Embed Size (px)

Citation preview

1

Macroeconomics for small and developing countries

René A. Hernández

DDPE/ECLAC

July 2007

2

Figure 1.1 : In 1997 developing countries accounted for 32% of world output.

132 of the 183 countries are developing countries. Although most of production takes place in the industrial

countries, country-specific macroeconomic policy formulation is carried out in a developing-country context.

Developing countries behave similarly to industrial countries, but operate in a different environment.

Standard analytical tools of modern macroeconomics are relevant to developing countries.

But different models are needed to analyze. Purposes to which the models have been applied also

distinguish macroeconomics in developing countries.

Introduction

3

Industrial countries51.9%

Developing countries31.7%

Countries in transition4.8%

China11.6%

Figure 1.1Distribution of World Output, 1997

(In percent of world GDP)

Source: International Monetary Fund.Notes: GDP shares are based on the purchasing power parity (PPP) valuation of country GDPs. The category "countries in transition" includes Mongolia and countries of the former Soviet Union and central Europe.

4

Monetarism, Structuralism, Neostructuralism and Developing Nations.

Economic Structure and Macroeconomics. Some Special Topics.

Introduction

5

Monetarism, Structuralism, Neostructuralism and Developing

Nations

6

The debate Debate on relevance of industrial-country

macroeconomic analysis to developing nations.

“Monetarist” or “orthodox” versus “structuralist”.

7

Long-run growth in developing countries is hampered by dirigiste policies that distort the allocation of resources.

Prescription: giving full scope to market mechanisms via free trade and noninterventionist domestic policies.

In the short run, high inflation and balance-of-payments deficits reflect excessive money growth fueled by large fiscal deficits.

Cure: tight fiscal policy and “getting prices right”, by devaluing and raising domestic interest rates.

Policies based on the orthodox view have been promoted by international financial institutions.

Orthodox view

8

Primary-exporting countries would face deteriorating terms of trade relative to the manufactured goods-exporting industrial-nation.

Reason: Lower income elasticities of demand for raw materials than for industrial goods.

Policy intervention was required to change the structure of production in the periphery.

Industrialization should be promoted by protecting “infant industry” against competition through:

use of trade barriers and foreign exchange controls; providing special advantages to the industrial sector.

This “import substitution” strategy was adopted in the immediate postwar period.

Early Structuralist School

9

Turned their attention to short-run macroeconomic stabilization.

The analytical framework is influenced by the keynesian and postkeynesian schools and focuses on the design and implementation of strategies and economic policies.

Best-known proponent: Lance Taylor. Taylor (1990) identifies “new structuralist” view.

many agents possess significant market power; macroeconomic causality in developing countries tends to

run from “injections” to “leakages”; money is often endogenous; structure of the financial system can affect macroeconomic

outcomes; imported intermediate and capital goods, complementarity

between public and private investment are empirically important.

“New structuralist” view (NSV)

10

New structuralists question orthodox short-run prescriptions.

Source of inflation: slow relative productivity growth in agriculture; administered prices in industry, together with wage

indexation. Monetary policy is passive in the face of these inflationary

forces. Combining devaluation with tight fiscal and monetary

policies will result in stagflation in the short run. Reason: Roles of working capital and imported inputs, and

substitution possibilities are more limited than assumed.

“New structuralist” view

11

Alternative new structuralist policy prescription: greater element of gradualism; direct intervention; emphasis on the medium-term resolution of

structural problems. Macroeconomic reality in the developing world

combines features of both. ECLAC’s “productive transformation and equity” is

an expression of the NSV

“New structuralist” view

12

Economic Structure and Macroeconomics

13

Openness to Trade in Commodities and Assets. Exchange Rate Management. Domestic Financial Markets. The Government Budget. Aggregate Supply and the Labor Market. Stability of Policy Regimes. Macroeconomic Volatility.

14

Openness to Trade in Commodities and Assets

15

Developing economies tend to be more open to trade in goods and services

than are the major industrial countries

Openness: trade share (sum of the shares of exports and imports) in GDP.

First panel of Figure 1.2: developing nations tend to be more open than the major industrial countries.

Mean value of the trade share is 45%, compared with about 25% in the G-7 countries.

