Embed Size (px)

Citation preview

3- 1Outline 3: Risk, Return, and Cost of Capital

3.1 Rates of Return 3.2 Measuring Risk3.3 Risk & Diversification3.4 Measuring Market Risk3.5 Portfolio Betas3.6 Risk and Return3.7 CAPM and Expected Return3.8 Security Market Line3.9 Capital Budgeting and Project Risk3.10 Cost of Capital3.11 Weighted Average Cost of Capital (WACC)3.12 Capital Structure3.13 Required Rates of Return

3- 2

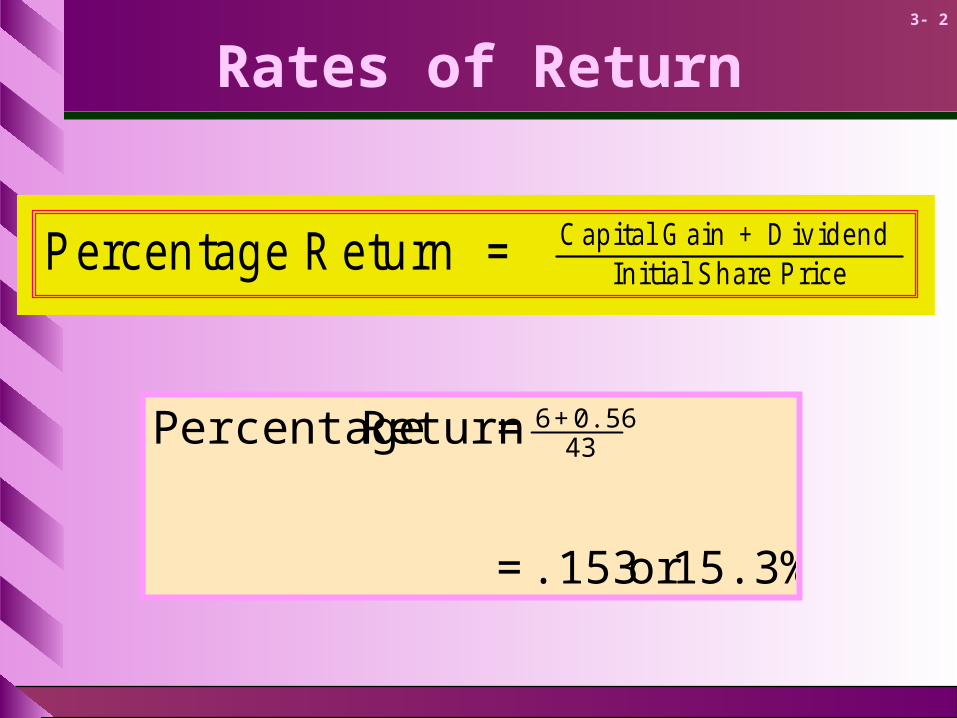

Rates of Return

15.3%or .153=

=Return Percentage 430.56 + 6

P e rc e n ta g e R e tu rn = C a p i ta l G a in + D iv id e n d In i t ia l S h a re P r ic e

3- 3

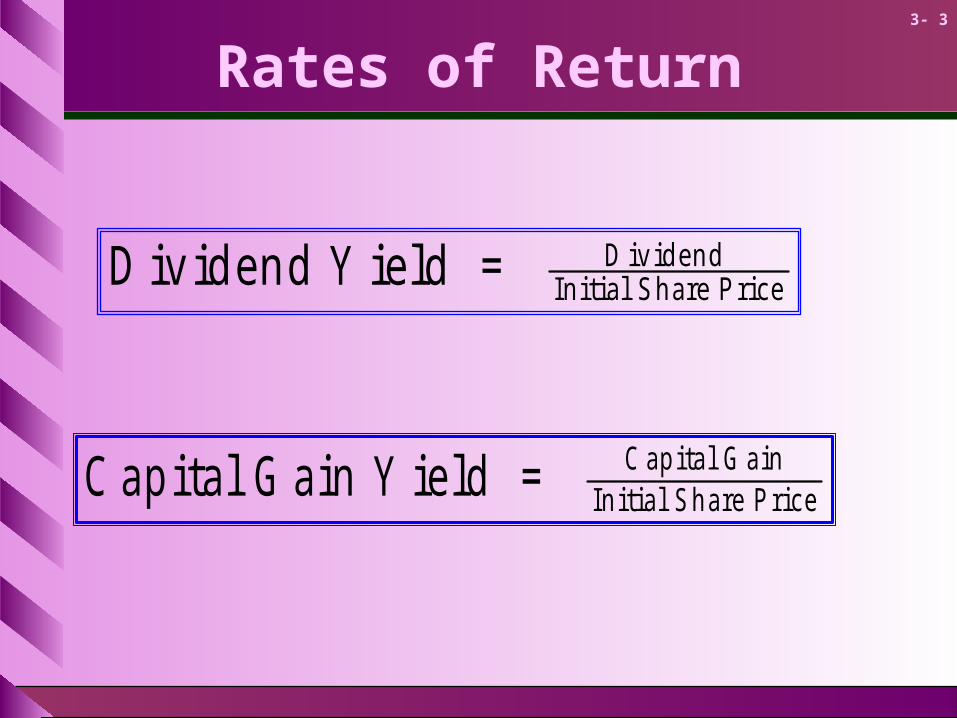

Rates of Return

D iv id e n d Y ie ld = D iv id e n d In i t ia l S h a re P r ic e

C a p i t a l G a in Y ie ld = C a p i t a l G a inIn i t i a l S h a r e P r i c e

3- 4

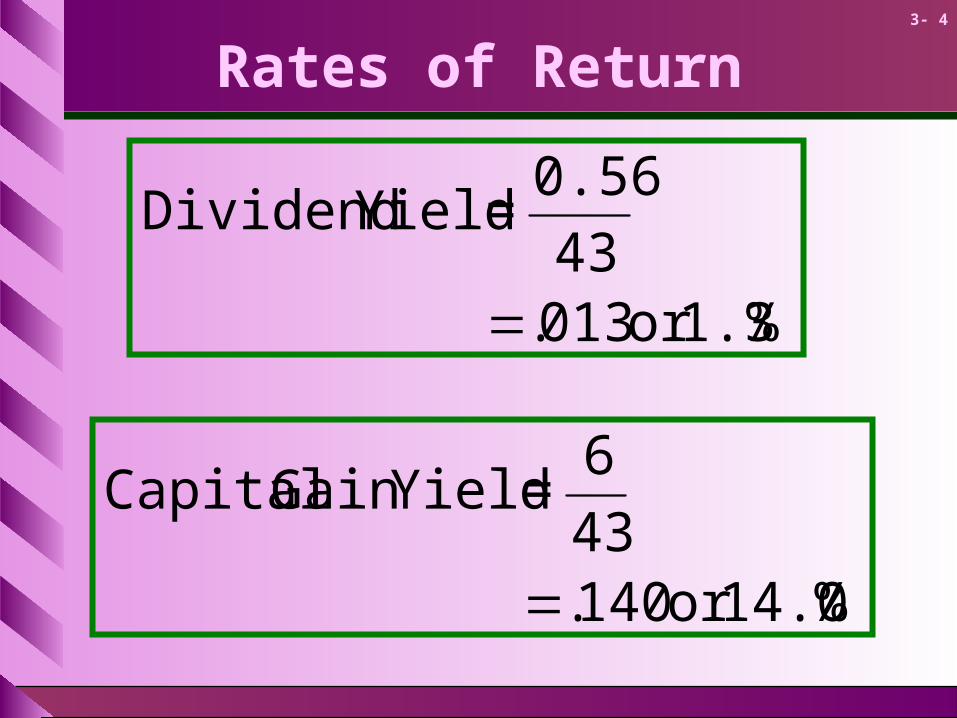

Rates of Return

%1.3or 013.43

0.56= Yield Dividend

%14.0or 140.43

6= YieldGain Capital

3- 5

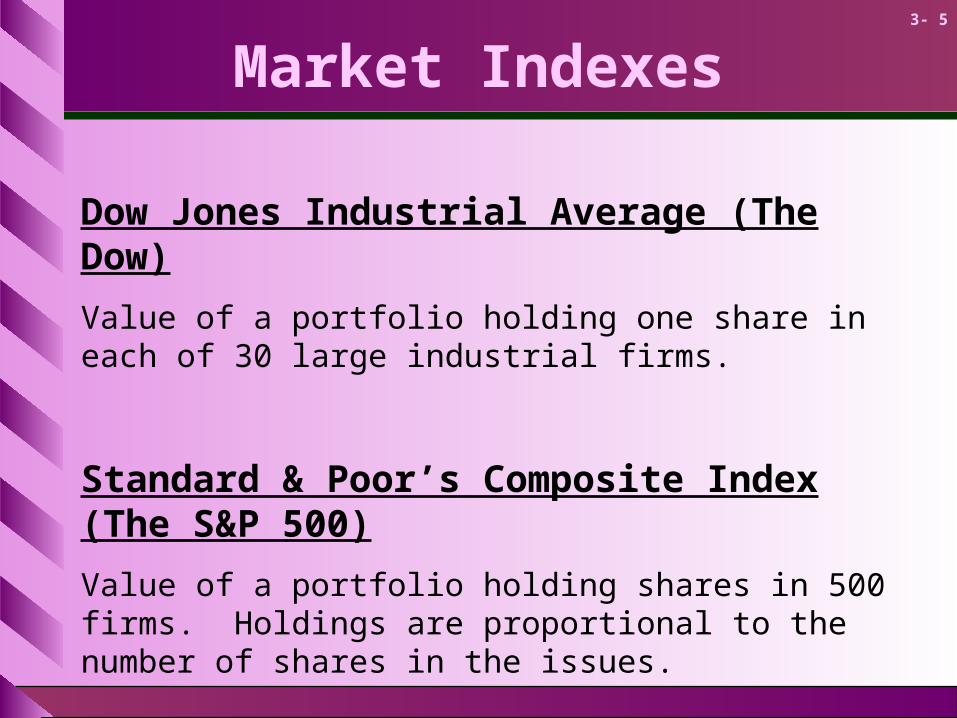

Market Indexes

Dow Jones Industrial Average (The Dow)

Value of a portfolio holding one share in each of 30 large industrial firms.

Standard & Poor’s Composite Index (The S&P 500)

Value of a portfolio holding shares in 500 firms. Holdings are proportional to the number of shares in the issues.

