Embed Size (px)

Citation preview

KGS

If opportunity doesn’t knock, build a door – Milton Berle

INTEGRITY FIRST

KGS

S. No. Topic

1.

Transitional Provisions under Goods & Service Tax Regime

2.

Mergers and Amalgamations under Companies Act, 2013

3.

Real Estate Regulations Act

4.

Impact of Ind AS Transfer Pricing

5.

Income Tax (8th Amendment) Rules, 2017

INDEX

Highlights:

Systematic Transition

Regulatory Transition

Transitional Provisions

of Goods & Service Tax

Garima Sharma and Deeksha Kaushik

KGS

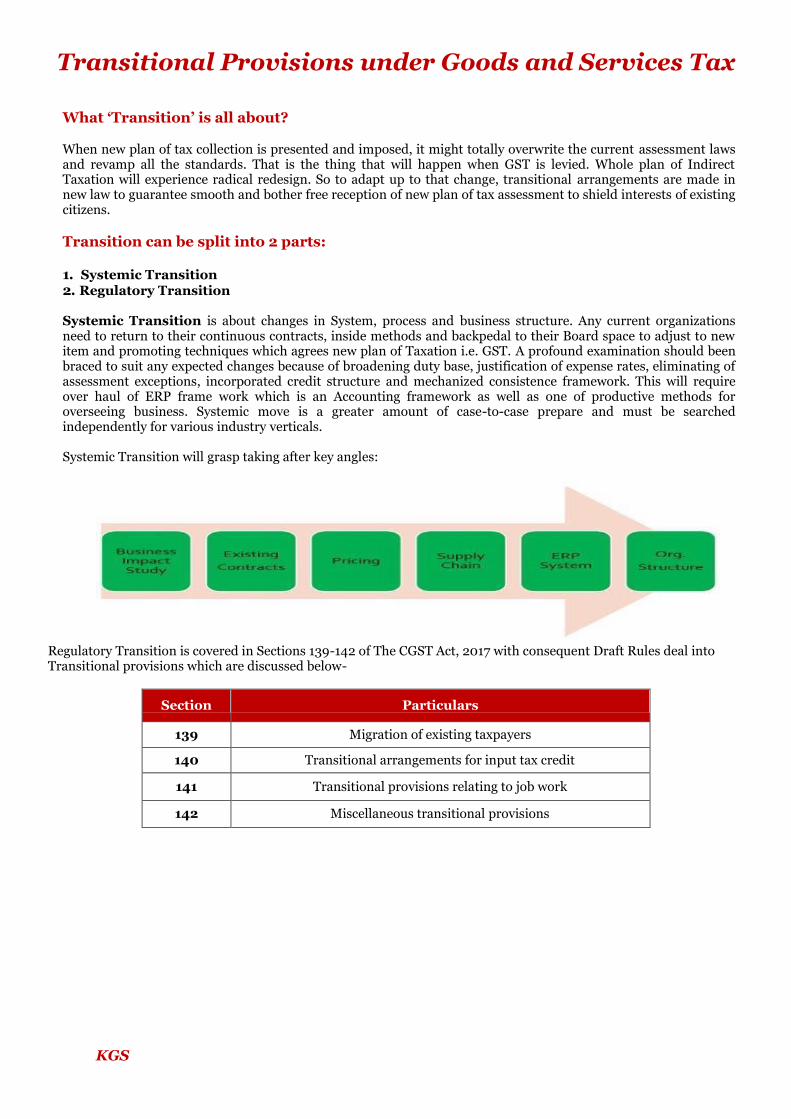

Transitional Provisions under Goods and Services Tax

What ‘Transition’ is all about?

When new plan of tax collection is presented and imposed, it might totally overwrite the current assessment laws and revamp all the standards. That is the thing that will happen when GST is levied. Whole plan of Indirect Taxation will experience radical redesign. So to adapt up to that change, transitional arrangements are made in new law to guarantee smooth and bother free reception of new plan of tax assessment to shield interests of existing citizens.

Transition can be split into 2 parts:

1. Systemic Transition 2. Regulatory Transition

Systemic Transition is about changes in System, process and business structure. Any current organizations need to return to their continuous contracts, inside methods and backpedal to their Board space to adjust to new item and promoting techniques which agrees new plan of Taxation i.e. GST. A profound examination should been braced to suit any expected changes because of broadening duty base, justification of expense rates, eliminating of assessment exceptions, incorporated credit structure and mechanized consistence framework. This will require over haul of ERP frame work which is an Accounting framework as well as one of productive methods for overseeing business. Systemic move is a greater amount of case-to-case prepare and must be searched independently for various industry verticals.

Systemic Transition will grasp taking after key angles:

Regulatory Transition is covered in Sections 139-142 of The CGST Act, 2017 with consequent Draft Rules deal into Transitional provisions which are discussed below-

