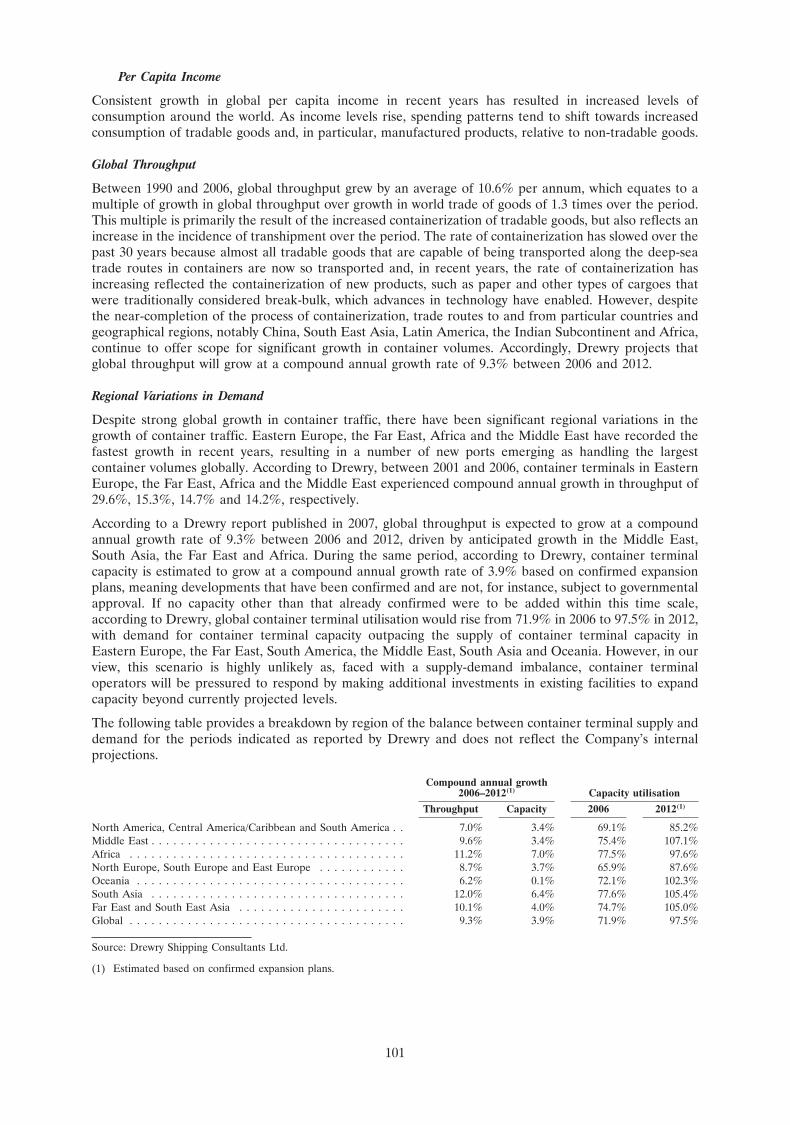

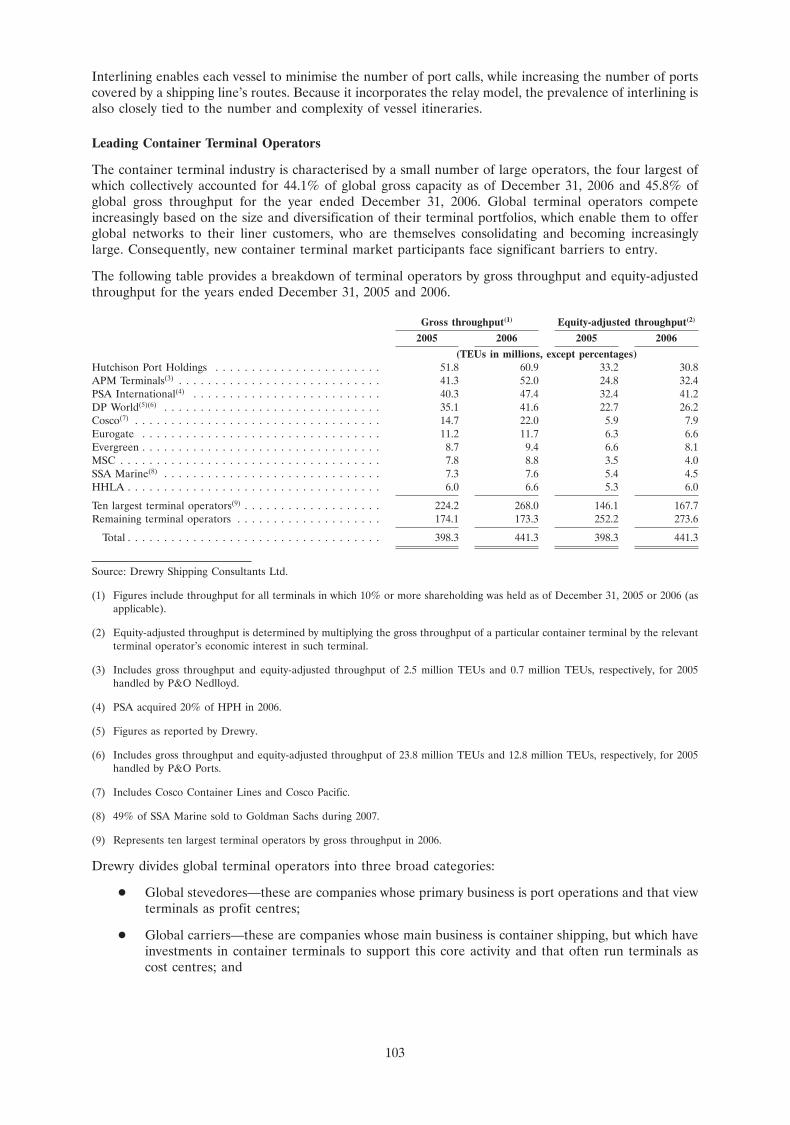

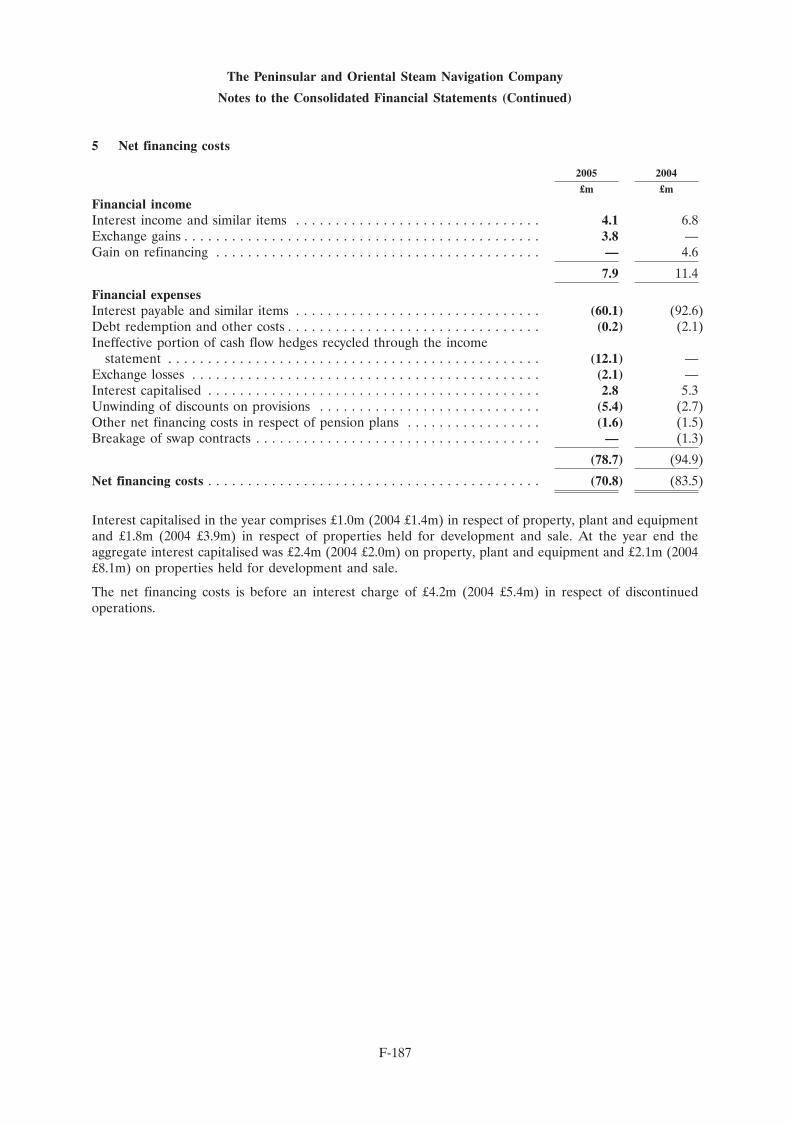

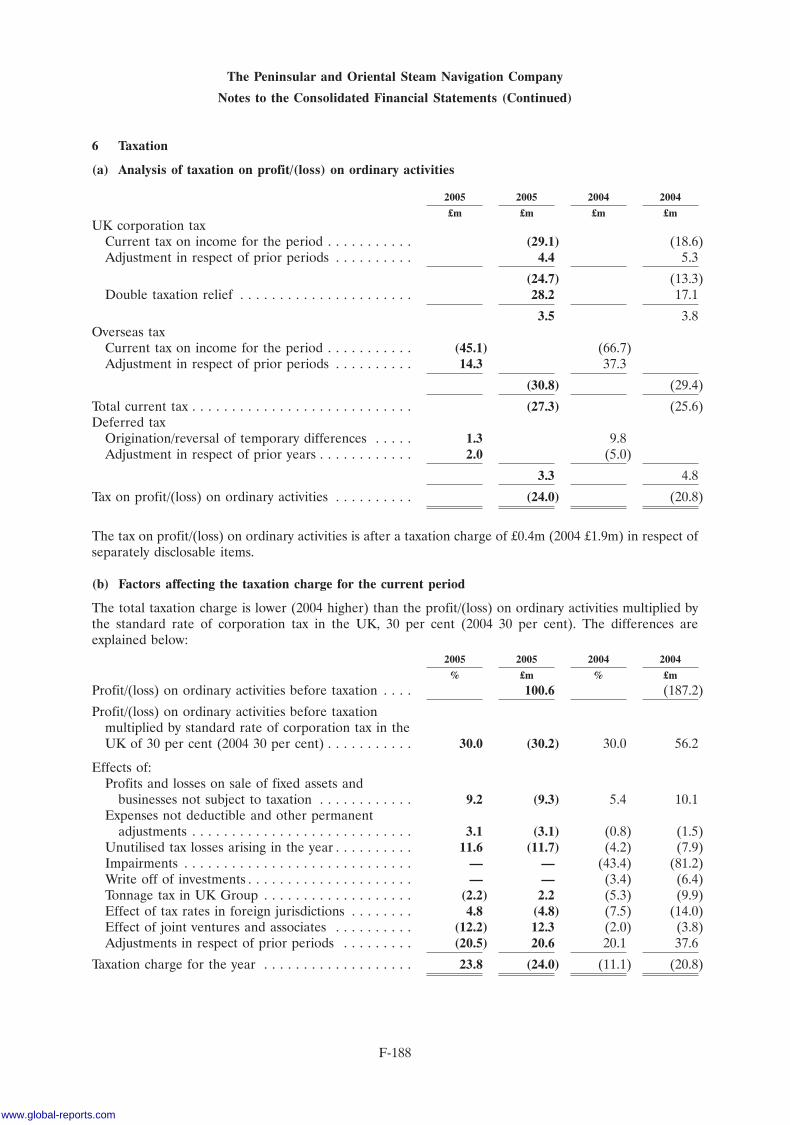

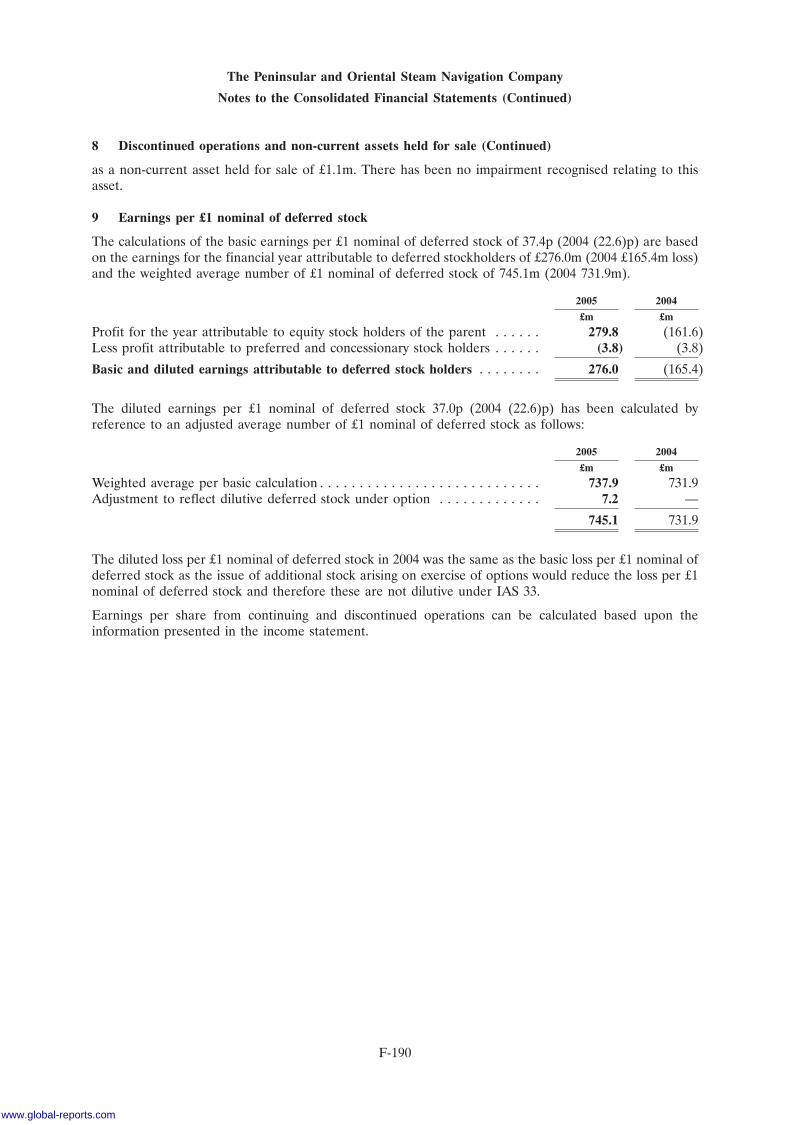

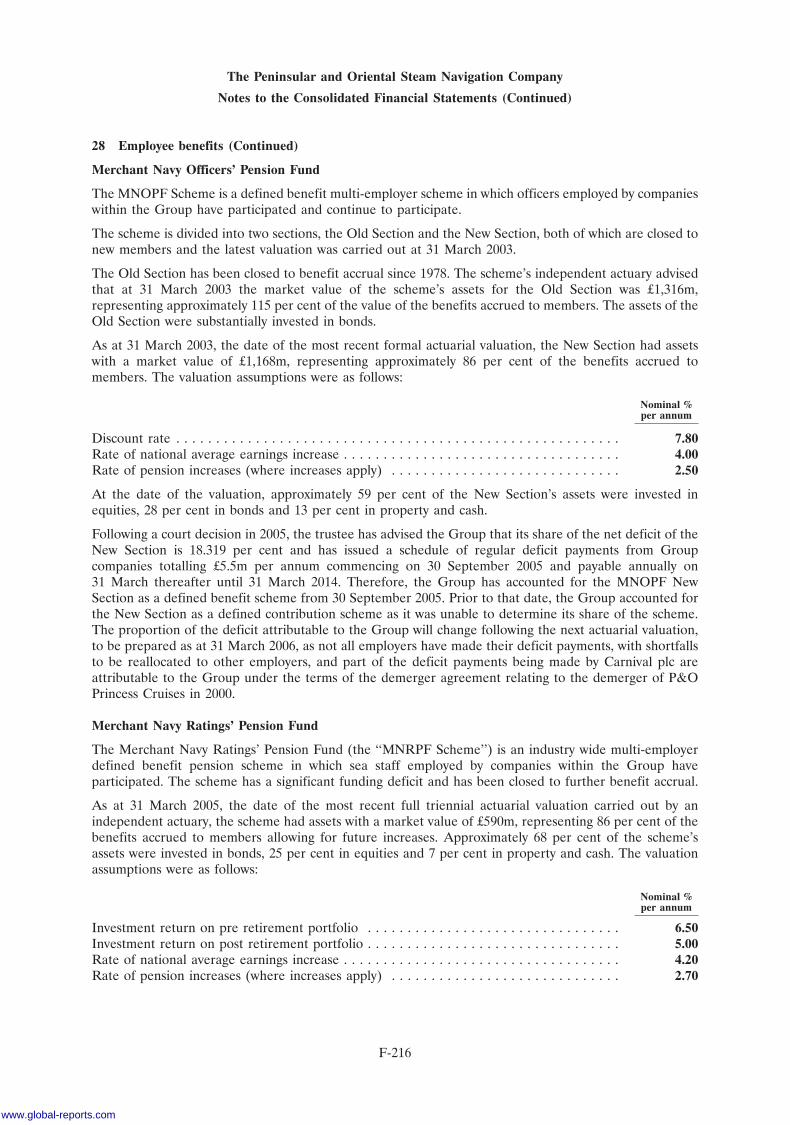

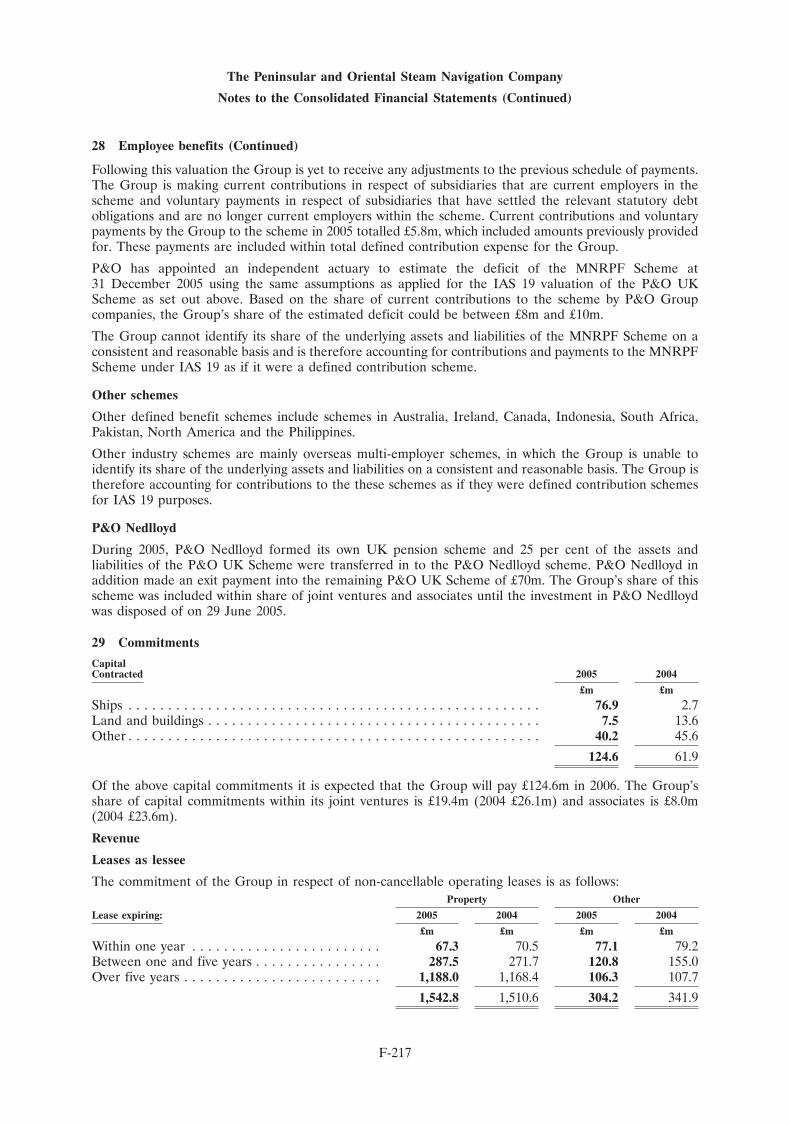

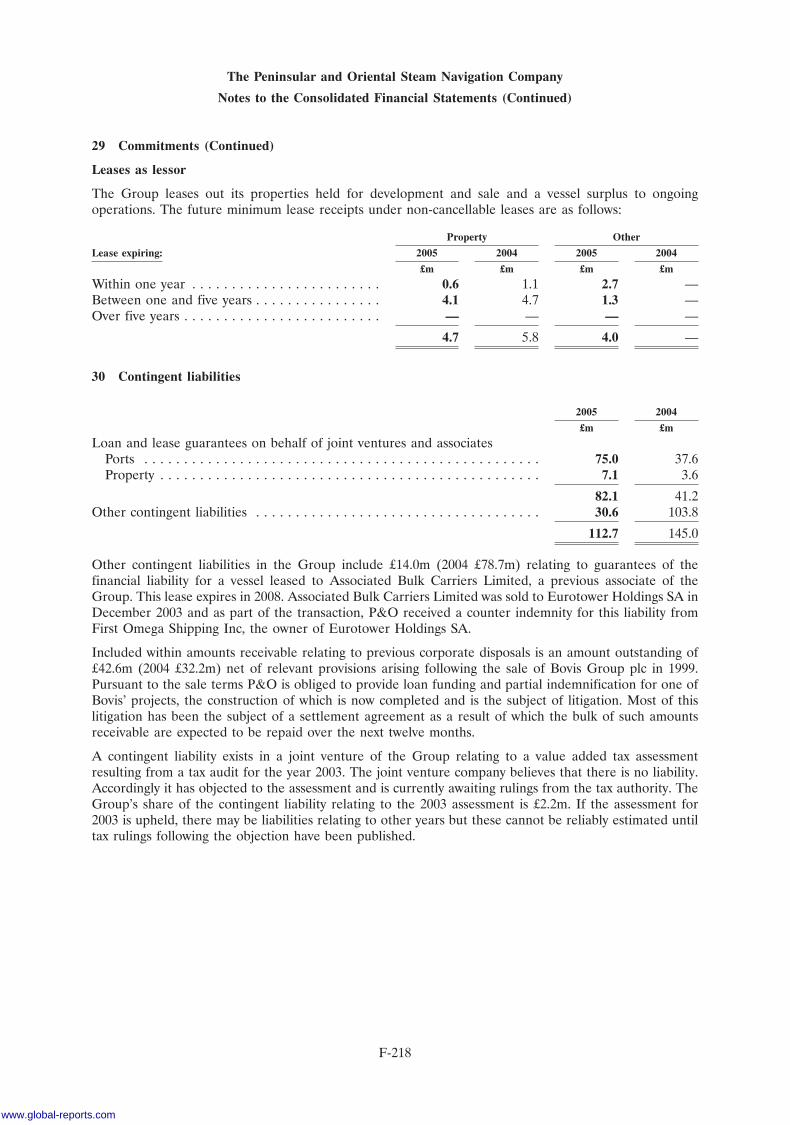

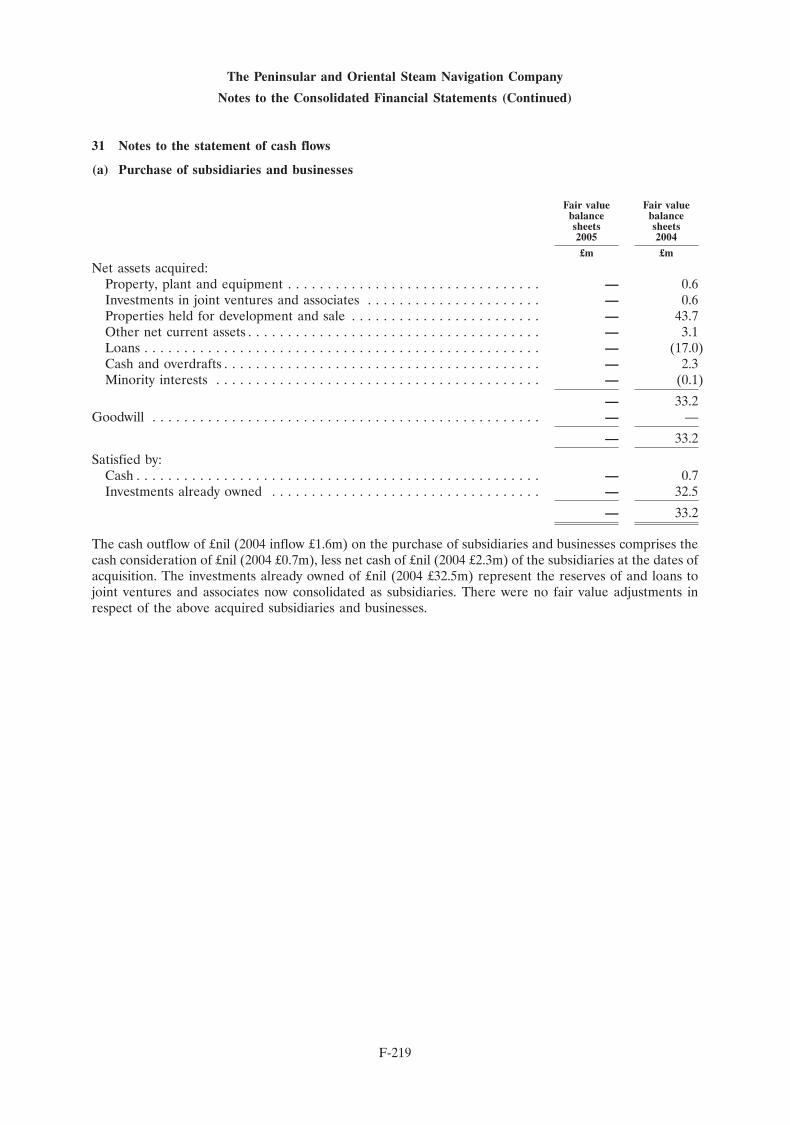

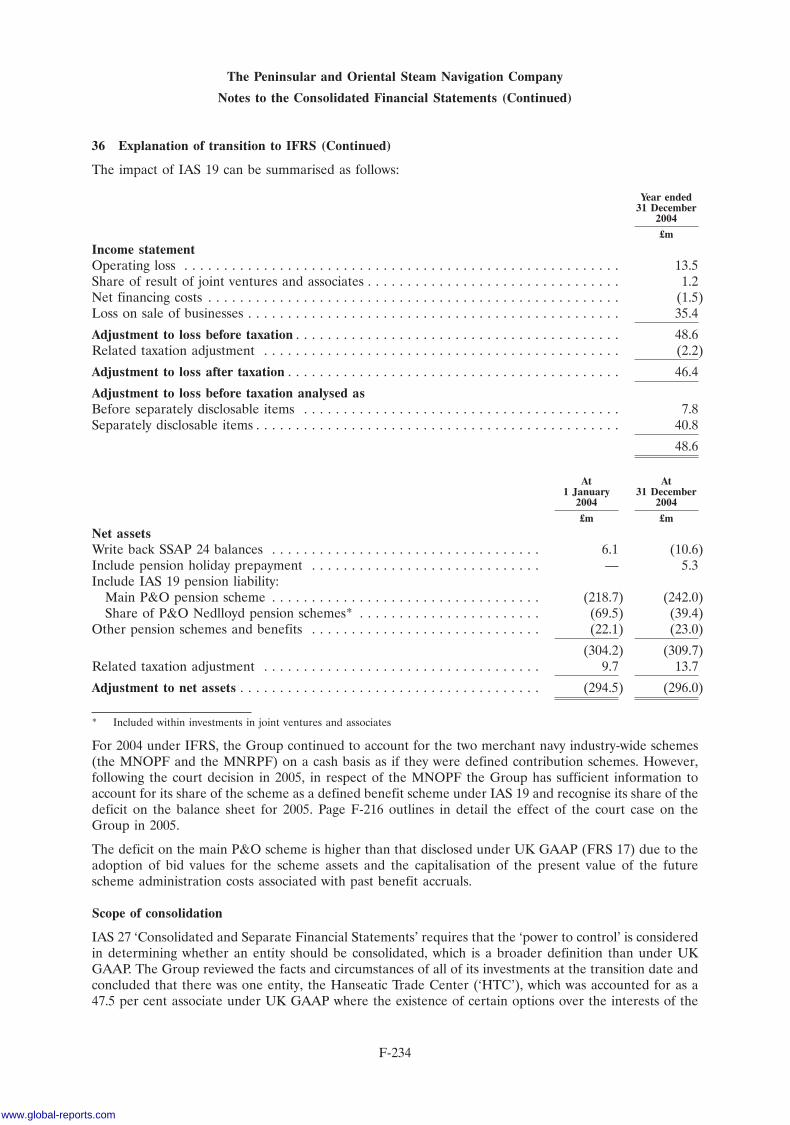

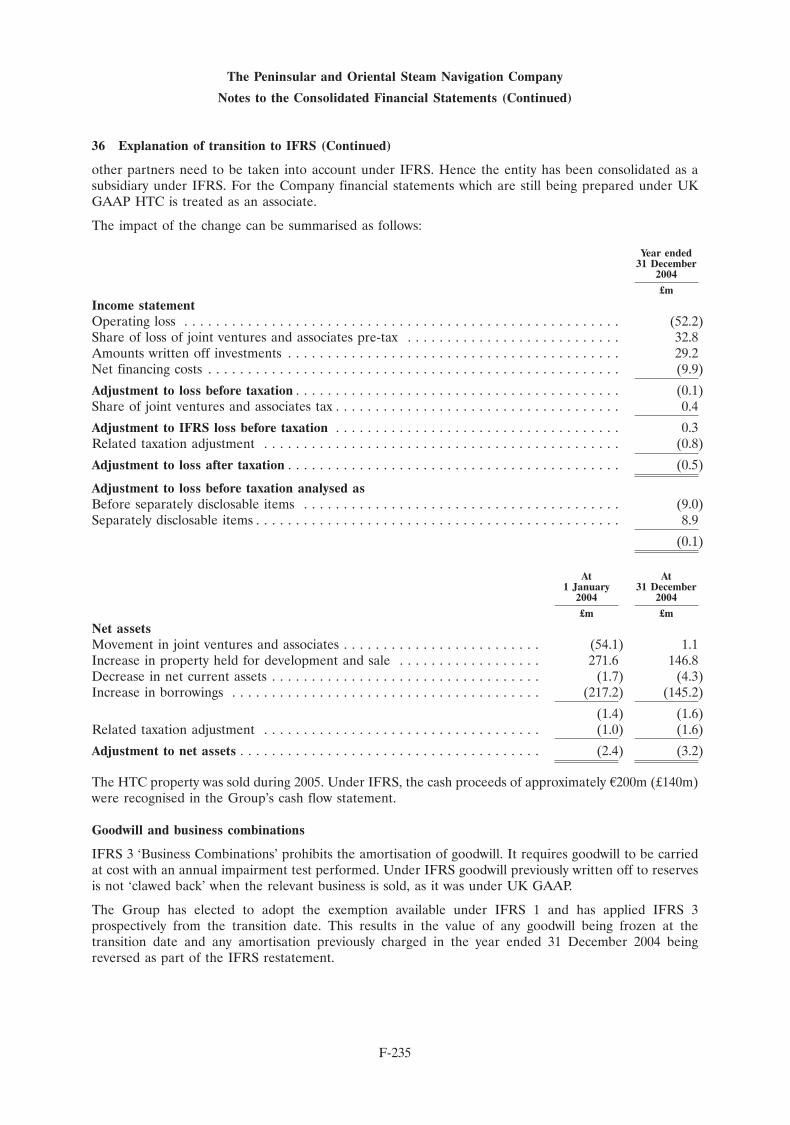

