Embed Size (px)

Citation preview

1

Finnair Q4 and FY 2017 result

16.2.2018Pekka Vauramo

2017 – A year of strong growth

• Comparable operating result at record level, 22.9 million euro (Q4 2016: 1.6)

• Fastest growth in Finnair history, ASK +17%• Four new long-haul routes opened• Added capacity to Lapland • Passenger revenue +12%, ancillary sales

+17%• Almost 3 million passengers, up +14%• Cargo revenue up +24%• Travel services revenue up +14%,

Aurinkomatkat Suntours is the market leader

2

A record Q4 concluded a strong year 2017

• Demand for flights between Asia and Europe increased across the Finnair network to almost every destination. Strong demand from Japan.

• Lapland was again the #1 destination for Finnair’s Chinese customers in the winter season.

• The air cargo market continued to grow, and cargo load factors and yields increased.

• Severe winter and wind condictions and overtime ban by IAU affected Finnair traffic in December.

• Industry consolidation continues in Europe.

3

Favourable market environment– also challenges towards the year end

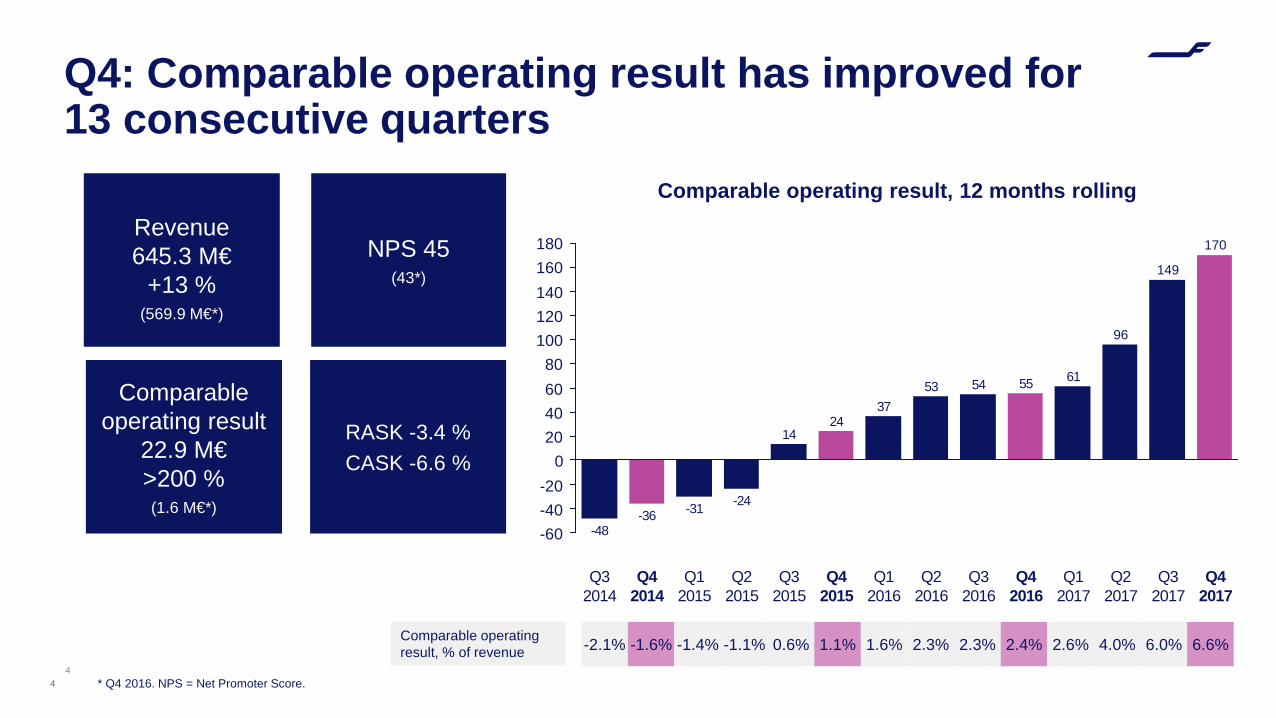

Q4: Comparable operating result has improved for 13 consecutive quarters

Comparable operating result, 12 months rolling

4

100

180

0

140

60

20

-60-40

80

-20

40

120

160

-48-36

Q3 2015

55

24

61

Q4 2016

Q1 2016

Q3 2017

149

Q2 2017

96

Q1 2017

53

Q3 2014

170

Q4 2017

Q3 2016

Q4 2014

54

Q4 2015

Q2 2015

14

-24

Q1 2015

-31

Q2 2016

37

4

Revenue645.3 M€

+13 %(569.9 M€*)

Comparable operating result

22.9 M€>200 %(1.6 M€*)

RASK -3.4 %CASK -6.6 %

NPS 45 (43*)

* Q4 2016. NPS = Net Promoter Score.

Comparable operating result, % of revenue -2.1% -1.6% -1.4% -1.1% 0.6% 1.1% 1.6% 2.3% 2.3% 2.4% 2.6% 4.0% 6.0% 6.6%