Section Particulars

139 Migration of existing taxpayers

140 Transitional arrangements for input tax credit

141 Transitional provisions relating to job work

142 Miscellaneous transitional provisions

KGS

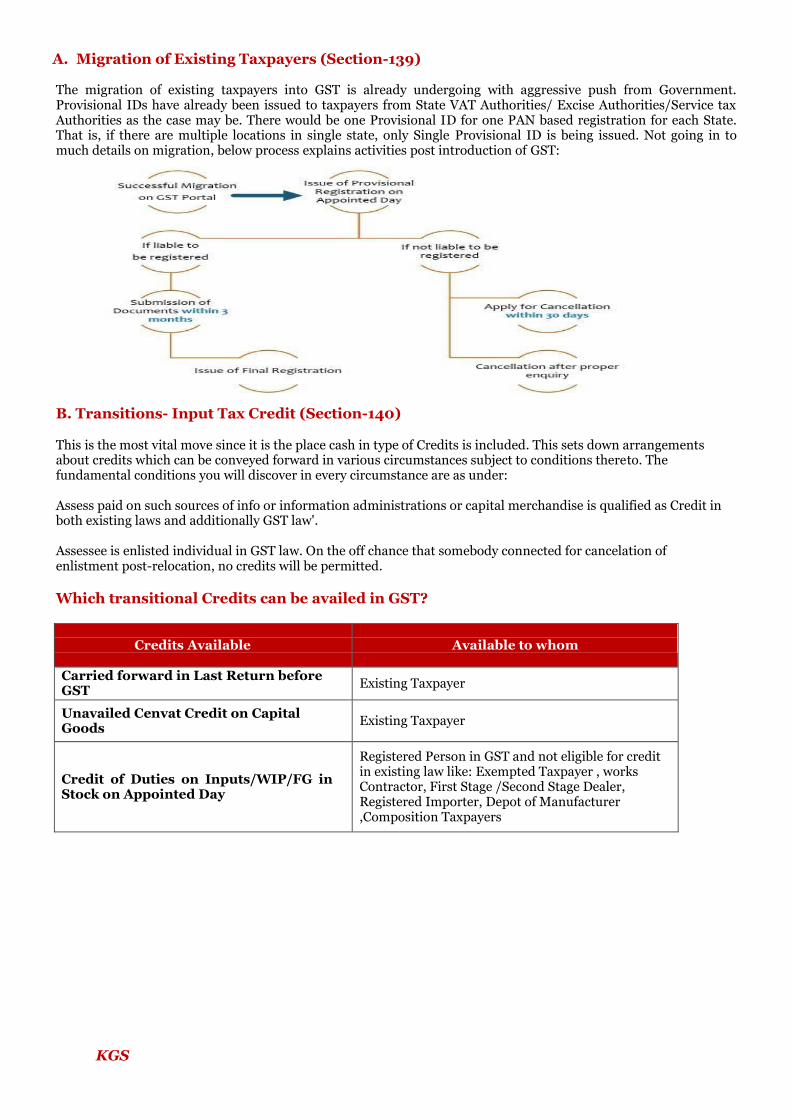

A. Migration of Existing Taxpayers (Section-139)

The migration of existing taxpayers into GST is already undergoing with aggressive push from Government. Provisional IDs have already been issued to taxpayers from State VAT Authorities/ Excise Authorities/Service tax Authorities as the case may be. There would be one Provisional ID for one PAN based registration for each State. That is, if there are multiple locations in single state, only Single Provisional ID is being issued. Not going in to much details on migration, below process explains activities post introduction of GST:

B. Transitions- Input Tax Credit (Section-140)

This is the most vital move since it is the place cash in type of Credits is included. This sets down arrangements about credits which can be conveyed forward in various circumstances subject to conditions thereto. The fundamental conditions you will discover in every circumstance are as under:

Assess paid on such sources of info or information administrations or capital merchandise is qualified as Credit in both existing laws and additionally GST law'.

Assessee is enlisted individual in GST law. On the off chance that somebody connected for cancelation of enlistment post-relocation, no credits will be permitted.

Which transitional Credits can be availed in GST?

Credits Available

Available to whom

Carried forward in Last Return before GST

Existing Taxpayer

Unavailed Cenvat Credit on Capital Goods

Existing Taxpayer

Credit of Duties on Inputs/WIP/FG in Stock on Appointed Day

Registered Person in GST and not eligible for credit in existing law like: Exempted Taxpayer , works Contractor, First Stage /Second Stage Dealer, Registered Importer, Depot of Manufacturer ,Composition Taxpayers