3- 6

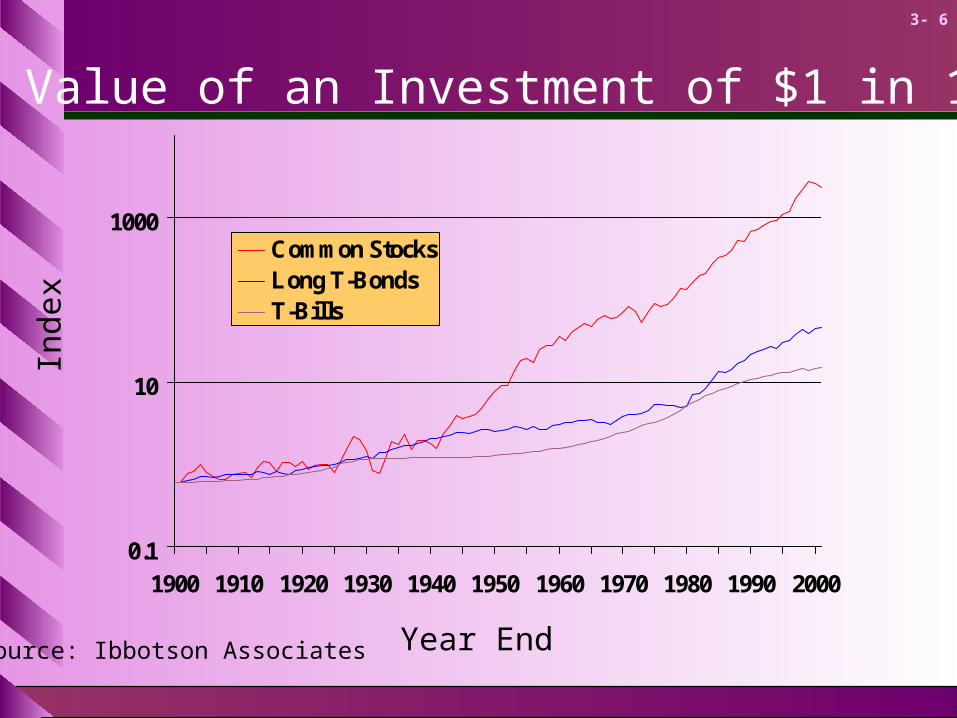

The Value of an Investment of $1 in 1900

Source: Ibbotson Associates

0.1

10

1000

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000

Common StocksLong T-BondsT-Bills

Inde

x

Year End

3- 7

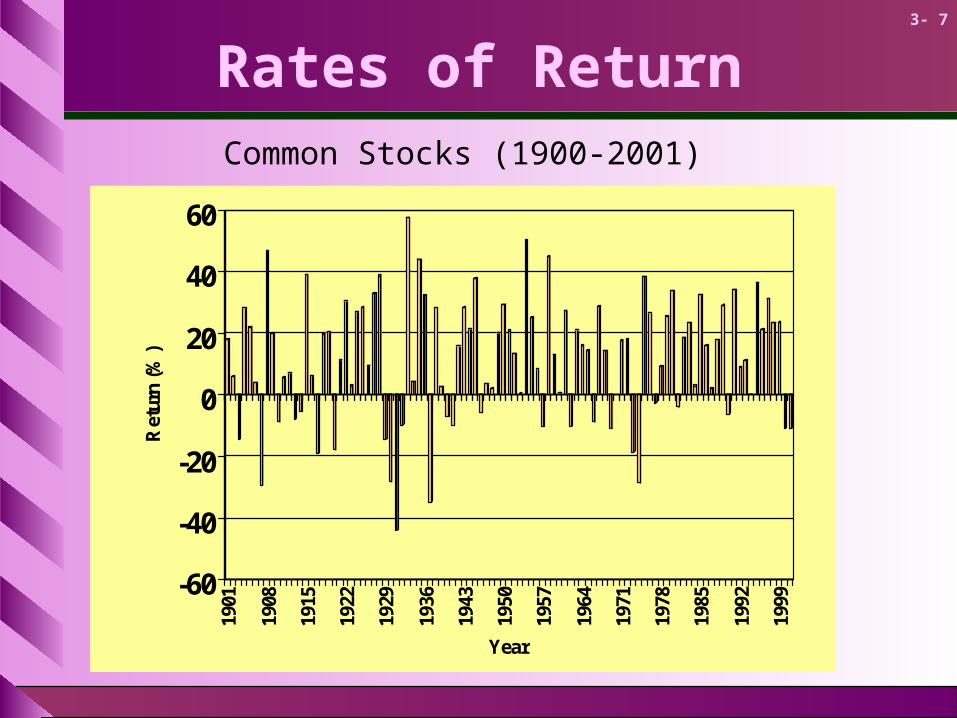

Rates of Return

-60

-40

-20

0

20

40

60

Ret

urn

(%)

1901

1908

1915

1922

1929

1936

1943

1950

1957

1964

1971

1978

1985

1992

1999

Year

Common Stocks (1900-2001)

3- 8

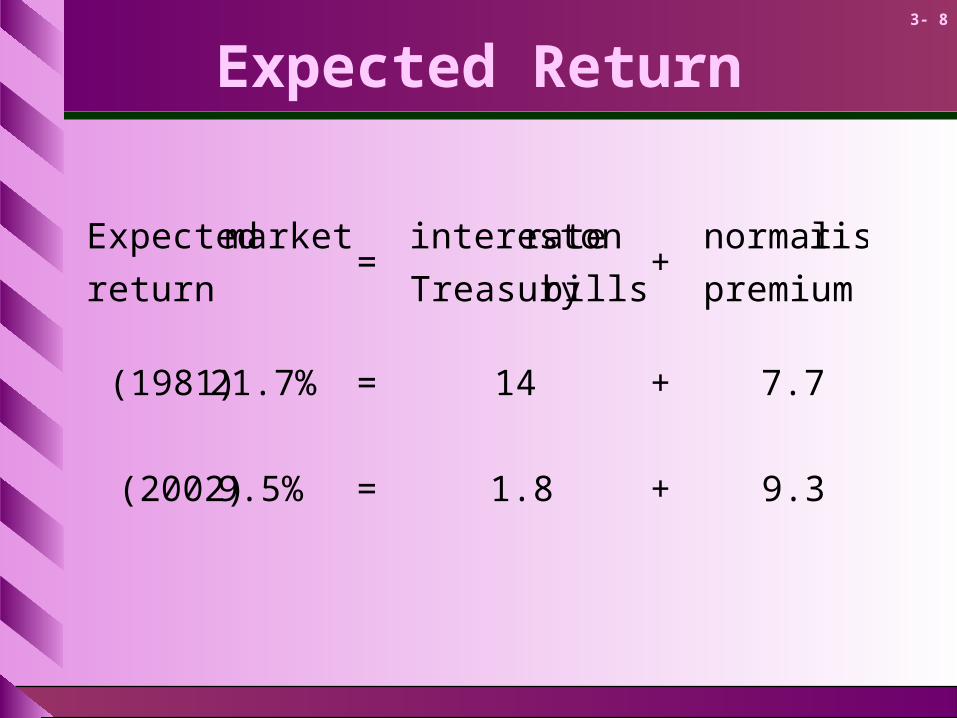

Expected Return

9.3+1.8=9.5% (2002)

7.7+14=21.7% (1981)

premium

risk normal+

billsTreasury

on rateinterest =

return

market Expected

3- 9

Measuring Risk

Variance - Average value of squared deviations from mean. A measure of volatility.

Standard Deviation - Average value of squared deviations from mean. A measure of volatility.

3- 10

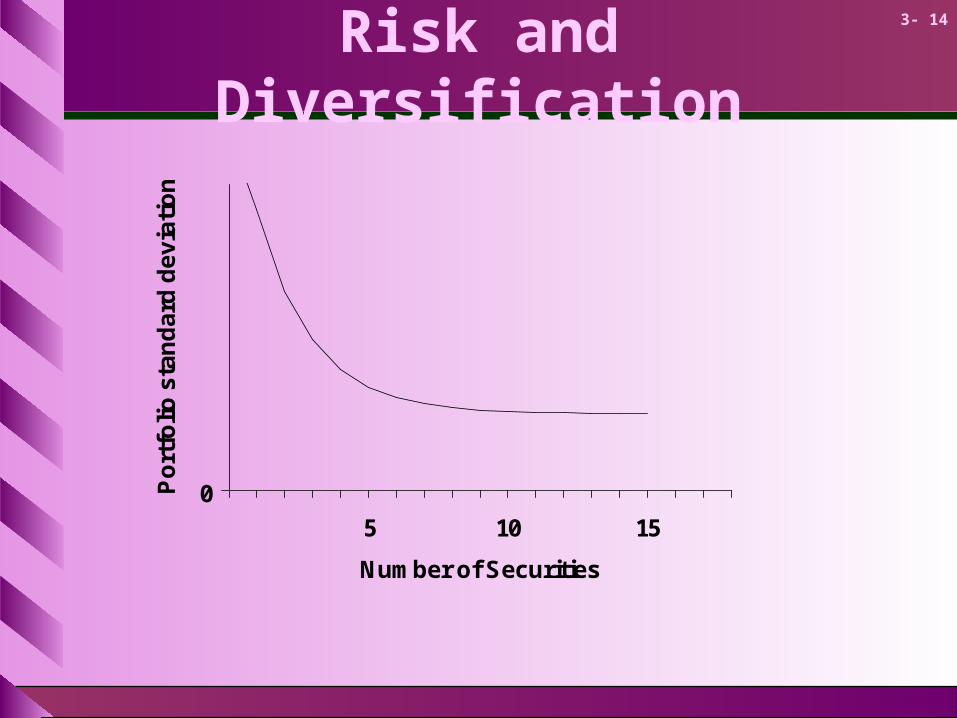

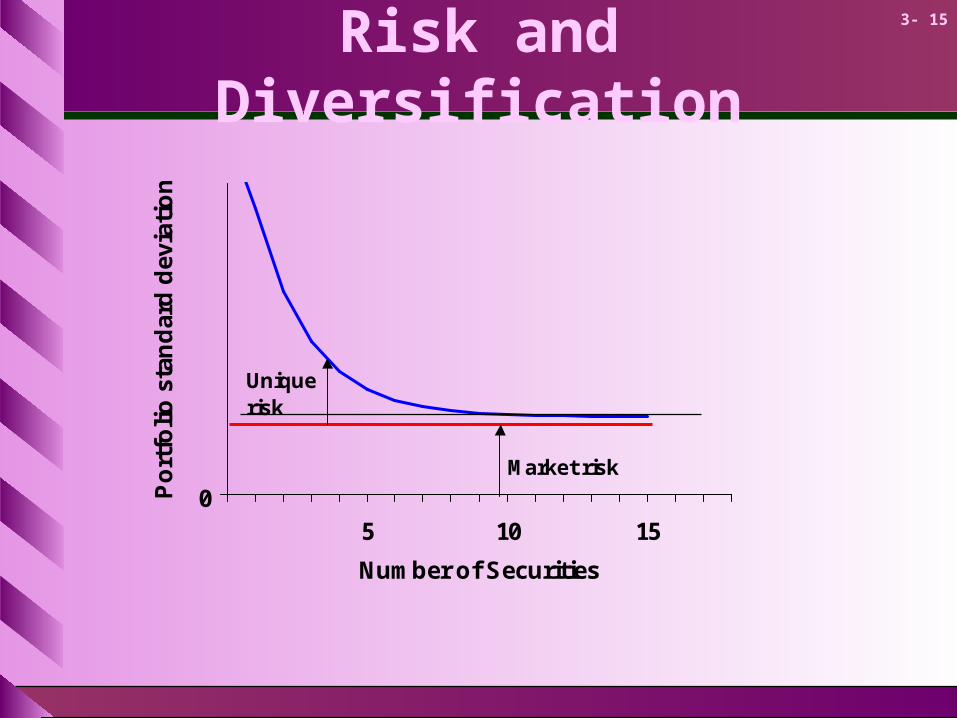

Risk and Diversification

Diversification - Strategy designed to reduce risk by spreading the portfolio across many investments.

