Embed Size (px)

DESCRIPTION

http://live.gea.com/global/de/binaries/1GEA%20on%20Roadshows%20and%20Conferences%20Q1%202014%20final_tcm30-25574.pdf

Citation preview

GEA Group

Düsseldorf, May 06, 2014

Q1 2014Presentation for Roadshows and ConferencesGEA continuing operations

engineering for a better world

Disclaimer

Forward-looking statements are based on our current assumptions and forecasts. These statements naturally entail

risks and uncertainties, which may cause the actual results of operations, financial position or performance to diverge

significantly from the estimates given here. Factors that could cause such a divergence include changes in the

economic and business environment, fluctuations in exchange rates and interest rates, launches of competing

products, poor acceptance of new products or services, and changes in business strategy. We are under no obligation

to update forward-looking statements.

Due to rounding, the sum of percentages of order intake and sales by region as well as by customer industry may vary

from 100%.

2 GEA on Roadshows and Conferences - Q1 2014

engineering for a better world

Table of Contents

GEA Group in Summary

GEA on Roadshows and Conferences - Q1 2014

Pages 5 - 20

GEA Group Industry Split Page 6

Segment Performance incl. Organic Growth Rates Pages 45 – 52

Q1 2014 Results Presentation Page 24 - 39

Outlook Pages 40 – 41

GEA Group Regional Split Page 7

Historical Key Figures GEA Group and Segments Pages 61 - 65

ADR Information Page 67

3

engineering for a better world

Agenda

The GEA Group

Results Q1 2014

Backup

GEA on Roadshows and Conferences - Q1 20144

engineering for a better world

The GEA Group in Summary

• GEA provides the world with innovative solutions for smart food processing and for a more efficient use of energy resources.

• Market and technology leader for demanding equipment and process technology particularly for the food industry (72% of group sales).

• Revenue 2013: EUR 4,320 million • Emerging Market Exposure: ~40% of total sales• Operating EBIT 2013: EUR 459 million / 10.6% margin• Cash Flow Driver 2013: EUR 414 million / 9.6% of sales• Employees per 31/12/13: Around 18,000

5 GEA on Roadshows and Conferences - Q1 2014

engineering for a better world

GEA – Our Industries

6 GEA on Roadshows and Conferences - Q1 2014

FY13 Sales split: 72% Food exposure

Pharma/Chemical

Food

Beverages14%

Dairy Processing22%

23%

Milking/Farming

Others

15%

13%

13%

• 1 out of 4 liters of milk isprocessed by GEA technology

• 1 out of 3 coffeeproduction lines aroundthe world comes fromGEA

• Every 2nd liter of beer isproduced with the help ofGEA‘s processingequipment

engineering for a better world

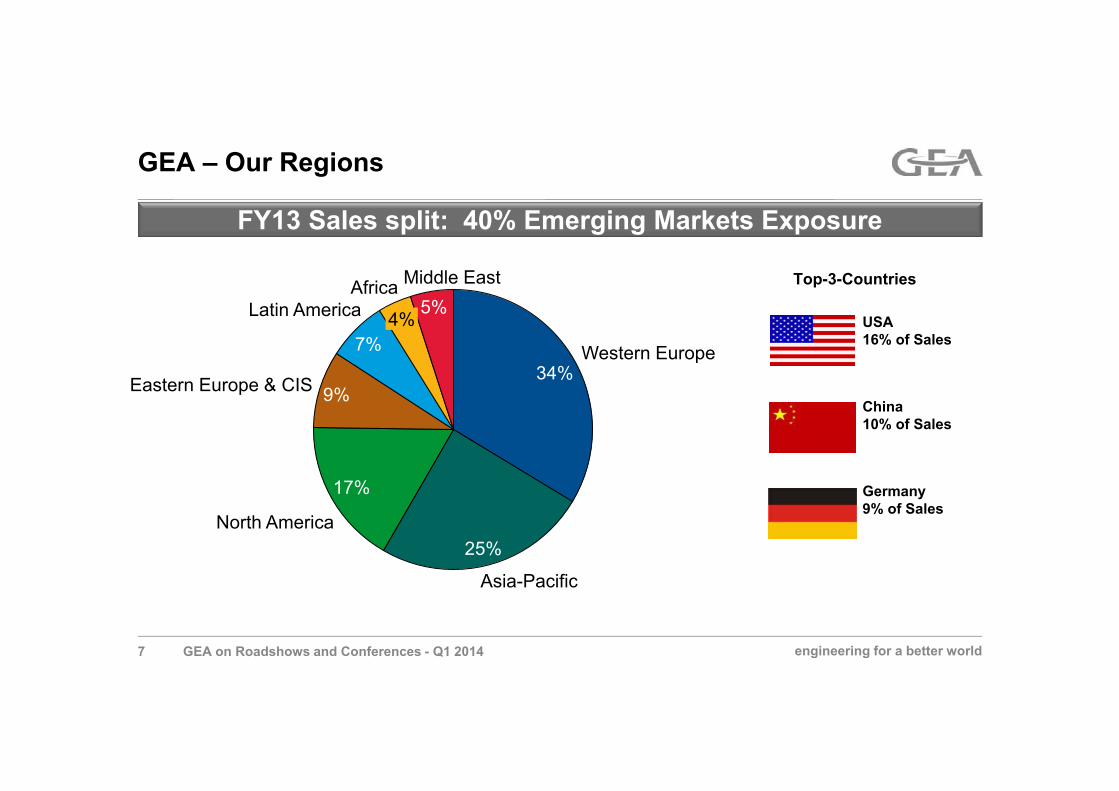

GEA – Our Regions

GEA on Roadshows and Conferences - Q1 20147

FY13 Sales split: 40% Emerging Markets Exposure

Middle East5%

17%

Asia-Pacific

25%

Africa

9%

7%34%

4%

North America

Western Europe

Latin America

Eastern Europe & CISChina10% of Sales

USA16% of Sales

Germany9% of Sales

Top-3-Countries

engineering for a better world

1,770 1,9702,562 2,956 3,070

0500

1.0001.5002.0002.5003.0003.5004.0004.500

2009 2010 2011 2012 2013

Food & Beverage

1,1761,068

1,287 1,317 1,454

0

500

1.000

1.500

2.000

2.500

3.000

2009 2010 2011 2012 2013

Emerging MarketsExposure

Food

exp

osur

e

[in EUR million]

GEA on Roadshows and Conferences - Q1 2014

Of group sales:64%

EM e

xpos

ure

GEA – increasing food and EM exposure

8

+11%+15%

+30%

+4%

+57%

+3%+38%

+5%

CAGR: +24%

CAGR: +15%Of group sales:68%

Of group sales:68%

Of group sales:72%

Of group sales:72%

Of group sales:27%

Of group sales:40%

Of group sales:43%

Of group sales:40%

Of group sales:40%

engineering for a better world

Growth drivers for GEA’s business

Megatrend Significance for demand Demand relevant for GEA

Steady growth in global population

Continuously rising demand for food and energy

Volume growth and catch-up potential especially in South and East Asia, Latin America and, in future, Africa

Growing interest in efficient production processes that conserve resources

Resource-conserving technologies/dry cooling

Energy-saving machines and processes/heat recovery

“Intelligent” engineering solutionsRising energy costs/ environmental regulations

Urbanization/expansion of middle class

Growing quality requirements for foodstuffs and pharmaceuticals

Processed foods/ready meals

Aseptic filling/enriched lifestyle drinks

Pharmaceuticals

9 GEA on Roadshows and Conferences - Q1 2014

engineering for a better world10 GEA on Roadshows and Conferences - Q1 2014

Dairy experts predict dairy trade flows to expand

• Prime export regions: NZL, NW Europe, USA, Argentina• Prime import regions: China, Russia, (sub) tropical latitudesMilk usually is shipped as powder (weighing 85% less, durable)Source and copyright of maps: © IFCN Dairy Research Center 2014, rendered by GEA Group with kind permission, consumption data: FAO Food Outlook, other (2012)

Per capita consumption:New Zealand 309 kgEU-27 287 kgUSA 276 kgBrazil 173 kg China 38 kgIndonesia 13 kg

engineering for a better world

0

20

40

60

80

100

120

140

2009 2010 2011 2012 2013

GDP GEA

GEA – Organic Sales

GEA on Roadshows and Conferences - Q1 2014

CAGR Global GDP growth 2009-2013:

+3.8%

CAGR GEA organic sales growth 2009-2013:

+5.8%

(Index 2009 = 100)

11

GEA‘s organic sales growth clearly outperforms GDP

engineering for a better worldGEA on Roadshows and Conferences - Q1 2014

722 732 802974

1,114 1,153 1,160

21.5%

26.0% 27.1%25.4%

26.9% 26.7% 26.7%

2008 2009 2010 2011 2012 2013 Q1 14 LTMService Sales GEA Service as % of Sales

GEA – Service Business

12

[in EUR million]

Service business already at EUR 1.2bn p.a.

engineering for a better world

3,3532,814 2,963

3,828 4,142 4,320 4,347

8.8%

6.8%

8.4%

10.5% 10.3% 10.6% 10.8%

0%

2%

4%

6%

8%

10%

12%

0

1000

2000

3000

4000

5000

6000

2008 2009 2010 2011 2012 2013 Q1 14 LTM

Sales Operating EBIT-margin (before ppa & one-offs)

GEA – EBIT Margin

13 GEA on Roadshows and Conferences - Q1 2014

[in EUR million]6,000

5,000

4,000

3,000

2,000

1,000

Continuous margin improvement

engineering for a better world

1,772 1,830 1,873 1,887 1,890 1,891 1,886 1,895 1,900

17.5%18.6% 18.6%

16.7%

18.8% 19.3%19.6%

22.1% 22.6%

0%

5%

10%

15%

20%

25%

0

500

1000

1500

2000

2500

3000

Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13 Q1 14

Capital Employed (average LTM) ROCE (average LTM)

GEA’s major bonus driversStrong focus on cash generation and ROCE

GEA on Roadshows and Conferences - Q1 2014

[in EUR million]

14

3,000

2,500

2,000

1,500

1,000

*ROCE LTM = EBIT (LTM) / Capital employed excluding goodwill from the acquisition of the former GEA AG by the former Metallgesellschaft AG in 1999 (average LTM)

ROCE*Cash Flow Driver Margin

500

0

142173 189 207

310355

387414 404

3.6%

4.3%4.6%

5.0%

7.4%

8.3%

9.0%9.6%

9.3%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0

50

100

150

200

250

300

350

400

450

Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13 Q1 14

Cash Flow Driver (LTM) Cash Flow Driver Margin (LTM)

engineering for a better world

GEA is independent of single customers due to very diversified customer base

Our largest customer has a revenue share of only 1.8 percent

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Top Customer Top 10 Top 50 Top 100 Top 150 Top 200

