Embed Size (px)

Citation preview

2013 Full Year Performance Review2013 Full Year Performance Review20 February 2014

Forward Looking Statements

The following presentation includes forward-looking statements, which involve known and unknown risks and uncertainties, that could cause actual results or performance to differ. Forward looking information is based on current views and assumptions of management, including, but not limited to, prevailing economic and market conditions. Such statements are not, and should not be interpreted as a forecast or projection of future performance.

1 2013 F ll Y P f R i B N Y t Ch1. 2013 Full Year Performance Review By Ng Yat ChungGroup President & CEO

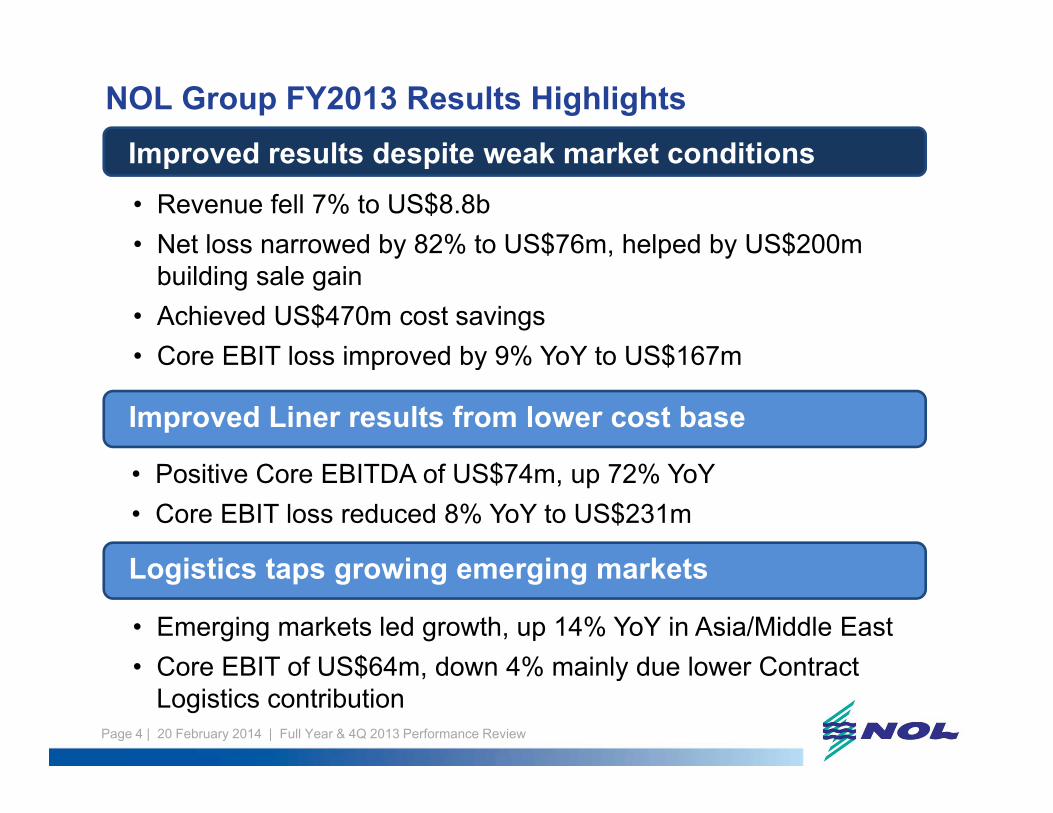

NOL Group FY2013 Results HighlightsImproved results despite weak market conditionsImproved results despite weak market conditions• Revenue fell 7% to US$8.8b• Net loss narrowed by 82% to US$76m, helped by US$200mNet loss narrowed by 82% to US$76m, helped by US$200m

building sale gain• Achieved US$470m cost savings• Core EBIT loss improved by 9% YoY to US$167m

Improved Liner results from lower cost base

• Core EBIT loss improved by 9% YoY to US$167m

L i ti t i i k t

• Positive Core EBITDA of US$74m, up 72% YoY• Core EBIT loss reduced 8% YoY to US$231m

Logistics taps growing emerging markets

• Emerging markets led growth, up 14% YoY in Asia/Middle East• Core EBIT of US$64m down 4% mainly due lower Contract

Page 4 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

• Core EBIT of US$64m, down 4% mainly due lower Contract Logistics contribution

Industry overcapacity drives down container freight rates

YoY % change Index

SCFI freight rate index falls 14% YoYIndustry capacity growth > Global volume growth

