Embed Size (px)

Citation preview

©2012 CliftonLarsonAllen LLP1 111

©20

12 C

lifto

nLar

sonA

llen

LLP

ASAE Foundation’s Association 990: A Powerful Tool for

Benchmarking

John N. Dripps, CPANational Association of

Secondary School Principals

Nat Bartholomew, CPACliftonLarsonAllen LLP

©2012 CliftonLarsonAllen LLP2

Agenda

• Define benchmarking and trendanalyses

• Why benchmark (quick summary)• What tools are available (benefits / limitations)• ASAE Foundation’s Association 990• Identifying key metrics• Utilizing ratio analyses• Case study – NASSP

©2012 CliftonLarsonAllen LLP3

Benchmarking – Internal and External

• Internal = Trend Analyses

Utilizing historical financial and non-financila information from your organization to spot trends

• External = Benchmarking

Utilizing financial and non-financial information from peer organizations to evaluate performance, financial condition, etc.

©2012 CliftonLarsonAllen LLP4

Why Benchmark?

• To compare like attributes or metrics from similar demographic data samples– To uncover business processes, practices, and strategies

• To provide a baseline for performance improvement• To gain best practices

– Measure by fact rather than intuition or opinion• Benchmark when you want to …

– Make better-informed decisions– Answer the question “how do I compare?”– Take pulse of your financial health– Obtain a single version of the truth

©2012 CliftonLarsonAllen LLP5

Why Benchmark?

As a way to share and collaborate, stimulate conversation and reflection, advocate for yourself, and take pulse of environmental trends.

©2012 CliftonLarsonAllen LLP6

What Tools Are Available – Benefits/Limitations

– Similar organization Federal Form 990 (public document)

– Annual reports or published financials– GuideStar – Lots of information stemming

from filed Federal Form 990s– ASAE’s Operating Ratio Report (ORR) or

Association 990– NTEN – IT statistics– NCCS – Operating reserves

©2012 CliftonLarsonAllen LLP7

What is ASAE’s ORR

• Compilation of financial data from participating associations

• First published in 1953• Collected via Federal Forms

990 and survey supplements

• 660 valid surveys utilized in 13th Edition – 5% more than prior ORR – and 8¼% response rate

• Compiled ’07 issued ’08• Next edition due out 2012!

©2012 CliftonLarsonAllen LLP8

ORR – Respondent Profile

• 67% were 501(c)(6) / 28% (c)(3)

• 47% reported total gross revenue > $5M

• Typical or median organization was $3.8M

• Largest concentrations - DC 27% / Chicago 10% / NY 3%

©2012 CliftonLarsonAllen LLP9

Extracting Relevant Data

ORR Cuts Data By Several Categories• Total Revenue (Six Tiers)• Membership Type – Trade vs. Professional• IRS Tax Status (c)(6) vs. (c)(3)• Geog. Scope (Int’l/Nat’l or Regional/State/Local)• Metropolitan Area (e.g., DC, NY, etc.)• Industry Sector/Interest Area (e.g., Bus/Industrial,

Education, or Healthcare/Medical – Each Separated by Membership Type)

ORR Interactive

©2012 CliftonLarsonAllen LLP10

Trend Analyses - Investment Composition(as a percentage of total assets)

35.4 31.2 27.7 26.2 24.8

14.4 19.4 23.1 27.434.3

0

10

20

30

40

1993 1996 1999 2003 2007

Invested Securities Invested Cash

©2012 CliftonLarsonAllen LLP11

Trend Analyses – Dues as a Percentage of Revenue (Dues Reliance)

©2012 CliftonLarsonAllen LLP12

ASAE Foundation’s “Association 990”

©2012 CliftonLarsonAllen LLP13

ASAE Foundation’s “Association 990”• Federal Form 990 – core form only• 18,952 ’08, 19,693 ‘09 and 23,339 ‘10 990s thus far• Functionality allows data sorts on the year and …

– 501(c) class (9 choices)– Number of employees (6 tiers)– Total revenue (8 tiers) and total expense (8 tiers)– Membership revenue (8 tiers)– Investment asset balance (8 tiers)– Unrelated business income (7 tiers)– Accounting method (accrual, cash or other)– ASAE member (yes/no)– State (52, includes DC and PR)– Metropolitan area (36 different areas)

©2012 CliftonLarsonAllen LLP14

ASAE Foundation’s “Association 990”Suite of Tools

• Association 990 - Key Ratios– Predefined reports – key ratios, revenue and expense detail, and balance sheet detail– Generated online– Sort functionality enumerated on the prior slide– Ability to export to Excel, Word or Adobe– Ability to print PDF copies of any Assn’s 990

