Embed Size (px)

Citation preview

1

Strictly Private and Confidential

International Food Aid & Development: Africa Agriculture

Kansas City – August 2010

2

Global representation

Rest of world Key regional officesAfrica

• 17 African countries• Over 1,000 Branches & 5,000 ATMs across these geographic regions

• 16 countries outside Africa

• 90 branches in Argentina

• Offices in key regional financial centre's including London, Moscow, New York, Hong Kong, Sao Paulo and Dubai

Standard Bank has extensive expertise in the complicated dynamics of emerging markets, enabling us to effectively partner clients and our stakeholders in achieving their strategic objectives

3

Outline

Looking ahead …

What are the emerging trends and opportunities shaping business in Africa?

Africa’s Changing landscape

Opportunity for Africa Agriculture

– Expand agricultural production;

– Develop agricultural value chain.

Financial Sector.

4

Section 1:

Looking ahead...

5

Shift from G7/8 to G20:Integration of other emerging markets, including Africa, into the world system, is the long term story for economic growth and development;

South Africa remains a major economy, but there is a shift of economic power to SSA & North Africa;

Investors are making more confident commitments to the continent!Shift from Aid towards investment and self development!

Growth in BRICs – in particular, China and India – has a major impact on Africa.Growth in BRICs – in particular, China and India – has a major impact on Africa.

With better governance and policies in place, Africa is poised to reap the economic bounty the demographic transition promises

Advances now allow Africa in some instances to leapfrog to “best of breed”.

Shift from Food Aid to Food Security. The time is now for Africa to fulfil this Agricultural potential.

7 Key Trends:

6

Then and now……

Africa in the 1950s and 1960s appeared to have a bright future. But that is not how it turned out. Why?

► Negative demographics

► Lack of communication technologies, mainly rural populations, Cold War rivalry – all worked to allow bad leaders to stay with wrong policies

► Stagnation for commodity producers

At the beginning of the 21st century, the outlook for Africa is positive – and fundamentally better. Why?

► Demographic dividend is beginning

► New technologies allow Africa to leapfrog to best of breed

► Better policies being implemented – no serious alternative to this; or else isolation

► Populations more urban, more educated, and technologies are a better check on bad policies

► Shift in locus of global growth to BRICs is very positive to Africa

The Agricultural growth story for Africa is compelling

7

Section 2:

Changing landscape creates opportunity for Africa Agriculture

8

Changing landscape creates opportunity for Africa Agriculture

Africa: More that a decade of > 5% average annual economic growth rates;

Average per capita production increased since mid-1980 (West & North) and mid-1990s (East & Southern);

Sea-change in the patterns of demand for food;

Africans have been urbanising at a rapid rate;

Concomitant rise in modern supply chains.

9

Changing landscape creates opportunity for Africa Agriculture

Opportunities:

Opportunity to expand production

Complex and more lucrative supply chains from farmers to urban markets;

Export opportunities as trade barriers gradually erode;

Import substitution that will arise from competitive African agribusinesses.

10

Section 3:

Expand Production

11Supply

Productivity improvements

– Cereal yields have only improved by 1.3% per annum in the past 20 years

– Upswing in yields in emerging markets holds significant potential

– Environmental requirements on fertilizer and pesticide usage and concern over genetically modified crops will limit upward trend in yields

Land availability

– Increasing industrialisation in the developing world and environmental restrictions reducing stock of land used for farming

– Global arable and permanent cropland has risen only 13% since 1961

– China and India are self sufficient in grains, but have degraded much of their arable land and are running at lower national stock levels. Slight variations in seasonal conditions have seen them forced to import in recent years

– Climate change remains a considerable risk and changing regional rain patterns can severely impair productive values

– Agri-stressed countries like Saudi, Kuwait, China and South Korea have contracted to lease or buy 9m Ha of farmland in 12 African countries in the last 3 years – SA grows 3m Ha of maize and wheat, so 3 SA’s.