5.7 6.0

1,254

1,300

Capacity

3.6 4.0

1,0781,100

14%

Capac tygrowth

2.0

1,078

Volumegrowth

-end 2013

% Annual Capacity Growth % Global Throughput Growth

900 Average for FY12 Average for FY13

Page 5 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

% Annual Capacity Growth % Global Throughput GrowthSource: SCFI. The SCFI is a composite index of 15 individual shipping

routesSource: Alphaliner

Operational & cost efficiencies offset weaker market conditions

24 50 4,900

US$m US$m

FY13 Core EBIT

4,711

4,801

(60)(50)

-

4,700

improved 9% YoY

4 435

(107)

(150)

(100)4,500

4,435 4,396 (207)

(250)

(200)4,300

(300)

( )

4,100 1H12 2H12 1H13 2H13

FY13 Revenue

Page 6 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

Revenue (LHS) Core EBIT (RHS) FY13 Revenuedeclined 7% YoY

Group achieves US$470m* cost savings

FY13 cost savings highlights

• Larger & more fuel-efficient vessels

Sl t i• Slow steaming

• Minimise empty box repositioningBunker &

Network-

Terminals, Land

Operations, Equipment

31% p g

• Improved cargo planning to reduce terminal handling lifts

Network-related52%

Others17% • Pre-emptive voyage planning

to avoid slowdowns from bad weather

17%

Page 7 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

*Excludes bunker price drop of 8%YoY

2. 2013 Full Year2. 2013 Full YearFinancial Performance By Cedric Foo

Group Deputy President & CFO

Group Financial HighlightsR d li d 7% k f i ht tRevenue declined 7% on weak freight rates

US$m

Revenue

9,512

10,000

US$m

8,831 9,000 7%

8,000 FY12 FY13

$ FY12 FY13 % ▲ Better/(US$m) FY12 FY13 % ▲ Better/ (Worse)

Liner 8,054 7,329 (9)Logistics 1,555 1,586 2

Page 9 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

Elimination (97) (84) 13Total 9,512 8,831 (7)

Group Financial HighlightsFY13 C EBITDA 24% C EBIT 9%

US$mUS$m

Core EBIT

FY13 Core EBITDA up 24%, Core EBIT up 9%

Core EBITDA

(150)

US$m

121

150 160

US$m

24%

(183)

(167)(175)110

9%

24%

(200)FY12 FY13

60 FY12 FY13

(US$m) FY12 FY13 % ▲ Better/ (Worse)(US$m) FY12 FY13 % ▲ Better/

(Worse)

1) With ff t f 3Q13 th d fi iti f C EBIT d C EBITDA h h d t l d fi d i C ti b t t d di l

Liner (250) (231) 8Logistics 67 64 (4)Total (183) (167) 9

Liner 43 74 72Logistics 78 76 (3)Total 121 150 24

Page 10 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

1) With effect from 3Q13, the definition of Core EBIT and Core EBITDA have changed to exclude finance expense and income. Comparative numbers restated accordingly2) Core EBIT excludes non-recurring items3) 2012’s results are restated for comparative purposes due to retrospective application of Amendments to FRS 19: Employee Benefit (Revised), which is effective from

financial year 2013..

Group Financial HighlightsN t l d t US$76 i d 82% Y YNet loss narrowed to US$76m, improved 82% YoY

EBIT Net Profit / (Loss)

(76)(100)

-

US$m

20

(50)

50

US$m

(400)

(300)

(200)

(250)

(150)

82%Swing topositive

(412)(500)

FY12 FY13

(287)(350)

FY12 FY13

Note:1) With effect from 3Q13, the definition of EBIT has changed to exclude finance expense and income. Comparative numbers restated accordingly2) EBIT includes non-recurring items. FY13 includes NOL building sale gain of US$200m3) FY13 includes realised foreign exchange gain of US$34 million arising from repayment of Singapore-dollar loan4) 2012’s results are restated for comparative purposes due to retrospective application of Amendments to FRS 19: Employee Benefit (Revised), which is

ff ti f fi i l 2013

Page 11 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

effective from financial year 2013.