KGS

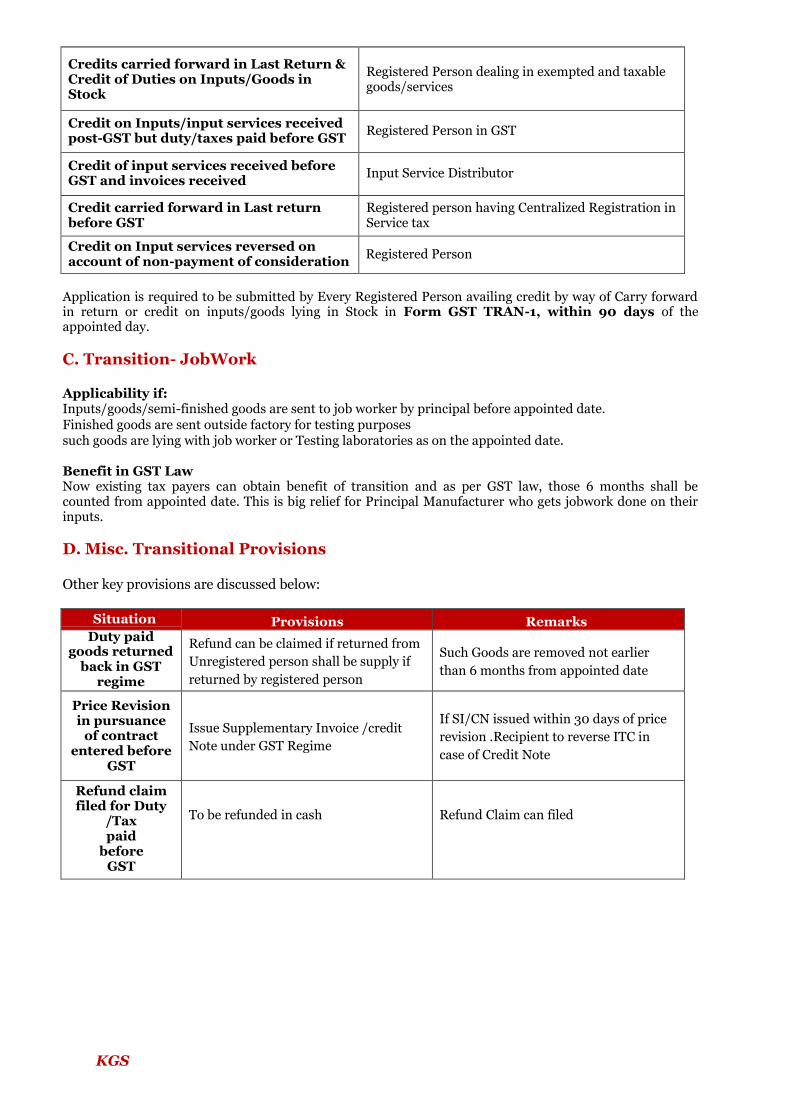

Credits carried forward in Last Return & Credit of Duties on Inputs/Goods in Stock

Registered Person dealing in exempted and taxable goods/services

Credit on Inputs/input services received post-GST but duty/taxes paid before GST

Registered Person in GST

Credit of input services received before GST and invoices received

Input Service Distributor

Credit carried forward in Last return before GST

Registered person having Centralized Registration in Service tax

Credit on Input services reversed on account of non-payment of consideration

Registered Person

Application is required to be submitted by Every Registered Person availing credit by way of Carry forward in return or credit on inputs/goods lying in Stock in Form GST TRAN-1, within 90 days of the appointed day.

C. Transition- JobWork

Applicability if: Inputs/goods/semi-finished goods are sent to job worker by principal before appointed date. Finished goods are sent outside factory for testing purposes such goods are lying with job worker or Testing laboratories as on the appointed date.

Benefit in GST Law Now existing tax payers can obtain benefit of transition and as per GST law, those 6 months shall be counted from appointed date. This is big relief for Principal Manufacturer who gets jobwork done on their inputs.

D. Misc. Transitional Provisions

Other key provisions are discussed below:

Situation Provisions Remarks Duty paid

goods returned back in GST

regime

Refund can be claimed if returned from

Unregistered person shall be supply if

returned by registered person

Such Goods are removed not earlier

than 6 months from appointed date

Price Revision in pursuance

of contract entered before

GST

Issue Supplementary Invoice /credit

Note under GST Regime

If SI/CN issued within 30 days of price

revision .Recipient to reverse ITC in

case of Credit Note

Refund claim filed for Duty

/Tax paid

before GST

To be refunded in cash

Refund Claim can filed

This article aims to:

Types of Mergers and Demergers

Methods of Valuation

Steps and Forms Involved u/s 230 & 232

Process of Mergers/ Amalgamation of Companies

Mergers and

Amalgamations under

Companies Act, 2013

Tayaab Ali and Kartik Saini

k

KGS

Mergers and Amalgamations under Companies Act, 2013

A Merger or Amalgamation is an arrangement whereby the assets of two or more companies become vested in one company (which may or may not be one of the original two companies). It is a legal process by which two or more companies are joined together to form a new entity or one or more companies are absorbed by another company and as a consequence the amalgamating company loses its existence and its shareholders become the shareholders of the new or amalgamated company.

De-merger is an arrangement whereby some part /undertaking of one company is transferred to another company which operates completely separate from the original company. Shareholders of the original company are usually given an equivalent stake of ownership in the new company.

De-merger is undertaken basically for two reasons. The first as an exercise in corporate restructuring and the second is to give effect to kind of family partitions in case of family owned enterprises. A de- merger is also done to help each of the segments operate more smoothly, as they can now focus on a more specific task.

Merger and Amalgamations plays an important role in Indian economy. It enables Indian companies to merge, demerge, amalgamate, and undertake compromise or enter into arrangements with other companies. It is one of the ways of achieving inorganic growth.

Types of Mergers

1- A vertical merger is a merger between two companies that operate at separate stages of the production

process for a specific finished product. A vertical merger occurs when two or more firms, operating at

different levels within an industry's supply chain, merge operations.

2- A horizontal merger is a merger or business consolidation that occurs between firms that operate in the

same space, as competition tends to be higher and the synergies and potential gains in market share are

much greater for merging firms in such an industry.

3- A congeneric merger is a type of merger where two companies are in the same or related industries but do

not offer the same products. In a congeneric merger, the companies may share similar distribution

channels, providing synergies for the merger.

4- A conglomerate merger is a merger between firms that are involved in totally unrelated business activities.

There are two types of conglomerate mergers: pure and mixed.

Types of Demergers

1- In a spin-off, the parent company distributes shares of the subsidiary that is being spun-off to its existing

shareholders on a pro rata basis, in the form of a special dividend. The parent company typically receives no

cash consideration for the spin-off. Existing shareholders benefit by now holding shares of two separate

companies after the spin-off instead of one.

2- In a carve-out, the parent company sells some or all of the shares in its subsidiary to the public through an

initial public offering (IPO). Unlike a spin-off, the parent company generally receives a cash inflow through

a carve-out.

3- In a split-off, shareholders in the parent company are offered shares in a subsidiary, but they have to choose

between holding shares of the subsidiary or the parent company. A shareholder thus has two choices: (a)

continue holding shares in the parent company, or (b) exchange some or all of the shares held in the parent

company for shares in the subsidiary.

