Embed Size (px)

DESCRIPTION

Canadian Institute of Actuaries. L’Institut canadien des actuaires. 2006 General Meeting Assemblée générale 2006 Chicago, Illinois. Bill C-57 and the Actuary Le Projet de Loi C-57 et L’Actuaire Nick Bauer Al Edwards. PD-22TR-22. Outline of Presentation. - PowerPoint PPT Presentation

Citation preview

2006 General Meeting

Assemblée générale 2006

Chicago, Illinois

2006 General Meeting

Assemblée générale 2006

Chicago, Illinois

Canadian Institute

of Actuaries

Canadian Institute

of Actuaries

L’Institut canadien desactuaires

L’Institut canadien desactuaires

2

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Bill C-57 and the Actuary

Le Projet de Loi C-57 et L’Actuaire

Nick Bauer Al Edwards

Bill C-57 and the Actuary

Le Projet de Loi C-57 et L’Actuaire

Nick Bauer Al Edwards

PD-22 TR-22PD-22 TR-22

3

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Outline of Presentation

• Bill C-57 Requirements

• Status of Changes

• New OSFI Par Guidelines

• Potential Issues

• CIA Response

• Fairness?

• Discussion

• Conclusion

4

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Bill C-57 Overview

• Introduce several new governance requirements for companies and actuaries with respect to:– participating business

– adjustable policies

• New actuarial opinions on fairness required (CIA guidance and/or standards will be needed)

• Emphasis on Disclosure to Policyholders

• Significant influence from recent UK developments

• Significant start-up work to develop policies and supporting processes

5

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Before C-57 – Canadian Companies

• Board Approves Participating Policyholder Dividend Policy (165.2 (e)) Investment Income Allocation Method (457 (b)) Expense (including Tax) Allocation Method (458 (b)) Declaration of Policyholder Dividends (464 (l))

• Actuary Opines Allocation Methods Fair and Equitable (460) 461 Payment does not affect Dividend Policy

Compliance/Maintenance (461 (c)) Policyholder Dividends comply with Dividend Policy

(464.2)

(all section references are to Insurance Companies Act of Canada)

6

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

After C-57 – Canadian Companies

• Board Approves Participating Policyholder Dividend Policy (165.2 (e)) Investment Income Allocation Method (457 (b)) Expense (including Tax) Allocation Method (458 (b)) Declaration of Policyholder Dividends (464 (l)) Policy for Management of Par Accounts (165.2 (e.1)) -

new Criteria for Changes to Adjustable Policies (165.2

(e.2)) - new

(all section references are to Insurance Companies Act of Canada)

7

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

After C-57 – Canadian Companies

• Actuary Opines Allocation Methods Fair and Equitable (460) 461 Payment does not affect Dividend Policy

Compliance/Maintenance (461 (c)) Policyholder Dividends comply with Dividend Policy (464.2) Fairness of Dividend Policy (165.3.1) - new Fairness of Par Management Policy (165.3.2) - new Fairness of Adjustable Change Criteria (165.3.3) - new Fairness of Proposed Policyholder Dividends (464.2) - new Fairness of Changes Made to Adjustable Policies and

Compliance with Criteria (464.1 (l)) - new

(all section references are to Insurance Companies Act of Canada)

8

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Participating Policyholders• Board to establish a policy regarding the management of each

par account• Appointed actuary (AA) annual report to Board on

(continuing) fairness to par policyholders of the dividend policy and the par account management policy

• AA report to Board on the fairness to par policyholders of a proposed dividend

• Board required to consider AA report before establish or amend either policy or declare dividend

• These AA reports to be prepared in accordance with generally accepted actuarial practice with changes or directions from OSFI

• Regulations for content of dividend policy, par account management policy, disclosure, etc.

