Embed Size (px)

Citation preview

FINAL REPORT

Government of the Hong Kong SAR

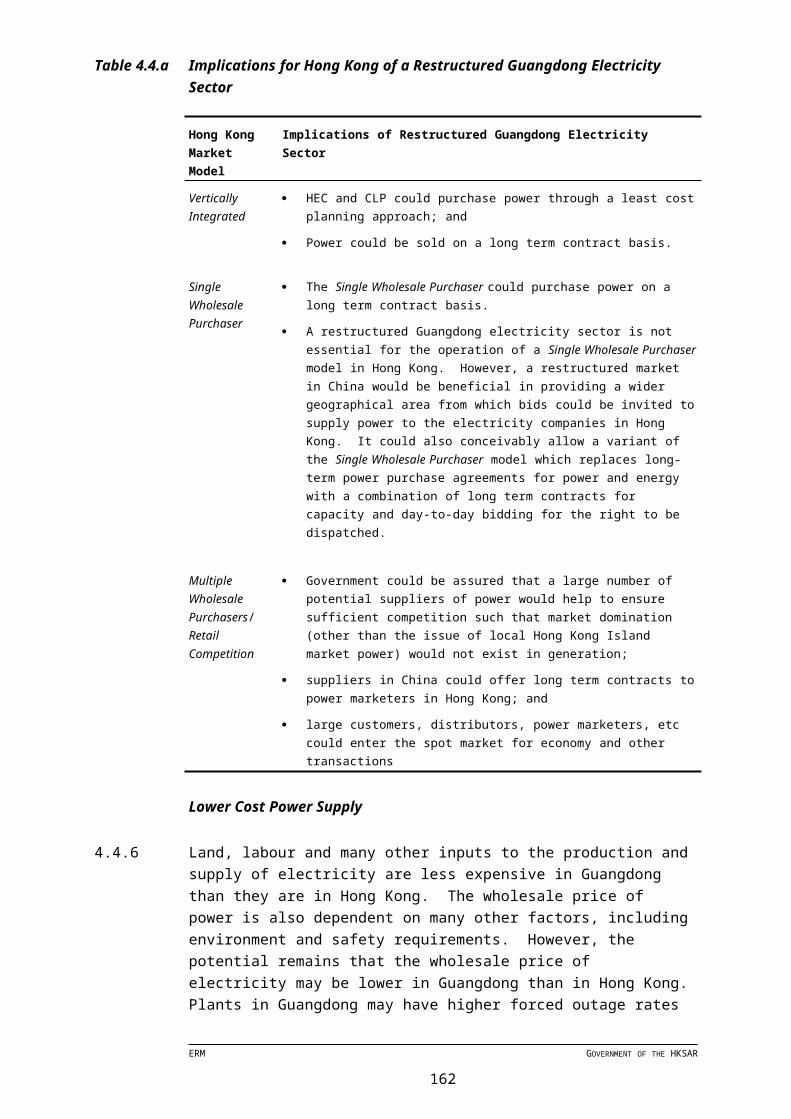

Interconnection and Competition in the Hong Kong Electricity Supply Sector

October 1999

Reference C1789

This report has been prepared by Environmental Resources Management the trading name of Environmental Resources Management Limited, with all reasonable skill, care and diligence within the terms of the Contract with the client, incorporating our General Terms and Conditions of Business and taking account of the resources devoted to it by agreement with the client.

We disclaim any responsibility to the client and others in respect of any matters outside the scope of the above.

This report is confidential to the client and we accept no responsibility of whatsoever nature to third parties to whom this report, or any part thereof, is made known. Any such party relies on the report at their own risk.

CONTENTS

EXECUTIVE SUMMARY i

1 OVERVIEW i2 INTERCONNECTION iv3 COMPETITION ix4 SOUTHERN CHINA ELECTRICITY SECTOR xi5 CONCLUSIONS AND RECOMMENDATIONS xii

FOREWORD xvGLOSSARY xviABBREVIATIONS xxi

1 INTRODUCTION AND OVERVIEW 1

1.1 BACKGROUND 11.2 STUDY OBJECTIVE 31.3 STUDY APPROACH 31.4 STRUCTURE OF THIS DOCUMENT 101.5 KEY TERMS 11

2 FEASIBILITY OF INCREASED INTERCONNECTION OF ELECTRICITY SYSTEMS IN HONG KONG 13

2.1 INTRODUCTION 132.2 GENERAL CONSIDERATIONS ASSOCIATED WITH ELECTRICITY

INTERCONNECTION 142.3 METHODOLOGY AND APPROACH 182.4 TECHNICAL FEASIBILITY OF INCREASED INTERCONNECTION 262.5 ECONOMIC FEASIBILITY OF INCREASED HEC-CLP

INTERCONNECTION 472.6 CONSUMER BILL AND TARIFF IMPACTS OF INCREASED HEC-CLP

INTERCONNECTION 552.7 KEY CONCLUSIONS ON INTERCONNECTION 62

3 FEASIBILITY OF THE INTRODUCTION OF ELECTRICITY SECTOR COMPETITION IN HONG KONG 65

3.1 INTRODUCTION 65

ERM GOVERNMENT OF THE HKSAR

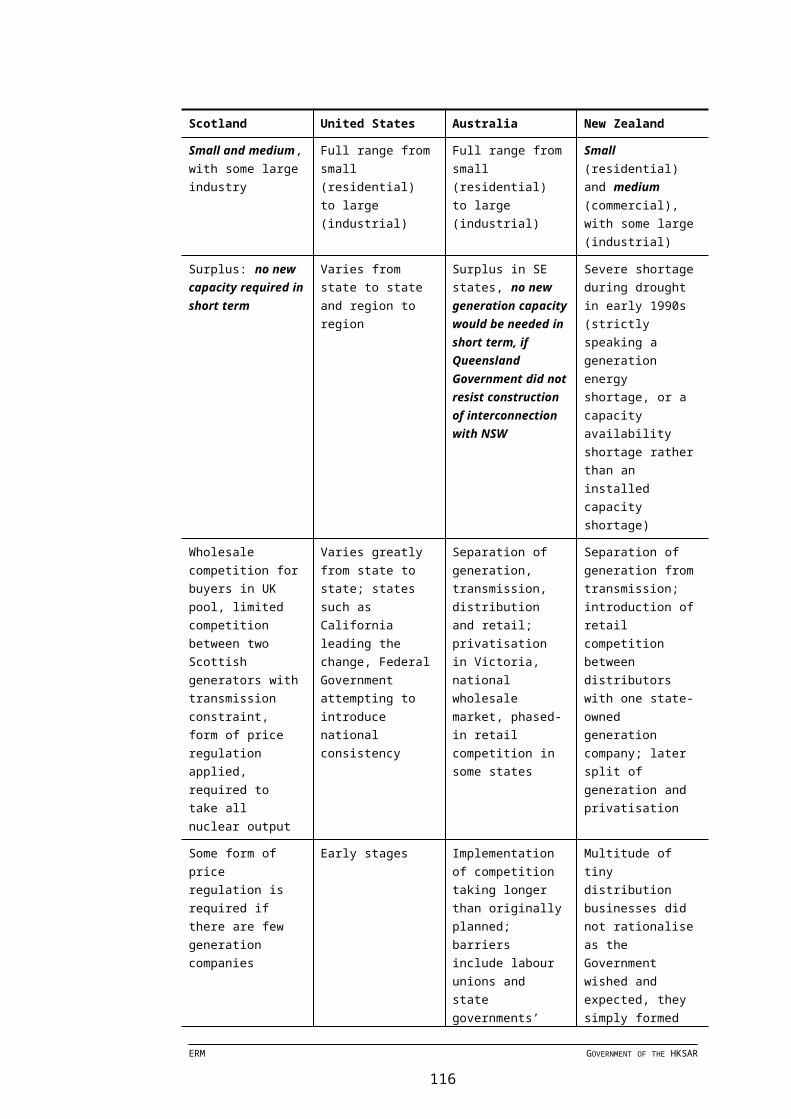

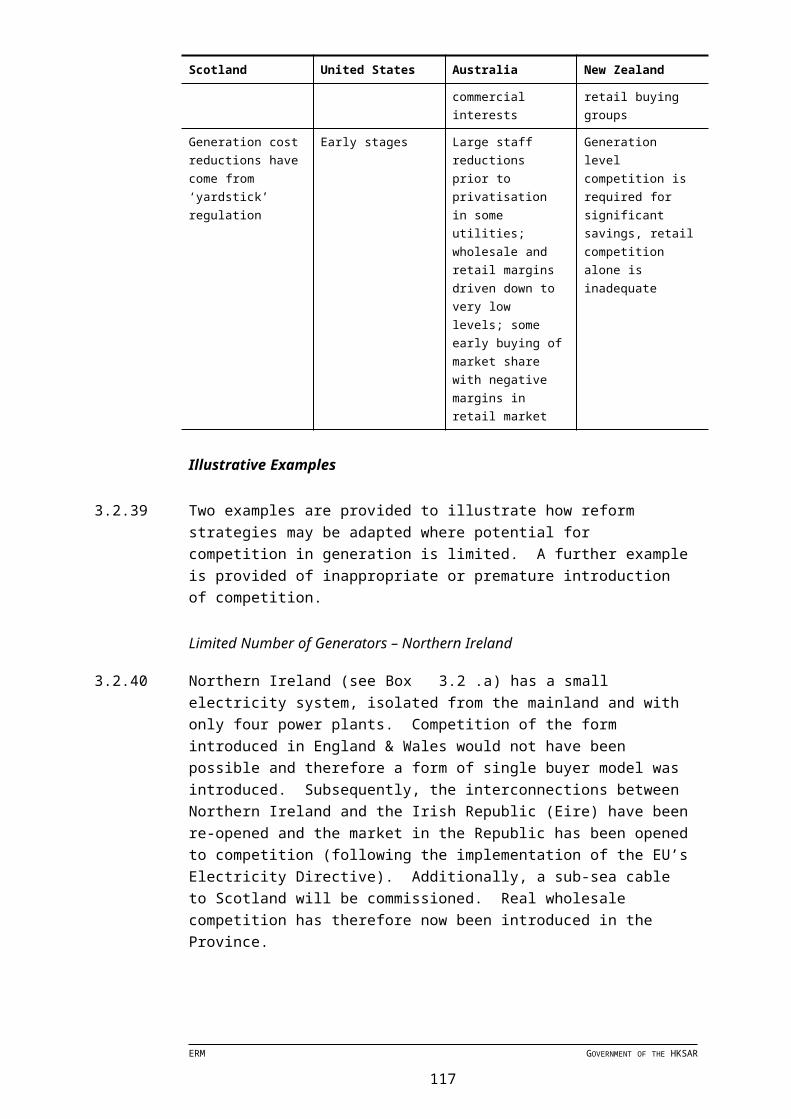

3.2 LOCAL AND WIDER CONTEXT FOR ELECTRICITY SECTOR COMPETITION 66

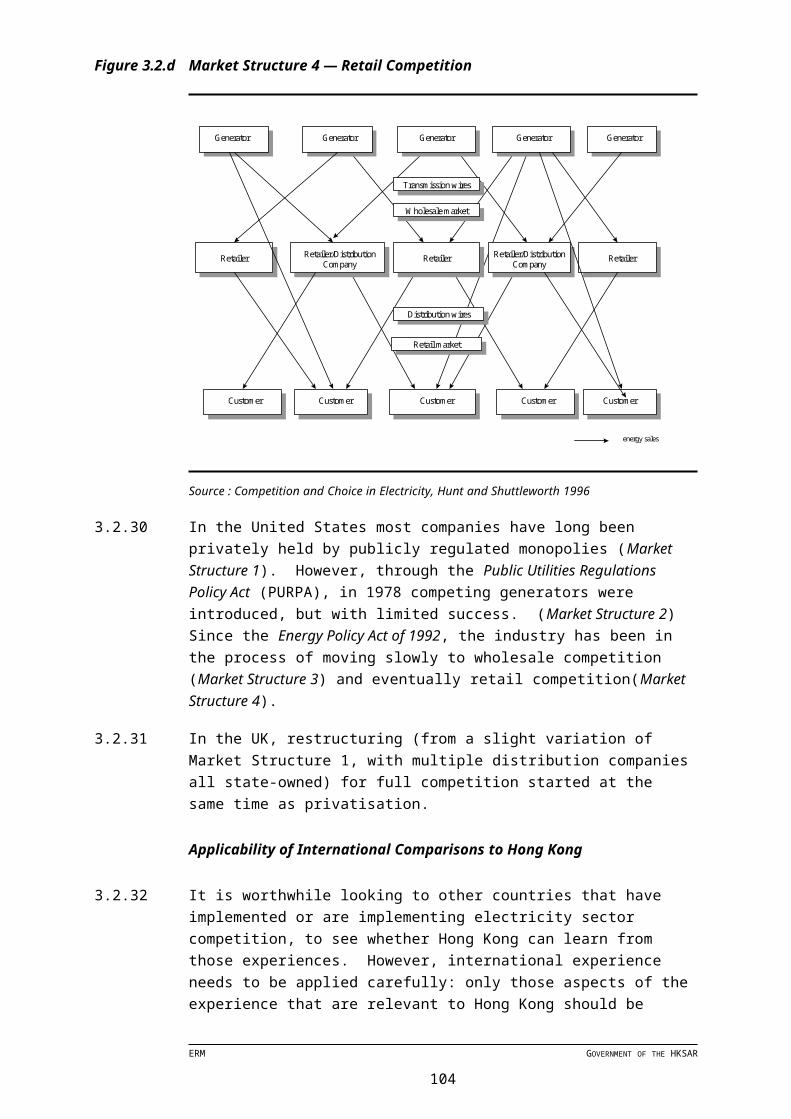

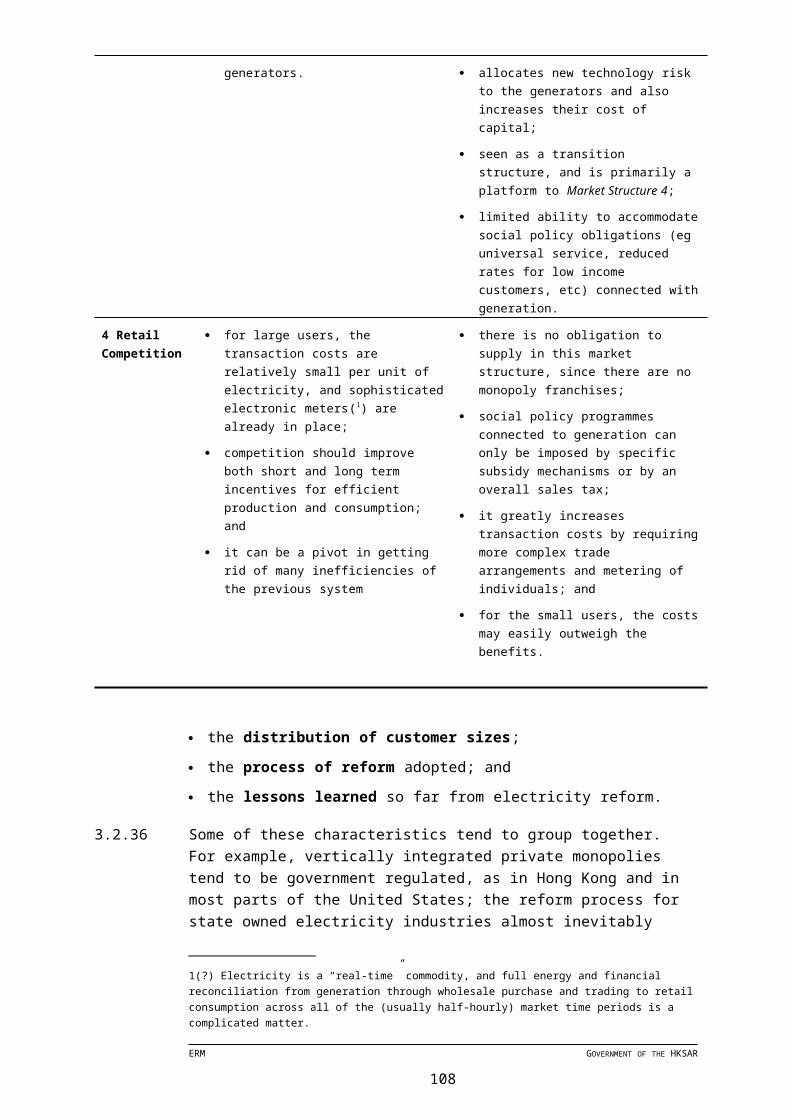

3.3 EVALUATION OF FOUR MARKET STRUCTURES APPLIED TO HONG KONG 89

3.4 DETAILED CONSIDERATION OF OPTIONS APPROPRIATE TO HONG KONG 97

3.5 KEY CONCLUSIONS ON COMPETITION 111

4 DEVELOPMENTS IN THE SOUTHERN CHINA ELECTRICITY SECTOR 113

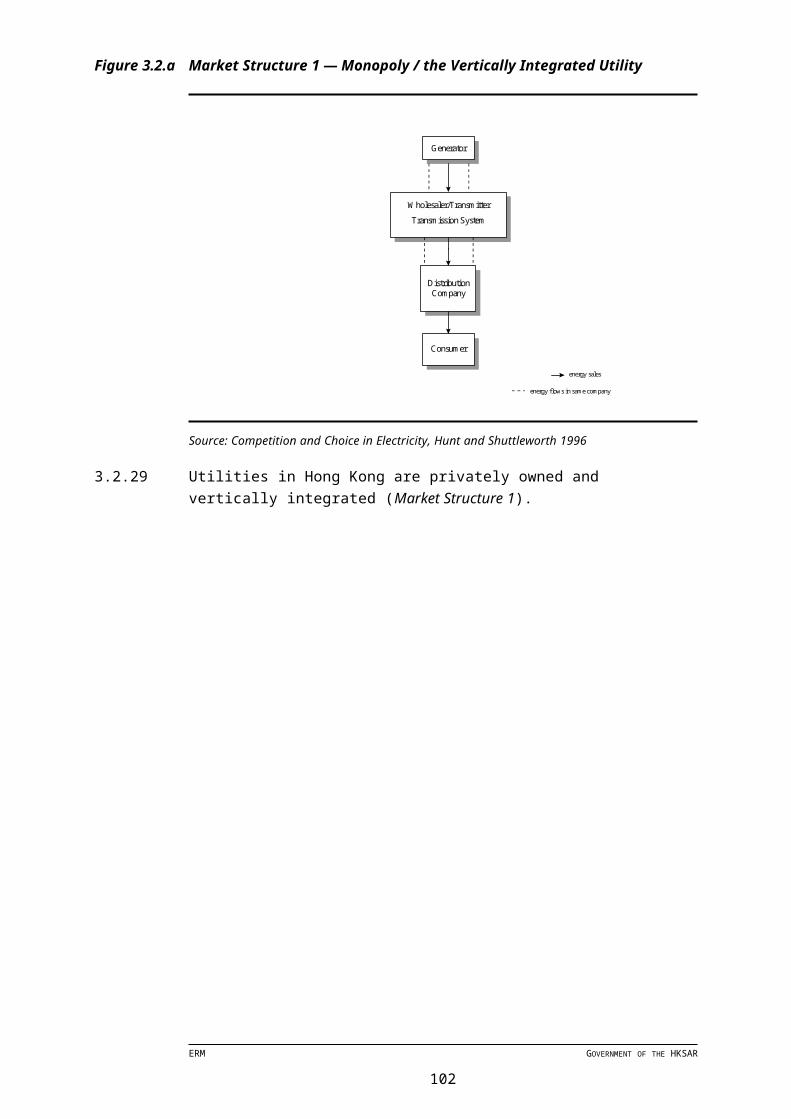

4.1 INTRODUCTION 1134.2 GUANGDONG ELECTRICITY SUPPLY INDUSTRY 1134.3 PROCESS OF RESTRUCTURING 1164.4 IMPLICATIONS FOR HONG KONG 1184.5 KEY CONCLUSIONS ON CO-ORDINATION WITH SOUTHERN CHINA 123