Average Agricultural Land Prices

0

5

10

15

20

25

$’00

0 p

er H

a

Source: Eurostat, USDA, FAO

0

10,000

20,000

30,000

40,000

50,000

60,000

1961

1966

1971

1976

1981

1986

1991

1996

2001

2006

China Africa South East Asia

India LatAm Middle East

The green revolution has not yet reached African yields

Source: FAO

12Africa’s Emerging Potential

Africa has abundant arable land and water, relative to Asia and the Middle East:

– Africa’s per capita water resource is 4,600m3, versus Asia’s 3,000m3 and ME’s 164m3

– Only 15% of Africa’s arable land is used, versus 60% in Asia and 140% in ME.

There is a shift from “food aid” to “food security”, driving policy changes and significant donor efforts to catalyse investment in both commercial and small scale farming:

– Measures to address constraints such as weak land tenure, poor seed, low use of fertilisers, and lack of access to finance and markets

– World Food Programme now sourcing in local markets

Rising per capita incomes are lifting domestic food demand, and attracting investors

The perception of a “Land Grab” needs to be addressed, and a combination of political pressure and donor support will put significant resources behind small scale farmers, using “out-grower’ and other models.

In China, “the land is little and the people are many”, while in Africa the opposite is true

Source: FAO

0 5 10 15 20

Arable land (% of world total)

Production (% of world total)

China Africa

Population (% of world total)

13

Africa is attracting a wall of money, from donors.... and Private Investors.

In 2009 the WB increased its spending on agri by 50% to USD 6bn

AGRA work with a number of local Banks to support finance to smallholder

agriculture

USAID & USDA – “Feed the Future”

AGRA, AFD (France), IFAD and AfDB have seeded a USD 500m African

Agriculture Fund – institutional investors have since committed.

USAID is supporting Agrifuturo in Mozambique and has committed USD 40m to

small scale agriculture in Zimbabwe last year (50% via commercial banks).

Number of Private Sector Investors / Equity Funds

14

Private Sector Investment: Return vs. Perceived Risk

Supportive agribusiness environment:

Access to markets and natural resources;

Good Infrastructure;

Stable macro-economic and political environment

Agric specific factors:

Risk Management;

Supply chain coordination;

Specialized infrastructure;

Support services related to compliance to international food safety &standards.

15

Section 4:

Value Chain

16Broad Themes in the Value Chain

Promoting market penetration (e.g. Yara in

Beira Corridor) Strategic value of

logistics

Seeking control over Production. More value

added processing

Demanding low cost plus food safety, traceability, working capital. Greater selling and sourcing in

emerging markets

Seeking direct access to market

Integrating inputs and logistics e.g. Poultry Co’s buying stock feed co’s;

BAT out-growers scheme

Input and Logistics Suppliers

Farmers (small and commercial)

Commodity Traders

Primary Processors

Food & Beverage Companies

Wholesales andRetailers

Greater drive to processed foods, locally sourced.

Ruthless on cost control

17

Section 5:

Financial Sector

18

Essentially a wholesale model that leverages commercial aggregators in the value chain

Through these aggregators, gain informed access to a large farmer base to gain access to smallholder farmers at scale

Secure market linkage through aggregators

Ability to provide insurance and price hedging products at bulk aggregator level

Resulting per farmer transaction and service cost is lowered

Partnership with risk partners and technical assistance providers

Opportunity to build a credit history of individual farmers in order to integrate into the formal banking economy

Small Farmers (private land)

Intermediary SPV

(Warehouse, exporter, miller)

Management Assistance & off - take agreement

Land owned by Community

Bank

Working Capital / Production finance

Farmers have a right to occupy

Strategic partner provides guaranteed off - take, ensure acceptable crop management practices, etc

