Embed Size (px)

Citation preview

8/18/2019 1 Effect of Governance on Credit Decitions

http://slidepdf.com/reader/full/1-effect-of-governance-on-credit-decitions 1/21

The Effect of Governance on Credit Decisionsand Perceptions of Reporting Reliability

Lori Holder-Webb

Western New England College

Divesh S. Sharma

Florida International University

ABSTRACT: We conduct an experiment to examine how lending decisions are affected

by lender perceptions of reporting and governance quality. We perform a set of experi-

ments to determine whether lenders are sensitive to the quality of governance as mea-

sured by board composition along multiple dimensions, whether their perceptions of

reporting reliability are a function of the strength of the board, and whether their lending

decisions are then affected by their perceptions of reporting reliability. Study partici-

pants are a group of 62 professional lenders from Singapore, with at least three years

of professional credit analysis and lending experience. We find that lenders are prima-

rily sensitive to financial condition and the perceived reliability of financial reporting.

While we also find that lenders are sensitive to board strength, further tests suggest

lenders appear particularly sensitive to board strength only for relatively high-

performing firms. We also find that the perceived reliability of the financial reports does

not appear to be affected by board strength or by the applicant’s financial condition. The

paper discusses implications for policy making, practice, and research.

Keywords: corporate governance; board independence; agency theory; resource de-pendence theory.

INTRODUCTION

The spate of accounting scandals of the early 2000s began with financial reporting failures

and ended with bankruptcies Catanach and Rhoades 2003; Cutler 2004. The attention of

regulators and the investing public was drawn to the guardians that had been entrusted with

preserving the integrity of the capital markets and ensuring the reliability of reported

information—primarily the institutions of transparency in disclosure, and corporate governance

mechanisms Cutler 2004. Sweeping regulation—the Sarbanes-Oxley Act of 2002 SOX—

dramatically emphasized both disclosure and governance. Among the most significant assumptions

of the Act is that independence with respect to the board of directors should be a primary focus

when establishing and revising governance structures, and that the board of directors, specifically,

We thank Lay Huay Yeap for her research assistance, and the bankers for their participation in this study. We also thank Jeff

Cohen for his comments.

BEHAVIORAL RESEARCH IN ACCOUNTING American Accounting AssociationVol. 22, No. 1 DOI: 10.2308/bria.2010.22.1.12010 pp. 1–20

Published Online: January 2010

1

8/18/2019 1 Effect of Governance on Credit Decitions

http://slidepdf.com/reader/full/1-effect-of-governance-on-credit-decitions 2/21

is charged with maintaining the integrity of the financial reporting process Cutler 2004. The

SOX-led reforms in the U.S. transcended cross-national boundaries and affected regulatory re-

forms across the globe as regulators worldwide attempted to regain and enhance investors’ con-

fidence in their capital markets.1

Significant developments in information technology combined with a societal objective of wealth accumulation fueled the exponential growth in cross-national capital flows Rezaee 2007.

Leading corporations traditionally domiciled in the U.S. and U.K. shifted their operations—and in

some cases, headquarters—to Asia, with many companies cross-listing on foreign exchanges

Monks and Minow 2008. Despite the prevalence and intensity of these cross-national economic

exchanges, there is no accepted global corporate governance regulation.

By the late 1990s, the lack of adequate governance regulation manifested in the Asian finan-

cial crisis, deterioration in the financial markets, numerous high-profile corporate failures, and

several scandals perpetrated by management Monks and Minow 2008. The World Bank, Inter-

national Monetary Fund IMF, and Organization for Economic Cooperation and Development

OECD pressured Asian nations to significantly reform their corporate disclosure regulations

toward greater transparency and introduce corporate governance regulations to better protect pro-

viders of capital Sharma et al. 2008.2

In an effort to maintain its position as the financial hub of

Asia, Singapore responded by introducing corporate governance reforms e.g., Code of Corporate

Governance 2001 and required the Singapore Stock Exchange to amend listing rules relating to

disclosure practices and corporate governance.3

One of the most important governance reforms in Singapore requires listed companies to

strengthen the independence and skill set of their boards of directors. The Singapore Code of

Corporate Governance 2001 hereafter, Singapore Code 2001 emphasizes that a board’s role is

not limited to providing oversight of management but also to manage risk and create value for

stakeholders. The implication of this emphasis is clear: it is assumed that governance, including

board composition, affects both reporting reliability and the risk of fraud, opportunistic behavior,

and corporate performance. However, while the Singapore governance reforms generally mimic

the U.S. SOX-driven governance regulations, they are guidelines and not legally binding, which

provides listed companies in Singapore considerable discretion in the formation, composition, and

disclosure of their governance practices.While the primary focus of the public attention and subsequent regulation revolved around

equity holders, the damage sustained by creditors in the financial reporting failures was significant

Lambert 2002; Schiesel and Romero 2002. The prominent role of the World Bank and IMF

pushing for corporate governance reforms illustrates the importance of losses suffered by lenders.

For example, the World Bank’s financial assistance to Asian nations and corporations was contin-

gent on progress toward more stringent and transparent corporate governance and financial report-

ing practices Monks and Minow 2008.

1 For example, Australia, U.K., and countries in Asia such as Malaysia and Singapore reformed their corporate gover-nance standards in a manner consistent with the provisions of SOX Rezaee 2007; Monks and Minow 2008; Sharma etal. 2008.

2 Singapore faced particular pressure to reform its corporate regulations because of the scandal-led collapse of Barings

Bank in 1995. Nick Leeson, a rogue trader in the Singapore office of Barings Bank, made unapproved risky investmentsand covered up losses that eventually led to the collapse of one of the largest financial institutions in the world.

3Most financial institutions operating in Singapore have global operations and elect to domicile themselves in Singaporeinstead of other Asian nations due to Singapore’s rigorous institutional framework and lending practices. Many U.S.financial institutions, including American Express, CitiBank, Bank of America, JPMorgan Chase, The Northern TrustCompany, and State Street Bank and Trust Company, as well as numerous major U.S. industrial corporations, alsoconduct major Asia-Pacific operations through Singapore offices Koh 2005. The 2004 Free Trade Agreement betweenthe U.S. and Singapore bolsters the presence and operations of U.S. financial institutions, industrial companies, andrecognition of U.S. qualifications in Singapore.

2 Holder-Webb and Sharma

Behavioral Research In Accounting Volume 22, Number 1, 2010American Accounting Association

8/18/2019 1 Effect of Governance on Credit Decitions

http://slidepdf.com/reader/full/1-effect-of-governance-on-credit-decitions 3/21

However, it is not clear from the extant literature if and how the improvements in corporate

governance will affect lending judgments. The nonbinding nature of the Singapore governance

regulation provides an attractive laboratory to explore lender incorporation of governance factors

in that Singapore lenders are customarily exposed to a broader range of governance quality than

U.S. lenders, who are now accustomed to evaluating firms in compliance with SOX. While it isunderstood that creditors make use of a wide array of information when making lending decisions,

the degree to which they consider governance has not been systematically examined Anderson et

al. 2004; Standard & Poor’s 2006.

Our paper contributes to this literature by examining how credit decisions are affected by

lender perceptions of reporting and governance quality. We perform a set of experiments to

determine whether lenders are sensitive to the quality of governance as measured by board com-

position along multiple dimensions, whether their perceptions of reporting reliability are a func-

tion of the strength of the board, and whether their lending decisions are then affected by their

perceptions of reporting reliability.4

Study participants are a group of 62 professional lenders from

Singapore, with at least three years of professional credit analysis and lending experience. We find

with these study participants that lenders are primarily concerned with the financial performance

of the firm and their perceptions of the reliability of corporate reporting. In general, corporate

governance as proxied by the strength of the board of directors influences lending decisions only

for high-performing firms.

In the following section, we address the topics of board strength, reporting reliability, finan-

cial condition, and the literature pertaining to these items with respect to credit decisions. We then

outline our experimental design, discuss the results, and conclude with a discussion of the limi-

tations of the study and directions for further research.