Openness limits at the applicability of the closed-economy textbook industrial-country model to the developing-country context.

16

Figure 1.2Trade Indicators

(In percent)

Algeria

BangladeshBarbados

Bolivia

BrazilChile

ColombiaCosta Rica

Côte d'IvoireEcuador

EgyptGabon

GhanaHaitiIndia

Indonesia

Israel

Jamaica

Kenya

KoreaMalaysia

Mauritania

MexicoMorocco

NigeriaPakistan

PhilippinesSenegal

Singapore

Sri Lanka

Syria

ThailandTunisia

Venezuela

Zaire

0 50 100 150 200

Trade (% of GDP)

1995

Algeria

BangladeshBarbados

Bolivia

BrazilChile

ColombiaCosta Rica

Côte d'IvoireEcuador

EgyptGabon

GhanaHaitiIndia

Indonesia

Israel

Jamaica

Kenya

KoreaMalaysia

Mauritania

MexicoMorocco

NigeriaPakistan

PhilippinesSenegal

Singapore

Sri Lanka

Syria

ThailandTunisia

Venezuela

Zaire

0 20 40 60 80 100

Export Share ofPrimary Commodities

(in percent), 1991

Algeria

BangladeshBarbados

Bolivia

BrazilChile

ColombiaCosta Rica

Côte d'IvoireEcuador

EgyptGabon

GhanaHaitiIndia

Indonesia

Israel

Jamaica

Kenya

KoreaMalaysia

Mauritania

MexicoMorocco

NigeriaPakistan

PhilippinesSenegal

Singapore

Sri Lanka

Syria

ThailandTunisia

Venezuela

Zaire

0 20 40 60 80 100

Share of Exports toIndustrial Countries(in percent), 1991

Source: Montiel (1993), World Bank, and International Monetary Fund.

17

Exogeneity of the terms of trade is suggested both by their small share in the world economy; by the composition of their exports.

In 1990 developing nations accounted for about one quarter of world exports and imports.

In 1991 over half of the exports of low- and middle-income countries consisted of primary commodities.

Second panel of Figure 1.2: share of primary commodities in the exports of a selected group of developing countries.

Third panel: two-thirds of the exports of the countries went to industrial countries.

Developing countries typically have little control over the prices of the goods they

export and import

18

Very few developing countries account for a significant portion of the world market.

Only sixteen developing countries account for as much as 10% of the world market.

These countries have little individual influence over the prices at which they buy and sell (Goldstein, 1986).

Exogenous terms of trade questions the usefulness of the open-economy model for developing nations.

Suitable models are Salter-Swan “dependent economy” model or three-good model consisting of exportables,

importables, and nontraded goods.

19

Such production structure permits a distinction between the exogenous terms of trade and an endogenous real exchange rate.

Importance of primary-commodity exports with exogenously determined prices: important source of macroeconomic instability.

Figure 1.3: prices of primary commodities tend to fluctuate sharply.

Top panel of Figure 1.4: several episodes of drastic changes in the terms of trade for developing countries.

Episodes are dominated by changes in oil prices. Bottom panel in Figure 1.4: nonfuel commodities have

undergone sharp fluctuations in price during the 1970s and 1980s.

20

Source: International Monetary Fund.

Figure 1.3aWorld Commodity Prices

(In U.S. cents per pound. Quotation in New York, unless otherwise indicated)

1970q1 1976q1 1982q1 1988q1 1994q10

50

100

150

200

250

300

350 Cocoa beans

1970q1 1976q1 1982q1 1988q1 1994q10

50

100

150

200

250

300

350 Coffee

21

Source: International Monetary Fund.

Figure 1.3bWorld Commodity Prices

(In U.S. cents per pound. Quotation in New York, unless otherwise indicated)

1970q1 1976q1 1982q1 1988q1 1994q130

50

70

90

110

130 Copper (London)

1970q1 1976q1 1982q1 1988q1 1994q120

40

60

80

100

120

140

160 Cotton (U.S. average price)

22

Source: International Monetary Fund.