Group Balance Sheet Highlights

US$m 27 Dec’ 13 28 Dec’ 12

Total Assets 9,029 8,220(Restated)1,2

Total Liabilities 6,898 6,027Total Equity 2,131 2,193

Total Debt 4 866 3 976Total Debt 4,866 3,976

Total Cash 981 897

Net Debt 3,885 3,079

Gearing (Gross) 2.28x 1.81x

Gearing (Net) 1.82x 1.40x

NAV per share (US$) 0 80 0 83NAV per share (US$) 0.80 0.83

(S$) 1.02 1.01

1 2012’s results are restated for comparative purposes due to retrospective application of Amendments to FRS 19: Employee Benefit

Page 12 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

2012 s results are restated for comparative purposes due to retrospective application of Amendments to FRS 19: Employee Benefit(Revised), which is effective from financial year 2013. 2 2012’s results are also restated due to finalisation of purchase price allocation exercise from acquisition of a subsidiary.

Group Cash Flow Highlights

US$m FY13 FY12

C h & C h E i l t B i i @ Q1 897 228Cash & Cash Equivalents – Beginning @ Q1 897 228

Cash Inflow / (Outflow)

Operating Activities 32 (13)Operating Activities 32 (13)

Investing/Capex Activities (910) (898)

Financing Activities 962 1,580

Cash & Cash Equivalents – Closing @ Q4 981 897

Page 13 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

Group Capital Expenditure

US$m FY13 FY12

1. Vessels 1,072 859

2. Equipment / Facilities 84 79

3 Drydock 48 213. Drydock 48 21

4. IT 97 40

5. Others 7 10

Total 1,308 1,009

Page 14 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

3 Li B K th Gl3. Liner By Kenneth GlennPresident, APL

Liner FY13 Results Highlights

Improved results in tough market conditionsImproved results in tough market conditions

• US$7.3b revenue, down 9% on capacity management & weaker freight rates

Managed down costs & increased efficiencies

g• Core EBITDA up 72% YoY to US$74m• Core EBIT loss improved 8% YoY to US$231mManaged down costs & increased efficiencies

• Cost of sales/FEU reduced by 8% YoY• Bunker consumption dropped by 14% YoY (386k MT)

Continued focus on yield & capacity management

p pp y ( )• 11 new ships* replaced 8 older/smaller ships sold/scrapped & 5

charter ships returned

Continued focus on yield & capacity management

• Fleet capacity increased but capacity management & reconfigured service network better align APL with lower demand levels

Page 16 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

g• Headhaul utilisation >90%* Excludes 3 x 14,000 TEU new ships chartered out to MOL

Liner Results SummaryRevenue Core EBIT

8 054

8,500

US$m

(200)

US$m

8,054

7 3297,500

8,000

(231)(240)

(220)

9%7,329

7,000 FY12 FY13

(250)(260)

( )

FY12 FY13

8%

FY13 Revenue decreased 9% or US$725m YoY, while Core EBIT improved 8% YoY due to cost, efficiency & yield focus.

Capacity management & weaker freight rates reduced Average Revenue per FEU to US$2,318.Cost of sales per FEU was 8% lower YoY due to operational cost efficiencies and lower bunker prices. Bunker prices averaged US$617/MT or 8% lower YoY.

N t

Page 17 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

Note:1) With effect from 3Q13, the definition of Core EBIT has changed to exclude finance expense and income. Comparative numbers restated accordingly2) 2012’s results are restated for comparative purposes due to retrospective application of Amendments to FRS 19: Employee Benefit (Revised), which is effective

from financial year 2013.

4Q13 freight rates among lowest in recent years

1,600

IndexShanghai Containerised Freight Index (Quarterly)

1,400

1,200

1,028 1,000

800 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13

Page 18 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

Source: SCFI. The SCFI is a composite index of 15 individual shipping routes

Liner impacted by market conditions

2,615 2 6012,650 1,500

Volume('000 FEUs) US$/FEU

APL Volume and Average Revenue/FEU Trend

2,598

2,539 2,539

2 420

,6 5 2,601

1,200

764 692 699

824 791

720 707 802 772

705 669

800

2,342

2,420 2,419

2,376

2,372

2,450

900

,2,315

2,218

2,250

300

600

2,050 -1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13

T t l V l (LHS) A R /FEU (RHS)

Page 19 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

Total Volume (LHS) Average Revenue/FEU (RHS)

Continuous & sustainable cost improvement

US$/FEU

$245/FEU*reduction

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13

Liner Cost of Sales/FEU Liner Cost of Sales/FEU at fixed bunker price*

Page 20 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

* Calculated cost of sales per FEU at fixed bunker price of US$600/MT from 1Q12 to 4Q13

