Embed Size (px)

Citation preview

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 1/39

EXECUTIVE SUMMARYInsurance is defined as the contract between Insurance co. (Insurer)and the customer (Insured). In this legal contract, the insurer agrees toindemnify (compensate) the insured in lieu of payment of premium, for anyfinancial loss due to risks covered in the Policy.

Since 1956, with the nationalization of insurance industry, the state-run Life Insurance Corporation of India (LIC) has held the monopoly in

that country's life insurance sector. General Insurance Corporation of India (GIC), with its four subsidiaries, was its counterpart in the generalinsurance sector. In 1999, the government passed the IRDA Bill toopen up the insurance sector in India.

In the last year, the country saw a large number of Indian and foreign players rushing to enter this lucrative and untapped insurance marketof India. The Indian Insurance sector is thus at the beginning of a newera. It has been only a year since the new players became active and itis difficult to say whether the reforms were successful. But it is

believed that the country has a vast untapped potential and the new players will surely use this to their best advantage.

This project aims to study the topic of Insurance and the IndianInsurance Sector in particular. The first part of the project covers theconcept of insurance, the need for insurance, the types of insurance. Inthe second part, we study the Indian insurance sector. Under the studyof the insurance sector, we will look at why the government decided toopen up the sector, a brief overview of the reforms, the potential of thesector, the requirement for entry into the market and the new playersin the market. We will also give a brief insight into the investment

1

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 2/39

regulations, the new regulatory authority, the distribution channels anda look at the times to come.

2

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 3/39

TABLE OF CONTENT

SR. NO TOPIC PG.NO

1 Introduction 32 Concept of insurance 43 Types of Insurance 10

4 Brief History of Insurance Sector in India 125 Reasons for Opening of Insurance Sector 156 Potential For Insurance Sector in India 177 Reforms in the Sector 198 Regulatory Authority 219 Investment Regulations 24

10 Current Players 2611 Distribution Channels 2812 Challenges Faced by the Insurance 31

Companies13 Future Scenario of Insurance Industry 34

14 Cases 35

3

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 4/39

INTRODUCTION

The Government of India ( GoI ) opened the insurance sector to private players on October 24. 2000, thus unraveling a new chapter in thisfield. This new policy of GOI is an outcome of India’s policy of liberlisation and also the result of its obligation as a signatory to theWTO to conform to its principles and guidelines relating to thereduction of barriers to trade in services. This epoch-making decision

has ushered in a new era that has transgressed four decades of complete control by the public sector over the insurance sector (lifeinsurance was nationalized in 1956 by merging 245 private insurancecompanies to form the life Insurance Corporation Of India (LIC), whilegeneral insurance was nationalized with the formation of generalInsurance Corporation (GIC) in 1972).

This decision of the GOI has been accompanied by a set of laws andregulations governing this domain. Accordingly the InsuranceRegulatory and Development Authority Act 1999 (The IRDA Act) wasenacted with the predominant aim of setting up an autonomous bodyknown as the Insurance Regulatory and Development Authority (theIRDA) to regulate, promote and ensure orderly growth of the insuranceindustry.

The influx of new players in both life and non-life sectors has made theinsurance market a consumers paradise. All new players are striving tointroduce innovative products. Where the old players (LIC and GIC)have a first mover advantage and have a wide spread network, thenew players are banking on their innovative products and superior services to surge them ahead.

4

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 5/39

It is too soon to say which of the new players will succeed and which of them will perish. But the opening up of the sector is a step that will be

beneficial both to the insured as well as the insurer.

THE CONCEPT OF INSURANCE

"Insurance is a contract between two parties whereby one party called insurer undertakes in exchange for a fixed sum called premiums, to pay the other party called

insured a fixed amount of money on the happening of a certain event."

Insurance is a protection against financial loss arising on thehappening of an unexpected event. Insurance companies collect

premiums to provide for this protection. A loss is paid out of the premiums collected from the insuring public and the InsuranceCompanies act as trustees to the amount collected.

For Example, in a Life Policy, by paying a premium to the Insurer, thefamily of the insured person receives a fixed compensation on thedeath of the insured. Similarly, in a car insurance, in the event of thecar meeting with an accident, the insured receives the compensationto the extent of damage.

It is a system by which the losses suffered by a few are spread over many, exposed to similar risks. Insurance is a mechanism for transferring risk and reducing risk by having a large number of individuals who share in the financial losses of the group. Risk inhibitsaction and is highly subjective on an individual basis. Insuranceobjectifies risk. People trade the possibility of financial loss for therelative certainty of the premium paid and reimbursement for loss.Insurance frees people to take action even in the face of possiblefinancial loss. Thus, insurance provides utility even if no loss ever occurs.

5

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 6/39

Some people believe insurance is similar to gambling or opening asavings account. Neither is true. When you place a bet, you create arisk and you have the chance of losing all or making more than your wager. Insurance companies write policies for pure not speculativerisks and indemnify you when you have a covered loss. In theinsurance industry, the word "indemnify" means you cannot be put in a

better position than you were before the loss.

BASIC INSURANCE TERMINOLOGIES

• Insured

The person known as the policyholder, a person with insurancecoverage.

• Insurer

A company licensed to transact the business of insurance andissue insurance policies.

• Policy

It's the written contract between an insurance company and itsinsured. It defines what the company agrees to cover for what

period of time and describes the obligations and responsibilitiesof the insured.

• Premium

It's the amount of money a policyholder pays for insurance protection.

6

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 7/39

• Claim

It's the notice to the insurance company that under the terms of a policy, a loss maybe covered.

• Indemnity

Legal principle that specifies an insured should not collect morethan the actual cash value of a loss but should be restored toapproximately the same financial position as existed before theloss.

• Agent

A licensed person or organization who sells insurance andrepresents the insurance company to the policyholder.

• Broker

An organization or person paid by the policy holder to look for insurance on their behalf.

• Deductible

It's the amount of the loss which the insured is responsible to

pay before the insurance company pays the benefits.

• Expiration Date

This is the date on which the policy ends.

• Grace Period

A period (usually 30 or 31 days) following each insurance premium due date, other than the first due date, during which anoverdue premium may be paid. All provisions of the policyremain in force throughout this period.

