Embed Size (px)

Citation preview

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 1/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 1

EX-99.C.2 2 e60672a1exv99wcw2.htm EX-99(C)(2): DUFF & PHELPS, LLC PRESENTATION

Exhibit (c)(2

F ai r n ess An al y s is C o n f i d en t i al P r esen t at io n t o t h eS p ecial C o m m i tt eeo f t h eB o ar d of Di r ect o r s Ap ri l 2 5 , 2 0 08 S T R I C T L YC ONF I DE NT I AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 2/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 2

DisclaimerThef ollowingpagescontainmater ialthatis beingprovidedbyDuff &Phelps,LLC(“D uff&Phelps”) totheSpecial Committeeofthe BoardofDire ctors(the“Committee”) ofAtari,Inc. (“Atari”or the“Company”)inthe contextofa meetingheldto consideraproposedtr ansactionbywhich InfogramesEntertainmentS.A. (“IESA”or“ Buyer”)willac quireallthe outstandingcommonstockof Atarinotowned byIESA(the “ProposedTransaction”).The accompanyingmaterialwas compiledorprepared onaconfidential basisforthe sole use ofthe Committee andnotwitha viewtowardpublic disclosure.Because thismaterialwas preparedfor use in the contextofan oralpresentationto the Committee,whichis familiarwiththe businessandaffairs ofAtari,neither AtarinorDuff &Phelps,norany oftheirr espective legalorfinanci aladvisorsor accountants,take anyresponsibilityfor the accuracyorc ompletenessofanyof the materialif usedbypersonsother thanthe Committee. These materialsare notintendedtor epresentanopinionbut rathertose rve asdiscussionmaterials forthe Boardtoreview andasa basisuponwhichDuff & Phelpsmayrender anopinionastothe fairness,from afinancialpoint ofview,to thestockholdersof theCompanyotherthan IESA(the“ PublicShareholders”)of theconsiderationto bereceivedby suchholdersinthe ProposedTransaction.Anopinion wouldnoti)a ddressthemerits oftheunderlyingbusiness decisionofAtari toenterinto theProposedTransaction;ii) constitutearecommendation toAtari,the BoardofDirec torsofAtari, theCommittee,the stockholdersofAtari, oranyother personasto howsuchpersonshould vote orasto anyotherspecific actionthatshouldbe takenin connectionwiththe ProposedTransaction;or iii) create anyfiduciaryduty onDuff&P helps’spartto anyparty.The informationutilizedin preparingthispresentation wasobtainedfrom Atari,public sources,andnon-public sources.Anyestimates andprojectionscontainedher einhave beenpreparedby the seniormanagementof Atariandinvolve numerousandsignificant subjective determinations,whichmay ormaynotprove tobe correct.Duff & Phelpsdidnotattempt toindependentlyverifysuch information. Norepresentationor warranty,expressedor implied, ismade astothe accuracyor completenessof suchinformationandnothing containedhereinis, orshallbe relieduponas, arepresentation,w hetherasto thepastor thefuture.No selectedcompanyor selectedtransactionused inouranalysisis directlycomparable toAtari,IESA, ortheProposedTra nsaction.STRICTLYCONFIDENTAL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 3/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 3

Assumptions,Qualificationsand LimitingConditionsDuff& Phelpshasmade numerousassumptionswithrespect toindustryperformance, generalbusiness,market andeconomicconditionsand othermatters,many ofwhichare beyondthecontrolof anypartyinvolvedin theProposedTransaction. Ouranalysisis necessarilybasedupon market,economic,financial andotherconditionsas theyexistandc anbeevaluated asofthe datehereof.D uff&Phelps assumed thatanyestimates, evaluationsandprojections (financialor otherwise)furnishedto Duff&Phelps were reasonablypreparedand baseduponthe bestcurrentlyavaila ble informationandgoodfaith judgmentofthe personorpersons furnishingthe same.Duff& Phelpsassumedthata llgovernmental,regulatory orotherconsents andapprovalsnecessary forthe consummationofthe ProposedTransactionwill be obtainedwithoutanyadverse effectonthe Companyorthe contemplatedbenefitsexpected tobe derivedinthe ProposedTransaction.Duff & Phelpsassumedwithoutver ificationthe accuracyandadequacy ofthe legaladvice givenbycounselto Atarionall legalmatterswith respecttothe ProposedTransactionandassumedal lproceduresrequired bylawto betakeninc onnectionwiththePr oposedTransactionhavebeen, orwillbe, duly,validlyandtimely takenandthatthe ProposedTransactionwill beconsummatedina mannerthatcomplies inallrespects withtheapplicable provisionsoftheS ecuritiesActof 1933,asamended,the SecuritiesExchangeAct of1934,asame nded,andallother applicablestatutes,rules andregulations.Duff &Phelpsdidnot make any independentevaluation,appraisal orphysicalinspectionof eitherthe Company’sorIESA’ssolvency orofany specific assetsorliabilities (contingentorotherwise) .Thispresentationshould notbe construedasa valuationopinion,creditr ating,solvencyopinion,an analysisofeither the Company’sorIESA’scr editworthinessor astaxadvice orasaccounting advice.Duff& Phelpshasnotbee nrequestedto,a nddidnot,(a) negotiate the termsofthe ProposedTransactionor( b)advise the BoardofDirec torsoranyother partywithrespect toalternativesto the ProposedTransaction.Inaddition, Duff& Phelpsisnotexpre ssinganyopinionasto the marketprice orvalue ofthe Company’scommonstockafter announcementofthe ProposedTransaction.Duff &Phelpsrelied uponthefact thattheBoard ofDirectors oftheCompany,the Committeeandthe Companyhavebeenadvised bycounselasto alllegalmatte rswithrespect totheProposed Transaction,includingwhethera llproceduresrequired bylawto betakeninc onnectionwiththePr oposedTransactionhavebeen duly,validlyandtimelyt aken;andDuff &Phelpshasnot made,andassumesno responsibility to make, any representation,orr enderanyopinion,as to anylegalmatter. S TRI CTLY CON FI DEN TI AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 4/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 4

TableofContents

I.Overview ofProposedTransaction

II.ObservationsRegar dingAtari

III.PublicMar ketValue

IV.SelectedPublic CompanyAnalysis

V.SelectedM&A TransactionAnalysis(Valuation Multiples)

VI.Selected M&ATransactionAnalysis( PremiumsPaid)

VII.Net AssetValueAnalysis

VIII.LiquidationAnalysis

4 S T R I C T L Y C O N F I D E N T I A L

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 5/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 5

I . Ov er v i ewo f P r o p o s ed Tr an s acti o n S T R I C T L YC ONF I D E NT I AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 6/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 6

OverviewofP roposedTransactionTransactionOver viewOnMarch 6,2008,Atari,Inc. (“Atari”or the“Company”)received anon-bindingexpressionof intentfromInfograme sEntertainmentS.A. anditsaffiliates (“IESA”or the“Buyer”),whic howns51.6%of theoutstandingsharesof Atari,toac quireallthe outstandingcommonstockof Atarinotowned byIESAfor apershare cashamountof$1.68 (the“ProposedTransaction”). OnMarch5, 2008,theclosing pricepershar e ofthe Ataricommonstock was$1.68.On March11,2008,Duff &Phelps,LLC(“Duff &Phelps”)was engagedasfinancial advisorto provide anopinionto the SpecialCommittee ofthe BoardofDirec torsofAtari (the “SpecialCommittee”) asto the fairness,from a financialpointof view,to the stockholdersofthe CompanyotherthanI ESA(the “Public Shareholders”)ofthe considerationto be receivedbysuch holdersin the ProposedTransaction.On behalfofthe SpecialCommittee, Duff& Phelpsheldmeetingsa nddiscussionswithAtari managementandAlixPartners, the Company’srestructuringadvisors, undertookinitialevaluationof the Companyandreached preliminaryvaluationfindings.Atthedirection oftheSpecial Committee,Duff& Phelpssubsequentlyengagedin limiteddiscussionswithLaz ard,Ltd.(“Lazard”), financialadvisorto IESA,withregard totheper sharecashconsidera tionof$1.68(“Per ShareCashConsiderat ion”).OnMarch 18,2008,Lazardinformed Duff&Phelps thatIESAwas notwillingtoincr easethePer ShareCashConsiderati on.Lazardcommunicatedon behalfofIESA thattheper shareprice ofthecommonstock hadincreasedin the fewdaysbefore the announcementofthe ProposedTransactionandthe PerShare CashConsiderationrepresented apremiumtothe share price five daysand30days priorto the announcement.Afterr eviewingthe PerShare CashConsiderationwith the SpecialCommittee andMilbankTweedHa dleyMcCloyLLP(“Milbank”), legaladvisorto the SpecialCommittee,and atthe directionofthe SpecialCommittee,Milbanke ngagedin discussionswithlegalc ounselofIESA torequestclarif icationonthe following:–IESA’sintention withrespectto fundingthe Company’soperatinglossesand workingcapitalneeds throughthe completionofthe ProposedTransaction;–I ESA’sintentionwithrespec ttoobtaininganextensionon theforbearance agreementwithBlueBa yAssetManagementplc (“BlueBay”);and –Theminimumshareholder approvalIESAis requiringtocomplete theProposedTransaction. OnApril11,2008, Atarireceived thefirstdra ftofthe mergeragreement effectingthePr oposedTransaction.OnApril 21,2008,Atarir eceivedthefir stdraftof thecreditagree mentprovidingfinancialsupport throughclosing.BetweenApr il11andApril 24,Atari,IESA, BlueBay,the Committee andtheirrespect ive counselengagedin numerousdiscussionsanddraft revisionsofthe transactiondocuments.S TRI CTLY CON FI DEN TI AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 7/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 7

