Embed Size (px)

Citation preview

PSG PSG KonsultKonsult PretoriaPretoria--OosOos

BeleggingsaanbiedingBeleggingsaanbieding

28 28 OktoberOktober 20102010

Agenda

• Little Big Things – Leon Ferreira BLC LLM, HDipTax, CFP®

• Entrepreneurskap – Willem Theron BCompt Hons, CA(SA)

• Die pad na herstel – Dawie Klopper BCom(Ekonomie), MBL, CFP®

• Aandeleportefeuljes – Leon Ferreira

• Go East Young Man – Chris Wehmeyer BCom, BProc, Lid van die JSE, CFP®

• Fondsprestasie – Leon Ferreira

• Hoe gebeur dit? – Johan Borcherds MCom(Belasting), CA (SA), CFP®

• Afsluiting – Leon Ferreira

The Little Big Things

Tom Peters

Oktober 2010

About the author

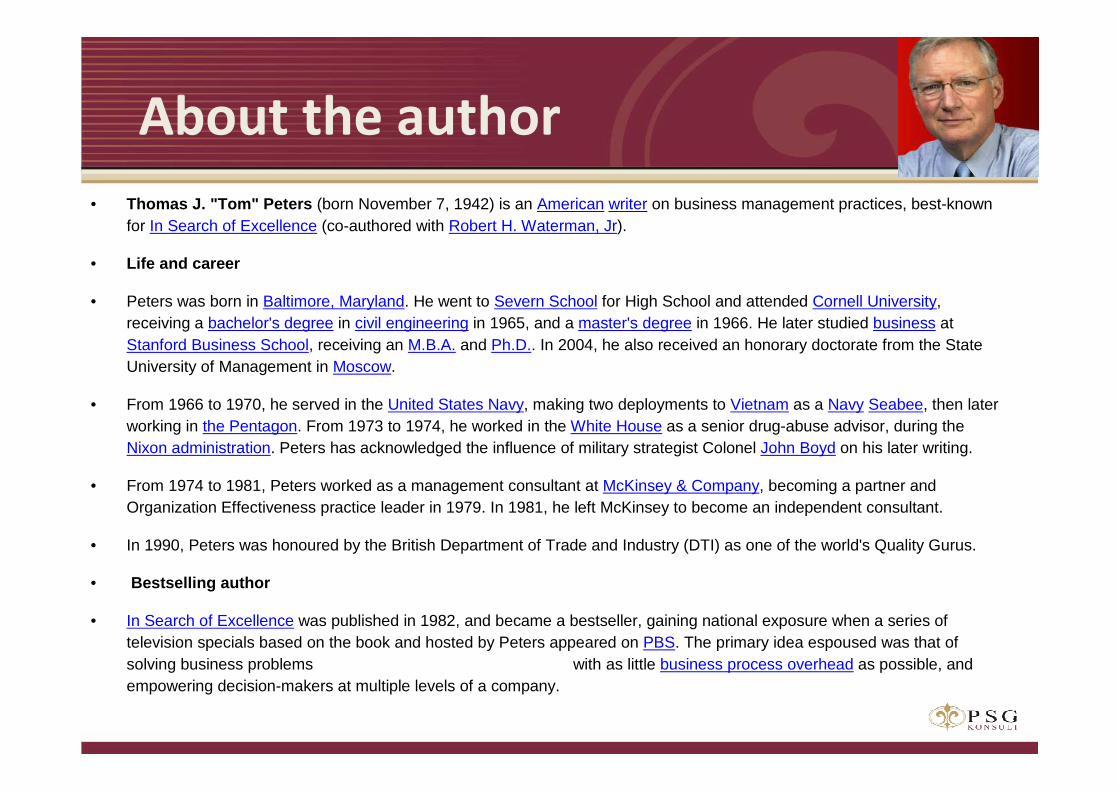

• Thomas J. "Tom" Peters (born November 7, 1942) is an American writer on business management practices, best-known for In Search of Excellence (co-authored with Robert H. Waterman, Jr).

• Life and career

• Peters was born in Baltimore, Maryland. He went to Severn School for High School and attended Cornell University, receiving a bachelor's degree in civil engineering in 1965, and a master's degree in 1966. He later studied business at Stanford Business School, receiving an M.B.A. and Ph.D.. In 2004, he also received an honorary doctorate from the StateUniversity of Management in Moscow.

• From 1966 to 1970, he served in the United States Navy, making two deployments to Vietnam as a Navy Seabee, then later working in the Pentagon. From 1973 to 1974, he worked in the White House as a senior drug-abuse advisor, during the Nixon administration. Peters has acknowledged the influence of military strategist Colonel John Boyd on his later writing.

• From 1974 to 1981, Peters worked as a management consultant at McKinsey & Company, becoming a partner and Organization Effectiveness practice leader in 1979. In 1981, he left McKinsey to become an independent consultant.

• In 1990, Peters was honoured by the British Department of Trade and Industry (DTI) as one of the world's Quality Gurus.

• Bestselling author

• In Search of Excellence was published in 1982, and became a bestseller, gaining national exposure when a series of television specials based on the book and hosted by Peters appeared on PBS. The primary idea espoused was that of solving business problems with as little business process overhead as possible, and empowering decision-makers at multiple levels of a company.

“OLD” Rules – yes, even in the age

of the internet

• “People turning 50 today have half their adult lives ahead of them”

Bill Novelli

• Americans on average own 13 cars in a lifetime, 7 are bought after

the age of 50. 13/7/50

• People age 55 and older are more active in online finance, shopping,

and entertainment than those under 55.

• Americans over 50 control a gargantuan share of the personal wealth

in the US. And are healthy.

• American woman over 50 control an enormous and growing share.

We are the Aussies & Kiwis & Americans & We are the Aussies & Kiwis & Americans & Canadians. We are the Western Europeans & Canadians. We are the Western Europeans &

Japanese. We are the fastest growing, Japanese. We are the fastest growing, the biggest, the wealthiest, the boldest, the mo st the biggest, the wealthiest, the boldest, the mo st

(yes) ambitious, the most experimental & (yes) ambitious, the most experimental & exploratory, the most different, the most indulge nt, exploratory, the most different, the most indulge nt, the most difficult & demanding, the most service & the most difficult & demanding, the most service & experience obsessed, the most vigorous, (the least experience obsessed, the most vigorous, (the least

vigorous,) the most health conscious, the most vigorous,) the most health conscious, the most female, the most profoundly important commercial female, the most profoundly important commercial

market in the history of the worldmarket in the history of the world ——andand

we will be the Center of we will be the Center of yyour universe for the next our universe for the next twenttwent yy--five five yyearsears .. We have arrived!We have arrived!

““Economic Growth Is Driven Economic Growth Is Driven

by by WomenWomen..””Source: Headline, Economist

“One thing is certain: Women’s rise to power, which is linked to

the increase in wealth per capita, is happening in all domains and

at all levels of society. Women are no longer content to provide

efficient labor or to be consumers with rising budgets and more

autonomy to spend. … This is just the beginning. The

phenomenon will only grow as girls prove to be more successful

than boys in the school system. For a number of observers, we

have already entered the age of ‘womenomics,’ the economy as

thought out and practiced by a woman.” —

Aude Zieseniss de Thuin, Women’s Forum

for the Economy and Society

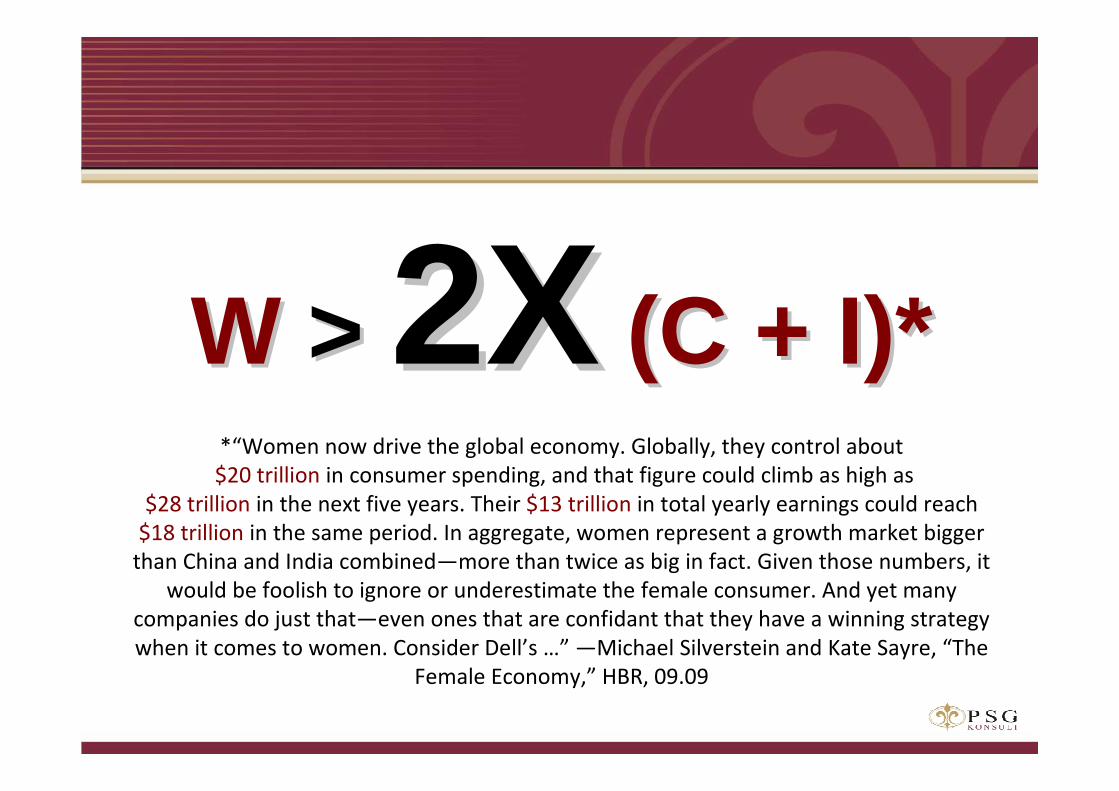

W W > > 2X2X (C + I)*(C + I)**“Women now drive the global economy. Globally, they control about

$20 trillion in consumer spending, and that figure could climb as high as

$28 trillion in the next five years. Their $13 trillion in total yearly earnings could reach

$18 trillion in the same period. In aggregate, women represent a growth market bigger

than China and India combined—more than twice as big in fact. Given those numbers, it

would be foolish to ignore or underestimate the female consumer. And yet many

companies do just that—even ones that are confidant that they have a winning strategy

when it comes to women. Consider Dell’s …” —Michael Silverstein and Kate Sayre, “The

Female Economy,” HBR, 09.09

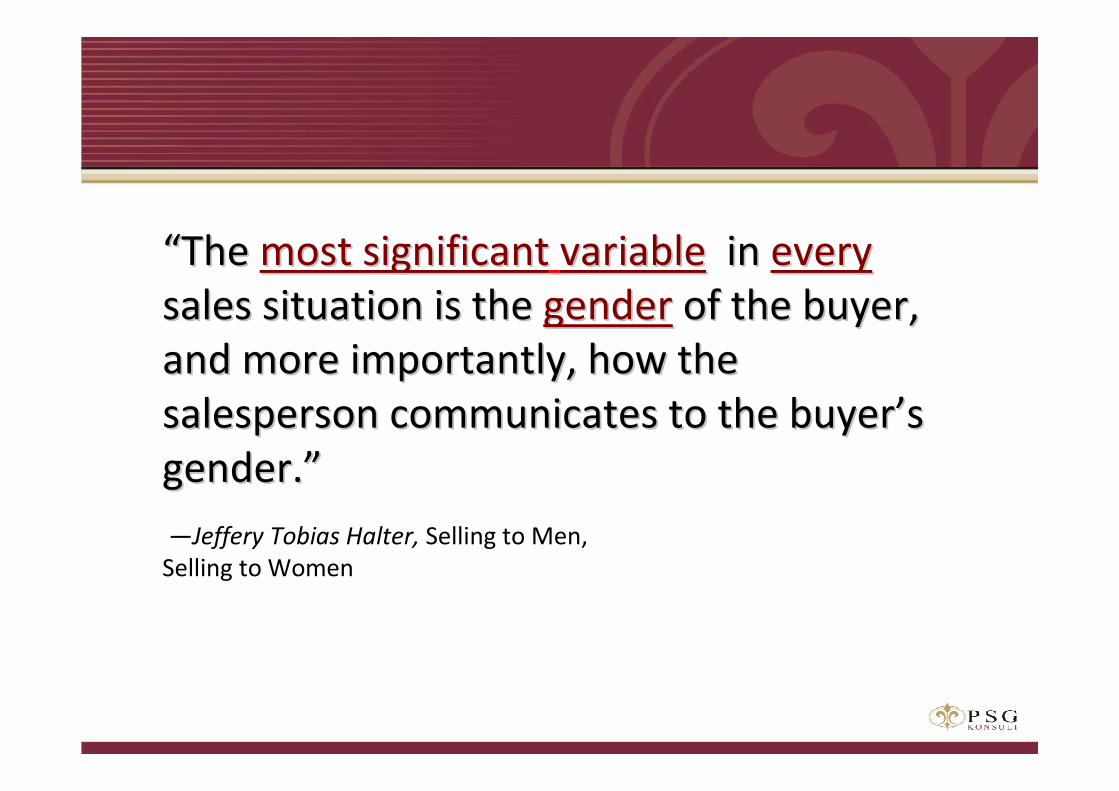

““The The most significantmost significant variablevariable inin everyevery

sales situation is thesales situation is the gendergender of the buyer, of the buyer,

and more importantly, how the and more importantly, how the

salesperson communicates to the buyersalesperson communicates to the buyer’’s s

gender.gender.””

—Jeffery Tobias Halter, Selling to Men,

Selling to Women

“Women donWomen don’’t buyt buy

brands. brands. They They

join themjoin them..””

EVEolutionEVEolution

WomenWomen’’s Strengths Match New Economy Imperativess Strengths Match New Economy Imperatives:: Link Link

[rather than rank] workers; [rather than rank] workers; favor interactivefavor interactive--collaborative collaborative

leadership style [empowerment beats topleadership style [empowerment beats top--down decision making];down decision making];

sustain fruitful collaborations; comfortable with sharing sustain fruitful collaborations; comfortable with sharing

information; information; see redistribution of power as victory, not surrendersee redistribution of power as victory, not surrender; ;

favor multifavor multi--dimensional feedback; dimensional feedback; value technical & interpersonal value technical & interpersonal

skills, individual & group contributions equally;skills, individual & group contributions equally; readily accept readily accept

ambiguity; ambiguity; honor intuition as well ashonor intuition as well as

pure pure ““rationalityrationality””;; inherently flexible; inherently flexible; appreciate cultural diversityappreciate cultural diversity..

——Judy B. Rosener,Judy B. Rosener,

AmericaAmerica’’s Competitive Secret: Women Managerss Competitive Secret: Women Managers

Gasspreker : Willem Theron

Hoof Uitvoerende Direkteur, PSG Konsult

Willem het groot geword in Johannesburg, gematrikuleer by HelpmekaarHoërskool en daarna sy B Compt (Hons) aan die Universiteit van Stellenboschvoltooi. Hy het sy klerkskap by die huidige firma van PriceWaterhouseCoopers in Stellenbosch gedoen waarna hy gekwalifiseerhet as GR (SA).

In 1976 begin hy die geoktrooieerde rekenmeestersfirma, Theron du Plessis in Middelburg wat in 1998 oor tien kantore in die Wes- en Oos-Kaap beskikhet.

In 1998, stig hy PSG Konsult en is sedertdien in sy huidige posisie as Hoof Uitvoerende Beampte. Hy dien ook op PSG Groep se direksie.

Willem geniet ‘n rondte gholf en sal altyd tyd maak om te jag. Verder het hyook boerderybelange in die Suid-Kaap. Hy is getroud met Annette en hullehet vier kinders en een kleindogter.

Entrepreneurskapen sukses

~ 28 Oktober 2010 ~Aanbieding deur Willem Theron

Wat is Entrepreneurskap ?

“Iemand wat nuwe dinge aanpak of nuwerigtings inslaan veral met betrekking tot die

oprigting van en die bestuur van sake-ondernemings”

- WAT / HAT

• Idee

• Dink

• Plan

• Mense

• Doen

Wat bepaal of jy‘n suksesvolleentrepreneur is??

SUKSES

Idee

• Duidelik

• Eenvoudig

• Anders

• Wettig / Moreel regverdigbaar

• Onkonvensioneel

Dink

• Beplan vir sukses

• Ken jou omgewing

• Ken jou opposisie

• Analiseer jou idees

• Kan dit wins maak?

Plan

• Skriftelik

• Tydsraamwerk

• Kapitaal

• Prosesse

• Begroting

• Tegnologie

• Wat is die opbrengs?

Mense

• Net die beste

• Opleiding

• Vergoed in verhouding met produksie

• Aangename werksomgewing

• Langtermyn verbintenis

• Kommunikasie

Doen

• Werk hard en eerlik

• Deursettingsvermoë

• Goeie etiek en administrasie

• Gun almal ‘n bestaan

• Betaal jou belastings

• Maandelikse resultate en evaluering

• Beskou probleme as uitdagings

• Maak planne

Behind every

Superman…

is a Superwoman

Sukses

• Nederigheid

• Erkenning

• Geduld – tyd

• Meetbaar:

- Monitêr

- Nie-monitêr

Tough times never last…

tough people do.

PSG Konsult

• Idee

• Dink

• Plan

• Mense

• Doen

• Sukses

1998 1998 -- 20102010

Missie

Om die voorste onafhanklike

privaat kliënte finansiële tussengangersgroep

in Suider Afrika en geselekteerde gebiede

oorsee te wees.