LITERATURE REVIEW AND HYPOTHESIS DEVELOPMENT

Governance Strength

Academic research demonstrates linkages between board strength and firm performance

Boyd 1990; Dalton et al. 1998; Hillman and Dalziel 2003; Monks and Minow 1995; Pfeffer 1972;

Pfeffer and Salancik 1978. Zahra and Pearce 1989 define four perspectives on board strengthwith respect to the relationship between governance and performance. The two perspectives with

the greatest degree of empirical support are resource dependency where the board is instrumental

in garnering resources critical to the firm’s performance and the agency view where the board

serves primarily to monitor actions of the managers and protect owner interests. Resource depen-

dence posits a direct relationship between board composition and performance and indicates that

the board should be comprised of directors who provide an interface between the company and

suppliers of necessary resources Baysinger and Butler 1985; Boyd 1990; Johnson et al. 1996;

Hillman et al. 2000; Hillman and Dalziel 2003. The agency view also suggests a direct link

between performance and board composition, in that independent directors are better able to limit

opportunistic behavior on the part of managers Watts and Zimmerman 1978, 1986.

Larcker et al. 2007 provide an extensive review of the agency-based governance-

performance literature and perform numerous statistical tests that yield mixed or unstable results.

4We acknowledge the need for caution when generalizing these results to the U.S. due to potential cultural and gover-nance differences. However, the U.S. and Singapore possess very similar investor protection regulation see La Porta etal. 1998, 2006; furthermore, economic globalization suggests that cross-national capital allocation decisions are in-creasingly common, while rationality indicates that capital providers should be attuned to institutional differencesbetween the two economies. Therefore, we believe that even though we employ a sample of Pacific Rim lenders, theresults possess the potential to inform the understanding of decisions made with respect to U.S. firms.

The Effect of Governance on Credit Decisions and Perceptions 3

Behavioral Research In Accounting Volume 22, Number 1, 2010American Accounting Association

8/18/2019 1 Effect of Governance on Credit Decitions

http://slidepdf.com/reader/full/1-effect-of-governance-on-credit-decitions 4/21

The resource-dependence literature yields more consistent results Boyd 1990; Coles et al. 2008;

Dalton et al. 1998; Pfeffer 1972. Nicholson and Kiel 2007 find case-specific support for per-

formance effects of both agency and/or resource dependence theories of board formation, and

conclude that no single theory explains the general pattern of behavior, as do Hillman and Dalziel

2003 and Cohen et al. 2004, 2007.

Professional and investing bodies such as the Business Roundtable BRT 2002 and the

Association for Investment Management and Research AIMR 1999 agree that independence is

important, but also argue that focusing on independence without regard to the strategic value-

creation ability of directors is myopic and may yield unintended consequences. These industry

players argue that a board’s roles go beyond a basic watchdog role to generating long-term

shareholder value which requires suitably qualified and experienced board members. They argue

that independent directors lacking relevant industry knowledge and experience are less effective

for strategic purposes. The Singapore Code 2001 explicitly states boards should comprise mem-

bers capable of exercising judgments independently of management and possessing appropriate

industry experience and qualifications to create value for stakeholders. The literature, then, does

not support a dominant perspective on what constitutes a “strong” board of directors. Therefore, in

this study, we define a “strong” board as one that is jointly strong on independence and onresource dependence.5

The linkages between governance strength and firm performance suggest linkages between

governance strength and credit assessments, to the extent that firm performance is a significant

determinant of the ability to repay debt. Standard & Poor’s 2006 explicitly identifies governance

matters as being of great relevance to credit assessments, but notes the lack of a universally

appropriate board structure. Hermalin and Weisbach 1988 and Dalton and Daily 1999 suggest

that firms that rely more heavily on debt financing require more advising. Dalton et al. 1998 and

Dalton et al. 2003 suggest a linkage between firm performance and board function that carries

implications for the firm’s ability to repay debt. Anderson et al. 2004 find a relationship between

the cost of publicly traded debt and board composition, but were unable to determine whether this

effect is due to effects on reporting reliability or through effects on firm performance. In light of

the established connection between board composition and firm performance, we posit the follow-ing research hypothesis:

H1: Governance board strength positively affects lenders’ decisions to extend credit.

Regulators consider the board of directors to be one of the “sentries” or “gatekeepers” of the

markets Cutler 2004. The SOX and the Singapore Code 2001 significantly increased the re-

sponsibilities of the board of directors in overseeing the reporting function, suggesting a link

between board strength and reliability of reporting. Empirical evidence supports this proposition

Anderson et al. 2004; Cutler 2004; Standard & Poor’s 2006.6

Klein 2002 demonstrates the

board’s role in monitoring and improving the reporting process. Carcello et al. 2007 find a link

between restatements and board structure. Dechow et al. 1996 and Abbott et al. 2000 find that

firms with demonstrably low-quality reporting practices exhibit weak governance structures, while

Beasley 1996 and Beasley et al. 2000 find linkages between weak governance and fraudulent

5 Sharma 2006 finds that investors rate investment risk as low and are willing to make larger investments when theboard is comprised of a majority of independent directors with relevant industry experience i.e., manifesting both theagency-driven independence and resource-dependence characteristics.

6 See Cohen et al. 2004 for a comprehensive review of the literature pertaining to corporate governance and reportingreliability.

4 Holder-Webb and Sharma

Behavioral Research In Accounting Volume 22, Number 1, 2010American Accounting Association

8/18/2019 1 Effect of Governance on Credit Decitions

http://slidepdf.com/reader/full/1-effect-of-governance-on-credit-decitions 5/21

financial reporting. As a consequence of the empirical work demonstrating linkages between

governance and reporting reliability, we advance the following research hypothesis:

H2: Governance board strength positively affects the perceived reliability of reported fi-

nancial information.

Additional evidence suggests a linkage between reporting reliability and credit decisions

through the need for lenders to assess borrowers’ ability to repay on an ongoing basis Danos et al.

1989; Leftwich 1983; Smith 1993; Beaulieu 1994; Standard & Poor’s 2006. Accounting numbers

provide a critical input into the initial credit analysis Standard & Poor’s 2006, while many

private lending agreements contain restrictive covenants based upon reported account balances

Dharan and Lev 1993; DeFond and Jiambalvo 1994; Sweeney 1994; Dichev and Skinner 2002.

Smith and Warner 1979 find evidence that debt pricing is sensitive to the availability of or

difficulty obtaining the information required to enforce binding constraints; Anderson et al.

2004 interpret this as indicating that if boards provide oversight to the reporting process, lending

agreements should also be sensitive to board characteristics. Anderson et al. 2004 premise their

study on the agency theory of optimal board composition and find that independent boards are

associated with a lower cost of debt, but do not directly test the implied relationship between

reporting reliability and the cost of debt. Based on the hypothesized relationships between gover-

nance and reporting reliability, and governance and the lending decision, as well as the empirical

work cited above, we advance the following hypothesis:

H3: Perceived reporting reliability positively affects the lender’s decision to extend credit.

Prior research suggests that financial condition is often an indicator of potential financial

misstatements. Kinney and McDaniel 1989, 74 note that “managements of firms in weak finan-

cial condition are more likely to window-dress in an attempt to disguise what may be temporary

difficulties.” Kreutzfeldt and Wallace 1986 show that companies experiencing financial problems

have significantly more financial statement errors. Such findings are consistent with more recent

evidence on management incentives to overstate income in order to avoid losses and meet marketexpectations e.g., Beasley 1996; Dechow et al. 1996. In order to reduce doubts about the loan

applicant’s financial information, lenders are likely to assess the source credibility of the financial

information, which in this case is the board’s ability to monitor the financial reporting process.

However, it is not clear how lenders would factor in the board’s attributes in the context of

financial condition. Lenders may be more sensitive to board attributes when a borrower is under-

performing. They may rate the financial information as less reliable when board attributes are

weaker or they may be more willing to extend credit to a marginal client with stronger board

attributes even if the firm’s financial performance is not strong. On the other hand, lenders may not

care much about board attributes if the borrower’s financial condition is strong or they may

evaluate board attributes for such borrowers to corroborate the reliability of their financial infor-

mation. In light of the lack of clear expectations about the relationship between governance

strength and financial condition on lending decisions, we propose a null hypothesis:

H4: There is no interaction between governance strength and financial condition on lending

decisions.

Our hypothesized associations are summarized in Figure 1, indicating the direction of hypoth-

esized effects and the predicted sign for each hypothesis is in parenthesis.

