Embed Size (px)

Citation preview

1

Housing Finance Subsidies: Handle with Care!

Douglas DiamondMarch, 2003

2

Overview

Brief Tour of the Top 8 Subsidies to Housing Finance Description and Examples Pros and Cons Best and Worst Cases

Details in the Paper with Marja

3

#1 Interest Rate Subsidy:Direct to Lender

Reducing the effective rate through direct subsidies to market lenders

E.g., reduce 15% rate by 1/3rd or by 5% or to 10% (from market); each is different

Life of loan or phase out? Delivery: cash payment, subsidy to funding

Rationales: Housing is too costly: general access Targeting: by income, size of loan, 1st time buyer,

age? Address the tilt effect of inflation (w/phase out)

4

#1 Interest Rate Subsidy:Direct to Lender

(Cont’d) Pros:

Simple to understand, relatively simple to implement Cons:

Pretty inefficient unless tightly targeted, because of “buying out the base”

Inequitable if not gradated by income Not useful for LIH issues: requires access to HF Requires competitive lenders Usually very bad budgeting practices If deep, it encourages excessive borrowing,

discourages early repayment

5

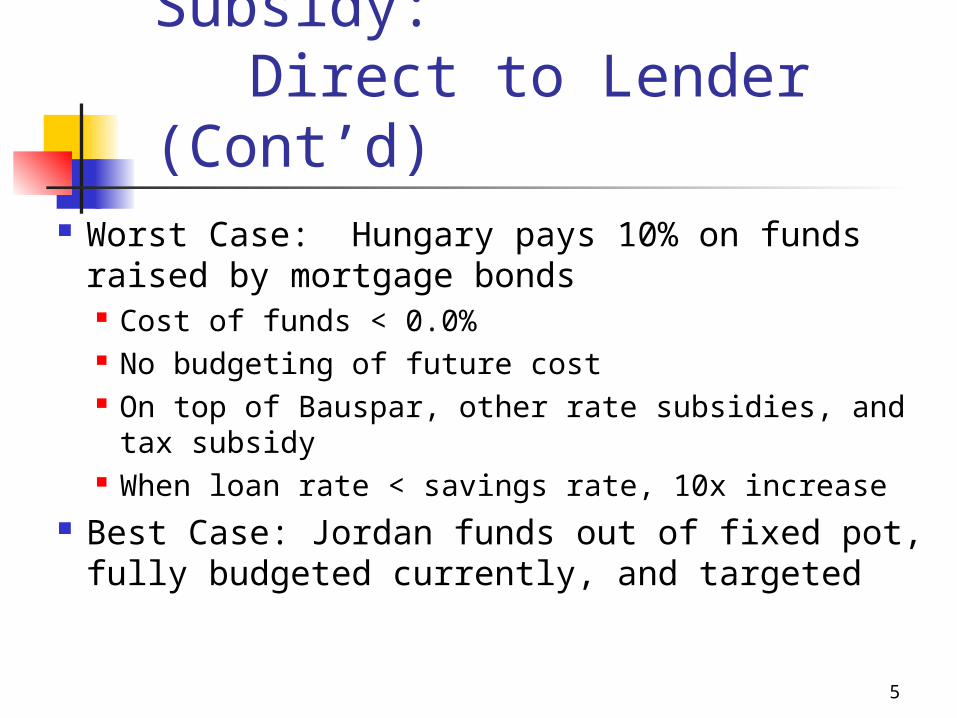

#1 Interest Rate Subsidy:Direct to Lender

(Cont’d) Worst Case: Hungary pays 10% on funds

raised by mortgage bonds Cost of funds < 0.0% No budgeting of future cost On top of Bauspar, other rate subsidies, and tax