5 CONCLUSIONS AND RECOMMENDATIONS 125

5.1 INTRODUCTION 1255.2 CONCLUSIONS ON THE TECHNICAL FEASIBILITY OF INCREASED

INTERCONNECTION 1265.3 CONCLUSIONS ON ECONOMIC ANALYSIS OF

INTERCONNECTION/GENERATION SCENARIOS 1275.4 CONCLUSIONS ON LOGISTICAL CONSIDERATIONS ASSOCIATED

WITH IMPLEMENTING INCREASED INTERCONNECTION 1325.5 WIDER IMPLICATIONS OF THE INTERCONNECTION/GENERATION

SCENARIOS 1335.6 CONCLUSIONS ON FINANCIAL AND TARIFF ANALYSIS OF

INTERCONNECTION CASES 1355.7 CONCLUSIONS ON ANALYSIS OF FUTURE COMPETITION OPTIONS 1375.8 RECOMMENDATIONS 139

6 CASE STUDIES 143

CASE STUDY 1: PROJECTING COMPETITIVE MARKET PRICING IN THE USA145

CASE STUDY 2: INTERNATIONAL EXPERIENCE OF ELECTRICITY COMPETITION — USA, UK, BRAZIL AND THE EU 149

CASE STUDY 3: HOW MANY PLAYERS ARE NEEDED FOR A MARKET TO BE GENUINELY COMPETITIVE? 155

CASE STUDY 4: STRANDED COSTS163

ERM GOVERNMENT OF THE HKSAR

CASE STUDY 5: COMPETITION IN THE TELECOMMUNICATIONS INDUSTRY IN HONG KONG167

CASE STUDY 6: PRICE SHOCKS IN THE US WHOLESALE MARKET173

LIST OF TABLES

Table 1.3.a Accuracy of Data and Information in Each Period of the Study Time-frame 7

Table 1.5.a Key Terms Used in this Study 11Table 2.2.a Spectrum of Benefits available from Considering Firm

Capacity of Interconnection 16Table 2.2.b Spectrum of Benefits Available from Considering Firm Power

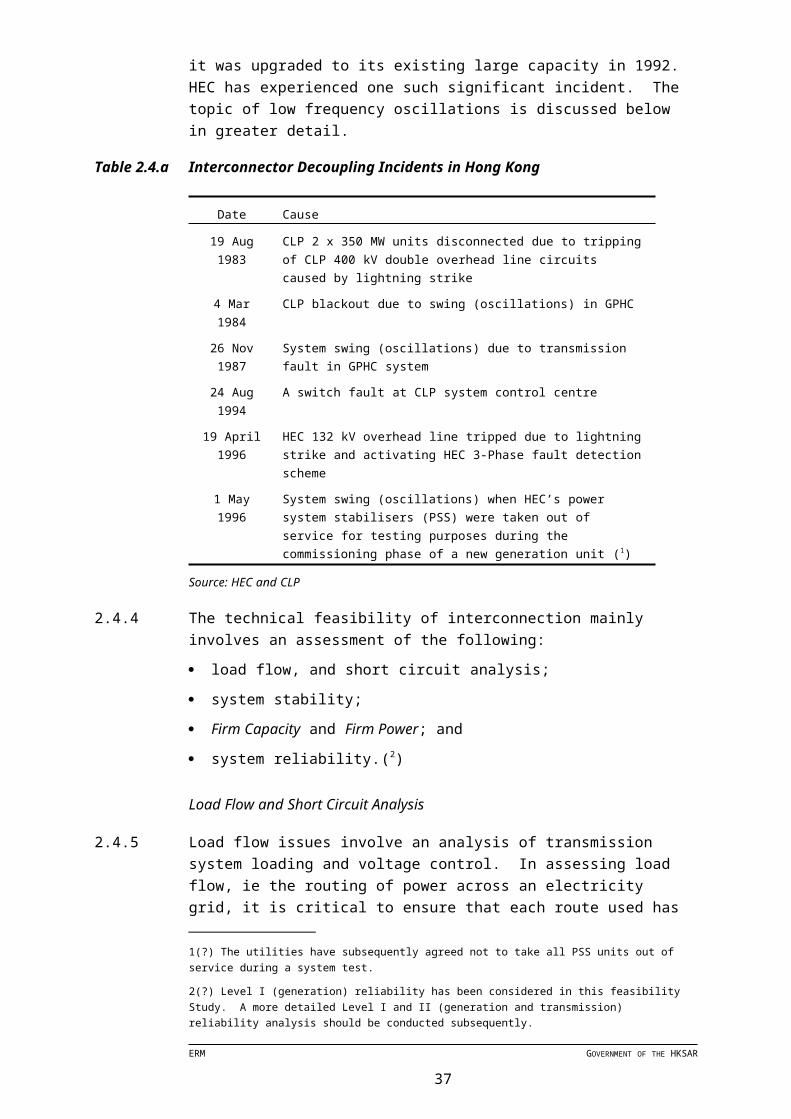

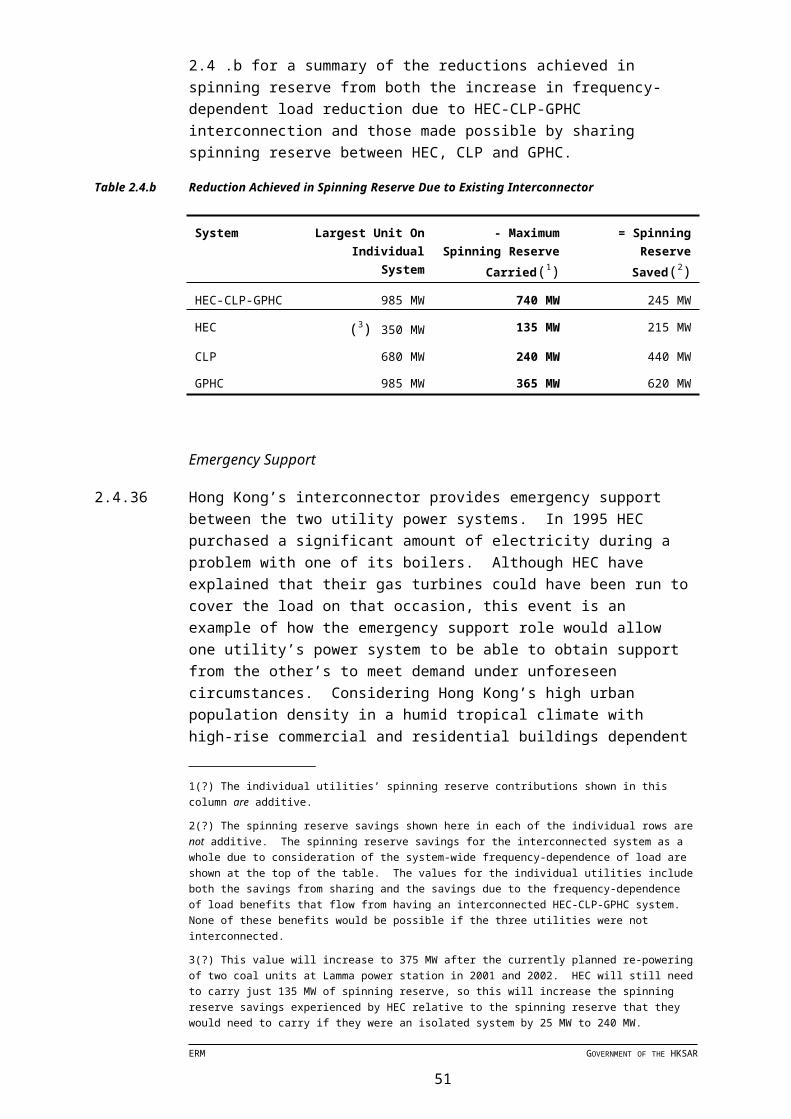

Transfer Across Interconnection 17Table 2.4.a Interconnector Decoupling Incidents in Hong Kong 27Table 2.4.b Reduction Achieved in Spinning Reserve Due to Existing

Interconnector 37Table 2.4.c Historical Fuel Cost Savings from Economy Exchanges 41Table 2.4.d Summary of Additional Benefits Potentially Available from

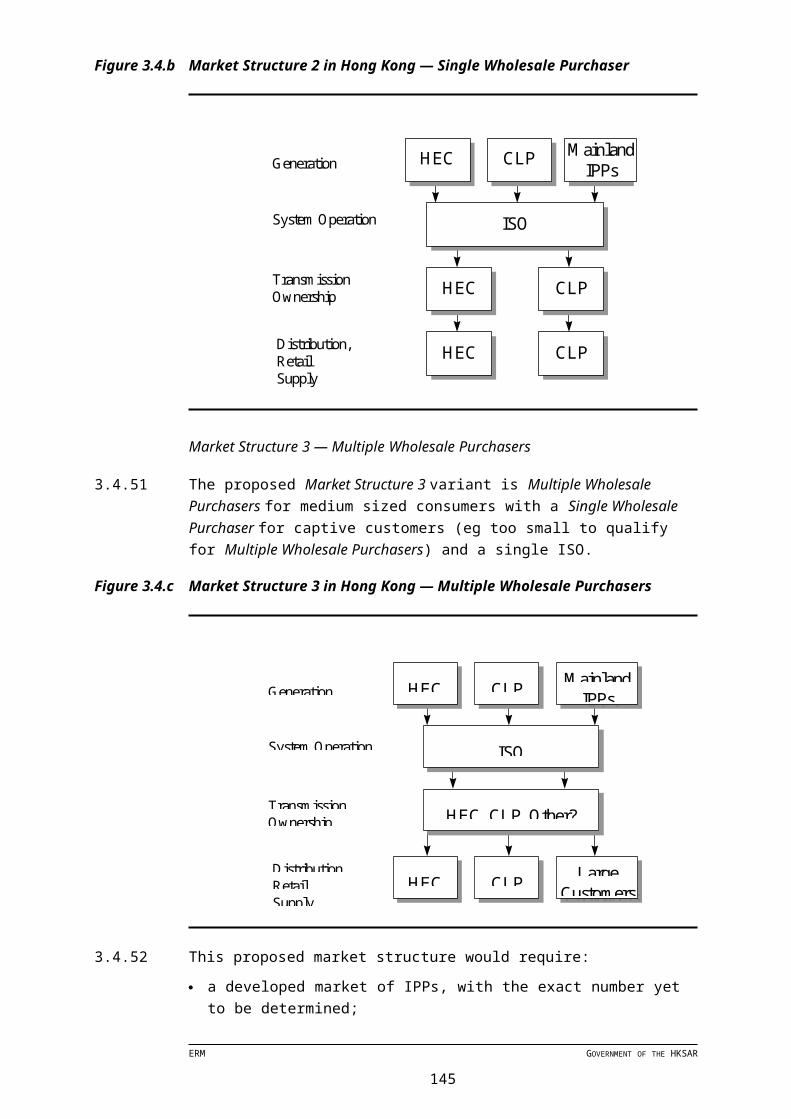

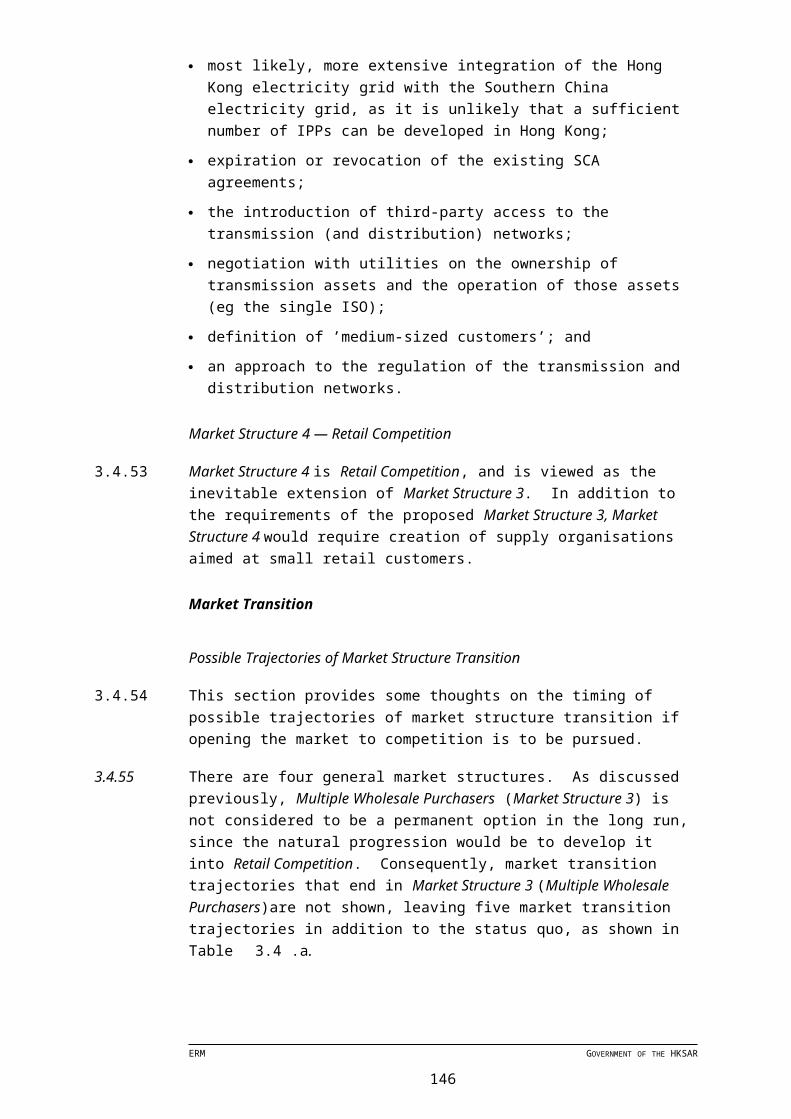

Increased Interconnection Capacity 42Table 2.5.a Discounted Present Values of Cumulative Incremental

Capital Expenditures for Interconnection and Generation Planning Scenarios Consolidated Across HEC and CLP 50

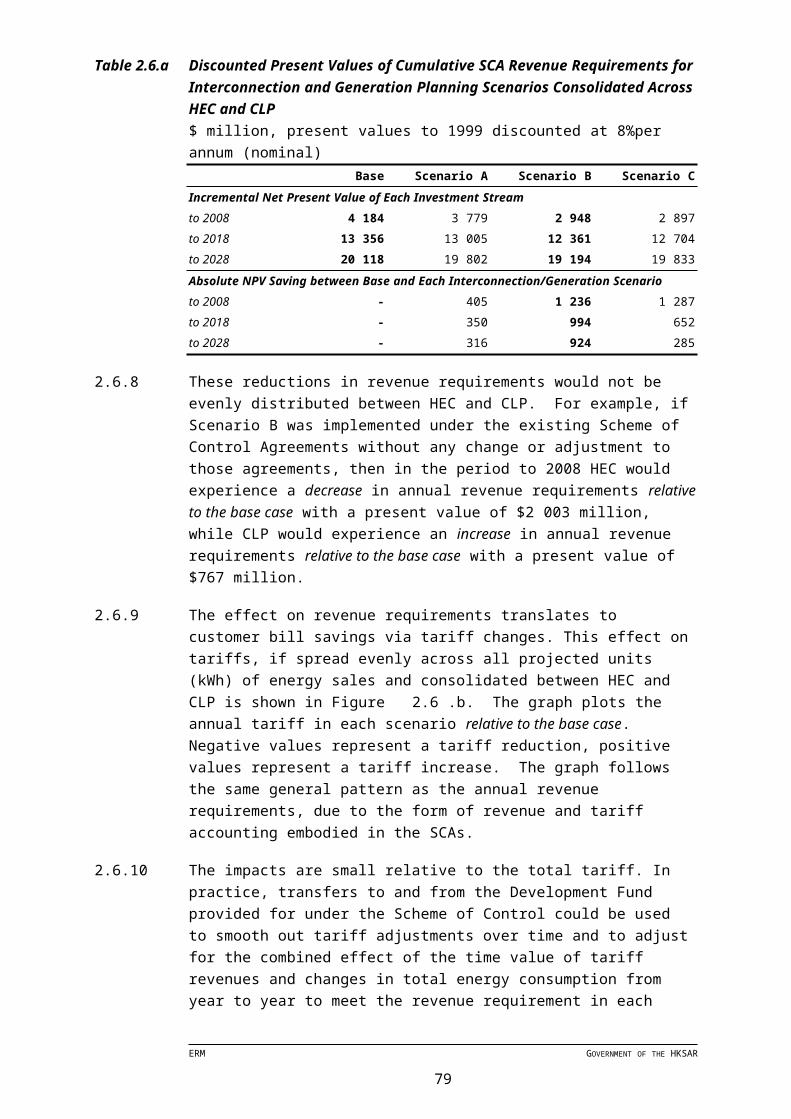

Table 2.6.a Discounted Present Values of Cumulative SCA Revenue Requirements for Interconnection and Generation Planning Scenarios Consolidated Across HEC and CLP 58