OverviewofP roposedTransactionSummaryof DueDiligenceI nconnectionwithour analysis,wehave madesuchreviews, analysesandinquiries, aswehave deemednecessarya ndappropriateunder thecircumstances.Duff &Phelpsalsotook intoaccountits assessmentofgeneral economic,marketand financialconditions,as wellasits experienceinse curitiesandbusinessvaluat ion,ingeneral,a ndwithrespect tosimilartransact ions,inparticular.O urduediligence and analysiswithregar dsto the ProposedTransactionincluded,but wasnotlimitedt o,the itemssummarizedbelow. – Discussedthe operations,financialconditions,f uture prospectsandprojected operationsandperformance ofthe Companyandthe ProposedTransactionwith the managementofthe Company;– Reviewedadraf tofthe MergerAgreement datedApril23, 2008;– Reviewedadra ftofthe CreditAgreement datedApril22, 2008;– Reviewedcertain publiclyavailable financialstatements andotherbusinessand financialinformationof the CompanyandIESA, respectively, andthe industriesinwhich theyoperate;– Reviewedcertain internalfinancial statementsandother financialandopera tingdataconcerningtheCompany,which theCompanyhasrespective lyidentifiedas beingthemostcurr entfinancialstateme ntsavailable;– Reviewedcertain financialforecasts, aswellas informationrelatingto certainstrategic, financialandoperational benefitsanticipatedfr omtheProposedTransaction, allasprepared bythemanagementof theCompany;–Reviewed thehistoricaltrading priceandtrading volumeoftheCompany CommonStock,andthe publiclytradedsecuritie sofcertain othercompaniesthat we deemedrelevant; – Comparedthe financialperformance ofthe Companyandthe pricesandtra dingactivityofthe CompanyCommonStockwith those ofcertain otherpubliclytraded companiesthatwe deemedrelevant;– Comparedcertainf inancialtermsof the ProposedTransactionto financialterms,to the extentpubliclyavailable, ofcertainother businesscombinationtransactionsthat we deemedrelevant;a nd– Conductedsuchotheranalyses andconsideredsuchother factorsaswe deemedappropriate. S TRI CTLY CON F IDE NTI AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 8/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 8

OverviewofP roposedTransactionFairness ConsiderationsIndetermining whetherthePer ShareCashConsideration tobereceived bythePublicShar eholdersintheP roposedTransactionbefa ir,froma financialpointof view,tothePublic Shareholders,Duff &Phelpsconsidered,among otherfactors: –Thecurrent, historicalandprojected financialperformance oftheCompanybase donare viewofthe Company’swellas ourdiscussionswiththe Company’smanagementandtheir advisors;– The PerShare CashConsiderationrelative to recentandhistoric tradingpricesof Ataricommonstock; – The adequacyofthe premiumimpliedbythe PerShare CashConsiderationrelative to the premiumspaidin selectedpublic-to-private transactions;and– Severalvaluationmet hodologies,including:• Selected publiccompanyanalysis • Selected M&Atransactionanalysis(valuation multiples) • Netassetvalue analysis • LiquidationanalysisTheCompany’s currentcashand liquiditypositionandits prospectsfor obtainingadditionalcashinfusions from personsotheraffi liates.–In connectionwiththe negotiationofamer ger,IESAand the Companyarenegotiatinga creditagreementwh i ch wi l l Atar i ’ s l i q ui d i t y co ns t r ai nt s . Ad i s co un t ed cas h f lo w( “DC F ”) an aly s i s was n ot u t i l i zed as man ag em en t d o es n o t pr ep ar ep r o ject i o ns p as t o n ey ear. S T R I C T L YC ONF I DE NT I AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 9/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 9

OverviewofP roposedTransactionValuationBenchmarks Duff&Phelps consideredseveralvaluat ionapproachestoesta blishvaluationbenchmarksagainst whichtocompare thePerShar eCashConsideration: PublicMarketValuation– Duff&Phelps analyzedtheclosing priceandtra dingvolumeofAtari commonstockoverthe past12months.Thisa nalysiswasusedto determinethera ngeoffair marketvaluethe markethasascr ibedtothecommon stockpriorto and on the date ofthe announcementofthe ProposedTransaction.Selected Public CompanyAnalysis– Duff&Phelps reviewedvaluationmultiples ofselectedpublicly tradedcompaniesand appliedvaluationmultiplesto Atari’sselectedrecentoperating results.The Company’snegative EBITDAlimitedthe relevance ofthe methodologyto the applicationofenterprise value to revenue multiplesforthe selectedcompanies.Selec tedM&ATransactionAnalysis (MultiplesValuation)– Duff& Phelpsreviewedvaluation multiplesofselected M&Atransactionsand appliedvaluationmultiples toAtari’sselect edrecentoperating results.The Company’snegative EBITDAlimitedthe relevance ofthe methodologytotheapplicationofenterprise valuetorevenue multiplesforthe selectedM&Atra nsactions.SelectedM&A TransactionAnalysis(Premiums Paid)–Duff &Phelpsreviewed thepremiumspaid inpublictoprivate transactionsinwhich themajorityshareholder purchasedtheremaining minorityequitystake.D uff&Phelpsc omparedthepremiums overthe1-day,5-day and30-daytradingpric epriorto theannouncementof suchtransactionstothe impliedpremium in the ProposedTransaction.Premiumspaid analysisisrelevant butlimitedbythe Company’sdependence onIESA,the majorityshareholderin the Company.NetAssetValue Analysis– Duff&Phelps reviewedthe Company’sauditedbalance sheetasof December31,2007 andthe Company’spreliminaryinternal balance sheetasof March31,2008to determine the netassetvalue ofAtariandaddedthe fairmarketval ue ofthe Company’sintellectualproperty.I ndeterminingthe fairmarket value ofthe intellectualproperty,Duff & Phelpsrelied,with independentverificationthere of, oninformationprovidedby management,includingthirdparty appraisals. LiquidationAnalysis–Since the Companyisinviolation ofitsweek l y cash f l o wco v enan t s o n i t s S eni o r S ecu r ed Cr ed i t f aci li t y p r o v id ed b y B l u eB ay , Du f f & P h el p s al s o anal y zed t h ep ot en t i al r eco v er i es by h o l d er s of At ar i ’ s co m mo n s t o ck i n aC hap t er 1 1 b ank r u p t cy . S T R I C T L Y C ONF I D E NT I AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 10/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 10

I I . Ob s er vat i o n s R eg ar d i ng At ar i S T R I C T L Y C ONF I DE NT I A L

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 11/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 11

ObservationsRegardingAtar iCompanyOverview Foundedin1992asG TInteractiveSoftw areCorporationand headquarteredinN ewYork,NY,the Companycompletedaninitial publicofferingin 1996.In1999,IESA, aFrenchcor porationlistedonthe Euronext,acquiredbeneficial ownershipofa majorityshareof theoutstandingcommonstockof theCompanyandsubsequently renamedtheCompanyI nfogrames,Inc.In May2003,theCompany changed itsname to Atari,Inc.a ndbegantradingon the Nasdaqunderthe ticker“ATAR”.IESA currentlyowns51.6% ofAtari’scommon stock.Atariengages in the publishing,development,anddistributionof videogamesoftware primarilyin NorthAmerica. Ataridistributesvideo gamesforvarious platforms,includingSonyPlaySta tion2,PlayStation3 andPSP,NintendoWiiandDS,and MicrosoftXboxandX box360,aswell asforper sonalcomputers.The Companyhasobtainedthe righttouse the “Atari” brandname undera license grantedfromAtar iInteractive, Inc., anIESA subsidiary,thatexpires in2013. Twootherlicense agreementsexpire inthe nextfive years:–The DragonBallZ license agreement,whichisAtari’slargest titleandreprese ntedapproximately28%of totalnetrevenue inFY2007,expiresin January2010;–IESA distributionagreementsreprese nted56%oftotal netrevenuein FY2007.Theagreements includetheOld DistributionAgreement,enacte din1999,which governsthedistributionof Atari’sclassic gamelibraryas wellasa Short-FormDistributionAgree ment,enactedin 2007,governingnewrelease s.TheOldDistr ibutionAgreementwould terminateif IESAreducedits holdingsin Atarito below25%.The Short-FormDistributionAgre ementexpiresin December2010;Until 2005,Atariwas activelyinvolvedin developingvideogamesand in financingdevelopmentof videogamesbyindependent developers,whichAtari wouldpublishanddistribute underlicensesfrom the developers.Beginningin 2005,because ofcashconstraints, Atarisubstantiallyreduced itsinvolvementin developmentofvideogames andannouncedplansto divestitsinternal developmentstudios.Source:S ECfilings, equityresearch,Bloomberg andAtariboard presentationsS TRI CTLY CON F IDE NTI AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 12/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 12