7

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 8/39

• Limit

It's the maximum amount paid by the insurance company under the terms of a policy.

• Underwriting

The process of classifying applicants for insurance by identifyingcharacteristics such as age, gender, health, occupation andhobbies. People with similar characteristics are grouped together and are charged a premium based on the group's level of risk.

REQUIREMENTS OF AN INSURABLE RISK

1. From the perspective of the insured:

8

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 9/39

The risk must be high. Losses with extremely high odds and

extremely low odds might best be handled in other ways.

The loss must be unaffordable.

The premium must be affordable or, at least, low in comparison

with the possible loss.

2. From the perspective of the insurer:

The loss must be fortuitous (unexpected in terms of timing and

magnitude).

The loss must non-catastrophic with neither the possibility of many

losses at one time or any one loss of overwhelming magnitude.

The losses must be personal because only people can suffer losses.

The loss must be definite in time, place and amount. This allows for

a reasonably accurate prediction of loss and thus calculation of premium.

CONCEPT OF INSURABLE INTEREST

The insured party must have an insurable interest in the person or

property covered. This means that he or she must stand to suffer a

loss should the peril occur.

Generally, insurable interest must exist at the time that the loss

occurs.

Requiring insurance supports the principle of indemnity, which

states that an insured should collect no more than the actual loss.

CONCEPT OF INSURANCE INDUSTRY

9

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 10/39

The important feature of insurance industry is the fact that not muchcapital is required to start and develop the business the equity base isalways much smaller than the liabilities undertaken and the resourcesgenerated. The resources accumulation in the form of reservesinvestmentand other assets are much more enormous than the equity base. Theneed for additional capital infusion in response to inflation and consequentincrease in management expenses and other input is very little andnon-existence. The premium income generated and proper husbandingof theresources take care of this aspect.

10

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 11/39

WHY DO PEOPLE IN INDIA TAKE INSURANCE

People in India have been viewing Insurance, especially life insuranceas a form of Investment . These are the common reasons why peoplein India take up insurance:

1 Insurance safeguards a person /his family /his business against possible losses on account of risks and perils. It provides financial

compensation for the losses suffered due to the happening of anyunforeseen events.2 Tax Relief:

a. Under Section 88 of Income Tax Act , a portion of premiums paid for life insurance policies (LIC) are deductedfrom tax liability. Similarly, exemption is available for Health Insurance Policy premiums.

b. Money paid as claim including Bonus under a life policy isexempted from payment of Income Tax.

3 Encourages Savings : An insurance scheme encourages thriftamong individuals. It inculcates the habit of saving compulsorily,unlike other saving instruments, wherein the saved money can beeasily withdrawn.

4 The beneficiaries to an insurance claim amount are protected fromthe claims of creditors by affecting a valid assignment.

5 Life Policies are accepted as a security for a loan. They can also besurrendered for meeting unexpected emergencies.

6 Based on the concept of sharing of losses, the society will benefit ascatastrophic losses are spread globally.

11

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 12/39

TYPES OF INSURANCE

Insurance has been classified into:• Life Insurance• General Insurance or Non-Life insurance

LIFE INSURANCE

Life insurance is a written contract between the insured and theinsurer, that provides for the payment of the insured sum on the dateof the maturity of the contract or on the unfortunate death of theinsured, whichever occurs earlier.

The different types of life insurance are:• Whole Life Assurance Plans

• Term Assurance Plans

• Annuities

NON LIFE INSURANCE

There are various broad categories of non-life or generalInsurance as follows:

Health Insurance:

Just like one looks to safeguard ones wealth, these policies ensureguarding the insurer's health against any calamities that may causelong term harm to ones life and even hamper ones earning ability for alifetime. Some examples of this type of policy are mediclaim policy,

personal accident, group accident, traffic accident, etc.

12

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 13/39

Business Insurance:

Risks of loss of profits/business, goods, plant and machinery are most profound in case of business. Under this head they cover the mostwidely used policies that cover a business from any loss of the abovekind. Some of these policies are burglary insurance, shopkeepersinsurance, key-man insurance, marine insurance, public liabilityinsurance, workmen compensation insurance, air transit insurance,fidelity guarantee insurance etc.

Automobile Insurance:

Auto Policy is required to be taken to cover the risks that arise to theowner, vehicle and third party. This includes the Compulsory VehiclePolicy (In India, by the Motor Vehicles Act, every car owner is requiredto covered against Act risks) and the Comprehensive Vehicle Policy.

Fire Insurance:

This policy is required to be taken to prevent any loss of profits / property from incidental fire. Eg: fire insurance and fire consequentialloss policy.

Travel Insurance

Every year number of tourists die while travelling. They lose their baggages, passports etc are left stranded in unfamiliar environments.Medical attention in a foreign land while very expensive is also verydifficult to find in foreign land. Travel policies are designed to take care

13

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 14/39

of all the problems that generally occur while travelling, whether domestic or foreign.

BRIEF HISTORY OF THE INSURANCE SECTOR IN INDIA

The insurance sector in India has come a full circle from being an opencompetitive market to nationalisation and back to a liberalised marketagain. Tracing the developments in the Indian insurance sector reveals

the 360 degree turn witnessed over a period of almost two centuries.Till the end of 1999-2000, two government insurance companies,namely, Life Insurance Corporation (LIC) and General InsuranceCorporation (GIC) were the monopoly insurance (both life and non-life)

providers in India.

In the year 2000-01, the Indian Government lifted all entry restrictionsfor private sector investors. Foreign investment insurance market wasalso allowed in the Indian market and the face of the Indian Insurancesector changed dramatically.

We will first take a brief look at the old players in the market andunderstand the position they were in before the opening up of theInsurance Sector.

LIFE INSURANCE CORPORATION OF INDIA (LIC)

In 1956, 245 Indian and foreign insurers and provident societies thatwere prevalent in India were taken over by the central government andnationalised to form the Life Insurance Corporation of India (LIC) with a

contribution of Rs. 5 crore from the Government of India. LIC wasformed to spread the message of life insurance in the country and

14

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 15/39

mobilise people's savings for nation-building activities. A monoliththen, the corporation, enjoyed a monopoly status and becamesynonymous with life insurance.

