of provisions or reserves Accounting Overvaluation of acquired in-process R&D in purchase

acquisitions Overstatement of restructuring charges and asset write-offs ‘Neutral’ Earnings that result from a neutral operation of the process Earnings ‘Aggressive’ Understatement of the provision for bad debts Accounting Drawing down provisions or reserves in an overly aggressive

manner. Violates GAAP

Recording sales before they are ‘realizable’ ‘Fraudulent’ Recording fictitious sales Accounting Backdating sales invoices Overstating inventory by recording fictitious inventory

Figure 2: The distinction between fraud and earnings management

Source: Earnings Management: Reconciling the Views of Accounting Academics,

Practioners, and Regulators. (Dechow and Skinner, 2000, p. 239)

Sometimes accounting manipulation cannot be justified, therefore it can be perceived

to be a specific type of fraud. Afterwards, an important and much debated question is

raised about who is responsible for fraud detection. It is the auditor’s role to ensure

the credibility of financial statements and then different user groups of such

statements expect auditors to give early warning of the misdeeds and misstatements.

On the other hand, it can also be argued that the current examination conducted by the

auditors to express an opinion on the financial statements prepared by management is

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 24 -

neither primarily nor specifically geared with regard to disclosing defalculations and

irregularities. Thus, although an auditor may discover a fraud by chance, an auditor’s

report cannot be completely relied on to reveal fraud.

2.3.3. Causes of Fraudulent Accounting

Smith (1992) states that much of the rapid growth of company profits in the 1980s

was because of exercise of accounting techniques rather than real boom in economy.

Levitt (2002) also comments that these kinds of scandals are symptomatic of a

breakdown of business ethical values over about 20 years. Academic analysis of the

systematic influences on accounting scandals has focused on three aspects: first,

inadequacies of oversight; second, weakness of accepted accounting principles; and

third, inappropriate incentives to executives. In terms of corporate oversight, the

boards have failed in representing shareholder interests and exerting scrutiny over

management. The structural weaknesses include: first, the chairman of board and

chief executive are a same person; and second, non-executive board members are lack

of independence, authority and autonomy.

However, when the ownership and management are isolated, agency problem arises.

Then business performance assessment is the key measurement assessing whether

company managers make decisions at shareholders’ interests. The assessment is

primarily based on company profit or share price, thus company management usually

window-dresses or falsifies financial statements to achieve individual interest

maximization (Li, 2003).

“In terms of accounting principles, the growing importance of intangibles, the

increased use of derivatives and off-balance sheet financing and the blurring of

current and capital items have undermined the ability of financial statements prepared

under accounting principles to reflect accurately past financial performance and future

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 25 -

risks” (Grant and Visconti, 2006, p. 363). Lastly, since short-term performance is

closely related to financial incentives, such as bonuses and stock options, perverse

incentives are created to senior managers (Grant and Visconti, 2006). Jensen and

Murphy (2004) argue that between the 1990s and 2000s, overvalued share prices

encouraged managers to make more aggressive accounting and operation decisions.

When the issues are failed to be resolved, managers will turn to further manipulation

even fraud under the pressures.

In addition, Grant and Visconti (2006) find that the strategy executives are working in

matters as well. Particularly, the strategy pursued should be consistent with the

requirements of the company business and its resources and capabilities. Nowadays,

in many organizations, top management seeks ways to be competitive and maintain

market position or just to survive (Reider, 2007). When a company’s strategy does not

fit its external and internal environments, company performance is likely to decline

and management will be induced to fabricate accounting information.

Lastly, Kranacher (2006) states that the complexity of accounting standards provides a

breeding ground to various fraudulent activities. The more detailed the standards, the

more loopholes that companies seek opportunities to take advantage. Enron is an

example of how fraud can be perpetrated by misusing the standards and principles

that are expected to protect public interests. The complexity of the deals and contracts

Enron used to blur the truth of company transactions is a part of why Enron’s

management was able to keep the fraud under the radar for such a long time (Nicholls,

2005).

By ‘cooking the books’, ‘fiddling the accounts’ or ‘window-dressing’, businesses can

appear to be more attractive to investors by good business performance and stability

(O’connor, 2002). The increased pressure from investors, managers and competitors

becomes the main reason for companies to window-dress their accounts. Companies

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 26 -

using fraudulent techniques are willing to pay a great deal of money to give a false

impression. Sen and Inanga (2003) state that financial fraudulence in a company may

arise under at least three conditions. First of all, companies float its shares and try to

develop a good price to attract investors. Secondly, listed companies try to make their

financial conditions more attractive. Thirdly, listed company try to pay dividend

through fabricated methods providing an image of good business performance to

investors.

