Embed Size (px)

Citation preview

2013 IIB Seminar on US Taxation of International Banks Tax Issues Arising from the Dodd Frank Act Melissa Heise (Moderator) Director & Tax Counsel, The Royal Bank of Scotland plc

Roger Brown Principal, Ernst & Young LLP Richard Coffman General Counsel, Institute of International Bankers

Fred Carchman Tax Director, Deloitte Tax LLP

Philip Fried Principal, PwC

Davis J. Wang Partner, Sullivan & Cromwell LLP

The Dodd Frank Act

Title VII: Swaps issues • Section 716 Swap Push Out • Swaps Dealers and Cross Border Issues

FBOs: Section 165 Enhanced Capital, Liquidity and Other Prudential Standards application to Foreign Banking Organizations

Basel III Tax Implications

Living Wills and Volker Rule

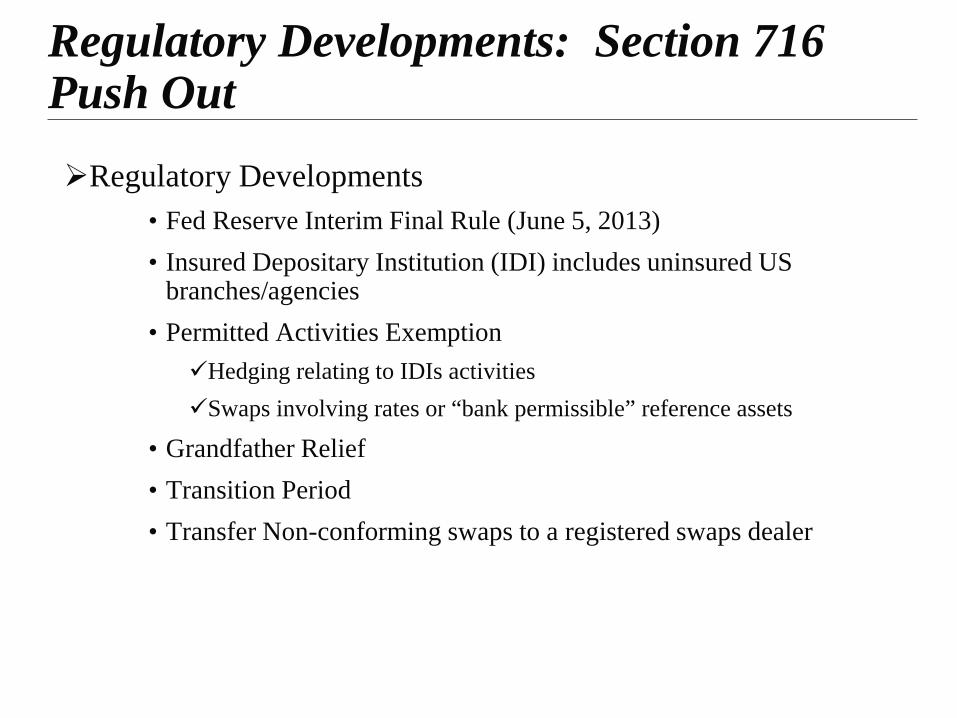

Regulatory Developments: Section 716 Push Out Regulatory Developments

• Fed Reserve Interim Final Rule (June 5, 2013) • Insured Depositary Institution (IDI) includes uninsured US

branches/agencies • Permitted Activities Exemption Hedging relating to IDIs activities Swaps involving rates or “bank permissible” reference assets

• Grandfather Relief • Transition Period • Transfer Non-conforming swaps to a registered swaps dealer

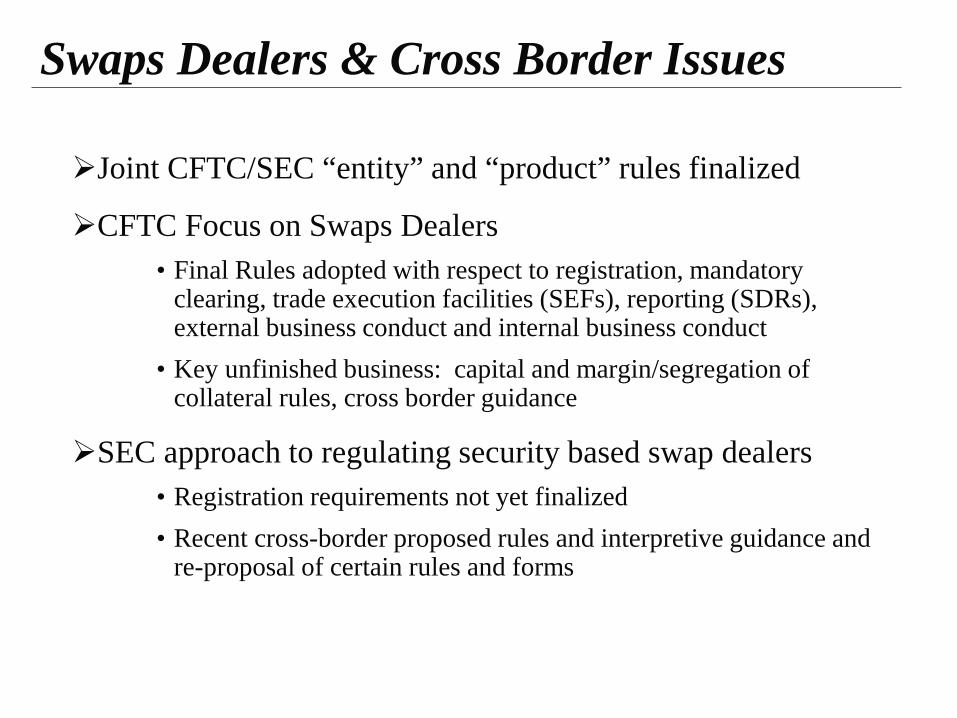

Swaps Dealers & Cross Border Issues

Joint CFTC/SEC “entity” and “product” rules finalized

CFTC Focus on Swaps Dealers • Final Rules adopted with respect to registration, mandatory

clearing, trade execution facilities (SEFs), reporting (SDRs), external business conduct and internal business conduct

• Key unfinished business: capital and margin/segregation of collateral rules, cross border guidance

SEC approach to regulating security based swap dealers • Registration requirements not yet finalized • Recent cross-border proposed rules and interpretive guidance and

re-proposal of certain rules and forms

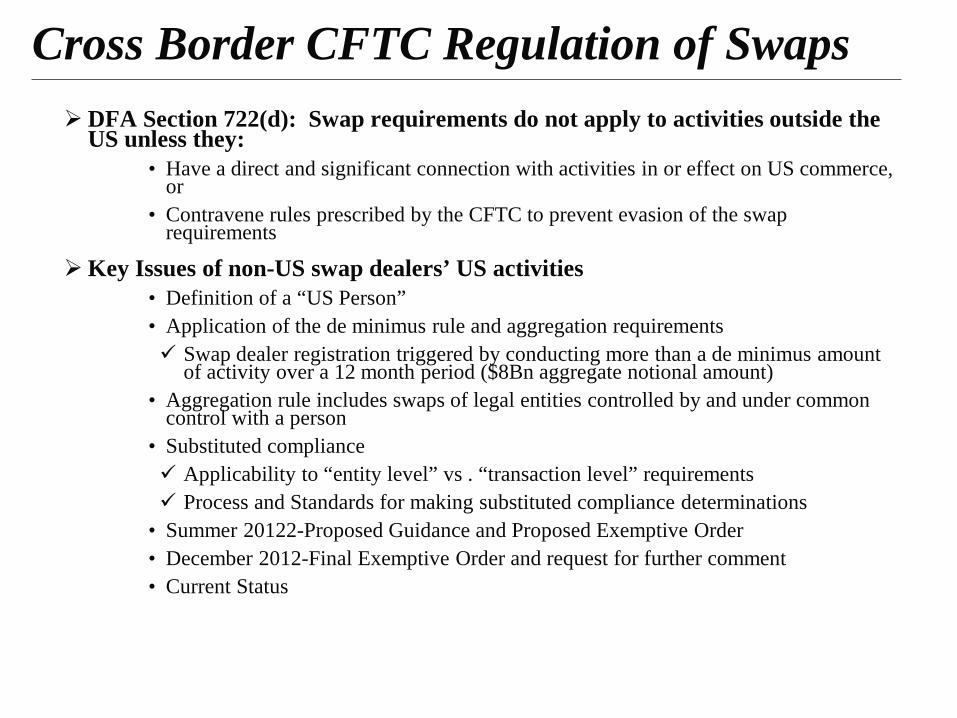

Cross Border CFTC Regulation of Swaps

DFA Section 722(d): Swap requirements do not apply to activities outside the US unless they:

• Have a direct and significant connection with activities in or effect on US commerce, or

• Contravene rules prescribed by the CFTC to prevent evasion of the swap requirements

Key Issues of non-US swap dealers’ US activities • Definition of a “US Person” • Application of the de minimus rule and aggregation requirements Swap dealer registration triggered by conducting more than a de minimus amount

of activity over a 12 month period ($8Bn aggregate notional amount) • Aggregation rule includes swaps of legal entities controlled by and under common

control with a person • Substituted compliance Applicability to “entity level” vs . “transaction level” requirements Process and Standards for making substituted compliance determinations

• Summer 20122-Proposed Guidance and Proposed Exemptive Order • December 2012-Final Exemptive Order and request for further comment • Current Status

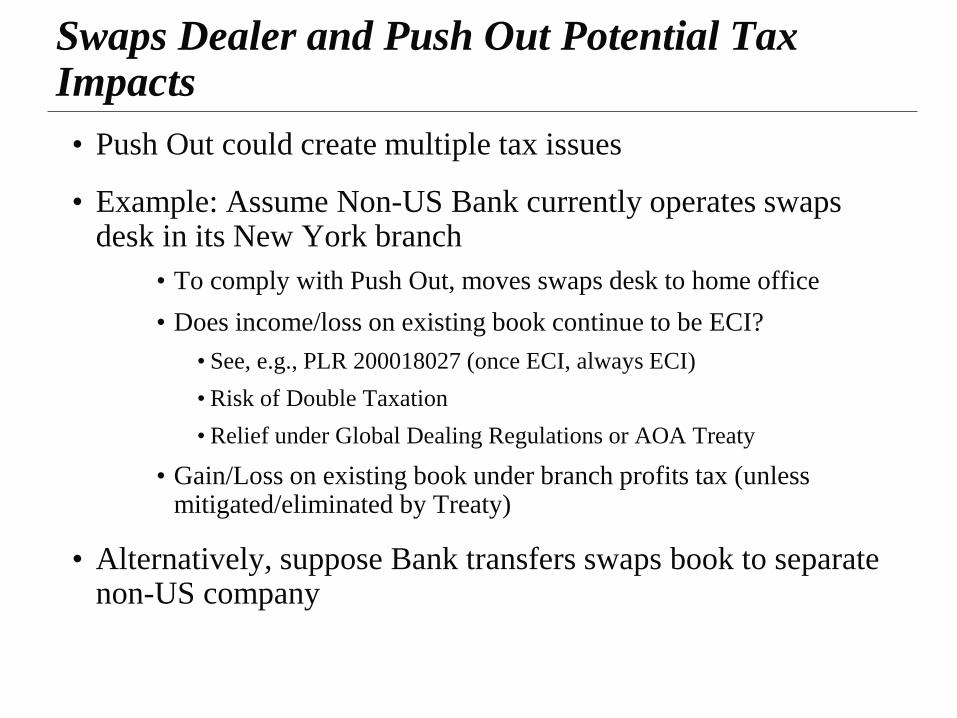

Swaps Dealer and Push Out Potential Tax Impacts

• Push Out could create multiple tax issues

• Example: Assume Non-US Bank currently operates swaps desk in its New York branch

• To comply with Push Out, moves swaps desk to home office • Does income/loss on existing book continue to be ECI?

• See, e.g., PLR 200018027 (once ECI, always ECI) • Risk of Double Taxation • Relief under Global Dealing Regulations or AOA Treaty

• Gain/Loss on existing book under branch profits tax (unless mitigated/eliminated by Treaty)

• Alternatively, suppose Bank transfers swaps book to separate non-US company

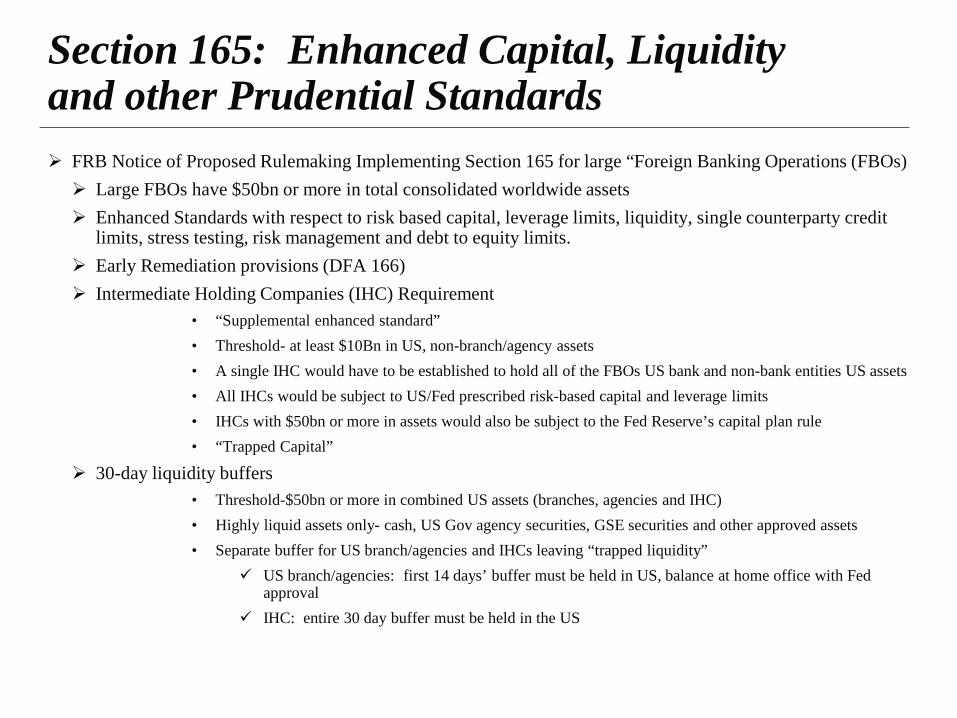

Section 165: Enhanced Capital, Liquidity and other Prudential Standards FRB Notice of Proposed Rulemaking Implementing Section 165 for large “Foreign Banking Operations (FBOs) Large FBOs have $50bn or more in total consolidated worldwide assets Enhanced Standards with respect to risk based capital, leverage limits, liquidity, single counterparty credit

limits, stress testing, risk management and debt to equity limits. Early Remediation provisions (DFA 166) Intermediate Holding Companies (IHC) Requirement

• “Supplemental enhanced standard” • Threshold- at least $10Bn in US, non-branch/agency assets • A single IHC would have to be established to hold all of the FBOs US bank and non-bank entities US assets • All IHCs would be subject to US/Fed prescribed risk-based capital and leverage limits • IHCs with $50bn or more in assets would also be subject to the Fed Reserve’s capital plan rule • “Trapped Capital”

30-day liquidity buffers • Threshold-$50bn or more in combined US assets (branches, agencies and IHC) • Highly liquid assets only- cash, US Gov agency securities, GSE securities and other approved assets • Separate buffer for US branch/agencies and IHCs leaving “trapped liquidity”

US branch/agencies: first 14 days’ buffer must be held in US, balance at home office with Fed approval

