Embed Size (px)

Citation preview

2017 Outlook: Continued challenging environment

Prepared by : Ranya Afifi, Director- MENATPresented to Mecomed

The Economist Group

The global consumer will impact oil, trade, and tourism in the region

global narrative

US economic strength promises a tightening cycle- tight liquidity in region has further pushed up interest rate differentials

Monetary policy

The New World Order will affect regional politics perhaps even ushering new roles within the region

geopolitical risks

GCC continues to feel the pinch of tighter liquidity, in spite of increase in oil prices- conditions to continue in 2017

liquidity

GCC asset class is in fierce competition with other EM for FDI and in competition with each other, however fundamentals remain in tact & render a compelling story

investment proposition

Factors Affecting MENA: Exogenous factors as well as regional and local business conditions

Source: ECN

Source:ECN

Saudi vs iran influence

GCC’s regional foreign policy will center around deterring Iran vis-a-vis building a Sunni alliance. Will Trump align with Russia and risk alienating Saudi?

saudi iran cold war syria & Yemen resolution

SUDAN

Saudi AllianceIran Alliance

Trump presidency could create multi-polar forces

isis & radical groups global populist wave

top geopolitical risks

King Salman's reign has ushered in a paradigm shift in policies, both internationally and domestically. Most recent directives help consolidate power.

Regional Yemen

Syria, Iraq, IS Saudi-Iran cold war

Egypt detente

Domestic Consolidation of Power

Cabinet reshuffles Accountability

International Trump Presidency Saudi-Asia Ties

King Salman's recent appointments: Prince Khalid bin Salman: ambassador to USA Prince Abdulaziz bin Salman: minister of state

for energy affairs

National security council: renders MBS exposure to domestic security

affairs, an area that has historically been dominated by MBN

Source: ECN

saudi

Source:wto.org

global tradeworld trade outlook indicator

Global narrative: global trade is set to witness flat growth with minimal upside potential as most regions struggle to source growth impetus

Commercial and foreign exchange risks, mismanagement of technology disruption have weighed on global trade alongside lower commodity prices

risks to global trade Versatility of shale producers makes quantifying excess capacity opaque, strong US$, & pricing strategies to keep prices range bound- lack of needed investments to bolster prices over medium term

