Embed Size (px)

Citation preview

1

2012 Half Year Result Briefing9 February 2012

Mr Stuart KennyCEO & Managing Director

Mr Anthony HardwickChief Financial Officer

2

Disclaimer

The information in this presentation:

• Is not an offer or recommendation to purchase or subscribe for securities in AusGroup Limited or to retain any securities currently held

• Does not take into account the potential and current individual investment objectives or the financial situation of investors

• Was prepared with due care and attention and is current at the date of the presentation

• Actual results may materially vary from any forecasts (where applicable) in the presentation

3

Agenda

• Highlights

• Financial Summary and Segment Analysis

• Business Update

• Strategy and Outlook

4

Financial (6 months

to Dec 2011)

Operating

Strategic

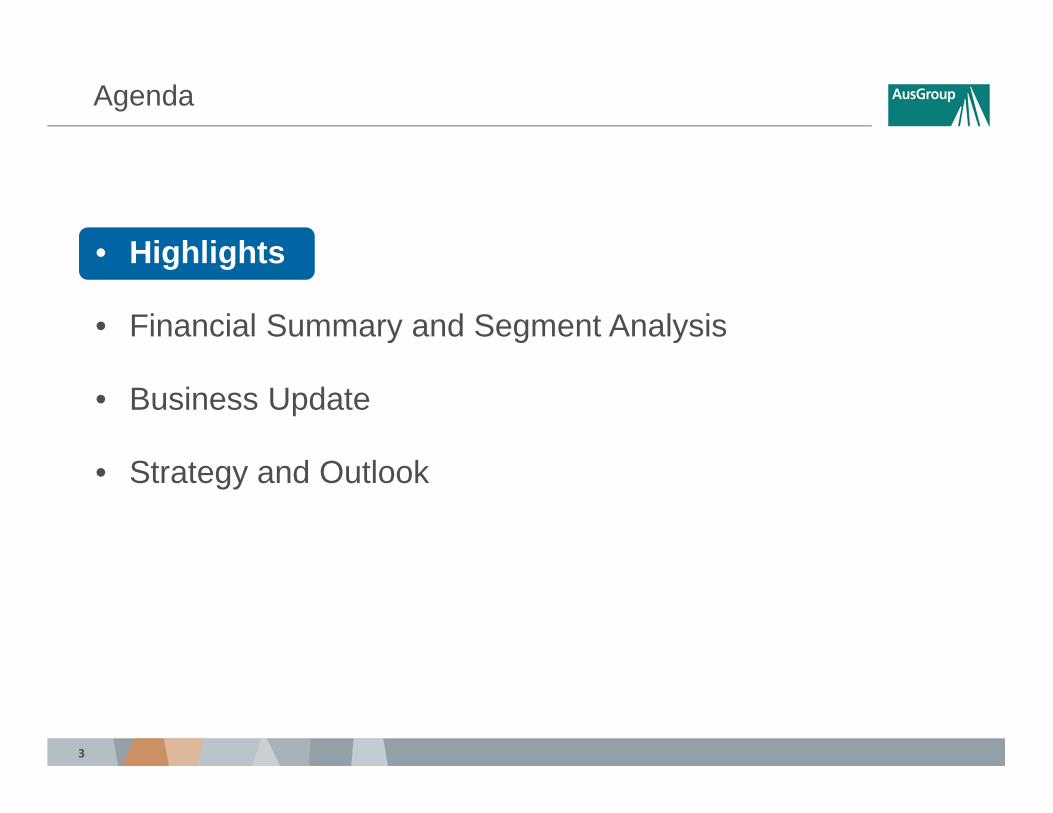

H1 FY2012 Highlights

• Revenue � 8% to A$274.4M

• EBIT Margin ����69% to 5.2%

• NPAT ����63% to A$8.3M

• Basic EPS ����38% to 1.8cps

• Net cash flow from operating activities ����12 times to A$10.6M

• Net debt to equity ratio -3.23% (FY11: -3.30%)

• Order book of A$321M (as of end Dec 2011)

• A$365M in new contracts & extensions secured in H1FY12

• Strong performance again from Integrated Services

• Improved group safety performance - TRIFR 4.46 (FY11: 3.95), LTIFR 0.34 (FY11: 0.00)

• Workforce numbers at 2,716* (� 27% from FY11)

• Project pipeline visibility

• Completed acquisition of Subsea Pressure Controls

• Strong pipeline

• Expansion in new geographical areas

*Employee numbers are as at 31 December 2011

5

Agenda

• Highlights

• Financial Summary and Segment Analysis

• Business Update

• Strategy and Outlook

6

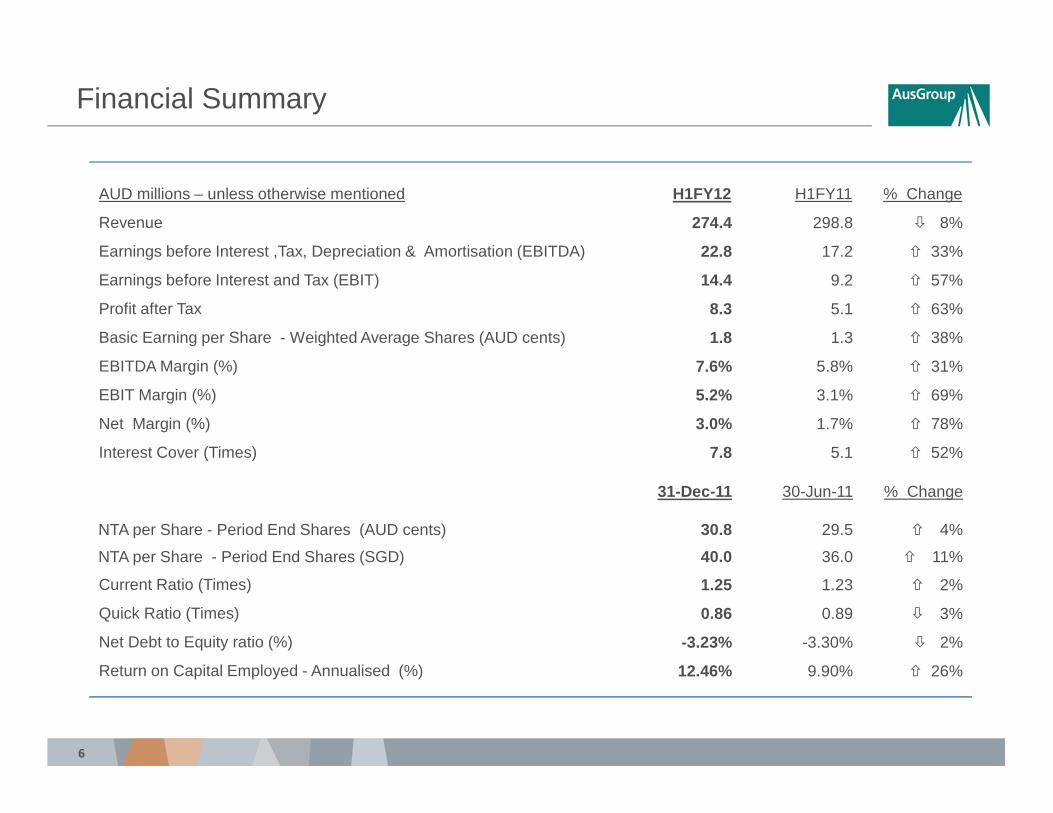

Financial Summary

AUD millions – unless otherwise mentioned H1FY12 H1FY11 % Change

Revenue 274.4 298.8 � 8%

Earnings before Interest ,Tax, Depreciation & Amortisation (EBITDA) 22.8 17.2 � 33%

Earnings before Interest and Tax (EBIT) 14.4 9.2 � 57%

Profit after Tax 8.3 5.1 � 63%

Basic Earning per Share - Weighted Average Shares (AUD cents) 1.8 1.3 � 38%

EBITDA Margin (%) 7.6% 5.8% � 31%

EBIT Margin (%) 5.2% 3.1% � 69%

Net Margin (%) 3.0% 1.7% � 78%

Interest Cover (Times) 7.8 5.1 � 52%

31-Dec-11 30-Jun-11 % Change

NTA per Share - Period End Shares (AUD cents) 30.8 29.5 � 4%

NTA per Share - Period End Shares (SGD) 40.0 36.0 � 11%

Current Ratio (Times) 1.25 1.23 � 2%

Quick Ratio (Times) 0.86 0.89 � 3%

Net Debt to Equity ratio (%) -3.23% -3.30% � 2%

Return on Capital Employed - Annualised (%) 12.46% 9.90% � 26%

7

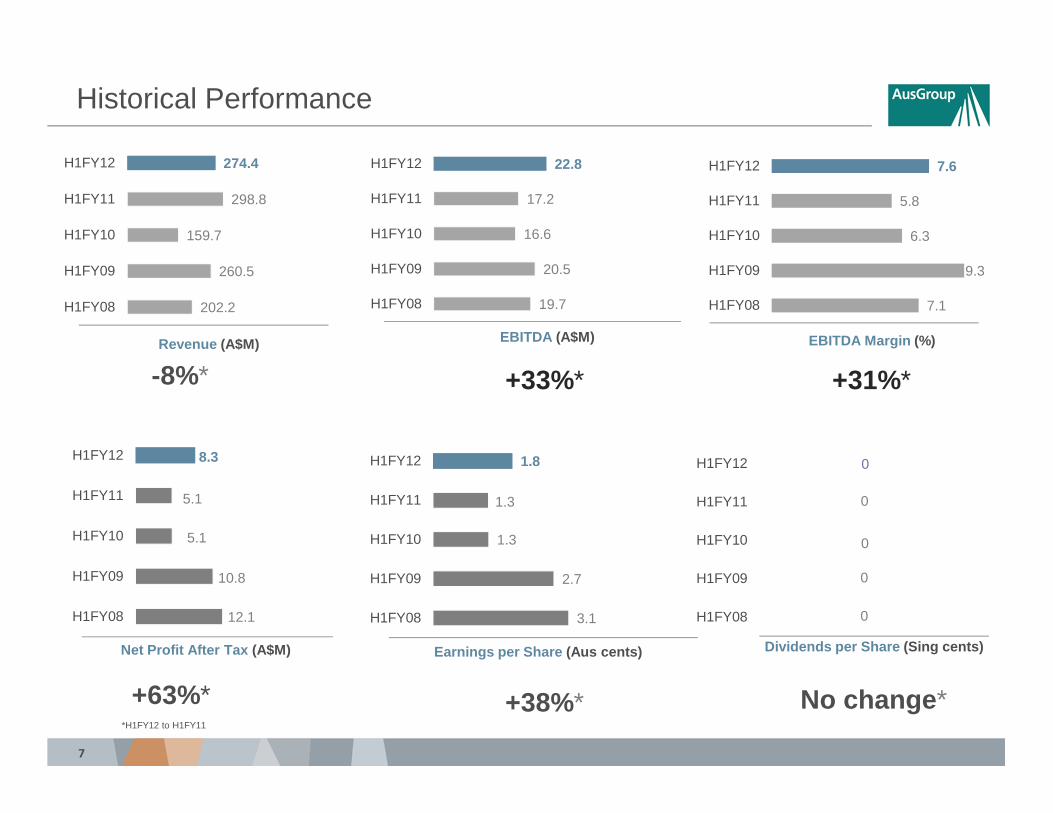

Historical Performance

202.2

260.5

159.7

298.8

274.4

H1FY08

H1FY09

H1FY10

H1FY11

H1FY12

Revenue (A$M)

19.7

20.5

16.6

17.2

22.8

H1FY08

H1FY09

H1FY10

H1FY11

H1FY12

EBITDA (A$M)

7.1

9.3

6.3

5.8

7.6

H1FY08

H1FY09

H1FY10

H1FY11

H1FY12

EBITDA Margin (%)