Unique Risk - Risk factors affecting only that firm. Also called “diversifiable risk.”

Market Risk - Economy-wide sources of risk that affect the overall stock market. Also called “systematic risk.”

3- 11

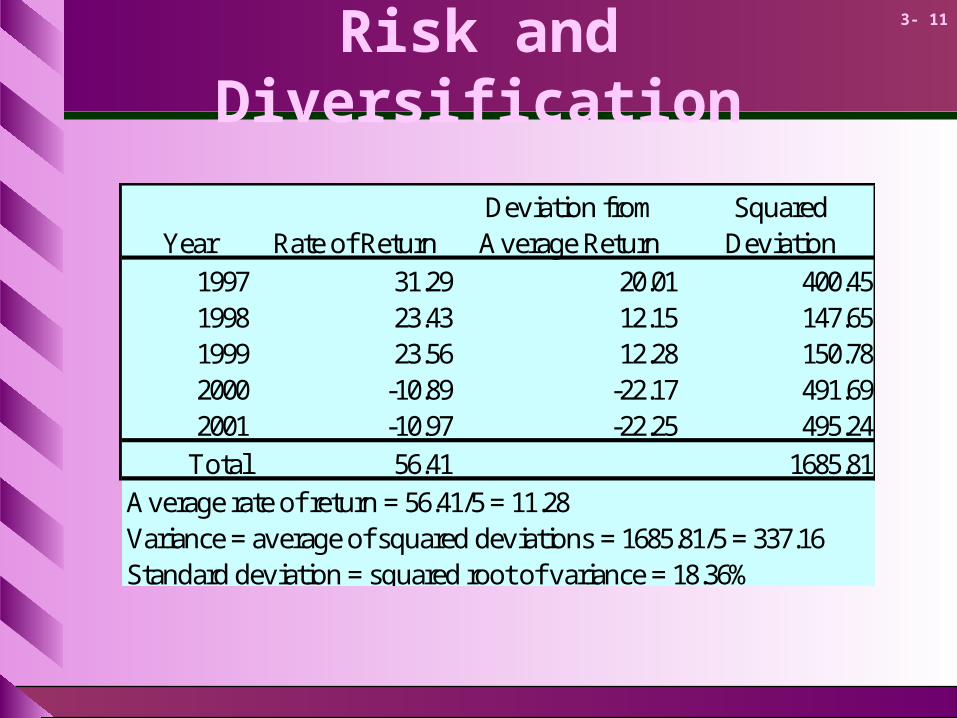

Risk and Diversification

Deviation from SquaredYear Rate of Return Average Return Deviation

1997 31.29 20.01 400.451998 23.43 12.15 147.651999 23.56 12.28 150.782000 -10.89 -22.17 491.692001 -10.97 -22.25 495.24

Total 56.41 1685.81

Average rate of return = 56.41/5 = 11.28Variance = average of squared deviations = 1685.81/5 = 337.16Standard deviation = squared root of variance = 18.36%

3- 12

Risk and Diversification

Portfolio rate

of return=

fraction of portfolio

in first assetx

rate of return

on first asset

+fraction of portfolio

in second assetx

rate of return

on second asset

((

(())

))

3- 13

Stock Market Volatility 1926-2001

0

10

20

30

40

50

60

1926

1935

1940

1945

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

Std

Dev

3- 14

Risk and Diversification

0

5 10 15

Number of Securities

Po

rtfo

lio s

tan

da

rd d

ev

iati

on

3- 15

05 10 15

Number of Securities

Po

rtfo

lio

sta

nd

ard

dev

iati

on

Market risk

Uniquerisk

Risk and Diversification

3- 16

Measuring Market Risk

Market Portfolio - Portfolio of all assets in the economy. In practice a broad stock market index, such as the S&P Composite, is used to represent the market.

Beta - Sensitivity of a stock’s return to the return on the market portfolio.

3- 17

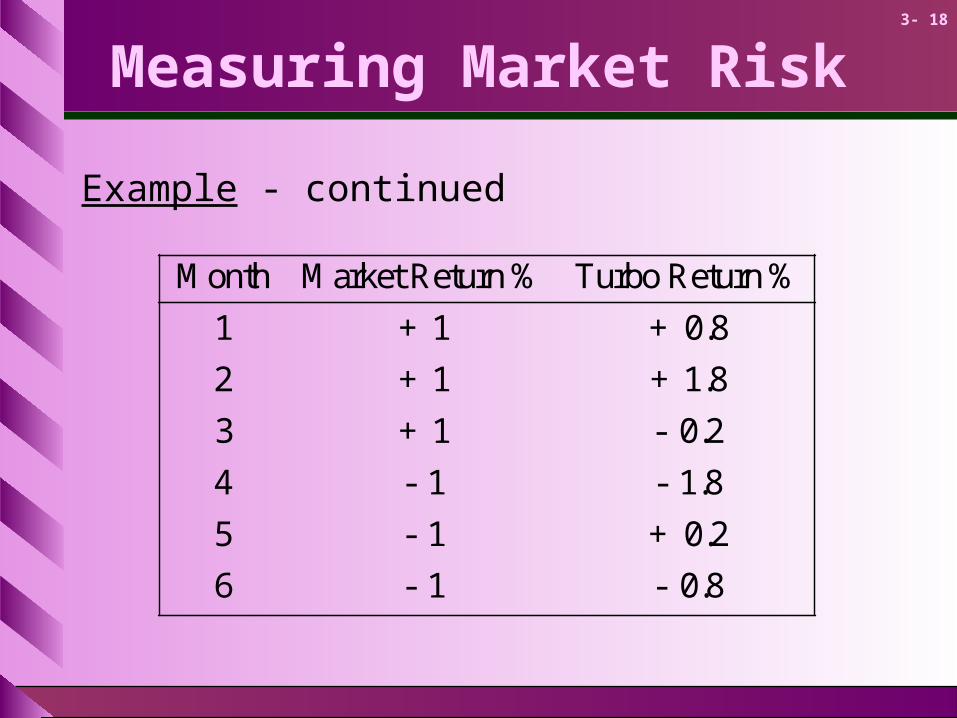

Measuring Market Risk

Example - Turbo Charged Seafood has the following % returns on its stock, relative to the listed changes in the % return on the market portfolio. The beta of Turbo Charged Seafood can be derived from this information.

3- 18

Measuring Market Risk

Month Market Return % Turbo Return %

1 + 1 + 0.8

2 + 1 + 1.8

3 + 1 - 0.2

4 - 1 - 1.8

5 - 1 + 0.2

6 - 1 - 0.8

Example - continued

3- 19

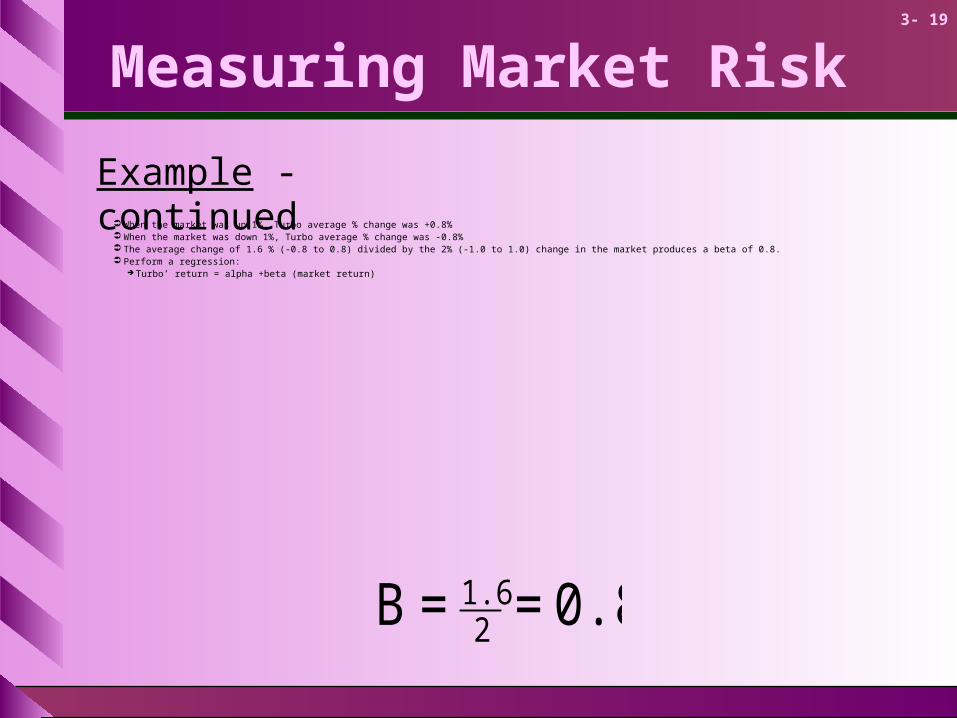

Measuring Market Risk

0.8==B 21.6

When the market was up 1%, Turbo average % change was +0.8% When the market was down 1%, Turbo average % change was -0.8% The average change of 1.6 % (-0.8 to 0.8) divided by the 2% (-1.0 to 1.0) change in the market produces a beta of 0.8. Perform a regression:

Turbo’ return = alpha +beta (market return)

Example - continued

3- 20

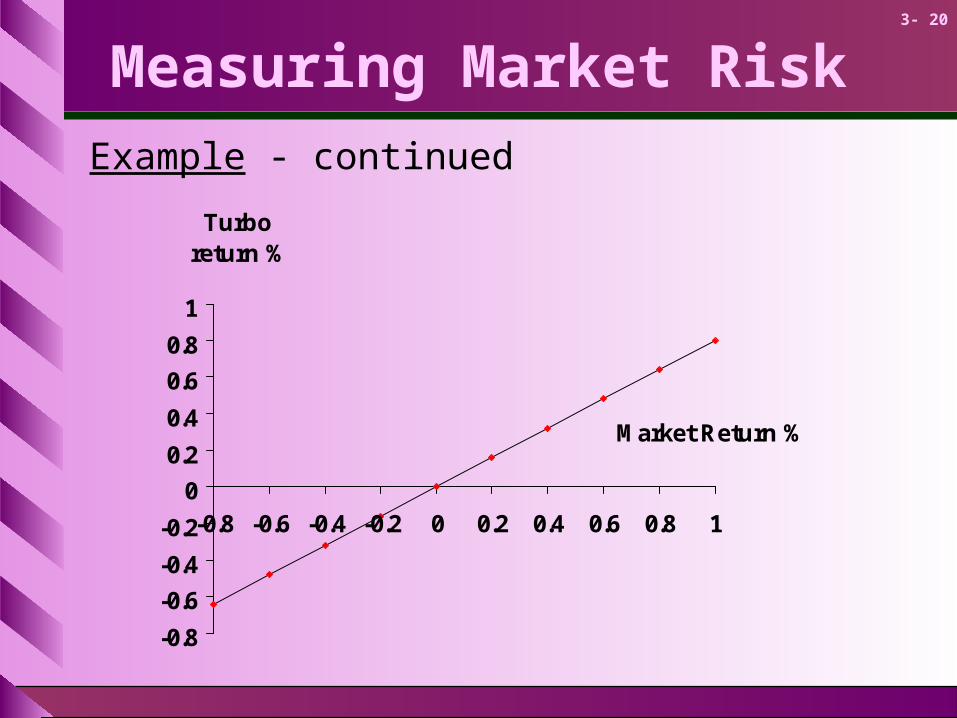

Measuring Market Risk

Example - continued

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

-0.8 -0.6 -0.4 -0.2 0 0.2 0.4 0.6 0.8 1

Market Return %

Turbo return %

3- 21

Portfolio Betas

Diversification decreases variability from unique risk, but not from market risk.

