Embed Size (px)

Citation preview

© Copyright 2014 Saul Ewing LLP

The Affordable Care Act

Employer Risk Management and Compliance Issues

2014, 2015 & 2016October 28, 2014

1

© Copyright 2014 Saul Ewing LLP

Disclaimer: The content of these presentation materials has been prepared by

Saul Ewing LLP for information purposes only. The provision and receipt of the information in these presentation materials should not be considered legal advice, does not create a lawyer-client relationship, and should not be acted on without seeking professional counsel who have been informed of the specific facts. Should you wish to contact the presenter to obtain more information regarding your company's particular circumstances, it may be necessary to enter into an attorney/client relationship.

2

© Copyright 2014 Saul Ewing LLP

2014 & 2015

2014 - Exchanges/Marketplaces Open2014 - Expanded Mandated Benefits2015 – Employer Shared Responsibility – Applicable Large Employers (ALEs) – 100 2016 – Employer Shared Responsibility – ALEs 50-99 – MAYBE!

3

© Copyright 2014 Saul Ewing LLP

2014 Mandated Benefits• Elimination of pre-existing condition

exclusions (for everyone)• Elimination of annual limitations on

“essential health benefits”• Limitations on cost-sharing, out-of-

pocket maximums and deductibles• Non-grandfathered – costs of clinical

trial participation

4

© Copyright 2014 Saul Ewing LLP

2014 Mandated Benefits• Limitation on waiting periods - maximum

of 90 days (coverage on 91st day)• Ok to impose substantive eligibility

conditions (other than the passage of time) before 90-day waiting period starts

• Ex: Hours of service per eligibility period –use a reasonable measurement period to determine (not more than 12 months)

5

© Copyright 2014 Saul Ewing LLP

2014 Mandated BenefitsImposition of up to 1,200 cumulative hour requirement will not violate 90-day rule. Ex: Part-time employees offered coverage after one year NO – after 1,200 cumulative hours of service OK. (Just a lapse of time requirement). New Hires that already satisfy all eligibility requirement – coverage by 91st day.

6

© Copyright 2014 Saul Ewing LLP

2014 Mandated Benefits90 days is not 3 Months ( Pay or Play Rule)Eligibility (other than ACA full-time) may pose a problem in 2015 unless NOT ALE.Waiting period rules permit a bona fide orientation period (up to one month) so that time periods relating to waiting periods and the non-assessment periods for assessable payments under pay or play coordinate.

7

© Copyright 2014 Saul Ewing LLP

What is the Employer Mandate?

• In a Nutshell: Generally, beginning in 2015, in order to avoid the risk of penalties called “assessable payments,” each separate member of an “applicable large employer” (as determined on a benefits controlled group basis) must “offer” “minimum essential coverage” that provides both “minimum value” and is “affordable” to its “ACA full-time employees” and their “dependents.”

8

© Copyright 2014 Saul Ewing LLP

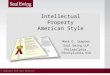

Who are “ACA Full-Time Employees?”• An ACA full-time employee is a common

law employee who is credited with an average of at least 30 hours of service a week or 130 hours of service per month.

• NOTE: All hours of service paid or to which an employee is entitled to be paid (vacation, paid leaves, etc.) have to be counted.

9

Key Terms

© Copyright 2014 Saul Ewing LLP

Key Terms

• Who are “dependents” of ACA full-time employees?• Children under age 26 (sons, adopted sons,

daughters, adopted daughters – does not include stepchildren or foster children)

• Does not include spouses.• Transition rule MAY delay offering dependent

coverage for 2015 plan year, if employer taking steps to provide coverage in 2016.