ObservationsRegardingAtar iCompanyOverview (Continued)Duringfiscal years2006and2007, Atarisolda numberofintellectual propertiesanddevelopment facilitiesinor dertoobtainca shtofundoperations. During2007,Atari raisedapproximately$35.0 millionthroughthesale oftherights toitsTestDr ivergamesand certainotherintelle ctualproperty,andthe saleofits ReflectionsandShiny studios.Bytheend of2007Atari nolongerownedany developmentstudios.Ataria lsoexitedthe software distributionbusinesswhichfurther contributedto the Company’sdecreasingrevenue. The reductionofdevelopment activitiessignificantlyreduced the numberofgames thatAtaripublished. Atarihasprojec tedFY2008netre venue of$78.6 millionafterr egisteringLTM netrevenue asofDecember 31,2007of$91.8 million.DuringFY2007,net revenue frompublishingactivities were $104.0 million,comparedwith$153.6 millionduringFY2006and $289.6millionduringFY2005. Atari’sbudgetfor fiscalyear 2009projectsnetr evenue of$126.5millionandEBITDA of$2.0million. –The budgetishighlydependent onIESA’srelease schedule andthe successofeach newtitlerelease. –Thebudgetwill requirefundingof asmuchas $18millionandthe Company’sabilitytoobtain additionalfinancingis uncertain.TheCompanyis engagedina multifacetedrelationshipw iththeParent, whichresultsin themajorityof Atari’sproductcoming fromIESA.Historic ally,Atarihas alsoreliedon IESAforf undingwhichhascome intheform ofthesale ofproductionstudiosand intellectualpropertyt oIESAas wellasloan facilitiesfrom IESA’slargestshareholder, BlueBay.Source:SEC filings,equityresearch, BloombergandAtari boardpresentationsS TRI CTLY CON FI DEN TI AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 13/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 13

ObservationsRegardingAtar iChronologyofRecent Events(April2007– YTD2008)April 5,2007–Atari announcesthatitsChair man/ActingCFOBruno Bonnellisdeparting.Bonnell’s departurefromA taricomesat thesametime ashisdeparture asCEOanddir ectorofIESA. May1,2007–A tariannouncesa 20%workforcer eduction.May22,2007– Atarielects ArturoRodriguezto serveasacting ChiefFinancialOf ficeruntilsomebodyis electedtoser ve permanently inthatcapacity. July24,2007– The BoardofDire ctorselectsMichael G.Corrigan,a memberofthe Boardsince November2005,toserve asitsnon-executive Chairman.September7, 2007– Atariannouncesthe resignationofMarcel NicolaiasSenior Vice President,ProductDevelopment OperationsandChief TechnologyOfficer.September 18,2007– The Companyfilesits SECForm10-Kf orthe periodendingMarch 31,2007in whichDeloitte &Touche LLPgivesaqualified opinionexpressingdoubtthat the Companycancontinue asa goingconcern.October 1,2007–GuggenheimCorpora te FundingLLC(“Guggenheim”)provides a waiverofcovenant defaultsasof June 30, 2007andreducestheaggregateborrowingcommitment oftherevolvingline ofcreditto $3million(downfr om$10million).October 5,2007–James Ackerly,RonaldC.Be rnard,MichaelG. Corrigan,DennisGuyennota ndAnnE.Kronen areremovedf romtheBoard ofDirectors ofAtariby actiontakenby IESA.October10, 2007–CurtisSolsvig IIIisa ppointedAtari’sChief RestructuringOfficer andAlixPartners,a firmatw hichMr.Solsvigis aManagingDirector, isretainedto advisethe Companyonitsoperational restructuringinitiatives.O ctober15,2007– Atariannouncesthe appointmentofWendellA dair,Eugene I.Davis,James B.Shein,and BradleyE.Scher asindependentboard members.Inconjunctionwit htheirrespective appointmentsto Atari’sBoardof Directors,Messrs Adair,Davis,Shein andScherare appointedto serve onthe board’sSpecialCommittee. October18,2007– Atariconsentsto the transferof the loansoutstandingof$3 millionfrom Guggenheimtoanaf filiate ofBlueBay.October 23, 2007–BlueBayamends the creditagreement,incr easingAtari’sborr owingcapacityto $10million. S TRI CTLY CON F IDE NTI AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 14/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 14

ObservationsRegardingAtar iChronologyofRecent Events(April2007– YTD2008)November13, 2007–Ataria nnouncesabusinessrestructur ingplantofocus theCompanysolelyon publishinganddistribution.TheCompanya lsoannouncedlicenseagr eementswithIESA regardingtheTestD rivefranchisegr antingIESAexclusive rightstothef ranchise.Atari alsoannouncesthere movalofDavidP ierceasCEO. CurtisSolsvig,currently theChiefRestructuri ngOfficer,assumes the role ofInterimCEO. December10,2007– Atariamendsits BlueBaycreditf acility,increasingAtari’ sborrowingcapacity from$10millionto $14million.February12, 2008– Atarireportse arningsforthe thirdquarterFY 2008andnine monthsendedDecember 31,2007.Despite decreasingrevenue,Ata ri’scost-cuttingeffor tsresultedin slightlyimprovedoperatingloss (quarter-over-quarter results).Asa resultofcovenant violations,the Companyentersintoa forbearance agreementwithBlueBay. March6,2008– Atarireceives a letterfrom IESA regardinga non-bindingexpressionofintent toacquire the outstandingcommonstockofA tarinotowned byIESA fora pershare cashprice of $1.68.March24,2008– Atarireceives aStaff DeterminationLetterf romtheNasdaq ListingQualificationsDepart mentstatingthatAta rihasnotgained compliancewiththe requirementsofN asdaqMarketplaceRule 4450(b)(3),andthat itssecuritiesar etherefore subjecttodelistingfr omTheNasdaqGl obalMarket.Atari hasrequesteda hearinganduntil adeterminationis reached,theCompany’s shareswillcontinue totradeont heNasdaq.March 26,2008– Atariannouncesthat ThomasSchmider,Co-Foundera ndCOOof IESA,resignedas amemberof Atari’sBoardof Directorseffe ctive March21,2008.March 31,2008– Atariannouncesthe appointmentofJimWilson asitsCEO andPresident,effec tive immediately.Mr.Wilsonis assumingthe responsibilitiesofCEO whichhave beenoverseenby CurtisG.SolsvigI II,Atari Inc.’sChiefRestructuri ngOfficersince October2007.April 4,2008– Atariannouncesthat CurtisG.Solsvig IIIresigneda scompany’sChiefRestr ucturingOfficer effective April2,2008. Mr.Solsvigwillcontinue toprovide servicestothe companypursuanttoan engagementletterpre viouslyenteredintobetwe enAtariand AlixPartnersLLP, whichwasretainedt oassistthecompany throughitsrestructuring process.April22,2008 –Atariannounces thatJean-MichelPerbet, DeputyCOOof IESAandChairman ofIESAEurope, resignedasa memberofAtari’s BoardofDire ctorseffective April16,2008.April 24,2008–Atari, IESA,BlueBay,the Committeeandtheir respectivecounselengaged innumerousdiscussionsanddra ftrevisionsof thetransactiondocuments. STRI CTLY CON FID ENT I A L

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 15/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 15

ObservationsRegardingAtar iFinancialSummary Thedeteriorationof Atari’sbusinesshas resultedfromincre asedcompetition,a weakproductpipeline, anindustry-widedecline inaveragesell ingpricefor gamesoftware, lackofan on-linepresencea ndlossofinternal talentandleader ship.Atari’scurrent budgetforFY2009is dependentonthetimely releaseandsucce ssofnew gamesandtheCompany’s abilitytosecure additionalfinancing.Atari, Inc.Historicala ndProjectedFinancial Performance FiscalYearEndedMarch31, ($in millions)FY2003AFY2004AFY 2005AFY2006AFY 2007ALTM(U) FY2008EFY2009BNetRevenue $506.5 $468.9 $343.8 $206.8 $122.3 $91.8 $79.2 $124.2 Growth na (7.4%)(26.7%)(39.8%) (40.9%)(24.9%)(35.2%) 35.3% CostofGoodsSold 257.6 260.1 203.6 136.7 74.8 52.7 41.4 80.4 GrossProfit248.9 208.8 140.2 70.1 47.5 39.1 37.9 43.8 GrossMargin49.1% 44.5% 40.8% 33.9% 38.8% 42.6% 47.8% 35.2% S,G& A129.5117.794.073.447.139.739.2 43.2R& D75.478.258.351.927.720.19.4 0.5D& A7.59.27.05.23.01.9 3.82.7______TotalOperating Expenses212.4205.1159.3130.577.861.7 52.446.5EBIT36.53.7(19.1)( 60.4)(30.3)(22.6)( 14.5)(2.7)EBITMargin 7.2%0.8%(5.6%) (29.2%)(24.8%)(24.6%) (18.4%)(2.2%)EBITDA $44.0$13.0($12.1)($55.1)($27.3) ($20.8)($12.3)$0.2EBITDA Margin8.7%2.8%(3.5%) (26.6%)(22.3%)(22.7%) (15.6%)0.2%LTM= AsofDecember 31,2007(3rdQuarter FY2008)EBITDA= Earningsbeforeinterest, taxes,depreciationand amortization,adjustedfor one-timegainsor lossesonthesale ofassetsand investments,discontinuedoperations,restr ucturingexpensesandgoodwill write-downs.In FY2007,the Companyincurreda $54.1 milliongoodwillwrite-down. Source:CompanySECFilings andCompanyManagementproject ionsSTR ICT LYCO NFI DEN TI AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 16/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 16

