Embed Size (px)

Citation preview

1

SOLAR ENERGY IN RAJASTHAN

Presented by

Mr. D.C.Samant, Chairman

Rajasthan Electricity Regulatory Commission

May 20, 2010

Cape Town (S.A.)

2

STRUCTURE

Rajasthan – Some Features

Policy Support for RE including National Solar Mission

State Support and Incentives

Regulatory Support

Emerging RE Scenario

Experience in handling some Issues/Constraints

Issues & Challenges

3

ABOUT RAJASTHAN

Rajasthan is the largest State of India (having 28 States and 7 Union Territories)

Population around 60 million

2/3rd of the State is desert and semi-desert with scanty rainfall and plenty of sunshine

Is deficient in conventional power resources such as Coal, Hydro, etc.

State has immense solar potential, the best in India and amongst the best in the world

State’s geo-climatic handicaps offer huge advantage as far as solar energy is concerned

4

SOLAR MAP OF INDIA

Delhi

Rajasthan

Gujarat

Mumbai

5

SOLAR POTENTIAL IN RAJASTHAN

Best solar radiation in India― Amongst the best in the world

Solar radiation being 6-7 kWh/sq. meter

More than 325 sunny days in a year (amongst the best in india)

Land in abundance and is available at comparatively low price

State’s desert has an area of around 200,000 sq. kms.― Land required to generate 10,000 MW is less than 400 sq. kms.

6

ENERGY SCENARIO (INDIA & RAJASTHAN)

Installed capacity― All India - 159,000 MW (16,800 MW

RE)

― Rajasthan - ~8,065 MW (1158 MW RE)

Rapidly growing demand due to― High GDP growth

― Access to power for all by 2012

Energy consumption grew by around 8% per annum in past 6 years (ending FY 2010)― Corresponding growth being around 11% in Rajasthan

― Overall energy shortage is around 10% (capacity shortage 13.3%) – All India level

Growth in demand has exceeded capacity addition― Widening of gap between demand and supply

― Power cuts even in some cities of India

7

POLICY FRAME FOR RENEWABLE ENERGY (RE)

Acceleration in RE generation imperative or rather urgent due to (i) Demand supply scenario; (ii) Depleting fossil resources and their rising costs; and (iii) Emerging serious threat of global warming

National action plan on climate change formulated by GoI envisages RE share in energy to reach 15% by 2020

Solar Mission has been launched in January 2010― India aims to become a global leader in the use of solar energy

The Electricity Act empowers State Regulatory Commissions to specify Renewable Energy Purchase Obligation (RPO)

The Tariff Policy formulated by GoI emphasises on enhancing RE through Feed-in tariff and other support

Policy notified by the State Govt. to support and provide incentive to growth of non-conventional energy

8

NATIONAL SOLAR MISSION

An ambitious programme launched by GoI― Aims at ultimate capacity of 20,000 MW by year 2020

Capacity enhancement targeted in three phases― 1300 MW by March, 2013(Phase–1)

→ 1100 MW grid connected and 200 MW off-grid

― 4000 MW or more by year 2017 (Phase-2)

Several off-grid applications, which are already commercially viable or near viability to be scaled up:― Solar thermal water heaters

― Solar lighting system for remote and in-accessible areas

9

NATIONAL SOLAR MISSION…..

To focus on R&D programme to address India-specific challenges in promoting solar energy.

Human resource development and other capacity building efforts to be taken up.

Development of domestic industries in manufacturing solar products and in indigenisation of various items and components.

Draft guidelines issued by Govt. of India and implementation to start from the current year.