9

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Adjustable Policyholders

• To be defined in the regulations; - expect will exclude Group, annuity, and participating policies

• Board to establish criteria for changing the premium or charge for insurance, amount of insurance or surrender value for adjustable policies

• AA annual report to Board on (continuing) fairness to adjustable policyholders of the criteria established

• Board required to consider AA report before establish or amend criteria

• AA annual report to Board on whether any changes made for adjustable policies during year comply with the criteria established and were fair to adjustable policyholders

• If changes made to adjustable policies or on renewal, must provide “prescribed info” to those adjustable policyholders

10

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

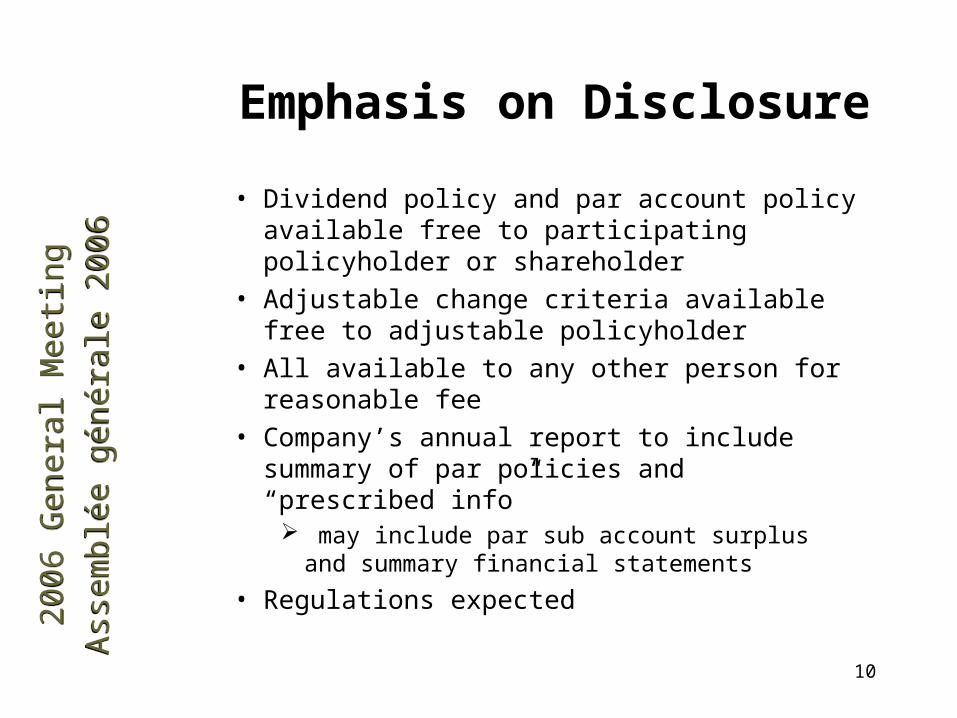

Emphasis on Disclosure

• Dividend policy and par account policy available free to participating policyholder or shareholder

• Adjustable change criteria available free to adjustable policyholder

• All available to any other person for reasonable fee

• Company’s annual report to include summary of par policies and “prescribed info”

may include par sub account surplus and summary financial statements

• Regulations expected

11

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Bill C-57 Status

• Amended Federal Insurance Companies Act; received Royal Assent Nov 2005

• Changes are not in effect until proclamation

• Regulations needed in order to implement

• Draft regulations from Finance for public exposure this fall

• C-57 also has several items re corporate governance matters

• Timing of implementation not yet clear

• New “Policy” items include period of six months to comply after proclamation

12

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

New OSFI Par Guidelines

• OSFI has developed new Par Guidelines; expect drafts to be released with C-57 draft regulations

• Several items expected:– disclosure to policyowners of items not covered in

Finance Regulations

– more detail in allocation policies (investment income, expense, tax)

