Embed Size (px)

Citation preview

25 September 2014

Page | 1 MCI (P) 046/11/2013 Ref. No.: SG2014_0154

Sinarmas Land Limited Rich landbank to underpin earnings growth traction

SINGAPORE | REAL ESTATE | COMPANY NOTE

Rating: BUY

We recently made a 2-day company site visit to two major Sinarmas Land (SML) projects in Jakarta and returned with more confidence on the company’s outlook. The land development sales performance has been optimistic with average selling price improving steadily over the recent years. With greater clarity in the business climate of Indonesia following the denouement of the presidential election, we believe Sinarmas Land will continue to post healthy margins with the positive real estate market outlook as new President Mr Jokowi will likely push for more pro-business policies and infrastructure developments in coming future. In this trip, we visited the 2 major land projects: Kota Deltamas and BSD City. We met up with the General Manager of Sales & Marketing of Kota Deltamas, Mr Stefanus Sehonanda, the Head of Investor Relations of PT Bumi Serpong Damai TbK., Ms Christy Grassela, the Executive Director, Mr Robin Ng, the Executive Director and Chief Financial Officer, Mr Ferdinand Sadeli, and Head of Corporate Investment Department, Mr Aswin A. Gunawan. Budding sales growth from the abundant land bank development Kota Deltamas is a mixed-use industrial development project between SML and Sojitz Corp. The accessibility of Kota Deltamas with neighbouring areas coupled with superb infrastructure for industrial estates has resulted in strong demand for the industrial land, with ASP increasing at a 35% CAGR in the past 2 years. As more companies move into the factory premises, the demand will grow for residential units in the surrounding vicinity. The 2014 target yearly sales is estimated to be USD 170mn. BSD City is the flagship development project for SML and covers an area of 6000 ha. Within this space, BSDE would build residential clusters, office buildings and retail malls. BSD City is developed in 3 phases, with the 1st phase (covering 1500 ha) currently near its completion stage. Development for 2nd phase started in mid-2008. Upcoming residential cluster projects include dePark, Greenwich Park, Eminent and Nava Park. BSD City also launched the Green Office Park (25 ha) and secured anchor tenant Unilever Indonesia with 2 office towers. As Jakarta becomes more densely populated and the residential prices in Jakarta escalating, BSD City will benefit from the rising demand of residential properties outside of Jakarta. Returning to Jakarta City SML has recently acquired 3 lots of lands (over 5 ha) in Epicentrum Kuningan in Jakarta City. See Figure 1. One of the larger lots will be for commercial purposes while the balance 2 lots will be used for residential developments. The launch for the first residential project in lot 16 is expected to be in early 2015. SML will likely form joint ventures for the development of the balance 2 projects. The total GDV for the 3 projects is estimated to be USD 2bn. Investment Action We remain positive on the outlook for SML for (1) the potential bottom-line growth with land sales from the huge land bank, (2) solid balance sheet with a strong cash holding and (3) expansion of international portfolio for recurring income. Our rating is BUY with target price $0.97 by previous analyst. The target price may alter with the change of analyst coverage.

Target Price (SGD) 0.97

Forecast Dividend (SGD-cents) 0.50

Closing Price (SGD) 0.645

Potential Upside 51.2%

Company Description

Company Data

Raw Beta (base on listing period to date) 1.45

Market Cap. (USD mn / SGD mn) 1551 / 1962

3M Average Daily T/O (mn) 2.0

Closing Px in 52 week range 0.45 0.72

Major Shareholders (%)

65.6

0.4

0.1

Valuation Method

SOTP

Analyst

Caroline Tay

+65 6531 1792

Sinarmas Land Ltd. Invests in, develops and

manage rea l estate. The company owns

commercia l bui ldings , hotel and resorts in

Indones ia , Malays ia , Singapore, UK, China.

1. Flambo Internationa l Ltd

2. Dimens ional Fund Advisors LP

3. Vanguard Group Incorporated

0

5

10

15

20

0.00

0.20

0.40

0.60

0.80

1.00

May-1

3

Au

g-13

No

v-13

Feb-1

4

May-1

4

Volume, mn SML SP EQUITY STI rebased

0% 50% 100%

1 October 2014

Page | 2

Key Financial Summary

FYE Dec FY11 FY12 FY13 FY14F FY15F

Revenue (SGD mn) 534 631 985 658 1,046

NPAT, adj. (SGD mn) 89 113 252 105 183

EPS, adj. (SGD) 0.03 0.04 0.08 0.03 0.06

P/E (X),adj. 22.1 17.4 7.8 18.7 10.7

BVPS (SGD) 0.69 0.76 0.76 0.84 0.97

P/B (X) 0.9 0.8 0.8 0.8 0.7

DPS (SGD) 0.29 0.38 0.50 0.50 0.50

Div. Yield (%) 0.4% 0.6% 0.8% 0.8% 0.8%

Source: Company Data, PSR est.

