Embed Size (px)

Citation preview

20 - 1©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Job Costing

Job Costing

Chapter 20

20 - 2©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Distinguish between job costing

and process costing.

Objective 1

20 - 3©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Job order costingJob order costing

Process costingProcess costing

Cost Systems

There are two basic systems used by manufacturers to assign costs to their products:

20 - 4©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

ChoppingChopping Mixing and canningMixing and canning

Process Costing Example

Laura Foods produces a garlic flavored tomato sauce.

Production of the sauce requires two major processes:

20 - 5©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

$20,000 ÷ 100,000 = $0.20/pint

Process Costing Example

Assume that Laura incurred $20,000 in the mixing and canning process to mix 100,000 pints of tomato sauce.

What is the mixing cost per pint?

20 - 6©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Job Costing

It is used by a manufacturer who produces products as individual units or in distinct batches or jobs.

20 - 7©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

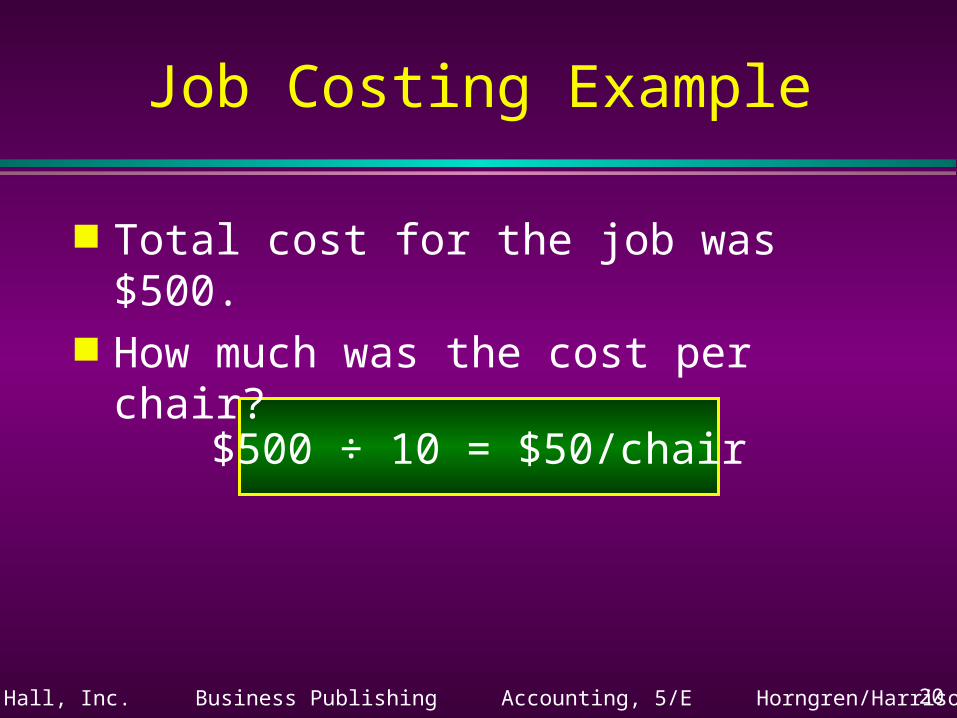

Job Costing Example

David, Bryan, and Co. is a small furniture manufacturing business in Texas.

They received an order for 10 chairs from a customer in Kansas City.

20 - 8©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

$500 ÷ 10 = $50/chair

Job Costing Example

Total cost for the job was $500. How much was the cost per chair?

20 - 9©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Job Costing

A cost object is anything to which costs are assigned.

A cost driver is any factor that affects cost. Job cost record is a document used to

accumulate the costs of a job.

20 - 10©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

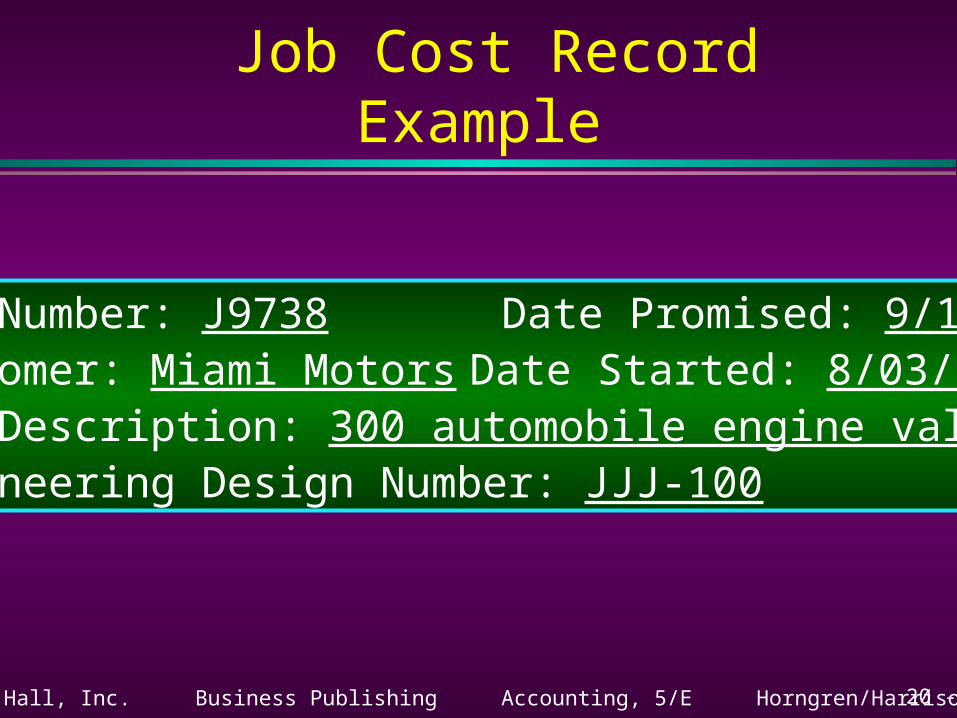

Job Number: J9738 Date Promised: 9/11/03Customer: Miami Motors Date Started: 8/03/03Job Description: 300 automobile engine valvesEngineering Design Number: JJJ-100