risks to rise in oil prices

global oil demandMn bpd

90

92

94

96

98

1Q 2013 Q3 1Q 2014 Q3 1Q 2015 Q3 1Q 2016 Q3

0

30

60

90

120

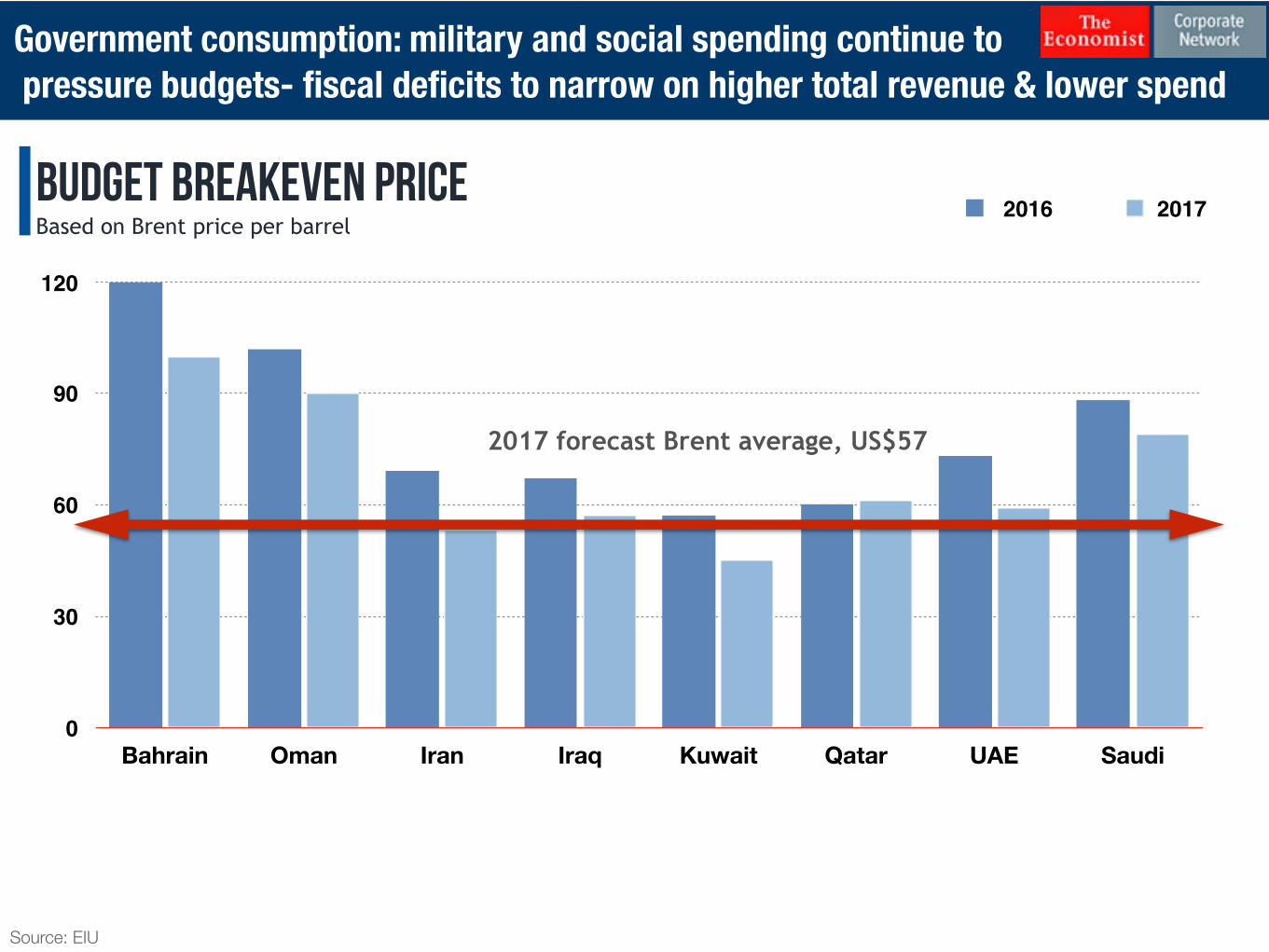

Bahrain Oman Iran Iraq Kuwait Qatar UAE Saudi

2016 2017

2017 forecast Brent average, US$57

Source: EIU

budget breakeven priceBased on Brent price per barrel

Government consumption: military and social spending continue to pressure budgets- fiscal deficits to narrow on higher total revenue & lower spend

EIB

OR

1.5

1.6

1.7

1.8

1.9

2.0

2.1

2.2

2.3

2.4

January 1, 2016- Feb 28, 2017

Source: EmiratesNBD

cost of debt EIBOR, 1 yr

Cost of Capital: EIBOR rises on two interest rate hikes & tight liquidity cost of debt expected to inch higher on additional rate hike(s) in 2017