The Effect of Governance on Credit Decisions and Perceptions 5

Behavioral Research In Accounting Volume 22, Number 1, 2010American Accounting Association

8/18/2019 1 Effect of Governance on Credit Decitions

http://slidepdf.com/reader/full/1-effect-of-governance-on-credit-decitions 6/21

RESEARCH DESIGN

Participants

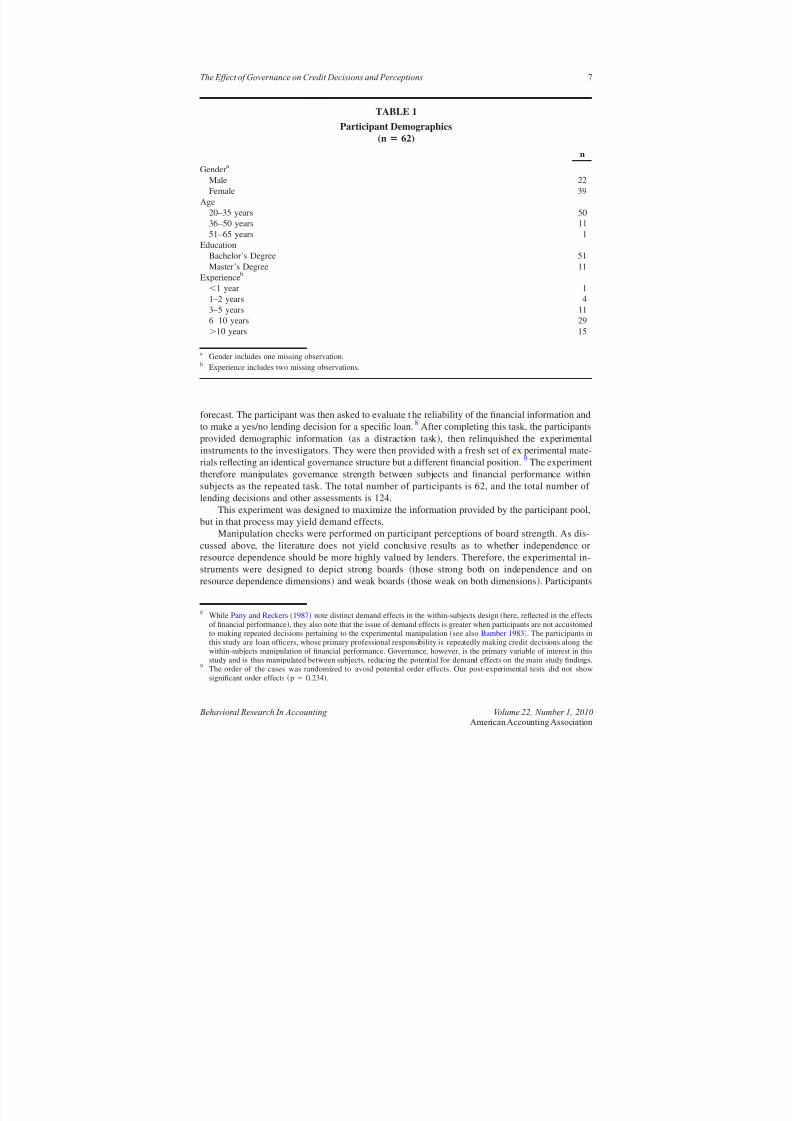

The sample of experimental participants consists of 62 experienced corporate lending man-

agers from two international commercial banks operating in Singapore.7

Discussions with the head

of corporate lending at each bank suggested that suitable participants are those with at least three

years of experience at the corporate lending level. These individuals have considerable experience

analyzing corporate borrowers and have undergone many years of formal and on-the-job training.The two banks providing sample participants from their corporate lending offices derive a signifi-

cant amount of business from U.S. multinationals operating in the Asia-Pacific region; therefore,

professional training for the participants has included significant emphasis on the U.S. business

context including governance reforms. The study was carried out in the second quarter of 2003 to

permit assimilation of the scope of U.S. and U.S.-influenced governance reforms and introduction

of Singapore Code 2001 that is modeled on the Anglo-Saxon governance regulations. All partici-

pants held university degrees. Their mean age was 38 years, with an average of more than ten

years of experience in the banking industry and eight years of experience in commercial lending.

Table 1 provides descriptive statistics about the participants.

The use of highly skilled participants imposes a limitation on the number of participants

available; therefore, this study employs a type of repeated measures design. Each participant was

presented with a single case incorporating information about the client, information about the

governance structure designed to be strong or weak , and financial data and ratios reflecting eithera high-normal or low-normal financial position. The participant was asked to evaluate the board of

directors along several dimensions independence, qualifications, financial expertise, and industry

experience, and to evaluate the firm’s financial position, profitability, and the un-audited financial

7Both banks are rated in the Business Insights Global Top 10 Retail Bank listing.

FIGURE 1

Summary of Hypothesized Associations

6 Holder-Webb and Sharma

Behavioral Research In Accounting Volume 22, Number 1, 2010American Accounting Association

8/18/2019 1 Effect of Governance on Credit Decitions

http://slidepdf.com/reader/full/1-effect-of-governance-on-credit-decitions 7/21

forecast. The participant was then asked to evaluate the reliability of the financial information and

to make a yes/no lending decision for a specific loan.8

After completing this task, the participants

provided demographic information as a distraction task , then relinquished the experimental

instruments to the investigators. They were then provided with a fresh set of experimental mate-rials reflecting an identical governance structure but a different financial position.9

The experiment

therefore manipulates governance strength between subjects and financial performance within

subjects as the repeated task. The total number of participants is 62, and the total number of

lending decisions and other assessments is 124.

This experiment was designed to maximize the information provided by the participant pool,

but in that process may yield demand effects.

Manipulation checks were performed on participant perceptions of board strength. As dis-

cussed above, the literature does not yield conclusive results as to whether independence or

resource dependence should be more highly valued by lenders. Therefore, the experimental in-

struments were designed to depict strong boards those strong both on independence and on

resource dependence dimensions and weak boards those weak on both dimensions. Participants

8 While Pany and Reckers 1987 note distinct demand effects in the within-subjects design here, reflected in the effectsof financial performance, they also note that the issue of demand effects is greater when participants are not accustomedto making repeated decisions pertaining to the experimental manipulation see also Bamber 1983. The participants inthis study are loan officers, whose primary professional responsibility is repeatedly making credit decisions along thewithin-subjects manipulation of financial performance. Governance, however, is the primary variable of interest in thisstudy and is thus manipulated between subjects, reducing the potential for demand effects on the main study findings.

9 The order of the cases was randomized to avoid potential order effects. Our post-experimental tests did not showsignificant order effects p 0.234.

TABLE 1

Participant Demographics

(n 62)

n

Gendera

Male 22

Female 39

Age

20–35 years 50

36–50 years 11

51–65 years 1

Education

Bachelor’s Degree 51

Master’s Degree 11

Experienceb

1 year 1

1–2 years 43–5 years 11

6–10 years 29

10 years 15

aGender includes one missing observation.

b Experience includes two missing observations.

The Effect of Governance on Credit Decisions and Perceptions 7

Behavioral Research In Accounting Volume 22, Number 1, 2010American Accounting Association

8/18/2019 1 Effect of Governance on Credit Decitions

http://slidepdf.com/reader/full/1-effect-of-governance-on-credit-decitions 8/21

were asked to rate their perceptions of four attributes of the board: independence, qualifications,

financial expertise, and industry expertise. Participant perceptions of these four attributes were

compared to the experimental conditions. Any participant receiving a “weak” governance case that

rated it a 7 “very strong” on any one of the four dimensions, and any participant receiving a

“strong” governance case but rating it a 1 “very weak” was considered to have failed themanipulation check. No participant misclassified the board strength in this manner. Likewise, any

participant rating the “low-normal” condition as “very strong” or rating the “high-normal” condi-

tion as “very weak” was also considered to have failed the manipulation check. No participant

misclassified the financial position of the company under this criterion. As with the governance

manipulation check, participants provided average ratings of the financial position of “low-

normal” firms that were significantly lower than ratings provided for “high-normal” firms.10

An additional manipulation check was performed to test participant sensitivity to the manipu-

lations beyond the gross error check discussed above. In this check, the mean participant percep-

tions pertaining to each of the four dimensions identified above and rated on seven-point Likert

scales were compared across experimental groups partitioned by “strong” versus “weak”

boards. For all four attributes the average rating for “strong” boards was higher than the average

rating for “weak” boards, and all differences between these means were significant at p 0.001.

Description of the Experimental Task

The fictitious case involved a listed food and beverage manufacturer seeking a loan to finance

working capital. The case was constructed with substantial corroboration from the managers of the

lending function at the two banks and pilot tested on corporate lending managers who did not

participate in the study. The nature and content of the information, including the background of the

borrower, industry and management information, summary financial statements, and financial

ratios were presented in a format normally used by the managers.11

A table defining each financial

ratio was also presented to ensure consistency.