ObservationsRegardingAtar iBalanceSheet SummaryAsof December31,2007, Atari’sworkingcapital wasnegative$10.3 millionanditsstockholders’ equitywasnegative $16.8million.Asa resultofsubstantial operatinglossesandsignific antcashrequirements tofundworkingcapita l,Atariis liquidityconstrainedand itsabilitytosec ureadditionalfinancing isuncertain.Atar i,Inc.Balance SheetSummary($ inmillions)December 31,March31,De cember31, March 31,2006200720072008(Estimated)Cash$ 3.6 $ 7.6 $ 5.4 $ 10.0 Receivables,net23.2 9.5 16.2 (0.3)Inventories13.4 8.8 7.4 6.5 PrepaidExpensesandOtherCurre ntAssets16.3 9.7 6.0 7.7 TotalCurrentAssets56.5 35.6 34.9 24.0 NetProperty,Plant &Equipment3.8 4.2 6.3 6.4 GoodwillandIntangibles55- - -OtherLong-TermAssets3.9 3.0 2.2 2.1 TotalAssets$ 119.5 $ 42.8 $ 43.5 $ 32.6 AccountsPayable $ 13.3 $ 11.0 $ 10.6 $ 9.7 AccruedLiabilities 15.4 13.4 11.5 6.8 RoyaltiesPayable 3.34.33.82.7Credit Facility7.0— 14.014.0Due to Related Parties9.95.7 5.32.7 OtherCurrentLiabilities0.4 —— 0.9TotalCurrentLiabilities 49.334.445.236.8 DuetoRelated Parties, Long-Term1.41.93.03.6Long-TermDeferred Rent—— 6.77.1RelatedPa rtyLicenseAdvance ——5.1 5.4OtherLong-TermLiabilities 2.03.40.3-TotalLiabilitie s52.739.760.352.9Stoc kholders’Equity66.83.1(16.8) (20.3)TotalLiabilities& Stockholders’Equity$119.5 $42.8$43.5$ 32.6Source:CompanySEC Filings,ManagementEstimates STRI CTLY CON FID ENTI AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 17/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 17

ObservationsRegardingAtar iFY2009MonthlyBudgetAta ri’sFY2009budgetis highlydependentonAtari’s (i)developmentpartners (principallyIESA) releasingtheirr espectivegametitles ontimeandthe performanceoft hesetitles,(ii) abilitytostreamline itsoperations,(iii) abilitytoinstill stabilityinmanysenior managementrolesand (iv)abilityto secureadditionalfinancing. Atari,Inc.Pr ojectedFinancialPer formance—FY 2009BudgetbyMonthFiscal YearEndingMarch31 ($in thousands)April MayJune July AugustSeptemberOctober NovemberDecember JanuaryFebruaryMar ch TotalNetRevenue $3,417$4,258$29,707$7,387$4,055$6,206$10,216$21,490$8,839$4,863$11,234$12,505$124,176Growth OverPriorYea rPeriod(11.6%) (0.8%)1,223.0% 15.4% (15.4%)194.8% 6.7% 24.1% (31.2%)(10.1%)111.9% 350.9% 60.9% CostofGoodsSold 2,0972,62018,3444,6382,5653,1936,76614,9655,889 3,3417,6568,33780,412GrossProf it1,3201,63811,3632,7491,4903,0133,449 6,5252,9511,5223,5784,16843,765Gross Margin38.6% 38.5% 38.2% 37.2% 36.7% 48.5% 33.8% 30.4% 33.4% 31.3% 31.8%33.3%35.2%TotalOperating Expenses2,6904,1416,6943,8582,7554,2664,508 4,0733,1033,4473,8543,11746,505EBIT( 1,371)(2,503)4,669(1,109)(1,265) (1,253)(1,059)2,453(152) (1,925)(276)1,050(2,741) EBITMargin(40.1%) (58.8%)15.7%(15.0%)( 31.2%)(20.2%)(10.4%) 11.4%(1.7%)(39.6%)( 2.5%)8.4%(2.2%)EBITDA ($1,052)($2,186)$4,982($800)($1,040) ($1,031)($840)$2,670$64($1,717) ($69)$1,255$237EBITDA Margin (30.8%) (51.3%)16.8% (10.8%)(25.6%)(16.6%) (8.2%)12.4% 0.7% (35.3%)(0.6%)10.0% 0.2% Source:CompanyManagement STRI CTLY CON FI DEN TI AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 18/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 18

Ob s er v at i o n s R egar d i n g At ar i S u m m ar y of Act u al an d P r oj ect ed C ash R ecei p t s and Di s b u rs em en t s An anal y s i s o f p r oj ect ed cas h r ecei p t s and d i s b u r sem en t s f or F Y2 0 0 9 t h r ou g h S ep t em b er 2 0 0 8 pr ep ar ed b y t heC o m p an y i nd i cat es t t h eC om p an y wil l n eed t o o b tai n ad d i ti o n al f u nd i n g as ear l y as M ay 2 0 0 8 . – C as h f u n d i ng r eq u i r emen t s ar eh i gh es t i n J u ne2 0 0 8 ( n eg at i v e$ 1 9 m il l i o n ). At ar i , I n c. C ash R ecei p t/ Di s b ur s em ent S ch ed u le( $ i n t h o u s and s ) Decem ber J an u ar y F eb r u ary M ar ch Ap r i l M ay J u n e J u l y Au g u st S ep t em b er 2 0 0 7 2 0 08 2 0 0 8 2 0 08 2 0 0 8 2 0 08 2 0 0 8 2 00 8 2 0 0 8 2 00 8 Act u al Act u al Act ual Act u al P r oj ect ed P r o j ected P r o j ected P r o j ected P r o j ected P r o j ected R ecei p ts P u b l i sh i n g 7 , 39 8 1 1 , 54 5 1 1 , 94 8 9 7 8 2 , 19 4 1 , 0 87 2 , 0 1 4 9 ,2 2 2 1 5 ,8 9 5 6 , 0 06 L i cen si n g / Ot h er 5 9 6 23 1 7 4 0 3 6 5 15 7 4 4 4 4 7 7 4 1 56 7 4 1 R el ated P ar t y ( R o yal t y / o t h er) 3 2 3 7 5 5 2 6 5 9 3 44 3 1 , 0 07 9 7 5 3 3 4 3 3 5 44 1 T o t al R ecei p t s 8 ,3 1 7 1 2 ,5 3 1 1 2 ,9 5 3 1 , 1 07 3 , 1 5 2 2 ,8 3 7 3 , 4 36 9 , 6 3 0 1 6, 3 8 7 7 , 18 8 Di s b ur s em ent s M an u f act u r i n g ( COGS ) 1 , 4 30 1 , 0 3 9 1 ,1 3 6 3 5 2 1 ,0 4 0 3 , 89 9 1 , 9 7 6 1, 4 7 9 2 , 97 5 2 , 8 2 3 Rel at ed P ar ty ( R o y al ty / Ot h er) 1 , 9 04,003944000 0000 Research&De velopment1,2281,022172362,5522,126 898505658A dvertising538653744859 3805231,2141,9122,4691,407Distr ibution/Freight27747033625303254 282264408286Royalties 3,14601,07138242 82981402,2130 Overhead5,6592,2153,241588 4,5582,5252,2462,2891,9781,955TotalD isbursements14,1789,4037,6441,8999,07410,1556,697 6,03510,0996,530CashFlow(5,861)3,128 5,309 (792) (5,922)(7,318)(3,261)3,5956,288 658CashBalance BeginningCashBalance (4,393)(10,254)(7,126)(2,761)(2,561) (8,483)(15,801)(19,062)(15,466) (9,178)Cashflowfrom Operations(5,861)3,1285,309 (792)(5,922)(7,318)( 3,261)3,5956,288658EndingCash( 10,254)(7,126)(1,817)(3,553) (8,483)(15,801)(19,062)(15,466)(9,178)( 8,520)CashFunding— bymonthCashFunding— in aggregate 14,00014,00014,00014,00014,00014,00014,00014,00014,00014,000Net Cash3,7466,87412,18310,4475,517(1,801) (5,062)(1,466)4,8225,480Source: CompanyManagementNote: Thisanalysiswasder ivedfroma weeklyanalysisperfor medbythe Companyanditsrestr ucturingadvisors.S TRIC T L Y C O N F I D E N T I A L

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 19/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 19

I I I . P u b l icM ar k et Val ueS T R I C T L YC ON F I DE NT I AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 20/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 20

PublicMarketValue AtariCommonStock DataAtari isaNASD AQlistedcompany with13,477,920sharesoutstanding.On April22nd,2008,Atar icommonstockclosed at$1.50whichis belowIESA’sPer ShareCashConsideration anddownapproximately61% fromits52-week highof$3.84.ATARICOMMON STOCKDATAAPRIL 23,2007THROUGH APRIL22,2008Offe rPrice( March6th,2008)$1.68Pr icePriorto Announcement$1.681-DayPre mium0.0%5-DayPr emium6.3% 30-DayPremium58.5% ClosingPrice on4/22/2008$1.5052-WeekHighEnded 4/22/2008$3.8452-WeekLowEnded4/22/2008 $0.86SharesOutstanding13,477,920Average DailyTradingVolume( 3mos.) 27,425InstitutionalOwnership27.09% InsiderOwnership51.58% AnalystCoverage WedbushMorganSource:Bloomberga ndCapitalIQ S TRI CTLY CON FI DEN TI AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 21/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 21

PublicMarketValue AtariCommonStock Data(Continued)At ari’ssharesar ethinlytraded,w ithaveragedaily tradingvolumeinthe lastthreemonthsof 27,424Inthelast twelvemonths,Atari’s shareshavetraded aboveandbelow PerShareCa shConsiderationandits volumeweightedprice was$1.45Sincethe releaseof Atari’smostre centForm10-Q onFebruary13, 2008throughApril22nd,2008,t heCompany’svolumeshare priceis$1.55.$5 1,000900$4800February 13,2008– Atarireleases its10-Qfor the March6,2008– IESA’s700(Thousands)period endingDecember offerfor Atariof$1.68 $331,2007(first nine pershare announced600monthsofFY 2008)500Price $2400Volume$1.68per share offerprice 300$1200100$- -4/23/20077/3/20079/13/200711/23/20072/6/20084/18/2008Source:BloombergS TRI CTLY CON FI DEN TI AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 22/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 22

I V. S el ected P u b l i cC om p an y Anal y s i s S T R I C T L YC ON F I DE NT I AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 23/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 23