Figure 1.3cWorld Commodity Prices

(In U.S. cents per pound. Quotation in New York, unless otherwise indicated)

1970q1 1976q1 1982q1 1988q1 1994q10

50

100

150

200 Rubber

1970q1 1976q1 1982q1 1988q1 1994q10

50

100

150

200

250 Sugar (U.S. import price)

23

Source: International Monetary Fund.

Figure 1.4aDeveloping Countries: Terms of Trade and Nonfuel Commodity Prices

(Annual change, in percent)

1971 1976 1981 1986 1991 1996

-10

0

10

20

30

40

50

0

-10

Terms of trade

24

Source: International Monetary Fund.

Figure 1.4bDeveloping Countries: Terms of Trade and Nonfuel Commodity Prices

(Annual change, in percent)

1971 1976 1981 1986 1991 1996

-20

-10

0

10

20

30

40

50

60

0

-20

Nonfuel commodity prices

25

Extent of external trade in assets has been more limited in developing countries, though this situation has recently begun to change

Developing countries have undergone an increase in their degree of integration with the world capital market.

Integration occurred in the context of immature domestic financial systems, limited policy flexibility, and fragile credibility.

This situation has caused to the capital inflow problem.

26

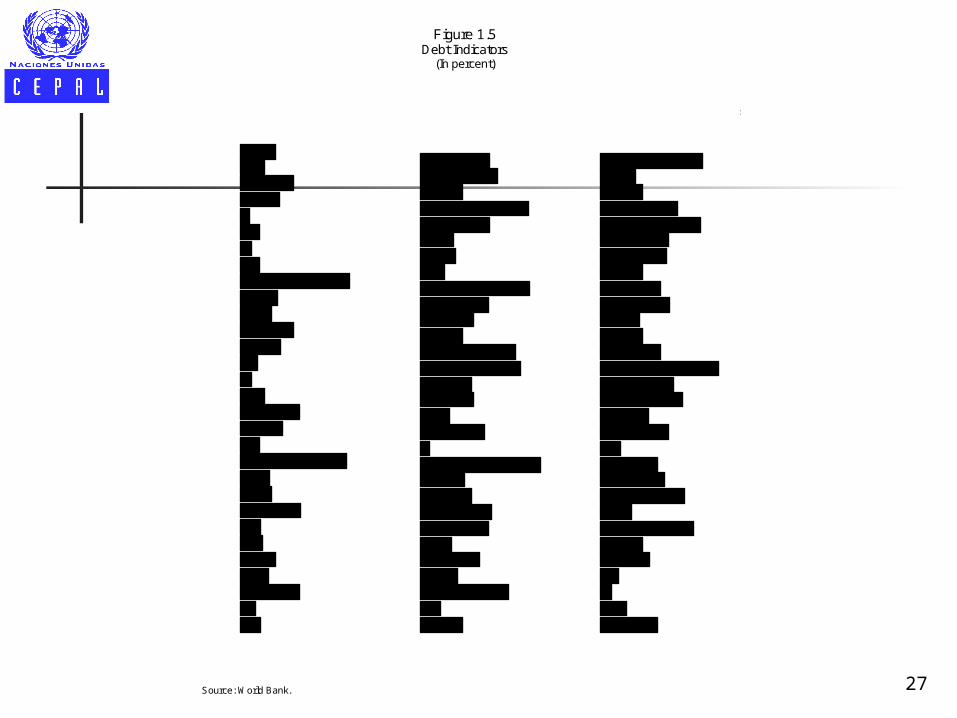

Figure 1.5: set of external-debt indicators. Debt crisis problem emerged because the domestic sector

that held the external assets was not the same as the sector that holds the external liabilities.

In countries that have recently become integrated with international capital markets, external debt has tended to be incurred by the private sector.

Policy challenges involve coping with potential macroeconomic overheating associated with the

sudden arrival of large inflows, vulnerability to macroeconomic volatility induced by

sudden capital flow reversals.

