Embed Size (px)

Citation preview

1

PUT TITLE HEREThe New Reporting Model

and Sample Forms

Information Session for School Board Finance Staff and External AuditorsTransfer Payments & Financial Reporting BranchFall 2008

2

Financial Reporting Model - Why??Financial Reporting Model - Why??

2 models of accounting in PSAB Handbook2 models of accounting in PSAB Handbook– Senior government reporting– Local government reporting

BackgroundBackground– Statement of Principles - September 2005– Exposure Draft - March 2006 (for comment)– Exposure Draft - November 2006 (approved)

Accounting StandardsAccounting Standards– PS 1000, PS1100, PS1200 - Senior – PS1700, PS1800 - Local (deleted effective Jan 1,

2009)

3

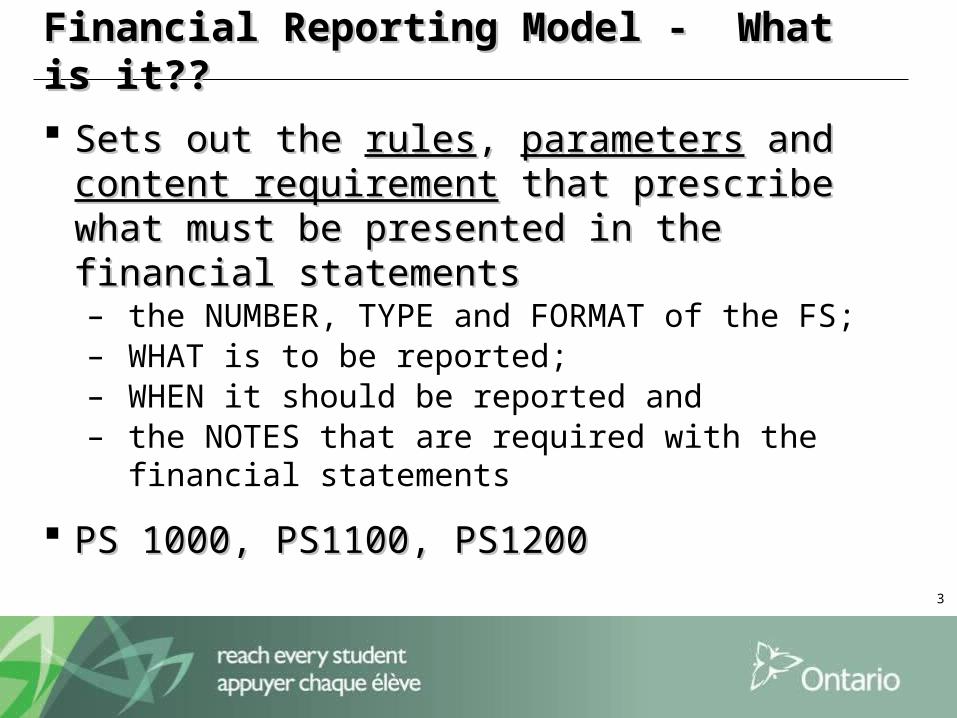

Financial Reporting Model - What is it??Financial Reporting Model - What is it??

Sets out the Sets out the rulesrules, , parametersparameters and and content content requirementrequirement that prescribe what must be that prescribe what must be presented in the financial statementspresented in the financial statements– the NUMBER, TYPE and FORMAT of the FS;– WHAT is to be reported;– WHEN it should be reported and– the NOTES that are required with the financial

statements

PS 1000, PS1100, PS1200PS 1000, PS1100, PS1200

4

Implementation Time FrameImplementation Time Frame

2008-09 DSB Financial Statements (Nov 09)2008-09 DSB Financial Statements (Nov 09)- Restatement of 2007/08 balances- Restatement of 2007/08 balances

2009-10 DSB Estimates (Jun 09)2009-10 DSB Estimates (Jun 09)

5

Key Features of New ModelKey Features of New Model

5 “Messages” about DSB finances:5 “Messages” about DSB finances:

Indicators of Financial Position1. Net Debt2. Accumulated surplus/deficit

Indicators of Changes in Financial Position3. Annual surplus/ (deficit)4. Change in net debt5. Cash Flows

Moves away from a one-dimensional focus on Moves away from a one-dimensional focus on surplus/deficitsurplus/deficit

6

What’s New? PSAB ChangesWhat’s New? PSAB Changes Statement of Financial Position Statement of Financial Position (page 2)(page 2)

– Tangible capital assets – Reserve Funds and Amounts to be Recovered (ATBR)

are gone– Indicator # 1: Net Debt– Indicator # 2: Accumulated Surplus / (deficit)

Statement of Operations Statement of Operations (page 3)(page 3) – Replaces Statement of Financial Activities – Gone are changes in prepaid expenses and changes

in ATBR– Includes amortization expense– Requires budgeted numbers– Indicator # 3: Annual surplus/ (deficit)

7

What’s New? PSAB ChangesWhat’s New? PSAB Changes

Statement of Changes in Net Debt - New Statement of Changes in Net Debt - New (page 4)(page 4)– Capital expenditures– Requires budgeted numbers– Indicator # 4: Change in Net Debt

Statement of Cash Flow Statement of Cash Flow (page 5)(page 5)– replaces Statement of Changes in Financial Position– New capital section– Indicator # 5: Cash Flows