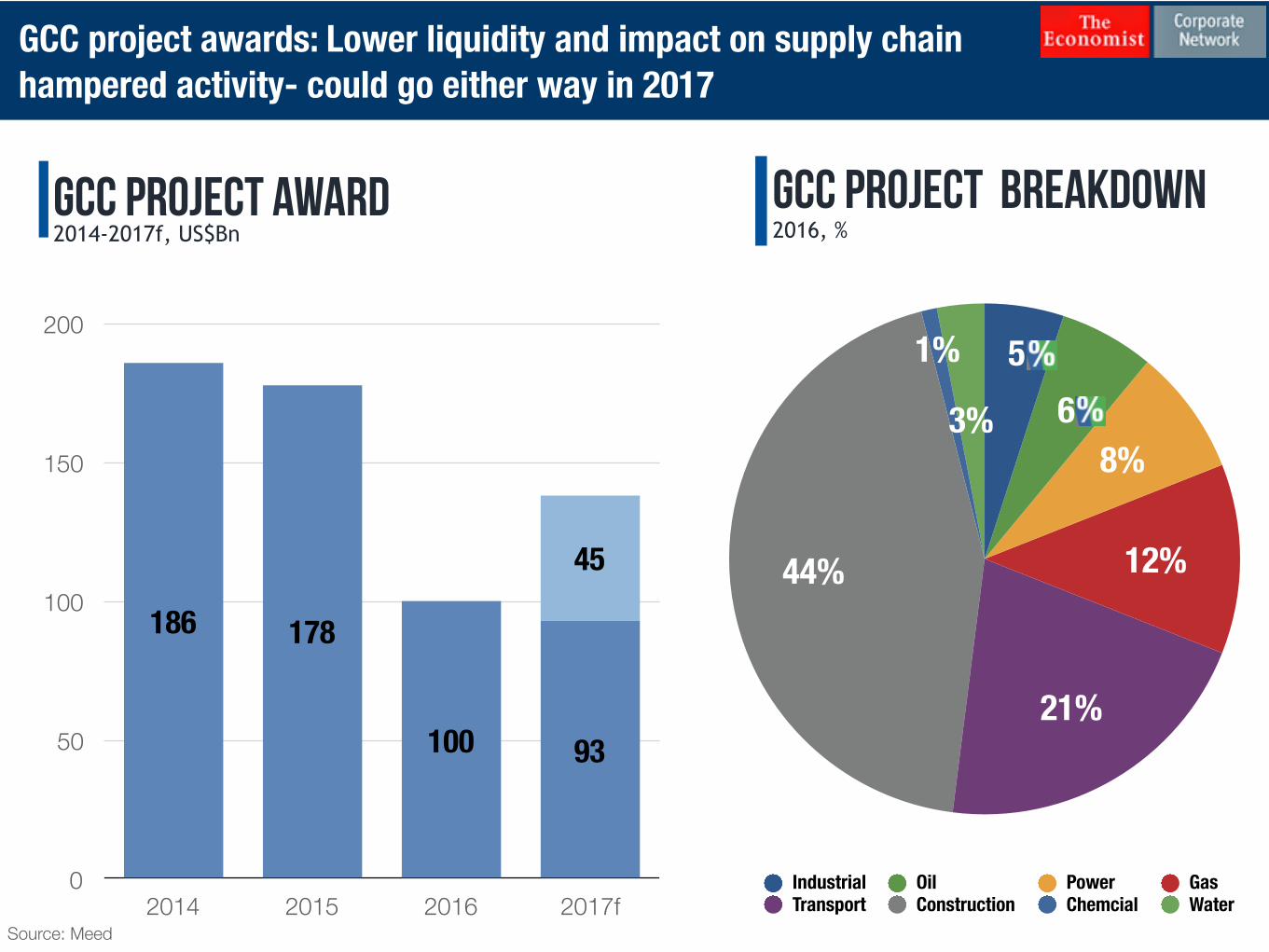

3%

1%

44%

21%

12%

8%6

5

Industrial Oil Power GasTransport Construction Chemcial Water

Source: Meed

0

50

100

150

200

2014 2015 2016 2017f

45

93100

178186

gcc project award2014-2017f, US$Bn

gcc project breakdown2016, %

GCC project awards: Lower liquidity and impact on supply chain hampered activity- could go either way in 2017

1

2

3

Bahrain Kuwait Oman Qatar Saudi UAE

2015 20162017 2018

Aggregate private consumption is

estimated to have dropped 5.4%

Source: EIU, ECN

private consumptionConsumer narrative weak in GCC

Lower private consumption: UAE openness renders most vulnerable consumer story, while subsidy cuts affects remainder of GCC

GCC operational environment UAE business cycle & outlook Saudi NTP2020 and outlook

operational riskslower ratings= lower risks

GCC operations face a multitude of challenges with labor market policies, legal frameworks, and government effectiveness the most pressing