12.1

10.8

5.1

5.1

8.3

H1FY08

H1FY09

H1FY10

H1FY11

H1FY12

Net Profit After Tax (A$M)

0

0

0

0

0

H1FY08

H1FY09

H1FY10

H1FY11

H1FY12

Dividends per Share (Sing cents)

-8%* +33%* +31%*

*H1FY12 to H1FY11

+63%* +38%* No change *

3.1

2.7

1.3

1.3

1.8

H1FY08

H1FY09

H1FY10

H1FY11

H1FY12

Earnings per Share (Aus cents)

Contribution by Division

A$379M A$478M A$367M

Contribution by Sector

Revenue Contribution

A$602M

Contribution by Geography

46%

60%53%

40%

18%

29%

30%

19%

17%

17%

25%

10%

28%

43%

65%

FY08 FY09 FY10 FY11 H1FY12

Integrated Services

Fabrication & Manufacturing

Major Projects

28%36%

56% 55%66%

72%64%

44% 45%34%

FY08 FY09 FY10 FY11 H1FY12

Oil & Gas Mineral Resources

A$274M A$379M A$478M A$367M A$602M A$274M A$379M A$478M A$367M A$602M A$274M

94% 94%89% 93% 93%

6% 6%11% 7% 7%

FY08 FY09 FY10 FY11 H1FY12

I Australia Asia

9

Agenda

• Highlights

• Financial Summary and Analysis

• Business Unit Update

• Strategy and Outlook

10

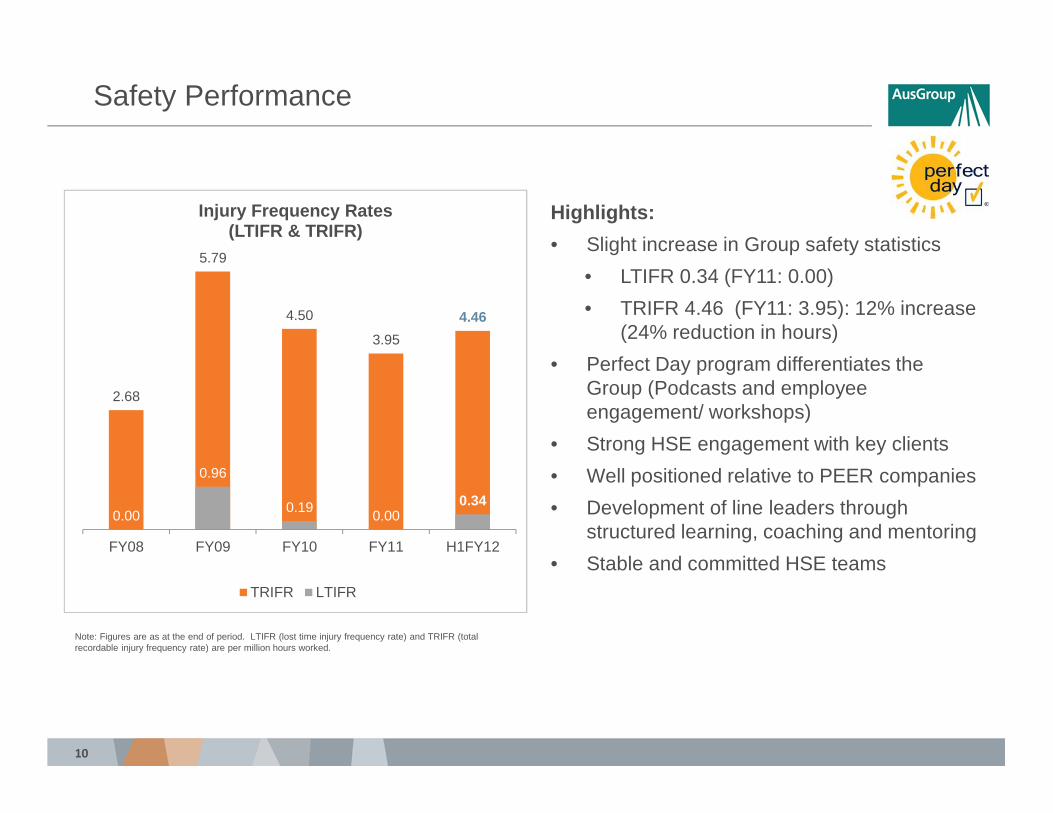

Safety Performance

2.68

5.79

4.50

3.95

4.46

0.00

0.96

0.190.00

0.34

FY08 FY09 FY10 FY11 H1FY12

Injury Frequency Rates (LTIFR & TRIFR)

TRIFR LTIFR

Highlights:

• Slight increase in Group safety statistics

• LTIFR 0.34 (FY11: 0.00)

• TRIFR 4.46 (FY11: 3.95): 12% increase (24% reduction in hours)

• Perfect Day program differentiates the Group (Podcasts and employee engagement/ workshops)

• Strong HSE engagement with key clients

• Well positioned relative to PEER companies

• Development of line leaders through structured learning, coaching and mentoring

• Stable and committed HSE teams

Note: Figures are as at the end of period. LTIFR (lost time injury frequency rate) and TRIFR (total recordable injury frequency rate) are per million hours worked.

11

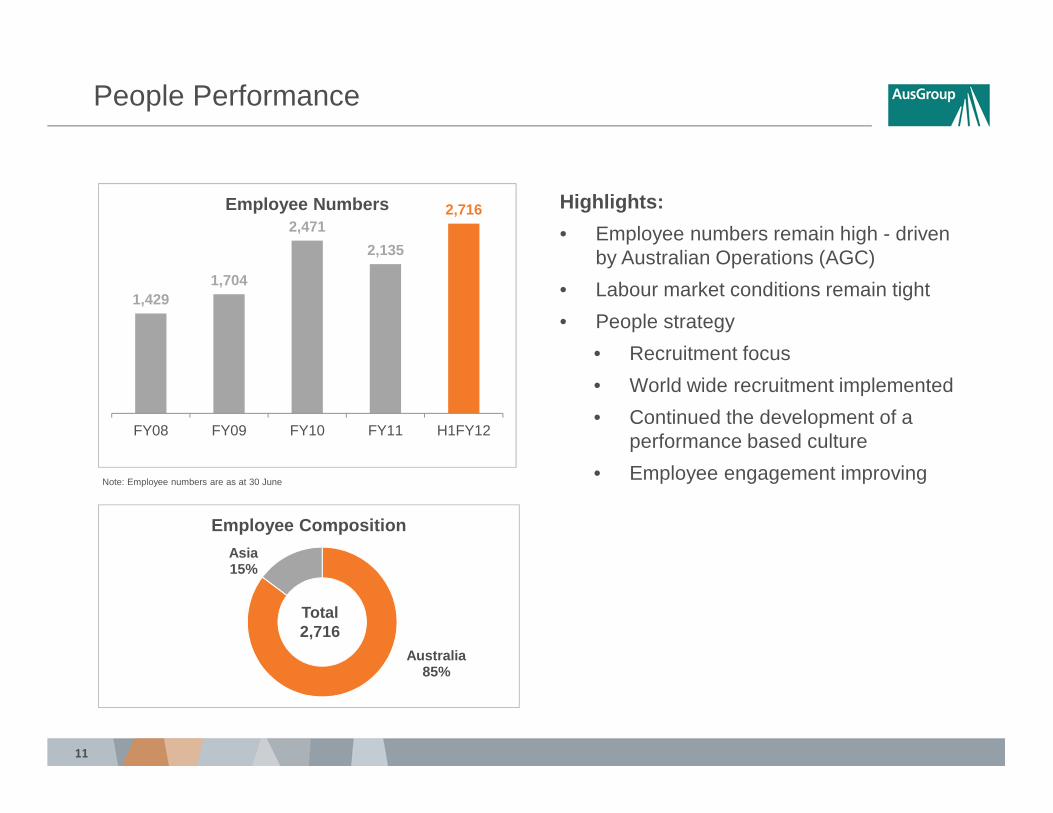

People Performance

Highlights:

• Employee numbers remain high - driven by Australian Operations (AGC)

• Labour market conditions remain tight

• People strategy

• Recruitment focus

• World wide recruitment implemented

• Continued the development of a performance based culture

• Employee engagement improving

1,4291,704

2,471

2,135

2,716

FY08 FY09 FY10 FY11 H1FY12

Employee Numbers

Note: Employee numbers are as at 30 June

Australia85%

Asia15%

Employee Composition

Total2,716

12

Fabrication & Manufacturing

52.8

46.8

H1FY11

H1FY12

Revenue (A$M)

Major Contracts Undertaken During The Period:• Transfield Worley Woodside Alliance - North West Fabrication

Contract (multi year contract)

• Outotec – Filter Assembly

• Metso Minerals - FMG Car Dumpers and Positioners (Restart Order)

• Metso Minerals - BHPB RGP 6 Car Dumpers & Positioners

• Chevron Australia - Gorgon Pipe Spools

• Chevron Australia - Gorgon Adjustable Pipe Supports

• Vetco - Ongoing Repeat Order (AusGroup Singapore)

• Aker - Frigstad Riser Project (AusGroup Singapore)

Fabrication & Manufacturing,

17%

Other, 83%

H1FY12 Revenue Contribution (%)

Major Contracts Won:• CB&I - Shear Keys

• Kiewiet – Plate Work

• Mammoet – Transport Frames

• Brockman 4 – Fabrication Work for MP

0.8

-0.5

H1FY11

H1FY12

EBIT (A$M)

13

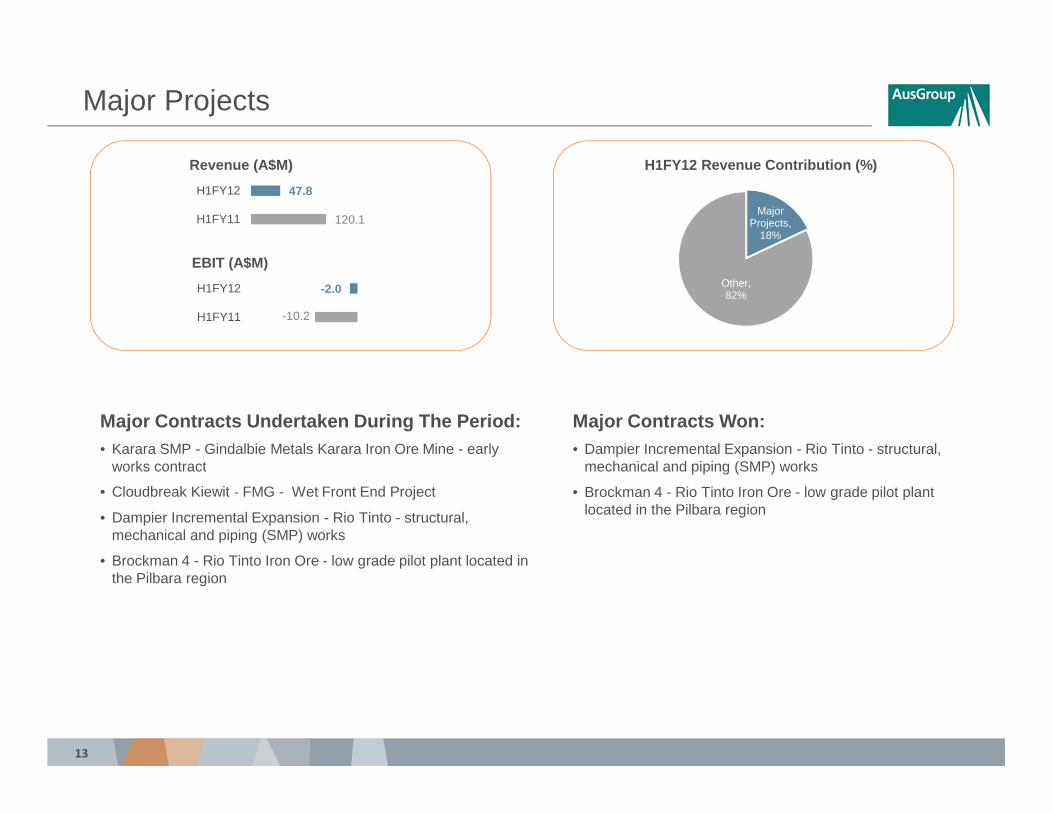

Major Projects

Major Contracts Undertaken During The Period:• Karara SMP - Gindalbie Metals Karara Iron Ore Mine - early

works contract

• Cloudbreak Kiewit - FMG - Wet Front End Project

• Dampier Incremental Expansion - Rio Tinto - structural, mechanical and piping (SMP) works