• Association 990 - Agenda Items– Drawn from the aggregate data, these slides (PDF and PPT)

provide comparative data on policy, procedure and certain organizational measures

©2012 CliftonLarsonAllen LLP15

Example Queries - Various

Demographic 2008 2009 2010

All Associations 18,952 19,693 23,339

501(c)(3) 6,830 7,779 8,342

501(c)(6) 4,992 4,971 6,158

DC Area 1,164 1,188 1,288

New York Area 604 561 567

Chicago Area 562 600 598

LA Area 349 402 368

Dallas Area 146 153 170

©2012 CliftonLarsonAllen LLP16

Example Queries – Number of Employees

Employees 2008 2009 2010

All 18,952 19,693 23,339

</= 5 5,417 5,939 8,457

6 – 10 3,038 3,442 4,351

11 – 20 3,237 3,206 3,760

21 – 50 3,120 3,195 3,384

51 – 100 1,673 1,621 1,532

100+ 2,467 2,290 1,855

©2012 CliftonLarsonAllen LLP17

Example Queries – Size (Revenue)

Total Revenue 2008 2009 2010

All 18,952 19,693 23,339

</= $1M 9,398 10,931 15,408

$1 - $2M 3,814 3,428 3,271

$2 - $5M 3,256 2,982 2,700

$5 - $10M 1,356 1,259 1,057

$10 - $20M 605 580 485

$20 - $30M 199 170 144

$30 - $50M 138 146 114

Over $50M 186 197 160

©2012 CliftonLarsonAllen LLP18

Best “Average” Measure

Median – ½ respondents above; ½ below

Mean – sum of all cases / total # of respondents

Median is a better measure for average when the upper limit is theoretically infinite (e.g., number of members in reporting associations, annual budget for reporting associations), as the mean can be strongly affected by very high values.

2010 # Employees (Mean = 79.8 / Median = 9.0)

2010 Total Rev. (Mean = $3.5M / Median = $563K)

©2012 CliftonLarsonAllen LLP19

Compensation GeographicallyMedian / Mean (Total Revenue >/= $1M)

Demographic Chicago NYC DC

# Associations 289 318 838

Median Revenue $3.5M $3.2M $3.8M

Average Revenue $10.5M $11.0M $14.6M

Median Compensation $52,462 $51,953 $69,131

Average Compensation $53,484 $63,544 $79,415

©2012 CliftonLarsonAllen LLP20

Dues / Total Revenue = Dues Reliance

Gross Revenue 2008 2009 2010

< $1M 35.9% 36.1% 36.8%

$1 - $2M 40.8% 40.3% 40.9%

$2 - $5M 43.9% 43.4% 43.4%

$5 - $10M 41.5% 41.0% 42.5%

$10 - $20M 36.0% 34.8% 35.6%

$20 - $30M 29.0% 32.1% 31.5%

$30 - $50M 32.1% 28.4% 33.6%

Over $50M 28.4% 28.1% 28.8%

©2012 CliftonLarsonAllen LLP21

2010 Average Compensation Geographically

©2012 CliftonLarsonAllen LLP22

2010 Average Benefits by Size(based upon total revenue)

Average Size (Revenue) Pension Benefits

</= $1M $766 $1,801

$1 – $2M $2,194 $3,726

$2 - $5M $2,585 $4,520

$5 - $10M $2,599 $4,920

$10 - $20M $3,321 $6,881

$20 - $30M $4,522 $6,672

$30 – $50M $5,381 $7,143

>$50M $6,762 $14,156

All $1,399 $2,773

©2012 CliftonLarsonAllen LLP23

2010 Average Pension and Benefits by Size (based upon total revenue)

©2012 CliftonLarsonAllen LLP24

Median Number of FTEs (Full-Time Employees)

Year 5M 10M 20M 30M 50M

2009 32 89 108 149 199

2010 29 62 96 137 226

©2012 CliftonLarsonAllen LLP25

2010 Revenue Growth(expressed as a percentage of revenue)

©2012 CliftonLarsonAllen LLP26

Unrelated Business Income – 2008/09/10

Classification Percentage Number of Records

All Organizations 2.7% 18,952

2.5% 19,693

2.5% 23,339

501(c)(3) 0.9% 6,830

0.8% 7,779

0.8% 8,342

501(c)(6) 3.8% 4,992

3.6% 4,971

3.3% 6,158

©2012 CliftonLarsonAllen LLP27

Unrelated Business Income – 2008/09/10

Total Revenue All Associations 501(c)(3) 501(c)(6)