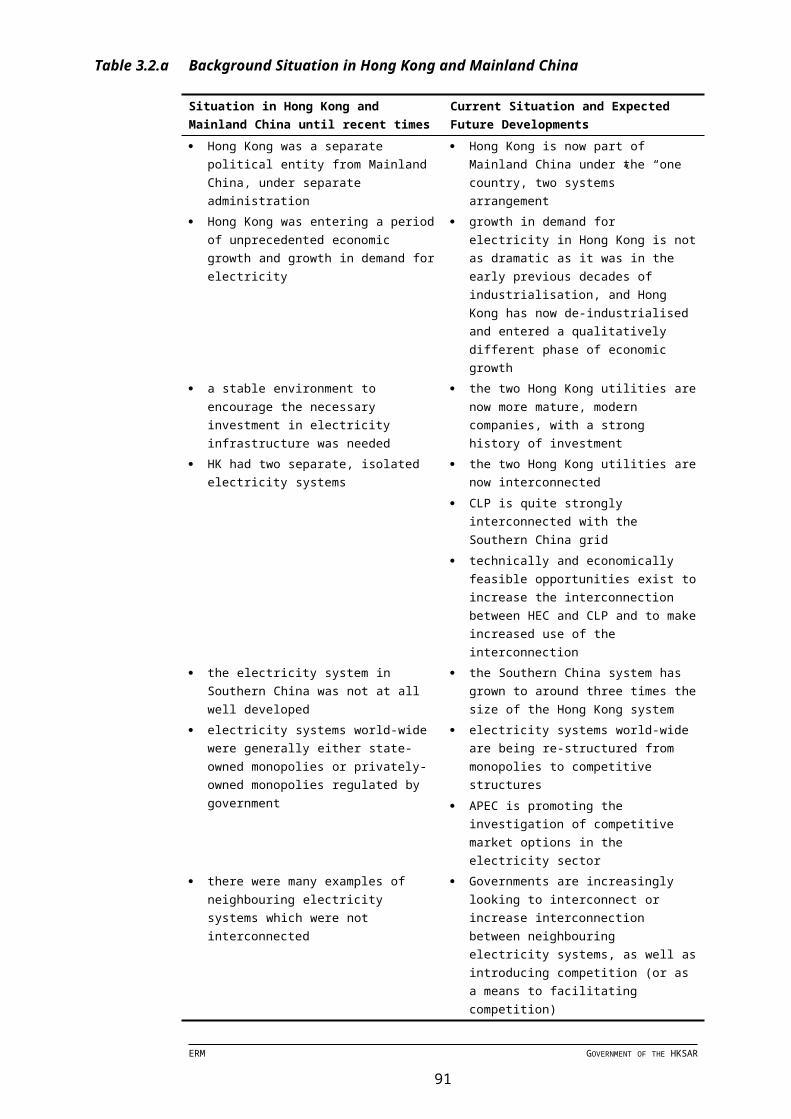

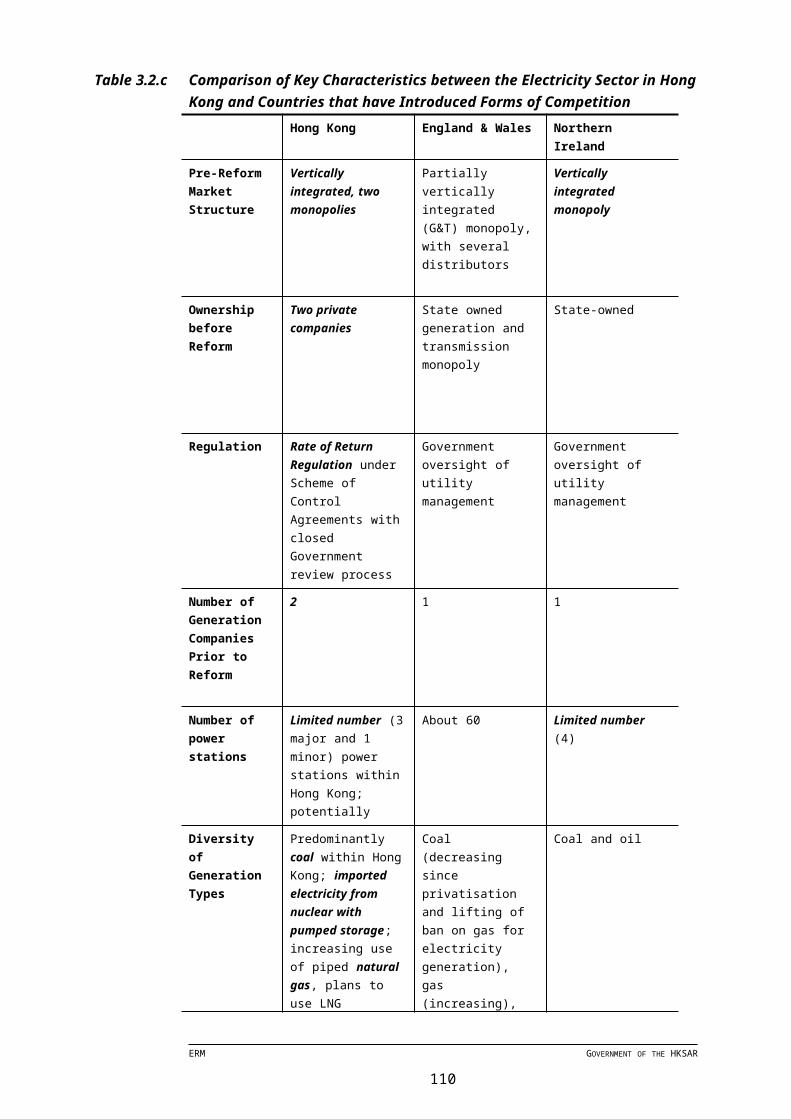

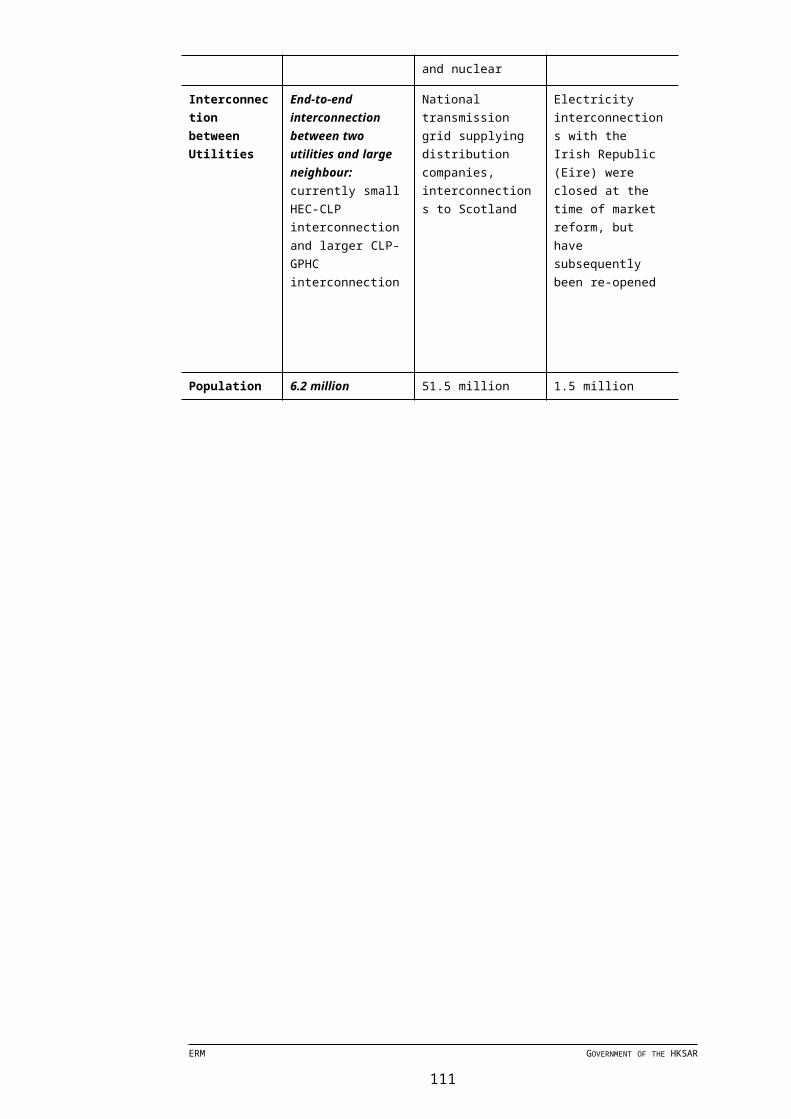

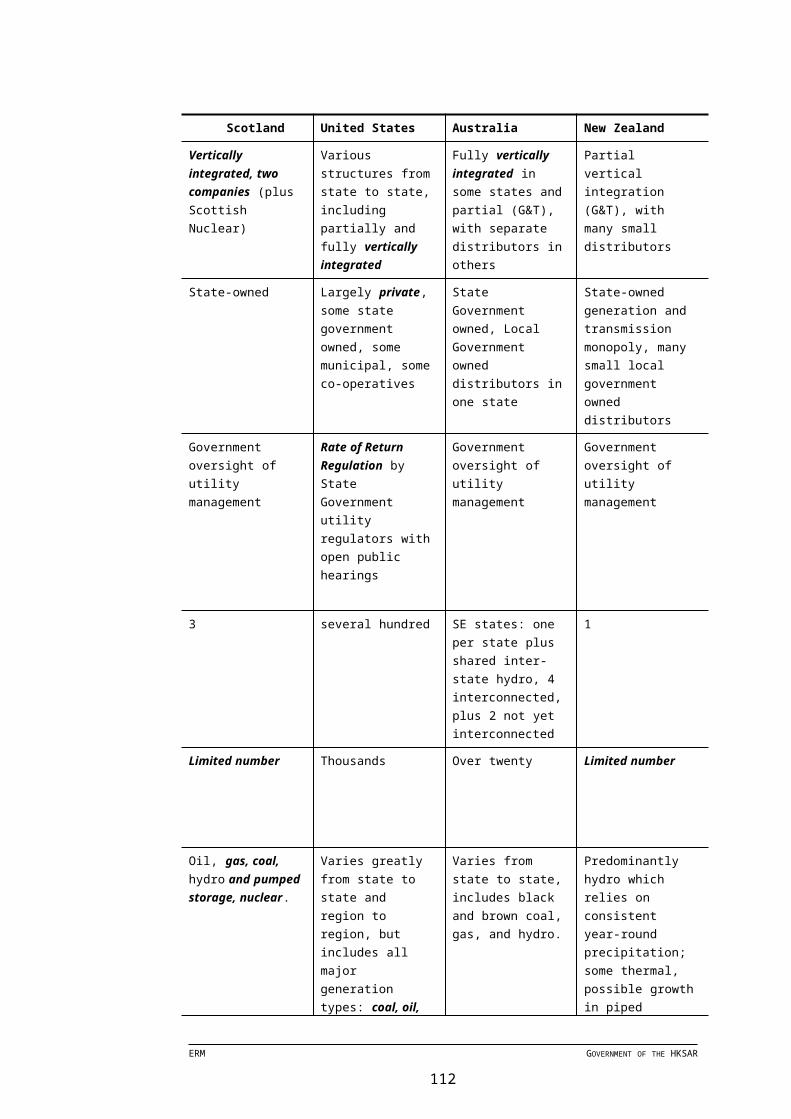

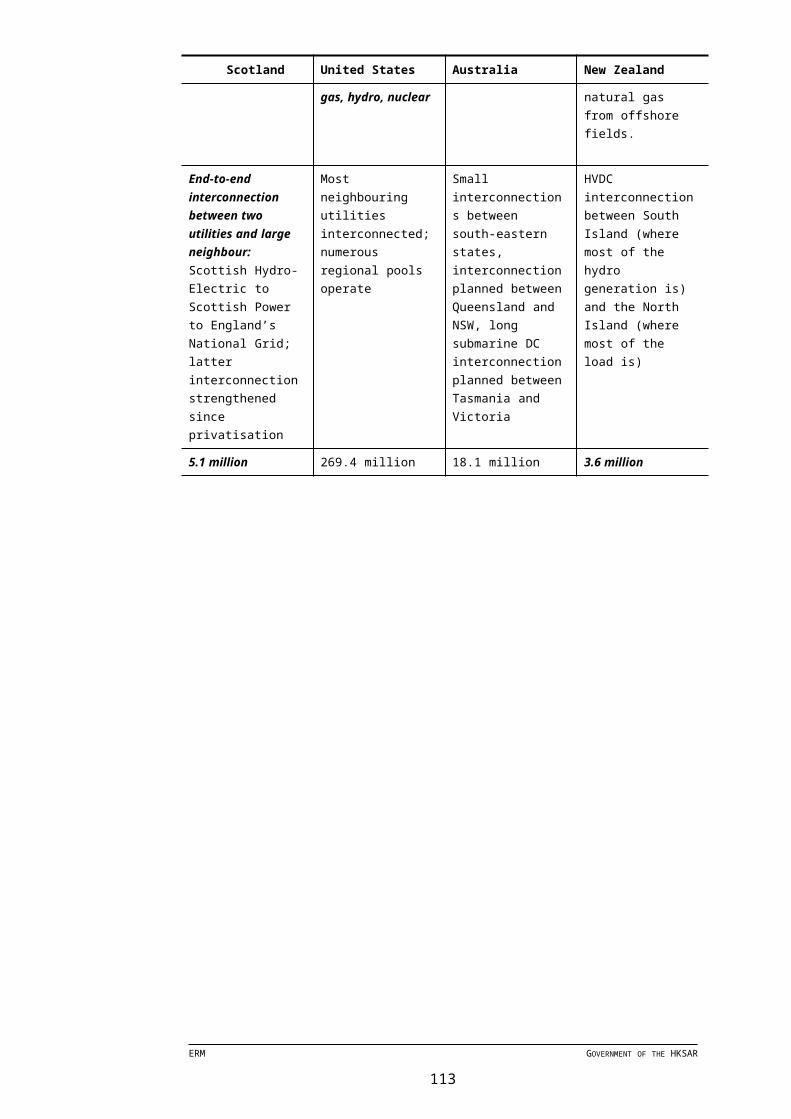

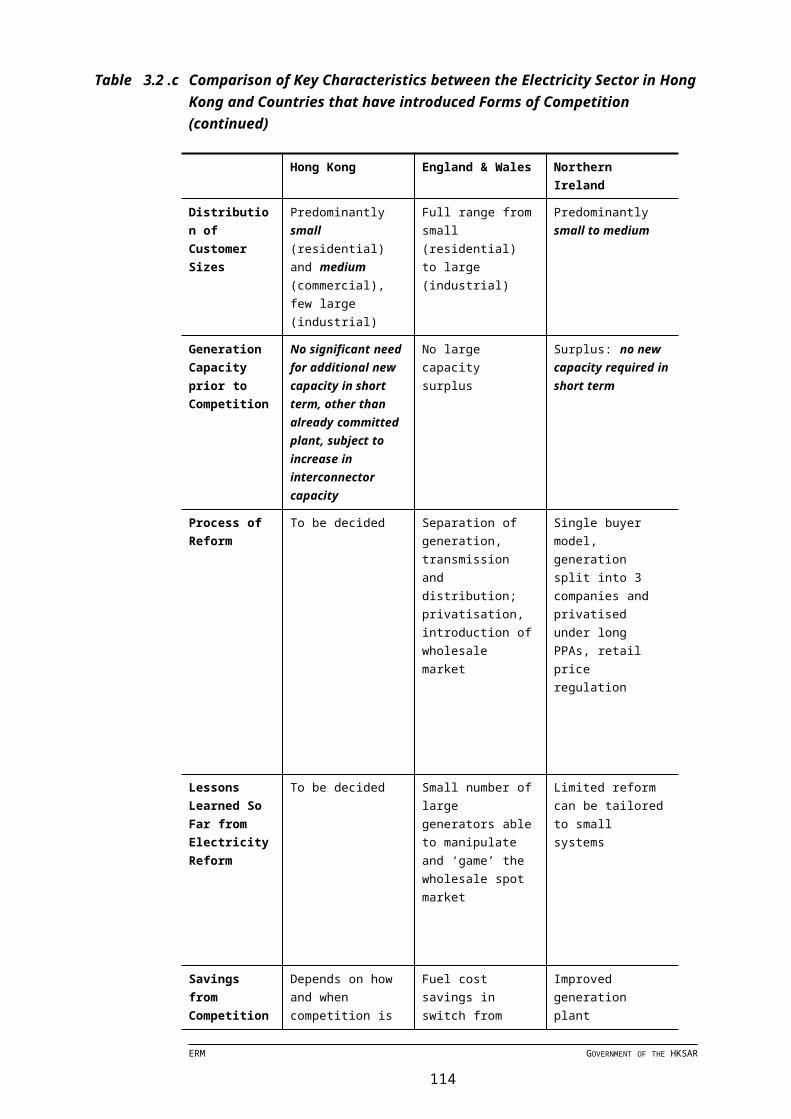

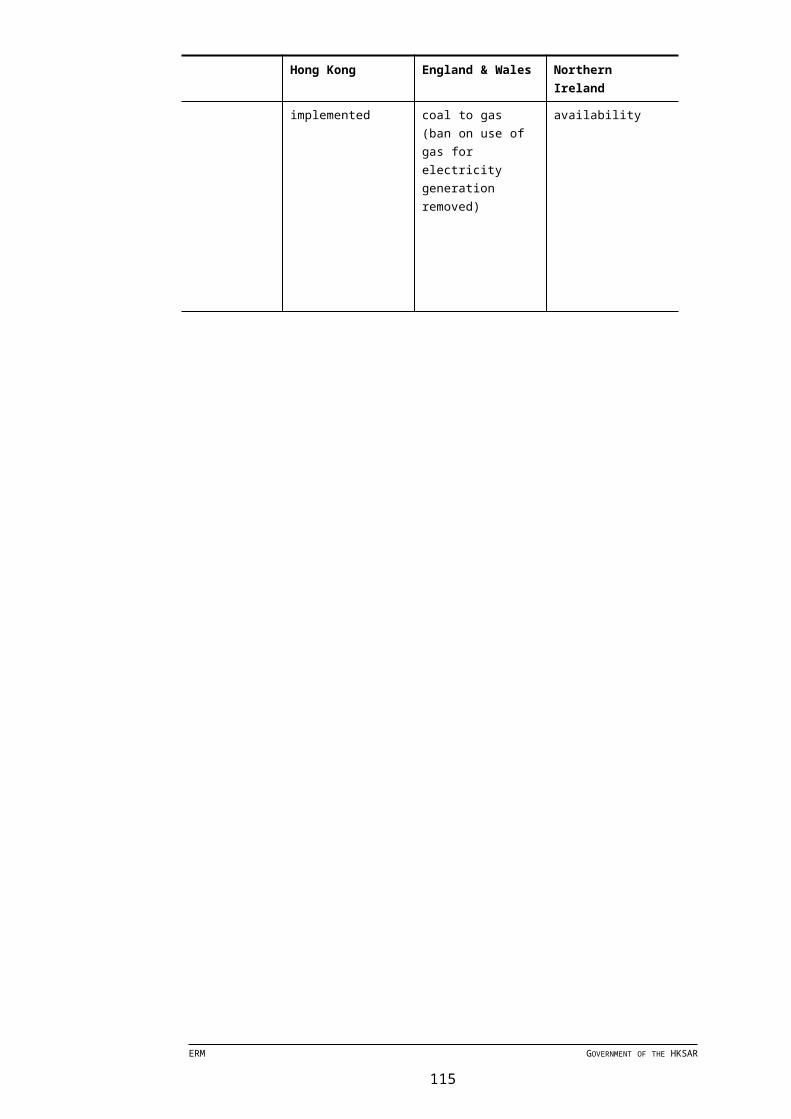

Table 3.2.a Background Situation in Hong Kong and Mainland China 68Table 3.2.b Advantages and Disadvantages of Each Market Structure 79Table 3.2.c Comparison of Key Characteristics between the Electricity