Today LIC has its central office in Mumbai and seven zonal offices atMumbai, Calcutta, Delhi, Chennai, Hyderabad, Kanpur and Bhopal andoperates through 100 divisional offices in important cities and 2,048

branch offices. LIC has 5.59 lakh active agents spread over thecountry. The Corporation also transacts business abroad and hasoffices in Fiji, Mauritius and United Kingdom. LIC is associated with jointventures abroad in the field of insurance, namely, Ken-India AssuranceCompany Limited, Nairobi; United Oriental Assurance CompanyLimited, Kuala Lumpur; and Life Insurance Corporation (International),E.C. Bahrain. It has also entered into an agreement with the Sun Life(UK) for marketing unit linked life insurance and pension policies in U.K

LIC sold 2,32,50,078 individual policies and earned a first premiumincome of Rs.14,844.05 crore during the financial year 2001-02.Post liberalisation, the company is bound to face stiff competition fromthe newer players in the market. However, LIC has the first mover advantage and today the common man relates life insurance with LIC

and this will be the companies biggest advantage.

GENERAL INSURANCE CORPORATION OF INDIA (GIC)

The General Insurance business in India was nationalized with effectfrom 1.1.1973 by the General Insurance Business (Nationalization) Act,1972 and a Government company known as General InsuranceCorporation of India was formed. 107 Indian and foreign insurers which

15

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 16/39

were operating in the country prior to nationalisation, were groupedinto four operating companies namely1. National Insurance Company Ltd.

2. Oriental Insurance Company Ltd.

3. New India Assurance Company Ltd.

4. United India Insurance Company Ltd.

The Government of India subscribed to the capital of GIC. GIC, in turn,subscribed to the capital of the above four companies. All the four companies are government companies registered under theCompanies Act.All the above four subsidiaries of GIC operate all over the countrycompeting with one another and underwriting various classes of general insurance business except for aviation insurance of nationalairlines and crop insurance which is handled by the GICGIC and its subsidiaries have representation either directly or through

branches in 18 countries and through associate/ locally incorporatedsubsidiaries in 14 other countries. A subsidiary company of GIC India

International Pvt. Ltd. is operating in Singapore and their joint venturecompany, Kenindia Assurance Company Ltd. in Kenya. On the whole,the foreign operations of the general insurance industry have been

profitable.

GIC was converted into India's national reinsurer from December,2000 and all the subsidiaries working under the GIC umbrella wererestructured as independent insurance companies.

Indian Parliament has cleared a Bill on July 30,2002 delinking the four subsidiaries from GIC. A separate Bill has been approved by Parliament

to allow brokers, cooperatives and intermediaries in the sector.

16

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 17/39

Currently insurance companies- both private and public-- has to cede20 percent of its reinsurance with GIC. GIC is planning to increase re-insurance premium by 20 percent which works out at Rs. 3000 cr. GICis actively considering entry into overseas markets including WestAsia, South-east Asia and SAARC region.

REASONS FOR OPENING UP OF THE SECTOR

INDUCE COMPETITION

It was seen that though the waves of competition were sweepingacross the economy, LIC and GIC remain overstaffed, hierarchialmonolithic monopolies with little competition even between thesubsidiaries. As a result, the consumers are deprived of benefits suchas wider range of products, efficient service and lower price of insurance covers.

LIBERALISATION EFFORT

The opening up of Insurance sector was a part of the on goingliberalization in the financial sector of India. The changing face of thefinancial sector and the entry of several companies in the field of lifeand non life Insurance segment are one of the key results of theseliberalization efforts. Insurance business by way of generating

premium income adds significantly to the GDP.

HIGH PREMIUM AND LOW RETURNS

Pointing out that the insurance industry's funds are preempted throughgovernment-mandated investments with low yield, the report said this

17

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 18/39

affects the financial results of the insurance companies. This is whyrates of insurance premia are so high and returns on savings investedin life insurance are so low. In the absence of competition, LIC's vastmarketing and services network was inadequately responsive tocustomer needs and there was excessive lapsation of policies.

INSURANCE MOBILISATION

The entry of several private insurance companies, particularlyinternational insurance companies, through joint ventures, will speedup the process of insurance mobilisation. The competition will unleashnew schemes and benefits, which will give consumers a better chanceto save as well as insure. The penetration of Insurance in India isextremely low and the opening up of the sector was seen as a wayincreasing penetration.

FLOW OF FDI

The policy of the government to open up the financial sector and theInsurance sector is expected to bring greater FDI inflow in to thecountry.