Benefits of Mergers

1- A merger may be accomplished tax-free for both parties.

2- A merger lets the target (in effect, the seller) realize the appreciation potential of the merged entity, instead

of being limited to sales proceeds.

3- A merger allows the shareholders of smaller entities to own a smaller piece of a larger pie, increasing their

overall net worth.

4- A merger of a privately held company into a publicly held company allows the target company share holders

KGS

to receive a public company's stock, despite the liquidity restrictions.

5- A merger allows the acquirer to avoid many of the costly and time-consuming aspects of asset purchases,

such as the assignment of leases and bulk-sales notifications.

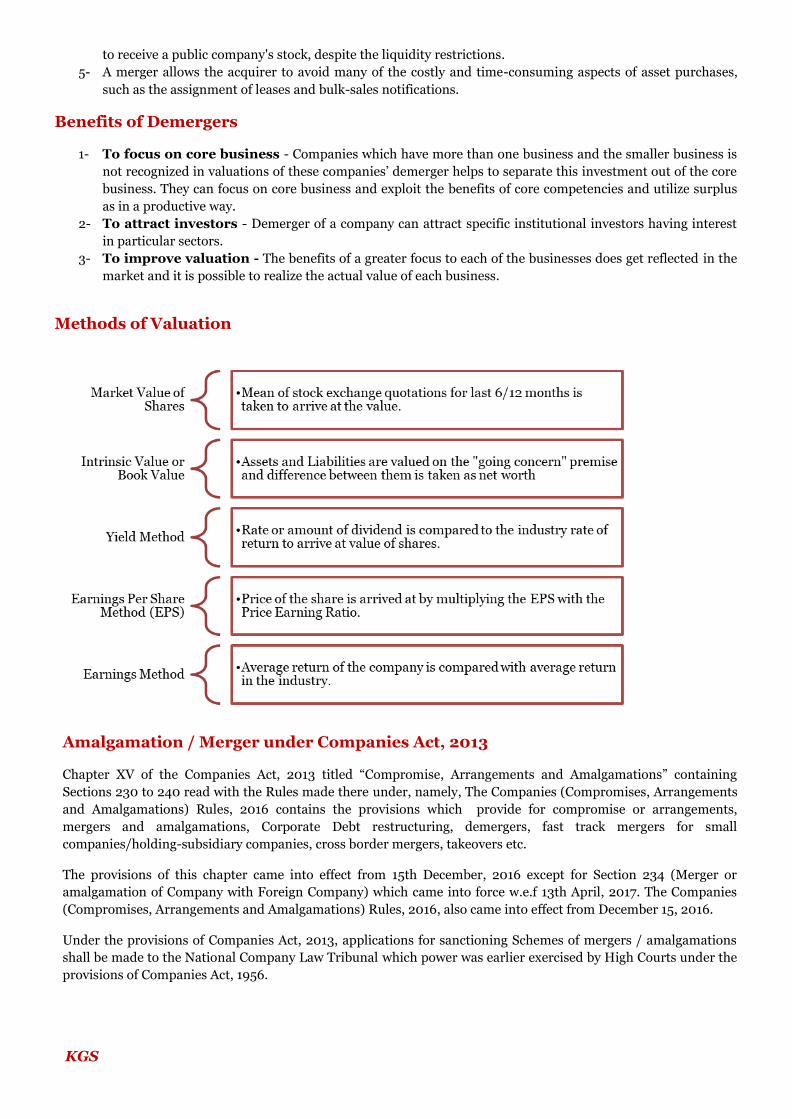

Benefits of Demergers

1- To focus on core business - Companies which have more than one business and the smaller business is

not recognized in valuations of these companies’ demerger helps to separate this investment out of the core

business. They can focus on core business and exploit the benefits of core competencies and utilize surplus

as in a productive way.

2- To attract investors - Demerger of a company can attract specific institutional investors having interest

in particular sectors.

3- To improve valuation - The benefits of a greater focus to each of the businesses does get reflected in the

market and it is possible to realize the actual value of each business.

Methods of Valuation

Amalgamation / Merger under Companies Act, 2013

Chapter XV of the Companies Act, 2013 titled “Compromise, Arrangements and Amalgamations” containing

Sections 230 to 240 read with the Rules made there under, namely, The Companies (Compromises, Arrangements

and Amalgamations) Rules, 2016 contains the provisions which provide for compromise or arrangements,

mergers and amalgamations, Corporate Debt restructuring, demergers, fast track mergers for small

companies/holding-subsidiary companies, cross border mergers, takeovers etc.

The provisions of this chapter came into effect from 15th December, 2016 except for Section 234 (Merger or

amalgamation of Company with Foreign Company) which came into force w.e.f 13th April, 2017. The Companies

(Compromises, Arrangements and Amalgamations) Rules, 2016, also came into effect from December 15, 2016.

Under the provisions of Companies Act, 2013, applications for sanctioning Schemes of mergers / amalgamations

shall be made to the National Company Law Tribunal which power was earlier exercised by High Courts under the

provisions of Companies Act, 1956.