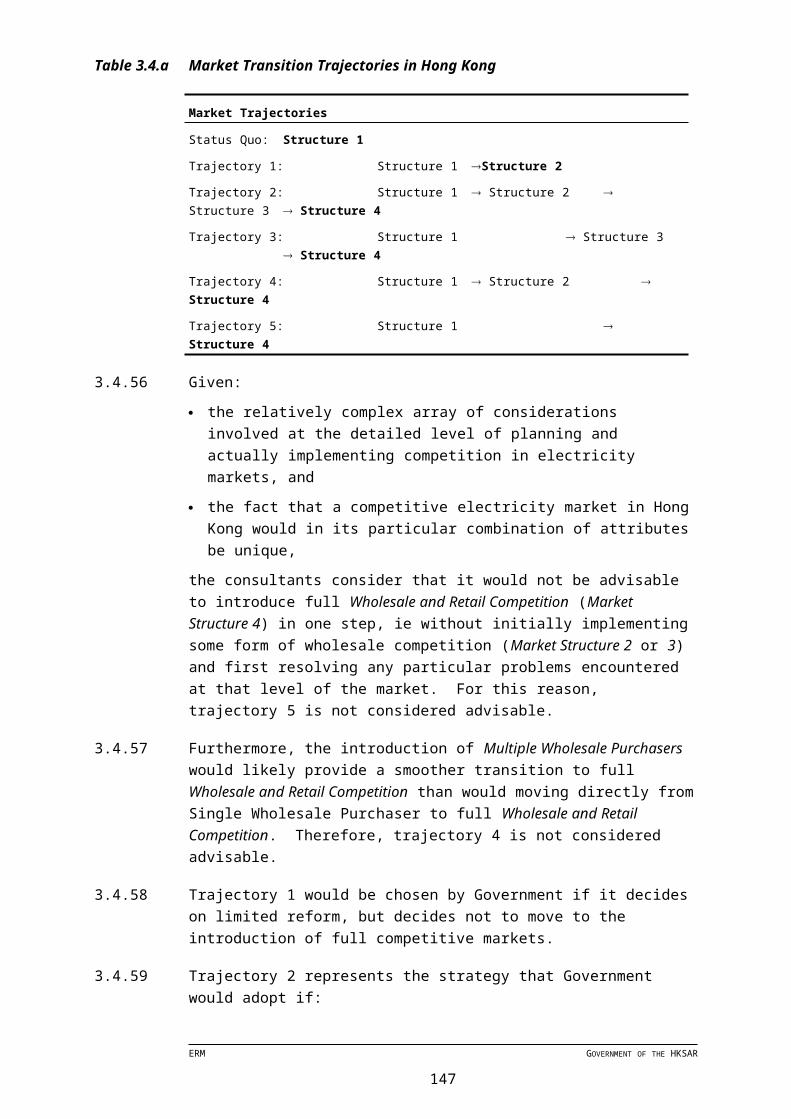

Sector in Hong Kong and Countries that have Introduced Forms of Competition 82

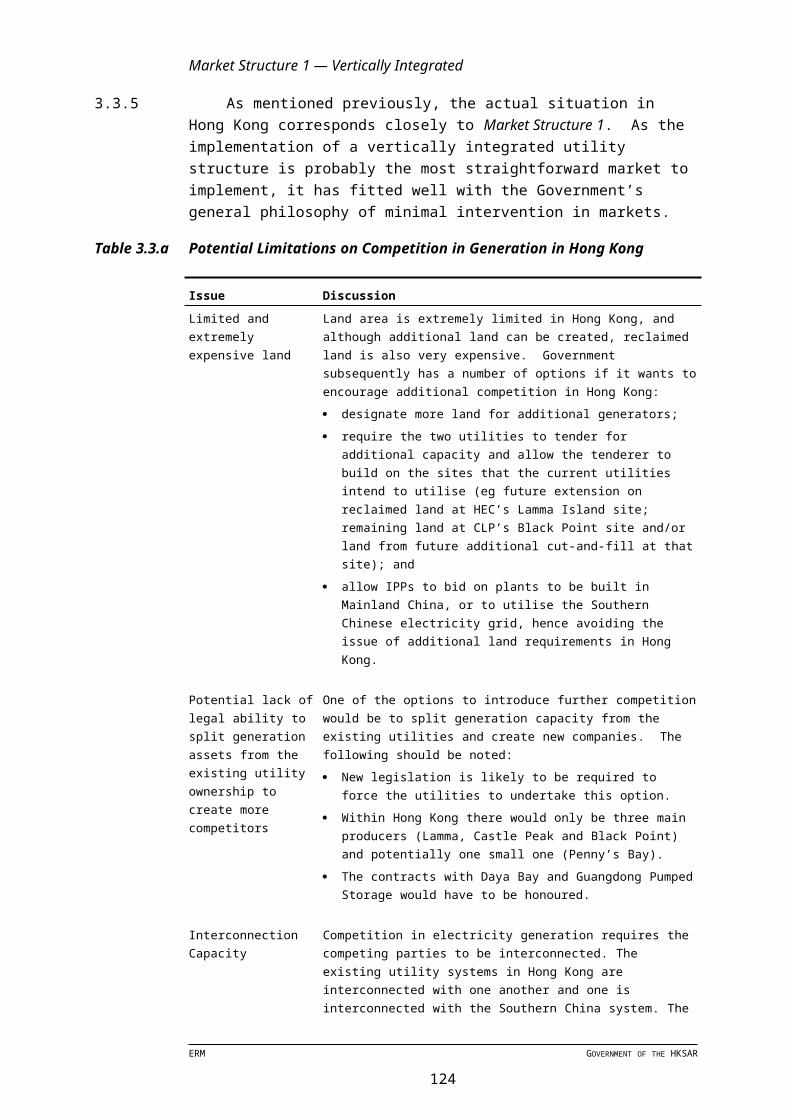

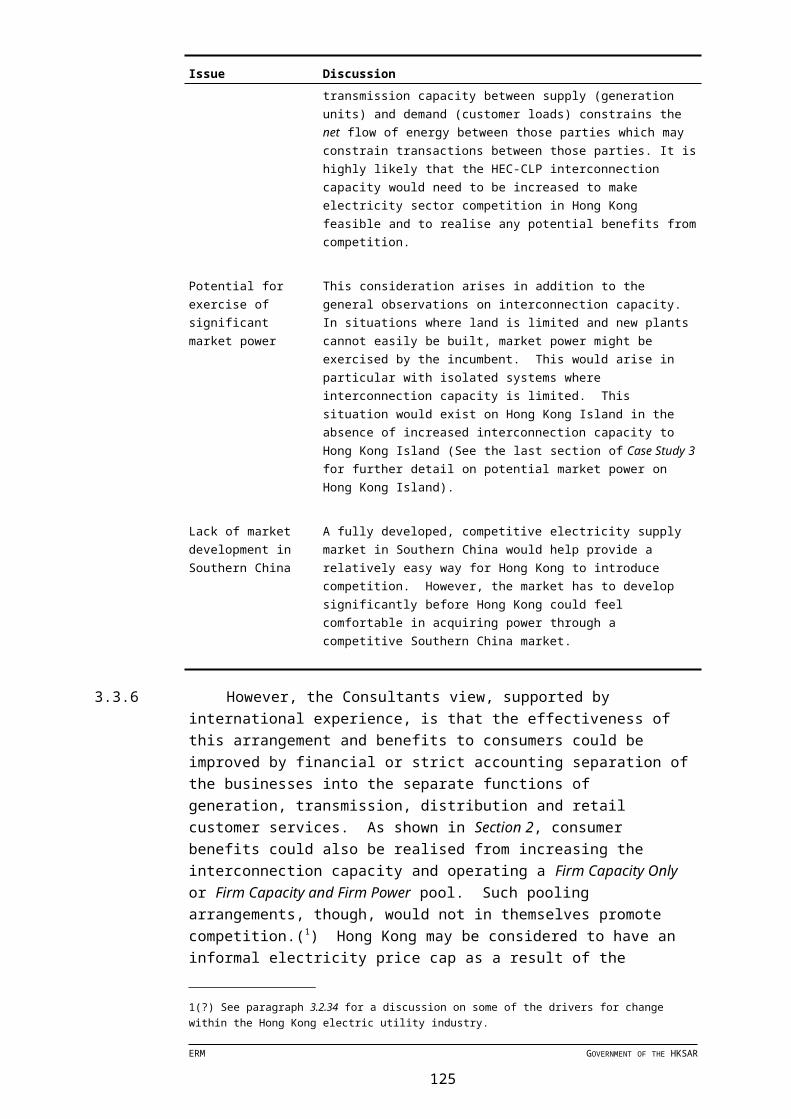

Table 3.3.a Potential Limitations on Competition in Generation in Hong Kong 91

Table 3.4.a Market Transition Trajectories in Hong Kong 107Table 3.4.b Windows of Opportunity for Implementation 110Table 4.2.a Comparison of Guangdong and Hong Kong Electricity Sectors

(1997) 114Table 4.2.b Capacity in the Three Provinces of South-West China 115Table 4.4.a Implications for Hong Kong of a Restructured Guangdong

Electricity Sector 120

ERM GOVERNMENT OF THE HKSAR

LIST OF FIGURES

Figure 1.1.a The Hong Kong and South China Interconnected System Configuration 2

Figure 2.2.a Potential Overall Benefits of Interconnected Systems 17Figure 2.5.a Discounted Present Values of Cumulative Incremental

Capital Expenditures for Interconnection and Generation Planning Scenarios Consolidated Across HEC and CLP 49

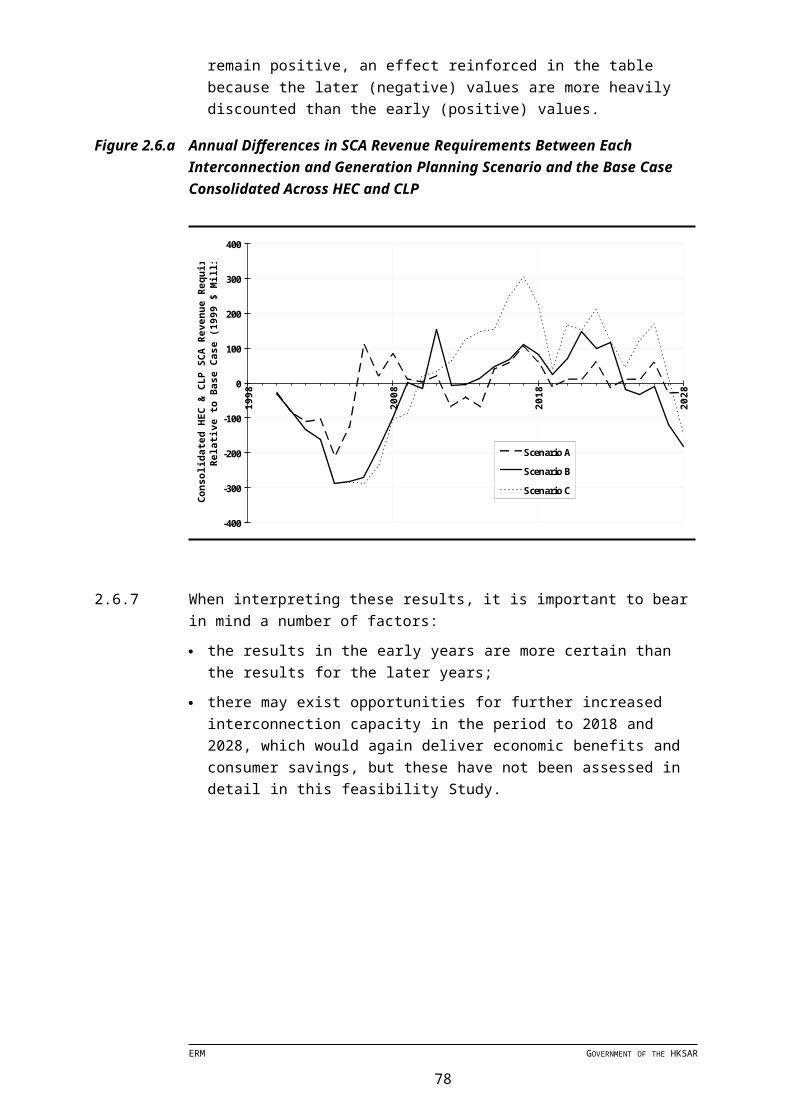

Figure 2.6.a Annual Differences in SCA Revenue Requirements Between Each Interconnection and Generation Planning Scenario and the Base Case Consolidated Across HEC and CLP 57

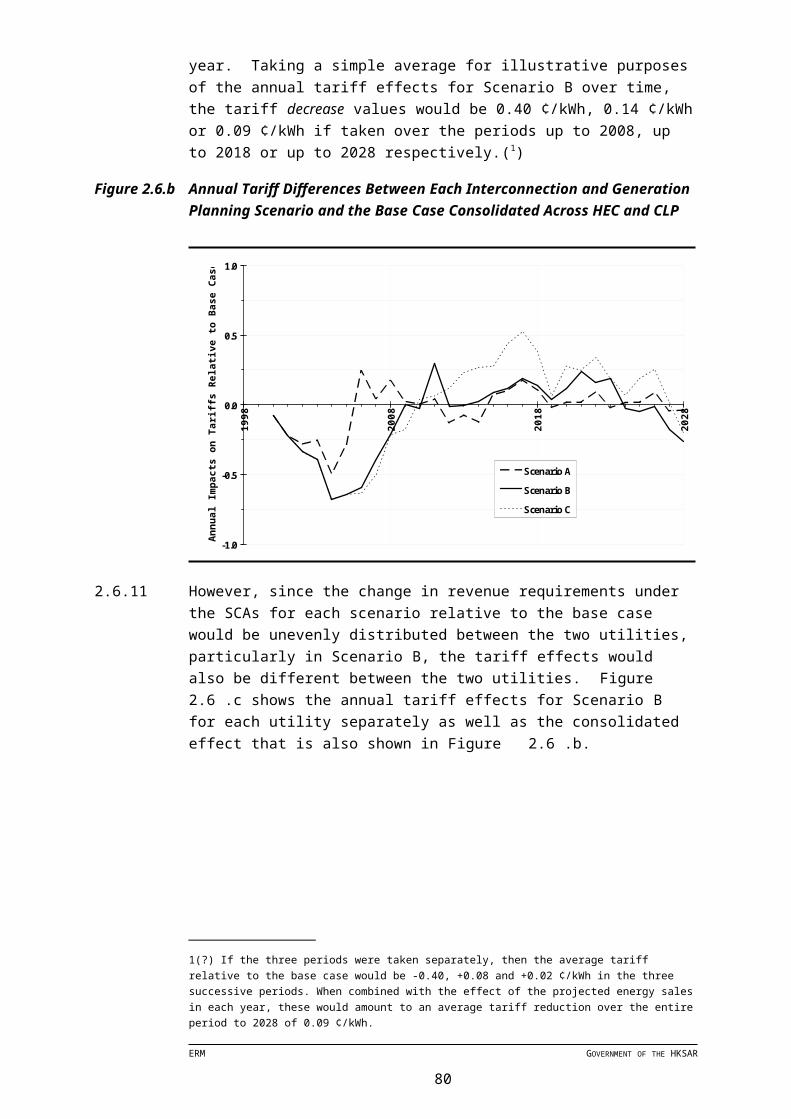

Figure 2.6.b Annual Tariff Differences Between Each Interconnection and Generation Planning Scenario and the Base Case Consolidated Across HEC and CLP 59