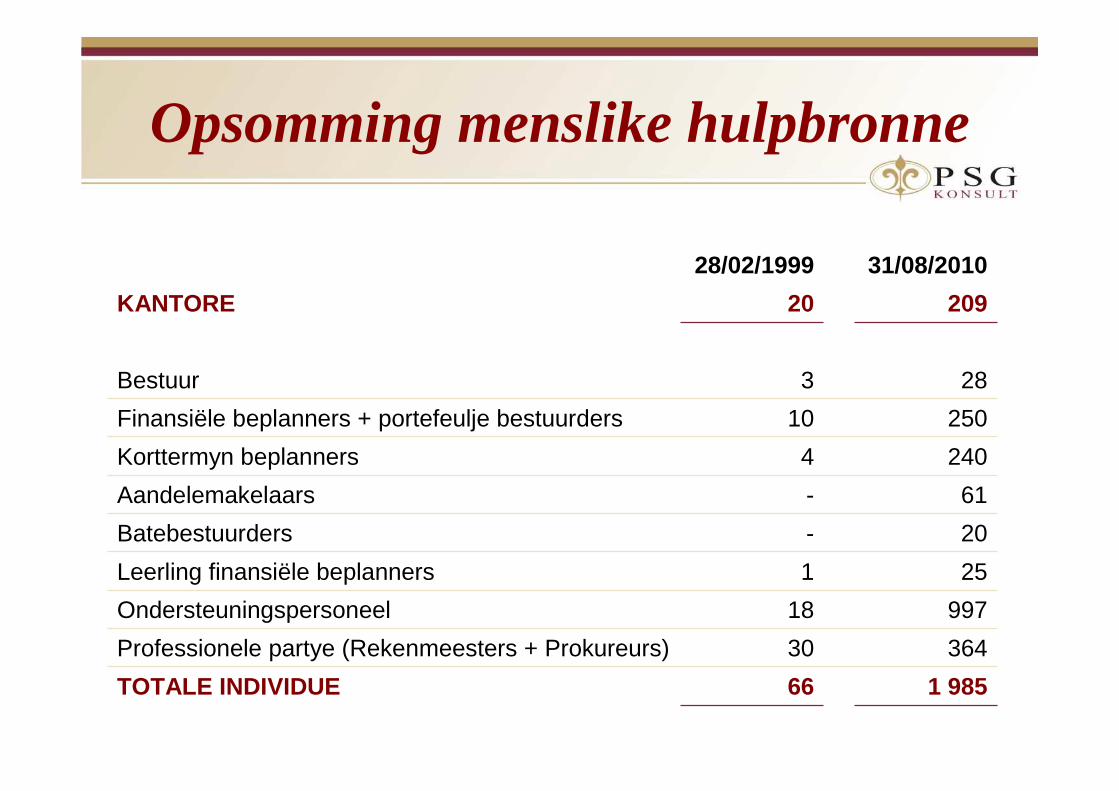

28/02/1999 31/08/2010

KANTORE 20 209

Bestuur 3 28

Finansiële beplanners + portefeulje bestuurders 10 250

Korttermyn beplanners 4 240

Aandelemakelaars - 61

Batebestuurders - 20

Leerling finansiële beplanners 1 25

Ondersteuningspersoneel 18 997

Professionele partye (Rekenmeesters + Prokureurs) 30 364

TOTALE INDIVIDUE 66 1 985

Opsomming menslike hulpbronne

0

100

200

300

400

500

600

700

800

900

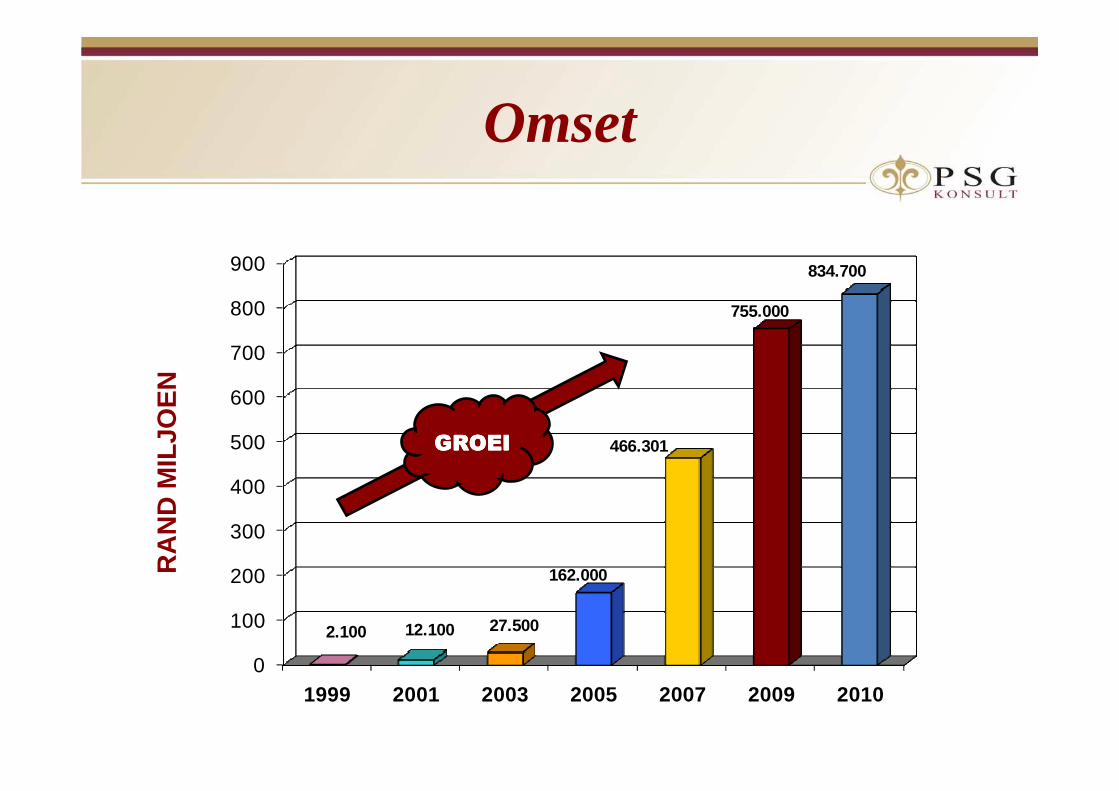

1999 2001 2003 2005 2007 2009 2010

2.100 12.100 27.500

162.000

466.301

755.000

834.700

OmsetR

AN

D M

ILJO

EN

GROEIGROEIGROEIGROEI

Hooflyn verdienste per aandeelS

EN

T

GROEIGROEIGROEIGROEI

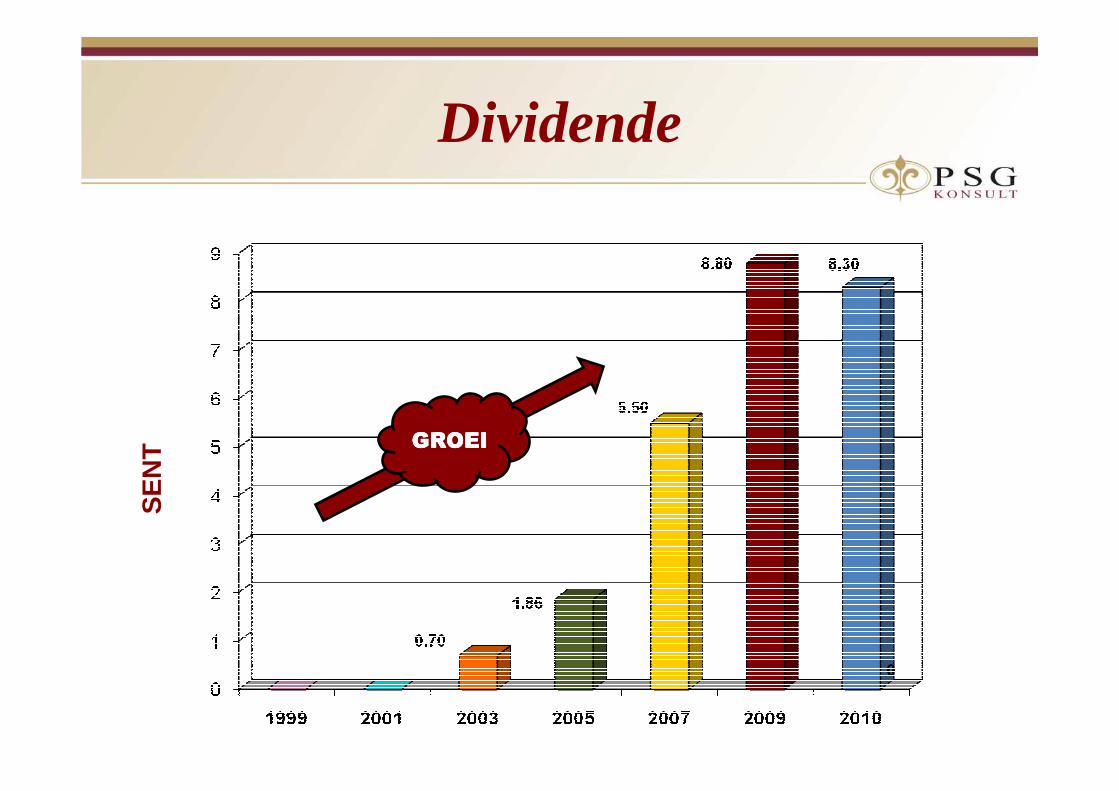

DividendeS

EN

T GROEIGROEIGROEIGROEI

28/02/99R’000

30/08/10R’000

EffekteTrusts 10 20 859

Aandeelportefeuljes 0 9 104

JSE bewaring 0 51 604

Totale fondse onder administrasie 10 81 567

Totale Korttermyn premies (jaarliks) 20 1,450

Kern Statistieke

“The future belongs to them who has faith in their dreams”

Nelson Mandela

“Laat jou lewe aan die Here oor en vertrou op Hom, Hy sal sorg”

Psalm 37.5

Die pad na herstel…

of

die son kom op in die

OosteDawie Klopper

Oktober 2010

Dubbele resessie?

• Slegte nuus oorheers die ekonomiese toneel sedert die begin van die jaar

• … en daar is vrese oor `n dubbel resessie.

• die resultaat is dat die VSA rentekoerse laag hou en alles in hulle vermoë

doen om hulle inflasiekoers weer aan die gang te kry.

• dit lei tot `n swakker dollar en druk op die Chinese om hulle geldeenheid te

versterk.

• China wil egter deflasie op die VSA en ander ekonomieë ( ontwikkelde en

opkomend) afdwing.

• In die tussentyd doen die Duitse ekonomie goed…

• teen die verwagting in want hulle uitvoere na China is baie stewig…

(Düsseldorf voorbeeld.)

• en dit hou die Europese ekonomie aan die gang

• Die “currency wars” het egter `n positiewe uitwerking op kommoditeite – en

edelmetaalpryse en dit ondersteun ons uitvoerpoging.