KGS

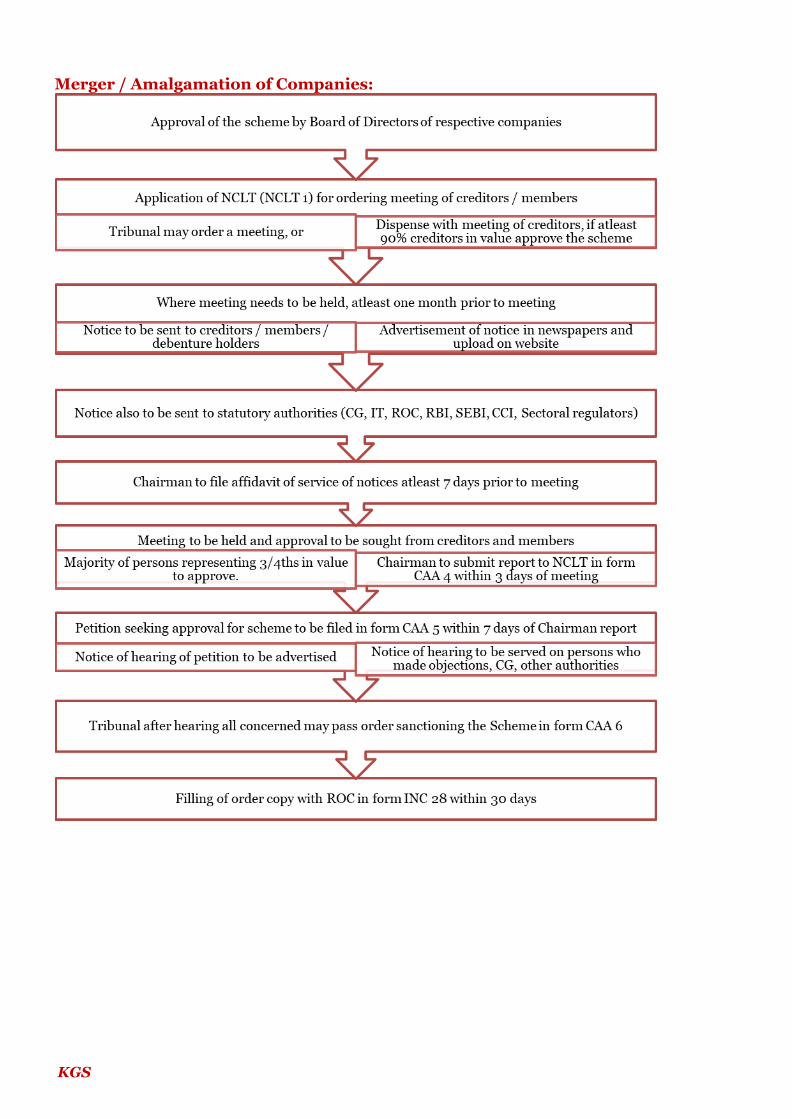

Merger / Amalgamation of Companies:

KGS

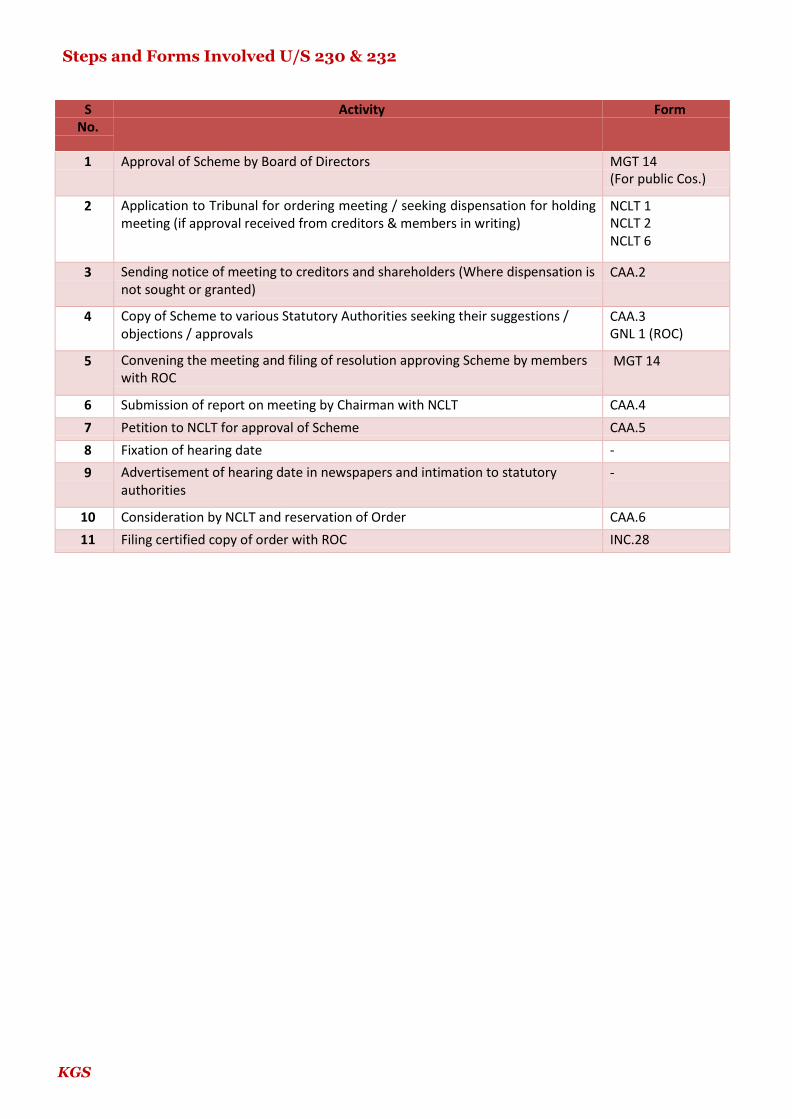

Steps and Forms Involved U/S 230 & 232

S

No. Activity Form

1 Approval of Scheme by Board of Directors MGT 14 (For public Cos.)

2 Application to Tribunal for ordering meeting / seeking dispensation for holding meeting (if approval received from creditors & members in writing)