Rev

enue

Sha

re

Customer

GEA on Roadshows and Conferences - Q1 201415

~ 30% of the Top 50 customers arealready coming from Developing Markets

engineering for a better world

GEA – Segment Structure

16 GEA on Roadshows and Conferences - Q1 2014

Milking & Cooling

Farm Services

Farm Equipment

GEA Farm Technologies

13 %of Group Sales

~ 100 %food related

Operating EBIT FY 2013: 7.7%

ROCEFY 2013: 12.7%

Separators & Decanters

Homogenizers & Flow Components

Food Solutions

GEA Mechanical Equipment

30 %of Group Sales

~ 64 %food related

Operating EBIT FY 2013: 14.1%

ROCEFY 2013: 17.4%

Dairy and Brewery Systems

Aseptic Filling

Pharma Systems

GEA Process Engineering

40%of Group Sales

~ 75 %food related

Operating EBIT FY 2013: 10.5%

ROCEFY 2013: 73.2%

Compressors

Ice Machines

Freezers

GEA Refrigeration Technologies

17 %of Group Sales

~ 62 %food related

Operating EBIT FY 2013: 8.4%

ROCEFY 2013: 22.7%

engineering for a better world

Structured strategic realignment

HX Divestment

Long-term strategicdirection

Comprehensive portfolio analysis of all GEA BUs

2012 2013 – 2014

„GEA Fit for 2020“

Technology & Competence Mapping

Application StrategyAnalysis of >30 applications and

selected technologies

2015

GEA on Roadshows and Conferences - Q1 201417

engineering for a better world

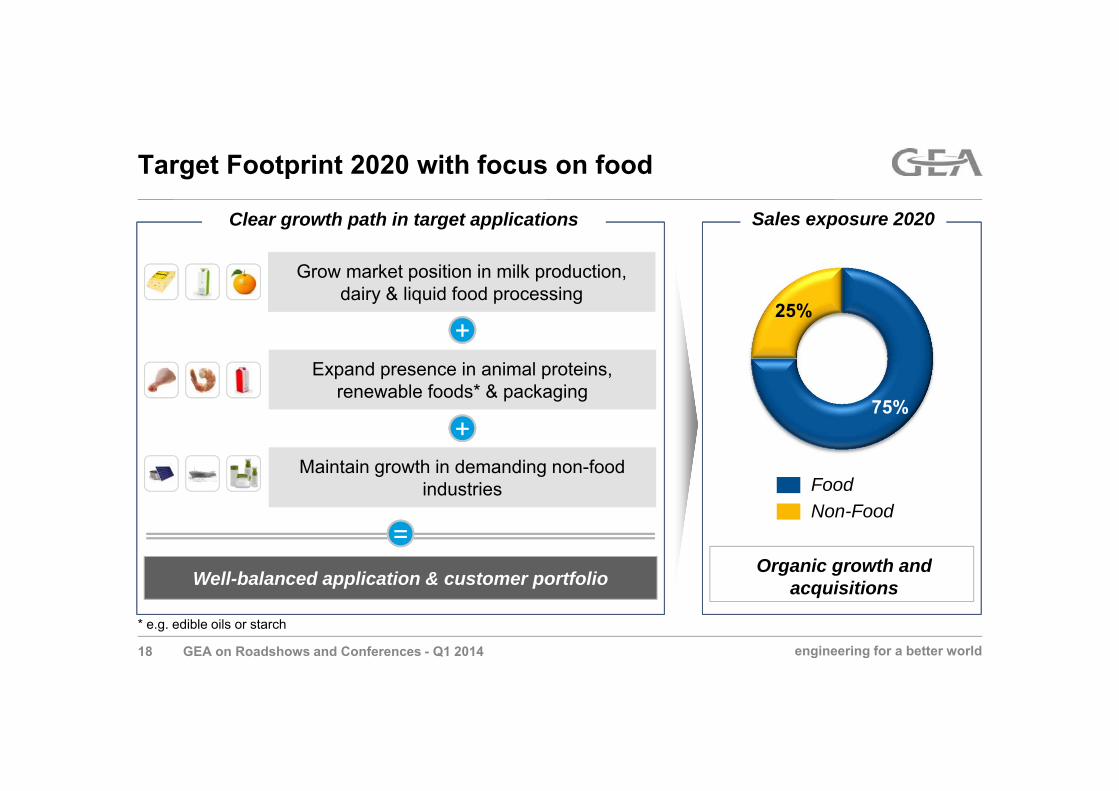

75%

25%

Target Footprint 2020 with focus on food

Clear growth path in target applications

Expand presence in animal proteins, renewable foods* & packaging

Maintain growth in demanding non-food industries

Well-balanced application & customer portfolio

++

==

Sales exposure 2020

Organic growth and acquisitions

Grow market position in milk production, dairy & liquid food processing

FoodNon-Food

++

* e.g. edible oils or starch

GEA on Roadshows and Conferences - Q1 201418

engineering for a better world

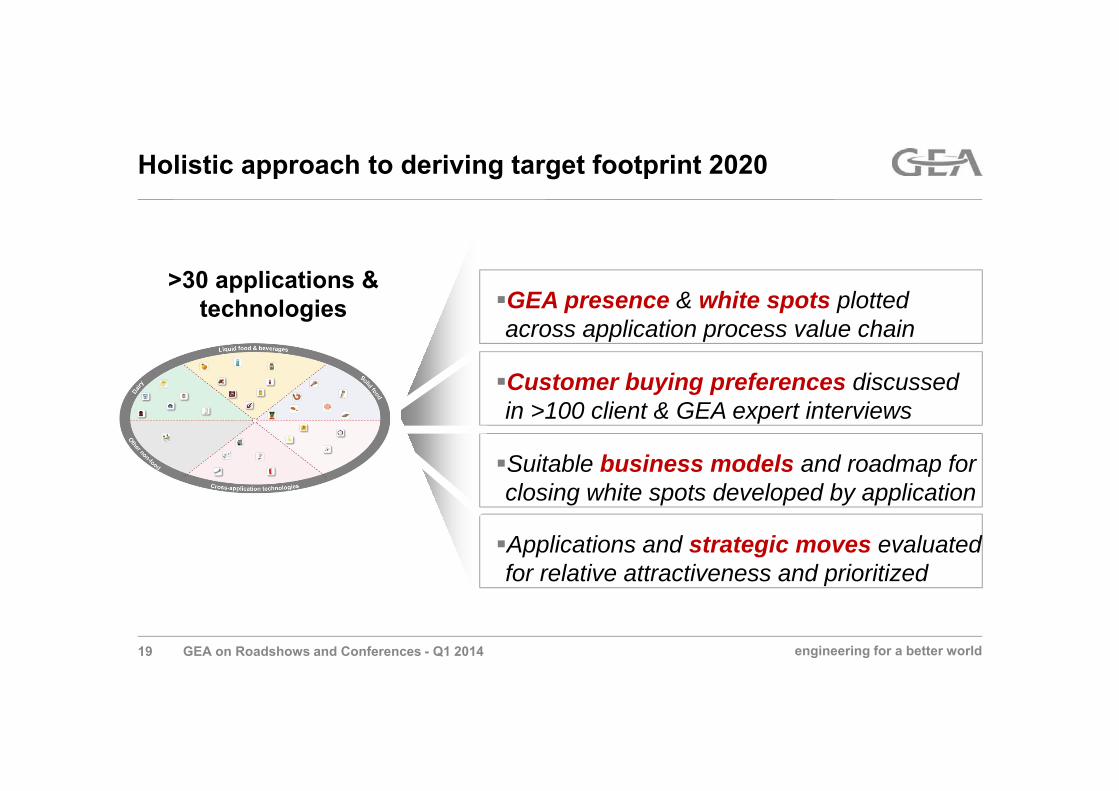

Holistic approach to deriving target footprint 2020

GEA on Roadshows and Conferences - Q1 201419

GEA presence & white spots plotted across application process value chain

>30 applications & technologies

Applications and strategic moves evaluated for relative attractiveness and prioritized

Customer buying preferences discussed in >100 client & GEA expert interviews

Suitable business models and roadmap for closing white spots developed by application

engineering for a better world

Business model & organizational cornerstones

GEA on Roadshows and Conferences - Q1 201420

Best-in-class components and engineering that meet customers’ specific application and regional preferences

Cross-business collaboration to deliver best value to customer on a global scale

Operational and organizational excellence

“Fit for 2020”

engineering for a better world21

Increasingly stringent hygiene and safety regulations in end markets

Growth driven by shift in consumer preferences towards functional, processed and convenience foods

Global leading positions with exceptionally high barriers to entry

Unrivalled quality and breadth of product range

Pure Play: Highly focused and resilient end market exposure

Balanced income split resting on strong food share of revenue of around 70-75 percent

1

2

3

4

5

6

The GEA VisionKey investment case post strategy implementation

GEA on Roadshows and Conferences - Q1 201421

engineering for a better world

Agenda

The GEA Group

Results Q1 2014

Backup

GEA on Roadshows and Conferences - Q1 201423

engineering for a better world

-2%(reported: -6%)

1,095 1,024

Q1 2013 Q1 2014

[in EUR million]

Order Intake +6%

(reported: +3%)

924 951

Q1 2013 Q1 2014

Sales

+20%

55 67

Q1 2013 Q1 2014

Operating EBIT +103 bps

6.0% 7.0%

Q1 2013 Q1 2014

Operating EBIT Margin

Key Figures continuing ops.GEA Q1 2014: Organic change YoY

GEA on Roadshows and Conferences - Q1 201424

engineering for a better world

Key Figures continuing ops.GEA Q1 2014: Operating EBITDA Development

5243 45

6268 72

85

7.0%6.3%

7.4%

8.8%

7.7% 7.8%

9.0%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0

10

20

30

40

50

60

70

80

90

Q1 08 Q1 09 Q1 10 Q1 11 Q1 12 Q1 13 Q1 14

Operating EBITDA Operating EBITDA Margin

+ 112 bps YoY[in EUR million]

Highest operating EBITDA and margin ever achieved in Q1

GEA on Roadshows and Conferences - Q1 201425

engineering for a better world

7 10

26 27

33 350

3

Q1 2013 Q1 2014

GEA FT

GEA ME

GEA PE

GEA RT

178 193

481 367

330339

139 162

Q1 2013 Q1 2014

GEA FT

GEA ME

GEA PE

GEA RT

Key Figures continuing ops.Segments Q1 2014

1,095 1,024

+3%

-24%

+8%

+16%

Operating EBIT Margin

[in EUR million]

-6%Order Intake

152 155

394 390

298 310111 127

Q1 2013 Q1 2014

GEA FT

GEA ME

GEA PE

GEA RT

924 951

+4%

-1%

+2%

+14%

+3%Sales

55 67

+4%

+6%

+36%

n.a.

+20%Operating EBIT

Q1 2013 Q1 2014 YoY

GEA FT 0.1% 2.4% +229 bps

GEA ME 11.0% 11.1% +17 bps

GEA PE 6.5% 6.8% +30 bps

GEA RT 4.8% 6.4% +161 bps

GEA Group 6.0% 7.0% +103 bps

GEA on Roadshows and Conferences - Q1 201426

engineering for a better world

[in EUR million]

Organic Growth Q1 2014 YoY: -2.5% due to missing large orders; base business strong +7% YoY

1,095

Q1 2014

1,024

OrganicFXQ1 2013

-4.0%

-2.5%

-44

-27

Q1 2014

1,024

Large Orders > EUR 15m

Orders > EUR 5m < EUR 15m

Base Orders < EUR 5m

Q1 2013

1,095 -88

+59

-8.0%

+5.4%

-6.5% -6.5%

Order Intake Bridge

-42

-3.8%

GEA on Roadshows and Conferences - Q1 201427

engineering for a better world

496 519 518 576 596 619705 686 669 737 711 702 745 710 722 724 747 754

163 157 139149 173 168

185 166 208214

172 221 175144

234 167211 160

38 61 6563

64135

135128 111

96102

124 107131

102132 67 88

16 40 3366 41

60 58100

4465 112

110

162144 121

22

0

200

400

600

800

1.000

1.200

1.400

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11(w/o FS)

Q2 11(incl.FS)

Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13 Q1 14

OI < EUR 1m OI >= EUR 1m < EUR 5m OI >= EUR 5m < EUR 15m OI >= EUR 15m

Performance continuing ops.Large Order Development since Q1 2010[in EUR million]

~7% YoY growth in orders < EUR 5m in Q1 2014 = good growth in base business

GEA on Roadshows and Conferences - Q1 201428

engineering for a better world

0 100 200 300 400 500 600

Q1 13Q2 13Q3 13Q4 13Q1 14

0 300 600 900 1200

Q1 13Q2 13Q3 13Q4 13Q1 14

0 100 200 300 400 500 600

Q1 13Q2 13Q3 13Q4 13Q1 14

0 100 200 300 400 500 600

Q1 13Q2 13Q3 13Q4 13Q1 14

0 100 200 300 400 500 600

Q1 13Q2 13Q3 13Q4 13Q1 14

0 100 200 300 400 500 600

Q1 13Q2 13Q3 13Q4 13Q1 14

0 100 200 300 400 500 600

Q1 13Q2 13Q3 13Q4 13Q1 14

0 100 200 300 400 500 600

Q1 13Q2 13Q3 13Q4 13Q1 14

Eastern Europe & CISWestern Europe

Asia Pacific

North America ∆ QoQ: -1% w/o LO*: -11%

∆ YoY: -17% w/o LO*: +8%

∆ QoQ: -32% w/o LO*: -40%

∆ YoY: -43% w/o LO*: -26%

∆ QoQ: +8% w/o LO*: -11%

∆ YoY: 0% w/o LO*: -18%

∆ QoQ: +38% w/o LO*: +22%

∆ YoY: -5% w/o LO*: +6%

∆ QoQ: -31% w/o LO*: -17%

∆ YoY: -2% w/o LO*: +25%

∆ QoQ: +10% w/o LO*: +10%

∆ YoY: -15% w/o LO*: -15%

∆ QoQ: -8% w/o LO*: +8%

∆ YoY: +5% w/o LO*: +9%

∆ QoQ: -10% w/o LO*: -5%

∆ YoY: -6% w/o LO*: +7%

[in EUR million]

Latin America

Middle EastAfrica GEA

* LO: large orders with volume of greater than EUR 5m are illustrated at the end of the bars.