subsidy When loan rate < savings rate, 10x increase

Best Case: Jordan funds out of fixed pot, fully budgeted currently, and targeted

6

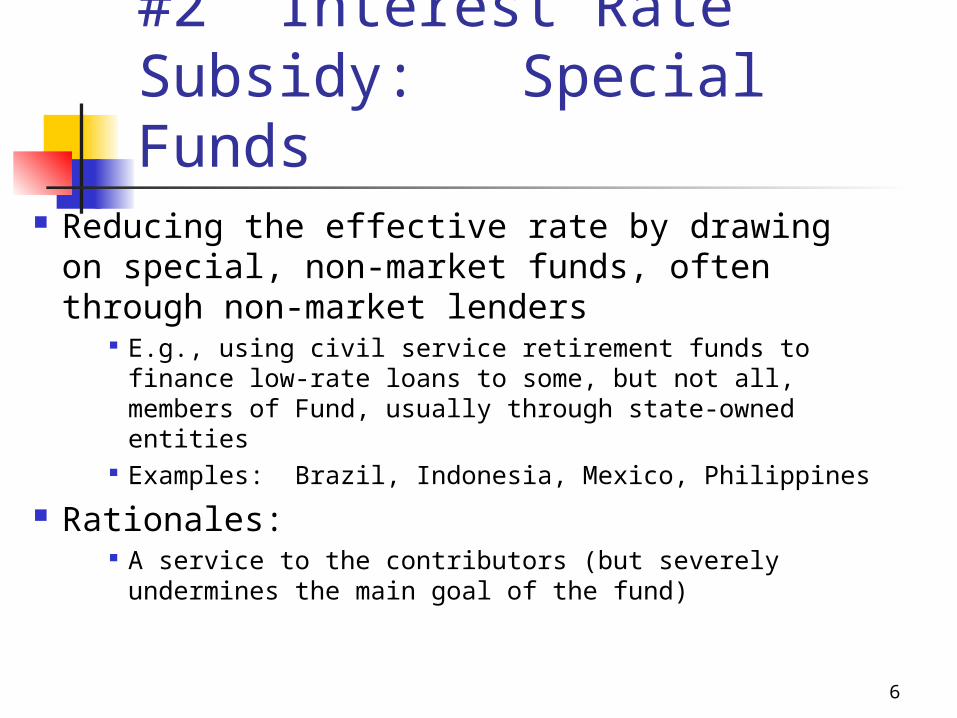

#2 Interest Rate Subsidy: Special Funds

Reducing the effective rate by drawing on special, non-market funds, often through non-market lenders

E.g., using civil service retirement funds to finance low-rate loans to some, but not all, members of Fund, usually through state-owned entities

Examples: Brazil, Indonesia, Mexico, Philippines

Rationales: A service to the contributors (but severely

undermines the main goal of the fund)

7

#2 Interest Rate Subsidy:

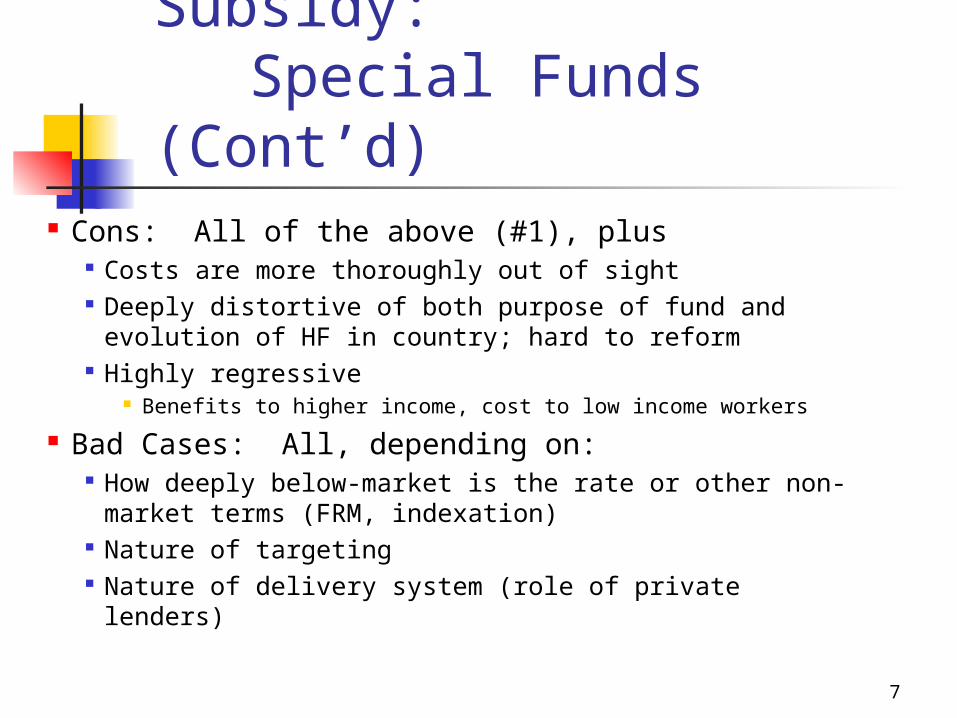

Special Funds (Cont’d)

Cons: All of the above (#1), plus Costs are more thoroughly out of sight Deeply distortive of both purpose of fund and

evolution of HF in country; hard to reform Highly regressive

Benefits to higher income, cost to low income workers

Bad Cases: All, depending on: How deeply below-market is the rate or other non-

market terms (FRM, indexation) Nature of targeting Nature of delivery system (role of private lenders)

8

#3 Interest Rate Subsidy:

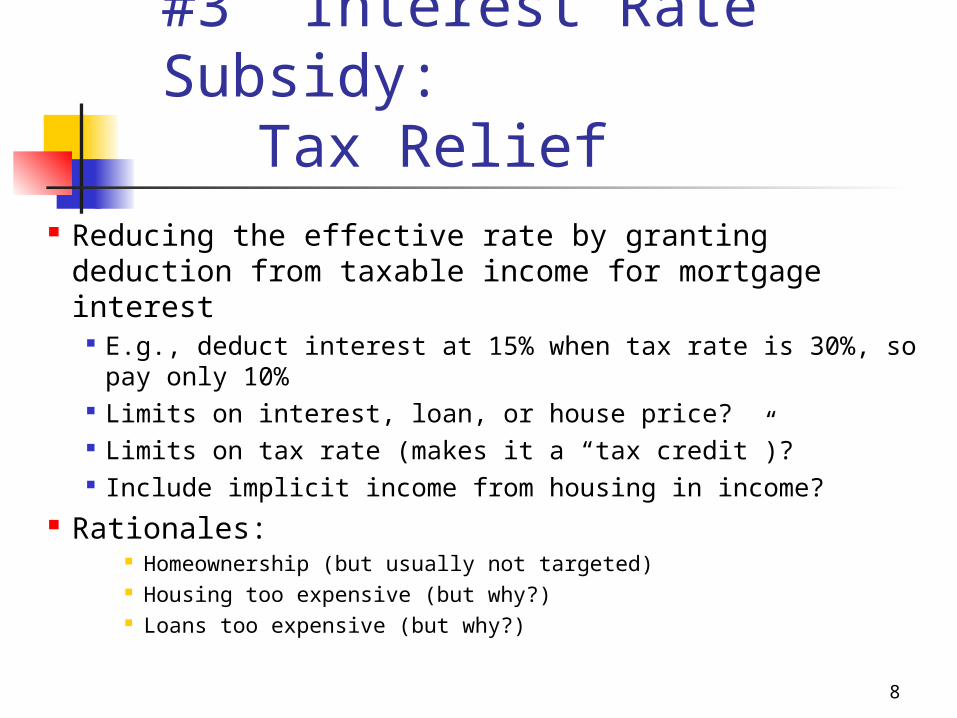

Tax Relief Reducing the effective rate by granting deduction

from taxable income for mortgage interest E.g., deduct interest at 15% when tax rate is 30%, so

pay only 10% Limits on interest, loan, or house price? Limits on tax rate (makes it a “tax credit”)? Include implicit income from housing in income?

