Embed Size (px)

Citation preview

2006 General Meeting

Assemblée générale 2006

Chicago, Illinois

2006 General Meeting

Assemblée générale 2006

Chicago, Illinois

Canadian Institute

of Actuaries

Canadian Institute

of Actuaries

L’Institut canadien desactuaires

L’Institut canadien desactuaires

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

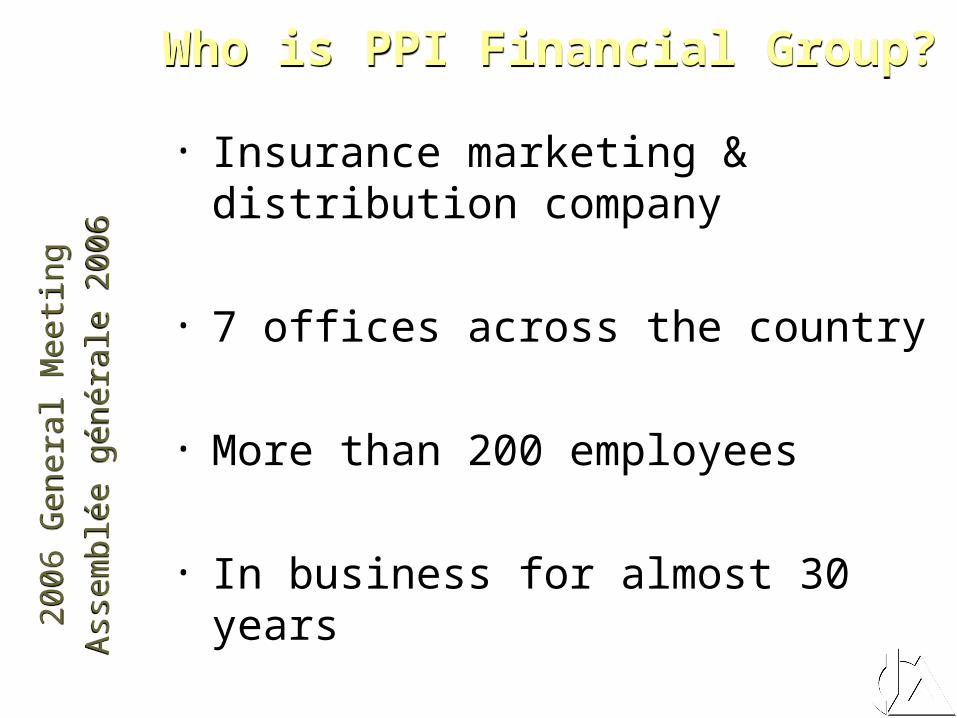

Who is PPI Financial Group?Who is PPI Financial Group?

• Insurance marketing & distribution company

• 7 offices across the country

• More than 200 employees

• In business for almost 30 years

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

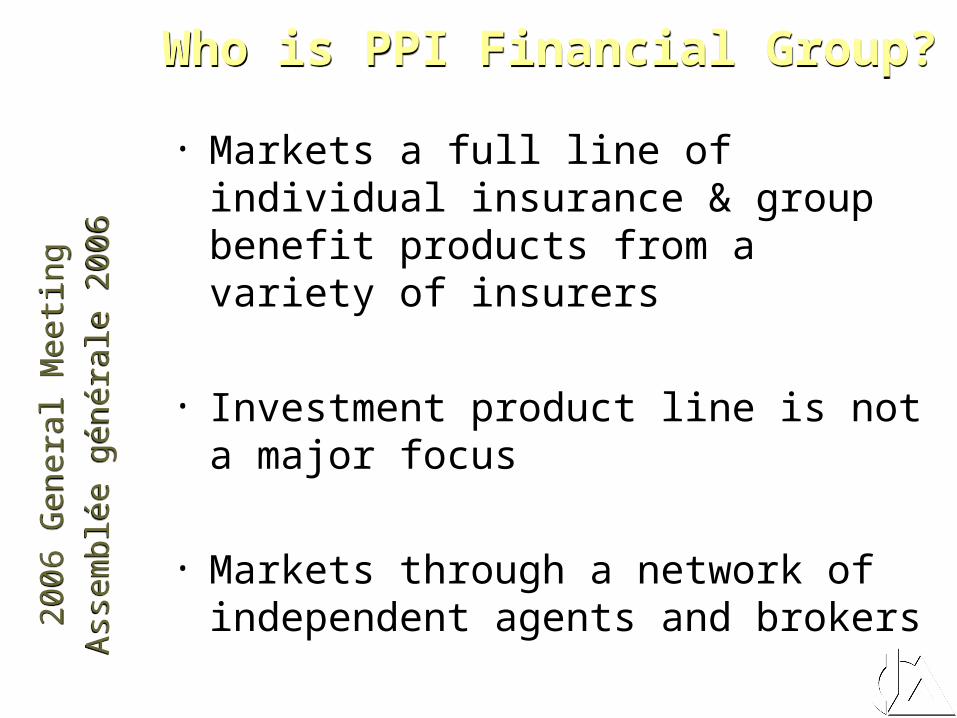

Who is PPI Financial Group?Who is PPI Financial Group?