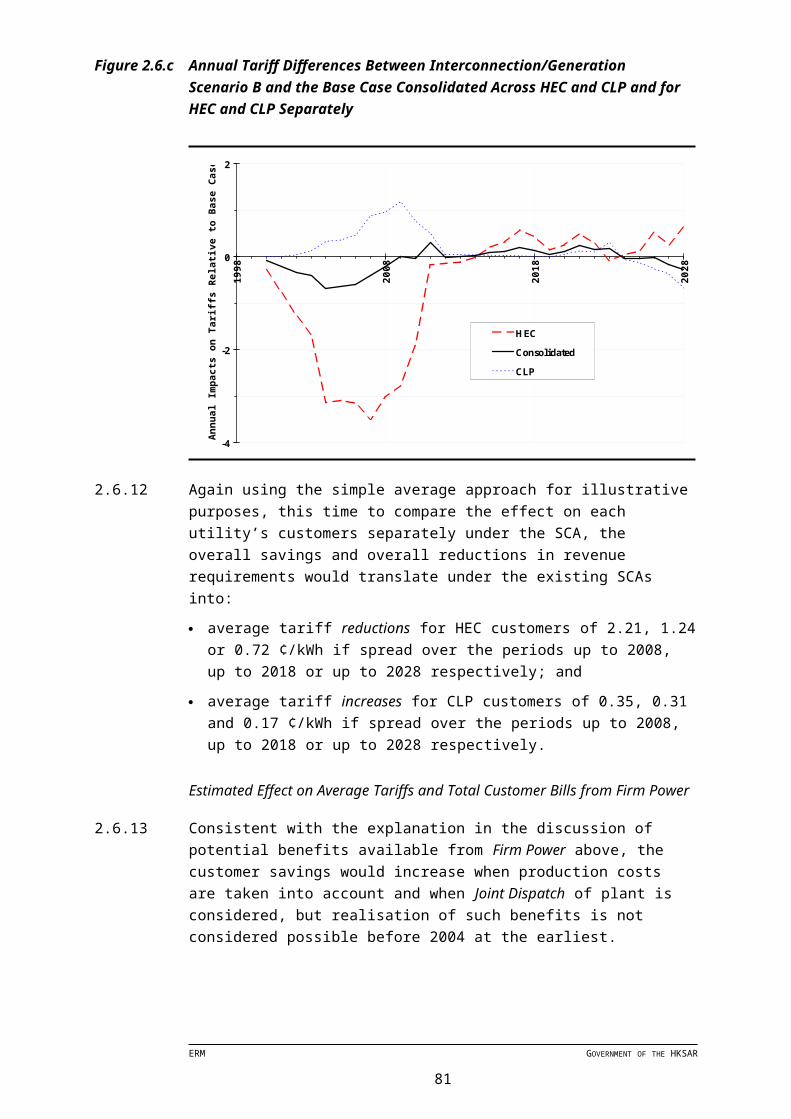

Figure 2.6.c Annual Tariff Differences Between Interconnection/Generation Scenario B and the Base Case Consolidated Across HEC and CLP and for HEC and CLP Separately 60

Figure 3.2.a Market Structure 1 — Monopoly / the Vertically Integrated Utility 75

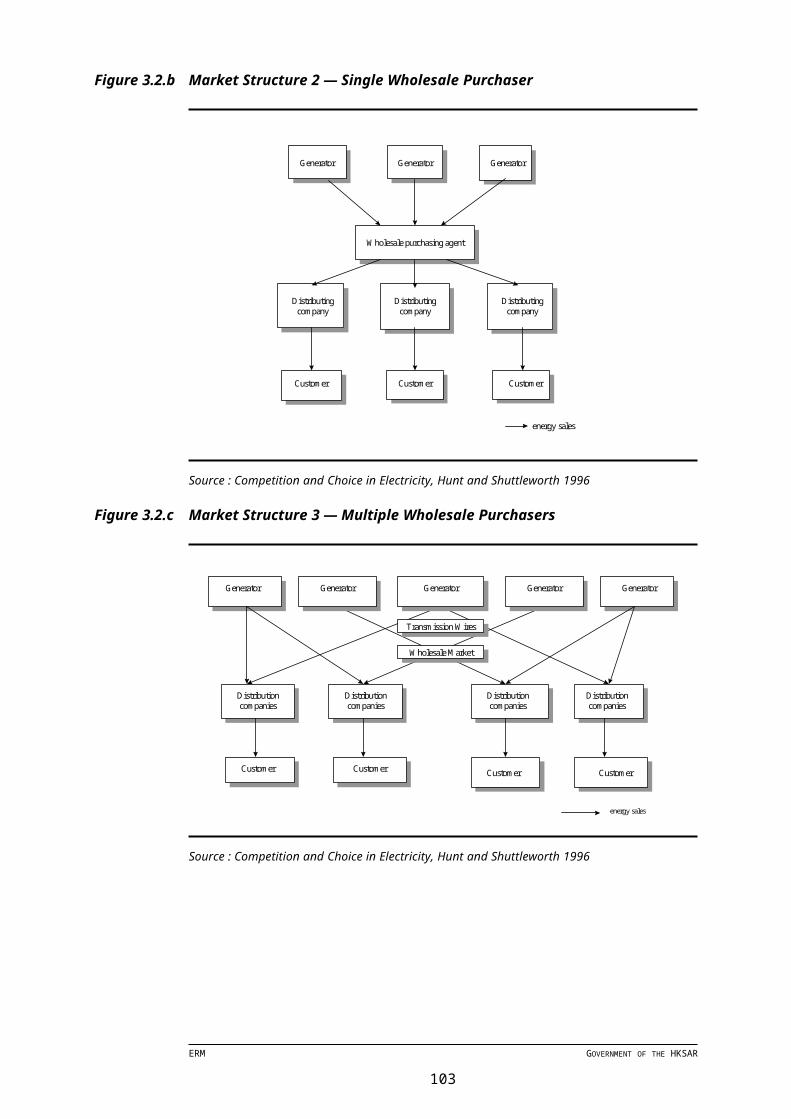

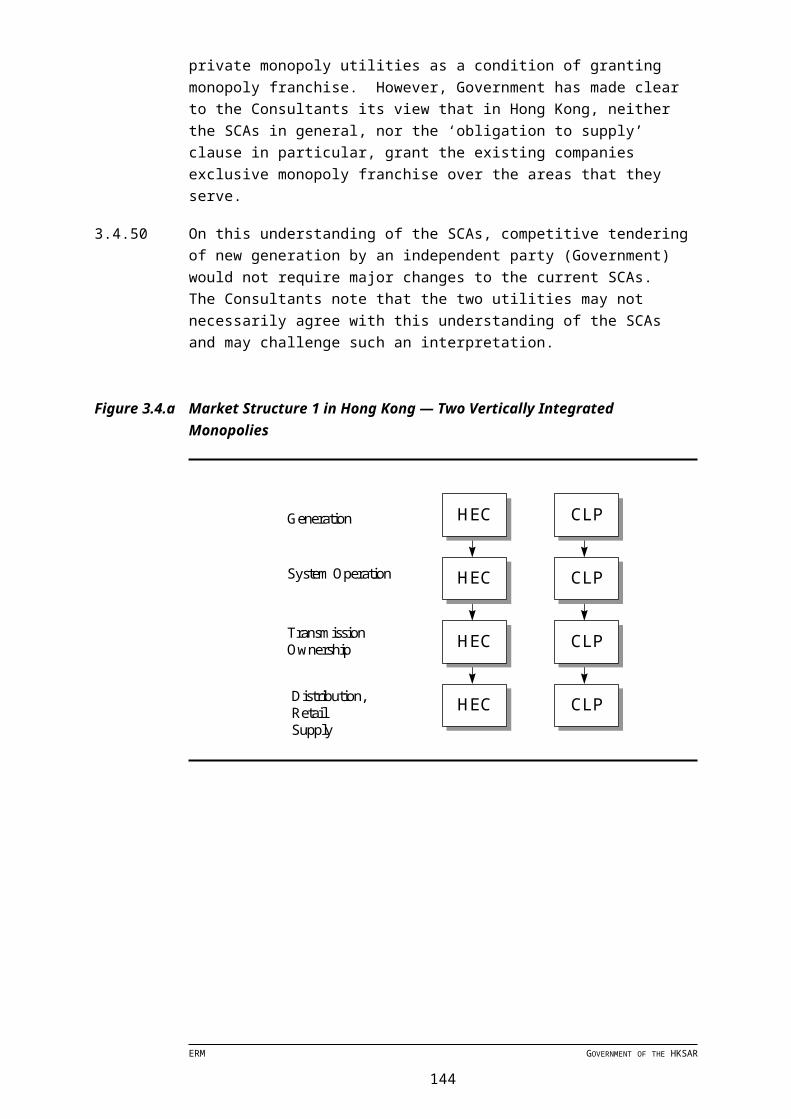

Figure 3.2.b Market Structure 2 — Single Wholesale Purchaser 76Figure 3.2.c Market Structure 3 — Multiple Wholesale Purchasers 76Figure 3.2.d Market Structure 4 — Retail Competition 77Figure 3.4.a Market Structure 1 in Hong Kong — Two Vertically Integrated

Monopolies 105Figure 3.4.b Market Structure 2 in Hong Kong — Single Wholesale

Purchaser 106Figure 3.4.c Market Structure 3 in Hong Kong — Multiple Wholesale Purchasers

106Figure 4.3.a Planned Process of Restructuring for Guangdong Electricity Sector

117

LIST OF BOXES

Box 3.2.a Northern Ireland’s Experience of Electricity Restructuring 87Box 3.2.b Scotland’s Experience of Electricity Restructuring 88Box 3.2.c Ukraine’s Experience of Electricity Restructuring 89

ERM GOVERNMENT OF THE HKSAR

NOTE

A Chinese translation of the Executive Summary of this report is available as a separate document.

ERM GOVERNMENT OF THE HKSAR

FOREWORD This report presents the results of a feasibility study of whether consumer benefits might be gained in Hong Kong’s electricity sector from increases in interconnection capacity between The Hongkong Electric Company (HEC) and CLP Hong Kong Limited (CLP) and the introduction of competition. Quantitative economic analysis of potential cost reductions from increased interconnection, expressed in terms of both total consumer benefits and the effect on tariffs was conducted at a level of detail appropriate for a feasibility study. Qualitative assessment was made of various electricity sector structures, including competitive market models. The assessment of the potential economic benefits of increased interconnection required the use of actual utility data, of available projections of peak load growth and of plant capital, fuel and operating costs. The use of such actual data specific to Hong Kong’s electricity sector improves the usefulness of this Study (compared with some alternative approaches such as generic international comparisons alone). However, several points must be borne in mind. This Study adopted a long-term (30-year) time horizon in order to focus on the medium- to long-term benefits potentially available. The utilities’ detailed generation and transmission expansion planning horizons are considerably shorter than this (in the order of 10 to 15 years, which is standard utility practice in most countries). The focus of this Study is therefore on long term policy questions, not on short-term utility planning.

ERM GOVERNMENT OF THE HKSAR

xv

GLOSSARY

Term Description

Available Transfer Capability (ATC)

As used in this Study: the amount of interconnection capacity available on the interconnector once the largest circuit outage contingency has been allowed for (N-1) and capacity has been set aside to allow inter-area spinning reserve obligations to be met.

Bill saving The reduction in electricity bills (summed across all customers) associated with a reduction in revenue requirement. In this Study, such reductions arise in the interconnection/generation scenarios due to reductions in capital expenditure requirements and associated reductions in absolute profit levels under the Scheme of Control framework.

Bus or bus-bar An electrical conductor to which are attached a number or circuits.

Captive customer

A customer who has no choice of supplier.

Carrying charges

See transmission fees.

Consolidated In this Study, the combined effect of economic and/or financial results on HEC and CLP and on the customers of the two companies. Key results are also presented for the two companies separately.

Contingencies A contingency is an event that could cause a disruption in the supply of electricity. Examples include the loss of output from a power station or loss of power flow across an interconnector circuit, which may occur due to protection equipment built into the system being “tripped.” Allowance in system planning for any single contingency is called an N-1 criteria, where there are N relevant elements (such as generators or transmission circuits) in the system. Allowance for double (two simultaneous) contingencies is known as an N-2 criteria.

Distribution The process of transforming electricity from high voltage to low voltage and distributing that energy to consumers.

Diversity in load profiles

Load diversity is a measure of difference between load profiles, where a load profile describes the variation in load or electrical demand over a period of time, such as a day or a year. If two given load profiles have high diversity, then they are dissimilar such that they have non-coincident peaks — one tends to have high load values at the time that the other has low values and vice versa — and when added together the resulting peak demand will be considerably smaller than the sum of the individual peak demands. In most electricity systems benefits of diversity exist between customer groups — many commercial customer loads peak during the day while residential customer loads peak during the evening. When the load profiles in two adjoining areas are diverse — as may happen when one that has a predominantly commercial load peaking in the middle of the day and another that has a predominantly residential load that peaks at night — opportunities exist for synergy, because the generation capacity necessary to meet the peak of the interconnected areas as a whole is lower than that required to meet each area individually. There is not a great deal of diversity between the HEC and CLP load profiles, so the opportunity for such synergy in Hong Kong

ERM GOVERNMENT OF THE HKSAR

xvi

Term Descriptionis limited.

Firm Capacity As used in this Study: the technical capability of the interconnection itself to provide “firm” inter-area generation capacity support as and when it is needed. (Note: this term is sometimes used to refer to generation capacity contracted between a supplier and a customer on a firm basis such that it could be considered the same as if the customer had ownership over the capacity. The existing Interconnector Agreement in Hong Kong uses a much more limited definition of firm capacity than this.)

Firm Power As used in this Study: the technical capability of the interconnection itself to support the regular, reliable transfer of energy between areas, as would be required if generation plant was jointly dispatched for the system as a whole. (Note: this term is sometimes used to refer to contractual arrangements between utilities for the supply of energy. The use of the term in this Study does not necessarily entail such arrangements, although neither does it preclude such arrangements being put in place.)

Generation The process of generating electricity. Also “generation plant:” power station units; “generation capacity:” maximum available instantaneous output from a power plant unit or collection of units.

Hot standby Generation capacity that must be able to be online within 30 minutes should spinning reserve not be able to meet a contingency.

Independent Power Producer (IPP)

IPPs are generally thought of as electricity generators who are not utility affiliated, eg this will not apply to Black Point or Lamma power stations under the current regulatory structure, but potentially a new power station in Hong Kong or elsewhere. Utilities may become IPPs if there is separation of ownership of generation from the transmission and distribution of electricity.

Independent System Administrator (ISA)

A variant on the Independent System Operator model for transmission system operation.

Independent System Operator (ISO)

Potentially separate from the owner of the transmission system, an ISO is the manager of the transmission system and often determines dispatch order, undertakes planning functions and ensures fair and non-discriminatory access to the transmission system. Generally considered a requirement for a competitive market.

Independent Transmission Company (ITC)

A variant on the Independent System Operation model for transmission system operation.

Independent Transmission System Operator

Same as Independent System Operator.

Interconnection Essentially a transmission line, but between two utilities.Joint Dispatch Centre (JDC)

Physical facility with control equipment for dispatching simultaneously the generation plants of more than one utility.

Joint dispatch Generally: dispatch of power plants that is undertaken in co-ordination with other utilities. As used in this Study: Operating or “dispatching” generation plants in separate areas on a joint basis to realise any available synergy and operational

ERM GOVERNMENT OF THE HKSAR

xvii

Term Descriptioneconomies to achieve the least cost generation production cost.

Joint planning As used in this Study: generation and transmission planning that is undertaken jointly between neighbouring utilities, taking into account interconnection options in order to achieve least-cost expansion of the system as a whole.

Load centres Centres of high load density, eg Central, Hong Kong.Load shedding The process of cutting the supply of electricity to customers.LOLE Loss of load expectation is the inverse of LOLP.LOLP Loss of load probability, or the likelihood that generation

capacity will not be sufficient to supply electricity to all customers who demand it.

Loose pool Referred to as Joint Planning in this Study, whereby two areas are interconnected to form one wider system and capacity additions are planned jointly taking into account the interconnection to allow load to be served at lower cost than would be possible for the systems independently, given a specified level of reliability.

Outage The planned withdrawal from service (usually for maintenance) or forced unavailability (unplanned interruption due to faults) of a generation unit, or any part of a transmission or distribution system, for a period of time. Usually measured in terms of weeks per year for planned maintenance outages and fraction of time or probability of unavailability for forced outages.

Performance-Based Regulation (PBR)

In a typical PBR system, prices are linked to a key economic index adjusted for expected increased in productivity. Generally used as an alternative to Rate of Return type of regulation.

Power marketer Within a market that has implemented retail competition, it is unlikely that small consumers will be willing to undertake the complex transactions required to arrange supply from a generator. Consequently, power marketers have emerged that will perform this function for small consumers.

Pooling arrangements

The set of arrangements or rules under which a particular power pool operates. Pooling arrangements can be constituted on a simple co-operative basis, as has been done for decades in some parts of the United States, or it can form the core of a wholesale competitive market. In the first case, it involves simple resource-sharing as defined by the agreements for the operation of the pool. In the second case, generation companies bid power into the pool, an independent power exchange or system operator with joint dispatch facilities dispatches the plant in economic merit order and wholesale purchasers (distribution companies who also retail energy, independent retail energy brokers and large customers) purchase energy from the pool at the real time ‘spot price’. In such competitive markets, the wholesale buyers and sellers usually also “hedge” against movements in the spot price via contracts. This Study deals in some detail with simple pooling arrangements such as Firm Capacity and Firm Power. Issues associated with more sophisticated pool arrangements and operations appropriate for a full competitive wholesale market will not be of concern for many years and so are not dealt with in detail in this Study.

Power pool When two or more utilities act together co-operatively or under the auspices of an independent entity to supply electricity through either joint planning of new facilities or joint

ERM GOVERNMENT OF THE HKSAR

xviii

Term Descriptiondispatching of their power stations.

Rate-of-Return (RoR) Regulation

A type of regulation that allows utilities to earn a rate of return on net fixed assets, as the Schemes of Control Agreement in Hong Kong allow.

Reliability The ability of the system to meet customer demand for energy. Full reliability analysis involves consideration of all three levels in the supply chain: Level I generation, Level II transmission and Level III distribution.

Reserve margins The sum of all available generating capacity, including firm capacity commitments, divided by the utility’s maximum demand, minus one (-1). The reserve margin is one of the key indicators of whether a utility has sufficient generating capacity in cases of emergency.

Retail competition

One step beyond Third Party Access whereby all customers have access to the transmission system.

Revenue requirement

The revenue required by a utility from the total of customer bill payments to cover all costs and allow a given level of profit.

Short, medium and long term

For the purposes of this Study, the periods are defined as 5 to 10, 10 to 20 and more than 20 years respectively.

Single buyer A type of electricity market structure whereby one organisation has a monopoly over the wholesale purchase and retail sale of all electricity. Usually considered a transition step towards a competitive market.

Stranded investment/costs

Usually defined as prudently incurred costs, usually approved by governments, that cannot be recovered in a changed regulatory environment or a competitive market. Such costs can be significant in issue when changes are made to electricity systems, because plant and infrastructure for electricity supply have relatively long service lives and involve investments which are recovered over a relatively long time frame. Where the physical assets associated with a stranded investment are held by an outside company, the stranded costs may appear in the form of a contract or contractual commitment within an electricity utility.

