Embed Size (px)

Citation preview

1

Current Account

2

Issues and Applications

• Global capital markets and the current account

• Debt crisis in developing countries

• Sovereign risk

3

Balance of Payments Accounting: The Current Account (CA)

• The current account (CA): measures a country’s trade in currently produced goods and services

• A negative CA implies that a country is importing more than it is exporting

4

The Current Account around the World

5

• The capital and financial account (KFA) measures a country’s trade in financial assets

• Note that selling assets (e.g. bonds) is equivalent to borrowing and leads to inflow of capital, that is the rest of the world is lending money to us

The Capital and Financial Account (KFA)

6

• The current account and the capital financial account sum to zero

CA+KFA=0

• This equation is an Accounting Identity!

The Link Between CA and KFA

7

Savings, Investment and the Current Account

• We know from the Introduction that

NX + NFP = CA = S – I

• Focusing on S – I is equivalent to looking at the CA or the KFA

8

U.S. Current Account

Source: US Bureau of Economic Analysis

www.bea.gov

9

Savings, Investment, and CA

10

U.S. Net International Debt

$2.5 trillion is approx. 25% of GDP

11

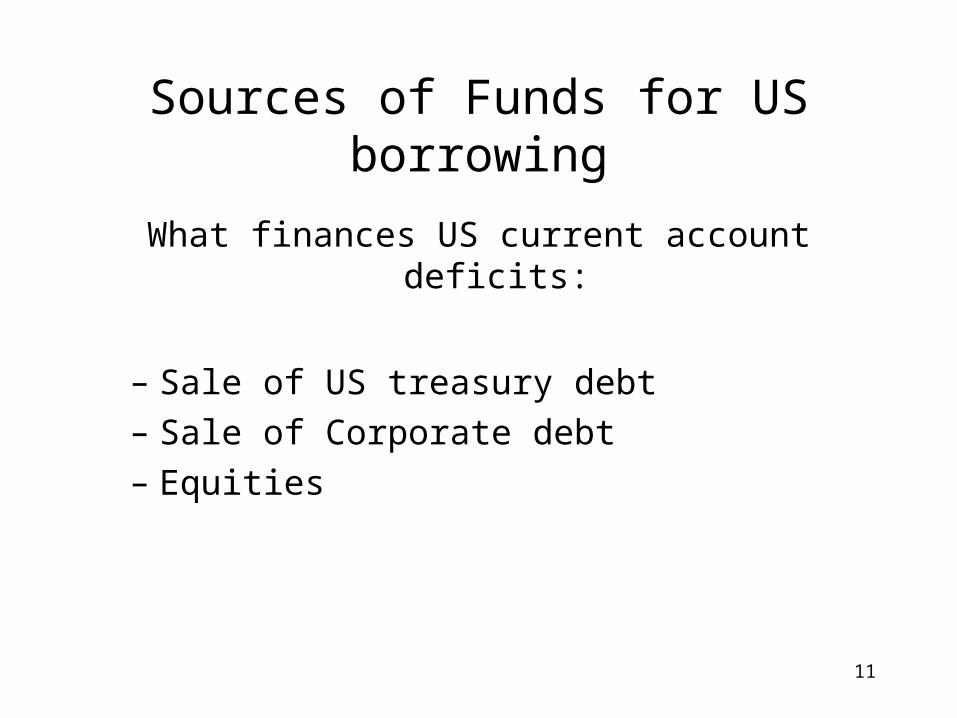

Sources of Funds for US borrowing

What finances US current account deficits:

– Sale of US treasury debt

– Sale of Corporate debt

– Equities

12

13

Global Capital Markets

• Financial markets in New York, London, Frankfurt, Tokyo

• Each country has savings

• All these savings enter global financial markets

• Each country has needs for investment in new plant and equipment

• The job of the global financial markets is to efficiently allocate the global pool of savings to investment opportunities in different countries

14

Determinants of Savings

• Aggregate savings is income minus consumption:

s = y – c – g

• Aggregate savings is the sum of private savings and government savings– Govt. Savings are Net Tax Revenue-Govt. expenditure

s = sp + sg

15

Determinants of National Saving

• An increase in the real interest rate causes desired national saving to rise, as the reward to savings rises, see Fig 1.