– make ‘demutualization closed block” rules permanent

– interpretations re Section 461 payments to shareholders

13

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

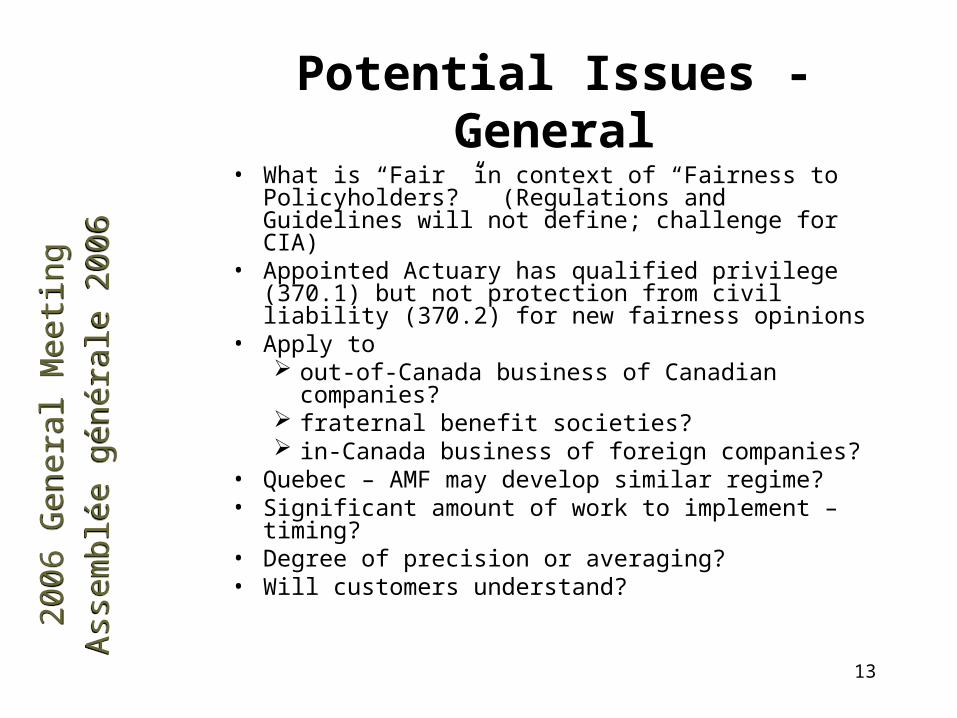

Potential Issues - General• What is “Fair” in context of “Fairness to

Policyholders?” (Regulations and Guidelines will not define; challenge for CIA)

• Appointed Actuary has qualified privilege (370.1) but not protection from civil liability (370.2) for new fairness opinions

• Apply to out-of-Canada business of Canadian companies? fraternal benefit societies? in-Canada business of foreign companies?

• Quebec – AMF may develop similar regime?• Significant amount of work to implement – timing?• Degree of precision or averaging?• Will customers understand?