Revenue, M€

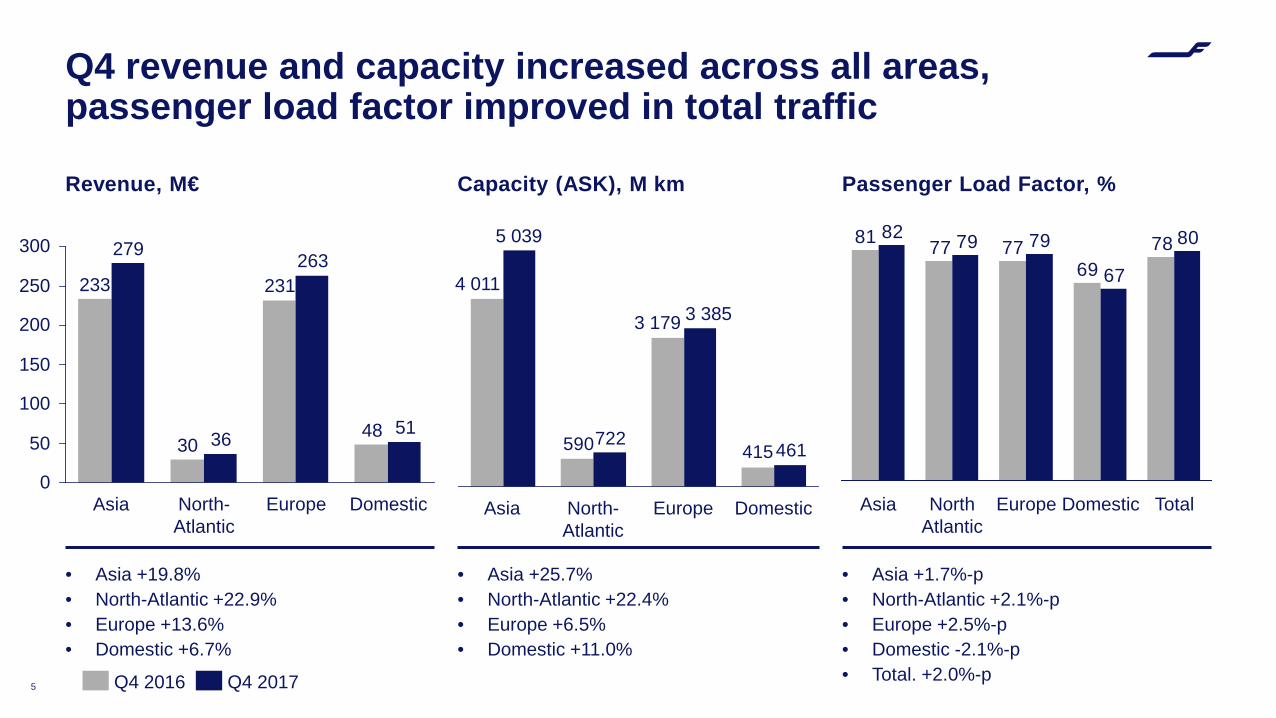

• Asia +19.8%• North-Atlantic +22.9%• Europe +13.6%• Domestic +6.7%

Passenger Load Factor, %

5

• Asia +1.7%-p• North-Atlantic +2.1%-p• Europe +2.5%-p• Domestic -2.1%-p• Total. +2.0%-p

Capacity (ASK), M km

• Asia +25.7%• North-Atlantic +22.4%• Europe +6.5%• Domestic +11.0%

415590 461722

Europe

3 3853 179

DomesticNorth-Atlantic

5 039

4 011

Asia

7869

777781 80

67

797982

Europe Domestic TotalNorth Atlantic

Asia

250

200

150

0

300

100

50 36

263

North-Atlantic

Asia

233 231

30

279

Europe Domestic

5148

Q4 2017Q4 2016

Q4 revenue and capacity increased across all areas, passenger load factor improved in total traffic

12

-36

24

55

170

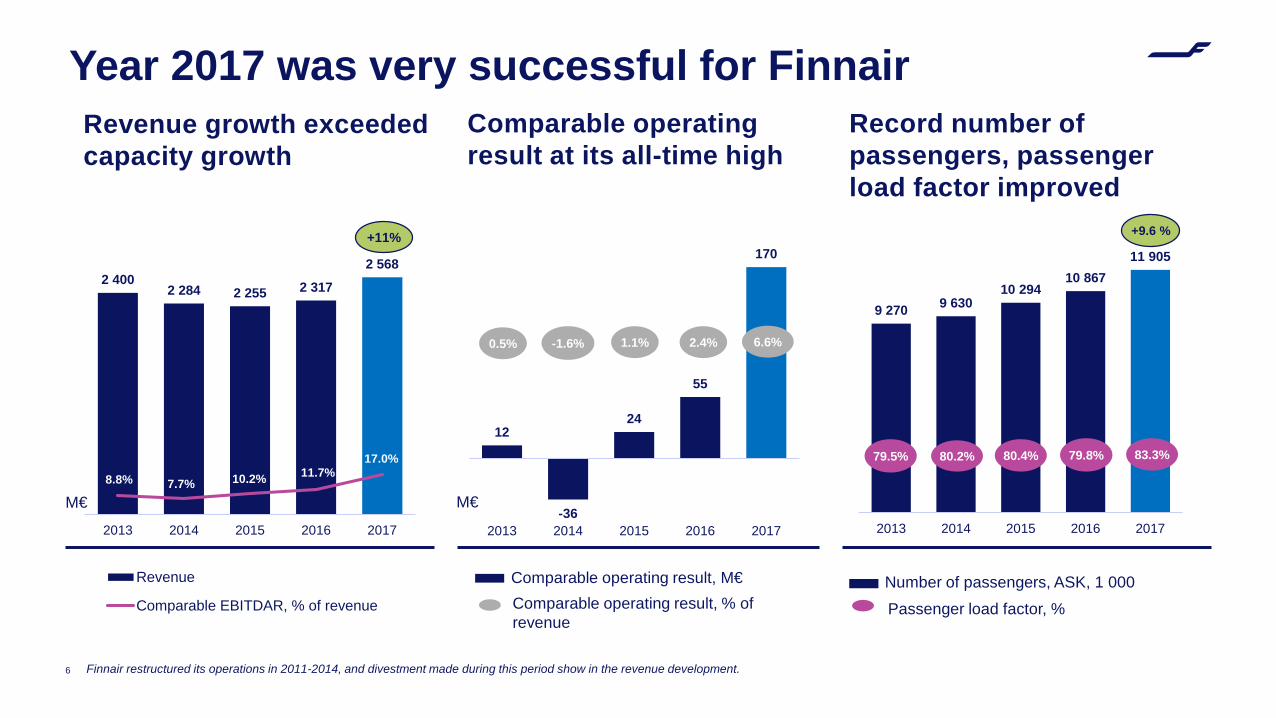

2013 2014 2015 2016 2017

Revenue growth exceeded capacity growth

Record number of passengers, passenger load factor improved

6

Year 2017 was very successful for Finnair

2 4002 284 2 255 2 317

2 568

8.8% 7.7% 10.2% 11.7%17.0%

2013 2014 2015 2016 2017

Revenue

Comparable EBITDAR, % of revenue

9 270 9 63010 294

10 86711 905

2013 2014 2015 2016 2017

Comparable operating result at its all-time high

1.1% 2.4%-1.6%0.5%

Comparable operating result, % of revenue

Finnair restructured its operations in 2011-2014, and divestment made during this period show in the revenue development.

79.8%

Passenger load factor, %

83.3%

6.6%

79.5% 80.2% 80.4%

M€ M€

+11%

Comparable operating result, M€ Number of passengers, ASK, 1 000

+9.6 %

Major steps forward in sustainability in 2017• A350 aircraft have reduced our CO2 emissions

considerably: • Emissions/RTK decreased by 6.7% • Emissions/ ASK decreased by 3.2%• Total emissions grew clearly less (+5.4%) than ATK (+9.9%).

• Finnair published its commitment to sustainability (Commitment 2050) and is committed to promote equality and non-discrimination in its own activities and in customer services

• We Together@Finnair survey also included the questions about non-discrimination. The result was 3.98/5.

• Inflight videos in sign-language and more accessible booking process.

