Embed Size (px)

Citation preview

2010 Blackstone Investor Day

September 23, 2010

Hilton New YorkNew York, NY

0

Forward‐Looking Statements and Important Disclosures

This presentation may contain forward‐looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934 which reflect Blackstone’s current views with respect to, among other things, Blackstone’s operations and financial performance. You can identify these forward‐looking statements by the use of words such as “outlook,” “believes,” “expects,” “potential,” “continues,” “may,”“will,” “should,” “seeks,” “approximately,” “predicts,” “intends,” “plans,” “estimates,” “anticipates” or the negative version of these words or other comparable words. Such forward‐looking statements are subject to various risks and uncertainties. Accordingly, there are or will be important factors that could cause actual outcomes or results to differ materially from those indicated in these statements. Blackstone believes these factors include but are not limited to those described under the section entitled “Risk Factors” in its Annual Report on Form 10‐K for the fiscal year ended December 31, 2009, as such factors may be updated from time to time in its periodic filings with the SEC, which are accessible on the SEC’s website at www.sec.gov. These factors should not be construed as exhaustive and should be read in conjunction with the other cautionary statements that are included in the SEC filings.

Blackstone undertakes no obligation to publicly update or review any forward‐looking statement, whether as a result of new information, future developments or otherwise.

This presentation includes Non‐GAAP Financial Measures. You should also read the appendix to this presentation –Reconciliation of Non‐GAAP Financial Measures.

This release is for informational purposes only and does not constitute an offer of any Blackstone fund or an offer to enter into any investment program with Blackstone. Such an offer may only be made by means of an offering memorandum, which would have a complete description of the relevant fund or program, including the risks applicable thereto.

2010 Blackstone Investor Day

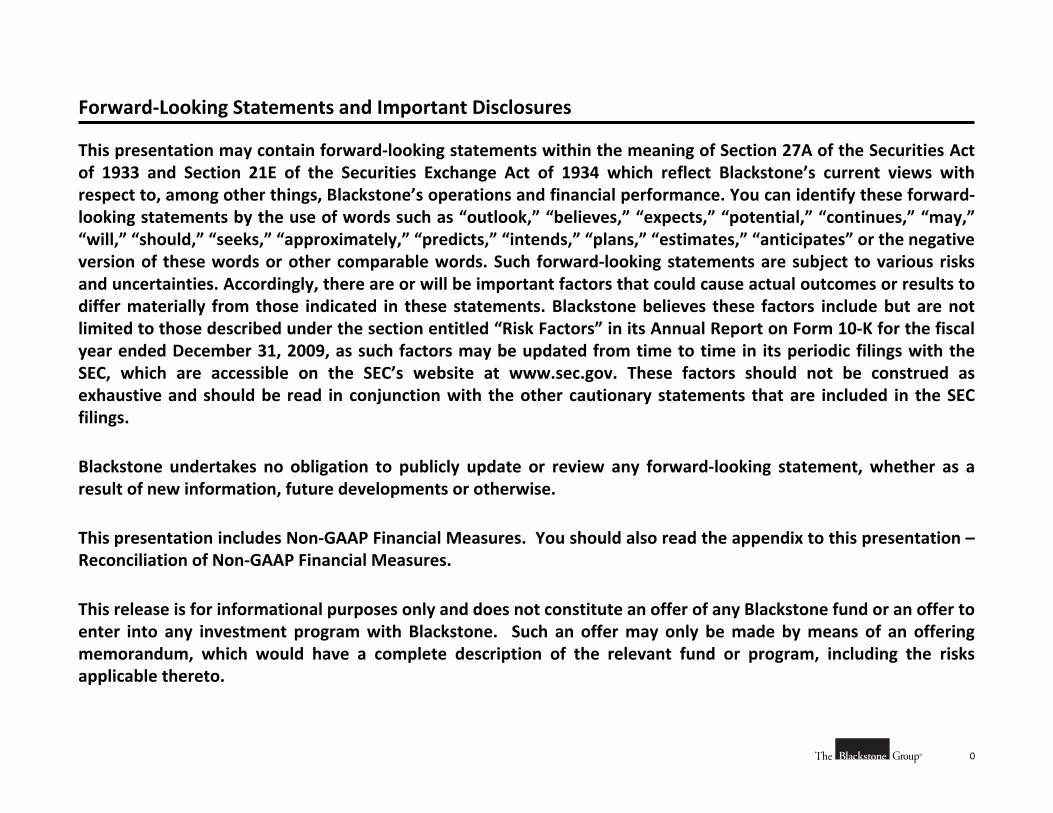

Agenda – Thursday, September 23, 2010Time Function Location 8:00 – 8:05 am Introduction and Overview of The Blackstone Group

Joan Solotar – Senior Managing Director, External Relations and Strategy, The Blackstone Group

Trianon Ballroom, 3rd Floor

8:05 – 8:20 am Welcome Remarks Stephen A. Schwarzman – Chairman, CEO & Co‐Founder, The Blackstone Group

Trianon Ballroom, 3rd Floor

8:20 – 9:00 am Financial Overview Laurence Tosi (“LT”) – Chief Financial Officer, The Blackstone Group

Trianon Ballroom, 3rd Floor

9:00 – 9:40 am Portfolio Operations Group James Quella – Senior Managing Director, The Blackstone Group

Trianon Ballroom, 3rd Floor

9:40 – 10:25 am Private Equity Garrett Moran – Senior Managing Director, The Blackstone Group Vikrant Sawhney – Senior Managing Director, The Blackstone Group

Trianon Ballroom, 3rd Floor

10:25 – 10:45 am BREAK – Cyber Café Petit Trianon, 3rd Floor 10:45 – 11:25 am Blackstone Advisory Partners

John Studzinski – Senior Managing Director, The Blackstone Group Trianon Ballroom, 3rd Floor

11:30 – 12:10 pm Restructuring & Reorganization Advisory Timothy Coleman – Senior Managing Director, The Blackstone Group

Trianon Ballroom, 3rd Floor

12:10 – 12:30 pm BREAK – Cyber Café Petit Trianon, 3rd Floor 12:30 – 1:30 pm GSO Credit Platform – Working Lunch

Bennett Goodman – Senior Managing Director, The Blackstone Group & Founder, GSO Capital Partners

Mercury Ballroom, 3rd Floor

1:30 – 1:45 pm BREAK – Cyber Café Petit Trianon, 3rd Floor 1:45 – 2:35 pm Real Estate

Jonathan Gray – Senior Managing Director, The Blackstone Group Trianon Ballroom, 3rd Floor

2:35 – 3:25 pm Blackstone Alternative Asset Management (“BAAM”) J. Tomilson Hill – Vice Chairman, The Blackstone Group

Trianon Ballroom, 3rd Floor

3:25 – 4:30 pm Wrap‐up and Q&A Stephen A. Schwarzman – Chairman, CEO & Co‐Founder, The Blackstone Group Hamilton E. James – President & COO, The Blackstone Group

Trianon Ballroom, 3rd Floor

4:30 – 5:30 pm COCKTAIL RECEPTION Petit Trianon, 3rd Floor

2010 Blackstone Investor Day

I. Introduction and Overview of The Blackstone Group

II. Financial Overview

III. Portfolio Operations Group

IV. Private Equity

V. Blackstone Advisory Partners

VI. Restructuring & Reorganization Advisory

VII. GSO Credit Platform

VIII. Real Estate

IX. Blackstone Alternative Asset Management (“BAAM”)

Appendix

A. Reconciliation of Non‐GAAP Financial Measures

B. Speaker Biographies

Table of Contents

I. Introduction and Overview of The Blackstone Group

2010 Blackstone Investor Day

1

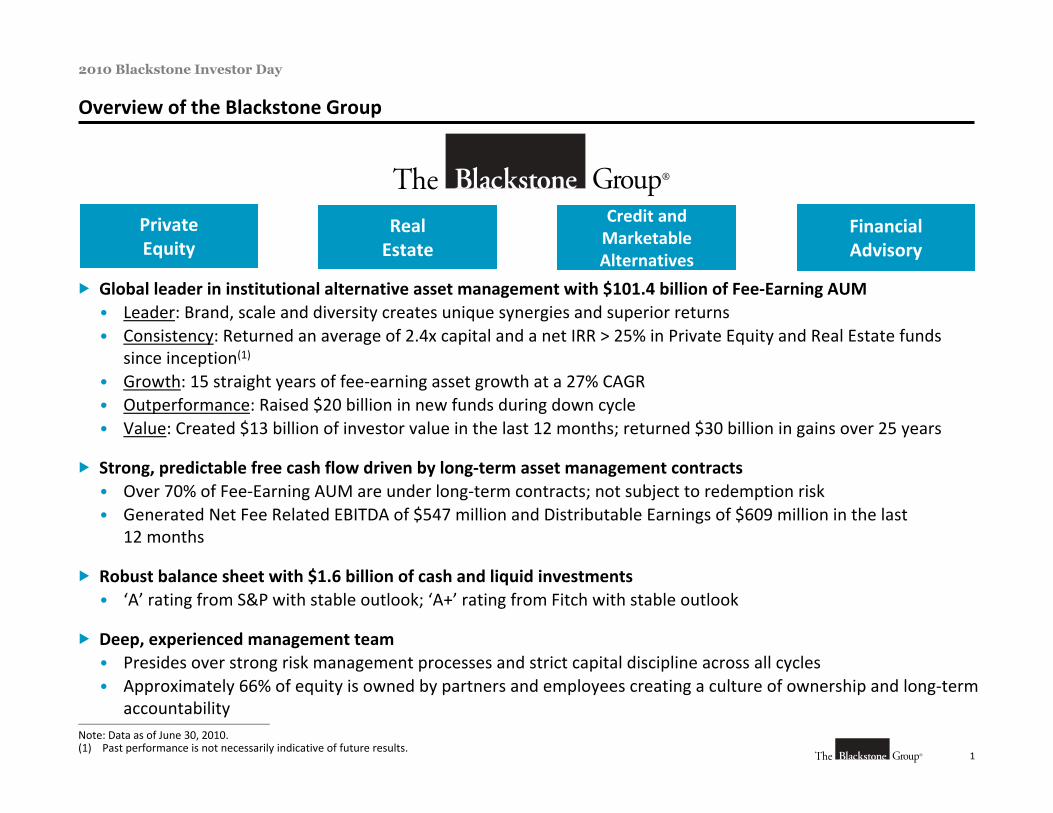

Overview of the Blackstone Group

Global leader in institutional alternative asset management with $101.4 billion of Fee‐Earning AUM • Leader: Brand, scale and diversity creates unique synergies and superior returns • Consistency: Returned an average of 2.4x capital and a net IRR > 25% in Private Equity and Real Estate funds

since inception(1)

• Growth: 15 straight years of fee‐earning asset growth at a 27% CAGR• Outperformance: Raised $20 billion in new funds during down cycle• Value: Created $13 billion of investor value in the last 12 months; returned $30 billion in gains over 25 years

Strong, predictable free cash flow driven by long‐term asset management contracts• Over 70% of Fee‐Earning AUM are under long‐term contracts; not subject to redemption risk• Generated Net Fee Related EBITDA of $547 million and Distributable Earnings of $609 million in the last

12 months

Robust balance sheet with $1.6 billion of cash and liquid investments• ‘A’ rating from S&P with stable outlook; ‘A+’ rating from Fitch with stable outlook

Deep, experienced management team • Presides over strong risk management processes and strict capital discipline across all cycles• Approximately 66% of equity is owned by partners and employees creating a culture of ownership and long‐term

accountability

Private Equity

Credit and Marketable Alternatives

RealEstate

FinancialAdvisory

________________________________________________

Note: Data as of June 30, 2010.(1) Past performance is not necessarily indicative of future results.

II. Financial Overview

1

2010 Blackstone Investor Day

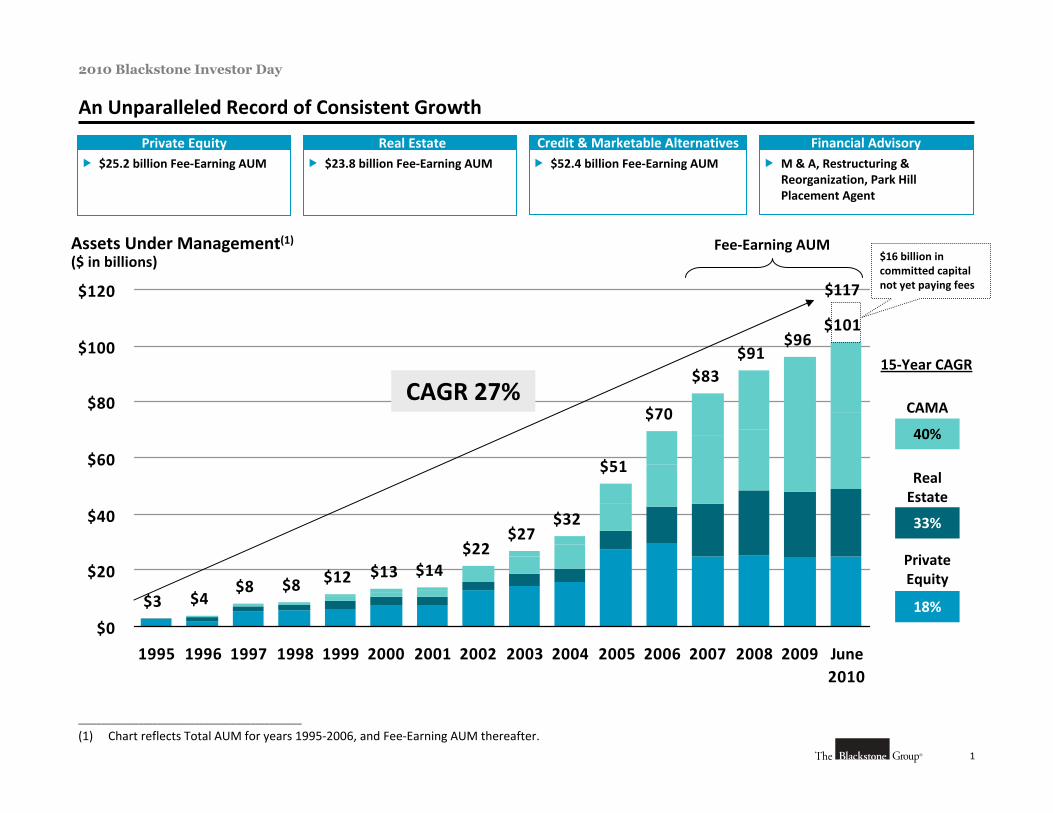

$3 $4$8 $8 $12 $13 $14

$22$27

$32

$51

$70

$83$91

$96$101

$0

$20

$40

$60

$80

$100

$120

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 June2010

An Unparalleled Record of Consistent Growth

Assets Under Management(1)($ in billions)

Fee‐Earning AUM

CAGR 27%

$52.4 billion Fee‐Earning AUM

Credit & Marketable Alternatives M & A, Restructuring &

Reorganization, Park Hill Placement Agent

Financial Advisory $23.8 billion Fee‐Earning AUM

Real Estate $25.2 billion Fee‐Earning AUM

Private Equity

CAMA

Private Equity

Real Estate

40%

33%

18%

15‐Year CAGR

$117

$16 billion in committed capital not yet paying fees

________________________________________________

(1) Chart reflects Total AUM for years 1995‐2006, and Fee‐Earning AUM thereafter.

2

2010 Blackstone Investor Day

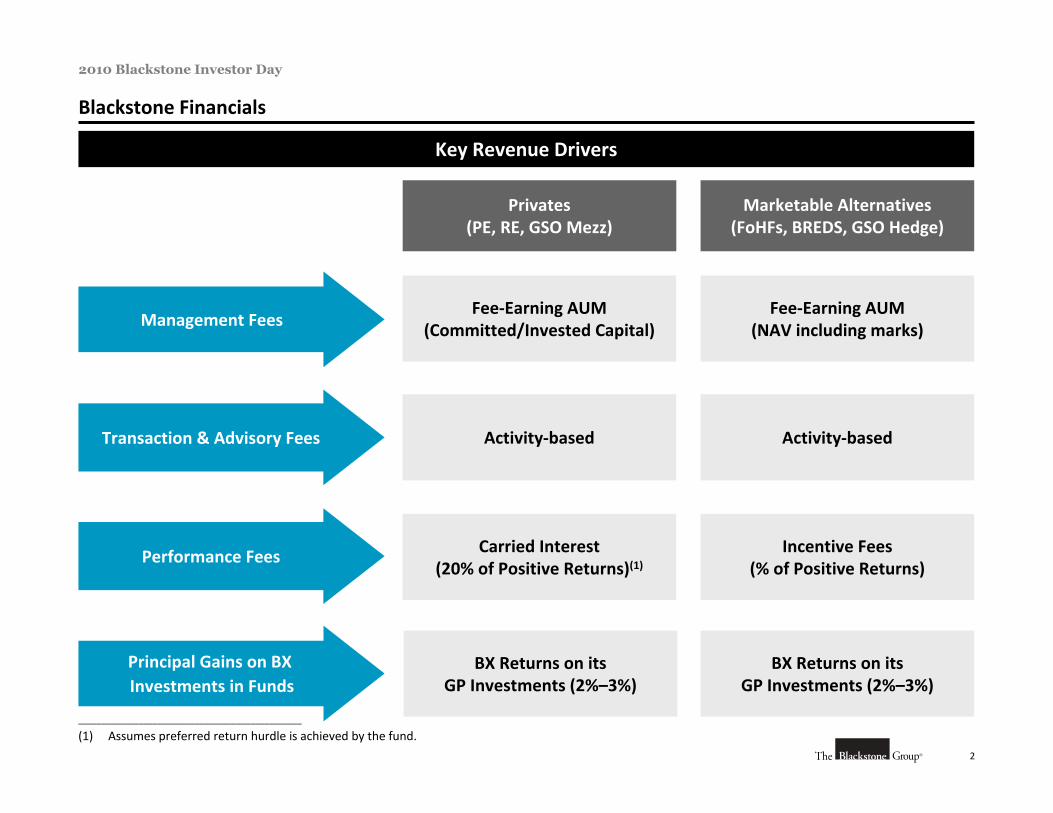

Blackstone Financials

Management Fees

Transaction & Advisory Fees

Principal Gains on BX Investments in Funds

Key Revenue Drivers

Fee‐Earning AUM (Committed/Invested Capital)

Fee‐Earning AUM(NAV including marks)

Privates(PE, RE, GSO Mezz)

Marketable Alternatives(FoHFs, BREDS, GSO Hedge)

Activity‐based

BX Returns on its GP Investments (2%–3%)

BX Returns on its GP Investments (2%–3%)

Activity‐based

Performance Fees Incentive Fees(% of Positive Returns)

Carried Interest(20% of Positive Returns)(1)

________________________________________________

(1) Assumes preferred return hurdle is achieved by the fund.

3

2010 Blackstone Investor Day

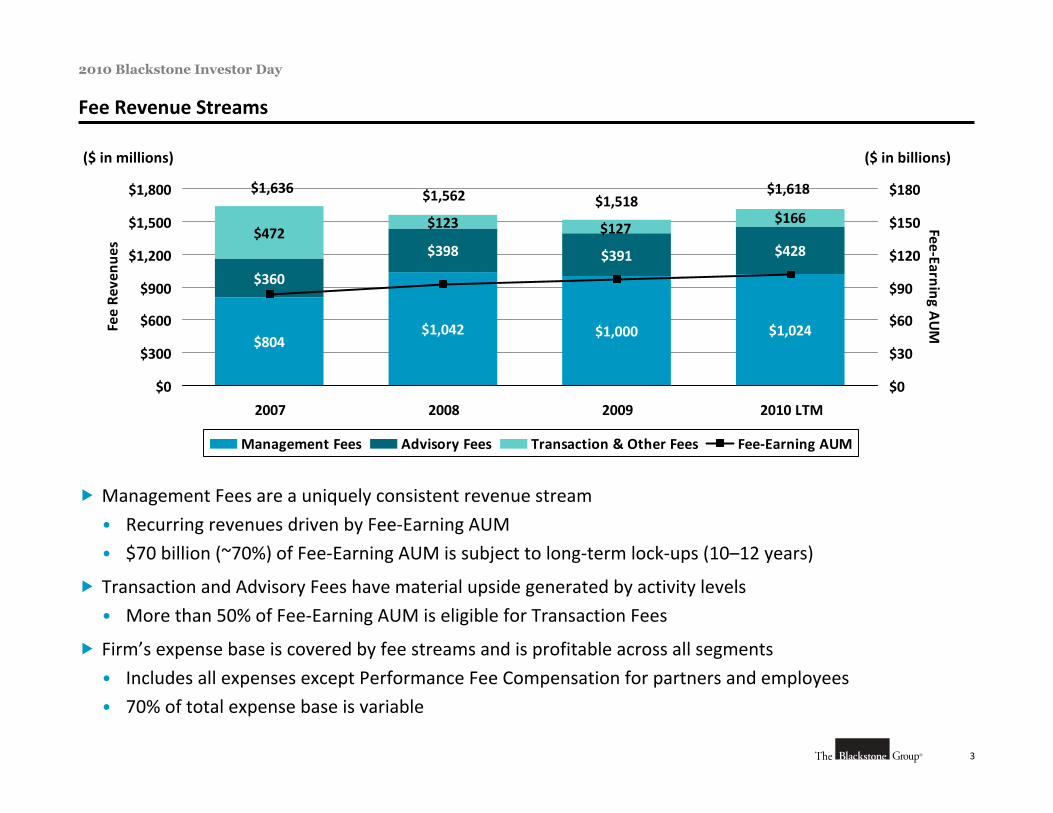

Fee Revenue Streams

Management Fees are a uniquely consistent revenue stream

• Recurring revenues driven by Fee‐Earning AUM

• $70 billion (~70%) of Fee‐Earning AUM is subject to long‐term lock‐ups (10–12 years)

Transaction and Advisory Fees have material upside generated by activity levels

• More than 50% of Fee‐Earning AUM is eligible for Transaction Fees

Firm’s expense base is covered by fee streams and is profitable across all segments

• Includes all expenses except Performance Fee Compensation for partners and employees

• 70% of total expense base is variable

$804$1,042 $1,000 $1,024

$360

$398 $391 $428$472

$123 $166$127

$0

$300

$600

$900

$1,200

$1,500

$1,800

2007 2008 2009 2010 LTM

Fee Re

venu

es

$0

$30

$60

$90

$120

$150

$180

Fee‐Earning AUM

Management Fees Advisory Fees Transaction & Other Fees Fee‐Earning AUM

$1,636 $1,562 $1,518$1,618

($ in millions) ($ in billions)

4

2010 Blackstone Investor Day

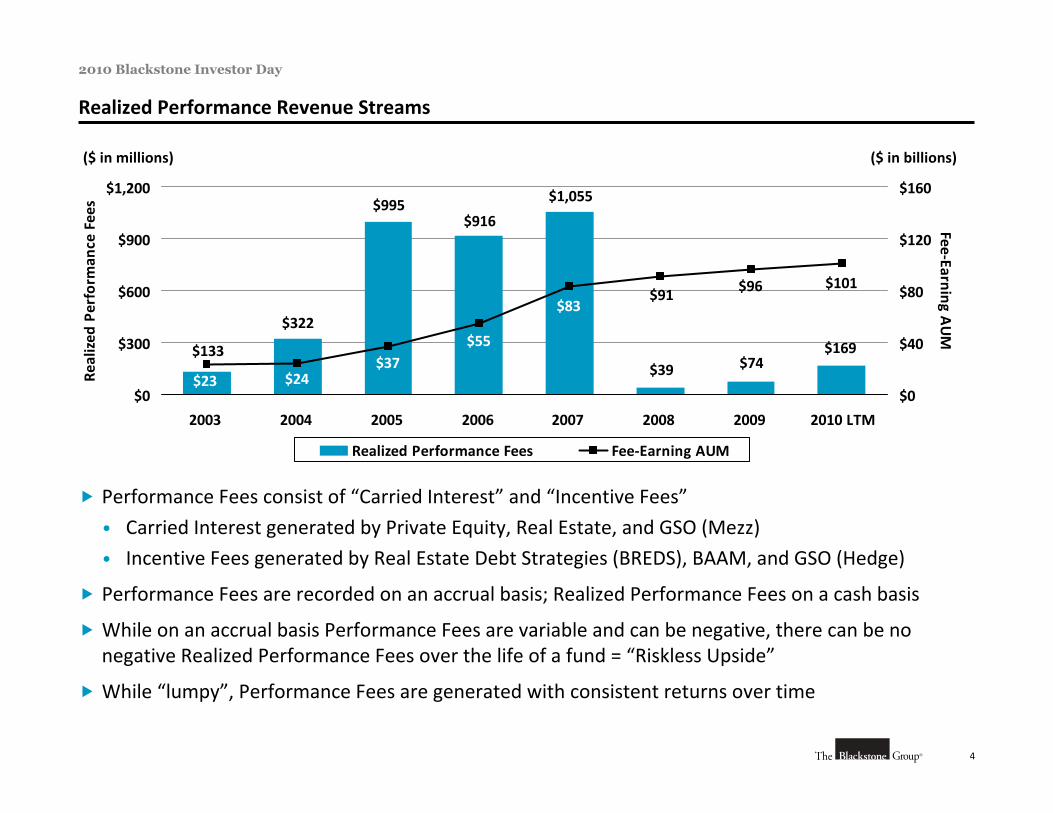

Realized Performance Revenue Streams

Performance Fees consist of “Carried Interest” and “Incentive Fees”

• Carried Interest generated by Private Equity, Real Estate, and GSO (Mezz)

• Incentive Fees generated by Real Estate Debt Strategies (BREDS), BAAM, and GSO (Hedge)

Performance Fees are recorded on an accrual basis; Realized Performance Fees on a cash basis

While on an accrual basis Performance Fees are variable and can be negative, there can be no negative Realized Performance Fees over the life of a fund = “Riskless Upside”

While “lumpy”, Performance Fees are generated with consistent returns over time

$169$74$39

$1,055

$916$995

$133

$322

$101$96$91$83

$55$37

$24$23$0

$300

$600

$900

$1,200

2003 2004 2005 2006 2007 2008 2009 2010 LTM

Realized

Perform

ance Fees

$0

$40

$80

$120

$160

Fee‐Earning AUM

Realized Performance Fees Fee‐Earning AUM

($ in millions) ($ in billions)

5

2010 Blackstone Investor Day

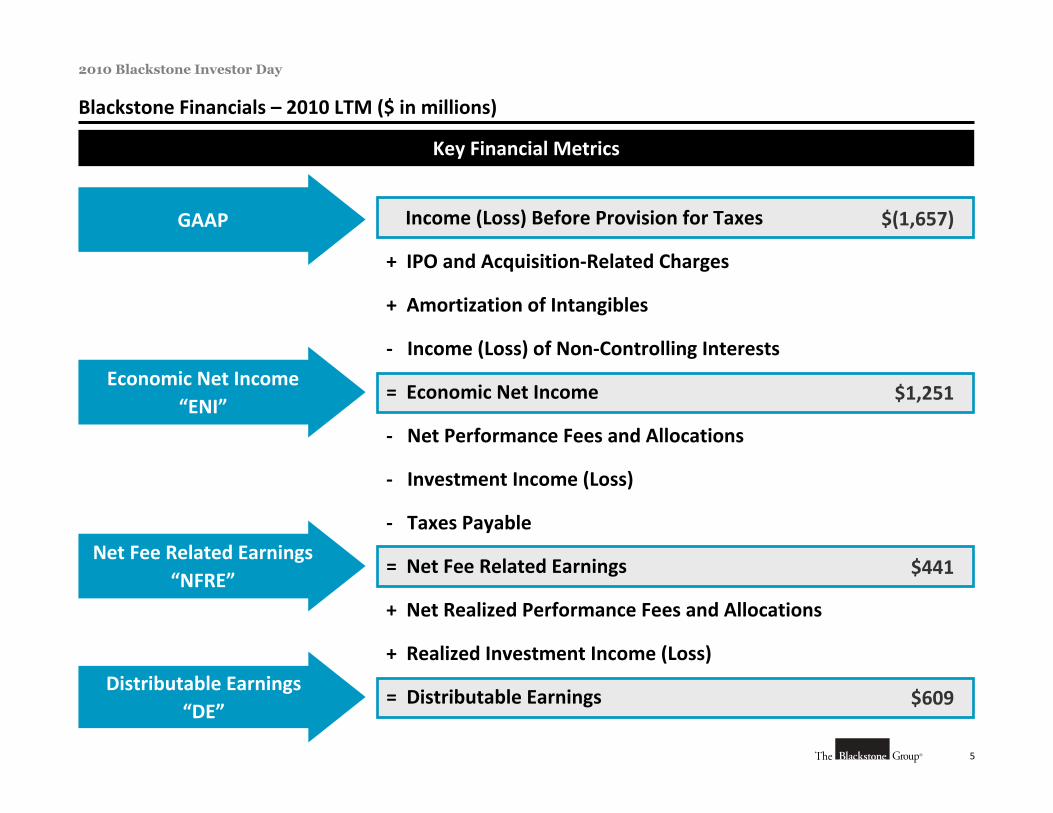

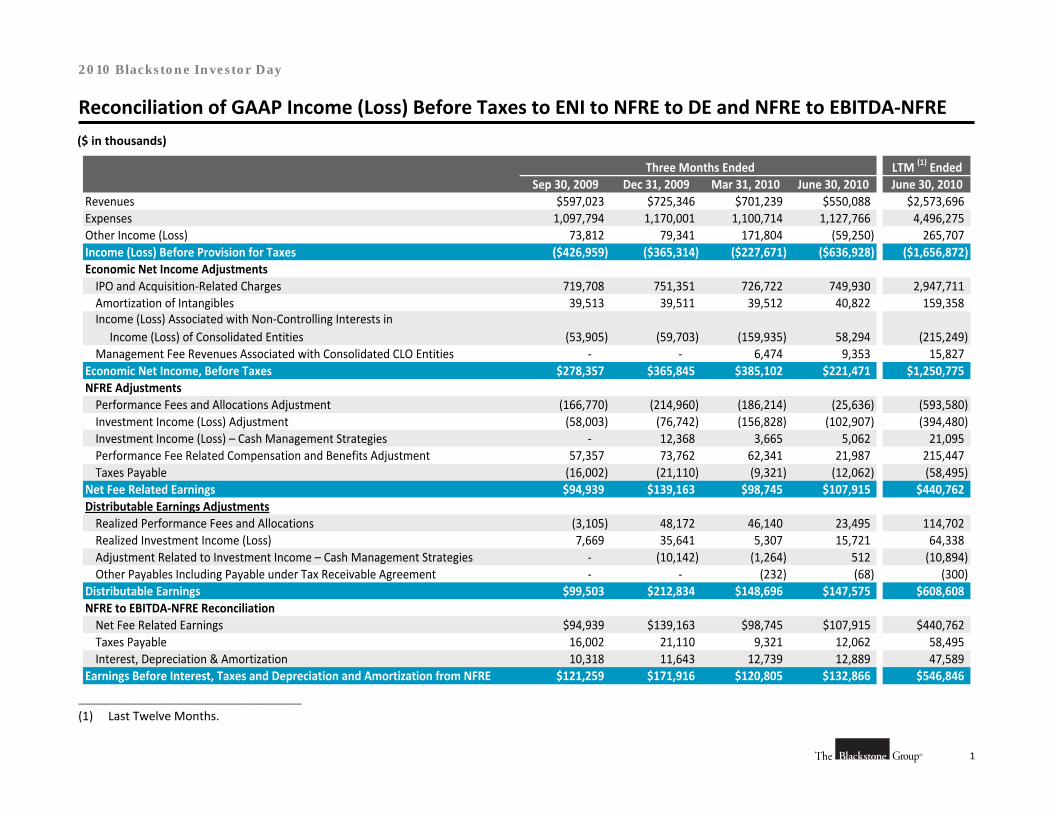

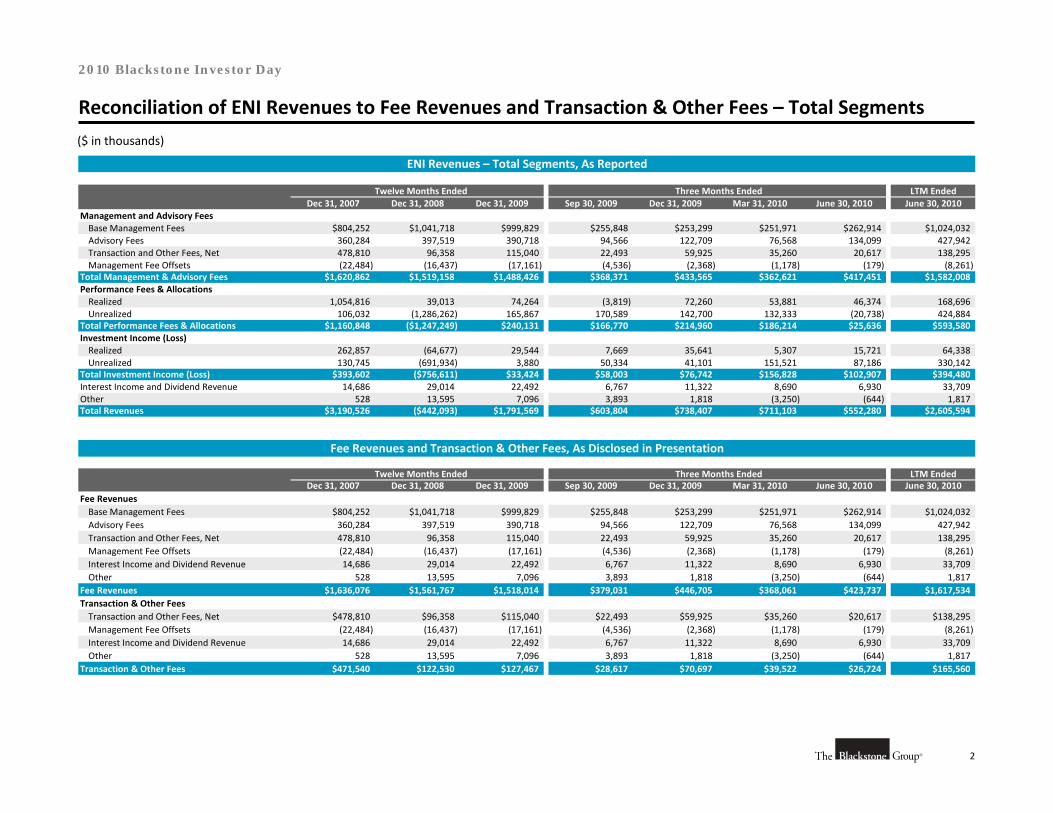

Blackstone Financials – 2010 LTM ($ in millions)

