Embed Size (px)

Citation preview

1

MF-852 Financial Econometrics

Lecture 10 Serial Correlation and

Heteroscedasticity

Roy J. EpsteinFall 2003

2

Topics Serial correlation

What is it? Effect on hypothesis tests Testing and correcting for serial

correlation Heteroscedasticity

Ditto. ARCH (or how to win a Nobel

prize)

3

Serial Correlation The error terms in the regression

should be independent, i.e., E(eiej) = 0 for any i and j.

If this assumption is not true then the errors are serially correlated.

Only a problem for time-series data.

4

Serial Correlation — Possible Causes Omitted variables.

Wrong functional form.

“inertia” in economic data—error term composed of many small effects, each with a similar trend.

5

Correlated Error Terms Suppose E(eiei-1) 0. Implies

neighboring observations are correlated, not independent. 1st-order process. Most common

form of serial correlation.

Suppose E(eiei-4) 0. 4th-order process. Often occurs

with quarterly data.

6

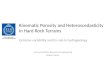

Graph of Residuals from a Regression

-200

-150

-100

-50

0

50

100

150

200

250

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36

Observation

7

Importance of Serial Correlation Regression coefficients (the

marginal effects) are unbiased.

BUT their standard errors are biased.

Bias generally understates the standard errors, so significance tests are biased against H0.

H0 is rejected too often.

8

Bias in Standard Errors Standard errors for the

coefficients depend on estimated variance of error term, s2

e.

Regression program assumes independent errors with mean 0, so program calculates 22

ie es

9

Why the Standard Errors are Biased Calculation ignores covariance

when errors are NOT independent.

Covariance between errors, when it exists, is usually positive.

So s2e would be understated and

standard errors would be biased downward.

10

Testing for Serial Correlation Most common test is Durbin-

Watson statistic Only used for 1st order serial

correlation

Calculated as

2

211

2

2

21

ˆ

ˆˆˆ2ˆ

ˆ

ˆˆ

i

iiii

i

ii

e

eeee

e

eeDW

11

Durbin-Watson Stat. When covariance between

neighboring observations is zero then DW should be close to 2. High covariance implies DW —> 0.

H0 for no 1st order serial correlation: DW = 2

Look up critical values in table (RR, p. 592) See sample regression in xls file.

12

Model with Serial Correlation Yt = 0 + 1Xt + et

Suppose et = et-1 + ut , where ut is another error with mean 0 that is serially independent and uncorrelated with e or X.

-1 < < 1 (or the process is explosive)

ut is called the innovation in e because it is the new component of e each period.

Serially correlated: E(etet-1) = var(et).

13

How to find Estimate it as = 1 – DW/2.

We can do this in Excel.

Fancier procedures: Cochrane-Orcutt and Hildreth-Liu and others.

A good regression program will calculate automatically.

14

Fixing Serial Correlation Suppose is known. Then “difference”

the model:

Yt – Yt-1 = 0(1–) + 1(Xt–Xt-1) + (et – et-1)

Or

Yt – Yt-1 = 0(1–) + 1(Xt–Xt-1) + ut

ut is a “well behaved” error.

Differenced model yields unbiased coefficients and unbiased standard errors.

See example.

15

Heteroscedasticity Strange name! Greek for

“different variances.”

Violation of last assumption about residual: same variance for each error term.

Can occur with any kind of data.

16

Heteroscedasticity — Possible Causes Wrong functional form.

Var(e) correlated with an included X variable on the right side of the regression. E(var(e), X) 0, NOT E(e, X)

0

17

Heteroscedasticity — Importance Regression coefficients (the

marginal effects) are unbiased.

BUT their standard errors are biased. Direction of bias not usually

known.

Confidence levels, p-values, t statistics not reliable.

18

Model with Heteroscedasticity Yt = 0 + 1Xt + et

Suppose var(et) = 2Xt2.

Var(e) is different for each observation.

19

Fixing Heteroscedasticity — Weighted Least Squares Observations with smaller error

variance are “better.” Give them more weight when estimating the model.

Weighted Least Squares (WLS): Multiply observations by weighting factors that equalize the variance.

(1/Xt)Yt = (1/Xt)0 + (1/Xt)1Xt + (1/Xt)et

Var((1/Xt)et) = ((1/Xt2)2Xt

2 = 2

20

Calculating WLS Suppose form of heteroscedasticity

is known, e.g., need to weight by Xt. You just need to create new

variables. (1/Xt)Yt = (1/Xt)0 + 1 + ut

Intercept in WLS is 1, slope on 1/X is 0.

“Well behaved” error term, yields unbiased coefficients and unbiased standard errors.

21

ARCH models AutoRegressive Conditionally

Heteroscedastic model Regression model with serial

correlation (“autoregressive”) AND heteroscedasticity.

Used to model volatility, i.e., variance, of returns.

22

ARCH models Sometimes you want to model

volatility itself (e.g., it’s an input to an option pricing model).

Volatility can change over time, periods of high and low volatility.

ARCH describes this process.

23

Formulation of ARCH model Yt = 0 + 1Xt + et

Var(et) = 0 + 1et-1.

1st order ARCH process.

Can estimate ’s and ’s and perform WLS.