10

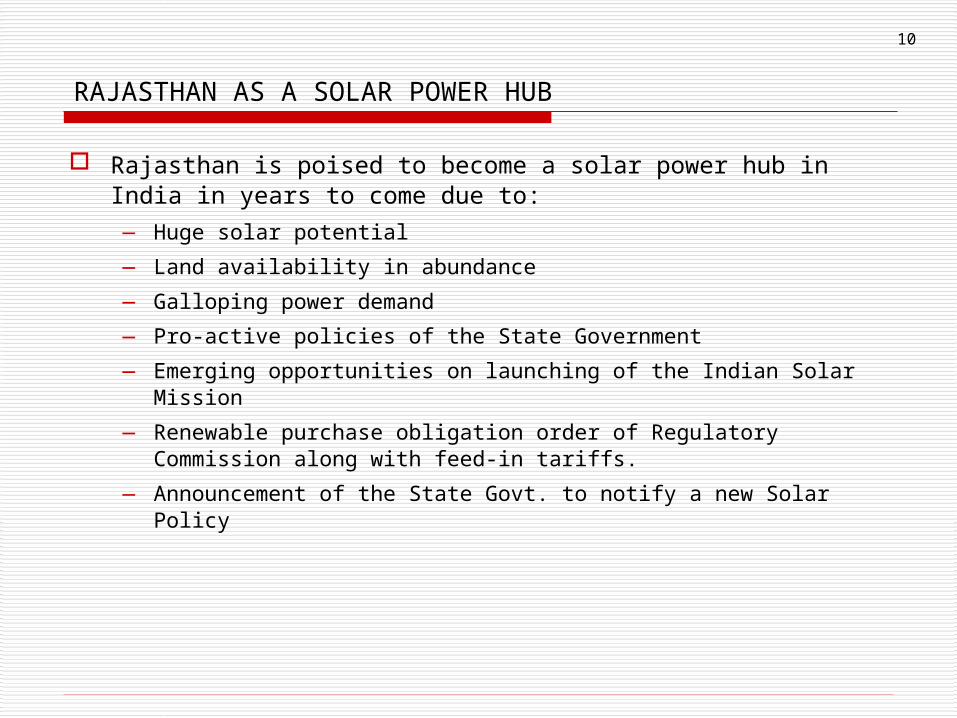

RAJASTHAN AS A SOLAR POWER HUB

Rajasthan is poised to become a solar power hub in India in years to come due to:― Huge solar potential

― Land availability in abundance

― Galloping power demand

― Pro-active policies of the State Government

― Emerging opportunities on launching of the Indian Solar Mission

― Renewable purchase obligation order of Regulatory Commission along with feed-in tariffs.

― Announcement of the State Govt. to notify a new Solar Policy

11

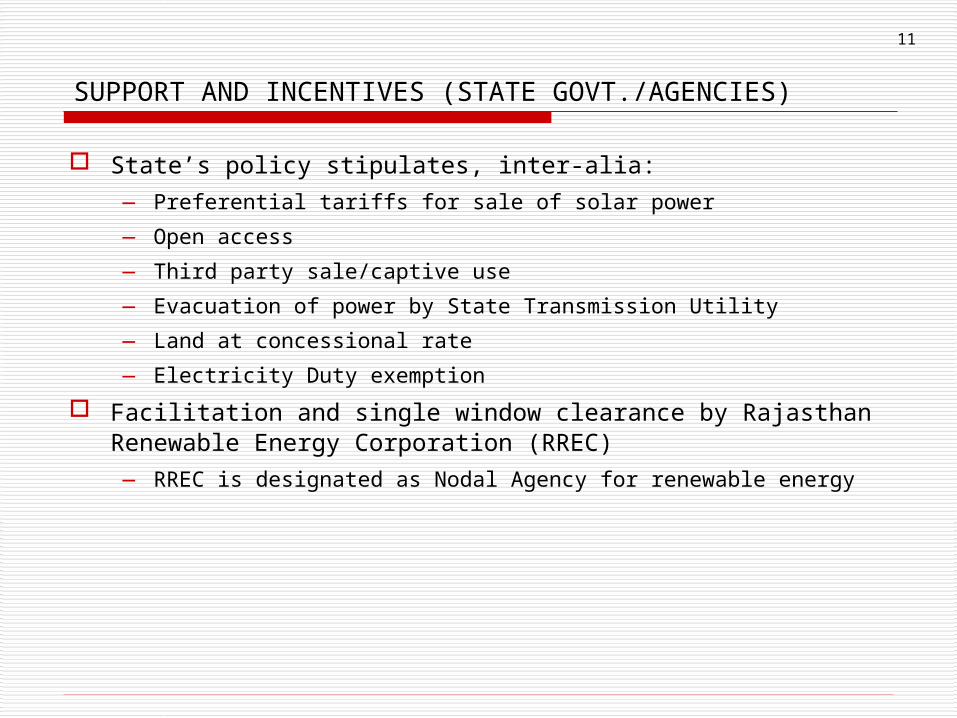

SUPPORT AND INCENTIVES (STATE GOVT./AGENCIES)

State’s policy stipulates, inter-alia:― Preferential tariffs for sale of solar power