As discussed above, the experiment consisted of four case scenarios featuring between-

subjects board strength manipulations and within-subjects financial position manipulations. Par-

ticipants were randomly assigned a strong board or weak board experimental packet.12

Each

packet contained two cases packaged separately that differed only with respect to the financialcondition of the fictitious loan applicant.

The between-subjects governance manipulation featured two scenarios, “strong” governance

and “weak” governance. The board strength attributes that were varied between the two gover-

nance classifications were independence, finance and accounting knowledge, appropriate business

qualifications, and industry experience. Board size was held constant at seven directors. In

the strong weak board case there are five two independent directors. Three out of five zero out

of two independent directors have finance and accounting knowledge, five out of five zero

out of two independent directors have relevant business qualifications, and two out of five

zero out of two independent directors have related industry experience. These attributes were

selected as a result both of the findings in the literature and regulatory reforms discussed in the

context of the hypothesis development, as well as discussions with the bank managers and their

credit training personnel at each participating bank. These discussions indicated that industry

10The average rating for the financial performance of the “low-normal” firms was 3.60, while the average rating for“high-normal” firms was 5.00; the difference in means is statistically significant at p 0.001.

11 Prior research shows that format influences human judgment Ashton and Ashton 1995. Post-experimental discussionsdid not show any concerns related to the format of the loan application documentation.

12 Results of a one-way ANOVA indicate no significant demographic differences p 0.10 between groups, suggestingthat random assignment is successful.

8 Holder-Webb and Sharma

Behavioral Research In Accounting Volume 22, Number 1, 2010American Accounting Association

8/18/2019 1 Effect of Governance on Credit Decitions

http://slidepdf.com/reader/full/1-effect-of-governance-on-credit-decitions 9/21

qualifications and experience are important considerations when lenders assess the likelihood of

the borrower succeeding in its investment strategies and servicing its debts. Consequently, the

“strong” governance scenario features a slate of directors that are predominantly independent, with

relevant industry experience and/or financial expertise. The “weak” governance scenario features

a slate of directors, many of whom are current or former officers of the company; nonemployees

offer little industry experience and/or less notable financial expertise. BOARD_STRENGTH is a

dichotomous variable assuming a value of 0 for the “weak” scenario and a value of 1 for the

“strong” scenario.

As explained earlier, we manipulated financial performance within-subjects because lenders

are accustomed to making repeated decisions based primarily on financial performance of a bor-

rower. The within-subjects financial performance manipulation included a “high-normal” scenario

and a “low-normal” scenario. In the “high-normal” scenario, the loan applicant’s three prior years

of operating performance and solvency based on audited financial statements increased steadily

and exceeded the industry average performance; unaudited forecasts indicated further improve-

ments. In the “low-normal” scenario, the audited and forecast performance and solvency of the

company are stable and just below the industry average. FINANCIAL_COND is a dichotomous

variable assuming a value of 1 for the “low-normal” scenario and a value of 0 for the “high-

normal” scenario.13

Participants were asked to rate the financial position, financial performance, and the fore-

casted financial data on a seven-point Likert scale anchored by “very weak” 1 and “very strong”

7. Our pilot tests and debriefing revealed that the loan and information contained therein are

realistic and the low-normal case created some degree of uncertainty.14

All other information e.g.,

management, auditor, industry, loan amount, collateral, purpose of the loan, etc. is held constant

for each case.

The experiment was conducted at each bank during a training session. Lenders typically

assess an applicant’s integrity, risk management processes, and financial information prior to

making a lending decision Ruth 1987. Our discussions with the corporate managers at the two

banks confirmed this sequence and suggested the tasks for rating the applicant’s financial status

and board should precede the lending judgment tasks. Based on the information provided aboutthe loan applicant, lenders were required to rate the board and financial condition of the loan

applicant. They were then asked to assess the credibility reliability of the loan applicant’s

financial information and to indicate their approval or nonapproval of the loan. RELIABLE is the

participant’s response to the request “Please rate the reliability of the financial information pro-

vided by the applicant” on a seven-point Likert scale anchored by “Not reliable at all” 1 and

“Very reliable” 7. MAKELOAN is the participant’s response to the question “Do you recommend

approval or rejection of the $5 million revolving loan application?” and is a binary variable

assuming the value of 0 if the participant would reject the loan application and 1 if the participant

would approve the loan application.

Univariate Analysis

Table 2 provides descriptive statistics pertaining to the two dependent variables MAKELOAN

and RELIABLE , partitioned by the experimental manipulations BOARD_STRENGTH and

13 This permits direct examination of the marginal effects of governance for underperforming firms.14 A t-test of the difference between lenders’ rating of financial condition for the moderate case and the midpoint 4 in the

1–7 point rating scale indicates no significant difference p 0.10.

The Effect of Governance on Credit Decisions and Perceptions 9

Behavioral Research In Accounting Volume 22, Number 1, 2010American Accounting Association

8/18/2019 1 Effect of Governance on Credit Decitions

http://slidepdf.com/reader/full/1-effect-of-governance-on-credit-decitions 10/21

TABLE 2

Descriptive Statistics of Participant Variables

Panel A: MAKELOAN by Experimental Cell [n, (%)]Board Strength

Weak

Reject Approve Reject

All Participants 46 18 35

71.9 28.1 58.3

Financial Performance

Low-Normal 29 3 26

90.6 9.4 86.7

High-Normal 17 15 9

53.1 46.9 30.0

Panel B: RELIABLE by Experimental Cell [n, (mean) {median}]

Board Strength

Weak

All Participants 64

5.281

5.000 Partitioned by Financial Performance

Low-Normal 32

5.250

5.000

High-Normal 32

5.312

5.500

B e h a v i or a

l R e s e ar c h I nA c c o u n t i n g

V o l u m e2 2 , N

u m b er 1 ,2 0 1 0

Am e r i c a nA c c o un t i n gA s s o c i a t i on

8/18/2019 1 Effect of Governance on Credit Decitions

http://slidepdf.com/reader/full/1-effect-of-governance-on-credit-decitions 11/21

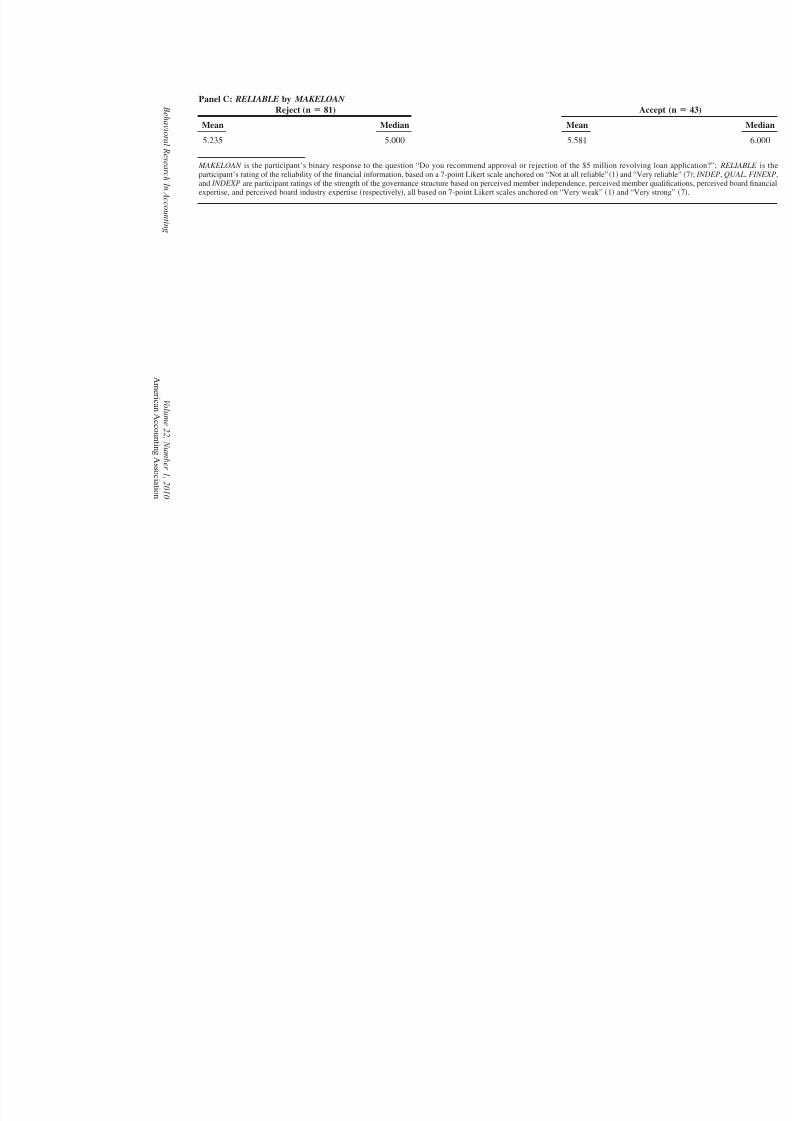

Panel C: RELIABLE by MAKELOAN

Reject (n 81) Accep

Mean Median Mean

5.235 5.000 5.581

MAKELOAN is the participant’s binary response to the question “Do you recommend approval or rejection of the $5 million revolving loaparticipant’s rating of the reliability of the financial information, based on a 7-point Likert scale anchored on “Not at all reliable” 1 and “Very reland INDEXP are participant ratings of the strength of the governance structure based on perceived member independence, perceived member quaexpertise, and perceived board industry expertise respectively, all based on 7-point Likert scales anchored on “Very weak” 1 and “Very stro