IHC: entire 30 day buffer must be held in the US

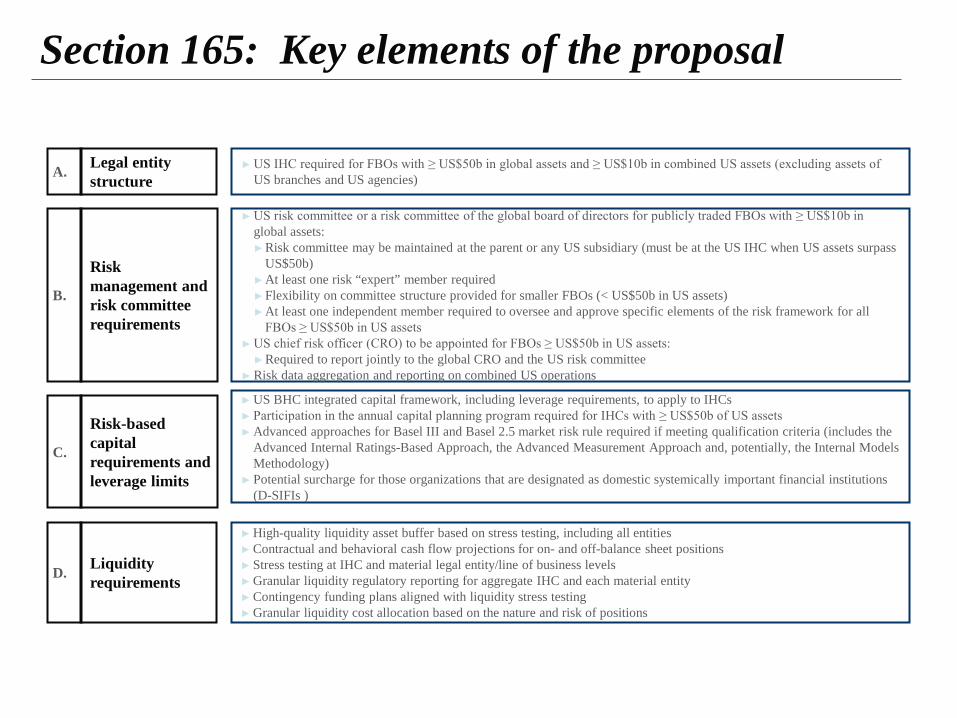

Section 165: Key elements of the proposal

► US IHC required for FBOs with ≥ US$50b in global assets and ≥ US$10b in combined US assets (excluding assets of US branches and US agencies)

Legal entity structure A.

► US risk committee or a risk committee of the global board of directors for publicly traded FBOs with ≥ US$10b in global assets: ►Risk committee may be maintained at the parent or any US subsidiary (must be at the US IHC when US assets surpass

US$50b) ►At least one risk “expert” member required ►Flexibility on committee structure provided for smaller FBOs (< US$50b in US assets) ►At least one independent member required to oversee and approve specific elements of the risk framework for all

FBOs ≥ US$50b in US assets ► US chief risk officer (CRO) to be appointed for FBOs ≥ US$50b in US assets:

►Required to report jointly to the global CRO and the US risk committee ► Risk data aggregation and reporting on combined US operations

Risk management and risk committee requirements

B.

► US BHC integrated capital framework, including leverage requirements, to apply to IHCs ► Participation in the annual capital planning program required for IHCs with ≥ US$50b of US assets ► Advanced approaches for Basel III and Basel 2.5 market risk rule required if meeting qualification criteria (includes the

Advanced Internal Ratings-Based Approach, the Advanced Measurement Approach and, potentially, the Internal Models Methodology)

► Potential surcharge for those organizations that are designated as domestic systemically important financial institutions (D-SIFIs )

Risk-based capital requirements and leverage limits

C.

► High-quality liquidity asset buffer based on stress testing, including all entities ► Contractual and behavioral cash flow projections for on- and off-balance sheet positions ► Stress testing at IHC and material legal entity/line of business levels ► Granular liquidity regulatory reporting for aggregate IHC and each material entity ► Contingency funding plans aligned with liquidity stress testing ► Granular liquidity cost allocation based on the nature and risk of positions

Liquidity requirements D.

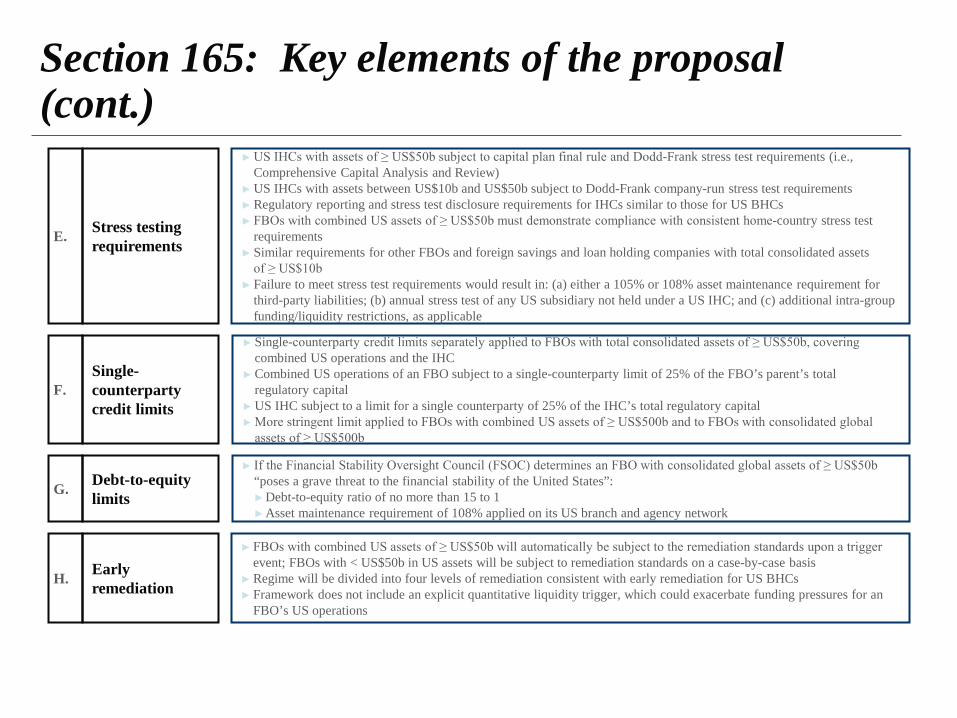

Section 165: Key elements of the proposal (cont.)

► Single-counterparty credit limits separately applied to FBOs with total consolidated assets of ≥ US$50b, covering combined US operations and the IHC

► Combined US operations of an FBO subject to a single-counterparty limit of 25% of the FBO’s parent’s total regulatory capital

► US IHC subject to a limit for a single counterparty of 25% of the IHC’s total regulatory capital ► More stringent limit applied to FBOs with combined US assets of ≥ US$500b and to FBOs with consolidated global

assets of ≥ US$500b

Single- counterparty credit limits

F.

► If the Financial Stability Oversight Council (FSOC) determines an FBO with consolidated global assets of ≥ US$50b “poses a grave threat to the financial stability of the United States”: ►Debt-to-equity ratio of no more than 15 to 1 ►Asset maintenance requirement of 108% applied on its US branch and agency network

Debt-to-equity limits G.

► FBOs with combined US assets of ≥ US$50b will automatically be subject to the remediation standards upon a trigger event; FBOs with < US$50b in US assets will be subject to remediation standards on a case-by-case basis

► Regime will be divided into four levels of remediation consistent with early remediation for US BHCs ► Framework does not include an explicit quantitative liquidity trigger, which could exacerbate funding pressures for an

FBO’s US operations

Early remediation H.

Stress testing requirements E.