Economic Net Income“ENI”

Distributable Earnings“DE”

Key Financial Metrics

Income (Loss) Before Provision for Taxes

+ IPO and Acquisition‐Related Charges

+ Amortization of Intangibles

‐ Income (Loss) of Non‐Controlling Interests

= Economic Net Income

‐ Net Performance Fees and Allocations

‐ Investment Income (Loss)

‐ Taxes Payable

= Net Fee Related Earnings

+ Net Realized Performance Fees and Allocations

+ Realized Investment Income (Loss)

= Distributable Earnings

Net Fee Related Earnings“NFRE”

GAAP $(1,657)

$1,251

$441

$609

6

2010 Blackstone Investor Day

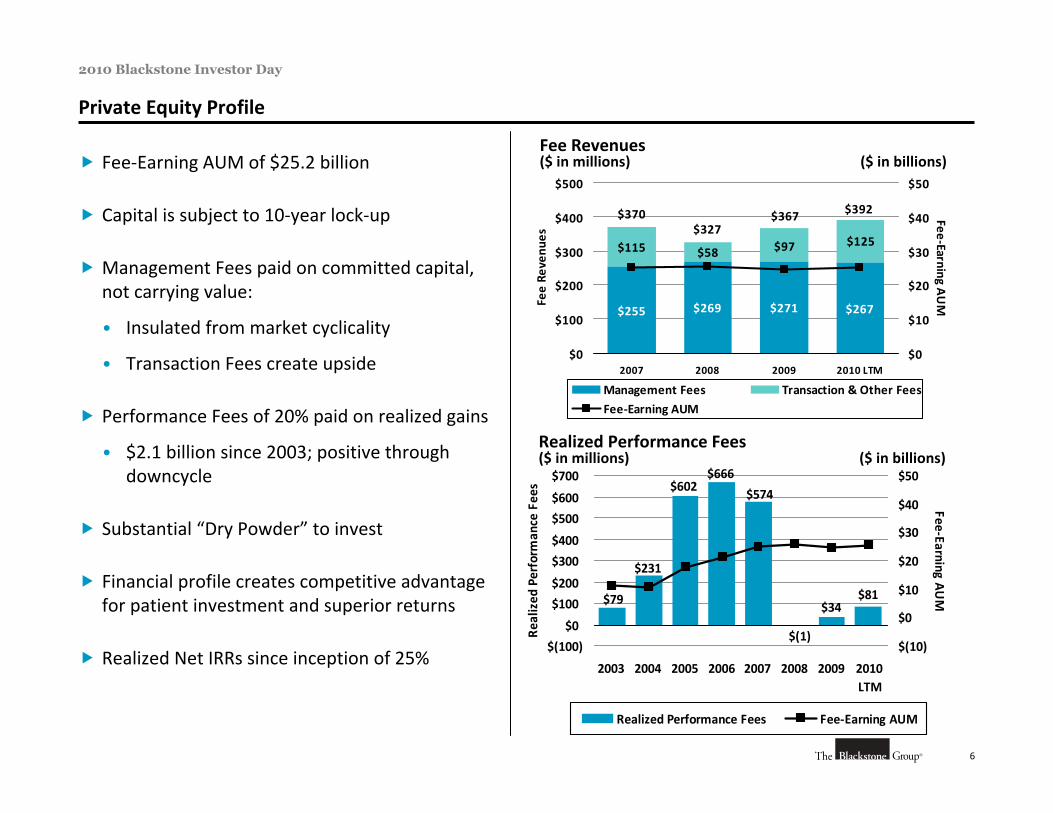

Private Equity Profile

$81$34

$(1)

$574

$666$602

$231

$79

$(100)

$0

$100

$200

$300

$400

$500

$600

$700

2003 2004 2005 2006 2007 2008 2009 2010LTM

Rea

lized

Perform

ance Fee

s

$(10)

$0

$10

$20

$30

$40

$50

Fee‐Earning AUM

Realized Performance Fees Fee‐Earning AUM

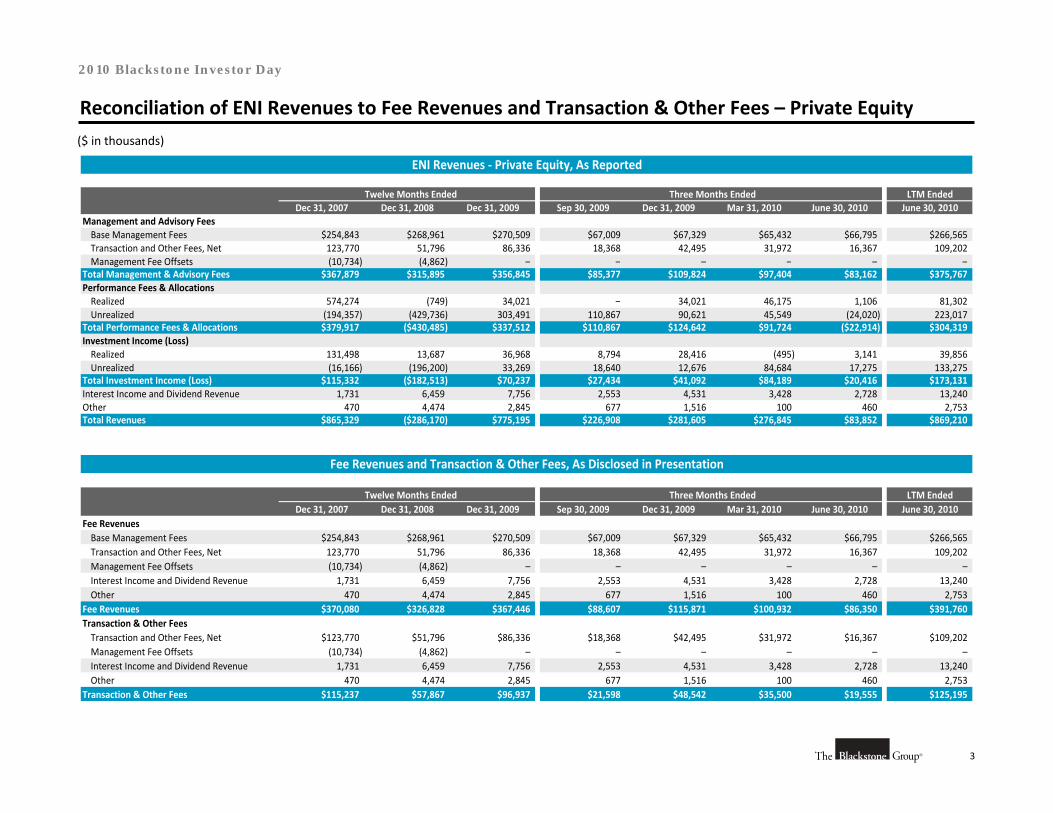

Fee Revenues($ in millions) ($ in billions) Fee‐Earning AUM of $25.2 billion

Capital is subject to 10‐year lock‐up

Management Fees paid on committed capital, not carrying value:

• Insulated from market cyclicality

• Transaction Fees create upside

Performance Fees of 20% paid on realized gains

• $2.1 billion since 2003; positive through downcycle

Substantial “Dry Powder” to invest

Financial profile creates competitive advantage for patient investment and superior returns

Realized Net IRRs since inception of 25%

Realized Performance Fees($ in millions) ($ in billions)

$255 $269 $271 $267

$115 $58$125$97

$392$367$327

$370

$0

$100

$200

$300

$400

$500

2007 2008 2009 2010 LTM

Fee Re

venu

es

$0

$10

$20

$30

$40

$50

Fee‐Earning AUM

Management Fees Transaction & Other Fees

Fee‐Earning AUM

7

2010 Blackstone Investor Day

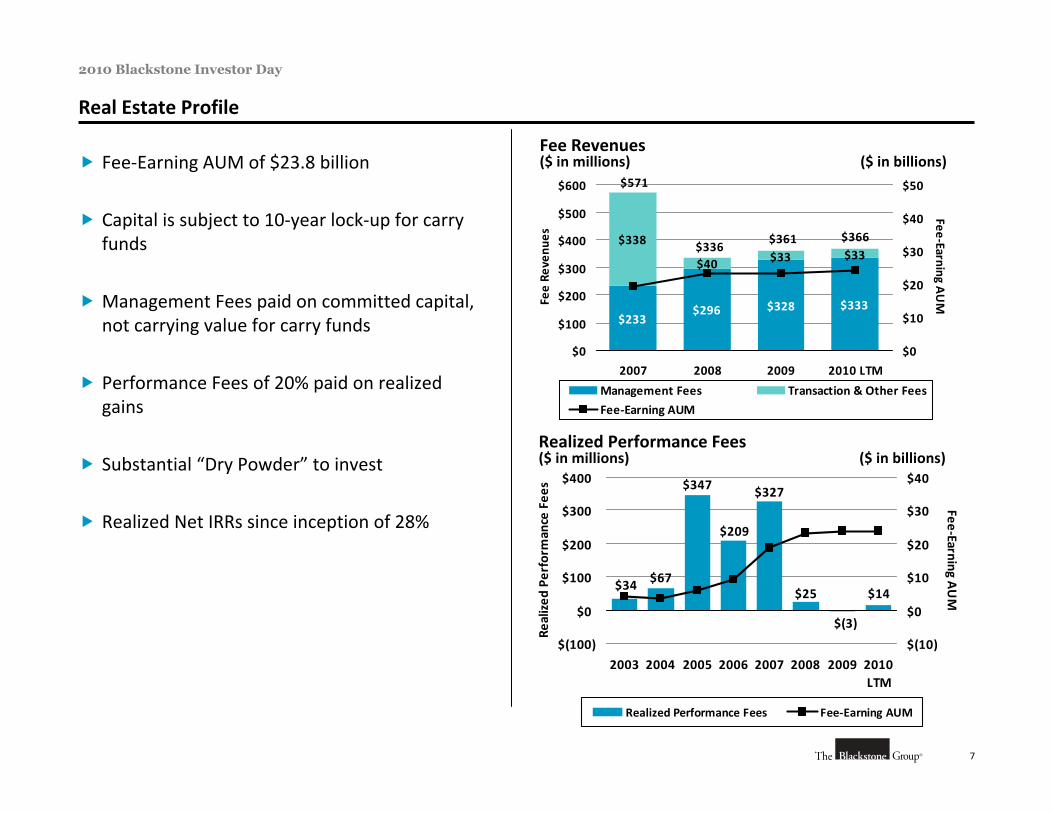

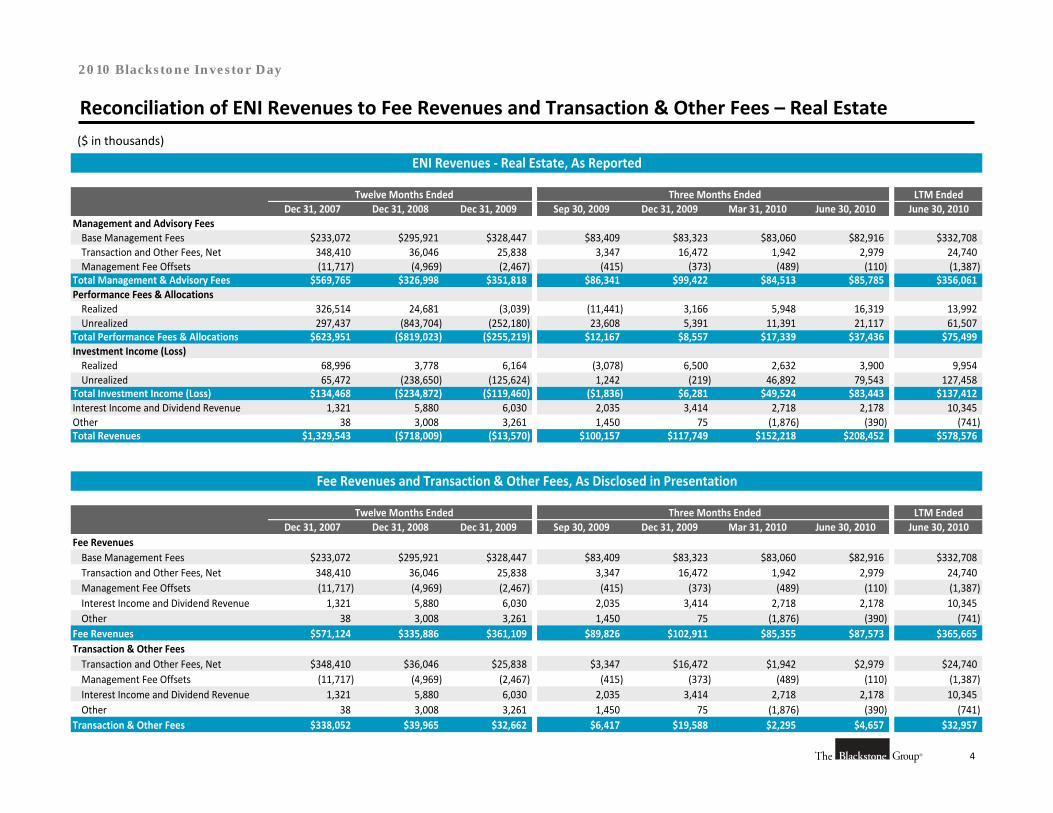

Real Estate Profile

$233$296 $328 $333

$338

$40 $33 $33$361

$571

$336$366

$0

$100

$200

$300

$400

$500

$600

2007 2008 2009 2010 LTM

Fee Re

venu

es

$0

$10

$20

$30

$40

$50

Fee‐Earning AUM

Management Fees Transaction & Other Fees

Fee‐Earning AUM

$(3)

$14$25

$327

$209

$347

$67$34

$(100)

$0

$100

$200

$300

$400

2003 2004 2005 2006 2007 2008 2009 2010LTM

Realized

Perform

ance Fee

s

$(10)

$0

$10

$20

$30

$40

Fee‐Earning AUM

Realized Performance Fees Fee‐Earning AUM

Fee‐Earning AUM of $23.8 billion

Capital is subject to 10‐year lock‐up for carry funds

Management Fees paid on committed capital, not carrying value for carry funds

Performance Fees of 20% paid on realized gains

Substantial “Dry Powder” to invest

Realized Net IRRs since inception of 28%

Fee Revenues($ in millions) ($ in billions)

Realized Performance Fees($ in millions) ($ in billions)

8

2010 Blackstone Investor Day

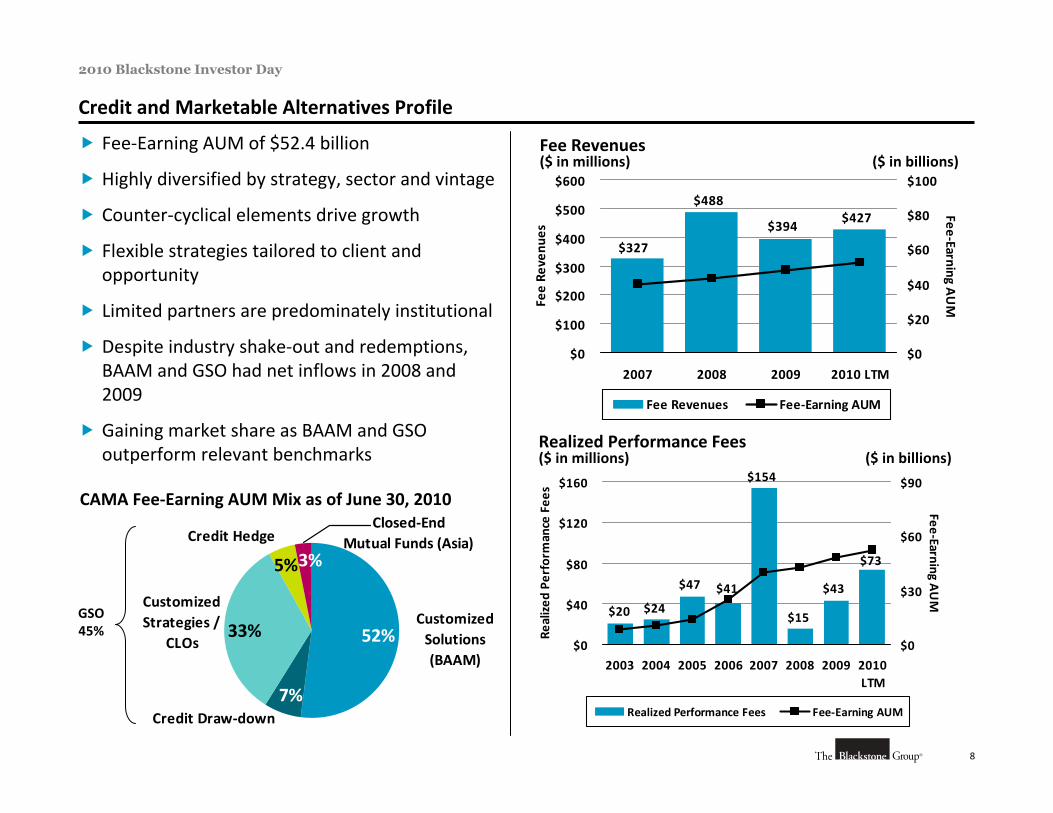

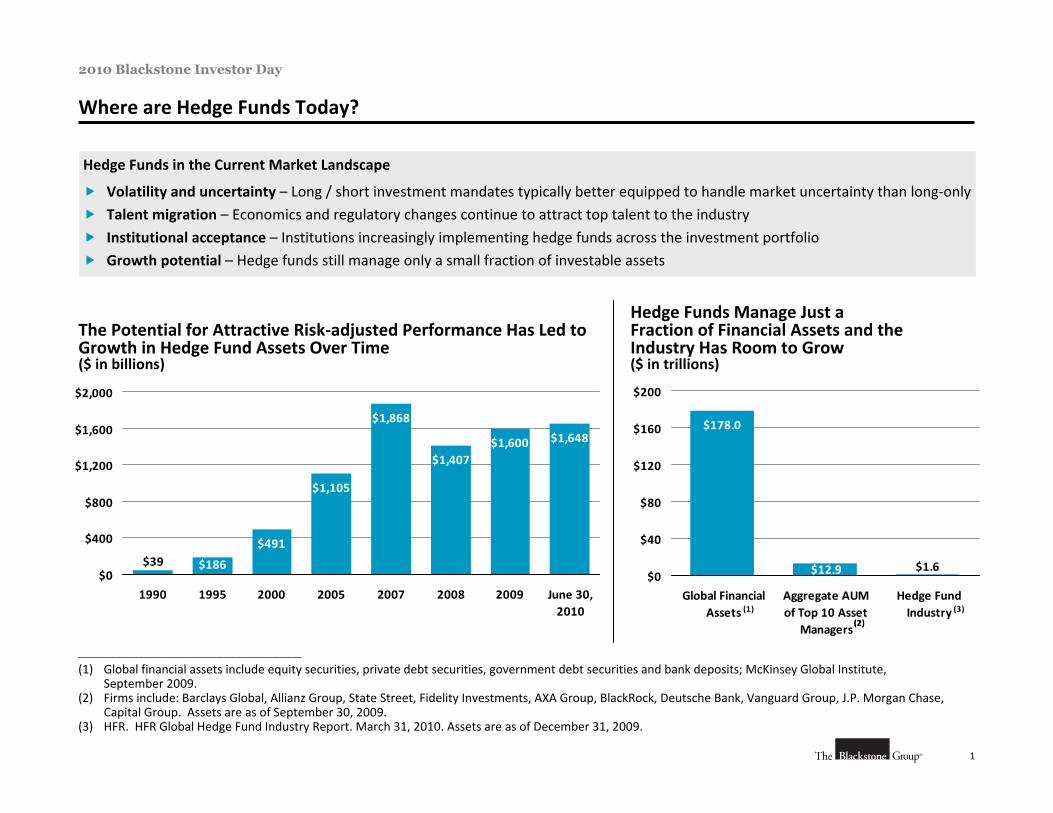

5%

7%

3%

33% 52%CustomizedSolutions(BAAM)

Credit Draw‐down

Customized Strategies /

CLOs

Credit HedgeClosed‐End

Mutual Funds (Asia)

Fee‐Earning AUM of $52.4 billion

Highly diversified by strategy, sector and vintage

Counter‐cyclical elements drive growth

Flexible strategies tailored to client and opportunity

Limited partners are predominately institutional

Despite industry shake‐out and redemptions, BAAM and GSO had net inflows in 2008 and 2009

Gaining market share as BAAM and GSO outperform relevant benchmarks

Credit and Marketable Alternatives Profile

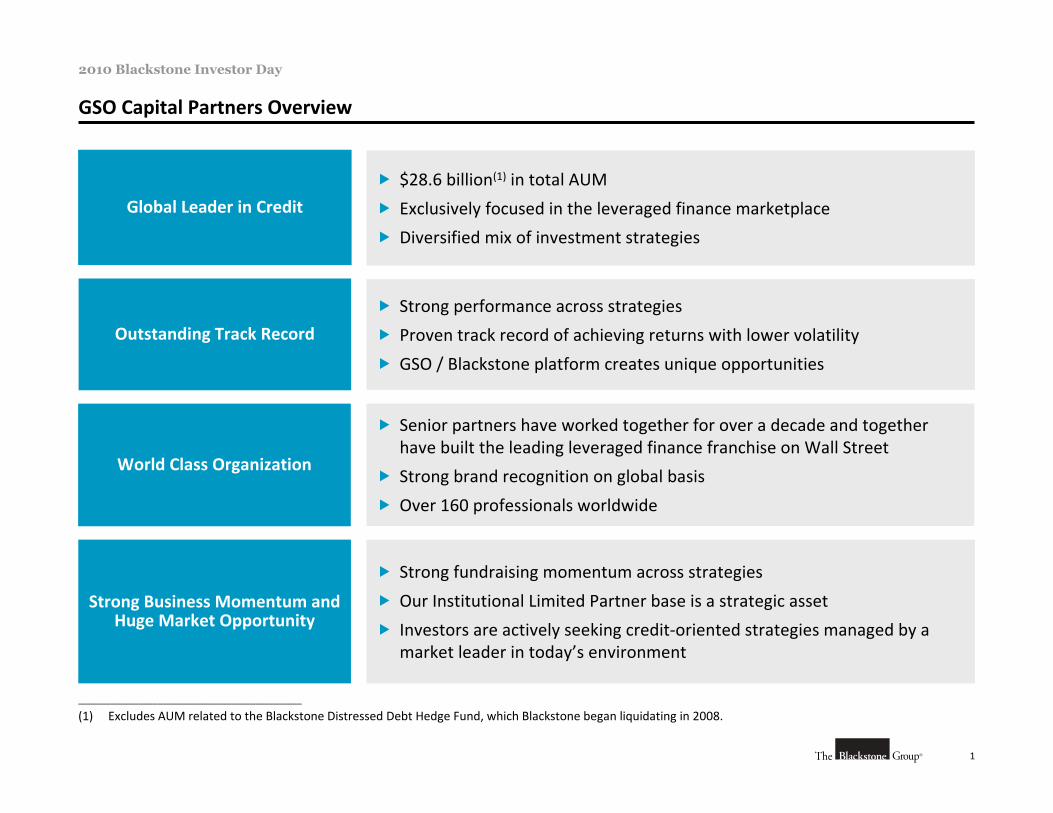

CAMA Fee‐Earning AUM Mix as of June 30, 2010

GSO45%

$43

$73

$15

$154

$41$47

$24$20

$0

$40

$80

$120

$160

2003 2004 2005 2006 2007 2008 2009 2010LTM

Realized

Perform

ance Fee

s

$0

$30

$60

$90

Fee‐Earning AUM

Realized Performance Fees Fee‐Earning AUM

$427$394

$488

$327

$0

$100

$200

$300

$400

$500

$600

2007 2008 2009 2010 LTM

Fee Re

venu

es

$0

$20

$40

$60

$80

$100

Fee‐Earning AUM

Fee Revenues Fee‐Earning AUM

Fee Revenues($ in millions) ($ in billions)

Realized Performance Fees($ in millions) ($ in billions)

9

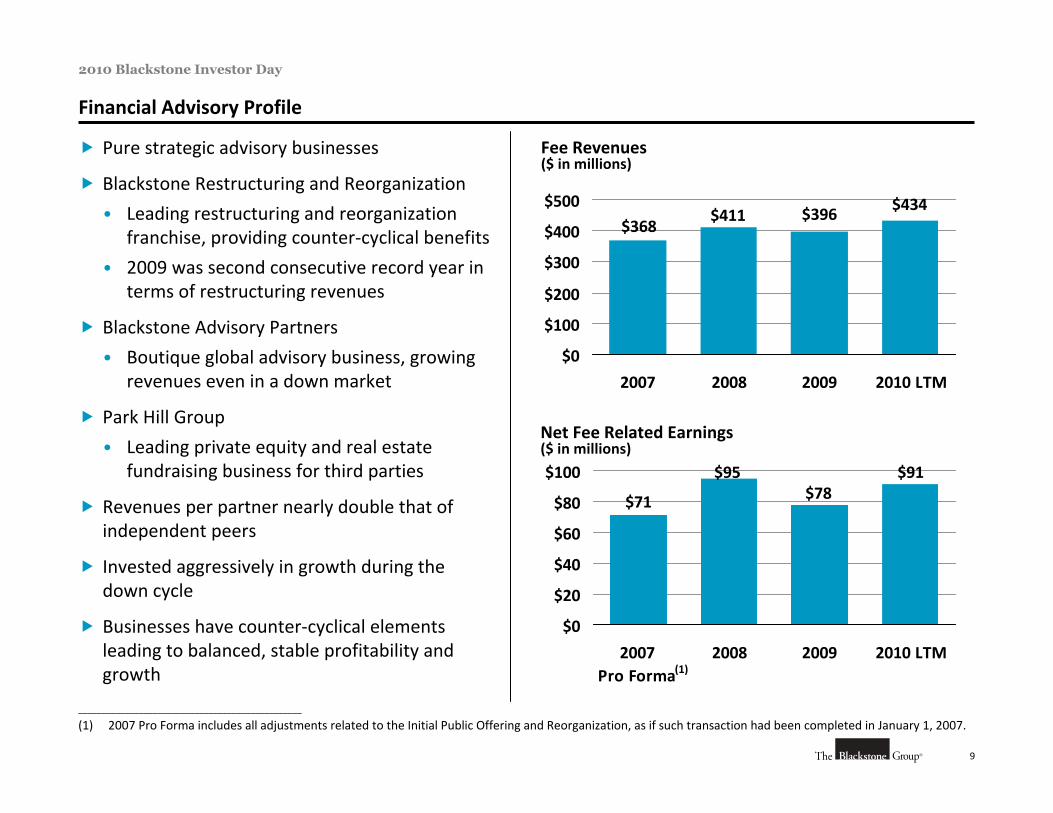

2010 Blackstone Investor Day

Pure strategic advisory businesses

Blackstone Restructuring and Reorganization

• Leading restructuring and reorganization franchise, providing counter‐cyclical benefits

• 2009 was second consecutive record year in terms of restructuring revenues

Blackstone Advisory Partners

• Boutique global advisory business, growing revenues even in a down market

Park Hill Group

• Leading private equity and real estate fundraising business for third parties

Revenues per partner nearly double that of independent peers

Invested aggressively in growth during the down cycle

Businesses have counter‐cyclical elements leading to balanced, stable profitability and growth

Financial Advisory Profile

Fee Revenues($ in millions)

$434$396$411$368

$0

$100

$200

$300

$400

$500

2007 2008 2009 2010 LTM

Net Fee Related Earnings($ in millions)

$91$78

$95

$71

$0

$20

$40

$60

$80

$100

2007 Pro Forma

2008 2009 2010 LTM

________________________________________________

(1) 2007 Pro Forma includes all adjustments related to the Initial Public Offering and Reorganization, as if such transaction had been completed in January 1, 2007.

(1)

10

2010 Blackstone Investor Day

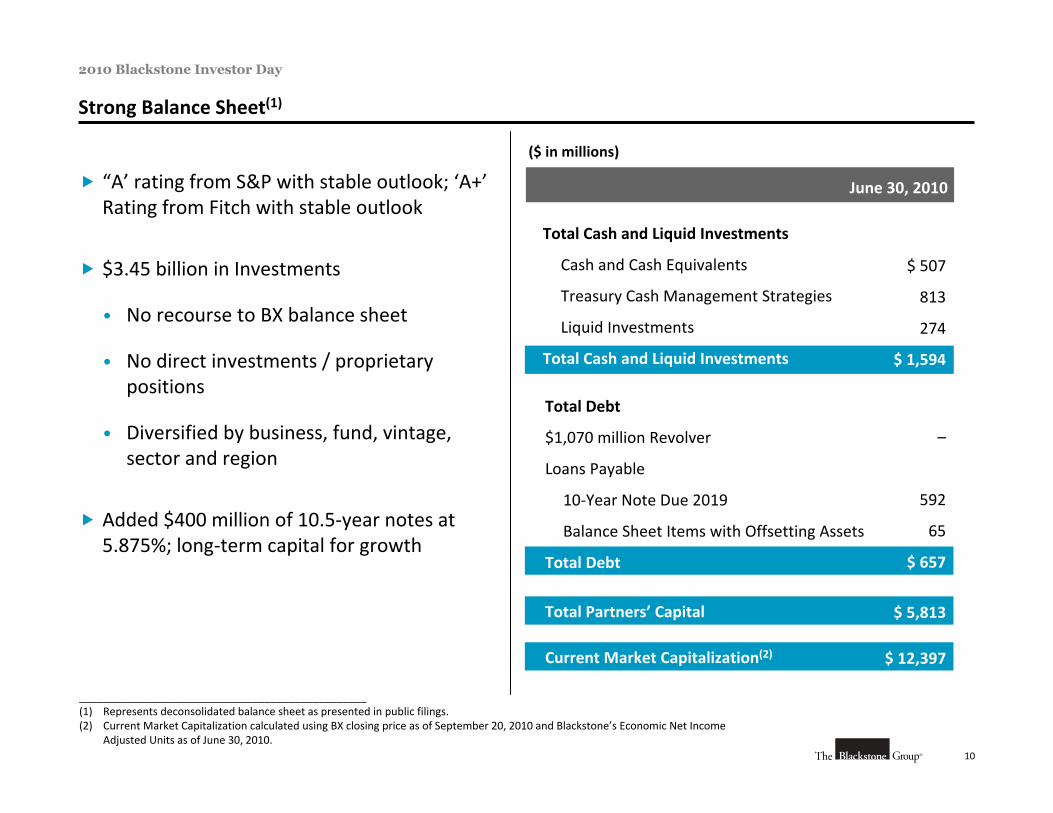

Strong Balance Sheet(1)

“A’ rating from S&P with stable outlook; ‘A+’Rating from Fitch with stable outlook

$3.45 billion in Investments

• No recourse to BX balance sheet

• No direct investments / proprietary positions

• Diversified by business, fund, vintage, sector and region

Added $400 million of 10.5‐year notes at 5.875%; long‐term capital for growth

June 30, 2010

Total Cash and Liquid Investments

Cash and Cash Equivalents

Treasury Cash Management Strategies

Liquid Investments

Total Cash and Liquid Investments

$ 507

813

274

$ 1,594

Total Debt

$1,070 million Revolver

Loans Payable

10‐Year Note Due 2019

Balance Sheet Items with Offsetting Assets

Total Debt

–

592

65

$ 657

($ in millions)

Total Partners’ Capital $ 5,813

________________________________________________(1) Represents deconsolidated balance sheet as presented in public filings.(2) Current Market Capitalization calculated using BX closing price as of September 20, 2010 and Blackstone’s Economic Net Income

Adjusted Units as of June 30, 2010.