Job Cost Record Example

20 - 11©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

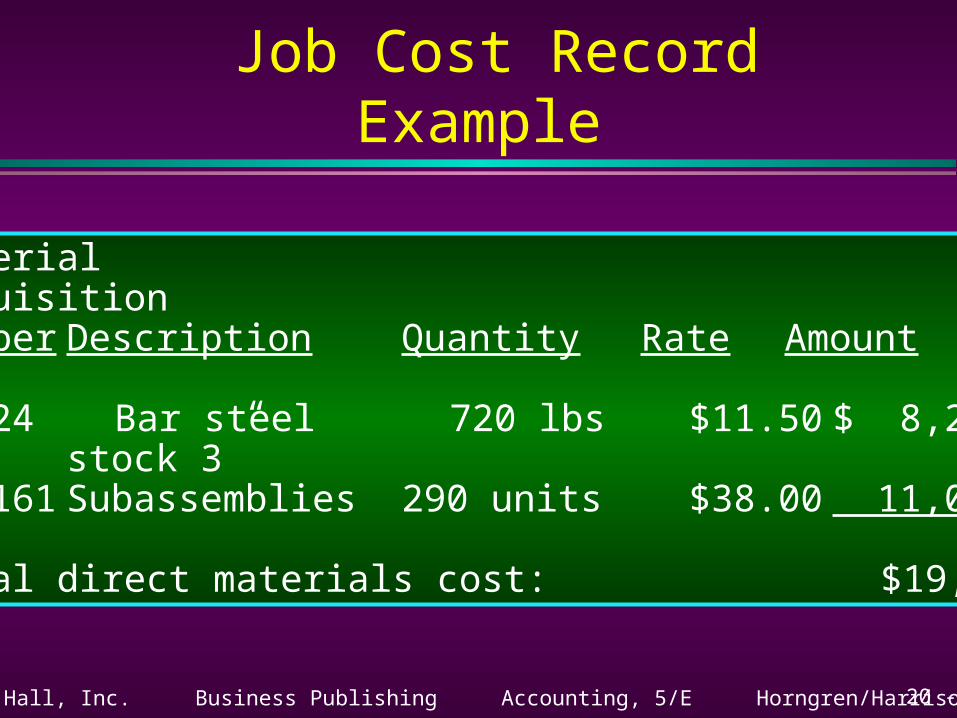

MaterialRequisitionNumber Description Quantity Rate Amount

47624 Bar steel 720 lbs $11.50 $ 8,280stock 3”

A35161 Subassemblies 290 units $38.00 11,020

Total direct materials cost: $19,300

Job Cost Record Example

20 - 12©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

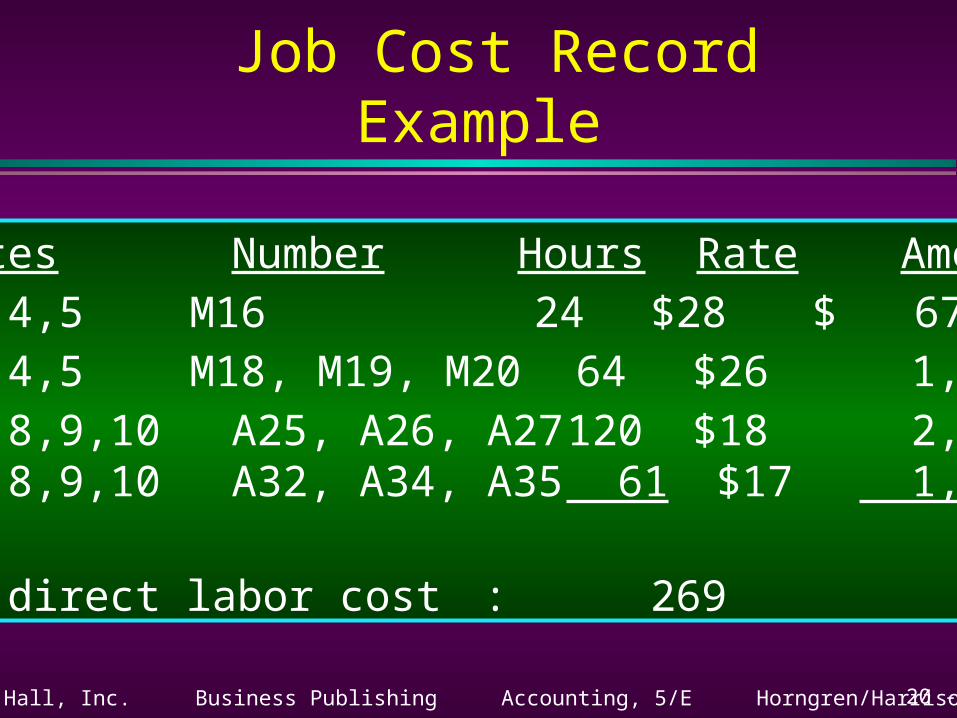

Dates Number Hours Rate Amount

8/2,3,4,5 M16 24 $28 $ 672

8/2,3,4,5 M18, M19, M20 64 $26 1,664

8/6,7,8,9,10 A25, A26, A27 120 $18 2,1608/6,7,8,9,10 A32, A34, A35 61 $17 1,037

Total direct labor cost: 269 $5,533

Job Cost Record Example

20 - 13©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Manufacturing Overhead Amount118 machine hours @ $40 per hour $ 4,720269 direct labor hours @ 36 per hour 9,684