Vessel utilisation >90% with strict capacity management

Average full year capacity <1% up

130%70,000

Average Capacity (weekly TEUs) Utilisation %FY2013FY2012

92% 91%94%

92% 93% 94% 94%92% 91% 90% 91%

93%

90%

110%

60,000

70%

50,000

50%40,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2011 2012 2013

Page 21 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

Note: Figures are based on the headhaul leg of main linehaul servicesThe capacity figures takes into account “winter program” initiations

Leaner cost base mitigated weak industry conditions; improved operating results

2 500 2,509

2,600

Liner Rev/FEUUS$

p p gCore EBIT improved despite Revenue/FEU fall

2,500 2,509

2,318

2,400

2,200

FY2011 FY2012 FY2013-

(250)(231)(250)

(424)

(500)

FY2011 FY2012 FY2013

Page 22 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

FY2011 FY2012 FY2013Liner Core EBIT

(US$m)

Operational Update

Volume (‘000 FEUs) FY13 FY12 % ▲ 4Q13 4Q12 % ▲Transpacific 855 857 - 235 232 1

Intra-Asia 1,296 1,313 (1) 354 348 2

Asia-Europe 422 472 (11) 112 118 (5)

Latin America 200 210 (5) 53 57 (7)

Transatlantic 173 168 3 46 47 (2)( )

Total 2,946 3,020 (2) 800 802 -

Average Revenue/FEU (US$) FY13 FY12 % ▲ 4Q13 4Q12 % ▲Transpacific 3,420 3,681 (7) 3,265 3,500 (7)Intra-Asia 1,386 1,559 (11) 1,317 1,493 (12)Asia-Europe 2,307 2,471 (7) 2,242 2,405 (7)Latin America 3,339 3,524 (5) 3,105 3,533 (12)Transatlantic 2,698 2,795 (3) 2,706 2,636 3Total 2,318 2,509 (8) 2,218 2,419 (8)

Page 23 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

Note: Based on point of sailing and inclusive of headhaul and backhaul trade.

10 newbuild deliveries in FY2014

180,000

14

TEUs 24 vessels delivered at end-2013 10 vessels to be delivered in 2014

120,000 106 x 14,000 TEU

10

60,000

,

4 x 14,000 TEU

10 x 10 000 TEU

0

6 x 9,000 TEU

6 x 9,000 TEU

2 x 8,100 TEU

10 x 10,000 TEU

2012 2013 2014

Total vessels

N t

Page 24 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

Note: 1) 5 out of the 10 x 14,000 TEU vessels for delivery between 2013 and 2014 will be chartered out to MOL

Operating Fleet UpdateD li i f l f l ffi i t hi i l t t

FY2014FY2013

Deliveries of larger, more fuel-efficient ships improve slot costs

Fleet 583,000 640,000 +57,000 -37,000 603,000

1 Jan 2013 Net change 27 Dec 2013 Net change 26 Dec 2014

capacity TEU TEUTEU TEU TEU

No of 7 20No. of vessels 128 121-7

vessels-20

charters expiring

+8

109

4 550 5 300 5 530

Note:

+8 newbuilds

Average vessel size

4,550 TEU

5,300 TEU

5,530 TEU

Page 25 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

1) FY2014 fleet changes are provisional and excludes APL capacity chartered out2) FY2014 capacity net change comprises -119,000 TEU linehaul vessel charters expiring and +82,000 TEU newbuild capacity 3) FY2014 vessel net change comprises -20 linehaul vessel charters expiring and +8 newbuild deliveries (excludes 2 vessels chartered

out to MOL)

Liner business conditions

Industry

• Recent large orders for new vessels to pressure freight rates g p gin low growth environment

• Cascading continues to impact all trades

APL

• Bunker prices remains high at around US$600/MT

• Charter returns and new fuel-efficient vessels are expected to further improve slot costs

• Long term benefit from improved cost structure and operational• Long-term benefit from improved cost structure and operational efficiencies

• Change to functional structure to speed up decision making and

Page 26 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

improve market responsiveness

4 L i ti B N Y t Ch4. Logistics By Ng Yat ChungGroup President & CEO

Logistics FY13 Results Highlights

Profitable growth despite weak global economy

• Revenue US$1 6b up 2% YoYRevenue US$1.6b, up 2% YoY• Core EBIT of US$64m, down 4% YoY mainly due to lower Contract

Logistics contribution C EBIT i f 4 0%

Emerging markets led growth

• Core EBIT margin of 4.0%

• Emerging markets revenue led by 14% growth in Asia/Middle East• International Services revenue up 10% YoY to US$585m on

business expansion in consumer and retail segmentsbusiness expansion in consumer and retail segments • Contract Logistics revenue down 2% YoY to US$1.0b mainly due to

extended customers’ automotive plant shutdown and slow auto sector recovery

Page 28 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

sector recovery

Logistics Results Highlights

1,700

US$m

80

US$m

Revenue Core EBIT*

1,555 1,586

1,350

67 64

60 4%

2%

1,000 FY12 FY13

40 FY12 FY13FY12 FY13 FY12 FY13

• Logistics achieved revenue of US$1.6b in FY13, growing 2% year-on-year (YoY), led by emerging markets in Asia/Middle East.