Current Market Capitalization(2) $ 12,397

III. Portfolio Operations Group

1

2010 Blackstone Investor Day

Our Mission: Sustainable Competitive Advantage Delivering Long‐Term Value

Blackstone’s Portfolio Operations Group… works with our investment teams and portfolio company senior management to help acquired businesses become more productive, competitive and efficient

In the process, we build stronger enterprises, preserve and create jobs, and enable our portfolio companies to achieve lasting value for both our fund investors and successor owners

2

2010 Blackstone Investor Day

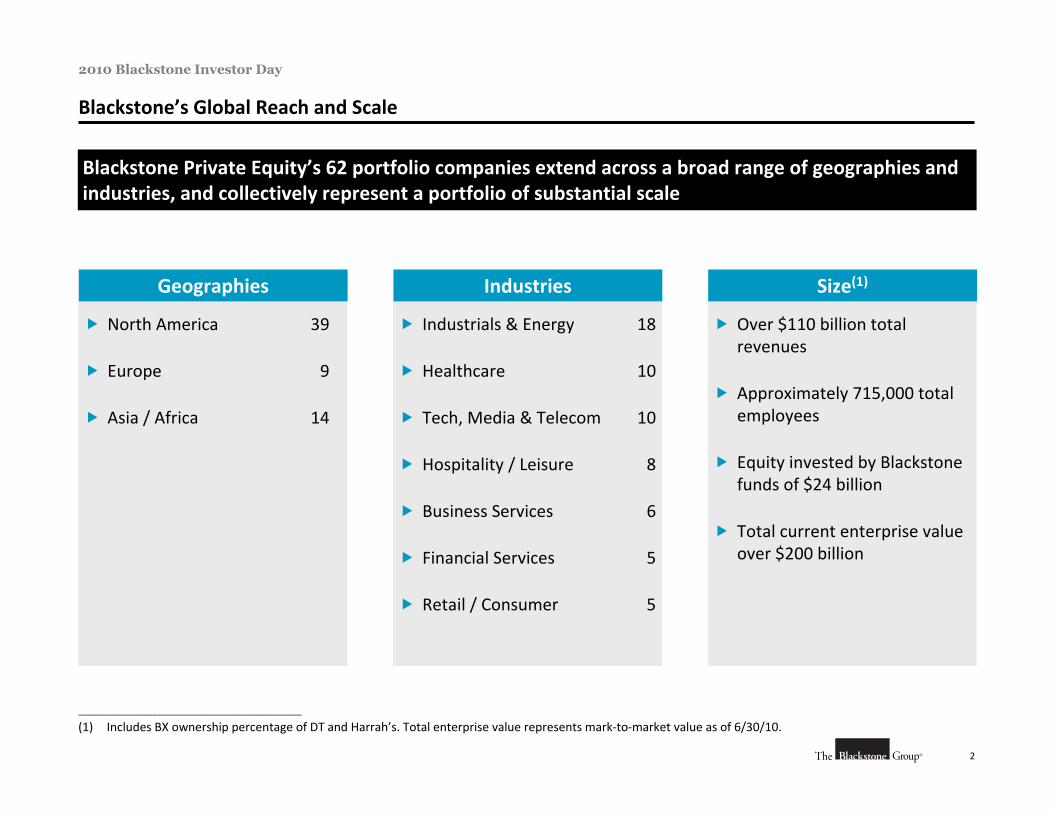

Blackstone’s Global Reach and Scale

Blackstone Private Equity’s 62 portfolio companies extend across a broad range of geographies and industries, and collectively represent a portfolio of substantial scale

North America 39

Europe 9

Asia / Africa 14

Geographies

Industrials & Energy 18

Healthcare 10

Tech, Media & Telecom 10

Hospitality / Leisure 8

Business Services 6

Financial Services 5

Retail / Consumer 5

Industries

Over $110 billion total revenues

Approximately 715,000 total employees

Equity invested by Blackstone funds of $24 billion

Total current enterprise value over $200 billion

Size(1)

________________________________________________

(1) Includes BX ownership percentage of DT and Harrah’s. Total enterprise value represents mark‐to‐market value as of 6/30/10.

3

2010 Blackstone Investor Day

Financial Stability

Productivity & Competitiveness

Structural Transformation

Revenue Optimization

Strategy & Performance Enhancement

Corporate Governance

Corporate Responsibility

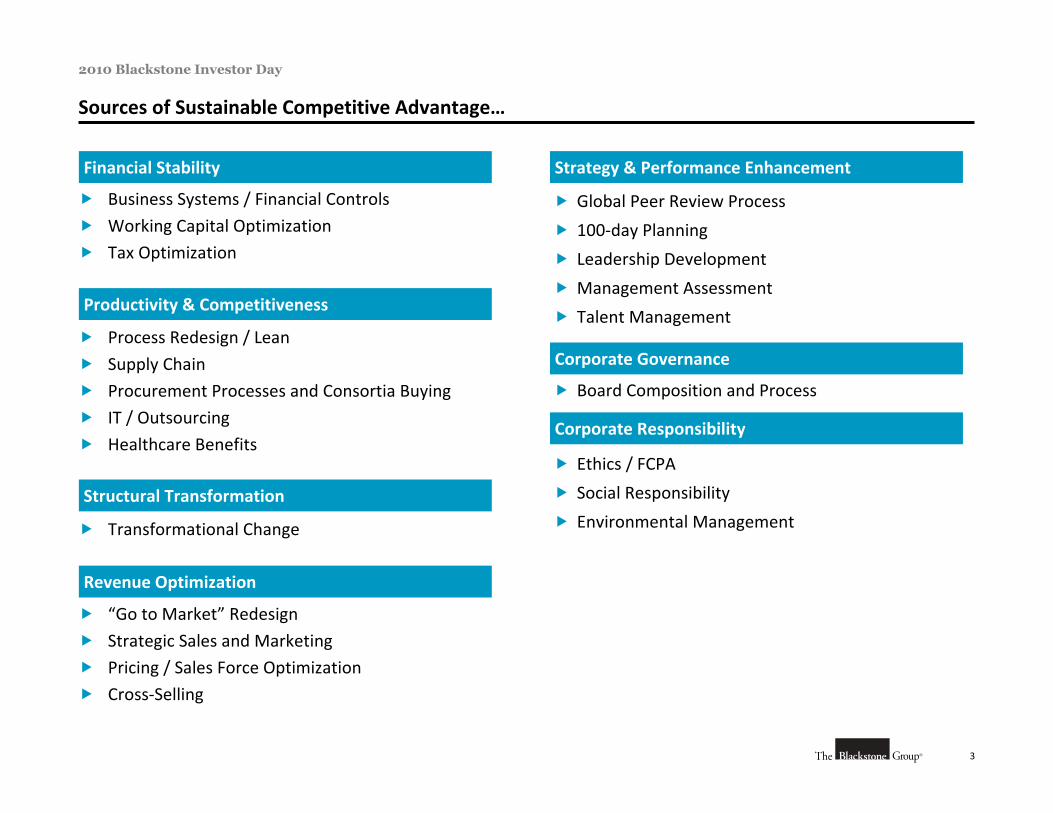

Sources of Sustainable Competitive Advantage…

Business Systems / Financial Controls

Working Capital Optimization

Tax Optimization

Process Redesign / Lean

Supply Chain

Procurement Processes and Consortia Buying

IT / Outsourcing

Healthcare Benefits

Transformational Change

“Go to Market” Redesign

Strategic Sales and Marketing

Pricing / Sales Force Optimization

Cross‐Selling

Global Peer Review Process

100‐day Planning

Leadership Development

Management Assessment

Talent Management

Board Composition and Process

Ethics / FCPA

Social Responsibility

Environmental Management

4

2010 Blackstone Investor Day

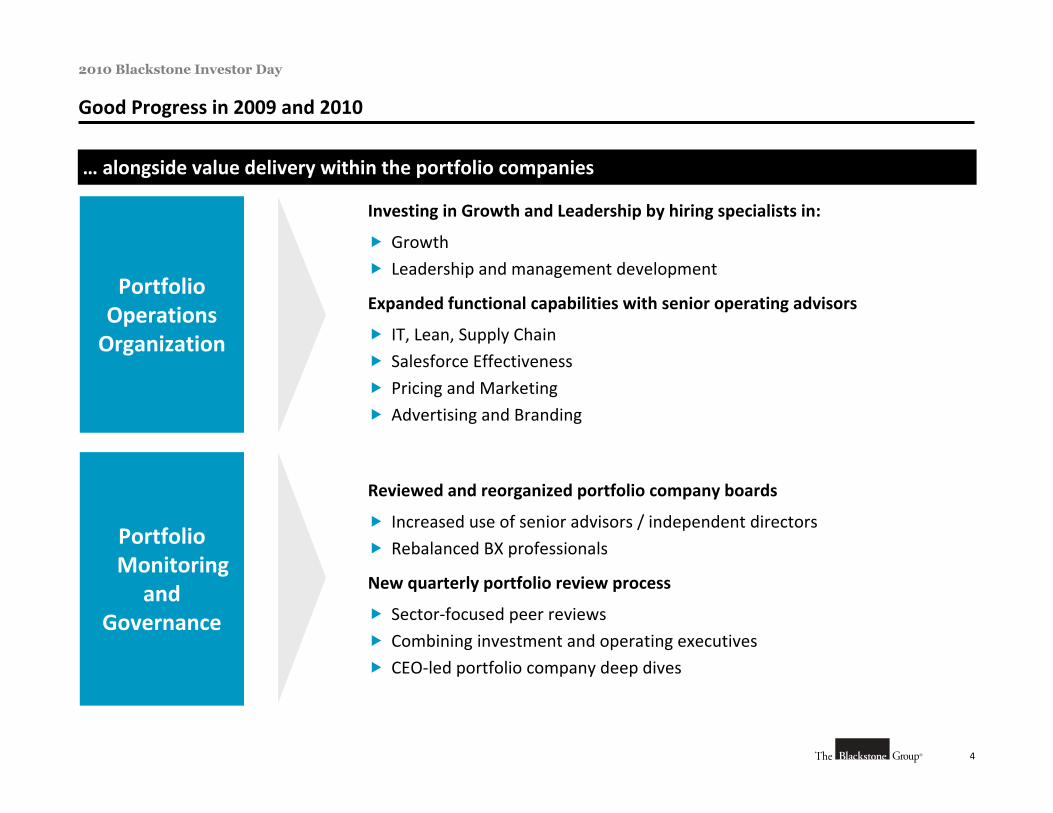

Good Progress in 2009 and 2010

… alongside value delivery within the portfolio companies

Portfolio Operations Organization

Investing in Growth and Leadership by hiring specialists in:

Growth

Leadership and management development

Expanded functional capabilities with senior operating advisors

IT, Lean, Supply Chain

Salesforce Effectiveness

Pricing and Marketing

Advertising and Branding

Portfolio Monitoring

and Governance

Reviewed and reorganized portfolio company boards

Increased use of senior advisors / independent directors

Rebalanced BX professionals

New quarterly portfolio review process

Sector‐focused peer reviews

Combining investment and operating executives

CEO‐led portfolio company deep dives

5

2010 Blackstone Investor Day

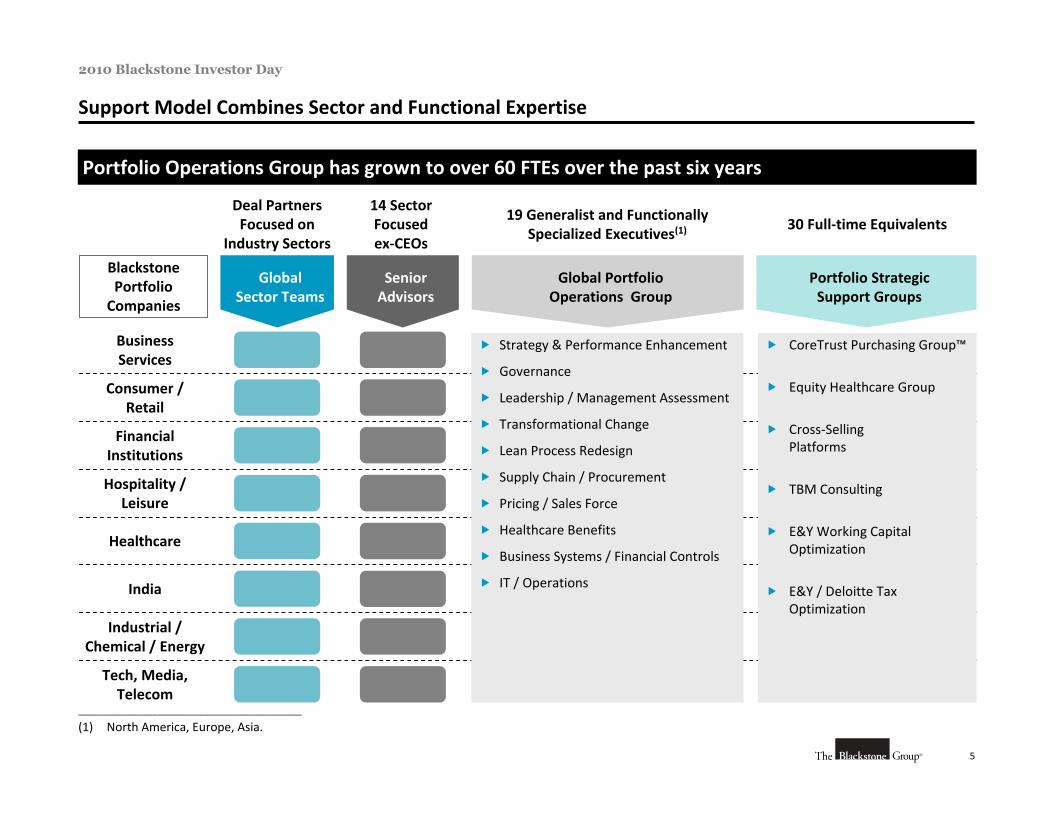

Support Model Combines Sector and Functional Expertise

Portfolio Operations Group has grown to over 60 FTEs over the past six years

________________________________________________

(1) North America, Europe, Asia.

Deal Partners Focused on

Industry Sectors

14 Sector Focused ex‐CEOs

19 Generalist and Functionally Specialized Executives(1)

30 Full‐time Equivalents

Blackstone Portfolio Companies

Portfolio Strategic Support Groups

GlobalSector Teams

Senior Advisors

Global PortfolioOperations Group

BusinessServices

Consumer / Retail

Financial Institutions

Hospitality / Leisure

Healthcare

India

Industrial /Chemical / Energy

Tech, Media, Telecom

Strategy & Performance Enhancement

Governance

Leadership / Management Assessment

Transformational Change

Lean Process Redesign

Supply Chain / Procurement

Pricing / Sales Force

Healthcare Benefits

Business Systems / Financial Controls

IT / Operations

CoreTrust Purchasing Group™

Equity Healthcare Group

Cross‐SellingPlatforms

TBM Consulting

E&Y Working Capital Optimization

E&Y / Deloitte Tax Optimization

6

2010 Blackstone Investor Day

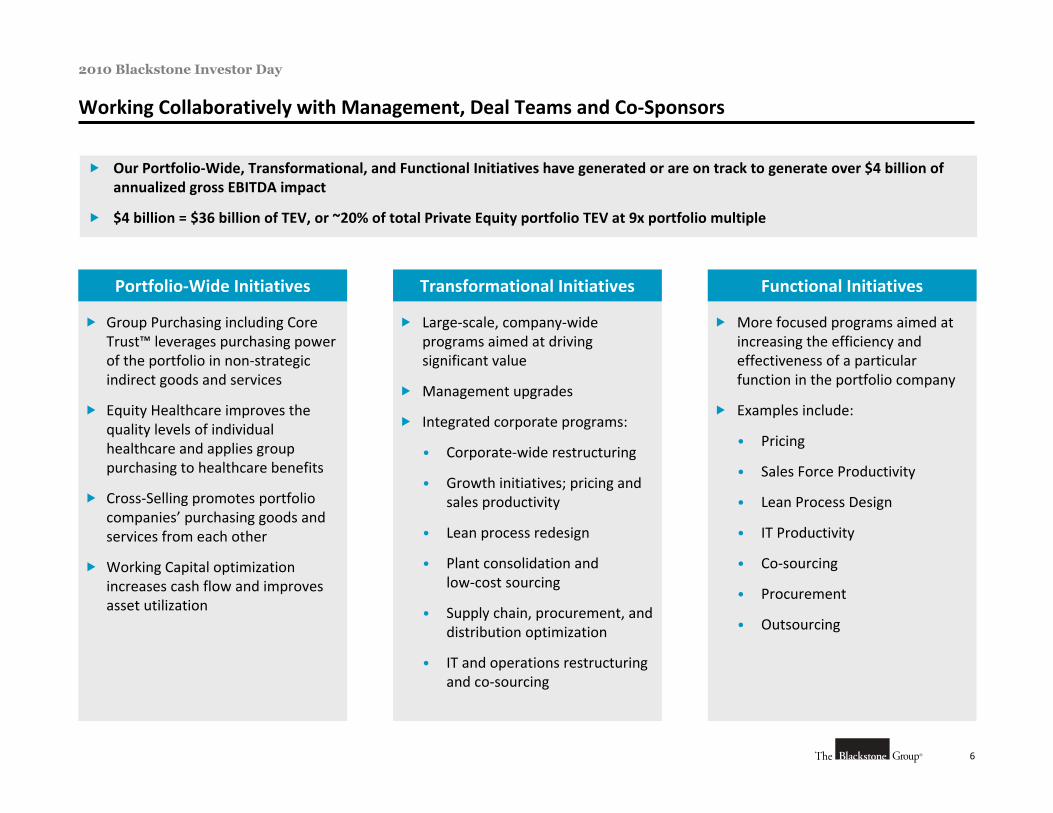

Working Collaboratively with Management, Deal Teams and Co‐Sponsors

Our Portfolio‐Wide, Transformational, and Functional Initiatives have generated or are on track to generate over $4 billion of annualized gross EBITDA impact

$4 billion = $36 billion of TEV, or ~20% of total Private Equity portfolio TEV at 9x portfolio multiple

Group Purchasing including Core Trust™ leverages purchasing power of the portfolio in non‐strategic indirect goods and services

Equity Healthcare improves the quality levels of individual healthcare and applies group purchasing to healthcare benefits

Cross‐Selling promotes portfolio companies’ purchasing goods and services from each other

Working Capital optimization increases cash flow and improves asset utilization

Portfolio‐Wide Initiatives

Large‐scale, company‐wide programs aimed at driving significant value

Management upgrades

Integrated corporate programs:

• Corporate‐wide restructuring

• Growth initiatives; pricing and sales productivity

• Lean process redesign

• Plant consolidation and low‐cost sourcing

• Supply chain, procurement, and distribution optimization

• IT and operations restructuring and co‐sourcing

Transformational Initiatives

More focused programs aimed at increasing the efficiency and effectiveness of a particular function in the portfolio company

Examples include:

• Pricing

• Sales Force Productivity

• Lean Process Design

• IT Productivity

• Co‐sourcing

• Procurement

• Outsourcing

Functional Initiatives

7

2010 Blackstone Investor Day

Freescale Semiconductor

Gokaldas Exports Hilton Hotels Michaels Stores

Nielsen

Travelport

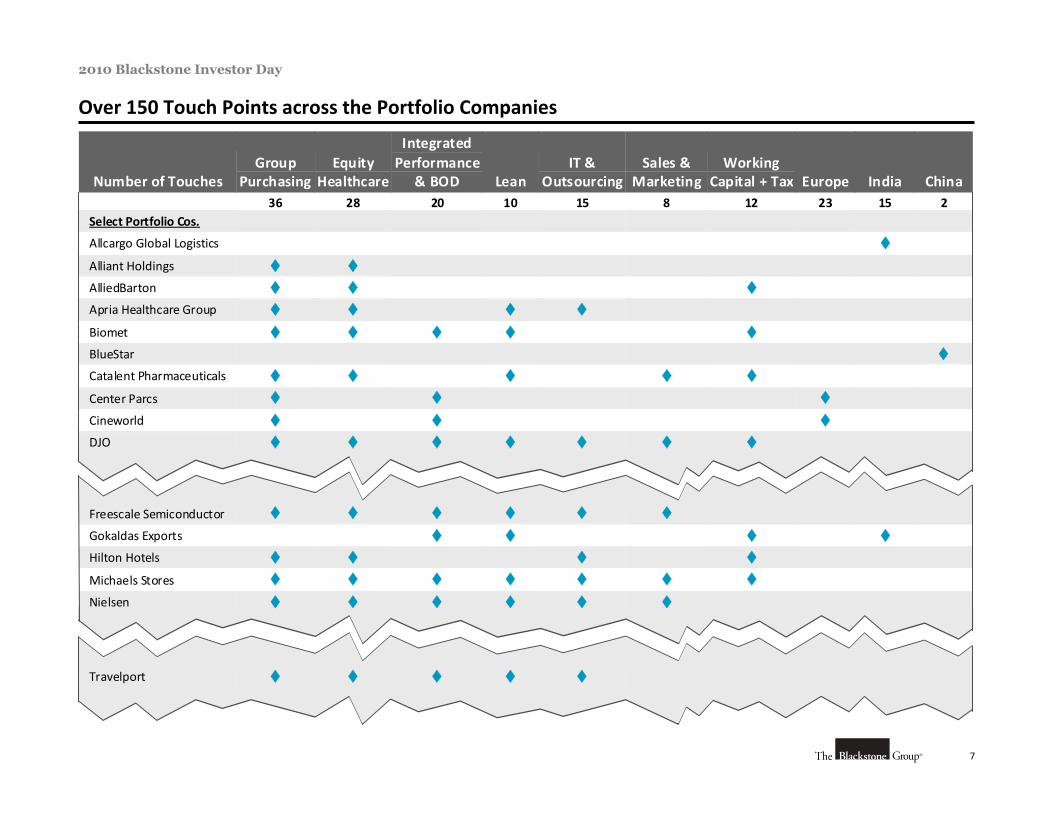

Number of Touches Group

Purchasing Equity

Healthcare

Integrated Performance

& BOD Lean IT &

Outsourcing Sales &

MarketingWorking

Capital + Tax Europe India China 36 28 20 10 15 8 12 23 15 2 Select Portfolio Cos. Allcargo Global Logistics

Alliant Holdings AlliedBarton Apria Healthcare Group Biomet BlueStar Catalent Pharmaceuticals Center Parcs Cineworld DJO

Over 150 Touch Points across the Portfolio Companies

8

2010 Blackstone Investor Day

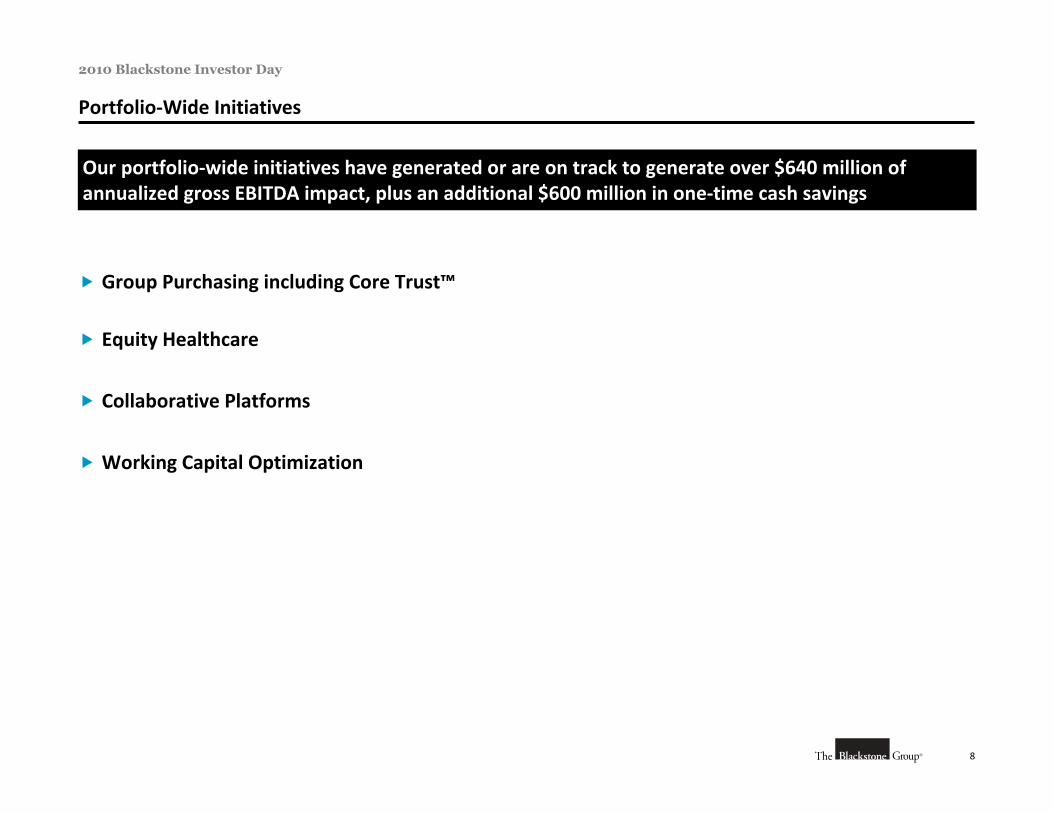

Portfolio‐Wide Initiatives

Group Purchasing including Core Trust™

Equity Healthcare

Collaborative Platforms

Working Capital Optimization

Our portfolio‐wide initiatives have generated or are on track to generate over $640 million of annualized gross EBITDA impact, plus an additional $600 million in one‐time cash savings

9

2010 Blackstone Investor Day

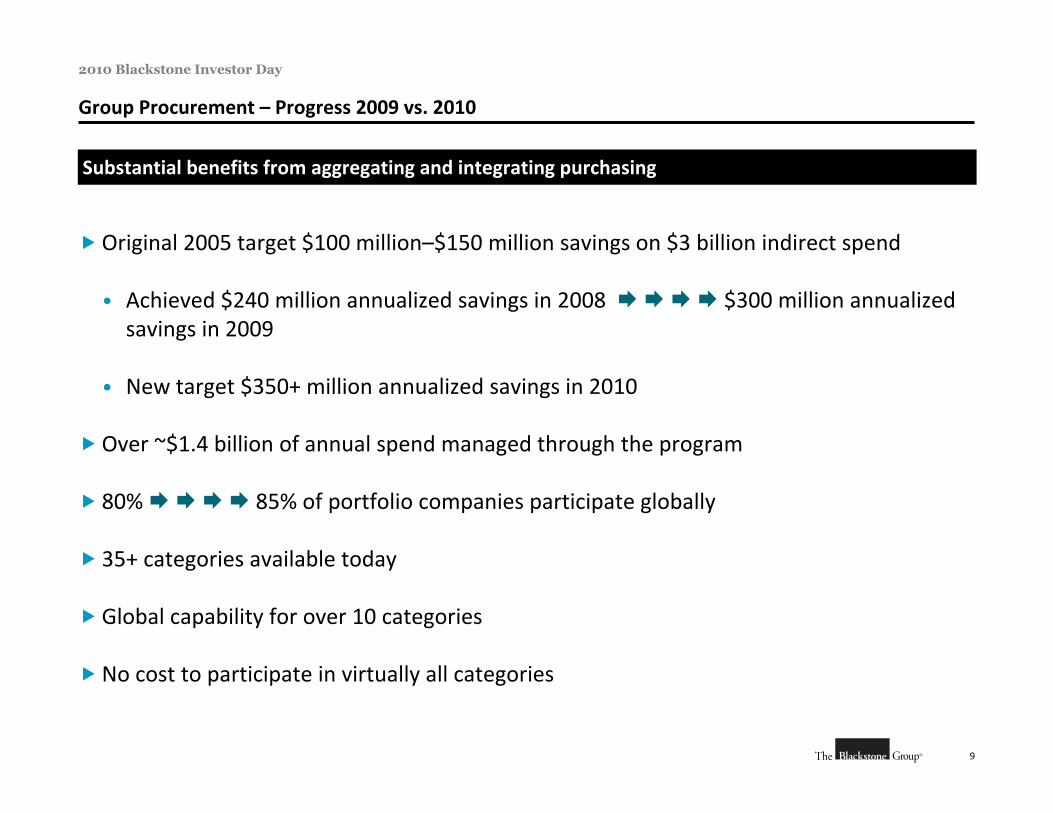

Group Procurement – Progress 2009 vs. 2010

Original 2005 target $100 million–$150 million savings on $3 billion indirect spend

• Achieved $240 million annualized savings in 2008 $300 million annualized savings in 2009

• New target $350+ million annualized savings in 2010

Over ~$1.4 billion of annual spend managed through the program

80% 85% of portfolio companies participate globally

35+ categories available today

Global capability for over 10 categories

No cost to participate in virtually all categories

Substantial benefits from aggregating and integrating purchasing

10

2010 Blackstone Investor Day

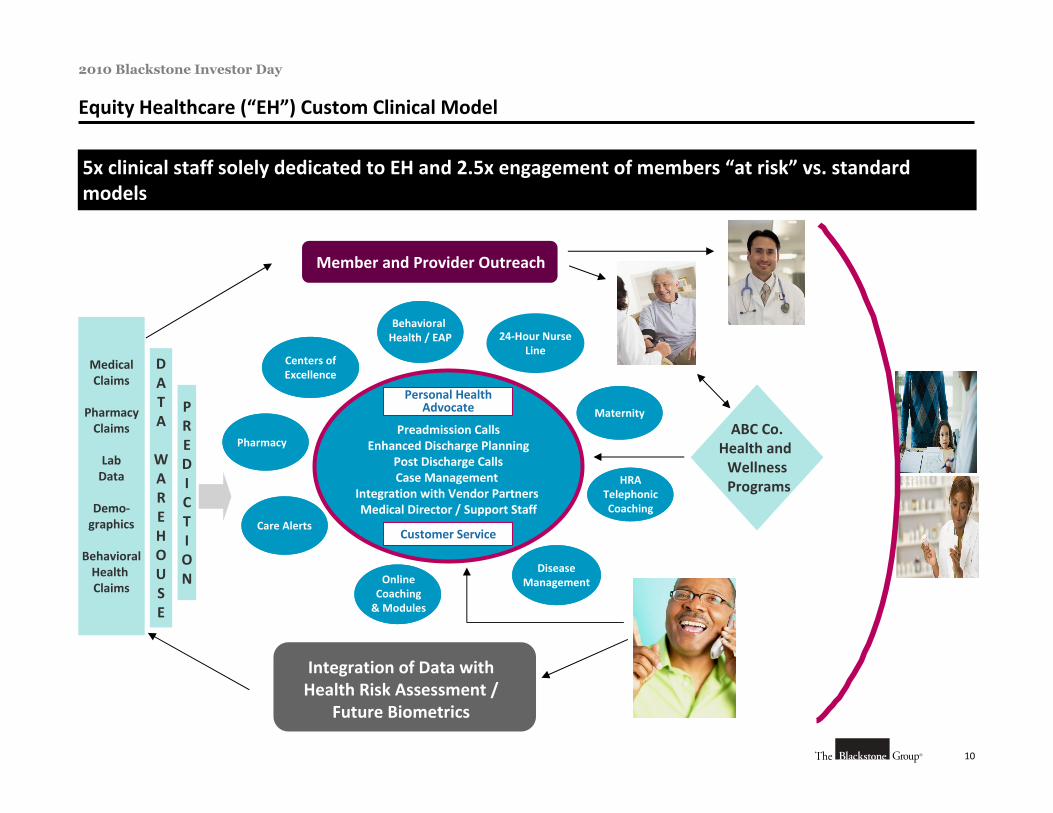

Equity Healthcare (“EH”) Custom Clinical Model

5x clinical staff solely dedicated to EH and 2.5x engagement of members “at risk” vs. standard models