Total overhead cost: $14,404

Job Cost Record Example

20 - 14©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

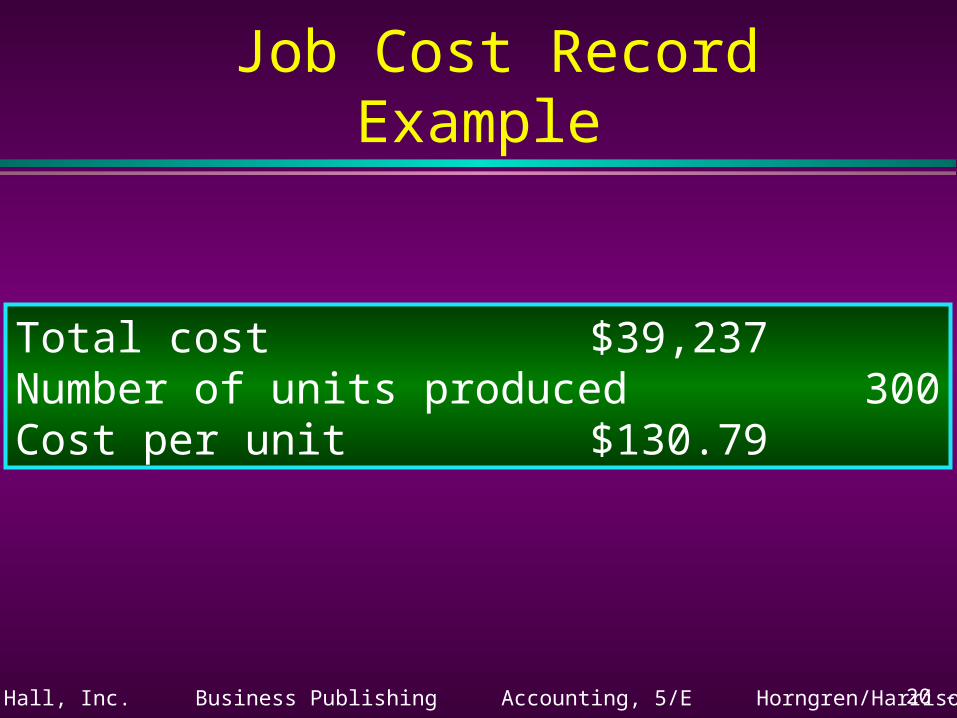

Total cost $39,237Number of units produced 300Cost per unit $130.79

Job Cost Record Example

20 - 15©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Account for materials and

labor in a manufacturer’sjob costing system.

Objective 2

20 - 16©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Materials Cost

Companies using job costing often use a perpetual system to account for direct materials.

A purchase order is used to order materials. A receiving report is prepared when the

ordered materials are received.

20 - 17©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

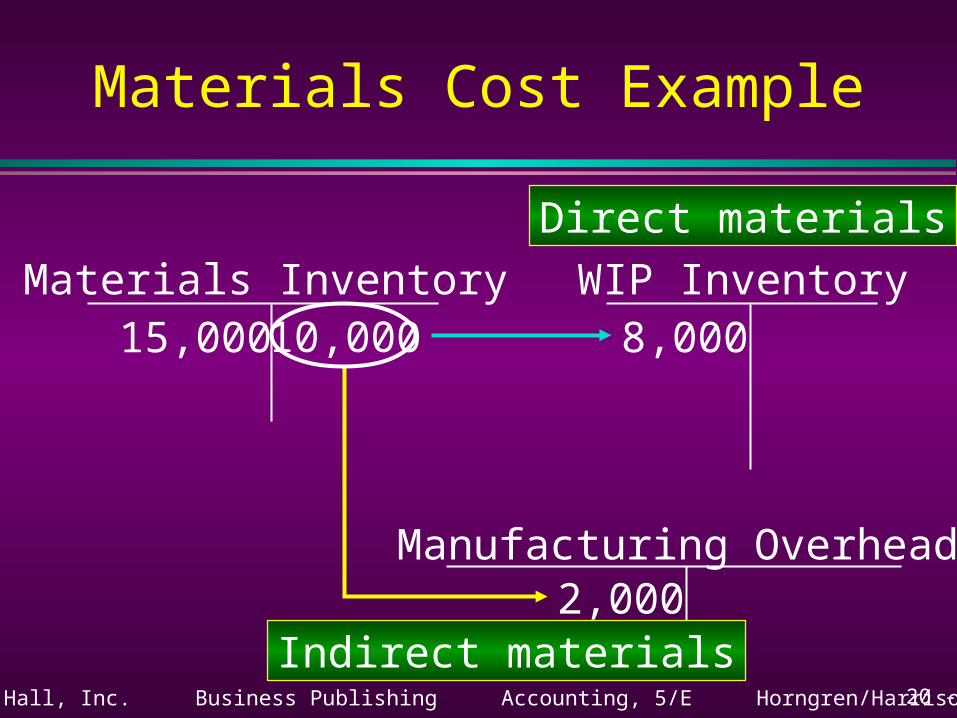

Materials Cost Example

Alec Clothing Co. purchased raw materials on account for $15,000.