B e h a v i or a

l R e s e ar c h I nA c c o u n t i n g

V o l u m e2 2 , N

u m b er 1 ,2 0 1 0

Am e r i c a nA c c o un t i

n gA s s o c i a t i on

8/18/2019 1 Effect of Governance on Credit Decitions

http://slidepdf.com/reader/full/1-effect-of-governance-on-credit-decitions 12/21

FINANCIAL_COND.15

Panel A displays frequencies and percentages for rejecting or approving

the loan application. When all cases are pooled, it is clear that participants are more inclined to

grant loans to applicants with higher quality boards. A Chi-square test rejects the null of no

association between the lending decision and board strength at p 0.081. The second portion of

Panel A partitions the sample by financial condition. At this level, it appears that the marginaleffect of board strength is only relevant for firms that are performing above the industry norm. A

Chi-square test fails to reject the null of no association at p 0.10 for the “low-normal” group;

a Chi-square test rejects the null at p 0.056 for the “high-normal” group. The results in Panel A

provide conditional support for H1, that governance is a factor in the lending decision.

Panel B displays mean and median values of RELIABLE . Mean and median assessments of

reliability are fairly high across the board; t-tests nonparametric tests for differences in means

medians do not reveal any statistically significant differences at p 0.10 between any of the

cells in this table. The results of Panel B, therefore, do not provide univariate support for H2, that

perceived reliability is a function of governance strength.

Panel C displays mean and median values for RELIABLE partitioned by MAKELOAN . Mean

median RELIABLE values for cases where the participant indicated approval of the loan are

significantly higher than those for cases where the loan would be denied; these differences are

significant at p 0.048 difference in means and p 0.042 difference in medians. The results

in this table, therefore, provide support for H3, that the perceived reliability of financial informa-

tion is a factor in the lending decision.

Multivariate Analysis

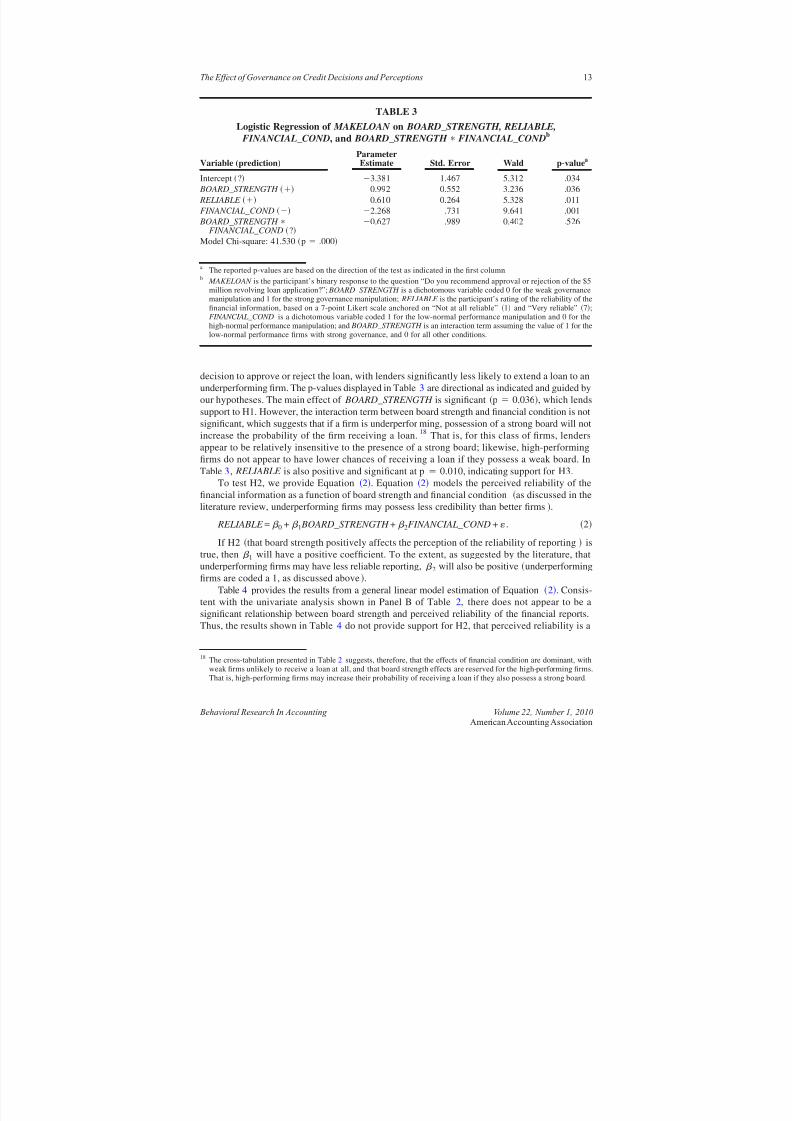

To test H1 and H3, we provide Equation 1. Equation 1 models the lending decision as a

function of the strength of the board, the perceived reliability of the financial data provided by the

applicant, and the financial condition of the applicant:16

MAKELOAN = 0 + 1 BOARD_STRENGTH + 2 RELIABLE + 3FINANCIAL_COND

+ BOARD_STRENGTH FINANCIAL_COND + . 1

If H1 that board strength positively affects the lending decision is true, 1 will have apositive coefficient. If H3 that perceived reliability positively affects the lending decision is true,

2 will also have a positive coefficient. To the extent that borrower financial condition affects

lending decisions, 3 will have a negative coefficient. If board strength makes a difference on the

margin for underperforming firms that is, if they can increase their probability of receiving a loan

through offering a strong board, then 4 will also be positive. The negative expectation on 3 is

due to the coding of financial condition, where weaker firms receive higher values; this coding is

necessary in order to draw conclusions about the value of governance for underperforming firms

in the interaction term.

Table 3 presents the results of a logistic regression estimation of Equation 1.17

As would be

expected, the financial condition of the loan applicant is a strong determinant of the lender’s

15 A Chi-square test rejects the null of no association between financial condition and the lending decision at p 0.001;as it is hardly surprising that lenders are more likely to grant loans to more financially solid clients than those that areunderperforming industry averages, this finding is not reported as a main result.

16Equation 1 was also run with a vector of demographic variables to control for participant-specific effects; however,none of these variables attained statistical significance and have consequently been omitted from the main analysis.Also, results of the model estimations do not change in significance when participants with fewer than three years of experience are removed from the analysis.

17 Results are qualitatively and quantitatively similar for simple ANOVA and logit estimations of this model. GLM resultsare presented for simplicity of assessment of the goodness-of-fit.

12 Holder-Webb and Sharma

Behavioral Research In Accounting Volume 22, Number 1, 2010American Accounting Association

8/18/2019 1 Effect of Governance on Credit Decitions

http://slidepdf.com/reader/full/1-effect-of-governance-on-credit-decitions 13/21

decision to approve or reject the loan, with lenders significantly less likely to extend a loan to an

underperforming firm. The p-values displayed in Table 3 are directional as indicated and guided by

our hypotheses. The main effect of BOARD_STRENGTH is significant p 0.036, which lends

support to H1. However, the interaction term between board strength and financial condition is not

significant, which suggests that if a firm is underperforming, possession of a strong board will not

increase the probability of the firm receiving a loan.18

That is, for this class of firms, lenders

appear to be relatively insensitive to the presence of a strong board; likewise, high-performing

firms do not appear to have lower chances of receiving a loan if they possess a weak board. In

Table 3, RELIABLE is also positive and significant at p 0.010, indicating support for H3.