The beta of your portfolio will be an average of the betas of the securities in the portfolio.

If you owned all of the S&P Composite Index stocks, you would have an average beta of 1.0

3- 22

Stock Betas

.31Heinz.H.J

.41ExxonMobil

.57Pfizer

.66sMcDonald'

.67PepsiCo

1.00Airlines Delta

1.05Ford

1.18GE

2.14erDellComput

3.30Amazon

BetaStock

B

3- 23

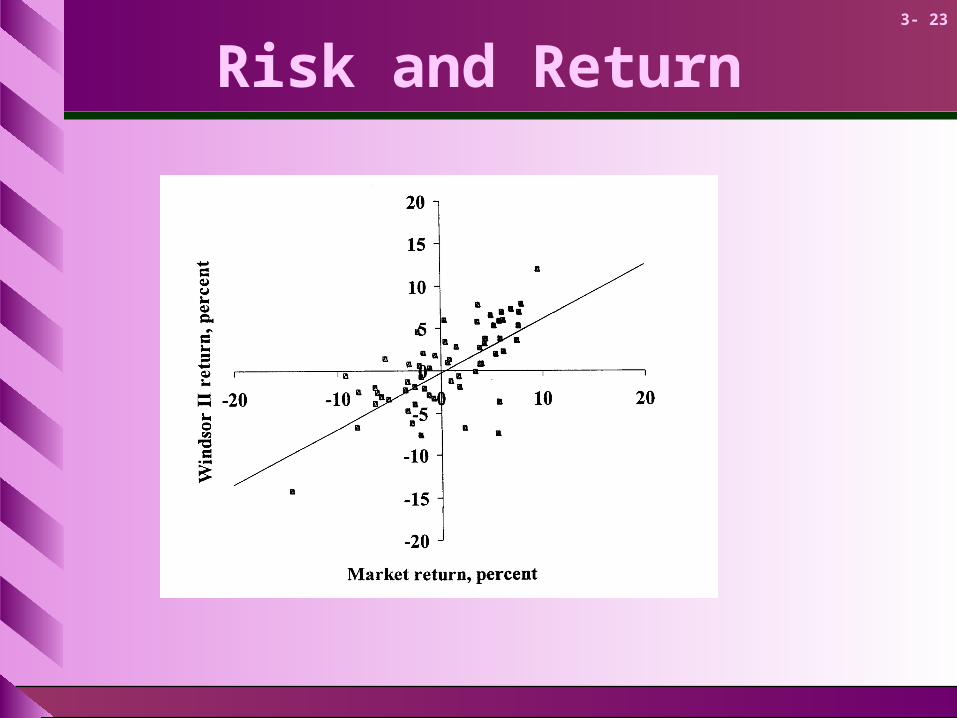

Risk and Return

3- 24

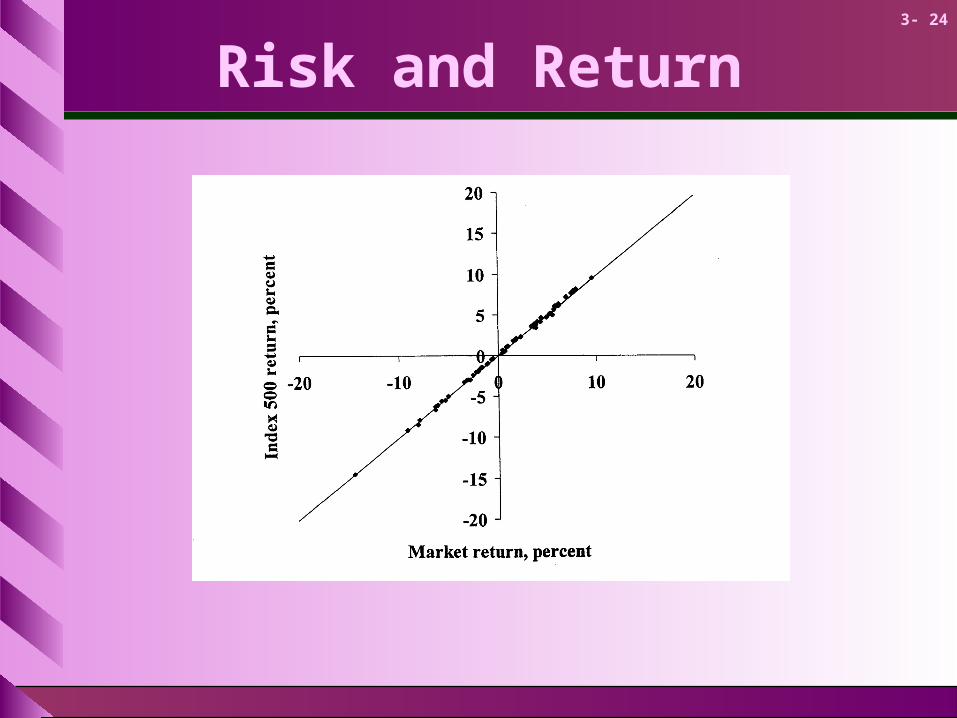

Risk and Return

3- 25

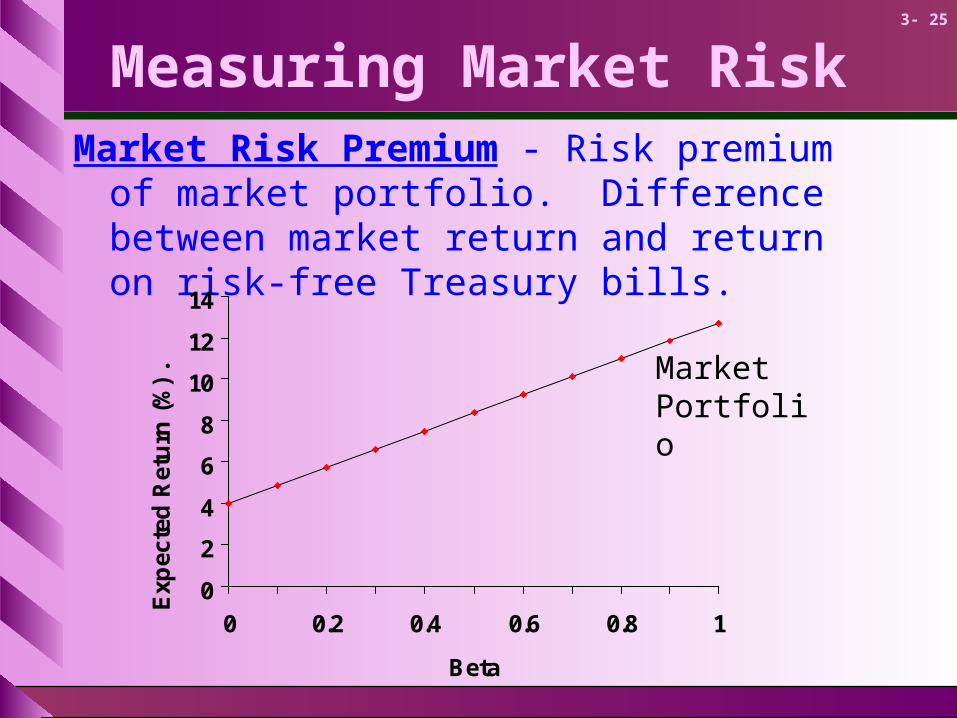

Measuring Market RiskMarket Risk Premium - Risk premium of market

portfolio. Difference between market return and return on risk-free Treasury bills.

0

2

4

6

8

10

12

14

0 0.2 0.4 0.6 0.8 1

Beta

Exp

ecte

d R

etu

rn (

%)

. Market Portfolio

3- 26

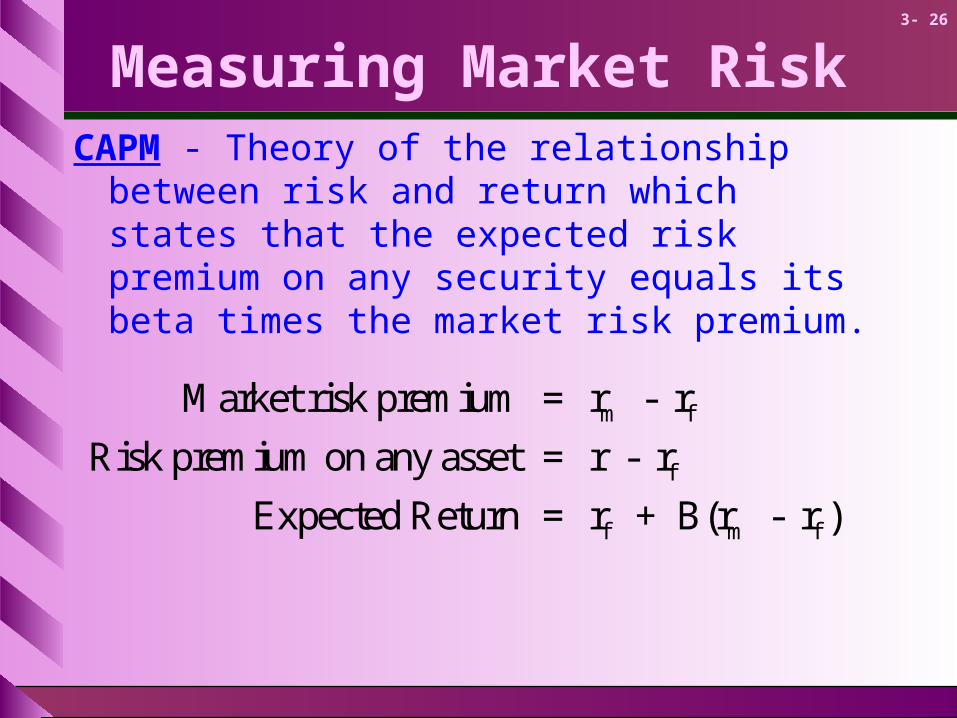

Measuring Market RiskCAPM - Theory of the relationship between risk and

return which states that the expected risk premium on any security equals its beta times the market risk premium.