1 st Loss Guarantee

Risk Partner

Linking Smallholders to the Market

The Bank launched a USD100m fundIn 2009, with AGRA / MCC / Kilimo Trust

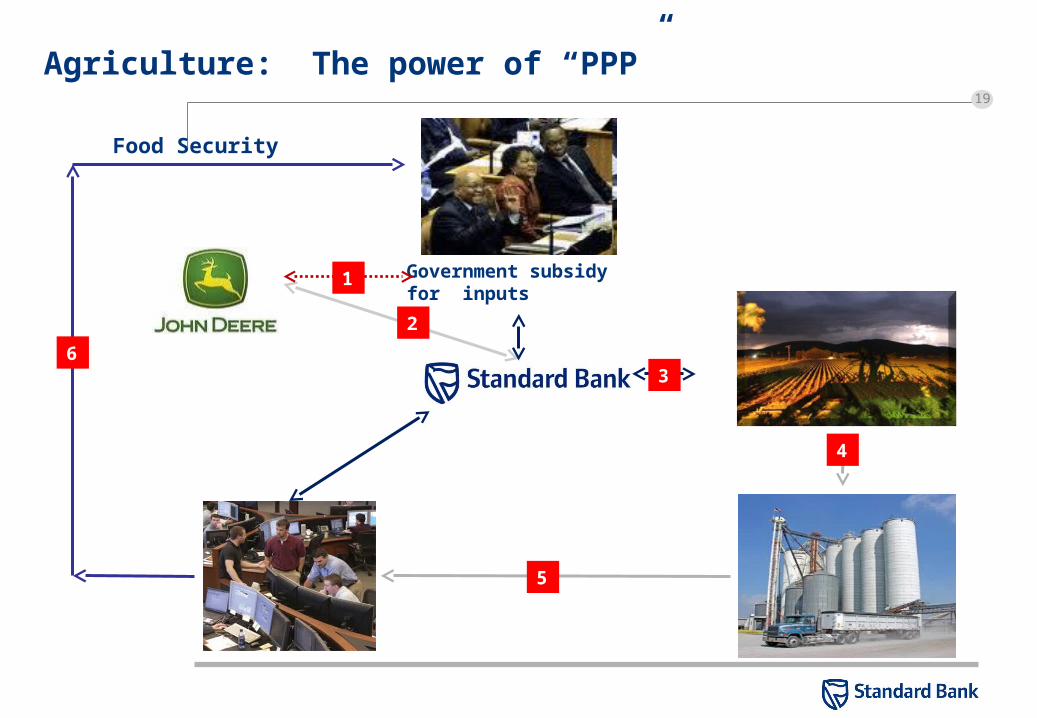

19

Agriculture: The power of “PPP”

Government subsidy for inputs

Food Security

1

2

3

4

5

6

20

DisclaimerConfidentiality and disclaimerThis document is provided on the express understanding that the information contained herein will be regarded and treated as strictly confidential and proprietary to The Standard Bank of South Africa Limited (“Standard Bank”), its holding company Standard Bank Group Limited, and the subsidiaries of its holding company (“the Standard Bank group”) . By retaining it the recipient undertakes that it is not to be delivered and nor shall its contents be disclosed to anyone other than the intended recipient, and nor shall it be reproduced or used, in whole or in part, for any purpose other than for the purpose described herein, without the prior written consent of Standard Bank.Whilst every effort has been made to ensure the accuracy and completeness of the information contained in this document, no responsibility is accepted by the Standard Bank group for the treatment by any court of law, tax, banking or other authorities in any jurisdiction of any transaction based on the information contained herein. There may be tax implications to consider in any transaction and these should be identified and understood before investing. Separate tax advice should therefore be sought when appropriate. Should anything contained herein contribute to the acquisition of a financial product the following must be noted: there are intrinsic risks involved in transacting in any products; no guarantee is provided for the investment value in a product; any forecasts based on hypothetical data are not guaranteed and are for illustrative purposes only; returns may vary as a result of their dependence on the performance of underlying assets and other variable market factors and past performances are not necessarily indicative of future performances. Any client that is not a merchant banking client as defined in the Financial Advisory and Intermediary Services Act must note that unless a financial needs analysis has been conducted to assess the appropriateness of any product, investment or structure to its circumstances, there may be limitations on the appropriateness of any information provided by a member of the Standard Bank group and careful consideration must be given to the implications of entering into any transaction, with or without the assistance of an investment professional.

CONTACT DETAILS

Jacques Taylor Mark ChiavielloDirector / Head: Agricultural Banking Director: International Development GroupStandard Bank, Africa Standard Bank, NY

![STRICTLY CONFIDENTIAL Accessories - Teams.pdfTITAN WATCHES. STRICTLY CONFIDENTIAL THANK YOU. Title: PowerPoint Presentation Author: KULJIT SINGH KOHLI [ Mumbai , Mumbai PVBU ] Created](https://img.pdfslide.net/doc/110x75/604b786e5fce1f4e244e6c26/strictly-accessories-teamspdf-titan-watches-strictly-confidential-thank-you.jpg)