Supply/Retailing The process of organising the physical supply of electricity from generation through transmission and distribution to final consumers. This is usually only discussed as a distinct activity in the context of a competitive market. Especially in a competitive market, this process may not necessarily be performed by the companies involved in the generation, transmission or distribution of electricity, but instead by an independent third party.

System security The ability of a system to continue to meet demand, following an abnormal occurrence, without overloading any component part of that system.

System stability The stability of a power system is characterised principally by the maintenance of frequency, voltage and power transfer within limits. It is also dependent on the design and operation of the transmission system, the response of generation units to disturbances and the availability of reactive power.

Take-or-pay A contractual obligation which requires a company to pay for some specified amount of a commodity (such as electricity or fuel), whether or not the company actually takes that quantity. Such contractual obligations may be simple or complex. It is possible for such contractual arrangements to allow some

ERM GOVERNMENT OF THE HKSAR

xix

Term Descriptiondegree of flexibility with respect to the timing of consumption of the commodity, although not usually with respect to payment for it.

Tariff adjustment/ effect/impact

The average effect on tariffs of a change in revenue requirement, calculated as the change in revenue requirement in dollars (positive or negative) divided by energy consumption in kiloWatt-hours.

Third Party Access

A type of electricity market structure whereby third-party generation companies — other than the company that owns the network — are granted access to that network to supply electricity to customers. The option for customers to obtain supply from third party generation companies (via bi-lateral contracts) is usually limited by size. Without Third Party Access arrangements, a generation company has a virtual monopoly over the customers to whom they have connected the electricity network, as it is usually either not economic or not practical to construct a parallel network to supply customers in competition with an incumbent generation/transmission/distribution company.

Tie or tie-line See interconnector.Tight pool Referred to as Joint Planning with Joint Dispatch in this Study.

The addition to a loose pool arrangement whereby the dispatch of all units included in the multi-area system is undertaken in economic order (subject to certain specified conditions or constraints).

Total Transfer Capability (TTC)

As used in this Study: the amount of interconnection capacity available on the interconnector once the largest circuit outage contingency has been allowed for (N-1).

Transformer A device used to step electricity from one voltage level to another. Transmission and distribution networks progressively step power down in standard increments from high voltage levels (which allow low current and therefore low loss transmission) to lower voltage levels (which ultimately allows distribution to customers at the standard supply voltage level required by their equipment).

Transmission fees

The fees charged by the owner of a transmission system to carry electricity from generators to final customers.

Transmission The process of transmitting electricity, at high voltage, from generators to distributors.

Unbundling Refers to the separation of functions previously undertaken by a single entity, and/or the separation of prices for various aspects of electricity supply. For example, the functions of an ISO and/or Single Buyer are required to be operationally separate from those of generation and distribution. Steps towards unbundling include the accounting separation of vertically integrated utilities.

Vertical integration

Full vertical integration involves the combination of the functions of generation, transmission, distribution and energy retailing within a single electricity utility company. The two separate electricity companies in Hong Kong are fully vertically integrated.

Wheeling of power

Another term for the transfer of power across transmission lines, usually by third parties who must pay fees for the use of the transmission system.

ERM GOVERNMENT OF THE HKSAR

xx

ERM GOVERNMENT OF THE HKSAR

xxi

ABBREVIATIONSAbbreviation

Full Text

AC Alternating currentAPEC Asia Pacific Economic Co-operationAVR Automatic Voltage Regulation CLP CLP Power Ltd (formerly China Light & Power Company Ltd)CPI-X Consumer Price Index minus X, a method of price regulationDC Direct currentEEI Edison Electric Institute, an association of electric utilities in the USAEHV Extra high voltageERM Environmental Resources ManagementFERC Federal Energy Regulatory CommissionFOR Forced Outage RateGPHC Guangdong Electric Power Holding Company in Mainland ChinaGWh GigaWatt-hourHEC Hongkong Electric Company LtdIPP Independent Power ProducerISA Independent System Administrator ISO Independent System OperatorITC Independent Transmission Company JDC Joint Dispatch Centre kV KiloVoltkW KiloWattkWh KiloWatt-hourLOLE Loss-of-load-expectationLOLP Loss-of-load probabilityLRMC Long-Run Marginal Costs MVA MegaVolt-AmpsMW MegaWattMWh MegaWatt-hourNERC North American Electricity Reliability Council, a USA based organised

of utilities which focuses on electricity reliability issuesNTS Nuclear Transmission SystemPAT Profits after taxesPBIT Profits before interest and taxesPBR Performance-Based Regulation PJM The Pennsylvania, New Jersey and Maryland power pool in the USAPOR Planned Outage RatePSS Power System StabilisersPUC Public Utility CommissionPWR Pressurised Water ReactorsPX California Power ExchangeRoCE Return on capital employedRoE Return-on-equityRoR Rate-of-Return regulationSCA Scheme of Control Agreement(s)SPA Seasonal Power AdjustmentSRMC Short-Run Marginal Costs TSO Transmission System OperatorUK United Kingdom

ERM GOVERNMENT OF THE HKSAR

xxii

1 INTRODUCTION AND OVERVIEW

1.1 Background

Study Team

1.1.1 Environmental Resources Management (ERM) was commissioned by the Government of the Hong Kong Special Administrative Region to undertake a study entitled: Interconnection and Competition in the Hong Kong Electricity Supply Sector. The Study Team comprised experts from the following organisations based in Hong Kong, the United Kingdom, Germany, the United States and Mainland China: ERM Hong Kong ERM Energy (UK) Fichtner GmbH & Co. Public Service Electric & Gas Co. Burns & Roe Co. Tabors, Caramanis & Associates Guangdong Energy Techno-Economic (ETE) Research Centre

Study Overview

1.1.2 The objective of the Study was to establish the feasibility of whether additional interconnection between Hong Kong’s two electricity utilities — joining the CLP Hong Kong Limited (CLP) network in Kowloon with The Hongkong Electric Company (HEC) network on Hong Kong Island — and encouragement of competition in the electricity supply sector would be in the interest of consumers.

Hong Kong Electricity Industry Structure

1.1.3 Hong Kong’s electricity needs are served by two separate electricity utilities, each with vertically integrated generation-transmission-distribution-retailing operations: HEC and CLP,(1) which have been serving Hong Kong since 1890 and 1901 respectively.

Institutional Arrangements

1.1.4 Government and the utilities have entered into Scheme of Control Agreements (SCAs) which regulate profits via a rate-of-return on assets approach. The current agreements are due to expire in 2008.

1(?) CLP has arrangements with several separate companies for the provision of electricity generation. For the purposes of the Scheme of Control Agreement and for this Study, they may be considered to operate as an integrated whole.

ERM GOVERNMENT OF THE HKSAR

1

The Existing Interconnected System

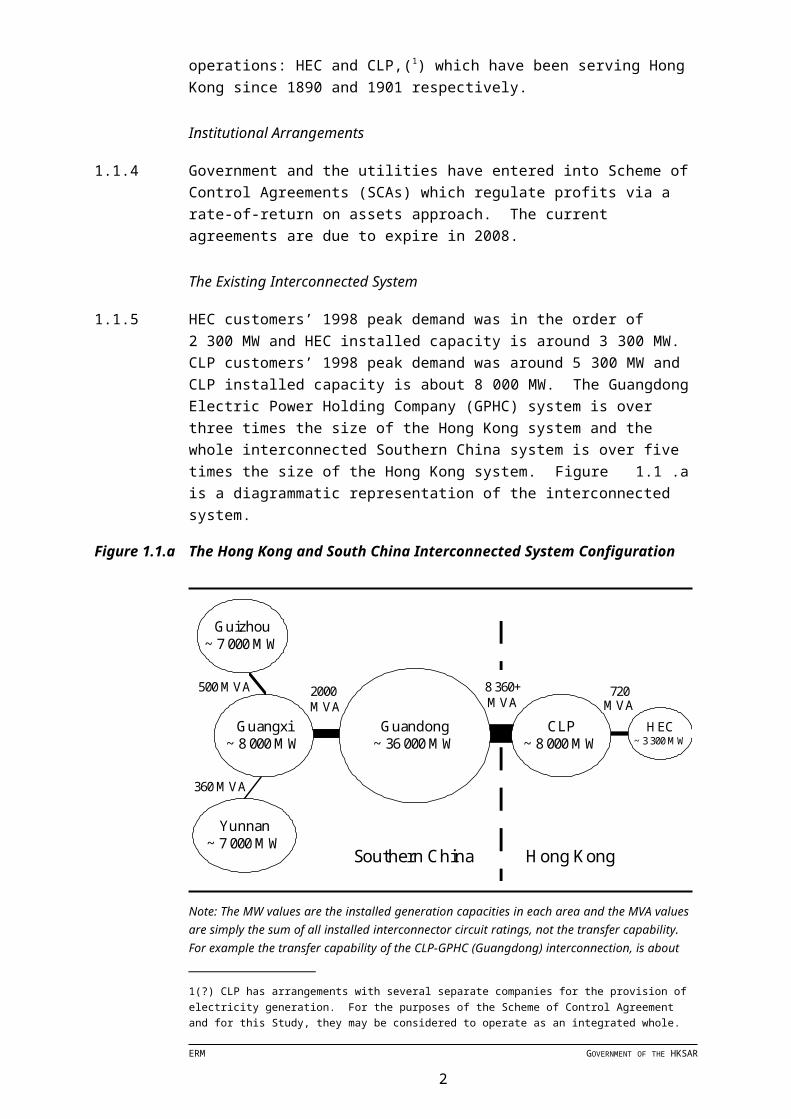

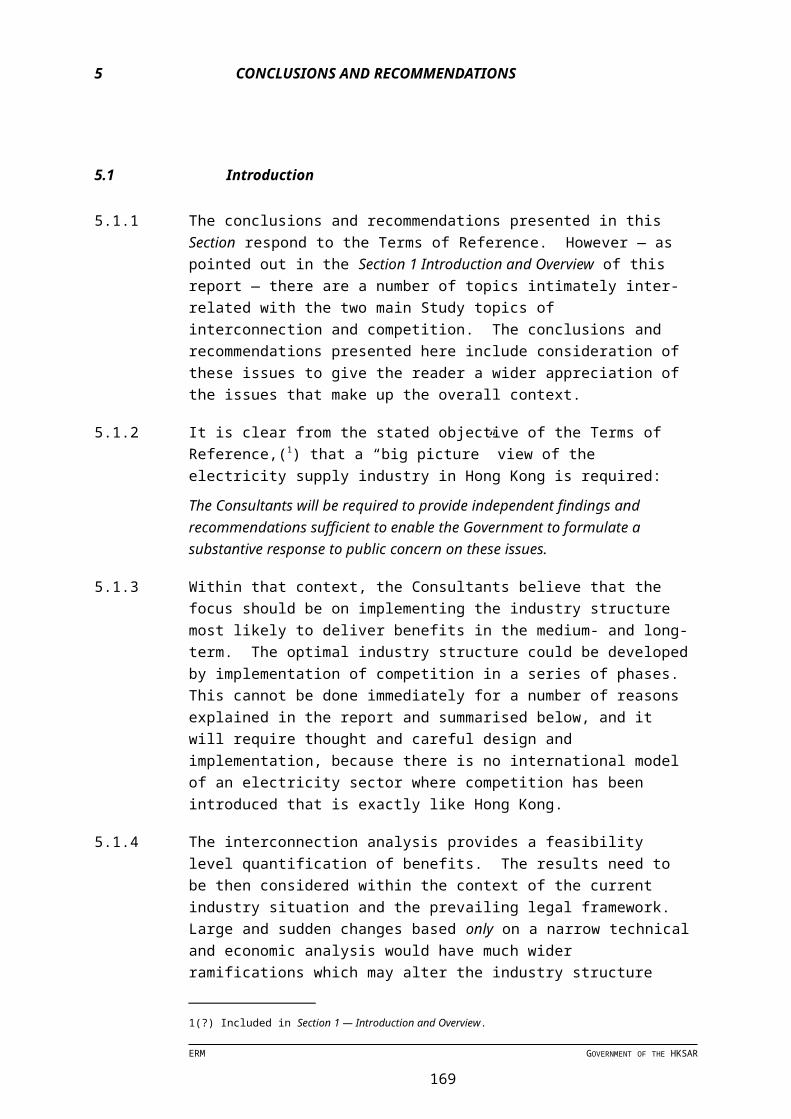

1.1.5 HEC customers’ 1998 peak demand was in the order of 2 300 MW and HEC installed capacity is around 3 300 MW. CLP customers’ 1998 peak demand was around 5 300 MW and CLP installed capacity is about 8 000 MW. The Guangdong Electric Power Holding Company (GPHC) system is over three times the size of the Hong Kong system and the whole interconnected Southern China system is over five times the size of the Hong Kong system. Figure 1.1.a is a diagrammatic representation of the interconnected system.

Figure 1.1.a The Hong Kong and South China Interconnected System Configuration

HEC~ 3 300 MW

Guandong~ 36 000 MW

CLP~ 8 000 MW

Yunnan~ 7 000 MW

Guizhou~ 7 000 MW

Guangxi~ 8 000 MW

8 360+MVA

720MVA

2000MVA

500 MVA

360 MVA

Southern China Hong Kong

Note: The MW values are the installed generation capacities in each area and the MVA values are simply the sum of all installed interconnector circuit ratings, not the transfer capability. For example the transfer capability of the CLP-GPHC (Guangdong) interconnection, is about 5 000 MVA. The transfer capability of the HEC-CLP interconnection is discussed in further detail in Section 2 of the report.

Existing Interconnections

1.1.6 The transmission networks of these two utilities have been interconnected since 1981. The CLP transmission network was interconnected with Southern China in 1979 and this interconnection was greatly strengthened in 1992.

1.1.7 The existing interconnection between Hong Kong Island and Kowloon linking the CLP and HEC systems has a somewhat limited capacity relative to the current size of the two systems.

ERM GOVERNMENT OF THE HKSAR

2

1.1.8 The existing HEC-CLP interconnection is used for emergency support, economy power interchanges, sharing of spinning reserve, and mutual backup of both systems. Its operation is governed by an Interconnection Agreement between the two utilities that was drawn up with some Government involvement, and entered into voluntarily by the utilities. It can be terminated by either utility by providing at least one year’s advance notice in writing.

1.1.9 CLP’s 400 kV transmission network is further connected to the Daya Bay Nuclear Power Station and to the Guangzhou Pumped Storage Plant via the 500 kV network in Guangdong Province. CLP and GPHC are also interconnected at 132/110 kV level as back-up circuits to supply power from CLP to GPHC. The total capacity of the interconnection between CLP and GPHC is almost 5 000 MVA.

1.1.10 The CLP-GPHC interconnection is used to deliver CLP’s share of the nuclear and pumped-storage energy from the Mainland to the CLP system and for bulk energy interchanges from CLP to GPHC. The two systems provide each other with some mutual emergency backup.

1.2 Study Objective

1.2.1 The objective of this Study, as stated in the Terms of Reference, is to: establish whether additional interconnection between Hong Kong’s two electricity supply companies and encouragement of competition in the electricity sector would be in the interests of consumers. The Consultants will be required to provide independent findings and recommendations sufficient to enable the Government to formulate a substantive response to public concern on these issues.

1.2.2 This is a feasibility-level Study. The Terms of Reference ask for answers to two main questions, under the following tasks: interconnection: assessment of the potential costs, benefits and

other implications of increasing interconnection capacity between CLP and HEC;

competition: assessment of the potential for competition in the electricity supply sector, evaluation of alternative market structures and identification of the optimal market structure.

1.3 Study Approach

Study Topics and Related Topics

1.3.1 The two topics of the Study — interconnection and competition — are somewhat inter-related, as the options for future electricity sector competition are determined (among other things) by the

ERM GOVERNMENT OF THE HKSAR

3

wider transmission system, including interconnections between systems.

1.3.2 This Study is not specifically about the following: generation expansion planning; the existing industry structure and ownership arrangements; the advantages and disadvantages of the Scheme of Control

Agreements; possible alternative forms of regulation.

1.3.3 However, it is not possible to consider the possibility of making increased use of interconnection without considering generation expansion planning in substantial detail. Similarly, it is not possible to consider possibilities regarding future competition without considering the existing industry structure and ownership, the existing form of regulation and adjustments, changes or reforms that could be made in future.

Study Constraints

1.3.4 International experience has shown that the process of electricity market restructuring is a long and challenging process, with extensive technical and economic analysis, research and consensus-building required over a significant period of time to accomplish consumer benefits. Hong Kong is no different. The Consultants consider the results of this Study robust, but they should be seen as the beginning of a process and not as the final answer.

1.3.5 This Study is the first of its kind in analysing the electricity market in Hong Kong and identifies issues which will require negotiation and discussion as well as further analysis. Constraints that were encountered in this Study include: the time frame within which to conduct analysis and research

into the complex issues central to the objectives of the Study; some disputed issues on the preciseness of technical and cost

issues concerning increased interconnection between HEC and CLP;

modelling assumptions that had to be made for a 30 year period; the complex policy context of some of the issues; and lack of detailed technical data on the Mainland China electricity

system.

Interpretation of the Results

1.3.6 The quantitative results of this feasibility study are intended to be indicative of the potential economic, financial and tariff benefits — they are not intended to imply formal review and acceptance by

ERM GOVERNMENT OF THE HKSAR

4

Government of such issues as commissioning dates for generating units as projected in the scenarios.

1.3.7 Three time periods are presented in this Study — to 2008, to 2018 and to 2028 — as required by the Terms of Reference. There is naturally greater certainty in the values in the near-term years than in the medium- to long-term years. Costs of generation plant and associated site, fuel supply and transmission costs for instance are more certain in the short than the long term. For example, international prices for combined cycle gas turbine units have fallen substantially in the last few years as the technology matures and the size of the market has increased. This technology was not generally available 30 years ago, and there is considerable uncertainty surrounding the technology that will be available 30 years from now. New technologies, such as small scale fuel cells, are appearing on the horizon and may reach commercialisation well within the time period. Furthermore, there is great uncertainty associated with predicting the effects of major market changes, within and outside the electricity sector in both Hong Kong and China over such a time period. Caution is advised in the interpretation of the medium- to long-term economic, financial and tariff results presented in this Study.