• Markets a full line of individual insurance & group benefit products from a variety of insurers

• Investment product line is not a major focus

• Markets through a network of independent agents and brokers

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Target Consumer MarketTarget Consumer Market

• Affluent & high net worth individuals

• Owners of small to mid-size companies

• Professionals & executives

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Target Agent MarketTarget Agent Market

• Agents that target the same consumer groups and that:

– Have a good reputation in the business

– Have a proven track record in this market or the desire and the potential to do so

– Are attracted to our value proposition

• PPI has relationships with several hundred agents that fit this description

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Agent Value PropositionAgent Value Proposition

• Provide agents with:

• Strong agency contracts

• Full range of products, including unique & proprietary products

• Strong case & marketing support for all lines of business

• Tax, legal, underwriting & product support

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Agent Value Proposition – Cont’dAgent Value Proposition – Cont’d

• Provide agents with:

• An attractive pooling arrangement

• Ongoing education on products & sales applications

• Post issue administrative support

• Advice & support in solving problems of all sorts

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Agent Value Proposition – Cont’dAgent Value Proposition – Cont’d

• In conclusion, we help agents to successfully & profitably grow their businesses

• Competitive base commission rates

• Override rates not nearly as competitive

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Consumer Value PropositionConsumer Value Proposition

• High quality & leading edge techniques for personal estate and/or business planning issues

• Emphasis on tax efficiency

• Ability to work cooperatively with client’s accountants & lawyers to achieve client objectives

• Not simply a product sale but an advisory relationship

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Individual Sales ResultsIndividual Sales Results

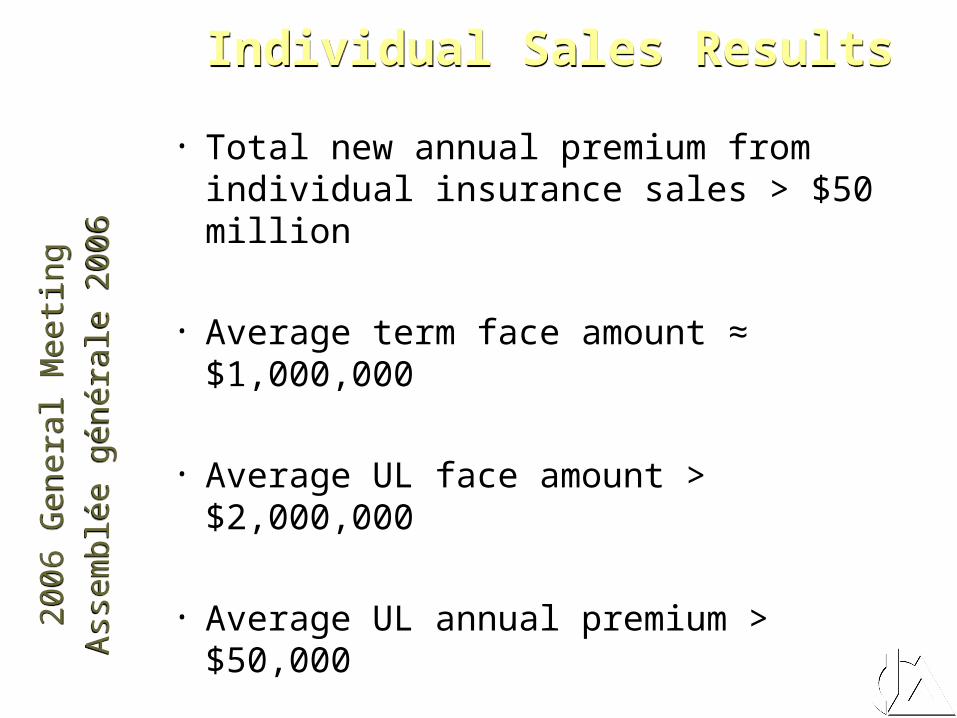

• Total new annual premium from individual insurance sales > $50 million

• Average term face amount ≈ $1,000,000

• Average UL face amount > $2,000,000

• Average UL annual premium > $50,000

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Past Events Impacting DistributionPast Events Impacting Distribution

• Move from career to brokerage & MGA distribution

• Significant consolidation at insurer level

• Significant reduction in recruiting of new sales people by insurers

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Brokerage & MGA DistributionBrokerage & MGA Distribution

• Variable cost distribution model

• Most brokerage companies & MGA’s have evolved to compete primarily on price and/or compensation levels

• Does not allow such entities to provide high levels of support to agents

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Brokerage & MGA Distribution – Cont’dBrokerage & MGA Distribution – Cont’d

• As you move upscale, sales application knowledge becomes much more important & complex than product knowledge

• In the brokerage & MGA markets, who is educating the agents in these areas?