14

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

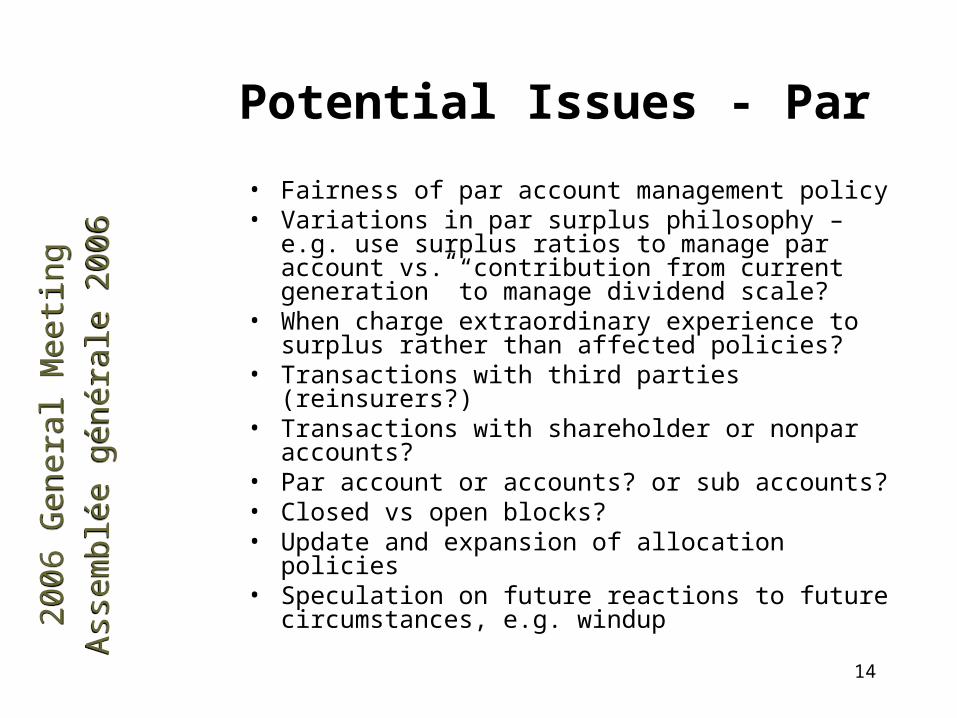

Potential Issues - Par

• Fairness of par account management policy• Variations in par surplus philosophy – e.g. use surplus

ratios to manage par account vs. “contribution from current generation” to manage dividend scale?

• When charge extraordinary experience to surplus rather than affected policies?

• Transactions with third parties (reinsurers?)• Transactions with shareholder or nonpar accounts?• Par account or accounts? or sub accounts?• Closed vs open blocks?• Update and expansion of allocation policies• Speculation on future reactions to future circumstances,

e.g. windup

15

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Potential Issues - Adjustable• Definition of adjustable policy is key

− Act specifies subjects for criteria, but definition to be in regulations

− Unilateral adjustment at company’s discretion?− Health products? Reinsurance?

• Fairness– If heavy death claims - fair to increase charges for those who

didn’t die? To cover future claims? To recover past losses? I.e, Measure fairness by lifetime, current or expected experience??

– Opinion on profit targets?– How do you demonstrate or prove fairness of actions?– Materiality considerations for small inactive blocks? – Degree of precision/averaging (e.g., policy size? Issue year?

Product? Distribution?)– If have increased reserves because of low lapse rates - is it fair to

increase charges?• Applies to in force adjustable policies as well as new sales

16

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006CIA Response

• CIA task force reporting to AA Committee– to develop guidance for AA on report preparation including

“generally accepted actuarial practice”– likely in form of Standards of Practice and educational notes– to comment on draft regulations and OSFI guidelines– to communicate to members

• Working group structure Adjustable Policies – Nick Bauer Dividend Policies – Al Edwards Par Account Management – Simon Curtis

• May need to develop “actuarial” definitions for terms used in regulations

• Need input on issues, practical problems, unidentified issues

• Some issues mix actuarial and legal considerations

17

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

What Does “Fair” Mean?

• Webster’s− marked by impartiality and honesty; free from self-interest,

prejudice or favouritism− fair implies an elimination of one’s own feelings, prejudices

and desires so as to achieve a proper balance of conflicting interests

• Black’s Legal Dictionary− just; equitable; even-handed− equal, as between conflicting interests

“Fair to policyholders” may mean - “it appropriately balances the interests of these policyholders

and other stakeholders”.