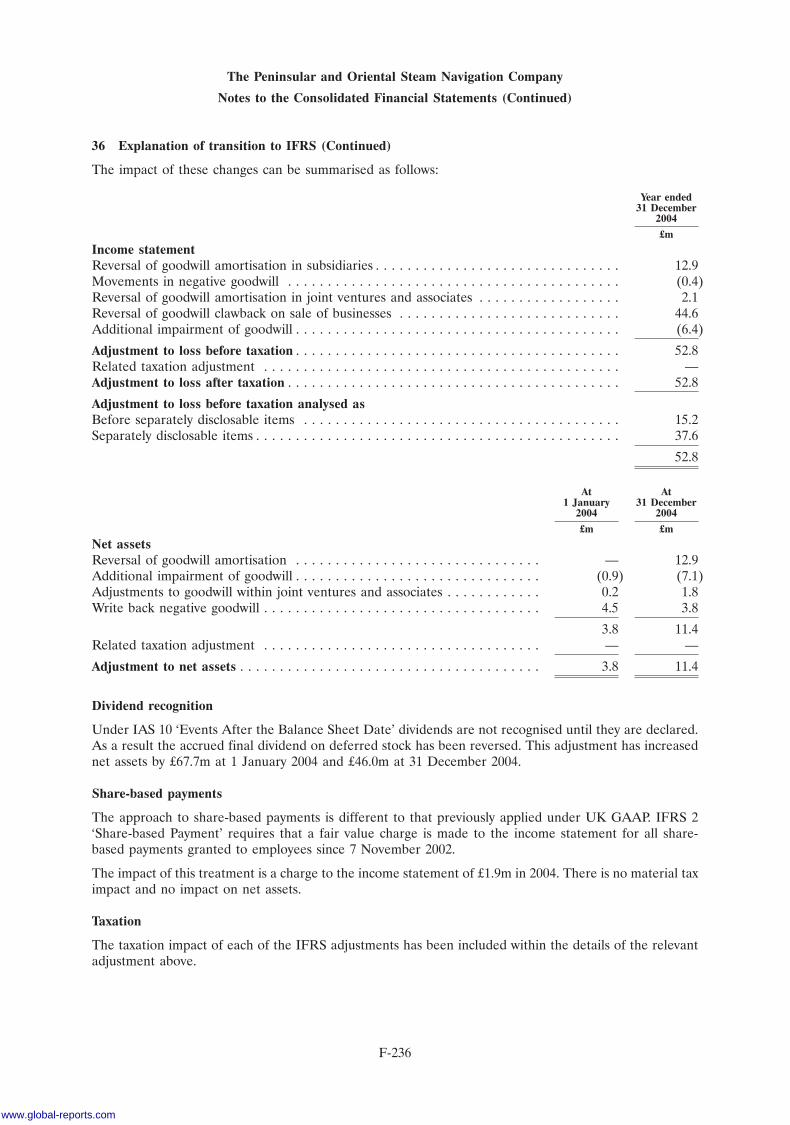

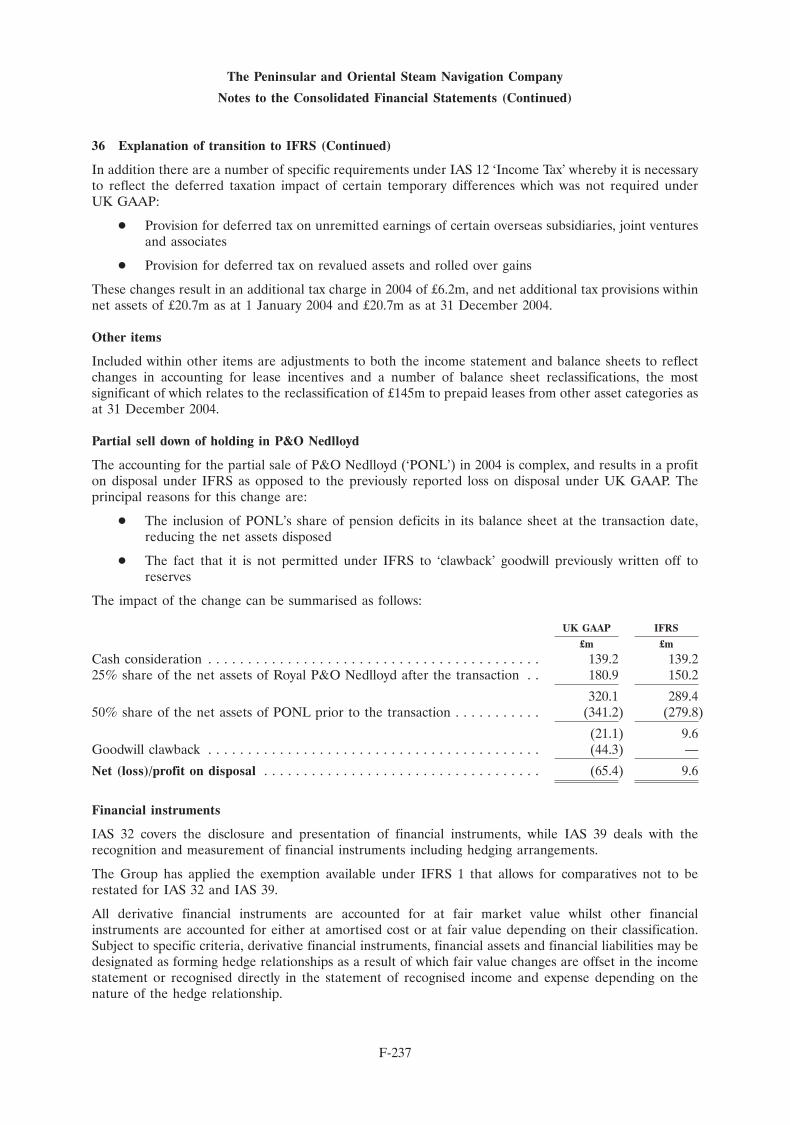

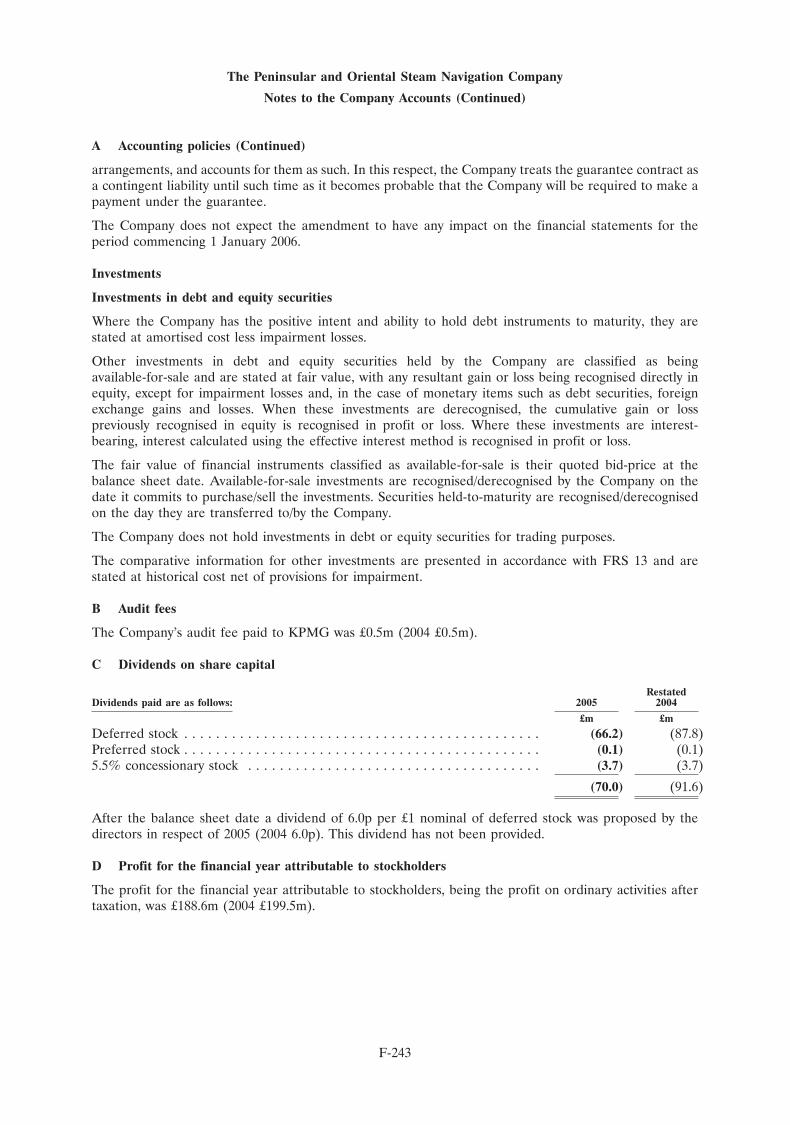

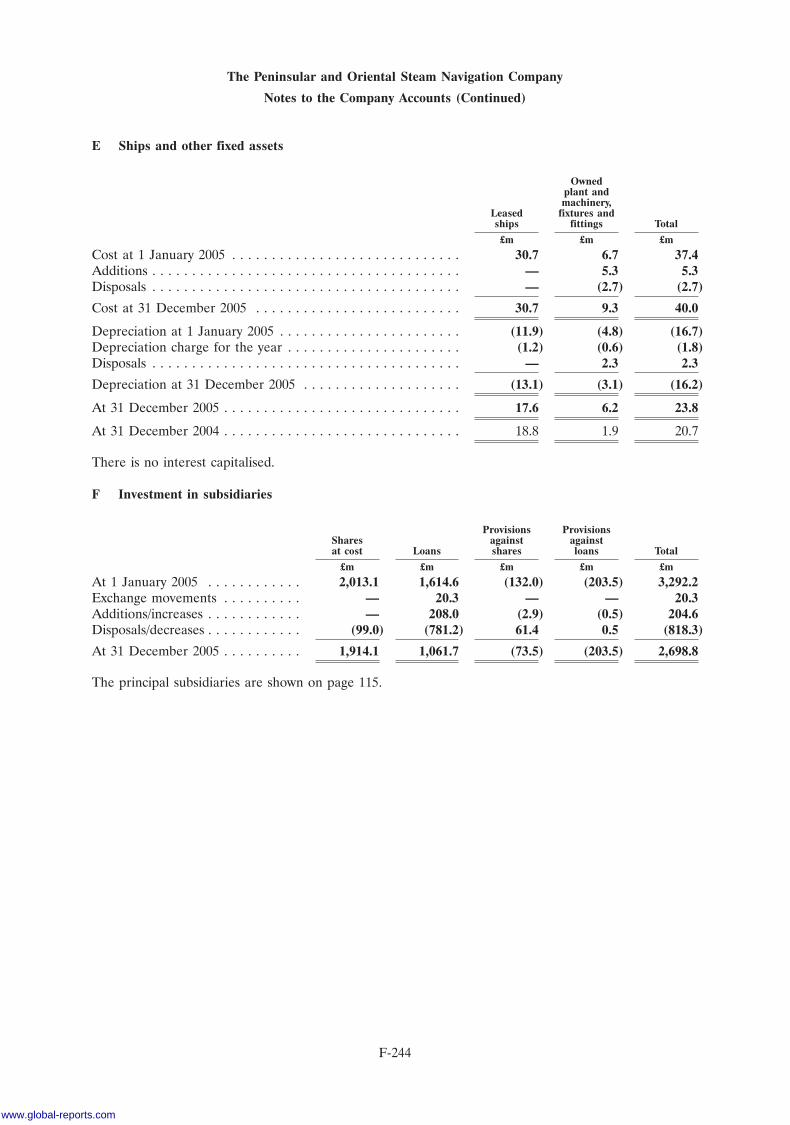

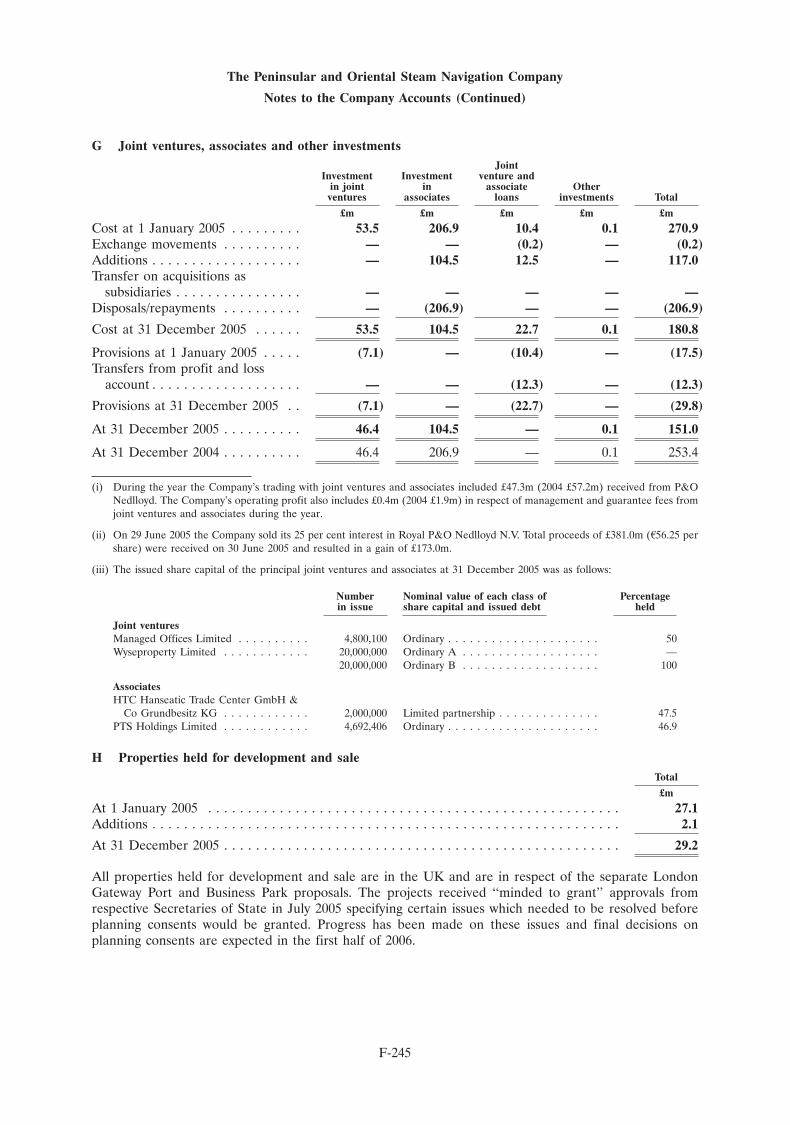

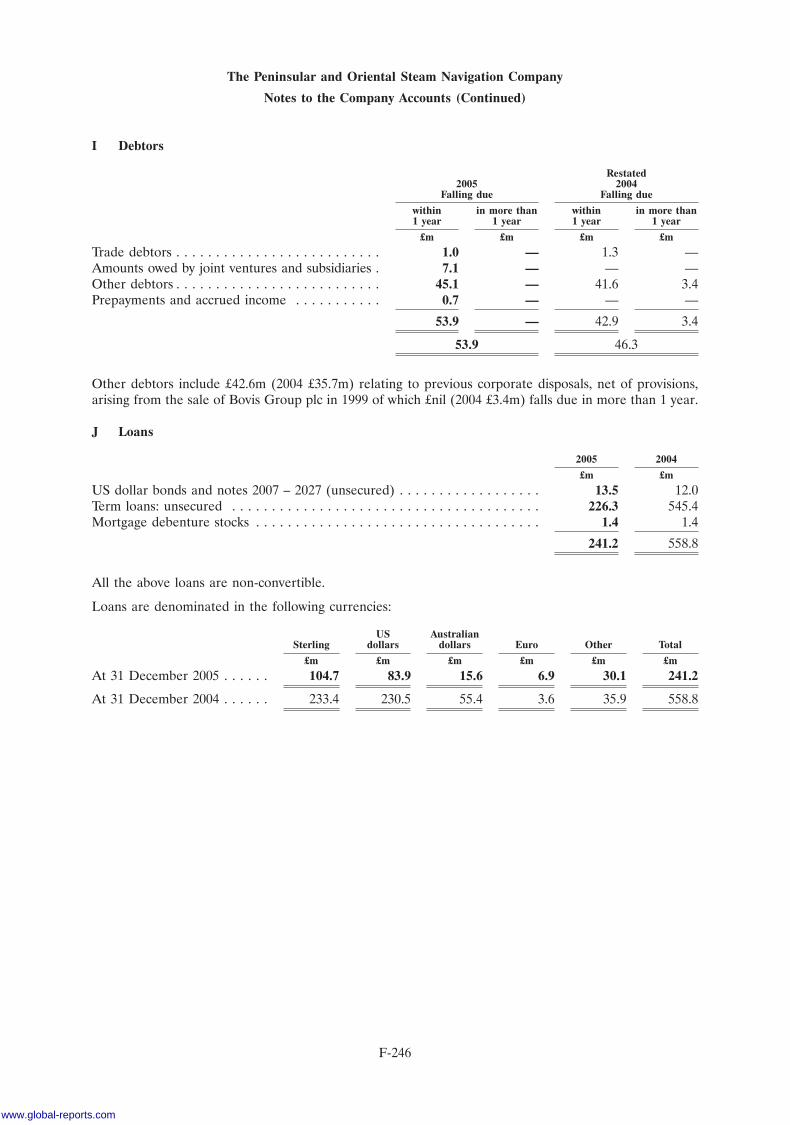

Embed Size (px)

Citation preview

30OCT200721261833

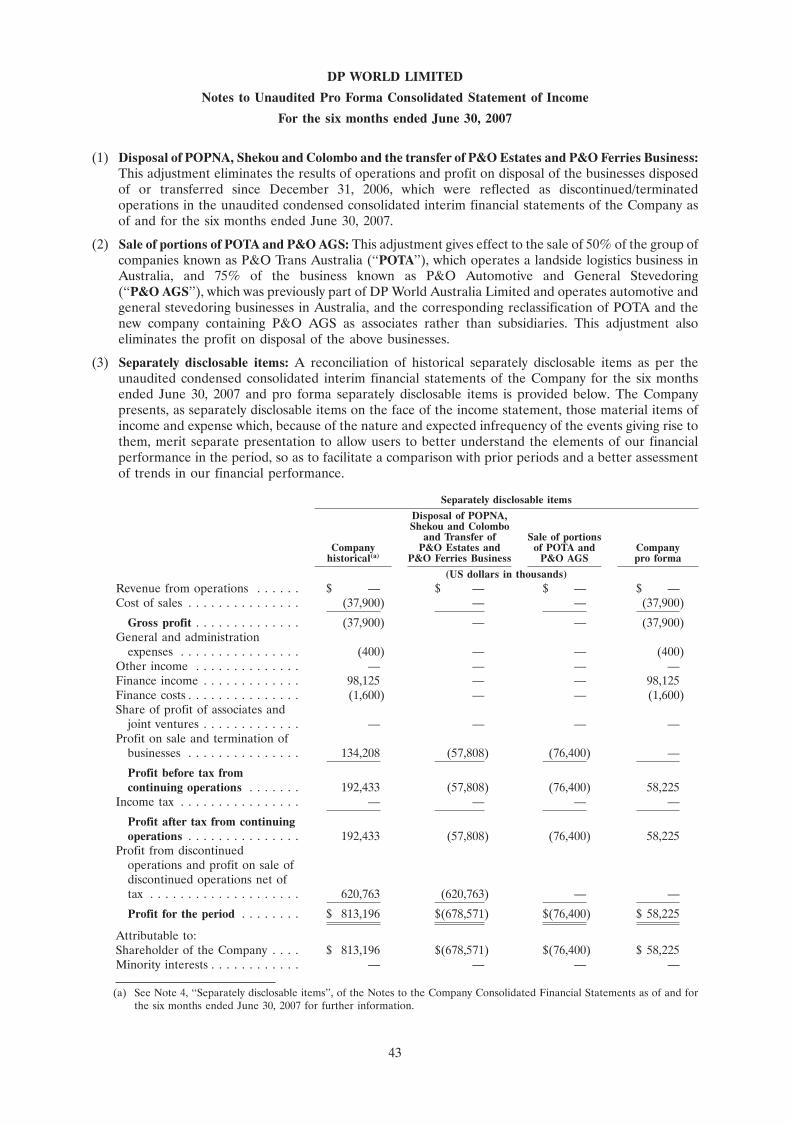

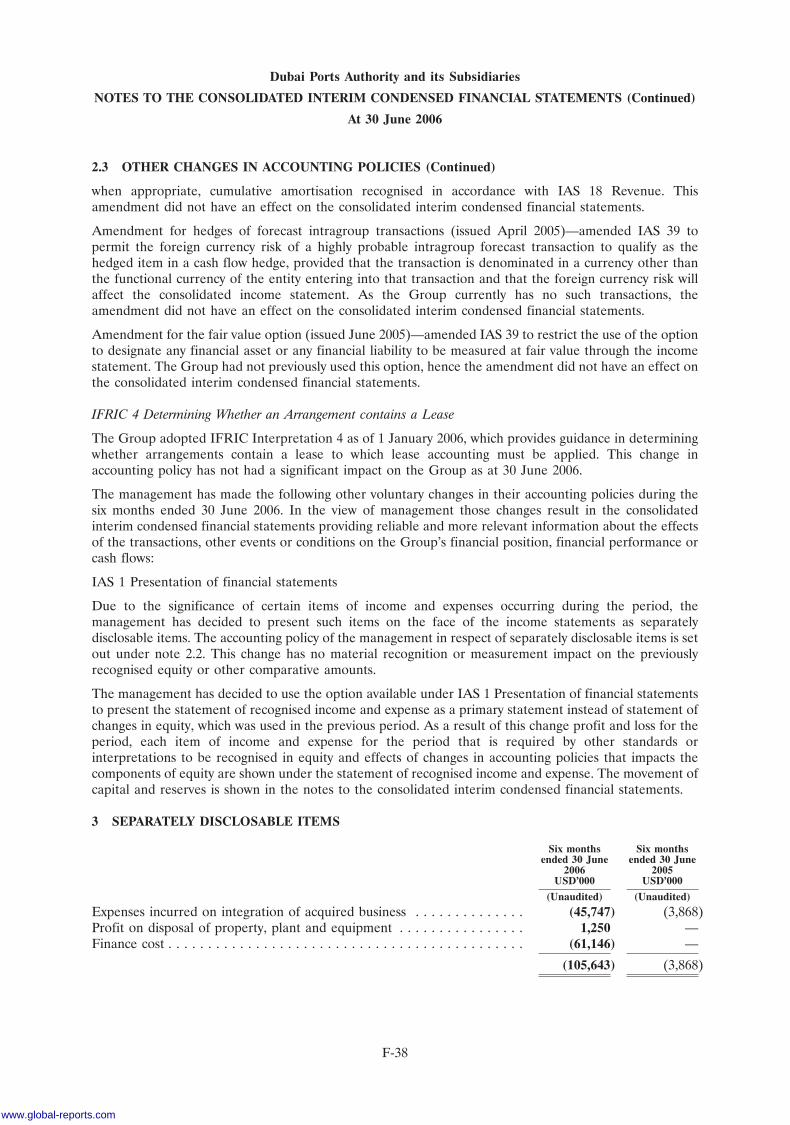

DP World Limited(a company limited by shares incorporated in the Dubai International Financial Centre)