• Retained distribution margins insufficient to permit an adequate job to be done

• Inadequate training has consequences

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Brokerage & MGA Distribution – Cont’dBrokerage & MGA Distribution – Cont’d

• Should also provide support to agents & ensure compliance

• Again, inadequate retained margins make this difficult

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Insurer ConsolidationInsurer Consolidation

• Significant consolidation in last 15 years

• Resulting insurer challenges:

• Acquisition indigestion

• Difficult, costly & time consuming systems integration

• Loss of many knowledgeable service staff

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Insurer Consolidation – Cont’dInsurer Consolidation – Cont’d

• Market Consequences:

• Companies too inwardly focused

• Difficulty in getting proper insurer support to service older new money and UL products

• Latter point much more problematic as you go upscale in the market

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Significant Reduction in RecruitingSignificant Reduction in Recruiting

• Graying & aging of existing distribution system

• Most products not priced to support recruiting & related training efforts

• Most companies do not seem particularly focused or concerned about bringing new sales people into the business

• In a demutualized industry, sales growth is a requirement for a healthy share valuation

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Distribution Company ConsolidationDistribution Company Consolidation

• Over the next 10 years, there will be significant consolidation at the MGA level, due to:

• Inadequate margins for many MGA’s

• The need to invest in technology

• Increasing legal & regulatory complexity, compliance & associated costs (PIPEDA, E&O requirements, Fintrac, etc)

• Surviving MGA’s will progressively increase their margins to sustaining levels

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Profile of New Sales PeopleProfile of New Sales People

• The average age of new sales people will increase significantly compared to the past:

• Insufficient compensation to make a living selling primarily term to young adults

• Family formation now much later than it was a generation ago

• Many new sales people will enter the business with some prior business experience

• Should result in lower agent failure rates

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Development of Sales People by MGA’sDevelopment of Sales People by MGA’s

• The surviving & larger MGA’s will become a source of new sales people:

• Some of their market support staff will evolve into sales people over time

• Affinity relationships with other financial services firms will naturally produce insurance sales people from such firms

• The numbers of such new sales people will not be great enough to satisfy industry needs & will tend to be focused on the upscale market

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Industry Level RecruitingIndustry Level Recruiting

• In the past, an insurer would take responsibility for recruiting new agents to market its products

• Going forward, recruiting & training new sales people will need to become an industry level initiative, involving all stakeholders

• Insurers• Industry associations (CLHIA, Advocis, CALU)• MGA’s• Agents

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Industry Level Recruiting – Cont’dIndustry Level Recruiting – Cont’d

• All industry stakeholders have a serious vested interest in this issue:

• Insurers & MGA’s have the most obvious interest

• The CLHIA has an interest in having healthy & domestically growing companies as members

• Advocis needs more rather than fewer members and can play an important role in training & education of new sales people

• The majority of today’s successful agents do not have a succession plan. Capable younger sales people are their best bet.

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Industry Level Recruiting – Cont’dIndustry Level Recruiting – Cont’d

• In the past, new sales people came into the business:

• At a very young age

• With little or no prior business experience

• Were thrust into full commission sales jobs after relatively short training & financial support periods

• Not surprisingly:

• The agent failure rates were high

• The quality of the business written was low

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Industry Level Recruiting – Cont’dIndustry Level Recruiting – Cont’d

• Going forward, sales apprenticeship programs need to be developed at an industry level and should involve:

• Much longer training periods

• Work experience in the industry that is relevant to sales & moves progressively towards a full sales role

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Banks & Insurance DistributionBanks & Insurance Distribution

• Unless the insurance industry can effectively service the broad based market, banks will eventually win on the issue of in branch retailing of insurance

• Industry sales people recruiting success is very relevant to the outcome of this issue

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Distribution CostsDistribution Costs

• In the upscale markets, particularly where permanent insurance is involved, agent compensation levels are fine

• In the younger issue age mid market, which is where most new sales people will be focused, the agent compensation levels not sufficient to attract & sustain the new sales people that the industry needs

• Over time, expect to see compression of compensation rates for the larger amount, older issue age market & higher compensation rates for the smaller amount, younger issue age market