Embed Size (px)

Citation preview

1

Topic 53: Property Titling Community property: states

Equal ownership property acquired during marriage Step up in basis for entire property

Even though only half included in gross estate Property also included in probate estate: not JWROS

Decedent controls disposition No need to split gifts

Quasi-community property Property acquired in a separate property state prior to

moving to a community property state treated as community property

Separate property Acquired before marriage Gift/inheritance Personal injury payment

2

Topic 53: Property Titling JWROS

Avoids probate First to die has no control over disposition Can sever interest to create tenant in

common Income divided equally on 1040 Step up in basis for one-half If not with spouse, include entire amount in

taxable estate unless show survivor’s contribution

3

Topic 53: Property Titling Tenancy by Entirety

Both spouse must consent to property transfer Not subject to claims against one spouse

Tenants in Common Control disposition Subject to probate

Trusts Not subject to probate Must actually transfer asset to trust

4

Topic 54: Methods Transfer at Death By law: JWROS By contract: life insurance and retirement beneficiaries

Primary/Contingent/None

By trust: under terms of trust POD/TOD Deed delivered to escrow agent

Completed gift for estate tax purposes although income still taxed to grantor until death since deed not recorded

5

Topic 54: Methods Transfer at Death

Intestate: die without valid will Distribution based on state law Generally closest to furthest relatives

Probate Public info Can be costly Reduces chances of creditor’s future claims

6

Topic 54: Methods Transfer at Death

Probate Estate All assets passing under will and assets

with estate as beneficiary Avoiding probate

JWROS Living trust Payable on death/Transfer on death

Ancillary probate Real estate located in another state

7

Topic 55: Estate Planning Documents

Wills Codicils: revisions Holographic: handwritten. Valid in some states Nuncupative: oral. Need disinterested

witnesses.

Will contest: challenge validity of will Not sound mind Undue influence Fraud

8

Topic 55: Estate Planning Documents Power of attorney: allow someone else to act

on your behalf Health care, property

Trusts: provide Management, reduce estate taxes, avoid

creditors, prevent waste, divide income/asset

Prenuptial agreements Both parties

Must disclose all assets Should be represented by own attorney

9

Topic 56: Gifting Lifetime gifts

To minors UTMA: child receives asset at majority/can hold any type of

asset such as real estate UGMA: can only hold cash, securities

Section 2503(b) trust Income must be distributed to child each year

Income interest is a present interest qualifying for annual gift exclusion

Remainder can go to a different beneficiary Section 2503(c) trust

All trust assets distributed to beneficiary at age 21 Considered present interest/can use annual exclusion Income accumulated until age 21

Trust tax rates:

10

Topic 56: Gifting

Lifetime gifts Crummey trusts

Beneficiary has noncumulative right to withdraw annual contribution to trust Qualifies for annual gift exclusion May be restricted to > $5,000 or 5% of trust

Can only gift unlimited amount to spouse Can only gift $145,000 to non-U.S.

citizen spouse

11

Topic 56: Gifting Lifetime gifts

Basis in property received as gift Appreciated property: Donor’s cost + gift tax

paid on appreciation Loss property: < of FMV date of gift or donor’s

basis

12

Topic 57: Gift Tax Gift tax return – Form 709 required if:

Gifts more than annual exclusion Gifts of future interest Split gifts with spouse

Must split all gifts for the year

Donor pays gift tax unless net gift which requires recipient to pay gift tax

Annual exclusion: $14,000 Unified credit: credit permits gifts above annual

exclusion of $5,340,000 without gift tax

13

Topic 57: Gift Tax Prior taxable gifts: added back in

calculating tax on current taxable gifts Stacking taxable gifts

Qualified transfers Medical: paid directly Tuition: paid directly

Charitable gifts Not limited

14

Topic 58: Incapacity Planning Powers of Attorney

General: act in all matters Limited Durable: act even if grantor incapacitated Springing: activated when incompetent

Living wills: medical treatments desired if incompetent Guardianship: typically for children Revocable Living Trust:

Trustee can manage assets if become incompetent

15

Topic 58: Incapacity Planning

Special Needs Trust Irrevocable Established for benefit of disabled

child/parent Trustee can make discretionary distributions Doesn’t reduce public assistance

16

Topic 59: Estate Tax Unified credit: offsets estate tax on $5,340,000

in 2014 Was scheduled to revert to $1 million in 2013 Form 706: filed nine months after death

Executor liable for tax Gross Estate:

Life insurance with incidents of ownership Life insurance transferred within three years

of death Joint and survivor annuity: present value of

survivor benefits

17

Topic 59: Estate Tax

Gross Estate: Gifts if retained life interest Revocable gifts Reversionary interest if five percent

probability would revert Life insurance transferred within three

years of death Gift tax paid in last three years

18

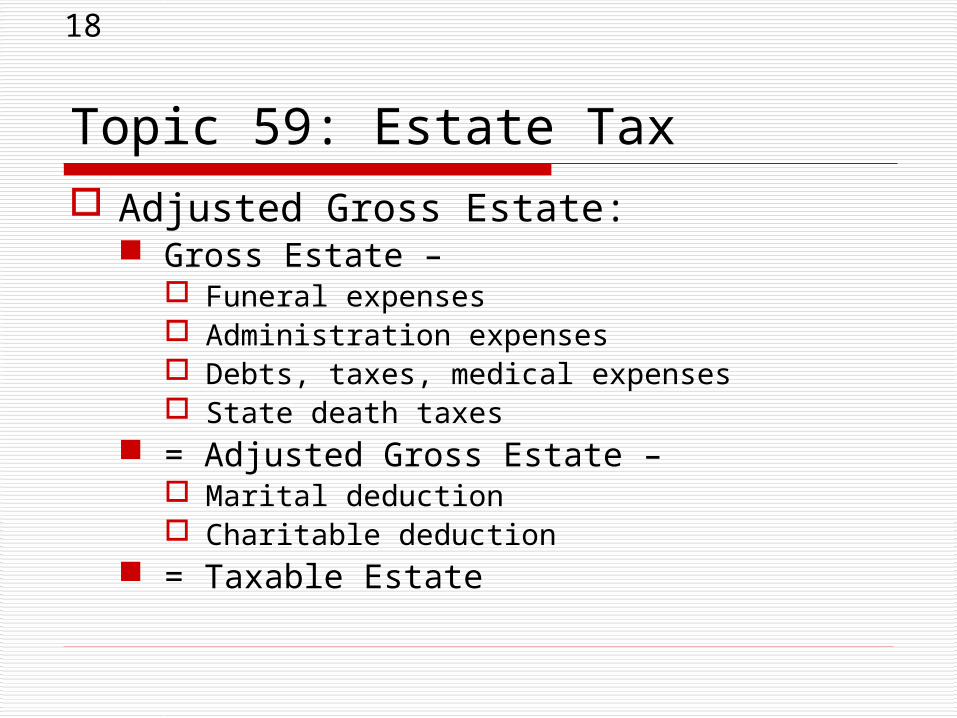

Topic 59: Estate Tax Adjusted Gross Estate:

Gross Estate – Funeral expenses Administration expenses Debts, taxes, medical expenses State death taxes