Rationales: Homeownership (but usually not targeted) Housing too expensive (but why?) Loans too expensive (but why?)

9

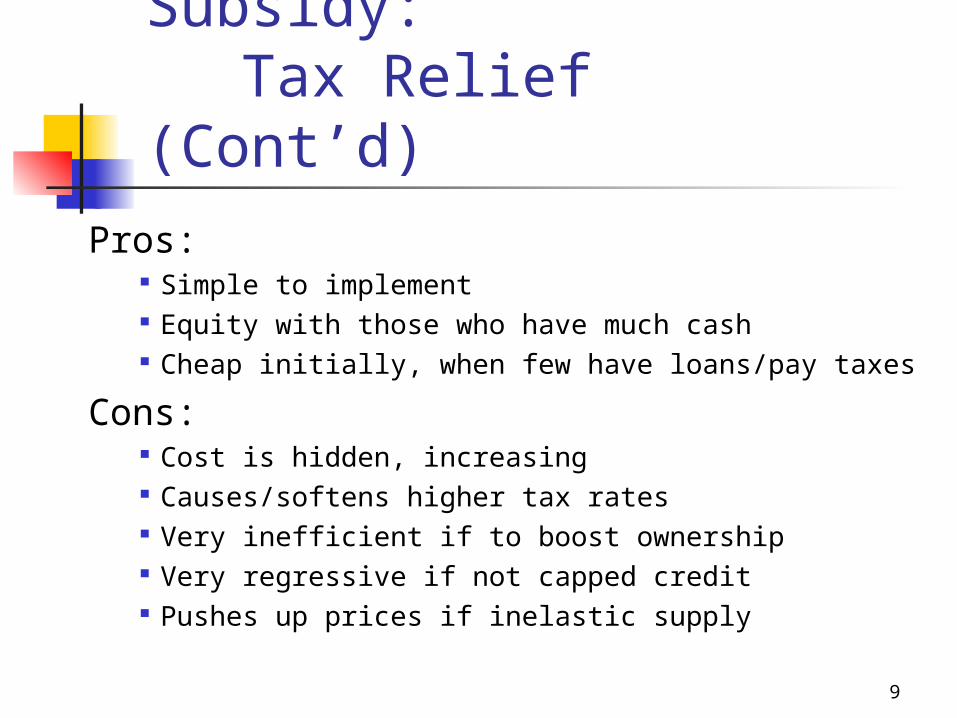

#3 Interest Rate Subsidy:

Tax Relief (Cont’d)

Pros: Simple to implement Equity with those who have much cash Cheap initially, when few have loans/pay taxes

Cons: Cost is hidden, increasing Causes/softens higher tax rates Very inefficient if to boost ownership Very regressive if not capped credit Pushes up prices if inelastic supply