*Forward multiples and yields are based on current price and his torica l

multiples and yields are based on his torica l prices

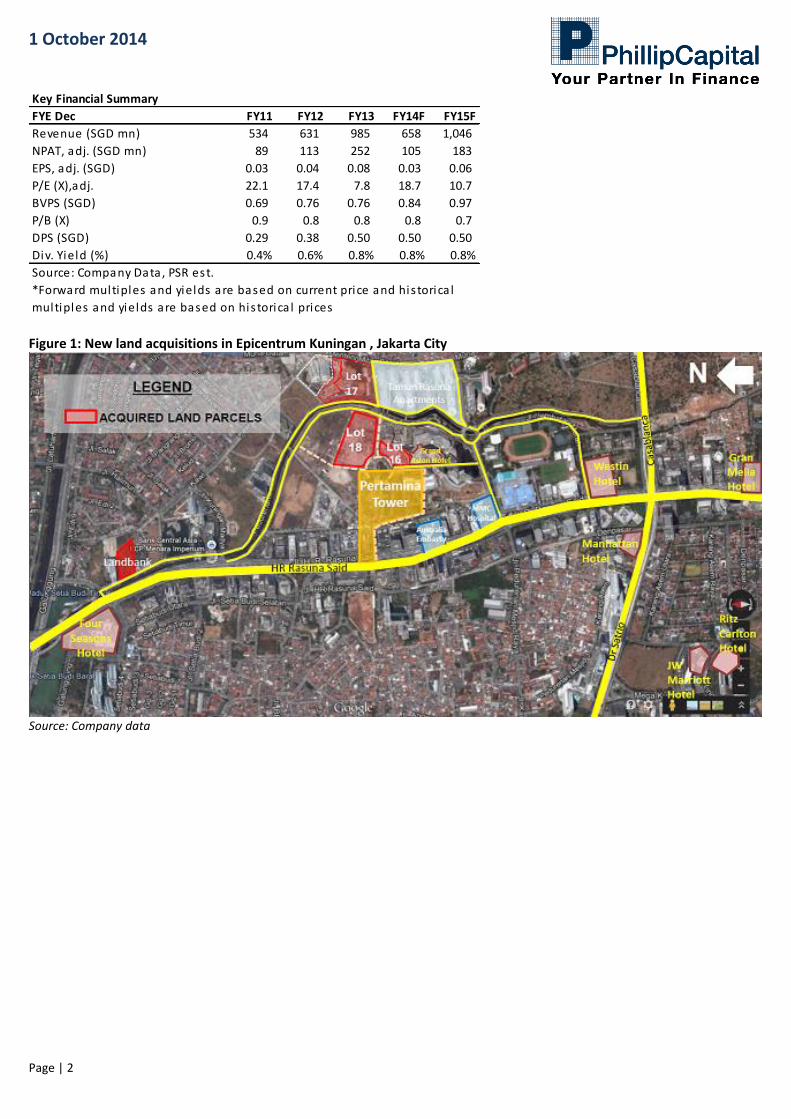

Figure 1: New land acquisitions in Epicentrum Kuningan , Jakarta City

Source: Company data

1 October 2014

Page | 3

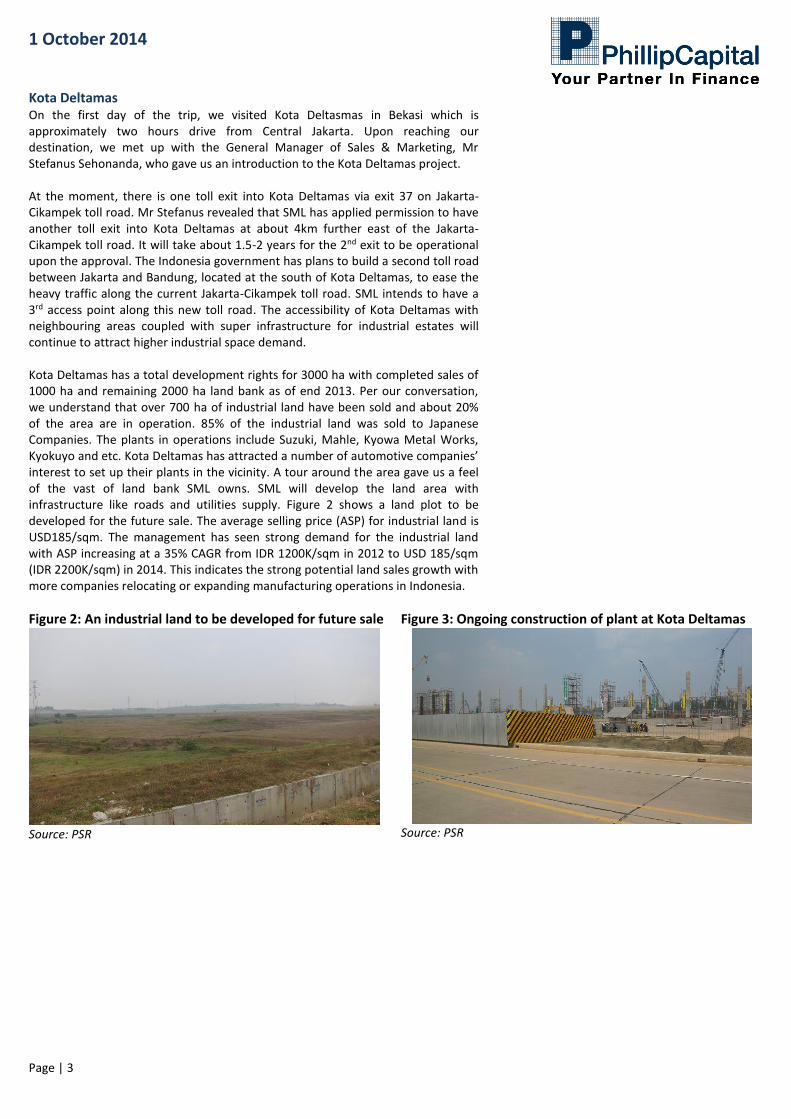

Kota Deltamas On the first day of the trip, we visited Kota Deltasmas in Bekasi which is approximately two hours drive from Central Jakarta. Upon reaching our destination, we met up with the General Manager of Sales & Marketing, Mr Stefanus Sehonanda, who gave us an introduction to the Kota Deltamas project. At the moment, there is one toll exit into Kota Deltamas via exit 37 on Jakarta-Cikampek toll road. Mr Stefanus revealed that SML has applied permission to have another toll exit into Kota Deltamas at about 4km further east of the Jakarta-Cikampek toll road. It will take about 1.5-2 years for the 2nd exit to be operational upon the approval. The Indonesia government has plans to build a second toll road between Jakarta and Bandung, located at the south of Kota Deltamas, to ease the heavy traffic along the current Jakarta-Cikampek toll road. SML intends to have a 3rd access point along this new toll road. The accessibility of Kota Deltamas with neighbouring areas coupled with super infrastructure for industrial estates will continue to attract higher industrial space demand. Kota Deltamas has a total development rights for 3000 ha with completed sales of 1000 ha and remaining 2000 ha land bank as of end 2013. Per our conversation, we understand that over 700 ha of industrial land have been sold and about 20% of the area are in operation. 85% of the industrial land was sold to Japanese Companies. The plants in operations include Suzuki, Mahle, Kyowa Metal Works, Kyokuyo and etc. Kota Deltamas has attracted a number of automotive companies’ interest to set up their plants in the vicinity. A tour around the area gave us a feel of the vast of land bank SML owns. SML will develop the land area with infrastructure like roads and utilities supply. Figure 2 shows a land plot to be developed for the future sale. The average selling price (ASP) for industrial land is USD185/sqm. The management has seen strong demand for the industrial land with ASP increasing at a 35% CAGR from IDR 1200K/sqm in 2012 to USD 185/sqm (IDR 2200K/sqm) in 2014. This indicates the strong potential land sales growth with more companies relocating or expanding manufacturing operations in Indonesia.