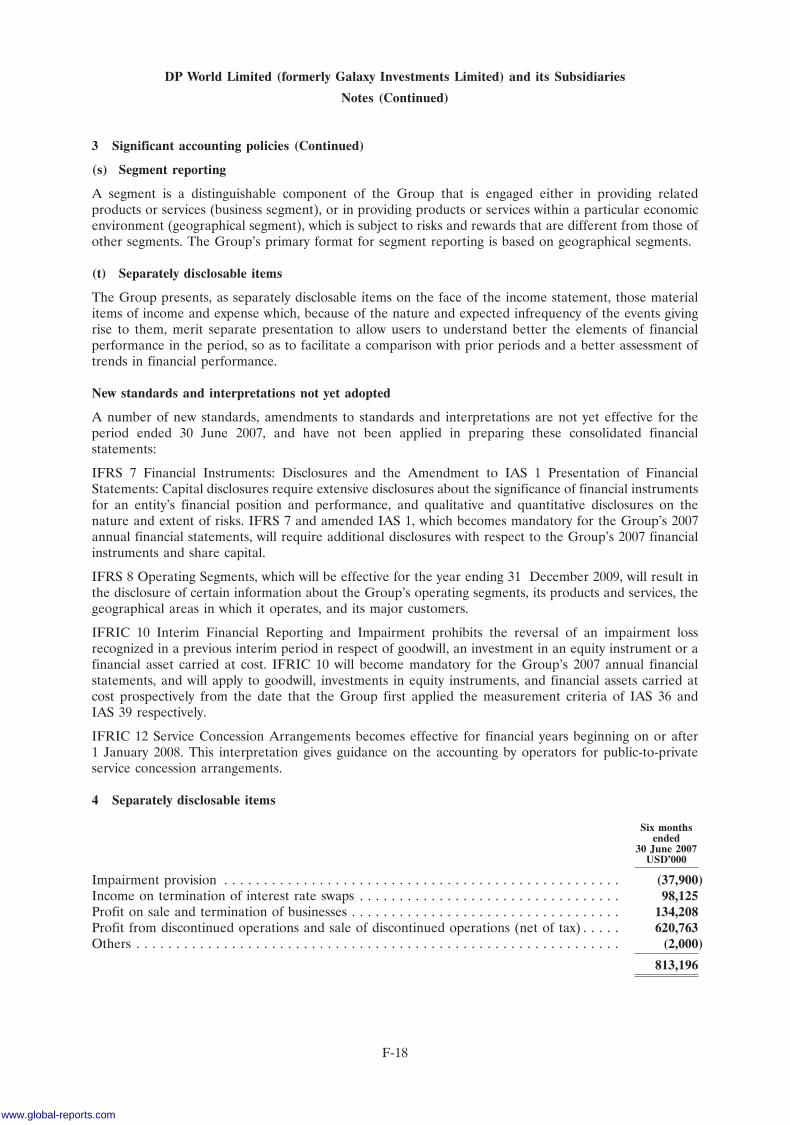

Global Offering of 3,245,300,000 Shares(subject to an over-allotment option in respect of up to 572,700,000 additional Shares)

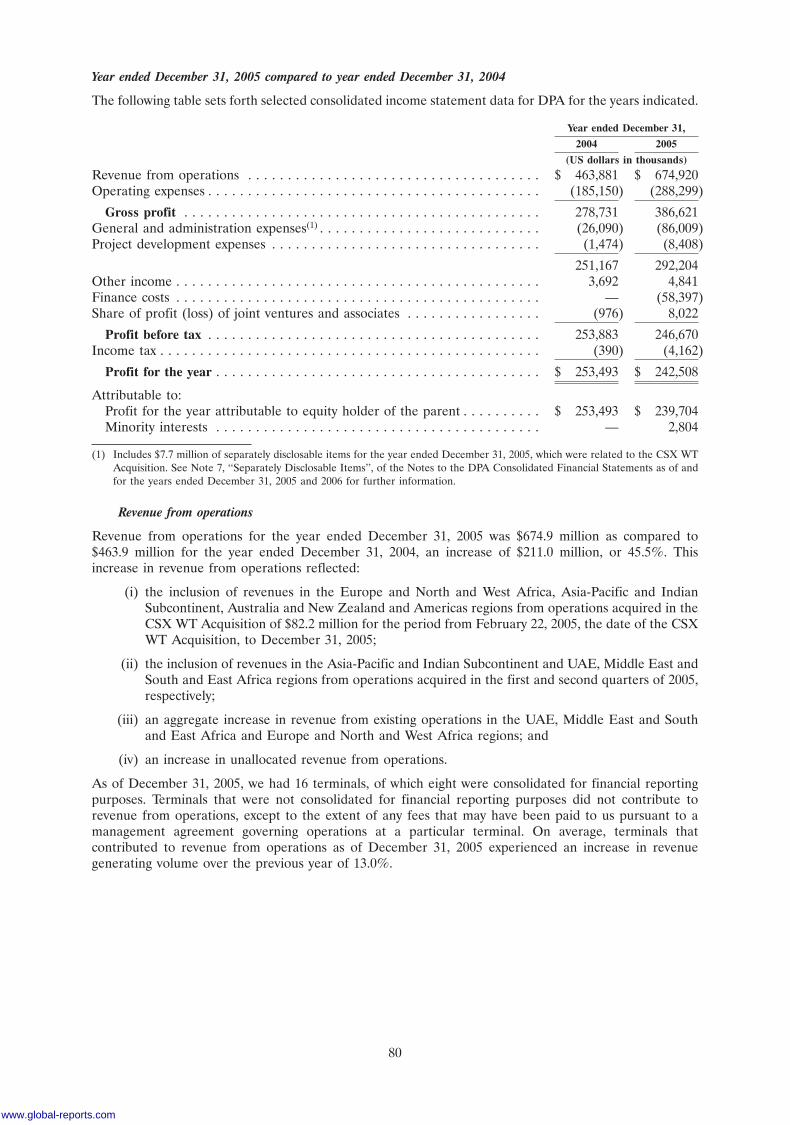

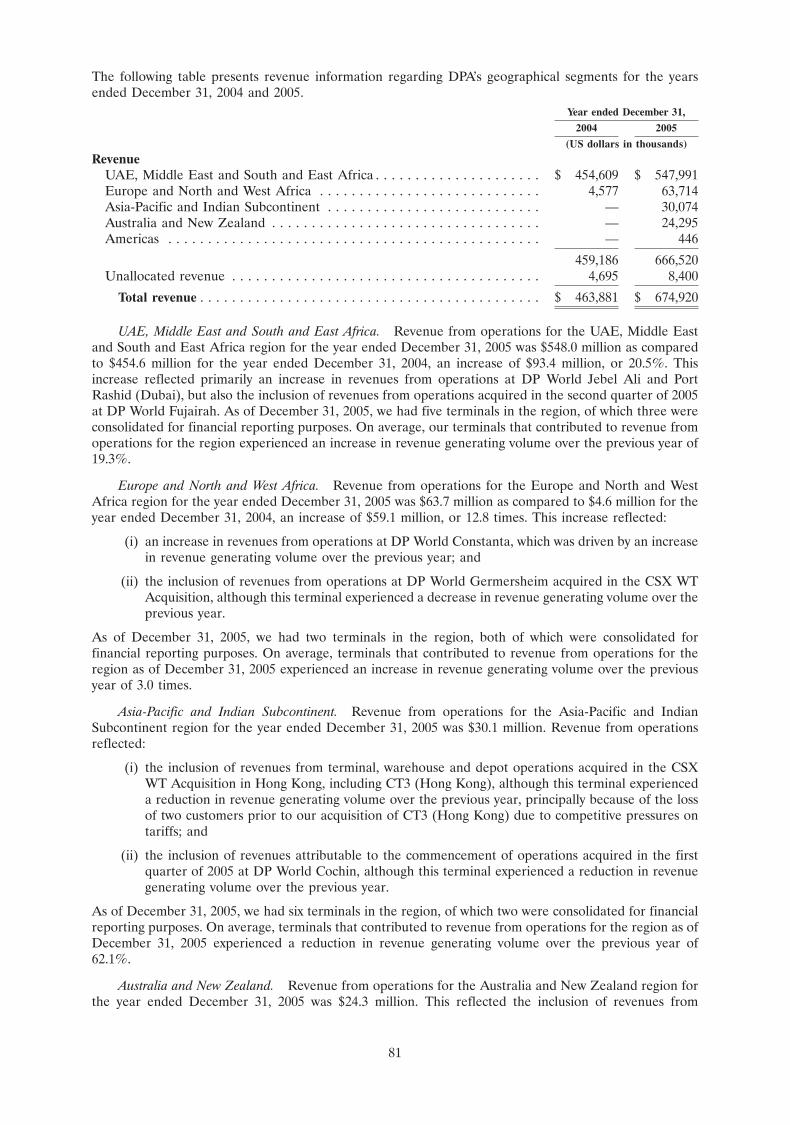

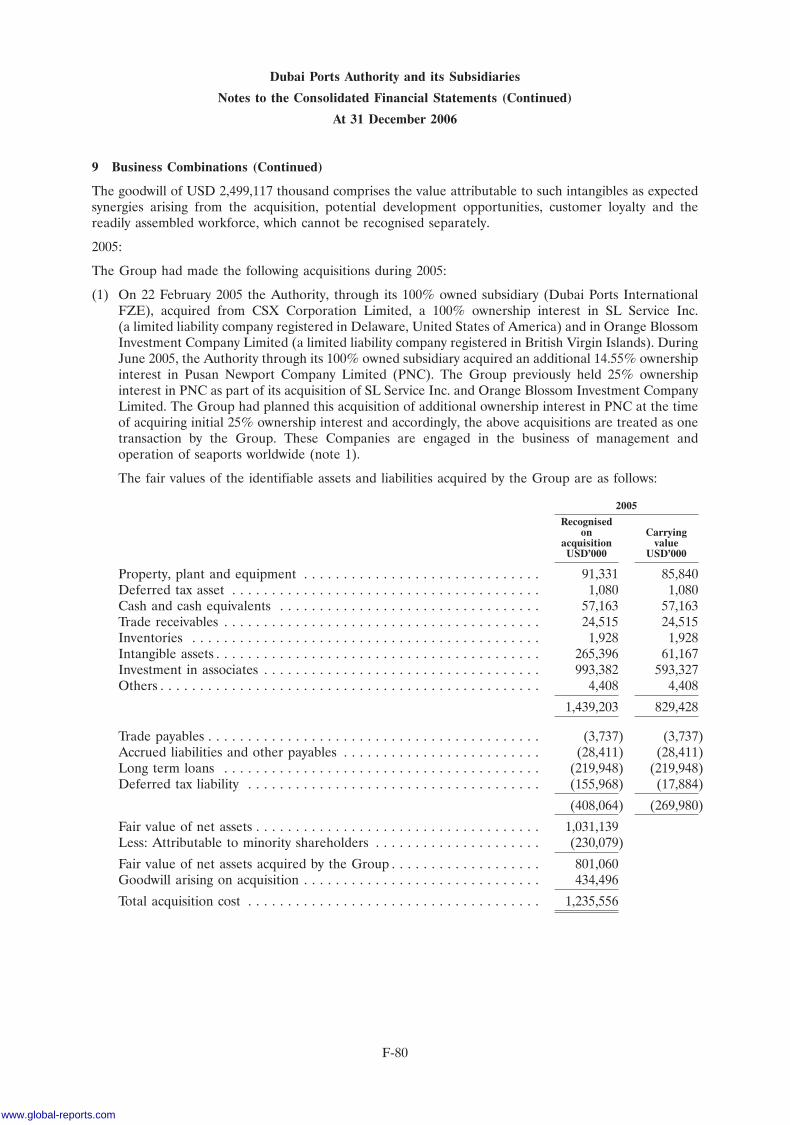

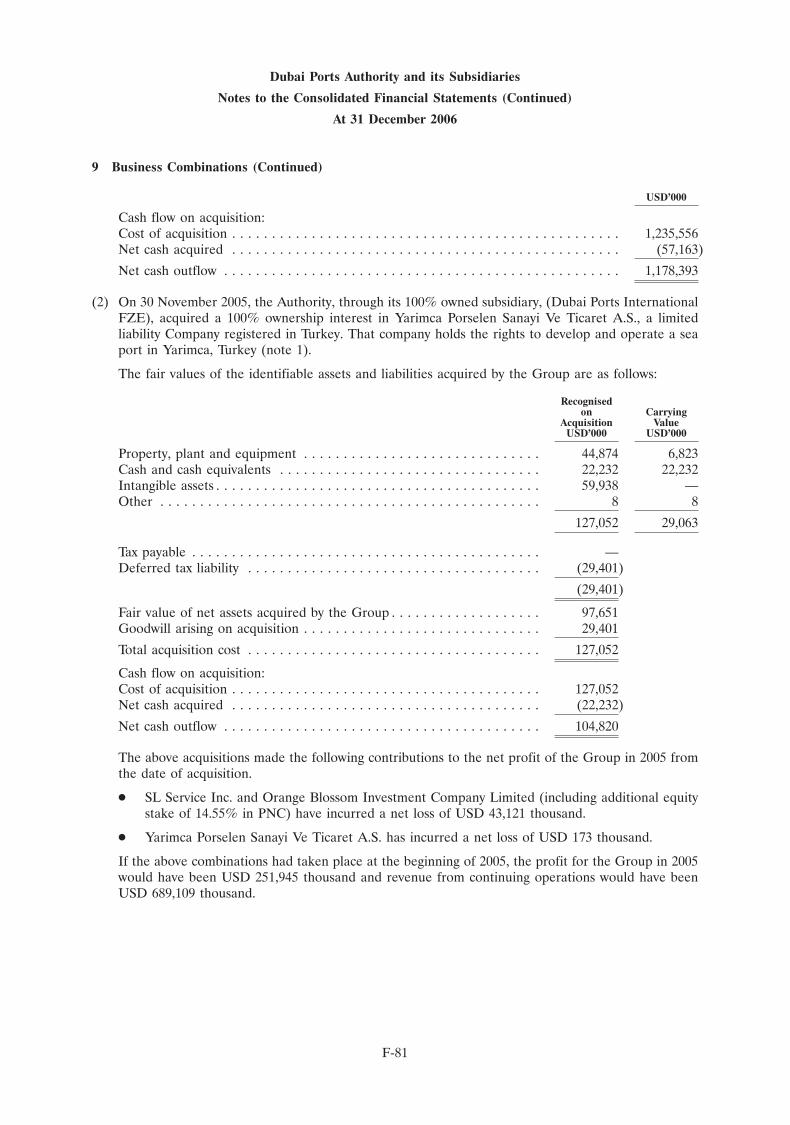

3,245,300,000 ordinary shares with a nominal value of $0.10 each (the ‘‘Shares’’) of DP World Limited (the ‘‘Company’’), acompany limited by shares incorporated in the Dubai International Financial Centre (the ‘‘DIFC’’), are being offered in thisglobal offering (the ‘‘Global Offering’’) by our sole shareholder, Port & Free Zone World FZE (the ‘‘Selling Shareholder’’).The Global Offering comprises an offering of (i) 2,129,527,994 Shares in the United States to qualified institutional buyers(each a ‘‘QIB’’) as defined in, and in reliance on, Rule 144A (‘‘Rule 144A’’) promulgated under the US Securities Act of1933, as amended (the ‘‘Securities Act’’), and outside the United States in reliance on Regulation S (‘‘Regulation S’’)promulgated under the Securities Act, including Shares being offered in the DIFC (the ‘‘Exempt Offer’’) pursuant to anexemption from registration under the Offered Securities Rules of the Dubai Financial Services Authority (the ‘‘DFSA’’)(collectively, the ‘‘International Offering’’), (ii) 307,692,306 Shares in the United Arab Emirates (the ‘‘UAE’’) to(A) nationals of the UAE or other Gulf Cooperation Council (‘‘GCC’’) countries who are resident in the UAE or anotherGCC country, (B) other UAE residents with a valid residency visa and (C) corporate entities organised under the laws ofthe UAE or another GCC country, who, in each case, hold a securities account with one of the participating brokers, applyfor Shares in the UAE and meet certain other requirements (the ‘‘UAE Retail Offer’’) and (iii) 808,079,700 Shares that willbe allocated to, or on behalf of, holders (the ‘‘Sukukholders’’) of the $3.5 billion Trust Certificates (Sukuk al Musharaka) due2008 (collectively, the ‘‘PCFC Development Sukuk’’) issued by the Company’s affiliate PCFC Development FZCO inconnection with the repayment in part of the PCFC Development Sukuk (the ‘‘Sukuk Allocation’’).Prior to the Global Offering, there has been no public market for the Shares. We have applied for the Shares to be admittedto the Official List of Securities of the Dubai International Financial Exchange (the ‘‘DIFX’’) and to list the Shares on theDIFX under the symbol ‘‘DPW’’ (the ‘‘DIFX Admission’’). There will be no conditional dealings in the Shares prior to theDIFX Admission. It is expected that the DIFX Admission will become effective and that dealings in the Shares will commenceon the DIFX on or about November 26, 2007 (the ‘‘Closing Date’’).

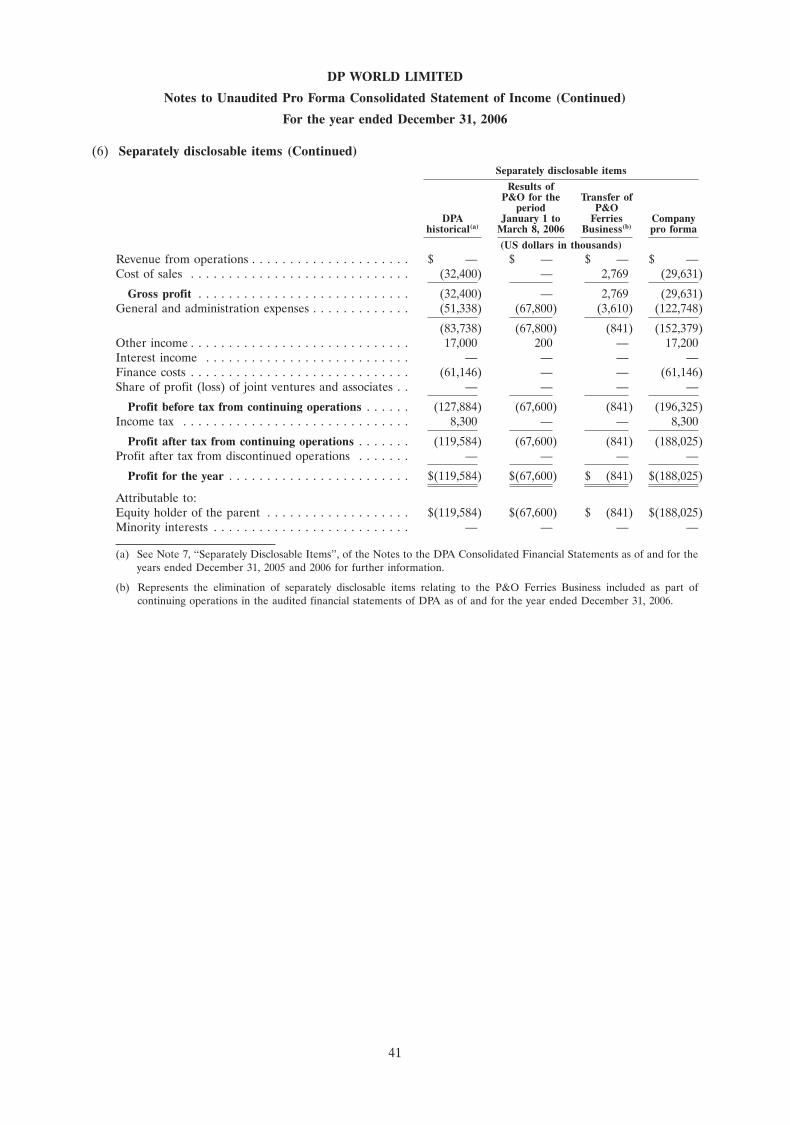

Investing in the Shares involves significant risks.

See ‘‘Risk Factors’’, including ‘‘Risks Relating to the DIFC and the DIFX’’, beginning on page 16.

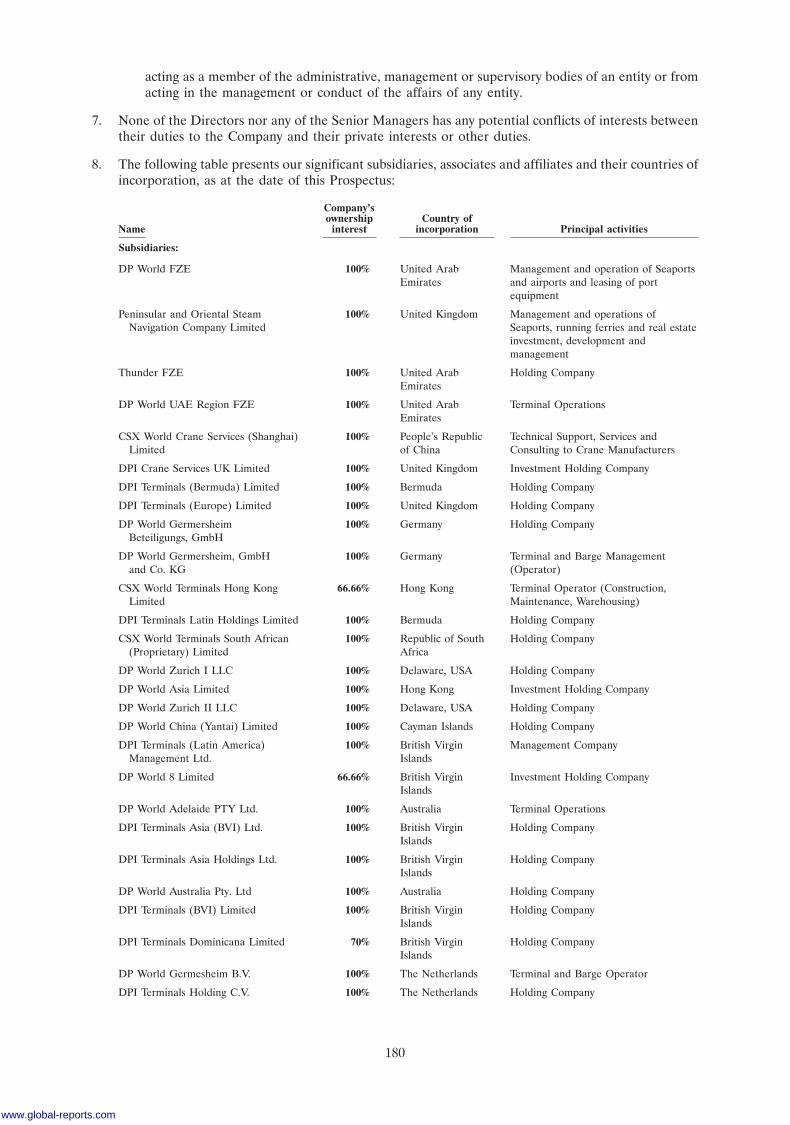

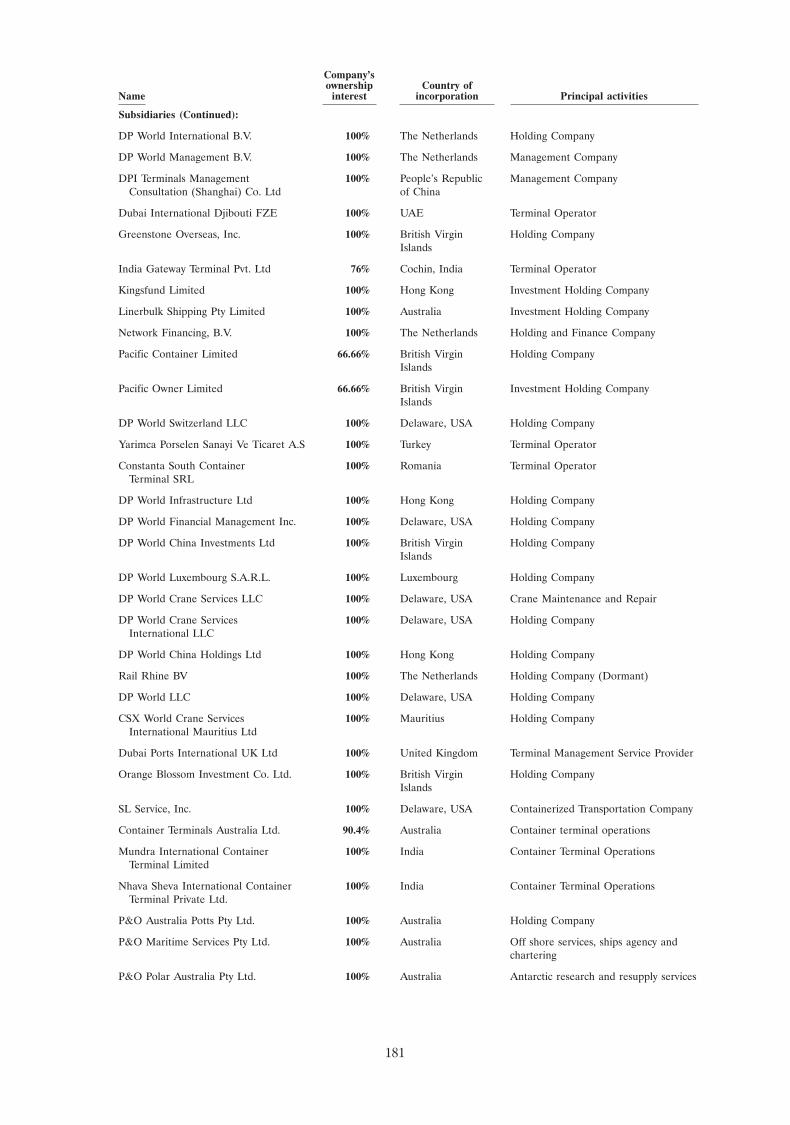

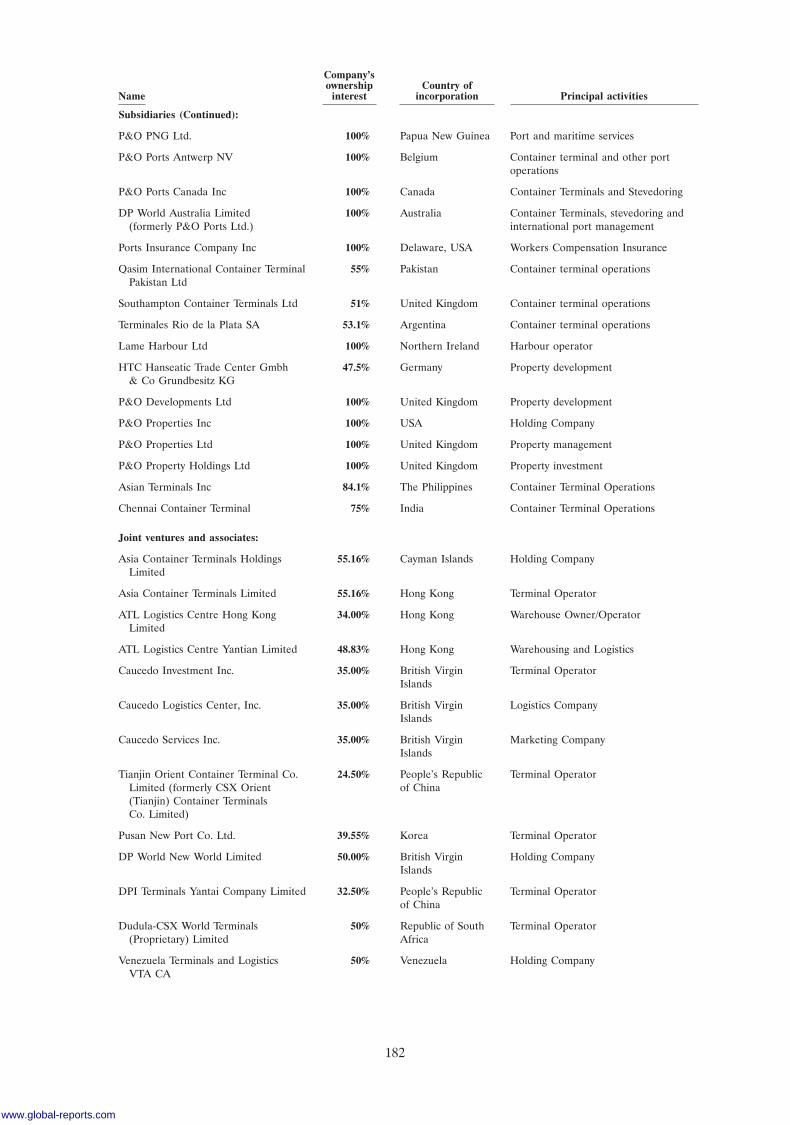

Offer Price: $1.30 per Share

The Shares have not been and will not be registered under the Securities Act and, subject to certain limited exceptions, maynot be offered or sold within the United States. The Shares are being offered and sold outside the United States in reliance onRegulation S and within the United States only to QIBs in reliance on Rule 144A. For a description of these and certain furtherrestrictions on offers, sales and transfers of the Shares and the distribution of this Prospectus, see ‘‘Subscription and Sale’’and ‘‘Transfer Restrictions’’.