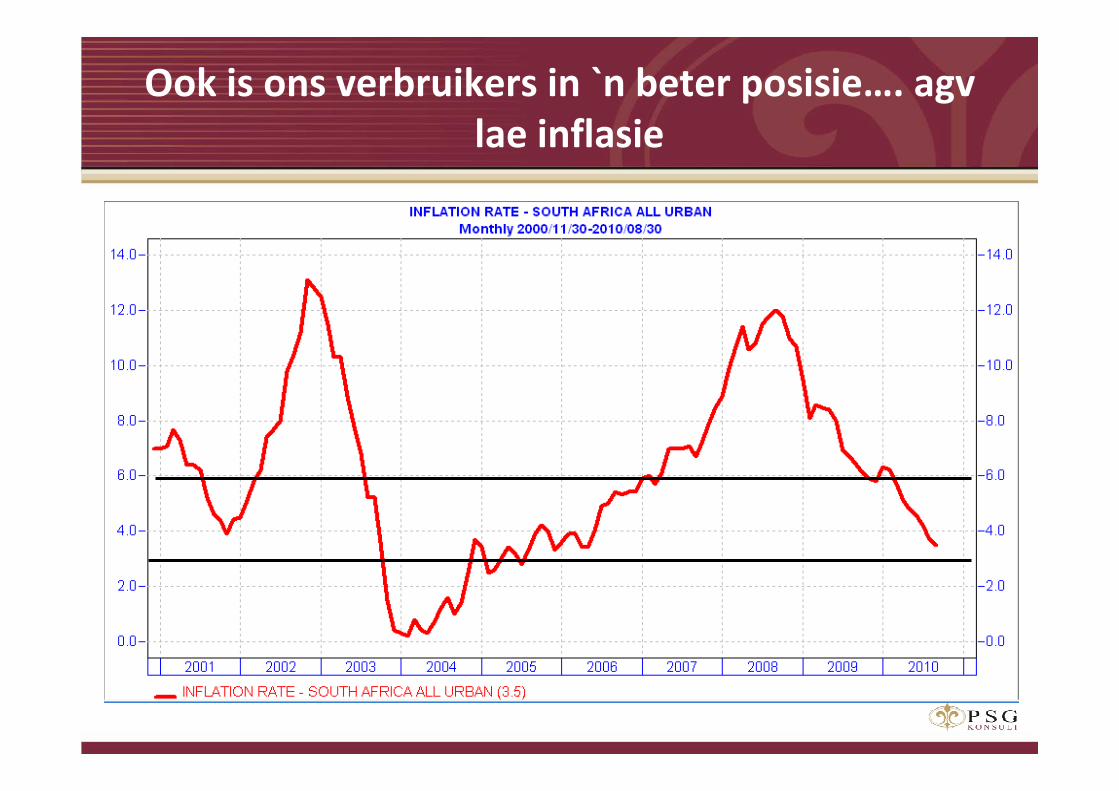

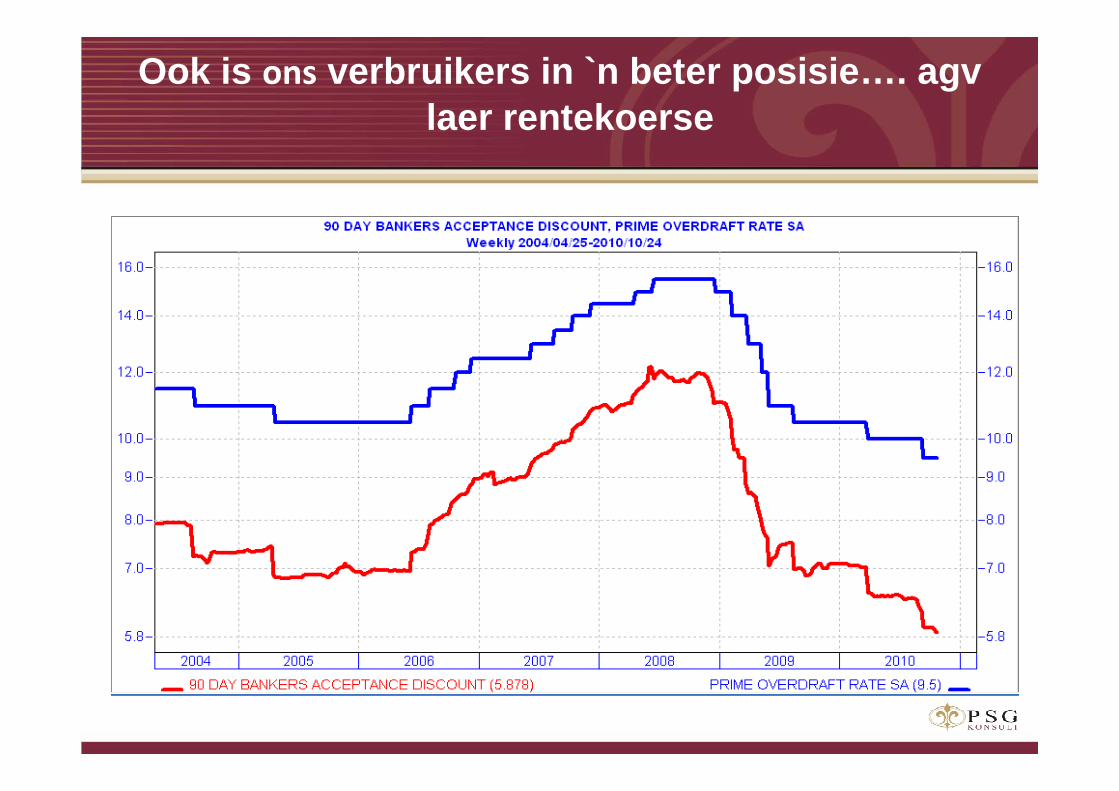

Ook is ons verbruikers in `n beter posisie…. agv

• stewige salarisverhogings

• lae inflasie en

• dalende rentekoerse

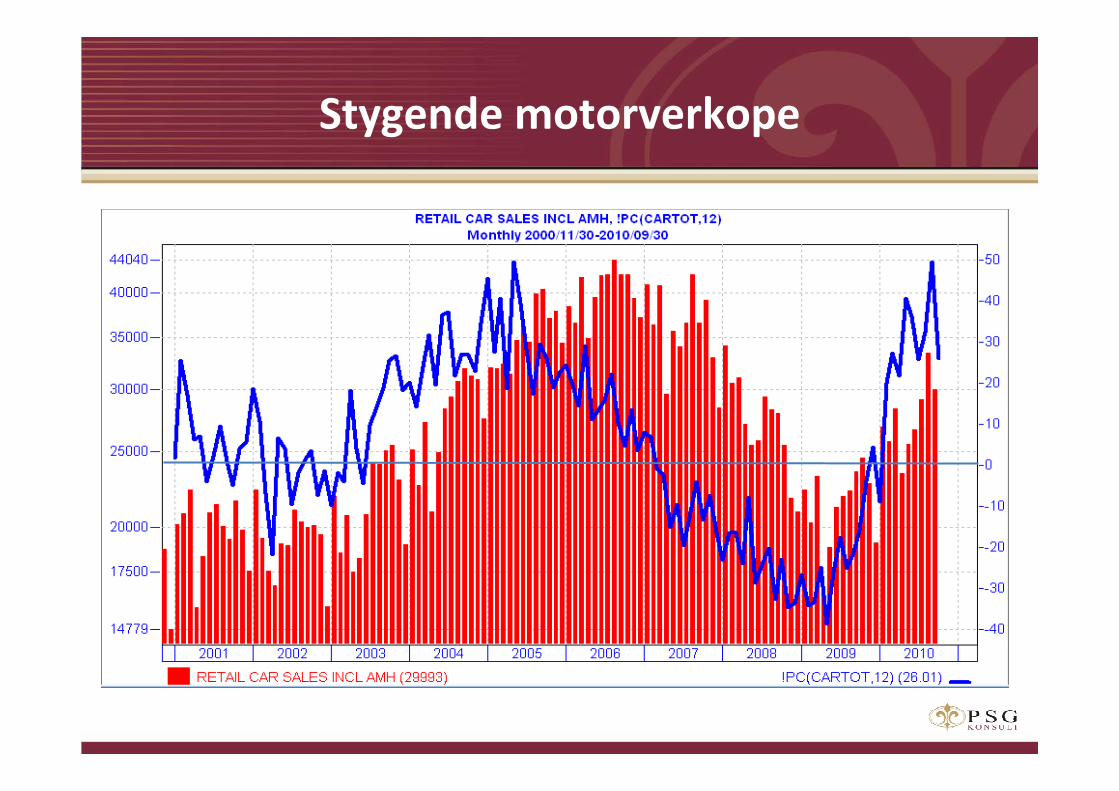

• Ons sien iets hiervan in stygende motorverkope

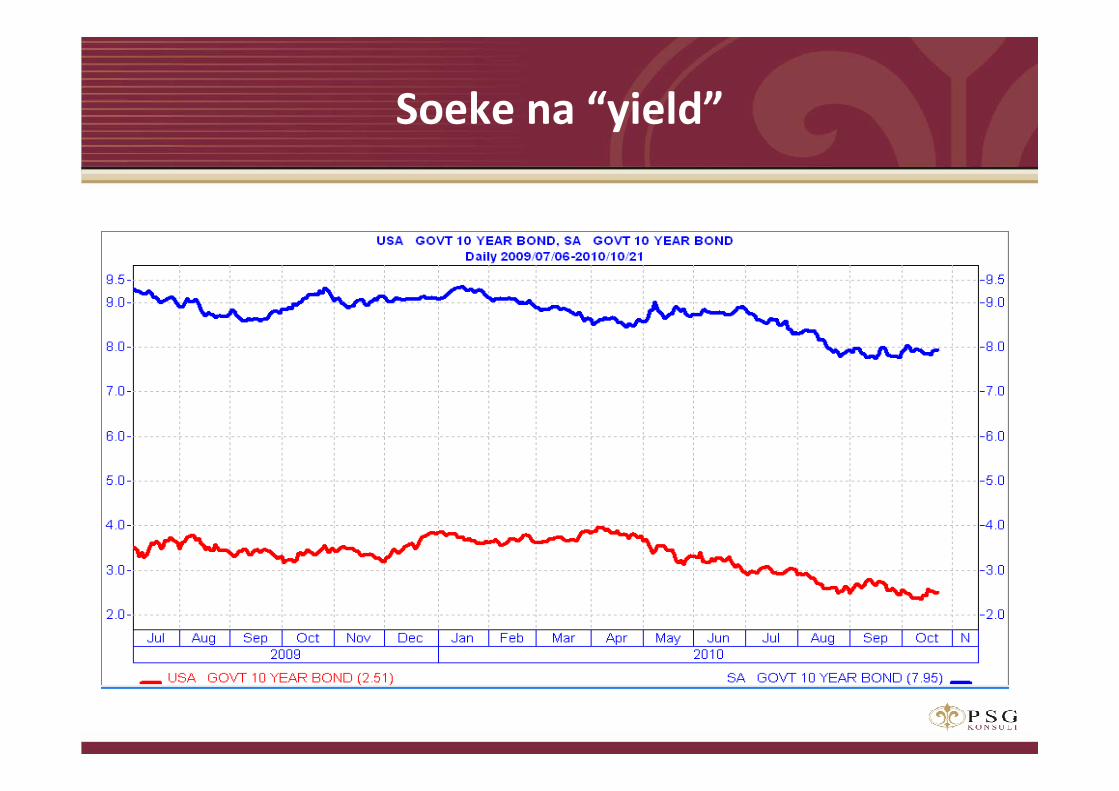

• Markte is oral op soek na ‘”yield’ ….

• en in SA is ons rentekoerse op die geldmark en kapitaalmark nog redelik hoog.

• Dit trek geld aan….

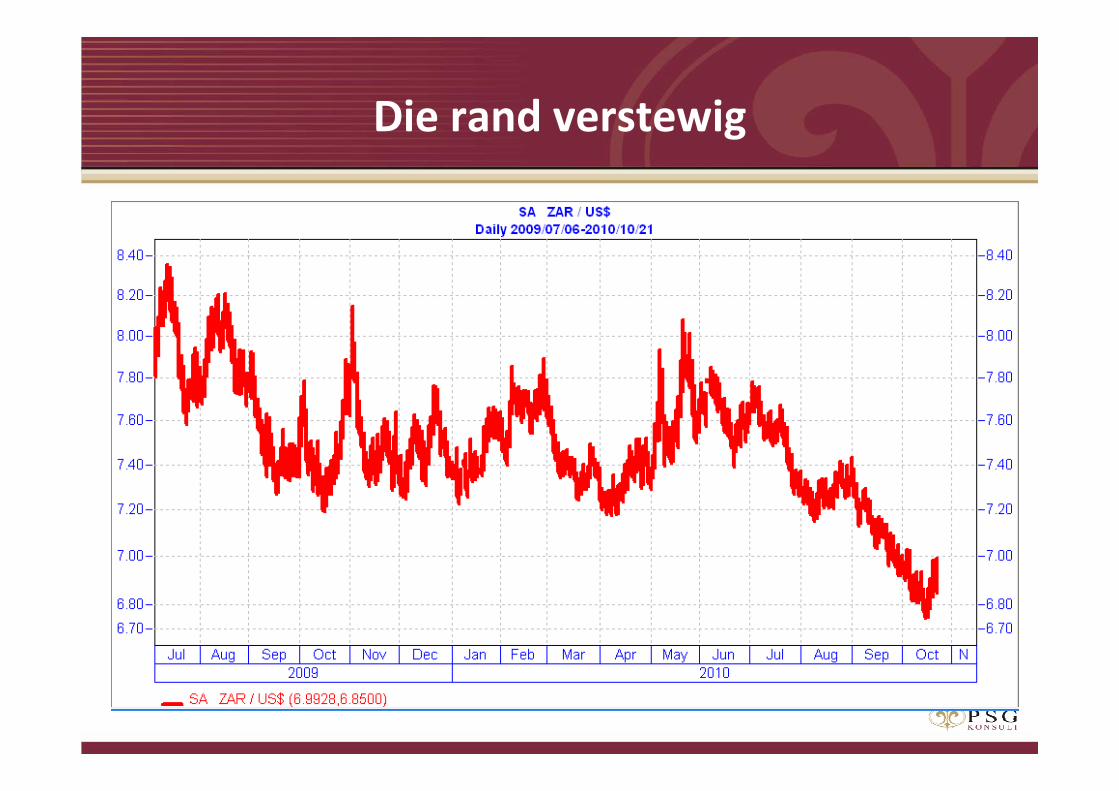

• en verstewig die rand

• Ons voer egter steeds te veel in en te min uit…

• wat die rand potensieel…. (Eendag) kwesbaar maak.

• Markwaardasies

Dubbele resessie? (vervolg)

Slegte nuus oorheers die ekonomiese toneel sedert

die begin van die jaar

… en daar is vrese oor `n dubbel ressessie

… wat dalk oordoen is?

VSA Kleinhandelverkope…

Globaal: `n Stadige herstel

Na die krisis:

Regerings: Hernude regulasie

Banke: Konserwatief en streng gereguleer

Huishoudings: matig, heropbou van welvaart

Handel: Proteksionisme

Bron: Sandra Gordon Onafhanklike Ekonoom

Die resultaat is dat die VSA rentekoerse laag

hou…

... en alles in hulle vermoë doen om hulle

inflasiekoers weer aan die gang te kry.

dit lei tot `n swakker dollar en druk op die Chinese

om hulle geldeenheid te versterk.

In die die tussentyd doen die Duitse ekonomie

goed…

Die “currency wars” het egter `n positiewe

uitwerking op kommoditeits – en edelmetaalpryse

+36%

Die “currency wars” het egter `n positiewe

uitwerking op kommoditeits – en edel metaalpryse

Die “currency wars” het egter `n positiewe

uitwerking op kommoditeits – en edel metaalpryse

… maar die sterk rand maak

dat die goudprys in $ terme

nie so goed styg nie

Ook is ons verbruikers in `n beter posisie…. agv

stewige salarisverhogings

Ook is ons verbruikers in `n beter posisie…. agv

lae inflasie

Ook is ons verbruikers in `n beter posisie…. agv laer rentekoerse

Stygende motorverkope

Soeke na “yield”

Die rand verstewig

Betalingsbalans is egter steeds kwesbaar

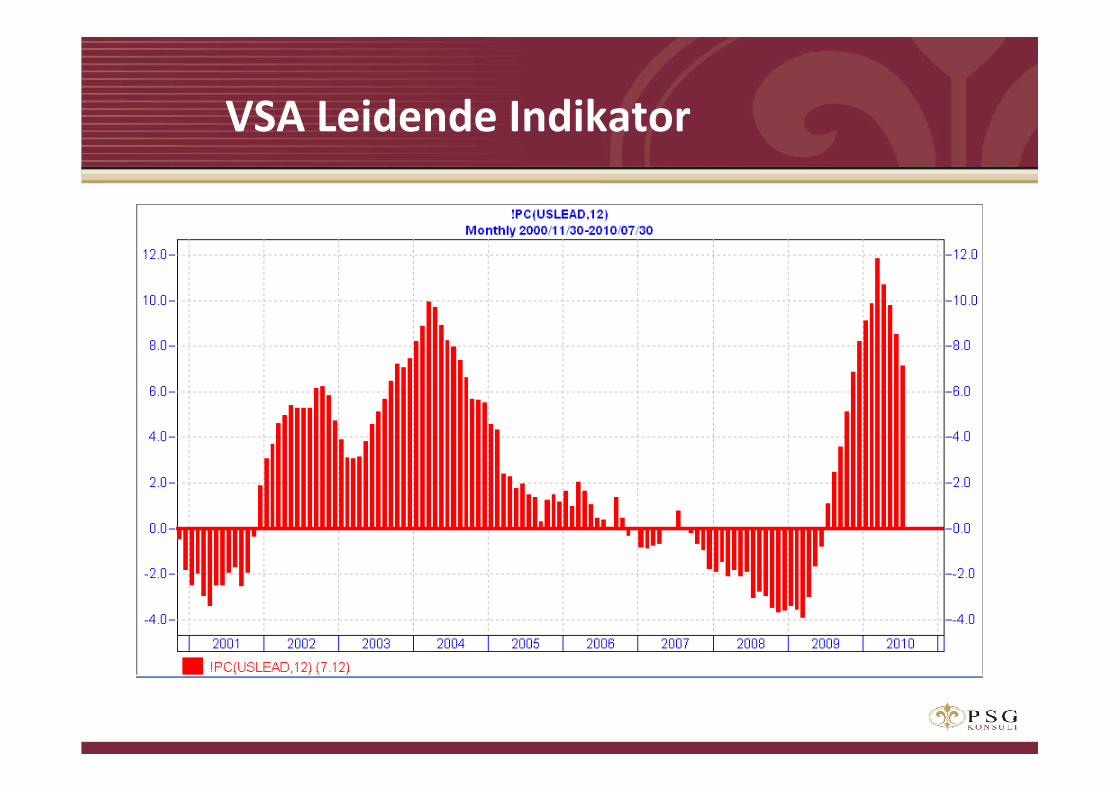

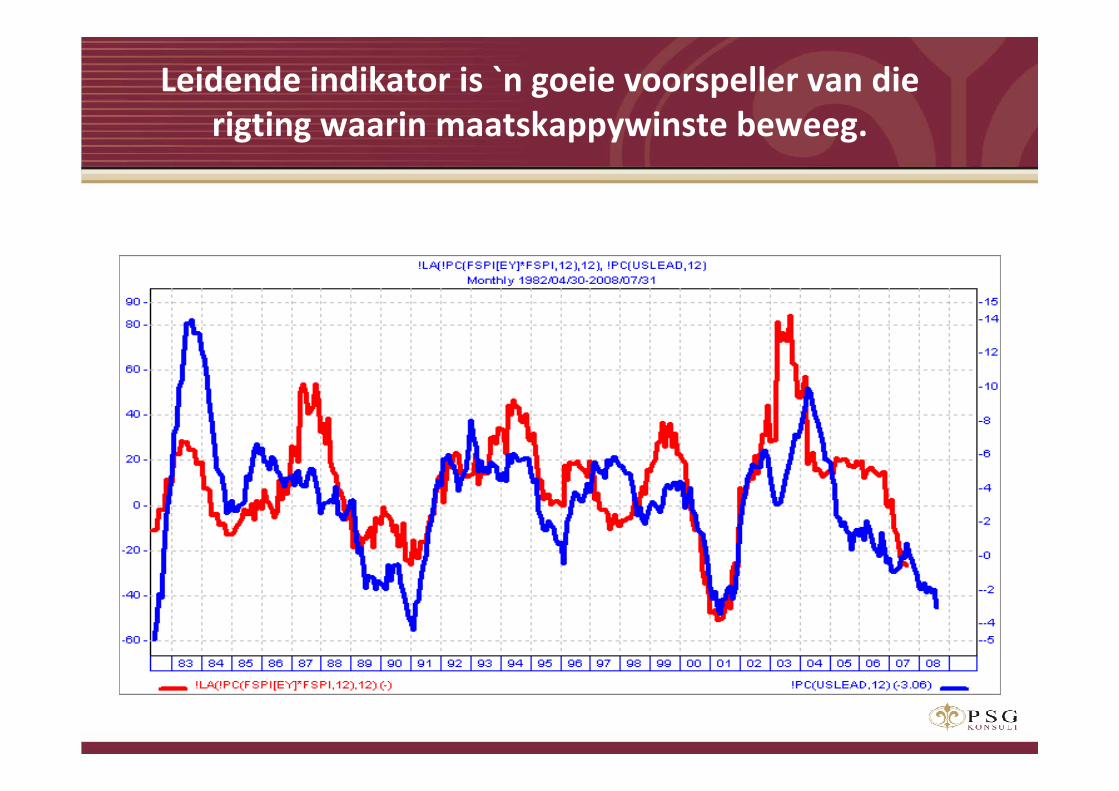

VSA Leidende Indikator

Leidende indikator is `n goeie voorspeller van die

rigting waarin maatskappywinste beweeg.

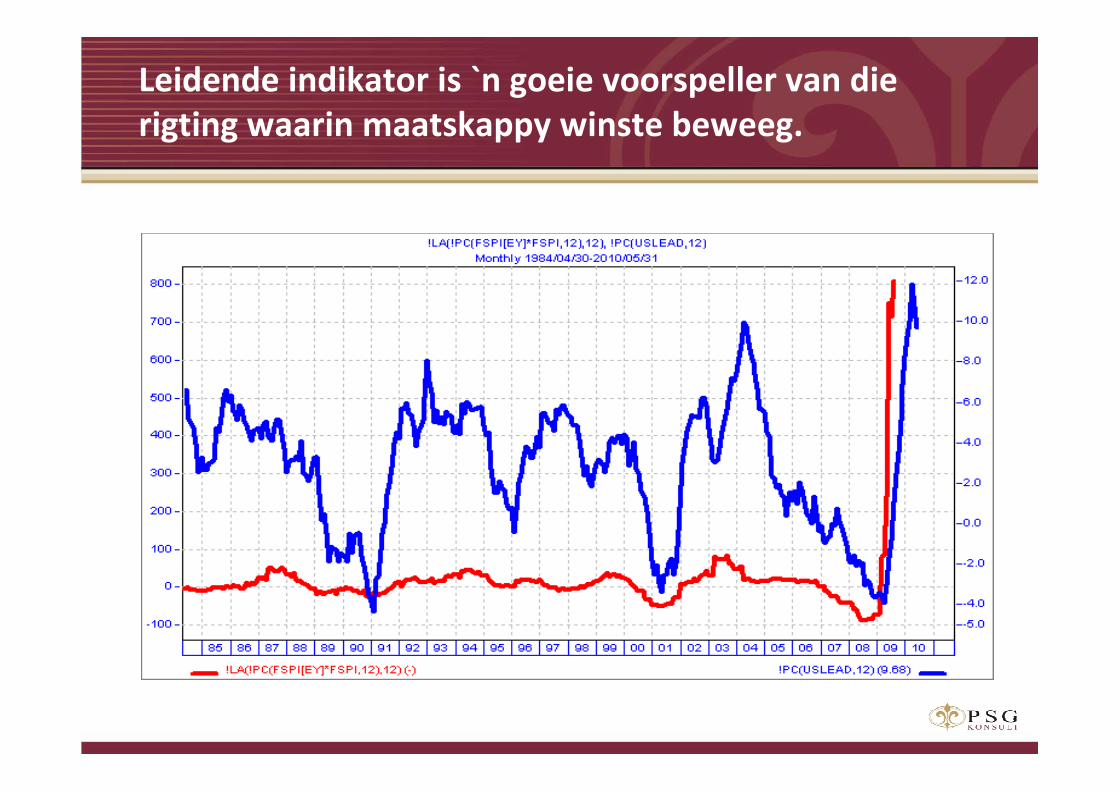

Leidende indikator is `n goeie voorspeller van die

rigting waarin maatskappy winste beweeg.

SA: Winste kan herstel; +40%

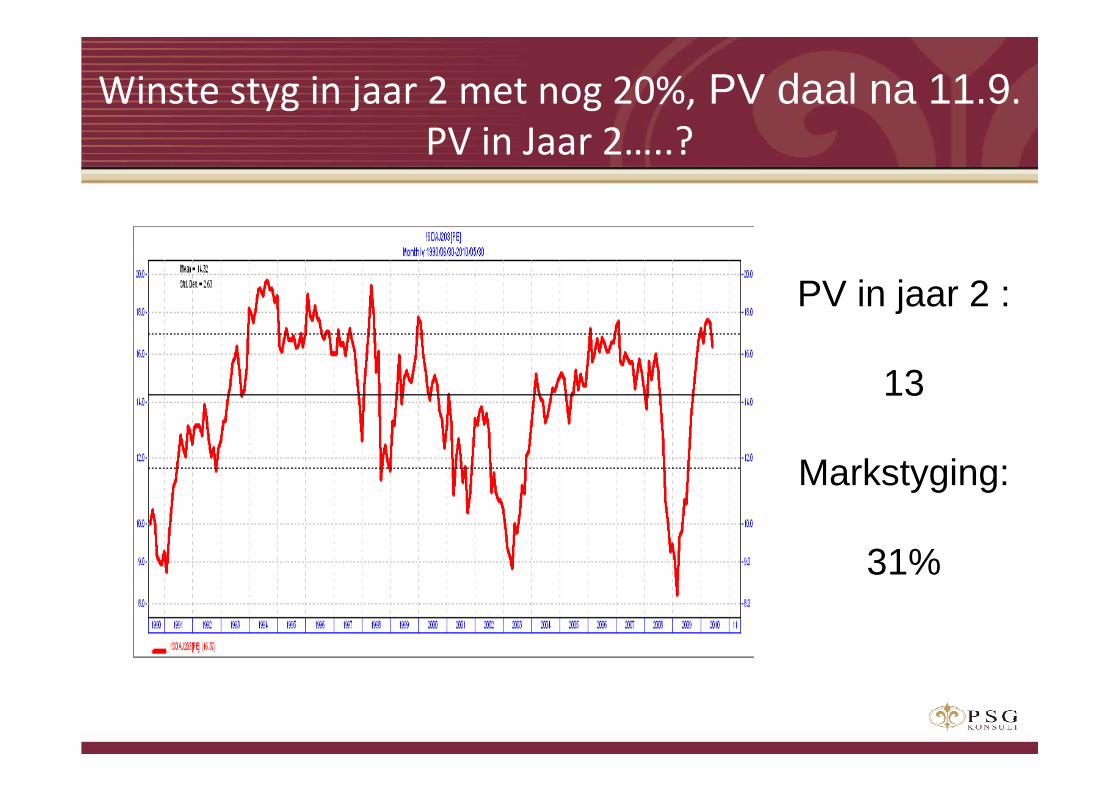

Winste styg in jaar 2 met nog 20%, PV daal na 11.9.