SelectedPublicCompany AnalysisPubliclyTraded CompanyAnalysis–MethodologyDuff &Phelpsreviewed thecurrenttra dingmultiplesofsix publiclytradedcompanies thatDuff& Phelpsdeterminedto berelevantto itsanalysis.Duff &Phelpsanalyzed theLTMandprojected revenuesandEBITDA foreachof thepublicly-tradedcompanies. Duff&Phelps thenanalyzedthe peergroup’strading multiplesofenterprise value(“EV”) totheirrespective LTMandprojected revenuesandEBITDA. EViscalculated asthe sumofthe equitymarketvalue (dilutedsharesoutstandingmultiplied bythe currentstockpric e)andnet indebtedness.Duff& Phelpsusedthe followingmethodologyto selectcompanies:– PrimaryandSe condarySICCodes: 7372(prepackagedsoftware) ,5045(computersand computerPeripheral equipmentandsoftware) and7822(motionpicture andvideotape distribution).–Duff &Phelpsreviewe dvariousSECdocuments andequityresearch reportsfordetail sregardingthe nature ofeachsele ctedcompany’sbusinessand financialperformance. –Duff& Phelpsexcludedthose companieswitha marketcapitalization equaltoor inexcessof $1billion.Sixcompanieswere selectedfallingunder twocategories: –Small-CapVideo GameDevelopers,Publishers andDistributors(Majesco EntertainmentCo.andMidway GamesInc.)– PackagedMediaDistri butors(HandlemanCo.,I mageEntertainmentInc., NavarreCorp. andSourceInterlink Companies,Inc.)None ofthecompanies utilizedforcomparative purposesinthef ollowinganalysisis,of course,identicalto Atari.Accordingly,a completevaluationanalysis cannotbe limitedto aquantitative reviewofthe selectedcompaniesand involvescomplexconsiderationsand judgmentsconcerningdifferences in financialandoperating characteristicsof suchcompanies,as wellasother factorsthatcould affecttheir value relative to thatofAtari. S TRI CTLY CON FI DEN TI AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 24/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 24

S el ect ed Pu b l i cC o mp an y An aly s i s P u bl i cl y T r ad ed C o m pan y An al ys i s ( $ i n m i l li o n s ex cep t p er s h ar ed ata) 2 3 - Ap r - 08 % o f E n t er p r is eVal u eas aM u l ti p l eo f L TM S t o ck 5 2 W k M ar k et E nt er p r i seR ev en u eE BI T DAE B I TDAR ev en u eC om p an y P r i ceHi g h Val u e Val u e2 00 7 A2 0 0 8E 2 0 0 9 E 2 00 7 A2 0 0 8E 2 0 0 9 E Mar g i n Gr o wt h S m al l - Cap Vi d eo GameDev el o p er s , P u b l is h er s an d Dis t r i b ut o r s M aj esco E n t er tai n m ent C o . $ 1 . 11 4 3 . 2 % $ 31 . 9 $ 2 3 .7 0 . 4 3 x 0 .3 6 x 0 . 3 4x 4 . 6 x NM NM 9 . 3 % ( 7 . 4) % M i d way Games I n c. 2 . 3 9 31 . 7 % 2 2 0. 0 2 9 3 .9 1 . 8 7 x 1 .2 9 x 1 . 1 6x NM NM NM NM ( 5 . 1 ) % Hi gh 4 3 . 2 % 1 . 87 x 1 . 2 9x 1 . 1 6 x 4 .6 x NA NA9 . 3 % ( 5 . 1) % M ed i an 3 7. 4 % 1 . 1 5x 0 . 8 3 x 0 .7 5 x 4 . 6x NA NA9 . 3 % ( 6 . 2) % M ean 3 7 . 4% 1 . 1 5 x 0 .8 3 x 0 . 7 5x 4 . 6 x NA NA9 . 3 % ( 6 . 2) % L o w3 1 . 7% 0 . 4 3 x 0 . 36 x 0 . 3 4 x 4. 6 x NA NA9 . 3 % ( 7 . 4) % P ack ag ed M ed i a Di s tr i b u t or s Han d l eman C o . $ 0 .4 4 5 . 8 % $ 9 .0 $ 6 6 . 6 0 .0 6 x NM NM 9 . 7 x NM NM 0 . 6 % ( 1 0 .1 ) % I m ag e E n ter t ai n men t I n c. 1 . 31 2 9 . 1 % 2 8. 5 5 4 . 3 0 .5 4 x NM NM NM NM NM1 . 1 % 0 . 1% Nav ar r eC o r p. 1 . 6 2 3 6 .0 % 5 8 . 7 1 11 . 8 0 . 1 6x 0 . 1 7 x 0 .1 7 x 3 . 4x 3 . 8 x NM 4 . 6 % 7 . 9% S o u r ceI n t er l i n k C o mp an i es, I n c. 1 . 4 4 19 . 5 % 7 5 .3 1 , 4 4 4 .5 0 . 6 4 x NM NM 1 0 . 6 x NM NM 6 . 0 % 2 3 .3 % Hi g h 3 6 .0 % 0 . 6 4 x 0 .1 7 x 0 . 17 x 1 0 . 6x 3 . 8 x NA6 . 0 % 2 3 .3 % M ed i an 24 . 3 % 0 . 35 x 0 . 1 7x 0 . 1 7 x 9 .7 x 3 . 8 x NA2 . 8 % 4 . 0% M ean 2 2 . 6% 0 . 3 5 x 0 . 17 x 0 . 1 7 x 7. 9 x 3 . 8 x NA3 . 1 % 5 . 3% L o w5 . 8 % 0 . 06 x 0 . 1 7x 0 . 1 7 x 3 .4 x 3 . 8 x NA0 . 6 % ( 1 0 . 1 ) % At ar i , I n c. $1 . 5 0 3 9. 2 % $ 2 0 . 2 $ 2 8 . 8 0 . 3 1 x 0. 3 8 x 0 . 40 x NM NM NM NM ( 3 4 . 4 )% S o u r ce: S EC f i l i n g s and o t h er p u bl i cl y av ai l ab l e i n f o r m at i on . S T R I C T L YC ONF I DE NT I A L

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 25/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 25

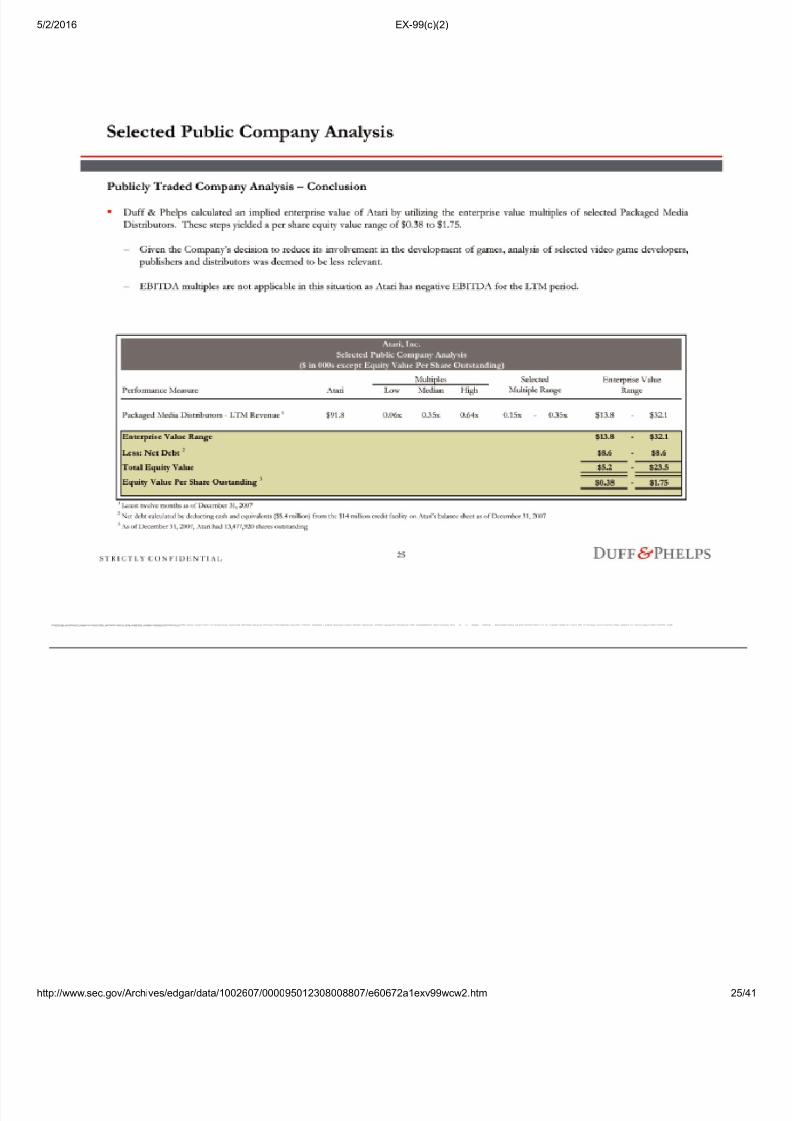

SelectedPublicCompany AnalysisPubliclyTraded CompanyAnalysis–ConclusionDuf f&Phelpsc alculatedanimplied enterprisevalue ofAtariby utilizingtheenterprise valuemultiplesof selectedPackaged MediaDistributors.These stepsyieldedape rshareequity valuerangeof $0.38to$1.75.–Given theCompany’sdecisionto reduceitsinvolvement inthedevelopmentof games,analysisof selectedvideogame developers,publishersanddistr ibutorswasdeemed to belessrelevant. –EBITDAmultiples are notapplicable in thissituationasAta rihasnegative EBITDAforthe LTM period.Atari,Inc. SelectedPublic CompanyAnalysis($in 000sexceptEquityValue PerShare Outstanding)MultiplesSelected Enterprise Value Performance Measure Atari Low MedianHigh Multiple Range Range PackagedMedia Distributors—LTM Revenue 1 $91.8 0.06x0.35x0.64x0.15x—0.35x $13.8 —$32.1Enterprise ValueRange $13.8—$32.1Less:N etDebt2 $8.6—$8.6TotalEquity Value $5.2-$23.5EquityValue PerShareO ustanding3$0.38—$1.75 1Latesttwelve monthsasof December31, 20072Netdebt calculatedbyd ed u cti n g cas h an d eq u i v alen t s ( $ 5 .4 m i l l i on ) f r o m t h e$ 1 4 m il l i o n cr ed i t f aci l i ty o n At ar i ’ s b al an ces h eet as o f Decem b er 3 1, 2 0 0 7 3 As o f Decemb er 3 1 , 2 0 07 , At ar i h ad 1 3, 4 7 7 ,9 2 0 s h ar es o u t s t and i n g S T R I C T L YC O NF I DE NT I AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 26/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 26