Preadmission CallsEnhanced Discharge Planning

Post Discharge CallsCase Management

Integration with Vendor Partners Medical Director / Support Staff

Vendors

Personal Health Advocate

Behavioral Health / EAP

Disease Management

Centers of Excellence

Customer Service

24‐Hour Nurse Line

Online Coaching & Modules

Care Alerts

Pharmacy

Maternity

MedicalClaims

PharmacyClaims

LabData

Demo‐graphics

BehavioralHealth Claims

DATA

WAREHOUSE

Health Risk Assessment

ABC Co.Health and Wellness ProgramsHRA

Telephonic Coaching

PREDICTION

Integration of Data with Health Risk Assessment /

Future Biometrics

Member and Provider Outreach

11

2010 Blackstone Investor Day

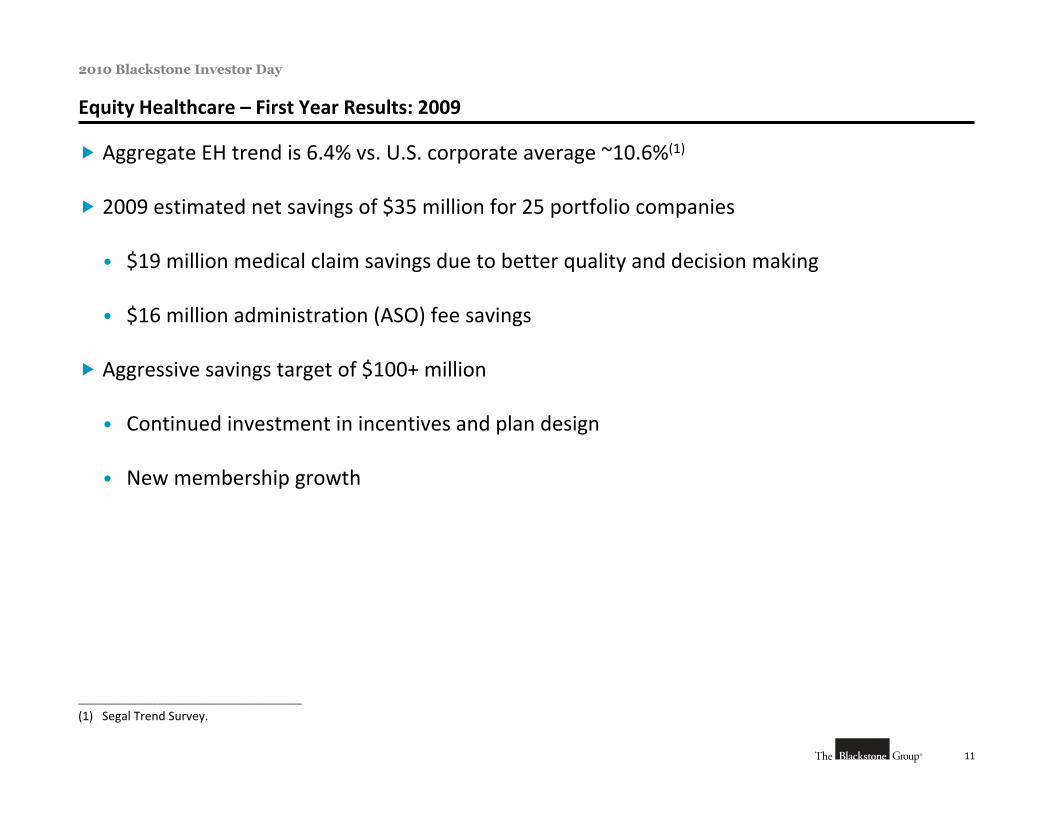

Equity Healthcare – First Year Results: 2009

Aggregate EH trend is 6.4% vs. U.S. corporate average ~10.6%(1)

2009 estimated net savings of $35 million for 25 portfolio companies

• $19 million medical claim savings due to better quality and decision making

• $16 million administration (ASO) fee savings

Aggressive savings target of $100+ million

• Continued investment in incentives and plan design

• New membership growth

________________________________________________

(1) Segal Trend Survey.

12

2010 Blackstone Investor Day

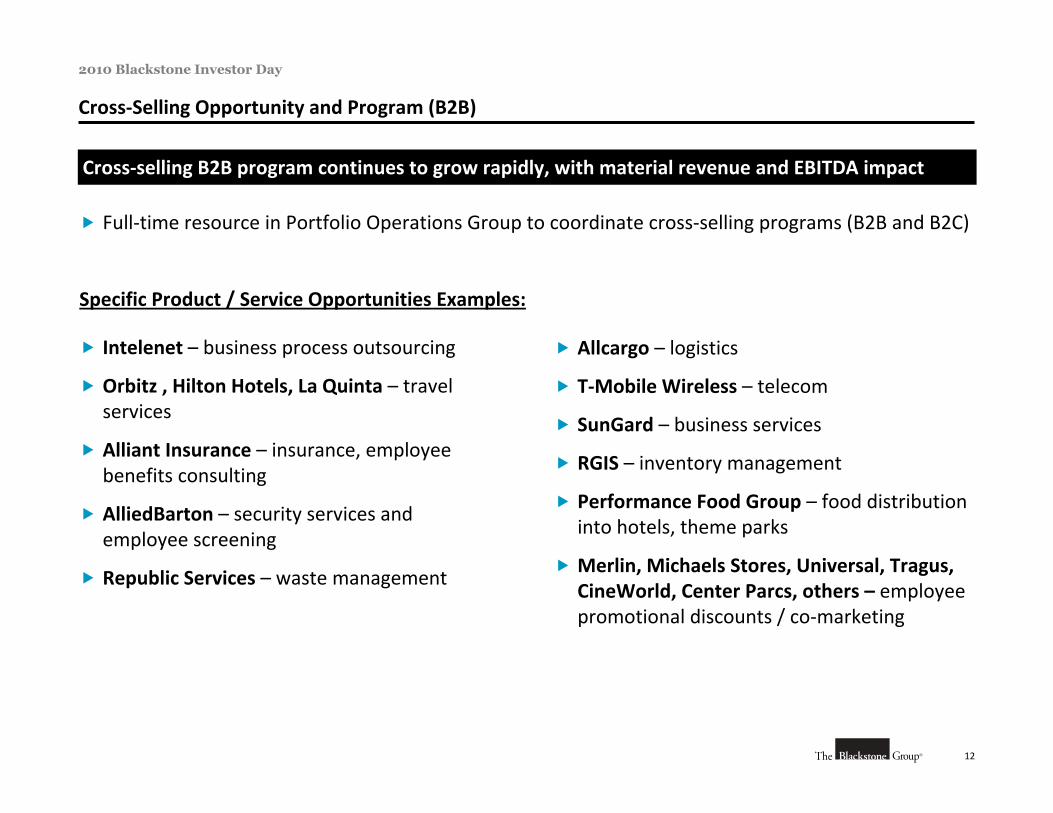

Cross‐Selling Opportunity and Program (B2B)

Cross‐selling B2B program continues to grow rapidly, with material revenue and EBITDA impact

Allcargo – logistics

T‐Mobile Wireless – telecom

SunGard – business services

RGIS – inventory management

Performance Food Group – food distribution into hotels, theme parks

Merlin, Michaels Stores, Universal, Tragus, CineWorld, Center Parcs, others – employee promotional discounts / co‐marketing

Intelenet – business process outsourcing

Orbitz , Hilton Hotels, La Quinta – travel services

Alliant Insurance – insurance, employee benefits consulting

AlliedBarton – security services and employee screening

Republic Services – waste management

Full‐time resource in Portfolio Operations Group to coordinate cross‐selling programs (B2B and B2C)

Specific Product / Service Opportunities Examples:

13

2010 Blackstone Investor Day

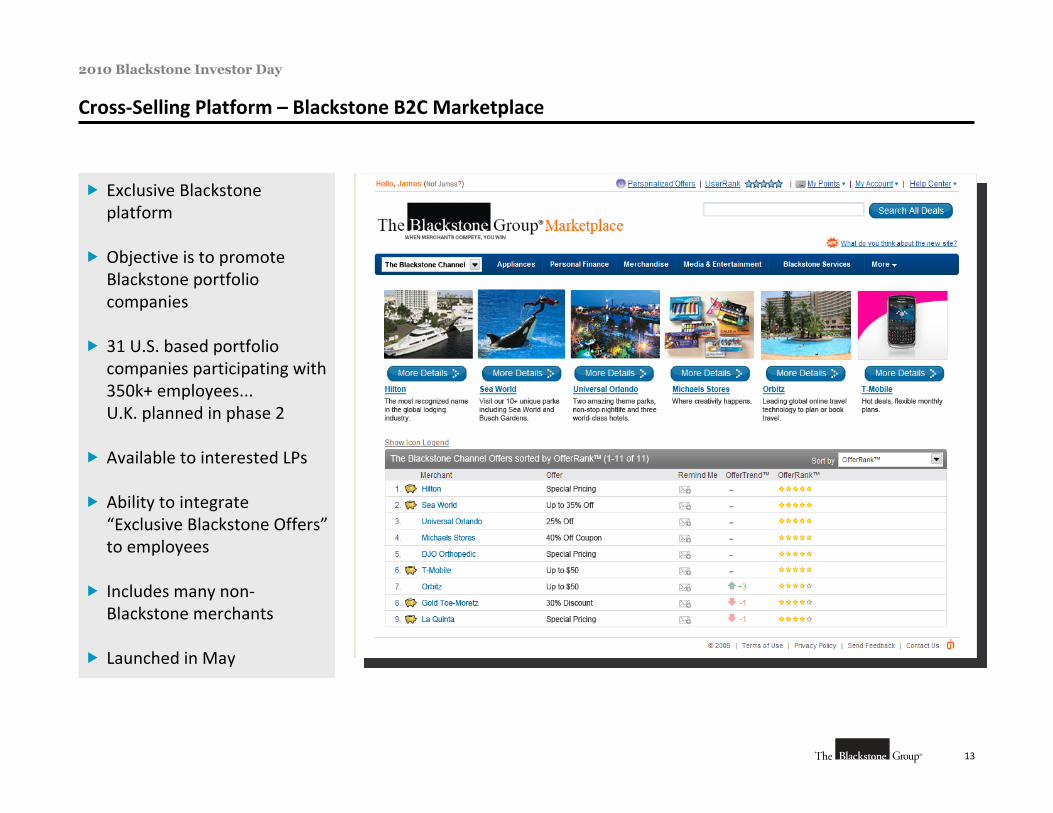

Cross‐Selling Platform – Blackstone B2C Marketplace

Exclusive Blackstone platform

Objective is to promote Blackstone portfolio companies

31 U.S. based portfolio companies participating with 350k+ employees... U.K. planned in phase 2

Available to interested LPs

Ability to integrate “Exclusive Blackstone Offers”to employees

Includes many non‐Blackstone merchants

Launched in May

14

2010 Blackstone Investor Day

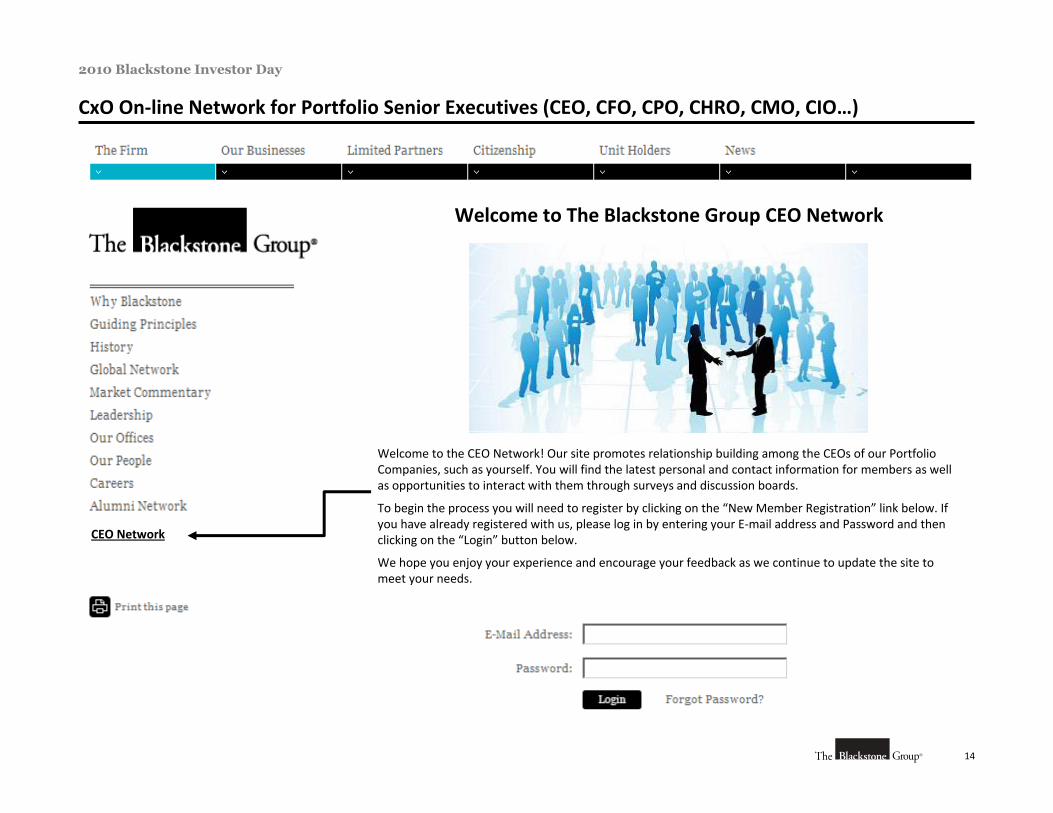

CxO On‐line Network for Portfolio Senior Executives (CEO, CFO, CPO, CHRO, CMO, CIO…)

Welcome to The Blackstone Group CEO Network

CEO Network

Welcome to the CEO Network! Our site promotes relationship building among the CEOs of our Portfolio Companies, such as yourself. You will find the latest personal and contact information for members as well as opportunities to interact with them through surveys and discussion boards.

To begin the process you will need to register by clicking on the “New Member Registration” link below. If you have already registered with us, please log in by entering your E‐mail address and Password and then clicking on the “Login” button below.

We hope you enjoy your experience and encourage your feedback as we continue to update the site to meet your needs.

15

2010 Blackstone Investor Day

Environmental Sustainability Initiative

Environmental Sustainability Task Force formed in 2008 to establish Blackstone as PE industry leader in environmental stewardship

Three primary areas of focus:

• Blackstone energy consumption and environmental impact

• Portfolio energy consumption and environmental impact (both PE and RE)

• Environmental risk assessment in all investment processes

Targeting meaningful energy and carbon reductions over the next five years

• Top‐tier of companies globally

• Sharing expertise across portfolio

• Full compliance with CRC mandate across European portfolio

Broad communication program being launched this quarter

• Documenting environmental and cost benefits for the firm and portfolio

Portfolio Operations Group plans to retain a Chief Sustainability Officer (“CSO”) to drive portfolio‐wide initiatives

16

2010 Blackstone Investor Day

Our Mission: Sustainable Competitive Advantage Delivering Long‐Term Value

Blackstone’s Portfolio Operations Group… works with our investment teams and portfolio company senior management to help acquired businesses become more productive, competitive and efficient

In the process, we build stronger enterprises, preserve and create jobs, and enable our portfolio companies to achieve lasting value for both our fund investors and successor owners

IV. Private Equity

1

2010 Blackstone Investor Day

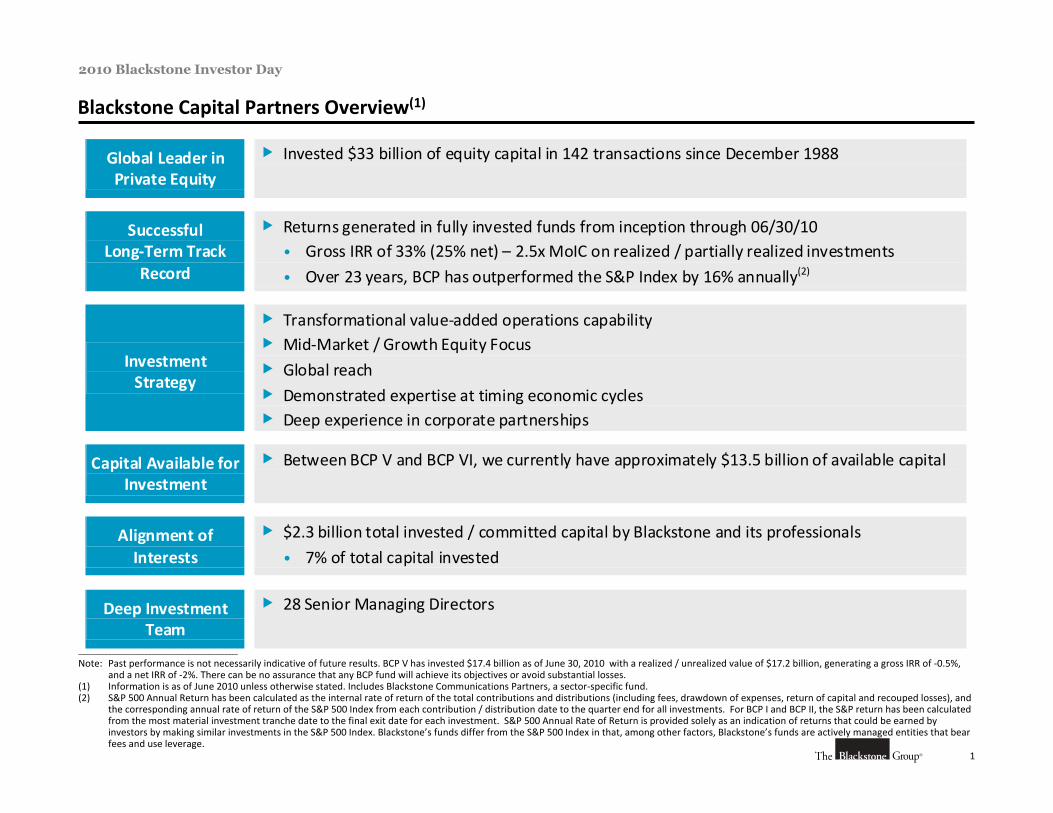

Blackstone Capital Partners Overview(1)

________________________________________________

Note: Past performance is not necessarily indicative of future results. BCP V has invested $17.4 billion as of June 30, 2010 with a realized / unrealized value of $17.2 billion, generating a gross IRR of ‐0.5%, and a net IRR of ‐2%. There can be no assurance that any BCP fund will achieve its objectives or avoid substantial losses.

(1) Information is as of June 2010 unless otherwise stated. Includes Blackstone Communications Partners, a sector‐specific fund.(2) S&P 500 Annual Return has been calculated as the internal rate of return of the total contributions and distributions (including fees, drawdown of expenses, return of capital and recouped losses), and

the corresponding annual rate of return of the S&P 500 Index from each contribution / distribution date to the quarter end for all investments. For BCP I and BCP II, the S&P return has been calculated from the most material investment tranche date to the final exit date for each investment. S&P 500 Annual Rate of Return is provided solely as an indication of returns that could be earned byinvestors by making similar investments in the S&P 500 Index. Blackstone’s funds differ from the S&P 500 Index in that, among other factors, Blackstone’s funds are actively managed entities that bear fees and use leverage.

Global Leader in Private Equity

Invested $33 billion of equity capital in 142 transactions since December 1988

Successful Long‐Term Track

Record

Returns generated in fully invested funds from inception through 06/30/10 • Gross IRR of 33% (25% net) – 2.5x MoIC on realized / partially realized investments

• Over 23 years, BCP has outperformed the S&P Index by 16% annually(2)

Investment Strategy

Transformational value‐added operations capability Mid‐Market / Growth Equity Focus Global reach Demonstrated expertise at timing economic cycles Deep experience in corporate partnerships

Capital Available for Investment

Between BCP V and BCP VI, we currently have approximately $13.5 billion of available capital

Alignment of Interests

$2.3 billion total invested / committed capital by Blackstone and its professionals

• 7% of total capital invested

Deep Investment Team

28 Senior Managing Directors

2

2010 Blackstone Investor Day

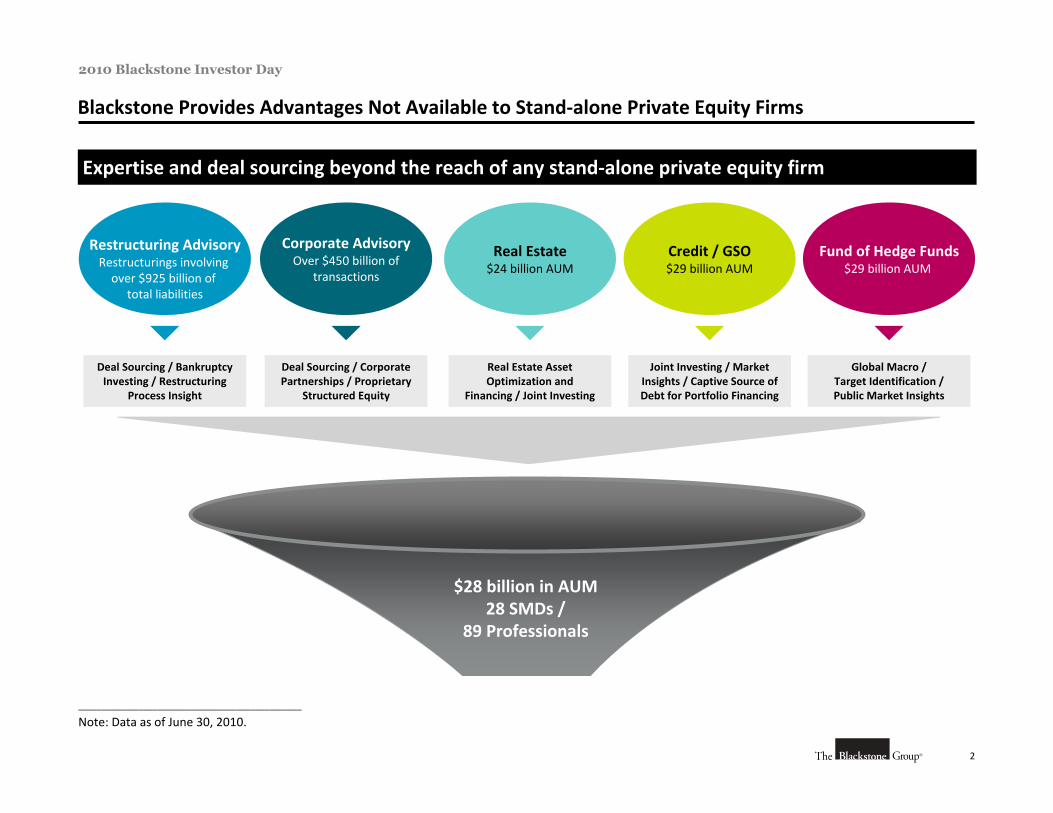

Blackstone Provides Advantages Not Available to Stand‐alone Private Equity Firms

Expertise and deal sourcing beyond the reach of any stand‐alone private equity firm

Real Estate$24 billion AUM

Restructuring AdvisoryRestructurings involving over $925 billion of

total liabilities

Corporate AdvisoryOver $450 billion of

transactions

Credit / GSO$29 billion AUM

Fund of Hedge Funds$29 billion AUM

$28 billion in AUM 28 SMDs /

89 Professionals

Global Macro /Target Identification / Public Market Insights

Joint Investing / Market Insights / Captive Source of Debt for Portfolio Financing

Real Estate Asset Optimization and

Financing / Joint Investing

Deal Sourcing / Corporate Partnerships / Proprietary

Structured Equity

Deal Sourcing / Bankruptcy Investing / Restructuring

Process Insight

________________________________________________

Note: Data as of June 30, 2010.

3

2010 Blackstone Investor Day

Distressed Investments /Rescue Financings

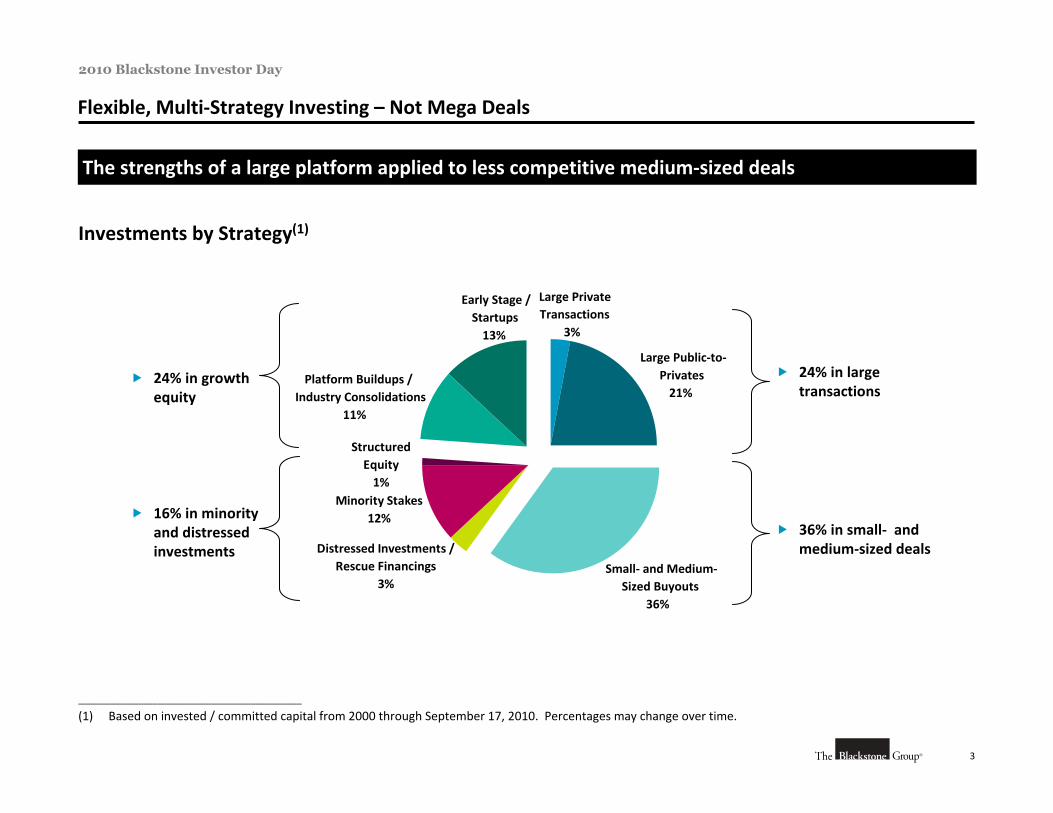

3%

Minority Stakes12%

Structured Equity1%

Flexible, Multi‐Strategy Investing – Not Mega Deals

The strengths of a large platform applied to less competitive medium‐sized deals

Investments by Strategy(1)

24% in large transactions

36% in small‐ and medium‐sized deals

24% in growth equity

16% in minority and distressed investments

________________________________________________

(1) Based on invested / committed capital from 2000 through September 17, 2010. Percentages may change over time.

Large PrivateTransactions

3%

Large Public‐to‐Privates21%

Platform Buildups /Industry Consolidations

11%

Early Stage /Startups13%

Small‐ and Medium‐Sized Buyouts

36%

4

2010 Blackstone Investor Day

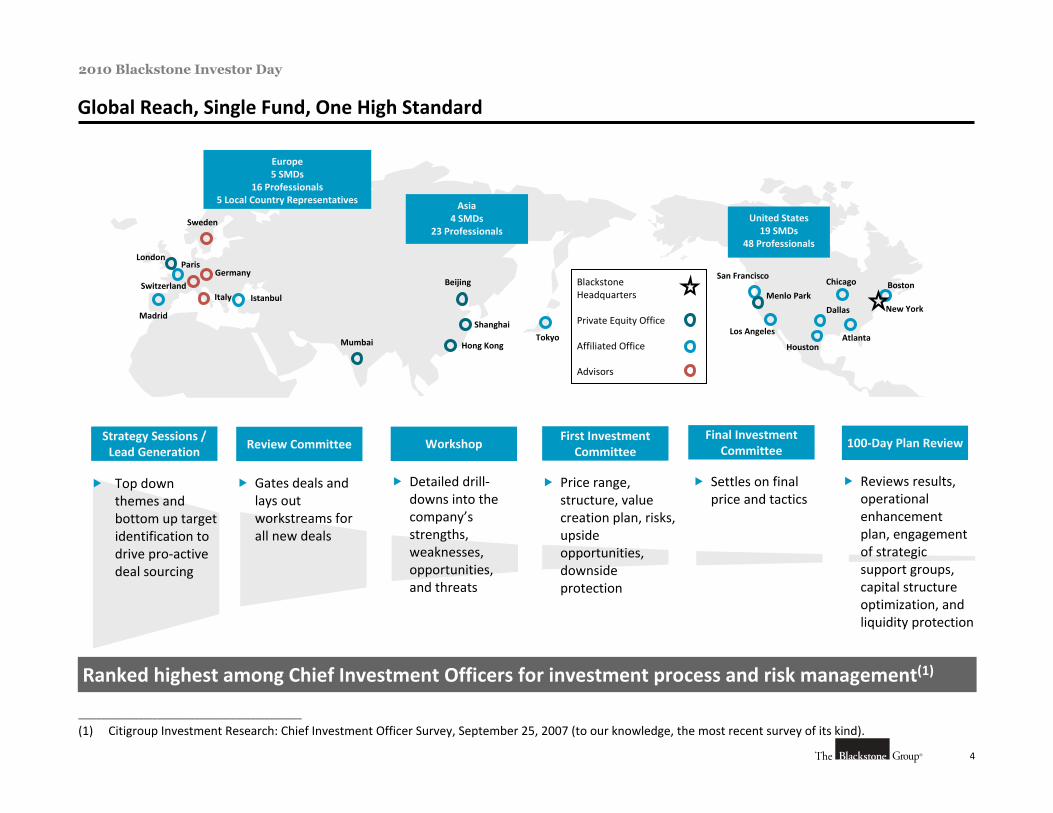

BlackstoneHeadquarters

Private Equity Office

Affiliated Office

Advisors

Global Reach, Single Fund, One High Standard

Paris

Mumbai Hong Kong

Madrid

GermanyBeijing

Asia4 SMDs

23 Professionals

Tokyo

IstanbulNew York

San Francisco

United States19 SMDs

48 Professionals

HoustonAtlanta

Boston

Los Angeles

Menlo Park

Dallas

Sweden

ItalySwitzerland

Shanghai

Chicago

Detailed drill‐downs into the company’s strengths, weaknesses, opportunities, and threats

Top down themes and bottom up target identification to drive pro‐active deal sourcing

Gates deals and lays out workstreams for all new deals

Price range, structure, value creation plan, risks, upside opportunities, downside protection

First InvestmentCommittee

Strategy Sessions /Lead Generation

Review Committee Workshop 100‐Day Plan ReviewFinal Investment

Committee

Settles on final price and tactics

Reviews results, operational enhancement plan, engagement of strategic support groups, capital structure optimization, and liquidity protection

Europe5 SMDs

16 Professionals5 Local Country Representatives

________________________________________________

(1) Citigroup Investment Research: Chief Investment Officer Survey, September 25, 2007 (to our knowledge, the most recent survey of its kind).