PV in Jaar 2…..?

PV in jaar 2 :

13

Markstyging:

31%

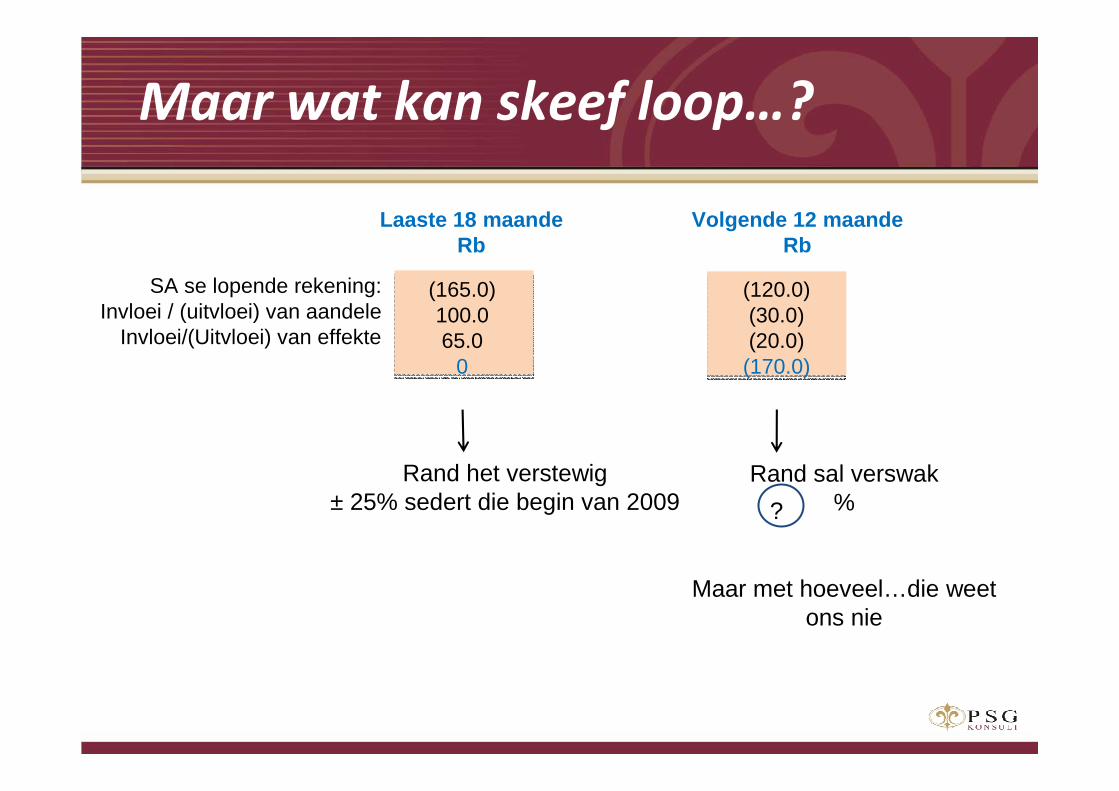

Maar wat kan skeef loop…?

Laaste 18 maandeRb

Volgende 12 maandeRb

(120.0)(30.0)(20.0)

(170.0)

(165.0)100.065.0

0

SA se lopende rekening:Invloei / (uitvloei) van aandele

Invloei/(Uitvloei) van effekte

Rand het verstewig± 25% sedert die begin van 2009

Rand sal verswak%

Maar met hoeveel…die weetons nie

?

Ter opsomming dus…

• Ek dink `n “double dip” resessie in die VSA is onwaarskynlik…

• maar dat die ekonomie wel stadig sal groei

• In die omstandighede het maatskappye tog daarin geslaag om hulle

winste sterk te groei

• en dit het die VSA beurs goedkoop gemaak

• Plaaslik het die politieke klimaat die afgelope maand versleg en

sou mens kon verwag dat die rand moes verswak het (SA se

soewereine risiko neem toe)…

• maar agv die sogenaamde “carry trade” het dit nog nie gebeur nie.

En kan die rand eers sterker word

• Sou die situasie (aantreklikheid van die “carry trade”) verander is

die rand baie kwesbaar.

• Maak dus seker dat u genoeg buitelandse bates of randverskansers

het.

Aandeelportefeuljes

Leon Ferreira

Braaivleisvure en

aandelemarkte

Braaivleisvure en aandelemarkte

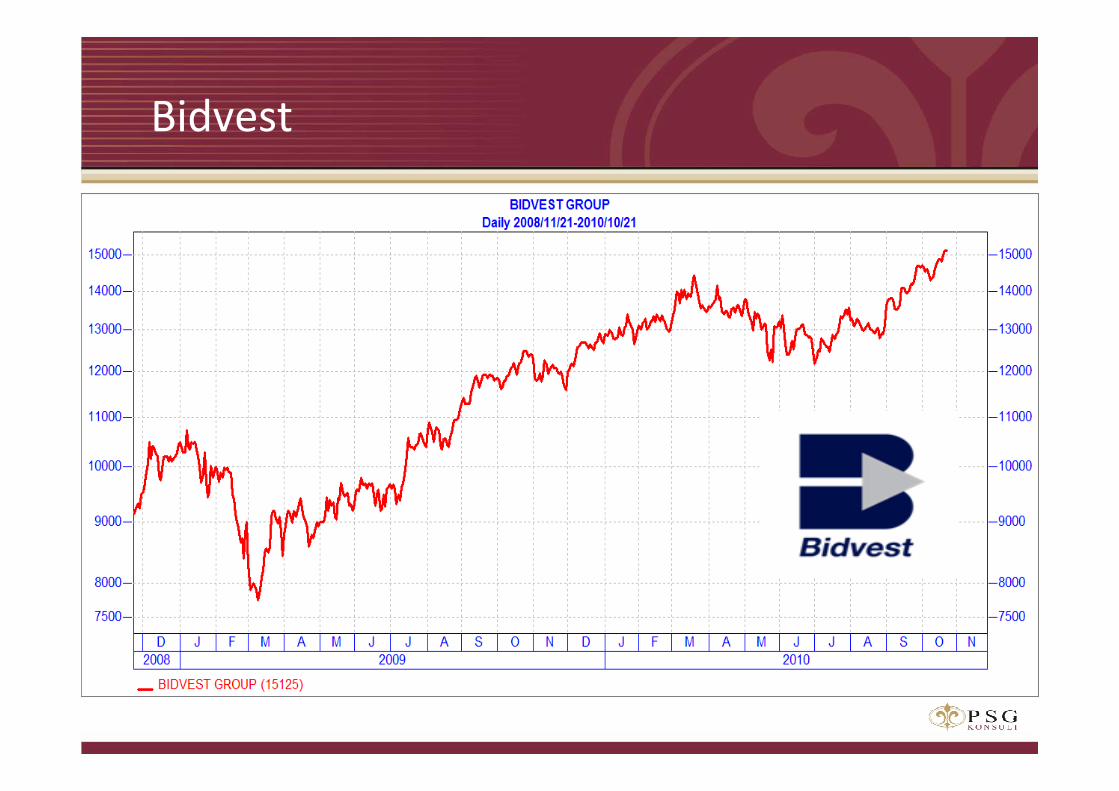

• Groei ten spyte van die resessie – omset > R100 miljard

• Voedseldienste grootste bydrae tot wins 36%

• Randverskanser 35% van wins kom uit oorsese bedrywighede

• Herstel potensiaal Bid Auto (McCarthy)

• Moontlike ontbondeling sal verder waarde ontlok

• Vooruit prysverdienste van 12.5

• Dividendopbrengs van 3.2%

Bidvest

Bidvest

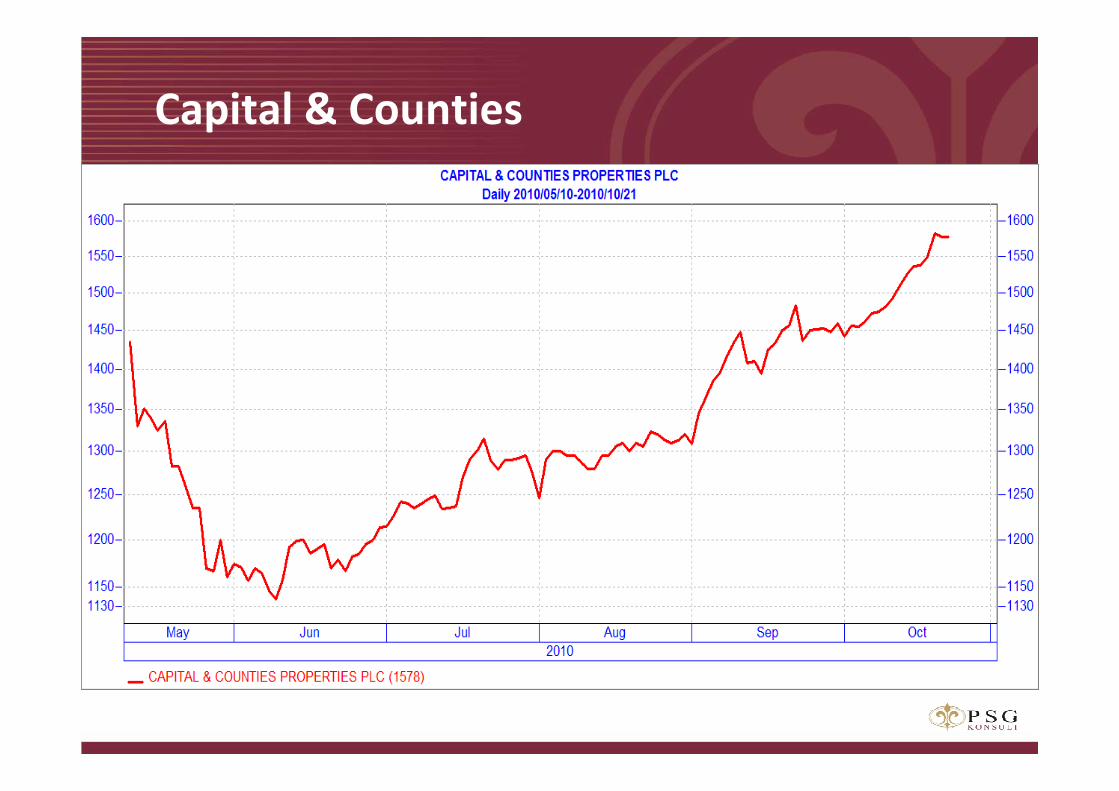

Capital & Counties

Capital & Counties

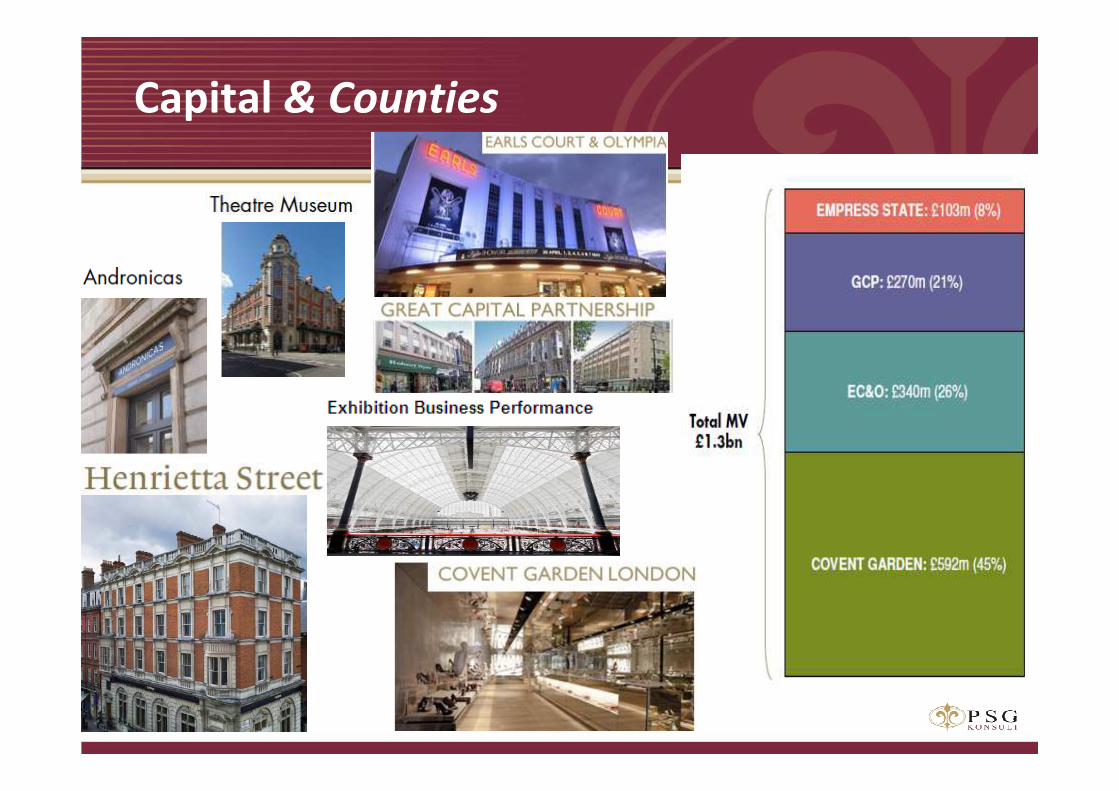

• Lae rentekoerse ondersteun plaaslike eiendom

• MAAR eiendomswaarde in VK is 36% laer as in 2007

• Sterk balansstaat – gebruik kontant vir opgraderings

• Opgraderings skep addisionele waarde

• Hersonering van eiendomme skep verdere waarde

• Waarde sal ontsluit vir langtermynbeleggers

Capital & Counties

• Prys styg 72% sedert begin 2010

• Sterk blootstelling aan Capitec (60% van markwaarde)

• Paladin Capital verdubbel sedert notering (PSG besit 87%)

• Pioneer Foods styg 125% sedert 2009 laagtepunt – ten spyte

van mededingendheidsboete

• Groot aandag op Curro skole op medium en langtermyn

PSG Group

• Wins herstel – oorsese chemiese afdelings

• Aanvang van produksie – Qatar GTL

• Hoogs sensitief vir die wisselkoers: elke 10c beweging

in die rand lei tot ʼn R615mil beweging op bedryfswins

• 2010 VPA 17% na R26.28 & Dividend 20% na R10.5

• Prysverdienste van 10.9

• Dividendopbrengs van 3.5%

SASOL

SASOL

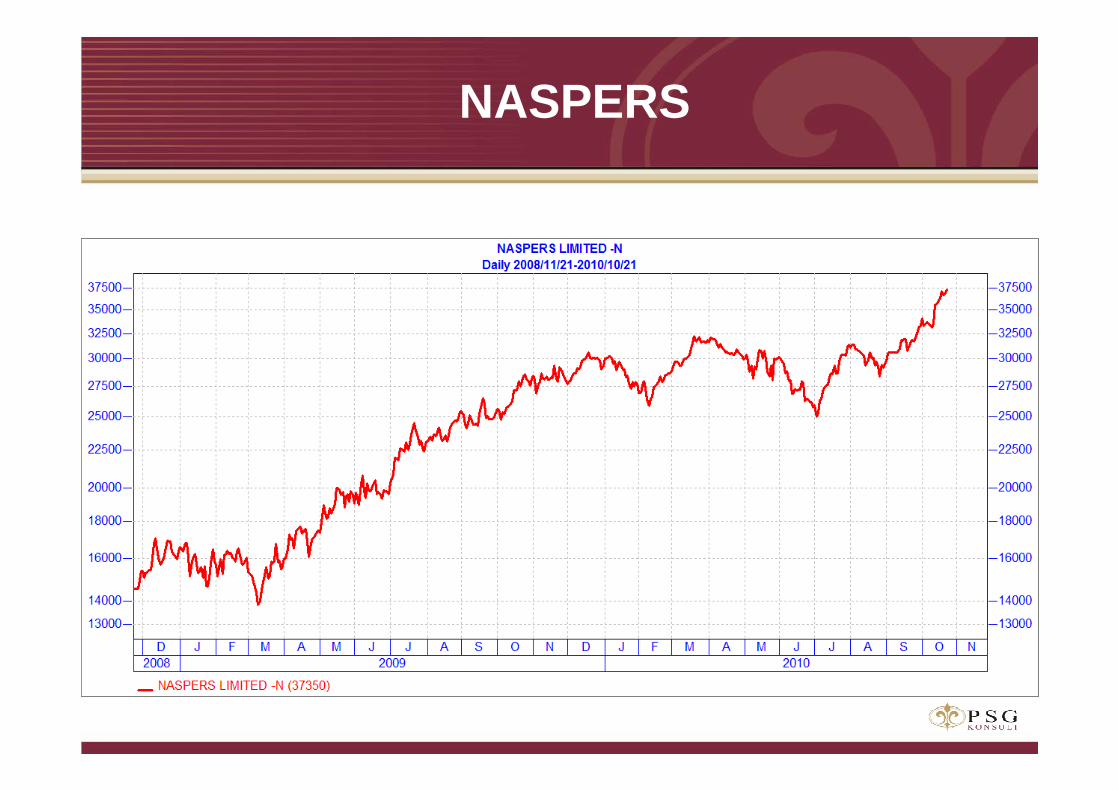

• Prys is 50% hoër sedert Tencent se regulatoriese skrik in Junie 2010

• Tencent het tans 600 miljoen kliente (Naspers besit 36%)

• Mail.ru notering op die Micex in Moscow (29% belang)

• Ander interessante belange in Allegro en Gadu-Gadu in Oos-Europa

• Verdere belange in Brasilië, Thailand, Wes-Europa, Indië,

Maleisië, die Filippyne en Afrika (Multichoice)

• Prysverdienste van 40, duur

• Dividendopbrengs van 0.6%

• Is daar enige verdere groei potensiaal?