► US IHCs with assets of ≥ US$50b subject to capital plan final rule and Dodd-Frank stress test requirements (i.e., Comprehensive Capital Analysis and Review)

► US IHCs with assets between US$10b and US$50b subject to Dodd-Frank company-run stress test requirements ► Regulatory reporting and stress test disclosure requirements for IHCs similar to those for US BHCs ► FBOs with combined US assets of ≥ US$50b must demonstrate compliance with consistent home-country stress test

requirements ► Similar requirements for other FBOs and foreign savings and loan holding companies with total consolidated assets

of ≥ US$10b ► Failure to meet stress test requirements would result in: (a) either a 105% or 108% asset maintenance requirement for

third-party liabilities; (b) annual stress test of any US subsidiary not held under a US IHC; and (c) additional intra-group funding/liquidity restrictions, as applicable

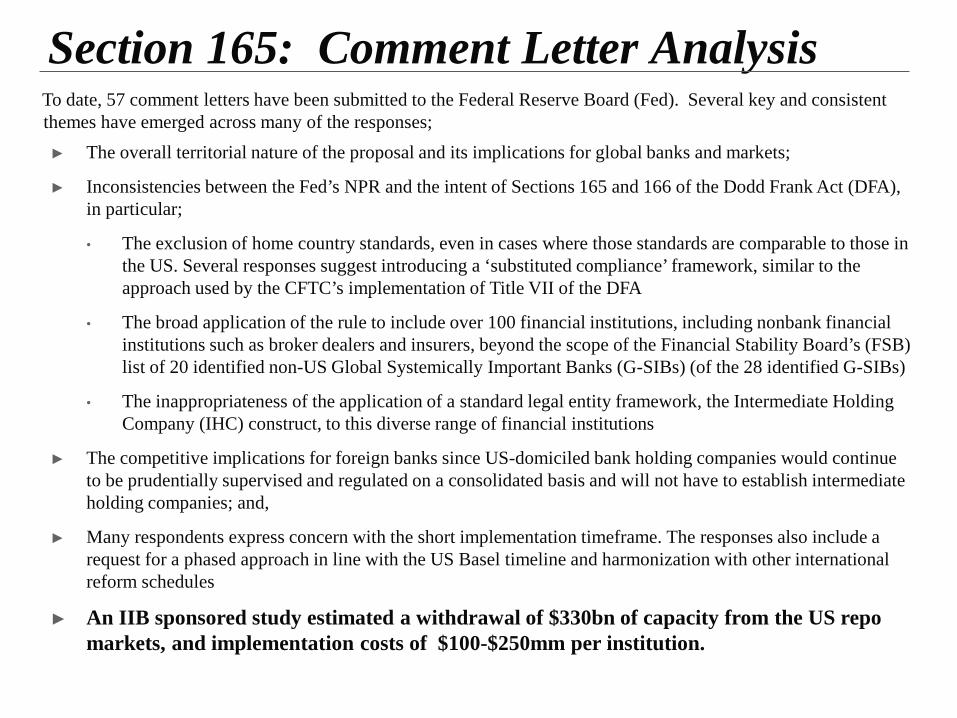

Section 165: Comment Letter Analysis To date, 57 comment letters have been submitted to the Federal Reserve Board (Fed). Several key and consistent themes have emerged across many of the responses; ► The overall territorial nature of the proposal and its implications for global banks and markets;

► Inconsistencies between the Fed’s NPR and the intent of Sections 165 and 166 of the Dodd Frank Act (DFA), in particular;

• The exclusion of home country standards, even in cases where those standards are comparable to those in the US. Several responses suggest introducing a ‘substituted compliance’ framework, similar to the approach used by the CFTC’s implementation of Title VII of the DFA

• The broad application of the rule to include over 100 financial institutions, including nonbank financial institutions such as broker dealers and insurers, beyond the scope of the Financial Stability Board’s (FSB) list of 20 identified non-US Global Systemically Important Banks (G-SIBs) (of the 28 identified G-SIBs)

• The inappropriateness of the application of a standard legal entity framework, the Intermediate Holding Company (IHC) construct, to this diverse range of financial institutions

► The competitive implications for foreign banks since US-domiciled bank holding companies would continue to be prudentially supervised and regulated on a consolidated basis and will not have to establish intermediate holding companies; and,

► Many respondents express concern with the short implementation timeframe. The responses also include a request for a phased approach in line with the US Basel timeline and harmonization with other international reform schedules

► An IIB sponsored study estimated a withdrawal of $330bn of capacity from the US repo markets, and implementation costs of $100-$250mm per institution.

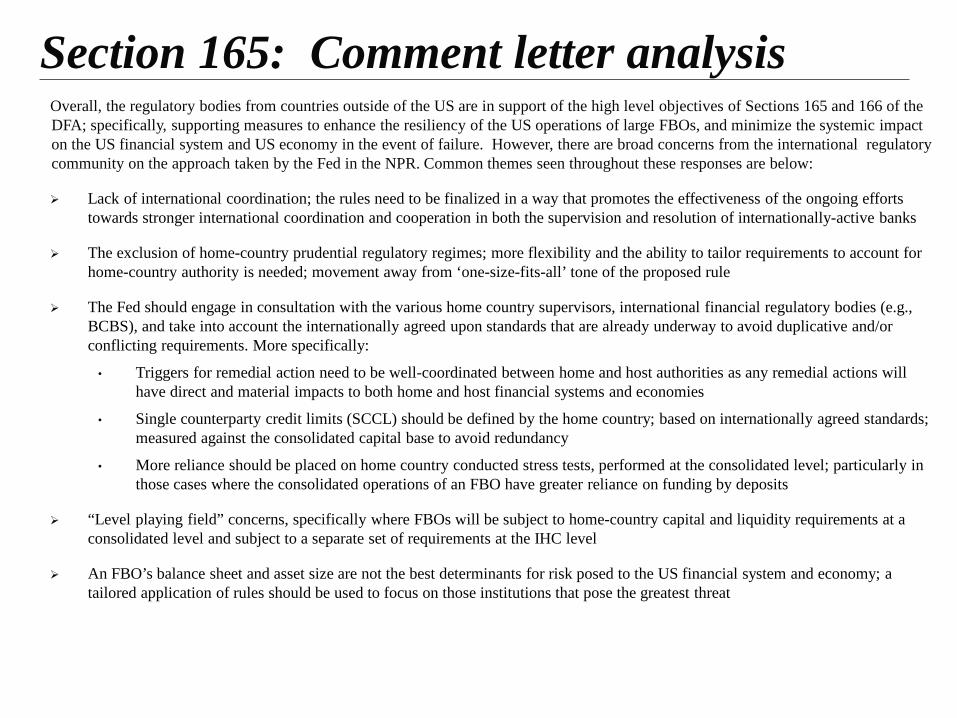

Section 165: Comment letter analysis Overall, the regulatory bodies from countries outside of the US are in support of the high level objectives of Sections 165 and 166 of the DFA; specifically, supporting measures to enhance the resiliency of the US operations of large FBOs, and minimize the systemic impact on the US financial system and US economy in the event of failure. However, there are broad concerns from the international regulatory community on the approach taken by the Fed in the NPR. Common themes seen throughout these responses are below:

Lack of international coordination; the rules need to be finalized in a way that promotes the effectiveness of the ongoing efforts towards stronger international coordination and cooperation in both the supervision and resolution of internationally-active banks

The exclusion of home-country prudential regulatory regimes; more flexibility and the ability to tailor requirements to account for home-country authority is needed; movement away from ‘one-size-fits-all’ tone of the proposed rule

The Fed should engage in consultation with the various home country supervisors, international financial regulatory bodies (e.g., BCBS), and take into account the internationally agreed upon standards that are already underway to avoid duplicative and/or conflicting requirements. More specifically:

• Triggers for remedial action need to be well-coordinated between home and host authorities as any remedial actions will have direct and material impacts to both home and host financial systems and economies

• Single counterparty credit limits (SCCL) should be defined by the home country; based on internationally agreed standards; measured against the consolidated capital base to avoid redundancy

• More reliance should be placed on home country conducted stress tests, performed at the consolidated level; particularly in those cases where the consolidated operations of an FBO have greater reliance on funding by deposits

“Level playing field” concerns, specifically where FBOs will be subject to home-country capital and liquidity requirements at a consolidated level and subject to a separate set of requirements at the IHC level

An FBO’s balance sheet and asset size are not the best determinants for risk posed to the US financial system and economy; a tailored application of rules should be used to focus on those institutions that pose the greatest threat