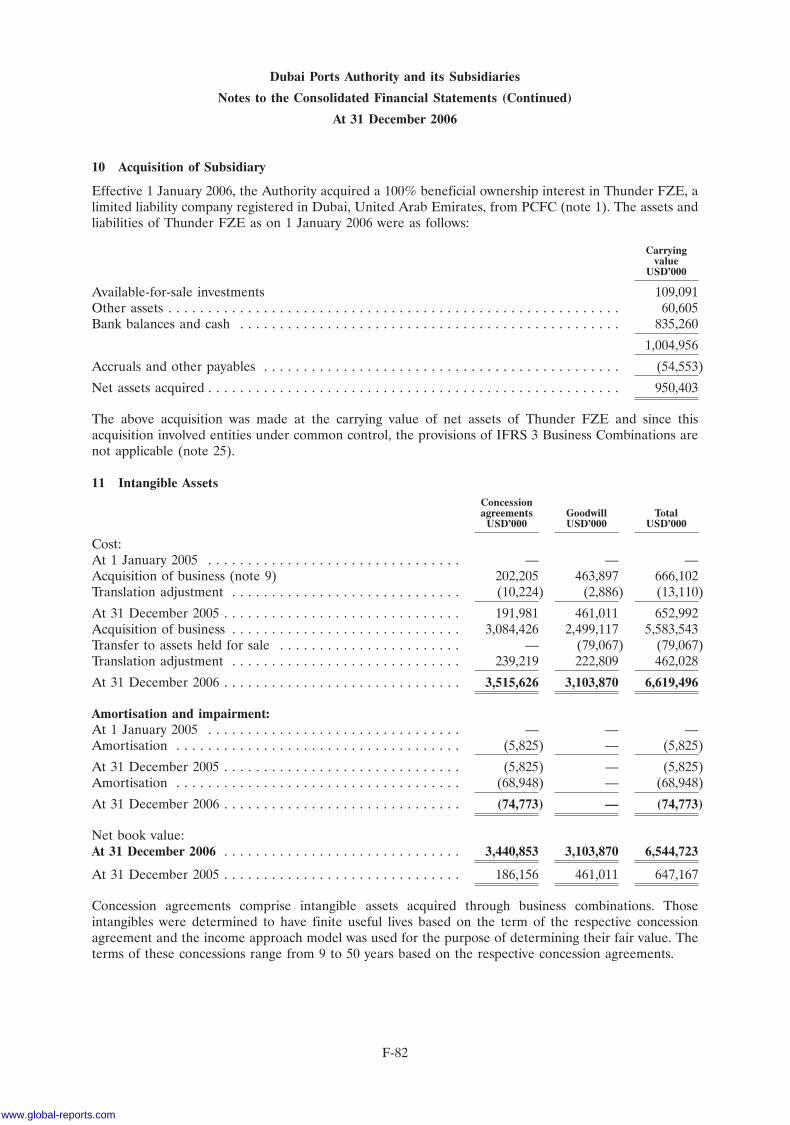

The Selling Shareholder has granted Deutsche Bank AG, London Branch (the ‘‘Stabilisation Manager’’), on behalf of theseveral Underwriters (as defined below), an over-allotment option (the ‘‘Over-allotment Option’’) to purchase up to anadditional 462,147,489 Shares at the initial offering price (the ‘‘Offer Price’’) within 30 days from the Closing Date to coverover-allotments, if any, made in connection with the Global Offering and to cover any short positions resulting fromstabilisation transactions. In addition, to the extent that the Over-allotment Option is exercised, up to an additional110,552,511 Shares will be allocated to, or on behalf of, Sukukholders.The Shares are offered by the Underwriters when, as and if delivered to, and accepted by, the Underwriters and subject totheir right to reject orders in whole or in part. Payment for, and delivery of, the Shares is expected to be made on thesettlement date, which is expected to be on or about the Closing Date, through the book-entry facilities of the CentralSecurities Depositary operated by the DIFX.The DIFX takes no responsibility for the contents of this Prospectus, makes no representations as to its accuracy orcompleteness and expressly disclaims any liability whatsoever for any loss howsoever arising from or in reliance upon any partof the contents of this Prospectus.

DIFC Exempt Offer Statement: This Prospectus relates to an Exempt Offer in accordance with the Offered Securities Rules ofthe DFSA. It is intended for distribution only to persons of a type specified in those rules. It must not be delivered to, or reliedon by, any other person. The DFSA has no responsibility for reviewing or verifying any documents in connection with ExemptOffers. The DFSA has not approved this Prospectus nor taken steps to verify the information set out in it and has noresponsibility for it. The securities to which this Prospectus relates may be illiquid and/or subject to restrictions on theirresale. Prospective purchasers of the securities offered should conduct their own due diligence on the securities. If you do notunderstand the contents of this Prospectus you should consult an authorised financial adviser.

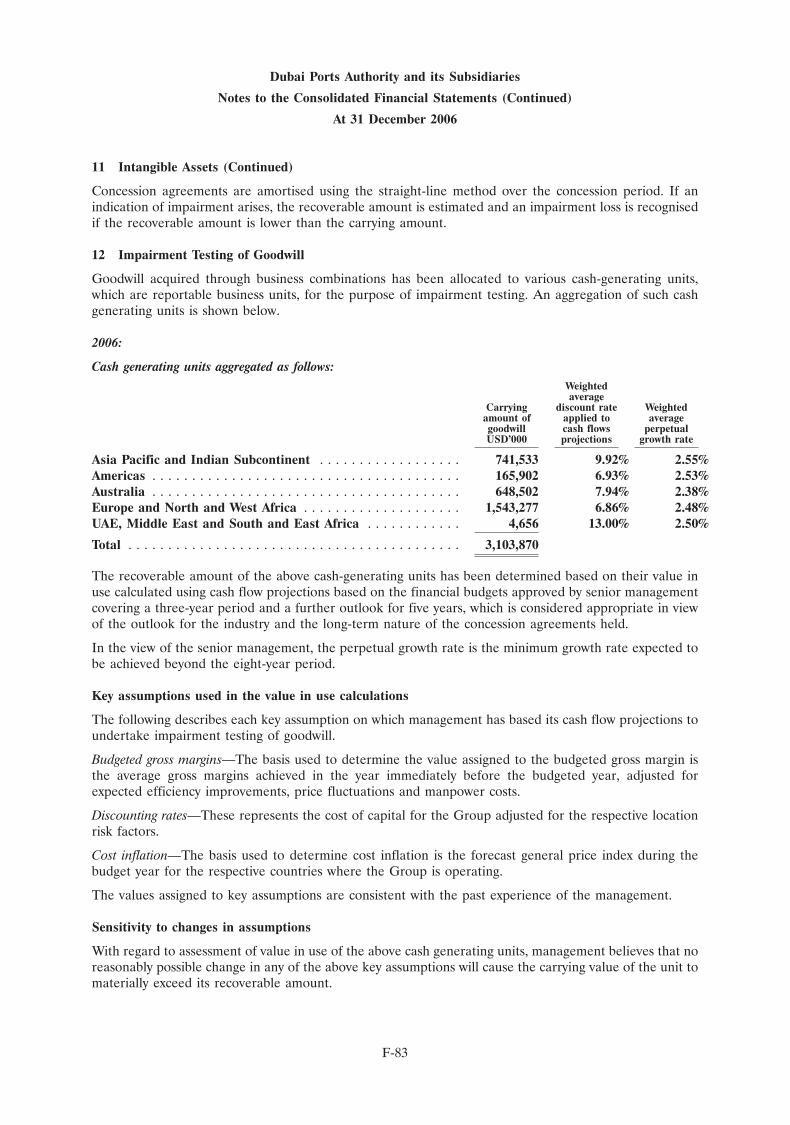

Joint Global Coordinators, Joint Bookrunners and Joint Lead Managers

Deutsche Bank Merrill Lynch Millennium Finance SHUAA CapitalInternational Corporation Ltd. PSC

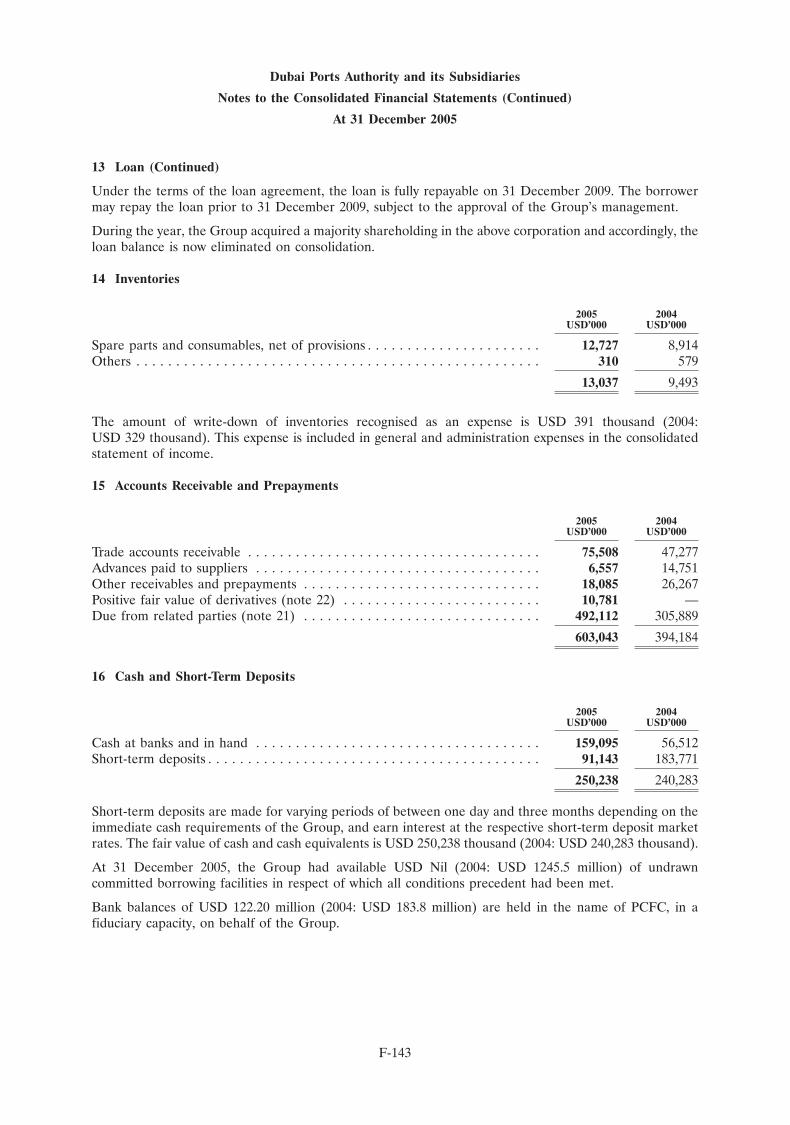

This Prospectus is dated November 21, 2007

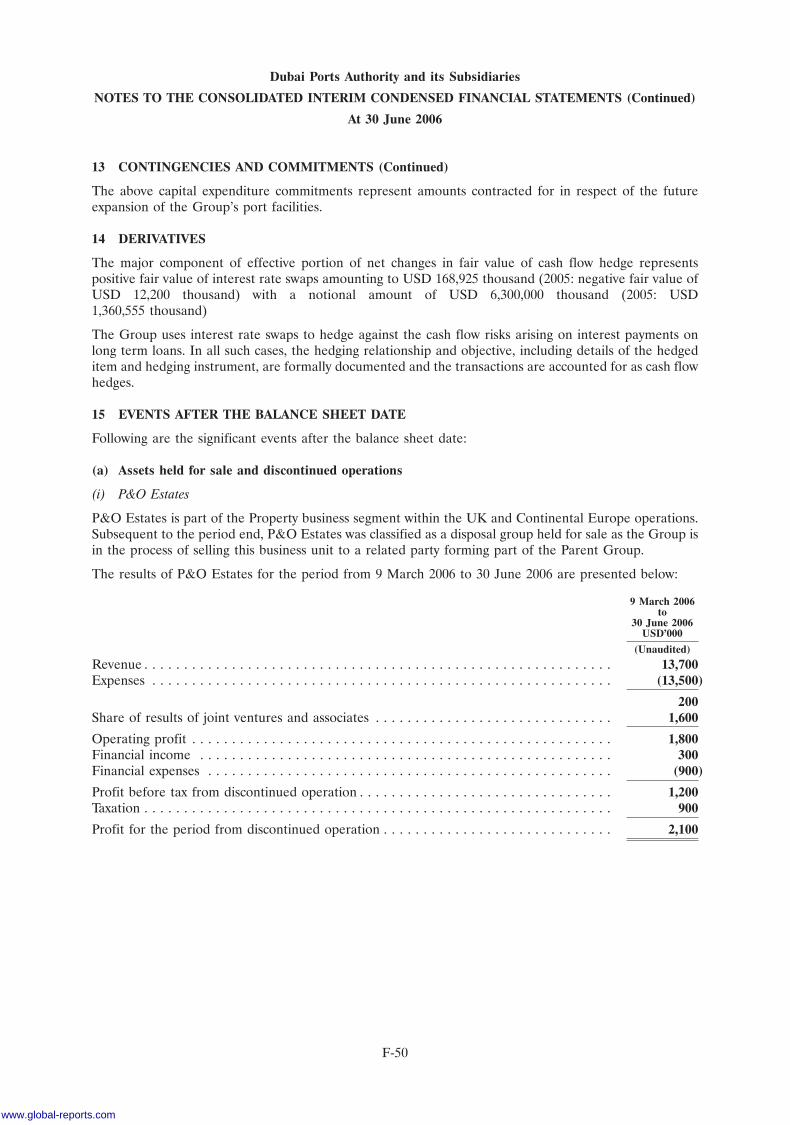

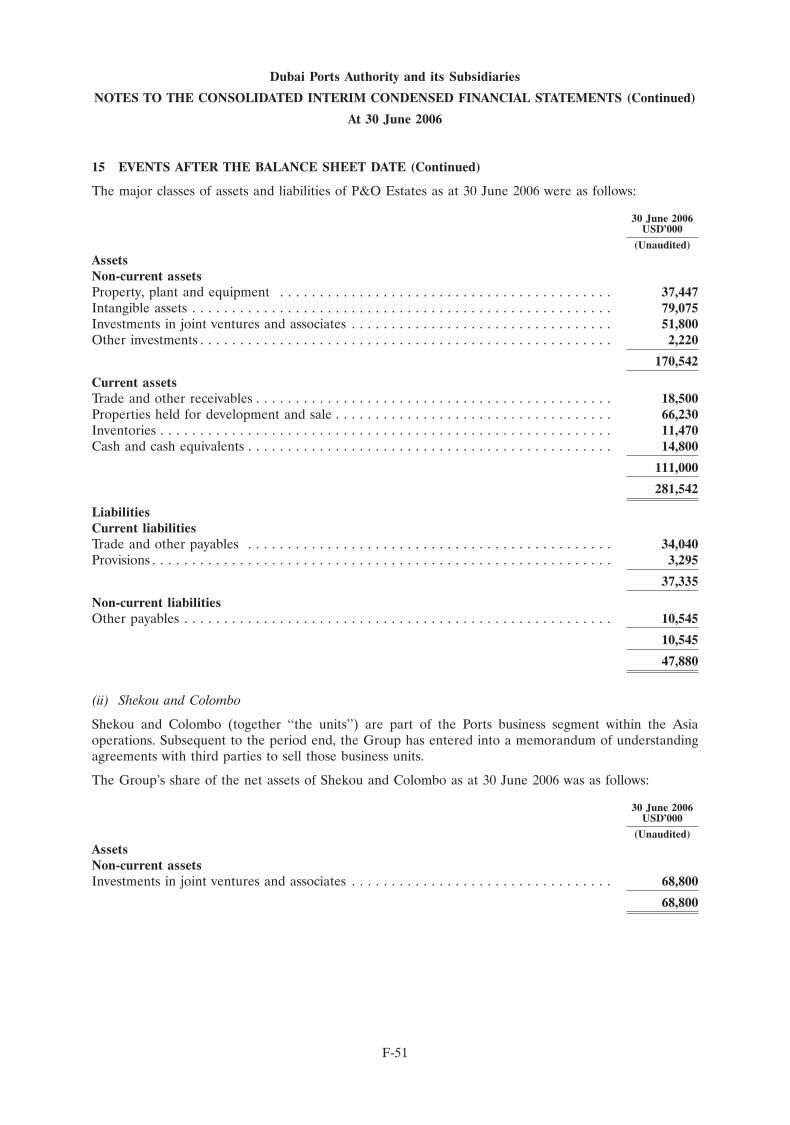

16OCT200720143290

www.global-reports.com

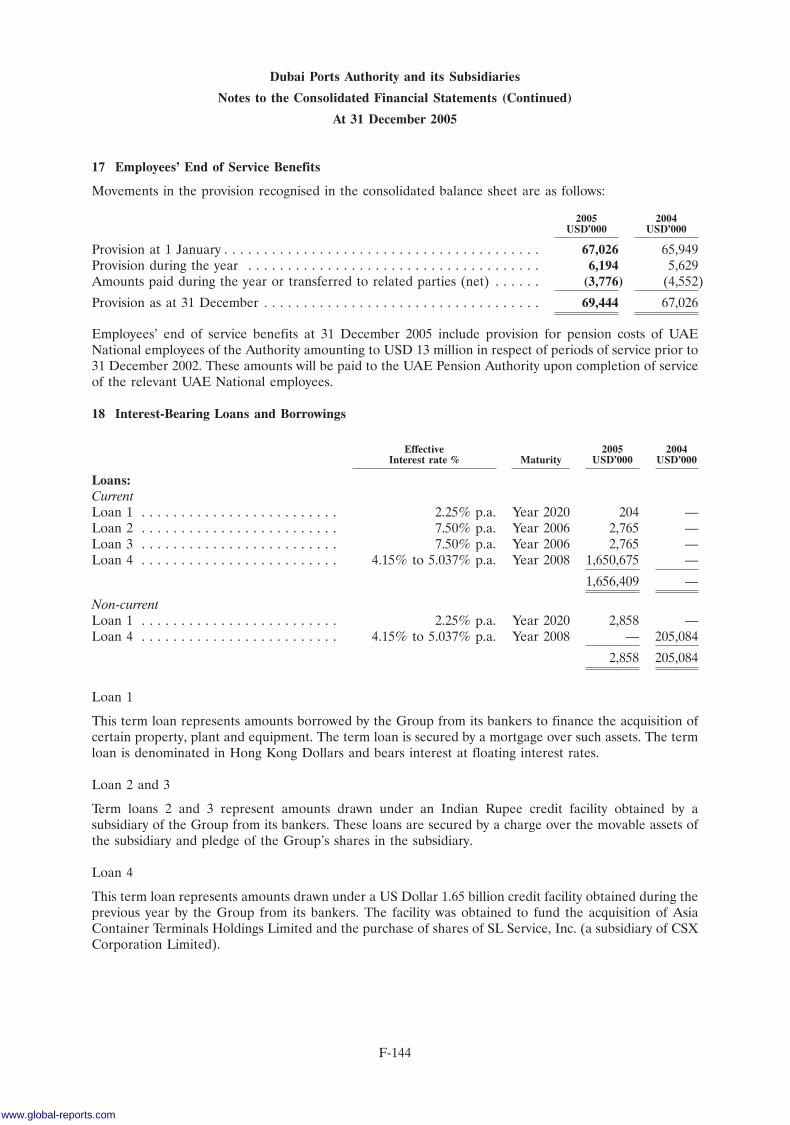

TABLE OF CONTENTS

Page

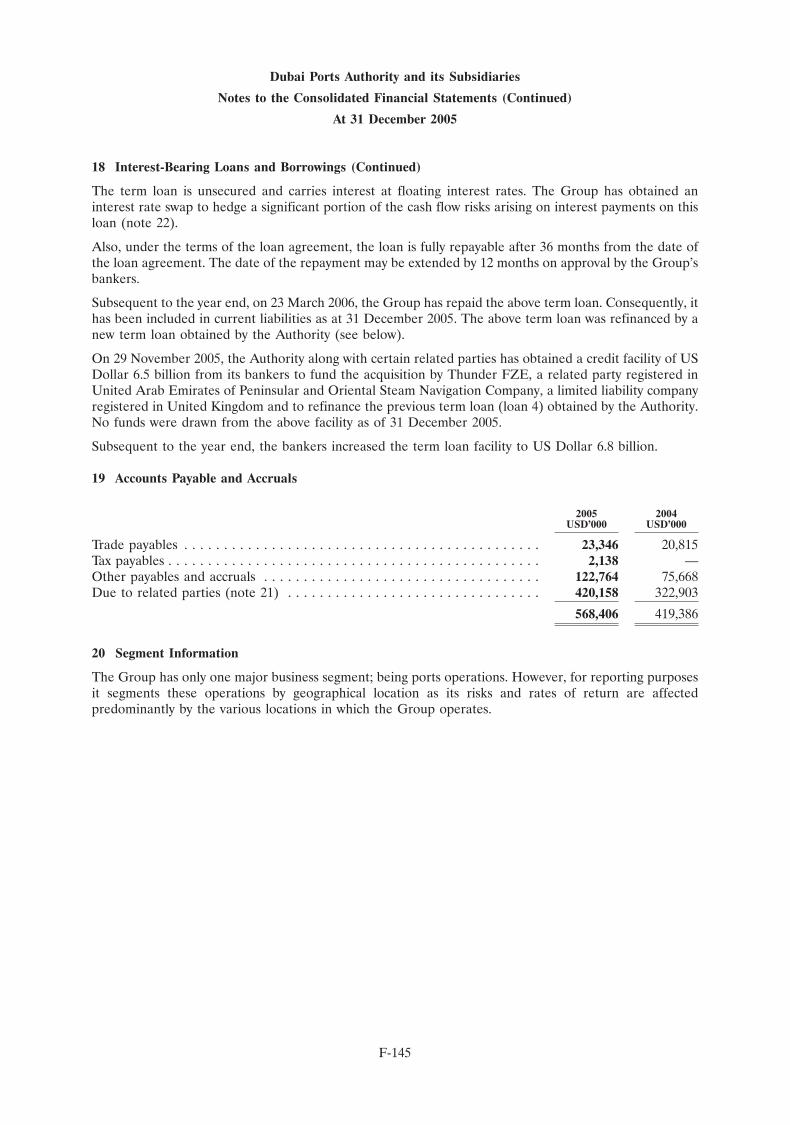

Notice to Investors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iiStabilisation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iiiNotice to UK Investors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iiiNotice to European Economic Area Investors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iiiNotice to Australian Investors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ivNotice to New Hampshire Residents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ivEnforcement of Foreign Judgments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ivCautionary Statement Regarding Forward-Looking Statements . . . . . . . . . . . . . . . . . . . . . . . . . ivPresentation of Certain Financial and Other Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . vNon-IFRS Measures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xPresentation of Market, Market Share and Industry Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xiAvailable Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xiSummary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1The Global Offering . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6Summary of Historical and Pro Forma Consolidated Financial and Operating Data . . . . . . . . . . 9Risk Factors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16Use of Proceeds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35Dividend Policy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36Exchange Rate Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37Unaudited Pro Forma Consolidated Financial Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38Selected Historical Consolidated Financial Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46Selected Historical Consolidated Financial Data of P&O . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50Management’s Discussion and Analysis of Financial Condition and Results of Operations . . . . . 53Industry Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100Business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 110Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 141Related Party Transactions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 146Principal and Selling Shareholder . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 149Description of Share Capital . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 150Clearance and Settlement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 158Description of the PCFC Development FZCO Sukuk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 159Overview of the UAE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 161Taxation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 164Subscription and Sale . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 167Transfer Restrictions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 174Legal Matters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 176Independent Auditors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 177Summary of Certain Differences Between IFRS and US GAAP . . . . . . . . . . . . . . . . . . . . . . . . 178Listing and General Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 179Index to Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F-1

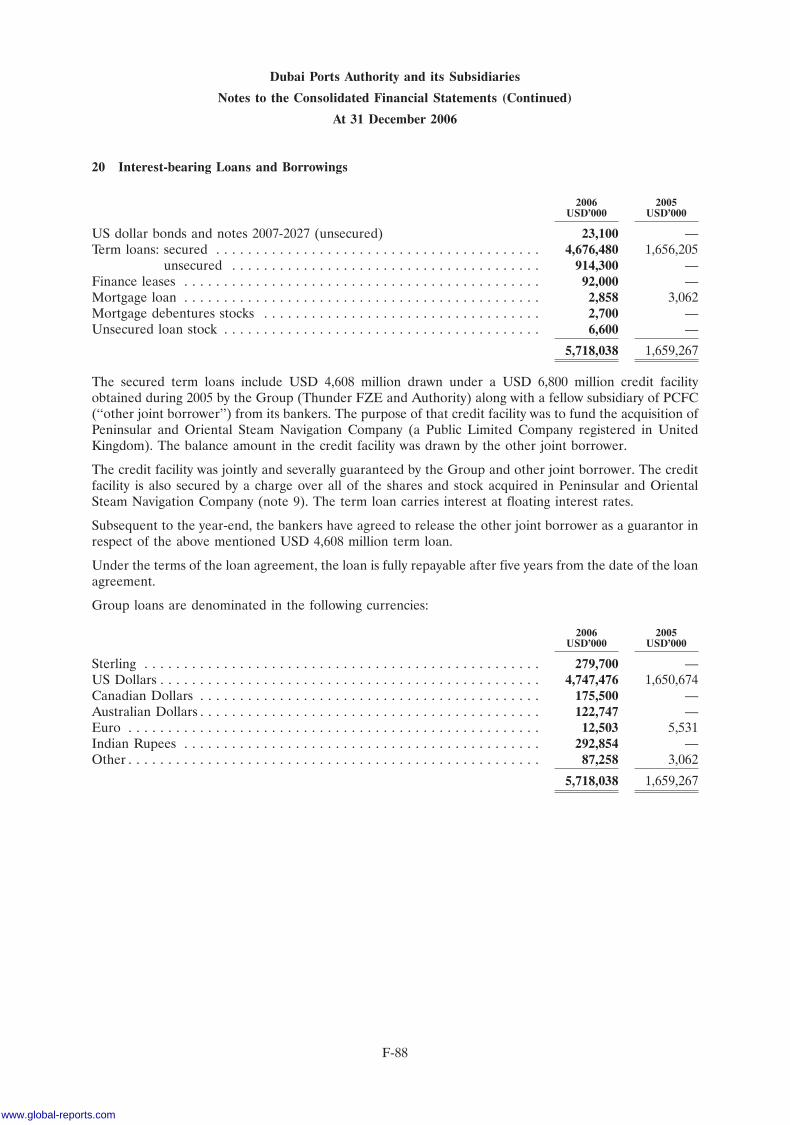

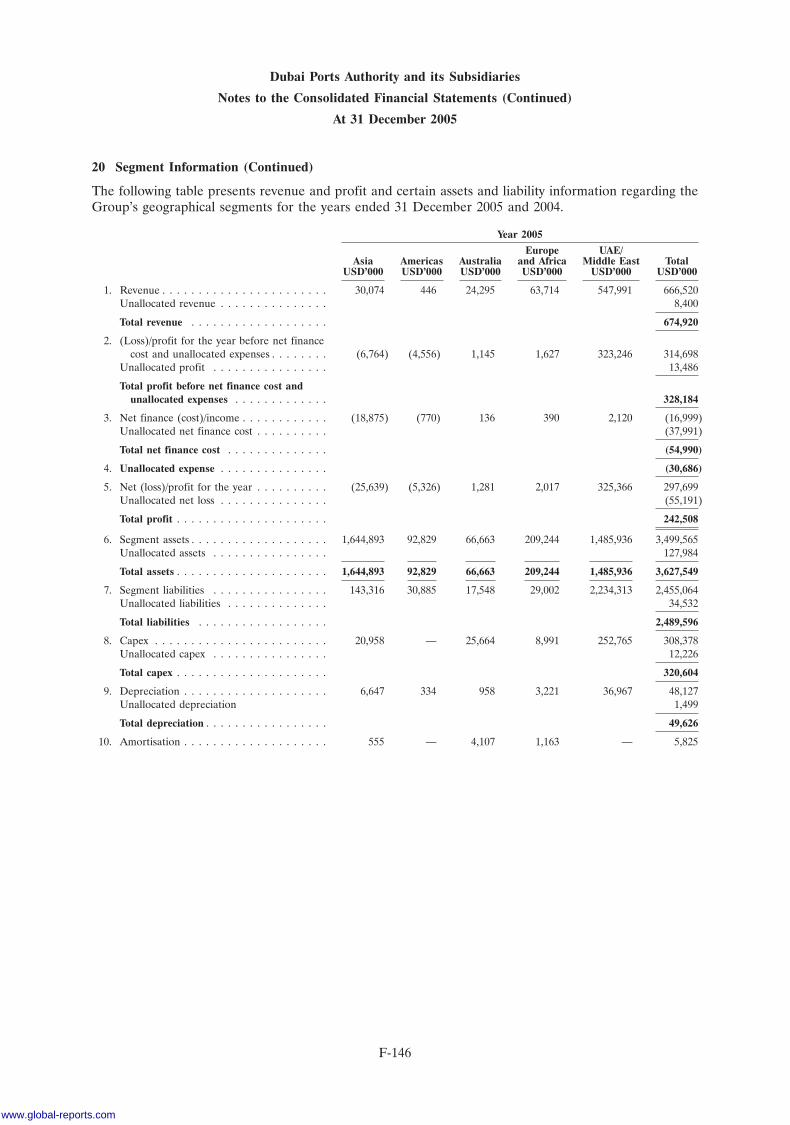

i

NOTICE TO INVESTORS

In this Prospectus, unless the context otherwise requires, the ‘‘Company’’ or the ‘‘Issuer’’ refers toDP World Limited, a company limited by shares incorporated in the DIFC, with Registration Number 0226issued on August 9, 2006, and ‘‘we’’, ‘‘our’’, ‘‘us’’ and the ‘‘Group’’ refer to the Company together with itsconsolidated subsidiaries, joint ventures and associates, as well as their respective predecessor companiesor entities, as applicable.