― Open access

― Third party sale/captive use

― Evacuation of power by State Transmission Utility

― Land at concessional rate

― Electricity Duty exemption

Facilitation and single window clearance by Rajasthan Renewable Energy Corporation (RREC)― RREC is designated as Nodal Agency for renewable energy

12

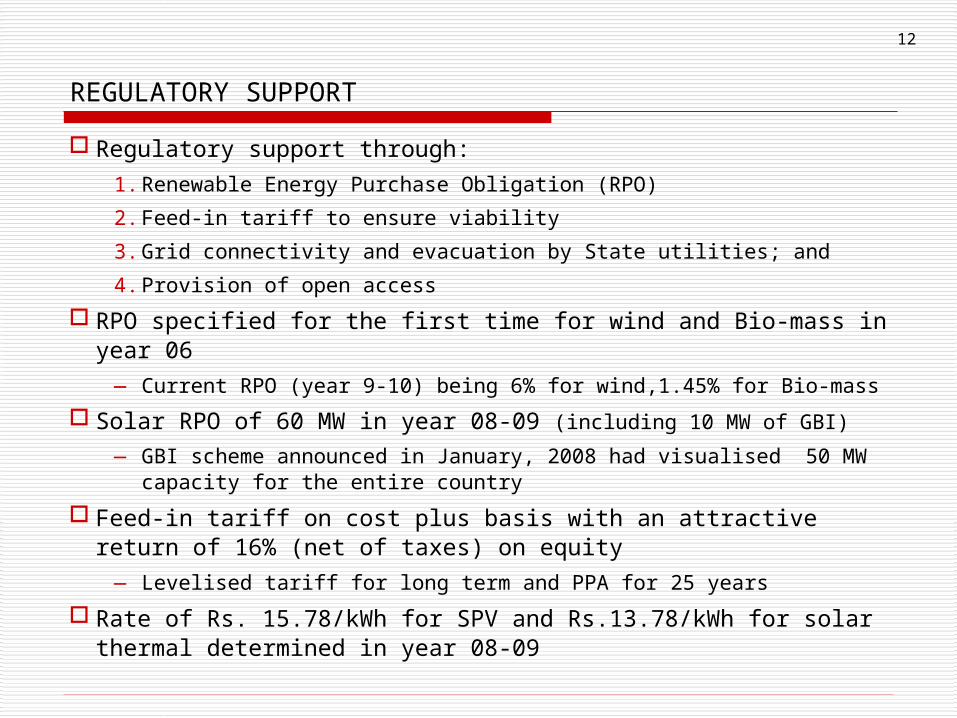

REGULATORY SUPPORT

Regulatory support through:

1. Renewable Energy Purchase Obligation (RPO)

2. Feed-in tariff to ensure viability

3. Grid connectivity and evacuation by State utilities; and

4. Provision of open access

RPO specified for the first time for wind and Bio-mass in year 06― Current RPO (year 9-10) being 6% for wind,1.45% for Bio-mass

Solar RPO of 60 MW in year 08-09 (including 10 MW of GBI)

― GBI scheme announced in January, 2008 had visualised 50 MW capacity for the entire country

Feed-in tariff on cost plus basis with an attractive return of 16% (net of taxes) on equity― Levelised tariff for long term and PPA for 25 years

Rate of Rs. 15.78/kWh for SPV and Rs.13.78/kWh for solar thermal determined in year 08-09

