Embed Size (px)

Citation preview

1

Tales From the Trenches

Scott H. HughesVisiting Professor of Law

University of Georgia

Dickason Professor of LawUniversity of New Mexico

2

Iowa

•June 1985

•Hwy 92 East of Council Bluffs

3

4

Causes of Farm Recession

•Rapid farm land inflation in late 70’s - early 80’s

•Price support programs expire

•Farmers expand production and plant fence row to fence row

•Commodity prices fall dramatically

•Lenders (FLB etc.) asset lending instead of cash flow lending

5

State of Farm Economy

•Corn as fuel

•Bank failures

•Land values decline

•Farmers on food stamps

•Cattle rustling

6

State of the Farmer

•radical increase in community health problems

•increase in depression and anxiety

•paralyzing some farmers

•murder and suicide

7

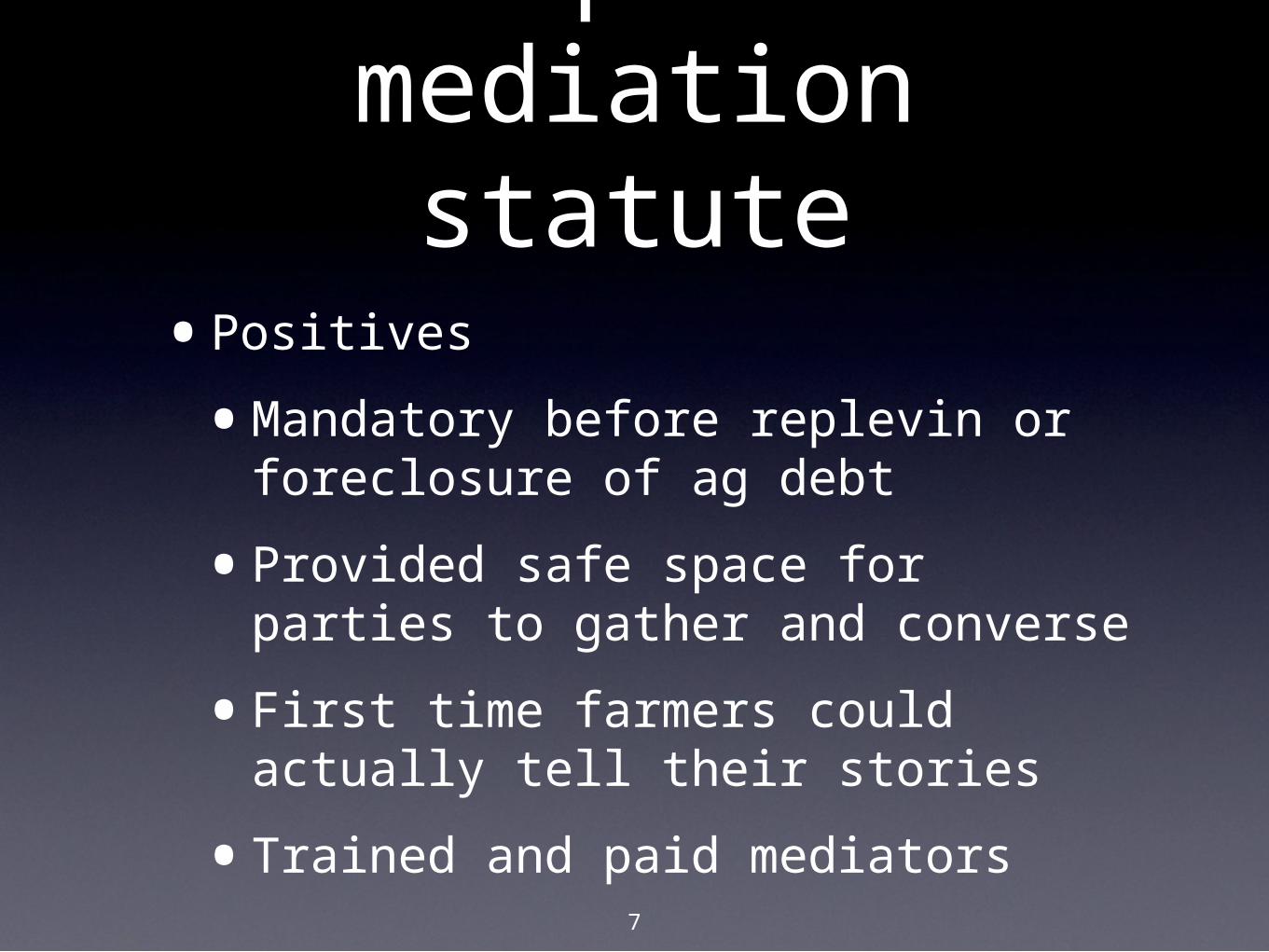

Iowa passes mediation statute

•Positives

•Mandatory before replevin or foreclosure of ag debt

•Provided safe space for parties to gather and converse

•First time farmers could actually tell their stories

•Trained and paid mediators

8

•Negatives

•Many farmers still pro se at this time

•Huge Power Imbalances

•few and weak defenses against the banks

9

Dealing w/ power imbalances

•Challenge every ambiguity in the mediation statute

•someone with settlement authority had to attend

•creditor could not attend by counsel only

•could not file suit to replevy or foreclose without actually having mediation certificate9