This Prospectus constitutes an Exempt Offer statement for purposes of Rule 3.2 of the Offered SecuritiesRules of the DFSA. This Prospectus is not a prospectus for purposes of Section 12(a)(2) or any otherprovision of, or rule under, the Securities Act.

To the best of the knowledge and belief of our directors, this Prospectus complies with the Markets Law2004 of the DIFC and the Offered Securities Rules of the DFSA and our directors accept responsibility,jointly and severally, for the information contained in this Prospectus and believe that there are no otherfacts the omission of which would make this Prospectus or any statement herein misleading or deceptive.The DFSA has no responsibility for reviewing or verifying any documents in connection with ExemptOffers. The DFSA has not approved this Prospectus nor taken steps to verify the information set out in itand has no responsibility for it.

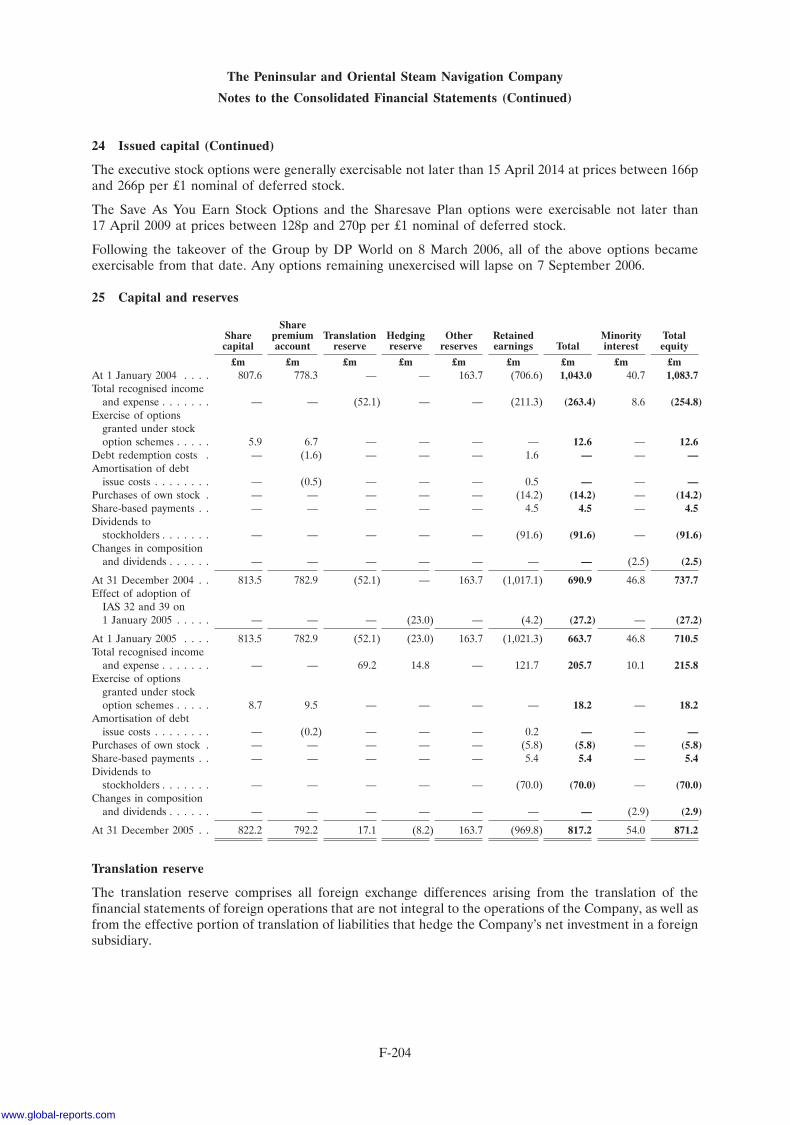

In making an investment decision, prospective investors must rely upon their own examination of us andthe terms of the Global Offering set out in this Prospectus, including the merits and risks involved.Prospective investors should exclusively rely on the information contained in this Prospectus. Neither wenor Deutsche Bank AG, London Branch, Merrill Lynch International, Millennium FinanceCorporation Ltd. or SHUAA Capital psc (collectively, the ‘‘Joint Global Coordinators’’) nor DeutscheBank AG, London Branch, Dubai Islamic Bank PJSC, Merrill Lynch International or SHUAA Capital psc(collectively, the ‘‘Underwriters’’) has authorised anyone, including any brokers participating in the UAERetail Offer, to provide prospective investors with information different from that contained in thisProspectus. The Joint Global Coordinators and the Underwriters make no representation or warranty,express or implied, as to the accuracy or completeness of the information contained in this Prospectus, andnothing contained in this Prospectus is, or shall be relied upon as, a promise or representation by the JointGlobal Coordinators, the Underwriters or their respective affiliates or advisors. The Joint GlobalCoordinators and the Underwriters are acting for the Company in relation to the Global Offering and forno one else and will not be responsible to anyone other than the Company for providing the protectionsafforded to their respective clients nor for providing advice in relation to the Global Offering or thecontents of this document or any transaction, arrangement or matter referred to herein. You agree to theforegoing by accepting delivery of this Prospectus. The information contained in this Prospectus is accurateonly as of the date of this Prospectus, regardless of the time of delivery of this Prospectus or of any sale ofour Shares.

The distribution of this Prospectus and the offering and sale of the Shares is restricted by law in certainjurisdictions, and this Prospectus does not constitute, and may not be used in connection with, any offer orsolicitation in any such jurisdiction or to any person to whom it is unlawful to make such offer orsolicitation. Other than in respect of the United Arab Emirates (the ‘‘UAE’’), no action has been or will betaken in any jurisdiction by us or the Joint Global Coordinators or the Underwriters that would permit apublic offering of the Shares or possession or distribution of a prospectus in any jurisdiction where actionfor that purpose would be required. The Shares have not been and will not be registered under theSecurities Act or with any securities regulatory authority of any state or other jurisdiction of the UnitedStates. The Shares may not be offered or sold within the United States, except in certain transactionsexempt from the registration requirements of the Securities Act.

The Shares are being offered and sold outside the United States in reliance on Regulation S and within theUnited States only to QIBs in reliance on Rule 144A. Prospective purchasers are hereby notified thatsellers of the Shares may be relying on the exemption from the provisions of Section 5 of the Securities Actprovided by Rule 144A. For a description of these and certain further restrictions on offers, sales andtransfers of Shares and distribution of this Prospectus, see ‘‘Subscription and Sale’’ and ‘‘TransferRestrictions’’.

Persons into whose possession this Prospectus may come are required by us, the Joint Global Coordinatorsand the Underwriters to inform themselves about and to observe the restrictions contained in thisProspectus. Neither we nor any of the Joint Global Coordinators or the Underwriters accepts any

ii

www.global-reports.com

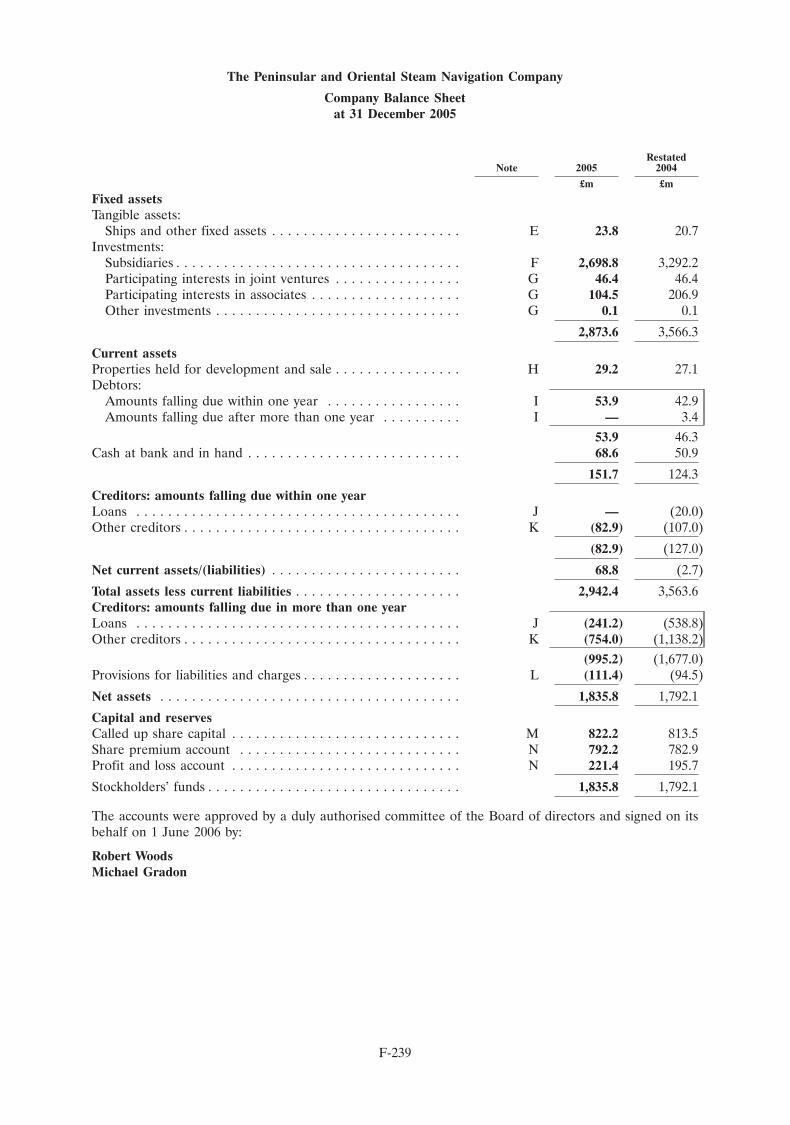

responsibility for any violation by any person, whether or not it is a prospective subscriber or purchaser ofthe Shares, of any of these restrictions.

Neither we nor any of the Joint Global Coordinators or the Underwriters, nor any of our or theirrespective representatives, make any representation to any purchaser of the Shares offered herebyregarding the legality of an investment by such purchaser under appropriate legal investment or similarlaws. Each purchaser should consult with its own advisors as to the legal, tax, business, financial and otherrelevant implications of the purchase of the Shares.

This Prospectus has been prepared by us in connection with the Global Offering solely for the purpose ofenabling a prospective investor to consider the purchase of the Shares. Reproduction and distribution ofthis Prospectus or disclosure or use of the information contained herein for any purpose other thanconsidering an investment in the Shares is prohibited.

NEITHER THE US SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIESCOMMISSION IN THE UNITED STATES NOR ANY OTHER US REGULATORY AUTHORITY HASAPPROVED OR DISAPPROVED OF THE SHARES OR PASSED UPON OR ENDORSED THE MERITSOF THE OFFERING OF THE SHARES OR THE ACCURACY OR ADEQUACY OF THIS PROSPECTUS.ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENCE IN THE UNITED STATES.

STABILISATION

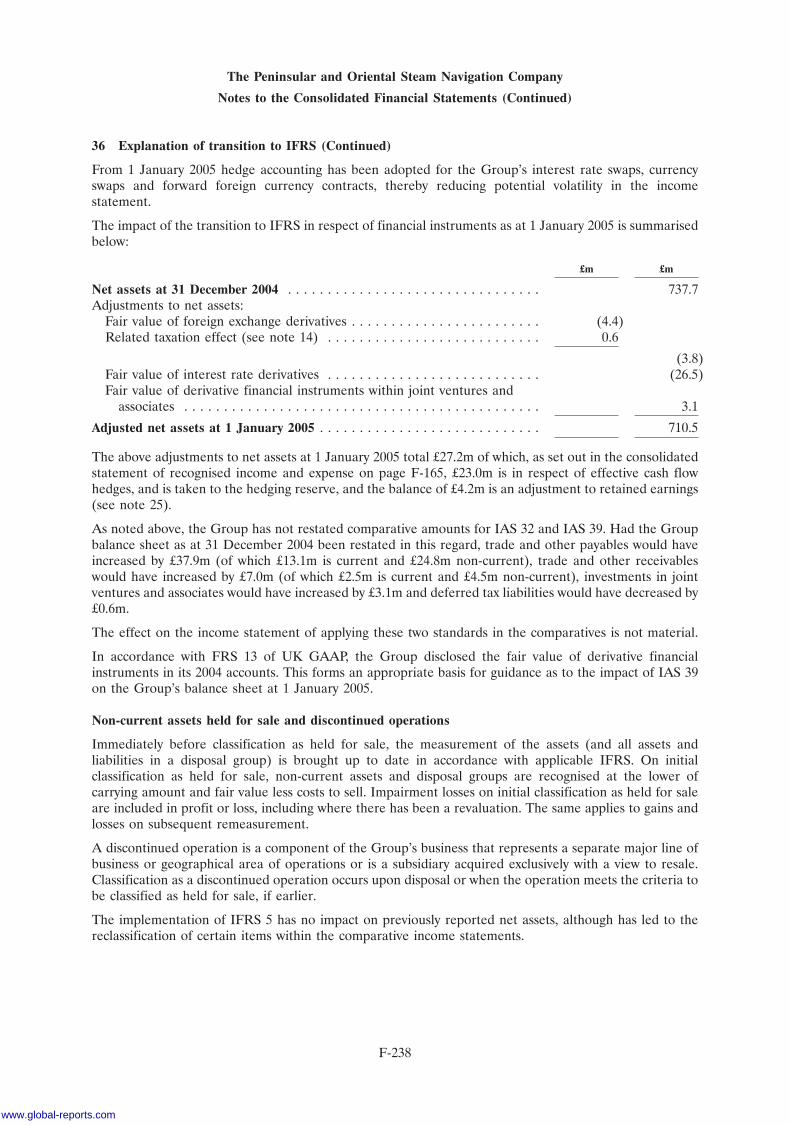

In connection with the Global Offering, the Stabilisation Manager, on behalf of the several Underwriters,or persons acting on its behalf, may over-allot the Shares or effect transactions that may support themarket price of the Shares at a level higher than that which might otherwise prevail. There is no assurance,however that the Stabilisation Manager, or any of its agents, will undertake stabilisation action. Any suchstabilisation may be conducted on the DIFX, in the open market or in over-the-counter transactions, ineach case, in accordance with the Price Stabilisation Module of the DFSA Rulebook. Such stabilisationactivities may be undertaken at any time during the period commencing on the date of the announcementof the Offer Price and ending on the date 30 days after the date of the Closing Date. Such stabilisation, ifcommenced, may be discontinued at any time without prior notice. The Stabilisation Manager has advisedus that in no event will measures be taken to stabilise the market price of the Shares above the Offer Price.The Stabilisation Manager has advised us that, except as required by law or regulation, neither theStabilisation Manager nor any of its agents intends to disclose the extent of any over-allotments madeand/or stabilisation transactions conducted in relation to the Global Offering.

NOTICE TO UK INVESTORS

This Prospectus is being distributed only to and is directed only at (i) persons who are outside the UnitedKingdom; (ii) investment professionals falling within Article 19(5) of the Financial Services and MarketsAct 2000 (Financial Promotion) Order 2005, as amended (the ‘‘Order’’); or (iii) high net worth entitiesfalling within Article 49(2)(a)-(d) of the Order (all such persons in (ii) and (iii) being referred to as‘‘relevant persons’’). The Shares are available only to, and any invitation, offer or agreement to purchase orotherwise acquire the Shares will be engaged in only with, relevant persons. Any person who is within theUnited Kingdom and not a relevant person should not act or rely on this Prospectus or any of its contents.

NOTICE TO EUROPEAN ECONOMIC AREA INVESTORS

This Prospectus and the Global Offering are only addressed to and directed at persons in member states ofthe European Economic Area that are ‘‘qualified investors’’ within the meaning of Article 2(i)(e) of theProspectus Directive (2003/71/EC (the ‘‘Prospectus Directive’’)). Any person in any member state of theEuropean Economic Area (the ‘‘EEA’’) other than the United Kingdom who is not such a qualifiedinvestor should not act or rely on this Prospectus or any of its contents.

This Prospectus has been prepared on the basis that all offerings of the Shares will be made pursuant to anexemption under the Prospectus Directive, as implemented in member states of the EEA, from therequirement to produce a prospectus for offerings of Shares. Accordingly, any person making or intendingto make any offering within the EEA of the Shares which are the subject of the Global Offering shouldonly do so in circumstances in which no obligation arises for us or any of the Joint Global Coordinators orthe Underwriters to produce a prospectus for such offering. Neither we nor any of the Joint GlobalCoordinators or the Underwriters have authorised or do authorise the making of any offering of the Shares

iii

through any financial intermediary, other than offerings made by the Joint Global Coordinators and theUnderwriters which constitute the final placement of the Shares contemplated in this Prospectus.

NOTICE TO AUSTRALIAN INVESTORS

This Prospectus has not been lodged with the Australian Securities and Investments Commission as adisclosure document under Chapter 6D of the Corporations Act 2001 (Cwth) (the ‘‘AustralianCorporations Act’’) and is not an offer to sell, or an invitation to purchase any Shares to persons in theCommonwealth of Australia who are not:

� investors falling within section 708(11) of the Australian Corporations Act; or

� investors falling within section 708(8) of the Australian Corporations Act.

NOTICE TO NEW HAMPSHIRE RESIDENTS

NEITHER THE FACT THAT A REGISTRATION STATEMENT OR AN APPLICATION FOR ALICENSE HAS BEEN FILED UNDER CHAPTER 421-B OF THE NEW HAMPSHIRE REVISEDSTATUTES ANNOTATED, 1955 (‘‘RSA 421-B’’), WITH THE STATE OF NEW HAMPSHIRE NORTHE FACT THAT A SECURITY IS EFFECTIVELY REGISTERED OR A PERSON IS LICENSEDIN THE STATE OF NEW HAMPSHIRE CONSTITUTES A FINDING BY THE SECRETARY OFSTATE OF NEW HAMPSHIRE THAT ANY DOCUMENT FILED UNDER RSA 421-B IS TRUE,COMPLETE AND NOT MISLEADING. NEITHER ANY SUCH FACT NOR THE FACT THAT ANEXEMPTION OR EXCEPTION IS AVAILABLE FOR A SECURITY OR A TRANSACTION MEANSTHAT THE SECRETARY OF STATE OF NEW HAMPSHIRE HAS PASSED IN ANY WAY UPONTHE MERITS OR QUALIFICATIONS OF, OR RECOMMENDED OR GIVEN APPROVAL TO,ANY PERSON, SECURITY OR TRANSACTION. IT IS UNLAWFUL TO MAKE, OR CAUSE TO BEMADE, TO ANY PROSPECTIVE PURCHASER, CUSTOMER OR CLIENT ANYREPRESENTATION INCONSISTENT WITH THE PROVISIONS OF THIS PARAGRAPH.

ENFORCEMENT OF FOREIGN JUDGMENTS

We are a company incorporated in, and under the laws issued by, the DIFC, with our headquarters in theEmirate of Dubai in the UAE. A substantial portion of our assets are located in a number of jurisdictionsoutside the United Kingdom and the United States. In addition, certain members of our board of directors(the ‘‘Board of Directors’’ or the ‘‘Board’’) and senior management reside in Dubai and all or a portion oftheir personal assets may be located in the UAE and/or other jurisdictions outside the United Kingdomand the United States. As a result, prospective investors may have difficulties effecting service of process inthe United Kingdom or the United States upon us or members of our Board of Directors or seniormanagement in connection with any lawsuits related to the Shares, including actions arising under the lawsof the United Kingdom or the federal securities laws of the United States. In the absence of any bilateraltreaty for the reciprocal enforcement of foreign judgments, UAE law sets out a procedure whereby thejudiciary of the UAE is able to ratify judgments, orders or awards of other jurisdictions. Such judgments,orders or awards which are ratified by the UAE court may be enforced within the UAE in the mannerprescribed by the Civil Procedure Code of the UAE. Investors may have difficulties in enforcing judgmentsof English or US courts against us or members of our Board of Directors or senior management in thecourts of the DIFC because the mechanism for enforcement of foreign judgments by the DIFC courts is asyet untested. Investors may also have difficulties in enforcing judgments of the DIFC courts and arbitrationawards ratified by the DIFC courts against us or members of our Board of Directors or seniormanagement in jurisdictions outside the DIFC because the mechanism for enforcement of judgments andawards issued by the DIFC courts in jurisdictions outside the DIFC is as yet untested.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Prospectus includes forward-looking statements. The words ‘‘anticipate’’, ‘‘believe’’, ‘‘expect’’, ‘‘plan’’,‘‘intend’’, ‘‘targets’’, ‘‘aims’’, ‘‘estimate’’, ‘‘project’’, ‘‘will’’, ‘‘would’’, ‘‘may’’, ‘‘could’’, ‘‘continue’’ andsimilar expressions are intended to identify forward-looking statements. All statements other thanstatements of historical fact included in this Prospectus, including, without limitation, those regarding ourfinancial position, business strategy, management plans and objectives for future operations, are forward-looking statements. These forward-looking statements involve known and unknown risks, uncertainties and

iv

www.global-reports.com

other factors, which may cause our actual results, performance or achievements, or industry results, to bematerially different from those expressed or implied by these forward-looking statements. These forward-looking statements are based on numerous assumptions regarding our present and future businessstrategies and the environment in which we expect to operate in the future. Important factors that couldcause our actual results, performance or achievements to differ materially from those in the forward-looking statements include, among other factors referenced in this Prospectus:

� our ability to integrate our newly-acquired operations and any future expansion of our business;

� our ability to realise the benefits we expect from existing and future investments in our existingoperations and pending expansion and development projects;

� our ability to obtain requisite governmental or regulatory approvals to undertake planned orproposed terminal development projects;

� our ability to obtain external financing or maintain sufficient capital to fund our existing andfuture operations;

� changes in political, social, legal or economic conditions in the markets in which we and ourcustomers operate;

� changes in the competitive environment in which we and our customers operate;

� our ability to secure or renew concessions at future or existing facilities;

� failure to comply with regulations applicable to our business;

� fluctuations in the currency exchange rates in the markets in which we operate;

� actions taken by our joint venture partners that may not be in accordance with our policies andobjectives; and

� actions taken by our controlling shareholder, Dubai World Corporation (‘‘Dubai World’’), thatare not in line with, or may conflict with, the best interests of the Company and/or our othershareholders.

Additional factors that could cause actual results, performance or achievements to differ materiallyinclude, but are not limited to, those discussed under ‘‘Risk Factors’’. Forward-looking statements speakonly as of the date of this Prospectus and we expressly disclaim any obligation or undertaking to publiclyupdate or revise any forward-looking statements in this Prospectus to reflect any change in ourexpectations or any change in events, conditions or circumstances on which these forward-lookingstatements are based. Given the uncertainties of forward-looking statements, we cannot assure you thatprojected results or events will be achieved and we caution you not to place undue reliance on thesestatements.

PRESENTATION OF CERTAIN FINANCIAL AND OTHER INFORMATION

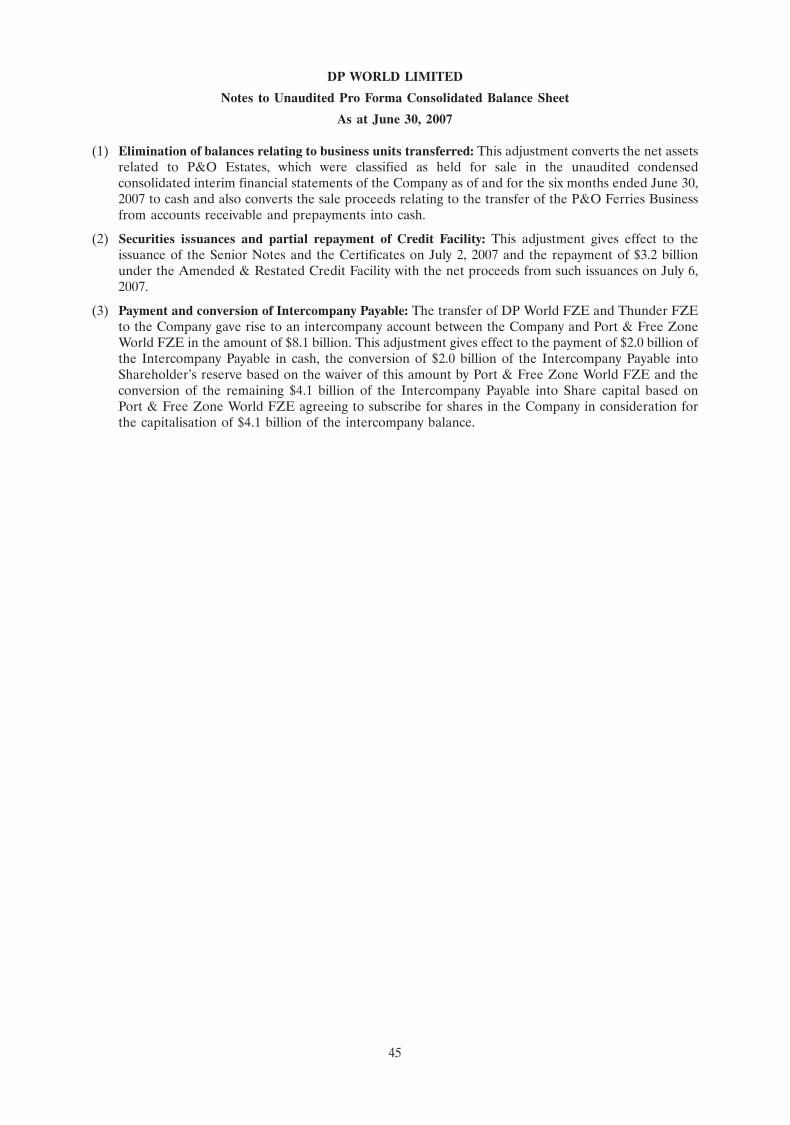

Pursuant to a restructuring plan (the ‘‘Restructuring’’) designed to separate the ports-related commercialand regulatory activities of the Government of Dubai, the Company was incorporated in the DIFC onAugust 9, 2006 for the purpose of becoming the holding company for the ports-related commercialactivities of Dubai World. On January 1, 2007, DP World FZE and Thunder FZE, which is the holdingcompany for the Peninsular and Oriental Steam Navigation Company (‘‘P&O’’), were transferred from anaffiliate of the Company, Dubai Ports Authority (‘‘DPA’’), to the Company. Consideration for the transferof DP World FZE and Thunder FZE is reflected in the Company Consolidated Financial Statements (asdefined below) as a payable (the ‘‘Intercompany Payable’’) to our parent company, Port & Free ZoneWorld FZE, which equalled $8,132.7 million as of June 30, 2007. Prior to the consummation of the GlobalOffering, we expect that we will have satisfied the Intercompany Payable through (i) the payment of$2.0 billion of the Intercompany Payable in cash, (ii) the conversion of $2.0 billion of the IntercompanyPayable into Shareholder’s reserve, based on the waiver of this amount by Port & Free Zone World FZEand (iii) the conversion of the remaining $4.1 billion of the Intercompany Payable into Share capital, basedon Port & Free Zone World FZE agreeing to subscribe for shares in the Company in consideration for thecapitalisation of $4.1 billion of the Intercompany Payable.