• Brockman 4 - Rio Tinto Iron Ore - low grade pilot plant located in the Pilbara region

Major Projects,

18%

Other, 82%

H1FY12 Revenue Contribution (%)

Major Contracts Won:• Dampier Incremental Expansion - Rio Tinto - structural,

mechanical and piping (SMP) works

• Brockman 4 - Rio Tinto Iron Ore - low grade pilot plant located in the Pilbara region

120.1

47.8

H1FY11

H1FY12

Revenue (A$M)

-10.2

-2.0

H1FY11

H1FY12

EBIT (A$M)

14

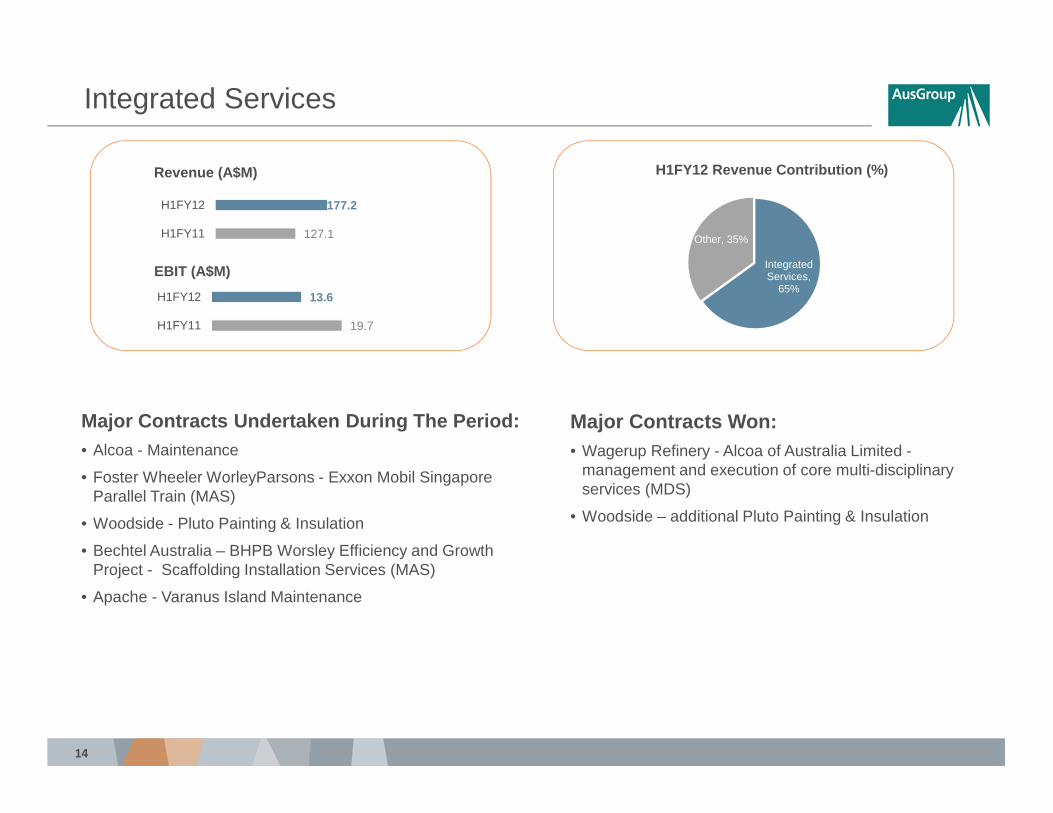

Integrated Services

Major Contracts Undertaken During The Period :• Alcoa - Maintenance

• Foster Wheeler WorleyParsons - Exxon Mobil Singapore Parallel Train (MAS)

• Woodside - Pluto Painting & Insulation

• Bechtel Australia – BHPB Worsley Efficiency and Growth Project - Scaffolding Installation Services (MAS)

• Apache - Varanus Island Maintenance

Integrated Services,

65%

Other, 35%

H1FY12 Revenue Contribution (%)

Major Contracts Won:• Wagerup Refinery - Alcoa of Australia Limited -

management and execution of core multi-disciplinary services (MDS)

• Woodside – additional Pluto Painting & Insulation

127.1

177.2

H1FY11

H1FY12

Revenue (A$M)

19.7

13.6

H1FY11

H1FY12

EBIT (A$M)

15

Agenda

• Highlights

• Financial Summary and Analysis

• Business Unit Update

• Strategy and Outlook

16

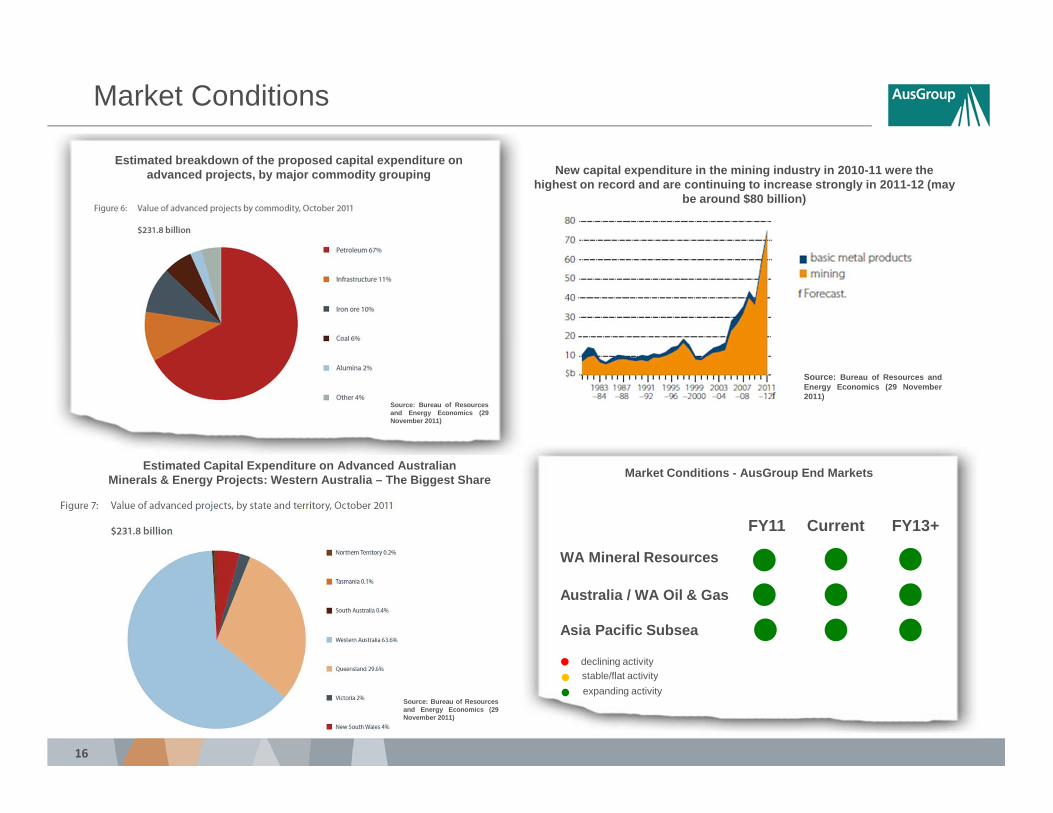

Market Conditions

Market Conditions - AusGroup End Markets

FY11

WA Mineral Resources

Australia / WA Oil & Gas

Asia Pacific Subsea

declining activitystable/flat activity

expanding activity

Current

Estimated Capital Expenditure on Advanced Australia n Minerals & Energy Projects: Western Australia – The Biggest Share

New capital expenditure in the mining industry in 2 010-11 were the highest on record and are continuing to increase str ongly in 2011-12 (may

be around $80 billion)

FY13+

Source: Bureau of Resources andEnergy Economics (29 November2011)

Source: Bureau of Resourcesand Energy Economics (29November 2011)

Estimated breakdown of the proposed capital expendi ture on advanced projects, by major commodity grouping

Source: Bureau of Resourcesand Energy Economics (29November 2011)

17

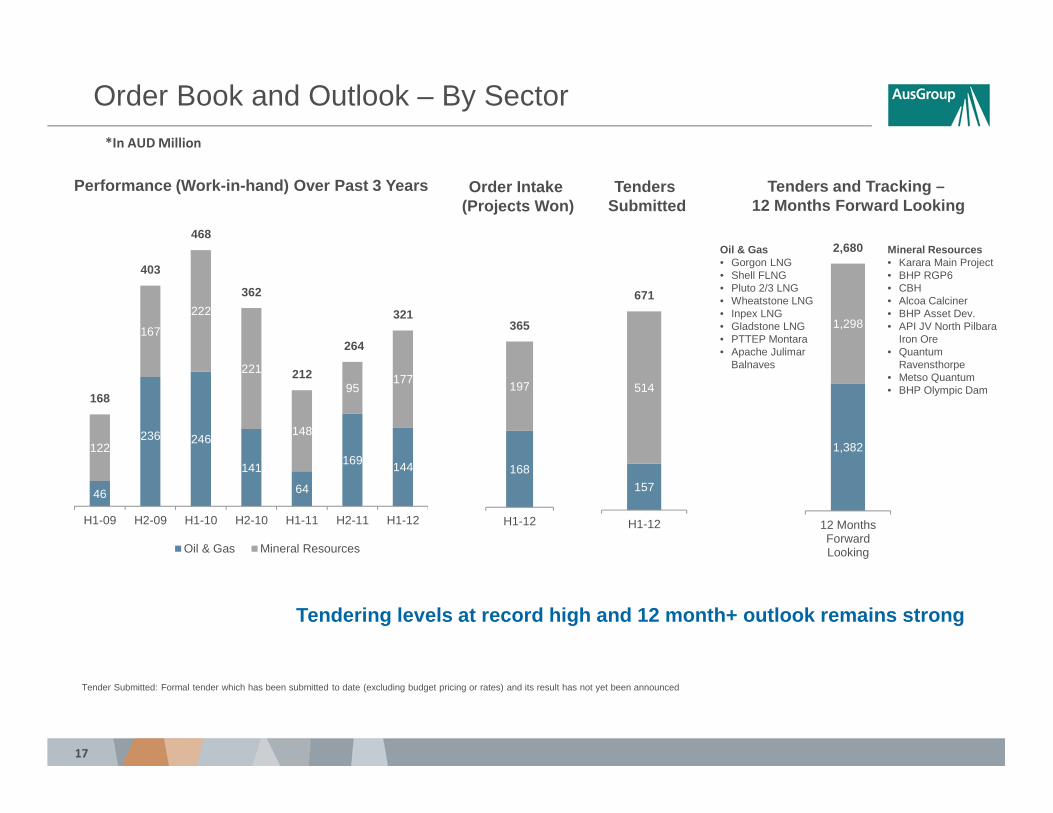

Tendering levels at record high and 12 month+ outloo k remains strong

Tenders and Tracking –12 Months Forward Looking

Performance (Work-in-hand) Over Past 3 Years

168

197

365

H1-12

Order Intake (Projects Won)

Tenders Submitted

*In AUD Million

157

514

671

H1-12

Oil & Gas• Gorgon LNG• Shell FLNG• Pluto 2/3 LNG• Wheatstone LNG • Inpex LNG• Gladstone LNG• PTTEP Montara• Apache Julimar