Performance continuing ops.Regional Order Intake Trend as of Q1 2014

GEA on Roadshows and Conferences - Q1 201429

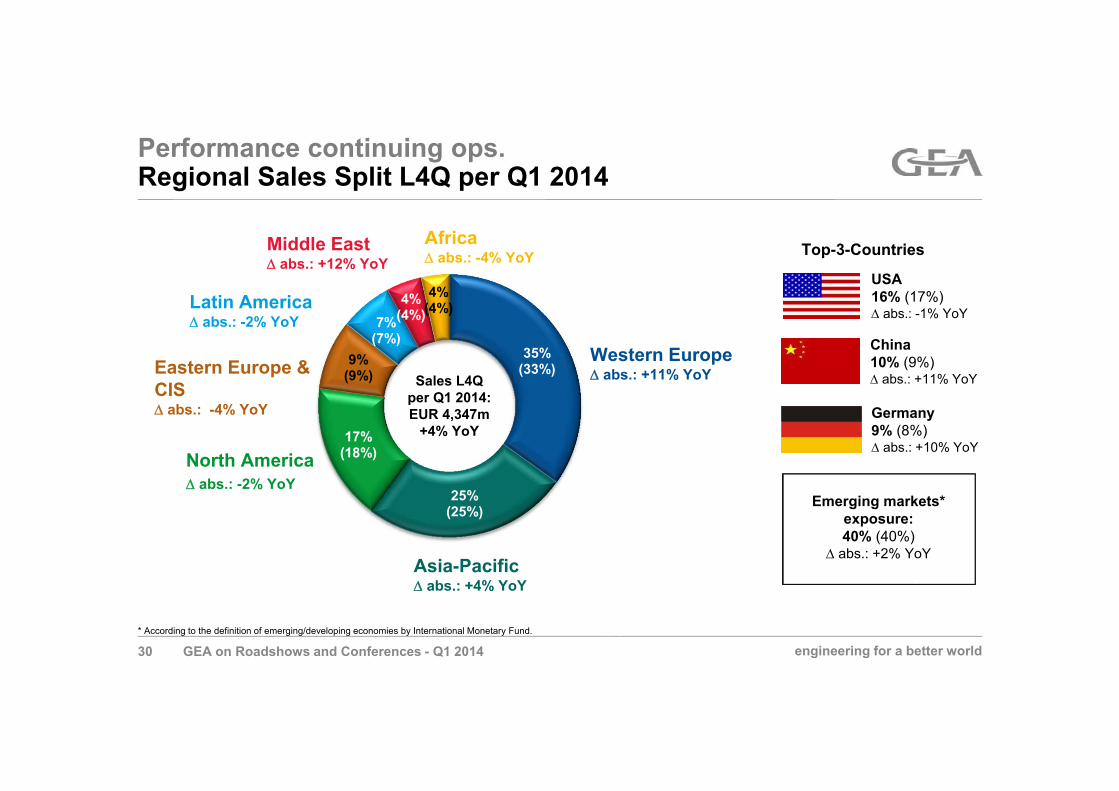

engineering for a better world

35%(33%)

25%(25%)

17%(18%)

9%(9%)

7%(7%)

4%(4%)

4%(4%)

Emerging markets* exposure: 40% (40%)

abs.: +2% YoY(Durchschnitt der Definition von Dow

Jones und MSCI*)

Sales L4Q per Q1 2014:EUR 4,347m

+4% YoY

Performance continuing ops.Regional Sales Split L4Q per Q1 2014

China10% (9%) abs.: +11% YoY

USA16% (17%) abs.: -1% YoY

Germany9% (8%) abs.: +10% YoY

Top-3-Countries

Western Europe abs.: +11% YoY

Asia-Pacific abs.: +4% YoY

North America abs.: -2% YoY

Latin America abs.: -2% YoY

Eastern Europe & CIS abs.: -4% YoY

Middle East abs.: +12% YoY

Africa abs.: -4% YoY

* According to the definition of emerging/developing economies by International Monetary Fund. Dow Jones Emerging Markets Index besteht aus 35 Ländern, von denen 20 für GEA relevant sind; MSCI definiert 21 Länder als Emerging Markets, von denen 17 für GEA relevant sind

GEA on Roadshows and Conferences - Q1 201430

engineering for a better world

13%

26%

22%

12%

12%

16%

OI L4Q per Q1 2014:

EUR 4,557m+4% YoY

Performance continuing ops.Order Intake by Customer Industry since Q4 2009*

* Average last four quarters: Q1 – Q4 2009 = Index 100

80%100%120%140%160%180%200%220%

Q409

Q110

Q210

Q310

Q410

Q111

Q211

Q311

Q411

Q112

Q212

Q312

Q412

Q113

Q213

Q313

Q413

Q114

Milking/Farming Dairy Processing GEA Group

80%

100%

120%

140%

160%

180%

Q409

Q110

Q210

Q310

Q410

Q111

Q211

Q311

Q411

Q112

Q212

Q312

Q412

Q113

Q213

Q313

Q413

Q114

Pharma/Chemical Other Industries GEA Group

80%

100%

120%

140%

160%

180%

Q409

Q110

Q210

Q310

Q410

Q111

Q211

Q311

Q411

Q112

Q212

Q312

Q412

Q113

Q213

Q313

Q413

Q114

Food Beverages GEA Group

Milking/Farming abs.: +8% YoY

Dairy Processing abs.: +32% YoY

Food abs.: -3% YoY

Beverages abs.: -19% YoY

Pharma & Chemical abs.: -12% YoY

Other Industries abs.: +11% YoY

GEA on Roadshows and Conferences - Q1 201431

engineering for a better world

Performance continuing ops.Book to Bill Ratios by Industry/Region L4Q

<= 0.8 > 0.8 and < 1.0 >= 1.2> 1.0 and < 1.2Colour code: Only cross-sections with a share of > 1% of group order intake are colored

Book to Bill categories

BtB % of OI BtB % of OI BtB % of OI BtB % of OI BtB % of OI BtB % of OI BtB % of OI BtB % of OI

Strong BtB-Ratios in Dairy Processing, Western Europe and Asia-Pacific

Book to bill ratio (L4Q) Q1 2014

Milking / Farming 1,06 5,3% 1,04 1,3% 1,03 4,3% 1,05 0,9% 1,00 0,0% 0,93 0,1% 1,01 1,4% 1,04 13,3%

Dairy Processing 1,61 12,2% 0,95 1,7% 0,67 2,3% 1,03 1,4% 1,02 0,7% 0,82 0,7% 1,26 7,2% 1,23 26,0%

Food 1,00 8,8% 0,76 1,7% 1,01 3,1% 1,23 1,5% 1,18 1,5% 1,11 0,9% 1,06 4,2% 1,01 21,7%

Beverages 0,76 3,0% 1,12 1,6% 0,60 0,9% 0,41 0,4% 1,35 0,9% 1,05 0,5% 0,90 4,2% 0,84 11,6%

Food & Beverages 1,16 29,3% 0,94 6,3% 0,87 10,6% 0,95 4,2% 1,18 3,1% 0,98 2,1% 1,08 17,0% 1,05 72,6%

Pharma 1,09 2,2% 0,90 0,6% 1,24 1,1% 1,13 0,5% 1,03 0,2% 1,54 0,3% 1,05 2,3% 1,09 7,3%

Chemical 0,75 1,0% 1,00 0,2% 0,94 0,9% 0,87 0,4% 1,40 0,1% 0,19 0,1% 1,07 1,9% 0,86 4,6%

Pharma/Chemical 0,95 3,3% 0,92 0,8% 1,08 2,0% 1,01 0,9% 1,08 0,3% 0,62 0,4% 1,06 4,2% 0,99 11,9%

Environment 1,06 1,5% 1,33 0,3% 0,67 0,5% 0,48 0,1% 0,35 0,0% 0,91 0,1% 1,56 1,4% 1,06 4,0%

Oil & Gas 1,76 0,8% 2,67 0,4% 0,93 0,8% 0,23 0,0% 0,32 0,0% 0,33 0,2% 1,17 1,5% 1,07 3,6%

Marine 0,94 1,3% 1,21 0,0% 1,02 0,1% 0,82 0,1% 0,75 0,0% 0,95 0,0% 1,43 1,6% 1,14 3,2%

Power 1,16 0,3% 12,05 0,3% 1,38 0,1% 0,98 0,2% 0,89 0,1% 0,80 0,3% 1,14 0,1% 1,23 1,4%

Others 1,01 1,0% 1,52 0,3% 1,08 0,3% 0,69 0,2% 0,97 0,1% 0,71 0,1% 1,06 1,2% 1,02 3,3%

Other Industries 1,09 4,9% 2,12 1,4% 0,88 1,9% 0,64 0,6% 0,64 0,3% 0,62 0,8% 1,29 5,7% 1,08 15,5%

Total 1,13 37,4% 1,03 8,5% 0,90 14,5% 0,91 5,7% 1,10 3,7% 0,81 3,3% 1,12 26,9% 1,05 100,0%

WesternEurope

Eastern Europe & CIS

North America Latin America Africa Middle - East Asia - Pacific Total

GEA on Roadshows and Conferences - Q1 201432

engineering for a better world

1,2501,450 1,550 1,600

331

391 433

487

0

500

1000

1500

2000

Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13 Q1 14

Order Backlog invoicable in respective FY Order Backlog invoicable after respective FY Order Intake Sales

2,000

1,500

1,000

500

0

Performance continuing ops.Top Line Trend / Order Backlog

2,136

1,581 1,644 1,7011,599

1,841 1,9011,983

2,085

1,8301,932

L4Q BtB ratio

1.07 1.04 1.06 1.06 1.07 1.081.07 1.06 1.05 1.07 1.05

#

[in EUR million]

2,015

1.07 1.05

2,087

GEA on Roadshows and Conferences - Q1 201433

engineering for a better world

1,772 1,830 1,873 1,887 1,890 1,891 1,886 1,895 1,900

17.5%18.6% 18.6%

16.7%

18.8% 19.3% 19.6%

22.1% 22.6%

0%

5%

10%

15%

20%

25%

0

500

1000

1500

2000

2500

3000

Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13 Q1 14

Capital Employed (average LTM) ROCE (average LTM)

Performance continuing ops.ROCE increases above 22%[in EUR million]

*ROCE LTM = EBIT (LTM) / Capital employed excluding goodwill from the acquisition of the former GEA AG by the former Metallgesellschaft AG in 1999 (average LTM)

0

3,000

2,500

2,000

1,500

1,000

500

+ 381 bps YoY

GEA on Roadshows and Conferences - Q1 201434

engineering for a better world

349 345 351269

404449 460

395

523 521 511

356

515 521 538

363

535

14.4%13.4%

12.4%11.6% 11.3% 11.0% 11.3% 11.4%

12.1%12.8% 12.9% 12.7% 12.2% 11.9% 11.7% 11.7% 11.8%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

100

200

300

400

500

600

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13 Q1 14

Working Capital Working Capital (average LTM) as % of sales (LTM)

- 260 bps

[in EUR million]

Working Capital / Sales ratio stabilised below 12% of sales

Performance continuing ops.Working Capital Development

GEA on Roadshows and Conferences - Q1 201435

engineering for a better world

142173 189 207

310355

387414 404

3.6%

4.3%4.6%

5.0%

7.4%

8.3%

9.0%9.6%

9.3%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0

50

100

150

200

250

300

350

400

450

Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13 Q1 14

Cash Flow Driver (LTM) Cash Flow Driver Margin (LTM)

Performance continuing ops.Cash Flow Driver Margin Development [in EUR million]

527404

122 -1

512 513

Ø WC Q2 12-Q1 13

Ø WC Q2 13-Q1 14

Cash Flow Driver LTM per Q1 14

WC LTMCAPEX LTM per Q1 14

EBITDA LTM per Q1 14

GEA on Roadshows and Conferences - Q1 201436

engineering for a better world

[in EUR million]

Cash generation LTM: EUR ~230m

Performance Net Liquidity Reconciliation incl. GEA HX

-105.9Dividend

Net Debt 31.03.2014 -432.4

CAPEX -154.4

Delta Working Capital -67.2

-261.1

-84.6

Net Debt bef. DOP, M&A and Dividend

-58.4Discontinuing Operations

Taxes / Interests

-7.0

-129.3

Others

668.4

Net Debt 31.03.2013 -494.0

Effect from acquisitions

EBITDA

+EUR 233m

GEA on Roadshows and Conferences - Q1 201437

engineering for a better world

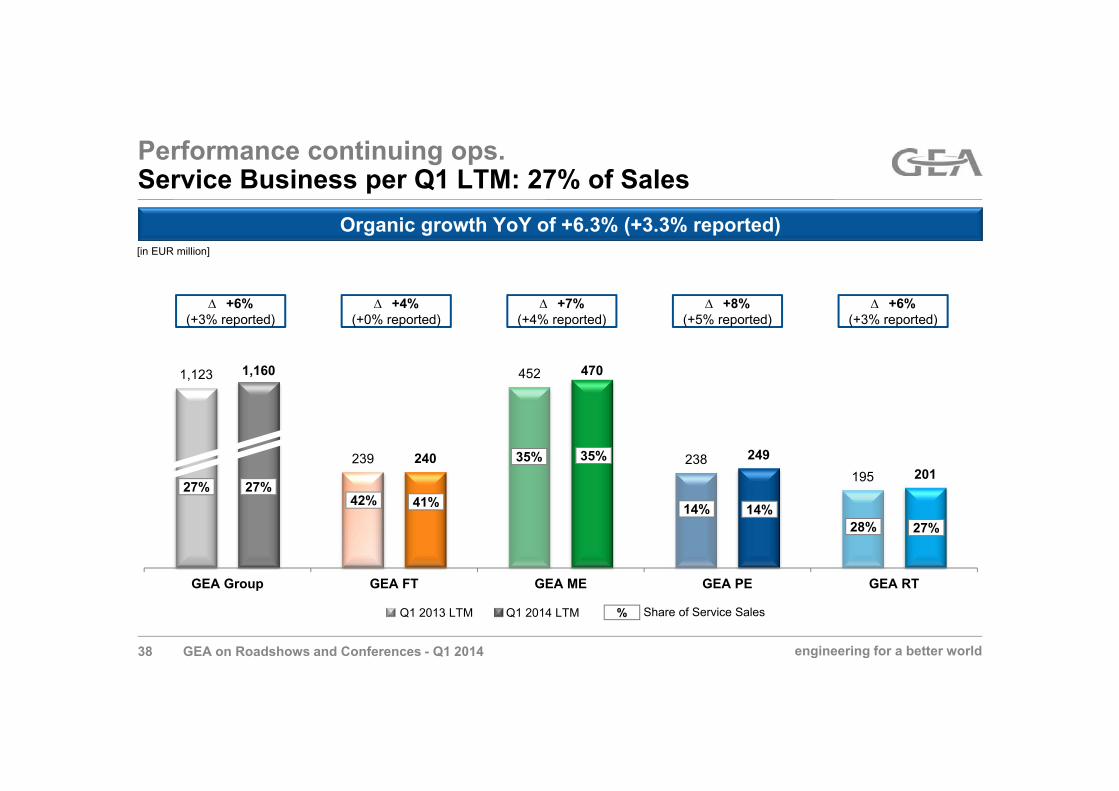

Performance continuing ops.Service Business per Q1 LTM: 27% of Sales

1,123

239

452

238195

1,160

240

470

249201

GEA Group GEA FT GEA ME GEA PE GEA RT

Share of Service Sales

Organic growth YoY of +6.3% (+3.3% reported)