Market risk premium = r - r

Risk premium on any asset = r - r

Expected Return = r + B(r - r )

m f

f

f m f

3- 27

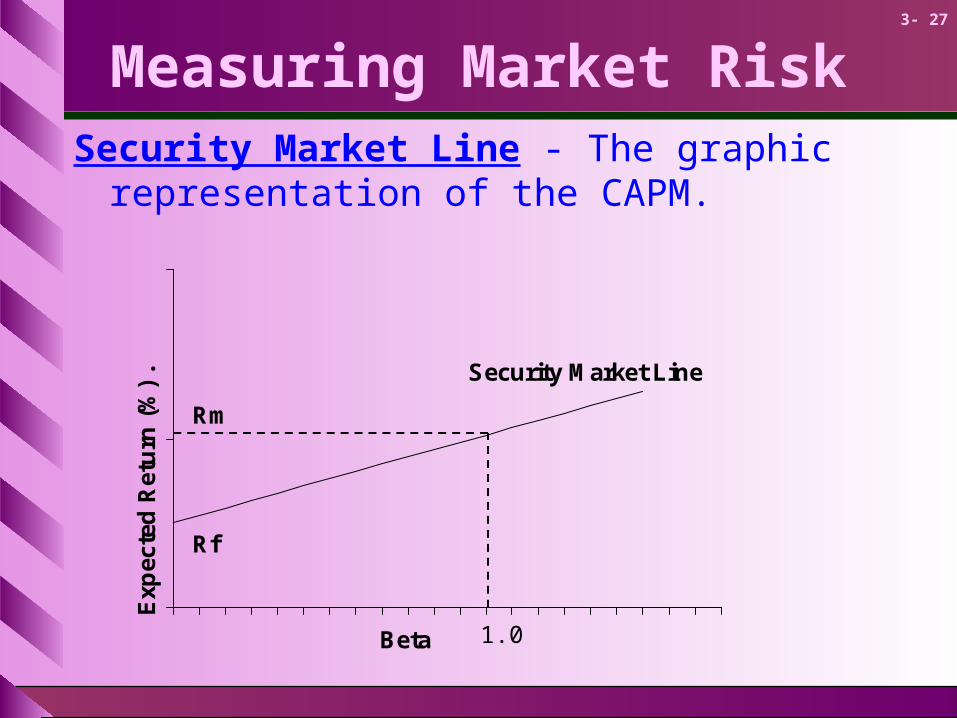

Measuring Market RiskSecurity Market Line - The graphic representation

of the CAPM.

Beta

Exp

ecte

d R

etu

rn (

%)

.

Rf

Rm

Security Market Line

1.0

3- 28

Capital Budgeting & Project Risk

The project cost of capital depends on the use to which the capital is being put. Therefore, it depends on the risk of the project and not the risk of the company.

3- 29

Capital Budgeting & Project Risk

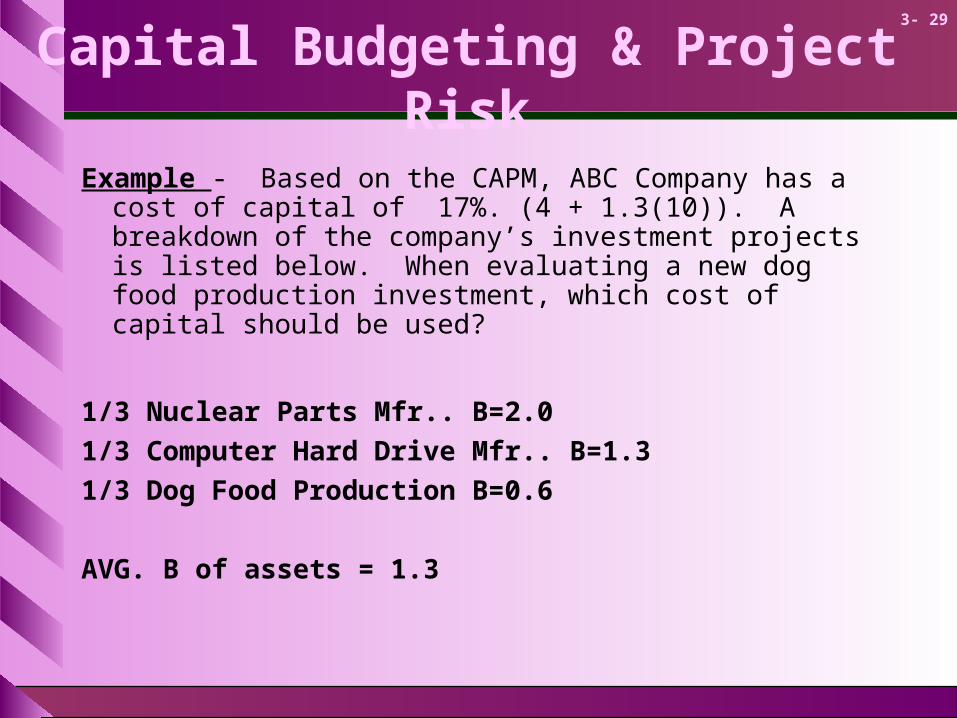

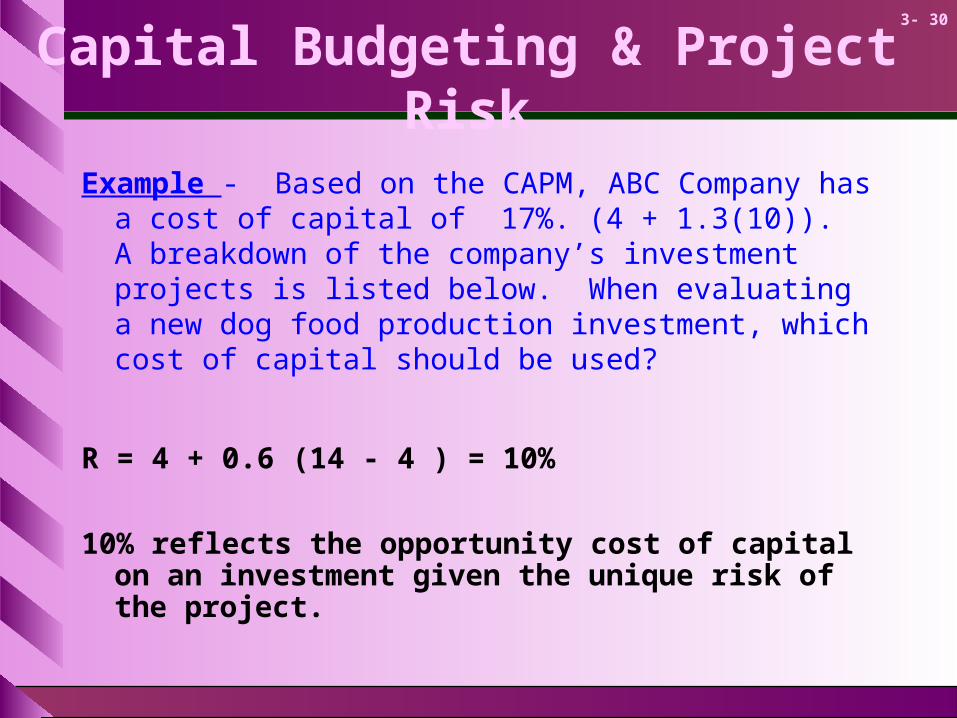

Example - Based on the CAPM, ABC Company has a cost of capital of 17%. (4 + 1.3(10)). A breakdown of the company’s investment projects is listed below. When evaluating a new dog food production investment, which cost of capital should be used?

1/3 Nuclear Parts Mfr.. B=2.0

1/3 Computer Hard Drive Mfr.. B=1.3

1/3 Dog Food Production B=0.6

AVG. B of assets = 1.3

3- 30

Capital Budgeting & Project Risk

Example - Based on the CAPM, ABC Company has a cost of capital of 17%. (4 + 1.3(10)). A breakdown of the company’s investment projects is listed below. When evaluating a new dog food production investment, which cost of capital should be used?

R = 4 + 0.6 (14 - 4 ) = 10%

10% reflects the opportunity cost of capital on an investment given the unique risk of the project.

3- 31

Cost of Capital

Cost of Capital - The return the firm’s investors expect to earn if they invested in securities with comparable degrees of risk.

Capital Structure - The firm’s mix of long term financing and equity financing.

3- 32

Cost of Capital

Example

Geothermal Inc. has the following structure. Given that geothermal pays 8% for debt and 14% for equity, what is the Company Cost of Capital?

3- 33

Cost of Capital

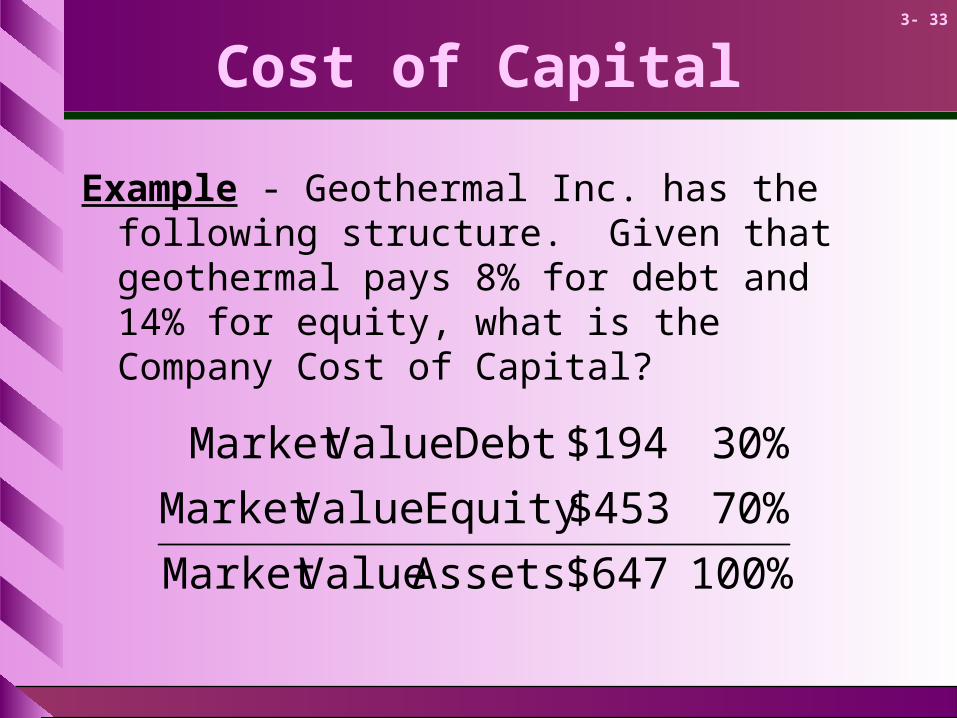

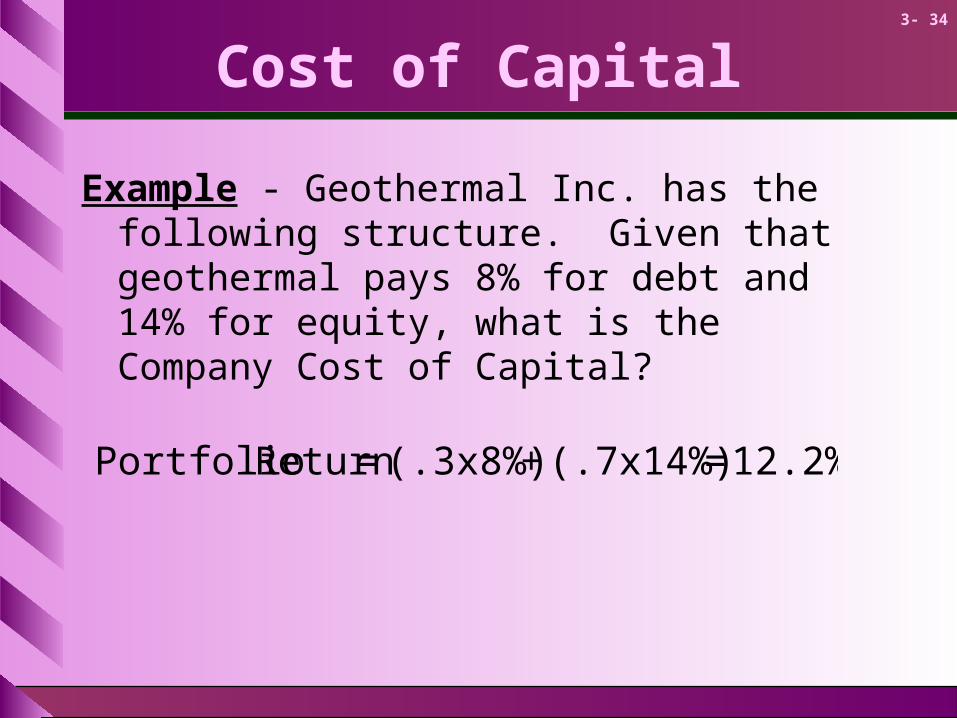

Example - Geothermal Inc. has the following structure. Given that geothermal pays 8% for debt and 14% for equity, what is the Company Cost of Capital?