On the date of the transfer of DP World FZE and Thunder FZE, property, plant and equipment wererevalued to fair market value and transferred at carrying value, which required that we incur an additional

v

depreciation charge of $13.0 million per annum. In addition, prior to the transfer, our wholly-ownedsubsidiary DP World UAE Region FZE (‘‘DP World UAE’’) entered into a concession agreement (the‘‘Concession Agreement’’) with DPA to operate DP World Jebel Ali, Port Rashid (Dubai) and Hamriya Portin Dubai on an arm’s-length basis. The ownership of these ports has been retained by DPA. While DPWorld UAE is not obligated to pay any concession fee to DPA under the Concession Agreement untilDecember 31, 2012, we have started to accrue such fees in an amount equal to $47.0 million per annum,which represents the average annual minimum fee payable over the term of the agreement. The totalimpact of these adjustments on our consolidated financial statements will be $60.0 million per annum andwill be reflected in cost of sales on our consolidated income statement.

As a result of the Restructuring, the Company, together with its operating subsidiaries, now conducts all ofthe ports-related commercial activities of Dubai World and DPA will continue to conduct all of the ports-related regulatory activities of the Government of Dubai. Such regulatory activities have not been and willnot be transferred to the Company. Prior to the transfer of DP World FZE and Thunder FZE, theCompany did not have any operations. As a result, a substantial portion of the historical financialinformation presented in this Prospectus is based on the DPA Consolidated Financial Statements and theP&O Consolidated Financial Statements (each as defined below).

In connection with the Restructuring, on December 29, 2006, the syndicated term loan and revolving creditfacility among DPA, Thunder FZE and Jebel Ali Free Zone Authority (‘‘JAFZA’’), as borrowers, Ports,Customs & Free Zone Corporation (‘‘PCFC’’) and the other guarantors party thereto, as guarantors, thelenders from time to time party thereto and Deutsche Bank Luxembourg S.A., as facility agent, wasamended and restated (the ‘‘Amended and Restated Credit Facility’’) to, among other things, (i) transfer aportion of borrowings thereunder from Thunder FZE to JAFZA, (ii) remove the requirement that theproceeds from the sale of P&O Ports North America, Inc. (‘‘POPNA’’) be used to prepay borrowingsthereunder, (iii) upon the satisfaction of certain conditions, remove JAFZA as a borrower and guarantorthereunder and (iv) upon the satisfaction of certain conditions, remove PCFC as a guarantor thereunder.In addition, immediately prior to the transfer of Thunder FZE to the Company, the Company became aborrower and guarantor under the Amended and Restated Credit Facility. On March 29, 2007, theoutstanding borrowings of DPA were transferred to DP World UAE Region FZE and DP World UAEassumed all the obligations of DPA as a borrower under the Amended and Restated Credit Facility.

On October 29, 2007, we repaid in full the amounts outstanding under the Amended and Restated CreditFacility with $1.3 billion in borrowings under a new unsecured syndicated loan facility, dated October 22,2007 (the ‘‘Syndicated Loan Facility’’), among the Company, DP World Holdings (Australia) Limited andP&O, as borrowers, the Company, as the sole guarantor, the lenders from time to time party thereto,Barclays Capital, Citibank N.A., Deutsche Bank AG, London Branch, and The Royal Bank of ScotlandPlc, as mandated lead arrangers, The Royal Bank of Scotland Plc, as issuing bank, and Deutsche BankLuxembourg S.A., as Facility Agent.

For a description of the Syndicated Loan Facility, including the undertakings and covenants includedtherein, see ‘‘Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Working Capital and Indebtedness—Revolving Credit SyndicatedFacility’’.

vi

www.global-reports.com

26SEP200717171345

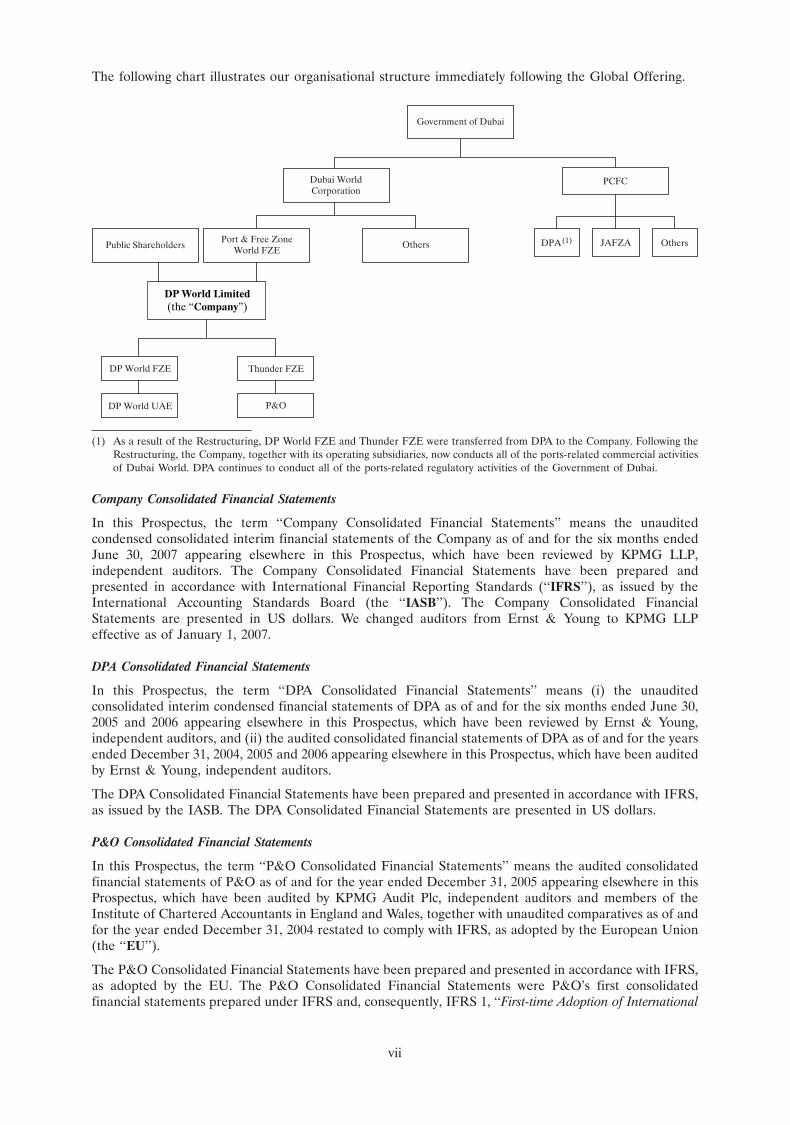

The following chart illustrates our organisational structure immediately following the Global Offering.

DP World Limited(the “Company”)

Port & Free ZoneWorld FZEPublic Shareholders Others

Dubai WorldCorporation

DPA(1) Others

PCFC

JAFZA

Government of Dubai

Thunder FZE

P&O

DP World FZE

DP World UAE

(1) As a result of the Restructuring, DP World FZE and Thunder FZE were transferred from DPA to the Company. Following theRestructuring, the Company, together with its operating subsidiaries, now conducts all of the ports-related commercial activitiesof Dubai World. DPA continues to conduct all of the ports-related regulatory activities of the Government of Dubai.

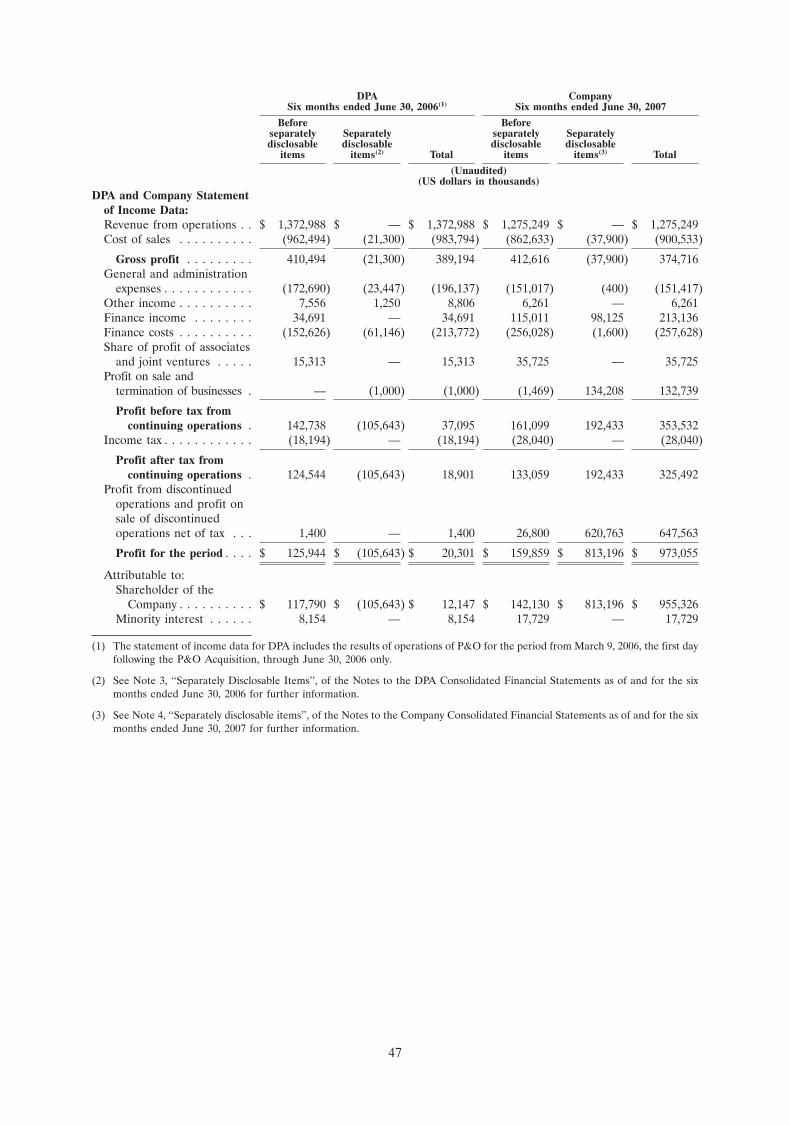

Company Consolidated Financial Statements

In this Prospectus, the term ‘‘Company Consolidated Financial Statements’’ means the unauditedcondensed consolidated interim financial statements of the Company as of and for the six months endedJune 30, 2007 appearing elsewhere in this Prospectus, which have been reviewed by KPMG LLP,independent auditors. The Company Consolidated Financial Statements have been prepared andpresented in accordance with International Financial Reporting Standards (‘‘IFRS’’), as issued by theInternational Accounting Standards Board (the ‘‘IASB’’). The Company Consolidated FinancialStatements are presented in US dollars. We changed auditors from Ernst & Young to KPMG LLPeffective as of January 1, 2007.

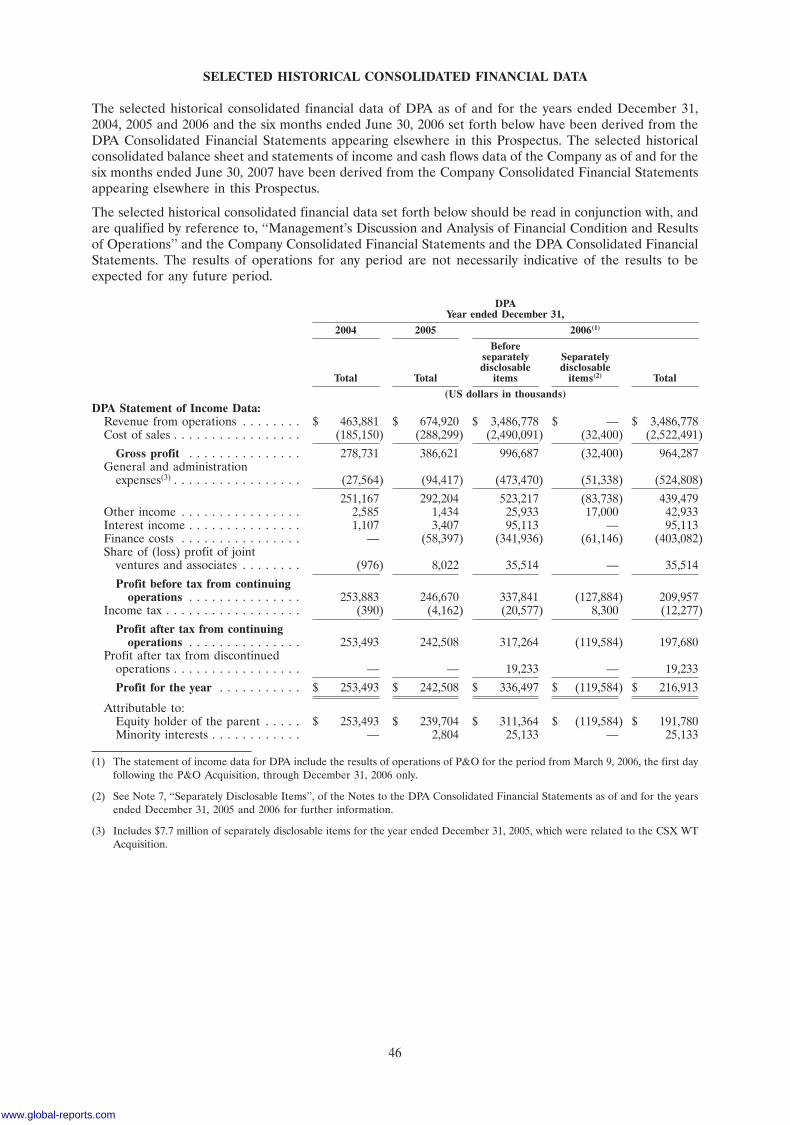

DPA Consolidated Financial Statements

In this Prospectus, the term ‘‘DPA Consolidated Financial Statements’’ means (i) the unauditedconsolidated interim condensed financial statements of DPA as of and for the six months ended June 30,2005 and 2006 appearing elsewhere in this Prospectus, which have been reviewed by Ernst & Young,independent auditors, and (ii) the audited consolidated financial statements of DPA as of and for the yearsended December 31, 2004, 2005 and 2006 appearing elsewhere in this Prospectus, which have been auditedby Ernst & Young, independent auditors.

The DPA Consolidated Financial Statements have been prepared and presented in accordance with IFRS,as issued by the IASB. The DPA Consolidated Financial Statements are presented in US dollars.

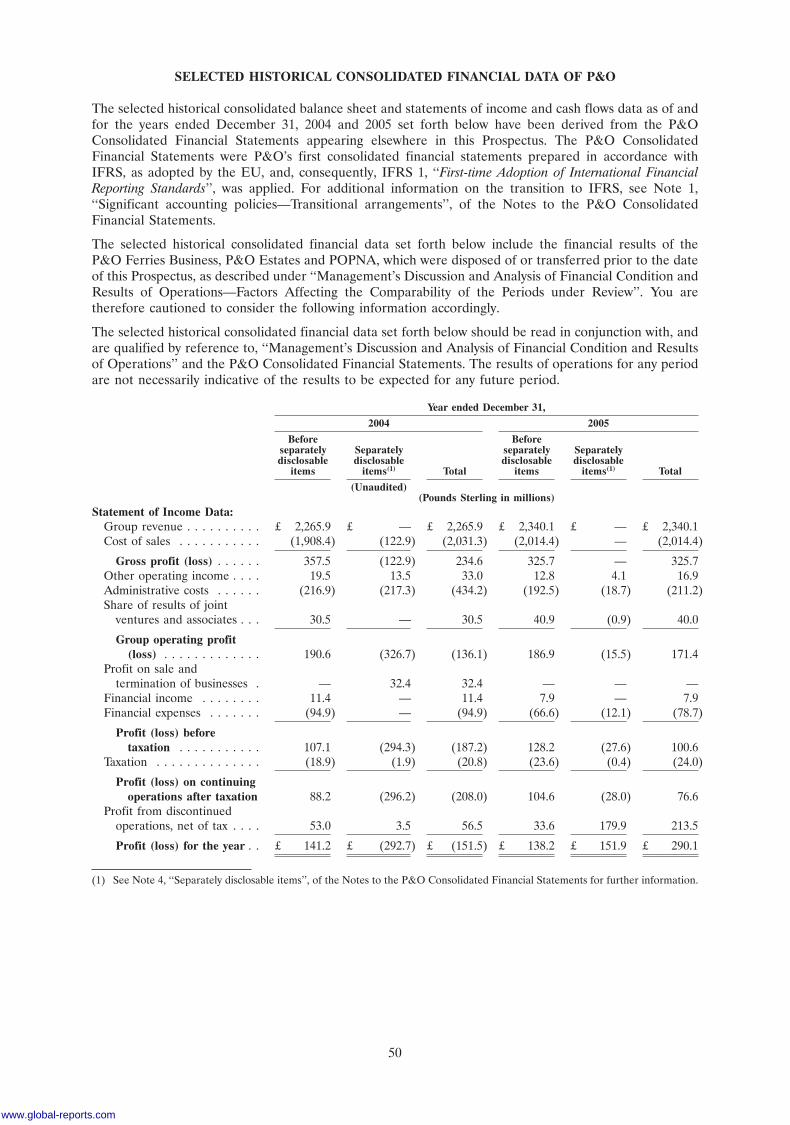

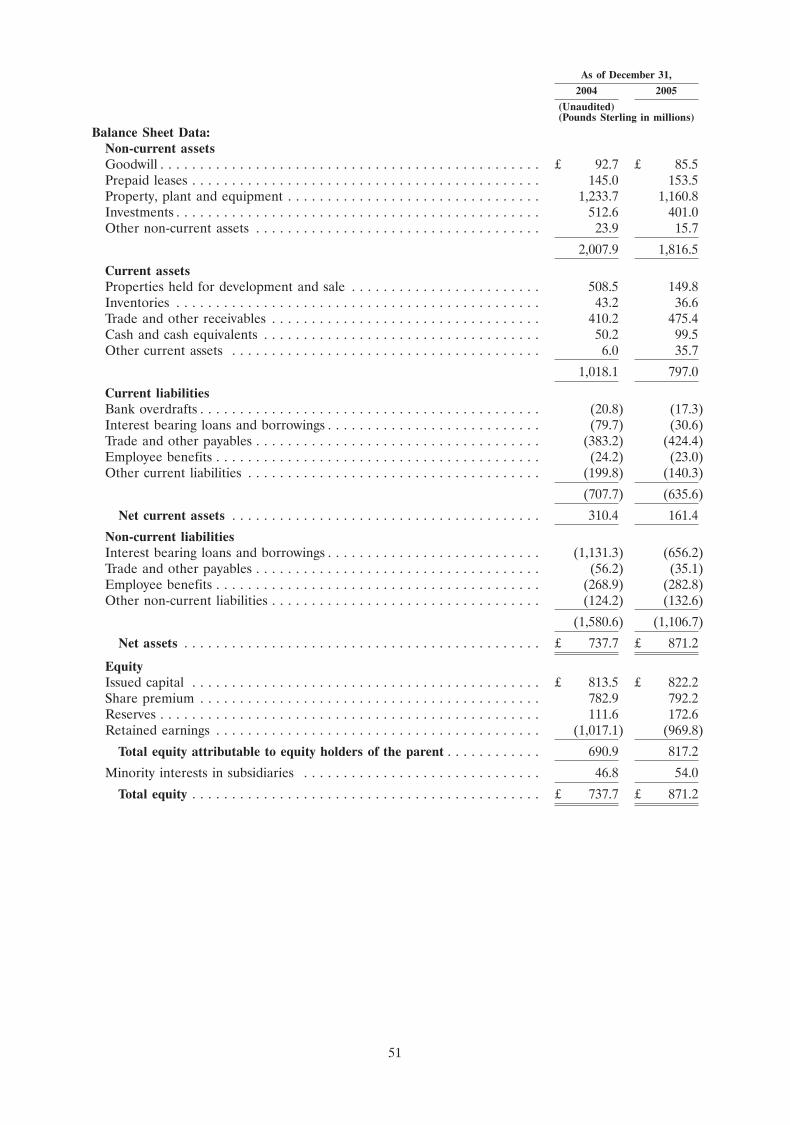

P&O Consolidated Financial Statements

In this Prospectus, the term ‘‘P&O Consolidated Financial Statements’’ means the audited consolidatedfinancial statements of P&O as of and for the year ended December 31, 2005 appearing elsewhere in thisProspectus, which have been audited by KPMG Audit Plc, independent auditors and members of theInstitute of Chartered Accountants in England and Wales, together with unaudited comparatives as of andfor the year ended December 31, 2004 restated to comply with IFRS, as adopted by the European Union(the ‘‘EU’’).

The P&O Consolidated Financial Statements have been prepared and presented in accordance with IFRS,as adopted by the EU. The P&O Consolidated Financial Statements were P&O’s first consolidatedfinancial statements prepared under IFRS and, consequently, IFRS 1, ‘‘First-time Adoption of International

vii

Financial Reporting Standards’’, was applied. For additional information on the transition to IFRS, seeNote 1, ‘‘Significant accounting policies—Transitional arrangements’’, of the Notes to the P&OConsolidated Financial Statements.

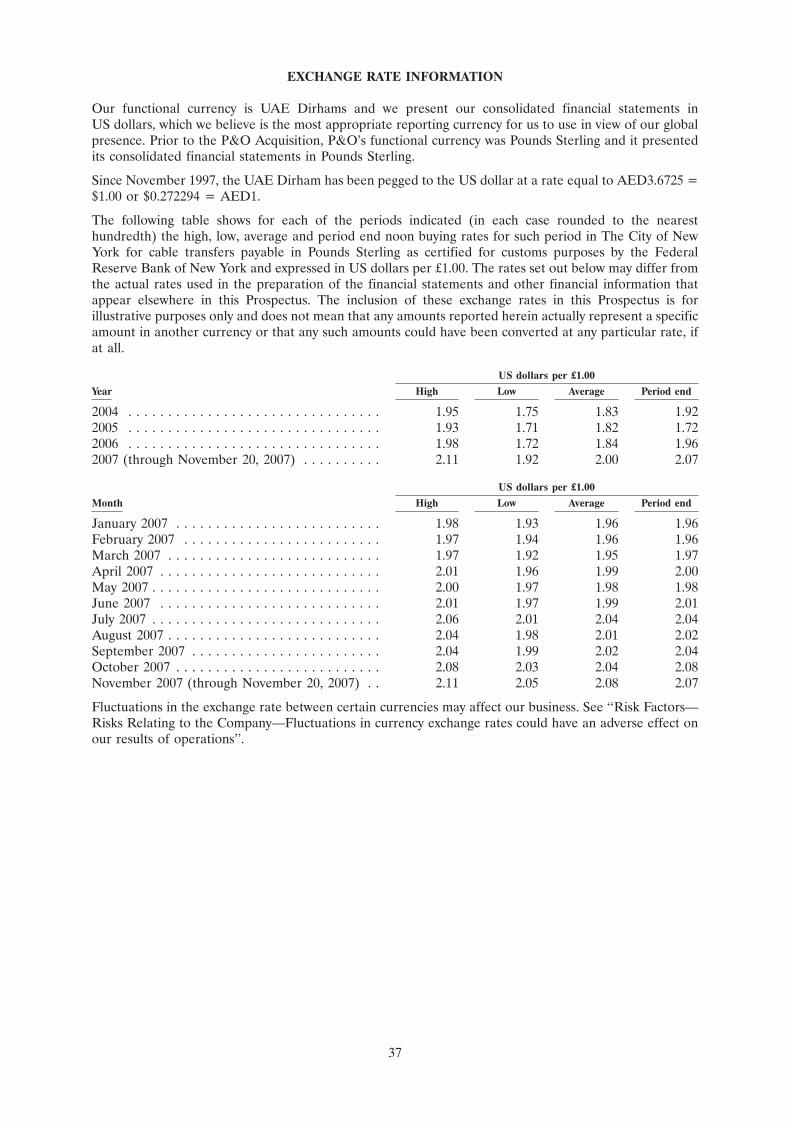

The P&O Consolidated Financial Statements are presented in Pounds Sterling. This Prospectus containshistorical data with respect to the high, low, average and period end noon buying rates for certain periodsin New York for cable transfers payable in Pounds Sterling as certified by the Federal Reserve Bank ofNew York for customs purposes. See ‘‘Exchange Rate Information’’. On November 20, 2007, the noonbuying rate in New York for cable transfers payable in Pounds Sterling as certified by the Federal ReserveBank of New York for customs purposes was $2.07 per £1.00. The inclusion of these exchange rates in thisProspectus is for illustrative purposes only, and does not mean that any amounts reported herein actuallyrepresent a specific amount in another currency or that any such amounts could have been converted atany particular rate, if at all.

Comparability of Historical Financial Information

The comparability of the historical financial information of DPA has been significantly affected by ouracquisitions of CSX World Terminals (‘‘CSX WT’’) in February 2005 and P&O in March 2006. Similarly,our historical and future results of operations are not and will not be directly comparable to the historicalfinancial information of DPA principally because the DPA Consolidated Financial Statements include thefinancial results of P&O for the period from March 9, 2006, the first day following our acquisition of P&O,through December 31, 2006 only, but also because the DPA Consolidated Financial Statements include thefinancial results of the regulatory activities of DPA. In addition, the DPA Consolidated FinancialStatements as of and for the six months ended June 30, 2006 and the year ended December 31, 2006 andthe Company Consolidated Financial Statements as of and for the six months ended June 30, 2007 includethe financial results of (i) P&O’s UK ferry operating business (‘‘P&O Ferries’’) and its European roadhaulage and freight management business (‘‘P&O Ferrymasters’’ and, together with P&O Ferries, the‘‘P&O Ferries Business’’) and (ii) POPNA and P&O’s property development businesses (‘‘P&O Estates’’).

The DPA Consolidated Financial Statements as of and for the six months ended June 30, 2006 reflect(i) the P&O Ferries Business and P&O Estates as continuing operations and not assets held for salebecause the decision to transfer these businesses was not taken until after June 30, 2006 and (ii) POPNA asassets held for sale and discontinued operations. The DPA Consolidated Financial Statements as of and forthe year ended December 31, 2006 reflect (i) the P&O Ferries Business as continuing operations and notassets held for sale because the decision to transfer this business was not taken until after December 31,2006 and (ii) POPNA and P&O Estates as assets held for sale and discontinued operations. The CompanyConsolidated Financial Statements reflect (i) P&O Estates as assets held for sale and discontinuedoperations and (ii) the P&O Ferries Business and POPNA as discontinued operations.