NCLT 1 NCLT 2 NCLT 6

3 Sending notice of meeting to creditors and shareholders (Where dispensation is not sought or granted)

CAA.2

4 Copy of Scheme to various Statutory Authorities seeking their suggestions / objections / approvals

CAA.3 GNL 1 (ROC)

5 Convening the meeting and filing of resolution approving Scheme by members with ROC

MGT 14

6 Submission of report on meeting by Chairman with NCLT CAA.4

7 Petition to NCLT for approval of Scheme CAA.5

8 Fixation of hearing date -

9 Advertisement of hearing date in newspapers and intimation to statutory authorities

-

10 Consideration by NCLT and reservation of Order CAA.6

11 Filing certified copy of order with ROC INC.28

This article aims to:

Major Provision of Real Estate Act

Impact of Real Estate Act

from 1st May 2017

CA. Puneet Mehra and Simran Aggarwal

k

KGS

Impact of Real Estate Act from 1st May 2017

1) Introduction of Real Estate Act

Real Estate Act comes into force from 1 May 2017. A new era begins, says the Government Ongoing

and new projects shall be registered with Regulatory Authorities by July end model Regulations issued

by the Government Regulation of real estate sector becomes a reality ending nine year wait

Ending the nine year long wait, regulation of real estate sector involving over 76,000 companies

across the county becomes a reality from May 1, 2017 with the Real Estate (Regulation &

Development) Act, 2016 coming in to force.

With all the 92 Sections of the Act coming in to effect from tomorrow, developers shall get all the on

going projects that have not received Completion Certificate and the new projects registered with

Regulatory Authorities within three months i.e. by July end. This enables the buyers to enforce their

rights and seek redressal of grievances after such.

2) Some of the major provisions of the Act, besides mandatory registration of

projects and Real Estate Agents include:

Depositing70%ofthefundscollectedfrombuyersinaseparatebankaccountincaseofnew projects and

70% of unused funds in case of on going projects;

Projects with plot size of minimum 500 sq.mt or 8 apartments shall be registered with

Regulatory Authorities;

Both developers and buyers to pay the same penal interest of SBI’s Marginal Cost of Lending Rate

plus 2% in case of delays;

Liability of developers for structural defects for five years ;and

Imprisonmentofuptothreeyearsfordevelopersanduptooneyearincaseofagentsand buyers for

violation of orders of Appellate Tribunals and Regulatory Authorities.

3) Chronology of events leading to regulation of real estate sector including both

residential and commercial segments from May 1,2017.

May,2008:Ministry of HUPA first prepared a Concept Paper on regulation of real estate sector and a

model law for legislation by States/UTs;

Conference of Ministers of Housing in 2011 suggested a central law for regulation of real estate

sector;

July,2011:Ministry of Law & Justice too suggested central legislation for regulation;

June,2013:Union Cabinet approved Real Estate Bill,2013

August, 2013: Real Estate Bill was introduced in Rajya Sabha and was referred to Standing

Committee.

KGS

February,2014: Report of Standing Committee was laid on the Tables of both houses of

Parliament;

February,2014: Attorney General up held validity of central law for regulation of the sector

April,2015: Union Cabinet approved official amendments based on recommendations of

Standing Committee;

May,2015:Matter referred to the Select Committee of Rajya Sabha

July,2015: Report of Select Committe established in RajyaSabha

December,2015: Real Estate Bill,2015 incorporating several modifications based on Select

Committee report and stakeholder consultations was approved by the Union Cabinet;

March 10, 2016: The Real Estate (Regulation & Development) Bill, 2016 passed by Rajya

Sabha;

March15,2016:LokSabha passed the Bill as passed by RajyaSabha;

March25,2016:President gives as sent to the Bill;

April 26, 2016: 59 Sections of the Act were notified making them effective from May 1, 2016

enabling preparation of Real Estate Rules, setting up of Regulatory Authorities and other

infrastructure;

April19,2017: Remaining 32 Sections of the Act notified making them effective from May 1st this

year requiring registration of projects with in three months from tomorrow.

May1,2017:New era begins for development of real estate sector in an atmosphere of investor

confidence.

4) KeyPoints:

Developers will have to submit as well a supload project details, including approved layout plan,

timeline, cost, and the sale agreement, that prospective buyers will have to sign to the proposed

regulator.

It makes it mandatory for all builders-developing a project where the land exceeds 500square metre

- to register with RERA before launching or even advertising their project. Developers have been

given time until July 31 to register.

Developers will have to put 50% of the money collected from a buyer in a separate account to meet

the construction cost of the project. This will put a check to the general practice by developers to

divert buyer’s money to start a new project instead of finishing the one for which money was

collected. This will ensure that construction is completed on time.

Thelawislikelytostabilisehousingprices.Itwillleadtoenhancedactivityinthesector,leading to more

housing units supplied to the market.

It will weed out fly-by-night operators from the sector and channelize investment in to it.

Builderswillalsobenefitasthelawhaspenalprovisionsforallotteeswhodonotpaydueson

time.Thebuildercanalsoapproachtheregulatorincasethereisanyissuewiththebuyer.

As of now, the real estate sector was largely unregulated in India. If a consumer had a complaint

against a developer they had to make rounds of consumer or civil courts. Now, in case of any

grievance, the consumer can go to the real estate regulator for red ressal.

Real Estate Appellate Tribunals to be set up in every state.