Balnaves

Mineral Resources• Karara Main Project• BHP RGP6• CBH • Alcoa Calciner• BHP Asset Dev.• API JV North Pilbara

Iron Ore• Quantum

Ravensthorpe• Metso Quantum• BHP Olympic Dam

Tender Submitted: Formal tender which has been submitted to date (excluding budget pricing or rates) and its result has not yet been announced

Order Book and Outlook – By Sector

46

236 246

141

64

169 144

122

167

222

221

148

95177

168

403

468

362

212

264

321

H1-09 H2-09 H1-10 H2-10 H1-11 H2-11 H1-12

Oil & Gas Mineral Resources

1,382

1,298

2,680

12 MonthsForwardLooking

18

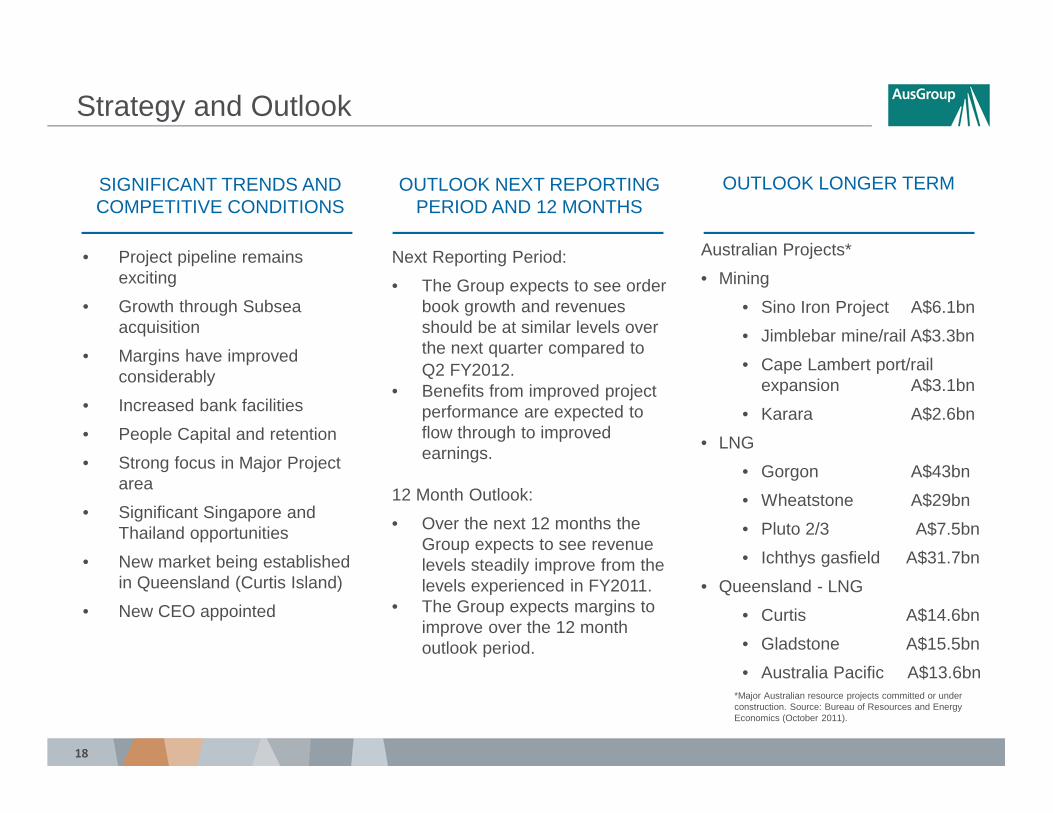

Strategy and Outlook

SIGNIFICANT TRENDS AND COMPETITIVE CONDITIONS

OUTLOOK NEXT REPORTING PERIOD AND 12 MONTHS

OUTLOOK LONGER TERM

• Project pipeline remains exciting

• Growth through Subsea acquisition

• Margins have improved considerably

• Increased bank facilities

• People Capital and retention

• Strong focus in Major Project area

• Significant Singapore and Thailand opportunities

• New market being established in Queensland (Curtis Island)

• New CEO appointed

Next Reporting Period:

• The Group expects to see order book growth and revenues should be at similar levels over the next quarter compared to Q2 FY2012..

• Benefits from improved project performance are expected to flow through to improved earnings.

12 Month Outlook:

• Over the next 12 months the Group expects to see revenue levels steadily improve from the levels experienced in FY2011.

• The Group expects margins to improve over the 12 month outlook period.

Australian Projects*

• Mining

• Sino Iron Project A$6.1bn

• Jimblebar mine/rail A$3.3bn

• Cape Lambert port/rail expansion A$3.1bn

• Karara A$2.6bn

• LNG

• Gorgon A$43bn

• Wheatstone A$29bn

• Pluto 2/3 A$7.5bn

• Ichthys gasfield A$31.7bn

• Queensland - LNG

• Curtis A$14.6bn

• Gladstone A$15.5bn

• Australia Pacific A$13.6bn*Major Australian resource projects committed or under construction. Source: Bureau of Resources and Energy Economics (October 2011).

19

2012 Half Year Result Briefing9 February 2012

Mr Stuart KennyCEO & Managing Director

Mr Anthony HardwickChief Financial Officer

End of presentation• For additional information, please visit our website

www.agc-ausgroup.com

20

2012 Half Year Results – AppendixAdditional Information9 February 2012

Mr Stuart KennyCEO & Managing Director

Mr Anthony HardwickChief Financial Officer

21

Appendix

• Company Snapshot

• Business Model

• AusGroup Operations

• Additional Market Outlook Data

22

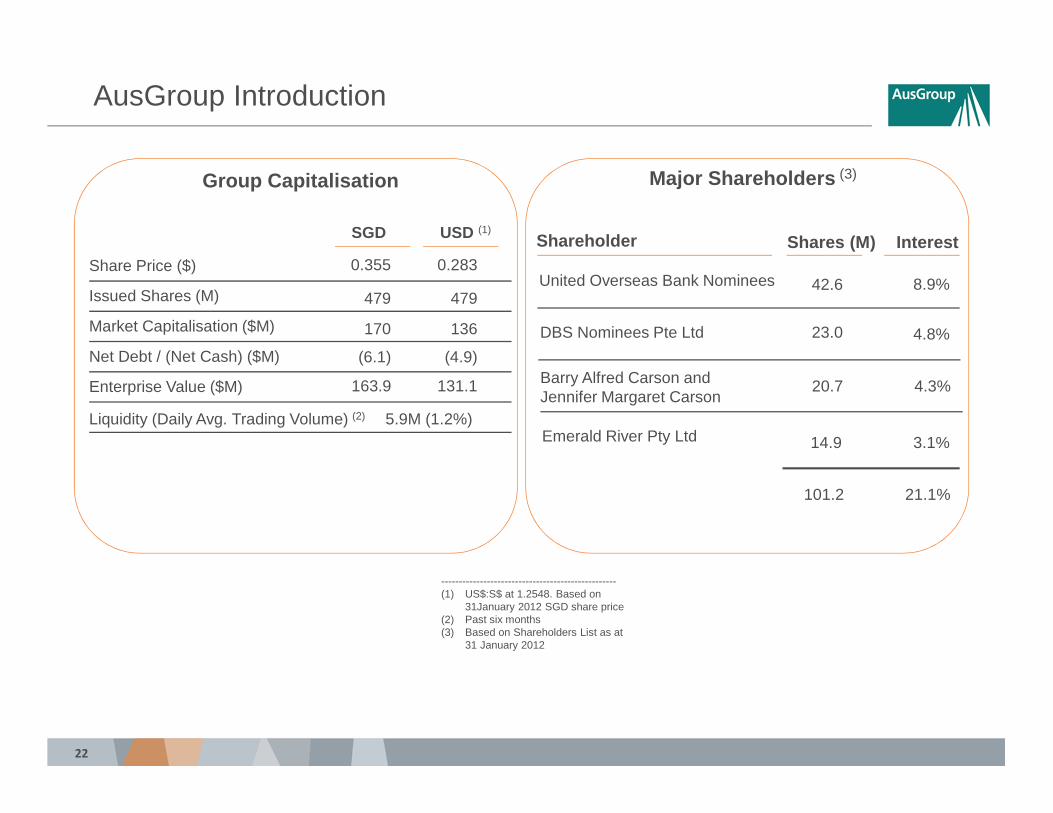

Group Capitalisation Major Shareholders (3)

SGD USD (1)

AusGroup Introduction

Enterprise Value ($M)

Liquidity (Daily Avg. Trading Volume) (2)

Net Debt / (Net Cash) ($M)

0.355Share Price ($)

Issued Shares (M)

Market Capitalisation ($M)

479

170

(6.1)

163.9

5.9M (1.2%)

0.283

479

136

(4.9)

131.1

--------------------------------------------------(1) US$:S$ at 1.2548. Based on

31January 2012 SGD share price(2) Past six months(3) Based on Shareholders List as at