+6%(+3% reported)

%

27% 27%41%

35% 35%

14% 14%28% 27%

42%

[in EUR million]

Q1 2013 LTM Q1 2014 LTM

+4%(+0% reported)

+7%(+4% reported)

+8%(+5% reported)

+6%(+3% reported)

GEA on Roadshows and Conferences - Q1 201438

engineering for a better world

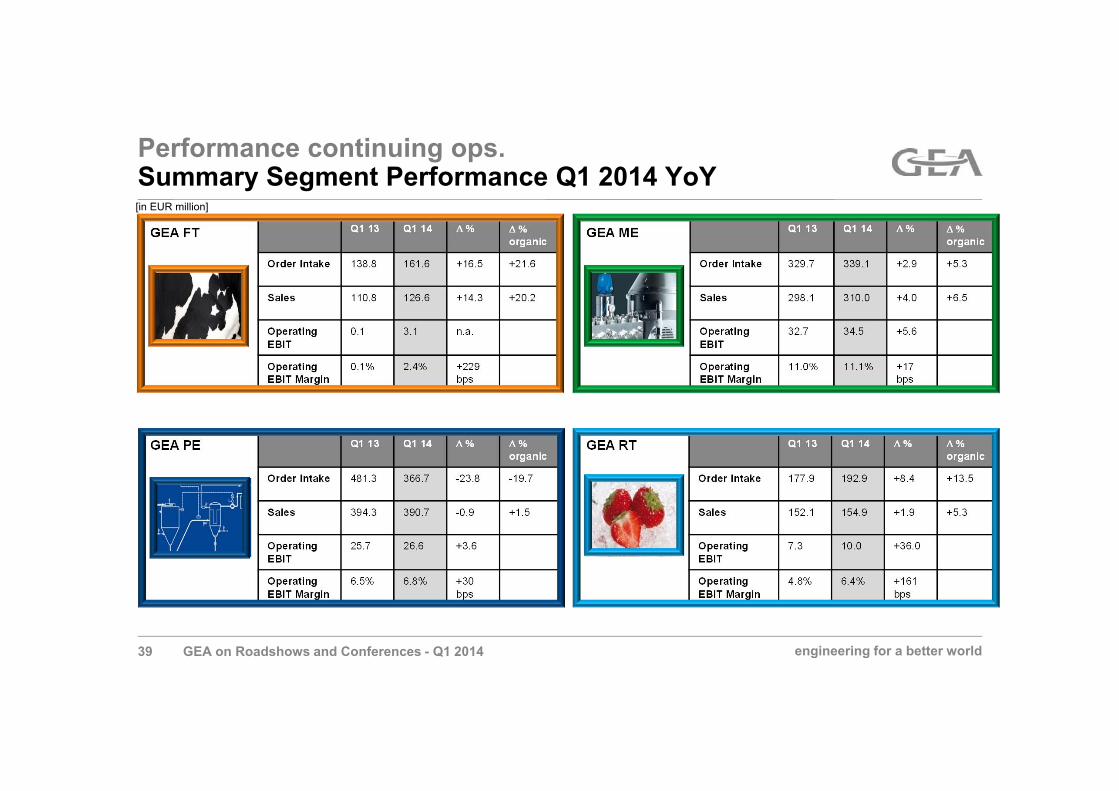

Performance continuing ops.Summary Segment Performance Q1 2014 YoY

Q1 13 Q1 14 organic

Order Intake 329.7 339.1 +2.9 +5.3

Sales 298.1 310.0 +4.0 +6.5

Operating EBIT

32.7 34.5 +5.6

Operating EBIT Margin

11.0% 11.1% +17bps

Q1 13 Q1 14 organic

Order Intake 138.8 161.6 +16.5 +21.6

Sales 110.8 126.6 +14.3 +20.2

Operating EBIT

0.1 3.1 n.a.

Operating EBIT Margin

0.1% 2.4% +229bps

GEA FT GEA ME

GEA PE GEA RT

[in EUR million]

Q1 13 Q1 14 organic

Order Intake 481.3 366.7 -23.8 -19.7

Sales 394.3 390.7 -0.9 +1.5

Operating EBIT

25.7 26.6 +3.6

OperatingEBIT Margin

6.5% 6.8% +30bps

Q1 13 Q1 14 organic

Order Intake 177.9 192.9 +8.4 +13.5

Sales 152.1 154.9 +1.9 +5.3

Operating EBIT

7.3 10.0 +36.0

OperatingEBIT Margin

4.8% 6.4% +161bps

GEA on Roadshows and Conferences - Q1 201439

engineering for a better world

Guidance FY 2014 continuing operations confirmed

Sales: moderate growth

Cash Flow Driver Margin:

EBITDA – Capex - / + Working Capital (LTM)Sales Sales Sales

Operating EBITDA: EUR 550m - EUR 590m

At the condition of no unexpected economic downturns, assuming constant FX-rates versus FY 2013 and disregarding potential acquisitions and one-off expenses we are aiming in 2014 for:

Cash Flow Driver Margin: 9.0% – 9.5%

GEA on Roadshows and Conferences - Q1 201440

engineering for a better world

Additional Financial Information for 2014 continuing ops.

Depreciation & amortization (incl PPA): around EUR 100m p.a.

Thereof impact from PPA in 2014 and around EUR 23m p.a.In subsequent years: thereof GEA FS around EUR 13m p.a.

Long term target capex level: around 2% of sales

Working Capital LTM: approx. 11% - 13% of sales LTM

Dividend policy: payout ratio around 1/3 of net income

Interest rate financial liabilities: below 3.5%

GEA on Roadshows and Conferences - Q1 201441

engineering for a better world

Investor Relations CalendarUpcoming Roadshows and Conferences

May 7, 2014 Roadshow Germany Frankfurt

May 22, 2014 Conference Sweden Stockholm

May 13, 2014 Conference Netherlands Amsterdam

May 14, 2014 Roadshow France Paris

June 3, 2014 Roadshow Germany Munich

June 11 - 13, 2014 Conference Germany Berlin

June 11 - 13, 2014 Conferences UK London

July 10 – 11, 2014 Capital Markets Day London

GEA on Roadshows and Conferences - Q1 201442

engineering for a better world

Financial Calendar

July 28, 2014 Interim Report Q2 2014

October 28, 2014 Interim Report Q3 2014

GEA on Roadshows and Conferences - Q1 201443

engineering for a better world

Agenda

The GEA Group

Results FY 2013

Backup

GEA on Roadshows and Conferences - Q1 201444

engineering for a better world

Performance continuing ops.GEA Farm Technologies

Order Intake by Customer Industry Order Intake by Region

[in EUR million]

48% 49%

32%32%

8%

7%7%

6%5%

6%

Q1 2013 Q1 2014

Latin America

Asia - Pacific

Eastern Europe& CIS

North America

Western Europe

100%100%

Q1 2013 Q1 2014

Milking/Farming∆ +17%

∆ +17%

∆ +14%

∆ +31%∆ +6%∆ -3%

Order Intake

Q12013

Q12014

∆(%)

138.8 161.6 +16.5

thereof organic: +21.6

Sales

Q12013

Q12014

∆(%)

110.8 126.6 +14.3

thereof organic: +20.2

Operating EBIT

Q12013

Q12014

∆(%)

0.1 3.1 n.a.

Operating EBIT Margin (%)

Q12013

Q12014

∆(bps)

0.1 2.4 +229

GEA on Roadshows and Conferences - Q1 201445

engineering for a better world

Performance continuing ops.GEA Farm Technologies

Quarterly Large Order Development

[in EUR million]

100116 115 116 126 130 140 129

147 144 146 143 139 151 149 151 161

1

31 1 1 5 2 1

1

0

20

40

60

80

100

120

140

160

180

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13 Q1 14OI < EUR 1m OI >= EUR 1m < EUR 5m OI >= EUR 5m < EUR 15m OI >= EUR 15m

Order Intake

L4Q per Q1 2013

L4Q per Q1 2014

∆(%)

574.5 619.6 +7.9

thereof organic: +8.8

Sales

L4Q per Q1 2013

L4Q per Q1 2014

∆(%)

573.9 593.4 +3.4

thereof organic: +4.3

Operating EBIT

L4Q per Q1 2013

L4Q per Q1 2014

∆(%)

44.5 47.5 +6.6

Operating EBIT Margin (%)

L4Q per Q1 2013

L4Q per Q1 2014

∆(bps)

7.8 8.0 +24

GEA on Roadshows and Conferences - Q1 201446

engineering for a better world

Performance continuing ops.GEA Mechanical Equipment

Order Intake by Region

[in EUR million]

40% 43%

15% 13%10% 8%8% 9%

27% 27%

Q1 2013 Q1 2014

Other Industries

Pharma/Chemical

Beverages

Dairy Processing

Food36% 39%

26% 28%

18% 15%6% 7%8% 6%4% 5%2% 2%

Q1 2013 Q1 2014

Africa

Middle - East

Latin America

Eastern Europe &CISNorth America

Asia - Pacific

Western Europe

∆ +8%

∆ -7%

∆ +7%

∆ -2%

∆ -13%

∆ +8%

∆ +8%

∆ -17%

∆ +30%∆ -30%∆ +7%∆ -10%

Order Intake

Q12013

Q12014

∆(%)

329.7 339.1 +2.9

thereof organic: +5.3

Sales

Q12013

Q12014

∆(%)

298.1 310.0 +4.0

thereof organic: +6.5

Operating EBIT

Q12013

Q12014

∆(%)

32.7 34.5 +5.6

Operating EBIT Margin (%)

Q12013

Q12014

∆(bps)

11.0 11.1 +17

Order Intake by Customer Industry

GEA on Roadshows and Conferences - Q1 201447

engineering for a better world

278 280 274336

280 271 289 289 300 301 283 311

46 30 49 42 44 26 1938 31 40

219 19 7 12 8 58 8 11 633

1718

0

50

100

150

200

250

300

350

400

Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13 Q1 14OI < EUR 1m OI >= EUR 1m < EUR 5m OI >= EUR 5m < EUR 15m OI >= EUR 15m

Performance continuing ops.GEA Mechanical Equipment

Quarterly Large Order Development

[in EUR million]

Order Intake

L4Q perQ1 2013

L4Q perQ1 2014

∆(%)

1,341.4 1,377.6 +2.7

thereof organic: +4.7

Sales

L4Q perQ1 2013

L4Q perQ1 2014

∆(%)

1,295.2 1,339.6 +3.4

thereof organic: +5.4

Operating EBIT

L4Q perQ1 2013

L4Q perQ1 2014

∆(%)

181.4 189.4 +4.4

Operating EBIT Margin (%)

L4Q perQ1 2013

L4Q perQ1 2014

∆(bps)

14.0 14.1 +13

GEA on Roadshows and Conferences - Q1 201448

engineering for a better world

Performance continuing ops.GEA Process Engineering

Order Intake by Region

[in EUR million]

44%45%

30%

20%

5%

6%

16%

21%

6%

9%

Q1 2013 Q1 2014

Other Industries

Pharma/Chemical

Food

Beverages

Dairy Processing 27% 31%

25% 31%

19%14%

9%

8%

14%

8%

2%

4%

4%

4%

Q1 2013 Q1 2014

Middle - East

Africa

Latin America

Eastern Europe& CISNorth America

Asia - Pacific

Western Europe

∆ -23%

∆ -49%

∆ -8%

∆ +3%

∆ +15%

∆ -12%

∆ -6%

∆ -42%∆ -29%∆ -59%∆ +46%∆ -29%

Order Intake

Q12013

Q12014

∆(%)

481.3 366.7 -23.8

thereof organic: -19.7

Sales

Q12013

Q12014

∆(%)

394.3 390.7 -0.9

thereof organic: +1.5

Operating EBIT

Q12013

Q12014

∆(%)

25.7 26.6 +3.6

Operating EBIT Margin (%)

Q12013

Q12014

∆(bps)

6.5 6.8 +30

Order Intake by Customer Industry

GEA on Roadshows and Conferences - Q1 201449

engineering for a better world

Performance continuing ops.GEA Process Engineering

Quarterly Large Order Development

[in EUR million]

Order Intake

L4Q per Q1 2013

L4Q per Q1 2014

∆(%)