100%$647Assets ValueMarket

70%$453 EquityValueMarket

30%$194 DebtValueMarket

3- 34

Cost of Capital

Example - Geothermal Inc. has the following structure. Given that geothermal pays 8% for debt and 14% for equity, what is the Company Cost of Capital?

12.2%=(.7x14%)+(.3x8%)= ReturnPortfolio

3- 35

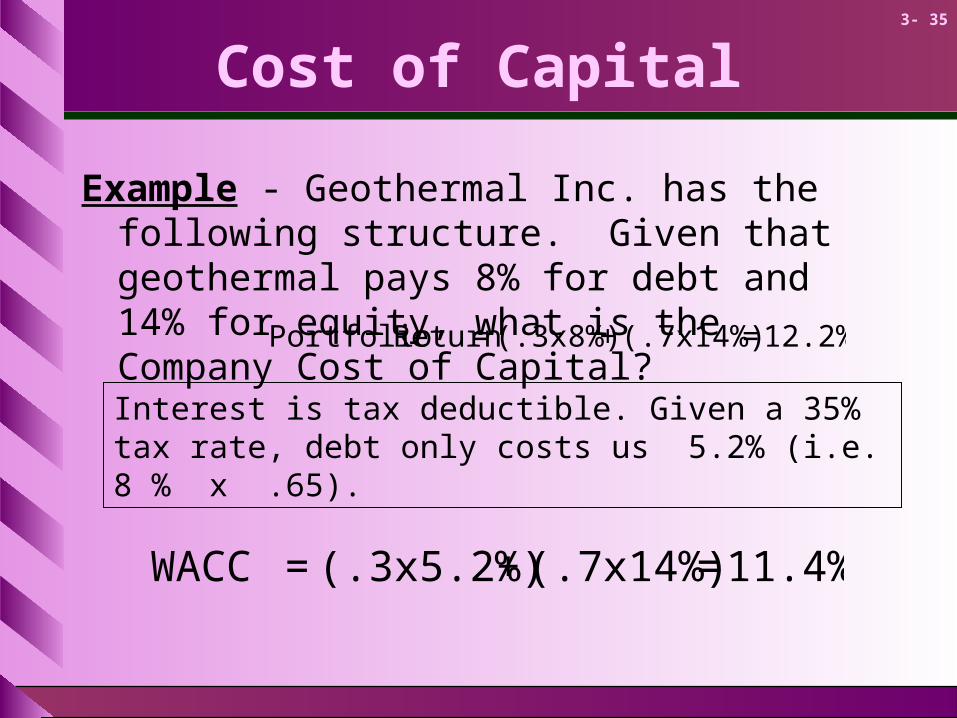

Cost of Capital

Example - Geothermal Inc. has the following structure. Given that geothermal pays 8% for debt and 14% for equity, what is the Company Cost of Capital? 12.2%=(.7x14%)+(.3x8%)= ReturnPortfolio

Interest is tax deductible. Given a 35% tax rate, debt only costs us 5.2% (i.e. 8 % x .65).

11.4%=(.7x14%)+(.3x5.2%)= WACC

3- 36

WACC

Weighted Average Cost of Capital (WACC) - The expected rate of return on a portfolio of all the firm’s securities.

Company cost of capital = Weighted average of debt and equity returns.

3- 37

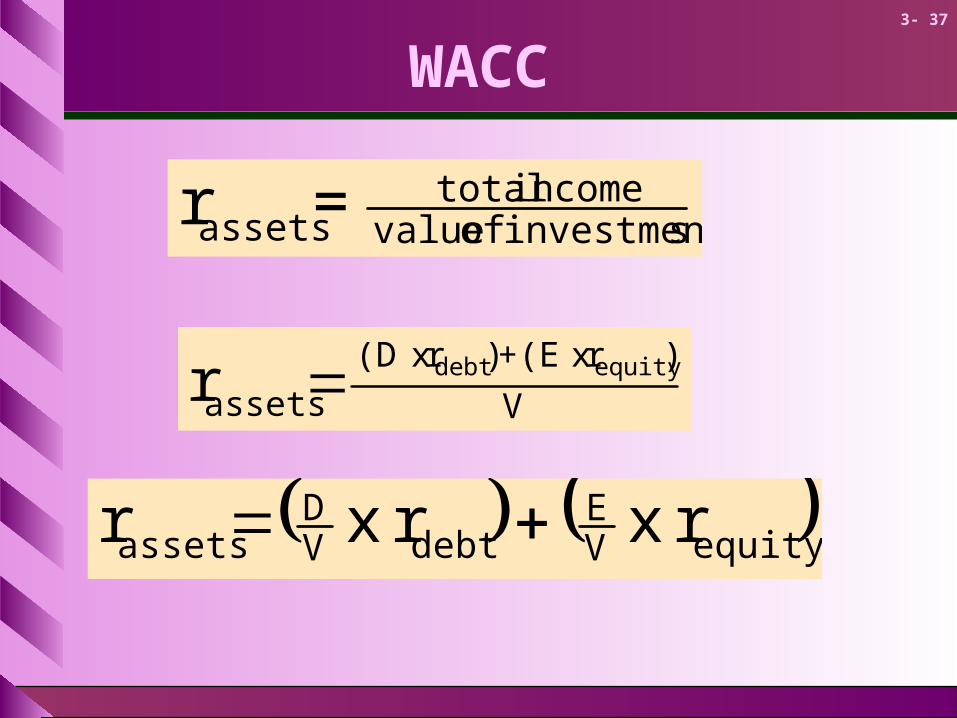

WACC

V

)r x (E+)r x (D

assetsequitydebtr

equityVE

debtVD

assets rx rx r

sinvestment of valueincome total

assets =r

3- 38

WACC

Three Steps to Calculating Cost of Capital

1. Calculate the value of each security as a proportion of the firm’s market value.

2. Determine the required rate of return on each security.

3. Calculate a weighted average of these required returns.

3- 39

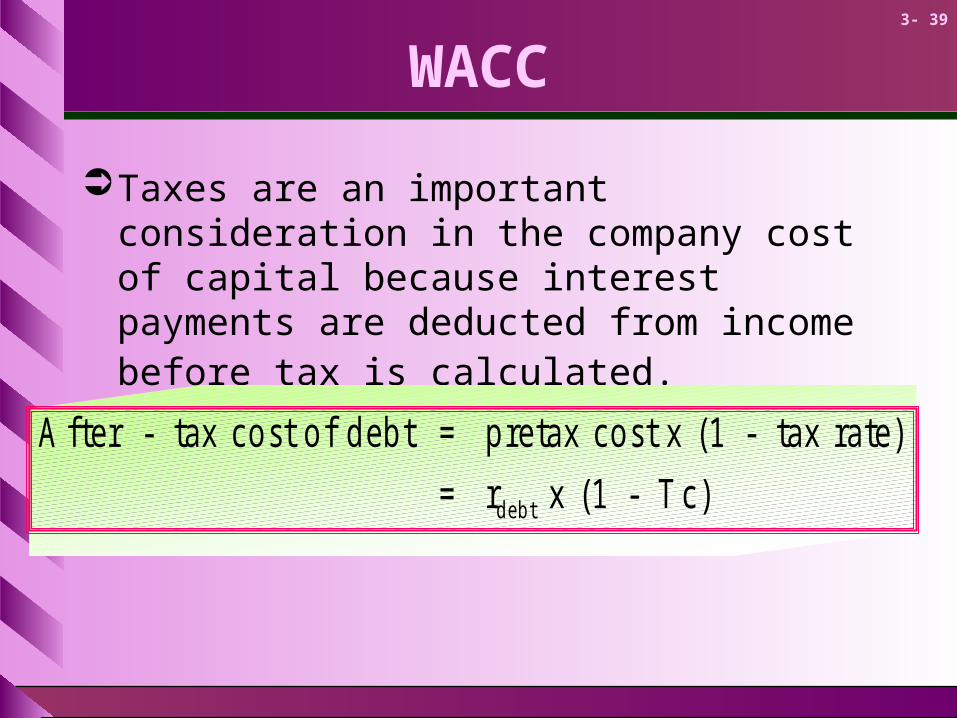

WACC

Taxes are an important consideration in the company cost of capital because interest payments are deducted from income before tax is calculated.

A f te r - ta x c o s t o f d e b t = p re ta x c o s t x (1 - ta x r a te )