Figure 2: An industrial land to be developed for future sale

Source: PSR

Figure 3: Ongoing construction of plant at Kota Deltamas

Source: PSR

1 October 2014

Page | 4

Figure 4: Some companies that are in operations in Kota Deltamas

Source: PSR Though at the moment, there are only 16 residential clusters housing 1800 families in Kota Deltamas, we believe as more companies’ plants and commercial activities commerce operations, the population will increase accordingly, thus driving demand for the residential housing. Mr Stefanus divulged that the residential prices in Kota Deltamas has tripled over the past 3 years and the growth momentum remains strong. The management also aims to launch more commercial land plots in the government center region this year. The 2014 target yearly sales is estimated to be USD 170mn. In additional to land sales, Kota Deltamas will generate recurring income via rental of service apartments, water treatment plant for provision of clean water and management fees. It is estimated to take at least another 8-10 years for the full completion of this mixed-use industrial township.

1 October 2014

Page | 5

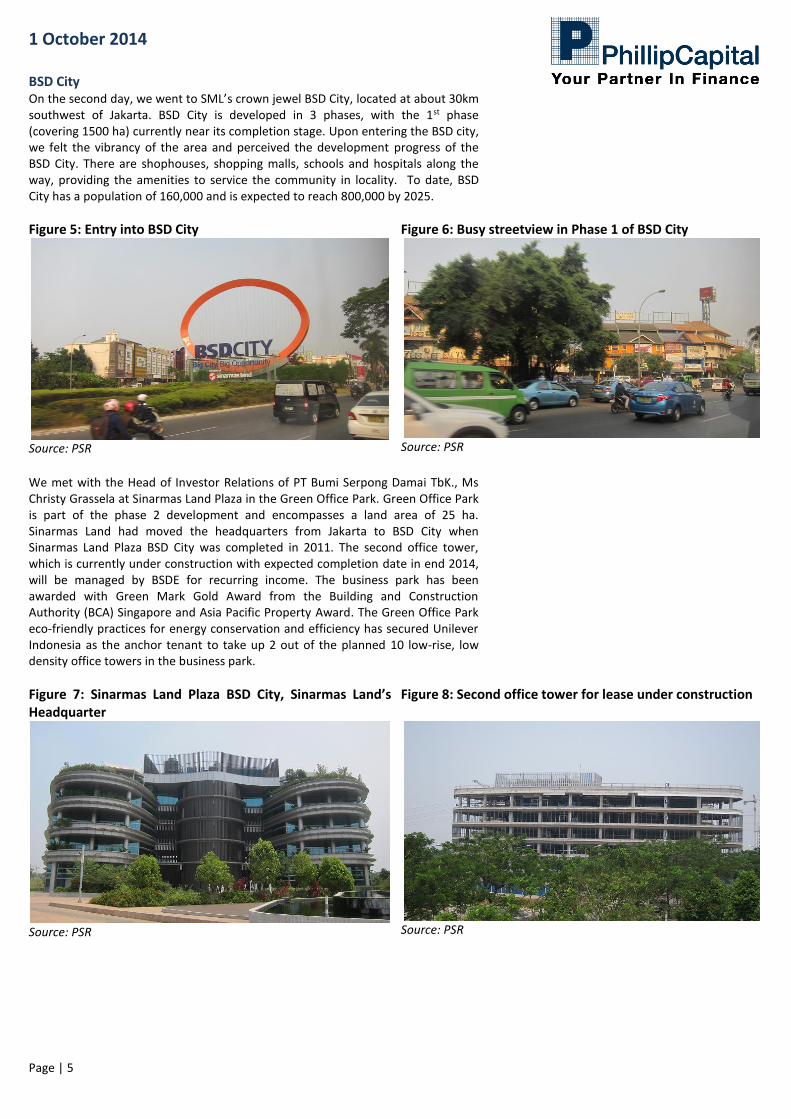

BSD City On the second day, we went to SML’s crown jewel BSD City, located at about 30km southwest of Jakarta. BSD City is developed in 3 phases, with the 1st phase (covering 1500 ha) currently near its completion stage. Upon entering the BSD city, we felt the vibrancy of the area and perceived the development progress of the BSD City. There are shophouses, shopping malls, schools and hospitals along the way, providing the amenities to service the community in locality. To date, BSD City has a population of 160,000 and is expected to reach 800,000 by 2025.

Figure 5: Entry into BSD City

Source: PSR

Figure 6: Busy streetview in Phase 1 of BSD City

Source: PSR

We met with the Head of Investor Relations of PT Bumi Serpong Damai TbK., Ms Christy Grassela at Sinarmas Land Plaza in the Green Office Park. Green Office Park is part of the phase 2 development and encompasses a land area of 25 ha. Sinarmas Land had moved the headquarters from Jakarta to BSD City when Sinarmas Land Plaza BSD City was completed in 2011. The second office tower, which is currently under construction with expected completion date in end 2014, will be managed by BSDE for recurring income. The business park has been awarded with Green Mark Gold Award from the Building and Construction Authority (BCA) Singapore and Asia Pacific Property Award. The Green Office Park eco-friendly practices for energy conservation and efficiency has secured Unilever Indonesia as the anchor tenant to take up 2 out of the planned 10 low-rise, low density office towers in the business park.