7

A great people experience builds a great customer experience

8

• Employee satisfaction up year-on-year• Investments in wellbeing are seen in

lower sickness and lower injury rates, LTIF (Lost Time Injury Frequency)

• 10 million euro training investment, a total of 370,000 training hours• Customer experience• Digital competencies• Leadership

• Finnair recruited 1,000 new employees in 2017, and has recruited a total of 1 800 new employees since beginning of 2016

Personnel was rewarded for

Finnair turnaround with up to €2,000

special reward

€6.7 million to Finnair’s

personnel fund

Positive developments in customer experience • Investments into personal service

• NPS 47 for the full year 2017 (43 in 2016), high point of 52 in Q3

• 2018 updates• Services and meals targeted at families

with children• New menus on board• Ancillary products, such as Seat & meal• New elements in long-haul business class• Wi-Fi for European Airbus fleet

9

NPS 47

in 2017

Digital developments support growth• Digital channels generate 24% of ticket sales,

up +18% year-on-year• 30% of ancillary sales through digital channels• Our webstore had on average 1.8 million

monthly visitors in 2017, up +17% year-on-year• 210,000 active users for Finnair mobile app• New sales channels and mobile payments:

• WeChat• Finnair flagship stores on partner platforms

(Alitrip, JD.com)• Alipay, WeChatPay, ApplePay

• Digitools for personnel • SkyPay• Mobile apps in Technical Services• iPhones and apps for Finnair personnel

10

Finnair equips all personnel with iPhones during

2018

11

Goa, IndiaPuerto Vallarta, Mexico Puerto Plata, Dominican republicHavana, Cuba

2018/2019: more flights than ever before

Nanjing three times a week as of May 2018, year-round destination38 weekly frequencies to both China and Japan. 97 weekly flights to Asia in summer 2018

Stuttgart, Lisbon, Bergen and Tromsø

Berlin, Tallinn, Moscow, Gdansk, Edinburgh, Barcelona, Madrid, ReykjavikTokyo, Bangkok, DelhiChicago, San FranciscoKuusamo

Over 230 new flights to LaplandNon-stop flights to Lapland from Paris, London, ZürichAdditional frequencies to Hongkong, Osaka, PhuketNew W17/18 destinations continue

New long-haul routes W17/18

More Asian traffic Summer 2018 additions

Winter 2018/2019Summer 2018 new destinations

Share price development past 12 months(15 Feb 2017 – 14 Feb 2018)

12

Closing 14 Feb 0188.70 euros,

Market cap 1,117.35million euros

Strategy 2018−2020

• The growth plan and the four previous focus areas were reviewed and confirmed:

• Doubling of Asian traffic in 2018 versus 2010 (two years ahead of original schedule)

• Doubling of ancillary revenues in 2020 versus 2016

• New target for the number of passengers, 20 million in 2030

13

Financial targets unchanged: • EBIT margin 6% over cycle • EBITDAR margin minimum of

17% over cycle• Adjusted gearing maximum of

175% • Return on capital employed

(ROCE) minimum of 7%

Growth Customer Experience

People Experience

Transfor-mation

Dividend proposal• The Board of Directors proposes to the Annual

general Meeting that a dividend of 0.30 euros per share be distributed for 2017.

• EPS 1.23 euros in 2017 (0.55).

• Annual General Meeting 2018 will be held in Helsinki on 20 March 2018.

14

• Global airline traffic is expected to grow strongly in 2018. Finnair expects increased competition as existing and new operators increase capacity, particularly on routes linking Europe with Asia and with North America.

• Finnair plans on increasing its capacity by more than 15 per cent in 2018, with most of this growth coming in the first half of the year. Passenger volume is expected to grow broadly in line with capacity while revenue growth is expected to be slightly lower.

• In line with its disclosure policy, Finnair will issue guidance on its full year comparable operating result as part of its half-year report in July.

15

Outlook

16

FinanceCFO Pekka Vähähyyppä

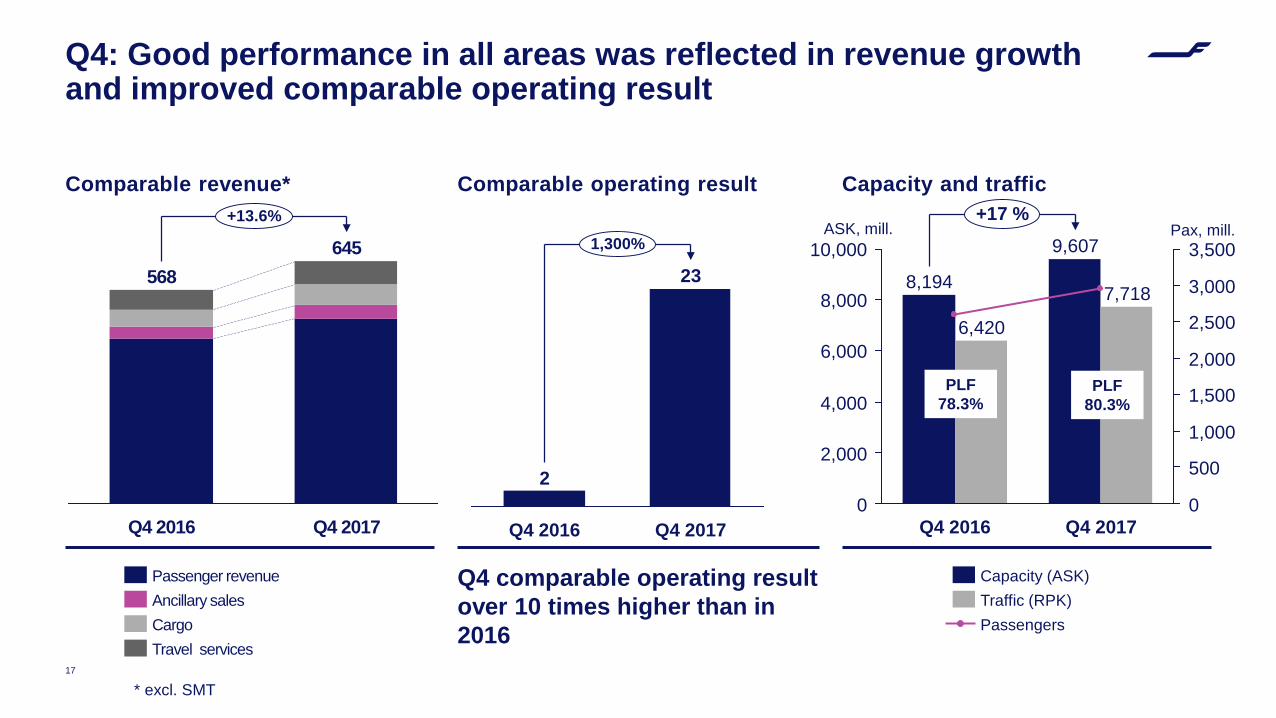

Comparable revenue*

Q4 comparable operating result over 10 times higher than in 2016

Capacity and traffic

17

Q4: Good performance in all areas was reflected in revenue growth and improved comparable operating result

Comparable operating result

568

Q4 2016

+13.6%

Q4 2017

645

Travel servicesCargoAncillary salesPassenger revenue

8,000

6,000

4,000

0

3,000

2,000

2,000

2,500

1,500

10,000 3,500

1,000

500

0

+17 %

Q4 2017

7,718

9,607

Q4 2016

8,194

6,420

Passengers

Capacity (ASK)Traffic (RPK)

Pax, mill.ASK, mill.