Further, fabrication may arise when cost is less than the gains the actions generate and

punishments are not rigorous (Li, 2003). The inadequacy of relevant Chinese laws to

punishment of fraudulence encourages corporate fraudulence. According to a research

on accounting fabrication cases in the last decade, the number of punished listed

companies is less than 100 (Jing, 2002), and the responsibility is mainly

administrative rather than criminal and civil. Thus, listed companies are likely to

fabricate under this circumstances.

2.3.4. Fraud Techniques

The fraudulent techniques can be viewed as fabricating techniques that are executed

on financial statements and discovered by financial analysts. The followings are some

major applications of fraud techniques.

2.3.4.1. Overstatement of Revenue

The scope for turnover tampering is often determined by the nature of company

activities. It is impossible for a cornershop which is primarily in a cash business to

manipulate its sales than it is for a motor vehicle leasing company, where the

relationship between cash received and actual sale is more tenuous (Griffiths, 1987).

However, it is still possible for most companies to keep a substantial control over the

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 27 -

figure of turnover.

Revenue overstatement includes the early recognition of sales income or the sales

transactions have no real substance. For example, a company is engaging with growth

performance may overstate operating revenues by early recognition. If an item issued

to a distributor on a ‘sale or return’ basis is recorded as sales, it will inflate sales and

profits even if the item is not returned. Another indicator that profits are being

overstated is when reported profits are higher than operating cash flow for the period.

This amount is not consistent with the real figure that the transaction should generate.

In other words, it might be fiction.

2.3.4.2. Understatement of Expenses

A company’s debtors and creditors are overshadowed by stock and cash or borrowings

in the balance-sheet under current assets. “The lack of attention which is paid to them

is misplaced if not misguided, since debtor and creditor management can be an

important influence in determining a company’s cash flow position” (Griffiths, 1987,

p. 23). A careful analysis of the relationship between creditors and debtors can give an

important indication of company’s performance and prospects. Business losses may

result in drop on share price; hence the company value will be reduced as well.

Concealment of losses is a technique to mask the effect of business losses. By

reducing losses or liabilities, this can have the effect of inflating profitability.

2.3.4.3. Tamper with Taxation

There is a close link between a company’s profits and the tax which will ultimately

pay for. Therefore, the creative accounting techniques used to influence those profits

should be seen in the context of the tax as well as the stock market implications

(Griffiths, 1987). The annual profits can even be determined completely by the

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 28 -

amount of tax that it prepares to pay. In other words, “it decides on the cash it will

hand over to the government and then constructs its profit and loss account in order to

arrive at the desired result” (Griffiths, 1987, p. 63). It is clearly that tax planning and

creative accounting go hand in hand. The rate at which tax will be charged to a

company’s profits is crucial in determining the earnings per share (EPS) which will be

used in calculating the price earnings ratio. The lower the tax charge the more profits

there are available for shareholders.

2.3.5. Consequences of Fraudulent Accounting

External users of financial statements will be greatly affected by fraudulent

accounting. Investors will consequently suffer great loss once the audited financial

statements do not disclose the frauds. This will result in a decline of public trust in

accounting and reporting practices. External investors who rely on the audited

financial statements but with material errors and frauds will be misled and hence

make wrong investment decisions.

Stakeholders, such as employees, competitors, customers, and banks, as the group of

people and/or organizations holding mutual interest or having inter-related

relationship with the company can influence company performance and as such is

influenced by company. Stakeholders’ interest in company may not be expressed in

moneytary terms as it is in the case of shareholders. When a corporate scandal occurs,

government authority will be questioned leading to a decline on public trust. The

impact of corporate fraud on stakeholders can be either direct or indirect, for instance,

employee layoff due to bankruptcy will affect local well-being because of

unemployment.

Fraudulent accounting by management has been costly for shareholders (Kedia and

Philippon, 2006). During the periods when firms misreport, firms hire and invest

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 2

- 29 -

more than comparable firms matched on age, industry and initial size (Kedia and

Philippon, 2006), and they grow at a significant higher rate. Once they are caught and

forced to restate, the firms shrink quickly.