= r x (1 - T c )d e b t

3- 40

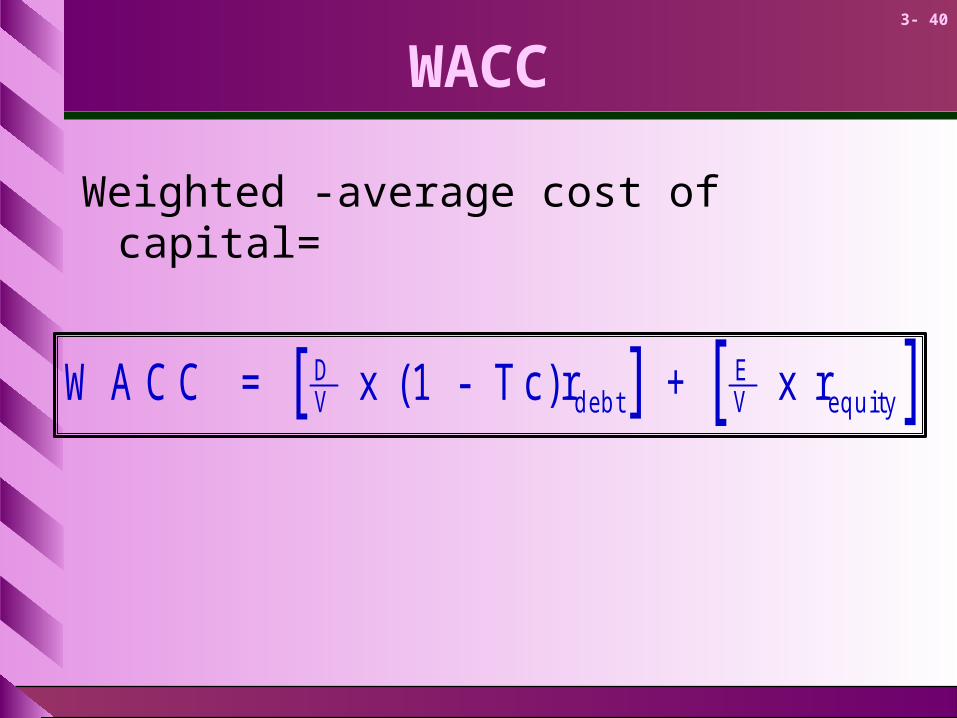

WACC

Weighted -average cost of capital=

[ ] [ ]W A C C = x ( 1 - T c ) r + x rDV d e b t

EV e q u i ty

3- 41

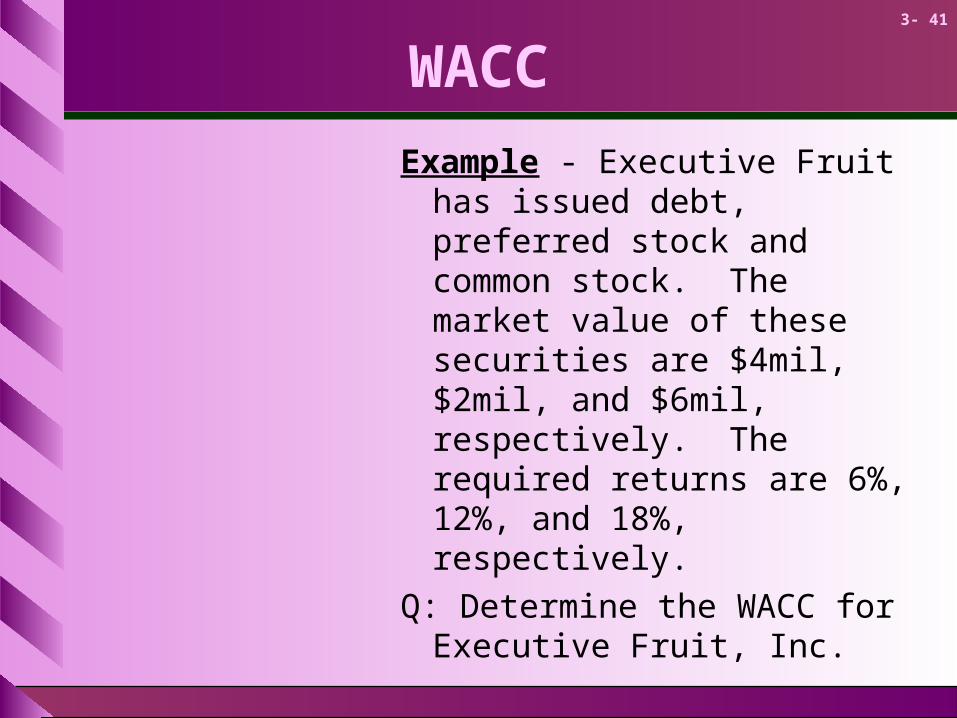

WACC

Example - Executive Fruit has issued debt, preferred stock and common stock. The market value of these securities are $4mil, $2mil, and $6mil, respectively. The required returns are 6%, 12%, and 18%, respectively.

Q: Determine the WACC for Executive Fruit, Inc.

3- 42

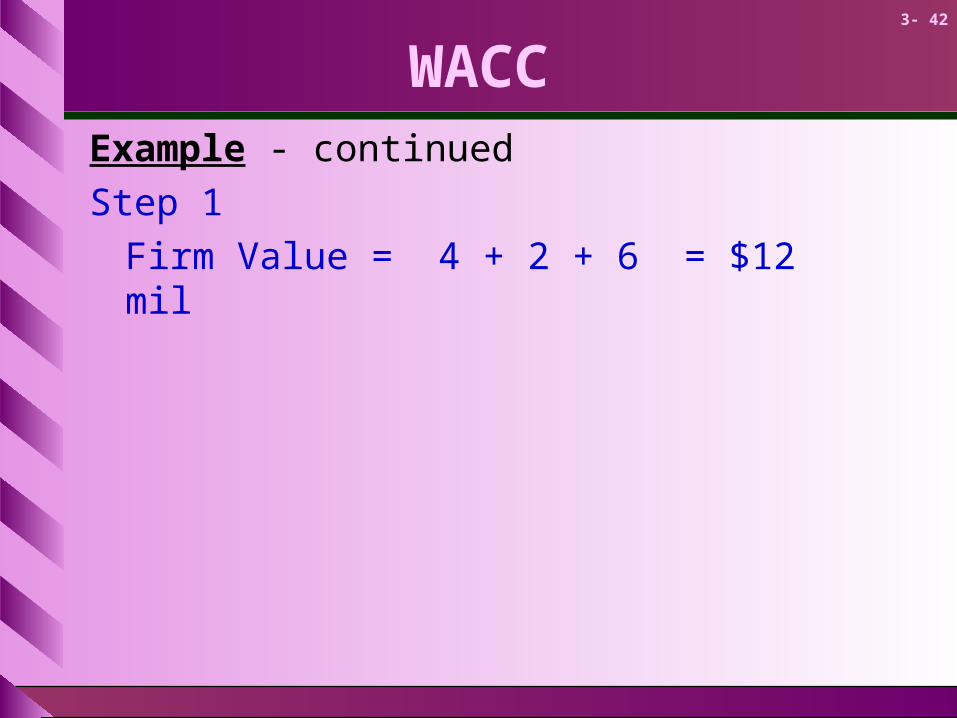

WACCExample - continued

Step 1

Firm Value = 4 + 2 + 6 = $12 mil

3- 43

WACCExample - continued

Step 1

Firm Value = 4 + 2 + 6 = $12 mil

Step 2

Required returns are given

3- 44

WACCExample - continued

Step 1

Firm Value = 4 + 2 + 6 = $12 mil

Step 2

Required returns are given

Step 3

[ ] ( ) ( )WACC = x(1-.35).06 + x.12 + x.18

=.123 or 12.3%

412

212

612

3- 45

WACC

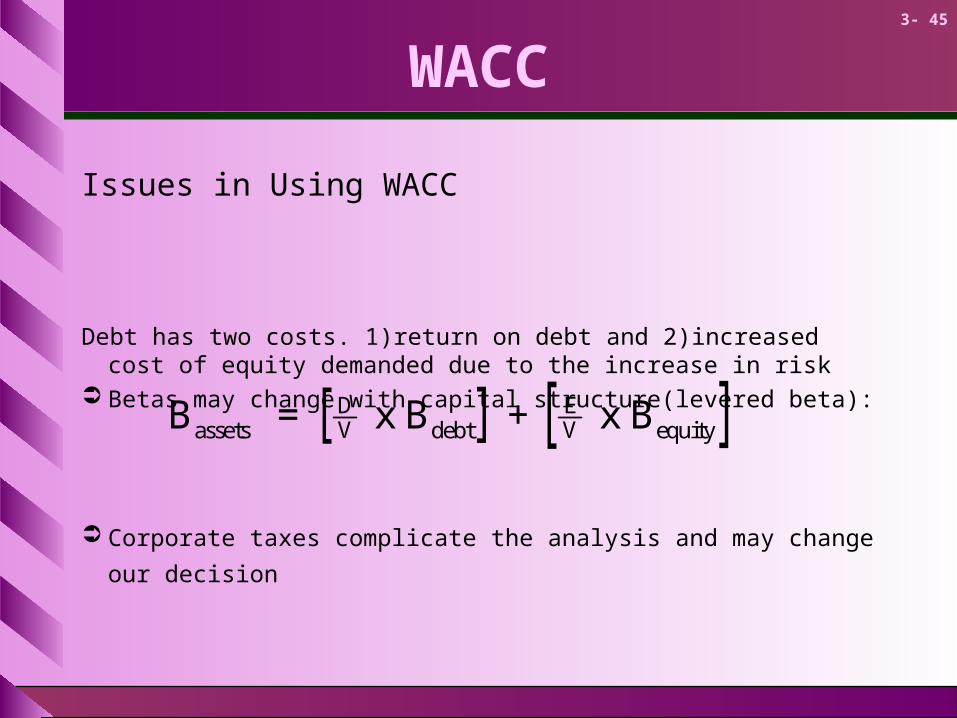

Issues in Using WACC

Debt has two costs. 1)return on debt and 2)increased cost of equity demanded due to the increase in risk

Betas may change with capital structure(levered beta):

Corporate taxes complicate the analysis and may change our

decision

[ ] [ ]B = x B + x BassetsDV debt

EV equity

3- 46

Measuring Capital Structure

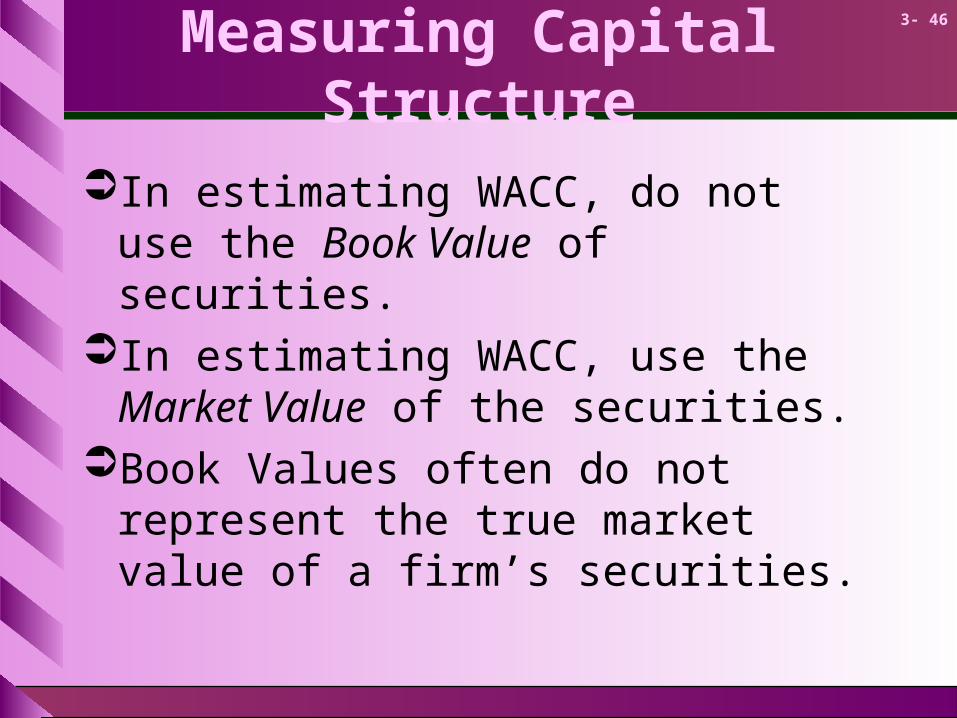

In estimating WACC, do not use the Book Value of securities.

In estimating WACC, use the Market Value of the securities.

Book Values often do not represent the true market value of a firm’s securities.

3- 47

Measuring Capital Structure

Market Value of Bonds - PV of all coupons and par value discounted at the current interest rate.

3- 48

Measuring Capital Structure

Market Value of Bonds - PV of all coupons and par value discounted at the current interest rate.