PLF 78.3%

PLF 80.3%

* excl. SMT

Q4 2016 Q4 2017

2

1,300%

23

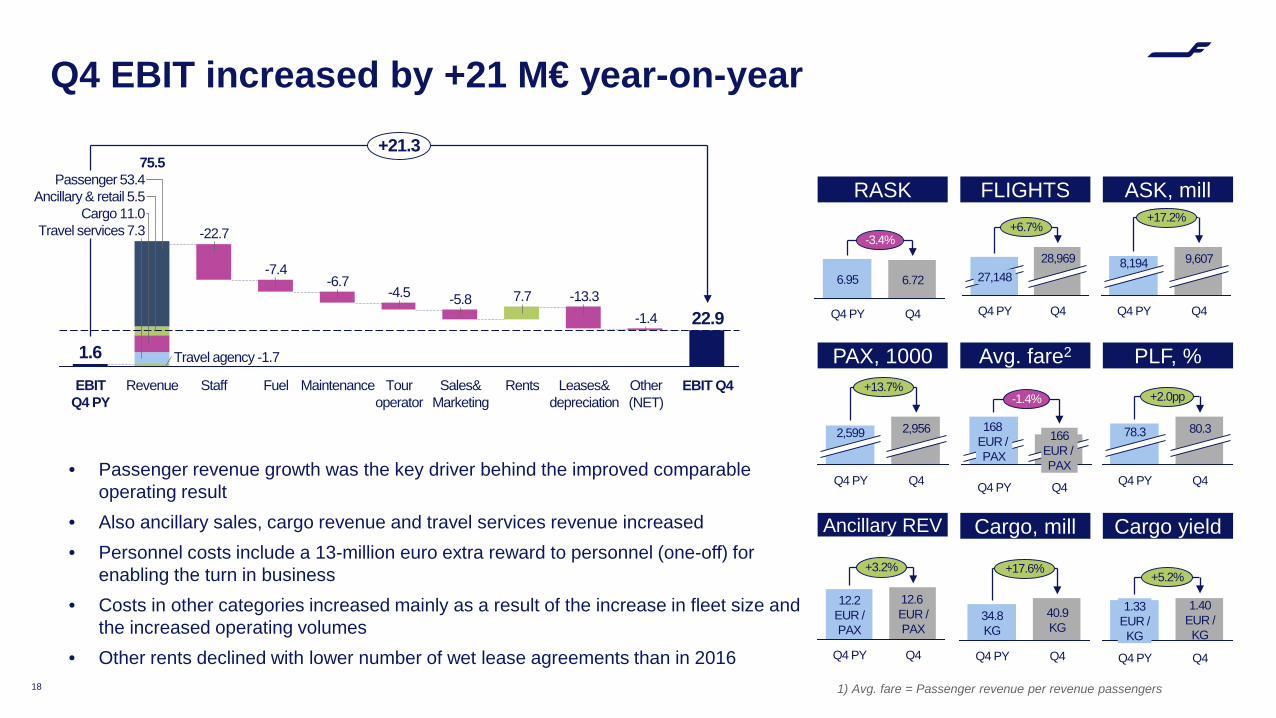

Q4 EBIT increased by +21 M€ year-on-year

• Passenger revenue growth was the key driver behind the improved comparable operating result

• Also ancillary sales, cargo revenue and travel services revenue increased• Personnel costs include a 13-million euro extra reward to personnel (one-off) for

enabling the turn in business• Costs in other categories increased mainly as a result of the increase in fleet size and

the increased operating volumes• Other rents declined with lower number of wet lease agreements than in 2016

18

-22.7

Revenue

Travel services 7.3

Ancillary & retail 5.5Passenger 53.4

EBIT Q4 PY

EBIT Q4

7.7

Tour operator

Other (NET)