= Adjusted Gross Estate – Marital deduction Charitable deduction

= Taxable Estate

19

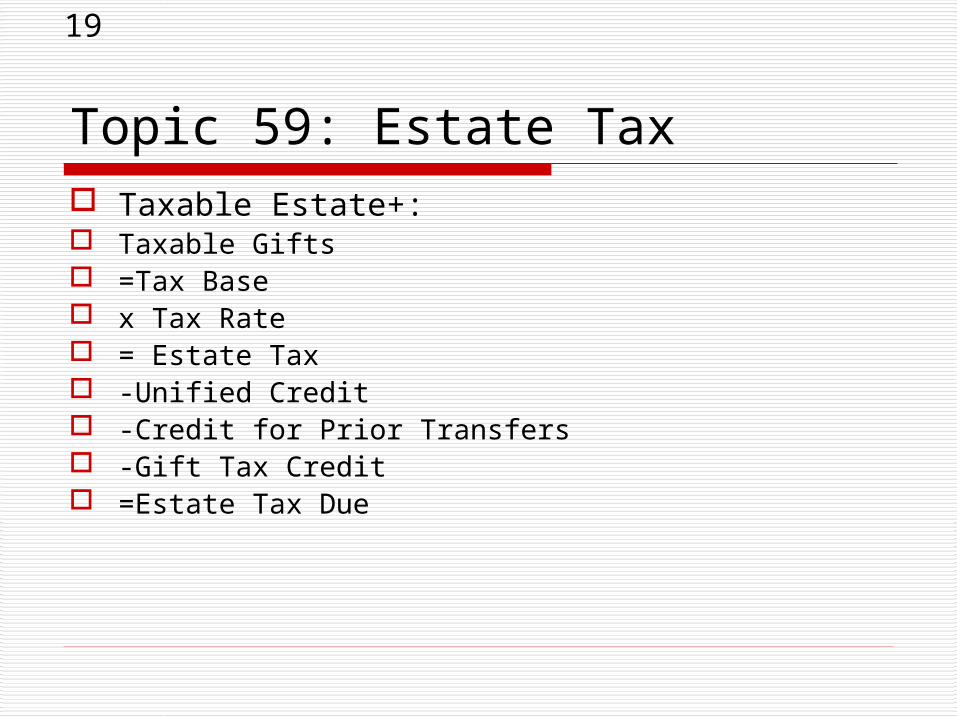

Topic 59: Estate Tax Taxable Estate+: Taxable Gifts =Tax Base x Tax Rate = Estate Tax -Unified Credit -Credit for Prior Transfers -Gift Tax Credit =Estate Tax Due

20

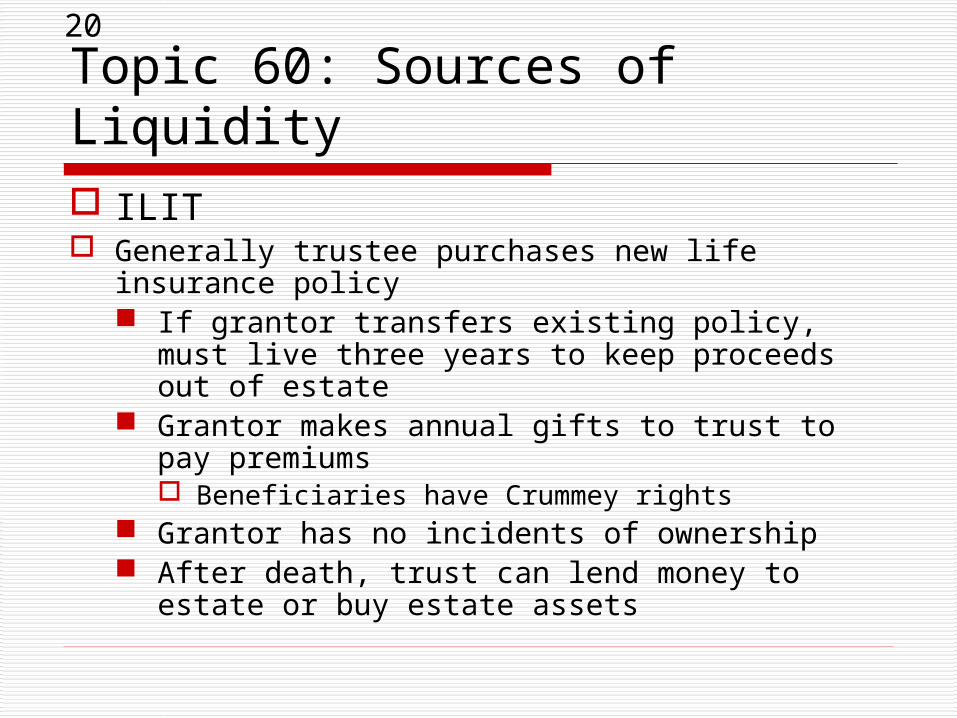

Topic 60: Sources of Liquidity ILIT Generally trustee purchases new life insurance

policy If grantor transfers existing policy, must live

three years to keep proceeds out of estate Grantor makes annual gifts to trust to pay

premiums Beneficiaries have Crummey rights

Grantor has no incidents of ownership After death, trust can lend money to estate