International Services achieved revenue of US$585m, a 10% YoY increaseContract Logistics achieved revenue of US$1.0b, a 2% YoY decrease

• Core EBIT of US$64m for FY13, a 4% YoY decrease

Page 29 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

*With effect from 3Q13, the definition of Core EBIT has changed to exclude finance expense & income. Comparative numbers restated accordingly

APL Logistics Revenue Trend by Region

27% (Asia/Middle East) 25% (Asia/Middle East)

Growth led by Asia/Middle East +14% and Europe +6%

27% (Asia/Middle East)

$436

25% (Asia/Middle East)

$382

63% (Americas)

$993$157

66% (Americas)

$1,025$148

$1,586 $1,555

10% (Europe) 9% (Europe)

FY13 Revenue Breakdown– by Region (US$m)

FY12 Revenue Breakdown– by Region (US$m)

Page 30 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

Performance Breakdown

Maintained profitable growth with FY13 Core EBIT of US$64m

FY13 FY12% ▲

Better/ 4Q13 4Q12% ▲

Better/FY13 FY12 Better/ (Worse)

4Q13 4Q12 Better/ (Worse)

Revenue (US$m) 1 586 1 555 2 434 435 -Revenue (US$m) 1,586 1,555 2 434 435

• Contract Logistics 1,001 1,022 (2) 275 282 (3)

• International Services 585 533 10 159 153 4

Core EBIT (US$m) 64 67 (4) 19 26 (27)

• Contract Logistics 22 36 (39) 3 15 (80)

• International Services 42 31 35 16 11 45

Core EBIT Margin (%) 4.0 4.3 4.4 6.0

• Contract Logistics 2.2 3.5 1.1 5.3

Page 31 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

• International Services 7.2 5.8 10.1 7.2

Revenue and Core EBIT Margin TrendSoft economic conditions in developed markets & slow auto sectorSoft economic conditions in developed markets & slow auto sector recovery in North America dampened 4Q13 margins

Weekly Revenue(US$m)

Core EBITMargin (%)

10.0%

30.0

35.0

3 3%

5.2%6.0%

3.7%

5.1%4.4% 5.0%

20 0

25.0

3.3%2.5%

2.9%

15.0

20.0

0.0%10.0 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13

Weekly Revenue (US$m) (LHS) Core EBIT Margin (%) (RHS)

Page 32 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

Logistics business conditions

Industry

• Weak macroeconomic conditions in developed end markets pslowed down industry growth

• Domestic consumption continued to grow in emerging markets• Greater adoption of multi-channel retailing provided new supply

APL Logistics

• Greater adoption of multi-channel retailing provided new supply chain management opportunities in emerging markets

APL Logistics

• Beat Simon appointed new APL Logistics President• Continue to look out for growth opportunities in emerging markets g pp g g

& US• Maintain efficiency and cost discipline focus

Page 33 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

5 G O tl k5. Group Outlook

Group Outlook

Global economic growth prospects are uncertain. Conditions in the liner industryare expected to remain challenging due to continued over-supply of capacity.Liner freight rates will remain under pressure. The Group will continue its focus

i t d ti l ffi i i ith th i t i iton managing costs and operational efficiencies with the aim to improve itsfinancial performance in 2014.

Page 35 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

A diAppendix

Group Financial Highlights

US$m FY13 FY12% ▲

Better/ (Worse)

4Q13 4Q12% ▲Better/

(Worse)

Revenue 8,831 9,512 (7) 2,334 2,499 (7)

(Restated) (Restated)

, ( ) , , ( )

Core EBITDA 150 121 24 7 25 (72)

Core EBIT (before non-recurring items)

(167) (183) 9 (82) (56) (46)recurring items)

Non-recurring items 187 (103) n.m. (11) 8 n.m.