This article aims to:

Introduction of IndAS

Impact on Transfer Pricing

Real Impact of Ind AS on

Transfer Pricing

CA Chandan Kumar and Mukul Maheshwari

KGS

Impact of Ind AS on Transfer Pricing

1) Introduction of Ind AS

Indian Accounting Standards (Ind-AS) were issued under the supervision and control of Accounting Standards

Board (ASB), which was constituted as a body in the year 1977. ASB is a committee under Institute of Chartered

Accountants of India (ICAI) which consists of representatives from government department, academicians, other

professional body’s viz. ICAI, representatives from ASSOCHAM, CII,FICCI, etc.

The Ind AS are named and numbered in the same way as the corresponding International Financial Reporting

Standards (IFRS). National Advisory Committee on Accounting Standards (NACAS) recommends these standards

to the Ministry of Corporate Affairs (MCA). MCA has to spell out the accounting standards applicable for companies

in India. As on date MCA has notified 39 Ind AS. This shall be applied to the companies of financial year 2015-16

voluntarily and from 2016-17 on a mandatory basis.

Based on the international consensus, the regulators will separately notify the date of implementation of Ind-AS for

the banks, insurance companies etc. Standards for the computation of Tax have been notified as ICDS in February

2015.

2) Impact on Transfer Pricing

Transfer pricing analysis using the Transactional Net Margin Method (TNMM) may be impacted substantially as a

result of transition to Ind-AS.

TNMM compares the profitability of the comparable companies using different PLIs. PLIs are ratios of financial

statement line items that are used to determine the profitability for a given company. The PLI selected is one that

produces the most reliable measure of income. Common PLIs include operating profit/sales, operating profit/

operating costs, return on operating assets and gross profits/ operating expenses (berry ratio). Computation of the

PLIs would be impacted by the accounting treatment of various items of income and expenditure.

Operating profit is a key metric used in many transfer pricing analysis. Timing of recognition of income and expense

can differ between Ind-AS and existing accounting standards. Classification between operating result and other

income/ expense can also differ. These differences could create comparability issues with regard to PLIs. Balance

sheet amounts are used in transfer pricing analysis for both PLI purpose (e.g. return on assets) and reliability

adjustments (e.g. working capital adjustments). Differences in balance sheet recognition and/ or classification could

present comparability issues and adjustment reliability issues.

In fact, the recently issued draft scheme on proposed transfer pricing rules seeks to make the use of a three year

average mandatory. Given the transition road map, it is possible that two different sets of accounting principles could

be included in the multi-year comparable data. Public databases that are currently used would not be able to present

both Ind-AS and existing accounting standards information for all the years in the analysis window. A mix of

standards in the analysis window could cause the analysis to become less reliable.

Conclusion

Any company with related party transactions that is expected to transition to Ind-AS should look very carefully at its

transfer pricing analysis and documentation since it may not be appropriate to compare "Ind-AS apples" with

"existing accounting standard oranges" used by comparables. The tested party may need to convert back to existing

accounting standard (for transfer pricing purpose) if that is the standard used by the comparables. Some companies

may see the range of arm's length profits shift due to the use of Ind-AS, even though the economics of their

companies and that of the comparable companies do not change. It may be the case that a company whose transfer

pricing was within arm's length range of profitability under existing accounting standards may find itself outside the

arm's length range of profitability under Ind-AS or on account of lack of harmonization in accounting policies on

account of the phased transition. Transfer pricing is a significant issue in transition to Ind-AS. Tax authorities would

need to work with industry and other stake holders to find a resolution to issues arising in connection with the

conversion. However, companies will be expected to take the initiative in evaluating and documenting why their

position supports an arm's length price.

This article aims to:

Valuation of Assets

Purpose of the rule

Income-Tax

(8th Amendment) Rules,

2017

CA.JITIN GIRDHAR

KGS

Income-tax (8th Amendment) Rules, 2017

1. They shall be deemed to have come into force from the 1st day of June,2016.

In the Income-tax Rules, 1962, after rule 17CA, the following rule shall be inserted, namely: “17CB. Method of

valuation for the purposes of sub-section (2) of section 115TD.

For the purpose of sub-section (2) of section 115 TD of the Act, the aggregate fair market value of the total assets of

the trust or institution, shall be the aggregate of the fair market value of all the assets in the balance sheet as reduced

by-

any amount of income-tax paid as deduction or collection at source or as advance tax payment as reduced by the

amount of income-tax claimed as refund under the Act, and

any amount shown as asset including the un amortised amount of deferred expenditure which does not represent

the value of any asset.

2. Valuation of Assets:

i. Valuation of shares and securities—

ii. the fair market value of quoted share and securities shall be the following:

the average of the lowest and highest price of such shares and securities quoted on a recognised stock

exchange as on the specified date; or

where on the specified date, there is no trading in such shares and securities on a recognised stock

exchange, the average of the lowest and highest price of such shares and securities on a recognised stock

exchange on a date immediately preceding the specified date when such shares and securities were

traded on a recognised stock exchange,

iii. the fair market value of unquoted equity shares shall be the value, on the specified date as determined in

accordance with the following formula, namely:

Fair market value of unquoted equity shares = (A+B - L) × (PV)/ (PE)where,

A = book value of all the assets in the balance sheet

(Other than bullion, jewellery, precious stone, artistic work, shares, securities, and immovable property)

as reduced by-

iv. any amount of income-tax paid as deduction or collection at source or as advance tax payment as reduced by

the amount of income-tax claimed as refund under the Act; and

v. any amount shown in the balance sheet as asset including the un amortised amount of deferred expenditure

which does not represent the value of any asset;

B=fair market value of bullion, jewellery, precious stone, artistic work, shares, securities and immovable

property as determined in the manner provided in this rule;