31 January 2012

42.6United Overseas Bank Nominees

Emerald River Pty Ltd

Shares (M) Interest

14.9

8.9%

3.1%

Shareholder

101.2 21.1%

23.0DBS Nominees Pte Ltd 4.8%

20.7Barry Alfred Carson and Jennifer Margaret Carson

4.3%

23

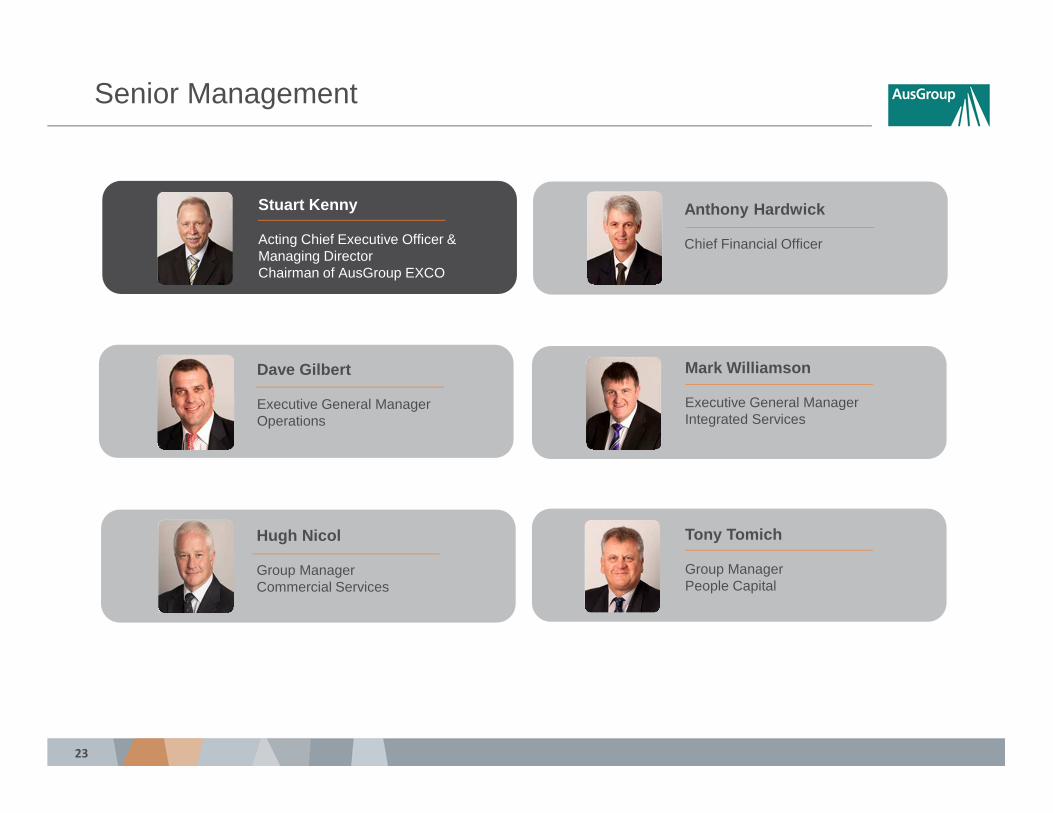

Senior Management

Hugh Nicol

Group Manager Commercial Services

Tony Tomich

Group Manager People Capital

Anthony Hardwick

Chief Financial Officer

Mark Williamson

Executive General Manager Integrated Services

Dave Gilbert

Executive General ManagerOperations

Stuart Kenny

Acting Chief Executive Officer & Managing DirectorChairman of AusGroup EXCO

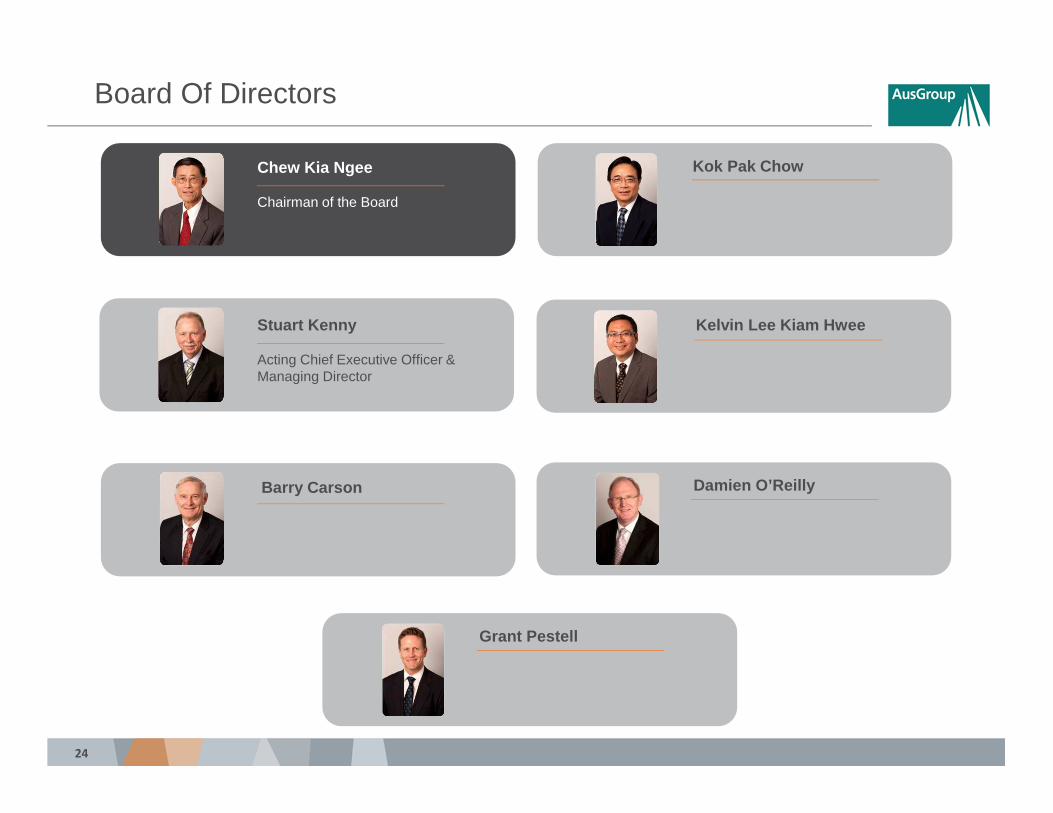

24

Board Of Directors

Barry Carson Damien O’Reilly

Kok Pak Chow

Kelvin Lee Kiam HweeStuart Kenny

Acting Chief Executive Officer & Managing Director

Chew Kia Ngee

Chairman of the Board

Grant Pestell

25

Our Values

Our Values

Our values guide our behaviours. They reflect the way we go about our business and are core to everything we do.

Safety & Wellbeing

We care about our people. For us this means the health and safety of our people at our work place, the impact we have on the environment and the communities we work in, and the support, encouragement and opportunities we provide to each other as we strive for our personal and professional goals.

Integrity

We are open, honest, consistent and fair in what we say, what we do and how we work together.

Mutual Accountability

We are responsible to each other and the teams we work in. We rely on each other to do the right thing to achieve our shared goals and aspirations. We shall be accountable for our words, our work and our actions.

Excellence

We set high standards in everything we do. We value being the best we possibly can be - as an individual, as a team and as a Company.

Courage

To be bold, to innovate, to challenge and to improve in everything that we do. We encourage our people to step up and take the initiative to challenge our performance, to push our boundaries and barriers and to continually improve ourselves and our Company.

26

Appendix

• Company Snapshot

• Business Model

• AusGroup Operations

• Additional Market Outlook Data

27

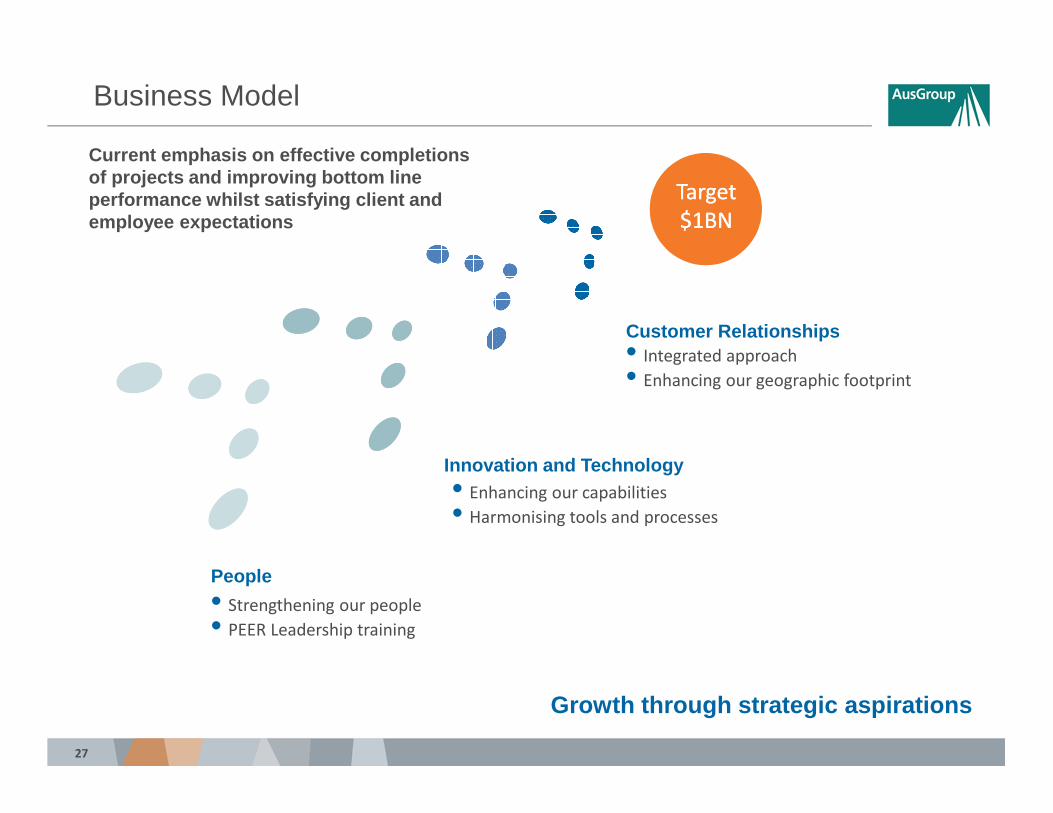

Business Model

• Integrated approach

• Enhancing our geographic footprint

Customer Relationships

• Enhancing our capabilities

• Harmonising tools and processes

Innovation and Technology

• Strengthening our people

• PEER Leadership training

People

Growth through strategic aspirations

Target

$1BN

Target

$1BN

Current emphasis on effective completions of projects and improving bottom line performance whilst satisfying client and employee expectations

28

Appendix

• Company Snapshot

• Business Model

• AusGroup Operations

• Additional Market Outlook Data

29

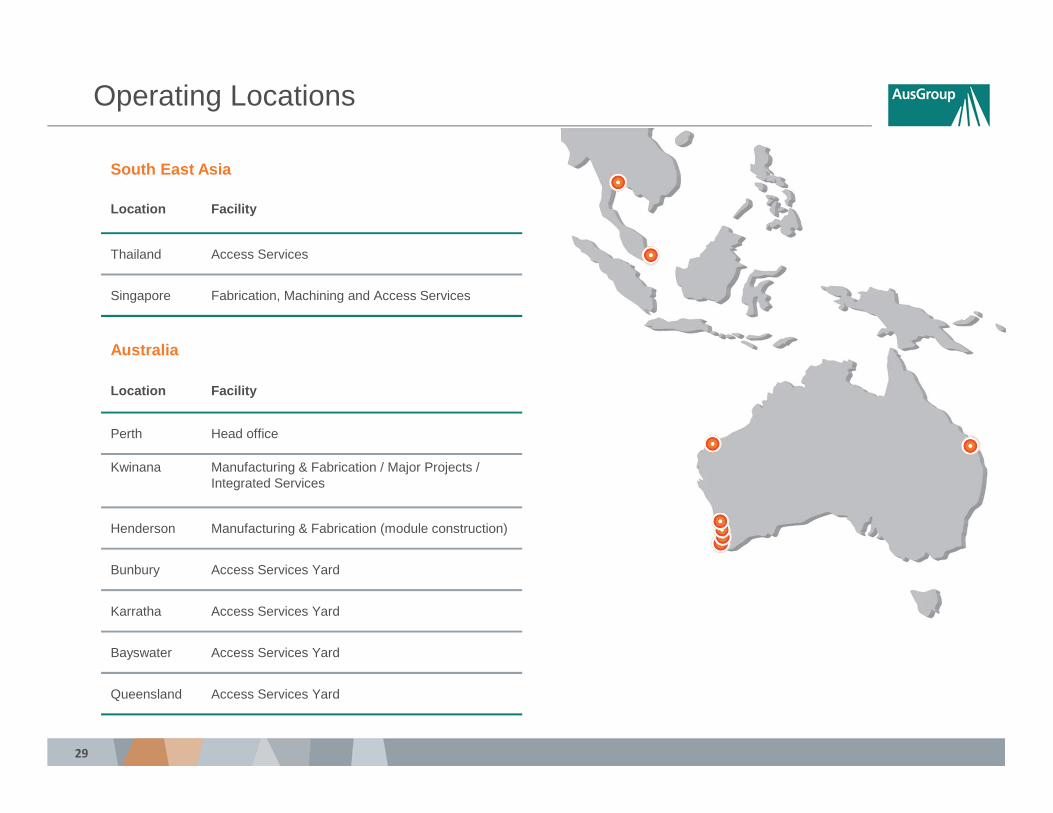

Operating Locations

South East Asia

Location Facility

Thailand Access Services

Singapore Fabrication, Machining and Access Services

Australia

Location Facility

Perth Head office

Kwinana Manufacturing & Fabrication / Major Projects / Integrated Services

Henderson Manufacturing & Fabrication (module construction)