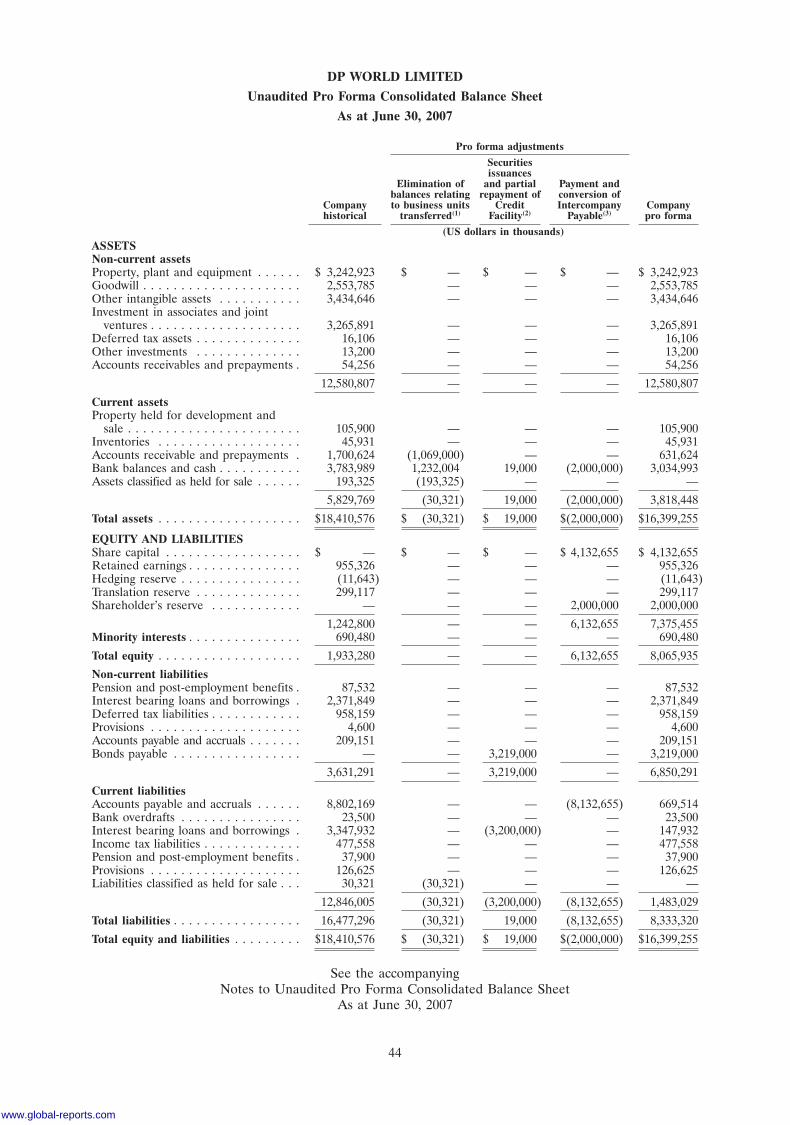

Unaudited Pro Forma Consolidated Financial Information

In this Prospectus, the term ‘‘Unaudited Pro Forma Consolidated Financial Information’’ means theunaudited pro forma consolidated statements of income of the Company for the year ended December 31,2006 and the six months ended June 30, 2007 and the unaudited pro forma consolidated balance sheet ofthe Company as of June 30, 2007. The unaudited pro forma consolidated statement of income of theCompany for the year ended December 31, 2006 is based on the audited consolidated statement of incomeof DPA for the year ended December 31, 2006 included in the DPA Consolidated Financial Statementsappearing elsewhere in this Prospectus. The unaudited pro forma consolidated statement of income of theCompany for the six months ended June 30, 2007 is based on the unaudited condensed consolidatedinterim income statement of the Company for the six months ended June 30, 2007 included in theCompany Consolidated Financial Statements appearing elsewhere in this Prospectus. The unaudited proforma consolidated balance sheet of the Company as of June 30, 2007 is based on the unaudited condensedconsolidated interim balance sheet of the Company as of June 30, 2007 included in the CompanyConsolidated Financial Statements appearing elsewhere in this Prospectus. The Unaudited Pro FormaConsolidated Financial Information is presented in US dollars.

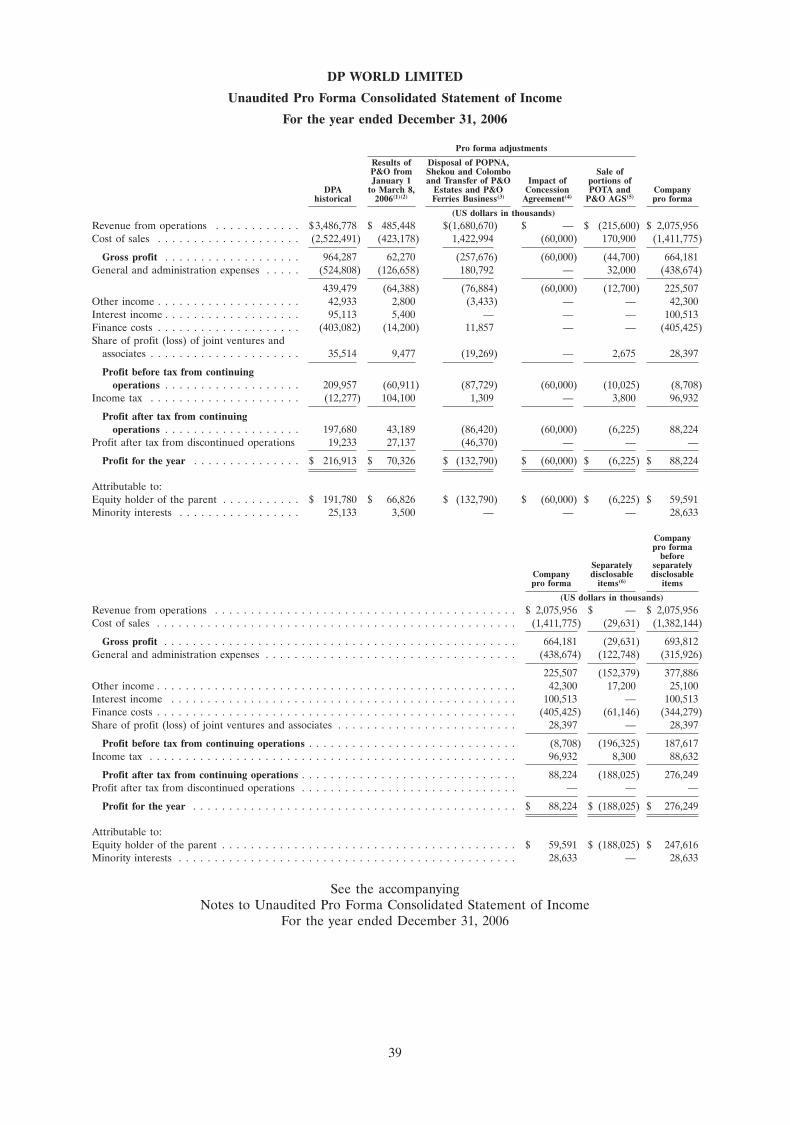

The unaudited pro forma consolidated statement of income of the Company for the year endedDecember 31, 2006 has been prepared for illustrative purposes only to show the effect of (i) the acquisitionof P&O; (ii) the disposal of POPNA, two container terminals in Shekou, China (the ‘‘Shekou Terminals’’)and one container terminal in Colombo, Sri Lanka (the ‘‘Colombo Terminal’’) and the transfer to affiliatesof the Company of the P&O Ferries Business and of P&O Estates; (iii) the effective commencement of the

viii

www.global-reports.com

Concession Agreement and (iv) the sale of 50% of the group of companies known as P&O Trans Australia(‘‘POTA’’), which operates a landside logistics business in Australia, and 75% of the business known asP&O Automotive and General Stevedoring (‘‘P&O AGS’’), which was previously part of DP WorldAustralia Limited and operates automotive and general stevedoring businesses in Australia, as if suchevents had occurred on January 1, 2006.

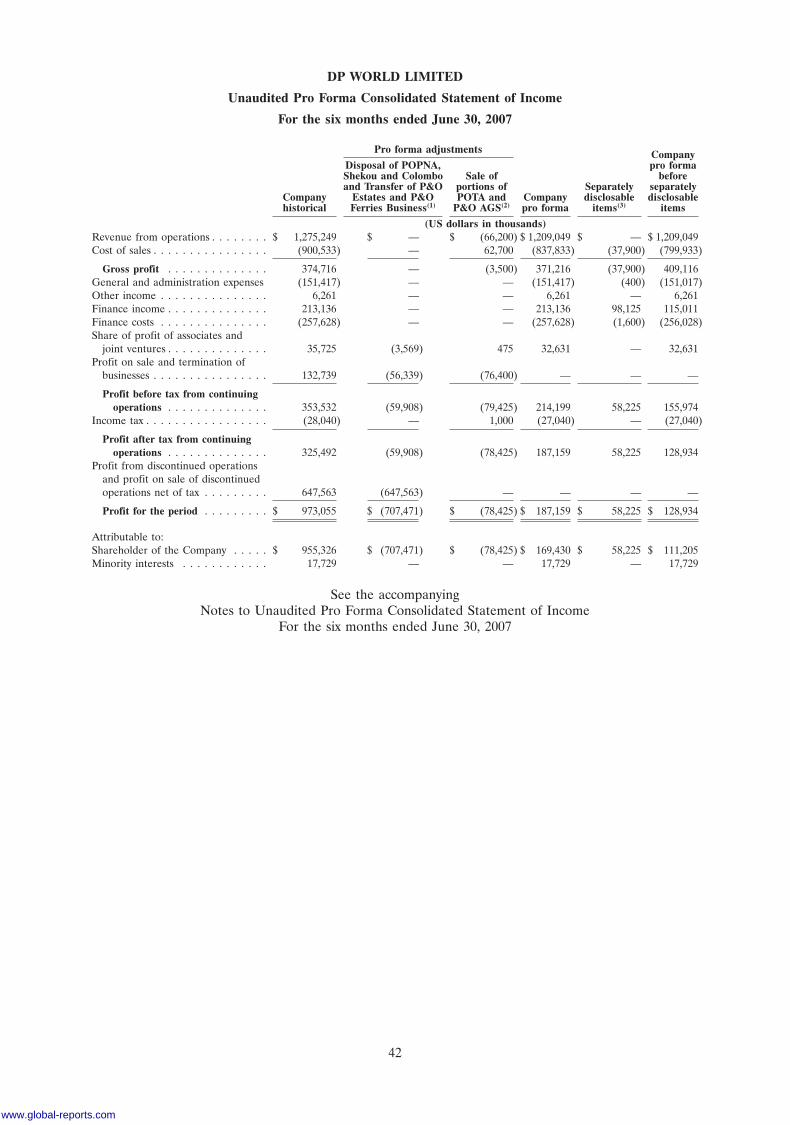

The unaudited pro forma consolidated statement of income of the Company for the six months endedJune 30, 2007 has been prepared for illustrative purposes only to show the effect of (i) the disposal ofPOPNA, the Shekou Terminals and the Colombo Terminal and the transfer to affiliates of the Company ofthe P&O Ferries Business and of P&O Estates and (ii) the sale of portions of POTA and P&O AGS as ifsuch events had occurred on January 1, 2007.

The unaudited pro forma consolidated balance sheet of the Company as of June 30, 2007 has beenprepared for illustrative purposes only to show the effect of (i) the transfer to affiliates of the Company ofthe P&O Ferries Business and of P&O Estates; (ii) the issuance of $1,750,000,000 aggregate principalamount of 6.85 per cent. Notes due 2037 (the ‘‘Senior Notes’’) and $1,500,000,000 face amount of TrustCertificates due 2017 (the ‘‘Certificates’’) and the repayment of $3.2 billion under the Amended &Restated Credit Facility with the net proceeds from such issuances and (iii) the payment of $2.0 billion ofthe Intercompany Payable in cash, the conversion of $2.0 billion of the Intercompany Payable intoShareholder’s reserve and the conversion of the remaining $4.1 billion of the Intercompany Payable intoShare capital.

The Unaudited Pro Forma Consolidated Financial Information, because of its nature, addresses ahypothetical situation and, therefore, does not represent our actual financial position or results had thetransactions described therein been completed at the dates assumed or any other date and should not beregarded as an indication of the operating results generated by us or of our future financial position.

The Unaudited Pro Forma Consolidated Financial Information for the year ended December 31, 2006 hasbeen prepared on a basis consistent with the accounting policies of DPA as of and for the year endedDecember 31, 2006 as set out in Note 2.3, ‘‘Summary of Significant Accounting Policies’’, of the Notes tothe DPA Consolidated Financial Statements as of and for the years ended December 31, 2005 and 2006.The Unaudited Pro Forma Consolidated Financial Information as of and for the six months endedJune 30, 2007 has been prepared on a basis consistent with the accounting policies of the Company as ofand for the six months ended June 30, 2007 as set out in Note 3, ‘‘Significant accounting policies’’, of theNotes to the Company Consolidated Financial Statements as of and for the six months ended June 30,2007.

Operational Data

Certain volume figures in this Prospectus are expressed in ‘‘TEUs’’. A TEU is a twenty-foot equivalent unitthat is based on the dimensions of a cargo container 20 feet long by 8 feet wide by 8 feet 6 inches high, witha maximum load of 24 tonnes.

‘‘Throughput’’ is a measure of container handling activity. The two main categories of containerthroughput are origin and destination (‘‘O&D’’), which is also often referred to as import and export, andtranshipment. Every container shipped by sea is by definition an export container at the originationterminal and an import container at the destination terminal. A container that is transferred from one shipto another at some point during the journey is said to be transhipped, which gives rise to transhipmentthroughput at an intermediate terminal somewhere between the load terminal and the discharge terminal.Throughput includes the handling of imports, exports, empty containers and transhipments.

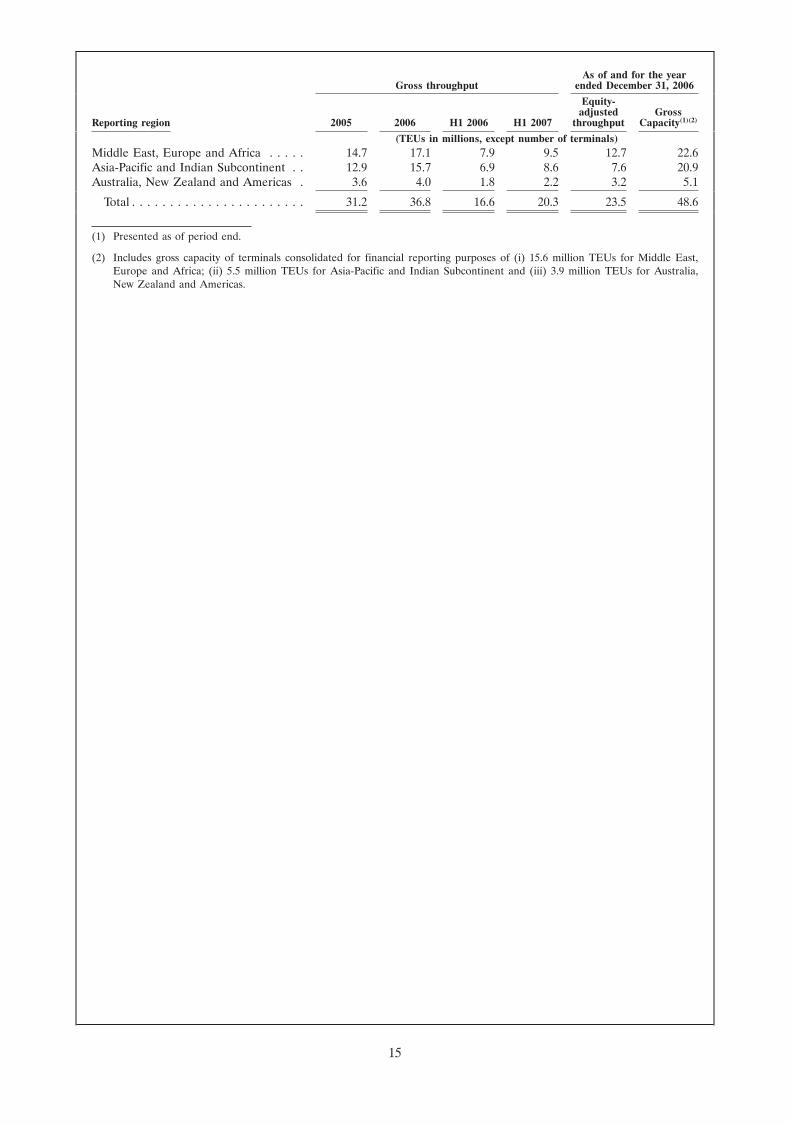

‘‘Gross throughput’’ refers to the total amount of throughput that a container terminal in our portfoliohandled over a period of time, regardless of our economic interest in such terminal or whether we heldsuch terminal for the entirety of such period. ‘‘Equity-adjusted throughput’’ is determined by multiplyingthe gross throughput of a particular container terminal by our economic interest in such terminal as ofDecember 31, 2006.

‘‘Capacity’’ refers to the theoretical amount of throughput that a container terminal could handle in a yearand is generally based on the size of the terminal’s container stacking area and the capacity of its quay,which in turn is based on the length of the quay and the capacity of the ship-to-shore cranes that areavailable.

ix

‘‘Gross capacity’’ refers to the capacity of a container terminal in our portfolio, regardless of our economicinterest in such terminal.

‘‘Revenue generating volume’’ is a measure of all movements of containers at a container terminal thatgenerate revenue. Descriptions of changes in revenue generating volume at a particular terminal or groupof terminals are presented based on the actual levels of revenue generating volume at such terminal orgroup of terminals, irrespective of changes in our ownership interest (including the acquisition thereof)therein during the period under review.

Unless otherwise stated, descriptions of our terminal portfolio, including aggregate throughput andcapacity figures, are based on its composition as of the date hereof and exclude the impact of the disposalof certain terminal operations, comprising the six container terminals operated by POPNA, the twoShekou Terminals and the one Colombo Terminal.

Following the Global Offering, for commercial reasons, we do not intend to continue to provideoperational data regarding our terminal portfolio with the same level of specificity as that set forth in thisProspectus. In particular, we do not intend to update the operational data that we have provided in thisProspectus on a terminal-by-terminal basis in the future. See ‘‘Risk Factors—Risks Related to the Shares—The market price of the Shares may be volatile, which could cause the value of your investment to decline’’.

General

In this Prospectus, unless otherwise specified or the context otherwise requires, references to ‘‘$’’, ‘‘US$’’,‘‘USD’’ and ‘‘dollars’’ are to US dollars, references to ‘‘dirham’’ and ‘‘AED’’ are to UAE dirham andreferences to ‘‘£’’, ‘‘Pounds Sterling’’ and ‘‘Sterling’’ are to the currency of the United Kingdom.

Certain financial and operating information contained in this Prospectus has been derived from unauditedmanagement accounts prepared by us.

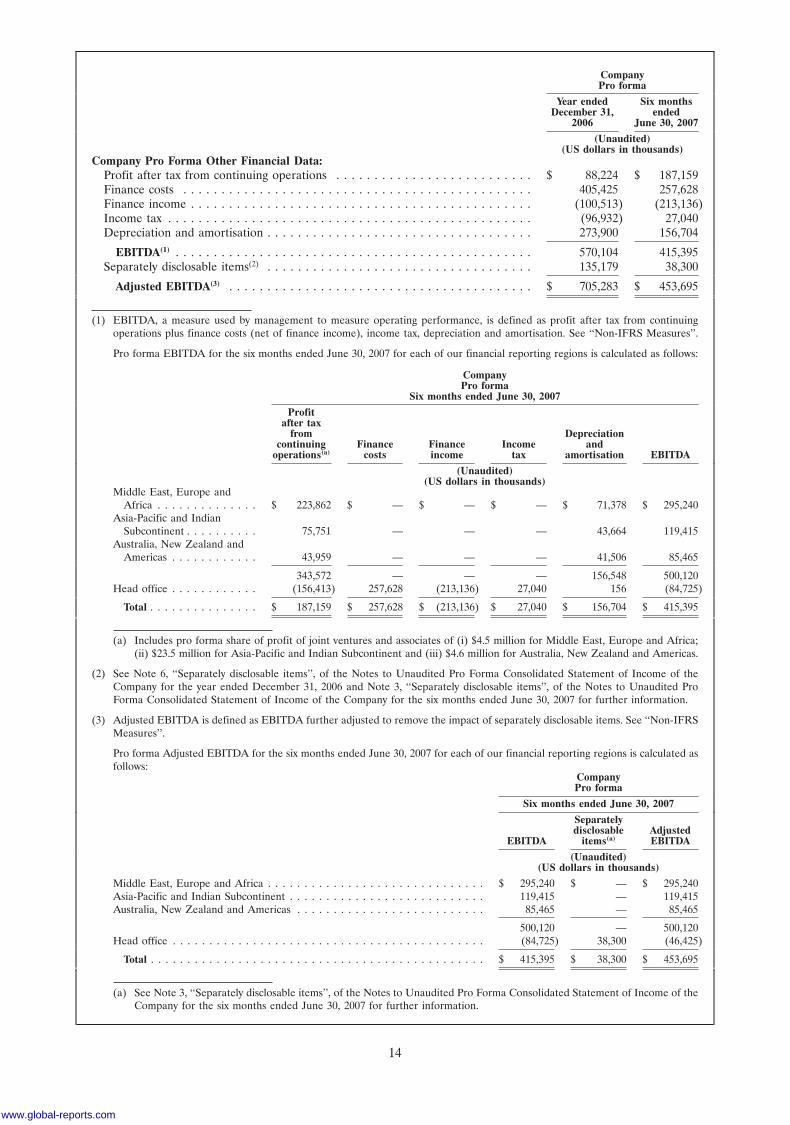

NON-IFRS MEASURES

Earnings before interest, taxes, depreciation and amortisation (‘‘EBITDA’’), a measure used bymanagement to measure operating performance, is defined as profit after tax from continuing operationsplus finance costs (net of finance income), income tax, depreciation and amortisation. ‘‘Adjusted EBITDA’’is defined as EBITDA further adjusted to remove the impact of separately disclosable items. See Note 7,‘‘Separately Disclosable Items’’, of the Notes to the DPA Consolidated Financial Statements as of and forthe years ended December 31, 2005 and 2006, Note 3, ‘‘Separately Disclosable Items’’, of the Notes to theDPA Consolidated Financial Statements as of and for the six months ended June 30, 2006, Note 4,‘‘Separately disclosable items’’, of the Notes to the Company Consolidated Financial Statements as of andfor the six months ended June 30, 2007 and Note 4, ‘‘Separately disclosable items’’, of the Notes to theP&O Consolidated Financial Statements for further information. EBITDA and Adjusted EBITDA are notrecognised terms under IFRS or US generally accepted accounting principles (‘‘US GAAP’’) and do notpurport to be alternatives to profit after tax from continuing operations as measures of operatingperformance or to cash flows from operating activities as measures of liquidity. Additionally, EBITDA andAdjusted EBITDA are not intended to be measures of free cash flow available for management’sdiscretionary use, as they do not consider certain cash requirements such as interest payments, taxpayments and debt service requirements. Management believes that EBITDA and Adjusted EBITDA arehelpful in highlighting trends because they exclude the results of decisions that are outside the control ofoperating management and can differ significantly from company to company depending on long-termstrategic decisions regarding capital structure, the tax jurisdictions in which companies operate and capitalinvestments. Management uses EBITDA and Adjusted EBITDA to supplement IFRS results to provide amore complete understanding of the factors and trends affecting the business than IFRS results alone.Because not all companies use identical calculations, these presentations of EBITDA and AdjustedEBITDA may not be comparable to other similarly titled measures used by other companies.

x

www.global-reports.com

PRESENTATION OF MARKET, MARKET SHARE AND INDUSTRY DATA

The market, market share and industry data contained in this Prospectus has been taken from industryreports. In particular, information and data relating to the international container shipping industry has beenderived from reports, databases and other sources made available in the public domain by, among others,Drewry Shipping Consultants Ltd (‘‘Drewry’’). We confirm that this information has been accuratelyreproduced and, so far as we are aware and have been able to ascertain from that published information,no facts have been omitted which would render the reproduced information inaccurate or misleading.However, the accuracy of such information is subject to the availability and reliability of the datasupporting such information and neither the published information nor the underlying data has beenindependently verified. In addition, the methodology of Drewry and of other industry sources for collectinginformation and data, and therefore the reported information, may differ from that used by us to compileour operational data and from the methodologies employed by other sources, and does not reflect all oreven necessarily a comprehensive set of the actual transactions occurring in the container shippingindustry. Drewry has made no representation, express or implied, and has not accepted any responsibility,with respect to the accuracy or completeness of any of the information in this Prospectus.

AVAILABLE INFORMATION

We have agreed that, for so long as any of the Shares are ‘‘restricted securities’’ as defined inRule 144(a)(3) under the Securities Act, we will during any period that we are neither subject to Section 13or 15(d) of the US Securities and Exchange Act of 1934, as amended (the ‘‘Exchange Act’’), nor exemptfrom reporting pursuant to Rule 12g3-2(b) thereunder furnish, upon request, to any holder or beneficialowner of the Shares or any prospective purchaser designated by any such holder or beneficial owner, theinformation required to be delivered pursuant to Rule 144A(d)(4) under the Securities Act.

xi

(This page has been left blank intentionally.)

www.global-reports.com

SUMMARY

This summary should be read as an introduction to, and is qualified in its entirety by reference to, the moreextensive information contained elsewhere in this Prospectus. This summary may not contain all of theinformation that prospective investors should consider before deciding to invest in the Shares and any suchdecision should be based on a consideration of this Prospectus as a whole. You should read this entireProspectus carefully, including the financial statements and related notes.

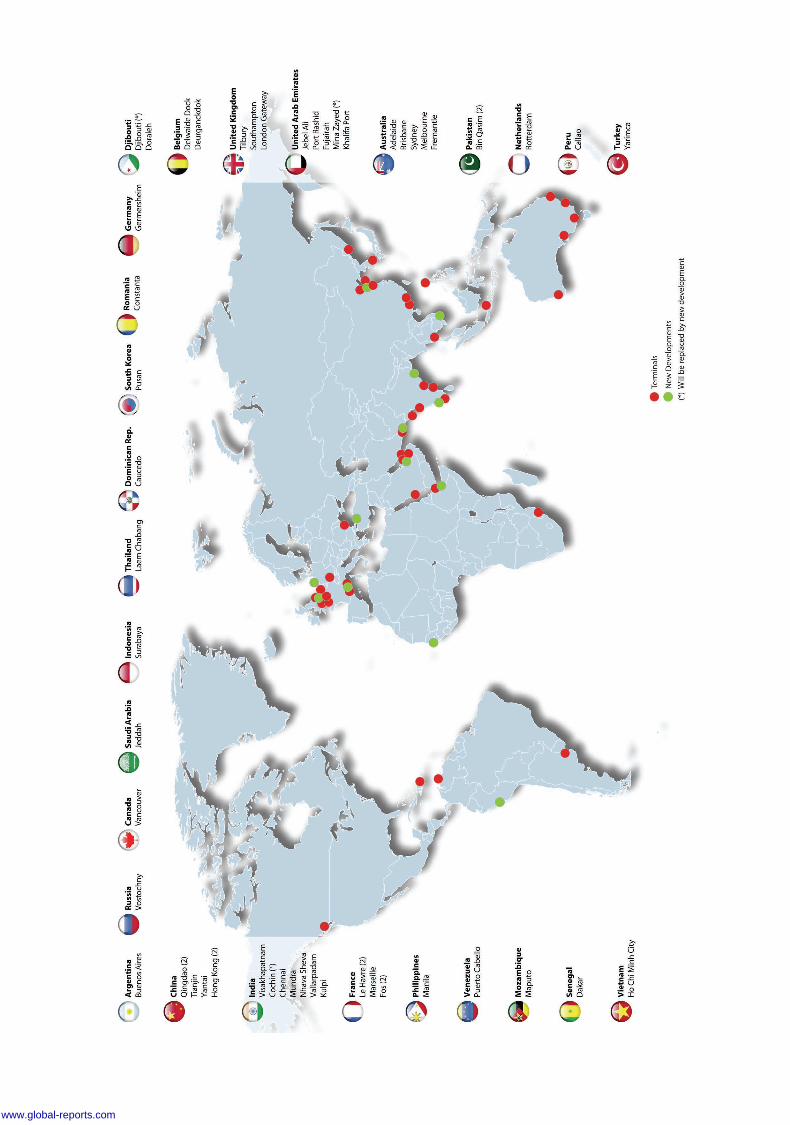

Overview

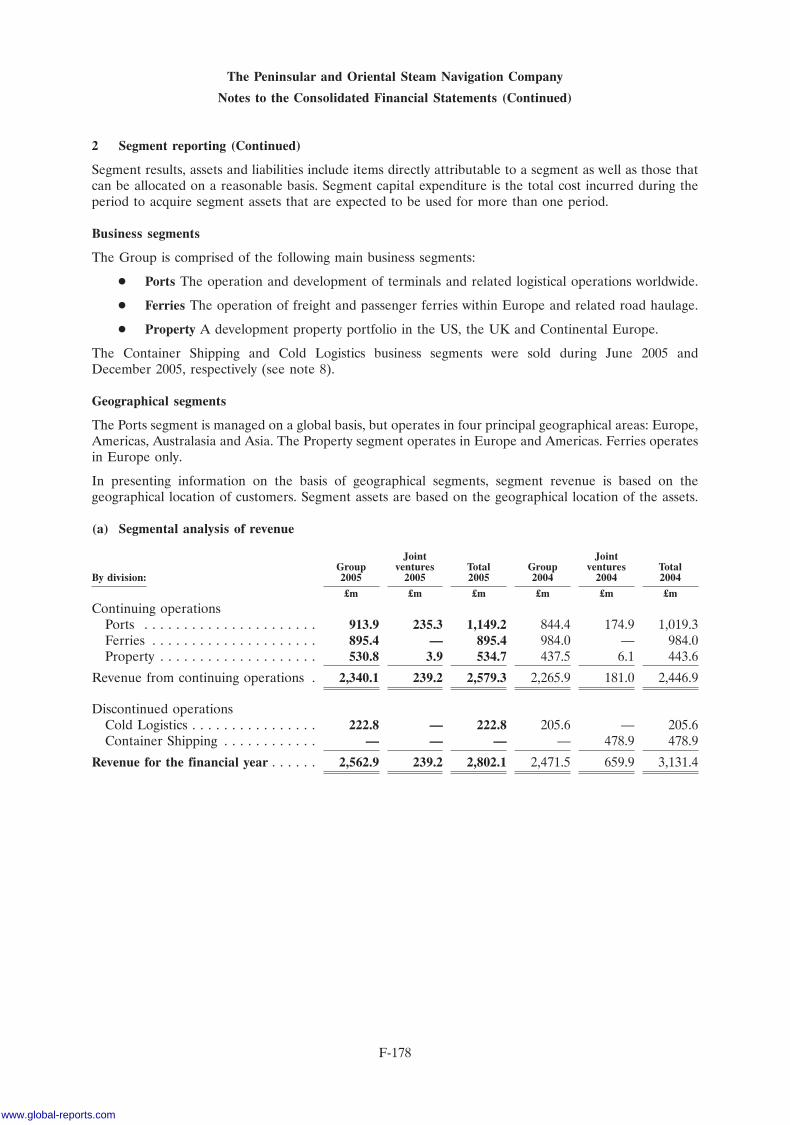

We are one of the largest container terminal operators in the world by capacity and throughput. We arealso one of the most geographically diversified container terminal operators in the world. Our 42 containerterminals, which span 22 countries, had a gross capacity of 48.6 million TEUs as of December 31, 2006 andgenerated gross throughput of 36.8 million TEUs (of which approximately 76% was O&D throughput) and20.3 million TEUs for the year ended December 31, 2006 and the six months ended June 30, 2007,respectively (in each case, excluding the six container terminals operated by POPNA, the two ShekouTerminals and the one Colombo Terminal). For the year ended December 31, 2006 and the six monthsended June 30, 2007, we generated pro forma revenue from operations (which does not include revenueattributable to our joint ventures and associates) of $2,076.0 million and $1,209.0 million, respectively, andpro forma Adjusted EBITDA of $705.3 million and $453.7 million, respectively.