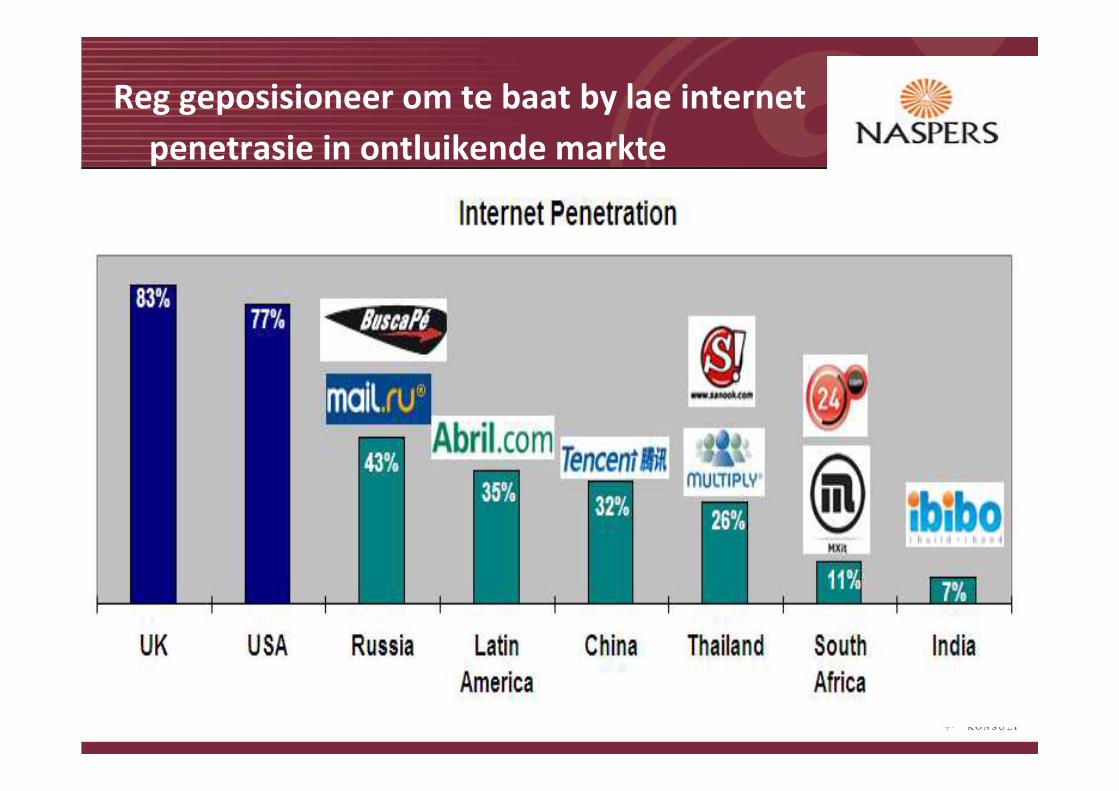

NASPERS

Reg geposisioneer om te baat by lae internet

penetrasie in ontluikende markte

NASPERS

• Prys styg 25% na goeie resultate in September

• Sterk balansstaat en kontantvloei generering

• Goed geposisioneer vir oornames

• Sterk groei in markaandeel

• Vinnigste groeiende sektor in die wêreld

• Groei VPA jaarliks met ± 20% al sedert 2000

• Prysverdienste van 9.0, steeds aantreklik

• Dividendopbrengs van 2.5%

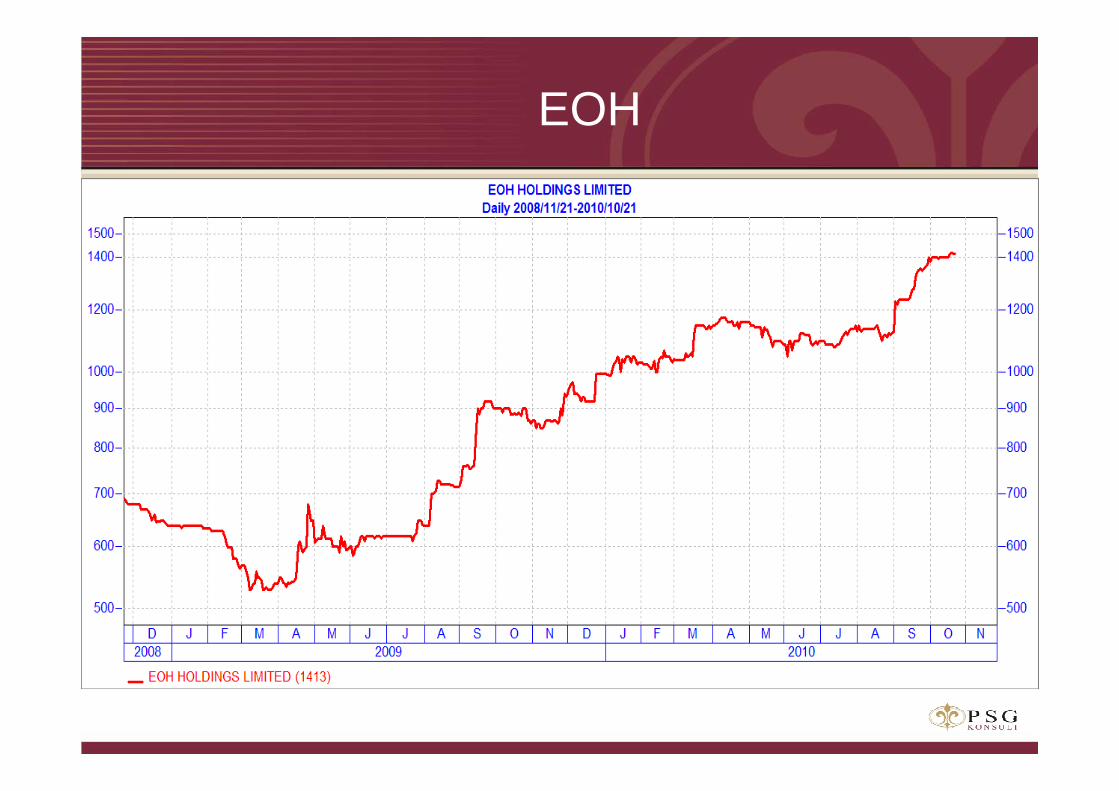

EOH

EOH

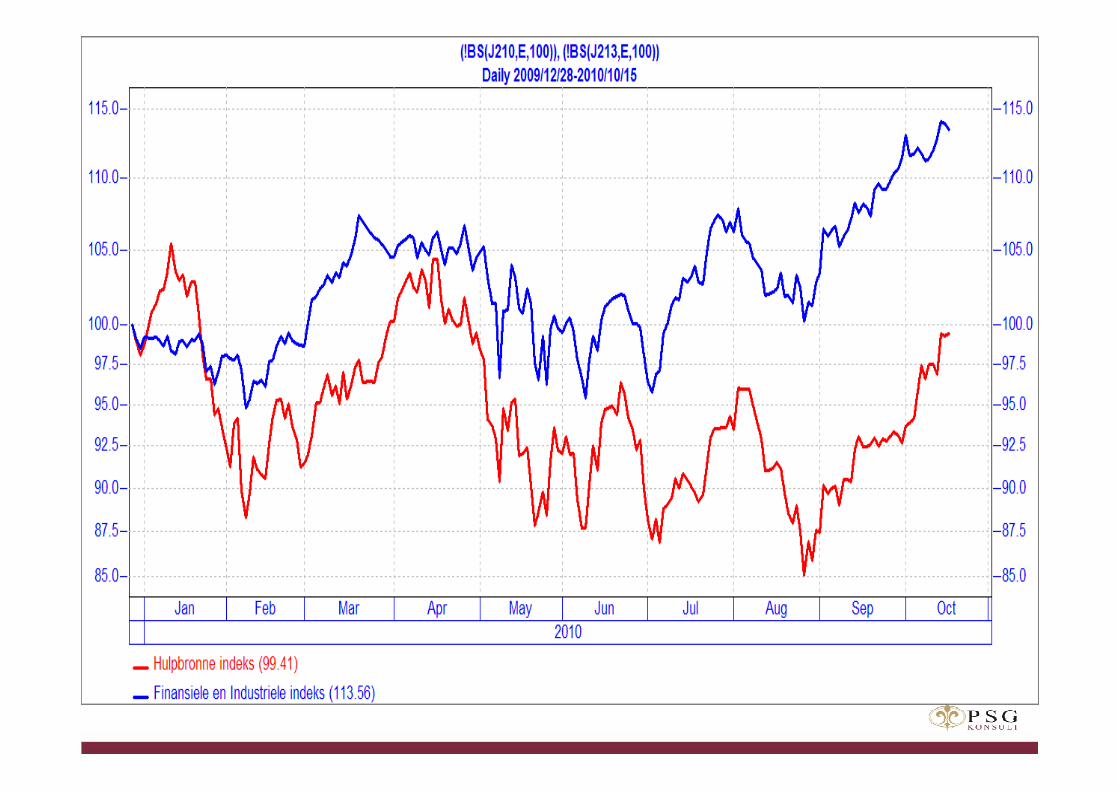

Hulpbronaandele

• Hulpbronne onderpresteer met 15% sedert Januarie

• Swakker dollar en groei uit China het sektor uit die

wegspringblokke gekry

• Bevestiging van sterk verdienstegroei is belangrik op die

mediumtermyn om pryse hoër te dryf

• Verkies Billiton, Anglo, Exxaro en Petmin

Go West East young man

Chris Wehmeyer

Shanghai Expo

Shanghai Expo

Shanghai Expo

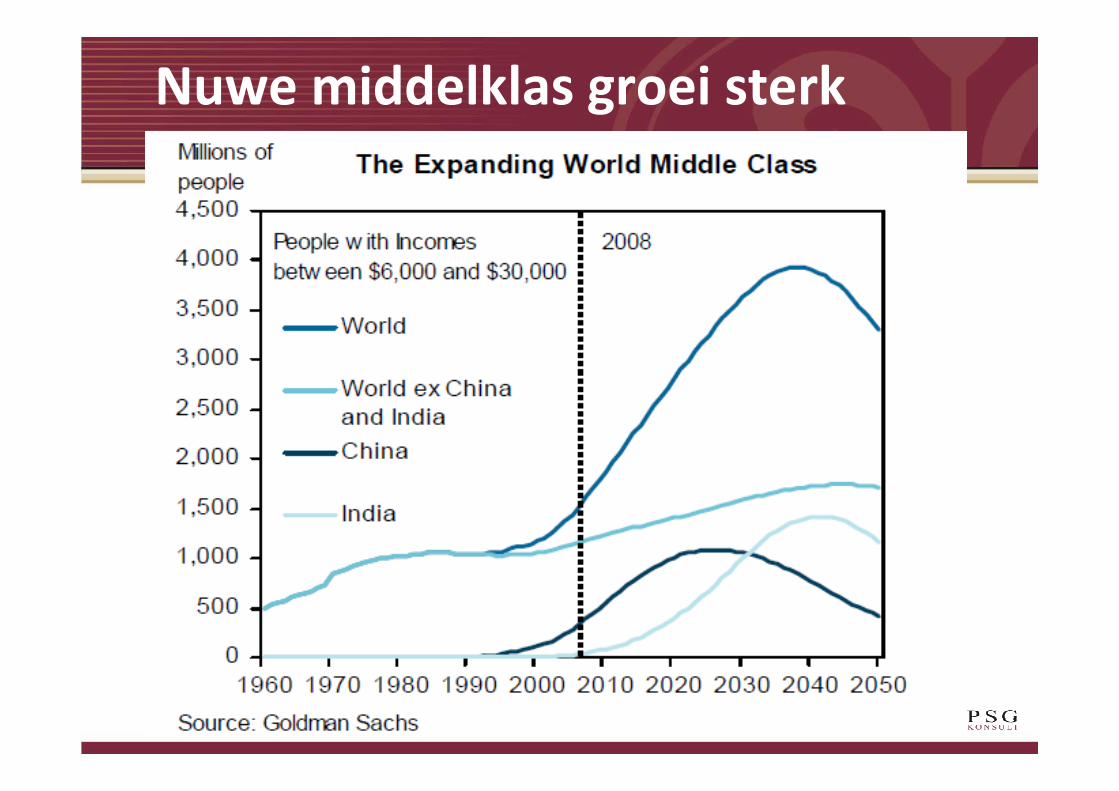

Nuwe middelklas groei sterk

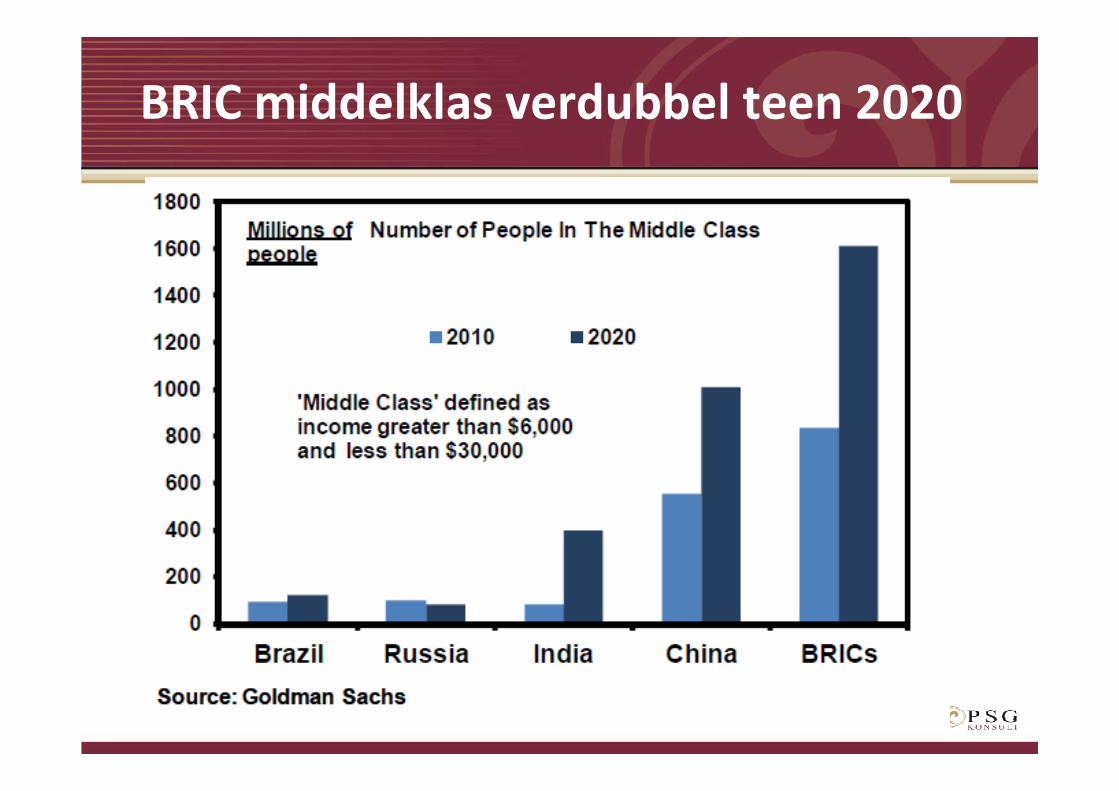

BRIC middelklas verdubbel teen 2020

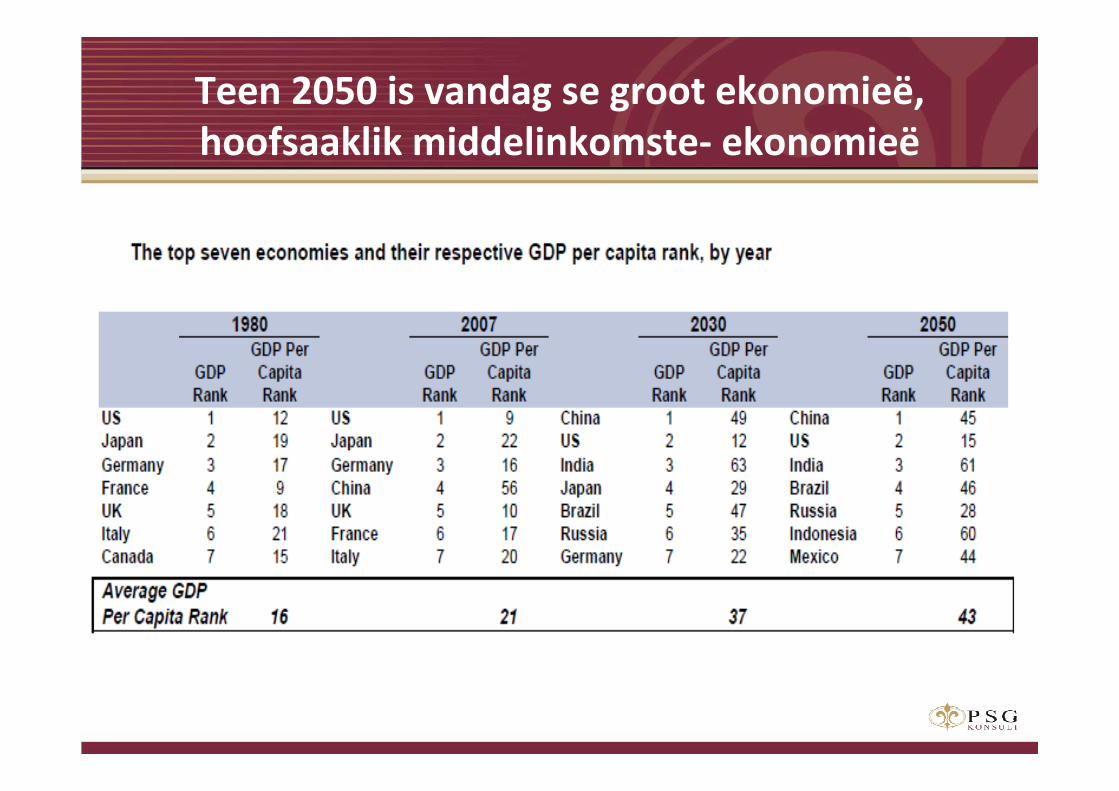

Teen 2050 is vandag se groot ekonomieë,

hoofsaaklik middelinkomste- ekonomieë

Wie is

bekommerd

oor kieme

in die huis?