Materials costing $10,000 were requisitioned for production.

Of this total, $2,000 was indirect materials.

20 - 18©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Indirect materials

Direct materials

15,000 10,000

2,000

8,000Materials Inventory WIP Inventory

Manufacturing Overhead

Materials Cost Example

20 - 19©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Labor Costs

Labor costs are accumulated using the payroll register and time tickets.

Labor time tickets identify the employee and the amount of time spent on each job.

20 - 20©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Labor Cost Example

The company incurred $30,000 of manufacturing wages for all jobs.

Assume that $25,000 can be traced directly to the jobs and $5,000 is for indirect labor.

20 - 21©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Indirect labor

Direct labor

30,000 30,000

5,000

25,000Manufacturing Wages WIP Inventory

Manufacturing Overhead

Labor Cost Example

20 - 22©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Manufacturing Overhead(Plant and Equipment) 20,000

Accumulated Depreciation(Plant and Equipment) 20,000

To record plant and equipment depreciation

Manufacturing Overhead Costs

The company incurred $20,000 of plant equipment depreciation.

20 - 23©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Cost assignment

Direct materials and direct labor

Cost Tracing

Manufacturingoverhead

Cost Allocation

CostObject(Job)

Manufacturing Overhead Costs

The general term cost assignment refers to both tracing direct costs and allocating indirect costs to cost objects.

20 - 24©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Budgeted overhead ÷ Estimated base = RateBudgeted overhead ÷ Estimated base = Rate

Manufacturing Overhead Rate

At the beginning of the year, a budgeted overhead application rate is estimated.

This budgeted rate is used to apply overhead to all jobs completed during the year.

20 - 25©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

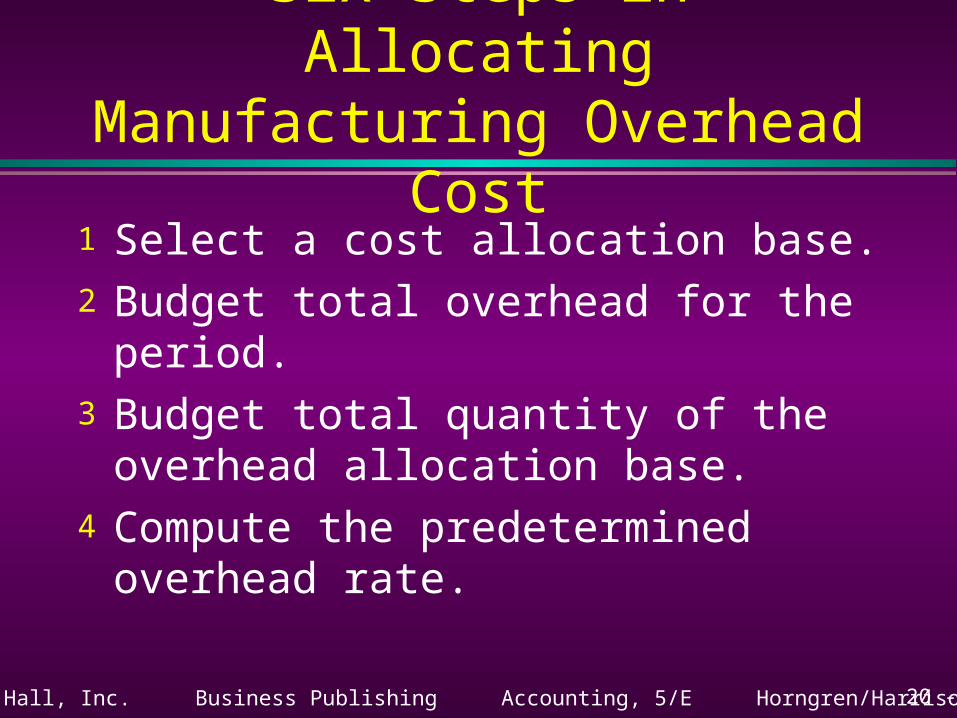

Six Steps in Allocating Manufacturing Overhead Cost

1 Select a cost allocation base.2 Budget total overhead for the period.3 Budget total quantity of the overhead

allocation base.4 Compute the predetermined overhead rate.

20 - 26©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Six Steps in Allocating Manufacturing Overhead Cost

5 Obtain actual quantities of the overhead allocation base.

6 Allocate manufacturing overhead by multiplying the predetermined manufacturing overhead rate by the actual quantity of the allocation base that pertains to each job.

20 - 27©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

$243,000 ÷ 4,500 = $54

Manufacturing Overhead Example

Alec Clothing Co.’s total budgeted overhead for the year equals $243,000.

The allocation rate is based on 4,500 direct labor hours.

What is the allocation rate?

20 - 28©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Work-in-Process Inventory 10,800Manufacturing Overhead 10,800

To record overhead applied to Job 51

Manufacturing Overhead Example

Assume that Job 51 used 200 direct labor hours.

What is the journal entry to record the manufacturing overhead applied?