18

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 19/39

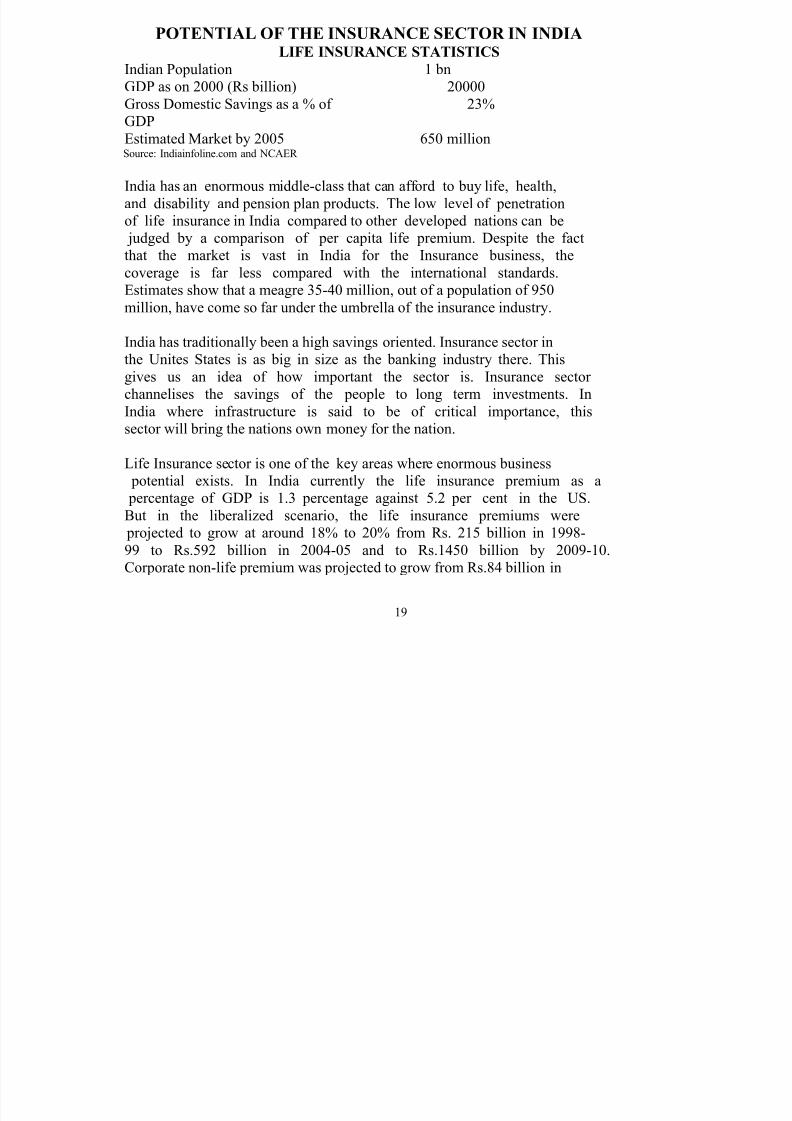

POTENTIAL OF THE INSURANCE SECTOR IN INDIALIFE INSURANCE STATISTICS

Indian Population 1 bnGDP as on 2000 (Rs billion) 20000Gross Domestic Savings as a % of 23%GDPEstimated Market by 2005 650 millionSource: Indiainfoline.com and NCAER

India has an enormous middle-class that can afford to buy life, health,and disability and pension plan products. The low level of penetrationof life insurance in India compared to other developed nations can be

judged by a comparison of per capita life premium. Despite the factthat the market is vast in India for the Insurance business, thecoverage is far less compared with the international standards.Estimates show that a meagre 35-40 million, out of a population of 950million, have come so far under the umbrella of the insurance industry.

India has traditionally been a high savings oriented. Insurance sector inthe Unites States is as big in size as the banking industry there. Thisgives us an idea of how important the sector is. Insurance sector

channelises the savings of the people to long term investments. InIndia where infrastructure is said to be of critical importance, thissector will bring the nations own money for the nation.

Life Insurance sector is one of the key areas where enormous business potential exists. In India currently the life insurance premium as a percentage of GDP is 1.3 percentage against 5.2 per cent in the US.But in the liberalized scenario, the life insurance premiums were

projected to grow at around 18% to 20% from Rs. 215 billion in 1998-99 to Rs.592 billion in 2004-05 and to Rs.1450 billion by 2009-10.Corporate non-life premium was projected to grow from Rs.84 billion in

19

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 20/39

1998-99 to Rs.386 billion in 2009-10 and personal line non-life fromRs.4 billion to Rs.51 billion.

The potential market is so huge that it can grow by 15 to 17 per cent per annum. Now with the entry of private insurance companies, theIndian Insurance Market may finally be able to make deeper

penetration into newer segments and expand the market sizemanifold.

20

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 21/39

REFORMS IN THE SECTOR The eagerly awaited Insurance Regulatory and Development Authority(IRDA) Bill to open the insurance sector in India to private and foreign

players, was passed by the Lok Sabha on December 2, 1999 and bythe Rajya Sabha on December 7, 1999.

The Bill seeks to grant statutory status to the interim InsuranceRegulatory Authority and amend the 1938 Insurance Act, the 1956 LifeInsurance Corporation Act and the 1972 General Insurance Business

(Nationalization) Act to end the public sector monopoly. The IRDA Billincorporates the recommendations made by the parliamentaryStanding Committee on Finance.

Salient Features of Insurance Sector Reform Bill:

The bill seeks to regulate, promote and ensure orderly growth of

the insurance industry and provides for solvency norms andspecifies that the funds of policyholders would be retained withinthe country.

The minimum capital requirement for life and general insurance

has been retained at Rs 100 crore ($23.02 million) and for reinsurance firms at Rs 200 crore ($46.04 million) as provided in theearlier IRA Bill.

It has been stipulated that the aggregate foreign holding in an

Indian insurance company shall not exceed 26 per cent of the paid-up equity. Moreover, to provide a level playing field, It has been

proposed that the Indian promoters would also be required to bringdown their equity holding to 26 percent after a period of 10 years

from the commencement of business.

21

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 22/39

The Bill has proposed solvency margins of Rs. 50 crores (US $

11.51 million) for life and general Insurance and Rs. 100 crores (US$ 23.02 million) for reinsurance companies.

IRDA, in addition to other functions, would supervise the

functioning of the Tariff Advisory Committee (TAC) and specify the percentage of premium income of the insurers to be set aside tofinance schemes for promoting and regulating professional

organizations in the insurance sectors.

22

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 23/39

REGULATORY AUTHORITY

INSURANCE REGULATORY AND DEVELOPMENT AUTHORITY

IRDA is formed as an authority to protect the interests of holders of insurance policies, to regulate, promote and ensure orderly growth of the insurance industry.

With the Insurance Regulatory and Development Act, the focus shifted

to the following:

The Insurance Regulatory and Development Authority (IRDA) •

should give priority to health insurance while issuing certificatesof registration

Policyholders' funds will be invested in the social sector and •

infrastructure. The percentage may be specified by the IRDA andsuch regulations will apply to all insurers operating in thecountry;

Insurers will be expected to undertake a certain percentage of •

business in the rural or social sector and provide policies to persons residing in rural areas, workers in the unorganised andinformal economically back;

In case the insurers fail to meet the social sector obligation a fine •

of Rs.2.5 mn would be imposed the first time. Subsequentfailures would result in cancellation of licenses.