V. S el ected M & AT r an sact i o n Anal y s i s ( Val u at i on M u l t i pl es ) S T R I C T L Y C ONF I D E NT I AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 27/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 27

SelectedM&ATransaction Analysis(ValuationMultiples) SelectedM&ATransaction Analysis–MethodologyDuff &Phelpsselected M&Atransactionsinvolvingtarget companiesthatDuff &Phelpsdetermined toberelevant toitsanalysis.D uff&Phelps computedtheLTMrevenuesa ndEBITDAfor eachofthe targetcompanies.Duff &Phelpsthenca lculatedtheimplied enterprisevaluef oreachtransact iontothetarget ’srespectiveLTMrevenue andEBITDAand comparedthe multiplesofthe selectedtransactionsto the multiplesimpliedin the ProposedTransaction.Duff &Phelpsrestricte dthe searchto include onlytransactionswith enterprise valueslessthan $500million.Duff& Phelpsusedthe followingmethodologyin selectingrelevantcompara ble transactions:– PrimaryandSecondary SICCodes:7372(pr epackagedsoftware), 5045(computersandcomputer Peripheralequipmentand software)and7822 (motionpicture andvideotape distribution).–Duff & Phelpsreviewedthe transactionhistoriesof relevantcomparable companies. –Because ofa limitedsample size, Duff& Phelpsinclude transactionsinvolvingforeign targetsaswell asU.S.based targets.Duff&Phelps ultimatelyselected8 precedenttransactionsf allingundertwo categories:–Video GameDevelopers, PublishersandDistributors –PackagedMedia DistributorsNoneof thetransactionsutilized forcomparativepurposes inthefollowing analysisis,of course,identicalto theProposedTransaction. Accordingly,acomplete valuationanalysiscannotbe limitedtoa quantitativereviewof theselectedtr ansactionsandinvolvescomplex considerationsandjudgments.S T RIC TLY CON FI DEN TI AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 28/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 28

SelectedM&ATransaction Analysis(ValuationMultiples) SelectedM&ATransactions Analysis–Selecte dPrecedentTransactions SELECTEDCOMPARABLETRANSACTIONS —VIDEOGA MEDEVELOPERS,PUBLISHERSAN DDISTRIBUTORSEnter priseValueas LTMDateAcquiror Name EnterpriseaMultiple ofLTM:EBITDAAnnounced TargetName TargetBusinessDescription Value RevenueEBITDAMargin 6/14/2007 EntertainmentOne Ltd.(AIM:ETO)Engagesin the acquisitionandexploitationof DVDdistributionrights fromthirdparty $98.8 2.00x8.0x25.1% ContenderEntertainmentGroupproducers in the UnitedKingdom.7/25/2006MattelI nc.(NYSE:MAT) Engagesin the development,manufacture,and distributionofelectronic entertainment$185.8 1.25x15.6x8.0% Radica GamesLtd.products includingelectronic games,videogamec ontrollersandaccessorie s.3/17/2006Electronic ArtsInc.(N asdaqNM:ERTS)Developsgamesf orpersonalcomputers andgame consolesforthe televisionandcomputer$45.0 1.52x5.3x28.7% DigitalIllusionsCE AB game smarketsworldwide. 9/3/2003Take-TwoInteractiveSoftware ,Inc.Engagesin developing,publishing,distributing,andmarketing interactiveentertainment $42.61.02x7.7x13.3%TDK Mediactive,Inc.softwar ebasedoninte llectualcontent.4/24/2002Atar i,Inc.(NasdaqNM:ATAR) Developsinteractivevideo gamesandcreates titlesforper sonalcomputersandvideo game$47.08.11x28.5x28.4%S hinyEntertainment,Inc.consoles. Median1.52x8.0x25.1%Mean 2.78x13.0x20.7%SELECTEDCOMPARABLETRANSACTION S —PACKAGEDMEDIA DISTRIBUTORS Enterprise Value as LTM DateAcquirorName Enterprise a Multiple ofLTM:EBITDAAnnouncedTarget Name TargetBusinessDescription Value Revenue EBITDAMargin5/9/2007Pea ce ArchEntertainment( AMEX:PAE) Operatesas adigitalversatile disc distributorin the UnitedStates.Its libraryincludesgenre $10.0 0.53x NA NATrinityHome Entertainment,LLCclassics, andbudgetandfir st-runfeature films. 2/14/2007MarwynInvestmentManagement LLP Owns anddistributesfilm andentertainmentcontent internationallyandengages in$150.50.33x6.9x4.8%EntertainmentOneLtd. wholesalingandspecialty retailinghomeentertainment products.10/20/2005HandlemanCo.(N YSE:HDL)Engagesin publishinganddistributinginteractive entertainmentsoftware forvideogame $112.00.43x4.8x9.1%Crave EntertainmentGroup,Inc. platformswithtitle sincludingaction/adventure,fi rst-personshooterand sportsgames.Median0.43x 5.9x6.9%Mean0.43x5.9x 6.9%Source:SECf ilings,CapitalIQ FactsetMergerstat, Bloomberg andotherpubliclyavaila ble information.S TRIC TLYC ONF I DEN TI AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 29/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 29

SelectedM&ATransaction Analysis(ValuationMultiples) SelectedM&ATransaction Analysis–ConclusionDuff &Phelpscalculated animpliedenterprise valueofAtari byutilizingtheenter prisevaluemultiples ofselectedtr ansactionsinwhichthe targetwas apackagedmedia distributor.Thesestepsyielded apershare equityvaluerange of$0.72to$1.41.– GiventheCompany’sdecision toreduceits involvementinthedevelopment ofgames,analysis of selected transactionsinvolvingvideogame developers,publishersanddistributors wasdeemedto be lessrelevant.– EBITDAmultiplesare notapplicable in thissituationas Atarihasnegative EBITDAforthe LTM period.Atari,Inc. SelectedM&ATransaction Analysis($in 000sexceptEquityValue PerShare Outstanding)Atari,I nc.Multiples SelectedEnterprise Value Performance Measure Low MedianHigh Multiple Range Range PackagedMedia Distributors—LTMRe venue 1$91.80.33x0.43x0.53x0.20x— 0.30x$18.4—$27.5Enterprise ValueRange $18.4—$27.5Less: NetDebt2 $8.6—$8.6Total EquityValue $9.8—$18.9EquityValue PerShare Oustanding3$0.72— $ 1 . 4 1 1 L at es t t wel vem o n t h s as o f Decem b er 3 1 , 2 00 7 2 Net d eb t cal cu l at ed b y ded u ct in g cas h an d eq ui v al en ts ( $ 5 . 4 m i ll i o n ) f r om t h e$ 1 4 m i l li o n cr ed i t f aci l i t y o n Atar i ’ s b al ances h eet as o f Decemb er 3 1 , 2 0 07 3 As o f Decem b er 3 1 , 20 0 7 , At ari h ad 1 3 , 4 77 , 9 2 0 sh ar es o u t st an d i ng S T R I C T L YC ONF I DE NT I AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 30/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 30

VI . S el ect ed M & AT r an sact i o n An al y s i s ( P r em i u m s P aid ) S T R I C T L Y C ONF I DE NT I A L

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 31/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 31