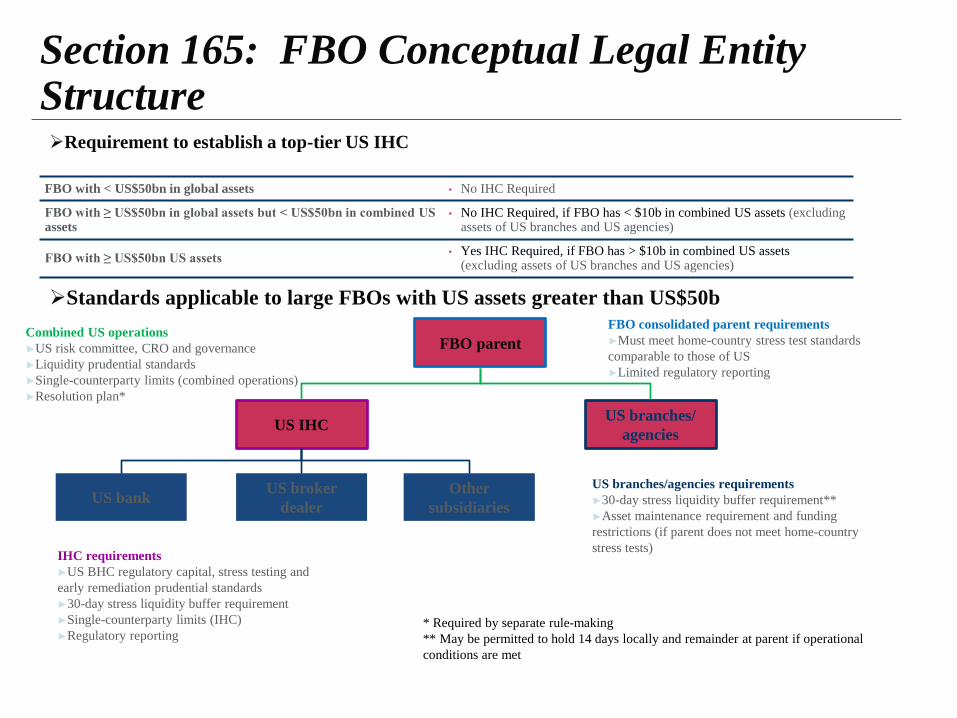

Section 165: FBO Conceptual Legal Entity Structure Requirement to establish a top-tier US IHC

FBO with < US$50bn in global assets • No IHC Required

FBO with ≥ US$50bn in global assets but < US$50bn in combined US assets

• No IHC Required, if FBO has < $10b in combined US assets (excluding assets of US branches and US agencies)

FBO with ≥ US$50bn US assets • Yes IHC Required, if FBO has > $10b in combined US assets (excluding assets of US branches and US agencies)

Standards applicable to large FBOs with US assets greater than US$50b Combined US operations ►US risk committee, CRO and governance ►Liquidity prudential standards ►Single-counterparty limits (combined operations) ►Resolution plan*

FBO consolidated parent requirements ►Must meet home-country stress test standards comparable to those of US ►Limited regulatory reporting

IHC requirements ►US BHC regulatory capital, stress testing and early remediation prudential standards ►30-day stress liquidity buffer requirement ►Single-counterparty limits (IHC) ►Regulatory reporting

US branches/agencies requirements ►30-day stress liquidity buffer requirement** ►Asset maintenance requirement and funding restrictions (if parent does not meet home-country stress tests)

FBO parent

US IHC US branches/ agencies

US bank US broker dealer

Other subsidiaries

* Required by separate rule-making ** May be permitted to hold 14 days locally and remainder at parent if operational conditions are met

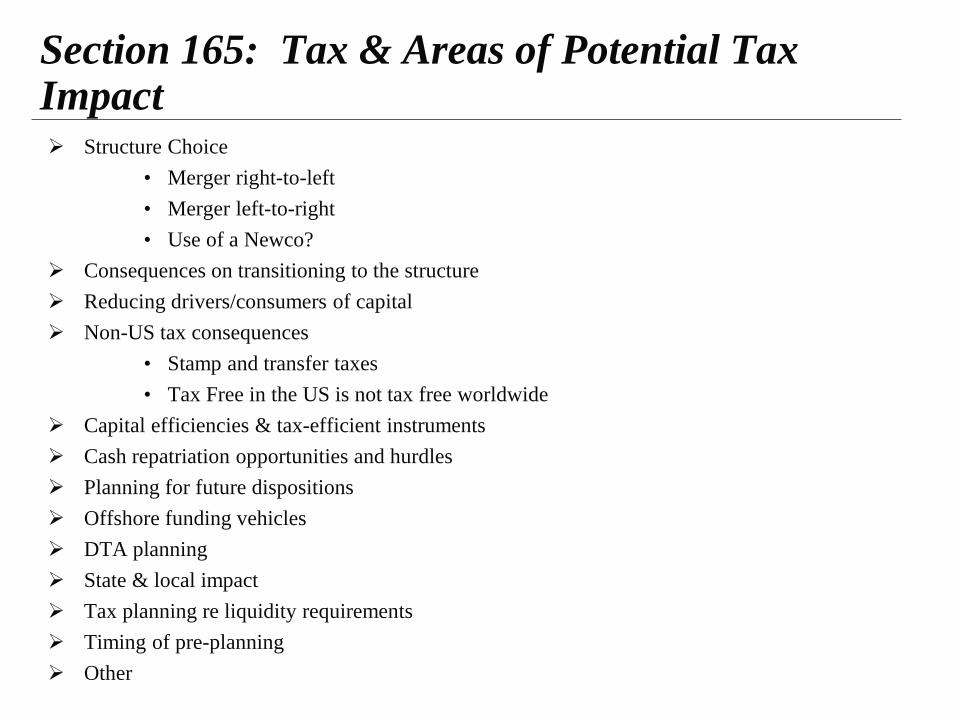

Section 165: Tax & Areas of Potential Tax Impact Structure Choice

• Merger right-to-left • Merger left-to-right • Use of a Newco?

Consequences on transitioning to the structure Reducing drivers/consumers of capital Non-US tax consequences

• Stamp and transfer taxes • Tax Free in the US is not tax free worldwide

Capital efficiencies & tax-efficient instruments Cash repatriation opportunities and hurdles Planning for future dispositions Offshore funding vehicles DTA planning State & local impact Tax planning re liquidity requirements Timing of pre-planning Other

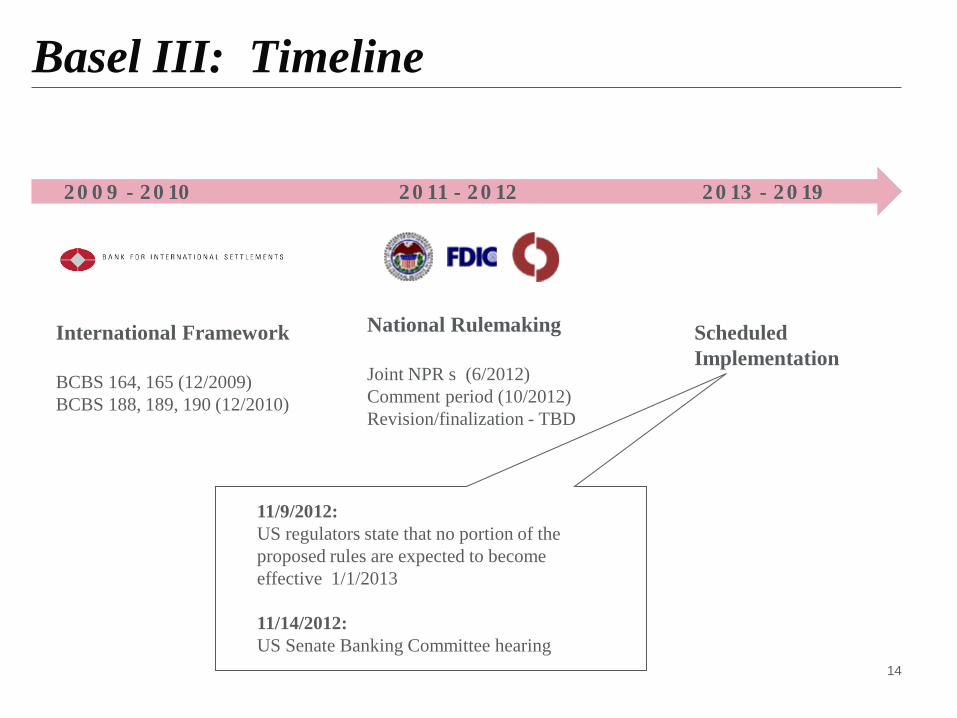

Basel III: Timeline

14

2009 - 2010

International Framework BCBS 164, 165 (12/2009) BCBS 188, 189, 190 (12/2010)

National Rulemaking Joint NPR s (6/2012) Comment period (10/2012) Revision/finalization - TBD