20 - 29©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

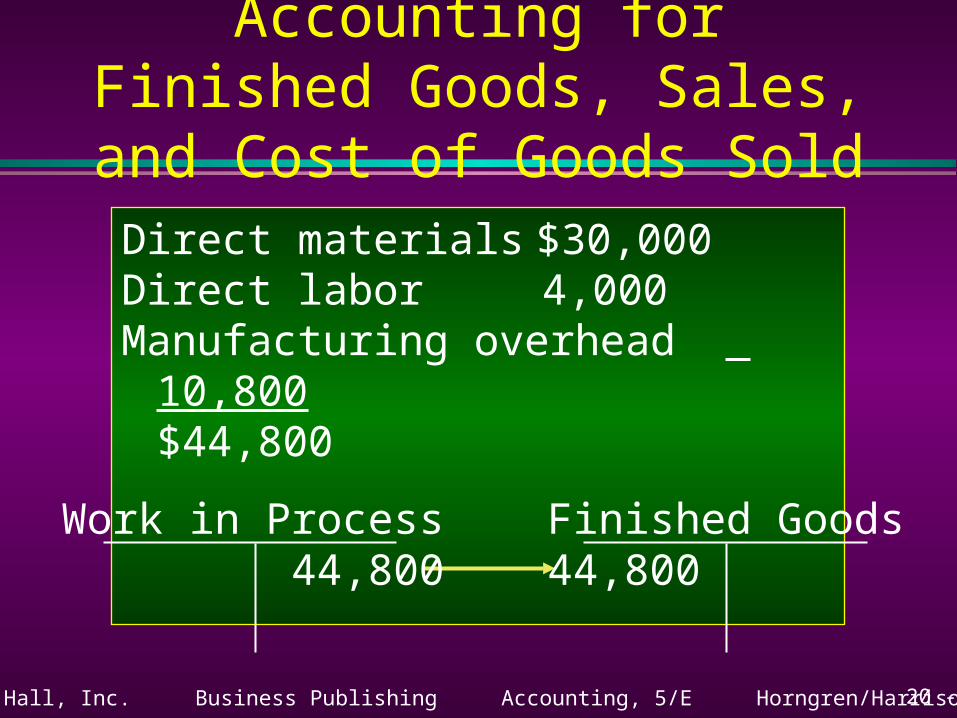

Accounting for Finished Goods, Sales, and Cost of Goods Sold

As jobs are completed they are transferred to finished goods inventory.

In addition to the overhead applied to Job 51, direct labor was $4,000 and direct materials totaled $30,000.

How much was transferred to Finished Goods Inventory?

20 - 30©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Direct materials$30,000

Direct labor 4,000Manufacturing overhead

10,800

$44,800Work in Process

44,800Finished Goods44,800

Accounting for Finished Goods, Sales, and Cost of Goods Sold

20 - 31©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

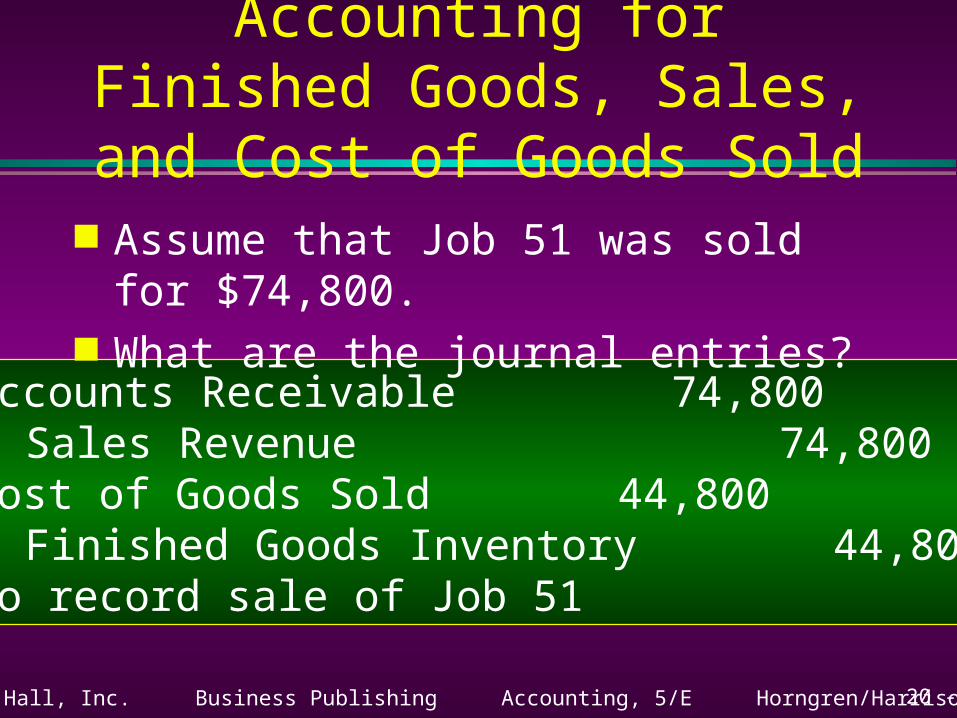

Accounts Receivable 74,800Sales Revenue 74,800

Cost of Goods Sold 44,800Finished Goods Inventory 44,800

To record sale of Job 51

Accounting for Finished Goods, Sales, and Cost of Goods Sold

Assume that Job 51 was sold for $74,800. What are the journal entries?

