Embed Size (px)

Citation preview

1

The Impact of The Global Crisis on

Central and Eastern Europe by

Tonny LybekIMF’s Resident Representative in Bulgaria and Romania

at

Romanian Financial and Banking Analyst Association

BucharestDecember 8, 2009

2

Agenda

I: World Economic Outlook– Uneven signs of recovery but no time for

complacency

II: Regional Economic Outlook– From excessive credit growth to a credit crunch

III: Global Measures: Role of The IMF

IV: European Bank Coordination Initiative

– Romania’s Economic Program

V: Conclusion

3

I.1 The Global Crisis Deepest global recession since the

1930’s: In 2009, world growth is expected to decline

(1.1 percent) for the first time in 60 years! International trade declining

The phases: Sub-prime in the USA

-> Financial fragility increases (from local to global)

Sep. 15, 2008: Lehman’s Bankruptcy -> Global uncertainty and downturn

March 2009: Downturn looses speed -> Global measures, but uneven recovery

4

I.2 How Long Will It Last?

Financial shocks: Financial shocks typically lasts longer! Global integration larger than most realized!

No obvious locomotive: Unemployment is lagging! Non-performing loans (NPLs) are lagging!

Normalization of activity? Re-stocking!

Positive signs, but no time for complacency! Cautious exit of anti-crisis programs (G20 on Nov

6–7): http://www.imf.org/external/np/g20/110709.htm

5

I.3 World Economic Outlook

2007 2008Time of projection: April June Sep April June Sep

World output 5.2 3.0 -1.3 -1.4 -1.1 1.9 2.5 3.1

Advanced economies 2.7 0.6 -3.8 -3.8 -3.4 0.0 0.6 1.3 United States 2.1 0.4 -2.8 -2.6 -2.7 0.0 0.8 1.5 Euro area 2.7 0.7 -4.2 -4.8 -4.2 -0.4 -0.3 0.3 Germany 2.5 1.2 -5.6 -6.2 -5.3 -1.0 -0.6 0.3 France 2.3 0.3 -3.0 -3.0 -2.4 0.4 0.5 0.9 Italy 1.6 -1.0 -4.4 -5.1 -5.1 -0.4 -0.1 0.2 Spain 3.6 0.9 -3.0 -4.0 -3.8 -0.7 -0.8 -0.7 Japan 2.3 -0.7 -6.2 -6.0 -5.4 0.5 1.7 1.7 United Kingdom 2.6 0.7 -4.1 -3.8 -4.4 -0.4 0.1 0.9 European Union 3.1 1.0 -4.0 -4.6 -4.2 -0.3 -0.1 0.5

World trade volume 7.3 3.0 -11.0 -12.2 -11.9 0.6 1.0 2.5 Imports of advanced economies 4.7 0.5 -12.1 -13.5 -13.7 0.4 0.6 1.2 Imports of emerg. & dev. countries 13.8 9.4 -8.8 -9.6 -9.5 0.6 0.8 4.6 Exports of advanced economies 6.3 1.9 -13.5 -14.9 -13.6 0.5 1.3 2.0 Exports of emerg. & dev. countries 9.8 4.6 -6.4 -6.5 -7.2 1.2 1.4 3.6

Source: Table 1.1 in World Economic Outlook, April 2009; Table 1 in World Economic Outlook Update , July 2009,

IMF; and Table 1.1 in World Economic Outlook, October 2009 , IMF.

2009 2010

Real GDP and World Trade, Annual Change in Percent

6

II.1 Central and Eastern Europe

The Good Times 2003–07—Catching-up: Vulnerabilities were building-up!

Private sector imbalances growing rapidly!– Increasing current account deficits– Increasing exposures to Western banks

Public finances looked much better than they were! Convergence process not fully appreciated!

Crisis came late to the region: Initial denial made it difficult to take early

action! The five stages: Denial -> Resentment -> Bargaining -> Depression -> Acceptance!

7

II.2 Current Account Deficits Increased

8

II.3 Current Account Deficits Fueled by Capital Inflows

Cumulative net capital inflows, 2003-07(Percent of 2003 GDP)

-50

0

50

100

150

200

Czech Republic Poland Hungary Slovak Republic Lithuania Estonia Romania Latvia Bulgaria

Other FDI Portfolio Total

9

II.4 Increasing Exposure to Western Banks

10

II.5 The Credit Boom Was Fueled by Western European

BanksChange in exposure Western Banks and Change in Credit to GDP ratio, 2003-08(Percent of GDP)

Slovakia

Romania

Poland

Lithuania

Latvia

Hungary

Estonia

Czech Republic

Bulgaria

0

10

20

30

40

50

60

0 10 20 30 40 50 60

Change in exposure Western Banks

Ch

ange

in C

red

it t

o G

DP

rat

io

11

II.6 Exposures During Previous Crises: Lessons To Be Learned?