Bunbury Access Services Yard

Karratha Access Services Yard

Bayswater Access Services Yard

Queensland Access Services Yard

30

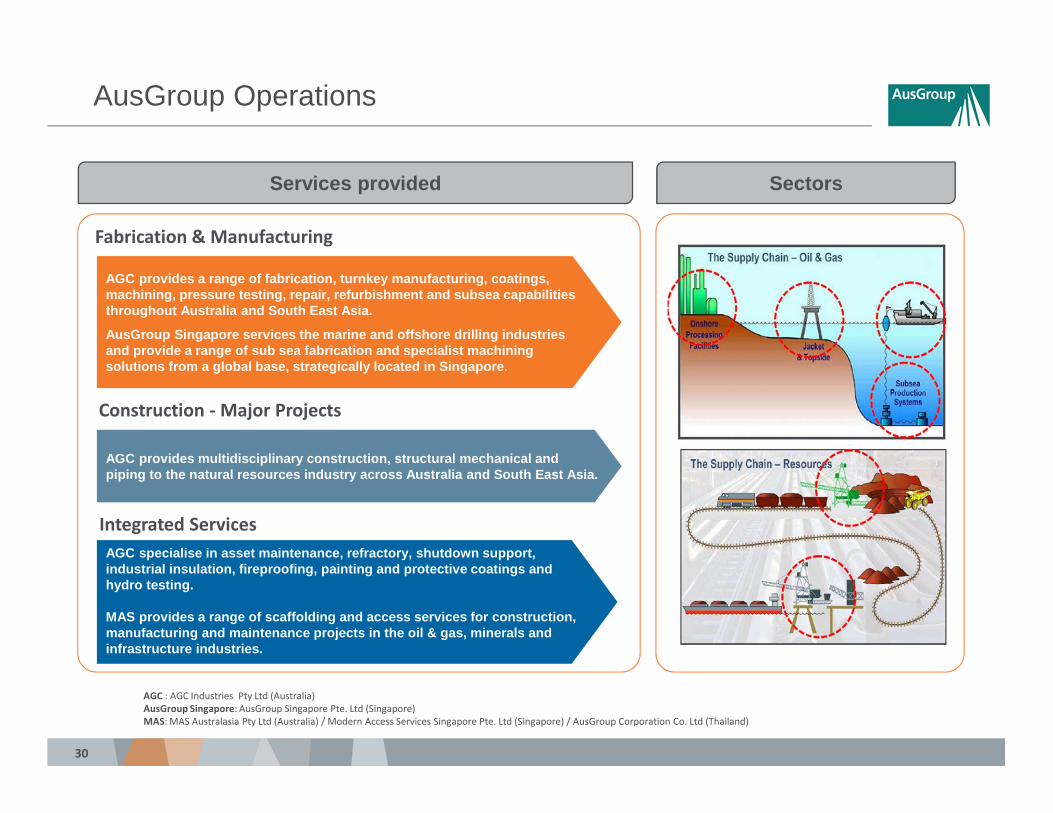

AusGroup Operations

AGC specialise in asset maintenance, refractory, sh utdown support, industrial insulation, fireproofing, painting and p rotective coatings and hydro testing.

MAS provides a range of scaffolding and access serv ices for construction, manufacturing and maintenance projects in the oil & gas, minerals and infrastructure industries.

AGC provides a range of fabrication, turnkey manufac turing, coatings, machining, pressure testing, repair, refurbishment and subsea capabilities throughout Australia and South East Asia.

AusGroup Singapore services the marine and offshore drilling industries and provide a range of sub sea fabrication and spec ialist machining solutions from a global base, strategically located in Singapore .

AGC provides multidisciplinary construction, struct ural mechanical and piping to the natural resources industry across Aus tralia and South East Asia.

Construction - Major Projects

Integrated Services

Fabrication & Manufacturing

Services provided Sectors

AGC : AGC Industries Pty Ltd (Australia)

AusGroup Singapore: AusGroup Singapore Pte. Ltd (Singapore)

MAS: MAS Australasia Pty Ltd (Australia) / Modern Access Services Singapore Pte. Ltd (Singapore) / AusGroup Corporation Co. Ltd (Thailand)

31

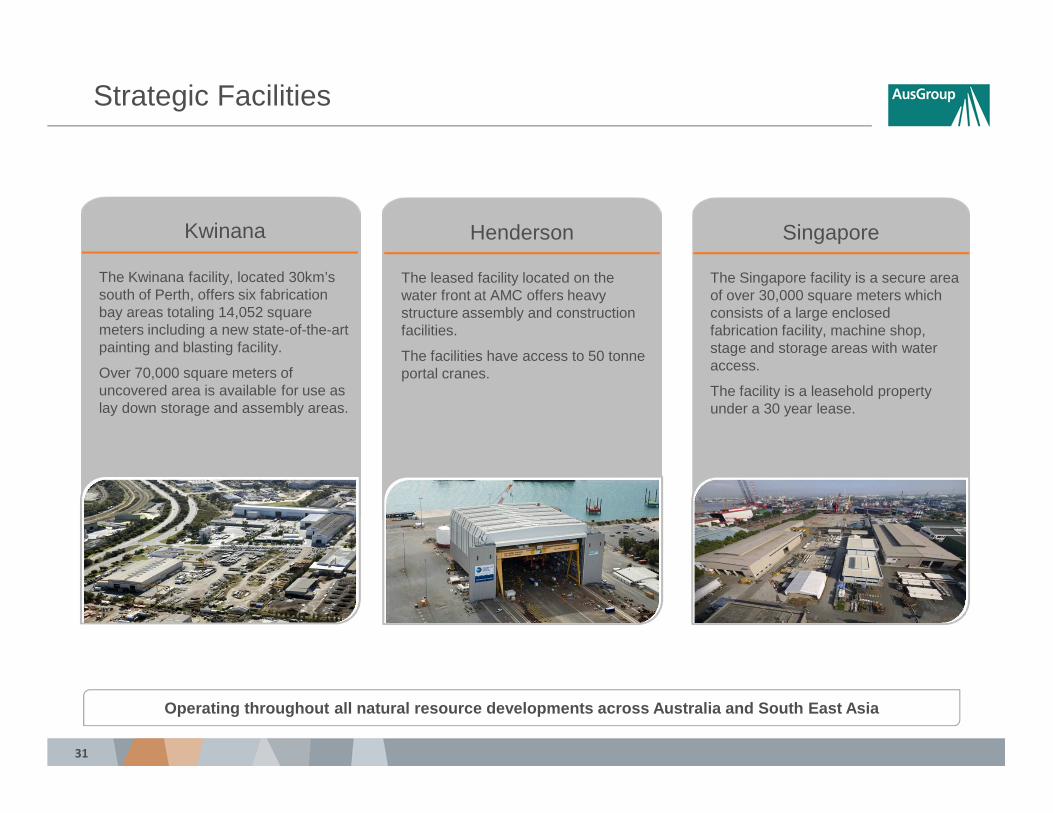

Strategic Facilities

Operating throughout all natural resource developme nts across Australia and South East Asia

Kwinana

The Kwinana facility, located 30km’s south of Perth, offers six fabrication bay areas totaling 14,052 square meters including a new state-of-the-art painting and blasting facility.

Over 70,000 square meters of uncovered area is available for use as lay down storage and assembly areas.

Henderson

The leased facility located on the water front at AMC offers heavy structure assembly and construction facilities.

The facilities have access to 50 tonneportal cranes.

Singapore

The Singapore facility is a secure area of over 30,000 square meters which consists of a large enclosed fabrication facility, machine shop, stage and storage areas with water access.

The facility is a leasehold property under a 30 year lease.

32

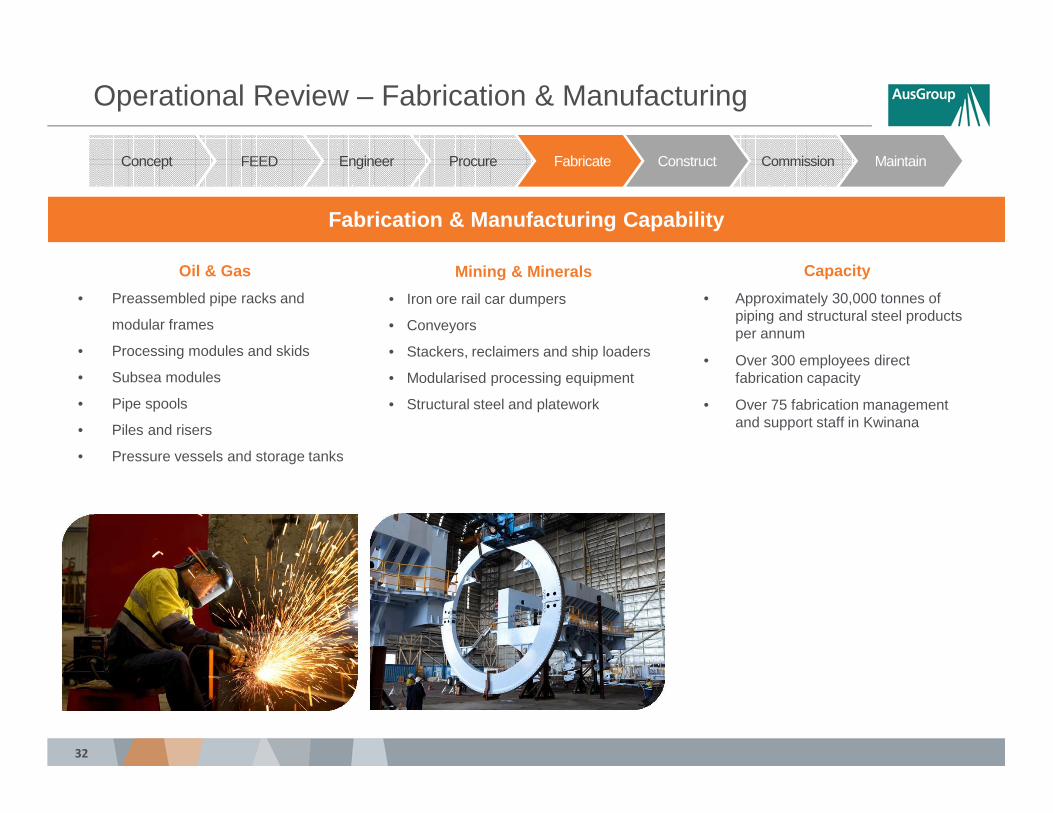

Operational Review – Fabrication & Manufacturing

Oil & Gas

• Preassembled pipe racks and

modular frames

• Processing modules and skids

• Subsea modules

• Pipe spools

• Piles and risers

• Pressure vessels and storage tanks

ProcureEngineer Fabricate Construct CommissionFEED MaintainConcept

Mining & Minerals

• Iron ore rail car dumpers

• Conveyors

• Stackers, reclaimers and ship loaders

• Modularised processing equipment

• Structural steel and platework

Fabrication & Manufacturing Capability

Capacity

• Approximately 30,000 tonnes of piping and structural steel products per annum

• Over 300 employees direct fabrication capacity

• Over 75 fabrication management and support staff in Kwinana

33

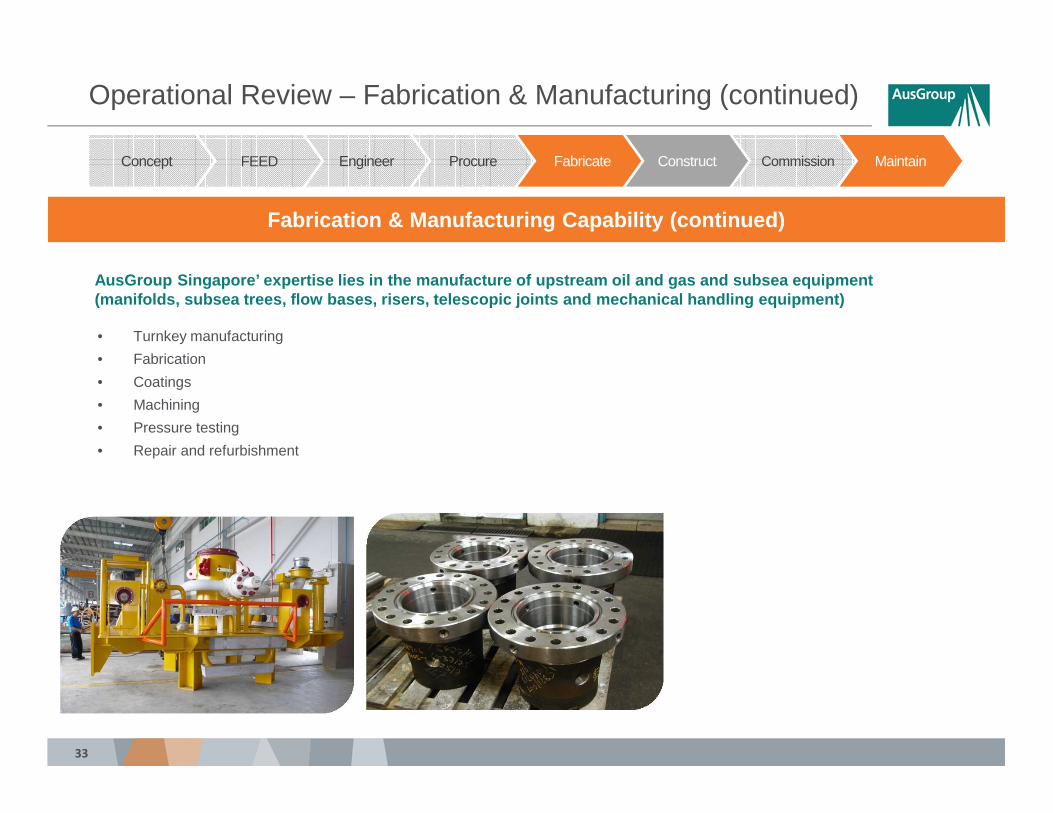

Operational Review – Fabrication & Manufacturing (continued)