1,820.2 1,946.4 +6.9

thereof organic: +9.7

Sales

L4Q per Q1 2013

L4Q per Q1 2014

∆(%)

1,737.4 1,794.3 +3.3

thereof organic: +6.0

Operating EBIT

L4Q per Q1 2013

L4Q per Q1 2014

∆(%)

171.8 189.2 +10.1

Operating EBIT Margin (%)

L4Q per Q1 2013

L4Q per Q1 2014

∆(bps)

9.9 10.5 +66

138 117 136 177 169 178 167 159 186 175 170 197 174 170 166 194 184

143121 110

119 133 122 116 121144

107 132 100 104 15598

13091

3861 43

58 59127

90 11182

75101 94 126

82124 50

6916 40 33

66 41 60 58100

4465 79 78

162127 121

22

0

100

200

300

400

500

600

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13 Q1 14OI < EUR 1m OI >= EUR 1m < EUR 5m OI >= EUR 5m < EUR 15m OI >= EUR 15m

GEA on Roadshows and Conferences - Q1 201450

engineering for a better world

Performance continuing ops.GEA Refrigeration Technologies[in EUR million]

Order Intake

Q12013

Q12014

∆(%)

177.9 192.9 +8.4

thereof organic: +13.5

Sales

Q12013

Q12014

∆(%)

152.1 154.9 +1.9

thereof organic: +5.3

Operating EBIT

Q12013

Q12014

∆(%)

7.3 10.0 +36.0

Operating EBIT Margin (%)

Q12013

Q12014

∆(bps)

4.8 6.4 +161

Order Intake by Region

57% 48%

4% 7%3% 4%8% 5%

28% 35%

Q1 2013 Q1 2014

Other Industries

Pharma/Chemical

Beverages

Dairy Processing

Food37% 42%

19%19%

13%14%15%

12%9%6%5%4%2%2%

Q1 2013 Q1 2014

Latin America

Middle - East

Africa

Asia - Pacific

North America

Eastern Europe& CISWestern Europe

Order Intake by Customer Industry

∆ -9%

∆ +38%∆ -32%

∆ +40%

∆ +22%

∆ +9%

∆ +24%

∆ -11%∆ +36%

∆ -12%∆ -28%

∆ +118%

GEA on Roadshows and Conferences - Q1 201451

engineering for a better world

Performance continuing ops.GEA Refrigeration Technologies

Quarterly Large Order Development

[in EUR million]

Order Intake

L4Q per Q1 2013

L4Q per Q1 2014

∆(%)

756.2 741.2 -2.0

thereof organic: +0.9

Sales

L4Q per Q1 2013

L4Q per Q1 2014

∆(%)

697.4 739.5 +6.0

thereof organic: +9.1

Operating EBIT

L4Q per Q1 2013

L4Q per Q1 2014

∆(%)

54.8 64.2 +17.0

Operating EBIT Margin (%)

L4Q per Q1 2013

L4Q per Q1 2014

∆(bps)

7.9 8.7 +82

113 121 122 120 128 145 126 135 140 139 146 142 140 134 139 146 134

1430 17 27 19

1720

35 29 2244 50

22 35 35 40 4610 5 6 19

8 2010 6

126 13

0

50

100

150

200

250

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13 Q1 14OI < EUR 1m OI >= EUR 1m < EUR 5m OI >= EUR 5m < EUR 15m OI >= EUR 15m

16

GEA on Roadshows and Conferences - Q1 201452

engineering for a better world

Performance continuing ops.Order Intake Q1 2014

Q1 2014 vs. Q1 2013

Q1 2014 vs. Q4 2013

Order Intake previousperiod 1,095 1,144

Structural Change 0 0% 0 0%

Currency Effects -44 -4.0% -4 -0.3%

Organic Development -27 -2.5% -116 -10.2%

Order Intake currentperiod 1,024 -6.5% 1,024 -10.5%

∆ abs. ∆ in % ∆ abs. ∆ in %

[in EUR million]

GEA on Roadshows and Conferences - Q1 201453

engineering for a better world

∆ abs. ∆ in % ∆ abs. ∆ in % ∆ abs. ∆ in %

[in EUR million]

Performance continuing ops.Sales Q1 2014

Q1 2014 vs. Q1 2013

Q1 2014 vs. Q4 2013

Salesprevious period 924 1,242

Structural Change 0 0% 0 0%

Currency Effects -29 -3.1% -4 -0.4%

Organic Development +55 +6.0% -287 -23.1%

Salescurrent period 951 +2.9% 951 -23.5%

∆ abs. ∆ in % ∆ abs. ∆ in %

GEA on Roadshows and Conferences - Q1 201454

engineering for a better world

Performance continuing ops. Operating EBITDA Q1 2014

∆ abs. ∆ in % ∆ abs. ∆ in % ∆ abs. ∆ in %

[in EUR million]

Q1 2014 vs. Q1 2013

Q1 2014 vs. Q4 2013

Operating EBITDA previous period 72.4 205.7

Structural Change 0 0% 0 0%

Currency Effects -2.0 -2.8% -0.2 -0.1%

Organic Development +14.8 +20.4% -120.4 -58.5%

Operating EBITDA current period 85.1 +17.6% 85.1 -58.6%

∆ abs. ∆ in % ∆ abs. ∆ in %

GEA on Roadshows and Conferences - Q1 201455

engineering for a better world

8387

72

85

Q1 2014 Operating EBITDA

One-OffsFXQ1 2014 Operating EBITDA

before FX

OrganicQ1 2013 Operating EBITDA

Q1 2014 Reported EBITDA

+15 -2 -2

+20.4%

-2.8% -2.9%

[in EUR million]

Performance continuing ops. EBITDA Bridge Q1 2014

GEA on Roadshows and Conferences - Q1 201456

engineering for a better world

USD

DKK

GBP

CNY

PLN

BRL

SGD

NZD

AUD

17%

7%

4%

5%

2%

2%

2%

3%

2%

-3.6%

0.0%

+2.8%

-1.6%

-0.7%

-18.6%

-6.0%

-3.4%

-16.8%

Currency % total Q1 3rd party Sales

FX developmentQ1 14 vs Q1 13 (avg)

Performance continuing ops.FX Development Q1 2014 YoY

CAD 1% -11.9%

GEA on Roadshows and Conferences - Q1 201457

engineering for a better world

625

551

615

872

929

912

506

647

510

477

470

481

515

363

535

TradeReceivables Inventories

Trade Payables

AdvancePayments

Working Capital

Q4 2013

Q1 2014

-17-2%

+64+12%

-137-21%

+11+2%

+172+47%

Q1 2013 +57+6%

-74-12%

+141+28%

-7-1%

-152-29%

_

_

_

[in EUR million]

Performance continuing ops.Working Capital Development

GEA on Roadshows and Conferences - Q1 201458

engineering for a better world

Performance GEA Heat Exchangers

Order Intake by Region

[in EUR million]

17%

36%

34%

32% 28%

14% 4%

5% 4%

4% 4%

3% 8%

6%

Q1 2013 Q1 2014

Others

Food &BeveragesPharma/ChemicalMarine

Power

Environment

Oil & Gas

46% 36%

10% 24%

19%

17%11%

10%3%

7%8%

3%3%

2%

Q1 2013 Q1 2014

Middle - East

Africa

Latin America

Eastern Europe &CISAsia - Pacific

North America

Western Europe

∆ +3%

∆ +42%

∆ -7%

∆ -11%

∆ +167%

∆ +1%

∆ -2%

∆ -14%∆ -50%∆ +131%

∆ -46%

Order Intake

Q12013

Q12014

∆(%)

361.9 399.7 +10.4

thereof organic: +14.8

Sales

Q12013

Q12014

∆(%)

318.1 311.4 -2.1

thereof organic: +1.1

Operating EBIT

Q12013

Q12014

∆(%)

17.8 17.6 -0.8

Operating EBIT Margin (%)

Q12013

Q12014

∆(bps)

5.6 5.7 +7

Order Intake by Customer Industry

∆ +137%

∆ -7%∆ -15%

GEA on Roadshows and Conferences - Q1 201459

engineering for a better world

Performance GEA Heat Exchangers

Quarterly Large Order Development

[in EUR million]

Order Intake

L4Q per Q1 2013

L4Q per Q1 2014

∆(%)

1,465.6 1,538.1 +4.9

thereof organic: +7.1

Sales

L4Q per Q1 2013

L4Q per Q1 2014

∆(%)

1,537.2 1,482.4 -3.6

thereof organic: -1.3

Operating EBIT

L4Q per Q1 2013

L4Q per Q1 2014

∆(%)

128.8 123.2 -4.4

Operating EBIT Margin (%)

L4Q per Q1 2013

L4Q per Q1 2014

∆(bps)

8.4 8.3 -7

250 266 256 239290 294 276 254 281 272 274

225 261 276 253 248 251

4052 46 74

37 47 6133

62 66 4554

65 48 57 61 601427 30 7 18

42 3272

33 128

3112 40

10 28 3253 73 80 31

63 104 3028 49

39 24 2989 56

0

50

100

150

200

250

300

350

400

450

500

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13 Q1 14OI < EUR 1m OI >= EUR 1m < EUR 5m OI >= EUR 5m < EUR 15m OI >= EUR 15m

GEA on Roadshows and Conferences - Q1 201460

engineering for a better world

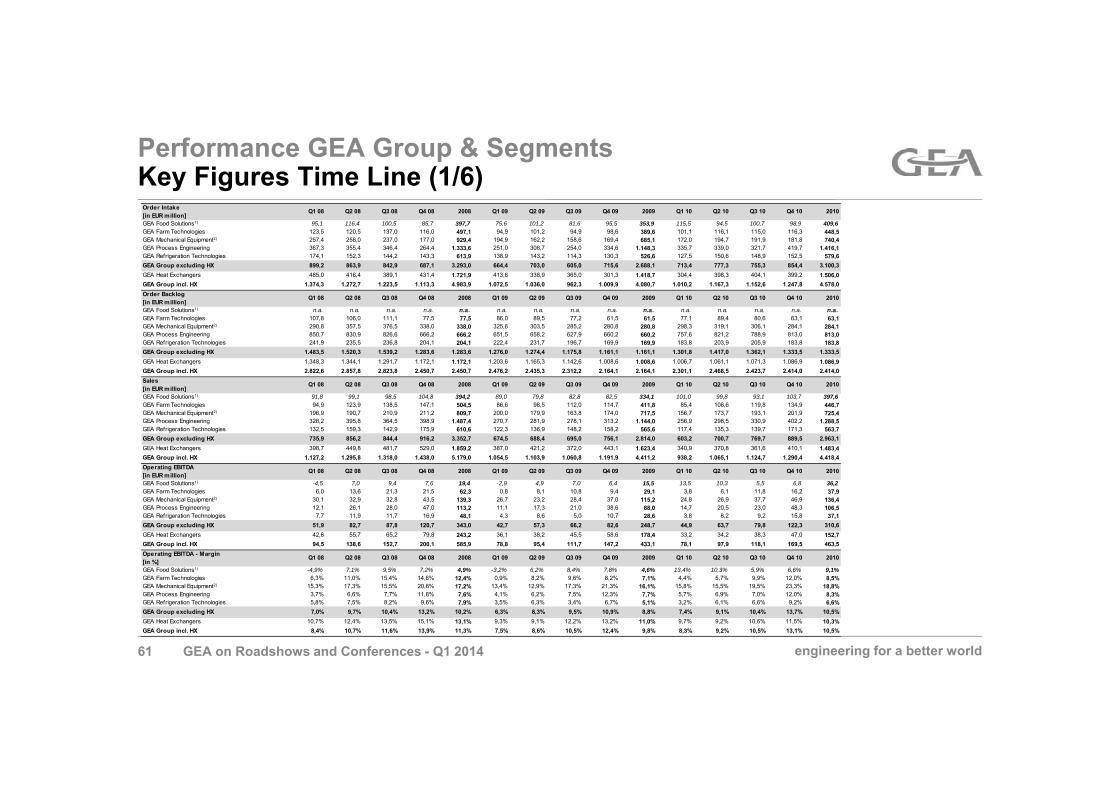

Performance GEA Group & SegmentsKey Figures Time Line (1/6)

Order Intake[in EUR million]

Q1 08 Q2 08 Q3 08 Q4 08 2008 Q1 09 Q2 09 Q3 09 Q4 09 2009 Q1 10 Q2 10 Q3 10 Q4 10 2010

GEA Food Solutions1) 95,1 116,4 100,5 85,7 397,7 75,6 101,2 81,6 95,5 353,9 115,5 94,5 100,7 98,9 409,6GEA Farm Technologies 123,5 120,5 137,0 116,0 497,1 94,9 101,2 94,9 98,6 389,6 101,1 116,1 115,0 116,3 448,5GEA Mechanical Equipment2) 257,4 258,0 237,0 177,0 929,4 194,9 162,2 158,6 169,4 685,1 172,0 194,7 191,9 181,8 740,4GEA Process Engineering 367,3 355,4 346,4 264,4 1.333,6 251,0 308,7 254,0 334,6 1.148,3 335,7 339,0 321,7 419,7 1.416,1GEA Refrigeration Technologies 174,1 152,3 144,2 143,3 613,9 138,9 143,2 114,3 130,3 526,6 127,5 150,6 148,9 152,5 579,6GEA Group excluding HX 899,2 863,9 842,9 687,1 3.293,0 664,4 703,0 605,0 715,6 2.688,1 713,4 777,3 755,3 854,4 3.100,3GEA Heat Exchangers 485,0 416,4 389,1 431,4 1.721,9 413,6 338,9 365,0 301,3 1.418,7 304,4 398,3 404,1 399,2 1.506,0GEA Group incl. HX 1.374,3 1.272,7 1.223,5 1.113,3 4.983,9 1.072,5 1.036,0 962,3 1.009,9 4.080,7 1.010,2 1.167,3 1.152,6 1.247,8 4.578,0Order Backlog[in EUR million]