20 - 32©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

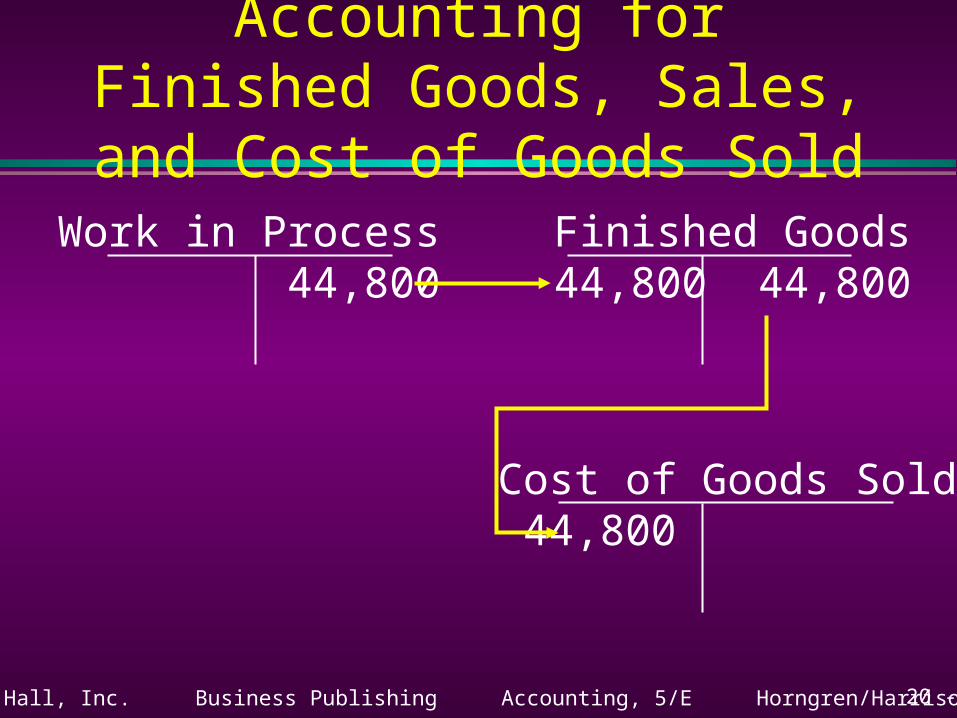

Work in Process44,800

Finished Goods 44,800 44,800

Cost of Goods Sold 44,800

Accounting for Finished Goods, Sales, and Cost of Goods Sold

20 - 33©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

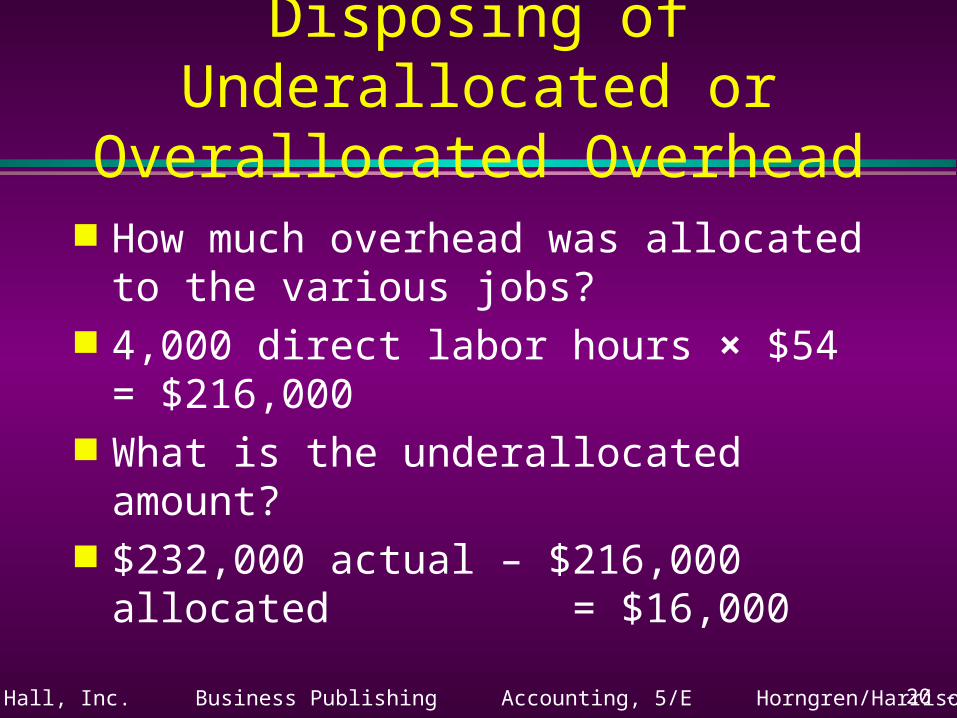

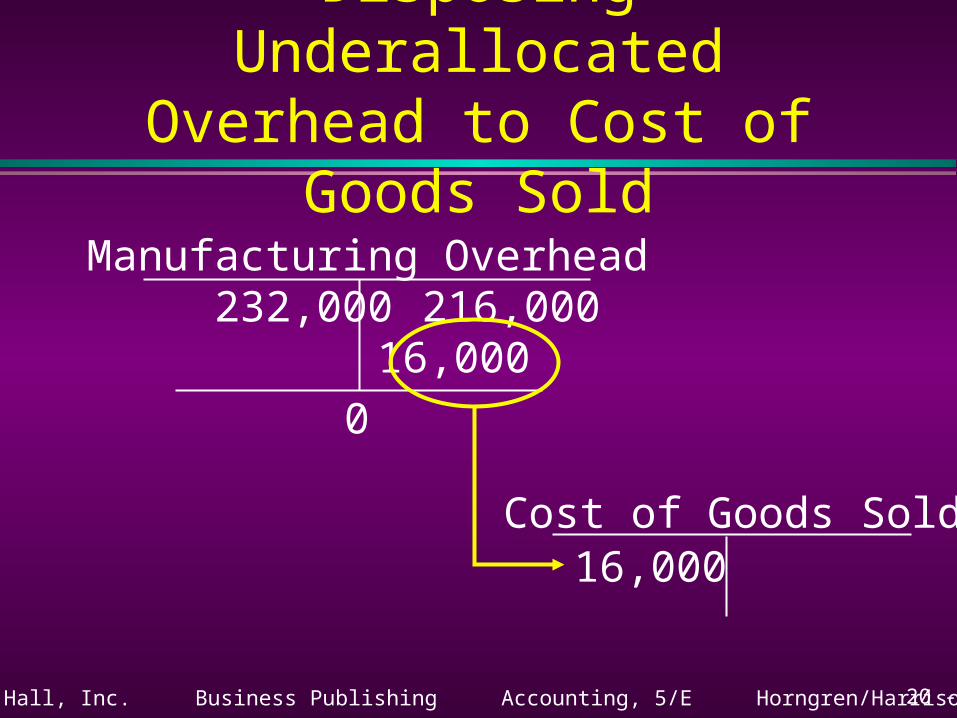

Disposing of Underallocated or Overallocated Overhead

Suppose that the company incurred $232,000 of actual manufacturing overhead during the year, and that actual direct labor hours worked were 4,000.

The actual manufacturing overhead rate would have been $232,000 ÷ 4,000 = $58.

The predetermined rate was $54.

20 - 34©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Disposing of Underallocated or Overallocated Overhead

How much overhead was allocated to the various jobs?

4,000 direct labor hours × $54 = $216,000 What is the underallocated amount? $232,000 actual – $216,000 allocated

= $16,000

20 - 35©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Manufacturing Overhead 232,000 216,000

16,000

Cost of Goods Sold16,000

0

Disposing Underallocated Overhead to Cost of Goods Sold

20 - 36©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

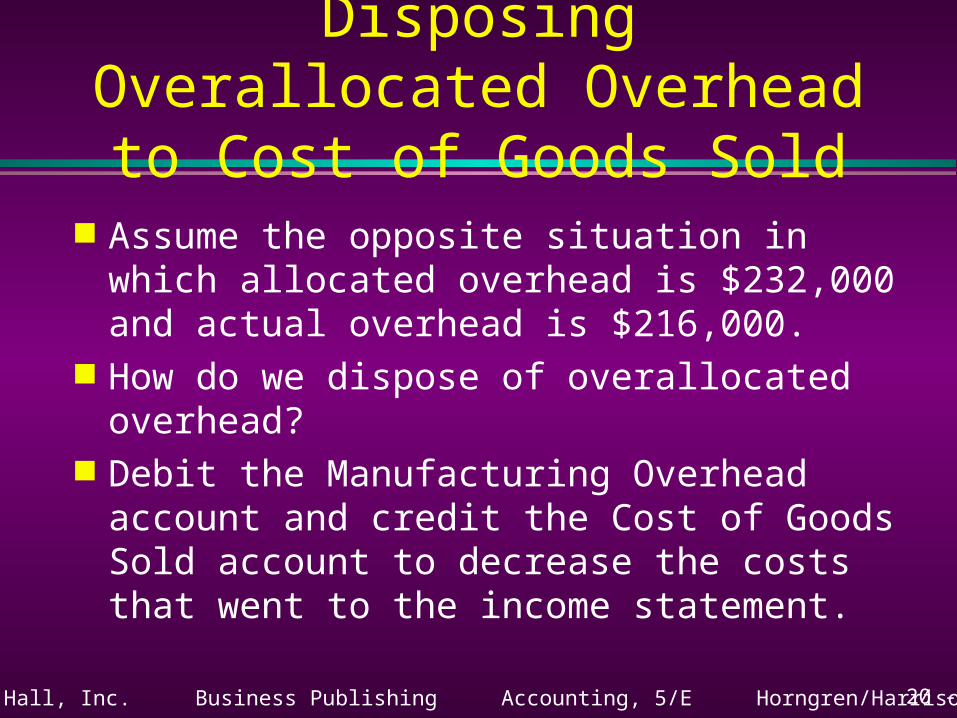

Disposing Overallocated Overhead to Cost of Goods Sold

Assume the opposite situation in which allocated overhead is $232,000 and actual overhead is $216,000.

How do we dispose of overallocated overhead? Debit the Manufacturing Overhead account

and credit the Cost of Goods Sold account to decrease the costs that went to the income statement.

20 - 37©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Manufacturing Overhead 216,000 232,000

16,000

0

Cost of Goods Sold16,000

Disposing Overallocated Overhead to Cost of Goods Sold

20 - 38©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Account for noninventoriable

costs in job costing.

Objective 4

20 - 39©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Job Costing in a Nonmanufacturing Company

How is direct labor traced to individual jobs in a nonmanufacturing company?

Employees complete a weekly time record. Jim, Abby, and Associates is a firm

specializing in composing and arranging music parts for different clients.

Musician Judy Lopez’s salary is $80,000 per year.

20 - 40©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

80,000 ÷ 2,000 = $40

Job Costing in a Nonmanufacturing Company

Assuming a 40-hour workweek and 50 workweeks in each year gives a total of 2,000 available working hours per year (40 hours × 50 weeks).

What is her hourly rate?