$0 - $5M 2.8% 0.8% 3.8%

2.5% 0.8% 3.7%

2.6% 0.7% 3.3%

$5 - $20M 2.7% 0.9% 3.7%

2.4% 1.0% 3.2%

2.3% 1.0% 3.3%

$20M+ 2.0% 1.5% 3.5%

1.7% 1.1% 3.1%

1.6% 1.3% 2.6%

©2012 CliftonLarsonAllen LLP28

2010 Investments as a % of Total Assets

©2012 CliftonLarsonAllen LLP29

After Login – 1St Page – Association 990

©2012 CliftonLarsonAllen LLP30

Building Your Report

©2012 CliftonLarsonAllen LLP31

Selecting One or More Categories

©2012 CliftonLarsonAllen LLP32

Generate the Report

©2012 CliftonLarsonAllen LLP33

Four Tabs

©2012 CliftonLarsonAllen LLP34

Tab 1 - Key Performance Ratios

©2012 CliftonLarsonAllen LLP35

Exporting to Excel

©2012 CliftonLarsonAllen LLP36

Tab 2 – Revenue and Expense

©2012 CliftonLarsonAllen LLP37

Tab 3 – Balance Sheet

©2012 CliftonLarsonAllen LLP38

Tab 4 – Ratio Definitions

©2012 CliftonLarsonAllen LLP39

Horizon Upgrades Contemplated

• Access to filed Federal Forms 990, similar to GuideStar• Quartile results• Association segments by industry/interest area (e.g.,

business/industrial, education, healthcare/medical, etc.)• Ability to create comparison groups• Drill-down functionality• Slide generator• Trend analyses functionality when multiple years of data are

available• Addition of Federal Form 990 Schedules to the database

(e.g., Schedule J)

©2012 CliftonLarsonAllen LLP40

Identification of Critical Indicators(Key Metrics)

• Financial Metrics

• Non-Financial Metrics

©2012 CliftonLarsonAllen LLP41

What Are Your Key Financial Metrics

Unrelated Business Income

Investment Income

Total Membership

Dues / Non-Dues Revenue

For-Profit Subsidiary Dividends

Total Contributions /

Total Unrestricted Contributions

Exposition $Certification $Publication $

©2012 CliftonLarsonAllen LLP42

What Are Your Key Non-Financial Metrics

Number of Attendees

Number of Members

Number of CE Hours Delivered

Number of Certificants

Number of Donors

Number of Clients Served

©2012 CliftonLarsonAllen LLP43

Basic Ratios

• Current = Current Assets (CA) / Cur. Liabilities

• Quick = CA Less Inventory / Current Liabilities

• Leverage = Total Liabilities / Total Net Assets

• Dues Reliance = Member Dues / Total Revenue

• Inventory Turnover = Sales / Inventory

• Avg. Collection Pd. = AR / Sales Per Day

• ROI = Income / Avg. Investment Balance

©2012 CliftonLarsonAllen LLP44444444

©20

12 C

lifto

nLar

sonA

llen

LLP

The NASSP Story

Using Financial Metrics -Information is Power

©2012 CliftonLarsonAllen LLP45

National Association of Secondary School Principals

• 25,000 individual members• 97 staff (92 FTE)• $23M budget• 501(c)(3)• Student programs serve over 30,000 schools and