Q1 08 Q2 08 Q3 08 Q4 08 2008 Q1 09 Q2 09 Q3 09 Q4 09 2009 Q1 10 Q2 10 Q3 10 Q4 10 2010

GEA Food Solutions1) n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. GEA Farm Technologies 107,8 106,0 111,1 77,5 77,5 86,0 89,5 77,2 61,5 61,5 77,1 89,4 80,6 63,1 63,1GEA Mechanical Equipment2) 290,8 357,5 376,5 338,0 338,0 325,6 303,5 285,2 280,8 280,8 298,3 319,1 306,1 284,1 284,1GEA Process Engineering 850,7 830,9 826,6 666,2 666,2 651,5 658,2 627,9 660,2 660,2 757,6 821,2 788,9 813,0 813,0GEA Refrigeration Technologies 241,9 235,5 236,8 204,1 204,1 222,4 231,7 196,7 169,9 169,9 183,8 203,9 205,9 183,8 183,8GEA Group excluding HX 1.483,5 1.520,3 1.539,2 1.283,6 1.283,6 1.276,0 1.274,4 1.175,8 1.161,1 1.161,1 1.301,8 1.417,0 1.362,1 1.333,5 1.333,5GEA Heat Exchangers 1.348,3 1.344,1 1.291,7 1.172,1 1.172,1 1.203,6 1.165,3 1.142,6 1.008,6 1.008,6 1.006,7 1.061,1 1.071,3 1.086,9 1.086,9GEA Group incl. HX 2.822,6 2.857,8 2.823,8 2.450,7 2.450,7 2.476,2 2.435,3 2.312,2 2.164,1 2.164,1 2.301,1 2.468,5 2.423,7 2.414,0 2.414,0Sales[in EUR million]

Q1 08 Q2 08 Q3 08 Q4 08 2008 Q1 09 Q2 09 Q3 09 Q4 09 2009 Q1 10 Q2 10 Q3 10 Q4 10 2010

GEA Food Solutions1) 91,8 99,1 98,5 104,8 394,2 89,0 79,8 82,8 82,5 334,1 101,0 99,8 93,1 103,7 397,6GEA Farm Technologies 94,9 123,9 138,5 147,1 504,5 86,6 98,5 112,0 114,7 411,8 85,4 106,6 119,8 134,9 446,7GEA Mechanical Equipment2) 196,9 190,7 210,9 211,2 809,7 200,0 179,9 163,8 174,0 717,5 156,7 173,7 193,1 201,9 725,4GEA Process Engineering 328,2 395,8 364,5 398,9 1.487,4 270,7 281,9 278,1 313,2 1.144,0 256,9 298,5 330,9 402,2 1.288,5GEA Refrigeration Technologies 132,5 159,3 142,9 175,9 610,6 122,3 136,9 148,2 158,2 565,6 117,4 135,3 139,7 171,3 563,7GEA Group excluding HX 735,9 856,2 844,4 916,2 3.352,7 674,5 688,4 695,0 756,1 2.814,0 603,2 700,7 769,7 889,5 2.963,1GEA Heat Exchangers 398,7 449,8 481,7 529,0 1.859,2 387,0 421,2 372,0 443,1 1.623,4 340,9 370,8 361,6 410,1 1.483,4GEA Group incl. HX 1.127,2 1.295,8 1.318,0 1.438,0 5.179,0 1.054,5 1.103,9 1.060,8 1.191,9 4.411,2 938,2 1.065,1 1.124,7 1.290,4 4.418,4Operating EBITDA[in EUR million]

Q1 08 Q2 08 Q3 08 Q4 08 2008 Q1 09 Q2 09 Q3 09 Q4 09 2009 Q1 10 Q2 10 Q3 10 Q4 10 2010

GEA Food Solutions1) -4,5 7,0 9,4 7,6 19,4 -2,9 4,9 7,0 6,4 15,5 13,5 10,3 5,5 6,8 36,2GEA Farm Technologies 6,0 13,6 21,3 21,5 62,3 0,8 8,1 10,8 9,4 29,1 3,8 6,1 11,8 16,2 37,9GEA Mechanical Equipment2) 30,1 32,9 32,8 43,5 139,3 26,7 23,2 28,4 37,0 115,2 24,8 26,9 37,7 46,9 136,4GEA Process Engineering 12,1 26,1 28,0 47,0 113,2 11,1 17,3 21,0 38,6 88,0 14,7 20,5 23,0 48,3 106,5GEA Refrigeration Technologies 7,7 11,9 11,7 16,9 48,1 4,3 8,6 5,0 10,7 28,6 3,8 8,2 9,2 15,8 37,1GEA Group excluding HX 51,9 82,7 87,8 120,7 343,0 42,7 57,3 66,2 82,6 248,7 44,9 63,7 79,8 122,3 310,6GEA Heat Exchangers 42,6 55,7 65,2 79,8 243,2 36,1 38,2 45,5 58,6 178,4 33,2 34,2 38,3 47,0 152,7GEA Group incl. HX 94,5 138,6 152,7 200,1 585,9 78,8 95,4 111,7 147,2 433,1 78,1 97,9 118,1 169,5 463,5Operating EBITDA - Margin[in %]

Q1 08 Q2 08 Q3 08 Q4 08 2008 Q1 09 Q2 09 Q3 09 Q4 09 2009 Q1 10 Q2 10 Q3 10 Q4 10 2010

GEA Food Solutions1) -4,9% 7,1% 9,5% 7,2% 4,9% -3,2% 6,2% 8,4% 7,8% 4,6% 13,4% 10,3% 5,9% 6,6% 9,1%GEA Farm Technologies 6,3% 11,0% 15,4% 14,6% 12,4% 0,9% 8,2% 9,6% 8,2% 7,1% 4,4% 5,7% 9,9% 12,0% 8,5%GEA Mechanical Equipment2) 15,3% 17,3% 15,5% 20,6% 17,2% 13,4% 12,9% 17,3% 21,3% 16,1% 15,8% 15,5% 19,5% 23,3% 18,8%GEA Process Engineering 3,7% 6,6% 7,7% 11,8% 7,6% 4,1% 6,2% 7,5% 12,3% 7,7% 5,7% 6,9% 7,0% 12,0% 8,3%GEA Refrigeration Technologies 5,8% 7,5% 8,2% 9,6% 7,9% 3,5% 6,3% 3,4% 6,7% 5,1% 3,2% 6,1% 6,6% 9,2% 6,6%GEA Group excluding HX 7,0% 9,7% 10,4% 13,2% 10,2% 6,3% 8,3% 9,5% 10,9% 8,8% 7,4% 9,1% 10,4% 13,7% 10,5%GEA Heat Exchangers 10,7% 12,4% 13,5% 15,1% 13,1% 9,3% 9,1% 12,2% 13,2% 11,0% 9,7% 9,2% 10,6% 11,5% 10,3%GEA Group incl. HX 8,4% 10,7% 11,6% 13,9% 11,3% 7,5% 8,6% 10,5% 12,4% 9,8% 8,3% 9,2% 10,5% 13,1% 10,5%

GEA on Roadshows and Conferences - Q1 201461

engineering for a better world

Performance GEA Group & SegmentsKey Figures Time Line (2/6)Order Intake[in EUR million]

Q1 11 Q2 11 Q3 11 Q4 11 2011 Q1 12 Q2 12 Q3 12 Q4 12 2012 Q1 13 Q2 13 Q3 13 Q4 13 2013 Q1 14

GEA Food Solutions1) 125,5 - - - - - - - - - - - - - - -GEA Farm Technologies 125,9 129,5 140,3 131,7 527,4 148,1 145,7 147,4 142,6 583,9 138,8 155,7 150,7 151,6 596,7 161,6GEA Mechanical Equipment2) 219,2 332,5 329,5 323,6 1.204,7 336,2 329,0 327,1 355,6 1.347,9 329,7 346,4 357,7 334,4 1.368,2 339,1GEA Process Engineering 401,5 426,2 433,3 449,0 1.709,9 511,3 401,2 468,5 469,2 1.850,2 481,3 570,0 515,2 494,6 2.061,0 366,7GEA Refrigeration Technologies 152,7 162,8 164,8 170,1 650,4 177,9 180,4 200,1 197,8 756,2 177,9 181,2 174,9 192,3 726,3 192,9GEA Group excluding HX 874,3 1.024,8 1.040,6 1.047,0 3.986,7 1.146,0 1.028,6 1.111,6 1.139,2 4.425,4 1.095,1 1.220,0 1.168,3 1.144,4 4.627,9 1.024,3GEA Heat Exchangers 375,5 445,6 369,8 462,3 1.653,2 406,1 379,0 375,1 349,7 1.509,8 361,9 363,5 348,1 426,8 1.500,3 399,7GEA Group incl. HX 1.242,1 1.462,5 1.402,8 1.502,2 5.609,7 1.544,9 1.401,0 1.477,3 1.477,9 5.901,1 1.447,1 1.574,0 1.509,2 1.562,5 6.092,7 1.415,1Order Backlog[in EUR million]

Q1 11 Q2 11 Q3 11 Q4 11 2011 Q1 12 Q2 12 Q3 12 Q4 12 2012 Q1 13 Q2 13 Q3 13 Q4 13 2013 Q1 14

GEA Food Solutions1) 104,4 - - - - - - - - - - - - - - -GEA Farm Technologies 85,4 92,5 93,9 74,4 74,4 104,5 117,3 107,1 79,9 79,9 107,8 120,9 112,2 85,6 85,6 114,3GEA Mechanical Equipment2) 304,1 431,2 445,9 395,2 395,2 446,5 452,9 442,5 438,4 438,4 442,6 446,5 456,8 428,4 428,4 456,3GEA Process Engineering 888,2 927,4 972,2 951,2 951,2 1.082,3 1.104,5 1.142,5 1.069,6 1.069,6 1.164,2 1.269,5 1.334,9 1.290,5 1.290,5 1.267,9GEA Refrigeration Technologies 210,4 206,6 206,1 197,0 197,0 224,4 245,8 265,4 257,0 257,0 283,6 268,8 253,1 229,5 229,5 272,2GEA Group excluding HX 1.581,2 1.643,7 1.700,9 1.599,2 1.599,2 1.841,1 1.900,9 1.932,4 1.829,9 1.829,9 1.982,6 2.085,3 2.136,2 2.015,5 2.015,5 2.086,7GEA Heat Exchangers 1.092,5 1.135,4 1.063,5 1.086,0 1.086,0 1.103,2 1.074,1 1.045,5 933,3 933,3 979,3 846,5 799,5 805,1 805,1 878,8GEA Group incl. HX 2.666,6 2.770,6 2.755,7 2.677,3 2.677,3 2.935,6 2.967,4 2.967,8 2.751,6 2.751,6 2.950,0 2.919,1 2.926,5 2.810,9 2.810,9 2.956,6Sales[in EUR million]

Q1 11 Q2 11 Q3 11 Q4 11 2011 Q1 12 Q2 12 Q3 12 Q4 12 2012 Q1 13 Q2 13 Q3 13 Q4 13 2013 Q1 14

GEA Food Solutions1) 112,9 - - - - - - - - - - - - - - -GEA Farm Technologies 99,6 118,3 138,1 153,8 509,8 117,8 133,1 157,8 172,3 580,9 110,8 133,8 156,9 176,2 577,7 126,6GEA Mechanical Equipment2) 191,6 311,1 317,0 371,0 1.190,7 269,3 319,2 328,6 349,2 1.266,4 298,1 334,0 336,3 359,3 1.327,8 310,0GEA Process Engineering 300,8 385,1 394,7 496,6 1.577,2 373,2 401,2 423,6 518,3 1.716,3 394,3 435,6 441,3 526,7 1.798,0 390,7GEA Refrigeration Technologies 132,8 166,6 166,2 181,6 647,2 149,5 165,2 177,0 203,1 694,8 152,1 189,2 184,8 210,6 736,6 154,9GEA Group excluding HX 706,7 964,6 980,5 1.176,4 3.828,3 880,5 994,1 1.060,5 1.207,2 4.142,3 924,2 1.064,6 1.089,1 1.242,2 4.320,0 950,7GEA Heat Exchangers 338,1 390,9 424,2 463,6 1.616,8 389,7 404,3 392,1 422,7 1.608,8 318,1 385,9 380,8 404,2 1.489,1 311,4GEA Group incl. HX 1.038,0 1.349,0 1.397,4 1.632,2 5.416,5 1.263,7 1.391,3 1.445,6 1.619,6 5.720,1 1.232,7 1.441,9 1.459,5 1.638,1 5.772,2 1.253,1Operating EBITDA[in EUR million]