Duties, powers and functions of IRDA

The following are the powers and the functions of the IRDA are asfollows:

23

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 24/39

(a) The IRDA issues, modifies, renews, suspends, withdrawsand cancels all certificate of registration for all parties thatapply.

(b) They are also responsible for the protection of the interestsof the policy holders in matters concerning assigning of

policy, nomination by policy holders, insurable interest,settlement of insurance claim, surrender value of policyand other terms and conditions of contracts of insurance.

(c) The IRDA specifies requisite qualifications, code of conductand practical training for intermediary or insuranceintermediaries and agents.

(d) It also specifies the code of conduct for surveyors and lossassessors.

(e) The IRDA has been given the responsibility of promotingefficiency in the conduct of insurance business.

(f) It is in charge of promoting and regulating professional

organisations connected with the insurance and re-insurance business;

It has been with the control of the Insurance (g) entrusted

sector by calling for information from, undertakinginspection of, conducting and investigations inquires

including audit of the insurers, intermediaries, insuranceintermediaries and other organisations connected with theinsurance business;

(h) It will also be responsible for the control and regulation of

the rates, advantages, terms and conditions that may beoffered by insurers.

24

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 25/39

(i) The IRDA will specify the form and manner in which booksof account shall be maintained and statement of accountsshall be rendered by insurers and other insuranceintermediaries.

(j) One of the most important functions is that of regulatinginvestment of funds by insurance companies and themaintenance of margin of solvency.

(k) The other function is that of adjudication of disputes between insurers and intermediaries or insuranceintermediaries.

25

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 26/39

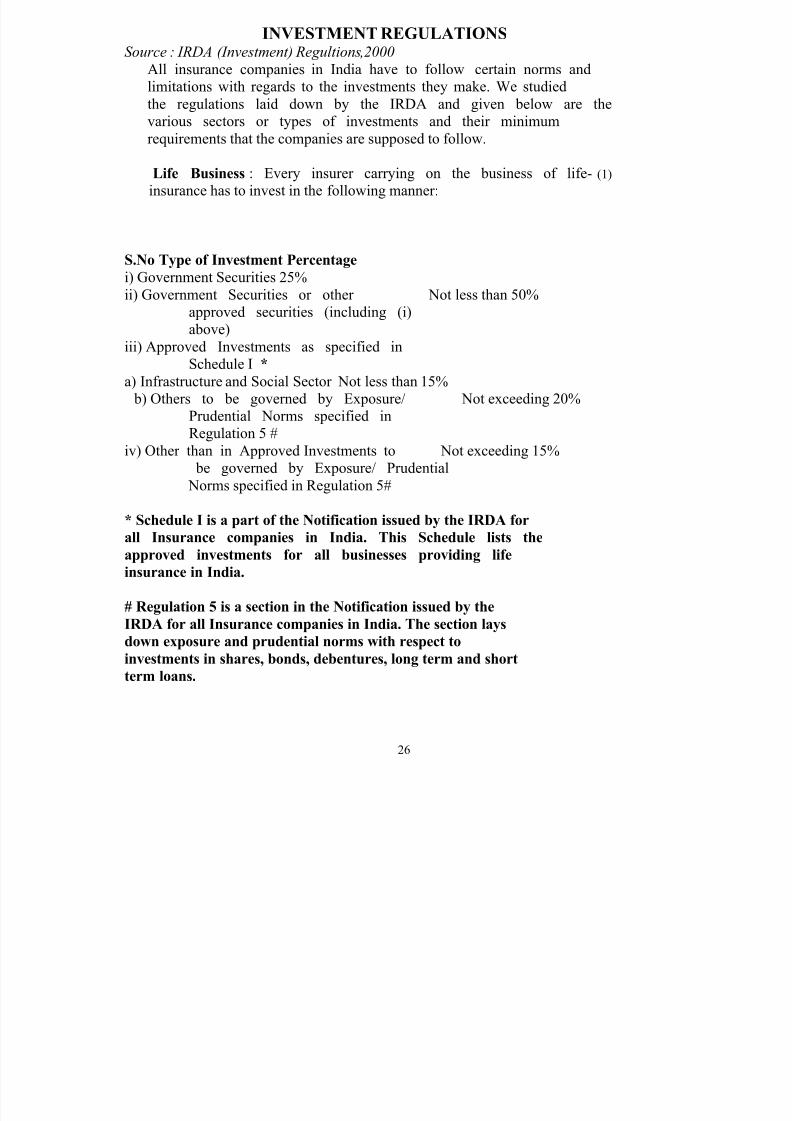

INVESTMENT REGULATIONSSource : IRDA (Investment) Regultions,2000

All insurance companies in India have to follow certain norms andlimitations with regards to the investments they make. We studiedthe regulations laid down by the IRDA and given below are thevarious sectors or types of investments and their minimumrequirements that the companies are supposed to follow.

Life Business : Every insurer carrying on the business of life- (1)

insurance has to invest in the following manner:

S.No Type of Investment Percentage

i) Government Securities 25%ii) Government Securities or other Not less than 50%

approved securities (including (i)above)

iii) Approved Investments as specified inSchedule I *

a) Infrastructure and Social Sector Not less than 15% b) Others to be governed by Exposure/ Not exceeding 20%

Prudential Norms specified inRegulation 5 #

iv) Other than in Approved Investments to Not exceeding 15% be governed by Exposure/ Prudential Norms specified in Regulation 5#

* Schedule I is a part of the Notification issued by the IRDA for

all Insurance companies in India. This Schedule lists the

approved investments for all businesses providing life

insurance in India.

# Regulation 5 is a section in the Notification issued by the

IRDA for all Insurance companies in India. The section lays

down exposure and prudential norms with respect to

investments in shares, bonds, debentures, long term and short

term loans.