or buy estate assets

21

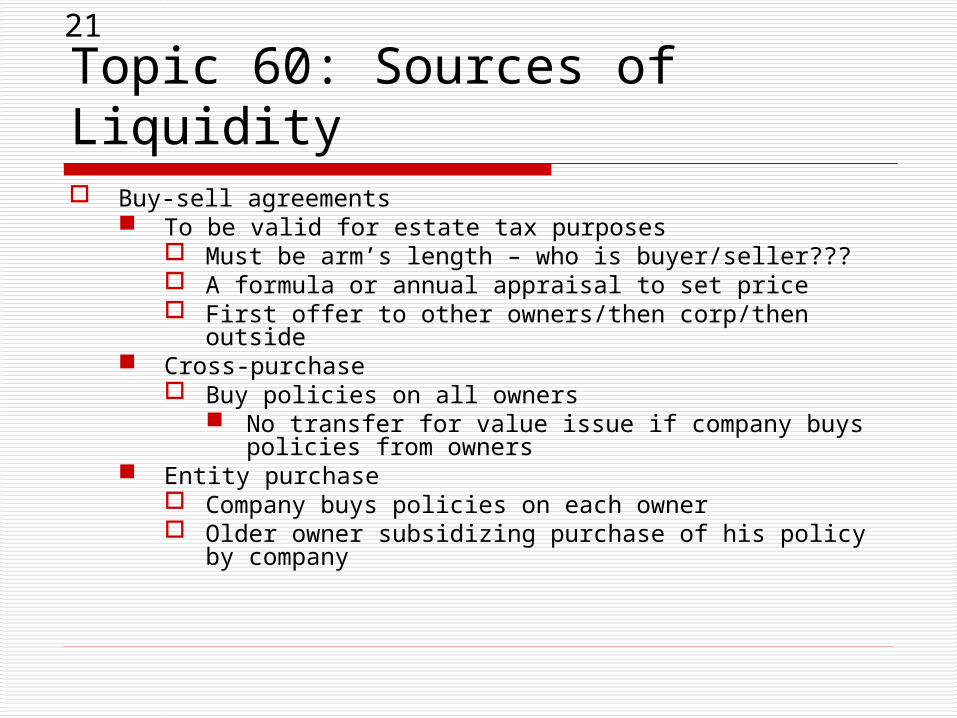

Topic 60: Sources of Liquidity Buy-sell agreements

To be valid for estate tax purposes Must be arm’s length – who is buyer/seller??? A formula or annual appraisal to set price First offer to other owners/then corp/then outside

Cross-purchase Buy policies on all owners

No transfer for value issue if company buys policies from owners

Entity purchase Company buys policies on each owner Older owner subsidizing purchase of his policy by

company

22

Topic 60: Sources of Liquidity Section 6166

Business is > 35% of adjusted gross estate Gift other assets to qualify Pay taxes in 10 payments starting five years

after death Low interest rates on deferred tax payments

Section 303 Corporation is > 35% of adjusted gross estate Stock can be redeemed to pay estate taxes and

final expenses, not to give cash to niece Redemption treated as a sale with generally no

capital gain due to step up in basis

23

Topic 61: Powers of Appointment Provide flexibility in estate plan

Final decision as to asset disposition left to others Needs better known at that time

General power of appointment Can transfer assets to anyone including holder

If holder predeceases grantor, assets included in holder’s estate

Limited power of appointment Can only transfer assets to certain individuals (not

holder)

24

Topic 61: Powers of Appointment

5 and 5 power: lapse of general power > $5,000 or 5% of trusts assets Taxable gift

To other trust beneficiaries If holder of power dies, assets which could

have been appointed to himself but weren’t during year included in estate

Crummey power General power to appoint must last at least

30 days

25

Topic 61: Powers of Appointment

Ascertainable Standard Health Education Maintenance Support

Limits power of appointment so not included in beneficiary’s estate

26

Topic 62: Types of Trusts Simple:

Must distribute all income Capital gains generally not income

Taxed to beneficiaries $300 exemption

Complex: Can accumulate income

If does so, taxable to trust Can make distributions to charities $100 exemption

27

Topic 62: Types of Trusts Revocable:

Can be changed by grantor at any time At death, becomes irrevocable

Not in probate estate In taxable estate

Irrevocable: Grantor gives up control over trust assets

Not in probate estate Not in taxable estate

28

Topic 62: Types of Trusts Inter vivos: created while alive Testamentary: created at death Totten: bank account

Beneficiary receives account at death No gift as depositor could withdraw

funds Spendthrift: limits access to trust

assets by beneficiaries to keep them from creditors, charming ex-spouses

29

Topic 62: Types of Trusts Bypass: receives assets equal to unified

credit ($ 5,3400,000 in 2014) Marital: qualifies for marital deduction as

surviving spouse has general power of appointment over assets

QTIP: decedent determines who will receive assets Qualifies for marital deduction as surviving

spouse has right to income from property Include in surviving spouse’s estate

30

Topic 62: Types of Trusts Pourover: often receives assets from

probate estate. “ Left over” assets Sprinkling: allows trustee to allocate

income among trust beneficiaries based on needs, abilities

Income beneficiary Remainder beneficiary: receives trust

assets after income interest terminates

31

Topic 62: Types of Trusts Rule Against Perpetuities

Trust must end 21 years after death of last beneficiary alive when trust was created Keeps assets from being removed from economy

States such as Illinois allow dynasty trusts Discretionary: trustee decides how much to distribute or

accumulate from trust

32

Topic 63: Qualified Interest Trusts GRAT (grantor retained annuity)