Q1 11 Q2 11 Q3 11 Q4 11 2011 Q1 12 Q2 12 Q3 12 Q4 12 2012 Q1 13 Q2 13 Q3 13 Q4 13 2013 Q1 14

GEA Food Solutions1) 6,2 - - - - - - - - - - - - - - -GEA Farm Technologies 5,0 8,4 15,0 16,8 45,2 5,0 11,2 17,8 24,5 58,5 3,1 8,5 17,6 27,8 56,9 6,1GEA Mechanical Equipment2) 32,7 50,9 51,5 69,9 204,9 32,9 47,7 54,9 63,8 199,3 38,6 48,3 56,8 71,0 214,7 42,1GEA Process Engineering 20,0 31,2 38,6 73,4 163,2 20,1 39,4 43,0 75,9 178,4 29,4 45,0 46,3 82,5 203,2 30,2GEA Refrigeration Technologies 8,9 14,5 14,1 22,4 60,0 11,0 13,4 16,0 24,9 65,2 9,6 16,8 17,1 27,5 71,0 12,4GEA Group excluding HX 62,4 100,3 119,8 187,0 469,6 68,0 110,7 132,3 183,5 494,4 72,4 118,4 133,5 205,7 530,1 85,1GEA Heat Exchangers 29,5 35,3 46,9 48,7 160,4 32,6 35,9 37,5 61,5 167,5 26,1 37,6 38,6 55,9 158,2 25,8GEA Group incl. HX 91,9 135,7 166,7 235,7 630,1 100,6 146,6 169,8 245,0 661,9 98,5 156,0 172,1 261,6 688,3 110,6Operating EBITDA - Margin[in %]

Q1 11 Q2 11 Q3 11 Q4 11 2011 Q1 12 Q2 12 Q3 12 Q4 12 2012 Q1 13 Q2 13 Q3 13 Q4 13 2013 Q1 14

GEA Food Solutions1) 5,5% - - - - - - - - - - - - - - -GEA Farm Technologies 5,0% 7,1% 10,8% 10,9% 8,9% 4,2% 8,5% 11,3% 14,2% 10,1% 2,8% 6,4% 11,2% 15,8% 9,9% 4,8%GEA Mechanical Equipment2) 17,1% 16,4% 16,2% 18,8% 17,2% 12,2% 14,9% 16,7% 18,3% 15,7% 12,9% 14,5% 16,9% 19,8% 16,2% 13,6%GEA Process Engineering 6,6% 8,1% 9,8% 14,8% 10,3% 5,4% 9,8% 10,1% 14,6% 10,4% 7,5% 10,3% 10,5% 15,7% 11,3% 7,7%GEA Refrigeration Technologies 6,7% 8,7% 8,5% 12,4% 9,3% 7,3% 8,1% 9,0% 12,2% 9,4% 6,3% 8,9% 9,3% 13,1% 9,6% 8,0%GEA Group excluding HX 8,8% 10,4% 12,2% 15,9% 12,3% 7,7% 11,1% 12,5% 15,2% 11,9% 7,8% 11,1% 12,3% 16,6% 12,3% 9,0%GEA Heat Exchangers 8,7% 9,0% 11,1% 10,5% 9,9% 8,4% 8,9% 9,6% 14,5% 10,4% 8,2% 9,7% 10,1% 13,8% 10,6% 8,3%GEA Group incl. HX 8,9% 10,1% 11,9% 14,4% 11,6% 8,0% 10,5% 11,7% 15,1% 11,6% 8,0% 10,8% 11,8% 16,0% 11,9% 8,8%

GEA on Roadshows and Conferences - Q1 201462

engineering for a better world

Performance GEA Group & SegmentsKey Figures Time Line (3/6)EBITDA reported[in EUR million]

Q1 08 Q2 08 Q3 08 Q4 08 2008 Q1 09 Q2 09 Q3 09 Q4 09 2009 Q1 10 Q2 10 Q3 10 Q4 10 2010

GEA Food Solutions1) -4,5 7,0 9,4 7,6 19,4 -2,9 4,9 7,0 6,4 15,5 13,5 10,3 5,5 6,8 36,2GEA Farm Technologies 6,0 13,6 21,3 21,5 62,3 0,8 6,0 10,2 5,9 23,0 3,8 5,7 11,7 13,1 34,3GEA Mechanical Equipment2) 30,1 32,9 32,8 43,5 139,3 26,7 23,1 26,6 27,1 103,5 24,8 25,3 28,9 45,2 124,1GEA Process Engineering 12,1 26,1 28,0 47,0 113,2 10,2 14,0 11,2 30,9 66,4 14,7 19,8 22,8 48,1 105,4GEA Refrigeration Technologies 7,7 11,9 11,7 16,9 48,1 4,0 8,1 3,9 6,6 22,5 3,7 7,5 7,1 2,6 21,0GEA Group excluding HX 49,8 80,5 85,6 118,5 334,4 38,6 49,0 48,3 51,7 187,6 47,0 57,2 65,4 102,3 271,9GEA Heat Exchangers 42,6 55,7 65,2 79,8 243,2 35,5 30,7 35,2 59,4 160,8 32,1 23,4 18,7 15,2 89,4GEA Group incl. HX 94,5 138,6 152,7 200,1 585,9 76,7 82,3 87,9 121,8 368,7 76,8 83,3 86,7 118,9 365,7Operating EBIT[in EUR million]

Q1 08 Q2 08 Q3 08 Q4 08 2008 Q1 09 Q2 09 Q3 09 Q4 09 2009 Q1 10 Q2 10 Q3 10 Q4 10 2010

GEA Food Solutions1) -8,6 3,4 6,1 4,4 5,3 -8,2 1,5 3,7 3,4 0,4 9,5 7,0 1,6 3,1 21,2GEA Farm Technologies 4,3 11,9 19,5 19,5 55,2 -1,3 6,0 8,6 7,0 20,3 1,0 3,1 8,8 13,4 26,3GEA Mechanical Equipment2) 27,2 29,9 29,6 39,7 126,4 23,3 19,4 24,7 32,8 100,2 20,8 22,8 33,6 39,7 117,0GEA Process Engineering 9,5 23,5 25,2 43,6 101,8 8,0 14,2 18,0 35,5 75,7 11,5 17,2 19,8 44,7 93,2GEA Refrigeration Technologies 5,9 10,0 9,9 15,4 41,2 2,5 6,6 3,1 8,9 21,1 1,9 6,3 7,3 13,9 29,4GEA Group excluding HX 40,6 71,0 75,4 107,2 294,1 29,4 43,4 52,4 66,3 191,6 29,9 48,5 65,3 104,1 247,9GEA Heat Exchangers 36,5 49,3 58,4 72,3 216,6 28,5 29,8 37,0 49,0 144,3 24,5 25,1 29,2 40,0 118,8GEA Group incl. HX 77,1 120,6 133,6 179,1 510,4 57,9 73,3 89,4 121,4 341,9 54,4 73,6 94,5 144,3 366,8Operating EBIT - Margin[in %]

Q1 08 Q2 08 Q3 08 Q4 08 2008 Q1 09 Q2 09 Q3 09 Q4 09 2009 Q1 10 Q2 10 Q3 10 Q4 10 2010

GEA Food Solutions1) -9,4% 3,4% 6,2% 4,2% 1,3% -9,2% 1,9% 4,5% 4,1% 0,1% 9,4% 7,0% 1,7% 3,0% 5,3%GEA Farm Technologies 4,6% 9,6% 14,1% 13,2% 10,9% -1,5% 6,1% 7,6% 6,1% 4,9% 1,2% 2,9% 7,4% 9,9% 5,9%GEA Mechanical Equipment2) 13,8% 15,7% 14,0% 18,8% 15,6% 11,6% 10,8% 15,1% 18,8% 14,0% 13,3% 13,1% 17,4% 19,7% 16,1%GEA Process Engineering 2,9% 5,9% 6,9% 10,9% 6,8% 3,0% 5,0% 6,5% 11,3% 6,6% 4,5% 5,8% 6,0% 11,1% 7,2%GEA Refrigeration Technologies 4,5% 6,3% 6,9% 8,7% 6,8% 2,0% 4,8% 2,1% 5,6% 3,7% 1,6% 4,6% 5,3% 8,1% 5,2%GEA Group excluding HX 5,5% 8,3% 8,9% 11,7% 8,8% 4,4% 6,3% 7,5% 8,8% 6,8% 5,0% 6,9% 8,5% 11,7% 8,4%GEA Heat Exchangers 9,2% 11,0% 12,1% 13,7% 11,7% 7,4% 7,1% 9,9% 11,1% 8,9% 7,2% 6,8% 8,1% 9,8% 8,0%GEA Group incl. HX 6,8% 9,3% 10,1% 12,5% 9,9% 5,5% 6,6% 8,4% 10,2% 7,8% 5,8% 6,9% 8,4% 11,2% 8,3%EBIT reported[in EUR million]

Q1 08 Q2 08 Q3 08 Q4 08 2008 Q1 09 Q2 09 Q3 09 Q4 09 2009 Q1 10 Q2 10 Q3 10 Q4 10 2010

GEA Food Solutions1) -8,6 3,4 6,1 4,4 5,3 -8,2 1,5 3,7 3,4 0,4 9,5 7,0 1,6 3,1 21,2GEA Farm Technologies 4,1 11,6 18,8 18,8 53,4 -1,6 3,6 7,4 3,1 12,4 0,5 2,2 8,1 9,2 20,0GEA Mechanical Equipment2) 27,0 29,7 29,4 39,5 125,6 23,0 19,1 22,7 22,7 87,6 20,5 21,0 24,6 37,6 103,8GEA Process Engineering 9,2 23,1 24,8 43,1 100,2 6,7 10,4 7,8 27,4 52,3 11,1 16,1 19,1 43,9 90,2GEA Refrigeration Technologies 5,9 9,8 9,7 15,2 40,7 1,8 5,9 1,7 3,9 13,3 1,5 5,3 5,0 0,4 12,2GEA Group excluding HX 37,6 67,7 71,7 103,5 280,5 24,0 33,7 33,0 33,4 124,2 30,5 40,4 49,3 82,0 202,2GEA Heat Exchangers 36,4 49,1 58,1 71,8 215,4 27,2 21,8 26,0 48,8 123,8 22,8 13,4 8,9 -15,2 29,9GEA Group incl. HX 76,1 119,3 131,8 177,1 504,2 53,8 58,1 63,5 92,8 268,2 51,0 56,4 60,8 68,2 236,5

GEA on Roadshows and Conferences - Q1 201463

engineering for a better world

Performance GEA Group & SegmentsKey Figures Time Line (4/6)

EBITDA reported[in EUR million]

Q1 11 Q2 11 Q3 11 Q4 11 2011 Q1 12 Q2 12 Q3 12 Q4 12 2012 Q1 13 Q2 13 Q3 13 Q4 13 2013 Q1 14

GEA Food Solutions1) 6,2 - - - - - - - - - - - - - - -GEA Farm Technologies 5,0 8,4 15,0 16,8 45,2 5,0 11,2 17,8 24,2 58,2 2,8 8,5 17,6 27,8 56,7 6,1GEA Mechanical Equipment2) 32,7 31,4 52,1 69,9 186,1 -3,0 43,5 48,3 46,1 134,9 38,6 48,3 56,8 71,0 214,7 42,1GEA Process Engineering 20,0 31,2 38,6 73,4 163,2 20,1 39,4 42,7 75,9 178,1 29,4 45,0 46,3 82,5 203,2 30,2GEA Refrigeration Technologies 8,9 14,3 14,1 21,7 59,0 11,0 13,4 16,0 24,9 65,2 9,6 16,8 17,1 27,5 71,0 12,4GEA Group excluding HX 59,9 78,1 117,9 184,4 440,3 29,4 104,1 123,0 163,5 420,1 71,1 113,8 130,0 200,3 515,2 83,0GEA Heat Exchangers 29,5 35,3 46,9 48,6 160,3 32,6 35,9 37,5 61,5 167,5 26,0 36,3 38,4 54,5 155,2 25,8GEA Group incl. HX 91,9 116,0 167,4 234,9 610,2 64,7 142,4 162,9 226,9 597,0 98,1 152,4 168,9 240,5 659,8 106,7Operating EBIT[in EUR million]

Q1 11 Q2 11 Q3 11 Q4 11 2011 Q1 12 Q2 12 Q3 12 Q4 12 2012 Q1 13 Q2 13 Q3 13 Q4 13 2013 Q1 14

GEA Food Solutions1) 2,8 - - - - - - - - - - - - - - -GEA Farm Technologies 2,1 5,6 12,1 14,0 33,8 1,9 8,2 14,7 21,5 46,3 0,1 5,5 14,4 24,5 44,6 3,1GEA Mechanical Equipment2) 28,6 44,4 44,8 64,0 181,7 26,8 42,6 49,1 57,0 175,5 32,7 42,0 50,1 62,8 187,6 34,5GEA Process Engineering 16,5 27,6 34,6 69,4 148,2 16,6 35,8 39,1 71,3 162,7 25,7 41,2 42,4 79,0 188,3 26,6GEA Refrigeration Technologies 7,1 12,3 11,9 20,1 51,3 8,7 11,1 13,8 22,6 56,2 7,3 14,3 14,7 25,2 61,5 10,0GEA Group excluding HX 48,2 83,2 101,9 169,3 402,6 50,7 94,9 115,4 164,7 425,8 55,4 101,0 115,6 186,8 458,8 66,8GEA Heat Exchangers 20,8 26,5 37,9 36,7 121,8 24,0 27,6 31,3 52,1 135,0 17,8 29,0 30,0 46,5 123,3 17,6GEA Group incl. HX 69,0 109,7 139,8 206,1 524,6 74,7 122,5 146,7 216,8 560,8 73,2 129,9 145,6 233,3 582,1 84,1Operating EBIT - Margin[in %]