Figure 12. Exposure of Western Banks to Selected Regions(Billions of US dollars, adjusted for exchange rate changes.

Source: BIS, locational statistics.

Eight New Member States

0

50

100

150

200

250

300

350

400

450

500

Dec.2002 Dec.2004 Dec.2006 Dec.2008

Emerging Europe

0

100

200

300

400

500

600

700

800

900

1000

Dec.2002 Dec.2004 Dec.2006 Dec.2008

Asia

0

50

100

150

200

250

300

350

400

450

500

Mar.1992 Sep.1993 Mar.1995 Sep.1996 Mar.1998 Sep.1999

Latin America

0

50

100

150

200

250

Dec.1977 Sep.1979 Jun.1981 Mar.1983 Dec.1984

12

II.7 Much of The Lending in FX

13

II.8 Impact of The Global Crisis

Shock I: Lower external demand Shock II: Slowdown in capital inflows:

Foreign direct investment (FDI) Funding of—mainly foreign-owned—banks! Direct borrowing by non-financial companies

Slow-down in domestic demand: Delaying investments, particularly construction Uncertainty about employment Slower wage growth and lower remittances Wealth effects (asset prices) => From excessive credit growth to a credit crunch!

Some already ripe for a home-grown crisis: Imbalances differed among CEE countries Cushions differed among countries => IMF has tried to stress differences in the region!

14

II.9 Vulnerabilities and Severity of Recessions

Have Varied

15

II.10 Regional Economic Outlook

2007 2008Time of projection April June Sep Nov April June Sep Nov

Baltics Estonia 7.2 -3.6 -10.0 … -14.0 … -1.0 … -2.6 … Latvia 10.0 -4.6 -12.0 … -18.0 … -2.0 … -4.0 … Lithuania 8.9 3.0 -10.0 … -18.5 … -3.0 … -4.0 …

Central Europe Hungary 1.2 0.6 -3.3 … -6.7 … -0.4 … -0.9 … Poland 6.8 4.9 -0.7 … 1.0 … 1.3 … 2.2 …

Southeastern Europe Bulgaria 6.2 6.0 -3.5 -7.0 -6.5 … -1.0 -2.5 -2.5 … Croatia 5.5 2.4 -3.5 … -5.2 … 0.3 … 0.4 … Romania 6.2 7.1 -4.1 -8.0 -8.5 -7.8 0.0 1.7 0.5 0.5

Source: Table 2.4 in World Economic Outlook, April 2009; Table 1 in World Economic Outlook Update ,

July 2009, IMF; and Table A4 in World Economic Outlook, October 2009, IMF.

2009 2010

Real GDP, Annual Change in Percent

16

III.1 Coordinated Global Measures

Avoid the mistakes of the 1930s: Avoid a liquidity crisis becoming a solvency crisis Avoid trade restrictions and capital controls Avoid excessive competing depreciations

Coordinated policy actions (G20 statements): Central banks provide ample liquidity Governments allow stimulus subject to fiscal

space Global coordination:

The changing role of the IMF World Bank, EBRD, EIB, etc. The European Union (EU)