18

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

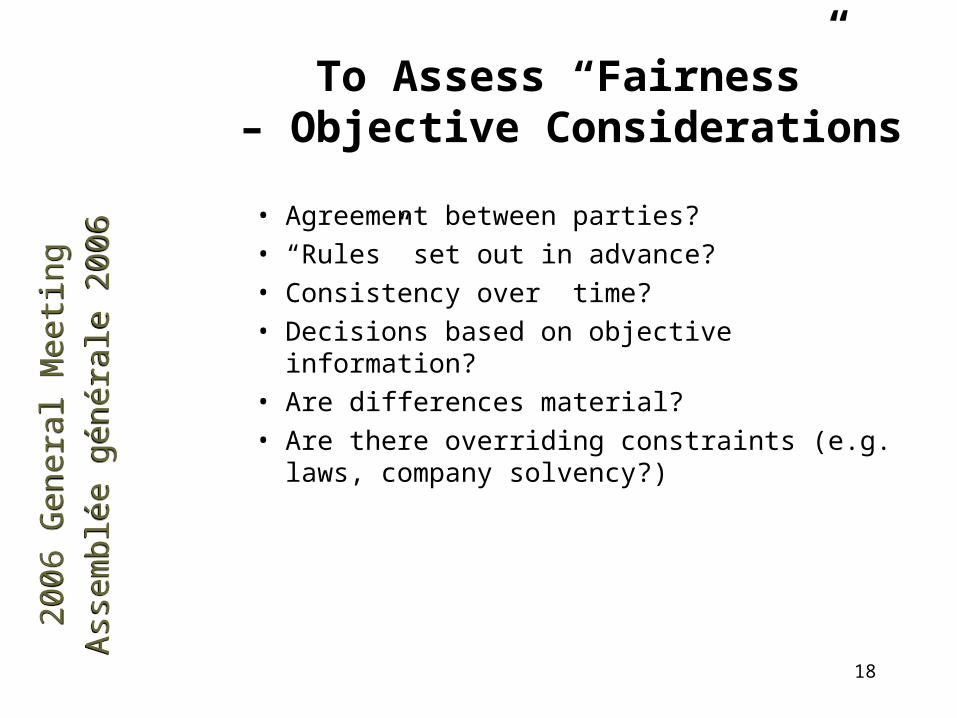

To Assess “Fairness”– Objective Considerations

• Agreement between parties?

• “Rules” set out in advance?

• Consistency over time?

• Decisions based on objective information?

• Are differences material?

• Are there overriding constraints (e.g. laws, company solvency?)

19

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

To Assess “Fairness” – Subjective Considerations

• Is the result reasonable?

• Was discretion or judgment exercised reasonably?

• Are individuals in same/different circumstances treated same/differently?

• Are the decisions or actions arbitrary?

• Are there circumstances that limit the ability to reflect differences?

20

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

Discussion

• Questions ??

• Comments

21

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

2006

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2006

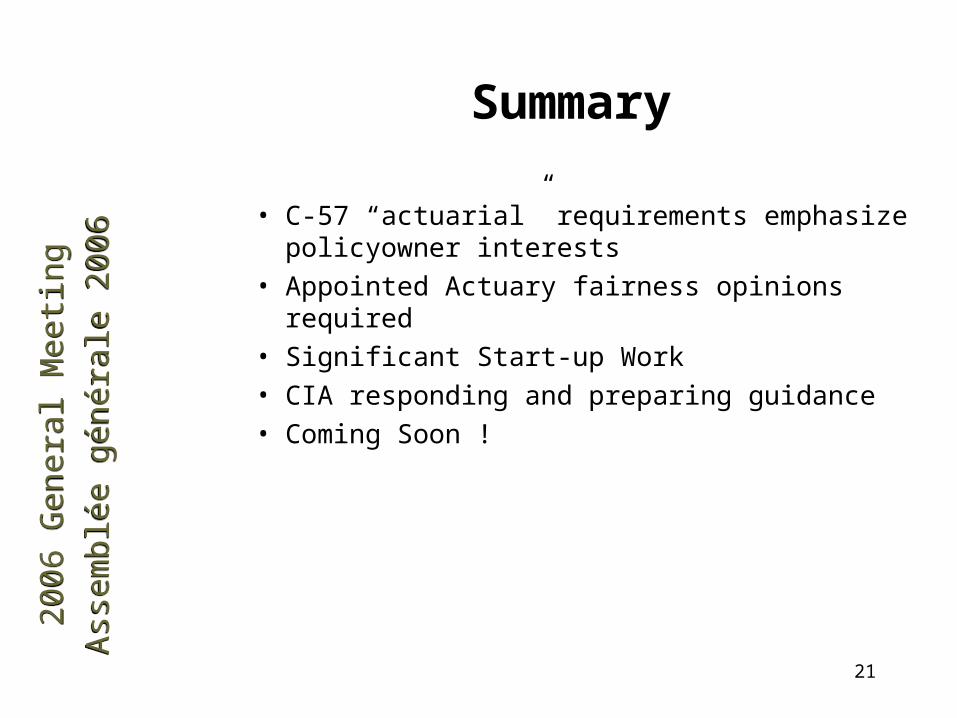

Summary

• C-57 “actuarial” requirements emphasize policyowner interests

• Appointed Actuary fairness opinions required

• Significant Start-up Work

• CIA responding and preparing guidance

• Coming Soon !