Figure 7: Sinarmas Land Plaza BSD City, Sinarmas Land’s Headquarter

Source: PSR

Figure 8: Second office tower for lease under construction

Source: PSR

1 October 2014

Page | 6

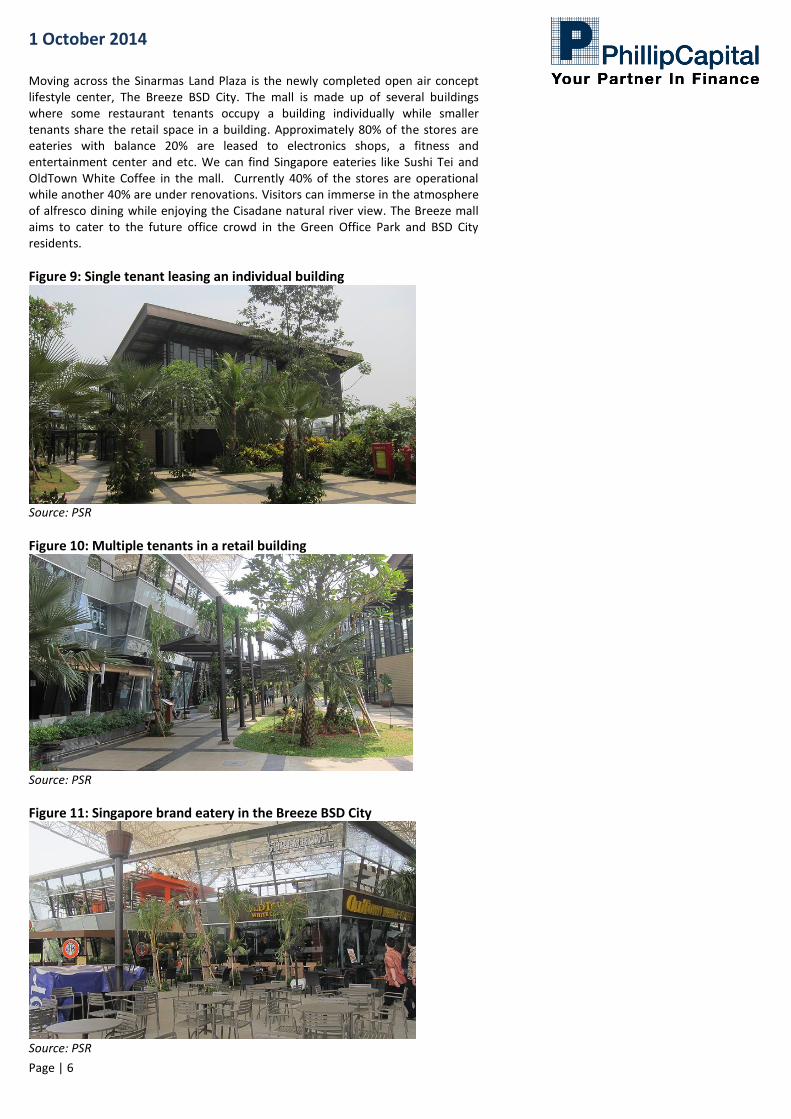

Moving across the Sinarmas Land Plaza is the newly completed open air concept lifestyle center, The Breeze BSD City. The mall is made up of several buildings where some restaurant tenants occupy a building individually while smaller tenants share the retail space in a building. Approximately 80% of the stores are eateries with balance 20% are leased to electronics shops, a fitness and entertainment center and etc. We can find Singapore eateries like Sushi Tei and OldTown White Coffee in the mall. Currently 40% of the stores are operational while another 40% are under renovations. Visitors can immerse in the atmosphere of alfresco dining while enjoying the Cisadane natural river view. The Breeze mall aims to cater to the future office crowd in the Green Office Park and BSD City residents.