-4.5-6.7

Travel agency -1.7

Staff Fuel

Cargo 11.0

Rents

-7.4

75.5

22.9

Leases&depreciation

Sales&Marketing

+21.3

-1.4-13.3-5.8

Maintenance

1.6

27,148

+6.7%

Q4Q4 PY

28,969 9,607

Q4 PY

+17.2%

8,194

Q4

2,599

+13.7%

Q4

2,956

Q4 PY

RASK

168EUR / PAX

Q4

166EUR / PAX

Q4 PY

-1.4%

Q4

+2.0pp

Q4 PY

78.3 80.3

-3.4%

6.95 6.72

Q4Q4 PY

Q4

40.9KG

+17.6%

34.8KG

Q4 PY Q4

1.40EUR /KG

Q4 PY

+5.2%

1.33EUR /KG

FLIGHTS ASK, mill

PAX, 1000 Avg. fare2 PLF, %

Ancillary REV Cargo, mill Cargo yield

12.6EUR /PAX

+3.2%

Q4Q4 PY

12.2EUR /PAX

1) Avg. fare = Passenger revenue per revenue passengers

19

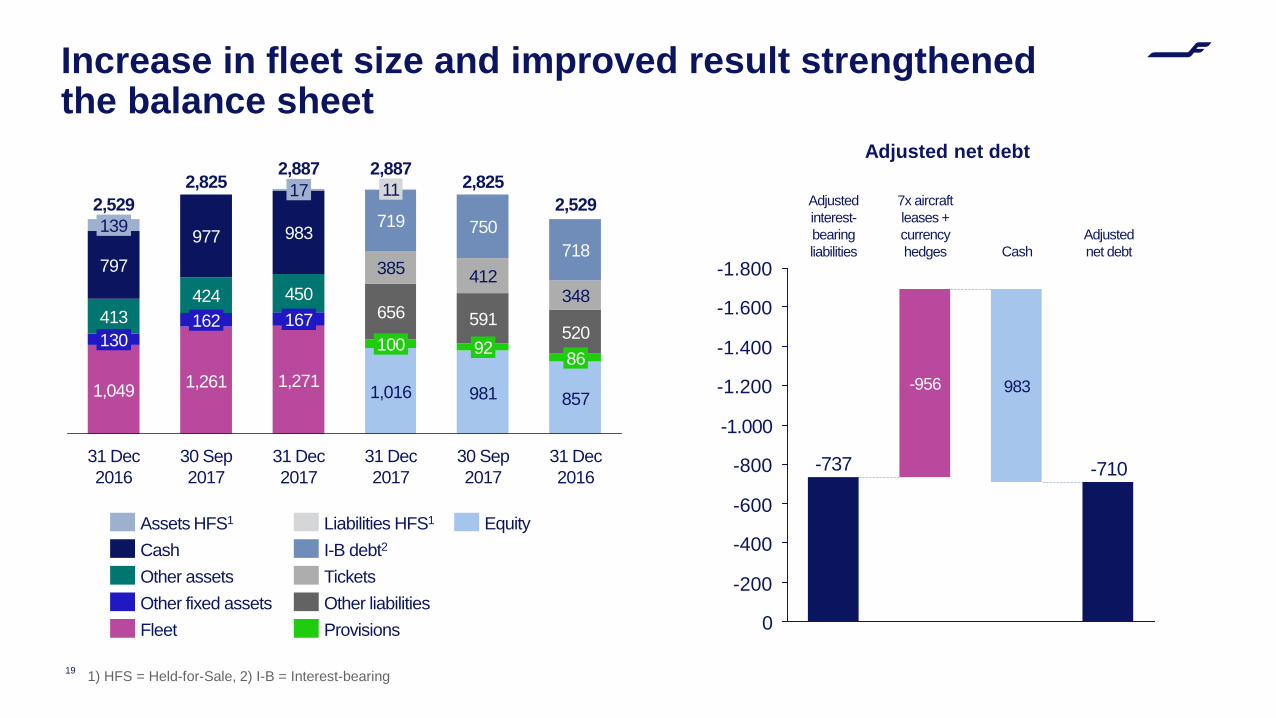

Adjusted net debt

-1.600

-400

-1.800

-1.400

-600

-200

-1.200

-800

0

-1.000

Adjusted net debt

Adjusted interest-bearing liabilities

-710

-956

-737

7x aircraft leases + currency hedges Cash

983

1) HFS = Held-for-Sale, 2) I-B = Interest-bearing

348412

750

591

1,016

2,529

2,8872,825

718

92520100

656

30 Sep 2017

31 Dec 2017

385

719

11

31 Dec 2017

31 Dec 2016

857

86

981

30 Sep 2017

983

162

977

2,529

130

797

139

2,887

1,271

17

450

2,825

1,261

424

31 Dec 2016

167

1,049

413

I-B debt2Liabilities HFS1 Equity

ProvisionsOther liabilitiesTickets

FleetOther fixed assets

Assets HFS1

CashOther assets

Increase in fleet size and improved result strengthened the balance sheet

20

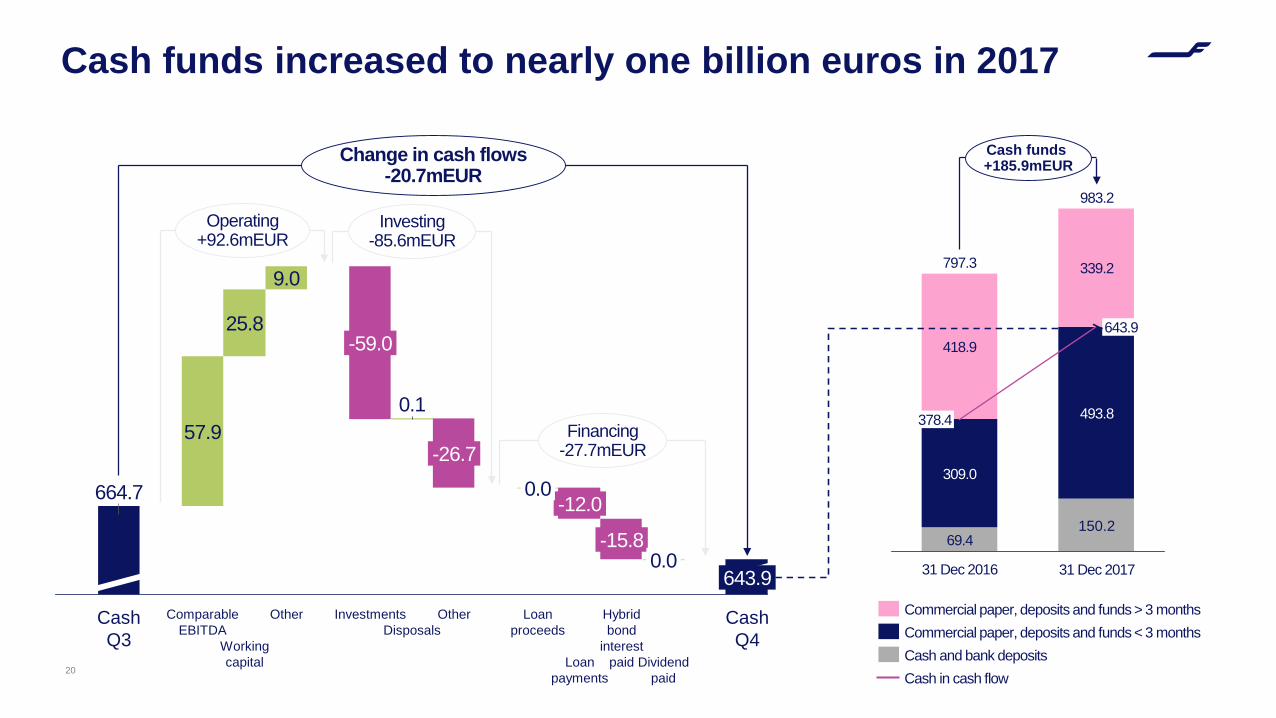

664.7

Working capital

Loan proceeds

-15.8

25.8-59.0

Change in cash flows-20.7mEUR

643.9

Dividend paid

-12.0

0.0

Hybrid bond

interest paid

Investing-85.6mEUR

Financing-27.7mEUR

Operating+92.6mEUR

Cash Q4

OtherOtherComparableEBITDA

0.157.9

Loan payments

0.0

DisposalsInvestments

9.0

Cash Q3

-26.7

Cash funds increased to nearly one billion euros in 2017

31 Dec 2016

797.3

309.0

983.2

493.8

Cash funds+185.9mEUR

31 Dec 2017

339.2

378.4

69.4

418.9643.9

150.2

Cash in cash flow

Commercial paper, deposits and funds > 3 monthsCommercial paper, deposits and funds < 3 monthsCash and bank deposits