10

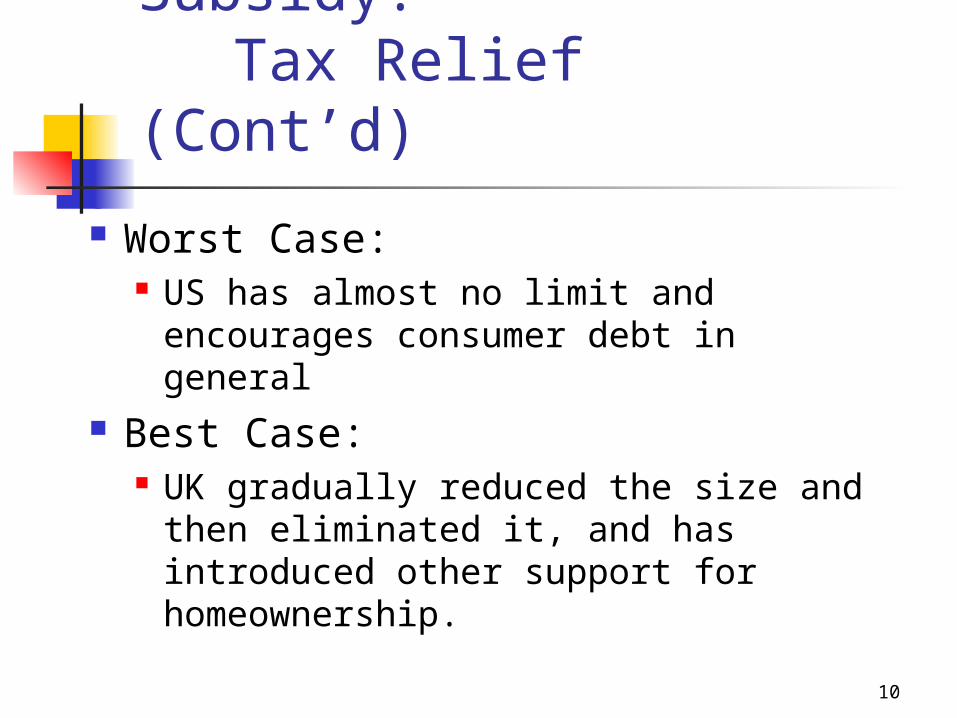

#3 Interest Rate Subsidy:

Tax Relief (Cont’d)

Worst Case: US has almost no limit and

encourages consumer debt in general Best Case:

UK gradually reduced the size and then eliminated it, and has introduced other support for homeownership.

11

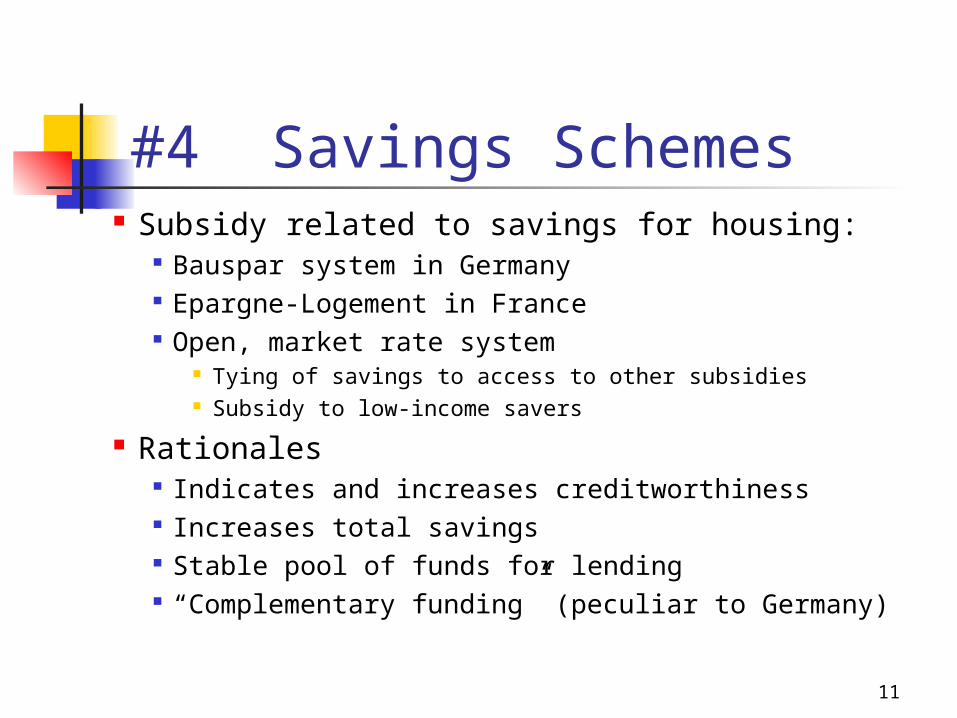

#4 Savings Schemes Subsidy related to savings for housing:

Bauspar system in Germany Epargne-Logement in France Open, market rate system

Tying of savings to access to other subsidies Subsidy to low-income savers

Rationales Indicates and increases creditworthiness Increases total savings Stable pool of funds for lending “Complementary funding” (peculiar to Germany)