Figure 9: Single tenant leasing an individual building

Source: PSR

Figure 10: Multiple tenants in a retail building

Source: PSR

Figure 11: Singapore brand eatery in the Breeze BSD City

Source: PSR

1 October 2014

Page | 7

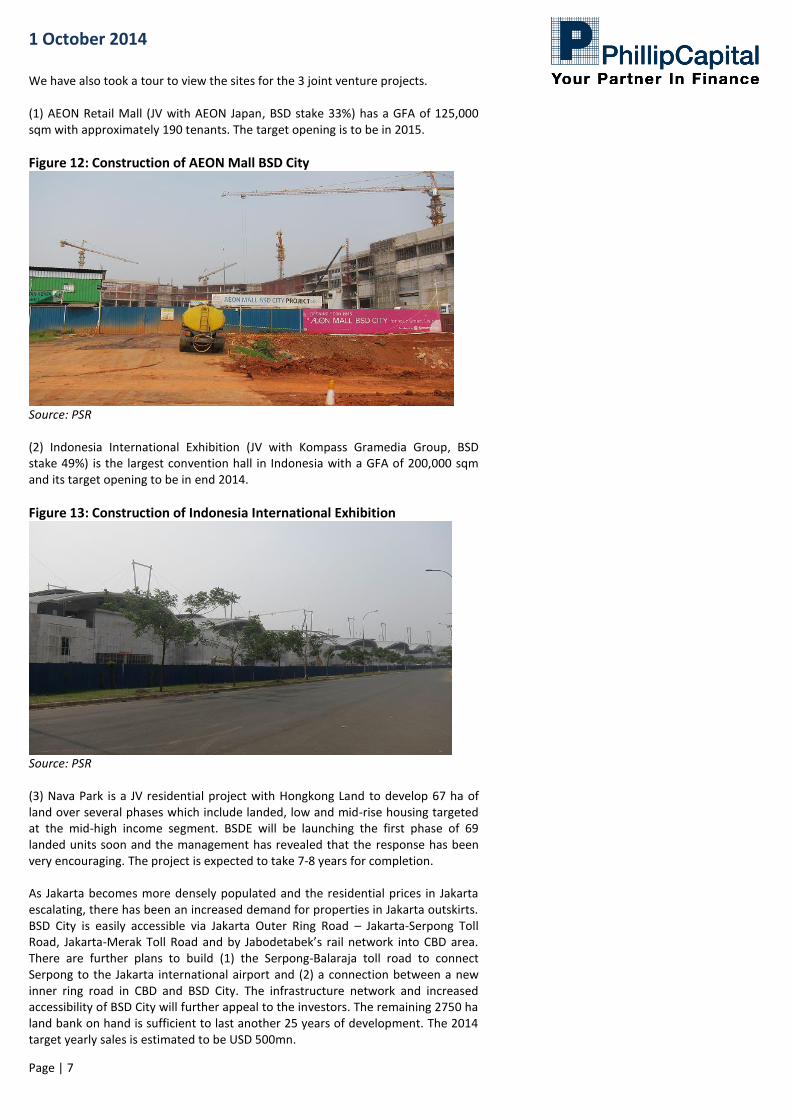

We have also took a tour to view the sites for the 3 joint venture projects. (1) AEON Retail Mall (JV with AEON Japan, BSD stake 33%) has a GFA of 125,000 sqm with approximately 190 tenants. The target opening is to be in 2015.

Figure 12: Construction of AEON Mall BSD City

Source: PSR (2) Indonesia International Exhibition (JV with Kompass Gramedia Group, BSD stake 49%) is the largest convention hall in Indonesia with a GFA of 200,000 sqm and its target opening to be in end 2014.

Figure 13: Construction of Indonesia International Exhibition

Source: PSR (3) Nava Park is a JV residential project with Hongkong Land to develop 67 ha of land over several phases which include landed, low and mid-rise housing targeted at the mid-high income segment. BSDE will be launching the first phase of 69 landed units soon and the management has revealed that the response has been very encouraging. The project is expected to take 7-8 years for completion. As Jakarta becomes more densely populated and the residential prices in Jakarta escalating, there has been an increased demand for properties in Jakarta outskirts. BSD City is easily accessible via Jakarta Outer Ring Road – Jakarta-Serpong Toll Road, Jakarta-Merak Toll Road and by Jabodetabek’s rail network into CBD area. There are further plans to build (1) the Serpong-Balaraja toll road to connect Serpong to the Jakarta international airport and (2) a connection between a new inner ring road in CBD and BSD City. The infrastructure network and increased accessibility of BSD City will further appeal to the investors. The remaining 2750 ha land bank on hand is sufficient to last another 25 years of development. The 2014 target yearly sales is estimated to be USD 500mn.