Developing countries are capital importers, and the servicing of external debt is a

central policy issue

27

Figure 1.5Debt Indicators

(In percent)

Algeria

Bangladesh

Barbados

Bolivia

Brazil

Chile

Colombia

Costa Rica

Côte d'Ivoire

Ecuador

Egypt

Gabon

Ghana

Haiti

India

Indonesia

Jamaica

Kenya

Malaysia

Mauritania

Mexico

Morocco

Nigeria

Pakistan

Philippines

Senegal

Sri Lanka

Syria

Thailand

Venezuela

0 75 150 225 300

External Debt (% of GDP) 1995

Algeria

Bangladesh

Barbados

Bolivia

Brazil

Chile

Colombia

Costa Rica

Côte d'Ivoire

Ecuador

Egypt

Gabon

Ghana

Haiti

India

Indonesia

Jamaica

Kenya

Malaysia

Mauritania

Mexico

Morocco

Nigeria

Pakistan

Philippines

Senegal

Sri Lanka

Syria

Thailand

Venezuela

0 125 250 375 500

External Debt(% exports of goods and services)

1995

Algeria

Bangladesh

Barbados

Bolivia

Brazil

Chile

Colombia

Costa Rica

Côte d'Ivoire

Ecuador

Egypt

Gabon

Ghana

Haiti

India

Indonesia

Jamaica

Kenya

Malaysia

Mauritania

Mexico

Morocco

Nigeria

Pakistan

Philippines

Senegal

Sri Lanka

Syria

Thailand

Venezuela

0 10 20 30 40 50

Debt service(% exports of goods and services)

1995

Source: World Bank.

28

Exchange Rate Management

29

Majority of developing countries have neither adopted fully flexible exchange rates

nor joined monetary unions

In developing countries officially determined rates predominate.

Exchange regimes in developing countries have evolved toward greater flexibility since the collapse of the Bretton Woods system in 1973.

This has meant that more frequent adjustments of an officially determined parity rather than the adoption of market-determined exchange rates.

30

Prevalence of official parities implies that issues relating to the macroeconomic consequences of pegging, altering the peg (devaluation), rules for moving the peg

are important in developing countries.

31

Domestic Financial Markets

32

Financial markets in developing nations have been characterized by the prevalence of rudimentary financial institutions and by

“financial repression

Only some of the developing countries have developed large equity markets.

Financial markets are dominated by commercial banks.

So assets available to private savers are limited. Equity markets tend to be dominated by a few

firms and exhibit very low turnover ratios.

33

The commercial banking sector has been heavily regulated and subjected to

high reserve and liquidity ratios; legal ceilings on interest rates; sectoral credit allocation quotas.

Thus credit rationing is legally imposed. Policies toward the financial sector is known as “financial

repression.” Restrictions cause the size of the commercial banking

system to be curtailed. Figure 1.6: monetization ratios (banking sector liabilities

over GDP) are lower in developing countries.

34

Figure 1.6aMonetization Ratios

(Money as percent of GDP, average over 1985-96)

Belgium

Canada

France

Germany

Italy

Japan

United Kingdom

United States

0 20 40 60 80 100

Industrial Countries

Burundi

Cameroon

Gabon

Kenya

Lesotho

Madagascar

Morocco

Nigeria

Tunisia

Zambia

0 20 40 60 80 100

Africa

Source: International Monetary Fund.

1/ The narrow money data are for 1985-91 period.

Narrow money Broad money

1/

35

India

Indonesia

Korea

Malaysia

Pakistan

Philippines

Singapore

Sri Lanka

Thailand

0 20 40 60 80 100

Asia

Argentina

Bolivia

Barbados

Chile

Colombia

Haiti

Jamaica

Mexico

Peru

Venezuela

0 20 40 60 80 100

Latin America and Caribbean

Figure 1.6bMonetization Ratios

(Money as percent of GDP, average over 1985-96)

Source: International Monetary Fund.

Narrow money Broad money

36

Informal financial sector has often arisen. Thus, instruments of monetary policy and monetary transmission

mechanism tend to be different. Thus, modification of standard textbook macroeconomic behavioral

relationships may be needed. Incorporate the implications of credit and foreign exchange

rationing in private decision rules by including quantity constraints in consumption and investment equations employing prices in informal credit and foreign exchange

markets. Weakness of the institutional framework in developing countries

has made both the frequency and depth of such financial crises much more extensive.