26

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 27/39

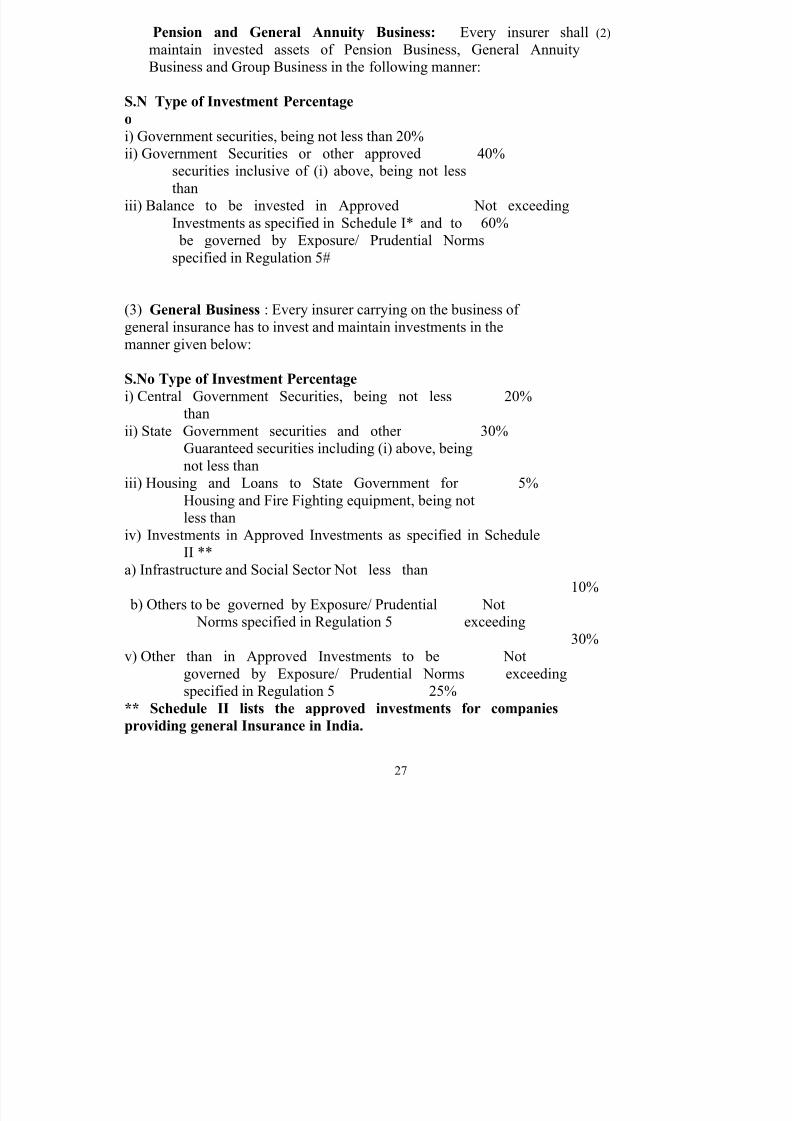

Pension and General Annuity Business: Every insurer shall (2)

maintain invested assets of Pension Business, General AnnuityBusiness and Group Business in the following manner:

S.N Type of Investment Percentage

o

i) Government securities, being not less than 20%ii) Government Securities or other approved 40%

securities inclusive of (i) above, being not lessthan

iii) Balance to be invested in Approved Not exceedingInvestments as specified in Schedule I* and to 60%

be governed by Exposure/ Prudential Normsspecified in Regulation 5#

(3) General Business : Every insurer carrying on the business of general insurance has to invest and maintain investments in themanner given below:

S.No Type of Investment Percentage

i) Central Government Securities, being not less 20%than

ii) State Government securities and other 30%Guaranteed securities including (i) above, beingnot less than

iii) Housing and Loans to State Government for 5%Housing and Fire Fighting equipment, being notless than

iv) Investments in Approved Investments as specified in ScheduleII **

a) Infrastructure and Social Sector Not less than

10% b) Others to be governed by Exposure/ Prudential Not

Norms specified in Regulation 5 exceeding30%

v) Other than in Approved Investments to be Notgoverned by Exposure/ Prudential Norms exceedingspecified in Regulation 5 25%

** Schedule II lists the approved investments for companies

providing general Insurance in India.