20 - 41©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

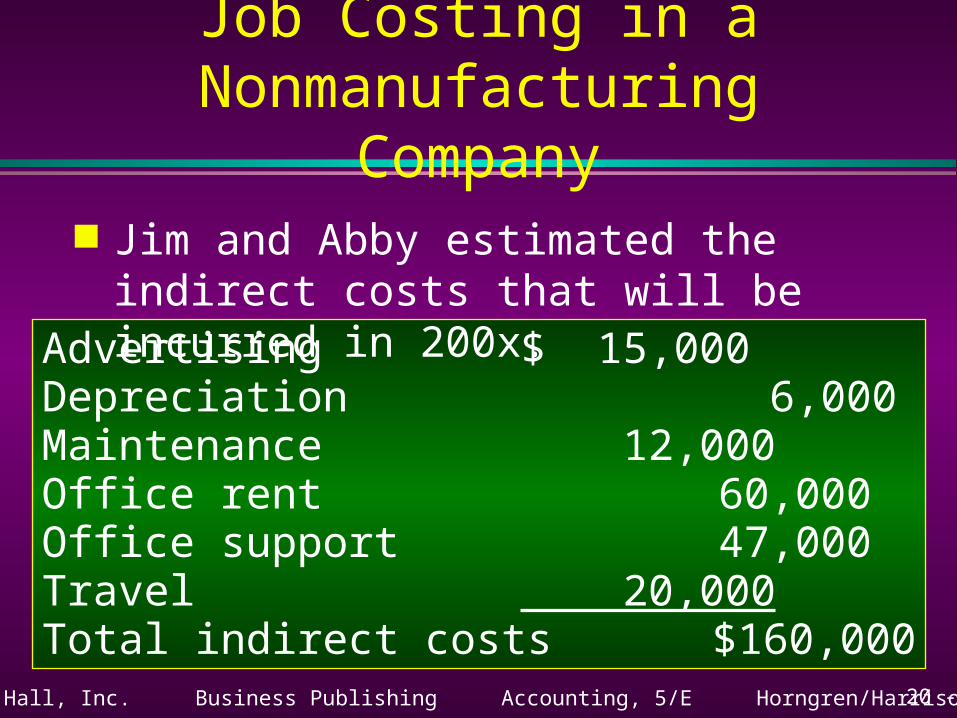

Advertising $ 15,000Depreciation 6,000Maintenance 12,000Office rent 60,000Office support 47,000Travel 20,000Total indirect costs $160,000

Job Costing in a Nonmanufacturing Company

Jim and Abby estimated the indirect costs that will be incurred in 200x.

20 - 42©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

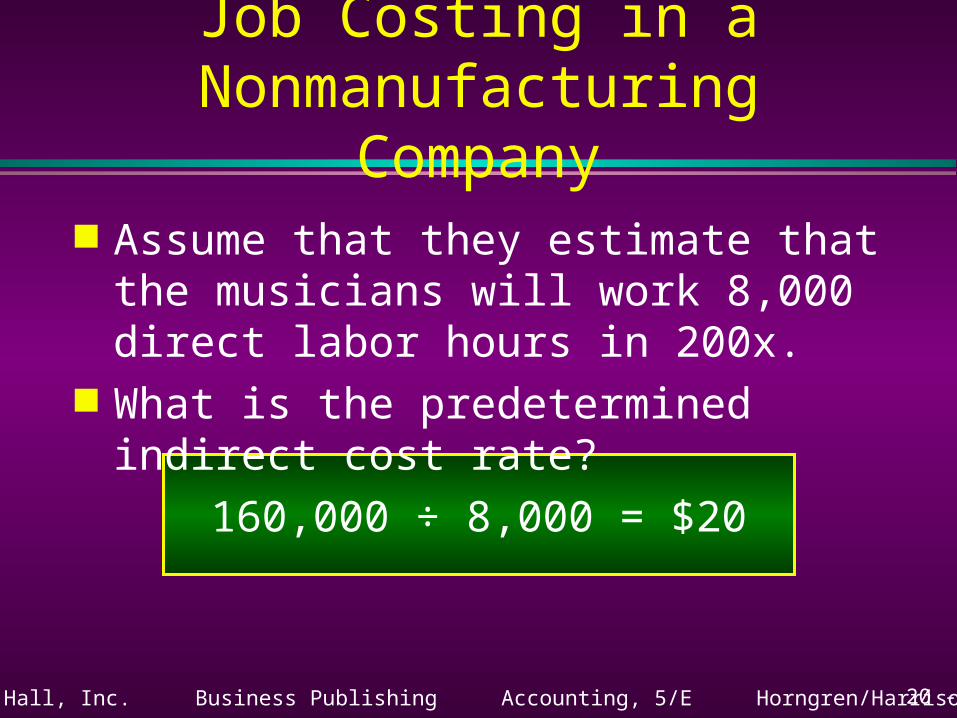

160,000 ÷ 8,000 = $20

Job Costing in a Nonmanufacturing Company

Assume that they estimate that the musicians will work 8,000 direct labor hours in 200x.

What is the predetermined indirect cost rate?

20 - 43©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Direct Labor: 25 hours × $40 = $1,000Indirect costs: 25 hours × $20 = 500Total costs: $1,500

Job Costing in a Nonmanufacturing Company

Records show that Judy Lopez worked 25 hours servicing Los Abuelos Music Co.

What is the total cost assigned to this client?

20 - 44©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

End of Chapter 20

End of Chapter 20