From the auditor point of view, fraudulence may increase the difficulties in audit work.

Corporation’s intentional fabrication destroys the internal control mechanism at the

first place, and then increases the controllable risk when carrying out sampling audit

and audit control procedures, which directly influence the audit quality in the end.

Since the fraudulent techniques used today are sophisticated and state-of-the-art, it is

very likely that auditors may fail to detect the misstatements. The failure in audit will

then affect external users of audited financial statements.

This chapter brings a general idea of the concept of audit risk and fraudulent

accounting. Following the methodology in chapter 3, theories can be used to compare

with the truth in practice. Nexct chapter will stress the reasons for using case study

research methodology and choosing China and a Chinese company as research target.

Additionally, merits and limitations of case study methodology will be given to have a

clear view of this research method.

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 3

- 30 -

CHAPTER 3

Methodology

This dissertation is going to use case study as the methodology, and mainly focuses on

qualitative method and secondary information. Case study is a non-experimental,

descriptive type of study and one of the forms of qualitative research design, which

offers a richness and depth of information not usually offered by other methods.

Robert K. Yin (1984, p. 23) defines the case study research method as “an empirical

inquiry that investigates a contemporary phenomenon within its real-life context,

when the boundaries between phenomenon and context are not clearly evident, and in

which multiple sources of evidence are used”. By attempting to capture as many

variables as possible, case study can identify how a complex set of circumstances

come together to produce a particular manifestation.

Yin (1993) identifies three types of case studies, exploratory, explanatory and

descriptive. Stake (1995) has his own three different from Yin’s, they are intrinsic,

instrumental and collective. When the researcher has an interest in a case, this is

intrinsic. When a case is used to understand more than what is obviously to be

observed, it is instrumental. When a group of cases is studied, it is collective (Tellis,

1997). Explanatory case studies may be used for doing causal investigations. This

dissertation is going to use explanatory case study to find the casual relationship

between audit risk and fraudulent accounting.

The author aims to examine the effectiveness of literature that developed in the west

in explaining a Chinese case. The objective of the dissertation lies in the likelihood

that the existence of gap between literature and the truth in case. China, after the start

of economic reform and opening up policy, has been speeding up its capital market

establishment. In terms of stock market development, China is new and less

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 3

- 31 -

experienced comparing with western countries. Particularly, the nature of Chinese

political regime significantly affects the stock market development and company

performance in stock market. The author is interested in investigating whether or not

the fraudulent accounting used by listed companies in a typical socialism country can

be explained by western literatures. Since the nationality of the author is Chinese, it is

supposed that secondary data and information is easier to obtain.

The “Guangxia” case is one of the well-known corporate scandals in China and has

being widely discussed in literature. It is the first “blue chip” in China Stock

Exchanges, hence its collapse leads to a stock crisis that has never experienced in

Chinese stock history. Guangxia is the most significant accounting scandal comparing

with the preceding cases in terms of falsification amount and fraudulence scale.

Guangxia is quite alike Enron in terms of significance and similarities so that

observers nickname Guangxia the “Chinese Enron”. Subsequently, the audit failure in

Guangxia calls for great attention to be put in stock market mechanism and auditing

profession. Government and involved bodies and organizations take measures to

remedy the problems and improve the system. A number of regulations and acts are

enacted after the exposure of Guangxia fabrication case to prevent further accounting

scandals.

The data and information used in case study primarily stem from secondary Chinese

literature. Since it is a well-known case to both corporate business and auditing

profession, there are loads of information and discussion available on journals and

websites analysed from both views. However, this source of information is limited by

a fact that most of the Chinese journals are repetitive on one or more issues without

new information. It can easily find what frauds Guangxia has perpetrated but the

information about how Guangxia fabricates is little. It is presumed that this problem

can be resolved by using primary research methodology, but due to the nature of

corporate scandal, it is harder to know the fabrication truth by using it.

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 3

- 32 -

The author tried to get in touch with Guangxia with the phone number got from its

website, but unfortunately, the author was refused by the employee who answered the

phone because it was unauthorized. In fact, it is reasonable to be refused as the author

is neither official nor journalist, Guangxia is not supposed to accept the interview.