27

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 28/39

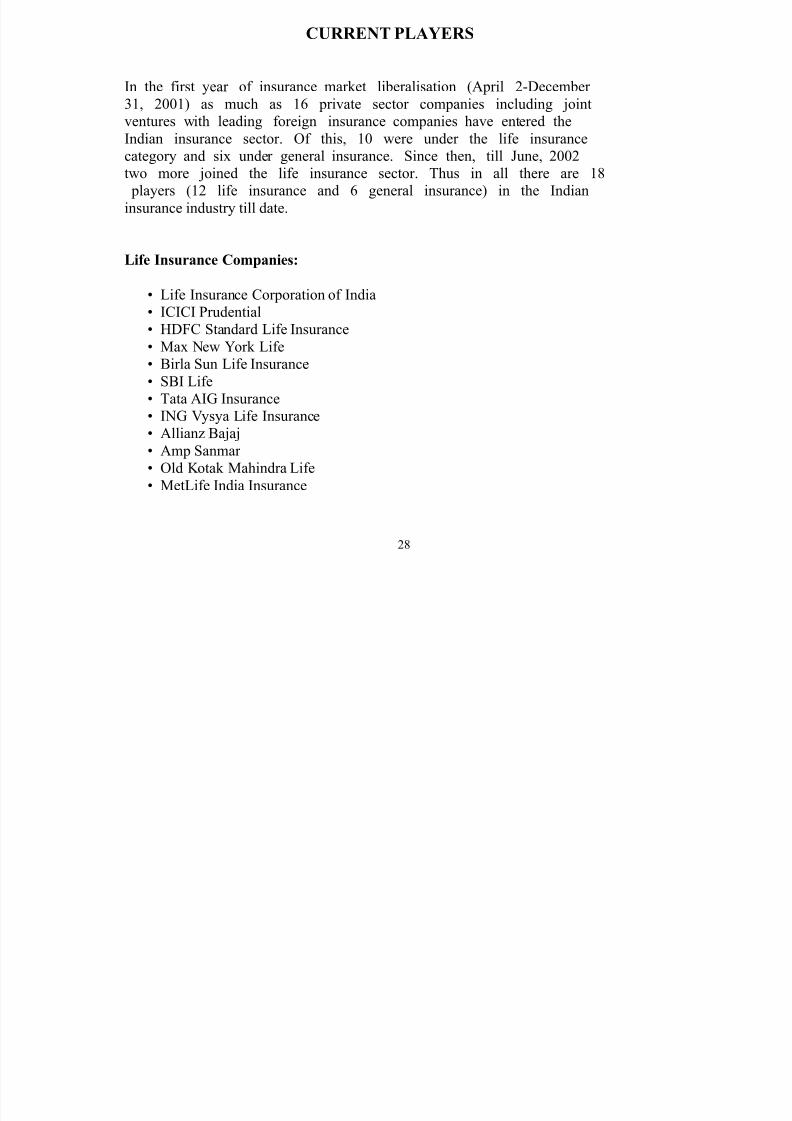

CURRENT PLAYERS

In the first year of insurance market liberalisation (April 2-December 31, 2001) as much as 16 private sector companies including jointventures with leading foreign insurance companies have entered theIndian insurance sector. Of this, 10 were under the life insurancecategory and six under general insurance. Since then, till June, 2002two more joined the life insurance sector. Thus in all there are 18

players (12 life insurance and 6 general insurance) in the Indianinsurance industry till date.

Life Insurance Companies:

• Life Insurance Corporation of India• ICICI Prudential• HDFC Standard Life Insurance• Max New York Life• Birla Sun Life Insurance• SBI Life• Tata AIG Insurance• ING Vysya Life Insurance• Allianz Bajaj• Amp Sanmar • Old Kotak Mahindra Life• MetLife India Insurance

28

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 29/39

29

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 30/39

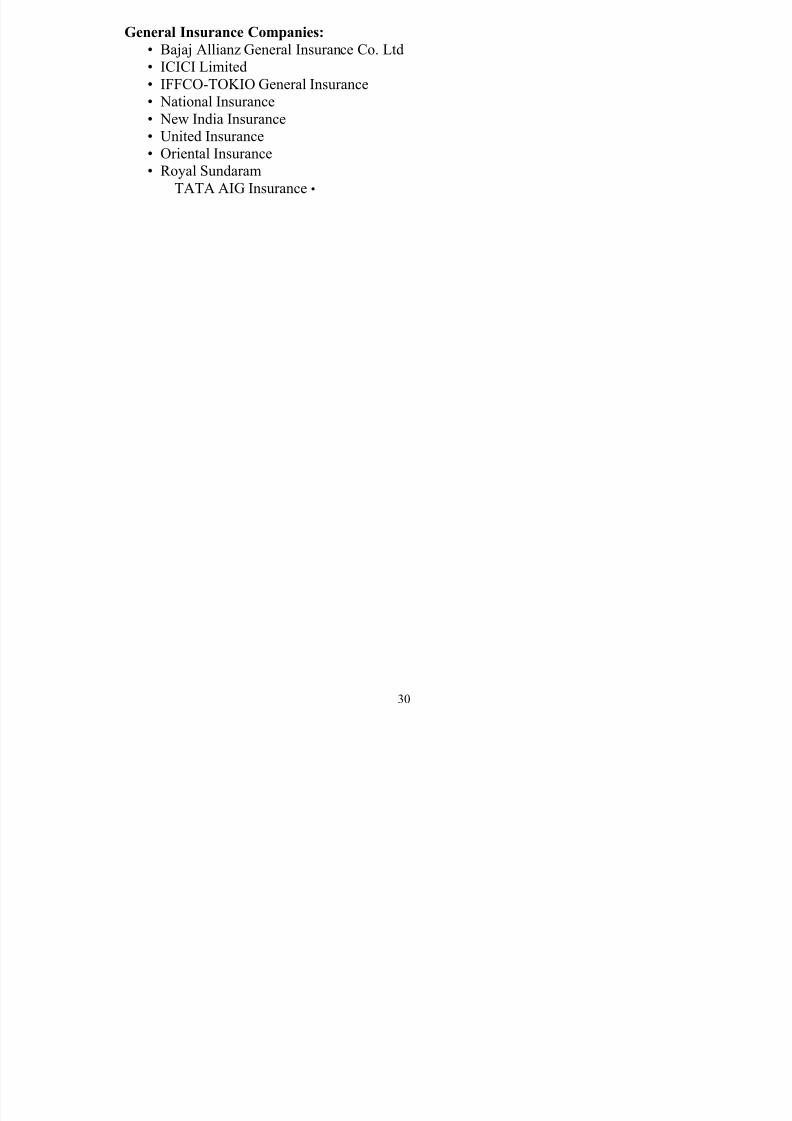

General Insurance Companies: • Bajaj Allianz General Insurance Co. Ltd• ICICI Limited• IFFCO-TOKIO General Insurance• National Insurance• New India Insurance• United Insurance• Oriental Insurance• Royal Sundaram

TATA AIG Insurance •

30

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 31/39

DISTRIBUTION CHANNELS

In the liberalized insurance market, there will be multiple distributionchannels, which will include agents, brokers, corporate intermediaries,

bank branches, affinity groups and direct marketing through telesalesand Internet. Some channels will be cheaper than others. Hence therewill be competition among the channels. The new insurers will operatewith the help of multiple distribution channels but the existing insurers

may be forced to operate only with the help of agents. Hence, intensecompetition will grow among the old and new insurers in the market towin the consumers. Firms will need to forge relationships with the

partners for strategic advantage. They need to have strong partner relationship management. For example, local partners may havestrong distribution channel in their line of business. That can be usedto sell insurance also in a cost-effective manner.All these will pose a great challenge to the insurers in the liberalizedinsurance market.

DISTRIBUTION THROUGH BANKS

Distribution of insurance products through banks are considered to bethe most popular banks are considered to be the most popular mediumas the private players prefer to utilise the wide network of banks for the distribution of insurance policies in India.Like in the European market, bancassurance can be an effectivechannel. In countries like Italy, France and Spain, insurance companieshave taken advantage of customers' typical loyalty to single banks and

pattern of long-term banking relationships by successfully selling their products through these banks. Here banks can leverage their existing

31

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 32/39

resources and earn supplementary fees while widening their range of available services. In the face of strong profitability pressures in their traditional banking services, banks will likely seize upon opportunitiesto expand their offerings by including insurance products.