ProcureEngineer Fabricate Construct CommissionFEEDConcept

Fabrication & Manufacturing Capability (continued)

AusGroup Singapore’ expertise lies in the manufactur e of upstream oil and gas and subsea equipment (manifolds, subsea trees, flow bases, risers, teles copic joints and mechanical handling equipment)

• Turnkey manufacturing

• Fabrication

• Coatings

• Machining

• Pressure testing

• Repair and refurbishment

Maintain

34

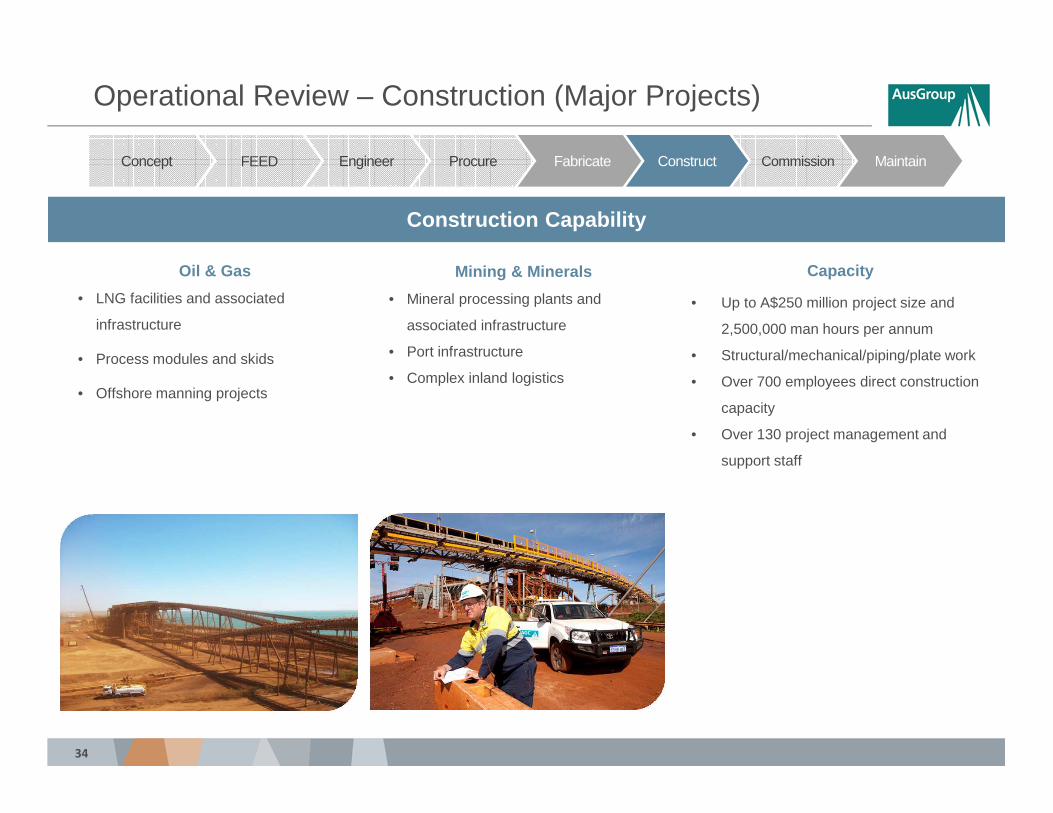

Operational Review – Construction (Major Projects)

Oil & Gas

• LNG facilities and associated

infrastructure

• Process modules and skids

• Offshore manning projects

ProcureEngineer Fabricate Construct CommissionFEED MaintainConcept

Mining & Minerals

• Mineral processing plants and

associated infrastructure

• Port infrastructure

• Complex inland logistics

Construction Capability

Capacity

• Up to A$250 million project size and

2,500,000 man hours per annum

• Structural/mechanical/piping/plate work

• Over 700 employees direct construction

capacity

• Over 130 project management and

support staff

35

Operational Review – Integrated Services

Total in-house service solutions for Oil & Gas and Mineral Resources

ProcureEngineer Fabricate Construct CommissionFEED MaintainConcept

Integrated Services Capability

• Asset maintenance, onshore and

offshore

• Shutdown support

• Commissioning

• Industrial insulation

• Fireproofing

• High end access services

• Refractory

• Hydrotesting

• Painting and protective coatings

36

Key Clients

Focused on building strategic customer relationships through:

• Existing customers, trusted partnerships

• New customers

• AGC’s unique capabilities

• Technical quality

• Value based relationships

• Consistent delivery

High quality client base across mineral resources a nd oil & gas industries

37

Current Projects

Location Cloudbreak, WAContract Value AU$40 millionContract Period Nov 2011-CurrentScope of Work The scope includes the addition of; a front end circuit of wet scrubbing and screening; new desandsmodule and tails thickening; tailings transfer and modifications to the existing desands modules for the Cloudbreak Enhancement Project at Fortescue's Cloudbreak mine site.

Cloudbreak Engineering Procurement & Construction Client: Fortescue Metals Group

Cloudbreak Early Contractor Involvement Client: Fortescue Metals Group

Location Karara, WAContract Value AU$60 millionContract Period March 2011-CurrentScope of Work Structural, mechanical and piping installation works at the company’s iron ore process plant. The Early Works contract involves all mechanical disciplines, scaffolding, rigging and procurement of piping for the main EPC contract.

Karara Early Works ContractClient: Karara Mining / Operator: Gindalbie Metals

Location Karara, WAContract Value AU$40 millionContract Period Nov 2011-CurrentScope of Work Following the award of the Early Works Contract in March 2011, AGC will continue to support KararaMining as it enters peak construction in the lead up to the first shipment of magnetite concentrate scheduled for June 2012.

Location Cloudbreak, WAContract Value AU$4.4 millionContract Period March 2011-CurrentScope of Work The contract awarded to the Cloudbreak Enhancement Project Team (CEPT), represents the first significant EPC opportunity pursued with JV partner Kiewit. The AGC Kiewit partnership, has partnered with engineer AMEC Minproc to execute the works in lead up to the full EPC contract.

Karara Preferred Supplier SMPClient: Karara Mining / Operator: Gindalbie Metals

38

Current Projects

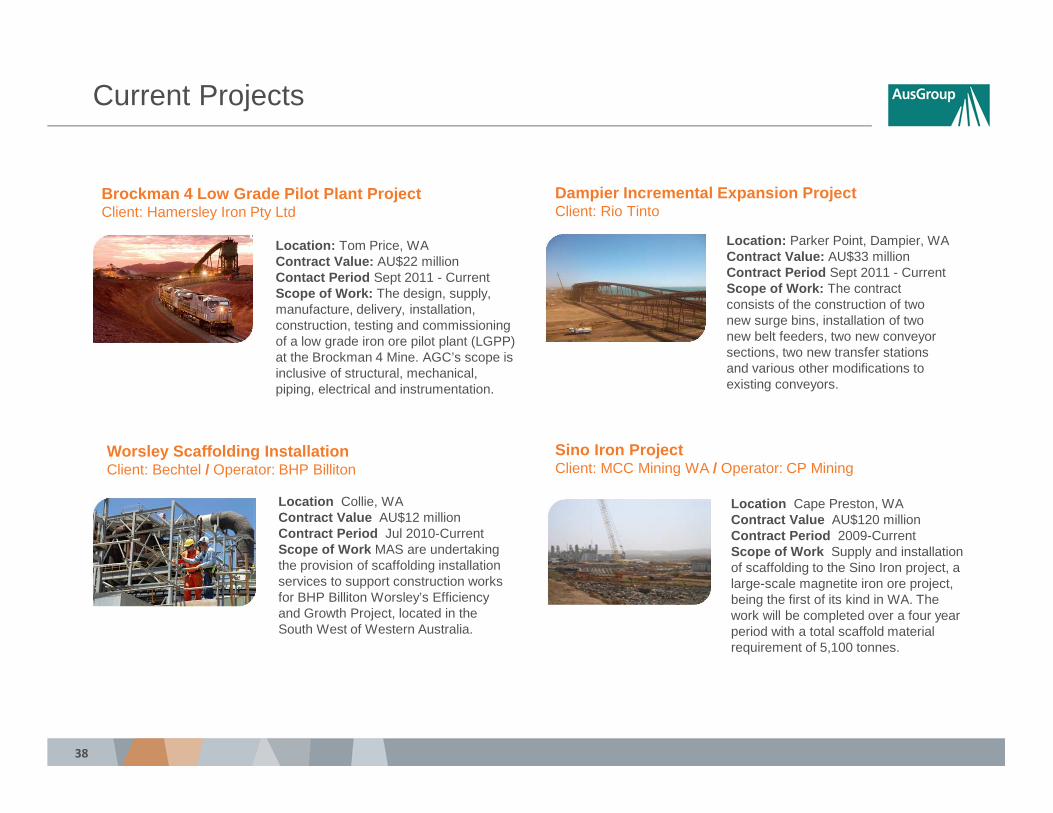

Dampier Incremental Expansion ProjectClient: Rio Tinto

Location: Parker Point, Dampier, WAContract Value: AU$33 millionContract Period Sept 2011 - CurrentScope of Work: The contract consists of the construction of two new surge bins, installation of two new belt feeders, two new conveyor sections, two new transfer stations and various other modifications to existing conveyors.

Location: Tom Price, WAContract Value: AU$22 millionContact Period Sept 2011 - CurrentScope of Work: The design, supply, manufacture, delivery, installation, construction, testing and commissioning of a low grade iron ore pilot plant (LGPP) at the Brockman 4 Mine. AGC’s scope is inclusive of structural, mechanical, piping, electrical and instrumentation.

Brockman 4 Low Grade Pilot Plant Project Client: Hamersley Iron Pty Ltd

Location Collie, WAContract Value AU$12 millionContract Period Jul 2010-CurrentScope of Work MAS are undertaking the provision of scaffolding installation services to support construction works for BHP Billiton Worsley’s Efficiency and Growth Project, located in the South West of Western Australia.

Worsley Scaffolding Installation Client: Bechtel / Operator: BHP Billiton

Sino Iron Project Client: MCC Mining WA / Operator: CP Mining

Location Cape Preston, WAContract Value AU$120 millionContract Period 2009-CurrentScope of Work Supply and installation of scaffolding to the Sino Iron project, a large-scale magnetite iron ore project, being the first of its kind in WA. The work will be completed over a four year period with a total scaffold material requirement of 5,100 tonnes.