Source: ECN, EIU

0

14

28

42

56

70

Overall Security Government Effectiveness Legal Labour Market

Saudi Arabia UAE Kuwait Qatar Oman Bahrain

Liquidity Lower oil prices, capital repatriation, longer payments, higher cost of capital

Growth Investment case over medium term is solid on back of numerous factors

Consolidation As a result of tight liquidity and

expensive assets, consolidation is expected to continue

Impetus Global growth, higher oil prices,

EXPO2020, Saudi Arabia growth cycle

TightOn-going

2018

Medium Term

UAE: Tight liquidity has ushered a dynamic that has seen consolidation across sectors. Impetus to drive growth not expected before 2018

Source: ECN

business cycle

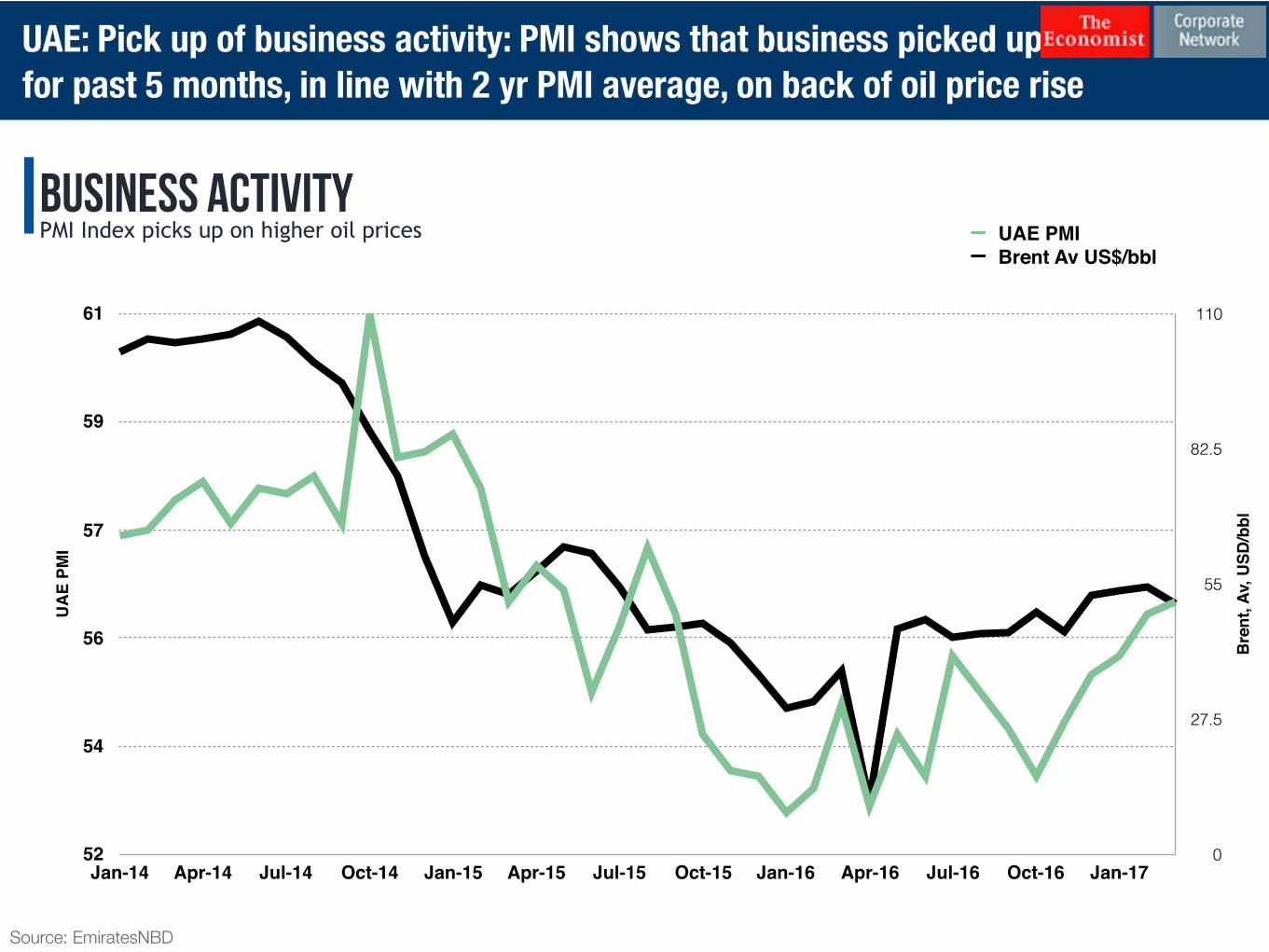

Bre

nt, A

v, U

SD/b

bl

0

27.5

55

82.5

110

UA

E PM

I

52

54

56

57

59

61

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16 Jul-16 Oct-16 Jan-17

UAE PMIBrent Av US$/bbl

Source: EmiratesNBD

business activityPMI Index picks up on higher oil prices

UAE: Pick up of business activity: PMI shows that business picked up for past 5 months, in line with 2 yr PMI average, on back of oil price rise

drivers of growth

Population of 500mn with aggregate GDP of US$4Trhub status for region

National program to encourage diversification, innovation to be supported by SMEs support, genius visa

innovation & diversification

Oil reserves can support global growth needs and production capacity is set to increase, gradually

Reserves

UAE benefits from any economic improvement in the region as it serves as a business and trade hub

regional improvement

UAE: Fundamentals and exogenous factors to support organic and imported-induced growth

Source: ECN

investment case

2017 2018 2019 2020

Tobacco/Drinks

IPO, Sukuks, Bonds

Expat levy

VAT 2Q 2018 (delayed from Jan 1st)

Public Investment Fund Assets USD 2Tr/GCC Common Market In Full Effect

Subsidy cuts

Excise Tax

State Revenue

Taxation

Taxation

Investments

Milestone

Source: ECN

Saudi National Transformation Plan 2020: Program stresses on fiscal sustainability alongside diversification- rendering a new investment proposition