1 October 2014

Page | 8

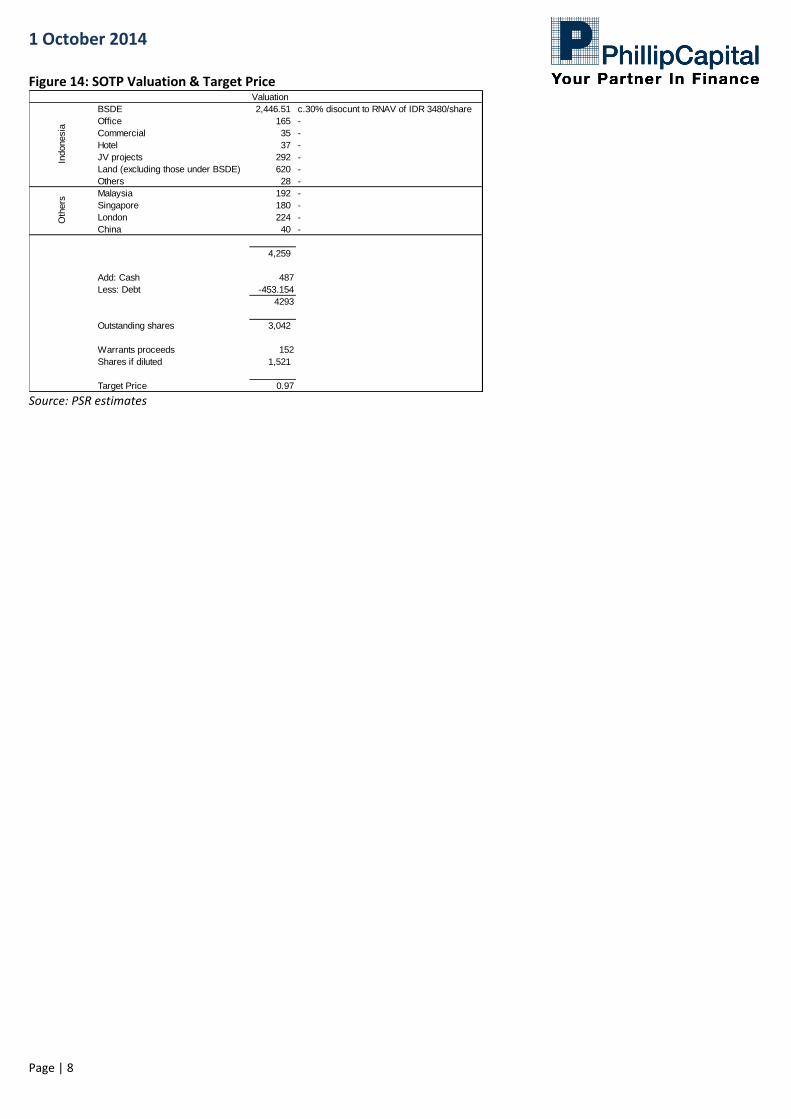

Figure 14: SOTP Valuation & Target Price Valuation

BSDE 2,446.51 c.30% disocunt to RNAV of IDR 3480/share

Office 165 -

Commercial 35 -

Hotel 37 -

JV projects 292 -

Land (excluding those under BSDE) 620 -

Others 28 -

Malaysia 192 -

Singapore 180 -

London 224 -

China 40 -

4,259

Add: Cash 487

Less: Debt -453.154

4293

Outstanding shares 3,042

Warrants proceeds 152

Shares if diluted 1,521

Target Price 0.97

Indonesia

Oth

ers

Source: PSR estimates

1 October 2014

Page | 9

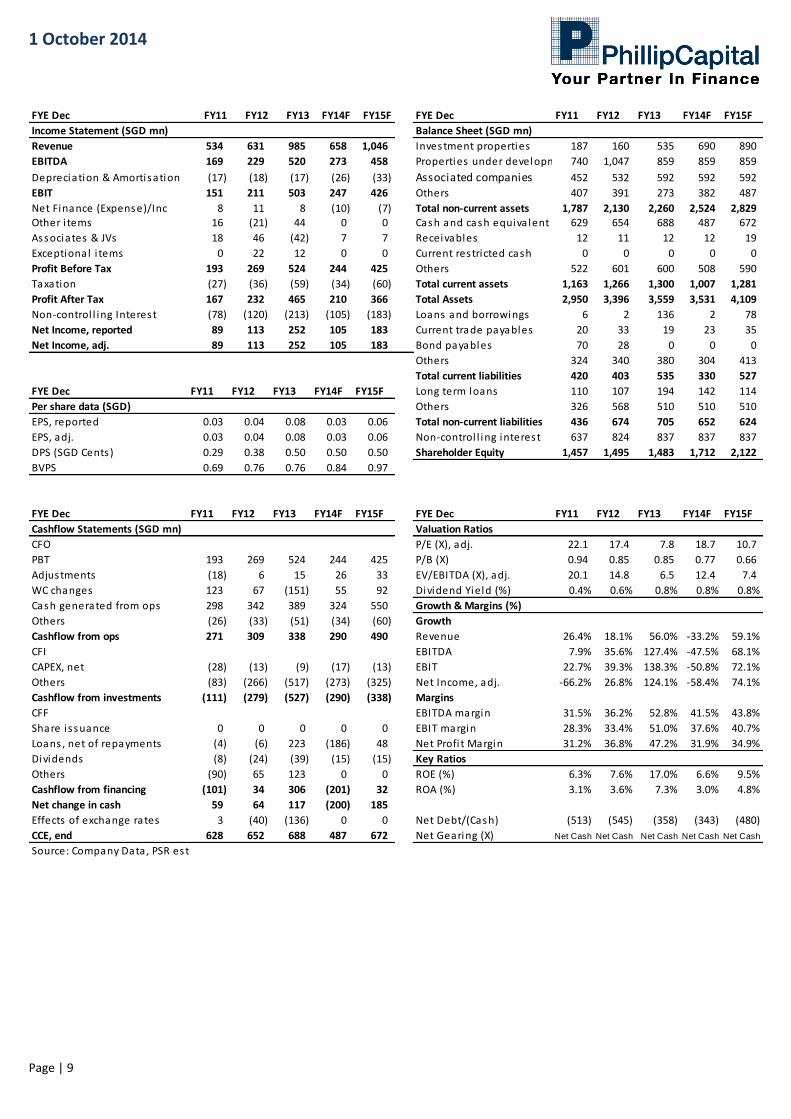

FYE Dec FY11 FY12 FY13 FY14F FY15F FYE Dec FY11 FY12 FY13 FY14F FY15F

Revenue 534 631 985 658 1,046 Investment properties 187 160 535 690 890

EBITDA 169 229 520 273 458 Properties under development for sa le740 1,047 859 859 859

Depreciation & Amortisation (17) (18) (17) (26) (33) Associated companies 452 532 592 592 592

EBIT 151 211 503 247 426 Others 407 391 273 382 487

Net Finance (Expense)/Inc 8 11 8 (10) (7) Total non-current assets 1,787 2,130 2,260 2,524 2,829

Other i tems 16 (21) 44 0 0 Cash and cash equiva lent 629 654 688 487 672

Associates & JVs 18 46 (42) 7 7 Receivables 12 11 12 12 19

Exceptional i tems 0 22 12 0 0 Current restricted cash 0 0 0 0 0

Profit Before Tax 193 269 524 244 425 Others 522 601 600 508 590

Taxation (27) (36) (59) (34) (60) Total current assets 1,163 1,266 1,300 1,007 1,281

Profit After Tax 167 232 465 210 366 Total Assets 2,950 3,396 3,559 3,531 4,109

Non-control l ing Interest (78) (120) (213) (105) (183) Loans and borrowings 6 2 136 2 78

Net Income, reported 89 113 252 105 183 Current trade payables 20 33 19 23 35

Net Income, adj. 89 113 252 105 183 Bond payables 70 28 0 0 0

Others 324 340 380 304 413

Total current liabilities 420 403 535 330 527

FYE Dec FY11 FY12 FY13 FY14F FY15F Long term loans 110 107 194 142 114

Others 326 568 510 510 510

EPS, reported 0.03 0.04 0.08 0.03 0.06 Total non-current liabilities 436 674 705 652 624

EPS, adj. 0.03 0.04 0.08 0.03 0.06 Non-control l ing interest 637 824 837 837 837

DPS (SGD Cents) 0.29 0.38 0.50 0.50 0.50 Shareholder Equity 1,457 1,495 1,483 1,712 2,122

BVPS 0.69 0.76 0.76 0.84 0.97

FYE Dec FY11 FY12 FY13 FY14F FY15F FYE Dec FY11 FY12 FY13 FY14F FY15F

CFO P/E (X), adj. 22.1 17.4 7.8 18.7 10.7

PBT 193 269 524 244 425 P/B (X) 0.94 0.85 0.85 0.77 0.66

Adjustments (18) 6 15 26 33 EV/EBITDA (X), adj. 20.1 14.8 6.5 12.4 7.4

WC changes 123 67 (151) 55 92 Dividend Yield (%) 0.4% 0.6% 0.8% 0.8% 0.8%

Cash generated from ops 298 342 389 324 550 Growth & Margins (%)

Others (26) (33) (51) (34) (60) Growth

Cashflow from ops 271 309 338 290 490 Revenue 26.4% 18.1% 56.0% -33.2% 59.1%

CFI EBITDA 7.9% 35.6% 127.4% -47.5% 68.1%

CAPEX, net (28) (13) (9) (17) (13) EBIT 22.7% 39.3% 138.3% -50.8% 72.1%

Others (83) (266) (517) (273) (325) Net Income, adj. -66.2% 26.8% 124.1% -58.4% 74.1%