Fixed payment to grantor for term of years Remainder to beneficiary

Removes appreciation from estate Gift = Assets transferred – retained annuity

Works very well now with low Sec 7520 rates Low rates = higher value of retained annuity Goal is for asset to outperform Sec 7520

rate Can’t make additional contributions to trust

33

Topic 63: Qualified Interest Trusts GRUT (grantor retained unitrust)

Fixed percent of assets to grantor for term of years Amount of payment would change each year

based on value of assets Assets should be easily valued

Remainder to beneficiary Doesn’t remove all appreciation from estate since

grantor shares Gift = Assets transferred – retained annuity Can make additional contributions to trust

34

Topic 63: QPRTs Transfer personal residence to trust

Gift to beneficiaries = home value –retained interest Retain right to live in for term of years At end of term, residence is transferred to trust

beneficiaries Grantor survives term

Residence removed from estate Must pay rent

Fail to survive, value of home in estate

35

Topic 64: Charitable Transfers CRUT (charitable remainder unitrust)

Fixed percent of assets to grantor for term of years (20 or less) or life

5 -50% of assets transferred to CRUT Remainder to charity

Must be at least 5% of initial value Gift = Assets transferred – retained

annuity Can make additional contributions to

trust

36

Topic 64: Charitable Transfers CRAT (charitable remainder annuity

trust) Fixed payment to grantor for term of

years (20 or less) 5 -50% of assets transferred to CRAT

Remainder to charity Must be at least 10% of initial value

Gift = Assets transferred – retained annuity

No additional contributions to trust

37

Topic 64: Charitable Transfers CLUT (charitable lead unitrust)

Fixed percent of assets to charity for term of years (20 or less)

5% minimum Remainder to beneficiary

Must be at least 5% of initial value Gift = Assets transferred – remainder

interest Can make additional contributions to

trust

38

Topic 64: Charitable Transfers

CLAT (charitable lead annuity trust) Fixed payment to charity for term of

years (20 or less) 5% minimum Remainder to beneficiary

Must be at least 5% of initial value Gift = Assets transferred – remainder

interest No additional contributions to trust

39

Topic 64: Charitable Transfers Pooled income fund

Transfer property, typically appreciated stock, to charitable trust

Contains property from other donors Annual payment to beneficiary based on

trust income for life Can name more than one income

beneficiary At death of last income beneficiary,

property transferred to charity

40

Topic 64: Charitable Transfers Private Foundations

Donor retains control over organization Major philanthropy Must distribute 5% of assets Can’t own more than 20% of corporation

Donor Advised Funds Contribute to fund, take deduction Later fund manager make grants to

charities as requested by donor

41

Topic 65: Life Insurance

Incident of ownership Name beneficiary Surrender and get cash value Receive dividends Borrow against policy Pledge as collateral

42

Topic 65: Life Insurance

Ownership Have insurable interest can buy policy Policies can be sold or transferred Beneficiary designation can be changed

unless irrevocable

Life insurance transferred within three years of death included in estate

43

Topic 67: Valuation Issues Estate freeze – transfer future appreciation

Exchange common stock for common and preferred stock Then gift common stock which should have most

future appreciation Chapter 14 rules now require value to generally all

be assigned to retained interest unless: Keep some common and preferred and give

some of both Retain preferred stock with a fixed dividend

payment Gift preferred and retain common

44

Topic 67: Valuation Issues Minority interest discount

No control = 10 –35% discount Control premium

Higher value for shares Marketability discount

Hard to sell = 15 – 50% discount Blockage discount

Large block publicly traded stock 1 – 5% discount

45

Topic 67: Valuation Issues Key person discount

Impact of death of key person on business Percent discount varies

Generally property valued at date of death Alternate valuation date: six months after death

Must lower estate taxes Doesn’t apply to assets such as IRA, 401(k)

Special Use Valuation $1,090,000 reduction in value of farm land in 2014 Heirs must continue to farm Farm must be at least 50% of estate

46

Topic 66: Marital Deduction Requirements

Surviving spouse U.S. citizen If not, must use QDOT

Not a terminable interest: Unless transferred to a QTIP Can require spouse to survive up to 180 days Terminable interest: trust income stops if

remarry Qualifying property

Outright bequests to spouse Transfers to marital trusts

47

Topic 66: Marital Deduction

QTIP Executor elects QTIP Must include QTIP property in surviving

spouse’s estate Income must be paid to spouse annually First to die spouse names remainder

beneficiaries of trust

48

Topic 66: Marital Deduction

QDOT Similar to QTIP For non U.S. citizen spouse When distribute trust principal must

withhold estate tax Estate taxes payable at death of second

spouse

49

Topic 67: Defer and Minimize Estate Tax

Minimize estate tax Lifetime gifts Valuation discounts Transfer of future appreciation Charitable gifts