17

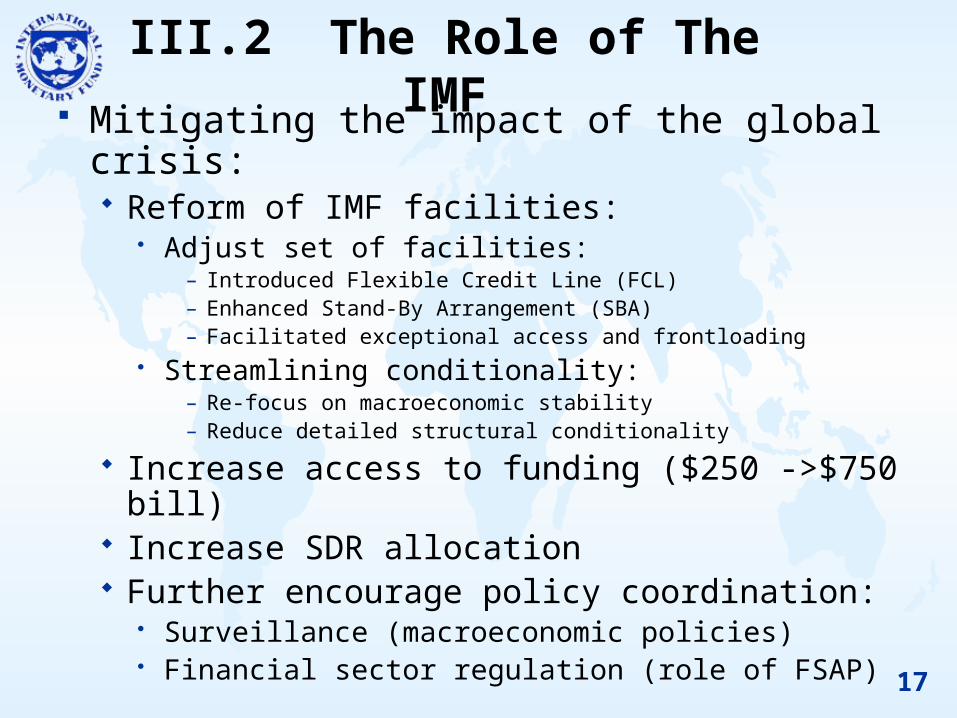

III.2 The Role of The IMF Mitigating the impact of the global crisis:

Reform of IMF facilities: Adjust set of facilities:

– Introduced Flexible Credit Line (FCL) – Enhanced Stand-By Arrangement (SBA)– Facilitated exceptional access and frontloading

Streamlining conditionality:– Re-focus on macroeconomic stability– Reduce detailed structural conditionality

Increase access to funding ($250 ->$750 bill)

Increase SDR allocation Further encourage policy coordination:

Surveillance (macroeconomic policies) Financial sector regulation (role of FSAP)

18

III.3 IMF Assistance Suddenly Needed

Access levels and growth declines in Fund arrangements

MNG

THA

IDN

KOR

ARG

PHL

IDN

UKR

BRA MEX

RUS

TUR

IDN

ARG

BRA

TUR

URY

BRA

COL

ARG ARG

TUR

IRQ

LVA

ISL ROM

HUN MEX

POL

COL

UKR

BIH

SRB

PAK

BLR

ARM

LKA

GEO

SLV CRI

GTM

SYC

-30

-25

-20

-15

-10

-5

0

5

10

1997 1999 2001 2003 2005 2007 2009

Perc

en

t ch

an

ge i

n r

eal

GD

P 1

/

Sources: WEO and staff calculations.1/ Maximum cumulative decline in three years from program inception; projected changes for current programs.

19

III.4 IMF Lending Activities

Member Date of Expiration Total Amount Undrawn OutstandingArrangement

Belarus SBA 12-Jan-09 11-Apr-10 2.3 0.9 1.4Bosnia and Herzegovina SBA 8-Jul-09 30-Jun-10 1.0 0.8 0.2Hungary SBA 6-Nov-08 5-Apr-10 10.5 2.9 7.6Iceland SBA 19-Nov-08 31-May-11 1.4 0.7 0.7Latvia SBA 23-Dec-08 22-Mar-11 1.5 0.8 0.7Romania SBA 4-May-09 3-May-11 11.4 5.4 6.1Serbia SBA 16-Jan-09 15-Apr-11 2.6 1.9 0.7Ukraine SBA 5-Nov-08 4-Nov-10 11.0 4.0 7.0Poland FCL 6-May-09 5-May-10 13.7 13.7 0.0Total Europe 55.5 31.1 24.4Total 108.8 78.6 30.9 o/w Europe in percent 51.0 39.6 79.0

Source: International Monetary Fund.Note: 1 SDR = 1.08804 € on October 31, 2009.

In billions of SDR

IMF Lending Arrangements, October 31, 2009

20

IV.1 Romania: A Case in Point

Global crisis made it increasingly difficult to secure external financing: Large short-term private debt

Large fiscal imbalances even in good years, make financing challenging during a recession

=> Emerging credibility problem!

=> In need of a “safety belt”!!