37

The Government Budget

38

The composition of the government budget differs between industrial and developing

countries

In developing nations, the pervasive role of the state in the economy is exercised through the activities of

nonfinancial public sector and financial institutions owned by the government.

Government tends to play an active role in production. Performance of public-sector enterprises is central in

determining the fiscal stance.

Figure 1.7: Central government absorbs a smaller fraction of output in

developing countries.

39

Figure 1.7aComposition of Central Government Expenditure

(Percent of total expenditure)

18.5%

8.9%

21.5%

8.3%

7.1%

35.8%

Industrial countries Africa

8.1%

7.3%

18.1%

37.7%

5.1%

23.8%

Education and health

Defense

General services

Other

Transport and communications

Social security

Defense

General services

Other

Social security

Education and health

Transport and communications

Source: Burgess and Stern (1993, p. 766).

40

Figure 1.7bComposition of Central Government Expenditure

(Percent of total expenditure)

16.3%

7.6%22.5%

19.0%

6.9%27.8%

17.9%

13.0%

19.6%

7.1%

11.2% 31.2%

Western HemisphereAsia

General services

DefenseEducation and health

Social security

Transport and communicationsOther

General services

Defense

Education and health

Social security

Transport and communicationsOther

Source: Burgess and Stern (1993, p. 766).

41

Composition of spending differs. Developing nations spend more on general public

services, defense, education, and other economic services.

Industrial nations spend more on health and social security.

Figure 1.8: Main source of central government revenue is taxation. Share of nontax revenue in total revenue is higher in

developing countries. Reason: Limited administrative capacity and political

constraints hinder collection of tax in developing countries.

42

Figure 1.8aComposition of Tax Revenue

Industrial countries Africa

35.8%

29.3%

28.4%

2.8%

3.7%

Income taxes

Taxes on goods and services

Social security

Other

Trade taxes

32.3%

25.8%

2.3%

28.4%

7.2%

4.0%

Income taxes

Taxes on goods and services

Social security

Import duties

Export duties

Other

Source: Burgess and Stern (1993, p. 766).

43

Figure 1.8bComposition of Tax Revenue

Asia Western Hemisphere

24.2%36.5%

12.0% 15.8%

5.5%

6.0%

Income taxesTaxes on goods and services

Social securityImport duties

Export duties

Other

27.4%

34.8%

0.2%

30.9%

4.1%

2.6%

Income taxes

Taxes on goods and services

Import duties

Export duties

Other

Source: Burgess and Stern (1993, p. 766).