12

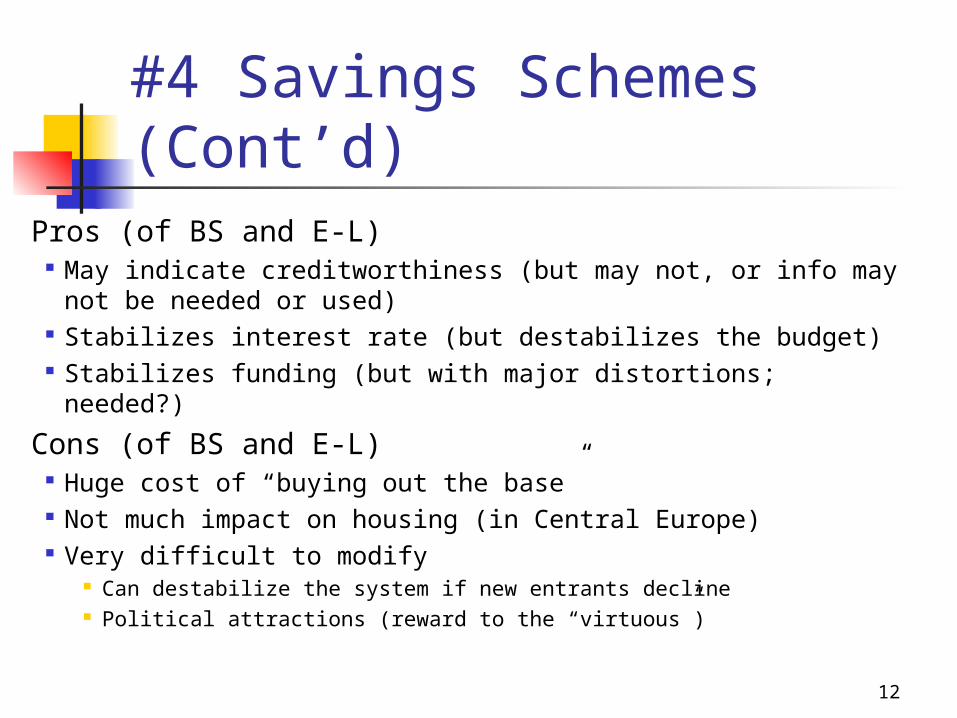

#4 Savings Schemes (Cont’d)

Pros (of BS and E-L) May indicate creditworthiness (but may not, or info may not

be needed or used) Stabilizes interest rate (but destabilizes the budget) Stabilizes funding (but with major distortions; needed?)

Cons (of BS and E-L) Huge cost of “buying out the base” Not much impact on housing (in Central Europe) Very difficult to modify

Can destabilize the system if new entrants decline Political attractions (reward to the “virtuous”)

13

#4 Savings Schemes (Cont’d)

Worst Case: The Czech Republic set up a BS system in 1993, and

has not changed the 25% premium despite a sharp decline in market rates on savings and lending (12% on BS v. 4% market). Now almost 50% of citizens have account

Best Case: Chile and South Africa tie priority access to lump-sum

subsidy to length and depth of savings Not aware of a supplement to market rate on savings

that is closely tied to income?

14

#5 Insurance: Primary Market

The state takes on some or all of the credit risk associated with individual housing loans

May or may not make an appropriate charge All or a share or the top part of risk? Optional or mandatory? Targeted?

Rationales Deal with uncertainties (small or large) about legal or

political environment for recovery Cover extra risks associated with lower-income or

high LTV lending

15

#5 Insurance: Primary Market

(Cont’d)

Pros Can diversify risk over submarkets and over lenders

within a country Can deal with some of the uncertainty about extending

credit at lower income levels or higher LTV ratios (but should only take part of risk that market cannot currently; set a sunset?)

Cons Dangers of adverse selection, moral hazard, political

pricing and management Reduction in pressure to resolve sources of risk

16

#5 Insurance: Primary Market

(Cont’d) Bad Cases:

Brazil insured against excessive accumulation of capitalized inflation and is still paying a huge bill.