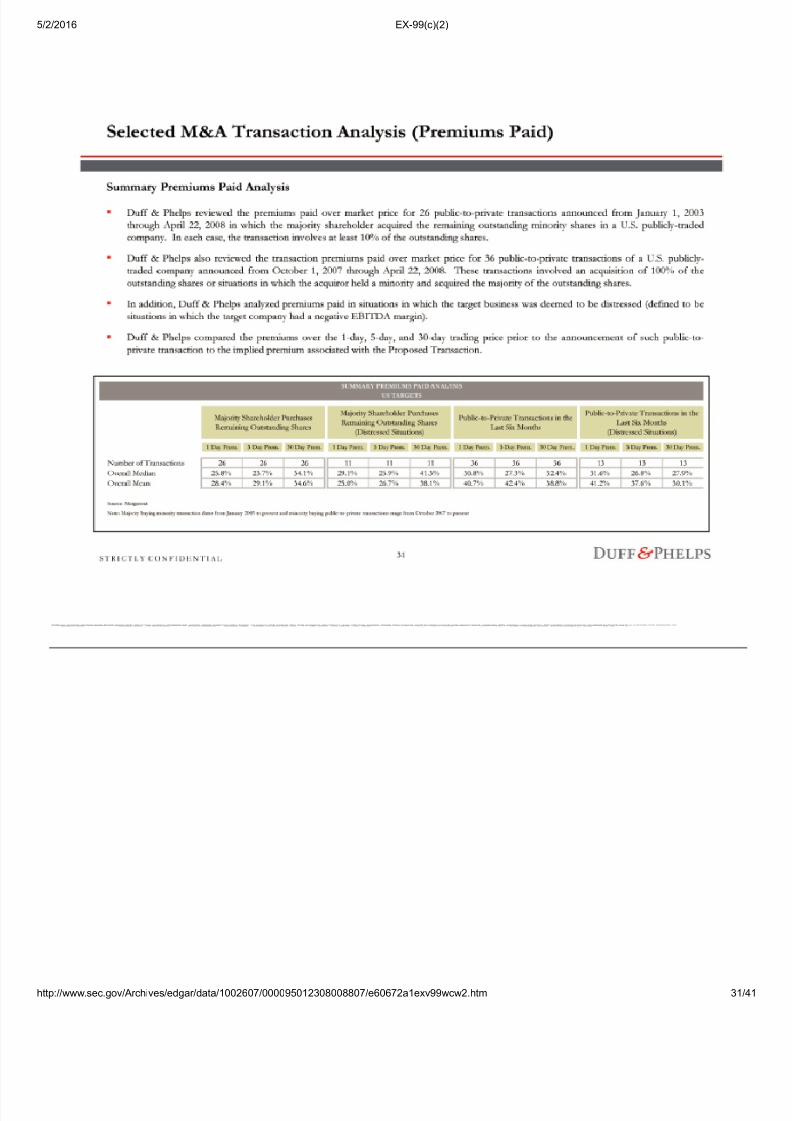

SelectedM&ATransaction Analysis(PremiumsPaid) SummaryPremiumsPaid AnalysisDuff& Phelpsreviewedthe premiumspaidover marketpricefor 26public-to-privatetransactions announcedfromJanuary1, 2003throughApril22,2008 inwhichthe majorityshareholderac quiredtheremaining outstandingminoritysharesin aU.S.publicly-tra dedcompany.Ineach case,thetr ansactioninvolvesatle ast10%ofthe outstandingshares.Duff &Phelpsalso reviewedthetr ansactionpremiumspaidover marketprice for36public-to-private transactionsofa U.S.publicly-tradedcompany announcedfromOctober 1,2007throughApril 22,2008.These transactionsinvolvedanac quisitionof100% ofthe outstandingsharesor situationsin whichthe acquirorhelda minorityandacquiredt he majorityofthe outstandingshares.Inaddition, Duff&Phelps analyzedpremiumspaid in situationsin whichthe targetbusinesswas deemedtobe distressed(definedto be situationsinwhich the targetcompanyhada negative EBITDAmargin).Duff & Phelpscomparedthe premiumsoverthe 1-day, 5-day, and30-daytradingpr ice priortothe announcementofsuchpublic- to-privatetransactiontothe impliedpremiumassociated withtheProposed Transaction.SUMMARYPREMIUMS PAIDANALYSIS USTARGETSMajorityShar eholderPurchases Public-to-PrivateTransactions intheMajority ShareholderPurchasesPublic- to-PrivateTransactionsin theRemainingOutstanding Shares LastSixMonthsRemaining OutstandingShares LastSixMonths(Distre ssedSituations)(Distressed Situations)1Day Prem.5Day Prem.30 Day Prem.1 DayPrem.5 DayPrem.30DayPre m.1 DayPrem.5 DayPrem.30DayPre m.1 DayPrem.5 DayPrem.30DayPre m.Numberof Transactions262626 111111363636 131313Overall Median25.8% 23.7% 34.1% 29.1% 25.9% 41.3% 30.8% 27.3% 32.4% 31.6% 26.8% 27.9% OverallMean28.4% 29.1% 34.6% 25.0% 26.7% 38.1% 40.7% 42.4% 38.8% 41.2% 37.6% 30.1% Source:Mergerstat Note:Majoritybuyingminority transactiondatesfrom January2003topresentand minoritybuyingpublic-to-private transactionsrange fromOctober2007 topresentS TRICTL YCO NF IDE NTI AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 32/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 32

SelectedM&ATransaction Analysis(PremiumsPaid) PremiumsPaid– SummaryofMajority ShareholderPurchases RemainingOutstandingShares PREMIUMSPAIDANALYSIS PUBLIC-TO-PRIVATETRANSACTIONS WITHUSTARGETS (MAJORITYSHAREHOLDERP URCHASESREMAINING OUTSTANDINGSHARES) ByEnterpriseValue sinceJanuary2003( $inmillions)Number of MedianEnterprise MedianPremiumOne Day BeforeMedianPr emiumFive DaysBefore MedianPremium30 DaysBefore Enterprise Value MedianLTM Revenue MedianLTM EBITDATransactions Value AnnouncementDate (%)AnnouncementDate (%)AnnouncementDate (%)$1Bil5 $3,167.4 $1,856.4 $433.5 25.6% 22.9% 15.4% $100Mil— $1Bil7$189.6 $146.2 ($9.2)29.1% 25.9% 41.3% $50Mil- $100Mil5 $56.4 $68.6 $2.2 22.5% 21.9% 30.3% $10Mil— $50Mil9 $19.7 $40.7 $2.0 35.3% 33.3% 52.8% OVERALLMEDIAN26 $73.4$116.9$2.325.8% 23.7% 34.1% OVERALLMEAN28.4% 29.1% 34.6% Atari, Inc.0.0% 6.3% 58.5% Source:Mergerstat S TRICTL YCO NF IDEN TIA L

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 33/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 33

SelectedM&ATransaction Analysis(PremiumsPaid) PremiumsPaid– MajorityShareholderPurc hasesRemainingOutstandingShar es(January1, 2003–Current)A nnounced %ofShares 1Day5D ay30DayEnter priseDateTarget BuyerAcquiredPremium PremiumPremiumValue 2-Aug-04CoxCommunications,Inc. CoxEnterprises,Inc. 38.4%26.0%24.6%15.4%$27,378.010-Mar- 08NationwideFinancial Services,Inc. NationwideMutualInsurance Co.33.5% 24.4% 16.2% 19.2% 8,311.5 24-Aug-07Hearst-Argyle Television,Inc.The HearstCorp.25.7% 14.9% 14.9% (0.7%)3,167.4 5-Nov-07Alfa Corp.Alfa MutualInsurance Co.46.1% 25.6% 22.9% 19.5% 1,844.3 17-Mar-06WilliamLyonH omes WilliamLyonHomes,Inc. 25.5% 44.0% 50.5% 7.7% 1,563.2 16-Jun-06Case Pomeroy&Co.CP Newco,Inc. 14.0% 5.2% 6.0% 6.8% 291.2 2-Dec-05FoodaramaSupermarkets,Inc. The SakerFamily Corp.49.0% 40.5% 35.1% 38.7% 251.518-Jan-08DominionHomes, Inc.DominionHomes, Inc.35.8% 41.3% 35.4% 41.3% 210.08-Jul-05CruzanInternational, Inc.V&S Vin& SpritAB36.4% 12.4% 9.1% 103.5% 189.66-Nov-06Moscow Cable Corp.RenovaGroupof Cos.19.0%29.1%25.9%42.5% 159.730-Jun-06TIMCOAviationSe rvices,Inc.LJH Ltd.10.9%56.9%97.0%61.3% 125.513-Jun-03AtalantaSosnoff CapitalLLC AtalantaSosnoff CapitalCorp.17.3%0.4% 6.7%12.5%116.55-May-03Se meleGroup,Inc. SemeleGroup,Inc. 46.9%25.0%25.0%21.2%78.5 29-Jul-03JanusHotels& Resorts,Inc.Janus Acquisition,Inc.29.6%(5.8%) (4.4%)(13.3%)68.3 7-Jul-05ObsidianEnterprises,I nc.ObsidianEnterprises Inc 22.7% 37.0% 27.6% 44.5% 56.4 5-Apr-04MinutemanInternational, Inc.Hako-Werke GmbH32.0% 22.5% 21.9% 30.3% 55.2 1-Aug-03OAOTechnologySolutions,Inc.TerrapinPa rtnersLLC49.0% 15.0% 10.9% 50.0% 55.2 31-Dec-03BoydBros.Transportation,I nc.BBTAcquistionCorp. 28.0% 53.0% 63.9% 97.4% 47.4 20-Nov-06HanoverDirect,Inc.ChelseyDi rectLLC31.5% (79.2%)(80.0%)(79.3%)37.9 13-Sep-04RagShops,Inc.Sun CapitalPartners, Inc.44.3% 23.2% 17.2% 37.8% 22.227-Jan-04Dover InvestmentsCorp. Lawrence WeissbergRevocable LivingTrust48.7% 35.3% 11.8% 14.7% 22.02-Dec-03Reeds Jewelers, Inc.Sparkle LLC12.5% 88.1% 94.3%95.2%19.720-Dec-04Elmer’ sRestaurants,Inc. ERIAcquisitionCorp. 41.1%(0.7%)(0.5%)0.0% 16.819-Feb-03RiversideG roup,Inc.Riverside Group,Inc.43.0%33.3% 33.3%60.0%14.02-Dec-03 KontronMobileComputing,Inc. KontronEmbeddedComputersAG 48.5%52.8%71.9%52.8%13.521-N ov-03ChefsInternational, Inc.LombardiRestaurant GroupInc38.7% 118.9%118.9%121.3%12.3High118.9% 118.9%121.3%Median25.8%23.7% 34.1%Mean 28.4% 29.1% 34.6% Low(79.2%)(80.0%) (79.3%)Source:Mergersta tSTR ICTL YCO NFI DEN TI AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 34/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 34