Q1 11 Q2 11 Q3 11 Q4 11 2011 Q1 12 Q2 12 Q3 12 Q4 12 2012 Q1 13 Q2 13 Q3 13 Q4 13 2013 Q1 14

GEA Food Solutions1) 2,5% - - - - - - - - - - - - - - -GEA Farm Technologies 2,1% 4,7% 8,7% 9,1% 6,6% 1,6% 6,2% 9,3% 12,5% 8,0% 0,1% 4,1% 9,2% 13,9% 7,7% 2,4%GEA Mechanical Equipment2) 14,9% 14,3% 14,1% 17,2% 15,3% 9,9% 13,3% 15,0% 16,3% 13,9% 11,0% 12,6% 14,9% 17,5% 14,1% 11,1%GEA Process Engineering 5,5% 7,2% 8,8% 14,0% 9,4% 4,4% 8,9% 9,2% 13,8% 9,5% 6,5% 9,5% 9,6% 15,0% 10,5% 6,8%GEA Refrigeration Technologies 5,3% 7,4% 7,2% 11,0% 7,9% 5,8% 6,7% 7,8% 11,1% 8,1% 4,8% 7,6% 8,0% 12,0% 8,4% 6,4%GEA Group excluding HX 6,8% 8,6% 10,4% 14,4% 10,5% 5,8% 9,5% 10,9% 13,6% 10,3% 6,0% 9,5% 10,6% 15,0% 10,6% 7,0%GEA Heat Exchangers 6,1% 6,8% 8,9% 7,9% 7,5% 6,2% 6,8% 8,0% 12,3% 8,4% 5,6% 7,5% 7,9% 11,5% 8,3% 5,7%GEA Group incl. HX 6,6% 8,1% 10,0% 12,6% 9,7% 5,9% 8,8% 10,1% 13,4% 9,8% 5,9% 9,0% 10,0% 14,2% 10,1% 6,7%EBIT reported[in EUR million]

Q1 11 Q2 11 Q3 11 Q4 11 2011 Q1 12 Q2 12 Q3 12 Q4 12 2012 Q1 13 Q2 13 Q3 13 Q4 13 2013 Q1 14

GEA Food Solutions1) 2,8 - - - - - - - - - - - - - - -GEA Farm Technologies 1,5 5,0 11,4 13,2 31,1 1,2 7,5 13,9 20,3 42,9 -0,9 4,8 13,7 23,7 41,2 2,3GEA Mechanical Equipment2) 28,4 17,6 38,9 60,3 145,2 -12,8 34,5 38,5 21,8 82,1 28,7 38,1 46,1 58,8 171,7 30,5GEA Process Engineering 16,1 27,2 34,1 68,8 146,1 15,9 35,0 38,1 70,8 159,8 25,0 40,6 41,8 78,3 185,7 26,0GEA Refrigeration Technologies 6,8 10,6 11,1 18,0 46,6 8,2 10,6 13,3 22,0 54,0 6,8 13,8 14,2 24,2 59,0 9,4GEA Group excluding HX 44,0 51,1 91,6 160,2 347,0 6,5 82,3 100,1 125,4 314,3 48,1 90,4 106,0 175,1 419,6 58,7GEA Heat Exchangers 20,2 25,7 37,2 35,0 118,0 23,4 27,0 30,7 49,2 130,3 17,1 27,1 29,3 42,4 116,0 17,0GEA Group incl. HX 66,8 79,3 131,3 197,2 474,6 32,6 111,7 133,1 176,5 453,9 66,2 119,7 135,8 203,2 525,0 73,6

GEA on Roadshows and Conferences - Q1 201464

engineering for a better world

Performance GEA Group & SegmentsKey Figures Time Line (5/6)

Capital Employed w/o goodwill3) (average LTM)[in EUR million]

Q1 08 Q2 08 Q3 08 Q4 08 2008 Q1 09 Q2 09 Q3 09 Q4 09 2009 Q1 10 Q2 10 Q3 10 Q4 10 2010

GEA Food Solutions1) n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.GEA Farm Technologies n.a. n.a. n.a. 204,0 204,0 219,7 235,5 241,7 241,4 241,4 250,5 260,9 271,3 284,0 284,0GEA Mechanical Equipment2) n.a. n.a. n.a. 349,8 349,8 364,3 371,3 374,2 367,7 367,7 346,5 327,9 309,9 300,7 300,7GEA Process Engineering n.a. n.a. n.a. 270,6 270,6 274,2 276,2 269,7 255,1 255,1 241,1 235,7 237,8 238,9 238,9GEA Refrigeration Technologies n.a. n.a. n.a. 221,1 221,1 236,8 249,9 258,6 258,7 258,7 244,9 226,6 202,4 177,9 177,9GEA Group excluding HX n.a. n.a. n.a. 1.063,4 1.063,4 1.097,4 1.117,9 1.113,4 1.094,3 1.094,3 1.078,4 1.071,0 1.066,0 1.069,5 1.069,5GEA Heat Exchangers n.a. n.a. n.a. 707,3 707,3 757,2 789,7 793,4 752,0 752,0 711,8 687,1 677,7 672,8 672,8GEA Group incl. HX n.a. n.a. n.a. 1.772,4 1.772,4 1.853,4 1.903,4 1.899,0 1.835,9 1.835,9 1.780,9 1.750,3 1.738,4 1.739,9 1.739,9ROCE w/o goodw ill4) LTM[in%]

Q1 08 Q2 08 Q3 08 Q4 08 2008 Q1 09 Q2 09 Q3 09 Q4 09 2009 Q1 10 Q2 10 Q3 10 Q4 10 2010

GEA Food Solutions1) n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.GEA Farm Technologies n.a. n.a. n.a. 26,2% 26,2% 21,7% 16,8% 11,6% 5,1% 5,1% 5,8% 5,0% 5,1% 7,1% 7,1%GEA Mechanical Equipment2) n.a. n.a. n.a. 35,9% 35,9% 33,4% 29,9% 27,9% 23,8% 23,8% 24,5% 26,5% 28,7% 34,5% 34,5%GEA Process Engineering n.a. n.a. n.a. 37,0% 37,0% 35,7% 30,8% 25,2% 20,5% 20,5% 23,5% 26,4% 31,0% 37,7% 37,7%GEA Refrigeration Technologies n.a. n.a. n.a. 18,4% 18,4% 15,5% 13,1% 9,5% 5,1% 5,1% 5,3% 5,5% 7,8% 6,9% 6,9%GEA Group excluding HX n.a. n.a. n.a. 26,4% 26,4% 24,3% 20,8% 17,4% 11,3% 11,3% 12,1% 12,8% 14,4% 18,9% 18,9%GEA Heat Exchangers n.a. n.a. n.a. 30,5% 30,5% 27,2% 22,7% 18,5% 16,5% 16,5% 16,8% 16,2% 13,8% 4,4% 4,4%GEA Group incl. HX n.a. n.a. n.a. 28,4% 28,4% 26,0% 22,1% 18,6% 14,6% 14,6% 14,9% 15,1% 15,0% 13,6% 13,6%

Capital Employed w/o goodwill3) (average LTM)[in EUR million]

Q1 11 Q2 11 Q3 11 Q4 11 2011 Q1 12 Q2 12 Q3 12 Q4 12 2012 Q1 13 Q2 13 Q3 13 Q4 13 2013 Q1 14

GEA Food Solutions1) n.a. n.a. n.a. n.a. n.a. - - - - - - - - - - -GEA Farm Technologies 288,6 289,7 292,5 297,7 297,7 302,1 308,2 314,8 319,3 319,3 324,7 327,9 327,4 325,4 325,4 322,4GEA Mechanical Equipment2) 303,6 481,6 625,8 770,7 770,7 874,7 903,6 929,1 949,5 949,5 966,9 972,6 977,2 985,9 985,9 999,0GEA Process Engineering 237,4 235,8 238,7 249,0 249,0 273,3 290,0 296,7 286,0 286,0 270,8 262,2 253,5 253,9 253,9 249,4GEA Refrigeration Technologies 176,5 187,8 205,4 225,9 225,9 241,8 249,0 253,6 254,7 254,7 255,6 256,1 257,3 259,5 259,5 259,1GEA Group excluding HX 1.117,9 1.266,4 1.436,7 1.619,6 1.619,6 1.771,9 1.830,3 1.872,7 1.887,4 1.887,4 1.890,1 1.890,6 1.886,5 1.895,0 1.895,0 1.900,4GEA Heat Exchangers 680,7 684,2 691,6 694,6 694,6 690,5 688,2 675,9 669,9 669,9 658,2 646,6 641,2 634,7 634,7 639,8GEA Group incl. HX 1.796,3 1.949,7 2.128,3 2.314,2 2.314,2 2.462,7 2.518,1 2.548,2 2.556,5 2.556,5 2.546,1 2.534,0 2.523,5 2.525,5 2.525,5 2.536,5ROCE w/o goodwill4) LTM[in%]

Q1 11 Q2 11 Q3 11 Q4 11 2011 Q1 12 Q2 12 Q3 12 Q4 12 2012 Q1 13 Q2 13 Q3 13 Q4 13 2013 Q1 14

GEA Food Solutions1) n.a. n.a. n.a. n.a. n.a. - - - - - - - - - - -GEA Farm Technologies 7,3% 8,3% 9,3% 10,4% 10,4% 10,2% 10,8% 11,3% 13,4% 13,4% 12,6% 11,6% 11,5% 12,7% 12,7% 13,8%GEA Mechanical Equipment2) 36,8% 22,5% 19,6% 18,8% 18,8% 11,9% 13,4% 13,0% 8,6% 8,6% 12,8% 13,1% 13,8% 17,4% 17,4% 17,4%GEA Process Engineering 40,1% 45,1% 50,8% 58,7% 58,7% 53,4% 53,0% 53,2% 55,9% 55,9% 62,4% 66,6% 70,3% 73,2% 73,2% 74,6%GEA Refrigeration Technologies 9,9% 12,2% 14,1% 20,6% 20,6% 19,8% 19,2% 19,7% 21,2% 21,2% 20,6% 21,8% 22,1% 22,7% 22,7% 23,8%GEA Group excluding HX 19,3% 17,9% 18,7% 21,4% 21,4% 17,5% 18,6% 18,6% 16,7% 16,7% 18,8% 19,3% 19,6% 22,1% 22,1% 22,6%GEA Heat Exchangers 4,0% 5,8% 9,8% 17,0% 17,0% 17,6% 17,8% 17,2% 19,4% 19,4% 18,8% 19,2% 19,1% 18,3% 18,3% 18,1%GEA Group incl. HX 14,0% 14,1% 16,2% 20,5% 20,5% 17,9% 18,8% 18,6% 17,8% 17,8% 19,2% 19,6% 19,7% 20,8% 20,8% 21,0%

GEA on Roadshows and Conferences - Q1 201465

engineering for a better world

Performance GEA Group & SegmentsKey Figures Time Line (6/6): Remarks

1) All historical figures for GEA FS before Q2 2011 are pro-forma figures only and haven't been audited due to the fact that GEA FS's Financial Year was ending end of February. The listed historical figures before Q2 2011 are not included in the Group-numbers of the corresponding period.

2) Since Q2 2011 GEA ME figures includes GEA FS

3) Capital employed excluding goodwill from the acquisition of the former GEA AG by the former Metallgesellschaft AG in 1999.

4) ROCE LTM = EBIT reported (LTM) / Capital employed excluding goodwill from the acquisition of the former GEA AG by the former Metallgesellschaft AG in 1999 (average LTM).

GEA on Roadshows and Conferences - Q1 201466

engineering for a better world

ADR Information

GEA on Roadshows and Conferences - Q1 2014

GEA Group has a sponsored level I ADR program

Ratio: 1 ADR = 1 Ordinary share

Bloomberg ticker: GEAGY:US CUSIP: 361592108 ISIN: US3615921083

Depositary bank: Deutsche Bank Trust Company Americas

Depositary bank contacts: ADR broker helpline

Tel: +1 212 250 9100 (New York) Tel: +44 207 547 6500 (London) Email: [email protected] and website: www.adr.db.com

Depositary bank’s local custodian: Deutsche Bank Frankfurt67

engineering for a better world

Investor Relations Contact: [email protected]

GEA on Roadshows and Conferences - Q1 2014

Donat von Müller+49 211 9136 [email protected]

Axel Wolferts+49 211 9136 [email protected]

68

Dr. Helmut Schmale+49 211 9136 [email protected]