Ranked highest among Chief Investment Officers for investment process and risk management(1)

London

5

2010 Blackstone Investor Day

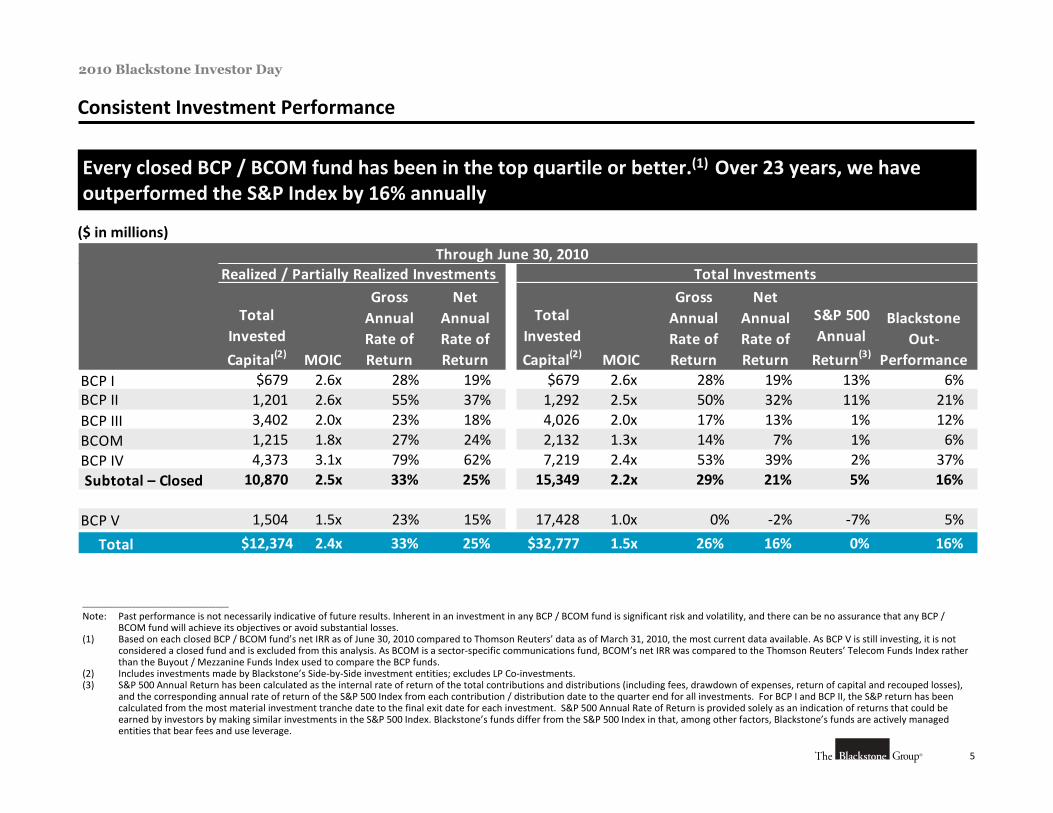

Consistent Investment Performance

____________________________________________

Note: Past performance is not necessarily indicative of future results. Inherent in an investment in any BCP / BCOM fund is significant risk and volatility, and there can be no assurance that any BCP / BCOM fund will achieve its objectives or avoid substantial losses.

(1) Based on each closed BCP / BCOM fund’s net IRR as of June 30, 2010 compared to Thomson Reuters’ data as of March 31, 2010, the most current data available. As BCP V is still investing, it is not considered a closed fund and is excluded from this analysis. As BCOM is a sector‐specific communications fund, BCOM’s net IRR was compared to the Thomson Reuters’ Telecom Funds Index rather than the Buyout / Mezzanine Funds Index used to compare the BCP funds.

(2) Includes investments made by Blackstone’s Side‐by‐Side investment entities; excludes LP Co‐investments. (3) S&P 500 Annual Return has been calculated as the internal rate of return of the total contributions and distributions (including fees, drawdown of expenses, return of capital and recouped losses),

and the corresponding annual rate of return of the S&P 500 Index from each contribution / distribution date to the quarter end for all investments. For BCP I and BCP II, the S&P return has been calculated from the most material investment tranche date to the final exit date for each investment. S&P 500 Annual Rate of Return is provided solely as an indication of returns that could be earned by investors by making similar investments in the S&P 500 Index. Blackstone’s funds differ from the S&P 500 Index in that, among other factors, Blackstone’s funds are actively managed entities that bear fees and use leverage.

Every closed BCP / BCOM fund has been in the top quartile or better.(1) Over 23 years, we have outperformed the S&P Index by 16% annually

Realized / Partially Realized Investments Total Investments

Gross Annual Rate of Return

Total Invested

Capital(2) MOIC

Gross Annual Rate of Return

S&P 500 Annual

Return(3)

BCP I $679 2.6x 28% 19% $679 2.6x 28% 19% 13% 6%BCP II 1,201 2.6x 55% 37% 1,292 2.5x 50% 32% 11% 21%BCP III 3,402 2.0x 23% 18% 4,026 2.0x 17% 13% 1% 12%BCOM 1,215 1.8x 27% 24% 2,132 1.3x 14% 7% 1% 6%BCP IV 4,373 3.1x 79% 62% 7,219 2.4x 53% 39% 2% 37% Subtotal – Closed 10,870 2.5x 33% 25% 15,349 2.2x 29% 21% 5% 16%

BCP V 1,504 1.5x 23% 15% 17,428 1.0x 0% ‐2% ‐7% 5%

Total $12,374 2.4x 33% 25% $32,777 1.5x 26% 16% 0% 16%

Blackstone Out‐

Performance

Through June 30, 2010

Net Annual Rate of Return

Net AnnualRate ofReturnMOIC

Total Invested

Capital(2)

($ in millions)

6

2010 Blackstone Investor Day

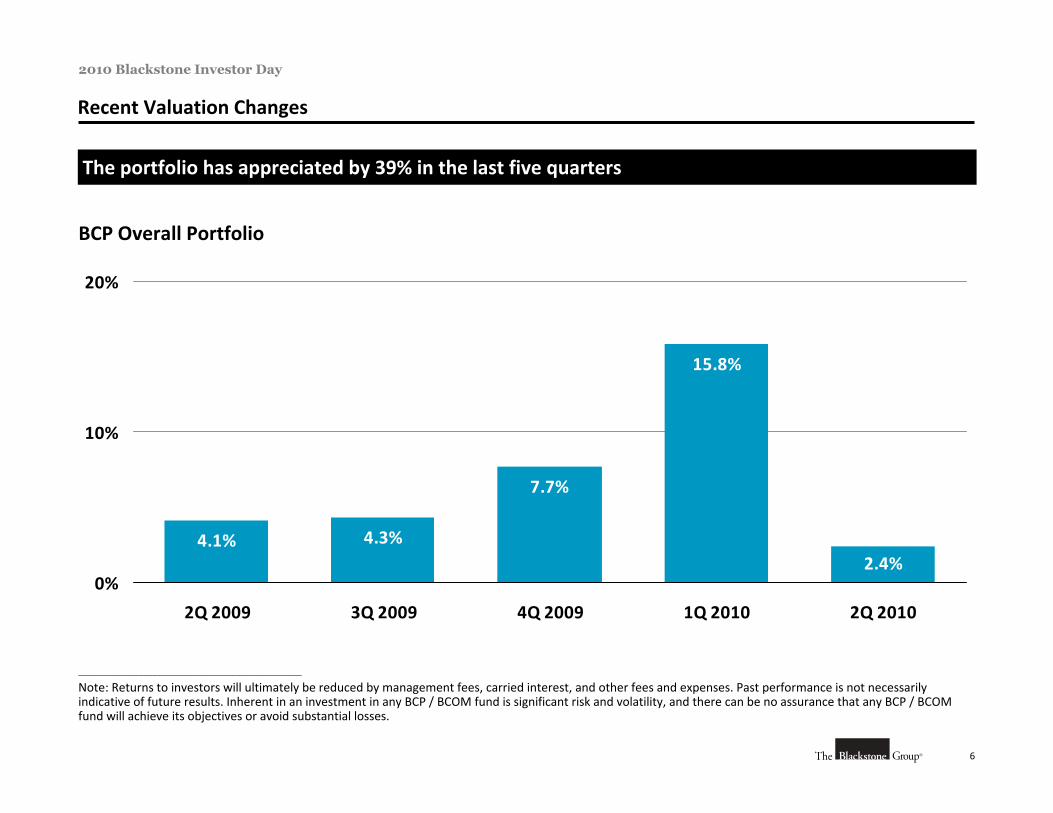

Recent Valuation Changes

The portfolio has appreciated by 39% in the last five quarters

BCP Overall Portfolio

7.7%

15.8%

2.4%4.1% 4.3%

0%

10%

20%

2Q 2009 3Q 2009 4Q 2009 1Q 2010 2Q 2010

________________________________________________

Note: Returns to investors will ultimately be reduced by management fees, carried interest, and other fees and expenses. Past performance is not necessarily indicative of future results. Inherent in an investment in any BCP / BCOM fund is significant risk and volatility, and there can be no assurance that any BCP / BCOM fund will achieve its objectives or avoid substantial losses.

7

2010 Blackstone Investor Day

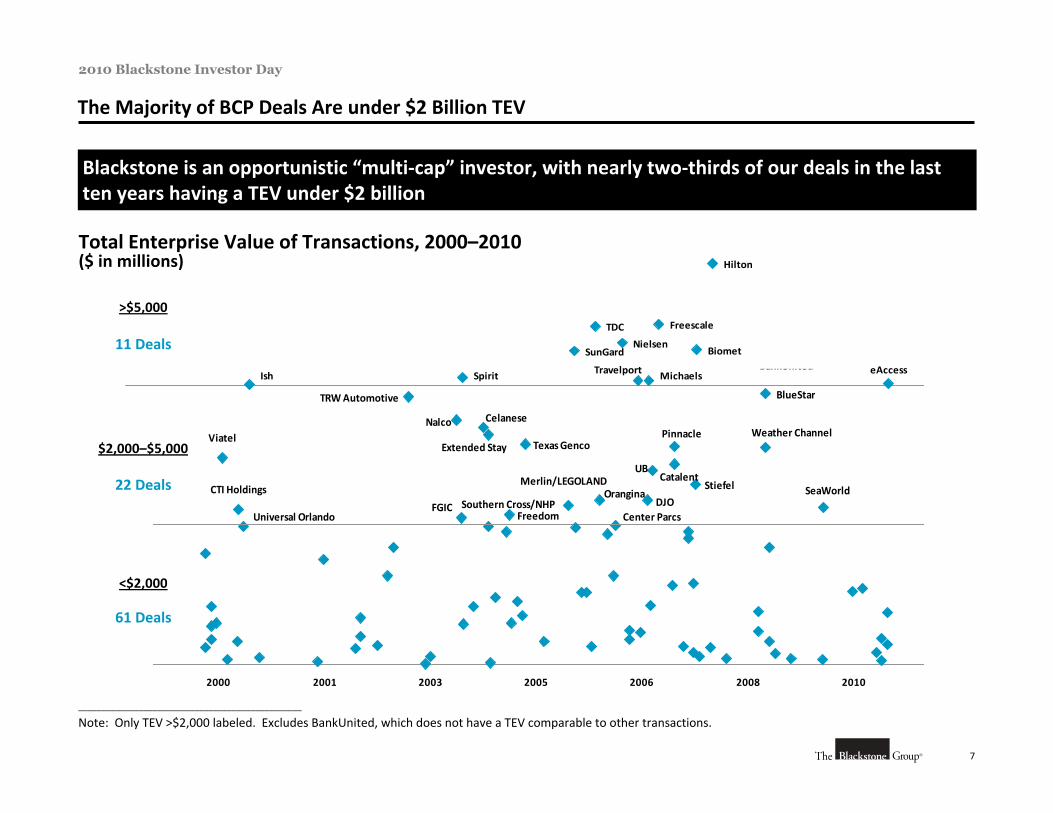

The Majority of BCP Deals Are under $2 Billion TEV

Blackstone is an opportunistic “multi‐cap” investor, with nearly two‐thirds of our deals in the last ten years having a TEV under $2 billion

________________________________________________

Note: Only TEV >$2,000 labeled. Excludes BankUnited, which does not have a TEV comparable to other transactions.

Total Enterprise Value of Transactions, 2000–2010($ in millions)

Viatel

CTI Holdings

Universal Orlando

TRW Automotive

Nalco

FGIC

Celanese

Freedom

Extended Stay

Southern Cross/NHP

Texas Genco

Merlin/LEGOLANDOrangina

Center ParcsDJO

UBCatalent

Pinnacle

Stiefel

Weather Channel

BlueStar

SeaWorld

2000 2001 2003 2005 2006 2008 2010 2011

>$5,000

$2,000–$5,000

<$2,000

11 Deals

22 Deals

61 Deals

Ish Spirit

SunGard

TDC

Nielsen

Travelport Michaels

Freescale

Biomet

Hilton

BankUnited eAccess

8

2010 Blackstone Investor Day

Advantages of Scale

Brand name matters

Dedicated 50+ person Portfolio Operations Group focused on creating value

High proportion of exclusive deals

Preferred access to debt financing in capital constrained markets

Process advantages from selling agents, including “last looks”

Broad network of relationships to find deals

Corporate partnerships

Global perspective – even on domestic companies

Deep financial and operating domain expertise in each major sector

Strategic alliances – China, Korea, Brazil

9

2010 Blackstone Investor Day

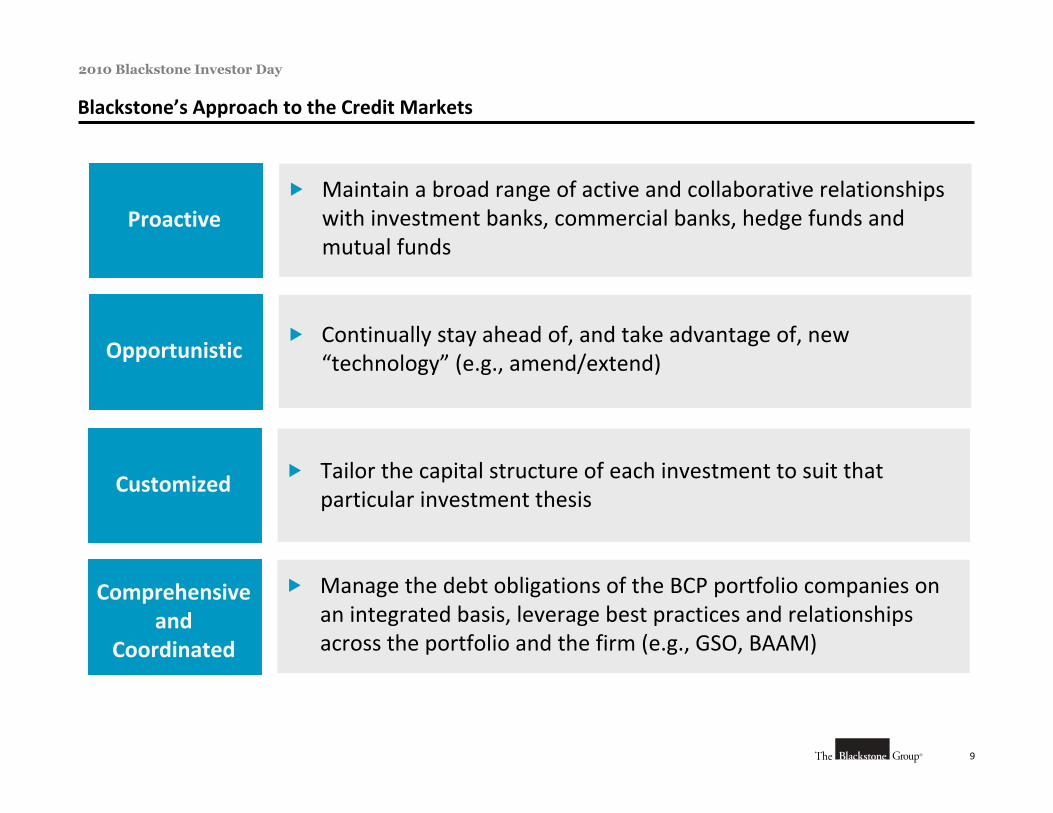

Blackstone’s Approach to the Credit Markets

Proactive Maintain a broad range of active and collaborative relationships

with investment banks, commercial banks, hedge funds and mutual funds

Opportunistic Continually stay ahead of, and take advantage of, new

“technology” (e.g., amend/extend)

Customized Tailor the capital structure of each investment to suit that particular investment thesis

Comprehensive and

Coordinated

Manage the debt obligations of the BCP portfolio companies on an integrated basis, leverage best practices and relationships across the portfolio and the firm (e.g., GSO, BAAM)

10

2010 Blackstone Investor Day

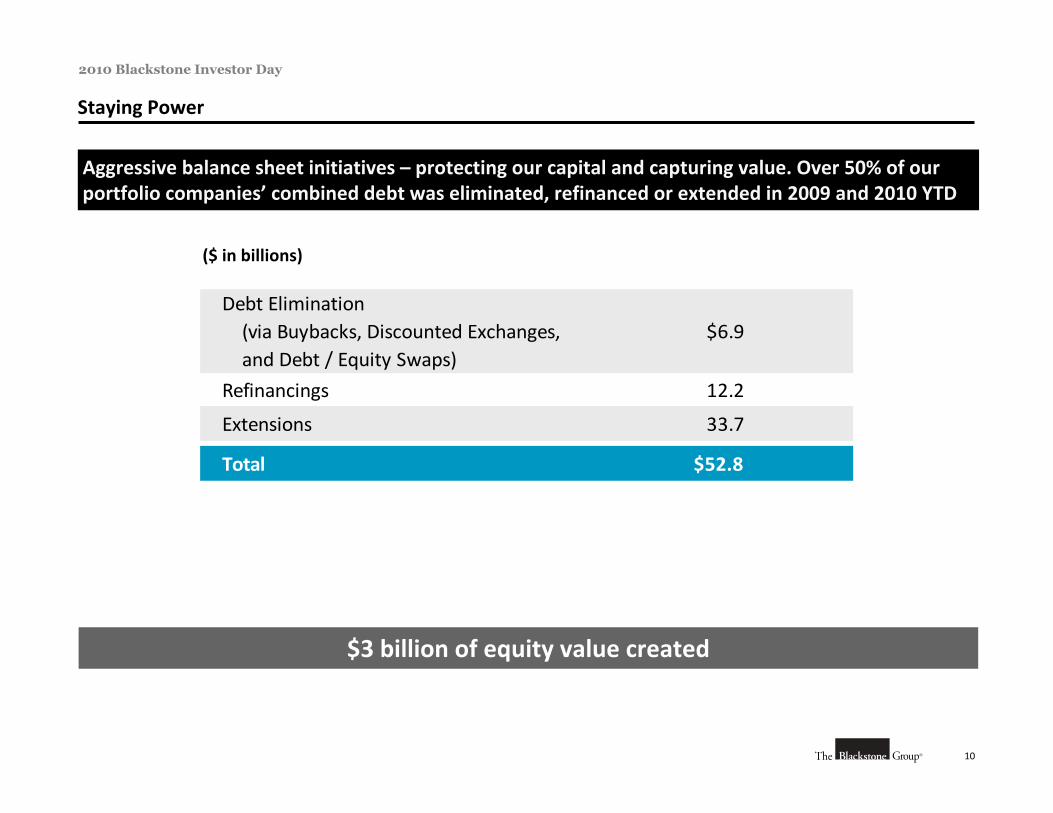

Staying Power

Aggressive balance sheet initiatives – protecting our capital and capturing value. Over 50% of our portfolio companies’ combined debt was eliminated, refinanced or extended in 2009 and 2010 YTD

($ in billions)

Debt Elimination (via Buybacks, Discounted Exchanges, and Debt / Equity Swaps)

$6.9

Refinancings 12.2

Extensions 33.7

Total $52.8

$3 billion of equity value created

11

2010 Blackstone Investor Day

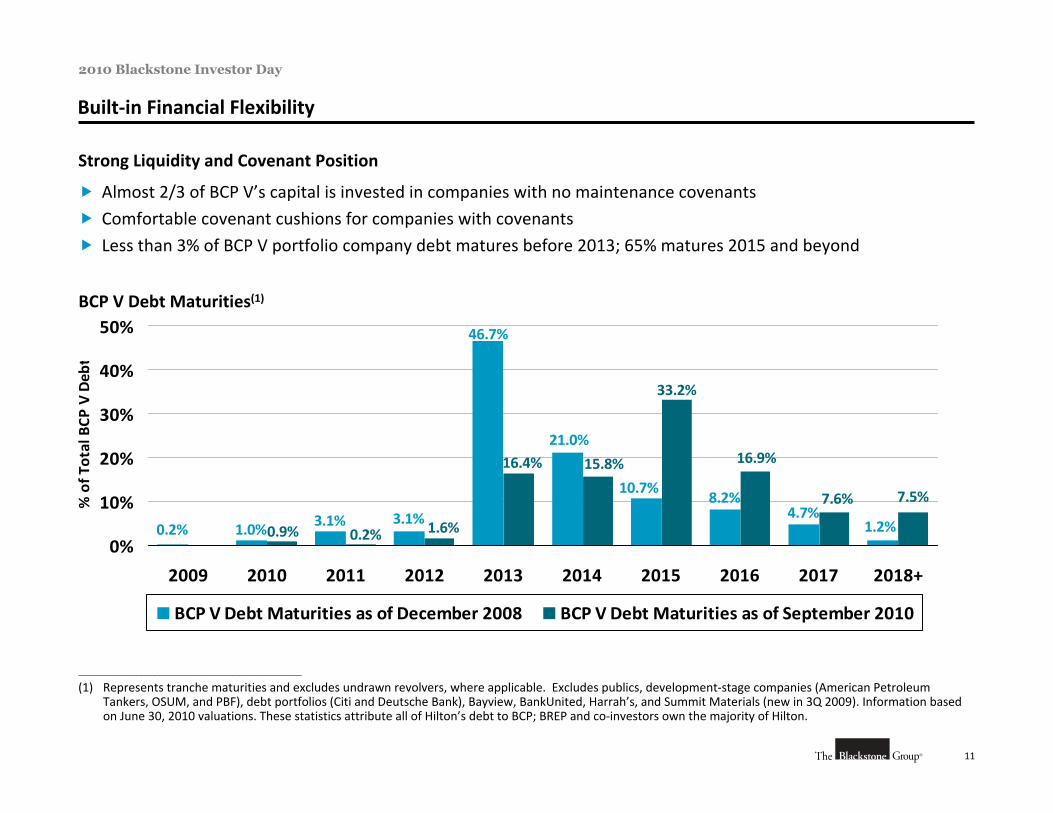

Built‐in Financial Flexibility

________________________________________________

(1) Represents tranche maturities and excludes undrawn revolvers, where applicable. Excludes publics, development‐stage companies (American Petroleum Tankers, OSUM, and PBF), debt portfolios (Citi and Deutsche Bank), Bayview, BankUnited, Harrah’s, and Summit Materials (new in 3Q 2009). Information based on June 30, 2010 valuations. These statistics attribute all of Hilton’s debt to BCP; BREP and co‐investors own the majority of Hilton.

Strong Liquidity and Covenant Position

Almost 2/3 of BCP V’s capital is invested in companies with no maintenance covenants

Comfortable covenant cushions for companies with covenants

Less than 3% of BCP V portfolio company debt matures before 2013; 65% matures 2015 and beyond

BCP V Debt Maturities(1)

7.5%

1.2%4.7%

8.2%10.7%

21.0%

46.7%

3.1%1.0%0.2% 3.1%

7.6%

16.9%

33.2%

15.8%16.4%

1.6%0.2%0.9%0%

10%

20%

30%

40%

50%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018+

% of T

otal BCP

V Deb

t

BCP V Debt Maturities as of December 2008 BCP V Debt Maturities as of September 2010

12

2010 Blackstone Investor Day

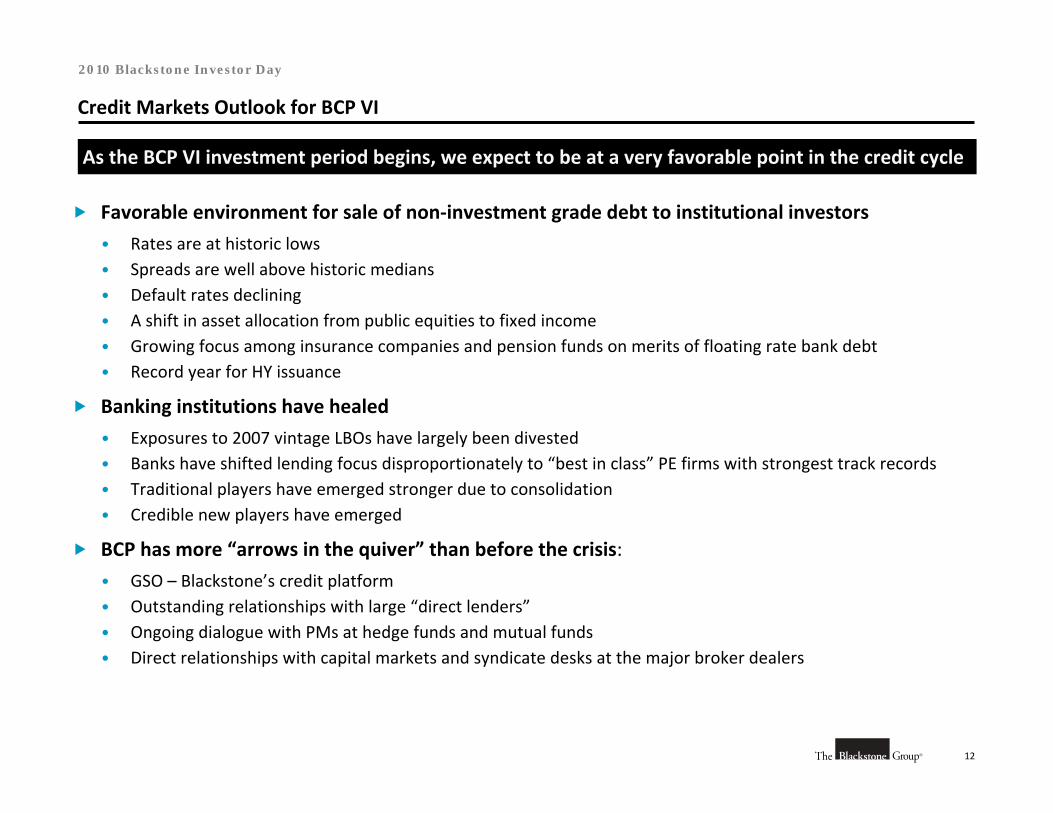

Credit Markets Outlook for BCP VI

As the BCP VI investment period begins, we expect to be at a very favorable point in the credit cycle

Favorable environment for sale of non‐investment grade debt to institutional investors

• Rates are at historic lows• Spreads are well above historic medians• Default rates declining• A shift in asset allocation from public equities to fixed income• Growing focus among insurance companies and pension funds on merits of floating rate bank debt• Record year for HY issuance

Banking institutions have healed

• Exposures to 2007 vintage LBOs have largely been divested• Banks have shifted lending focus disproportionately to “best in class” PE firms with strongest track records• Traditional players have emerged stronger due to consolidation• Credible new players have emerged

BCP has more “arrows in the quiver” than before the crisis:

• GSO – Blackstone’s credit platform• Outstanding relationships with large “direct lenders”• Ongoing dialogue with PMs at hedge funds and mutual funds• Direct relationships with capital markets and syndicate desks at the major broker dealers

13

2010 Blackstone Investor Day

BCP V Outlook

We expect BCP V to generate a 2x MOIC(1)

• Average revenue and EBITDA growth rates of 5.1% and 8.3%, respectively

• Average margin improvement of 80 bps

Solid balance sheets with comfortable covenant and maturity profiles

91% of BCP V capital invested / committed

• Expect to close investment period in the next few months

________________________________________________

(1) While Blackstone currently believes that the assumptions on which this projection is based are reasonable under current circumstances, there is no guarantee that the conditions on which such assumptions are based will materialize or otherwise be applicable to these funds. There can be no assurance that any fund managed by Blackstone will be profitable or avoid substantial losses. Above projections do not include any assumptions regarding investment time horizon or the rate of return on funds managed by Blackstone. Ultimate returns to investors will be reduced by management fees, fund expenses and carried interest.”

14

2010 Blackstone Investor Day

Overview of Current Environment

Blackstone has a track record of generating compelling returns across all cycles and is well positioned to take advantage of this economic environment

Market Environment

We are cautious on economic growth prospects

An abundance of private equity in the market makes on‐the‐run deals very difficult

Debt markets have rebounded and support attractive dealmaking…

• …but credit spreads are higher and covenants are tighter

Equity valuations are relatively attractive

• But cyclicals ran sooner in this cycle than previously

• We assume valuations will not return to ’06/’07 levels

Opportunity

Post‐recession vintages have historically provided the highest returns

BCP has significant dry powder and a global opportunity set

Focus on exclusive opportunities driven byindustry / regional depth

Recent Investments

• Summit Materials – Aggregates build‐up

• PBF Refining – depressed refining opportunities

• Sea World – furthering our theme park franchise

• Dili – modernizing distribution in China

15

2010 Blackstone Investor Day

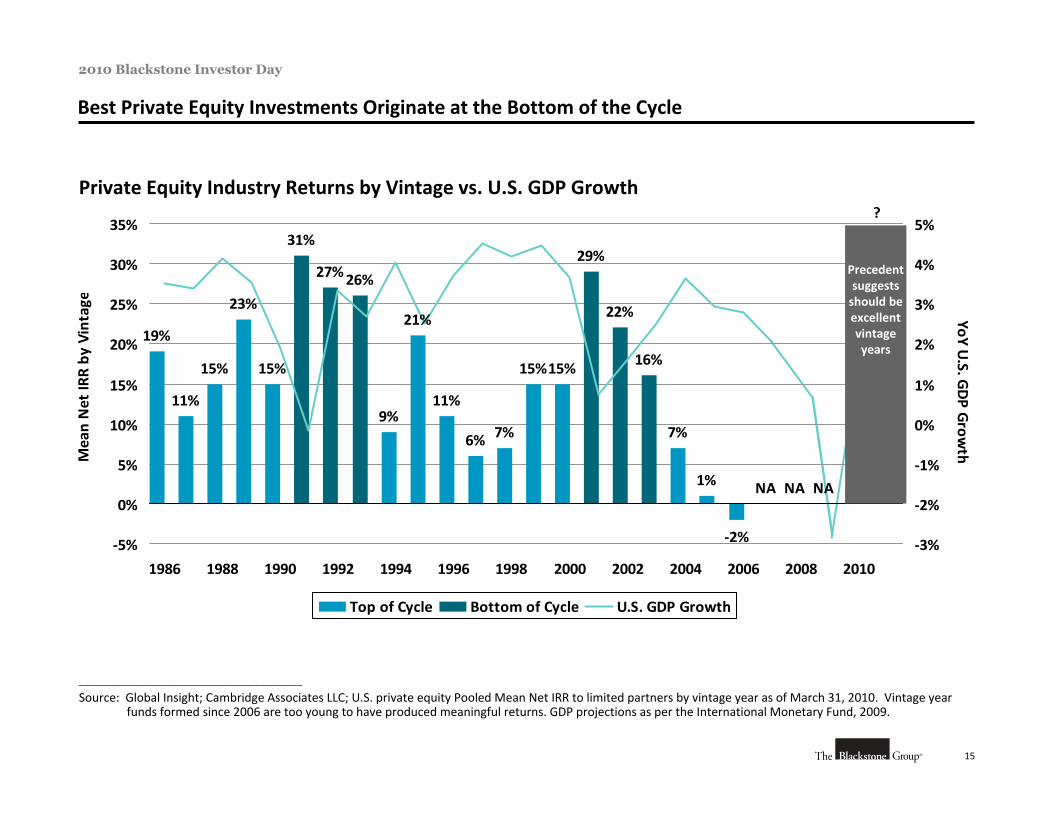

Best Private Equity Investments Originate at the Bottom of the Cycle

________________________________________________

Source: Global Insight; Cambridge Associates LLC; U.S. private equity Pooled Mean Net IRR to limited partners by vintage year as of March 31, 2010. Vintage year funds formed since 2006 are too young to have produced meaningful returns. GDP projections as per the International Monetary Fund, 2009.