Philippines was operating a system that seemed not actuarially sound.

US’ FHA has had to be recapitalized twice

Good Cases: Lithuania and South Africa have limited their capital

commitments to mortgage insurers, and operate on commercial principles. South Africa’s MI has commercially reinsured its risks.

17

#6 Insurance: Funding Market

The state takes on some or all of the financial risks associated with the operation of wholesale funding systems

Implicit or explicit? Public or public/private or private? Securitization or liquidity facility or mortgage bank

Rationales A “blanket guarantee” removes all perceived risks

involved in potentially more efficient ways of accessing capital markets, helping to achieve larger scale and greater innovation

18

#6 Insurance: Funding Market

(Cont’d)Pros

Such direct intervention can force change in the funding market

Useful for redirecting funds within a diverse country

Cons As with all guarantees, the losses are potentially

very large and there may be incentives to take advantage of the situation to some degree

Needs to be matched with statutory or regulatory limits that limit risk taking and encourage prudent management; also a sunset might be the best idea.

19

#6 Insurance: Funding Market

(Cont’d) Good Case:

A private securitization conduit such as Fannie Mae can drive a lot of good innovation, but also has incentives to take on excessive risk (e.g., act as a mortgage bank).

Better Case: Liquidity facilities such the US’ Federal Home

Loan Bank, Cagamas in Malaysia, and the JMRC in Jordan, are inherently lower risk.

20

#7 Lump Sum Grant In principle, the state provides those in the

target group a sum of money to use to buy a house in the way they see best

This is potentially the most efficient and transparent subsidy, since the size of grant is clear, the use is least constrained, and the least distortion to the market

In practice, the assistance comes with strings, such as buying a newly constructed house at a specific location, or it is tied to borrowing. It may also be difficult to implement.

21

#7 Lump Sum Grant (Cont’d)

Pros Cost is transparent and budgeted Allocation can be made transparent (forces discussion of

“equity”) and can be used to encourage savings Beneficiary evaluation tends to be closer to market costs

Cons Usually tie in to “non-market” new housing, with

debatable resale value and perhaps dubious locations May require “non-market” finance to make feasible

22

#7 Lump Sum Grant (Cont’d)

Good Cases: Chile pioneered this, but had to rely on state-

sponsored lending to make it work (see #8) South Africa did so on a massive scale, but relied on

“free” land and infrastructure and “first-come, first-served” allocation, and did not integrate finance

Pure Case: Germany offers all first time homebuyers a grant

spread over 8 years, that can help downpayment or with financing

No redistribution, but much better than other subsidies to middle-class ownership

23

#8 State Housing Banks Direct state intervention into the primary

market, through a state-controlled entity Could be partly private, or on commercial principles Market or special funding, instruments

Rationales In theory, it can pioneer the business of market-

rate lending for housing. In practice, it is usually a convenient shortcut in

developing housing finance without establishing proper conditions.

24

#8 State Housing Banks (Cont’d)

Pros Such an institution will deliver in the short-run, and,

if run on commercial principles, could possibly draw private lenders into the market

Cons Irresistible to political process to shortcut funding

and credit risk realities Also tends to prevent private entry, incur huge credit

losses, use inappropriate instruments, be a channel for corruption, and have high operating costs. Often a financial disaster.

25

#8 State Housing Banks (Cont’d)

Bad Cases Almost all, especially when tied into

special funds (see #2) Not So Bad Cases

Jordan and Thailand were able to keep theirs on commercial principles, and demonstrate potential for lending at lower middle income levels.

26

Summary Ratings? Good, bad, or ugly?

One can make such generalizations, but in fact, not black and white, so won’t do so here. E.g.,

Tax subsidies not so bad if a credit and tightly limited Lump-sum subsidies not so good if require access to

finance, and that’s not possible without hidden subsidies (e.g., state housing bank)

Key is close connection to goal, structuring to be efficient, transparent, equitable, and non-abused