The Current Situation and Context

1.3.8 Both of the questions to be answered by this Study — on increased interconnection and future competition — are inter-related with a number of other broader considerations regarding the current situation of the electricity sector in Hong Kong. The context is therefore crucial to this Study. Relevant aspects of the current situation are outlined below: The SCAs, as they have developed historically, are based on a

model of two separate and independent utilities. The current SCAs are not due to expire until 2008, although there

is a five-year interim review due in 2003. The utilities each plan their own systems then obtain permission

from Government to construct the proposed assets so that they may then count those items in their asset base to obtain a return on them as permitted in the SCAs. The Government does not plan the development of the electricity system, it regulates it.

There exist a given set of investments in generation assets and transmission infrastructure, and one committed but partially completed investment in generation, that are the result of the historical forecasting, planning and approval process.

In power system terms, HEC is small, CLP is somewhat larger and GPHC and the wider Southern China system are very large.

ERM GOVERNMENT OF THE HKSAR

5

Implications of the Current Situation for this Study

1.3.9 Each of these aspects of the actual situation at present has implications for the two questions to be answered by this Study.

1.3.10 The given set of investments in place have an influence on the economic analysis of future investments.

1.3.11 The form of regulation embodied in the SCAs — rate-of-return on fixed assets — has a number of advantages,(1) however one particular disadvantage of this form of regulation is that it discourages the regulated company from seeking least-cost investments in fixed assets, because the permitted return is a function of the company’s fixed assets. This can be managed readily by sound regulation in the case of individual, independent companies, since construction of assets must be approved by the regulator. So the regulatory model — whereby Government has the role of passive approval and the utility has the role of active planner — is well suited to the situation of two separate utilities that developed historically in Hong Kong.

1.3.12 However, these regulatory arrangements tend not to fit so naturally with a situation where a least-cost capital expenditure option would require co-operation between two separate and separately-regulated companies. An example of this is the form of co-ordinated or joint planning that is implicit in consideration of making increased use of interconnection — a topic of this Study. Therefore, the existence of the current SCAs, which are legally binding agreements between Government and commercial entities, may in practice constrain to some extent the options available prior to 2008.

1.3.13 Increasing interconnection between HEC and CLP, would open up the potential in future for meeting some or all of the generation reserve requirements of one area with plant capacity from the other area and/or serving some of the load in one area with generation plants located outside that area. Under the present SCA structure or under possible future competitive electricity market structures, or both, the utility companies may be concerned about this from a commercial perspective.

1.3.14 This may be a greater concern to the smaller HEC system than to the medium-sized CLP system, when only the two Hong Kong utilities are considered, as was the case in this Study, However, CLP is already strongly interconnected with the very large neighbouring GPHC system, and therefore CLP may also have a similar commercial concern with respect to increased use of the CLP-GPHC interconnection.

1(?) Refer to Section 3.3 under Current Alternative Forms of Regulation for the Non-Competitive Parts of the Industry for a discussion of the advantages and disadvantages of various forms of regulation, including rate-of-return regulation.

ERM GOVERNMENT OF THE HKSAR

6

1.3.15 In the short term, increased use of the CLP-GPHC interconnection could, for example, take the form of explicit recognition of the Southern China system for the purposes of determining reserve plant requirements as well as purchase of surplus electricity.(1) In the longer term it would involve exploring the possibilities for introducing competition. Such consideration of competition is discussed in Section 3 of this Report but the opportunity for making increased use of the large, existing CLP-GPHC interconnection for either meeting reserve requirements or for purchase of surplus capacity was not a part of the brief for this Study. It should be borne in mind that the calculations underlying the reserve capacity requirements used to determine the economic benefits of interconnection assume that CLP does not receive any capacity support from Southern China and that sufficient reserve plant must be constructed within Hong Kong(2) to meet Hong Kong’s generation level reliability requirements.

Utility Planning Horizon and Study Time Frame

1.3.16 The utilities currently plan generation and transmission resources to meet expected customer demand for electricity for a period some ten to fifteen years into the future. This planning horizon is typical of most electricity utilities around the world. The options available, particularly in the earlier part of the planning period are developed in detail by the utility planners. Options for the later years are more general or “conceptual.”

1.3.17 As indicated above, the Study brief requires consideration of three time periods — to 2008, to 2018 and to 2028. Table 1.3.a shows the accuracy of the data and information on each of the three main areas considered in this Study — interconnection, competition and the development of the Southern China electricity sector — for each of the three time periods. The quantitative analysis on interconnection in Section 2 and the qualitative analysis of competition in Section 3, should be read bearing in mind the degree of accuracy in the input data and information about the future for each of the three time periods.

1(?) Refer to the discussion of the projected surpluses in Southern China in Section 4.

2(?) The installed capacity considered in the calculation includes 70% of the Daya Bay nuclear plant and 50% of the 1 200 MW Guangdong pumped storage, consistent with CLP’s contractual entitlements.

ERM GOVERNMENT OF THE HKSAR

7

Table 1.3.a Accuracy of Data and Information in Each Period of the Study Time-frame

Time Period Information on generation and interconnection RESOURCE OPTIONS

Development of COMPETITION

Physical and institutional development of Southern CHINA electricity sector

to 2008 detailed, including sites and quite detailed engineering cost estimates

options for initial steps possible but limited by practical considerations

reasonable predictions can be made

to 2018 generic and more approximate, particularly towards the end of the period

options for reform quite open if planned in advance

predictions are quite uncertain

to 2028 must be considered very approximate

options for reform very open if planned well in advance

predictions are extremely uncertain

Interconnection

Technical and Economic Analysis of Increased HEC-CLP Interconnection

1.3.18 An assessment of the overall economic benefits is necessary to calculate the potential consumer benefits from increased interconnection between the Hong Kong utilities. To achieve this, it is logically necessary to calculate the economics of alternative resource options from an overall least-cost system planning approach.

1.3.19 Sources of economic benefits include: reducing the overall reserve plant required in the interconnected

system, such that the additional capital cost of increased interconnection is more than offset by the savings in generation capital cost;

increasing the degree of flexibility available for selecting future plant sites; and

benefits whereby greater flexibility of generation plant dispatch can allow overall lower cost system operation.

1.3.20 The first step in such an exercise is to identify the alternative resource options available to meet expected (or “forecast”) customer demand for electricity with the desired level of reliability.

ERM GOVERNMENT OF THE HKSAR

8

(1) This includes integrated consideration of generation and transmission (in this case specifically increased use of HEC-CLP interconnection) resource options. This allows comparison between several scenarios. Each scenario in this Study is based on common information on projected customer peak demand and energy consumption in each utility area for the Study period. Under this approach, the potential economic benefits of each particular investment scenario is determined by comparison with the base case investment scenario. The total benefits of the overall least-cost option are then simply the difference between the present value of its cost stream and that of the base case.

Resource Options Considered in the Scenarios

1.3.21 The specific near-term generation resource options developed by the utilities’ planners were used in this Study but the brief for this Study required analysis up to 2028 — which extends well beyond the utilities’ planning horizon — so additional options had to be sketched out for the later years required by the brief.

1.3.22 The generation resource options considered for the near term included: the last two single shaft 312.5 MW combined cycle gas turbine

(CCGT) units at the Black Point power station (for which the civil works and transmission connections are already in place) fuelled by the existing piped natural gas supply;(2) and

six single shaft combined cycle gas turbine (CCGT) units of approximately 300 MW at the proposed reclaimed land extension to the Lamma power station fuelled by natural gas supplied by a proposed pipeline from a proposed LNG terminal in southern China.

1.3.23 For the period after this, the conceptual plans of one utility include some small gas turbine units to meet peak load requirements and some 660 MW conventional coal-fired units. This Study however, was based on the following generation configurations to be the scenario for this period: several small gas turbine units on available space at the Black

Point site; and

1(?) In comparing resource options and the costs of various scenarios, it is important that the reliability level specified be the same between the various cases, to enable the economic feasibility of interconnection to be isolated from the effects of changed reliability levels. This Study endeavoured to specify reliability levels the same as those currently applied by the utility planners in Hong Kong to model the various scenarios. However, there are some differences between the two utilities with respect to reliability criteria and the analytical methodology currently applied by system planners. There was a logical necessity to harmonise reliability criteria to the extent possible for the purposes of the economic feasibility analysis in this Study. This Study notes that a review of system planning and reliability criteria may be appropriate in Hong Kong, although the results of such a review would be very unlikely to affect the overall conclusions of this Study. 2(?) CLP has contractual commitments, based on agreements with Government, to purchase these two units.

ERM GOVERNMENT OF THE HKSAR

9

future generic combined cycle units,(1) with large 680 MW triple-shaft CCGTs instead of coal-fired steam plant, in line with the current Government thinking that there will be a move away from coal-fired electricity generation in favour of lower emission gas-fired plant for environmental reasons.

Financial and Tariff Analysis of Each Scenario

1.3.24 The manner in which the overall economic benefits flow through to consumers depends on the way that revenue requirements (including profits) and tariffs are determined. Hong Kong electricity revenues and tariffs are determined by the Scheme of Control. The investment schedules of each interconnection/generation scenario for each electricity company from the economic analysis can therefore be used together with the formulae in the Scheme of Control accounting system to calculate the aggregate effect on customer bills and the average effect on customer tariffs of each scenario relative to the base case.

Considerations of Ownership Structure

1.3.25 The technical and economic analysis of least cost interconnection/generation scenarios is done from an overall integrated system or total resource point of view. Such consideration is quite distinct from questions of the division of asset ownership between areas within the interconnected electricity supply system. Nevertheless, such considerations are important, and were considered by this Study. Considerations related to ownership include: the effect on the management and control of each utility system; each individual company’s ability to serve reliably the load of

customers within its supply area and the extent to which it needs to rely on inter-area generation capacity support and energy supply from a separate company in a neighbouring area; and

the effect of least cost investment options on the commercial and financial position of each individual company in the interconnected system.

1.3.26 These considerations are discussed in this report in the context of the extent to which the existing Scheme of Control regulatory framework and the Interconnection Agreement would require adjustments or modifications to those agreements to permit solutions to be found to these issues.

1(?) The first 680 MW unit could be accommodated within available site space, but subsequent units would require formation of additional space at the Black Point site or creation of a new site. Sufficient transmission capacity exists at Black Point to accommodate such additional units up to and including the first 680 MW combined cycle gas turbine. Units beyond that would require construction of additional transmission capacity.

ERM GOVERNMENT OF THE HKSAR

10

Competition

1.3.27 Examination of the potential for the future introduction of electricity sector competition allows the wider implications of making increased use of the HEC-CLP interconnection to be considered, including future development of the industry, and the future relationship between the electricity industry in Hong Kong and the rapidly developing Southern China system, with which Hong Kong is already strongly interconnected.

1.3.28 After the technical and economic analysis of interconnection from the perspective of the overall Hong Kong system, the Study report focuses on the potential for introduction of competition. It: examines the local and wider context; describes alternative electricity market structures; evaluates in detail the most appropriate options for Hong Kong,

indicating a set of options and possible time-frames for transition from the existing structure.

1.4 Structure of this Document

1.4.1 This document is organised into Sections as follows.

1.4.2 Section 2: Feasibility of Increased Interconnection of Electricity Systems in Hong Kong – including: general considerations associated with electricity interconnection; methodology and approach adopted to determine the technical

and economic feasibility of increased interconnection between HEC and CLP;

an analysis of the technical feasibility of increased HEC-CLP interconnection; and

an analysis of the economic feasibility of increased HEC-CLP interconnection.

1.4.3 Section 3: Feasibility of the Introduction of Electricity Sector Competition in Hong Kong – including: local and wider context for electricity sector competition; evaluation of four market structures applied to Hong Kong; and detailed consideration of the most appropriate options for

Hong Kong.

1.4.4 Section 4: Developments in the Southern China Power Markets – including: Guangdong and Southern China electricity sector; process of restructuring; and implications for Hong Kong.

ERM GOVERNMENT OF THE HKSAR

11

1.5 Key Terms

1.5.1 To ensure clarity and avoid confusion when describing the various options and case studies analysed, a description of terms used in the report is detailed in the glossary at the beginning of the document. Specific terms used in the tasks and modelling are included in Table 1.5.a.

Table 1.5.a Key Terms Used in this Study

Topic Key Term Description

Planning and Operation of Interconnection

Joint Planning Planning generation and transmission taking into account interconnection options in order to achieve least-cost expansion of the system as a whole.

Firm Capacity Joint planning would require that the interconnection be able to provide “firm” inter-area generation capacity support as and when it is needed. The use of the term “firm capacity” in this report refers to the technical capability of the interconnection itself. It does not mean that generation capacity in one area is set aside or reserved for the sole or preferential use of the other area.

Joint Dispatch Operating or “dispatching” generation plants in separate areas on a joint basis to realise any available synergy and operational economies to achieve the least cost generation production cost.

Firm Power Joint dispatch of plant would require that the interconnection be able to support the regular, reliable transfer of energy. The use of the term “firm power” in this report refers to the technical capability of the interconnection itself. It does not necessarily refer to contractual arrangements between utilities for the supply of energy, although neither does it preclude such arrangements being put in place.

Technical and Economic Analysis of Interconnection

4 Interconnection Cases

The four interconnection cases were developed as generation/interconnection scenarios to examine in detail the potential for increased use of interconnection to benefit consumers.

Financial and Tariff Analysis of Interconnection Cases

Financial Model

Taking the recommendations from Task 1, the Financial and Tariff Analysis provides an indication of the average effect on electricity consumer tariffs of each of the interconnection cases under the financial arrangements of the existing Scheme of Control.

Competition 4 Market Models each with several variants

A wider analysis of options to introduce competition into the Hong Kong electricity market.

ERM GOVERNMENT OF THE HKSAR

12

2 FEASIBILITY OF INCREASED INTERCONNECTION OF ELECTRICITY SYSTEMS IN HONG KONG

2.1 Introduction

2.1.1 World-wide there is a trend towards increasing interconnection between utility systems. This trend is in response to customer demand for delivery of competitively priced electricity to their area as well as helping to facilitate the introduction of competition in the electricity industry. The decision to introduce competition is often based on a general conviction among policy makers that competitive markets tend to deliver the best solutions for customers, offer a means of ensuring that the optimum amount of generating capacity is provided with minimal or no Government intervention and provide a framework that naturally encourages economic exchange of energy and sharing of capacity requirements between systems. In implementing decisions on interconnection, utilities look for associated benefits in reducing generating capacity, providing emergency support, improving security of supply, reducing fuel costs, gaining economies of scale and enhancing the possibilities for increased competition in the longer term, where their market position may lend an advantage. This section focuses on the technical and economic aspects of the actual interconnection itself between the HEC and CLP systems.

This Section

2.1.2 The interconnection of electricity systems is important in helping to ensure security of supply, the provision of economic benefits to consumers, the facilitation of possible competition in future and many other benefits. Given these considerations, this Section discusses: general considerations associated with interconnection; the methodology and approach adopted to assess the technical

feasibility of increased HEC-CLP interconnection; the technical feasibility of increased interconnection between

HEC and CLP; and the economic feasibility of increased interconnection between

HEC and CLP, including an assessment of the overall economic benefit to Hong Kong and the consequent effect on average tariffs and total consumer bills (or conversely on utility revenues) under the current Scheme of Control Agreements between Government and the utilities, of the economic benefits from increased interconnection.

ERM GOVERNMENT OF THE HKSAR

13

2.2 General Considerations Associated with Electricity Interconnection

What is Interconnection?

2.2.1 Interconnection is simply the linking of two electricity systems to tie together the major electric system facilities, generation resources and customer demand centres of the previously separate systems.

2.2.2 The systems of the two electricity companies in Hong Kong — HEC and CLP — are already interconnected by a submarine cable link of relatively limited capacity. Because the HEC system is on an island, any future upgrades to the interconnection capacity would also need to be by submarine cables.

2.2.3 Interconnecting transmission systems is one of the principal ways of achieving a reliable electricity supply. Like all transmission systems, interconnected systems must be planned, designed and constructed to operate reliably within thermal, voltage and stability limits, while: delivering electric power to areas of customer demand; providing flexibility for changing system conditions; allowing for reduced reserve costs; allowing the amount of installed generating capacity required to

meet the specified reliability level to be lower than would otherwise be the case; and

providing for economic exchange of electric power among systems.

Potential Benefits from Interconnection

2.2.4 Realising potential economic benefits from interconnection requires that a system be planned or operated or both planned and operated to take maximum advantage of that interconnection. The former is referred to in this report as Joint Planning and the latter as Joint Dispatch. The maximum technical and economic benefits of interconnection, potentially available from optimising the generation and transmission configuration of multiple areas that make up an interconnected system and from operating or “dispatching” the generation plant in the most economic or least cost way can be determined independently of the ownership structure of the individual utilities within the interconnected system.(1) The implications of the particular commercial realities of a given system — including the ownership structure and regulatory framework — must be considered in addition to the technical and economic analysis of the potential benefits of interconnection. This feasibility

1(?) This feasibility Study focuses primarily on the interconnected HEC-CLP system — there may be additional potential economic benefits available in future from taking full advantage of the interconnection with the Southern China

ERM GOVERNMENT OF THE HKSAR

14

Study does so, taking into account technical, economic, consumer and utility commercial considerations in turn.

Modes of Operation of Interconnection

2.2.5 The approach to planning and/or operation of interconnected systems requires consideration of the alternative modes of operation of the interconnection between those systems. The benefits available from interconnection depend on these modes of operation, and the extent to which they are reflected in system planning.

2.2.6 The main modes of interconnection operation are referred to in this report as: Firm Capacity, necessary for Joint Planning; Firm Power; necessary for Joint Dispatch; and the combination of Firm Capacity and Firm Power, necessary for

the combination of Joint Planning and Joint Dispatch. The combination of Firm Capacity and Firm Power is commonly employed internationally.

2.2.7 These modes represent two basic characteristics of electricity systems whereby demand fluctuates continuously, but supply and demand must at all times be equal. The two characteristics are: capacity: the need to have sufficient generation capacity to meet

customer demand at its maximum (peak demand) and a transmission system of sufficient capacity to meet that demand as it is distributed throughout the network; and

energy (referred to here as “power”): the requirement to supply energy.