Cashflow from investments (111) (279) (527) (290) (338) Margins

CFF EBITDA margin 31.5% 36.2% 52.8% 41.5% 43.8%

Share i ssuance 0 0 0 0 0 EBIT margin 28.3% 33.4% 51.0% 37.6% 40.7%

Loans , net of repayments (4) (6) 223 (186) 48 Net Profi t Margin 31.2% 36.8% 47.2% 31.9% 34.9%

Dividends (8) (24) (39) (15) (15) Key Ratios

Others (90) 65 123 0 0 ROE (%) 6.3% 7.6% 17.0% 6.6% 9.5%

Cashflow from financing (101) 34 306 (201) 32 ROA (%) 3.1% 3.6% 7.3% 3.0% 4.8%

Net change in cash 59 64 117 (200) 185

Effects of exchange rates 3 (40) (136) 0 0 Net Debt/(Cash) (513) (545) (358) (343) (480)

CCE, end 628 652 688 487 672 Net Gearing (X) Net Cash Net Cash Net Cash Net Cash Net Cash

Source: Company Data, PSR est

Income Statement (SGD mn)

Per share data (SGD)

Cashflow Statements (SGD mn)

Balance Sheet (SGD mn)

Valuation Ratios

1 October 2014

Page | 10

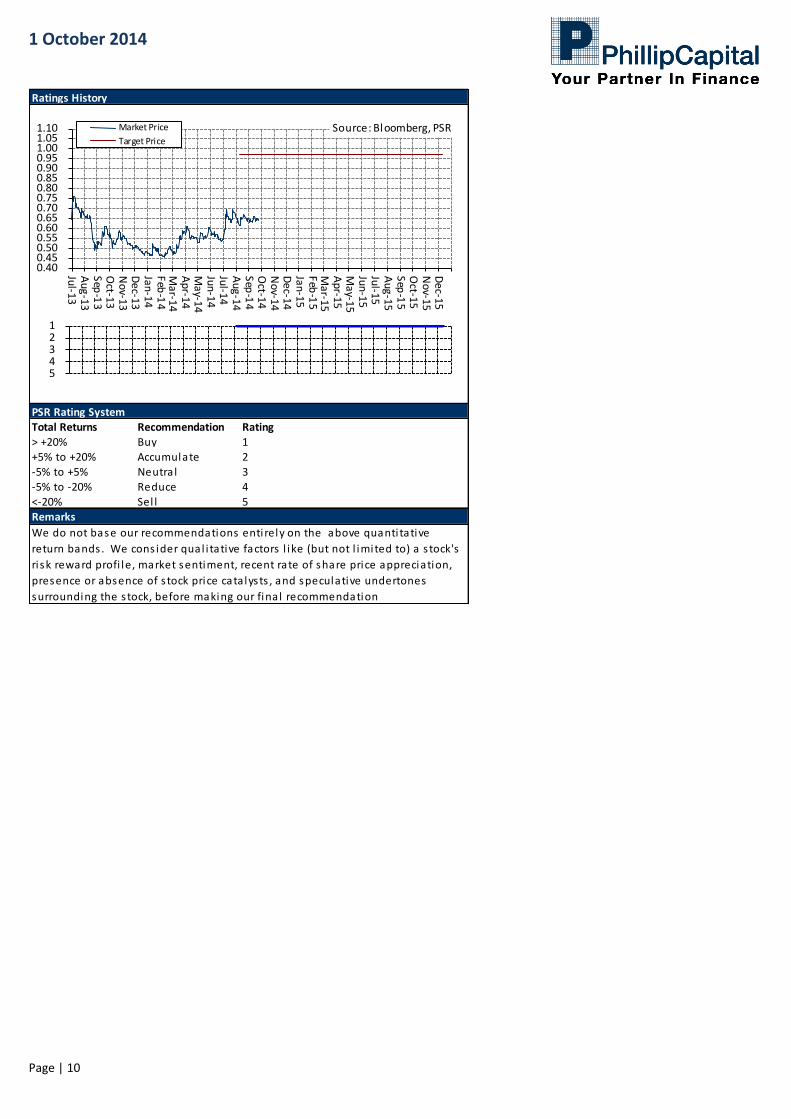

Total Returns Recommendation Rating> +20% Buy 1+5% to +20% Accumulate 2-5% to +5% Neutra l 3-5% to -20% Reduce 4<-20% Sel l 5

Ratings History

PSR Rating System

Remarks

We do not base our recommendations entirely on the above quanti tative

return bands . We cons ider qual i tative factors l ike (but not l imited to) a s tock's

ri sk reward profi le, market sentiment, recent rate of share price appreciation,

presence or absence of s tock price catalysts , and speculative undertones

surrounding the s tock, before making our fina l recommendation

1 2 3 4 5

0.400.450.500.550.600.650.700.750.800.850.900.951.001.051.10

Jul-1

3A

ug

-13

Sep

-13

Oct-1

3N

ov-1

3D

ec-1

3Ja

n-1

4F

eb-1

4M

ar-1

4A

pr-1

4M

ay-1

4Ju

n-1

4Ju

l-14

Au

g-1

4S

ep-1

4O

ct-14

No

v-14

De

c-14

Jan

-15

Feb

-15

Ma

r-15

Ap

r-15

Ma

y-15

Jun

-15

Jul-1

5A

ug

-15

Sep

-15

Oct-1

5N

ov-1

5D

ec-1

5

Source: Bloomberg, PSRMarket Price

Target Price

1 October 2014

Page | 11

Important Information

This publication is prepared by Phillip Securities Research Pte Ltd., 250 North Bridge Road, #06-00, Raffles City Tower, Singapore 179101 (Registration Number: 198803136N), which is regulated by the Monetary Authority of Singapore (“Phillip Securities Research”). By receiving or reading this publication, you agree to be bound by the terms and limitations set out below. This publication has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this document by mistake, please delete or destroy it, and notify the sender immediately. Phillip Securities Research shall not be liable for any direct or consequential loss arising from any use of material contained in this publication. The information contained in this publication has been obtained from public sources, which Phillip Securities Research has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this publication are based on such information and are expressions of belief of the individual author or the indicated source (as applicable) only. Phillip Securities Research has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete, appropriate or verified or should be relied upon as such. Any such information or Research contained in this publication is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the preparation or issuance of this report, (i) be liable in any manner whatsoever for any consequences (including but not limited to any special, direct, indirect, incidental or consequential losses, loss of profits and damages) of any reliance or usage of this publication or (ii) accept any legal responsibility from any person who receives this publication, even if it has been advised of the possibility of such damages. You must make the final investment decision and accept all responsibility for your investment decision, including, but not limited to your reliance on the information, data and/or other materials presented in this publication. Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this material are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this publication is not indicative of future results. This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This publication should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this publication has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this material is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this publication involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks. Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this research should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this publication, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this publication.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment. To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold a interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this publication. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, which is not reflected in this material, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the preparation or issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this material. The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