50

Topic 68: Intra-Family and Business Transfers Buy-sell agreements

Cross-purchase Each owner agrees to sell business interest

to other owners Each owner buys life insurance on other

owners’ lives Lots of policies; unfair if big age difference

Entity Business buy owner’s interest with life

insurance proceeds Fewer policies needed

51

Topic 66: Intra-Family and Business Transfers Installment notes

Creates income tax deferral Depreciation recapture in year of sale If seller dies before all payments received, PV of

remaining payments asset included in estate SCIN: installment note cancelled on death

Used in sale of family business Must have higher sales price due to SCIN provision No value from notes included in estate

52

Topic 67: Intra-Family and Business Transfers Private annuities

Property transferred in exchange for unsecured annuity Payments are part interest, return of basis, capital

gain Used when seller in poor health

Intrafamily loans Use proceeds to buy family business Must have market interest rate

53

Topic 67: Intra-Family and Business Transfers

Gift/sale leaseback Gift/sell property to younger generation

then lease back

IDGT: defective grantor trust Trust assets removed from estate

Irrevocable Trust income taxable to grantor

54

Topic 67: Intra-Family and Business Transfers

FLP Best for active business; not just investments Make gifts of limited partnership interests Retain general partner ownership Control business while

Removing most of business value from estate Restrict transfer of partnership interests

Qualify for minority and marketability discounts

55

Topic 69: GST

Imposed on transfers two or more generations younger than donor Grandchildren

Unless parent deceased Unrelated 37 ½ years younger than

donor 40% tax rate: in addition to estate/gift

tax

56

Topic 69: GST

Direct skip: lifetime or testamentary gift to skip person

Taxable distribution: from trust to skip person

57

Topic 69: GST

GST exemption: $5,340,000 in 2014 GST annual exclusion: $14,000 each year

Must be present interest

Calculating GST Subtract annual exclusion from taxable

gifts Allocate GST exemption to gift Multiply taxable gift after exemption x

40% (in 2014)

58

Topic 70: Fiduciaries

Types Executor: act in best interest of estate

beneficiaries Trustee: act in best interest of trust

beneficiaries Guardian: act in best interest of

minor/incompetent person

59

Topic 70: Fiduciaries Duties

Act in best interest of party represented Full disclosure Prudent investments Be impartial with regards to beneficiaries No self-dealing

Breach of duties May be personally liable Corporate/professional trustee held to higher

standards

60

Topic71: IRD

Income earned but not received before death Retirement accounts

Except Roth accounts Dividends declared/not paid Rents receivable Installment notes

Income taxed to recipient

61

Topic 71: IRD

IRD Deduction Estate tax attributable to IRD is

miscellaneous itemized deduction Not subject to 2% of AGI limitation

IRD assets No step up in basis Contrast with 10,000 shares Exxon

owned fee simple

62

Topic 72: Postmortem Planning

Alternate Valuation Date Qualified Disclaimer

Must be Irrevocable In writing Made within nine months

Can’t control who receives asset when disclaim

63

Topic 72: Postmortem Planning

Section 6166 Closely held business > 35% adjusted

gross estate Pay estate taxes over 10 years

Starts five years after return is due Reduced interest rate charged by IRS

64

Topic 72: Postmortem Planning

Section 303 Closely held business > 35% adjusted

gross estate Stock redemption treated as sale, not

dividend Capital gains treatment Amount of gain

Must use proceeds to pay estate taxes, administration and funeral expenses

65

Topic 72: Postmortem Planning Section 2032A

Real estate > 25% gross estate Farm/business > 50% gross estate Real estate valued based on current use

(farm) rather than best use Maximum reduction in value $1,090,000 in

2014 Property must pass to family members Family members must continue business

for 10 years after death

66

Topic 73: Non-Traditional Relationships

Children of prior relationships Child support Guardians

Courts prefer surviving parent Cohabitation

No marital deduction Use trust, beneficiary designations to avoid will

contests Have medical and general power of attorneys

67

Topic 73: Non-Traditional Relationships

Adoption Inherit from adopted parents

Can be disinherited In some states, from natural parents