Revenue Comparable operating result

21

Revenue and comparable operating result development

0

100

700

800

500

400

300

600

200

735641

Q2

633554 570

Q1

536

Q4

645570

Q3

521 544622 568

201720162015

40

100

0

60

-20

120

20

-40

80

Q1

-9-151

Q3 Q4

2

119

6664

Q2

38

3-13

-28

23

2015 20172016

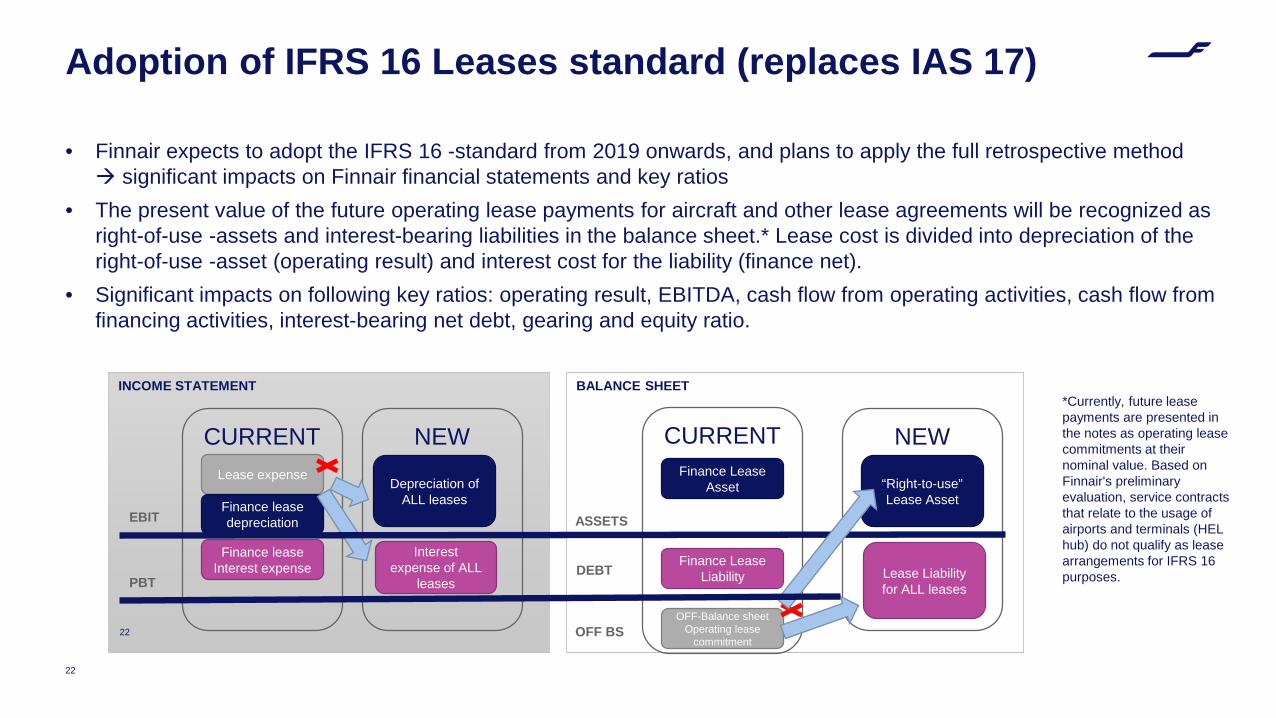

Adoption of IFRS 16 Leases standard (replaces IAS 17)

22

• Finnair expects to adopt the IFRS 16 -standard from 2019 onwards, and plans to apply the full retrospective method significant impacts on Finnair financial statements and key ratios

• The present value of the future operating lease payments for aircraft and other lease agreements will be recognized as right-of-use -assets and interest-bearing liabilities in the balance sheet.* Lease cost is divided into depreciation of the right-of-use -asset (operating result) and interest cost for the liability (finance net).

• Significant impacts on following key ratios: operating result, EBITDA, cash flow from operating activities, cash flow from financing activities, interest-bearing net debt, gearing and equity ratio.

INCOME STATEMENT

22

Lease expense Depreciation of ALL leases

Interest expense of ALL

leases

EBIT

PBT

CURRENT NEW

Finance lease depreciation

Finance lease Interest expense

BALANCE SHEET

CURRENT NEWFinance Lease

Asset

Finance Lease Liability

OFF-Balance sheet Operating lease

commitment

“Right-to-use” Lease Asset

Lease Liability for ALL leases

ASSETS

DEBT

OFF BS

*Currently, future lease payments are presented in the notes as operating lease commitments at their nominal value. Based on Finnair's preliminary evaluation, service contracts that relate to the usage of airports and terminals (HEL hub) do not qualify as lease arrangements for IFRS 16 purposes.