Social security

44

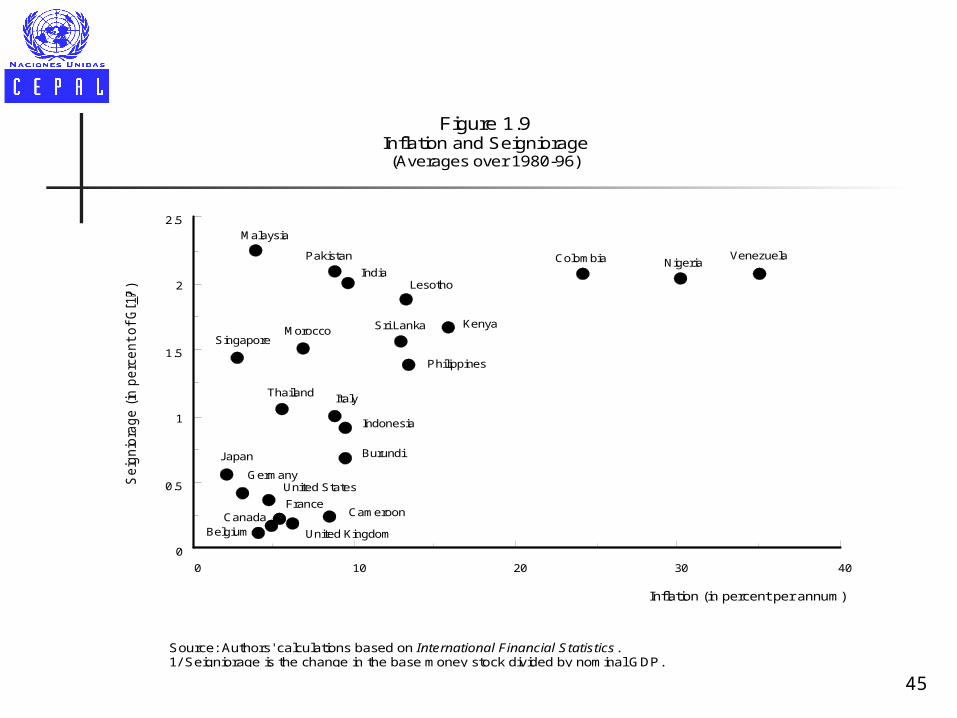

Direct taxes, taxes on domestic goods and services, and taxes on foreign trade have equal shares of total tax revenue in developing countries.

Industrial countries: income taxes have the largest share. Reliance on seigniorage, and therefore to higher levels of

inflation in developing countries due to lack of tax collection, limited issuance of domestic debt.

Figure 1.9: Industrial countries: seigniorage revenue is less than 0.8% of

GDP. Developing countries: more than 1% of GDP. Macroeconomic implications of budget institutions:

45

Figure 1.9Inflation and Seigniorage(Averages over 1980-96)

Source: Authors' calculations based on International Financial Statistics.1/ Seigniorage is the change in the base money stock divided by nominal GDP.

Inflation (in percent per annum)

Se

ign

iora

ge

(in

pe

rce

nt

of

GD

P)

1/

0 10 20 30 40

0

0.5

1

1.5

2

2.5

VenezuelaColombia Nigeria

Philippines

Lesotho

Sri Lanka Kenya

Italy

Cameroon

Indonesia

India

Pakistan

Morocco

Thailand

Singapore

United Kingdom

France

Burundi

BelgiumCanada

GermanyUnited States

Malaysia

Japan

46

Macroeconomic implications of budget institutions: nature of the constitutional rules used to impose

constraints on the size of the fiscal deficit; procedural rules that guide the elaboration of the

budget by the executive branch, its approval by the legislative branch, and its execution;

type of rules that may enhance the transparency of the budgetary process.

47

Aggregate Supply and the Labor Market

48

Due to large direct role of the state in production, size and efficiency of the public

capital stock figures prominently in the aggregate production

Figure 1.10: importance of the public sector in capital accumulation.

Glen and Sumlinski (1998): public sector accounted for 39% of total investment over 1980-1989 and 36% over 1990-1996.

In recent years, several developing countries have undertaken massive privatizations of nonfinancial public enterprises.

49

Figure 1.10 Share of Private Investment in Total Investment

(In percent)

Argentina

Bangladesh

Bolivia

Chile

Colombia

Costa Rica

Côte d'Ivoire

Ecuador

El Salvador

Ghana

Guatemala

India

Indonesia

Kenya

Korea

Malawi

0 30 60 90

Malaysia

Mauritius

Mexico

Morocco

Nepal

Nigeria

Pakistan

Paraguay

Peru

Philippines

Singapore

Sri Lanka

Thailand

Tunisia

Uruguay

Venezuela

0 30 60 90

Source: Pfeffermann and Madarassy (1993). For 1991-96 , Glen and Sumlinski (1998). 1991-96 data for the following countries are from World Bank, World Development Indicators: Ghana, Nepal, Nigeria, Singapore.