Even if the interview can be conducted with insiders or former employees of

Guangxia, the credibility of research results can be questioned. It is very likely that

they may not tell truth due to various reasons, such as significant pressures from

management, personal career considerations, and fears of taking responsibility and so

on. After all it is a past event, thus people may not want to be in a trouble.

Case study can provide different views from what happens in practice, but it cannot

offer a comprehensive understanding. It is a single individual or just a few, thus may

not offer reliability or generality of findings. Some also believe that “intense exposure

to study of the case biases the findings”, and some believe that case study research

only useful as an exploratory tool (Soy, 1997). Therefore, based upon the arguments,

case study may not be the best methodology to this dissertation.

Before examining the case study, an overview of Chinese auditing environment is

given to obtain a preview of auditing under Chinese context in next chapter. The

auditing conditions in China provides some causal factors for corporate accounting

fraud, thus helps understand why fraud could happen in the case of Guangxia. Both

the intrinsic and extrinsic characteristics of current auditing environment can give rise

to corporate accounting scandal and auditing scandal, therefore they must be

investigated first.

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 4

- 33 -

CHAPTER 4

Overview of Chinese Auditing Environment

4.1. Inherent Pitfalls of Equity Structure and Company Management

Most listed companies in China are whole state-owned enterprises (SOE) before

going public. Government owns an absolutely large stake of shares even after listing.

Institutional shareholders are the second large group shareholders except state

shareholders (Wan and Tian, 2003). They are non-circulating shares and make up a

large portion of the total shares. Thus, the inappropriate proportion of shares makes

non-circulating shareholders have an absolute say at board meetings. Non-circulating

shareholders make decisions from their own interests, so that the interest of small and

medium shareholders might be violated. Normally, the biggest shareholders are the

founder of company. They endlessly use company capital and pass the buck to

circulating shareholders who become innocent ‘scapegoat’ when financial crisis

arises.

The directors of board are normally administrative staff from management; most

importantly the chairman of board is also the manager which threatens the problem of

corporate governance (Wang and Liu, 2004). Hence, the appointment of audit firm

does not make any sense at the board meeting since it is decided by the administrative

management. Although annual board meeting, board of directors and supervisory

board are established according to ‘Company law’ and regulations of listed company,

they do not effectively function well. Non-executive directors are not qualified,

because lots of companies invite university or research institute professors and other

distinguished scholars to be non-executives (Wan and Tian, 2003). Further, since the

board is controlled by non-circulating shareholders, non-executives could not

investigate more and have a say on decision-makings.

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 4

- 34 -

Investors in western countries make investment decisions highly rely on audited

reports. They more prefer trusting the audited financial statements from experienced

audit firms with good reputation to small and less-experienced ones, whereas the

Chinese investors in the environment of growing stock market less rely on audited

information due to the characteristics of gambling (Wang and Liu, 2004). This to

some extent may promote the development of unfavorable conditions in stock market.

Therefore, inappropriate company management, inefficient jurisprudence and

unreasoning investments lead to auditing market inefficiency and poor audit quality.

4.2. Auditor Profession

4.2.1. Due-risks

Audit firms or CPAs get engagements from auditee companies, carry out audit work

and issue audit report. During the course of audit work, auditors may be encountered

with audit risk when collecting audit evidence. Audit risk involves non-controllable

risk and controllable risk, among which quality control risk is more important to

auditors. It is always determined by auditor’s proficiency and competency. The audit

fee in China is priced by government and has two pricing approaches. The first

approach is based on the number of working hours of auditors and the second

approach is on the auditee company’s value (Zhou and Liu, 2006). Since the number

of working hours of auditors are difficult to be quantified, most audit firms adopt the

second approach. But this approach gets lots of critics from practitioners, who believe

that business complexity and risks should be considered when deciding audit fees.

One partner from a domestic audit firm added that audit fees charged by domestic

firms are much lower than Big 4 and other non-big 4 foreign firms, but the actual fee

got is only half of the price (Guo and Ma, 2004).