2011 - 2012 2013 - 2019

Scheduled Implementation

11/9/2012: US regulators state that no portion of the proposed rules are expected to become effective 1/1/2013 11/14/2012: US Senate Banking Committee hearing

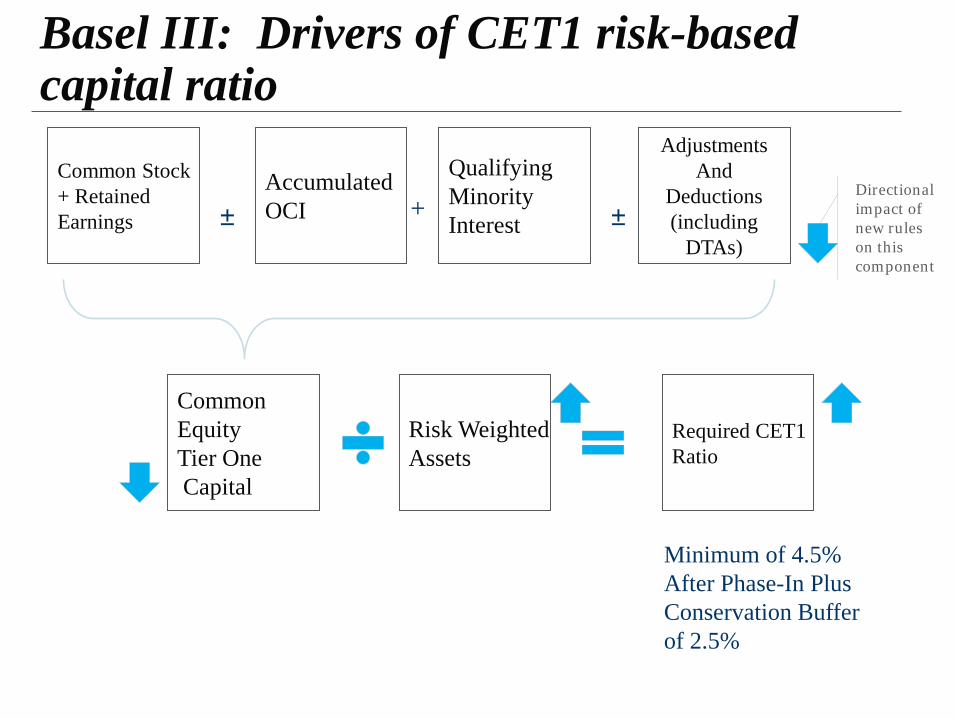

Basel III: Drivers of CET1 risk-based capital ratio

Common Stock + Retained Earnings

Accumulated OCI

Qualifying Minority Interest

Adjustments And

Deductions (including

DTAs)

Common Equity Tier One Capital

Risk Weighted Assets

± ± +

Required CET1 Ratio

Minimum of 4.5% After Phase-In Plus Conservation Buffer of 2.5%

Directional impact of new rules on this component

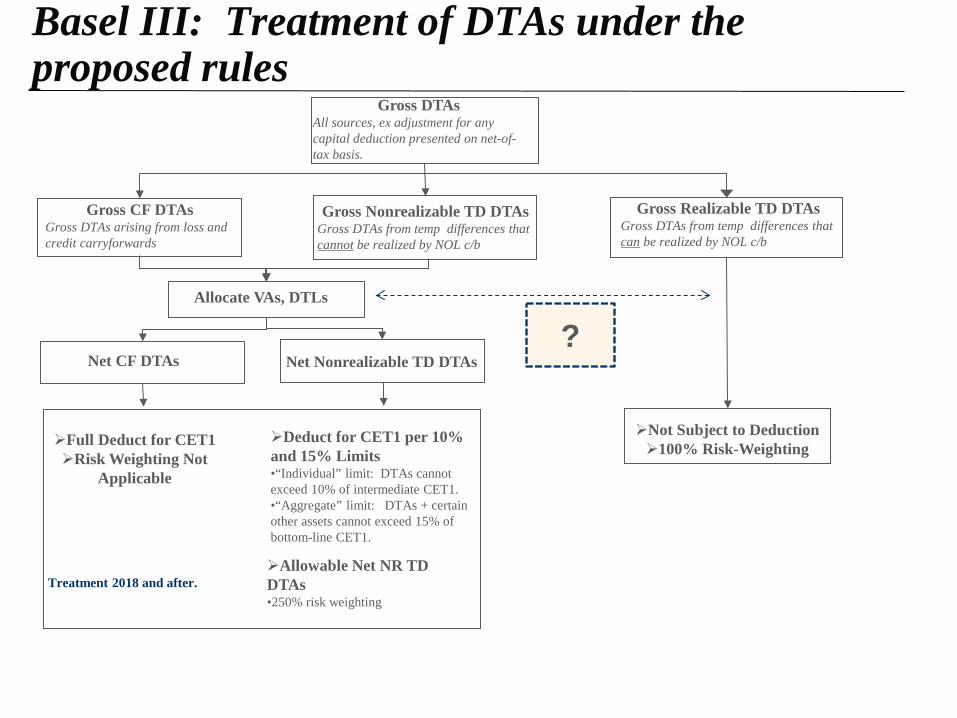

Basel III: Treatment of DTAs under the proposed rules

Gross DTAs All sources, ex adjustment for any capital deduction presented on net-of-tax basis.

Deduct for CET1 per 10% and 15% Limits •“Individual” limit: DTAs cannot exceed 10% of intermediate CET1. •“Aggregate” limit: DTAs + certain other assets cannot exceed 15% of bottom-line CET1.

Allowable Net NR TD DTAs •250% risk weighting

Gross Realizable TD DTAs Gross DTAs from temp differences that can be realized by NOL c/b

Gross Nonrealizable TD DTAs Gross DTAs from temp differences that cannot be realized by NOL c/b

Gross CF DTAs Gross DTAs arising from loss and credit carryforwards

Allocate VAs, DTLs

Net CF DTAs Net Nonrealizable TD DTAs

Not Subject to Deduction 100% Risk-Weighting Full Deduct for CET1

Risk Weighting Not Applicable

Treatment 2018 and after.

?

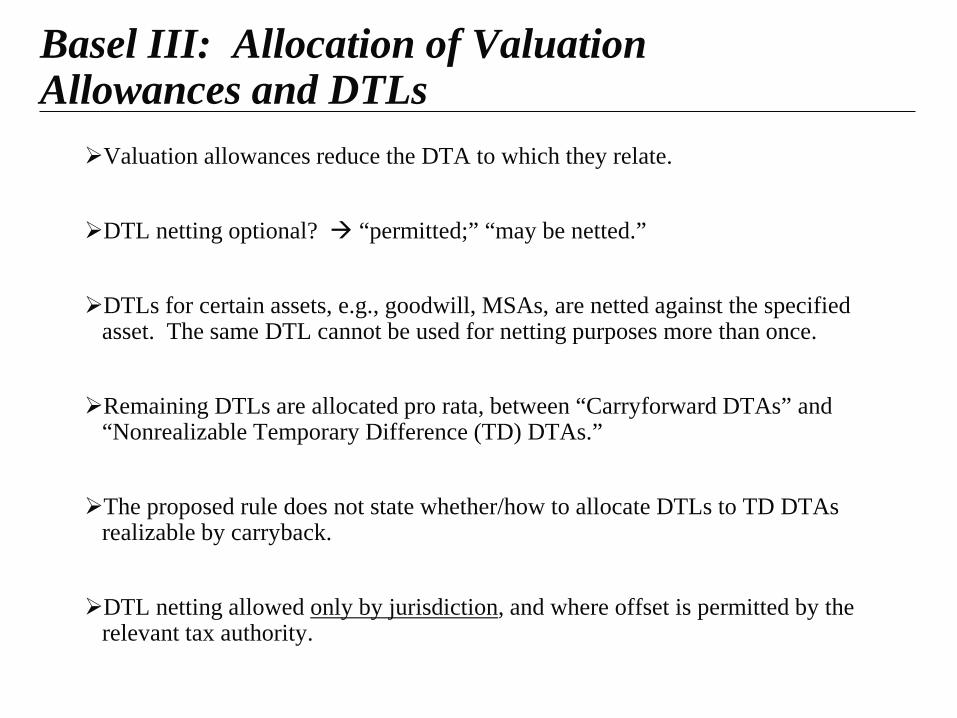

Basel III: Allocation of Valuation Allowances and DTLs

Valuation allowances reduce the DTA to which they relate. DTL netting optional? “permitted;” “may be netted.” DTLs for certain assets, e.g., goodwill, MSAs, are netted against the specified

asset. The same DTL cannot be used for netting purposes more than once. Remaining DTLs are allocated pro rata, between “Carryforward DTAs” and

“Nonrealizable Temporary Difference (TD) DTAs.” The proposed rule does not state whether/how to allocate DTLs to TD DTAs

realizable by carryback. DTL netting allowed only by jurisdiction, and where offset is permitted by the

relevant tax authority.