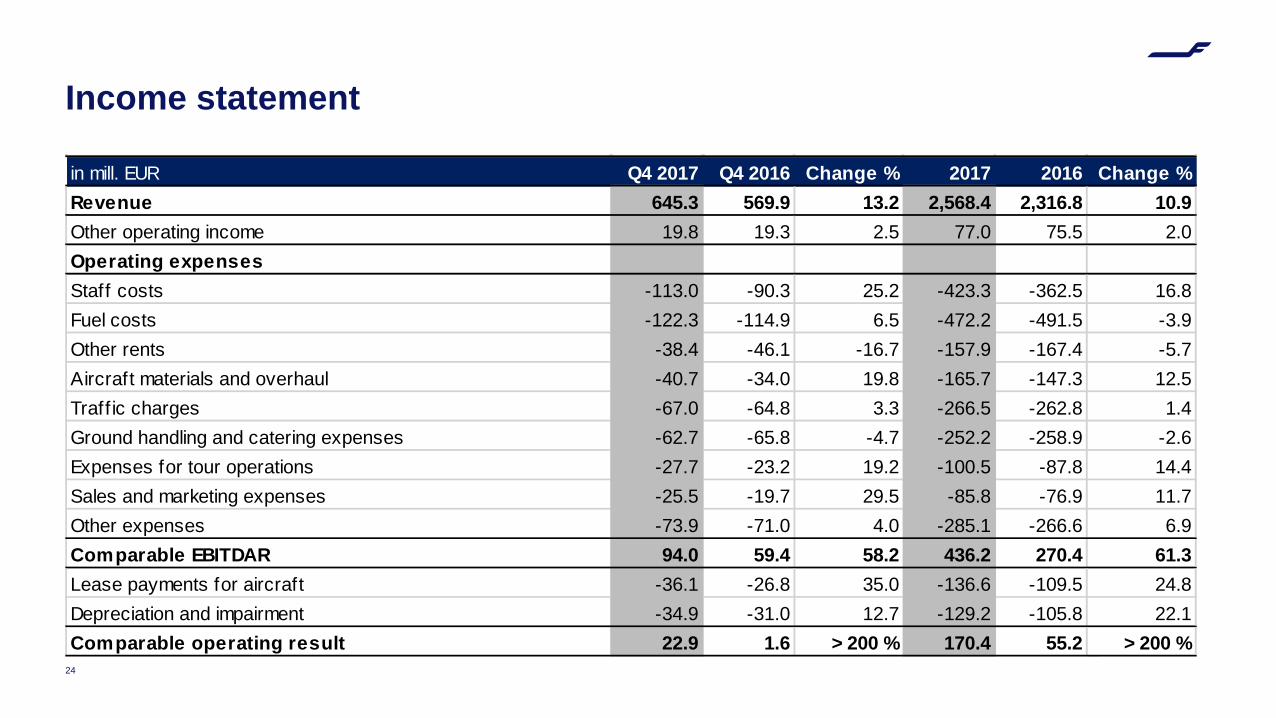

Income statement

24

in mill. EUR Q4 2017 Q4 2016 Change % 2017 2016 Change %Revenue 645.3 569.9 13.2 2,568.4 2,316.8 10.9Other operating income 19.8 19.3 2.5 77.0 75.5 2.0Operating expensesStaff costs -113.0 -90.3 25.2 -423.3 -362.5 16.8Fuel costs -122.3 -114.9 6.5 -472.2 -491.5 -3.9Other rents -38.4 -46.1 -16.7 -157.9 -167.4 -5.7Aircraft materials and overhaul -40.7 -34.0 19.8 -165.7 -147.3 12.5Traff ic charges -67.0 -64.8 3.3 -266.5 -262.8 1.4Ground handling and catering expenses -62.7 -65.8 -4.7 -252.2 -258.9 -2.6Expenses for tour operations -27.7 -23.2 19.2 -100.5 -87.8 14.4Sales and marketing expenses -25.5 -19.7 29.5 -85.8 -76.9 11.7Other expenses -73.9 -71.0 4.0 -285.1 -266.6 6.9Comparable EBITDAR 94.0 59.4 58.2 436.2 270.4 61.3Lease payments for aircraft -36.1 -26.8 35.0 -136.6 -109.5 24.8Depreciation and impairment -34.9 -31.0 12.7 -129.2 -105.8 22.1Comparable operating result 22.9 1.6 > 200 % 170.4 55.2 > 200 %