• An increase in G causes desired aggregate savings to fall, as overall consumption rises, Fig. 2.

• An temporary increase in Y causes desired national saving to rise, as households spread the rise in income over current and future consumption, Fig. 3.

r

S

r

S

r

S

Fig. 1 Fig. 2

Fig. 3

s1

s1

s2

s1

s2

16

Determination of the Current Account

Variables subscripted by w refer to global variables, and those subscripted by arg refer to Argentina.

17

Current Account

• The global capital markets determine the world real interest rate

• A country’s savings and investment determines its current account

18

Good Prospects and the Current Account

Does a country that experiences a permanent rise in TFP and thereby produces more goods and services respond by on net importing or exporting more goods and services?

19

Growth and the Current Account

20

Recessions and the Current Account

Current account deficit falls during recessions and rises during booms

21

Recent U.S. Current Account

Current account deficit continues to get larger

22

23

Economic Growth

Average Growth of GNP per Capita, 1965-90

0 1 2 3 4 5 6

HPAEs

South Asia

Middle East and Mediterranean

Sub-Saharan Africa

OECD Economies

Latin America and the Caribbean

GNP per capita growth rate (percent)

OECD refers to Organization of Economic Cooperation and Development. This includes the world’s 24 richest economies.

High performance Asian economies (HPAE) are: Singapore, Hong Kong, Thailand, Indonesia, Taiwan, Malaysia, Korea.

24

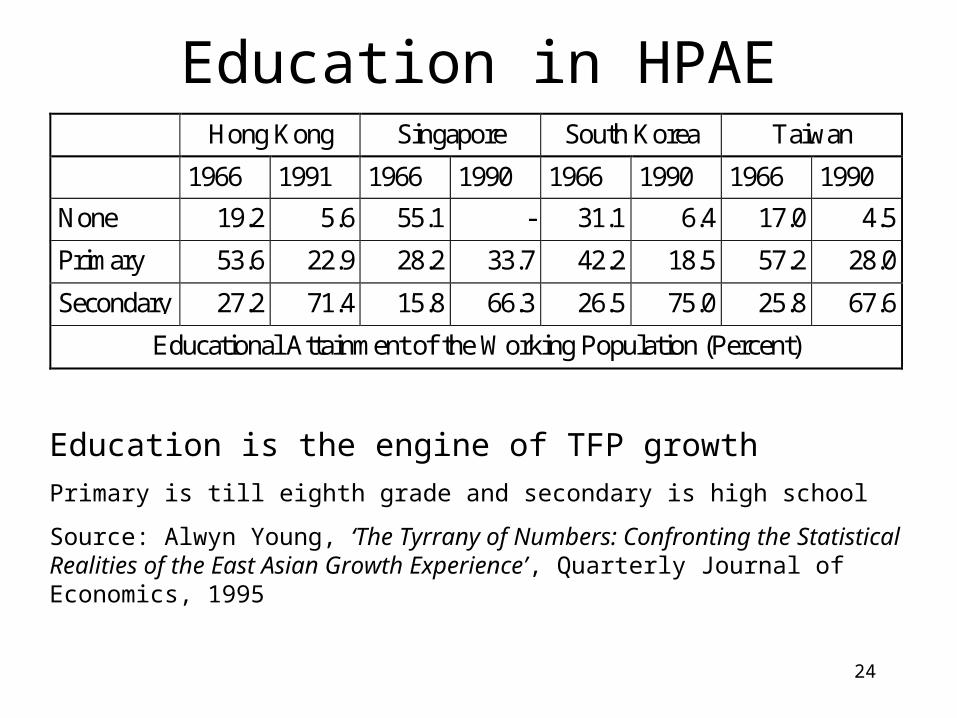

Education in HPAEHong Kong Singapore South Korea Taiwan

1966 1991 1966 1990 1966 1990 1966 1990

None 19.2 5.6 55.1 - 31.1 6.4 17.0 4.5

Primary 53.6 22.9 28.2 33.7 42.2 18.5 57.2 28.0

Secondary 27.2 71.4 15.8 66.3 26.5 75.0 25.8 67.6

Educational Attainment of the Working Population (Percent)