Market Value of Equity - Market price per share multiplied by the number of outstanding shares.

3- 49

Measuring Capital Structure

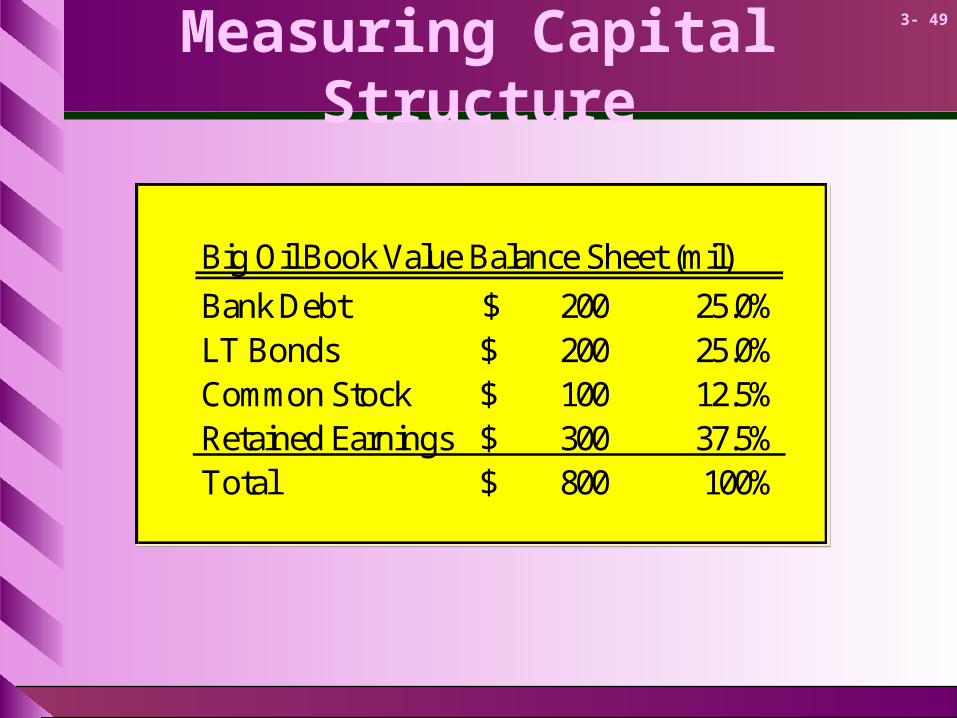

Big Oil Book Value Balance Sheet (mil)

Bank Debt 200$ 25.0%LT Bonds 200$ 25.0%Common Stock 100$ 12.5%Retained Earnings 300$ 37.5%Total 800$ 100%

Big Oil Book Value Balance Sheet (mil)

Bank Debt 200$ 25.0%LT Bonds 200$ 25.0%Common Stock 100$ 12.5%Retained Earnings 300$ 37.5%Total 800$ 100%

3- 50

Measuring Capital Structure

Big Oil Book Value Balance Sheet (mil)

Bank Debt 200$ 25.0%LT Bonds 200$ 25.0%Common Stock 100$ 12.5%Retained Earnings 300$ 37.5%Total 800$ 100%

Big Oil Book Value Balance Sheet (mil)

Bank Debt 200$ 25.0%LT Bonds 200$ 25.0%Common Stock 100$ 12.5%Retained Earnings 300$ 37.5%Total 800$ 100%

If the long term bonds pay an 8% coupon and mature in 12 years, what is their market value assuming a 9% YTM?

70.185$09.1

216....

09.1

16

09.1

16

09.1

161232

PV

3- 51

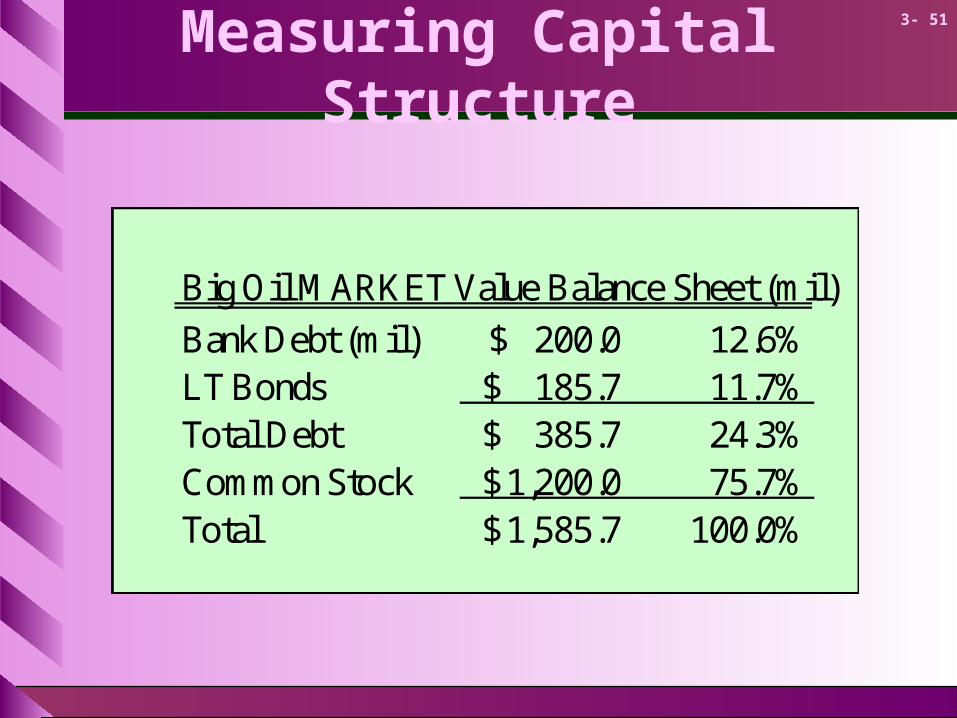

Measuring Capital Structure

Big Oil MARKET Value Balance Sheet (mil)

Bank Debt (mil) 200.0$ 12.6%LT Bonds 185.7$ 11.7%Total Debt 385.7$ 24.3%Common Stock 1,200.0$ 75.7%Total 1,585.7$ 100.0%

3- 52

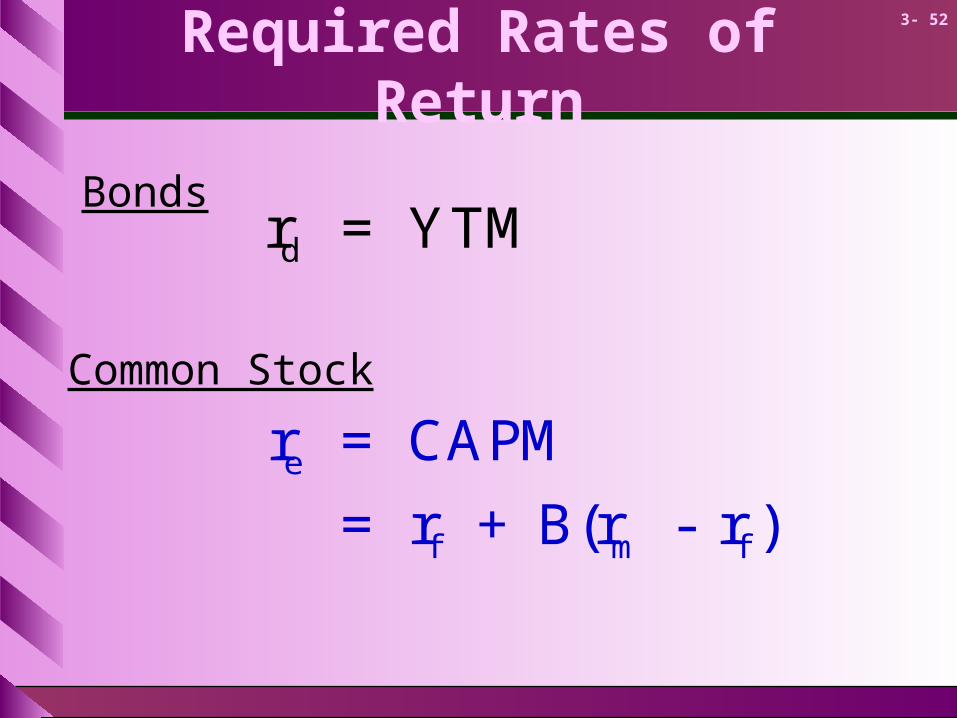

Required Rates of Return

Bondsr = YTMd

r = CAPM

= r + B(r - r )e

f m f

Common Stock

3- 53

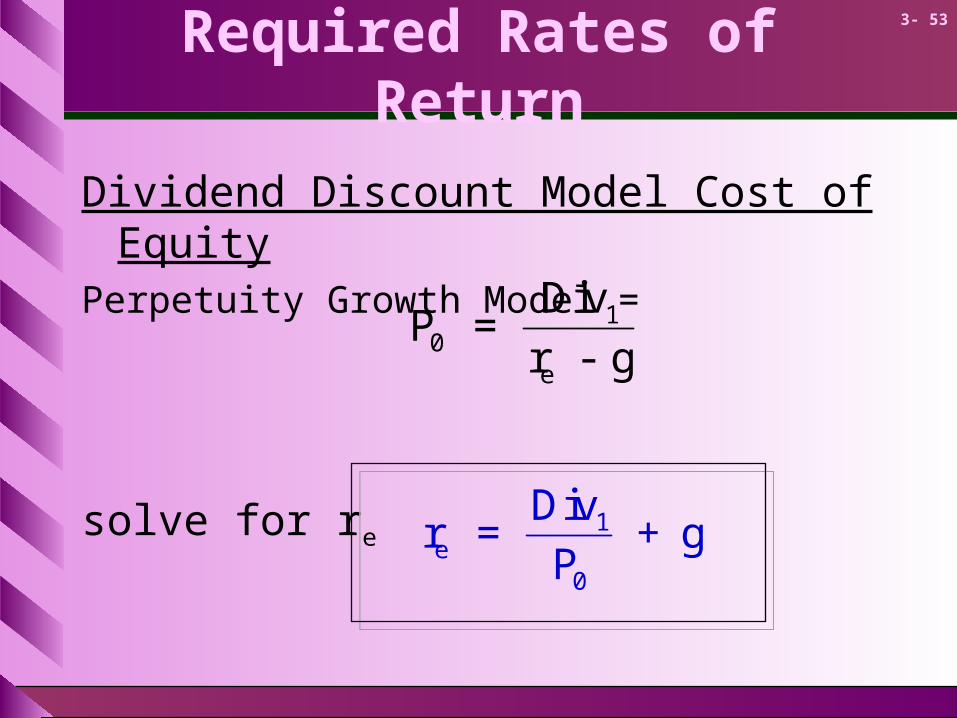

Required Rates of Return

Dividend Discount Model Cost of EquityPerpetuity Growth Model =

solve for re

P =Div

r - g01

e

r =Div

P+ ge

1

0

3- 54

Required Rates of Return

Expected Return on Preferred StockPrice of Preferred Stock =

solve for rpreferred

P =Div

r01

preferred

r =Div

Ppreferred1

0

3- 55

Flotation Costs

The cost of implementing any financing decision must be incorporated into the cash flows of the project being evaluated.

Only the incremental costs of financing should be included.