Badseep

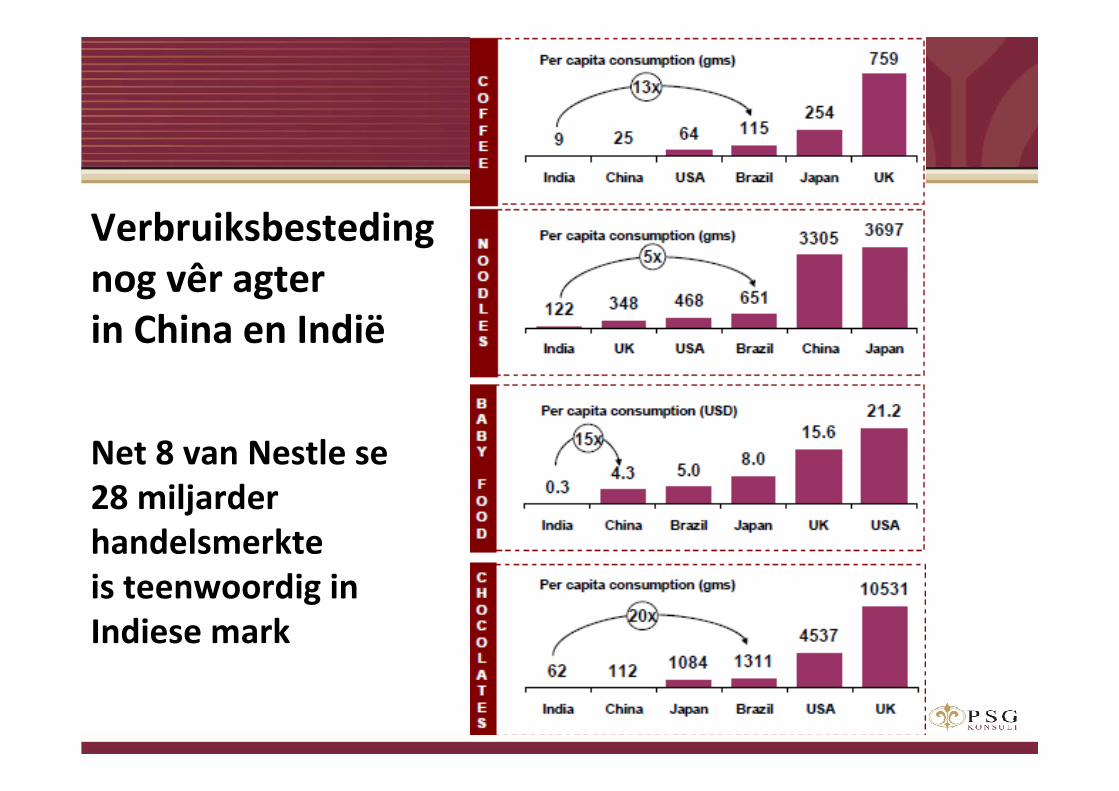

Verbruiksbesteding

nog vêr agter

in China en Indië

Net 8 van Nestle se

28 miljarder

handelsmerkte

is teenwoordig in

Indiese mark

Ontluikende markblootstelling

• British American Tobacco 60%

• Coca Cola 50%

• Philip Morris 46%

• Unilever 52%

• Nestlé 35%

• Novartis 34%

• Reckitt Benckiser 24%

Handelsmerke is kern

Handelsmerke van €1 miljard en meerUnilever plc

Miljard dollar handelsmerkeNestlé

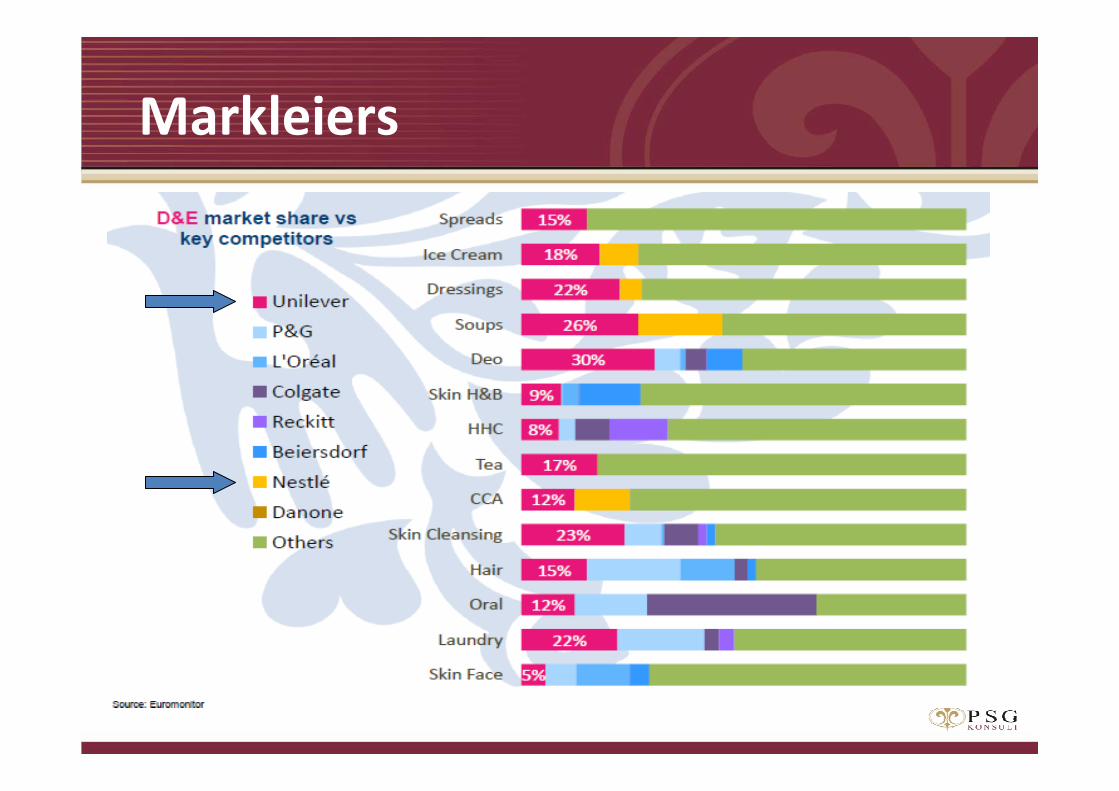

Markleiers

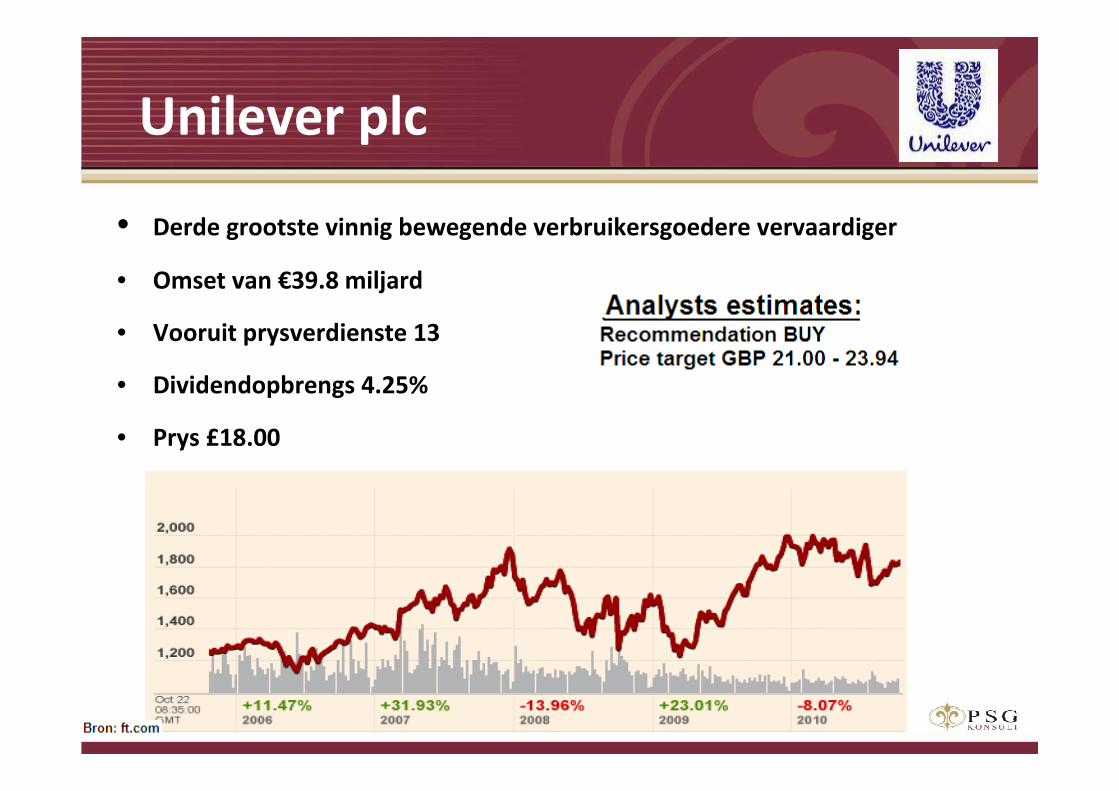

Unilever plc

• Derde grootste vinnig bewegende verbruikersgoedere vervaardiger

• Omset van €39.8 miljard

• Vooruit prysverdienste 13

• Dividendopbrengs 4.25%

• Prys £18.00

Nestlé

• Wêreld se grootste voedselvervaardiger

• Omset van USD 102.8 miljard

• Vooruit prysverdienste 16

• Dividendopbrengs 3%

• Prys CHF 54.00

Plaaslike voedselmaatskappye

• Tiger Brands – 13.1 p/v

• AVI – 15.1 p/v

• Pioneer Foods – 18.5 p/v

• Remgro 15.4 p/v

(25% belang in Unilever SA en Israel)

Hoekom buitelandse maatskappye?

• Goeie waardasies

• Blootstelling aan ander eerste wêreld en

ontluikende markte

• Gebruik sterk rand nou om goeie buitelandse

maatskappye te koop

Die pad na herstelLeon Ferreira

Oktober 2010

PSG KONSULT FONDS VAN FONDSE PRESTASIE30 SEPTEMBER 2010

Beleggingsfilosofie

Kontant

Kontant*Eiendom*Aandele

Aandele :