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 4

- 35 -

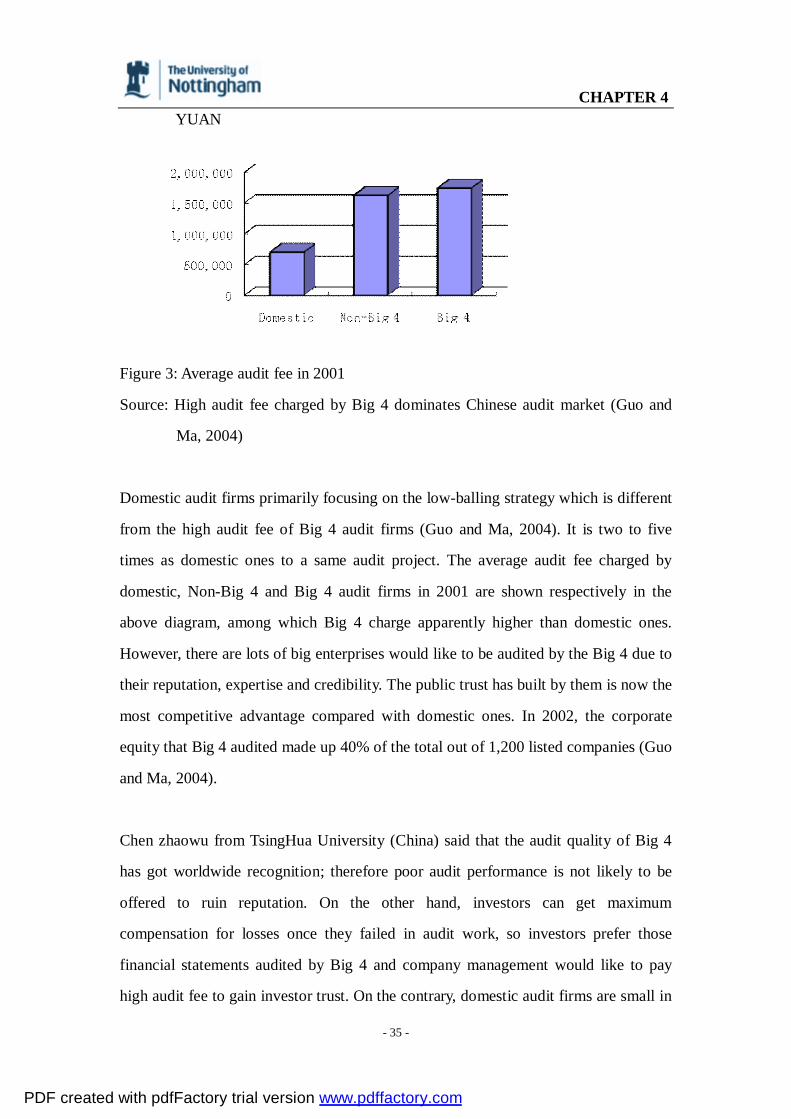

YUAN

Figure 3: Average audit fee in 2001

Source: High audit fee charged by Big 4 dominates Chinese audit market (Guo and

Ma, 2004)

Domestic audit firms primarily focusing on the low-balling strategy which is different

from the high audit fee of Big 4 audit firms (Guo and Ma, 2004). It is two to five

times as domestic ones to a same audit project. The average audit fee charged by

domestic, Non-Big 4 and Big 4 audit firms in 2001 are shown respectively in the

above diagram, among which Big 4 charge apparently higher than domestic ones.

However, there are lots of big enterprises would like to be audited by the Big 4 due to

their reputation, expertise and credibility. The public trust has built by them is now the

most competitive advantage compared with domestic ones. In 2002, the corporate

equity that Big 4 audited made up 40% of the total out of 1,200 listed companies (Guo

and Ma, 2004).

Chen zhaowu from TsingHua University (China) said that the audit quality of Big 4

has got worldwide recognition; therefore poor audit performance is not likely to be

offered to ruin reputation. On the other hand, investors can get maximum

compensation for losses once they failed in audit work, so investors prefer those

financial statements audited by Big 4 and company management would like to pay

high audit fee to gain investor trust. On the contrary, domestic audit firms are small in

PDF created with pdfFactory trial version www.pdffactory.com

CHAPTER 4

- 36 -

business size; proficiency and internal management are inadequate, so that it is

difficult to acquire big audit projects (Guo and Ma, 2004). Competition among

domestic audit firms are so severe that a buyer’s market prevails, which results in

worries of being dismissed if requirements are not met. The excessive competition

subsequently leads to price war, therefore, to survive, they even take illegal actions to

attract customers and maximize business profits (Wang and Liu, 2004).

4.2.2. Agency Problems

The agency problem exists among financial statement users, auditee company and