ARAMCO Assets to be IPO’dFDI

State Revenue IPO, Sukuks, Bonds, foreign equity listings

Taxation Capital gains tax, remittance tax

Tadawul upgrade to MSCI emerging index- effective June 2019FDI

Expat dependants & SAR400/month levy on expat labour exceeding quota

CMA working on facilitating listing of foreign companies on Tadawul to add depth and breadth to market

Fiscal Sustainability

Strengthening Private Sector

Diversification of Economy/Localize

Creating non-public jobs

Encouraging FDI

Source: SAMA

POs transactionsValue, SAR 000s

Spending was adversely impacted by salary cuts- PoS transactions continued to climb, however price sensitivity led to lower value transactions

30,000,000

36,250,000

42,500,000

48,750,000

55,000,000

1Q 2013 1Q 2014 1Q 2015 1Q 2016 1Q 2017157,500

170,625

183,750

196,875

210,000

1Q 2013 1Q 2014 1Q 2015 1Q 2016 1Q 2017

atm cash withdrawalValue, SAR Mn

Stabilization

17

Saudi: Consumer confidence expected to improve on the back of rising income, SARc.40bn although that may also be capped as taxes come into play

Source: EIU

consumer behavior

operational risks

Saudi business cycle highly correlated to oil prices, capping growth in short term. Saudization poses the second highest threat to Saudi operations

Source: EIU

0

14

28

42

56

70

Saudi Arabia

Overall Security Political Stability Government Effectiveness Legal MacroeconomicFinancial Labour Market Tax Policy Infrastructure

Scenario Probability Impact Growth slumps owing to low oil prices Very High High

Saudization hinders business growth prospects Very High High Poor payment record to worsen supply chain High High

Shortage of marketable skills increase Moderate High Economic Program Stalls Low High

Source: EmiratesInvestmentBank

asset allocationHNWI

GCC high net worth individuals’ are allocating more of their wealth into cash in 2017 than previous years

Egypt recovery story Iran reintegration narrative

recovery timeline

Egypt’s outlook continues to improve as liquidity gets a boost from FDI and portfolio investments- US$9.2bn in portfolios since free float