Private Equity Industry Returns by Vintage vs. U.S. GDP Growth

19%

11%

15%

23%

15%

31%

27%26%

9%

21%

11%

6% 7%

15%15%

29%

22%

16%

7%

1%

‐2%

– –NA NA NA

‐5%

0%

5%

10%

15%

20%

25%

30%

35%

1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Mean Net IR

R by

Vintage

‐3%

‐2%

‐1%

0%

1%

2%

3%

4%

5%

YoY U.S. G

DP G

rowth

Top of Cycle Bottom of Cycle U.S. GDP Growth

Precedent suggests should be excellent vintage years

?

16

2010 Blackstone Investor Day

Fundraising and New Initiatives

BCP VI

• Some subscription documents still outstanding, however we anticipate a final fund size of over $13.5 billion

• Given the current and expected investments / commitments for BCP V, we expect to close the BCP V investment period in the next few months

Clean Technology – Growth equity in disruptive technologies

• Estimated fund size of $500 million

• Expect final close in 1Q 2011

RMB Fund – China growth strategies

• Estimated fund size of 5 billion RMB (approximately $740 million)

• First close expected in 4Q 2010

17

2010 Blackstone Investor Day

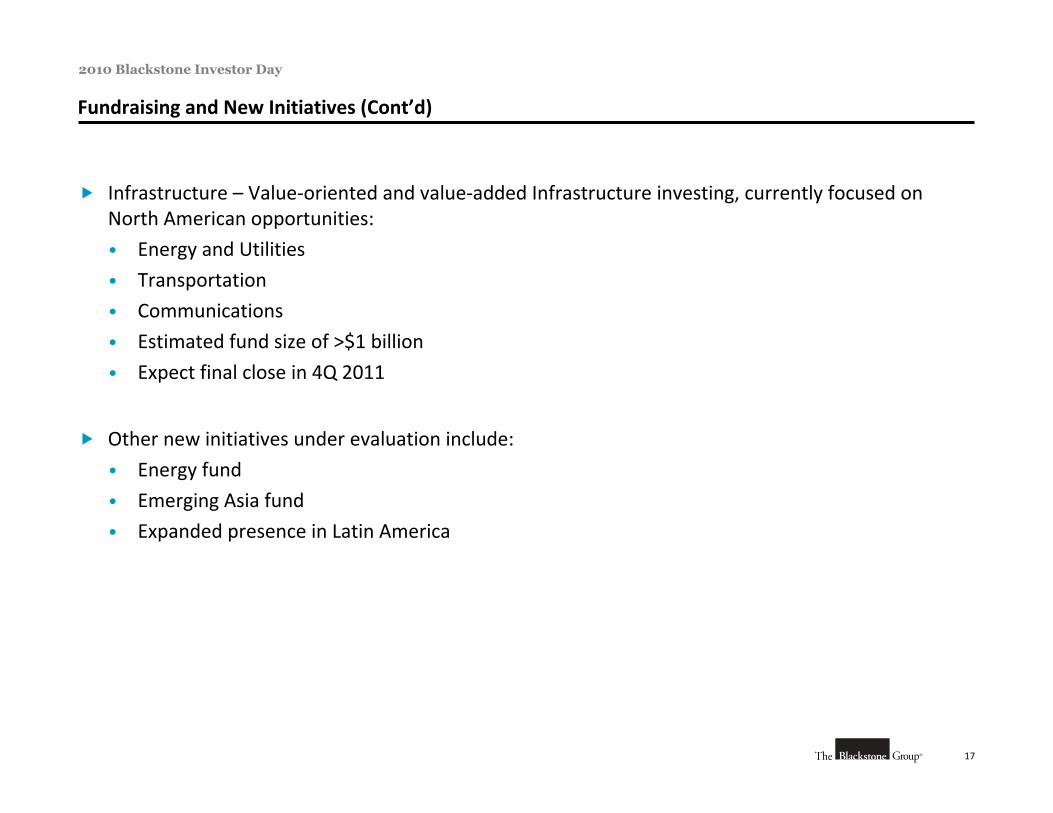

Fundraising and New Initiatives (Cont’d)

Infrastructure – Value‐oriented and value‐added Infrastructure investing, currently focused on North American opportunities:

• Energy and Utilities

• Transportation

• Communications

• Estimated fund size of >$1 billion

• Expect final close in 4Q 2011

Other new initiatives under evaluation include:

• Energy fund

• Emerging Asia fund

• Expanded presence in Latin America

V. Blackstone Advisory Partners

A. BAP Overview

2

2010 Blackstone Investor Day

A. BAP Overview

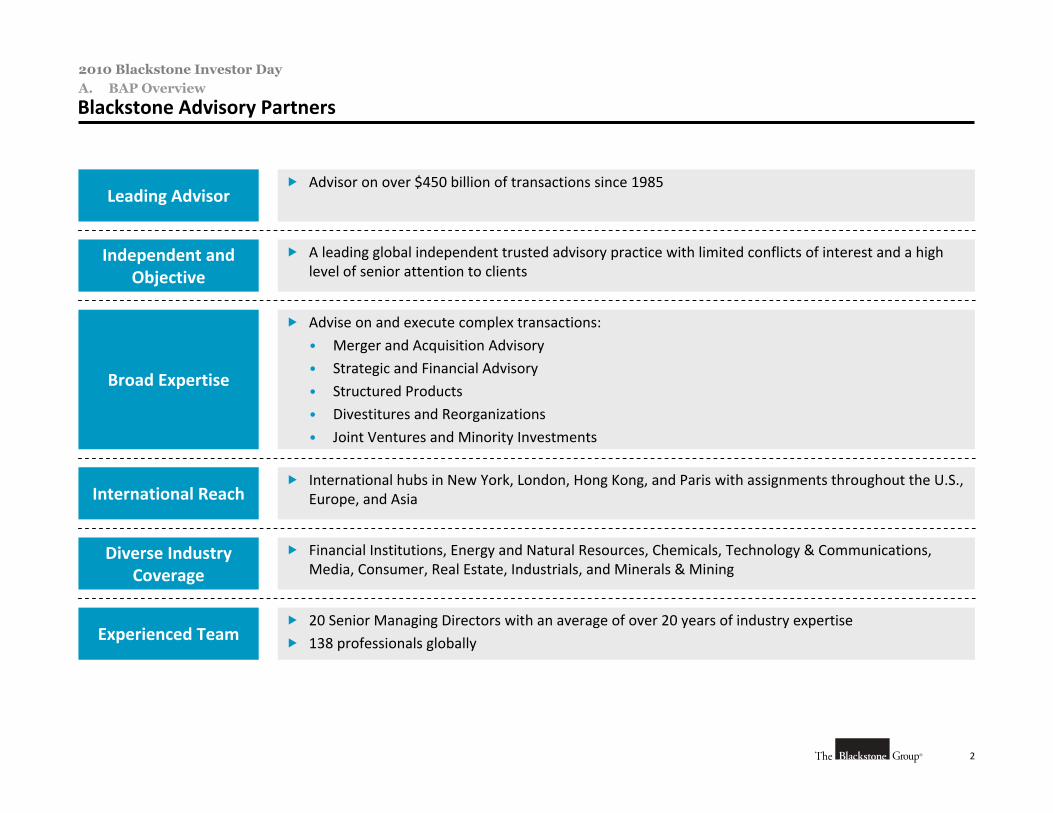

Blackstone Advisory Partners

Leading Advisor Advisor on over $450 billion of transactions since 1985

Independent and Objective

A leading global independent trusted advisory practice with limited conflicts of interest and a high level of senior attention to clients

Broad Expertise

Advise on and execute complex transactions:

• Merger and Acquisition Advisory

• Strategic and Financial Advisory

• Structured Products

• Divestitures and Reorganizations

• Joint Ventures and Minority Investments

International Reach International hubs in New York, London, Hong Kong, and Paris with assignments throughout the U.S.,

Europe, and Asia

Diverse Industry Coverage

Financial Institutions, Energy and Natural Resources, Chemicals, Technology & Communications, Media, Consumer, Real Estate, Industrials, and Minerals & Mining

Experienced Team 20 Senior Managing Directors with an average of over 20 years of industry expertise

138 professionals globally

3

2010 Blackstone Investor Day

A. BAP Overview

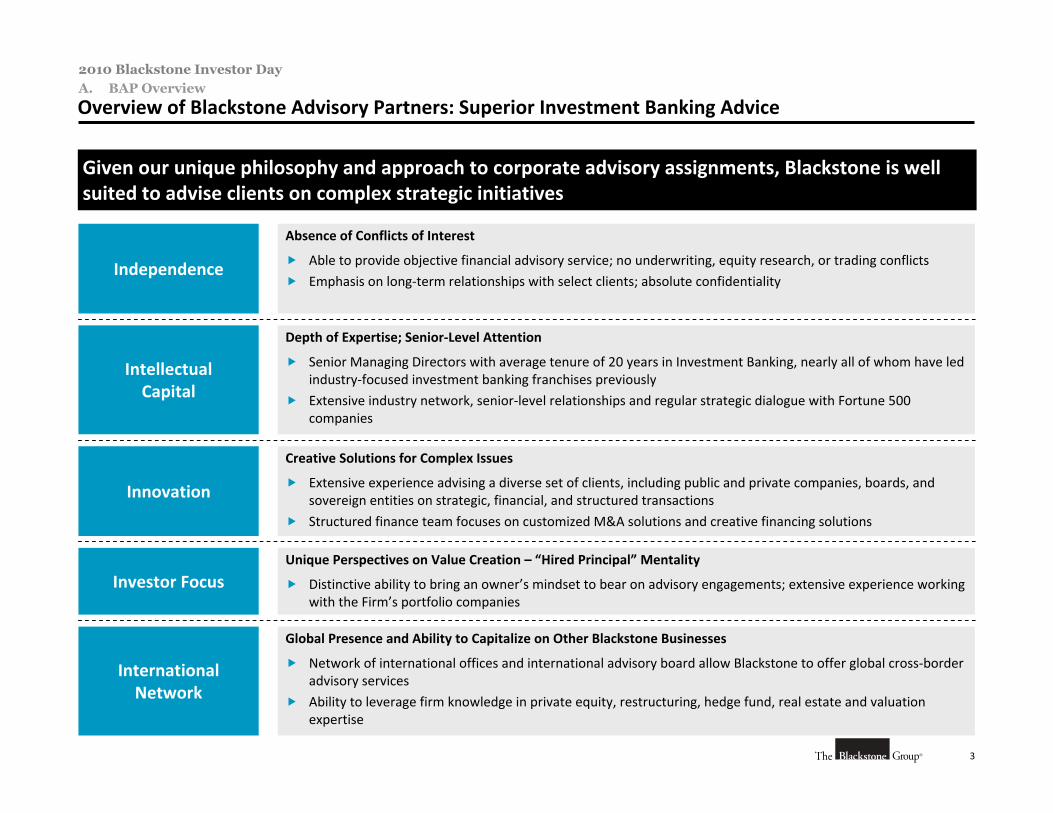

Overview of Blackstone Advisory Partners: Superior Investment Banking Advice

Independence

Absence of Conflicts of Interest

Able to provide objective financial advisory service; no underwriting, equity research, or trading conflicts

Emphasis on long‐term relationships with select clients; absolute confidentiality

Intellectual Capital

Depth of Expertise; Senior‐Level Attention

Senior Managing Directors with average tenure of 20 years in Investment Banking, nearly all of whom have led industry‐focused investment banking franchises previously

Extensive industry network, senior‐level relationships and regular strategic dialogue with Fortune 500 companies

Innovation

Creative Solutions for Complex Issues

Extensive experience advising a diverse set of clients, including public and private companies, boards, and sovereign entities on strategic, financial, and structured transactions

Structured finance team focuses on customized M&A solutions and creative financing solutions

Investor FocusUnique Perspectives on Value Creation – “Hired Principal” Mentality

Distinctive ability to bring an owner’s mindset to bear on advisory engagements; extensive experience working with the Firm’s portfolio companies

International Network

Global Presence and Ability to Capitalize on Other Blackstone Businesses

Network of international offices and international advisory board allow Blackstone to offer global cross‐border advisory services

Ability to leverage firm knowledge in private equity, restructuring, hedge fund, real estate and valuation expertise

Given our unique philosophy and approach to corporate advisory assignments, Blackstone is well suited to advise clients on complex strategic initiatives

4

2010 Blackstone Investor Day

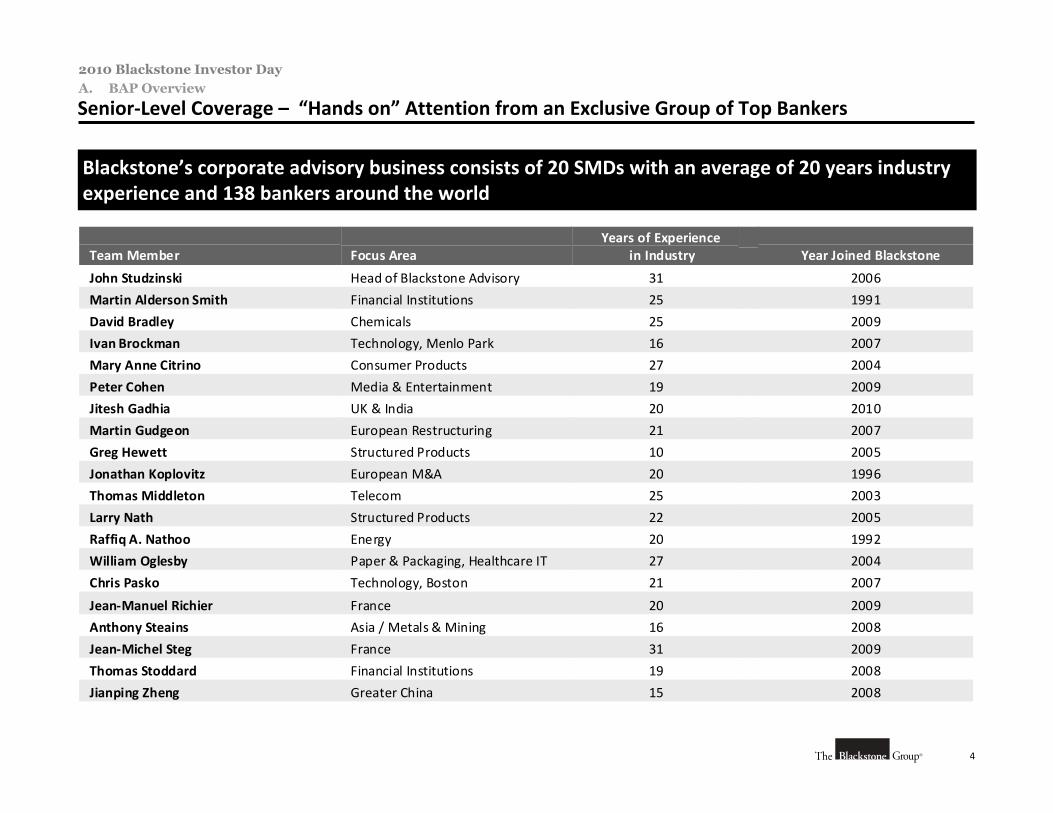

Senior‐Level Coverage – “Hands on” Attention from an Exclusive Group of Top Bankers

Blackstone’s corporate advisory business consists of 20 SMDs with an average of 20 years industry experience and 138 bankers around the world

A. BAP Overview

Team Member Focus Area

Years of Experience in Industry Year Joined Blackstone

John Studzinski Head of Blackstone Advisory 31 2006

Martin Alderson Smith Financial Institutions 25 1991

David Bradley Chemicals 25 2009

Ivan Brockman Technology, Menlo Park 16 2007

Mary Anne Citrino Consumer Products 27 2004

Peter Cohen Media & Entertainment 19 2009

Jitesh Gadhia UK & India 20 2010

Martin Gudgeon European Restructuring 21 2007

Greg Hewett Structured Products 10 2005

Jonathan Koplovitz European M&A 20 1996

Thomas Middleton Telecom 25 2003

Larry Nath Structured Products 22 2005

Raffiq A. Nathoo Energy 20 1992

William Oglesby Paper & Packaging, Healthcare IT 27 2004

Chris Pasko Technology, Boston 21 2007

Jean‐Manuel Richier France 20 2009

Anthony Steains Asia / Metals & Mining 16 2008

Jean‐Michel Steg France 31 2009

Thomas Stoddard Financial Institutions 19 2008

Jianping Zheng Greater China 15 2008

5

2010 Blackstone Investor Day

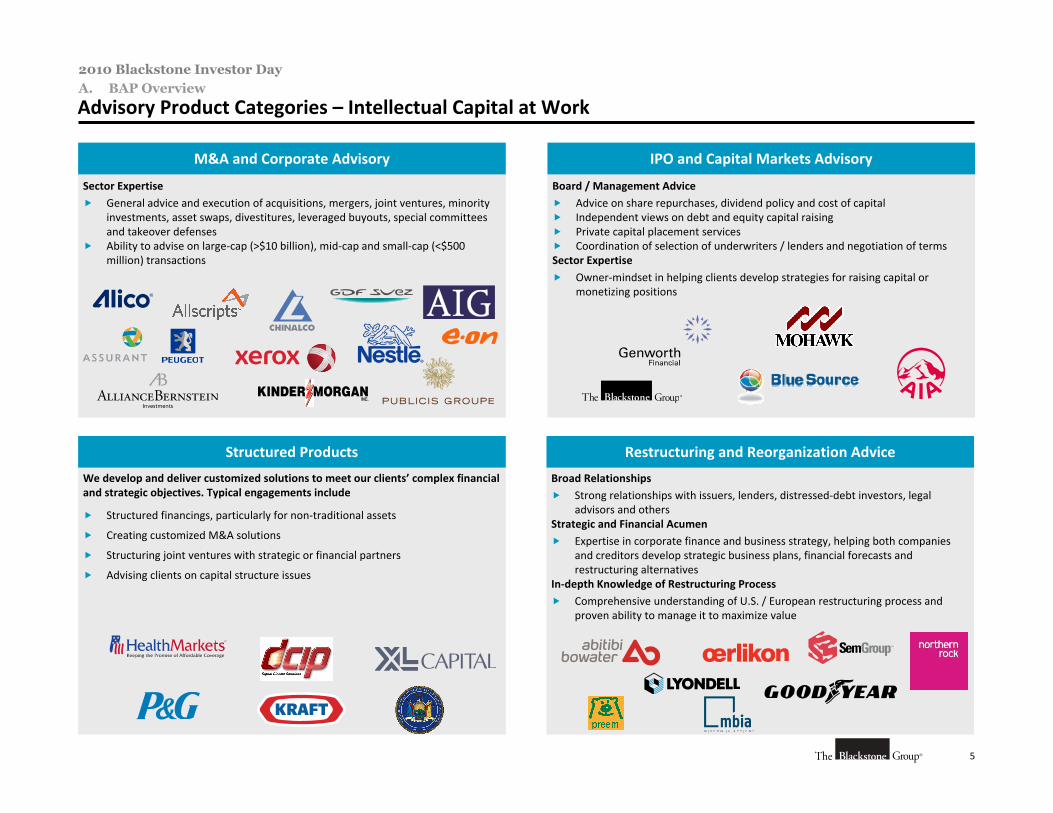

Advisory Product Categories – Intellectual Capital at Work

Sector Expertise General advice and execution of acquisitions, mergers, joint ventures, minority

investments, asset swaps, divestitures, leveraged buyouts, special committees and takeover defenses

Ability to advise on large‐cap (>$10 billion), mid‐cap and small‐cap (<$500 million) transactions

M&A and Corporate Advisory

Board / Management Advice Advice on share repurchases, dividend policy and cost of capital Independent views on debt and equity capital raising Private capital placement services Coordination of selection of underwriters / lenders and negotiation of termsSector Expertise

Owner‐mindset in helping clients develop strategies for raising capital or monetizing positions

IPO and Capital Markets Advisory

Broad Relationships Strong relationships with issuers, lenders, distressed‐debt investors, legal

advisors and othersStrategic and Financial Acumen Expertise in corporate finance and business strategy, helping both companies

and creditors develop strategic business plans, financial forecasts and restructuring alternatives

In‐depth Knowledge of Restructuring Process Comprehensive understanding of U.S. / European restructuring process and

proven ability to manage it to maximize value

Restructuring and Reorganization Advice

A. BAP Overview

We develop and deliver customized solutions to meet our clients’ complex financial and strategic objectives. Typical engagements include

Structured financings, particularly for non‐traditional assets

Creating customized M&A solutions

Structuring joint ventures with strategic or financial partners

Advising clients on capital structure issues

Structured Products

6

2010 Blackstone Investor Day

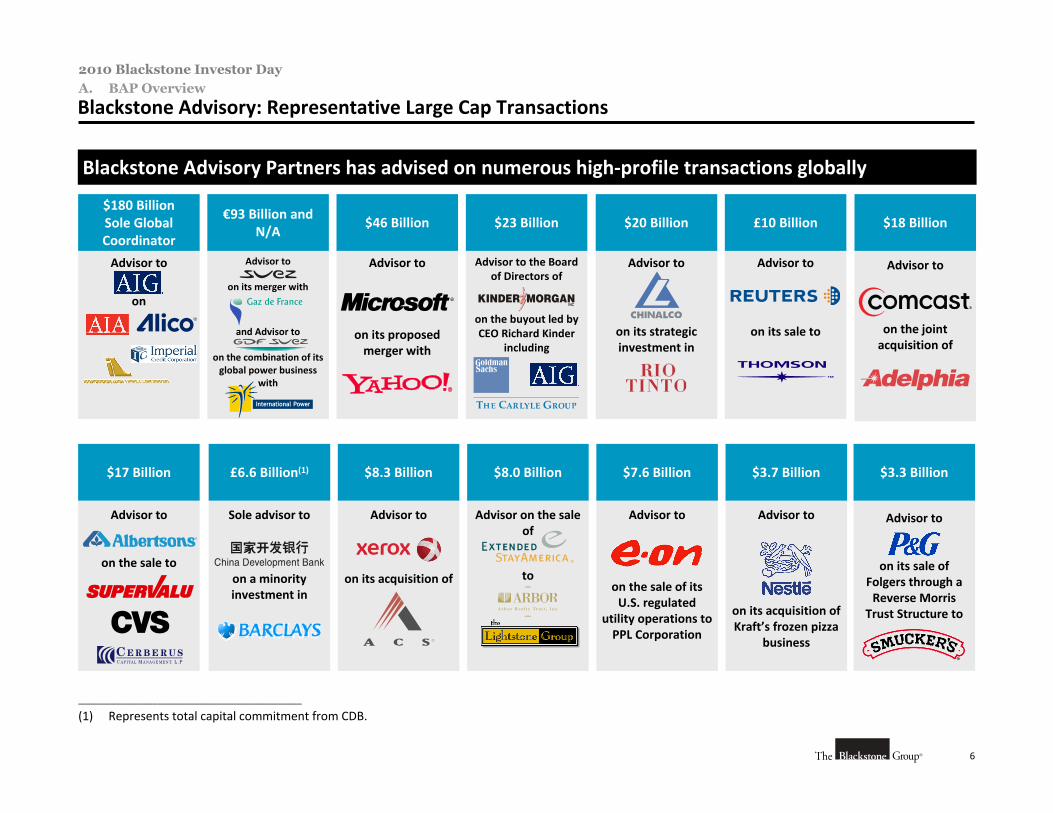

Blackstone Advisory: Representative Large Cap Transactions

Blackstone Advisory Partners has advised on numerous high‐profile transactions globally

________________________________________________

(1) Represents total capital commitment from CDB.

Advisor to

on

$180 BillionSole Global Coordinator

Advisor to

on its acquisition of

$8.3 Billion

Advisor to

on its acquisition ofKraft’s frozen pizza

business

$3.7 Billion

Advisor to

on the sale of its U.S. regulated

utility operations to PPL Corporation

$7.6 Billion

Advisor to

on its merger with

and Advisor to

on the combination of its global power business

with

€93 Billion and N/A

Sole advisor to

on a minority investment in

£6.6 Billion(1)

Advisor to

on its sale to

£10 Billion

Advisor to

on its proposed merger with

$46 Billion

Advisor to the Board of Directors of

on the buyout led by CEO Richard Kinder

including

$23 Billion

Advisor to

on the joint acquisition of

$18 Billion

Advisor to

on the sale to

$17 Billion

Advisor on the sale of

to

$8.0 Billion

Advisor to

on its strategic investment in

$20 Billion

A. BAP Overview

Advisor to

on its sale of Folgers through a Reverse Morris

Trust Structure to

$3.3 Billion

B. BAP Highlights

8

2010 Blackstone Investor Day

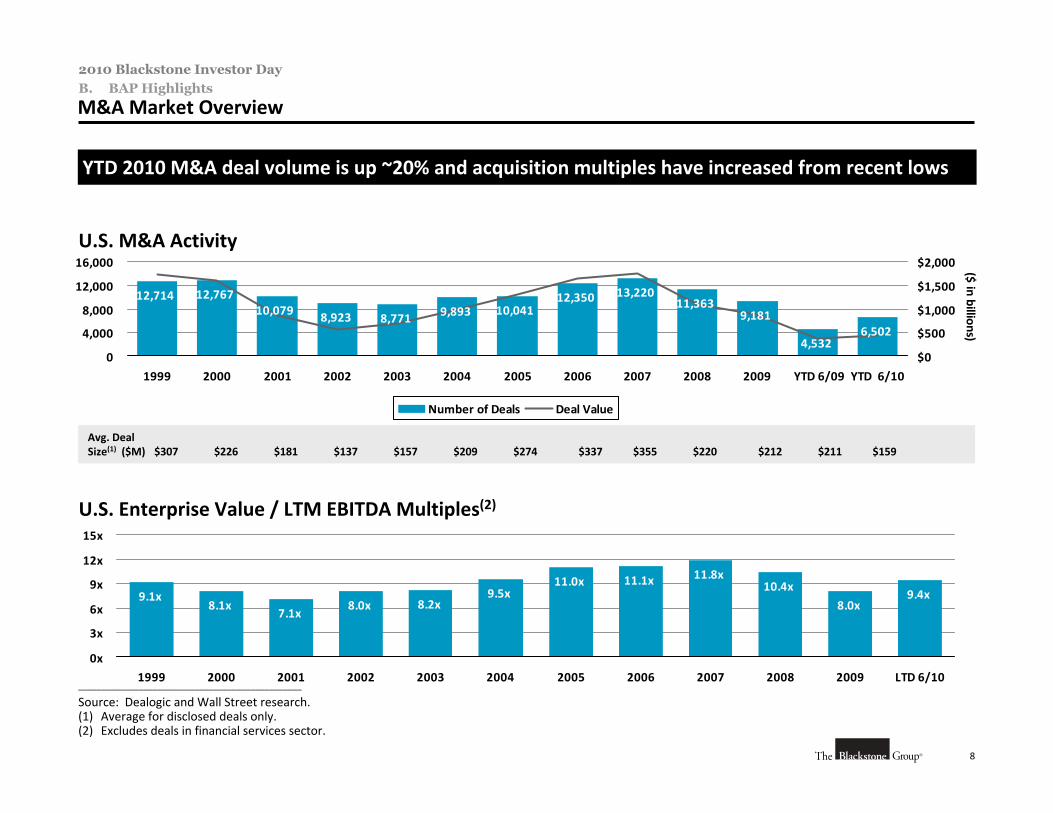

M&A Market OverviewB. BAP Highlights

________________________________________________

Source: Dealogic and Wall Street research.(1) Average for disclosed deals only.(2) Excludes deals in financial services sector.

U.S. M&A Activity

10,079 8,923 8,771 9,893 10,04112,350 13,220

11,3639,181

4,5326,502

12,76712,714

0

4,000

8,000

12,000

16,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 YTD 6/09 YTD 6/10

$0

$500

$1,000

$1,500

$2,000 ($ in billions)

Number of Deals Deal Value

U.S. Enterprise Value / LTM EBITDA Multiples(2)

7.1x8.0x 8.2x

9.5x11.0x 11.1x 11.8x

10.4x

8.0x9.4x

8.1x9.1x

0x

3x

6x

9x

12x

15x

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 LTD 6/10

YTD 2010 M&A deal volume is up ~20% and acquisition multiples have increased from recent lows

Avg. DealSize(1) ($M) $307 $226 $181 $137 $157 $209 $274 $337 $355 $220 $212 $211 $159

9

2010 Blackstone Investor Day

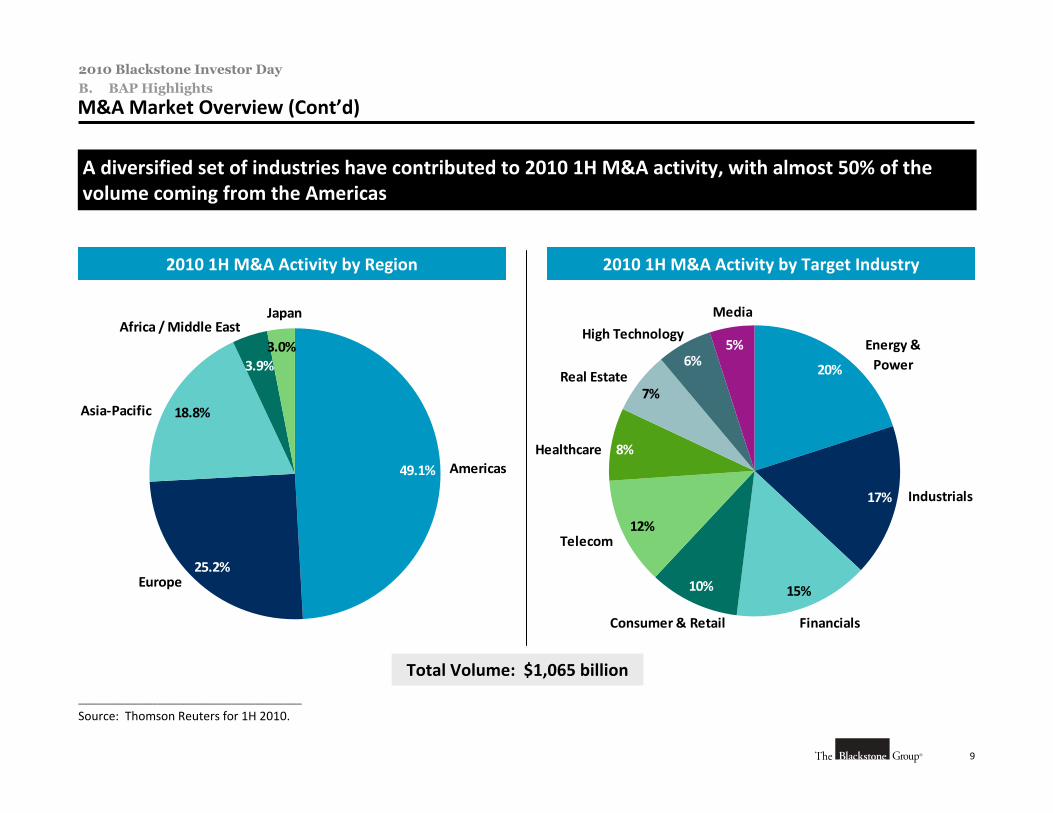

M&A Market Overview (Cont’d)

2010 1H M&A Activity by Region 2010 1H M&A Activity by Target Industry

3.9%3.0%

18.8%

25.2%

49.1% Americas

Europe

Asia‐Pacific

Africa / Middle EastJapan

5%

20%

17%

15%

12%

7%

6%

8%

10%

Energy & Power

Industrials

FinancialsConsumer & Retail

Telecom

Healthcare

Real Estate

High Technology

Media

Total Volume: $1,065 billion

________________________________________________

Source: Thomson Reuters for 1H 2010.