8

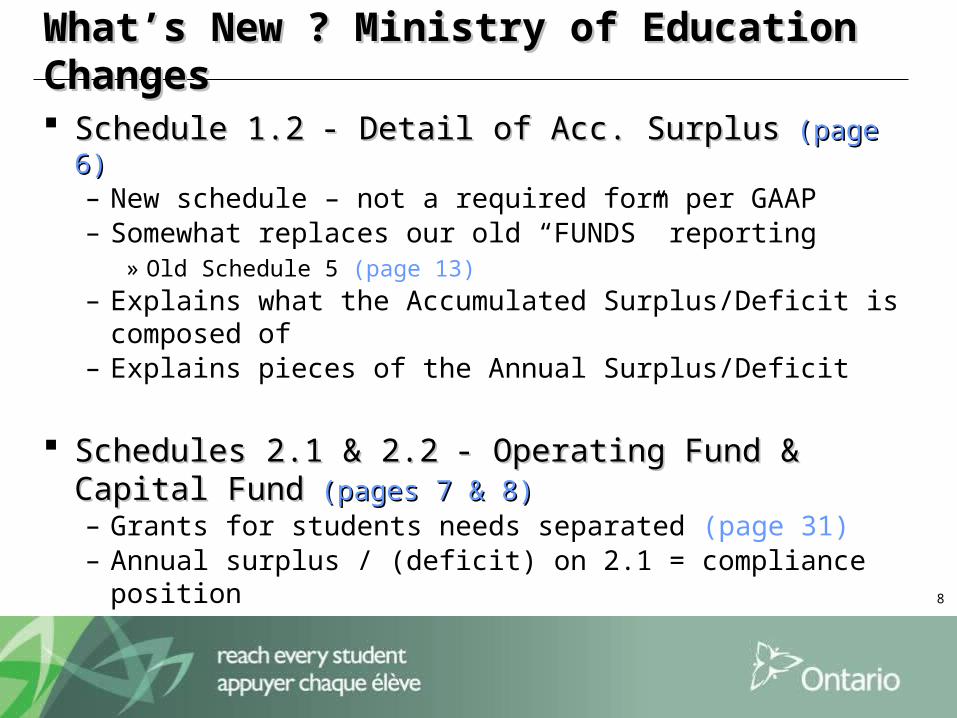

What’s New ? Ministry of Education Changes What’s New ? Ministry of Education Changes

Schedule 1.2Schedule 1.2 - Detail of Acc. Surplus- Detail of Acc. Surplus (page 6) (page 6)– New schedule – not a required form per GAAP– Somewhat replaces our old “FUNDS” reporting

» Old Schedule 5 (page 13)

– Explains what the Accumulated Surplus/Deficit is composed of

– Explains pieces of the Annual Surplus/Deficit

Schedules 2.1 & 2.2Schedules 2.1 & 2.2 - Operating Fund & Capital - Operating Fund & Capital FundFund (pages 7 & 8) (pages 7 & 8)– Grants for students needs separated (page 31)– Annual surplus / (deficit) on 2.1 = compliance position

9

What’s New ? Ministry of Education ChangesWhat’s New ? Ministry of Education Changes

Schedules 2.3 & 2.4Schedules 2.3 & 2.4 - Reserve Funds & School - Reserve Funds & School Activity FundsActivity Funds (pages 9 & 10) (pages 9 & 10)– Schedules are gone

Schedule 3 - Capital Expenditures Schedule 3 - Capital Expenditures (pages 11 & 12)(pages 11 & 12)– Page 1 is gone capital expenditures– Page 2 needs to be revamped

Schedule 8 - TCA Continuity Schedule 8 - TCA Continuity (pages 16 - 18)(pages 16 - 18)– By major asset class– Cost table– Accumulated amortization table– Inter-entity TCA transactions

10

What’s New ? Ministry of Education ChangesWhat’s New ? Ministry of Education Changes

Schedule 9 - RevenuesSchedule 9 - Revenues (pages 19 - 22) (pages 19 - 22)– Reorganization of schedule to align with statement of

operations groupings– Includes all sources of revenue – Segregation of capital & operating type revenues

Schedule 10 - ExpensesSchedule 10 - Expenses (pages 23 & 24) (pages 23 & 24)– Expenses and not expenditures– Schedule 3 disappears– Includes amortization expense– Same changes brought to Schedules 10.1, 10.2, 10A &

10B

11

What’s New ? Ministry of Education ChangesWhat’s New ? Ministry of Education Changes

Schedule 10ADJ - Compliance Schedules Schedule 10ADJ - Compliance Schedules (pages (pages 25 & 26)25 & 26)– Schedule gone / part of Schedule 2.1

Section 1 - Summary of AllocationsSection 1 - Summary of Allocations (page 31) (page 31)– Segregation of capital type grants from operating type

grants

12

Useful Reference DocumentUseful Reference Document

20 Questions about Government Financial 20 Questions about Government Financial ReportingReporting

http://www.psab-ccsp.ca/index.cfm/ci_id/18658/la_id/1 http://www.psab-ccsp.ca/index.cfm/ci_id/18658/la_id/1

Published in 2003 Published in 2003

Refers to Senior Levels of Government but still applicableRefers to Senior Levels of Government but still applicable

13

OtherOther

Hoping to finalize forms by DecemberHoping to finalize forms by December

Hands-on training sessions Feb / March 2009Hands-on training sessions Feb / March 2009– Video-conference + live in 1 central location

Constructive Comments & FeedbackConstructive Comments & FeedbackDoreen LamarcheDoreen LamarcheSenior Business & Policy AnalystSenior Business & Policy Analyst(613) 225-9210 x.113(613) 225-9210 [email protected]@ontario.ca