Education is the engine of TFP growth

Primary is till eighth grade and secondary is high school

Source: Alwyn Young, ‘The Tyrrany of Numbers: Confronting the Statistical Realities of the East Asian Growth Experience’, Quarterly Journal of Economics, 1995

25

High Investment

26

Current Account in HPAE

Current Account as % of GDP

-11

-6

-1

4

9

14

Ind

on

esia

Ko

rea

Mal

aysi

a

Sin

gap

ore

Th

aila

nd

1975

1985

1994

27

CA surplus in China, Germany, and Euro.Why?

High savings rate leads to a current account surplus

28

Sovereign Debt, External Debt, and Risk

29

Sovereign debt is debt issued by a government (also public debt)

30

Risk And Sovereign Debt

• Countries cannot be taken to court if they default on their borrowings

• This leads to sovereign risk which is reflected in the cost of borrowing

• Sovereign risk depends on the credibility of not defaulting on the debt

• Sovereign risk ratings are almost entirely determined by the macroeconomics of the country

– Lower Per-Capita income, Higher inflation, and Higher External Debt --- lower the country’s credit rating

– Sovereign debt to GDP is a key measure of the sustainability of government debt (although credible governments can sustain high debt-to-GDP levels)

31

Macro-economy and Sovereign Risk

Fiscal balance and external balance are relative to GDP. External debt refers to foreign currency debt relative to exports.

32

Sovereign Debt to GDP Ratio by Country

33

External Debt and Default

• External debt (foreign debt) is debt held by foreigners

• External debt must be paid off with future current account surpluses (excluding the possibility of default)

• External debt to GDP is a key indicator of sustainability of external debt

• External debt to GDP rises – if growth rate of GDP falls – if the cost of external borrowing rises