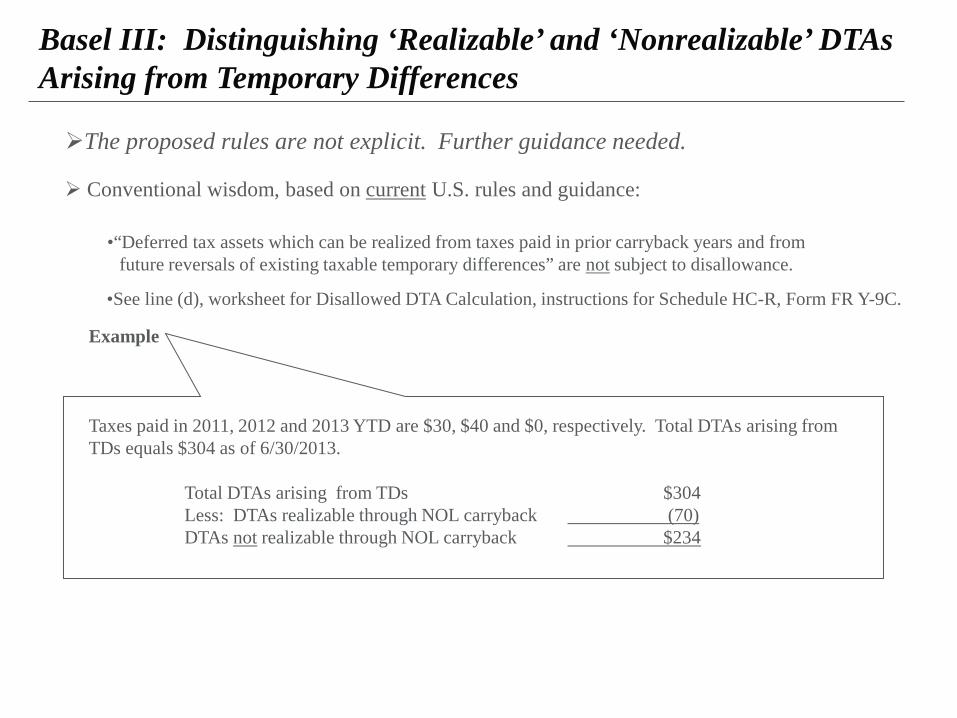

The proposed rules are not explicit. Further guidance needed. Conventional wisdom, based on current U.S. rules and guidance:

•“Deferred tax assets which can be realized from taxes paid in prior carryback years and from future reversals of existing taxable temporary differences” are not subject to disallowance.

•See line (d), worksheet for Disallowed DTA Calculation, instructions for Schedule HC-R, Form FR Y-9C.

Example Taxes paid in 2011, 2012 and 2013 YTD are $30, $40 and $0, respectively. Total DTAs arising from TDs equals $304 as of 6/30/2013. Total DTAs arising from TDs $304 Less: DTAs realizable through NOL carryback (70) DTAs not realizable through NOL carryback $234

Basel III: Distinguishing ‘Realizable’ and ‘Nonrealizable’ DTAs Arising from Temporary Differences

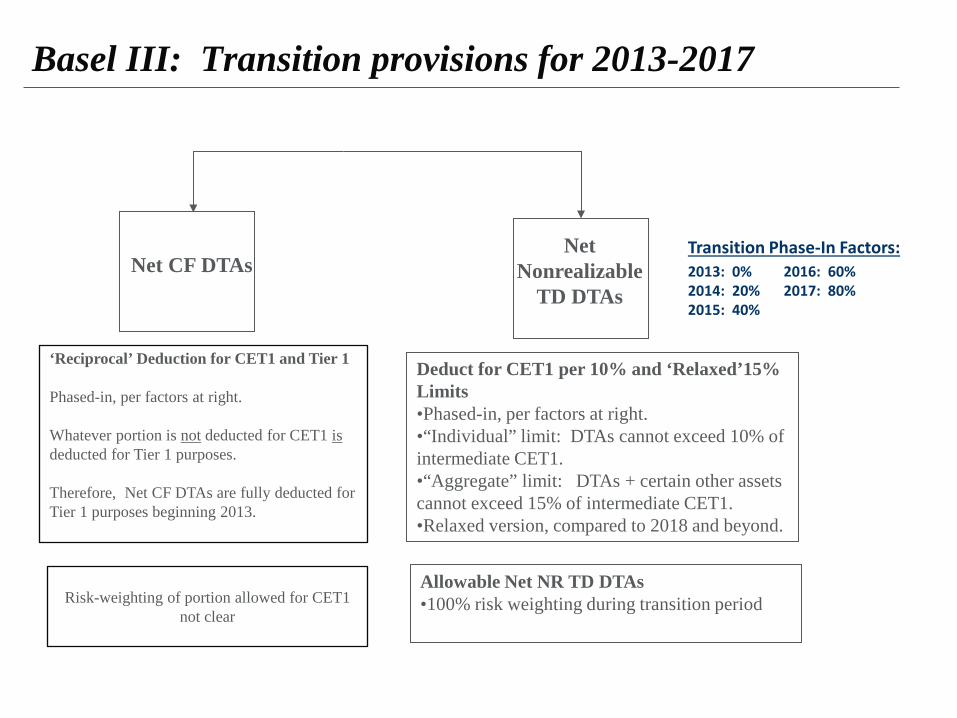

Basel III: Transition provisions for 2013-2017

Net CF DTAs Net

Nonrealizable TD DTAs

Deduct for CET1 per 10% and ‘Relaxed’15% Limits •Phased-in, per factors at right. •“Individual” limit: DTAs cannot exceed 10% of intermediate CET1. •“Aggregate” limit: DTAs + certain other assets cannot exceed 15% of intermediate CET1. •Relaxed version, compared to 2018 and beyond.

Allowable Net NR TD DTAs •100% risk weighting during transition period

Risk-weighting of portion allowed for CET1 not clear

‘Reciprocal’ Deduction for CET1 and Tier 1 Phased-in, per factors at right. Whatever portion is not deducted for CET1 is deducted for Tier 1 purposes. Therefore, Net CF DTAs are fully deducted for Tier 1 purposes beginning 2013.

Transition Phase-In Factors: 2013: 0% 2016: 60% 2014: 20% 2017: 80% 2015: 40%

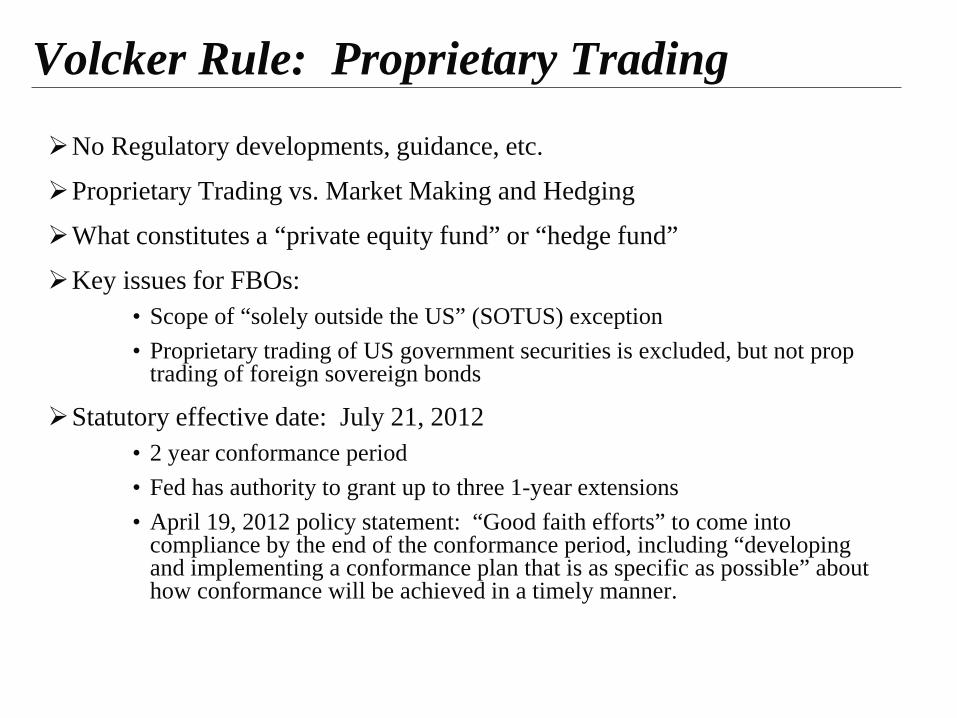

Volcker Rule: Proprietary Trading

No Regulatory developments, guidance, etc.