10

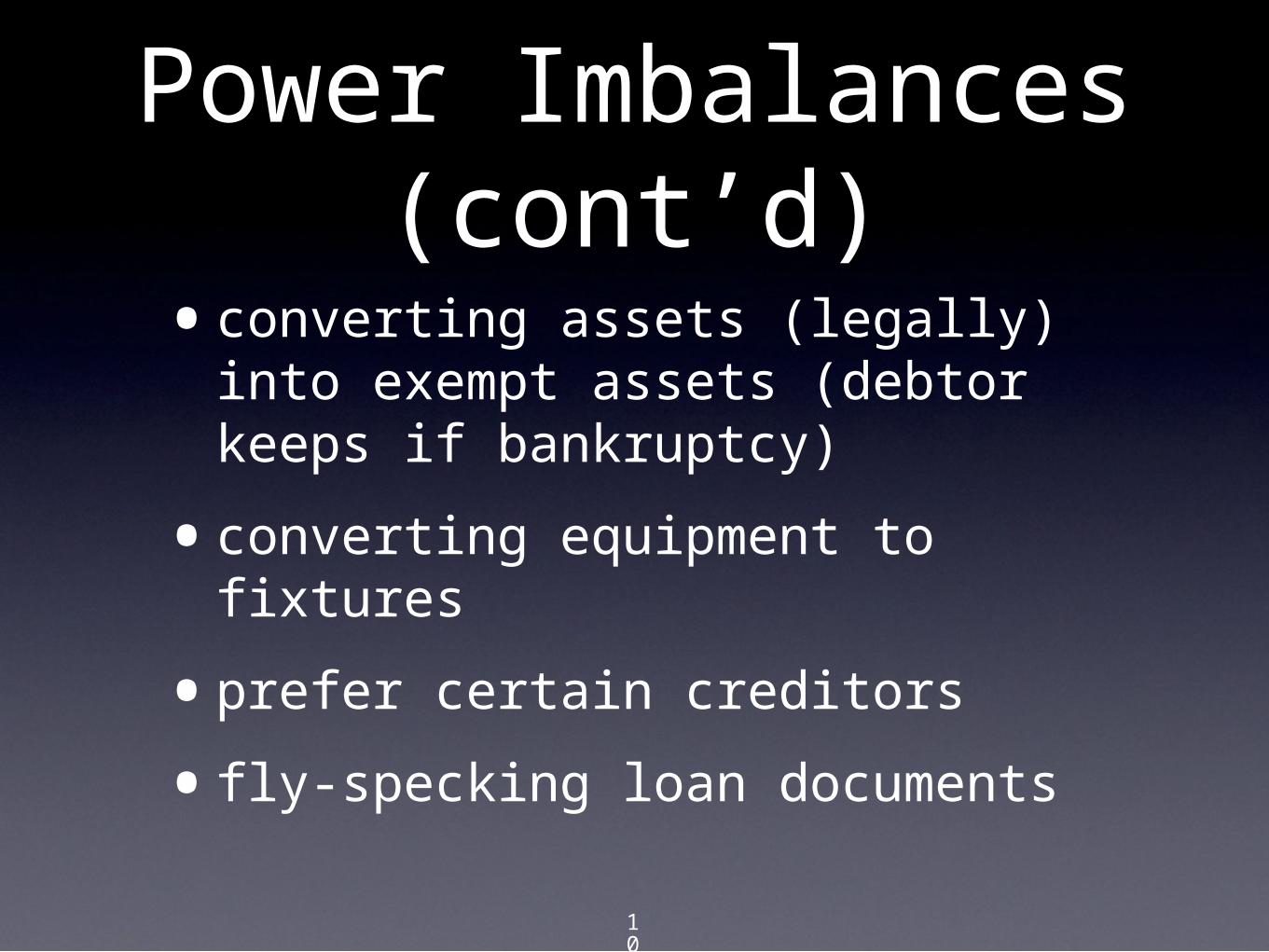

Power Imbalances (cont’d)

•converting assets (legally) into exempt assets (debtor keeps if bankruptcy)

•converting equipment to fixtures

•prefer certain creditors

•fly-specking loan documents

11

Results

•Mostly technical challenges

•Mostly unsuccessful

•Gain: mostly just delay

12

leveling the playing field

•empowering the farmers:

•Chapter 12

•cram down

•re-amortization

•lower interest rates

•new financing

13

Impact

•success rate of mediation and negotiation improved dramatically

•increased efficiency of negotiation process

•farm economy slowly crawled out of the recession in the late 80’s

14

Criticism of mediation program

•Mediators received little training on dealing with emotions

•Potential loss of home and livelihood at same time

•many Century Farms

15

16

Birth of Housing Bubble

•Principles:

•Lending often not based upon ability to repay

•Others pushed into subprime that qualified for prime lending

•100% lending

17

continued

•Adjustable payment and reverse amortization mortgages

•Lenders pass risk down the line

•Long term lending based upon short term borrowing

•Radically increase leverage

18

continued

•Ratings vastly inflated

•Regulators asleep at the wheel

19

The Players

•Investment banks

•MBS & CDO

•Tranches

•Ratings Agencies

•Flim-flammed customers around globe

20

Conflict Resolution and the Housing

Crisis

•emotions and decision making

•problems with power imbalance

21

Strong Emotions

•Anger

•Sadness

•Shame

•Frustration

•Hate

22

Emotions as major foci of mediation•need to share their stories

•need to have emotions acknowledged

•mediator as surrogate listener

•maybe first time that they have had their stories heard

23

Emotions as major foci of mediation

•Emotional Flooding

•Theory of Antonio Demasio

24

leveling the playing field

•Problems:

•Not much chance of Chapter 12-like solution for homeowners

•Wall Street owns Washington

25

continued

•Problems

•Lenders may not have authority to restructure loans - who owns paper?

•No incentive - “lenders” paid to liquidate asset, not to restructure loan

26

continued

•Possible Opportunity:

•Collateralization Process

•Challenge every mortgage

•missing notes/mortgages

•failure to record

•no assignments

27

End Run

•If:

•upside down in loan to value of house

•lender waives deficiency

28

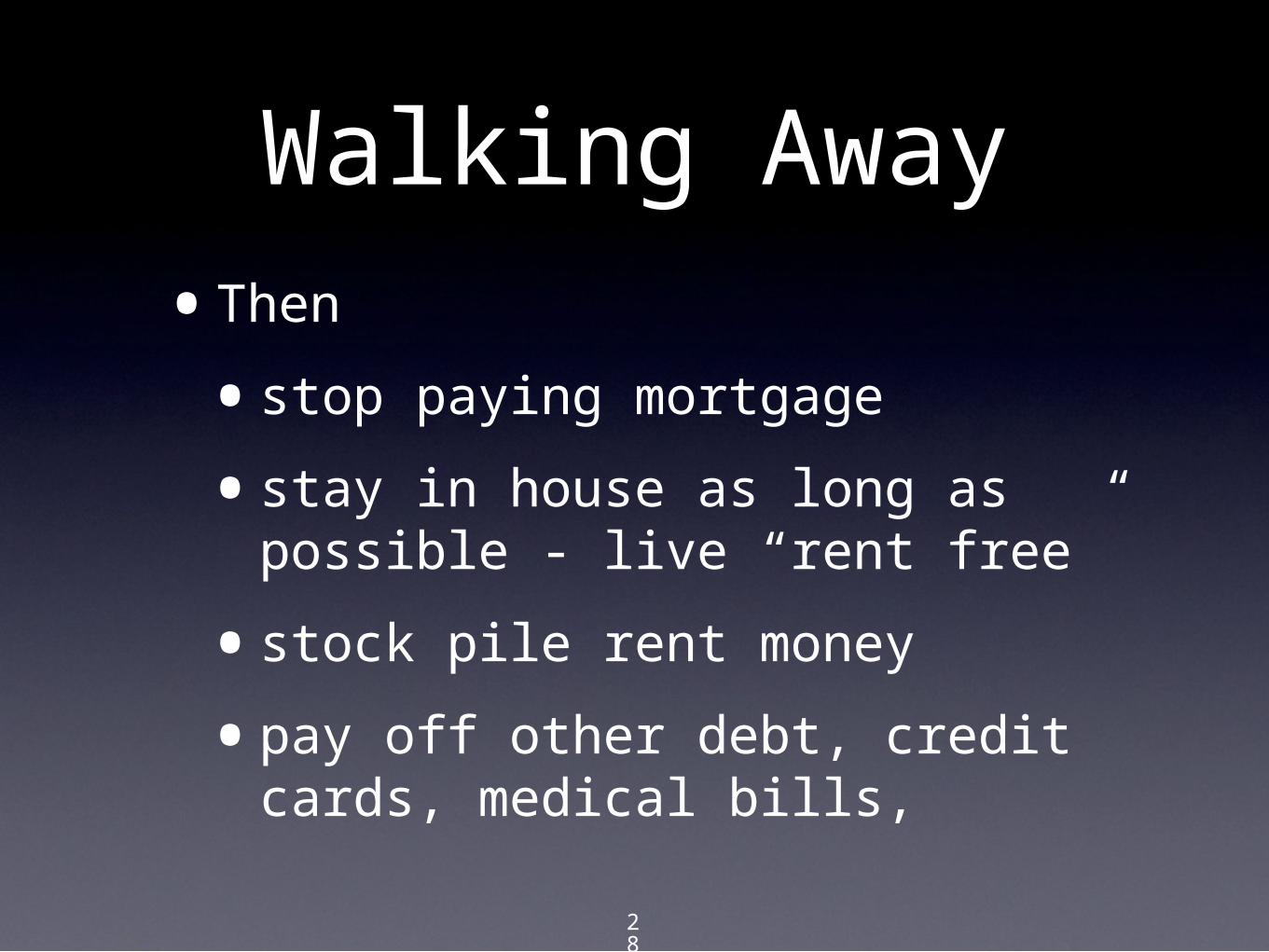

Walking Away•Then

•stop paying mortgage

•stay in house as long as possible - live “rent free”

•stock pile rent money

•pay off other debt, credit cards, medical bills,

29

•Walk away from mortgage

•No moral obligation to pay debt

•Mortgage brokers and bankers on Wall Street felt no moral obligation when they fleeced millions of homeowners and their customers around the world that bought the worthless paper

30

•Purely a cost/benefit analysis

•between doing nothing

•and

•walking and impact on your credit rating

31

Disclaimer•This is not meant as legal advice

(it is legal information only)

•By giving this presentation, there is no intent to create an attorney/client relationship

•Consult an attorney before taking any actions

•Not represent the position (official or otherwise of UGA or UNM)

32

Prognosis

•Billions of ARMS and Alt-A’s resetting each month

•L shaped bottom (at best)

•Decade or more to overcome losses

•50% loss requires 100% comeback

33

Housing industry

•At height of bubble geared up for

•Entry level buyers

•Move-up buyers

•Investor/speculator/flipper

•Second home buyer

•NINJA/subprime buyers