10

© Copyright 2014 Saul Ewing LLP

Key Terms

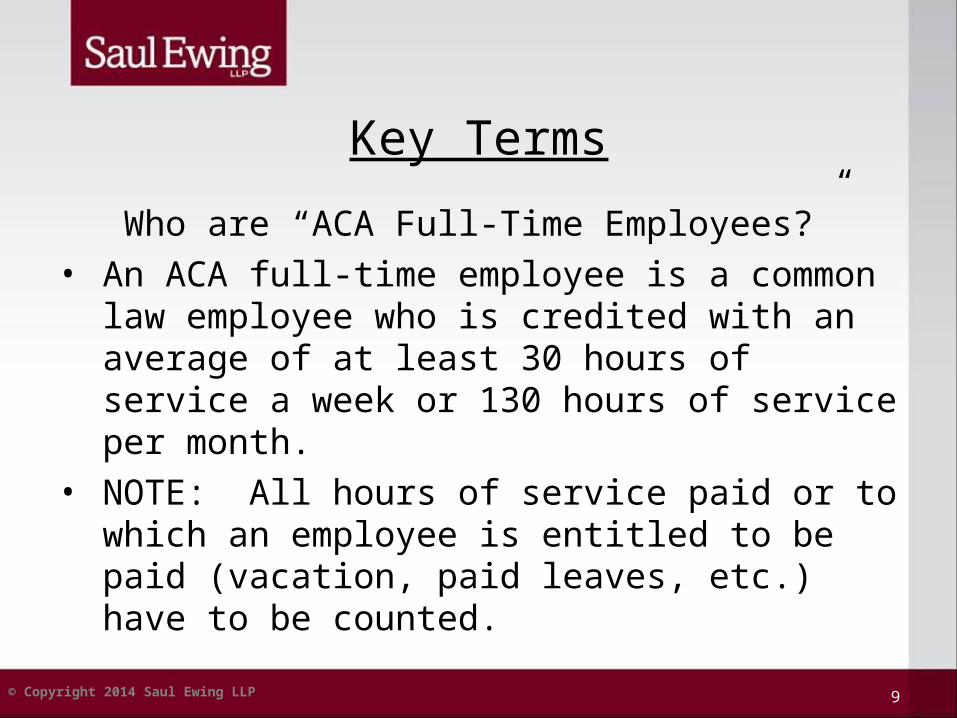

• Is Your Company or Organization an “applicable large employer” or ALE? Or - HOW DO YOU COUNT TO 50?

• 50 or more ACA full-time (at least 30 hours or service a week) and/or full-time equivalent employees

• Looks at preceding calendar year and based on hours of service during the preceding year.

• Aggregate hours of service of part-time employees (up to 120 per employee a month) and then divide by 120

• Looks at your organization’s benefits “controlled group”- same as for testing retirement plans

• Seasonal worker exception.

11

© Copyright 2014 Saul Ewing LLP

Key Terms

• Coverage is “affordable” if the employee pays no more than 9.56% of his or her household income for employee-only coverage under the lowest cost minimum value plan.

• Three safe harbor rules for determining affordability.• W-2 (Box 1) – Year-End Determination• Rate of Pay – 9.56% x 130 hours x hourly rate or 9.5% x monthly

salary• Federal Poverty Level for a single person (based upon current FPL

of $11,670) – 9.56% x $11,670 = $1,115.65 divided by 12 = $92.97 per month – easiest to use can use FPL in effect up to six months before beginning of plan year.

12

© Copyright 2014 Saul Ewing LLP

Key Terms

• A plan provides “minimum value” if the plan’s share of the total allowed cost of benefits is at least 60%.

• Minimum value determined by minimum value calculators, designed-based safe harbors, actuarial certification

13

© Copyright 2014 Saul Ewing LLP

Key Terms• “Minimum essential coverage” or MEC means (at least until

further guidance) any health care coverage – but not vision or dental.

• Employer Mandate requires ALE members to offer “minimum essential coverage” to substantially all ACA full-time employees or risk assessable payments.

• “Minimum essential coverage” is also the type of coverage that must be maintained under the “individual mandate” or pay penalties in the form of additional taxes (effective in 2014).

14

© Copyright 2014 Saul Ewing LLP

Key Terms

• Employer must “offer” coverage to ACA full-time employees.

• Offers from a multiemployer plan treated as an offer by employer making contributions for ACA full-time employee under CBA.

• Employee must have an effective opportunity to decline if the coverage offered does not provide minimum value or monthly contribution higher than (9.5% of the Federal Poverty Level) divided by 12.

• Can maintain evergreen elections in place, so long as there is the ability to “opt out.”

15

© Copyright 2014 Saul Ewing LLP

What is the “Pay” in Pay or Play?

• “No Offer” Penalty - $2,000 x all ACA full-time employees (minus 30, minus 80 for 2015 – allocated pro-rata among all ALE members) if minimum essential coverage is not offered to substantially all (95%/5, 70% for 2015) ACA full-time employees (and certain dependents), and just one ACA full-time employee gets subsidized Marketplace Coverage. – “A” Penalty

• “Inadequate Coverage” Penalty – Coverage is offered to substantially all ACA full-time employees (and certain dependents) but it either does not provide minimum value or is not affordable - $3,000 x each ACA full-time employees who get subsidized Marketplace Coverage. - “B” Penalty

• Both penalties assessed at the end of the year, but look at whether coverage was offered to each ACA full-time employee during each month

• Both penalties are non-deductible• Penalties apply separately to each member of the ALE’s controlled group

(ALE Member)

16

© Copyright 2014 Saul Ewing LLP

When Do You Have to Comply?