more than 1 million students• Own HQ building w/35,000+ sq. ft. – Reston, VA

©2012 CliftonLarsonAllen LLP46

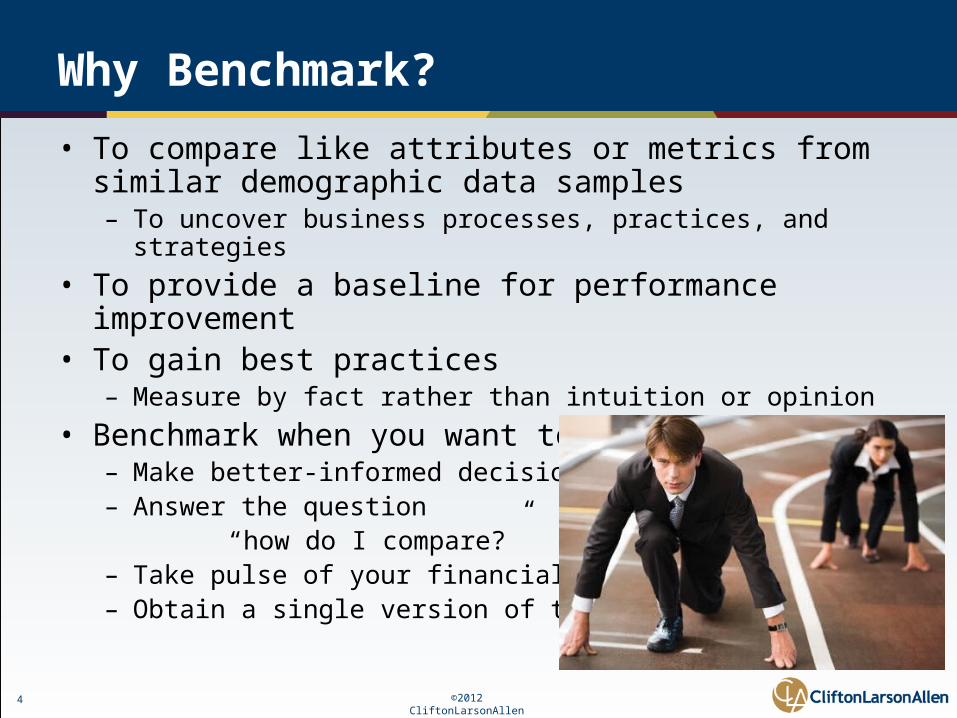

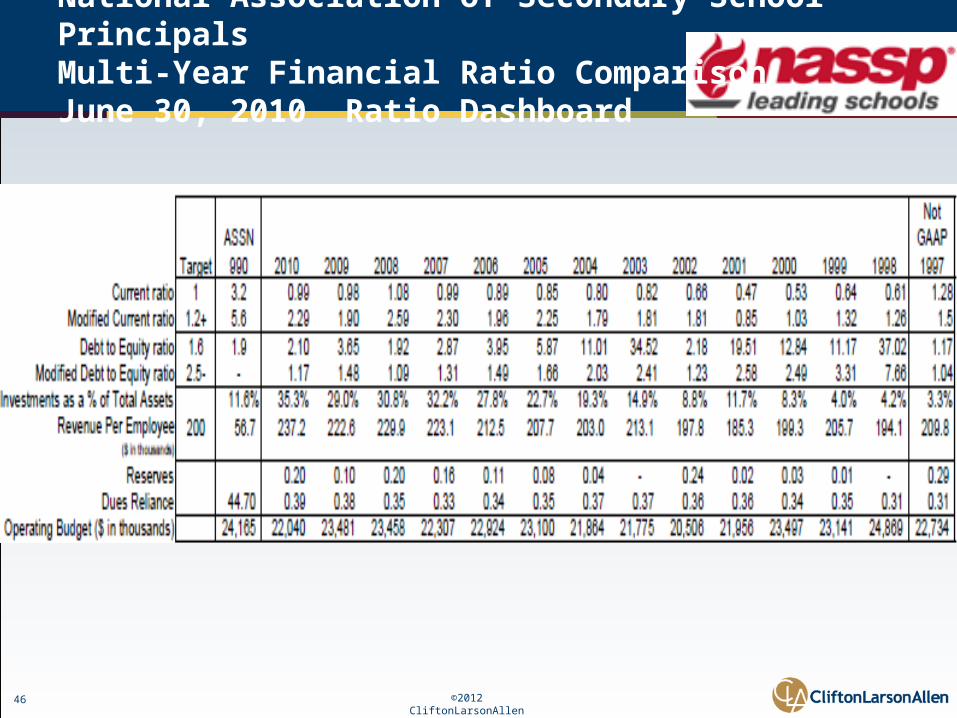

National Association of Secondary School PrincipalsMulti-Year Financial Ratio ComparisonJune 30, 2010 Ratio Dashboard

©2012 CliftonLarsonAllen LLP47474747

©20

12 C

lifto

nLar

sonA

llen

LLP

2010

National Associationof

Secondary School Principals

©2012 CliftonLarsonAllen LLP48

Total LiabilitiesTotal Net Assets

Statement of Financial PositionLiabilities and Net Assets

©2012 CliftonLarsonAllen LLP49

Total Liabilities -- $11,713,093

Total Net Assets – $5,582,436

2.10

Displays on the Dashboard

Current Ratio

©2012 CliftonLarsonAllen LLP50

National Association of Secondary School PrincipalsMulti-Year Financial Ratio ComparisonJune 30, 2010

Debt to Equity

©2012 CliftonLarsonAllen LLP51

National Association of Secondary School PrincipalsMulti-Year Financial Ratio ComparisonJune 30, 2010

©2012 CliftonLarsonAllen LLP52

National Association of Secondary School PrincipalsMulti-Year Financial Ratio ComparisonJune 30, 2010

©2012 CliftonLarsonAllen LLP53

That’s a Wrap!