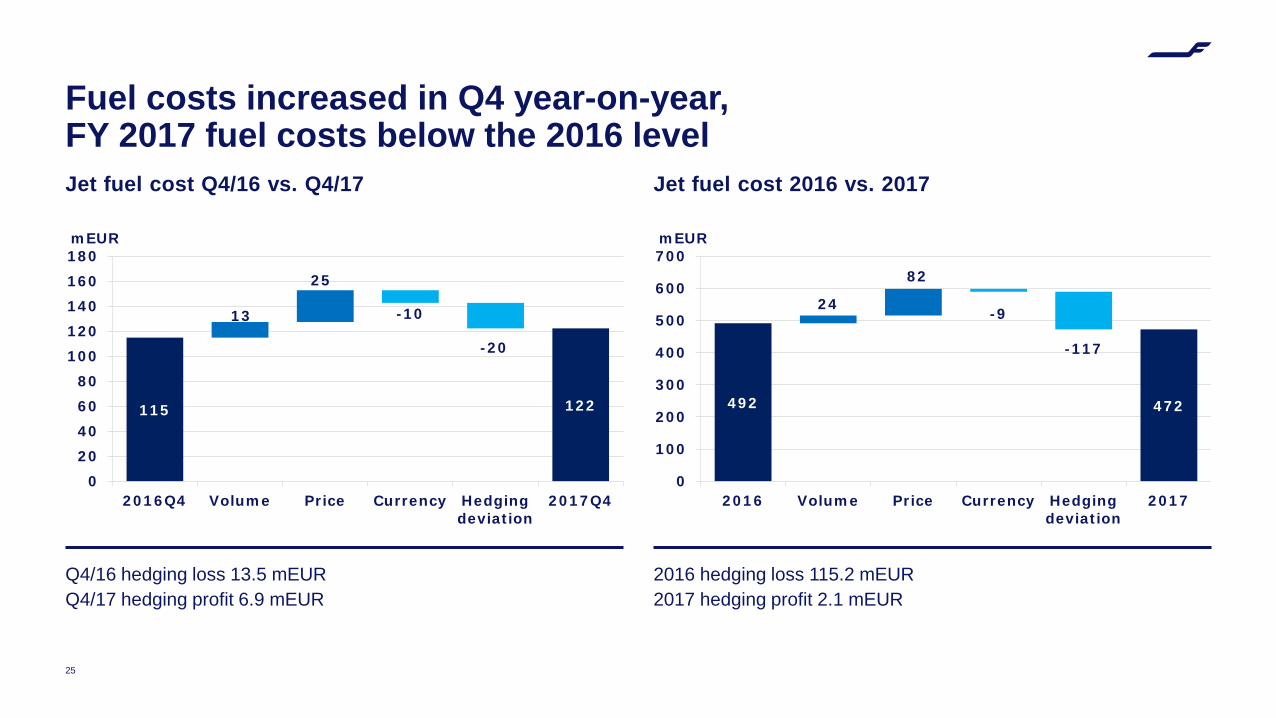

Jet fuel cost Q4/16 vs. Q4/17

Q4/16 hedging loss 13.5 mEURQ4/17 hedging profit 6.9 mEUR

Jet fuel cost 2016 vs. 2017

25

Fuel costs increased in Q4 year-on-year,FY 2017 fuel costs below the 2016 level

2016 hedging loss 115.2 mEUR2017 hedging profit 2.1 mEUR

115 122

13

-20

25

-10

020406080

100120140160180

2016Q4 Volume Price Currency Hedgingdeviation

2017Q4

mEUR

492 472

24

-117

82

-9

0

100

200

300

400

500

600

700

2016 Volume Price Currency Hedgingdeviation

2017

mEUR

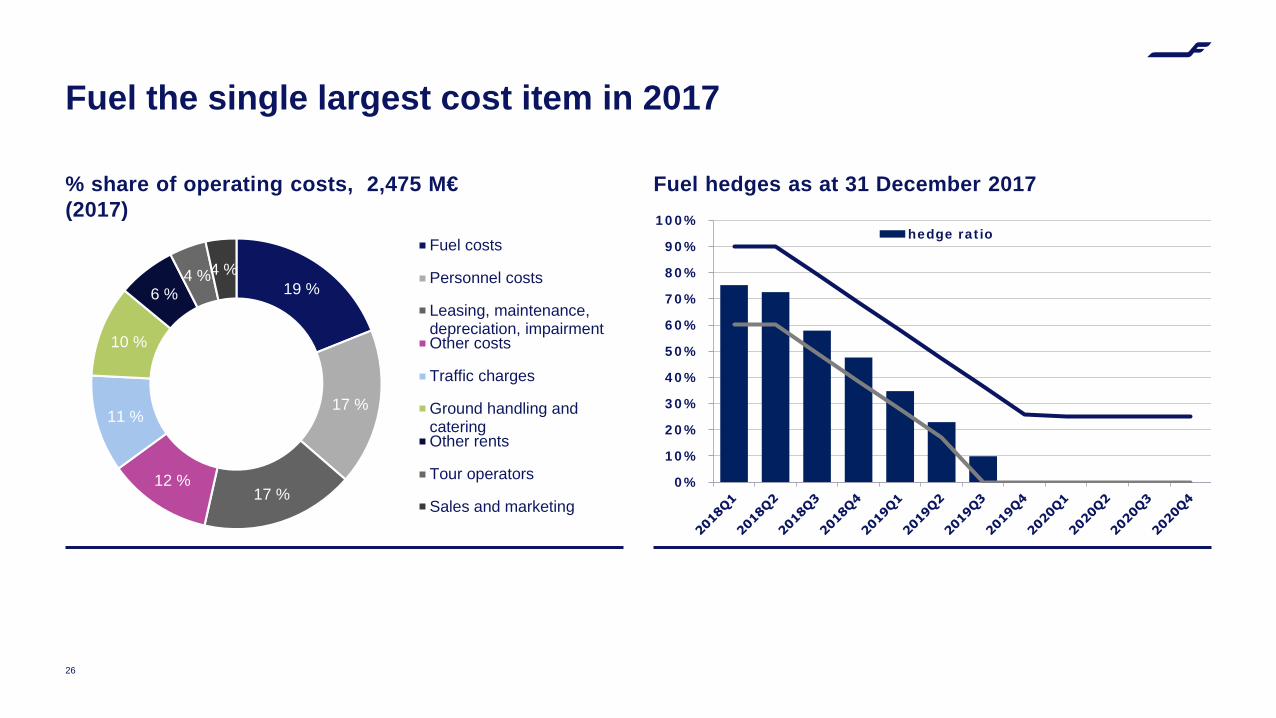

% share of operating costs, 2,475 M€ (2017)

Fuel hedges as at 31 December 2017

26

Fuel the single largest cost item in 2017

19 %

17 %

17 %12 %

11 %

10 %

6 %4 %4 %

Fuel costs

Personnel costs

Leasing, maintenance,depreciation, impairmentOther costs

Traffic charges

Ground handling andcateringOther rents

Tour operators

Sales and marketing0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%hedge ratio

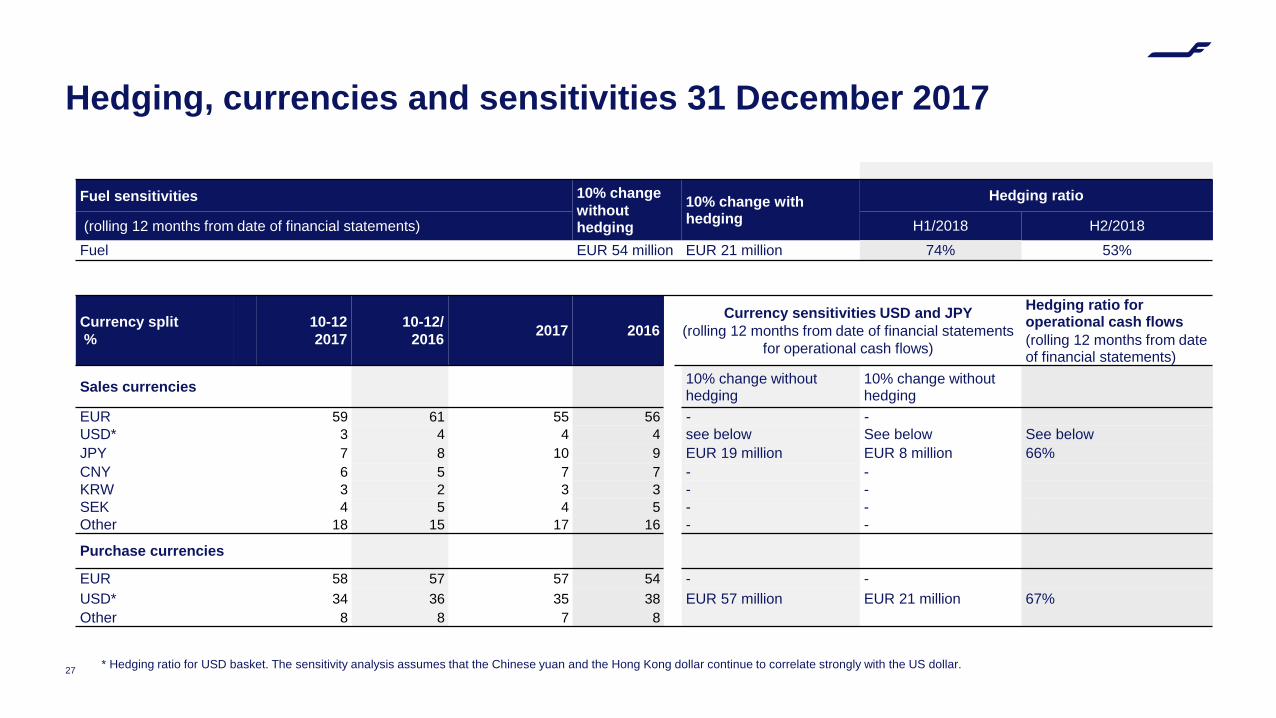

Hedging, currencies and sensitivities 31 December 2017

Fuel sensitivities 10% change without hedging

10% change with hedging

Hedging ratio

(rolling 12 months from date of financial statements) H1/2018 H2/2018Fuel EUR 54 million EUR 21 million 74% 53%

Currency split%

10-122017

10-12/2016 2017 2016

Currency sensitivities USD and JPY(rolling 12 months from date of financial statements

for operational cash flows)

Hedging ratio for operational cash flows(rolling 12 months from date of financial statements)

Sales currencies 10% change without hedging

10% change without hedging

EUR 59 61 55 56 - -USD* 3 4 4 4 see below See below See belowJPY 7 8 10 9 EUR 19 million EUR 8 million 66%CNY 6 5 7 7 - -KRW 3 2 3 3 - -SEK 4 5 4 5 - -Other 18 15 17 16 - -

Purchase currencies

EUR 58 57 57 54 - -USD* 34 36 35 38 EUR 57 million EUR 21 million 67%Other 8 8 7 8

27 * Hedging ratio for USD basket. The sensitivity analysis assumes that the Chinese yuan and the Hong Kong dollar continue to correlate strongly with the US dollar.