A Portefeulje van besighede

INKOMSTE

WELVAART BESKERMINGWELVAART SKEPPING

PRESERVER FoF &

MODERATE FoF

CREATOR FoF &

INTERNATIONAL FoFGeldmark

Inkomste FoF TYD

OPBRENGS

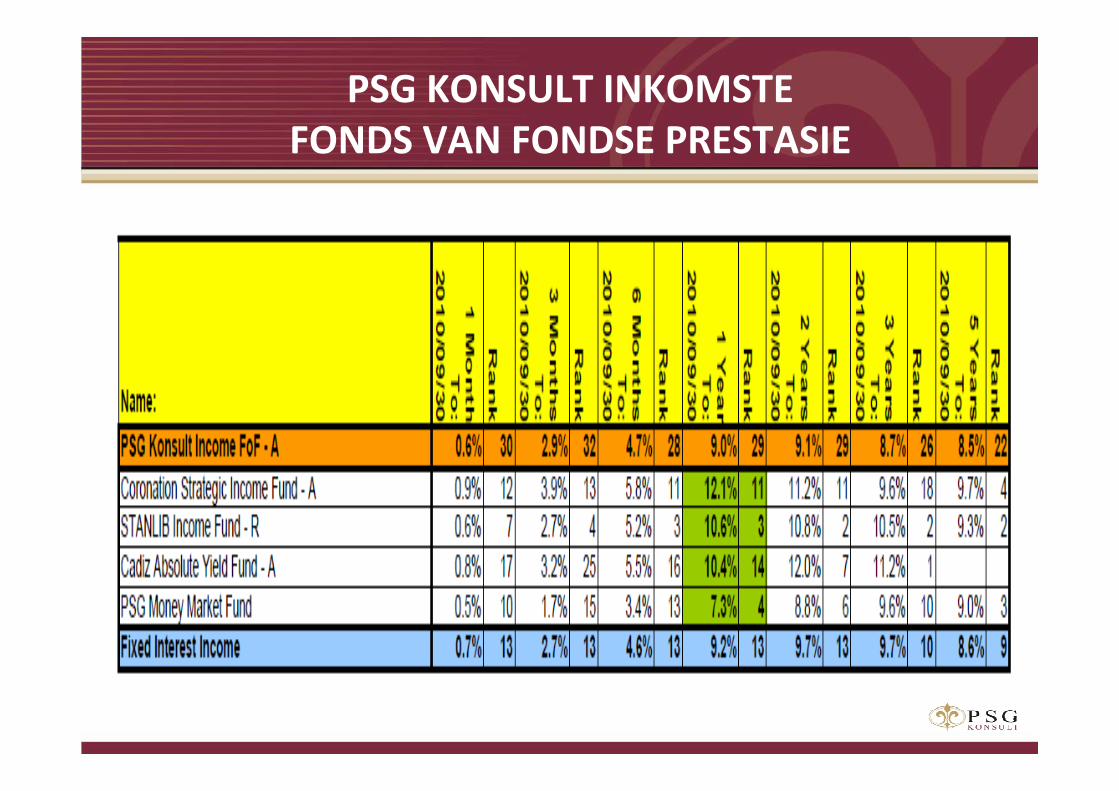

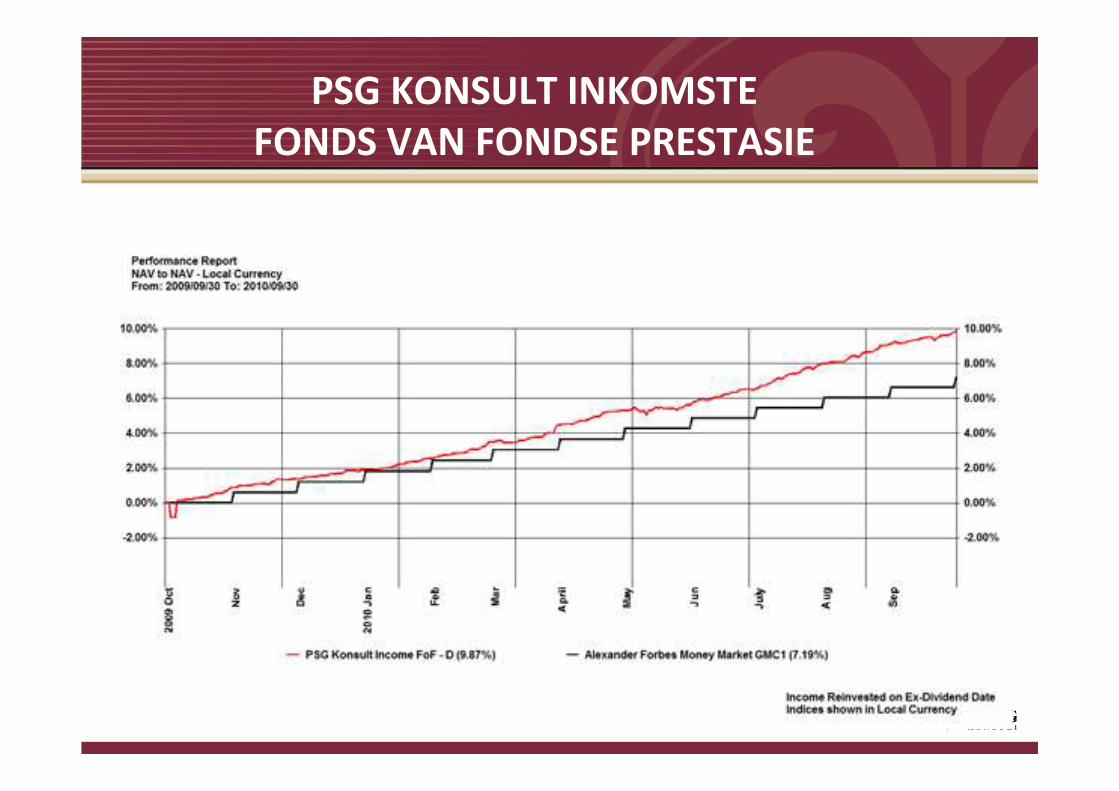

PSG KONSULT INKOMSTE

FONDS VAN FONDSE PRESTASIE

PSG KONSULT INKOMSTE

FONDS VAN FONDSE PRESTASIE

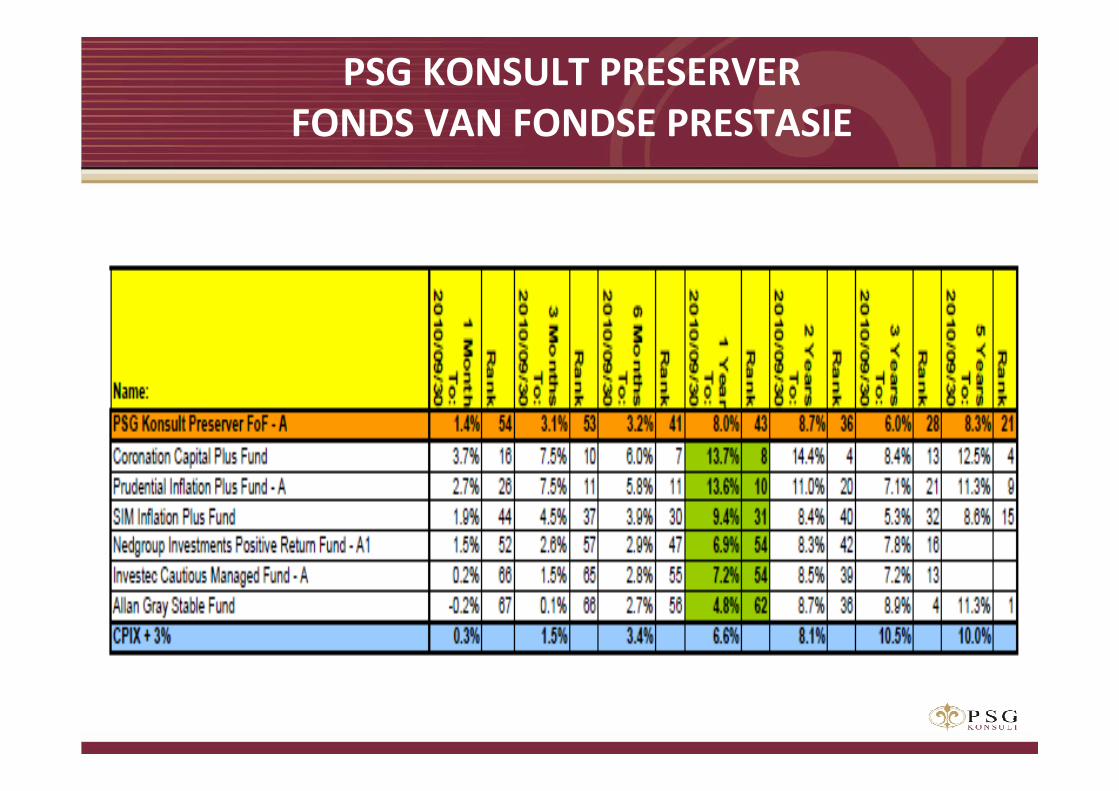

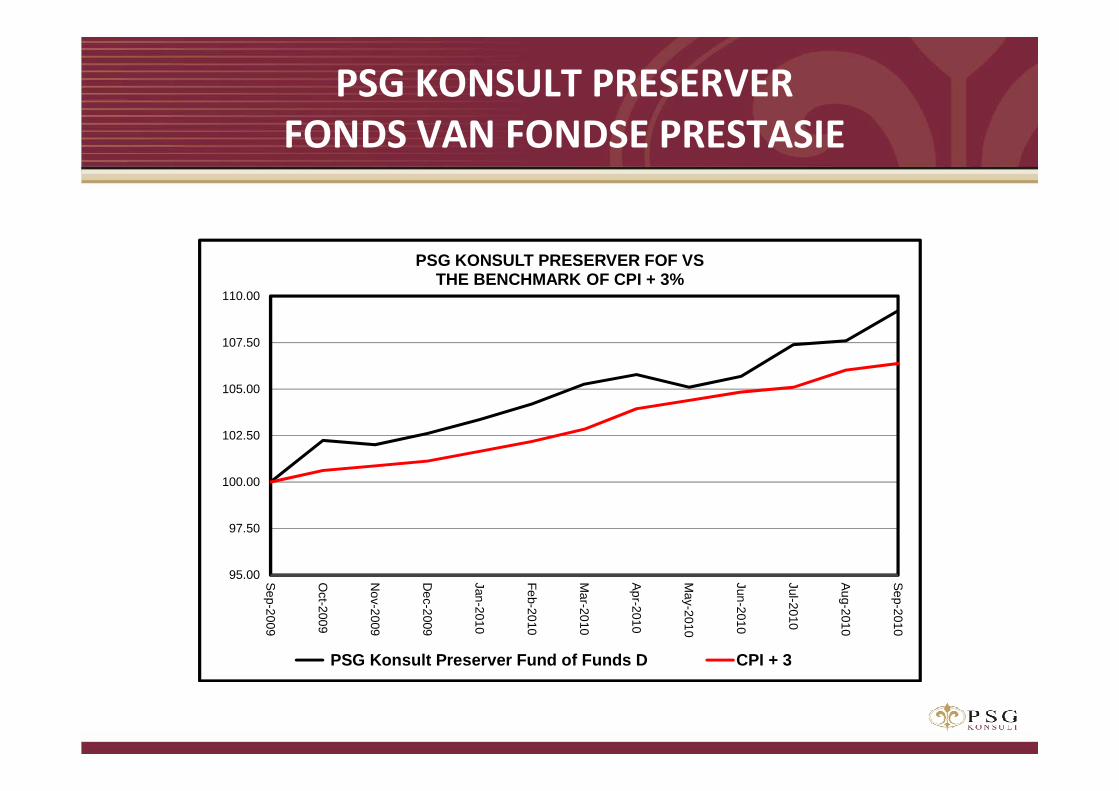

PSG KONSULT PRESERVER

FONDS VAN FONDSE PRESTASIE

PSG KONSULT PRESERVER

FONDS VAN FONDSE PRESTASIE

95.00

97.50

100.00

102.50

105.00

107.50

110.00

Sep-2009

Oct-2009

Nov-2009

Dec-2009

Jan-2010

Feb-2010

Mar-2010

Apr-2010

May-2010

Jun-2010

Jul-2010

Aug-2010

Sep-2010

PSG KONSULT PRESERVER FOF VS THE BENCHMARK OF CPI + 3%

PSG Konsult Preserver Fund of Funds D CPI + 3

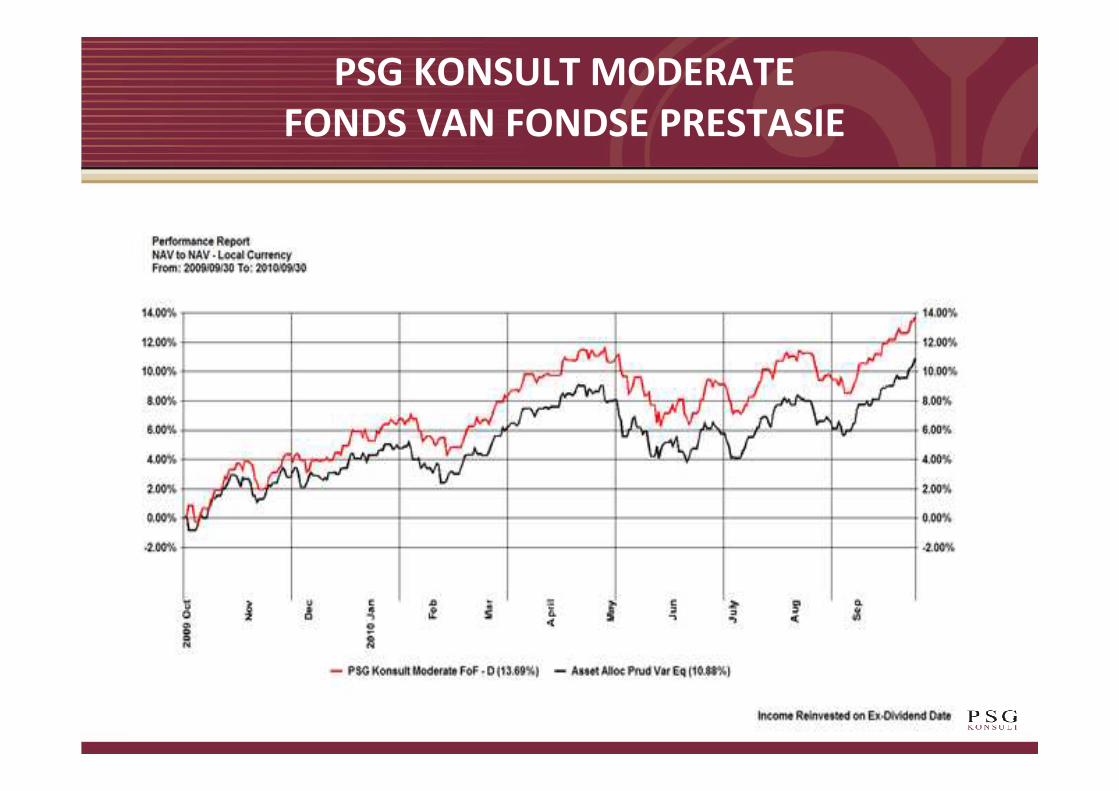

PSG KONSULT MODERATE

FONDS VAN FONDSE PRESTASIE

PSG KONSULT MODERATE

FONDS VAN FONDSE PRESTASIE

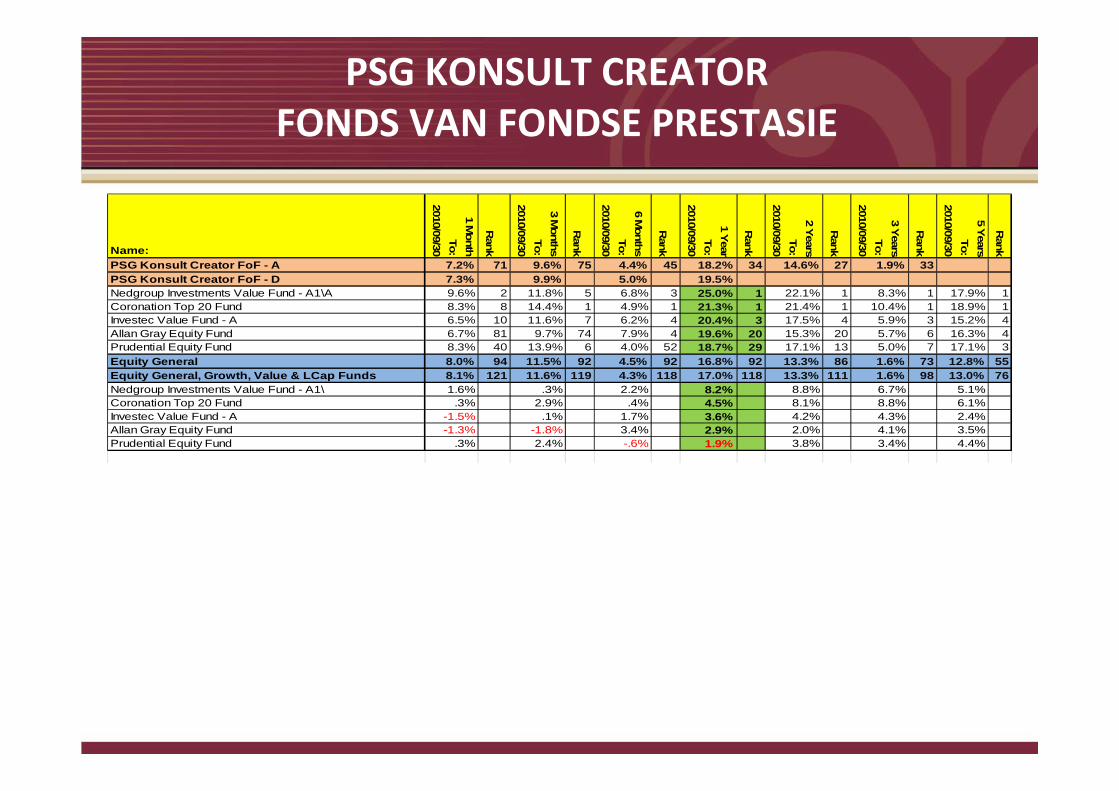

PSG KONSULT CREATOR

FONDS VAN FONDSE PRESTASIE

Name:

1 Month

To:

2010/09/30

Rank

3 Months

To:

2010/09/30

Rank

6 Months

To:

2010/09/30

Rank

1 Year

To:

2010/09/30

Rank

2 Years

To:

2010/09/30

Rank

3 Years

To:

2010/09/30

Rank

5 Years

To:

2010/09/30

Rank

PSG Konsult Creator FoF - A 7.2% 71 9.6% 75 4.4% 45 18.2% 34 14.6% 27 1.9% 33PSG Konsult Creator FoF - D 7.3% 9.9% 5.0% 19.5%Nedgroup Investments Value Fund - A1\A 9.6% 2 11.8% 5 6.8% 3 25.0% 1 22.1% 1 8.3% 1 17.9% 1Coronation Top 20 Fund 8.3% 8 14.4% 1 4.9% 1 21.3% 1 21.4% 1 10.4% 1 18.9% 1Investec Value Fund - A 6.5% 10 11.6% 7 6.2% 4 20.4% 3 17.5% 4 5.9% 3 15.2% 4Allan Gray Equity Fund 6.7% 81 9.7% 74 7.9% 4 19.6% 20 15.3% 20 5.7% 6 16.3% 4Prudential Equity Fund 8.3% 40 13.9% 6 4.0% 52 18.7% 29 17.1% 13 5.0% 7 17.1% 3Equity General 8.0% 94 11.5% 92 4.5% 92 16.8% 92 13.3% 86 1.6% 73 12.8% 55Equity General, Growth, Value & LCap Funds 8.1% 121 11.6% 119 4.3% 118 17.0% 118 13.3% 111 1.6% 98 13.0% 76Nedgroup Investments Value Fund - A1\ 1.6% .3% 2.2% 8.2% 8.8% 6.7% 5.1%Coronation Top 20 Fund .3% 2.9% .4% 4.5% 8.1% 8.8% 6.1%Investec Value Fund - A -1.5% .1% 1.7% 3.6% 4.2% 4.3% 2.4%Allan Gray Equity Fund -1.3% -1.8% 3.4% 2.9% 2.0% 4.1% 3.5%Prudential Equity Fund .3% 2.4% -.6% 1.9% 3.8% 3.4% 4.4%

Equity Value 8.2% 10 11.9% 10 5.2% 10 19.5% 10 17.6% 10 5.1% 10 15.6% 8Equity Growth 8.0% 5 11.9% 5 4.2% 5 18.3% 5 11.2% 5 -0.6% 5 12.4% 5Equity Large Cap 8.8% 12 13.0% 12 2.3% 11 17.7% 11 12.9% 10 2.2% 10 14.5% 8Equity General 8.0% 94 11.5% 92 4.5% 92 16.8% 92 13.3% 86 1.6% 73 12.8% 55

BenchCoronation Equity Fund - A 8.3% 43 14.7% 2 6.7% 11 23.5% 4 17.7% 9 6.7% 5 15.6% 7Absa Select Equity Fund 8.6% 31 13.4% 13 6.6% 14 21.0% 12 20.3% 3 9.2% 2 19.1% 1Nedgroup Investments Growth Fund - A1 6.6% 5 9.6% 5 4.5% 3 20.8% 2 14.2% 2 0.7% 2 12.7% 2Prudential Dividend Maximiser Fund 7.8% 7 12.9% 3 3.9% 7 18.7% 5 17.9% 3 6.9% 2 17.6% 2Nedgroup Investments Rainmaker Fund - A1 8.1% 49 13.2% 16 6.7% 11 18.2% 33 14.5% 29 4.2% 14 14.4% 14PSG Equity Fund - A 9.4% 13 11.3% 51 7.2% 8 17.1% 47 15.7% 19 0.4% 50 11.5% 39Equity General 8.0% 94 11.5% 92 4.5% 92 16.8% 92 13.3% 86 1.6% 73 12.8% 55Coronation Equity Fund - A .3% 3.2% 2.2% 6.8% 4.4% 5.2% 2.8%Absa Select Equity Fund .6% 1.9% 2.1% 4.3% 7.0% 7.7% 6.3%Nedgroup Investments Growth Fund - A1 -1.4% -1.9% -.0% 4.0% .9% -.9% -.1%Prudential Dividend Maximiser Fund -.3% 1.4% -.7% 1.9% 4.6% 5.3% 4.9%Nedgroup Investments Rainmaker Fund - A1 .1% 1.7% 2.2% 1.4% 1.2% 2.6% 1.6%PSG Equity Fund - A 1.4% -.2% 2.6% .3% 2.4% -1.2% -1.3%

PSG KONSULT CREATOR

FONDS VAN FONDSE PRESTASIE

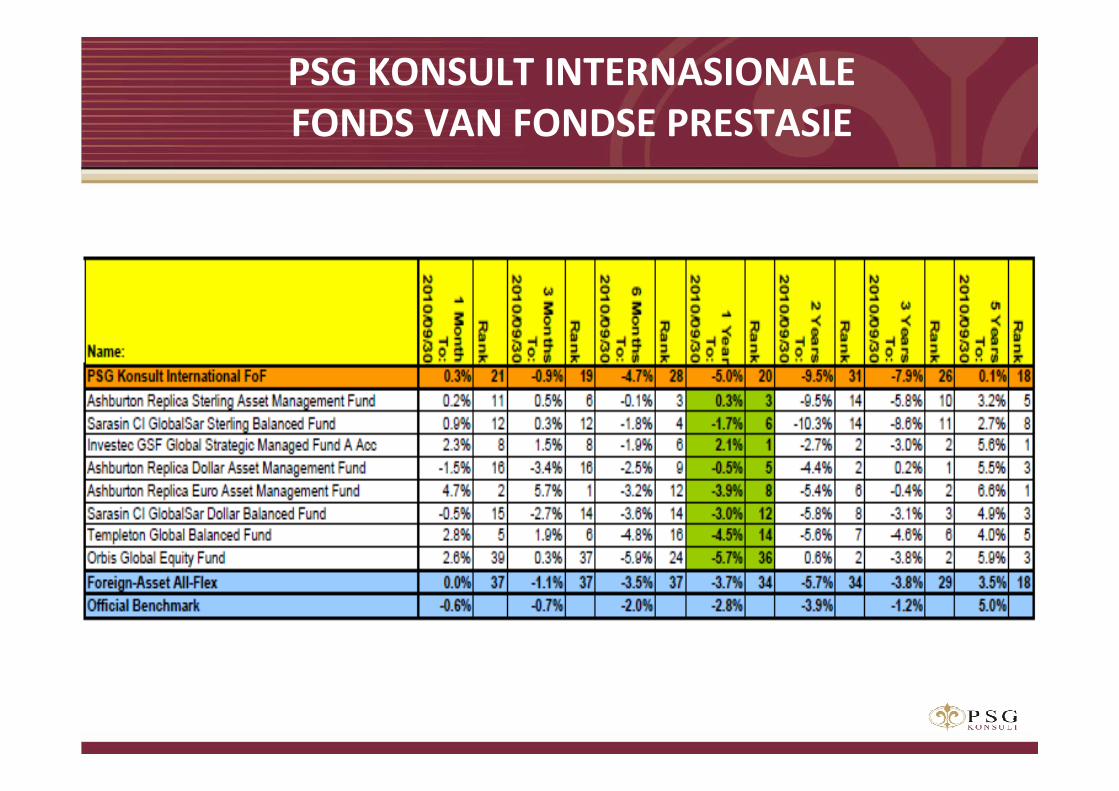

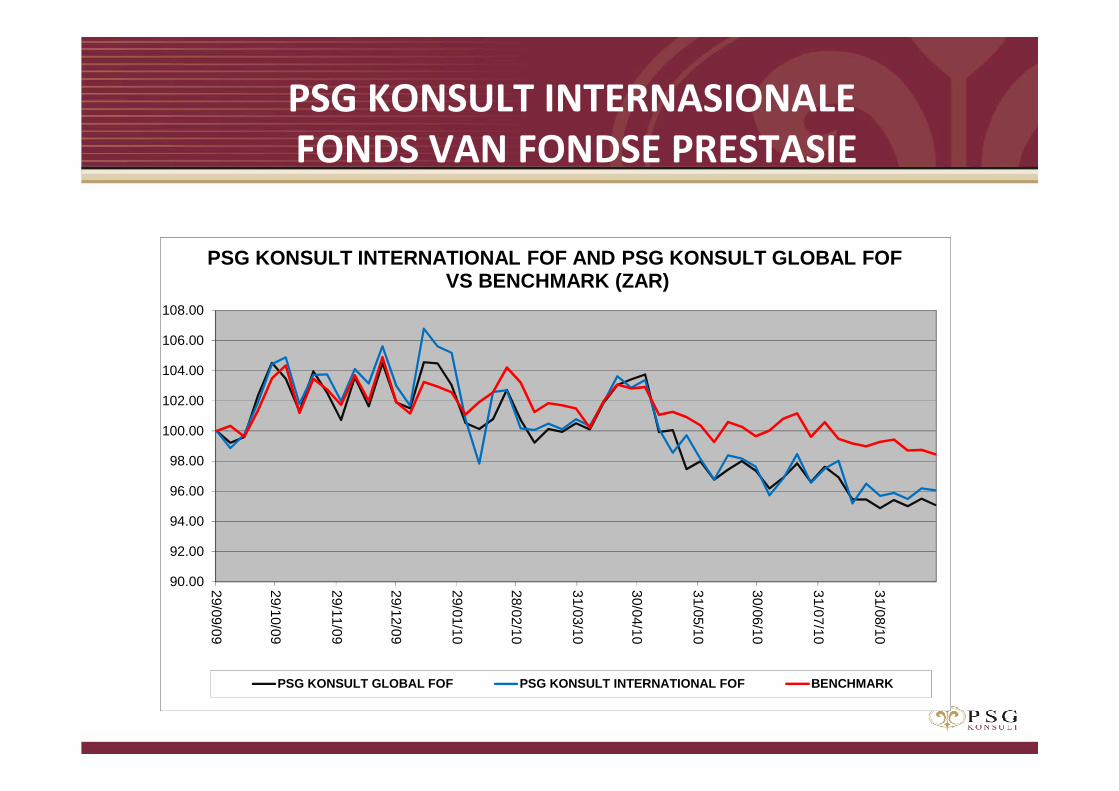

PSG KONSULT INTERNASIONALE

FONDS VAN FONDSE PRESTASIE

PSG KONSULT INTERNASIONALE

FONDS VAN FONDSE PRESTASIE

90.00

92.00

94.00

96.00

98.00

100.00

102.00

104.00

106.00

108.00

29/09/09

29/10/09

29/11/09

29/12/09

29/01/10

28/02/10

31/03/10

30/04/10

31/05/10

30/06/10

31/07/10

31/08/10

PSG KONSULT GLOBAL FOF PSG KONSULT INTERNATIONAL FOF BENCHMARK

PSG KONSULT INTERNATIONAL FOF AND PSG KONSULT GLOBA L FOFVS BENCHMARK (ZAR)

Hoe gebeur dit?