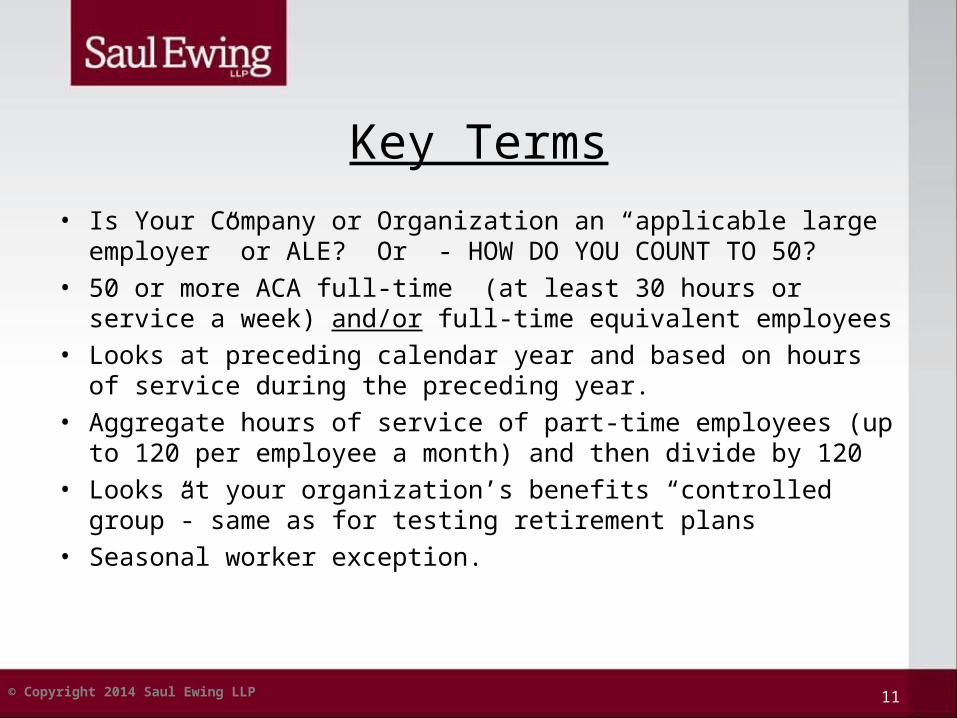

• Generally, 2015, but special transition rule MAY be available for ALEs that have 50 or more full-time/full-time equivalent employees, but less than 100.

• Non-calendar year transition rules MAY apply to avoid penalties being assessed for months prior to beginning of 2015 non-calendar year plan year.

• Transition rules require satisfaction of a number of requirements.

17

© Copyright 2014 Saul Ewing LLP

Determining ACA Full-time Status• Only two methods: Monthly (new) and Look-back

measurement methods. • Monthly: ACA full-time status is determined by looking

each month at an employee’s hours of service. (Cannot average hours). Must use “Monthly” for all new hires that are “reasonably expected to work full time,” until employed for at least one standard measurement period

• Look-back: ACA full-time status is determined for a future time period (called a “stability period”) by counting average hours of service in a prior period (“measurement period”).

18

© Copyright 2014 Saul Ewing LLP

Using the Look-Back Method• Measurement periods can be no shorter than three (3) consecutive

months, no longer than twelve (12) months,• Stability periods can be no shorter than (6) consecutive months and

must be equal in length to the corresponding measurement period,• Standard measurement period for “ongoing” employees • “Initial” measurement period for newly hired “seasonal,” “part-time,”

or “variable hour employees.”• Optional “administrative period” (up to 90 days) to determine ACA

full-time status and conduct open enrollment – cannot shorten or extend either the measurement or stability period - overlaps.

• “Initial measurement period and administrative period, combined, cannot extend beyond the last day of the first calendar month beginning on or after the first anniversary of the employee’s hire date.

19

© Copyright 2014 Saul Ewing LLP

Look-Back Terminology• An “ongoing employee” is generally an employee who

has been employed by the employer for at least one complete standard measurement period.

• New employees whom the employer reasonably expects to work part-time (on average fewer than 30 hours a week) is “part-time.”

• New employees where don’t know if they will work more than 30 hours a week - “variable hour employee.”

• “Seasonal employee” – employee hired into a position for which the customary annual employment is six months or less.

20

© Copyright 2014 Saul Ewing LLP

Rules for Measurement/Stability Periods

• Each ALE member can establish its own measurement/stability periods, but limited to the following categories: • Collectively-bargained, non-collectively bargained.• Salaried, hourly• Each group of collectively-bargained employees covered

under a separate collective bargaining agreement• Employees located in different States.

Requires uniformity and consistency for all employees in the same category.