To test H2, we provide Equation 2. Equation 2 models the perceived reliability of the

financial information as a function of board strength and financial condition as discussed in the

literature review, underperforming firms may possess less credibility than better firms.

RELIABLE = 0 + 1 BOARD_STRENGTH + 2FINANCIAL_COND + . 2

If H2 that board strength positively affects the perception of the reliability of reporting is

true, then 1 will have a positive coefficient. To the extent, as suggested by the literature, that

underperforming firms may have less reliable reporting, 2 will also be positive underperforming

firms are coded a 1, as discussed above.

Table 4 provides the results from a general linear model estimation of Equation 2. Consis-

tent with the univariate analysis shown in Panel B of Table 2, there does not appear to be asignificant relationship between board strength and perceived reliability of the financial reports.

Thus, the results shown in Table 4 do not provide support for H2, that perceived reliability is a

18 The cross-tabulation presented in Table 2 suggests, therefore, that the effects of financial condition are dominant, withweak firms unlikely to receive a loan at all, and that board strength effects are reserved for the high-performing firms.That is, high-performing firms may increase their probability of receiving a loan if they also possess a strong board.

TABLE 3

Logistic Regression of MAKELOAN on BOARD_STRENGTH, RELIABLE,

FINANCIAL_COND, and BOARD_STRENGTH FINANCIAL_CONDb

Variable (prediction)Parameter

Estimate Std. Error Wald p-valuea

Intercept ? 3.381 1.467 5.312 .034

BOARD_STRENGTH 0.992 0.552 3.236 .036

RELIABLE 0.610 0.264 5.328 .011

FINANCIAL_COND 2.268 .731 9.641 .001

BOARD_STRENGTH FINANCIAL_COND ?

0.627 .989 0.402 .526

Model Chi-square: 41.530 p .000

a The reported p-values are based on the direction of the test as indicated in the first column.b

MAKELOAN is the participant’s binary response to the question “Do you recommend approval or rejection of the $5million revolving loan application?”; BOARD_STRENGTH is a dichotomous variable coded 0 for the weak governancemanipulation and 1 for the strong governance manipulation; RELIABLE is the participant’s rating of the reliability of thefinancial information, based on a 7-point Likert scale anchored on “Not at all reliable” 1 and “Very reliable” 7;FINANCIAL_COND is a dichotomous variable coded 1 for the low-normal performance manipulation and 0 for thehigh-normal performance manipulation; and BOARD_STRENGTH is an interaction term assuming the value of 1 for thelow-normal performance firms with strong governance, and 0 for all other conditions.

The Effect of Governance on Credit Decisions and Perceptions 13

Behavioral Research In Accounting Volume 22, Number 1, 2010American Accounting Association

8/18/2019 1 Effect of Governance on Credit Decitions

http://slidepdf.com/reader/full/1-effect-of-governance-on-credit-decitions 14/21

function of governance. They are also somewhat inconsistent with the maintained hypothesis in

the literature that underperforming firms suffer from a credibility problem. Effects of the main

variables are not remotely significant, and the model as a whole possesses very poor explanatory

power.

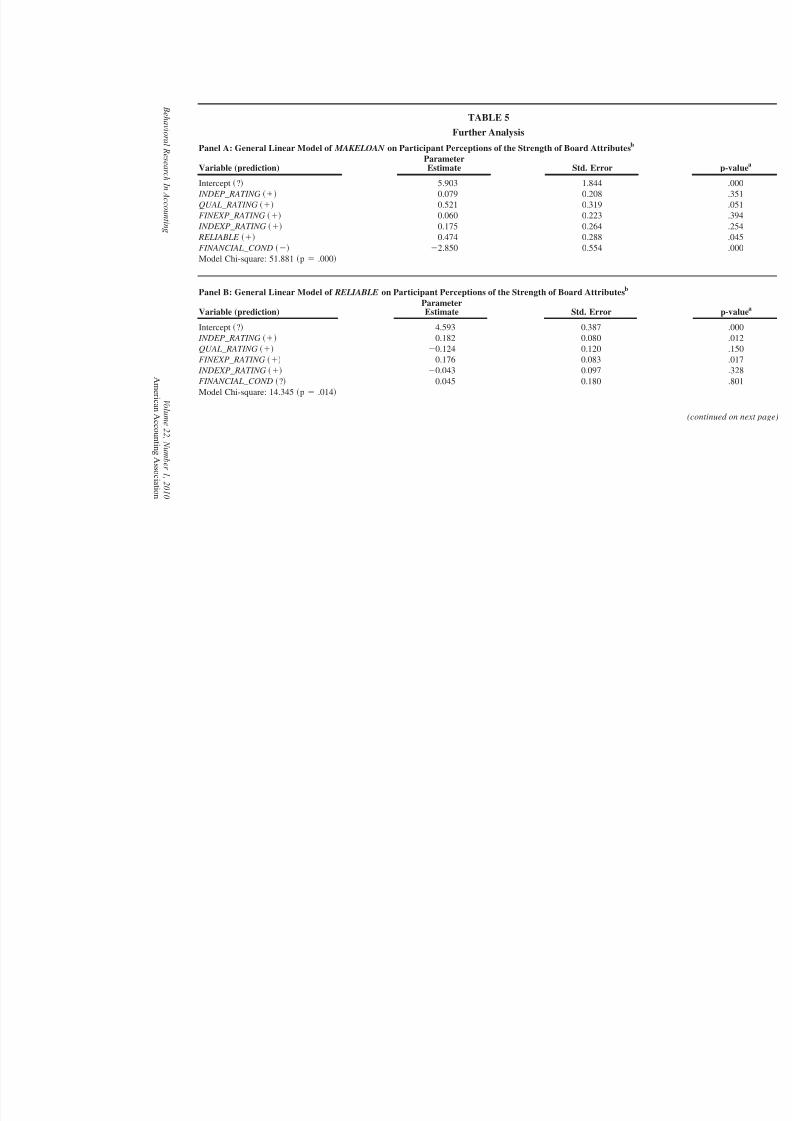

Further Analysis

The main analyses follow the experimental manipulation, which is a simple binary definition

of strong versus weak governance. Given that the results of the multivariate tests above suggest

that lenders are sensitive to governance factors, it is possible that they evaluate these factors on a

more nuanced basis than provided by the researchers. Therefore, participants were asked to ratetheir perceptions of the independence of the board members INDEP_RATING, the qualifications

of the board members QUAL_RATING, the financial expertise of the board FINEXP_RATING,

and the industry expertise INDEXP_RATING of the board on four seven-point Likert scales

anchored by “very weak” 1 and “very strong” 7. Equations 1 and 2 were re-estimated,

substituting the four attributes of perceived board strength for the binary BOARD_STRENGTH

experimental manipulation. Results are displayed in Table 5. As with the results in Tables 3 and 4,

all p-values shown are directional as indicated; the board strength, financial condition, and reli-

ability variables have directional expectations and should be evaluated with one-tailed significance

levels.

Panel A of Table 5 shows results of the estimation of the effects of the perceived governance

attributes on the lending decision. As before, RELIABLE and FINANCIAL_COND are positive and

significant. Of the four governance perceptions, the only one that is significant is the lender

perception of board qualifications p 0.051. Panel B shows results of the estimation of gover-nance perceptions on RELIABLE . While the binary manipulation of “strong” and “weak” gover-

nance is not significantly related to perceptions of reliability as shown in Table 4, there do appear

to be some significant relationships between the perception of governance strength and the per-

ception of reliability. In particular, it appears that perceived independence p 0.012 and per-

ceived financial expertise p 0.017 affects the perception of the reliability of the financial

information. This finding is consistent with the prior literature e.g., Dechow et al. 1996; Beasley

TABLE 4

OLS Regression of RELIABLE on BOARD_STRENGTH and FINANCIAL_CONDb

Variable (prediction)

Parameter

Estimate Std. Error t-statistic p-valuea

Intercept ? 5.265 .144 36.611 .000

BOARD_STRENGTH 0.152 .168 0.906 .184

FINANCIAL_COND ? 0.032 .168 0.192 .848

R2: .084

Adj. R2: .009

F 0.429, p .652

aThe reported p-values are based on the direction of the test as indicated in the first column.

b RELIABLE is the participant’s rating of the reliability of the financial information, based on a 7-point Likert scaleanchored on “Not at all reliable” 1 and “Very reliable” 7; BOARD_STRENGTH is a dichotomous variable coded 0 forthe weak governance manipulation and 1 for the strong governance manipulation; and FINANCIAL_COND is a dichoto-mous variable coded 1 for the low-normal performance manipulation and 0 for the high-normal performancemanipulation.