1981-85 1986-90 1991-96

50

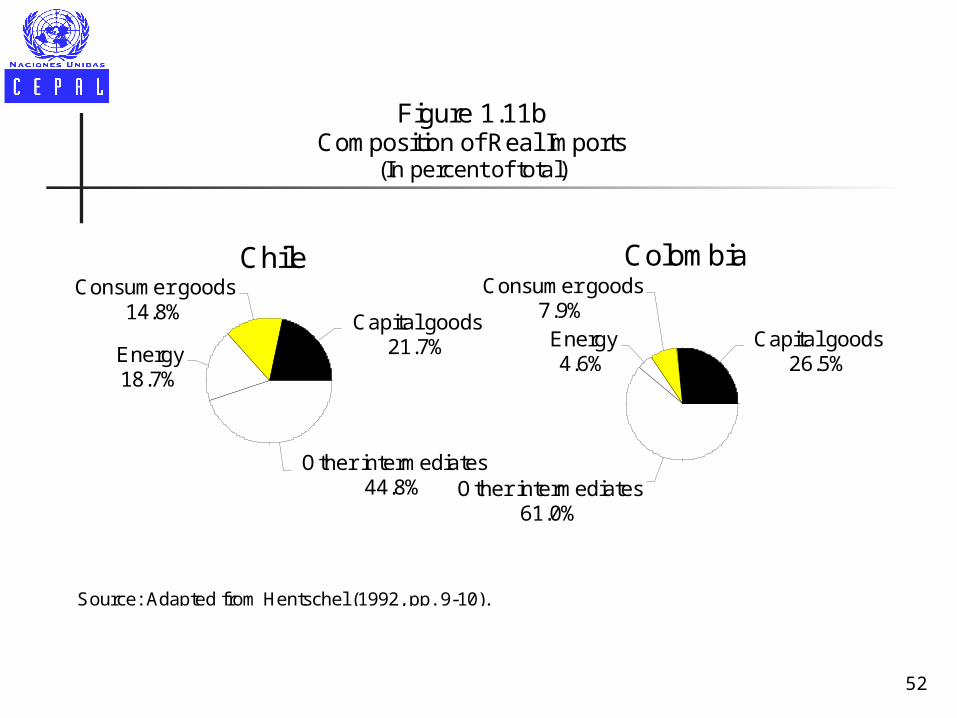

Mirakhor and Montiel (1987): Such goods account for half of all developing-country imports.

Figure 1.11: In some countries the share of energy and non-energy intermediate imports can even exceed 70%.

Results: Difference between the value of domestic production

and domestic value added is larger. Exchange rate has an important influence on the

position of the economy's short-run supply curve. Availability of foreign exchange may have a direct effect

on the position of the short-run supply curve.

Imported intermediate goods play an important role in the aggregate production

function

51

Capital goods22.2%

Consumer goods7.0%Energy

9.8%

Other intermediates61.0%

Argentina

Capital goods11.1%

Consumer goods5.9%Energy

46.6%

Other intermediates36.4%

Brazil

Figure 1.11aComposition of Real Imports

(In percent of total)

Source: Adapted from Hentschel (1992, pp. 9-10).

52

Figure 1.11bComposition of Real Imports

(In percent of total)

Capital goods21.7%

Consumer goods14.8%

Energy18.7%

Other intermediates44.8%

Chile

Capital goods26.5%

Consumer goods7.9%

Energy4.6%

Other intermediates61.0%

Colombia

Source: Adapted from Hentschel (1992, pp. 9-10).

53

Figure 1.11cComposition of Real Imports

(In percent of total)

Capital goods28.7%

Consumer goods9.4%

Energy1.1%

Other intermediates60.8%

Ecuador

Capital goods27.7%

Consumer goods5.8%Energy14.8%

Other intermediates51.7%

Indonesia

Source: Adapted from Hentschel (1992, pp. 9-10).

54

Capital Goods22.8%

Consumer Goods15.5%

Energy9.4%

Other intermediates52.3%

Malaysia

Capital goods27.7%

Consumer goods9.4%

Energy2.7%

Other intermediates60.2%

Mexico

Source: Adapted from Hentschel (1992, pp. 9-10).

Figure 1.11dComposition of Real Imports

(In percent of total)

55

Capital goods27.6%

Consumer goods16.7%

Energy2.1%

Other intermediates53.6%

Peru

Capital goods14.1%

Consumer goods6.9%Energy

28.7%

Other intermediates50.3%

Philippines

Source: Adapted from Hentschel (1992, pp. 9-10).

Figure 1.11eComposition of Real Imports

(In percent of total)

56

Capital goods15.9%

Consumer goods13.0%

Energy31.3%

Other intermediates39.8%

UruguayCapital goods

28.5%Consumer goods

18.8%Energy1.5%

Other intermediates51.2%

Venezuela

Source: Adapted from Hentschel (1992, pp. 9-10).

Figure 1.11fComposition of Real Imports

(In percent of total)

57

Costs of working capital tend to give interest rates and credit availability an important short-run supply-side role But empirical importance of this is mixed. If relevant, contractionary monetary policy may have short-run stagflationary consequences.