39

Current Projects

Location North West Shelf, WAContract Value AU$5 million per annumContract Period Jan 2010-CurrentScope of Work General and campaign services, and minor capital works at Apache’s Varanus Island facilities and offshore assets. The scope involves all mechanical disciplines, sheet-metal fabrication, insulation, scaffolding, rigging and electrical and instrumentation.

Apache Integrated Services ContractClient: Apache Energy Limited

Murrin Murrin Maintenance ContractClient: Minara Resources

Location Leonora, WAContract Value AU$20 million per annumContract Period 2008-CurrentScope of Work Multidisciplineshutdown and maintenance support services at the Murrin Murrin Nickel Processing Plant. AGC also provides continuous support for emergency fabrication and specialist call out needs required by the mining and processing operations.

Location Pinjarra, Kwinana & Wagerup, WAContract Value AU$15 million per annumContract Period 2007-CurrentScope of Work Multidisciplinemaintenance shutdown support services to Alcoa’s Alumina Refineries in WA. Additional to the planned and unplanned shutdowns on the calcination circuits, AGC was also awarded capital work upgrades and refurbishment projects which included fabrication and onsite installation at the Pinjarra and Wagerup refineries.

Alcoa Maintenance Contract Client: Alcoa Alumina Australia

Location Karratha, WAContract Value AU$90 millionContract Period Apr 2010-CurrentScope of Work Painting and insulation works for the Pluto LNG onshore plant.The scope of work includes the supply and installation of all insulation, cladding and ancillary materials; fabrication and application of cladding products; and painting and fireproofing coatings of the storage tanks and associated utilities, pipelines and jetty facilities.

Pluto LNG Painting & Insulation Client: FWW / Operator: Woodside

40

Current Projects

Location North-west coast of WAContract Value AU$60 million Contract Period Jul 2011-CurrentScope of Work The manufacture of pipe spools for the Gorgon Project, The scope of work covers receiving material, fabrication, storage, coating and testing of 19,000 pipe spools of various diameters, weighing approximately 7,500 tonnes.

Gorgon Pipe Spools Fabrication Client: Chevron Australia

Metso Minerals Car Dumpers (x5) RGP6

Location Port Hedland, WAContract Value AU$10 million Contract Period Mar 2010-Current Scope of Work The supply, fabrication and assembly of a twin cell car dumper and two positioners as part of BHP Billiton’s Rapid Growth Project – Due to continued strong relationships with client Metso, AGC has successfully delivered five car dumpers to Metso for various operators including BHPB, Rio Tinto and Fortescue Metals Group.

Location North-west coast of WA Contract Value AU$12 million Contract Period Jul 2011-CurrentScope of Work Fabrication, supply, testing, inspection, storage and delivery of adjustable pipe support structures weighing in excess of 900 metric tonnes.

Gorgon Adjustable Pipe Supports Fabrication Client: Chevron Australia

41

Appendix

• Company Snapshot

• Business Model

• AusGroup Operations

• Additional Market Outlook Data

42

Our market

“Investment within the mining and resources sector has been largely unaffected (to date) by the ongoing global economic uncertainty, and recent falls in commodity prices. This is not particularly surprising given the long-term framework mining and

resource companies utilise, in determining the viability of investment projects. Encouragingly, in WA there is increasing interest in

infrastructure investment by both public and private sector parties.

The Western Australia economy, is, for the most par t, continuing to power on. There is no evidence of firms shelving investment plans in the

mining sector, and firms appear little troubled by the recent pullback in commodity prices.”

Source : ANZ RESEARCH – AUSTRALIAN ECONOMICS WEEKLY – 9 DECEMBER 2011

43

Australia’s energy resources

44

Major Australian Resource Projects – Oil & Gas

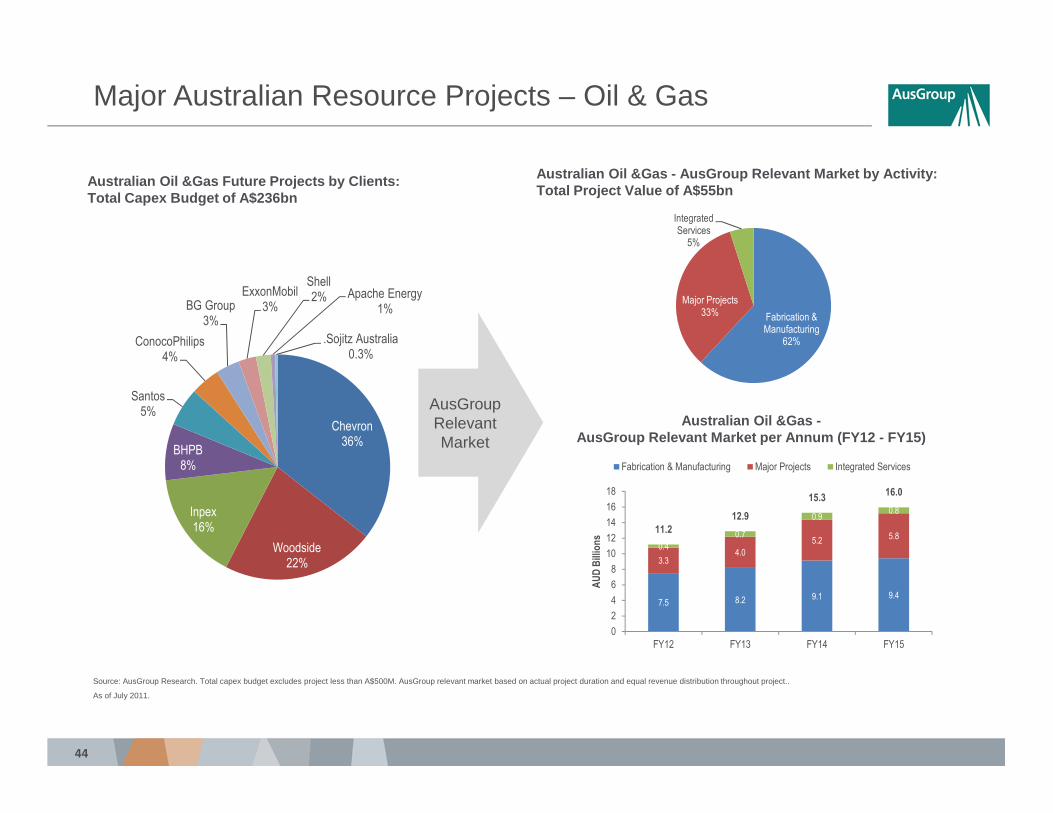

Australian Oil &Gas Future Projects by Clients: Total Capex Budget of A$236bn

Australian Oil &Gas - AusGroup Relevant Market by Ac tivity: Total Project Value of A$55bn

Australian Oil &Gas -AusGroup Relevant Market per Annum (FY12 - FY15)

AusGroup Relevant Market

Source: AusGroup Research. Total capex budget excludes project less than A$500M. AusGroup relevant market based on actual project duration and equal revenue distribution throughout project..

As of July 2011.

Chevron36%

Woodside22%

Inpex16%

BHPB8%

Santos5%

ConocoPhilips4%

BG Group3%

ExxonMobil3%

Shell2% Apache Energy

1%

.Sojitz Australia0.3%

Fabrication & Manufacturing

62%

Major Projects33%

Integrated Services

5%

7.5 8.2 9.1 9.4

3.34.0

5.25.8

0.4

0.7

0.90.8

11.2

12.9

15.316.0

0

2

4

6

8

10

12

14

16

18

FY12 FY13 FY14 FY15

AU

D B

illio

ns

Fabrication & Manufacturing Major Projects Integrated Services

45

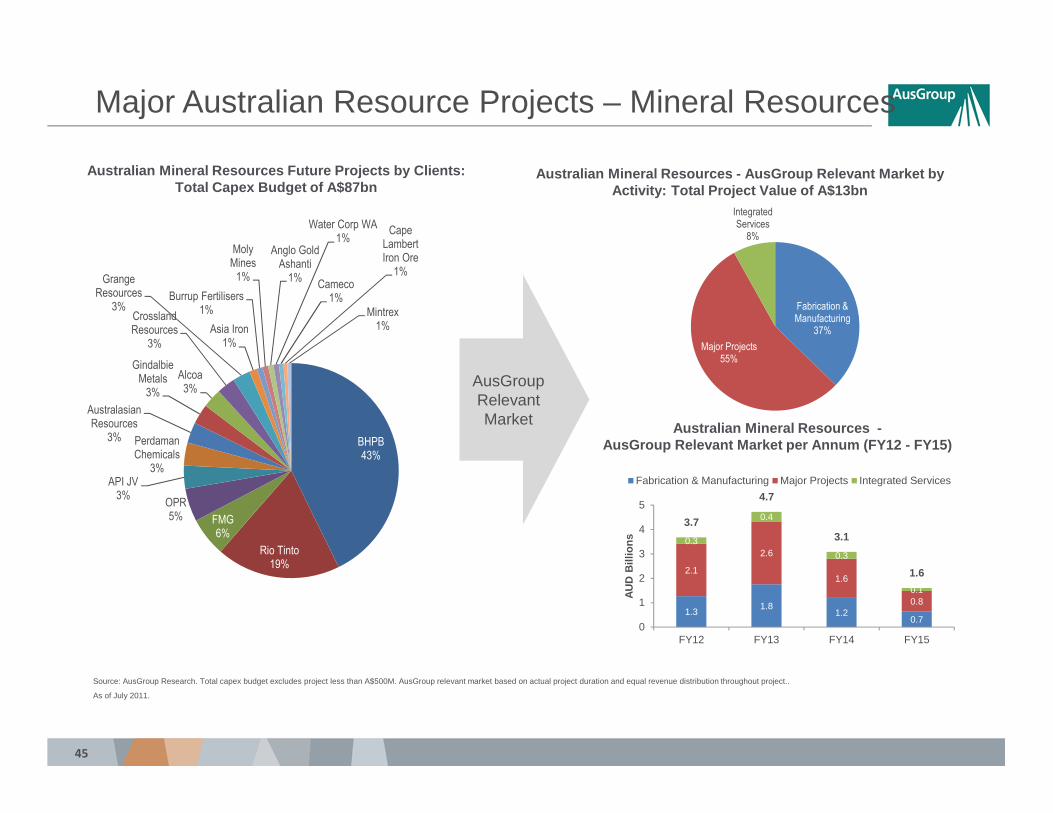

Australian Mineral Resources Future Projects by Cli ents: Total Capex Budget of A$87bn

Australian Mineral Resources - AusGroup Relevant Mar ket by Activity: Total Project Value of A$13bn

Australian Mineral Resources -AusGroup Relevant Market per Annum (FY12 - FY15)

Major Australian Resource Projects – Mineral Resources

Source: AusGroup Research. Total capex budget excludes project less than A$500M. AusGroup relevant market based on actual project duration and equal revenue distribution throughout project..

As of July 2011.

AusGroup Relevant Market

1.31.8

1.20.7

2.1

2.6

1.6

0.8

0.3

0.4

0.3

0.1

3.7

4.7

3.1

1.6

0

1

2

3

4

5

FY12 FY13 FY14 FY15A

UD

Bill

ions

Fabrication & Manufacturing Major Projects Integrated Services

BHPB43%

Rio Tinto19%

FMG6%

OPR5%

API JV3%

Perdaman Chemicals

3%

Australasian Resources

3%

Gindalbie Metals

3%

Alcoa3%

Crossland Resources

3%

Grange Resources

3%

Asia Iron1%

Burrup Fertilisers 1%

Moly Mines

1%

Anglo Gold Ashanti

1%

Water Corp WA1%

Cameco1%

Cape Lambert Iron Ore

1%

Mintrex1%

Fabrication & Manufacturing

37%

Major Projects55%

Integrated Services

8%

46

2012 Half Year Result Briefing9 February 2012

Mr Stuart KennyCEO & Managing Director

Mr Anthony HardwickChief Financial Officer