Proprietary Trading vs. Market Making and Hedging

What constitutes a “private equity fund” or “hedge fund”

Key issues for FBOs: • Scope of “solely outside the US” (SOTUS) exception • Proprietary trading of US government securities is excluded, but not prop

trading of foreign sovereign bonds

Statutory effective date: July 21, 2012 • 2 year conformance period • Fed has authority to grant up to three 1-year extensions • April 19, 2012 policy statement: “Good faith efforts” to come into

compliance by the end of the conformance period, including “developing and implementing a conformance plan that is as specific as possible” about how conformance will be achieved in a timely manner.

Tax Considerations Related to the “Volcker Rule” The “Volcker Rule” generally prohibits banking entities from

engaging in “proprietary trading” or retaining any equity, partnership, or other interest in or sponsoring a hedge fund or a private equity fund.

In order conform their activities to the Volcker Rule (during the regulatory conformance period which ends in July 2014, with the possibility of extensions), affected entities have engaged in a number of transactions:

• Eliminating certain trading books either by disposing of the underlying positions to third parties or moving them to different customer-facing areas within a firm (including moving employees);

• Migrating trading activity to non-U.S. exchanges/markets; and • Disposing of most LP and all GP interests in hedge funds and private

equity funds.

Tax Considerations Related to the “Volcker Rule”

Many of the tax considerations related to any internal restructurings to comply with the Volcker Rule are similar as those discussed in connection with living wills.

• Spin-offs and internal reorganizations may be considered.

Where a different party becomes the counterparty of a contract with a third party, the contract may be viewed as terminated by the original parties and entered into between the new parties for tax purposes.

Transfer pricing issues are relevant when shifting activities off-shore.

In addition, gain recognition may be required when moving assets off-shore unless an agreement is entered into with the IRS.

continued

Succession Planning: “Living Wills” Regulatory Developments

• The first prescribed Section 165 enhanced prudential standard • Annual submissions, but staged implementation based on size of non-bank

assets (for FBOs – U.S. operations only) Stage 1: $250 billion or more – first plans submitted July 1, 2012

o Due date for 2013 plans extended to October 1 Stage 2: between $250 billion and $100 billion – first filing required July 1,

2013 Stage 3: < $100 billion – first filing required December 31, 2013

o “Tailored” plans for those with at least 85% “banking” assets in the US

• Ultimately: regulatory authority to require changes in size and structure if plans are not “credible”

• FBO resolution plans focuses on U.S. operations and their interconnections with non-U.S. operations Identification of material entities, core business lines, critical operations Key impediments to resolution (e.g., servicing arrangements)

Tax Considerations Related to “Living Wills” Under Dodd-Frank, certain large bank holding companies (as well as certain

foreign banking organizations and non-bank financial companies) are required report to U.S. financial regulators on their plans for “rapid and orderly resolution in the event of material financial distress or failure” under the U.S. Bankruptcy Code.

• These reports have come to be known as “living wills.”

In order to substantiate that their “living wills” are credible, affected financial institution groups have engaged in a number of internal transactions to reduce the level of complexity of their structure, including:

• eliminating entities by merger, liquidation, or otherwise; • reconfiguring their subsidiaries to reduce complex ownership structures;

and • terminating ongoing inter-company transactions and contractual

relationships.

Tax Considerations Related to “Living Wills” Transactions Between Affiliates:

• Generally, transactions taking place between and among members of an affiliated group do not give rise to immediate tax liability for federal income tax purposes.

• However, certain states without analogous regimes may impose tax on transactions which are not taxable at the federal level. For example, transactions between so-called Article 9-A filers (most corporations) and so-called Article 32 filers (“banking corporations”) in New York can give rise to tax in the state.

• Because only entities treated as corporations for tax purposes that are connected through 80% or greater stock ownership may file a consolidated return with their affiliates, transactions between such corporations and entities that are treated as partnerships for tax purposes, even if all the partnership interests are ultimately held within the affiliated group, are not automatically exempt from current taxation at the federal level.

• Foreign entities may not join a U.S. affiliated group of corporations. Complex rules apply when assets or stock is transferred to foreign corporations in otherwise tax-free exchanges to allow a domestic transferor to ensure deferred tax treatment.

continued

Tax Considerations Related to “Living Wills” Contributions of Assets or Stock:

• Generally, contributions to partnerships and controlled corporations are tax-deferred transactions.

• However, where the contributee controlled corporation is an “investment company” or the contributee partnership would be an “investment company” if it were a corporation, tax-deferred treatment is generally denied where the transfers result in diversification of the transferors’ interests.

• An “investment company” is defined as a regulated investment company, a REIT, or a corporation more than 80% of the value of whose assets are held for investment and are readily marketable stocks or securities or interests in RICs or REITs.

• Cash is treated as a diversifying asset. • In the context of transactions to accommodate the establishment of “living wills,”

the investment company issue often becomes relevant because such entities are commonly encountered in large banking organizations.

continued

Tax Considerations Related to “Living Wills” Distributions of Assets or Stock:

• Intercompany dividends generally do not give rise to immediate tax liability but when property other than cash that was distributed as a dividend is subsequently transferred outside of the affiliated group, the built-in gain at the time of the distribution is taxable.

• Distributions by a corporation of stock of a corporation which it controls (generally, by owning more than 80% thereof) may also be structured to qualify as tax-free spin-offs.

• However, the requirements that must be met to qualify under the spin-off rules are relatively burdensome and complex, and the IRS has recently receded from certain taxpayer-friendly ruling practices.

• In particular, the requirement that both the distributing and the controlled corporations be engaged in an active business has to be considered carefully where passive entities are involved.

• Acquisition of active business in taxable vs. non-taxable transactions. • Acquisition of active business in internal restructurings vs. from independent third

parties.

continued

Tax Considerations Related to “Living Wills”

Certain Other Issues: • Restructurings designed to qualify under the reorganization

provisions of the Code and that involve passive entities have to confront a similar “investment company” issue and whether the “continuity of business enterprise” test can be met.

• Restructurings involving foreign disregarded entities may trigger previously made domestic use elections with respect to dual consolidated losses incurred as a result of the activities of such entities; such triggering events can generally be cured if the relevant transferee domestic owners make renewed domestic use elections.

• Transactions involving the reconfiguration of partnerships may lead to partnership terminations which raise a number of issues.

continued

![SDRS PRICE M? -S0.76 ABSTP ACT This module is ... › fulltext › ED103404.pdfDOCUMENT RESUME ED 103 404 SP 009 011 AUTHOR Pransson, Dale TITLE [Group Dynamics.] MOTE 43p, SDRS PRICE](https://img.pdfslide.net/doc/110x75/5f12b8591c856c2a641841c6/sdrs-price-m-s076-abstp-act-this-module-is-a-fulltext-a-document-resume.jpg)

![[Webinar] Give Your SDRs An Unfair Advantage with Predictive](https://img.pdfslide.net/doc/110x75/58e9eeaa1a28ab9c208b550f/webinar-give-your-sdrs-an-unfair-advantage-with-predictive.jpg)