21

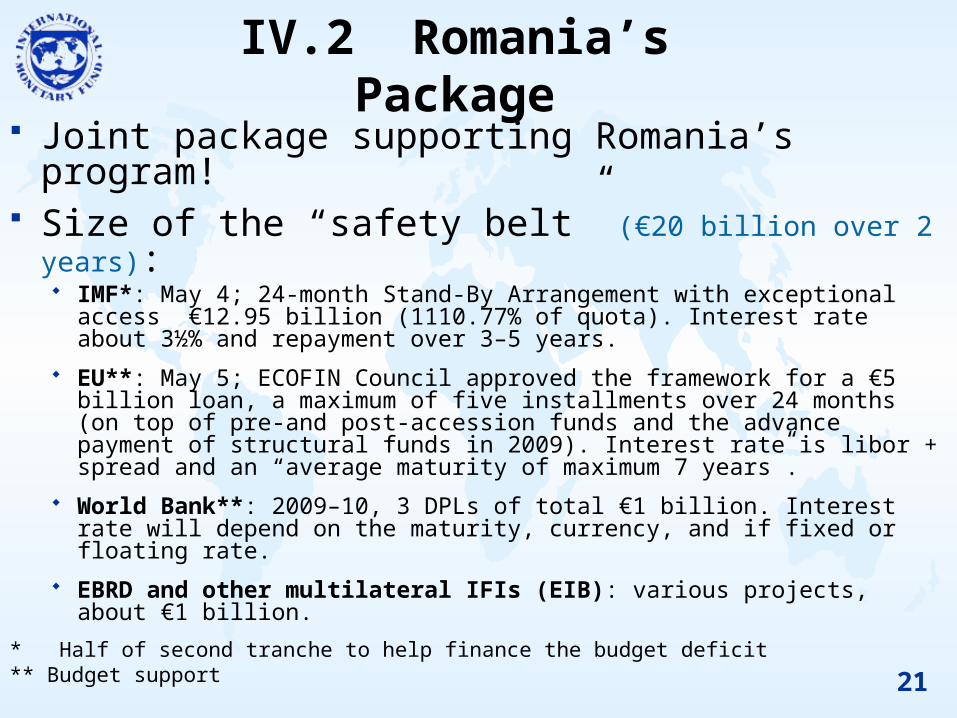

IV.2 Romania’s Package

Joint package supporting Romania’s program!

Size of the “safety belt” (€20 billion over 2 years): IMF*: May 4; 24-month Stand-By Arrangement with exceptional

access €12.95 billion (1110.77% of quota). Interest rate about 3½% and repayment over 3–5 years.

EU**: May 5; ECOFIN Council approved the framework for a €5 billion loan, a maximum of five installments over 24 months (on top of pre-and post-accession funds and the advance payment of structural funds in 2009). Interest rate is libor + spread and an “average maturity of maximum 7 years”.

World Bank**: 2009–10, 3 DPLs of total €1 billion. Interest rate will depend on the maturity, currency, and if fixed or floating rate.

EBRD and other multilateral IFIs (EIB): various projects, about €1 billion.

* Half of second tranche to help finance the budget deficit** Budget support

22

IV.3 Romania’s Economic Program

A: “European Bank Coordination Initiative”: foreign- owned banks remain committed to Romania!

B: Government addresses fiscal imbalances: Fiscal consolidation: ensure sustainability! Improve fiscal governance: ensure predictability!

C: NBR continues to maintain sound banking system: Ensure prompt and early action

D: Price stability remains primary objective of monetary policy (inflation-targeting)

23

IV.4 European Bank Coordination Initiative

For instance, part of programs in: Romania, Hungary, Serbia, Bosnia & Herzegovina

Romania: Nine largest foreign-owned banks committed to: (i) maintain exposure to Romania, and (ii) increase capital (CAR 8% -> 10) in line with

stress tests during the program period:– Vienna meeting on March 26, 2009– Brussels meeting on May 19, 2009– Bucharest meeting on August 6, 2009– Brussels meeting on November 18, 2009

24

IV.5 Market ReactionsEURNM CDS Spreads 5-year(In basis points)

0

200

400

600

800

1000

1200

1400

Jun-08 Sep-08 Dec-08 Mar-09 Jun-09 Sep-09 Dec-09

Bulgaria

Czech Republic

Estonia

Latvia

Lithuania

Hungary

Poland

Romania

Slovak Republic

Source: Bloomberg

September 15, 2008Lehmann Brothers files for bankruptcy

March 25, 2009 Agreement at staff level on Romania's Economic Program

April 2, 2009 G20 Statement

in London

October 1, 2009 Romania's coalition government splits

25

V Conclusion Global financial crisis is deep!

Financial integration is significant! Positive signs, but not time for complacency!

The IMF is mitigating the crisis by: Intensified coordination:

member countries, other IFIs, EU, and banks Providing financing to smooth the

adjustment:– Should not be an excuse to delay structural reforms!

Functioning as an external anchor provided authorities are committed!

26

Thank you very much for your attention