14 Holder-Webb and Sharma

Behavioral Research In Accounting Volume 22, Number 1, 2010American Accounting Association

8/18/2019 1 Effect of Governance on Credit Decitions

http://slidepdf.com/reader/full/1-effect-of-governance-on-credit-decitions 15/21

TABLE 5

Further Analysis

Panel A: General Linear Model of MAKELOAN on Participant Perceptions of the Strength of Board Attributes

b

Variable (prediction)Parameter

Estimate Std. Error

Intercept ? 5.903 1.844

INDEP_RATING 0.079 0.208

QUAL_RATING 0.521 0.319

FINEXP_RATING 0.060 0.223

INDEXP_RATING 0.175 0.264

RELIABLE 0.474 0.288

FINANCIAL_COND 2.850 0.554

Model Chi-square: 51.881 p .000

Panel B: General Linear Model of RELIABLE on Participant Perceptions of the Strength of Board Attributesb

Variable (prediction)Parameter

Estimate Std. Error

Intercept ? 4.593 0.387

INDEP_RATING 0.182 0.080

QUAL_RATING 0.124 0.120

FINEXP_RATING 0.176 0.083

INDEXP_RATING 0.043 0.097

FINANCIAL_COND ? 0.045 0.180

Model Chi-square: 14.345 p .014

B e h a v i or a

l R e s e ar c h I nA c c o u n t i n g

V o l u m e2 2 , N

u m b er 1 ,2 0 1 0

Am e r i c a nA c c o un t i

n gA s s o c i a t i on

8/18/2019 1 Effect of Governance on Credit Decitions

http://slidepdf.com/reader/full/1-effect-of-governance-on-credit-decitions 16/21

a The reported p-values are based on the direction of the test as indicated in the first column.b

MAKELOAN is the participant’s binary response to the question “Do you recommend approval or rejection of the $5 million revolving loan ap

participant’s rating of the independence of the board from the Management; QUAL_RATING is the participant’s rating of the qualifications of participant’s rating of the Board’s financial/accounting knowledge; and INDEXP_RATING is the participant’s rating of the Board’s industry-reitems are all based on a 7-point Likert scale anchored on “very weak” 1 and “very strong” 7. RELIABLE is the participant’s rating of the relbased on a 7-point Likert scale anchored on “not at all reliable” 1 and “very reliable” 7; and FINANCIAL_COND is a dichotomous vperformance manipulation and 0 for the high-normal performance manipulation.

B e h a v i or a

l R e s e ar c h I nA c c o u n t i n g

V o l u m e2 2 , N

u m b er 1 ,2 0 1 0

Am e r i c a nA c c o un t i n gA s s o c i a t i on

8/18/2019 1 Effect of Governance on Credit Decitions

http://slidepdf.com/reader/full/1-effect-of-governance-on-credit-decitions 17/21

1996; Klein 2002 that demonstrates an association between board oversight and financial report-

ing choices.

CONCLUSIONS AND DIRECTIONS FOR FURTHER RESEARCHThe study is motivated by the debates between regulators and the business community re-

garding the composition of the board and the growing worldwide corporate governance reforms at

the board level, and the lack of research on how information about corporate governance is

incorporated in investment decisions. In contrast to the legally enacted governance regulations in

the U.S. e.g., SOX, governance reforms elsewhere e.g., U. K., Australia, Singapore are not

mandatory or enforceable by law. Emerging research on equity investors’ consideration of gover-

nance factors provides mixed results and suggests we do not know if the recent worldwide

governance reforms will enhance users’ confidence in the financial reporting process and the

resultant financial information.

In this study, we explore the degree to which lending decisions are affected by governance

strength and financial reporting credibility. We also explore the degree to which governance

strength affects credibility and how the lending decision and credibility are affected by the finan-

cial condition of the firm. We find that lenders appear to incorporate governance factors into thelending decision, and that this effect is more pronounced for firms that are outperforming the

industry when compared to those that are underperforming the industry. One possibility for this

effect is that lenders may possess asymmetric loss functions whereby the risk of a loss is weighted

more heavily than the possibility of a gain similar to that observed by Smith and Kida 1991.

Because of the uniformly high rejection of low-performing loans 89 percent of applications from

these firms would have been denied, the governance effect is observed only in the population of

firms that are evidently considered suitable candidates for a loan. We also find, consistent with

expectations from the literature, that the perceived reliability of a financial report is a factor in the

lending decision.

While we are unable to identify a direct effect between the manipulation of board strength and

the perception of reliability—that is, there are no differences in the mean perceptions of reliability

based on this experimental condition—we do find that perceptions of some components of board

strength are relevant to the assessment of reporting reliability. In particular, the perceived inde-

pendence and perceived financial expertise of the board are significant determinants of perceived

reliability. This finding is consistent with the literature that suggests that independence and finan-

cial expertise provide a degree of oversight that may lead to better financial reporting.

This exploratory study has several policy, practice, and research implications. Our results

provide marginal support to regulators e.g., AIMR, BRT, IMF, World Bank pushing for reforms

to the boards of directors. Our results suggest that regulatory reforms to board independence and

competence enhance financial statements users’ perceptions of the integrity of the financial report-

ing process, and hence, their confidence in the resultant information. From a practice perspective,

our results provide evidence that board attributes are important at the individual level in the

private debt market. Further, the contextual sensitivity to governance factors evinced by profes-

sional lenders suggests that there may be a need for explicit training with respect to their under-

standing of the role of the board of directors. The primary implication for future governanceresearch is that board effectiveness as a construct embodies various attributes. Future research may

consider these attributes instead of employing a single proxy for board effectiveness such as the

proportion of outside or independent directors on the board.

Our study offers several directions for further research. This paper provides preliminary

evidence that lenders value different aspects of board strength; future research should evaluate

whether lenders prize independence or strategic resource dependence more highly. Second, this

The Effect of Governance on Credit Decisions and Perceptions 17

Behavioral Research In Accounting Volume 22, Number 1, 2010American Accounting Association

8/18/2019 1 Effect of Governance on Credit Decitions

http://slidepdf.com/reader/full/1-effect-of-governance-on-credit-decitions 18/21

study makes use of a participant pool of professional lenders from Singapore, and is a limitation

of the study. While these participants are familiar with the U.S. perspectives on governance due to

the need to service their major U.S. clients, it is possible that cultural factors and institutional

differences may affect the perceptions of reliability and the lending decision. We caution against

generalizing our results across cross-national boundaries because of such differences. Future re-search could consider evaluating these effects among a broader population. Third, the study makes

use of an instrument built around a single industry; while this is a common industry, if lenders

specialize in particular industries there may be specialization effects.

REFERENCES

Abbott, L., Y. Park, and S. Parker. 2000. The effects of audit committee activity and independence on

corporate fraud. Managerial Finance 26 11: 55–67.

Anderson, R. C., S. A. Mansi, and D. M. Reeb. 2004. Board characteristics, accounting report integrity, and

the cost of debt. Journal of Accounting and Economics 37: 315–342.

Ashton, R. H., and A. H. Ashton. 1995. Judgment and Decision-Making Research in Accounting and Audit-

ing. New York, NY: Cambridge University Press.

Association for Investment Management and Research AIMR. 1999. Letter from the Financial Accounting

Policy Committee to the Blue Ribbon Committee on Improving the Effectiveness of Corporate Audit

Committees. January 28, 1999. Charlottesville, VA: AIMR.

Bamber, E. M. 1983. Expert judgment in the audit team: A source reliability approach. Journal of Accounting

Research 21 2: 396–422.

Baysinger, B., and H. N. Butler. 1985. Corporate governance and the board of directors: performance effects

of changes in board composition. Journal of Law Economics and Organization 1: 101–124.

Beasley, M. S. 1996. An empirical analysis of the relation between the board of director composition and

financial reporting fraud. The Accounting Review 81 5: 443–466.

——–, J. Carcello, D. Hermanson, and P. D. Lapides. 2000. Fraudulent financial reporting: Consideration of

industry traits and corporate governance mechanisms. Accounting Horizons 14 4: 441–454.

Beaulieu, P. 1994. Commercial lenders’ use of accounting information in interaction with source credibility.

Contemporary Accounting Research 10: 557–585.

Boyd, B. 1990. Corporate linkages and organizational environment: A test of the resource dependence model.

Strategic Management Journal 11: 419–430.

Business Roundtable. 2002. Principles of Corporate Governance. Available at: http://jobfunctions.bnet.com/

abstract.aspx?docid62360.