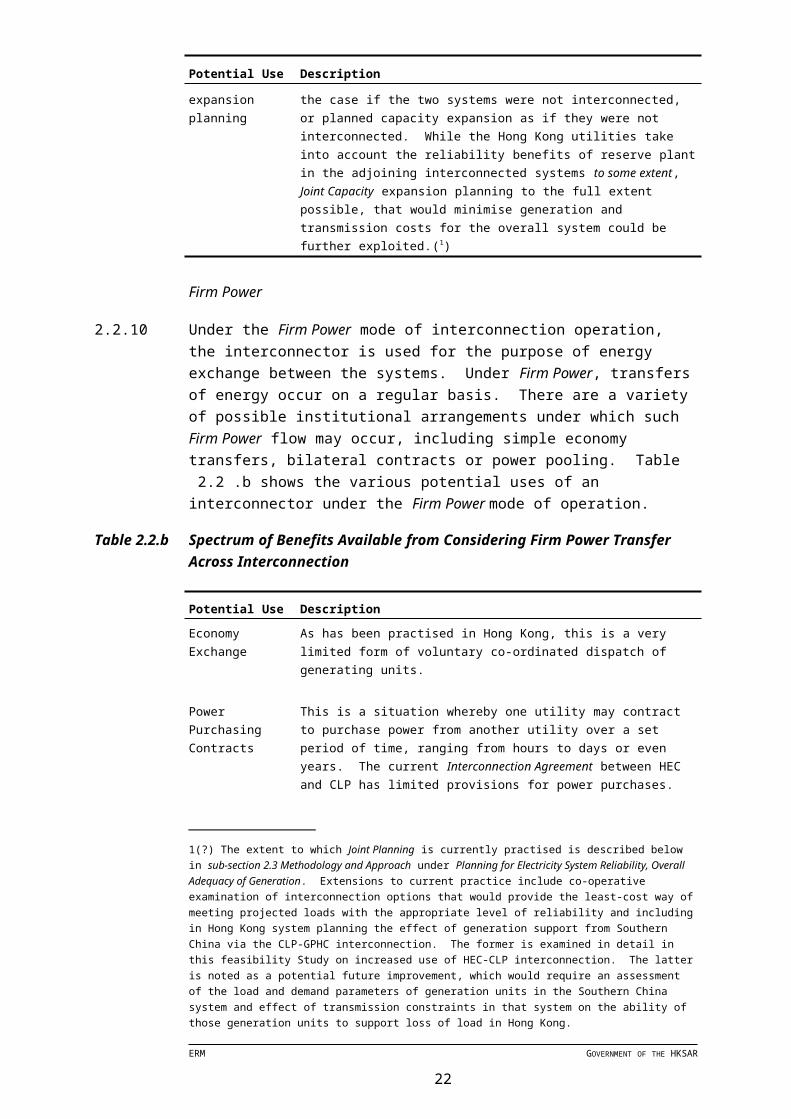

2.2.8 Interconnection between two or more separate systems allows greater flexibility in the planning of additional generating units, reduced reserve margins, and the other benefits discussed later in this section, by utilising the interconnector under ‘Firm Capacity’. The situation may arise where no power at all is passed across the interconnector and the benefits are from the rationalisation of investment in new generating units. In such cases, benefits usually arise from reduced reserve margins, reduced spinning reserve, emergency support and security of supply (these issues are further described below and represented in Figure 2.2.a). However, Firm Capacity is not defined as one type of activity, rather it is a series of activities, some of which are already practised here in Hong Kong. See Table 2.2.a for a description of the spectrum of activities that would be considered under Firm Capacity (all issues summarised in the table are discussed in full later).

ERM GOVERNMENT OF THE HKSAR

15

Firm Capacity

2.2.9 Under the Firm Capacity mode of interconnection operation, the interconnector is used to provide mutual capacity support between the interconnected utilities. Flows of energy are very small, because they occur only for relatively short periods on those infrequent occasions when backup support is needed by one or other utility. Table 2.2.a shows the various potential uses of an interconnector under the Firm Capacity mode of operation.

Table 2.2.a Spectrum of Benefits available from Considering Firm Capacity of Interconnection

Potential Use Description

Increased Level I (Generation) and Level II (Transmission) Reliability

Increasing the level of interconnection within and between electricity systems increases their reliability, as it increases the number of possible combinations of generation sources and transmission network paths that can be used to supply load, which reduces the probability that load cannot be served in the event of a fault at any particular point in the system. Hong Kong already experiences some of these benefits to the extent allowed by the capacity of the existing interconnection.

Sharing of Spinning Reserve and Load-Frequency Dependence

The next step is to share spinning reserve, the sum of the spare capacity in spinning generation units available for instantaneous support in the event of a generator being “tripped” (unexpectedly forced out of service). Interconnection allows spinning reserve to be shared among the interconnected parts of the wider system and also provides advantages from the frequency-dependence of load. Both of these types of benefit are currently captured in Hong Kong, where spinning reserve is currently shared between HEC, CLP and GPHC on the wider interconnected system and where the frequency-dependence of load across the wider interconnected system means that the maximum spinning reserve that needs to be carried is just 75% of the largest unit on the wider interconnected system. This consideration and the calculation that shows how the 75% is arrived at are explained later in this Section.

Co-ordinated or joint generating capacity expansion planning

By interconnecting with a neighbouring utility, installed reserve generating capacity can be shared such that less generation is required in total to meet the desired generation reliability level than would be the case if the two systems were not interconnected, or planned capacity expansion as if they were not interconnected. While the Hong Kong utilities take into account the reliability benefits of reserve plant in the adjoining interconnected systems to some extent, Joint Capacity expansion planning to the full extent possible, that would minimise generation and transmission costs for the overall system could be further exploited.(1)

1(?) The extent to which Joint Planning is currently practised is described below in sub-section 2.3 Methodology and Approach under Planning for Electricity System Reliability, Overall Adequacy of Generation. Extensions to current practice include co-operative examination of interconnection options that would provide the least-cost way of meeting projected loads with the appropriate level of reliability and including in Hong Kong system planning the effect of generation support from Southern China via the CLP-GPHC interconnection. The former is examined in detail in this feasibility Study on increased use of HEC-CLP interconnection. The latter is noted as a potential future improvement, which would require an assessment of the

ERM GOVERNMENT OF THE HKSAR

16

Firm Power

2.2.10 Under the Firm Power mode of interconnection operation, the interconnector is used for the purpose of energy exchange between the systems. Under Firm Power, transfers of energy occur on a regular basis. There are a variety of possible institutional arrangements under which such Firm Power flow may occur, including simple economy transfers, bilateral contracts or power pooling. Table 2.2.b shows the various potential uses of an interconnector under the Firm Power mode of operation.

Table 2.2.bSpectrum of Benefits Available from Considering Firm Power Transfer Across Interconnection

Potential Use DescriptionEconomy Exchange

As has been practised in Hong Kong, this is a very limited form of voluntary co-ordinated dispatch of generating units.

Power Purchasing Contracts

This is a situation whereby one utility may contract to purchase power from another utility over a set period of time, ranging from hours to days or even years. The current Interconnection Agreement between HEC and CLP has limited provisions for power purchases.

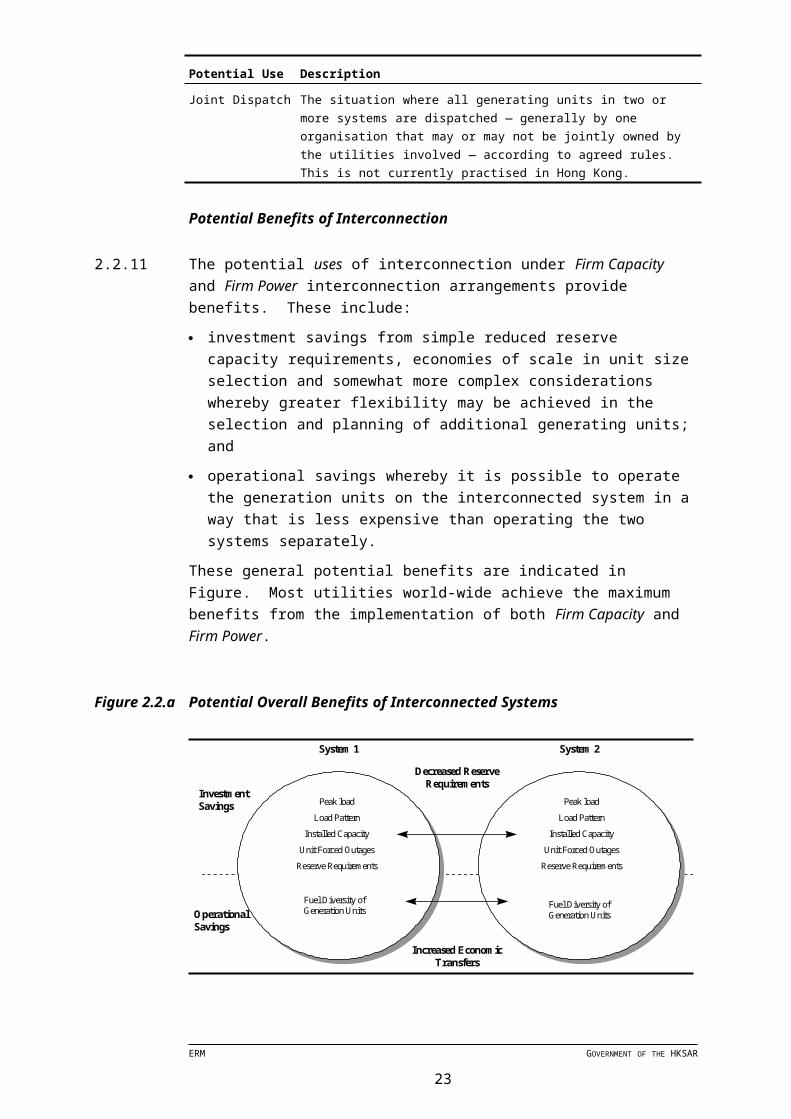

Joint Dispatch The situation where all generating units in two or more systems are dispatched — generally by one organisation that may or may not be jointly owned by the utilities involved — according to agreed rules. This is not currently practised in Hong Kong.

Potential Benefits of Interconnection

2.2.11 The potential uses of interconnection under Firm Capacity and Firm Power interconnection arrangements provide benefits. These include: investment savings from simple reduced reserve capacity

requirements, economies of scale in unit size selection and somewhat more complex considerations whereby greater flexibility may be achieved in the selection and planning of additional generating units; and

operational savings whereby it is possible to operate the generation units on the interconnected system in a way that is less expensive than operating the two systems separately.

These general potential benefits are indicated in Figure 2.2.a. Most utilities world-wide achieve the maximum benefits from the implementation of both Firm Capacity and Firm Power.

load and demand parameters of generation units in the Southern China system and effect of transmission constraints in that system on the ability of those generation units to support loss of load in Hong Kong.

ERM GOVERNMENT OF THE HKSAR

17

Figure 2.2.a Potential Overall Benefits of Interconnected Systems

OperationalSavings

InvestmentSavings

System 1 System 2

Peak load

Load Pattern

Installed Capacity

Unit Forced Outages

Reserve Requirements

Fuel Diversity ofGeneration Units

Peak load

Load Pattern

Installed Capacity

Unit Forced Outages

Reserve Requirements

Fuel Diversity ofGeneration Units

Increased EconomicTransfers

Decreased ReserveRequirements

2.3 Methodology and Approach

General Approach Adopted to Assess Potential Benefits

2.3.1 The Consultants were asked to undertake a feasibility-level study of the benefits and costs of increased interconnection in Hong Kong. This is not a generation expansion planning exercise as such. However, the only way to assess the economic benefits of increased interconnection is to develop scenarios that combine generation expansion planning under alternative interconnection cases.

2.3.2 Therefore, the general approach adopted to assess the potential benefits of increased interconnection was broadly as follows: identify alternative interconnection upgrade options; develop a base case generation expansion scenario for the case

with the existing level of interconnection, taking into account a specified set of planning criteria;

assess by inspection of plant installation dates and costs, and systematic steps, the most appropriate installation dates of each of the alternative interconnection upgrade options identified;

define the best candidates among these as cases; develop generation expansion plans for each interconnection case

to form an interconnection/generation scenario, taking into account the specified set of planning criteria;

use the capital expenditures over time on each of the transmission and generation installations to calculate discounted net present values for each scenario;

assess the differences in net present value between each alternative scenario and the base case scenario for the Firm Capacity economic analysis.

ERM GOVERNMENT OF THE HKSAR

18

Both this general approach and the detailed analytical method adopted ensure that reliability for each individual area (HEC and CLP) would be equivalent for the generation expansion plans under each of the various generation/interconnection scenarios, by applying a common and consistent set of reliability criteria. Reliability considerations in general and the particular reliability criteria and their application for this Study are discussed below.

Planning for Electricity System Reliability

2.3.3 Electricity is supplied to customers by a system that extends from the generation plant through a high voltage transmission network and finally a low voltage distribution network to the customers’ premises. An interruption anywhere in this chain of supply to a particular customer or group of customers will result in the loss of supply or “loss of load” for those customers.

2.3.4 Clearly, problems further up the network have the potential to affect large numbers of customers unless sufficient redundancy is built into the system. For this reason, electricity system reliability planning needs to consider overall Level I (generation) and Level II (transmission) reliability to determine the optimum amount and mix of reserve generation, its location within the transmission network, and the optimum configuration and degree of redundancy in the transmission network necessary to ensure the desired level of reliability. Level III (distribution) reliability represents a more detailed level of planning and is less critical from an overall system point of view, as distribution level faults affect only local areas.

Generation (Level I) Reliability

2.3.5 Generation level reliability is assessed by ensuring that for the expected level of hourly load throughout each day, week, month and year of the planning period there will be an adequate amount of generation plant installed overall to allow for: units to be taken out for maintenance; sudden and unpredictable unavailability of generation units; and the ability to cope with unpredicted peak loads. Maintenance is performed at the low demand times of the year, and is known as “planned outage,” expressed in terms of a planned outage rate POR, in percentage of time or weeks per year. Sudden loss of units — due to units being “tripped” by the automatic protection equipment that is built into the generation and transmission system to ensure that it operates safely — is known as “forced outage” and is expressed in terms of a forced outage rate or FOR, in percentage of time.

2.3.6 Two tests are applied to assess the required levels of installed generation:

ERM GOVERNMENT OF THE HKSAR

19

a probabilistic test, that assesses the generation units not on maintenance at each time of the year against the expected load at each time of year, then finds the combinations of plant outages that would result in available generation being less than the load in each time period and uses the FOR (probability) values for each plant to calculate the overall “loss of load probability” or LOLP, which is then compared to a specified LOLP criterion; and

an operational test, that checks whether for each year of the planning period there would be sufficient installed capacity to allow the peak load to be served under a specified contingency.

Overall Adequacy of Generation

2.3.7 The specified LOLP or “primary” criterion currently used by HEC for system planning is 20 hours per year. The specified LOLP or “primary” criterion currently used by CLP for system planning is 0.5 days/year.

2.3.8 Before construction of the interconnector, HEC applied an LOLP criterion of 2.5 hours/year. After construction of the existing interconnection, HEC continued to model their system as an isolated system, but relaxed their LOLP criterion to 20 hours/year, and to take its existence into account continued to model their system as an isolated system. HEC calculated that the result of this approach would be approximately the same as continuing to use a 2.5 hours/year LOLP criterion and conducting a two-area LOLP analysis of the interconnected HEC-CLP system.(1) However, the approximation made in the adjustment to the criterion allows the continued application of a single-area LOLP approach, rather than requiring application of the more complex two-area LOLP approach.

2.3.9 CLP apply their 0.5 days/year LOLP criterion to their system, taking into account the existing interconnection with HEC; including their share of Daya Bay nuclear plant capacity and Guangdong pumped storage; but excluding the interconnection of the CLP network with the wider Southern China grid. The existence of the interconnection with the Southern China grid means that the level of generation reliability experienced by the CLP system is in fact higher (lower LOLP) than the calculated level. In other words, using 0.5 days/year and not taking account of the interconnection with the Southern China grid would be equivalent to using a lower LOLP criterion and explicitly taking account of support via the interconnection with the much larger Southern China system.

Allowance for Generation Contingencies

2.3.10 As well as having an adequate total level of installed generation capacity to keep the probability of loss of load within the specified

1(?) Note that single-area to two-area equivalent LOLP values would change as the system changes, so the value used is quite approximate. This Study adopted a full two-area LOLP approach, which obviates the need for making a single-area equivalence approximation.

ERM GOVERNMENT OF THE HKSAR

20

limit, the generation system must be able to continue to serve load in the event of specified contingencies. It is only necessary to specify the worst case generation contingency, which is represented by the loss of the largest unit or units. Once this contingency can be met, all other smaller generation contingencies will automatically be met.

2.3.11 The specified generation level operational contingency or “secondary criteria” currently applied differ between the two utilities. They are: HEC Reserve Capacity > Largest Unit + Hot Standby(1) CLP Installed Capacity > Max Demand + 2 x Largest Unit +

Spinning Reserve(2)

Transmission (Level II) Reliability

2.3.12 Transmission level reliability analysis assesses the reliability of the energy transport system. It requires consideration of the distribution of loads throughout the network (substation loads), rather than simply the total system load as used in generation level reliability assessment and planning. It applies methods which examine the ability of the system to remain stable and serve load given the occurrence of faults or “contingencies” in the network. If, for example, a single contingency or N-1 rule is applied, then the failure of each single transmission network element is examined in turn to determine whether there is sufficient redundant capacity in the network to continue to serve load under all planning contingencies, or whether additions or modifications to the network configuration are required. More precise methods also require consideration of all relevant system stability effects such as transient stability as well as system oscillations.

Application of Reliability Analysis for this Feasibility Study

Generation

2.3.13 A consistent and systematic approach to generation planning criteria was required for this study across all scenarios examined to allow the economic benefits of deferral of capital expenditure of plant due to the interconnector to be clearly identified.

2.3.14 The following approach to generation planning criteria was applied for this feasibility study across all scenarios examined to allow the

1(?) Hot Standby is the commitment to provide further emergency support after all spinning reserve is utilised. The current value for this is 180 MW in the HEC system. 2(?) Not all generating plants in a power system are operating at their full output capacity all of the time. Spinning reserve is the sum across the system of reserve capacity (rated output capacity minus current output) in units that are “spinning” or currently generating electricity. Spinning reserve is shared between HEC, CLP and GPHC. CLP’s commitment to the system is currently 240 MW.

ERM GOVERNMENT OF THE HKSAR

21