EBIT 20 (287) n.m. (93) (49) (90)

Net loss to owners of the company

(76) (412) 82 (137) (91) (51)

Net loss to owners of the company (before non-recurring items)

(263) (309) 15 (126) (99) (27)

Note: 1)With effect from 3Q13 the definition of Core EBITDA Core EBIT and EBIT have changed to exclude finance expense and income Comparative numbers restated

Page 37 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

1)With effect from 3Q13, the definition of Core EBITDA, Core EBIT and EBIT have changed to exclude finance expense and income. Comparative numbers restated accordingly.

2) 2012’s results are restated for comparative purposes due to retrospective application of Amendments to FRS 19: Employee Benefit (Revised), which is effective from financial year 2013.

Financial Highlights by Business Segment

Revenue (US$m) FY13 FY12% ▲

Better/ (Worse)

4Q13 4Q12% ▲

Better/ (Worse)

Liner 7 329 8 054 (9) 1 922 2 089 (8)Liner 7,329 8,054 (9) 1,922 2,089 (8)

Logistics 1,586 1,555 2 434 435 -

Elimination (84) (97) 13 (22) (25) 12

Total Revenue 8,831 9,512 (7) 2,334 2,499 (7)

C EBIT (US$ ) FY13 FY12% ▲

/ 4Q13 4Q12% ▲

/(Restated) (Restated)

Core EBIT (US$m) FY13 FY12 Better/ (Worse)

4Q13 4Q12 Better/ (Worse)

Liner (231) (250) 8 (101) (82) (23)

Logistics 64 67 (4) 19 26 (27)Logistics 64 67 (4) 19 26 (27)

Total Core EBIT (167) (183) 9 (82) (56) (46)

Note:1) With effect from 3Q13 the definition of Core EBIT has changed to exclude finance expense and income Comparative numbers restated accordingly

Page 38 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

1) With effect from 3Q13, the definition of Core EBIT has changed to exclude finance expense and income. Comparative numbers restated accordingly2) 2012’s results are restated for comparative purposes due to retrospective application of Amendments to FRS 19: Employee Benefit (Revised), which is

effective from financial year 2013.

Liner Results Summary

US$m FY13 FY12% ▲Better/

(Worse)4Q13 4Q12

% ▲Better/

(Worse)

Revenue 7 329 8 054 (9) 1 922 2 089 (8)

(Restated) (Restated)

Revenue 7,329 8,054 (9) 1,922 2,089 (8)

Core EBITDA 74 43 72 (15) (4) (275)

Core EBIT (231) (250) 8 (101) (82) (23)

EBIT (71) (351) 80 (111) (74) (50)

Core EBIT margin (%) (3.1) (3.1) (5.3) (3.9)

Note:1) With effect from 3Q13, the definition of Core EBITDA, Core EBIT and EBIT have changed to exclude finance expense and income. Comparative numbers restated

accordingly2) 2012’s results are restated for comparative purposes due to retrospective application of Amendments to FRS 19: Employee Benefit (Revised), which is effective

from financial year 2013.

Page 39 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

Logistics Results Highlights

US$m FY13 FY12% ▲

Better/ (Worse)

4Q13 4Q12% ▲Better/

(Worse)

(Restated) (Restated)

Revenue 1,586 1,555 2 434 435 -

Core EBITDA 76 78 (3) 22 29 (24)

Core EBIT 64 67 (4) 19 26 (27)Core EBIT 64 67 (4) 19 26 (27)

EBIT 91 64 42 18 25 (28)

Core EBIT margin (%) 4.0 4.3 4.4 6.0

Note:1) With effect from 3Q13, the definition of Core EBITDA, Core EBIT and EBIT have changed to exclude finance expense and income. Comparative numbers restated

accordingly2) 2012’s results are restated for comparative purposes due to retrospective application of Amendments to FRS 19: Employee Benefit (Revised), which is effective

from financial year 2013.

Page 40 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

Group Fuel and Currency Exposures

Bunker

• The Group continues to recover part of its fuel price increases from customers through bunker adjustment factors.j

• The Group also maintains a policy of hedging its bunker exposures.

Foreign exchange

• Major foreign currency exposures are in Euro, Singapore Dollar, Canadian Dollar, Japanese Yen and Chinese Renminbi.

• The Group maintains a policy of hedging its foreign exchange exposures.

Page 41 | 20 February 2014 | Full Year & 4Q 2013 Performance Review

Neptune Orient Lines Ltd456 Alexandra Road, NOL BuildingEnd of Presentation

Thank You

NOL BuildingSingapore 119962Tel: (65) 6278 9000Fax: (65) 6278 4900Company registration number : 196800632Dnumber : 196800632DWebsite: www.nol.com.sg