Carcello, J., T. L. Neal, Z.-V. Palmrose, and S. Scholz. 2007. CEO involvement in selecting board members

and audit committee effectiveness. Working paper, The University of Tennessee.

Catanach, A. H., Jr., and S. C. Rhoades. 2003. Enron: A financial reporting failure? Villanova Law Review 48

4: 1057–1080.

The Code of Corporate Governance. 2001. Council on corporate Disclosure and Governance. Singapore.

Cohen, J., G. Krishnamoorthy, and A. Wright. 2004. The corporate governance mosaic and financial report-

ing quality. Journal of Accounting Literature 23: 87–152.

——–, ——–, and ——–. 2007. Form versus substance: The implications for auditing practice and research

of alternative perspectives on corporate governance. Working paper, Boston College.

Coles, J. L., N. D. Daniel, and L. Naveen. 2008. Boards: Does one size fit all? Journal of Financial

Economics 87: 329–356.

Cutler, S. M. 2004. Speech by SEC Staff: The Themes of Sarbanes-Oxley as Reflected in the Commission’s

Enforcement Program September 20. Available at: http://www.sec.gov/news/speech/

spch092004smc.htm.

Dalton, D. R., C. M. Daily, A. Ellstrand, and J. Johnson. 1998. Meta-analytic review of board composition,

leadership structure, and financial performance. Strategic Management Journal 19: 269–290.

——–, and ——–. 1999. What’s wrong with having friends on the board? Across the Board 36 March:

28–32.

18 Holder-Webb and Sharma

Behavioral Research In Accounting Volume 22, Number 1, 2010American Accounting Association

8/18/2019 1 Effect of Governance on Credit Decitions

http://slidepdf.com/reader/full/1-effect-of-governance-on-credit-decitions 19/21

——–, ——–, T. Certo, and R. Roengpitya. 2003. Meta-analyses of financial performance and equity: Fusion

or confusion? Academy of Management Journal 46: 13–26.

Danos, P., D. Holt, and E. Imhoff. 1989. The use of accounting information in bank lending decisions.

Accounting, Organizations and Society 14: 235–246.

Dechow, P. M., R. G. Sloan, and A. P. Sweeney. 1996. Causes and consequences of earnings manipulation:An analysis of firms subject to enforcement actions by the SEC. Contemporary Accounting Research

13 1: 1–36.

DeFond, M. L., and J. Jiambalvo. 1994. Debt covenant violation and manipulations of accruals. Journal of

Accounting and Economics 17: 145–176.

Dharan, B. G., and B. Lev. 1993. The valuation consequences of accounting changes: A multi-year exami-

nation. Journal of Accounting, Auditing and Finance 8: 475–495.

Dichev, I., and D. Skinner. 2002. Large sample evidence on the debt covenant hypothesis. Journal of

Accounting Research 40: 1091–1124.

Hermalin, B. E., and M. S. Weisbach. 1988. The determinants of board composition. The Rand Journal of

Economics 19: 589–606.

Hillman, A. J., A. A. Cannella, Jr., and R. L. Paetzold. 2000. The resource dependence role of corporate

directors: Strategic adaptation of board composition in response to environmental change. Journal of

Management Studies 37 2: 235–255.

——–, and T. Dalziel. 2003. Boards of directors and firm performance: Integrating agency and resource

dependence perspectives. Academy of Management Review 28 3: 383–396.

Johnson, J. L., C. M. Daily, and A. E. Ellstrand. 1996. Boards of directors: A review and research agenda.

Journal of Management 22: 409–439.

Kinney, W. R., and L. McDaniel. 1989. Characteristics of firms correcting previously reported quarterly

earnings. Journal of Accounting and Economics 11: 71–93.

Klein, A. 2002. Audit committee, board of director characteristics, and earnings management. Journal of

Accounting and Economics 33: 375–400.

Koh, T. 2005. USSFTA: The year in review. Business Times January 29: 14. Available at: http://

www.spp.nus.edu.sg/ips/docs/pub/

pa_tk_BT_USSFTA%20The%20Year%20in%20Review%20_29%20Jan%2005_pg%2014.pdf .

Kreutzfeldt, R. W., and W. Wallace. 1986. Error characteristics in audit populations: Their profile and

relationships to environmental factors. Auditing: A Journal of Practice & Theory 6: 20–43.

La Porta, R., F. Lopez-de-Silanes, A. Shleifer, and R. Vishny. 1998. Law and finance. The Journal of Political Economy 106: 1113–1155.

——–, ——–, and ——–. 2006. What works in securities laws? The Journal of Finance 61: 1–32.

Lambert, W. 2002. Enron’s creditors may get 20–25% of debt back, but total is unknown. Wall Street Journal

February 18.

Larcker, D. F., S. A. Richardson, and A. I. Tuna. 2007. Corporate governance, accounting outcomes, and

organizational performance. The Accounting Review 82 4: 963–1009.

Leftwich, R. 1983. Accounting information in private markets: Evidence from private lending agreements.

The Accounting Review 58: 23–43.

Monks, R. A. G., and N. Minow. 1995. Corporate Governance. Oxford, U.K.: Blackwell Business.

——–, and ——–. 2008. Corporate Governance. Oxford, U.K.: Wiley-Blackwell.

Nicholson, G. J., and G. C. Kiel. 2007. Can directors impact performance? A case-based test of three theories

of corporate governance. Corporate Governance: An International Review 15 4: 585–608.

Pany, K., and P. M. J. Reckers. 1987. Within- versus between-subjects experimental designs: A study of

demand effects. Auditing: A Journal of Practice & Theory 7 1: 39–53.

Pfeffer, J. 1972. Size and composition of corporate boards of directors: The organization and its environment.

Administrative Science Quarterly 17: 218–228.

——–, and G. Salancik. 1978. The External Control of Organizations: A Resource Dependence Perspective.

New York, NY: Harper & Row.

Rezaee, Z. 2007. Corporate Governance Post-Sarbanes Oxley. Hoboken, NJ: John Wiley.

Ruth, G. 1987. Commercial Lending. Washington, D.C.: American Bankers Association.

The Effect of Governance on Credit Decisions and Perceptions 19

Behavioral Research In Accounting Volume 22, Number 1, 2010American Accounting Association

8/18/2019 1 Effect of Governance on Credit Decitions

http://slidepdf.com/reader/full/1-effect-of-governance-on-credit-decitions 20/21

Sarbanes-Oxley Act. 2002. The Sarbanes-Oxley Act of 2002. Public Law 107-204 H. R. 3763. Washington,

D.C.: Government Printing Office.

Schiesel, S., and S. Romero. 2002. WorldCom creditors said to be restless. New York Times September 20.

Sharma, D. S. 2006. Effects of professional and non-professional investors’ perceptions of board effective-

ness on their judgments: An experimental study. Journal of Accounting and Public Policy 25: 91–115.——–, E. Boo, and V. Sharma. 2008. The impact of non-mandatory corporate governance on auditors’ client

acceptance, risk, and planning judgments. Accounting and Business Research 38: 105–120.

Smith, C. 1993. A perspective on accounting-based debt covenant violations. The Accounting Review 68:

289–303.

——–, and J. Warner. 1979. On financial contracting: An analysis of bond covenants. Journal of Financial

Economics 7: 117–161.

Smith, J. F., and T. Kida. 1991. Heuristics and biases: Expertise and task realism in auditing. Psychological

Bulletin 109 33: 472–489.

Standard & Poor’s. 2006. Corporate Ratings Criteria. New York, NY: Standard & Poor’s.

Sweeney, A. P. 1994. Debt-covenant violations and managers’ accounting responses. Journal of Accounting

and Economics 17: 281–308.

Watts, R., and J. Zimmerman. 1978. Toward a positive theory of the determination of accounting standards.

The Accounting Review 53: 112–134.

——–, and ——–. 1986. Positive Accounting Theory. Upper Saddle River, NJ: Prentice-Hall.

Zahra, S. A., and J. A. Pearce, II. 1989. Boards of directors and corporate financial performance: A review

and integrative model. Journal of Management 15 2: 291–334.

20 Holder-Webb and Sharma

Behavioral Research In Accounting Volume 22, Number 1, 2010American Accounting Association

8/18/2019 1 Effect of Governance on Credit Decitions

http://slidepdf.com/reader/full/1-effect-of-governance-on-credit-decitions 21/21

Reproducedwithpermissionof thecopyrightowner. Further reproductionprohibitedwithoutpermission.