21

© Copyright 2014 Saul Ewing LLP

Avoiding a Pay or Play Penalty• Employers are not required to offer group health coverage to any

employee, but if you “play” – only have to offer coverage to employees who are ACA full-time employees

• No penalty unless an ACA full-time employee receives a premium tax credit or cost-sharing reduction for Health Insurance Marketplace coverage

• Individuals will not qualify for a premium tax credit or cost-sharing reduction unless their household income equals 100% to 400% of the federal poverty line

• Penalties do not apply for ACA full-time employees who enroll in your coverage – regardless of its affordability or minimum value.

• Penalties do not apply for ACA full-time employees who qualify for Medicaid.

22

© Copyright 2014 Saul Ewing LLP

Avoiding a Pay or Play Penalty

• You could incur penalties if you do not satisfy all of the conditions of certain transition rules (ALEs with fewer than 100 FTEs; Non-Calendar Year Plans).

• You could incur penalties if you don’t know how to count to 50 (using the controlled group rules and counting your full-time equivalents).

• You could incur penalties if you use contingent workers that may really be your common law employees and fail to include them in your head count and/or they get subsidized coverage in the Marketplace.

23

© Copyright 2014 Saul Ewing LLP

Assessing Your Options

• Pay or Play may not be as obvious an economic decision as it first appears

• Some facts to consider: • Premiums are deductible, the penalty is not• Offers to spouses are not required• You only have to offer coverage, actual enrollment is

not required• Affordability component is based on the lowest value

option offered for single-only coverage• If you offer higher value options that are not

“affordable” that’s okay

24

© Copyright 2014 Saul Ewing LLP

Traps for the Unwary

• Recordkeeping will be a key element to successfully navigating the ACA’s pay or play requirement. Final rules on IRS reporting standards and employee statements.

• Need to be able to substantiate that an employee was or was not an ACA full-time employee.

• Need to be able to show that each of your ACA full-time employees was, in fact, offered coverage (you will get advance notice of a potential penalty and have a chance to challenge it).

25

© Copyright 2014 Saul Ewing LLP

Traps for the Unwary

• Using contingent workers, such as independent contractors, has its risks.

• The ACA uses a common-law employee definition.

• If a contingent employee gets subsidized exchange coverage, then, in addition to pay or play penalties, you may incur additional liabilities if these individuals are reclassified as your employees.

26

© Copyright 2014 Saul Ewing LLP

Questions?

IRS CIRCULAR 230 DISCLOSURE: TO ENSURE COMPLIANCE WITH REQUIREMENTS IMPOSED BY THE IRS, WE INFORM YOU THAT ANY U.S. FEDERAL TAX ADVICE CONTAINED IN THIS COMMUNICATION (INCLUDING ANY ATTACHMENTS) IS NOT INTENDED OR WRITTEN TO BE USED, AND CANNOT BE USED, FOR THE PURPOSE OF (I) AVOIDING PENALTIES UNDER THE INTERNAL REVENUE CODE OR (II) PROMOTING, MARKETING OR RECOMMENDING TO ANOTHER PARTY ANY TRANSACTION OR MATTER ADDRESSED HEREIN.

27

© Copyright 2014 Saul Ewing LLP

BaltimoreLockwood Place • 500 East Pratt Street, Suite 900 • Baltimore, MD 21202-3171 • (tel) 410.332.8600 • (fax)

410.332.8862Boston

131 Dartmouth Street, Suite 501 • Boston, MA 02116 • (tel) 617.723.3300 • (fax) 617.723.4151

HarrisburgPenn National Insurance Plaza • 2 North Second Street, 7th Floor • Harrisburg, PA 17101-1619 • (tel) 717.257.7500 •

(fax) 717.238.4622New York

245 Park Avenue, 24th Floor • New York, NY 10167 • (tel) 212.672.1995 • (fax) 212.372.8798

NewarkOne Riverfront Plaza • Newark, NJ 07102 • (tel) 973.286.6700 • (fax) 973.286.6800

PhiladelphiaCentre Square West • 1500 Market Street, 38th Floor • Philadelphia, PA 19102-2186 • (tel) 215.972.7777 • (fax)

215.972.7725

Princeton650 College Road East, Suite 4000 • Princeton, NJ 08540-6603 • (tel) 609.452.3100 • (fax) 609.452.3122

Washington1919 Pennsylvania Avenue, N.W. Suite 550 • Washington, DC 20006-3434 (tel) 202.333.8800 • (fax) 202.337.6065

Wilmington222 Delaware Avenue • Suite 1200 P.O. Box 1266 • Wilmington, DE 19899• (tel) 302.421.6800 • (fax) 302.421.6813

Chesterbrook1200 Liberty Ridge Drive, Suite 200 • Wayne, PA 19087-5569 • (tel) 610.251.5050 • (fax) 610.651.5930

PittsburghOne PPG Place • 30th Floor • Pittsburgh, PA 15222 • (tel) 412.209.2500 • (fax) 412.209.2570