Adjustments 2016

Recovery 2018

‣ Subsidy cuts

‣ Devaluation/Free Float

Stabilisation 2017

‣ Inflationary pressure eases

‣ Market equilibrium in foreign exchange markets

‣ Egyptian businesses adjust to new prices

‣ FDI begins to trickle

‣ FDI flows

‣ Jobs & wage growth

‣ Private consumption begins to accelerate

‣ EGP continues to appreciate

‣ Social safety net begins to take shape

Source: ECN

Egypt’s economy depends greatly on consumption, 83% of GDP comes from private sector consumption. 2017 pressured by various factors.

consumption Contraction continues

population

0

1

3

4

5

2011 2012 2013 2014 2015 2016 2017 2018 2019

Private Consumption Growth, y-o-y, %

public & army investments

remittances

undervALUED EGP

inflation

supporting & pressuring factors

Source: EIU, ECN

Iran: Diversified economy with potential to be region’s economic powerhouse

diversified economy Supportive fundamentals

fundamentals

Population of 85 million in middle income backed, of which 50% are below age of 30

demographics

Well educated population human capital

Second largest oil reserves in the world, largest gas reserves of the world, and numerous mineral reserves

Reserves

Whereas food security is an issue in the GCC, Iran boasts an agricultural base that contributes 10% of GDP

agriculture

Source: ECN

Iran: Doing business in Iran: Trump presidency not likely to thwart agreement, however lack of US$ in the system, capped lending to stifle recovery

Strength Weakness Opportunity Threat

‣ Diversified economy; natural resources (energy & agri)

‣ Highly educated labor (engineers, science)

‣ Transport network offers domestic & cross-border connections meeting current supply chain needs

‣ Outlook on lifting of sanctions is positive

‣ Lack of hard currency (US$) availability

‣ Domestic consumption of energy high & aging infrastructure to limit export capacity

‣ Sanctions discourage foreign investors from bringing know-how and equipment

‣ High cost of capital, employment & transport

‣ Regional role in Syria and Yemen resolution

‣ Energy sector investments- gas sector underdeveloped

‣ Shortage of Housing- residential segment

‣ Development of road & rail network - domestic and with neighboring countries

‣ Infrastructure, Airlines, tourism, logistics

‣ Trump foreign policy

‣ Lower oil prices to dampen public spending

‣ Capital flight if agreement fails

‣ High taxes and corruption

‣ Banking sector suffers from high NPLs, shady books, and is need or recapitalization

Source: ECN

Fundamentals & growth outlook

26

MENAT Fundamentals: Aggregate GDP of US$4Tr with a concentration in the middle-income bracket- bracket of inflection point for many industries

0.0

1.3

2.5

3.8

5.0

0 12,500 25,000 37,500 50,000

Turkey

EgyptSaudi Arabia

Kuwait

UAE

Iran

Morocco

Iraq

Algeria

Sudan

Jordan

Lebanon Bahrain

Oman

2015 GDP Gr, %

500 MnPopulation

300 Mnunder 30

147 Mnbtw 15-29

27

Technological advancements

Regional competition for FDI

Megatrends & drivers for growth: Global and regional themes present opportunities for change and business

Saudi female workforce

Digital economy

Privatization/localization

Artificial Intelligence

Infrastructure- connectivity

Entrepreneurship/SMEs

Water, energy, food security

Demographics

Source: ECN

28

Digital technology will drive growth throughout much of the region. Laggard markets to suffer if investments do not match growth needs

Source: EIU

29

Megatrends & drivers for growth: Digital economy contribution to GDP varies across the region and lags behind majority of G-20 countries

infrastructure ` skillslegal framework`

challenges

Source: EIU

30

0

2

3

5

6

Egypt Iran Jordan Kuwait Lebanon Oman Qatar Saudi UAE Morocco Pakistan

2016 2017 2018Real GDP Growth, %

Economic growth outlook: Mixed bag of expectations with strongest growth expected in Iran and slowest growth in Saudi Arabia

Source: EIU

Thank You

Prepared by : Ranya Afifi, Director- MENAT

The Economist Group