SelectedM&ATransaction Analysis(PremiumsPaid) PremiumsPaid– SummaryofMajority ShareholderPurchases RemainingOutstandingShares (Distressed)PREMIUMSPAI DANALYSISD ISTRESSEDPUBLIC-TO-PRIVATETRANSACTIONS (MAJORITYSHAREHOLDER PURCHASESREMAINING OUTSTANDINGSHARES) ByEnterpriseValue sinceJanuary2003($ inmillions)Number of MedianEnterprise MedianPremiumOne DayBefore MedianPremiumFive DaysBefore MedianPremium30 DaysBefore Enterprise Value MedianLTM Revenue MedianLTM EBITDATransactions Value AnnouncementDate (%)AnnouncementDate (%)AnnouncementDate (%)$1Bil 0NA NANA NA NA NA$100Mil —$1Bil6 $174.7 $146.2 ($9.2)34.8% 30.5% 41.9% $50Mil—$100 Mil2 $67.5 $43.9 ($2.7)31.0% 26.3% 32.9% $10Mil—$50 Mil3 $22.2 $116.9$1.723.2% 17.2% 37.8% OVERALLMEDIAN11$116.5$116.9 ($0.5)29.1% 25.9% 41.3% OVERALLMEAN25.0% 26.7% 38.1% Atari, Inc.0.0% 6.3% 58.5% Source:MergerstatN ote:Adistressed targetwas deemedtobe a businesswithEBITDA marginsator belowzero.S TRIC TLYC ONF IDE NTI AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 35/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 35

SelectedM&ATransaction Analysis(PremiumsPaid) PremiumsPaid– MajorityShareholderPurc hasesRemainingOutstandingShar es(Distressed) (January1,2003– Current)Announced %ofShares 1Day5D ay30DayEnter priseDateTarget BuyerAcquiredPremium PremiumPremiumValue 2-Dec-05FoodaramaSuper markets,Inc.The SakerFamilyCorp. 49.0%40.5%35.1%38.7%$251.518-Ja n-08DominionHomes,Inc. DominionHomes,Inc. 35.8%41.3% 35.4%41.3% 210.0 8-Jul-05CruzanInter national,Inc.V&S Vin &SpritAB 36.4% 12.4% 9.1% 103.5% 189.6 6-Nov-06MoscowCable Corp.Renova GroupofCos.19.0% 29.1% 25.9% 42.5% 159.7 30-Jun-06TIMCOAviationSer vices,Inc.LJH Ltd.10.9% 56.9% 97.0% 61.3% 125.5 13-Jun-03Atalanta SosnoffCapitalLLC Atalanta SosnoffCapitalCorp.17.3% 0.4% 6.7% 12.5% 116.5 5-May-03Semele Group,Inc.Semele Group,Inc.46.9% 25.0% 25.0% 21.2% 78.57-Jul-05ObsidianEnterprise s, Inc.ObsidianEnterprises Inc 22.7% 37.0% 27.6% 44.5% 56.420-Nov-06HanoverD irect, Inc.ChelseyDirectLLC31.5% (79.2%)(80.0%)(79.3%)37.913-Sep-04 RagShops, Inc.SunCapitalPartners,Inc.44.3%23.2% 17.2%37.8%22.22-Dec-03 ReedsJewelers, Inc.SparkleLLC 12.5%88.1%94.3%95.2%19.7H igh88.1%97.0%103.5%Median 29.1%25.9%41.3%Mean 25.0%26.7%38.1%Low(79.2%) (80.0%)(79.3%)Source: MergerstatNote:A distressedtargetw asdeemedto beabusinesswith EBITDAmarginsat orbelowzer o.STR ICT LYC ONF IDE NTI AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 36/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 36

SelectedM&ATransaction Analysis(PremiumsPaid) Conclusion–MajorityShare holderPurchasesRemaining OutstandingSharesIn reviewingthe26 transactionsinwhich themajorityshareholder purchasedtheremaining outstandingsharesofa publicly-tradedsubsidiary,Duff &Phelpsobservedthe meanandmedian ofthepremiums paidoverthe1- day,5-dayand30-day tradingpriceprior toannouncement.1-Day Premium5-DayPremium 30-DayPremiumMedian 25.8%23.7% 34.1% Mean28.4% 29.1% 34.6% StandardDeviation0.3400.378 0.408Inreviewingthe 11distressedtransactionsin whichthe majorityshareholderpurchase dthe remainingoutstandingshares ofapublicly-traded subsidiary,Duff& Phelpsobservedthe meanandmedianofthe premiumspaidoverthe 1-day,5-dayand30-day tradingprice priorto announcement.1-DayPremium 5-DayPremium30-Da yPremiumMedian29.1% 25.9% 41.3% Mean25.0% 26.7% 38.1% StandardDeviation0.396 0.4460.456The PerShare CashConsiderationinthe ProposedTransactionreprese ntsa 1-day, 5-dayand30-daypremium of0.0%,6.3% and58.5%,respectively. The relevance ofthe premiumspaidan al y si s i s l i m i t ed b y t h eC o m pan y ’ s d epen d en ceo n I E S A, t h em ajo r i t y s h ar eh o l der i n t h eC o m p an y , f o r n ewr el eas ep r o d uct . S T R I C T L YC ONF I D E NT I AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 37/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 37

VI I . Net As s et Val u eAn al ys i s S T R I C T L Y C ONF I DE NT I A L

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 38/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 38

NetAssetValue AnalysisCalculationof NetAsset ValueDuff& PhelpsreviewedAta ri’sDecember 31,2007balancesheet aswellas theCompany’sestimatedinter nalMarch31,2008 tocalculatethe netassetvalue (“NAV”)oft heCompany.Asof December31,2007,At ari’stotalassets andtotalliabilities were$43.5million and$60.3million,respectively, foraNAV ofnegative$16.8million Estimatedasof March31,2008,Atari’ stotalassets andtotalliabilities were $32.6millionand $52.9 million,respectively,for aNAVof negative $20.3 millionAtari,I nc.Balance Sheet Summary($in millions) December31,Mar ch31,20072008(Estimated) Cash$ 5.4 $ 10.0 Receivables, net16.2 (0.3)Inventories7.4 6.5 Pr epaidExpensesandOther CurrentAssets6.0 7.7 Total CurrentAssets34.9 24.0 N etProperty,Plant &Equipment6.3 6.4 Goodwilland Intangibles—-O therLong-TermAssets2.2 2.1TotalAssets$ 43.5$ 32.6 AccountsPayable $ 10.6$9.7Accrued Liabilities11.5 6.8Royalties Payable3.82.7 Credit Facility14.014.0Due toRelatedPartie s5.32.7 Other Curr entLiabilities— 0.9TotalCurrentLiabilities 45.236.8Due to Related Parties,Long-Term 3.03.6Long-TermDeferredRe nt6.77.1Related PartyLicenseAdvance 5.15.4Other Long-TermLiabilities0.3-Total Liabilities60.352.9Stockholders’ Equity(16.8)(20.3)Total Liabilities&Stockholders’ Equity$43.5$32.6 Source:CompanySECFilings, ManagementEstimatesSource: SECfilingsS TRIC TLYC ONF IDE NTI AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 39/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 39

VI I I . L i q ui d at i on An al y s is S T R I C T L YC ONF I DE NT I A L

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 40/41

5/2/2016 EX-99(c)(2)

http://www.sec.gov/Archives/edgar/data/1002607/000095012308008807/e60672a1exv99wcw2.htm 40

LiquidationAnalysisSummaryof LiquidationAnalysisDuff& Phelpsprepareda liquidationanalysisassumingan orderlyliquidationin whichtheCompanywould realize70% ofbookvaluefor accountsreceivable, 50%bookvaluefor inventoryand70%bookvalue forproperty,plant andequipment.Tothisa mount,weaddedthe bookvalueofcash andmarketablesecuriti es.Additionally,Atari ownscertainintellec tualpropertythat isnotreflecte donthebalance sheet.Ina liquidationscenario,we assumedthatthe Companywouldrealize 100% ofthe estimatedfair marketvalue ofthe IP.A25% discountforbankruptcyc ostswasapplied andthe resultingvalue wasdiscountedback one andone-halfyears to presentvalue ata20% discountrate to adjustforthe time periodrequiredto complete the liquidation.S TRI CTLY CON FI DEN TI AL

8/17/2019 2008-04-25 Atari Fairness Opinion Special Committee to the Board of Directors

http://slidepdf.com/reader/full/2008-04-25-atari-fairness-opinion-special-committee-to-the-board-of-directors 41/41

5/2/2016 EX-99(c)(2)

LiquidationAnalysisLiquidationAnalysis Inaliquidationsce nario,thevalue ofthecommonstock wouldbezero. Atari,Inc.Liquidation Analysis($inmilli on)EstimatedEstimated LiquidationBookValue RecoveryValueCash $5.4100%$5.4AccountsRec eivable16.870%11.8I nventory7.450%3.7N etPP&E6.370% 4.4IntellectualPr operty(1)13.3100% 13.3Total38.5Less:Bankruptcy Costs@25%(2) 9.6NetTotal28.9 Less:DiscountFactor (3) 0.7607 TotalLiquidationValue 22.0 AtariLiabilities60.3 LiquidationValue Available to CommonShareholders($38.3)N otes:(1)Estimated value ofAtari’sinte llectualproperty,based onOceanTomo analysisasofJanuary1,2007. Appliedthe midpointofthe range ofvalue ($17.0 millionto $29.9 million)indicated.The rightsto TestDrive were licensedto IESAfor$5.0 millionin November2007,therefore, the estimatedvalue ofTestDrive ($10millionto $15million)wassubtracted.The license agreementisfor a sevenyearterm, therefore, itwasassumed thatnoresidual value relatedtothe TestDrive IP exists.(2)Estimated liquidation/bankruptcycosts. (3)Discountfa ctorof20% overa 1.5year period.STR ICT LYCO NFI DEN TIA L