L=book value of liabilities shown in the balance sheet, but not including the following amounts, namely:

vi. representing contingent liabilities other than arrears of dividends payable in respect of the paid-up capital in

respect of equity shares;

vii. the amount set apart for payment of dividends on preference shares and equity shares;

viii. reserves and surplus, by whatever name called, even if the resulting figure is negative, other than those set

apart towards depreciation;

ix. any amount representing provision for taxation, other than amount of income-tax paid as deduction or

collection at source or as advance tax payment as reduced by the amount of income-tax claimed as refund

under the Act, to the extent of the excess over the tax payable with reference to the book profits in accordance

with the law applicable thereto;

x. any amount representing provisions made for meeting liabilities, other than ascertained liabilities;

xi. any amount cumulative preference shares;

PE = total amount of paid up equity share capital as shown in the balance-sheet; PV= the paid up value

KGS

of such equity share,

xii. The fair market value of shares and securities other than equity shares shall be estimated to be price it would

fetch if sold in the open market on the specified date based on the valuation report from a merchant banker or

an accountant in respect of such valuation.

xiii. The fair market value of an immovable property shall be higher of the following-

xiv. price that the property shall ordinarily fetch if sold in the open market on the specified date on the basis of the

valuation report from a registered valuer; and

xv. stamp duty value as on the specified date.

xvi. The fair market value of a business undertaking, held by a trust or institution, shall be its net assets

determined in accordance with the following formula:-

Fair market value = (A + B-L), which shall be determined in the manner provided in sub-clause (b) of clause (I) of sub

rule (2).

The fair market value of any asset, other than those referred to in clauses (I), (II) and (III), shall be the

price that the asset shall ordinarily fetch if sold in the open market on the specified date on the basis of

valuation report from a registered valuer: Provided that in case no valuer is registered for valuation of such

assets, the valuation report shall be obtained from a valuer who is a member of any one of the professional

valuer bodies.

Institution of Valuers, Institution of Surveyors (Valuation Branch), Institution of Government Approved

Valuers, Practicing Valuers Association of India, the Indian Institution of Valuers, Centre for Valuation

Studies, Research and Training, Royal institute of Chartered Surveyors; India Chapter, American Society of

Appraisers, USA; Appraisal institute, USA or a valuer who is appointed by any public sector bank or public

sector undertakings for valuation purposes.

xvii. For the purpose of sub-section (2) of section 115 TD of the Act, the total liability of the trust or institution shall

be the book value of liabilities in the balance sheet on the specified date but not including the following

amounts, namely:—

reserves or surpluses or excess of income over expenditure, by whatever name called;

any amount representing contingent liability;

any amount representing provisions made for meeting liabilities, other than ascertained liabilities;

xviii. Any amount representing provision for taxation, other than amount of tax paid as deduction or collection at

source or as advance tax payment as reduced by the amount of income-tax claimed as refund under the Act, to

the extent of the excess over the income-tax payable with reference to the income in accordance with the law

applicable thereto.

3. Explanation for the Purpose of this Rule: 1. "accountant" shall mean a fellow of the Institute of Chartered Accountants of India within the meaning of the

Chartered Accountants Act, 1949 (38 of 1949) who is not appointed by the trust or institution as an auditor;

2. "balance-sheet” in relation to any trust or institution, shall mean the balance-sheet of such trust or institution

(including the notes annexed thereto and forming part of the accounts) as drawn up on the specified date which

has been audited by an accountant;

3. “merchant banker” shall mean a category I merchant banker registered with Securities and Exchange Board of

India established under section 3 of the Securities and Exchange Board of India Act, 1992 (15 of1992);

4. "quoted share or security" in relation to share or security means a share or security quoted on any recognised

stock exchange with regularity from time to time, where the quotations of such shares or securities are based

on current transaction made in the ordinary course of business;

5. "Recognised stock exchange" shall have the same meaning as assigned to it in clause(f) of section 2 of the Securities Contracts (Regulation) Act, 1956 (42 of 1956);

6. "registered valuer" means a person registered as a valuer under section 34AB of the Wealth-tax Act, 1957 (27

of1957);

7. "securities" shall have the same meaning as assigned to it in clause (h) of section 2 of the Securities Contracts

(Regulation) Act, 1956 (42 of1956);

KGS

8. “specified date" means the date referred to in Explanation to section 115TD of the Act;

9. "stamp duty value" means the value adopted or assessed or assessable by any authority of the Central

Government or a State Government for the purpose of payment of stamp duty in respect of an immovable

property;

10. “Unquoted share and security” in relation to share or security means share or security which is not a quoted

share or security.”

KGS

Contact Name E-mail Mobile

Mr. Anuj Somani [email protected] +91 9871098777 Mr. Bhuvnesh Maheshwari [email protected] +91 9810031993

Head office: Branch Offices: Network Offices: DELHI MUMBAI BANGALORE

Delite Cinema Hall 3rdFloor, Gate No. 2, New Delhi, India

GHAZIABAD

GURGAON

BHOPAL

BUBNESHWAR

SILIGURI CHENNAI

CHENNAI KOLKATA

Disclaimer

• This material and the information contained herein prepared by the authors is of a general nature and

does not exhaustively deal with the subject discussed. • Although the authors have put their earnest effort in providing accurate and appropriate information,

the article is not intended to be relied upon as the sole basis for any decision which may affect you or your business.Theauthorsrecommendyoutakeprofessionaladvicebeforeactingonspecificissues.

• KGS is neither responsible for any views, opinions and statements made by the authors nor is liable for consequences, if any, arising from actions based on such views or opinion.

Contact Us