B. BAP Highlights

A diversified set of industries have contributed to 2010 1H M&A activity, with almost 50% of the volume coming from the Americas

10

2010 Blackstone Investor Day

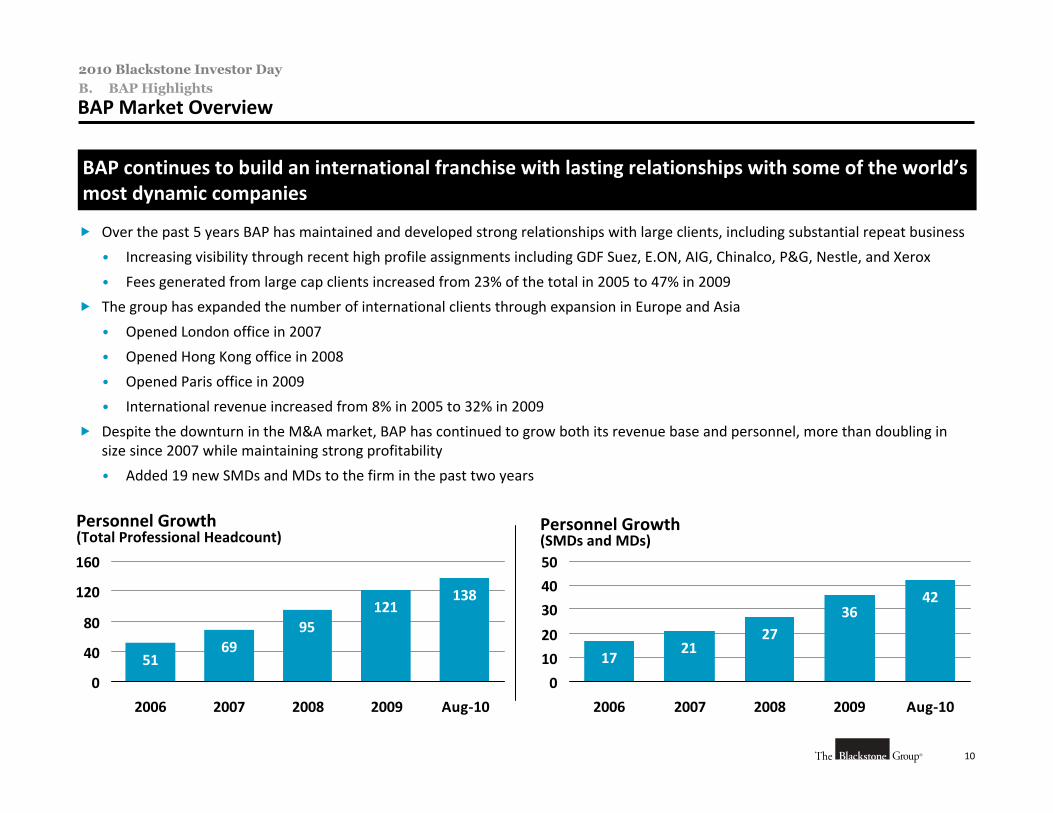

BAP Market OverviewB. BAP Highlights

Personnel Growth (Total Professional Headcount)

138121

9569

51

0

40

80

120

160

2006 2007 2008 2009 Aug‐10

Personnel Growth(SMDs and MDs)

BAP continues to build an international franchise with lasting relationships with some of the world’s most dynamic companies

Over the past 5 years BAP has maintained and developed strong relationships with large clients, including substantial repeat business

• Increasing visibility through recent high profile assignments including GDF Suez, E.ON, AIG, Chinalco, P&G, Nestle, and Xerox

• Fees generated from large cap clients increased from 23% of the total in 2005 to 47% in 2009

The group has expanded the number of international clients through expansion in Europe and Asia

• Opened London office in 2007

• Opened Hong Kong office in 2008

• Opened Paris office in 2009

• International revenue increased from 8% in 2005 to 32% in 2009

Despite the downturn in the M&A market, BAP has continued to grow both its revenue base and personnel, more than doubling in size since 2007 while maintaining strong profitability

• Added 19 new SMDs and MDs to the firm in the past two years

4236

2721

17

0

10

20

30

40

50

2006 2007 2008 2009 Aug‐10

11

2010 Blackstone Investor Day

BAP Market Overview (Cont’d)B. BAP Highlights

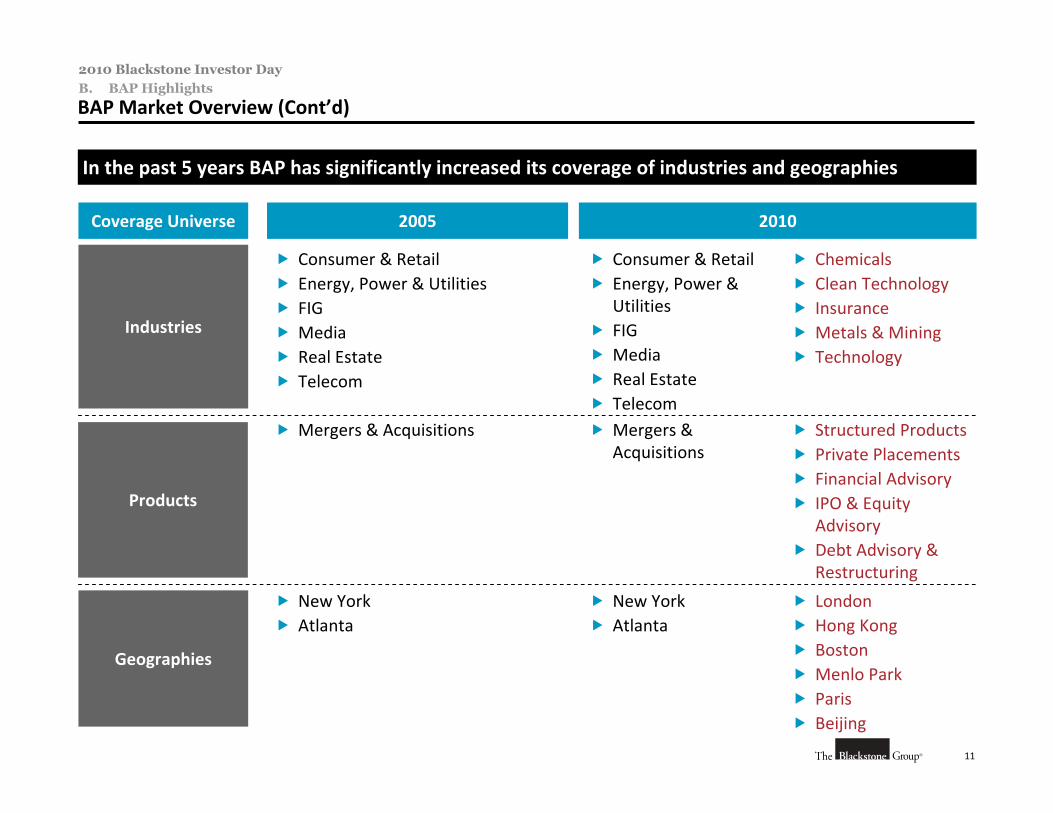

In the past 5 years BAP has significantly increased its coverage of industries and geographies

2005 2010Coverage Universe

Industries

Products

Geographies

Consumer & Retail Energy, Power & Utilities FIG Media Real Estate Telecom

Consumer & Retail Energy, Power &

Utilities FIG Media Real Estate Telecom

Chemicals Clean Technology Insurance Metals & Mining Technology

Mergers & Acquisitions Mergers & Acquisitions

Structured Products Private Placements Financial Advisory IPO & Equity

Advisory Debt Advisory &

Restructuring

New York Atlanta

New York Atlanta

London Hong Kong Boston Menlo Park Paris Beijing

12

2010 Blackstone Investor Day

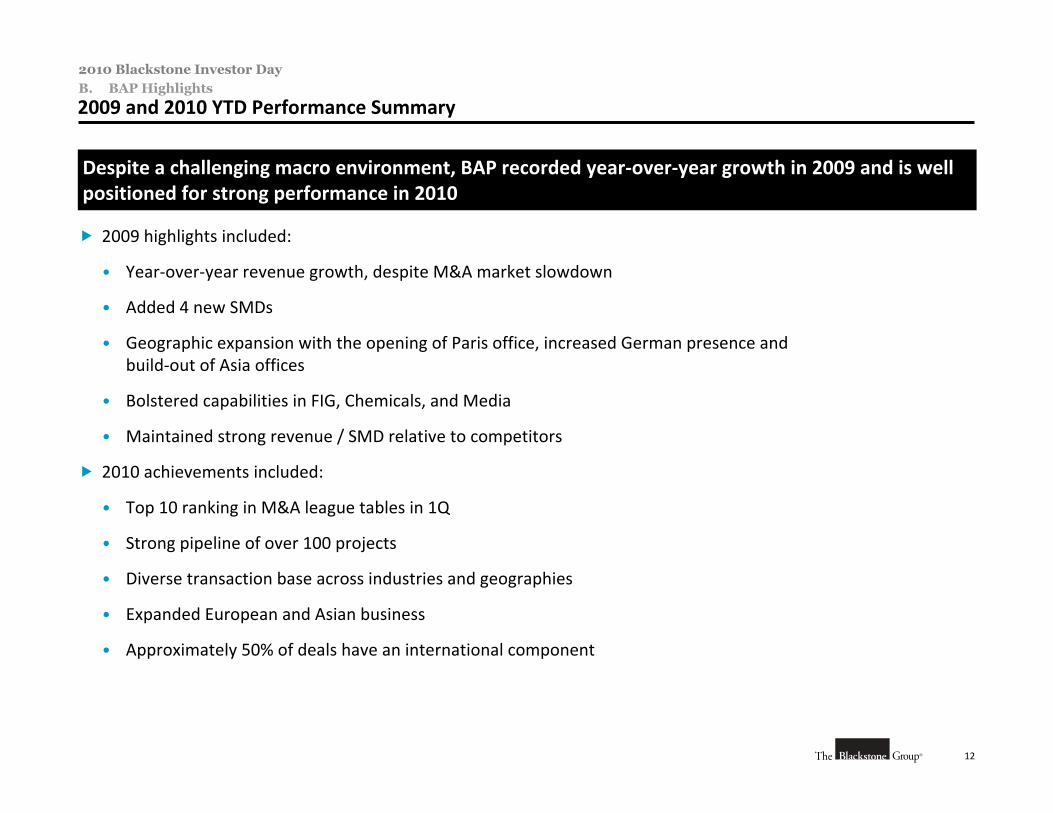

2009 and 2010 YTD Performance SummaryB. BAP Highlights

Despite a challenging macro environment, BAP recorded year‐over‐year growth in 2009 and is well positioned for strong performance in 2010

2009 highlights included:

• Year‐over‐year revenue growth, despite M&A market slowdown

• Added 4 new SMDs

• Geographic expansion with the opening of Paris office, increased German presence and build‐out of Asia offices

• Bolstered capabilities in FIG, Chemicals, and Media

• Maintained strong revenue / SMD relative to competitors

2010 achievements included:

• Top 10 ranking in M&A league tables in 1Q

• Strong pipeline of over 100 projects

• Diverse transaction base across industries and geographies

• Expanded European and Asian business

• Approximately 50% of deals have an international component

13

2010 Blackstone Investor Day

B. BAP Highlights

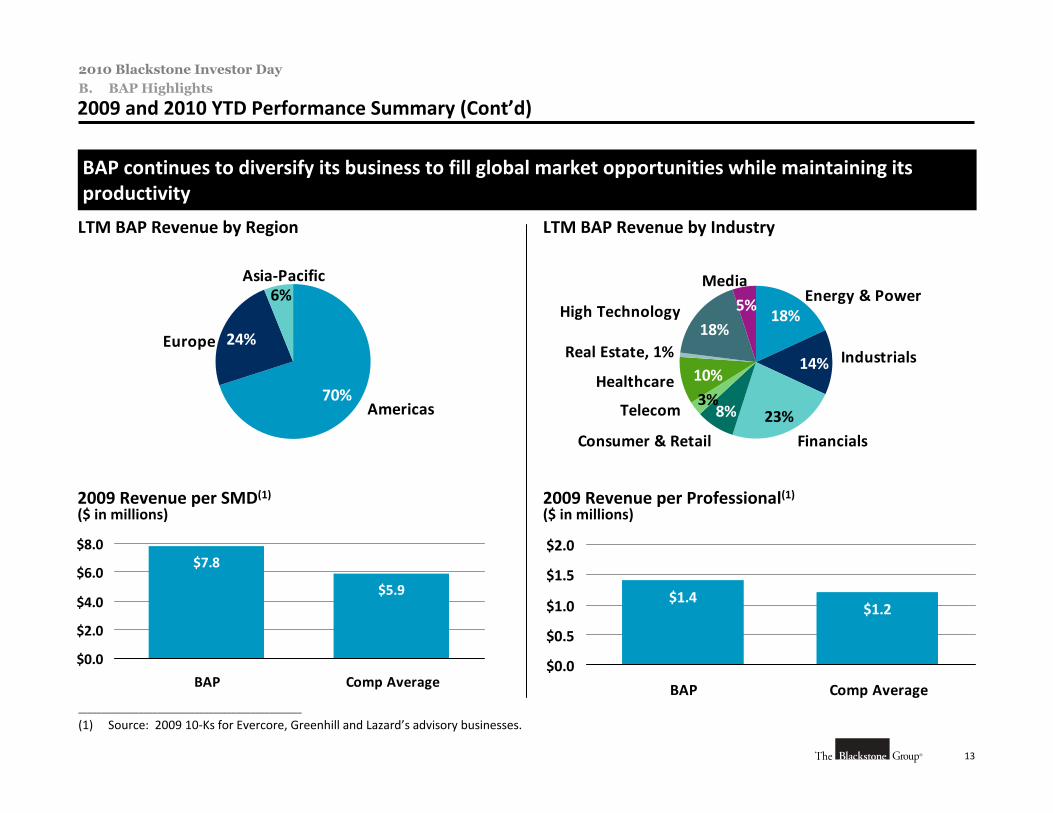

BAP continues to diversify its business to fill global market opportunities while maintaining its productivity

70%

6%

24%

Americas

Europe

Asia‐Pacific

LTM BAP Revenue by IndustryLTM BAP Revenue by Region

$7.8

$5.9

$0.0

$2.0

$4.0

$6.0

$8.0

BAP Comp Average

2009 Revenue per SMD(1)

($ in millions)

$1.4$1.2

$0.0

$0.5

$1.0

$1.5

$2.0

BAP Comp Average

2009 Revenue per Professional(1)($ in millions)

________________________________________________

(1) Source: 2009 10‐Ks for Evercore, Greenhill and Lazard’s advisory businesses.

5%18%

23%3%

18%

14%

8%

10%

Energy & Power

Industrials

FinancialsConsumer & Retail

Telecom

Healthcare

Real Estate, 1%

High Technology

Media

2009 and 2010 YTD Performance Summary (Cont’d)

14

2010 Blackstone Investor Day

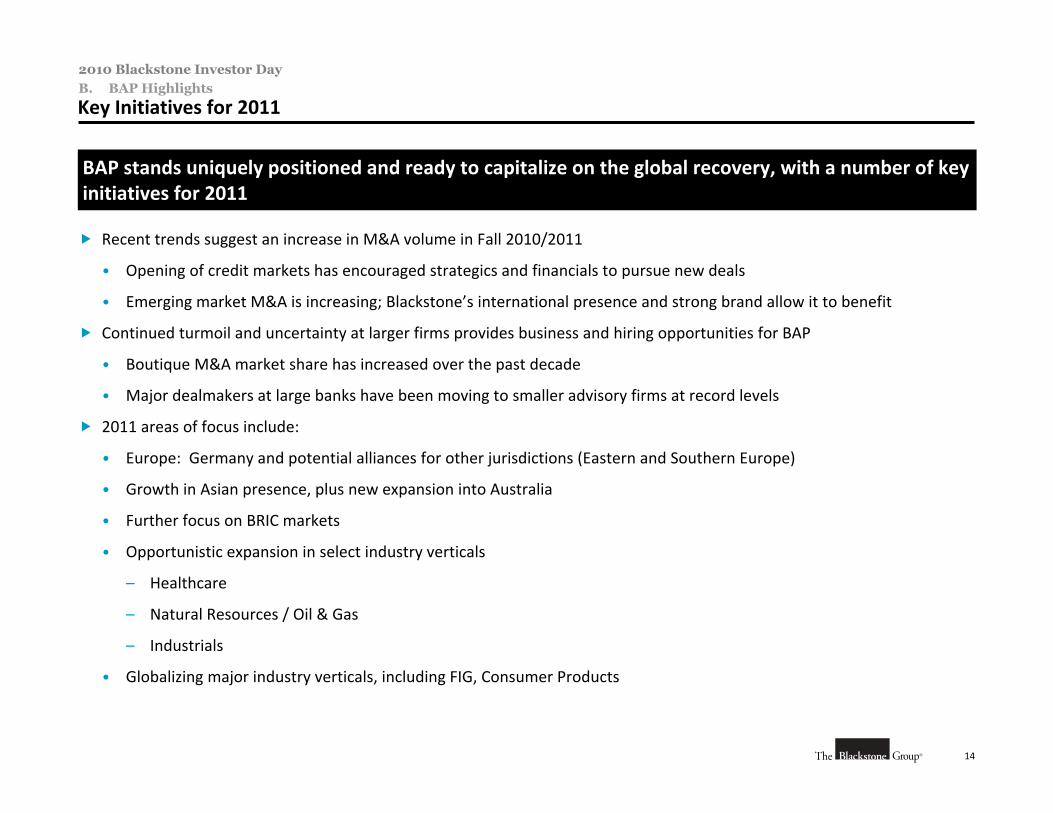

Key Initiatives for 2011B. BAP Highlights

BAP stands uniquely positioned and ready to capitalize on the global recovery, with a number of key initiatives for 2011

Recent trends suggest an increase in M&A volume in Fall 2010/2011

• Opening of credit markets has encouraged strategics and financials to pursue new deals

• Emerging market M&A is increasing; Blackstone’s international presence and strong brand allow it to benefit

Continued turmoil and uncertainty at larger firms provides business and hiring opportunities for BAP

• Boutique M&A market share has increased over the past decade

• Major dealmakers at large banks have been moving to smaller advisory firms at record levels

2011 areas of focus include:

• Europe: Germany and potential alliances for other jurisdictions (Eastern and Southern Europe)

• Growth in Asian presence, plus new expansion into Australia

• Further focus on BRIC markets

• Opportunistic expansion in select industry verticals

– Healthcare

– Natural Resources / Oil & Gas

– Industrials

• Globalizing major industry verticals, including FIG, Consumer Products

VI. Restructuring & Reorganization Advisory

A. Restructuring Group Overview

2

2010 Blackstone Investor Day

A. Restructuring Group Overview

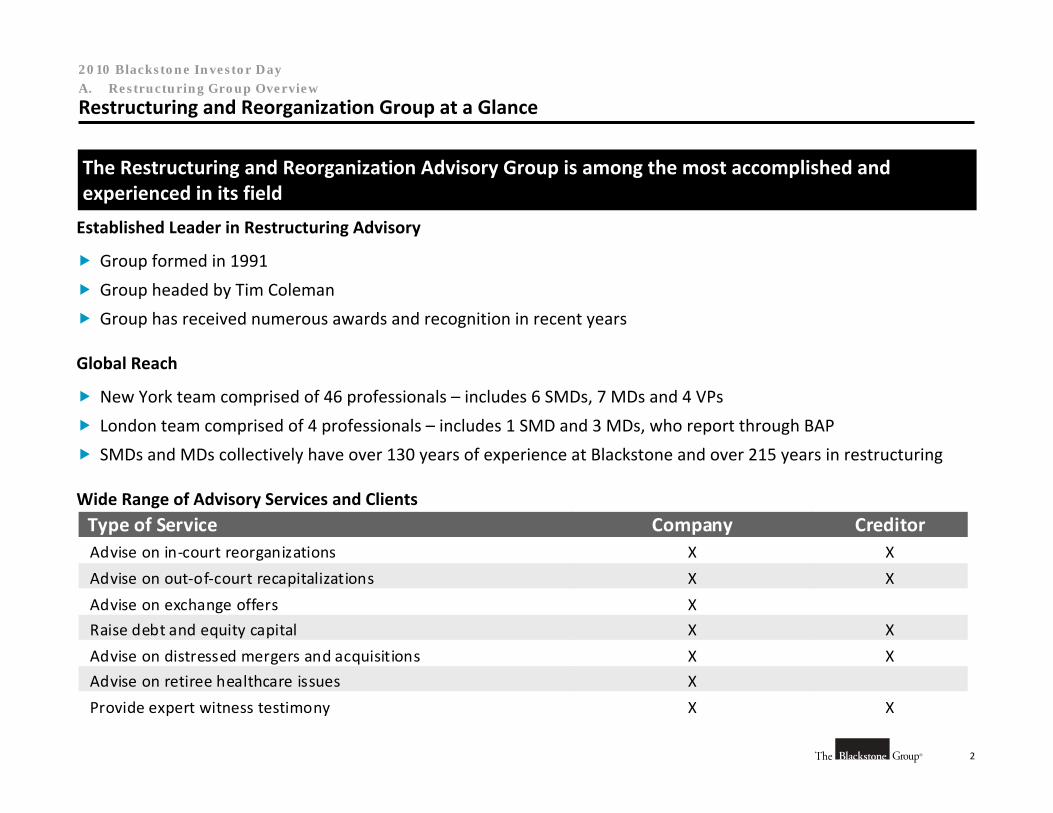

Restructuring and Reorganization Group at a Glance

The Restructuring and Reorganization Advisory Group is among the most accomplished and experienced in its field

Established Leader in Restructuring Advisory

Group formed in 1991

Group headed by Tim Coleman

Group has received numerous awards and recognition in recent years

Global Reach

New York team comprised of 46 professionals – includes 6 SMDs, 7 MDs and 4 VPs

London team comprised of 4 professionals – includes 1 SMD and 3 MDs, who report through BAP

SMDs and MDs collectively have over 130 years of experience at Blackstone and over 215 years in restructuring

Wide Range of Advisory Services and ClientsType of Service Company CreditorAdvise on in‐court reorganizations X X

Advise on out‐of‐court recapitalizations X X

Advise on exchange offers X

Raise debt and equity capital X X

Advise on distressed mergers and acquisitions X X

Advise on retiree healthcare issues X

Provide expert witness testimony X X

3

2010 Blackstone Investor Day

A. Restructuring Group Overview

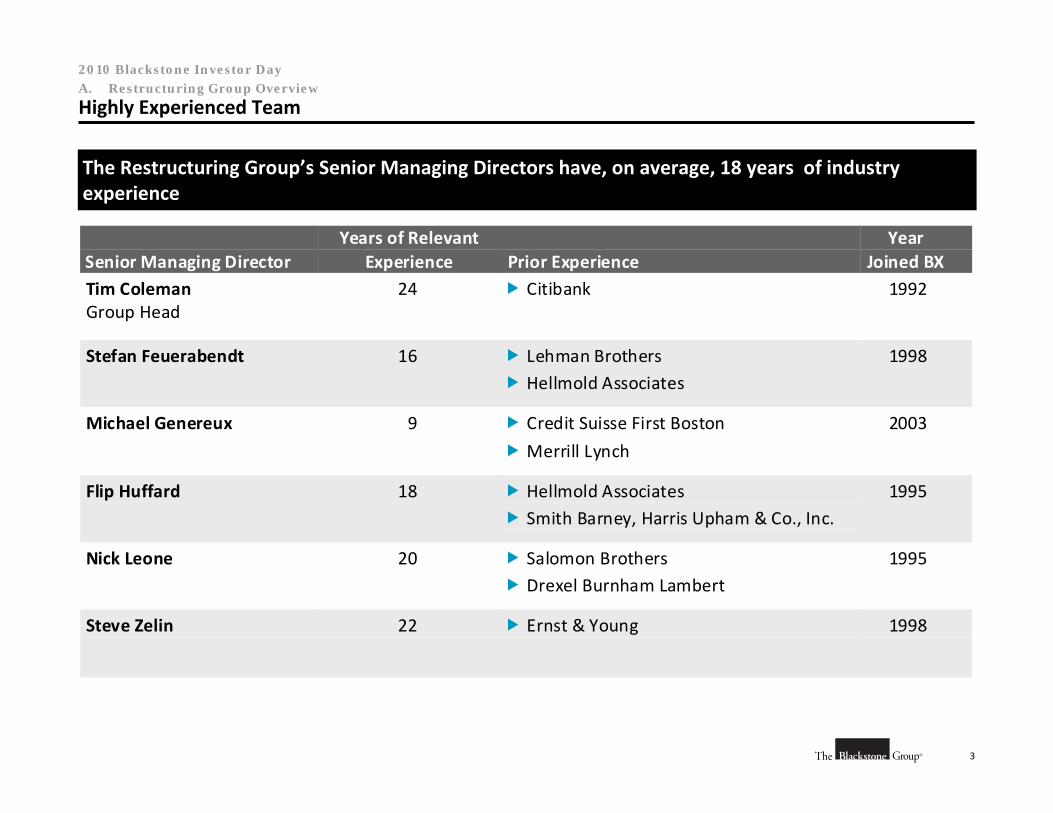

Highly Experienced Team

The Restructuring Group’s Senior Managing Directors have, on average, 18 years of industry experience

Senior Managing Director Years of Relevant

Experience Prior Experience Year

Joined BX Tim Coleman Group Head

24 Citibank 1992

Stefan Feuerabendt 16 Lehman Brothers Hellmold Associates

1998

Michael Genereux 9 Credit Suisse First Boston Merrill Lynch

2003

Flip Huffard 18 Hellmold Associates Smith Barney, Harris Upham & Co., Inc.

1995

Nick Leone 20 Salomon Brothers Drexel Burnham Lambert

1995

Steve Zelin 22 Ernst & Young 1998

4

2010 Blackstone Investor Day

A. Restructuring Group Overview

Blackstone Restructuring Recognition

Blackstone’s restructuring advisory efforts have received substantial praise over recent years

Thomson’s International Financing Review

Awarded “Restructuring Deal of the Year” in 2009 for the Ford Motor Company tender offer and deleveraging transactions

Awarded “Restructuring of the Year” in 2008 for the restructuring of Credit‐Based Asset Servicing and Securitization LLC (“C‐BASS”)

Named “North American Restructuring House of the Year” for the years 2004 and 2005

Turnaround Atlas Awards

Awarded “Turnaround of the Year” ($5+ billion) and “Automotive Industry & Services Deal of the Year” in 2010 for the restructuring of Ford Motor Company

Awarded “Turnaround of the Year” ($1+ billion) in 2010 for the SemGroup Corporation reorganization

Awarded “Corporate Turnaround Deal of the Year” ($500+ million) in 2010 for the restructuring of Merisant Company

Awarded “Beverage, Food & Service Deal of the Year” in 2009 for the reorganization of Mrs. Fields Companies

Turnaround Management Association

Awarded “Mega Company Turnaround of the Year” in 2007 for the Winn‐Dixie Stores reorganization

5

2010 Blackstone Investor Day

A. Restructuring Group Overview

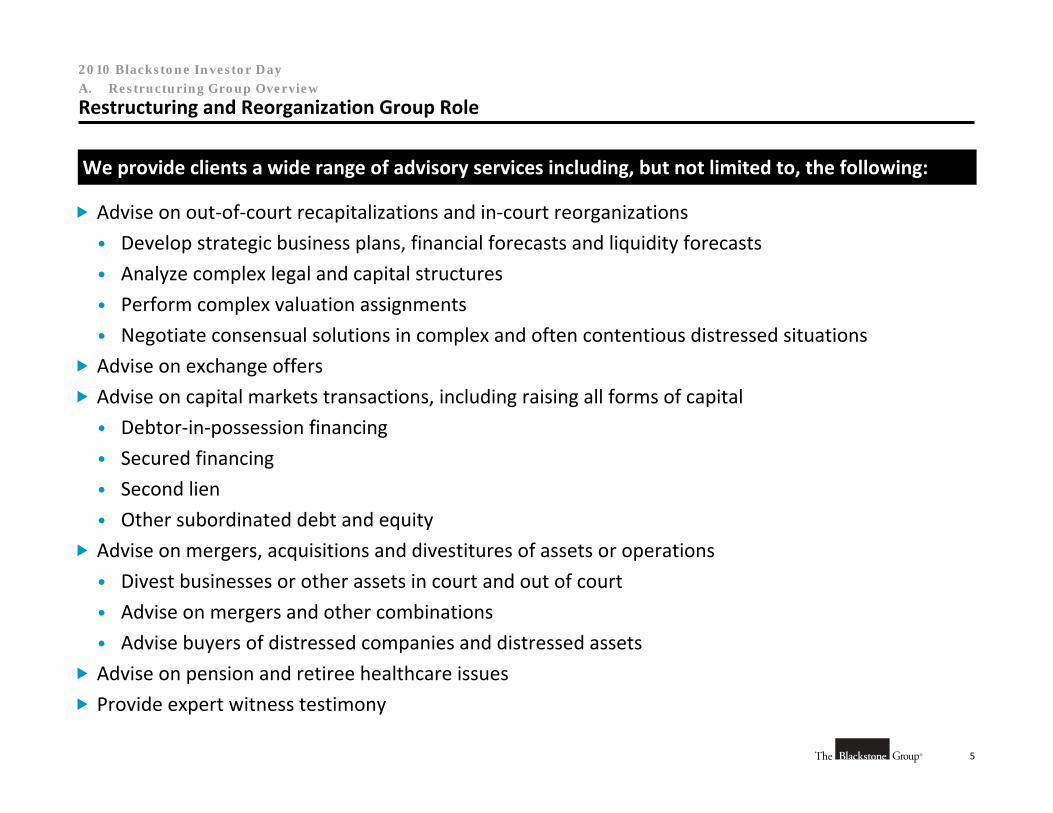

Restructuring and Reorganization Group Role

We provide clients a wide range of advisory services including, but not limited to, the following:

Advise on out‐of‐court recapitalizations and in‐court reorganizations

• Develop strategic business plans, financial forecasts and liquidity forecasts

• Analyze complex legal and capital structures

• Perform complex valuation assignments

• Negotiate consensual solutions in complex and often contentious distressed situations

Advise on exchange offers

Advise on capital markets transactions, including raising all forms of capital

• Debtor‐in‐possession financing

• Secured financing

• Second lien

• Other subordinated debt and equity

Advise on mergers, acquisitions and divestitures of assets or operations

• Divest businesses or other assets in court and out of court

• Advise on mergers and other combinations

• Advise buyers of distressed companies and distressed assets

Advise on pension and retiree healthcare issues

Provide expert witness testimony

6

2010 Blackstone Investor Day

A. Restructuring Group Overview

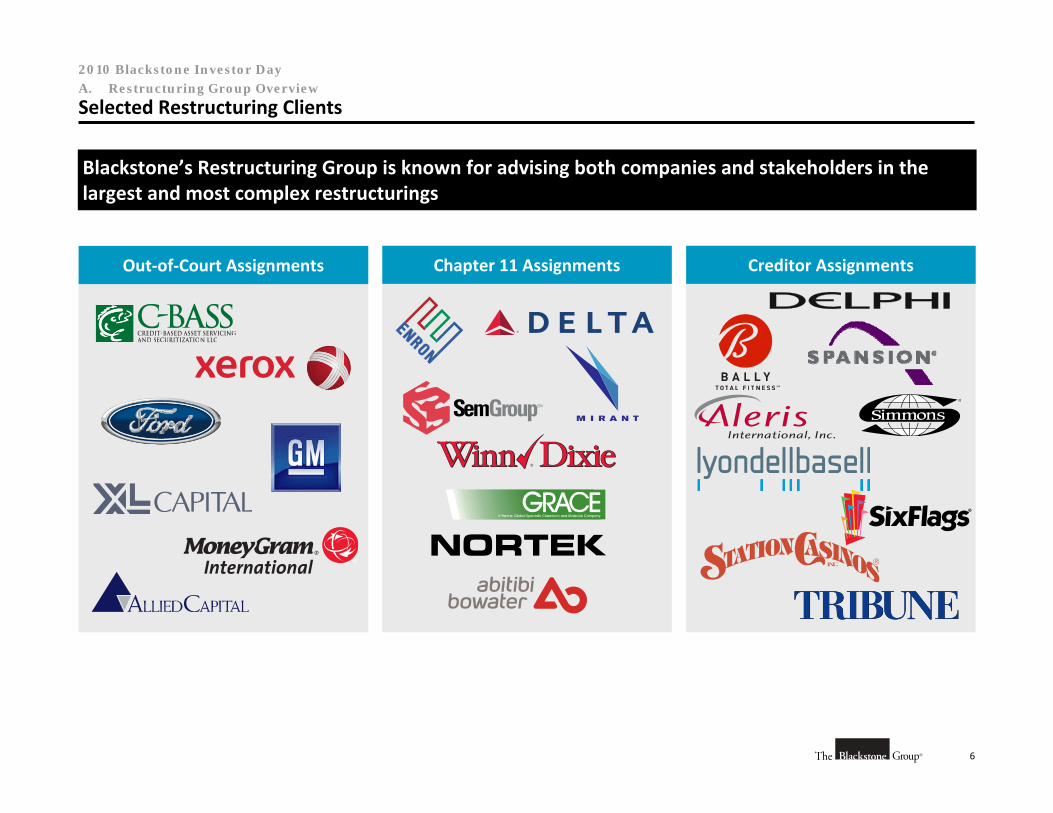

Selected Restructuring Clients

Blackstone’s Restructuring Group is known for advising both companies and stakeholders in the largest and most complex restructurings