13

ACCELERATION IN RE GENERATION

Quantum jump in wind genration― From 2 MW in 99-2000 to 1085 MW in March, 2010

― 50% added in past two years

Actual

0

200

400

600

800

1000

1200

Up

to

20

03

-04

Up

to

20

04

-05

Up

to

20

05

-06

Up

to

20

06

-07

Up

to

20

07

-08

Up

to2

00

8-0

9

Up

to

20

09

-10

MW

Actual

GROWTH OF WIND ENERGY OVER THE YEAR

14

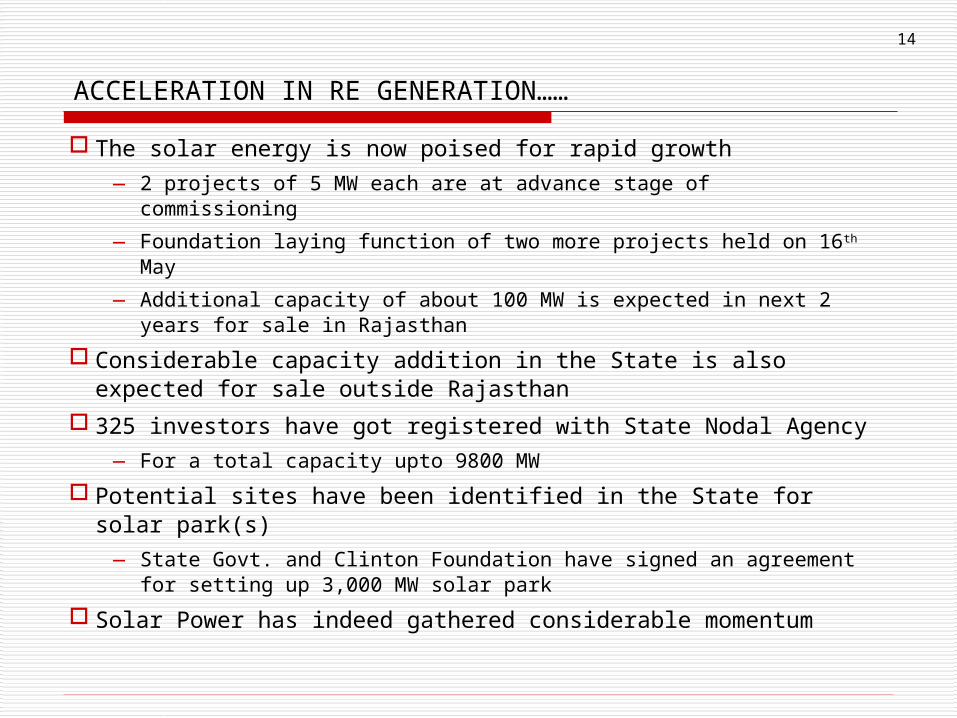

ACCELERATION IN RE GENERATION……

The solar energy is now poised for rapid growth― 2 projects of 5 MW each are at advance stage of commissioning

― Foundation laying function of two more projects held on 16th May

― Additional capacity of about 100 MW is expected in next 2 years for sale in Rajasthan

Considerable capacity addition in the State is also expected for sale outside Rajasthan

325 investors have got registered with State Nodal Agency ― For a total capacity upto 9800 MW

Potential sites have been identified in the State for solar park(s) ― State Govt. and Clinton Foundation have signed an agreement for

setting up 3,000 MW solar park

Solar Power has indeed gathered considerable momentum

15

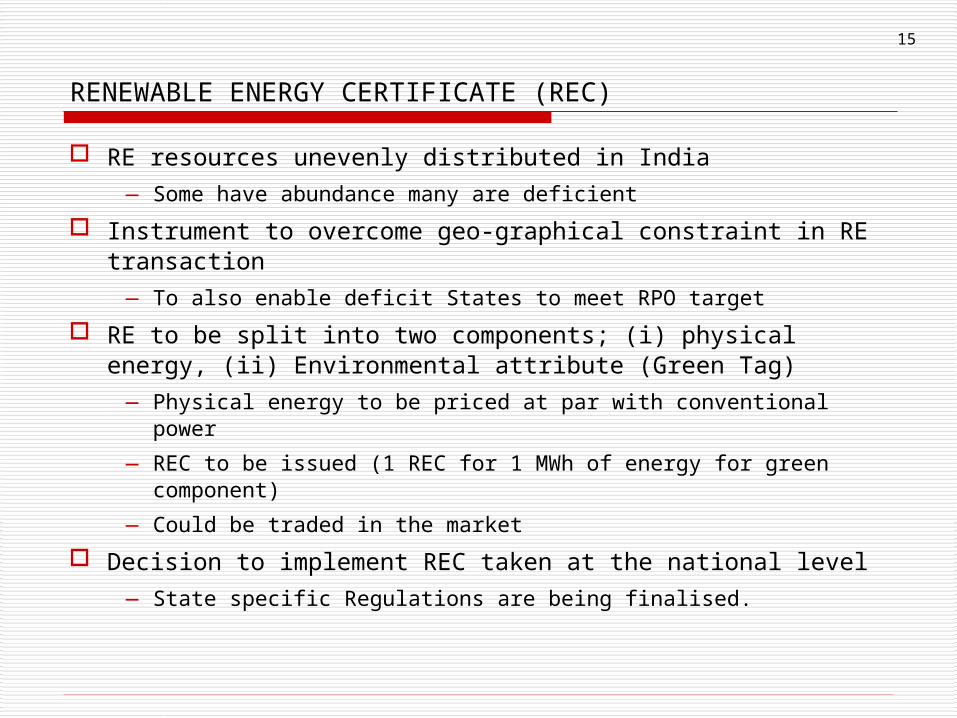

RENEWABLE ENERGY CERTIFICATE (REC)

RE resources unevenly distributed in India― Some have abundance many are deficient

Instrument to overcome geo-graphical constraint in RE transaction― To also enable deficit States to meet RPO target

RE to be split into two components; (i) physical energy, (ii) Environmental attribute (Green Tag)― Physical energy to be priced at par with conventional power

― REC to be issued (1 REC for 1 MWh of energy for green component)

― Could be traded in the market

Decision to implement REC taken at the national level ― State specific Regulations are being finalised.