Johan Borcherds

Oktober 2010

Krion-7 gevonnis

Waar het dit alles begin?

“A Ponzi scheme is a fraudulent investment

operation that pays returns to separate

investors from their own money or money

paid by subsequent investors, rather than

from any actual profit earned.” - Wikipedia

- Vernoem na Charles Ponzi in 1920

- Oorspronklike skema gebaseer op arbitrasie

van internasionale betalings koepons vir

posseëls; beleggers se kapitaal naderhand

gebruik om betalings aan vroeëre beleggers

te ondersteun asook vir Ponzi se eie welvaart

Bekende Ponzi skemas

• “Kubus” skema – Adriaan Nieuwoudt (Januarie 1984)

• Bernard Madoff (Desember 2008) - $65 miljard

• Practical Property Portfolio (Januarie 2009) - £ 80 miljoen

Onlangse Suid-Afrikaanse skemas

• Tannenbaum R12 miljard

• Krion R1,5 miljard

• KingFin R680 miljoen

• Bluezone R270 miljoen

• Sharemax ???

“Financial Advisory and Intermediary Services Act”

Reguleer en verbeter verhouding tussenfinansiële adviseurs en hul kliënte

• “105 persone betrokke by toepassingsproses wat 13 875 sleutelindividue polisieer”

• “Geen blaf nie, geen byt nie, geen verrassing datgewetenlose operateurs genoeg vertroue het om die reguleerders die stryd aan te sê nie.”

- Marc Ashton; Artikel uit Finweek 21 Oktober 2010

Navorsing deur Prof Jan Venter

“An analysis of the expectation gap in the

personal financial services industry in South Africa”

studie deur Professor Jan Venter (professor in belasting aan Unisa)

as deel van sy PHD graad aan die Universiteit van Noordwes

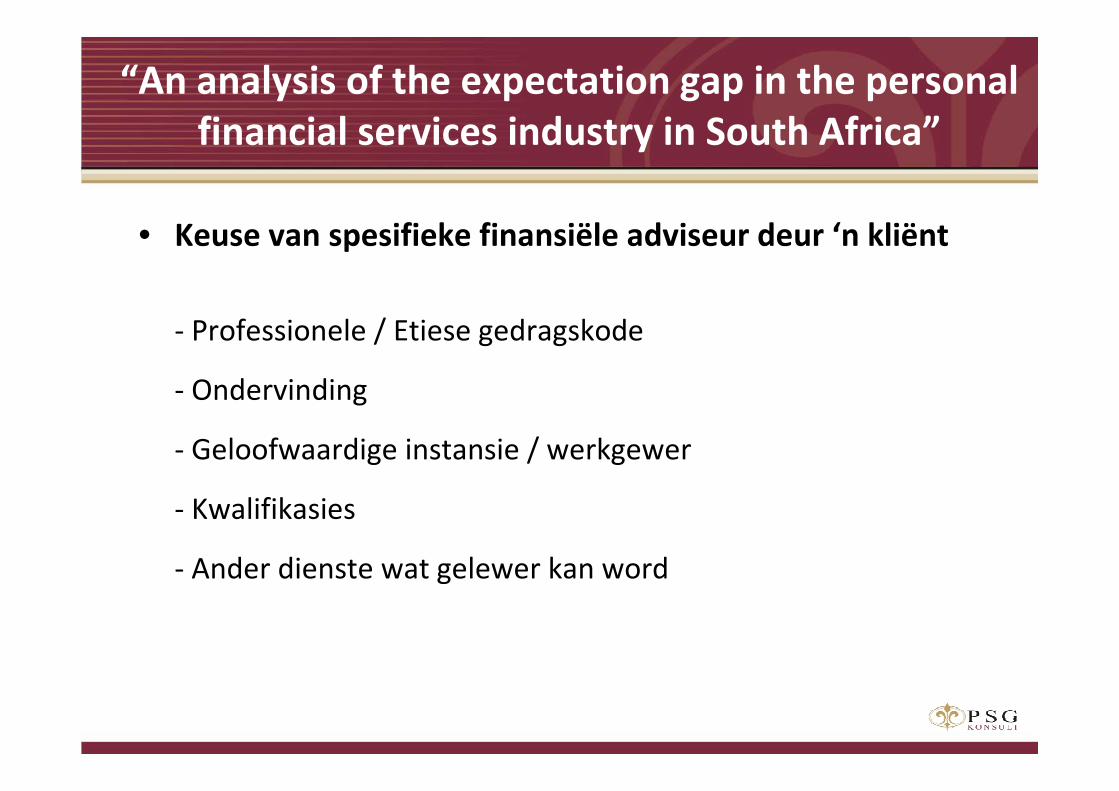

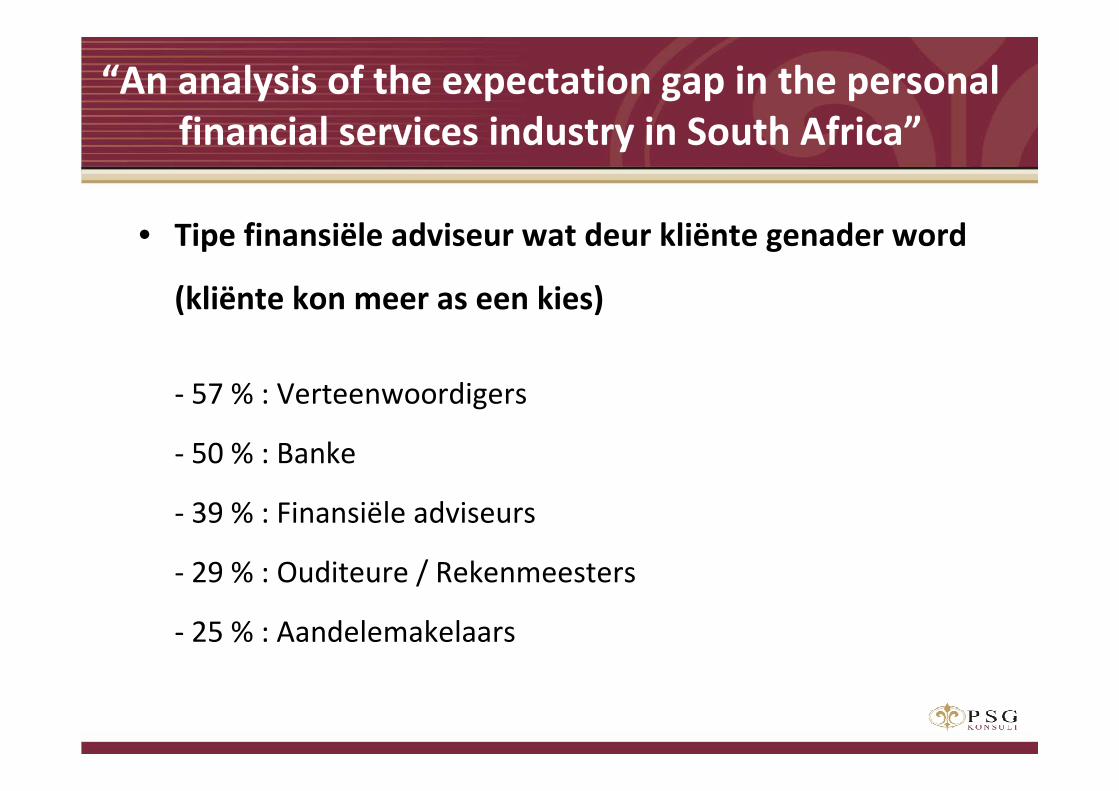

“An analysis of the expectation gap in the personal

financial services industry in South Africa”

• Keuse van spesifieke finansiële adviseur deur ‘n kliënt

- Professionele / Etiese gedragskode

- Ondervinding

- Geloofwaardige instansie / werkgewer

- Kwalifikasies

- Ander dienste wat gelewer kan word

• Tipe finansiële adviseur wat deur kliënte genader word

(kliënte kon meer as een kies)

- 57 % : Verteenwoordigers

- 50 % : Banke

- 39 % : Finansiële adviseurs

- 29 % : Ouditeure / Rekenmeesters

- 25 % : Aandelemakelaars

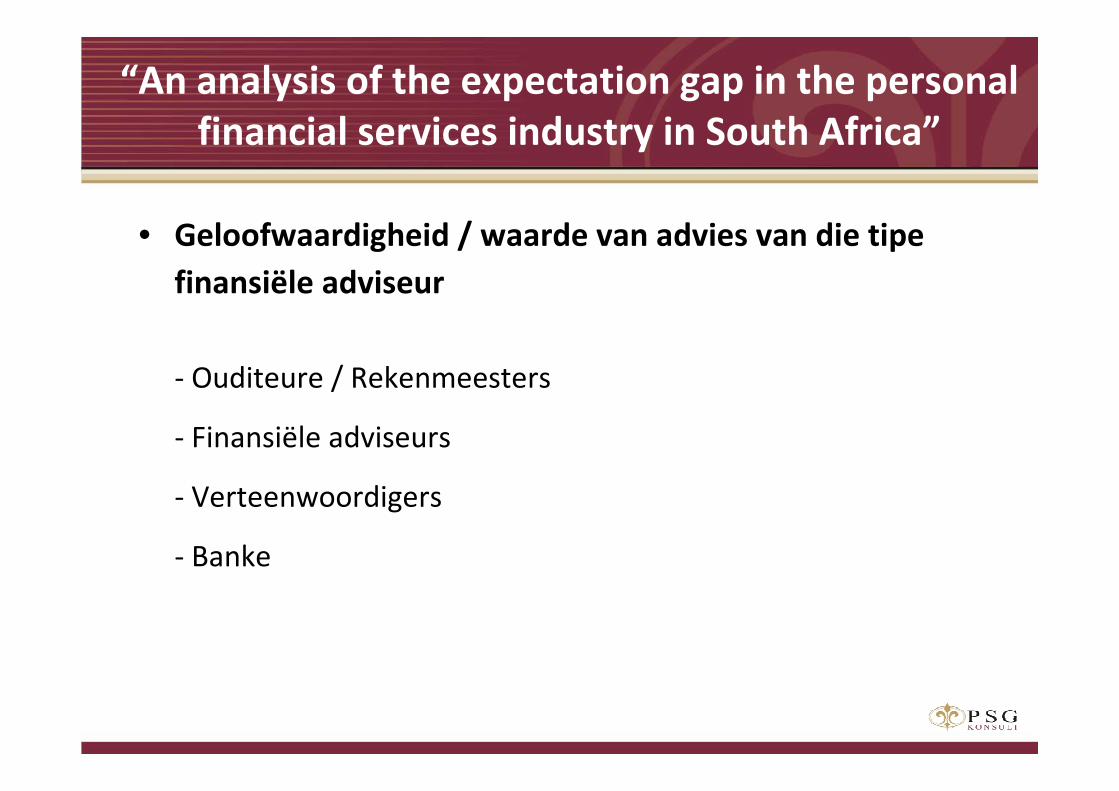

“An analysis of the expectation gap in the personal

financial services industry in South Africa”

• Geloofwaardigheid / waarde van advies van die tipe

finansiële adviseur

- Ouditeure / Rekenmeesters

- Finansiële adviseurs

- Verteenwoordigers

- Banke

“An analysis of the expectation gap in the personal

financial services industry in South Africa”

Die studie plaas baie klem op die vertrouensverhouding

tussen finansiële adviseur en kliënt.

Dit is ‘n verhouding wat gewoonlik oor jare opgebou word

maar kan ongelukkig ook misbruik word.

“An analysis of the expectation gap in the personal

financial services industry in South Africa”

Donald Rumsfeld

(voormalige VSA Minister van Verdediging)

“There are known knowns.

These are the things we know that we know.

There are known unknowns.

That is to say, there are things that we know we don’t know.

But there are also unknown unknowns.

These are things we don’t know we don’t know.”

Dr Christo Wiese – Mei 2010

“When confronted with incomplete data one often draws

incorrect conclusions and therefore people often think

they know more than they actually do know.”

Eienskappe van ‘n moontlike skema

(Lectric Law Library)

• Persone met gesofistikeerde verkoopstegnieke

• Senior burgers is gewoonlik die teiken

• Belofte van ‘n veilige belegging – jy kan nie verloor nie

• Belegging bied ongekende hoë rente of kapitaal groei

• Beleggers het gewoonlik min tyd om besluit te maak

Wat kan ek as belegger doen?

• Raak meer betrokke by jou finansiële sake

• Kies die regte adviseur

• Vertrou op geloofwaardige verwysings

• Verstaan die struktuur van jou beleggings

• Diversifiseer jou beleggings

• Volg ‘n konserwatiewe benadering rakende opbrengste

• Geen betalings aan verkoopspersoon

• Vertrou jou voorgevoel – moet nie belê as jy twyfel nie

Aanhaling van Langenhoven

“Dis nie swaar om die waarheid te praat nie.

Wat swaar is, is om jou gedrag so te hou dat die waarheid

binne jou vermoë bly”

Dankie

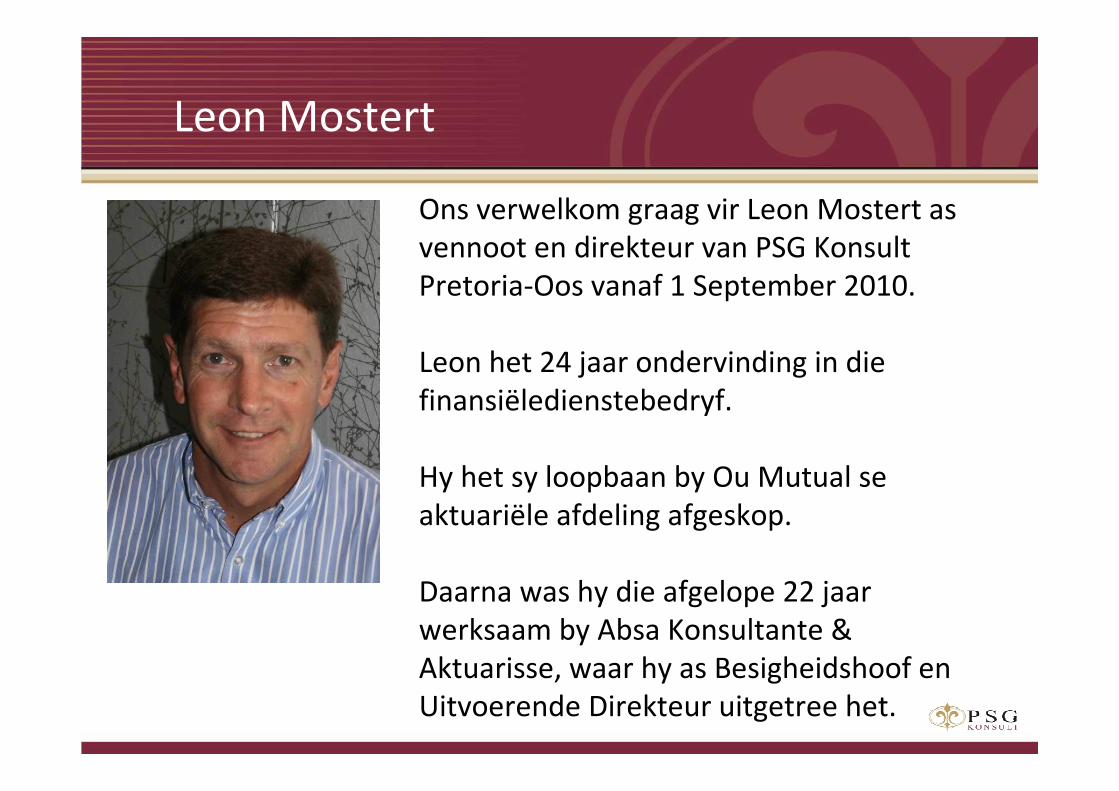

Leon Mostert

Ons verwelkom graag vir Leon Mostert as

vennoot en direkteur van PSG Konsult

Pretoria-Oos vanaf 1 September 2010.

Leon het 24 jaar ondervinding in die

finansiëledienstebedryf.

Hy het sy loopbaan by Ou Mutual se

aktuariële afdeling afgeskop.

Daarna was hy die afgelope 22 jaar

werksaam by Absa Konsultante &

Aktuarisse, waar hy as Besigheidshoof en

Uitvoerende Direkteur uitgetree het.

Drikus Combrinck werk byna vier

jaar as ‘n aandeelmakelaar en

leerling portefeuljebestuurder

saam met ons. Hy is ook ‘n CFA

kandidaat, voltooing van sodanige

kandidaatskap behoort ‘n verdiepte

element van kundigheid aan ons

kliente te bring

Drikus Combrinck

Ander dienste wat ons bied

• Fidusiêre Dienste (Trusts, Testamente en Boedelbeplanning) – Tian Ebersohn

• Lewensversekering en ander dekking(ongeskiktheid, gevreesde siekte)

• Korttermyn versekering - PSG Konsult Meesterplan

• Werknemersvoordele – Leon Mostert

PSG Konsult Pretoria-Oos

• 35 Persone

• 30 Grade

• Een doel : ‘n Ongeëwenaarde Beleggingservaring / Unequaled Investment Experience