34

Sovereign Credit Default Swap (CDS) Spreads

The buyer of a CDS receives a payment if the credit instrument goes into default

35

36

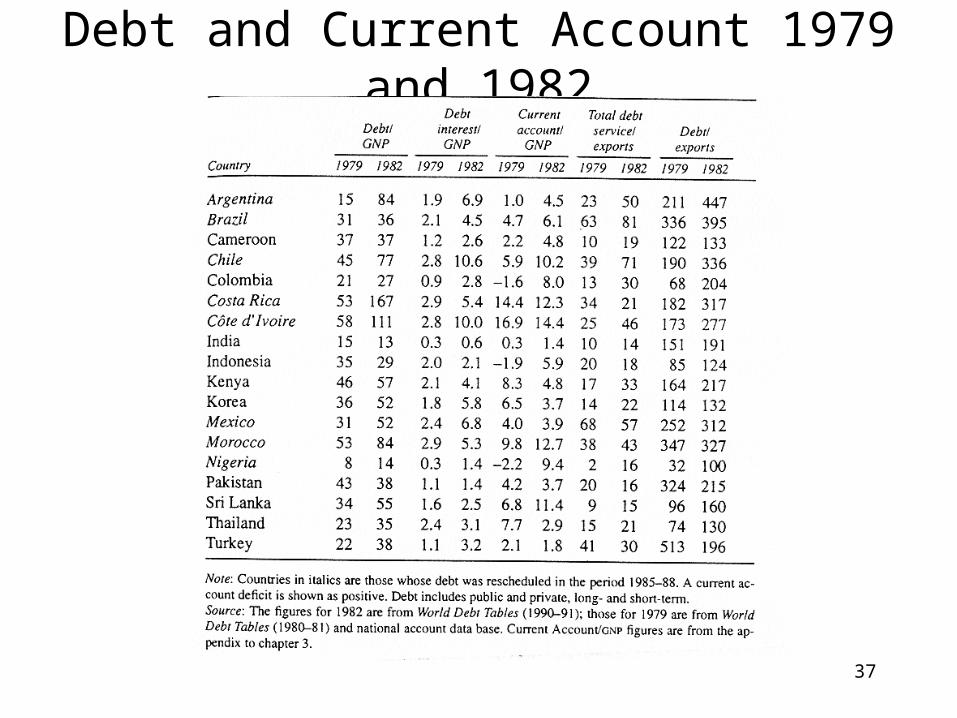

The Lesser-Developed Country (LDC) Debt Crises

• Prior to 1979, a run-up in commodity prices such as coffee and oil led to an investment boom in many Latin American countries

• Consequently, many Latin American borrowed heavily and raised the External Debt to GDP ratios

• Global recession in 1979-82 lowered demand for exports

• Interest rates on dollar denominated adjustable rate debt rose

• Debt to exports and debt to GDP rose dramatically

• In August 1982 Mexico declared a moratorium on interest payments. This led to the debt crises

37

Debt and Current Account 1979 and 1982

38

Current Account Reversals

Current account rises (perhaps reverses from deficit to surplus) during a crisis

39

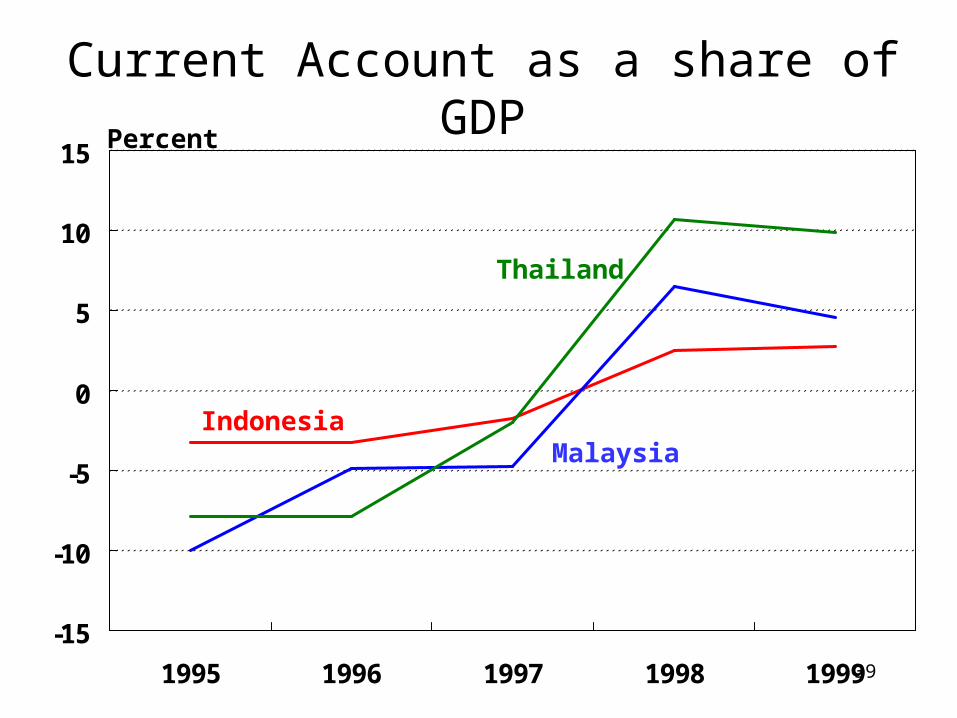

-15

-10

-5

0

5

10

15

1995 1996 1997 1998 1999

Thailand

MalaysiaIndonesia

Percent

Current Account as a share of GDP

40

The Worldwide Real Interest Rate

41

Capital Market Equilibrium for the World Economy

42

Global Capital Markets

Variables subscripted by w refer to global variables, and those subscripted by arg refer to Argentina.

43

An Increase in future TFP

Expectations of better growth prospects for the future increase investment today

Investment determined by (i) real interest rate (ii) future prospects

44

A Decline in Savings

A fall in Savings can raise the interest rate and lower investment