Section 27 of the Financial Advisers Act (Cap. 110) of Singapore and the MAS Notice on Recommendations on Investment Products (FAA-N01) do not apply in respect of this publication.

1 October 2014

Page | 12

This material is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this material may not be suitable for all investors and a person receiving or reading this material should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

Please contact Phillip Securities Research at [65 65311240] in respect of any matters arising from, or in connection with, this document.

This report is only for the purpose of distribution in Singapore.

Contact Information (Singapore Research Team) Management Chan Wai Chee (CEO, Research - Special Opportunities)

+65 6531 1231 Research Operations Officer Jaelyn Chin +65 6531 1240

Joshua Tan (Head, Research - Equities & Macro)

+65 6531 1249

Equities | Macro Market Analyst | Equities US Equities Joshua Tan +65 6531 1249 Kenneth Koh +65 6531 1791 Wong Yong Kai +65 6531 1685 Soh Lin Sin +65 6531 1516 Bakhteyar Osama +65 6531 1793 Finance Real Estate Benjamin Ong +65 6531 1535 Caroline Tay +65 6531 1792 Telecoms Transport Colin Tan +65 6531 1221 Richard Leow, CFTe +65 6531 1735

Contact Information (Regional Member Companies) SINGAPORE

Phillip Securities Pte Ltd Raffles City Tower

250, North Bridge Road #06-00 Singapore 179101 Tel +65 6533 6001 Fax +65 6535 6631

Website: www.poems.com.sg

MALAYSIA Phillip Capital Management Sdn Bhd

B-3-6 Block B Level 3 Megan Avenue II, No. 12, Jalan Yap Kwan Seng, 50450

Kuala Lumpur Tel +603 2162 8841 Fax +603 2166 5099

Website: www.poems.com.my

HONG KONG Phillip Securities (HK) Ltd

11/F United Centre 95 Queensway Hong Kong

Tel +852 2277 6600 Fax +852 2868 5307

Websites: www.phillip.com.hk

JAPAN

Phillip Securities Japan, Ltd. 4-2 Nihonbashi Kabuto-cho Chuo-ku,

Tokyo 103-0026 Tel +81-3 3666 2101 Fax +81-3 3666 6090

Website: www.phillip.co.jp

INDONESIA PT Phillip Securities Indonesia

ANZ Tower Level 23B, Jl Jend Sudirman Kav 33A Jakarta 10220 – Indonesia

Tel +62-21 5790 0800 Fax +62-21 5790 0809

Website: www.phillip.co.id

CHINA Phillip Financial Advisory (Shanghai) Co Ltd

No 550 Yan An East Road, Ocean Tower Unit 2318,

Postal code 200001 Tel +86-21 5169 9200 Fax +86-21 6351 2940

Website: www.phillip.com.cn

THAILAND Phillip Securities (Thailand) Public Co. Ltd

15th Floor, Vorawat Building, 849 Silom Road, Silom, Bangrak,

Bangkok 10500 Thailand Tel +66-2 6351700 / 22680999

Fax +66-2 22680921 Website www.phillip.co.th

FRANCE King & Shaxson Capital Limited

3rd Floor, 35 Rue de la Bienfaisance 75008 Paris France

Tel +33-1 45633100 Fax +33-1 45636017

Website: www.kingandshaxson.com

UNITED KINGDOM King & Shaxson Capital Limited

6th Floor, Candlewick House, 120 Cannon Street, London, EC4N 6AS

Tel +44-20 7426 5950 Fax +44-20 7626 1757

Website: www.kingandshaxson.com

UNITED STATES Phillip Futures Inc

141 W Jackson Blvd Ste 3050 The Chicago Board of Trade Building

Chicago, IL 60604 USA Tel +1-312 356 9000 Fax +1-312 356 9005

Website: www.phillipusa.com

AUSTRALIA Phillip Capital Limited

Level 12, 15 William Street, Melbourne, Victoria 3000, Australia

Tel +61-03 9629 8288 Fax +61-03 9629 8882

Website: www.phillipcapital.com.au

SRI LANKA Asha Phillip Securities Limited

2nd Floor,Lakshmans Building, No.321, Galle Road, Colombo 03, Sri Lanka

Tel: (94) 11 2429 100 Fax: (94) 2429 199

Website: www.ashaphillip.net

INDIA

PhillipCapital (India) Private Limited No.1, 18th Floor

Urmi Estate 95, Ganpatrao Kadam Marg

Lower Parel West, Mumbai 400-013 Maharashtra, India

Tel: +91-22-2300 2999 / Fax: +91-22-2300 2969 Website: www.phillipcapital.in

TURKEY PhillipCapital Menkul Degerler

Dr. Cemil Bengü Cad. Hak Is Merkezi No. 2 Kat. 6A Caglayan 34403 Istanbul, Turkey

Tel: 0212 296 84 84 Fax: 0212 233 69 29

Website: www.phillipcapital.com.tr

DUBAI Phillip Futures DMCC

Member of the Dubai Gold and Commodities Exchange (DGCX)

Unit No 601, Plot No 58, White Crown Bldg, Sheikh Zayed Road, P.O.Box 212291

Dubai-UAE Tel: +971-4-3325052 / Fax: + 971-4-3328895

Website: www.phillipcapital.in