DISTRIBUTION THROUGH INSURANCE AGENTS

Insurance agents and development officers provide another vital link ininsurance selling and various surveys have proven this aspect. Theseintermediaries help the insurance companies to keep in touch with

policyholders, assist claimants, and act as advisors to those who investtheir claim proceeds.

NEW CHANNELS

Other approaches, like call-center, direct marketing, and the Internetwill grow dramatically in importance over the next several years. Theseensure direct contact with the customers. It will enable firms to

acquire, retain and build loyalty among customers while loweringtransaction costs. To make multiple channel delivery work, all channelsmust be integrated tightly to deliver on the promise of serviceanytime, anywhere. Information gathered by each channel must becombined to provide a consolidated view of the customer relationshipand identify likely financial needs. The online media is definitelyconsidered to be one of the most effective modes of distribution as anumber of websites have already started offering policies online. At

present, 12 per cent of the world's insurance products are sold throughthe Internet, a figure likely to grow exponentially with a likely increase

32

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 33/39

in customer usage of the Internet for their own research and productcomparisons.

Extensive use of information technology can make the role of theseintermediaries more effective and buyer-friendly.

OTHER MODES OF DISTRIBUTION

Marketing alliances with people/companies having a strong physical presence is gaining popularity and is considered to be a gooddistribution strategy as well.

33

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 34/39

CHALLENGES BEFORE THE INDUSTRY

The new as well as the old insurers will have to face a number of challenges in the liberalized market.

New Insurers

The new insurers will have to invest a minimum capital of Rs. 100crores. The normal gestation period is of five years. The generation of

profit normally starts in the sixth year. Hence the new insurers willhave to be ready for locking up their capital for at least 5 years beforeearning any profits. Besides they will face problems of shortage of trained manpower for the insurance industry. The setting up of variousoffices and distribution network is a time consuming process. Further the new insurers will have to compete with the established insurancecompanies like LIC and GIC which have a corporate image and market

presence for several years.

Expectation of the consumers Today LIC has more than 60 products and GIC has more than 180

products to offer in the market. But most of them are outdated, as theyare not suitable to the needs of the consumers. Hence old as well asnew insurers will have to offer innovative products to the consumers.The consumers are particularly expecting good pension plans, healthinsurance, term insurance and investment products like unit-linkedinsurance, from the life insurers. Similarly the consumers expectinnovative products from the general insurers for managinghealthcare, property insurance, accident insurance and other productsrelated to the personal line of insurance.

34

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 35/39

The consumers also expect reduction in the premium of the insurance products as the mortality rate in India has come down by three timesin the last 50 years.

Distribution Channel

In the liberalized insurance market, there will be multiple distributionchannels, which will include agents, brokers, corporate intermediaries,

bank branches, affinity groups and direct marketing through telesalesand Internet. Some channels will be cheaper than others. Hence therewill be competition among the channels. The new insurers will operatewith the help of multiple distribution channels but the existing insurersmay be forced to operate only with the help of agents. Hence, intensecompetition will grow among the old and new insurers in the market towin the consumers. This will pose a great challenge to the insurers inthe liberalized insurance market.

Consumer Education Very soon the market will be flooded by a large number of products bya fairly large number of insurers operating in the Indian market. Evenwith limited range of products offered by LIC and GIC, the consumersare confused in the market. Their confusion will further increase in the

face of a large number of products in the market. The existing level of awareness of the consumers for insurance products is very low, it is so

because only 62% of the population of India is literate and less than10% well educated. Even the educated consumers are ignorant aboutthe various products of insurance. Hence it is necessary that all theinsurers should undertake the extensive plan for education of consumers. The consumer organizations and the media also can playvery important role in education of the consumers. This will result inexpansion of the insurance market and will also enable the needyconsumer to purchase appropriate products.

35

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 36/39

Consumer Grievance Redressal The insurers will have to face an acute problem of the redressal of theconsumers, grievances for deficiency in products and services. TheInsurance Regulatory Development Authority (IRDA), the regulatory

body has already appointed Ombudsman for looking into thegrievances of the policyholders, his judgement will be binding oninsurers. Further, under Consumer Protection Act 1986, the consumer courts are operating at district, state and the national level. In thecompetitive market, awareness level of the consumers will increaseand it will help consumers to fight for their legal right for deficiency inservices. Hence the number of legal cases filed by the consumersagainst insurers is likely to increase substantially in future. This will bea challenge to the insurers.

36

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 37/39

FUTURE SCENARIO OF INSURANCE INDUSTRY

The size of the existing insurance market is very large and is growingat the rate of 10% per year. The estimated potential of the Indianinsurance market in terms of premium was around Rs. 3,44,000 croresin the year 1999. Only 10% of the market share has been tapped byLIC and GIC and the balance 90% of the market still remains untapped.

This vast potential can be tapped only by a large number of insurers.To serve 100 crores of population, Indian insurance market offerstremendous opportunities to prospective insurers. Hence, the regulator should issue licenses to a large number of insurers if the insurancemarket has to grow at a fast rate.

With the increase in the life span of individuals and disintegration of the joint family system, each Individual now has arranged insurancecover for himself and for his family. Hence, coverage of insurers, whichwas around 7% of the population in 1999, has to grow very fast. In factall the citizens in the middle class, estimated around 314 million canafford insurance from their own financial resources. The remaining

population has to be given subsidized insurance with the help of thegovernment as well as the insurers.

The huge fund from insurance investments can be utilized for financingthe infrastructure industry as well as a support to other industries inthe country. Hence insurance industry is likely to play a key role inchanging the economic landscape of the country. However the successof the insurance industry will primarily depend upon meeting the risingexpectations of the consumers who will be the real king in theliberalized insurance market in future.

37

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 38/39

PROJECT COMPILED BY

SR. NAME ROLL NO

NO

1 OMIKA MEHRA

2 JENNET M

3 BINITA RUPANI

4 AKHILESH SETHI

5 PRIYADARSHINI SHINDE

38

8/8/2019 25153014 Insurance Sector

http://slidepdf.com/reader/full/25153014-insurance-sector 39/39