16

EXPERIENCE IN HANDLING SOME ISSUES/CONSTRAINTS

First issue was in specifying RPO for solar energy― Major deterrent being extremely high cost of solar energy (4 to 5

times of conventional power) and

― Absence of single MW scale project in India until a few years ago.

→ However, after discussion and deliberation and assessment of impact on consumer tariff Commission decided to specify RPO of 60 MW for the year 2008 in the larger interest of paving the way for growth of solar energy, particularly for Rajasthan, where solar energy is in abundance.

Second issue was whether there should be generic feed-in tariff or project specific tariff― The Commission has adopted generic tariff for wind and bio-mass in

the year 2006 but was left open for Solar energy

17

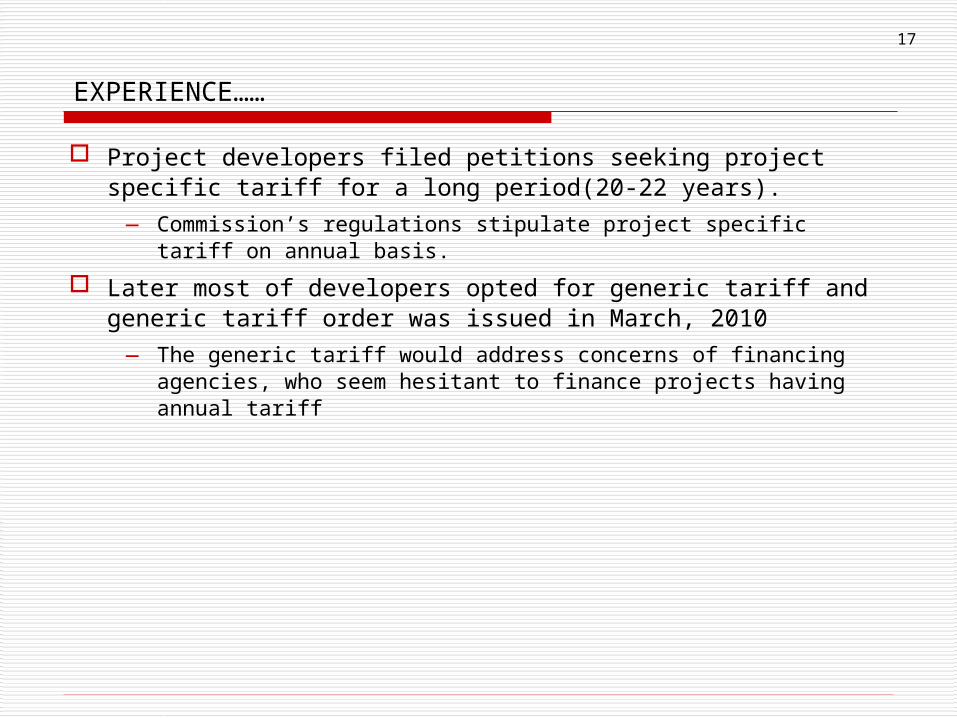

EXPERIENCE……

Project developers filed petitions seeking project specific tariff for a long period(20-22 years).― Commission’s regulations stipulate project specific tariff on annual

basis.

Later most of developers opted for generic tariff and generic tariff order was issued in March, 2010― The generic tariff would address concerns of financing agencies,

who seem hesitant to finance projects having annual tariff

18

ISSUES/CHALLENGES

High cost of solar energy continues to be the major concern― The success of solar mission hinges on rapid cost reduction

Indigenization and development of manufacturing base in India important for cost reduction― It needs support of technology suppliers as well as equipment and

component manufacturers

Peak demand in India is normally after sun-set― Solar capacity with storage would be required for the solar energy

to become the primary source of energy.

THANK YOU

FOR YOUR PATIENT HEARING AND KIND ATTENTION