Chapter 11 AssignmentsOut‐of‐Court Assignments Creditor Assignments

7

2010 Blackstone Investor Day

A. Restructuring Group Overview

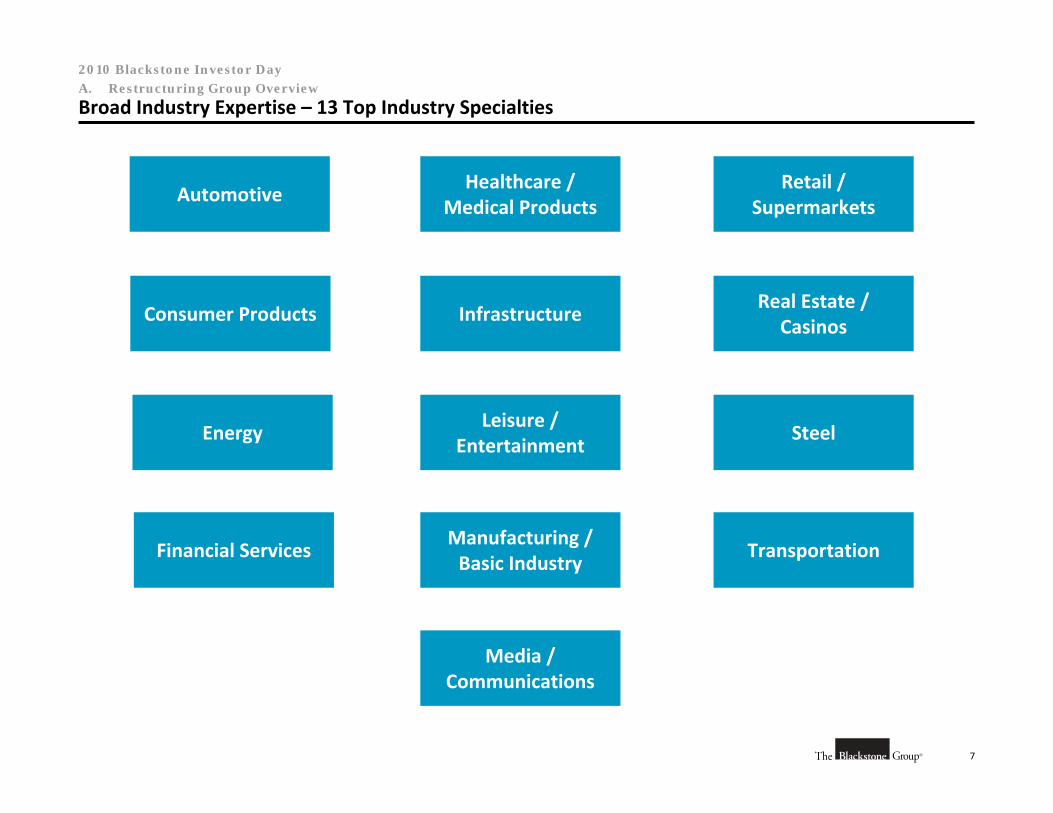

Broad Industry Expertise – 13 Top Industry Specialties

Automotive

Energy

Consumer Products

Financial Services

Healthcare / Medical Products

Infrastructure

Leisure / Entertainment

Manufacturing / Basic Industry

Media / Communications

Retail / Supermarkets

Steel

Transportation

Real Estate / Casinos

B. Restructuring Market Trends

9

2010 Blackstone Investor Day

B. Restructuring Market Trends

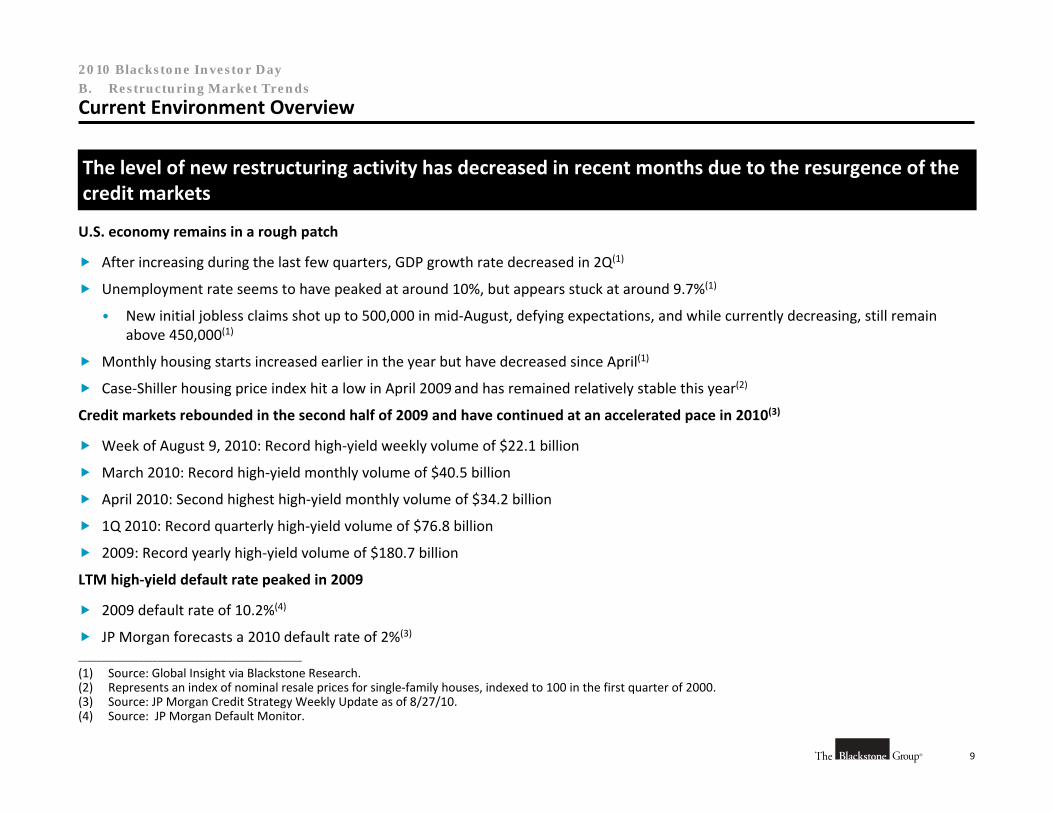

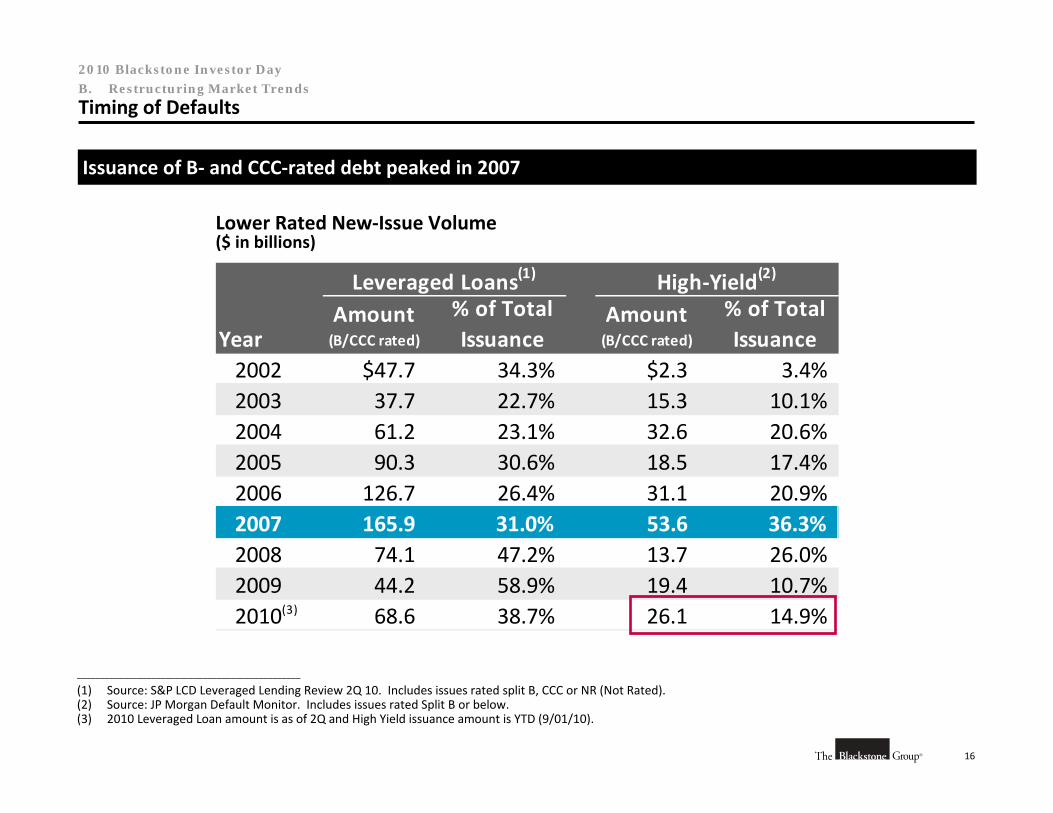

Current Environment Overview

The level of new restructuring activity has decreased in recent months due to the resurgence of the credit markets

U.S. economy remains in a rough patch

After increasing during the last few quarters, GDP growth rate decreased in 2Q(1)

Unemployment rate seems to have peaked at around 10%, but appears stuck at around 9.7%(1)

• New initial jobless claims shot up to 500,000 in mid‐August, defying expectations, and while currently decreasing, still remain above 450,000(1)

Monthly housing starts increased earlier in the year but have decreased since April(1)

Case‐Shiller housing price index hit a low in April 2009 and has remained relatively stable this year(2)

Credit markets rebounded in the second half of 2009 and have continued at an accelerated pace in 2010(3)

Week of August 9, 2010: Record high‐yield weekly volume of $22.1 billion

March 2010: Record high‐yield monthly volume of $40.5 billion

April 2010: Second highest high‐yield monthly volume of $34.2 billion

1Q 2010: Record quarterly high‐yield volume of $76.8 billion

2009: Record yearly high‐yield volume of $180.7 billion

LTM high‐yield default rate peaked in 2009

2009 default rate of 10.2%(4)

JP Morgan forecasts a 2010 default rate of 2%(3)

________________________________________________

(1) Source: Global Insight via Blackstone Research.(2) Represents an index of nominal resale prices for single‐family houses, indexed to 100 in the first quarter of 2000.(3) Source: JP Morgan Credit Strategy Weekly Update as of 8/27/10. (4) Source: JP Morgan Default Monitor.

10

2010 Blackstone Investor Day

Unemployment Rate and New Jobless Claims(2)(Claims in thousands)

4%5%6%7%8%9%10%11%

Jan‐08 Jul‐08 Jan‐09 Jul‐09 Jan‐10 Aug‐10

0100200300400500600700

Unemployment Rate

Jobless Claims

Monthly Housing Starts(Thousands)

400

600

800

1,000

1,200

Jan‐08 Jul‐08 Jan‐09 Jul‐09 Jan‐10 Aug‐10

Case‐Shiller Housing Price Index(3)

130

145

160

175

190

Jan‐08 Jul‐08 Jan‐09 Jul‐09 Jan‐10 Aug‐10

B. Restructuring Market Trends

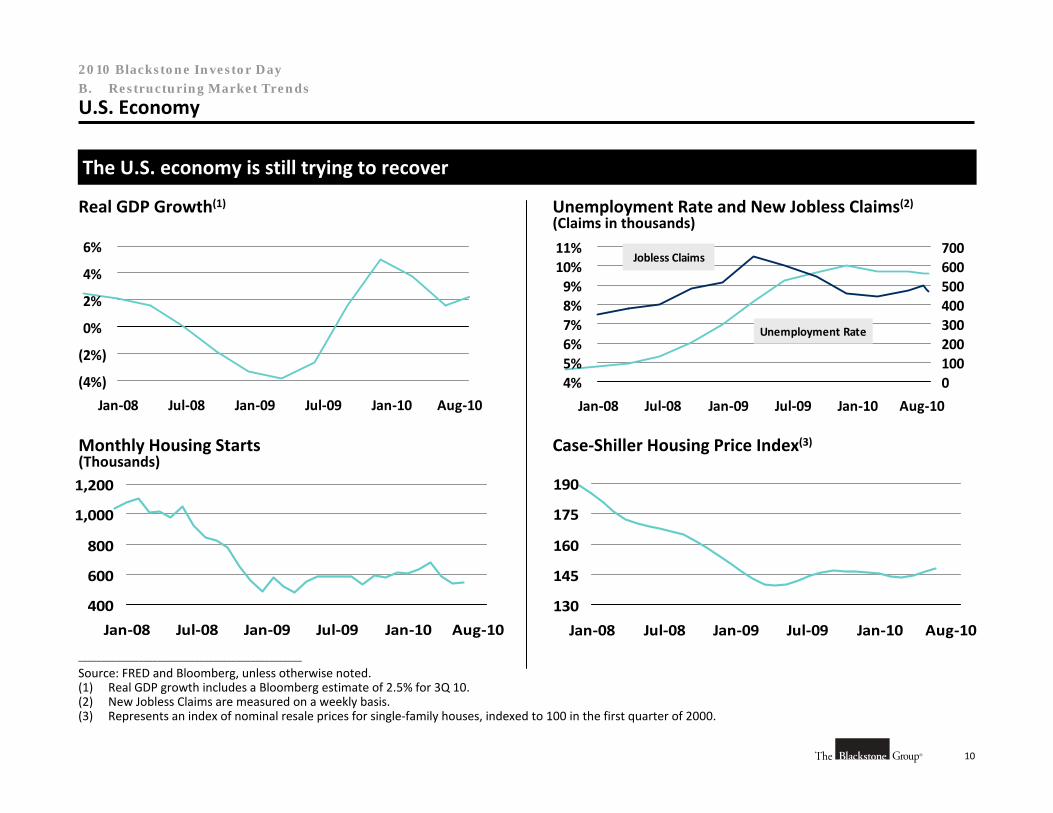

U.S. Economy

The U.S. economy is still trying to recover

________________________________________________

Source: FRED and Bloomberg, unless otherwise noted.(1) Real GDP growth includes a Bloomberg estimate of 2.5% for 3Q 10.(2) New Jobless Claims are measured on a weekly basis.(3) Represents an index of nominal resale prices for single‐family houses, indexed to 100 in the first quarter of 2000.

Real GDP Growth(1)

(4%)

(2%)

0%

2%

4%

6%

Jan‐08 Jul‐08 Jan‐09 Jul‐09 Jan‐10 Aug‐10

11

2010 Blackstone Investor Day

31

39

22

57

44

61

12

31

8

36

7

13

55

52

60

77

50

1

49

$0

$20

$40

$60

$80

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q

2006 2007 2008(2) 2009 2010

B. Restructuring Market Trends

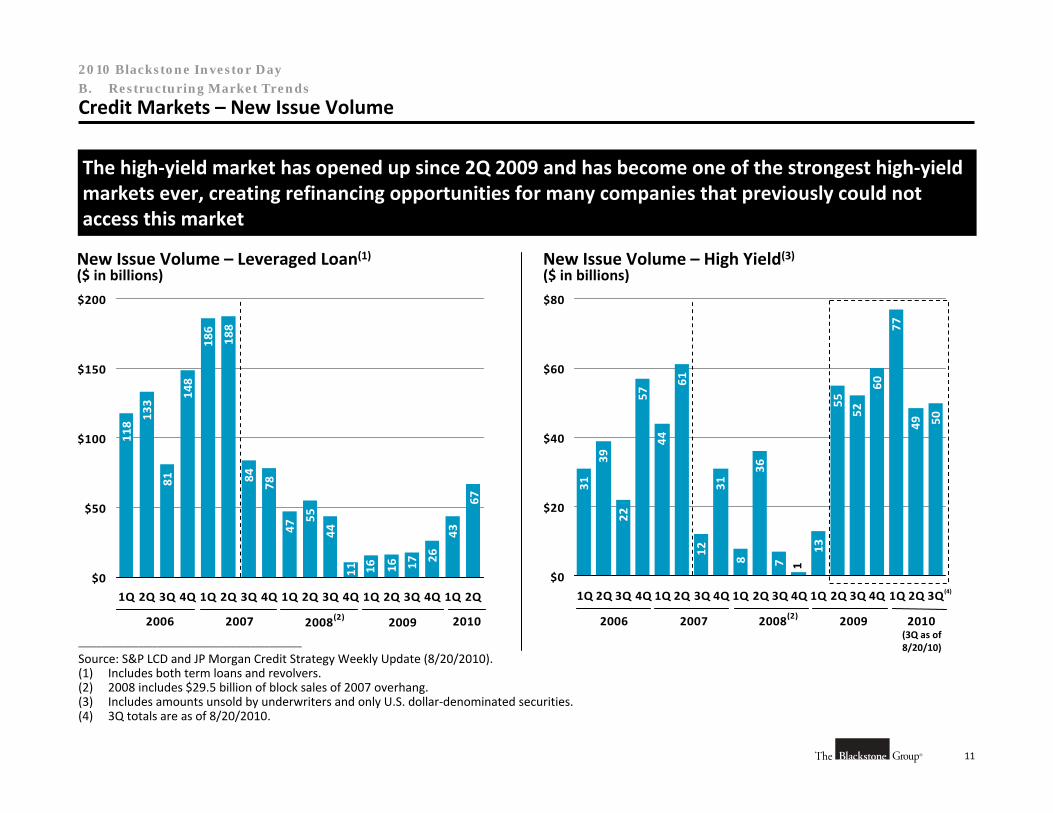

Credit Markets – New Issue Volume

The high‐yield market has opened up since 2Q 2009 and has become one of the strongest high‐yield markets ever, creating refinancing opportunities for many companies that previously could not access this market

________________________________________________

Source: S&P LCD and JP Morgan Credit Strategy Weekly Update (8/20/2010).(1) Includes both term loans and revolvers.(2) 2008 includes $29.5 billion of block sales of 2007 overhang.(3) Includes amounts unsold by underwriters and only U.S. dollar‐denominated securities.(4) 3Q totals are as of 8/20/2010.

New Issue Volume – Leveraged Loan(1)($ in billions)

118

133

81

148

186

188

84

78

47

55

44

17 26

43

67

161611$0

$50

$100

$150

$200

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q

2006 2007 2008(2) 2009 2010

New Issue Volume – High Yield(3)

($ in billions)

(3Q as of 8/20/10)

(4)

12

2010 Blackstone Investor Day

B. Restructuring Market Trends

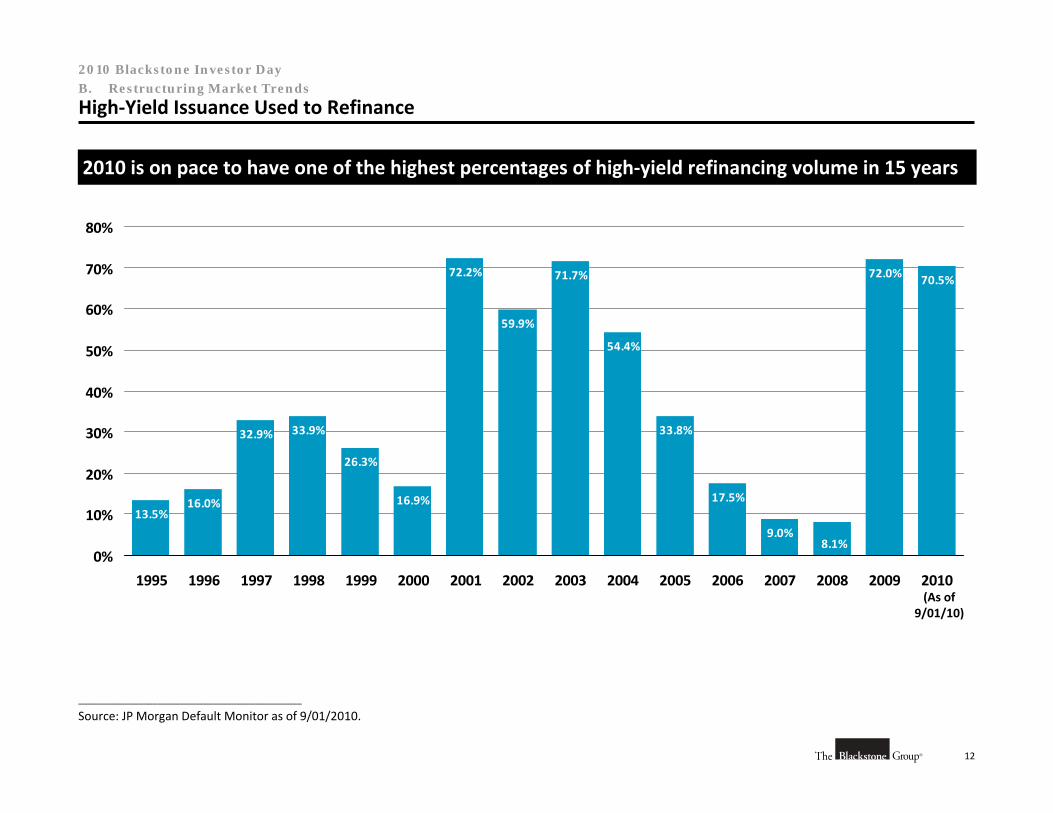

High‐Yield Issuance Used to Refinance

13.5%16.0%

32.9% 33.9%

26.3%

16.9%

72.2% 71.7%

54.4%

33.8%

72.0% 70.5%

8.1%9.0%

17.5%

59.9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

2010 is on pace to have one of the highest percentages of high‐yield refinancing volume in 15 years

________________________________________________

Source: JP Morgan Default Monitor as of 9/01/2010.

(As of 9/01/10)

13

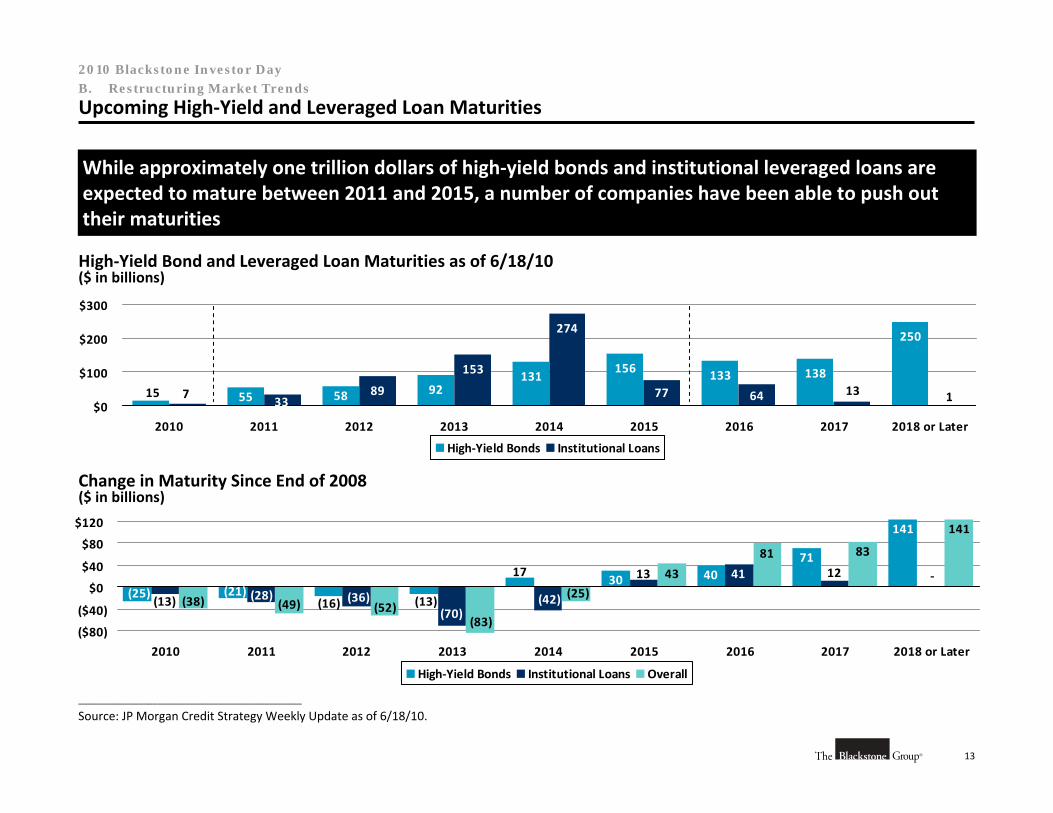

2010 Blackstone Investor Day

141

71

(25) (21)(16) (13)

1730 40

(13) (28) (36)(70)

(42)

12 ‐13 41

141

8381

(25)(52)(38)

43

(49) (83)

($80)

($40)

$0

$40

$80

$120

2010 2011 2012 2013 2014 2015 2016 2017 2018 or Later

High‐Yield Bonds Institutional Loans Overall

B. Restructuring Market Trends

Upcoming High‐Yield and Leveraged Loan Maturities

While approximately one trillion dollars of high‐yield bonds and institutional leveraged loans are expected to mature between 2011 and 2015, a number of companies have been able to push out their maturities

________________________________________________

Source: JP Morgan Credit Strategy Weekly Update as of 6/18/10.

High‐Yield Bond and Leveraged Loan Maturities as of 6/18/10($ in billions)

138

250

77133156

131925855 15 64 113

274

153

8933

7$0

$100

$200

$300

2010 2011 2012 2013 2014 2015 2016 2017 2018 or Later

High‐Yield Bonds Institutional Loans

Change in Maturity Since End of 2008($ in billions)

14

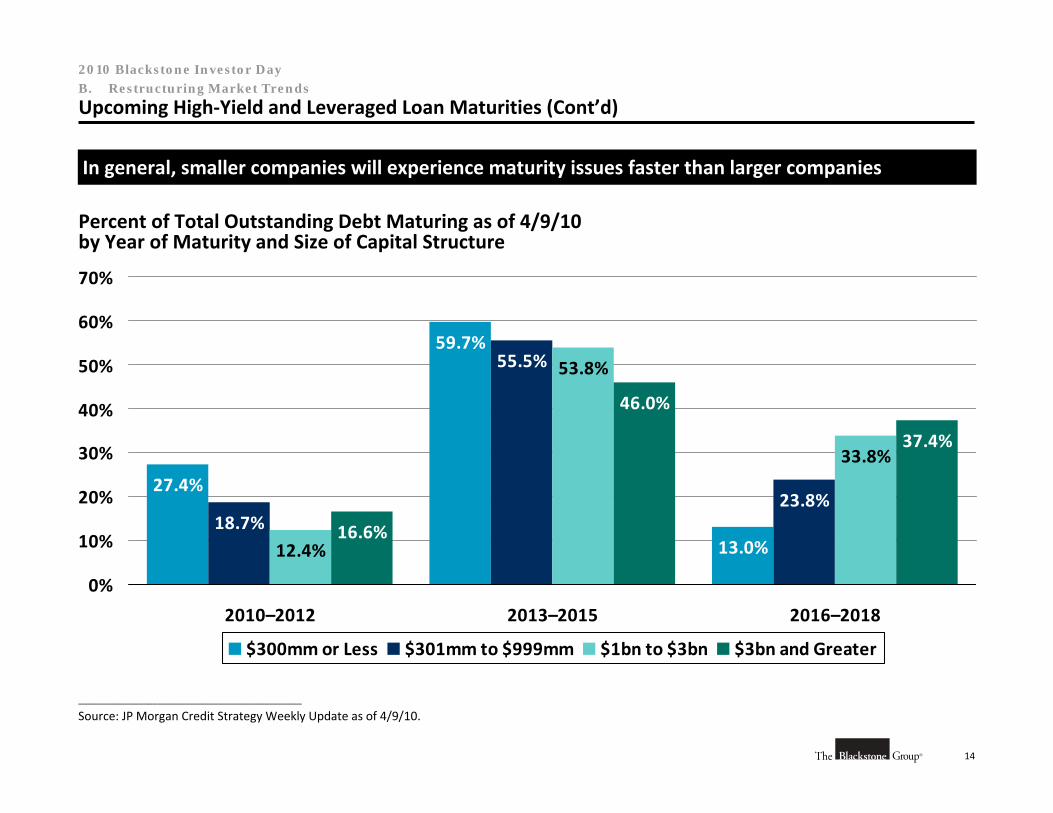

2010 Blackstone Investor Day

B. Restructuring Market Trends

Upcoming High‐Yield and Leveraged Loan Maturities (Cont’d)

________________________________________________

Source: JP Morgan Credit Strategy Weekly Update as of 4/9/10.

In general, smaller companies will experience maturity issues faster than larger companies

Percent of Total Outstanding Debt Maturing as of 4/9/10by Year of Maturity and Size of Capital Structure

27.4%

59.7%

13.0%18.7%

55.5%

23.8%

12.4%

53.8%

33.8%

16.6%

46.0%

37.4%

0%

10%

20%

30%

40%

50%

60%

70%

2010–2012 2013–2015 2016–2018

$300mm or Less $301mm to $999mm $1bn to $3bn $3bn and Greater

15

2010 Blackstone Investor Day

B. Restructuring Market Trends

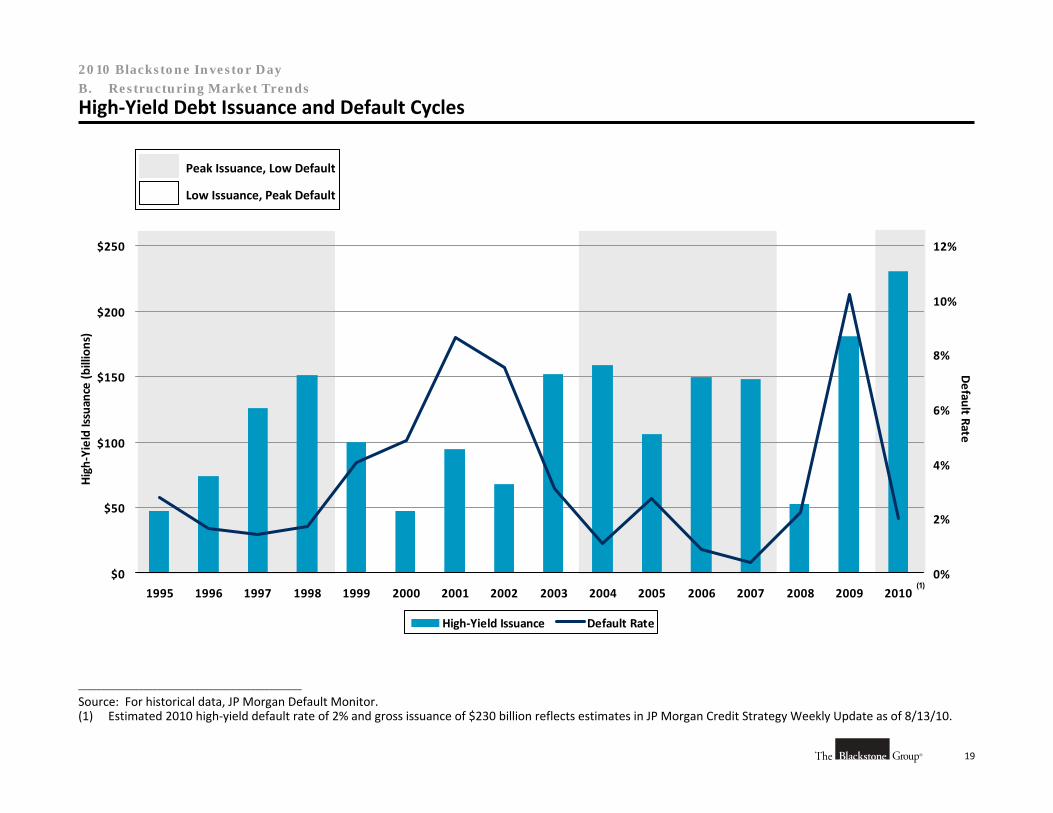

High‐Yield Debt Issuance and Restructuring Cycles

Restructuring cycles are driven largely by the high‐yield and the institutional leveraged loan markets