Informal sector plays an important role in the determination of wages and employment Informal urban sector accounts up to 60% of economic activity and total employment in developing countries. Result: segmentation of the urban labor market.

Short-run supply functions may be significantly affected by working-capital

considerations

58

Stability of Policy Regimes

59

Developing countries exhibit higher fiscal deficits, higher rates of inflation, higher average growth rates.

During 1979-88: Industrial countries: real GDP growth is 2.8% per

annum and inflation is 6.3%. Developing countries: real GDP growth is 4.3% per

annum and inflation is 31.8%.During 1989-1998: Industrial countries: real GDP growth is 2.2% per

annum and inflation is 3.1%.

60

Developing countries: real GDP growth is 5.8% per annum and inflation is 33.2%.

High inflation has been a symptom of policy instability and has been associated with policy uncertainty.

Policy uncertainty is important in: triggering currency substitution; capital flight; exchange-rate crises; collapse of private investment.

Uncertainty in policy environment must be included in developing-country macroeconomic models, design of macroeconomic reform programs.

61

Macroeconomic Volatility

62

Macroeconomic environment in developing countries is much more volatile

Roots of macroeconomic instability are both external and internal: Volatility in the terms of trade and international

financial conditions. Inflexibility of domestic macroeconomic

instruments and political instability.Figure 1.12: Latin America case. All components of the governments budget is

less stable.

63

Figure 1.12Macroeconomic Volatility

(Standard deviation of percentage change)

Source: Inter-American Development Bank, 1996 Annual Report.

Note: All data are population-weighted averages of the underlying country volatilities. Fiscal data are measured in percent of GDP.1/ All series refer to 1970-92, except for change in total surplus and change in primary surplus for which the period is 1970-94.

Industrial countries Latin America

Real GDP

Real private

consumption

Terms of trade

Real exchange rate

Change in

total surplus

Change in

primary surplus

0 5 10 15 20

1970-92 1/

Total revenue

Nontax revenue

Tax revenue

Total expenditure

Capital expenditure

Current expenditure

0 5 10 15 20 25

1970-94

64

Instability causes relative prices such as the terms of trade and real

exchange rate; unstable growth rates of real GDP and private

consumption. Gavin and Perotti (1997): volatility in some Latin American

countries have been compounded by a procyclical fiscal policy response:

increase in government expenditure and fiscal deficits during periods of expansion;

fall during recessions. Overall, boom and bust phenomena tend to be much more

common and more costly in developing countries.

65

Some Special Topics

66

Long-standing issues: desirability of alternative exchange-rate regimes; “new structuralist” critique of the role of the

exchange rate in orthodox stabilization. Recent issues:

macroeconomic consequences of alternative nominal exchange-rate rules;

role of the exchange rate as a nominal anchor in an open economy.

Exchange-Rate Management

67

Alternative approaches to price-level stabilization ranging from “orthodox” money-based programs relying

on tight fiscal and monetary policies and exchange-rate policy,

to “heterodox” programs based on tight aggregate demand policies, an exchange-rate freeze, and wage and price controls.

The evaluation of this experience and its lessons for future stabilization efforts have been important.

Stabilization of High Inflation

68

Since the early 1990s many Asian and Latin American countries have faced a surge in capital inflows.

The causes of such inflows, their welfare implications, and appropriate policy responses have been the subject of much recent attention.

Managing Capital Flows

69

Currency Crises

In recent years research have focused on roles of self-fulfilling expectations and

policymakers' preferences, links between banking and currency crises

and predictive content of various economic indicators.

70

Reforms are designed to enhance role of financial intermediaries in

channeling domestic saving give the real economy a more outward

orientation. But these reforms have been controversial. Their relationship with macroeconomic stabilization

has been a focus of attention.

Trade and Financial Reform

71

Political Aspects of the Macroeconomy

Political factors are important to understand many macroeconomic phenomena, such as inflation inertia, setting of policy instruments, sustainability of reform programs.

72

Important issues: incidence of labor market segmentation, role of government regulations, low degree of labor mobility across sectors in

the short run.

The Functioning of Labor Markets