The creation of the Company represents an important step in the development of a global containerterminal business designed to serve the needs of a global and consolidating customer base. As a result ofthe winning of new concessions and our acquisitions of CSX WT in February 2005 and P&O inMarch 2006, our business has been transformed from one focused principally on container terminaloperations located primarily in the UAE to a truly global container terminal business.

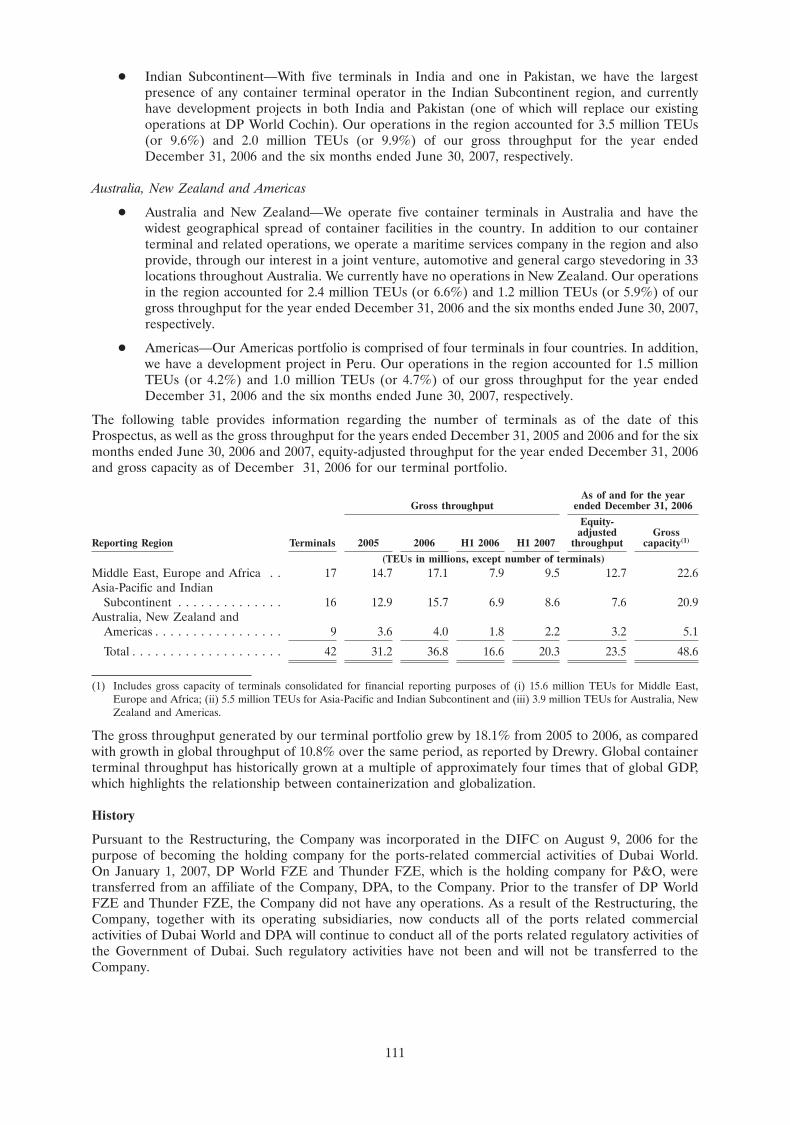

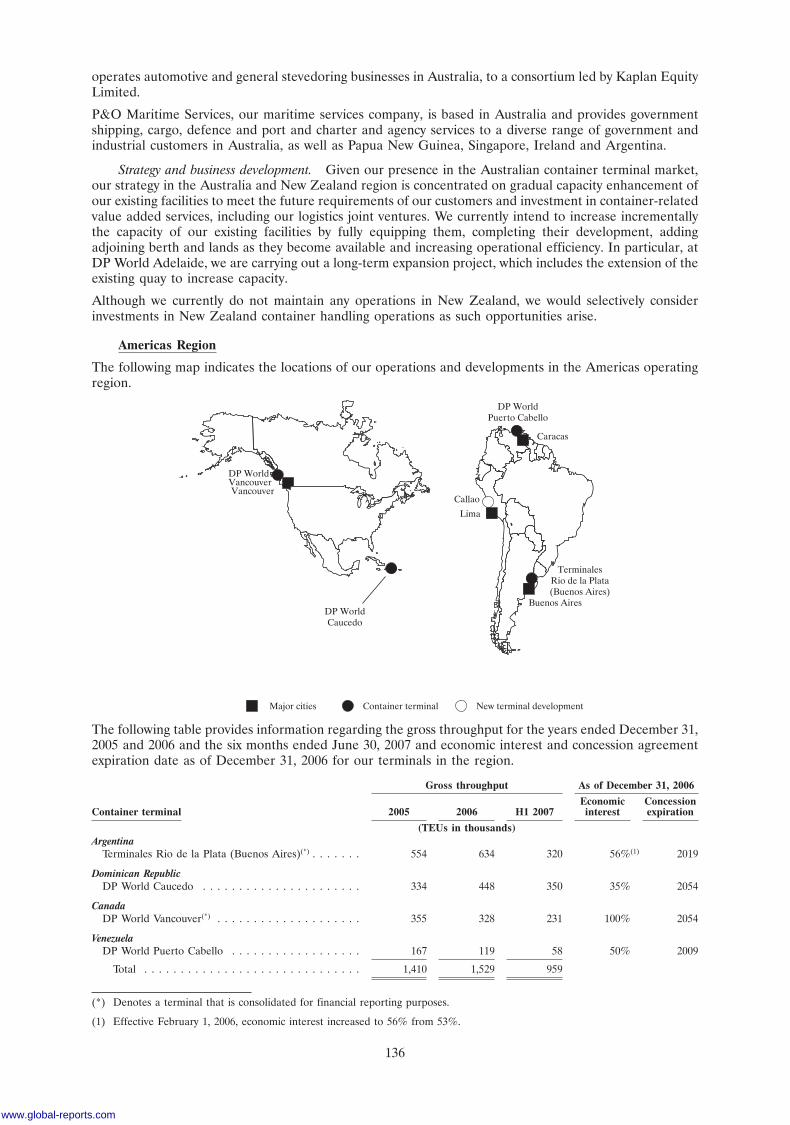

The following table provides information regarding the number of terminals as of the date of thisProspectus, as well as the gross throughput for the years ended December 31, 2005 and 2006 and the sixmonths ended June 30, 2006 and 2007, equity-adjusted throughput for the year ended December 31, 2006and gross capacity as of December 31, 2006 for our terminal portfolio.

As of and for the yearended December 31, 2006Gross throughput

Equity-adjusted Gross

Reporting region Terminals 2005 2006 H1 2006 H1 2007 throughput capacity(1)

(TEUs in millions, except number of terminals)Middle East, Europe and

Africa . . . . . . . . . . . . . . 17 14.7 17.1 7.9 9.5 12.7 22.6Asia-Pacific and Indian

Subcontinent . . . . . . . . . 16 12.9 15.7 6.9 8.6 7.6 20.9Australia, New Zealand and

Americas . . . . . . . . . . . . 9 3.6 4.0 1.8 2.2 3.2 5.1

Total . . . . . . . . . . . . . . . 42 31.2 36.8 16.6 20.3 23.5 48.6

(1) Includes gross capacity of terminals consolidated for financial reporting purposes of (i) 15.6 million TEUs for Middle East,Europe and Africa; (ii) 5.5 million TEUs for Asia-Pacific and Indian Subcontinent and (iii) 3.9 million TEUs for Australia,New Zealand and Americas.

The gross throughput generated by our terminal portfolio grew by 18.1% from 2005 to 2006, as comparedwith growth in global throughput of 10.8% over the same period, as reported by Drewry. Global containerterminal throughput has historically grown at a multiple of approximately four times that of global grossdomestic product (‘‘GDP’’), which highlights the relationship between containerization and globalization.

Competitive Strengths

We have built our global container terminal business through the combination of our regional andinternational operations, the CSX WT Acquisition, the P&O Acquisition and our terminal developmentand expansion projects. We believe that each of these components provides us with complementarystrengths, which together position us as a market leader in the global container terminal industry. Inparticular, we believe that our business is characterised by the following key competitive strengths.

1

A Globally Diversified, Market-Leading and Balanced Portfolio of Terminals

With 42 terminals in 22 countries, we believe that we have the most geographically diversified portfolio ofterminals in the industry and that the size and diversity of our portfolio gives us a competitive advantageover smaller and more concentrated operators because of the relatively high barriers to entry thatcharacterise the container terminal industry. Our asset base includes a diverse mixture of both establishedand newer terminals and a significant number of greenfield and brownfield projects that we are in theprocess of developing. We believe that this combination of development sites and fully operating facilitiesis key to facilitating our future growth strategies and that our portfolio allows us to take advantage of thetypically stable returns on equity in lower-risk established markets such as Europe and Australia and thepotential for greater returns on equity in higher-risk emerging markets such as Latin America and Africa,which have experienced high growth in recent years. In addition, we believe that our portfolio, which isdiversified within the regions in which we operate, should help to mitigate any region-specific downturns.

Strong Pipeline of New Projects and Additional Growth Potential

We have extensive experience in developing terminal operations around the globe, including byconstructing new terminals on both greenfield sites and brownfield sites as a result of concession wins. Wehave a strong track record of winning concessions globally based on our customer and business partnerrelationships, operating and technical credentials, willingness to invest in new capacity to meet demandand focus on key governmental issues, such as security and sustainability. Consequently, we believe that wewill win, on financial terms that we consider to be attractive, the majority of the concessions that weactively pursue and where we submit a bid.

Our new projects currently in development include a total of 13 terminal development projects and10 terminal expansion projects, which, subject to various final regulatory approvals in some cases, areexpected to become operational at various times over the next 10 years and to add 27.7 million TEUs and10.2 million TEUs, respectively, of gross capacity to our portfolio, based on anticipated capacity as ofcompletion, of which we expect 9.8 million TEUs and 9.2 million TEUs, respectively, will be operational bythe end of 2010. In addition, we commenced operations at the first phase of the expansion project at DPWorld Jebel Ali and the Phase III(b) expansion project at Qingdao Qianwan Container Terminal earlierthis year, which together added 4.0 million TEUs of gross capacity to our portfolio. We anticipate that14.5 million TEUs and 4.8 million TEUs of the expected additional gross capacity to be provided by ourterminal development projects and terminal expansion projects, respectively, will be provided by projectsthat we expect will be consolidated for financial reporting purposes, of which we expect 6.2 million TEUsand 4.0 million TEUs, respectively, will be operational by the end of 2010. We also have a pipeline ofpotential projects in various stages of review, and continue to look for innovative opportunities for theownership and management of terminal and terminal-related assets both inside and outside of ports.

Strong Relationships with Key Customers

We maintain a diverse customer base and enjoy close and long-standing relationships with our keycustomers, who are, for the most part, leaders in the global shipping industry. We believe that we havebeen successful in attracting and maintaining key customers as a result of our strong reputation in theindustry, continued achievement of operational excellence and the diversification of our global portfolio,each of which helps our customers succeed in their businesses. For example, seven of our current top tenglobal customers were also our customers ten years ago. We target key customers and seek to buildstrategic relationships based on an internal programme of customer segmentation, which we believe isunique to our industry. Through this programme, we seek to identify key commercial relationships byconsidering a number of different factors that we believe will assist us in evaluating our customers anddetermining how we can best serve them in the future.

Strategic Relationships with Dubai World and its Affiliates

As a majority-owned indirect subsidiary of Dubai World, a holding company owned by the Government ofDubai, following the Global Offering we expect to continue to benefit from the commitment of DubaiWorld to promote Dubai and its portfolio of businesses and projects both domestically and internationally.In addition, we have in the past benefited from and expect to continue to leverage relationships withaffiliates that engage in complementary businesses, which we believe allows us to offer a combination ofservices that is unique in the container terminal industry and provides us with an advantage over ourcompetitors.

2

www.global-reports.com

Operational Excellence and Innovation

We are one of the innovators in the container terminal industry and have been successful in developing andenhancing container terminal capacity and efficiency in the regions in which we operate based on the needsand attributes of particular terminals. In 2007, our international achievements were recognised by ourwinning Best Seaport in the Middle East for DP World Jebel Ali for the 13th year in a row and Best ContainerTerminal in Asia under 4 million TEUs per annum for CT3 (Hong Kong) at the Asian Freight & SupplyChain Awards. We also won various awards in 2006, including the Lloyd’s List’s Port Operator of the YearAward. Our commitment to operational excellence is reflected in the increase in our average global craneproductivity from approximately 25 gross moves per hour for the year ended December 31, 2005 toapproximately 27 gross moves per hour for the year ended December 31, 2006. This increase in ouraverage global crane productivity is made possible not only through the implementation of newtechnologies but also by significant improvements in operating efficiency that we have been able to makeat existing terminals, as well as at new terminals constructed on greenfield sites.

Experienced and International Management Team

Our global business is run out of our head office in Dubai by the 11 members of our executivemanagement team, who have significant industry experience, and some of whom also have experience inthe container shipping industry. In addition, our local operations are managed by eight regional managers,who also have significant experience in the container terminal industry and extensive local and regionalknowledge, and are supported by a highly experienced team of local container terminal managers.

Our Vision and Mission

Our vision is to be the ‘‘Port of Choice’’ for our customers in each of our locations, to excel in operations,sales and customer service to our clients and to enhance the position of the local communities andcountries in which we operate as gateways for global trade. Our mission is to provide world-class portservices and to be a global player in operating and managing ports. We aim to provide value-for-money,high quality services to our customers through motivated and innovative employees who are empowered tomake optimum use of modern facilities, technology and resources while ensuring a reasonable return oninvestment.

Corporate Strategy

We have historically grown our business through a combination of organic growth and corporateacquisitions, which have helped to establish our global footprint and fundamentally change thecomposition and dynamics of our industry. Going forward, we have a strong pipeline of new terminaldevelopment projects, which are expected to add 27.7 million TEUs of gross capacity to our portfolio overthe next 10 years, based on anticipated capacity as of completion. We will adopt a selective approachtowards future acquisition opportunities. The following strategic principles have therefore been developedto aid our objectives, with a focus on people, customers, quality and global reach.

Optimise Existing Asset Base and Current Capacity

We believe that operational excellence and innovation create opportunities to generate additional valueout of our existing facilities. We seek to improve our operational efficiency and increase the capacity of ourexisting facilities by investing in advanced handling equipment and streamlining our operational processes.We believe that this strategy is one of the most cost-effective methods for increasing capacity at ourexisting facilities. In addition, we continually communicate with our customers and essential stakeholdersin the port and shipping community to maximise the connectivity, responsiveness, accuracy and speed thatwe are able to offer.

Maximise Customer Satisfaction with Innovative and Tailored Solutions

Providing our global customers and their customers with value enhancing port and logistics solutions is acornerstone of our operating strategy. We seek to sustain our consultative approach to customerrelationship management to ensure we invest in facilities around the globe where our services are required.We employ a proactive management process that focuses on the key elements of connectivity, informationsharing and security, which can provide strategic solutions in inventory and cost control in the global supplychain. We believe that the reliability and efficiency of our operations and information flow will enhanceour customers’ competitive edge.

3

22SEP200718423235

Enhance Relationships with Sector Participants

We continually evaluate our relationships with both current and potential future partners and stakeholdersto ensure that we stay at the forefront of our industry, seizing the most attractive commercial opportunitiesby involving the relevant stakeholders from the outset. We believe that our credentials as one of theworld’s largest container terminal operators make us a natural partner of choice, and we seek to enhancethis perception across the globe. In addition, we believe that leveraging our relationships with our affiliateswithin Dubai World as we explore new opportunities will ultimately transform the local economies of thecountries in which we operate and consequently enhance the value proposition for our business.

Deploy Capital for Sustained Growth, Profitability and Market Leadership

We intend to pursue investment opportunities based on our assessment of their potential for valuecreation, growth and sustained profitability. We continue to ensure that our assessment of potentialinvestment opportunities is performed on a risk-adjusted basis, such that any capital deployed in morevolatile markets is accompanied by a commensurate increase in the expected return. Within thisframework, we emphasise operational control of new projects while ensuring that we have the mostappropriate partners on board where required. We seek to position ourselves to react to changes in bothour and our customers’ industries to ensure that we remain the port operator of choice.

Create a Place of Great Opportunity and Professional Enhancement for Employees

We believe that our achievement of operational excellence and innovation depends on the abilities,creativity and dedication of our employees. By implementing policies that allow us to be a good employerand good corporate citizen, we seek to create a culture of global excellence that will define ourorganisation and the container terminal industry. We plan to continue to invest in the personaldevelopment of our employees to ensure that we attract and retain the most experienced, motivated andknowledgeable workforce.

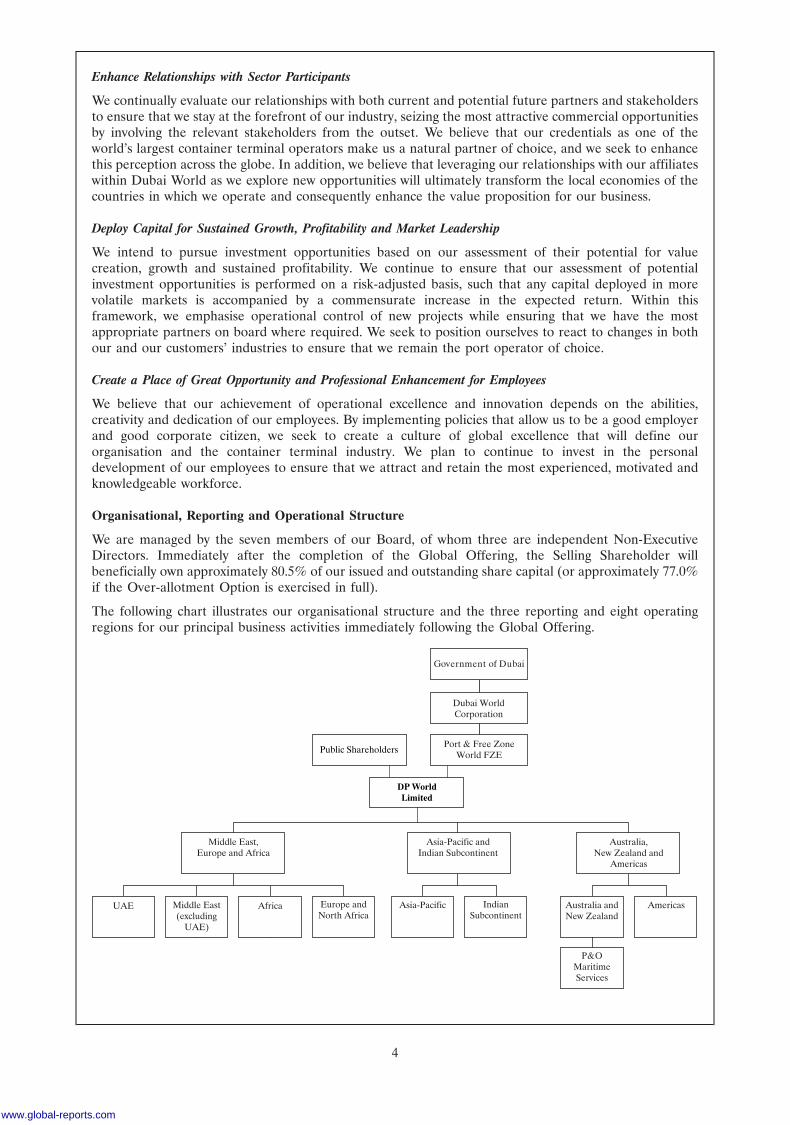

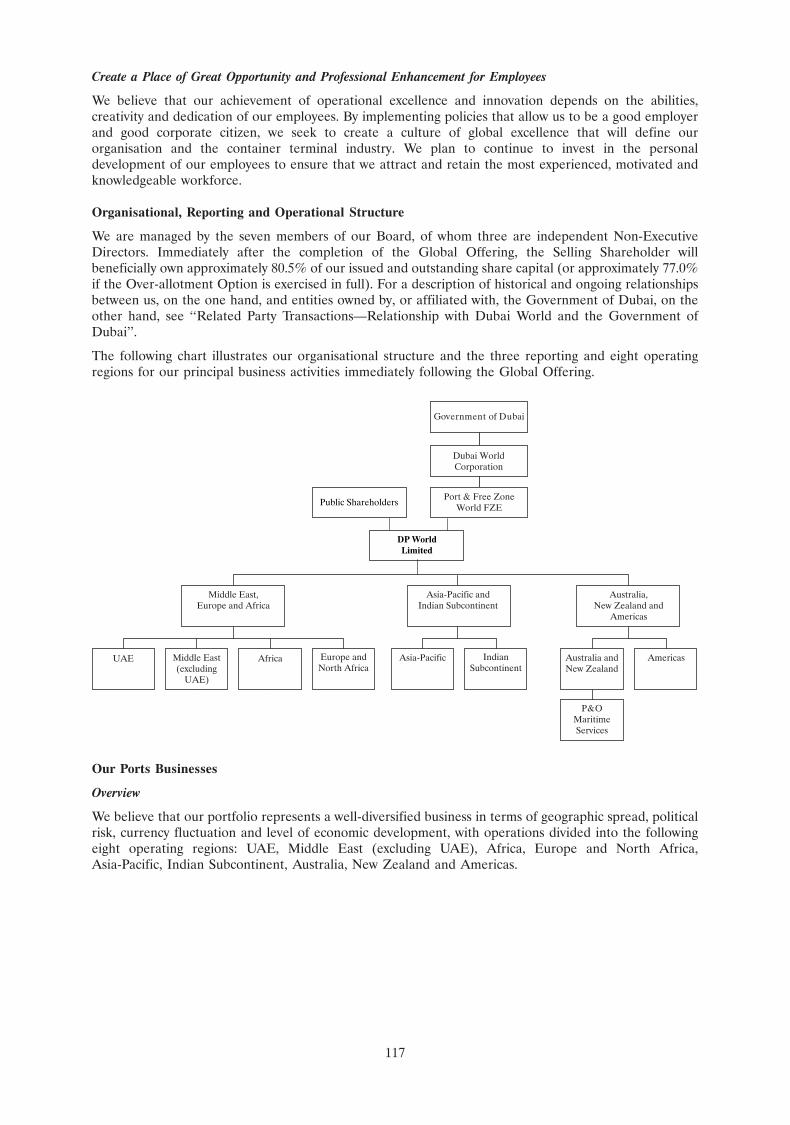

Organisational, Reporting and Operational Structure

We are managed by the seven members of our Board, of whom three are independent Non-ExecutiveDirectors. Immediately after the completion of the Global Offering, the Selling Shareholder willbeneficially own approximately 80.5% of our issued and outstanding share capital (or approximately 77.0%if the Over-allotment Option is exercised in full).

The following chart illustrates our organisational structure and the three reporting and eight operatingregions for our principal business activities immediately following the Global Offering.

DP WorldLimited

Port & Free ZoneWorld FZE

Dubai WorldCorporation

Government of Dubai

Middle East,Europe and Africa

Asia-Pacific andIndian Subcontinent

Australia,New Zealand and

Americas

UAE Middle East(excluding

UAE)

Europe andNorth Africa

IndianSubcontinent

Asia-PacificAfrica Americas

P&OMaritimeServices

Australia andNew Zealand

Public Shareholders

4

www.global-reports.com

Risk Factors

An investment in the Shares involves significant risks, including: (i) risks relating to the newly-establishedand largely untested nature of the DIFC and the DIFX; (ii) risks relating to the Company, such as risksassociated with the transformative nature of our recent acquisitions, the capital and other requirements ofour development projects and our reliance on joint ventures; (iii) risks relating to our ports business, suchas risks associated with the high level of competition that we face in the container terminal industry forconcessions and an increasingly consolidated customer base, as well as risks relating to the political,regulatory, economic and social environments of the regions and countries in which we operate; and(iv) risks relating to the Shares, such as illiquidity, the control that Dubai World will retain over usfollowing the Global Offering and fluctuations in securities markets and the market price of the Shares.

Recent Developments

On October 30, 2007, we entered into an agreement to acquire a 90% stake in Egyptian ContainerHandling Co., which owns Sokhna Port Development Company (‘‘SPDC’’), for consideration ofapproximately $670 million. SPDC operates Sokhna Port in Egypt (‘‘Sokhna’’) under a concessionagreement that expires in 2027. Sokhna is located on the Red Sea coast within the North West SuezEconomic Zone and is the closest container port to Cairo, Egypt. Sokhna is currently expanding capacityand we expect that it will have capacity of approximately 1.2 million TEUs by the end of 2009. We believethat Sokhna will be an important addition to our existing Red Sea operations at Jeddah South ContainerTerminal and Port Autonome International de Djibouti. The transaction is subject to our receipt of certainregulatory approvals and is expected to be completed before the end of 2007.

Our principal executive offices are located at LOB 17, Jebel Ali Free Zone, Dubai, UAE. Our registeredoffice is PO Box 17000, Dubai, UAE. Our telephone number is +971 4 881 1110. Our website address iswww.dpworld.com. The information contained on our website is not incorporated by reference into, orotherwise included in, this Prospectus.

5

THE GLOBAL OFFERING

Company . . . . . . . . . . . . . . . . . DP World Limited.

The Selling Shareholder . . . . . . Port & Free Zone World FZE, a free zone establishment formed andregistered under the laws promulgated by JAFZA, currently holds100% of our issued and outstanding share capital. Immediatelyfollowing completion of the Global Offering, the Selling Shareholderwill own approximately 80.5% of our issued and outstanding sharecapital (or approximately 77.0% assuming the Over-allotment Optionis exercised in full). See ‘‘Principal and Selling Shareholder’’.

Global Offering . . . . . . . . . . . . 3,245,300,000 Shares are being offered in the Global Offering by theSelling Shareholder. The Global Offering comprises the InternationalOffering (which includes the Exempt Offer), the UAE Retail Offerand the Sukuk Allocation. The Shares are being offered outside theUnited States in reliance on Regulation S and within the UnitedStates only to QIBs in reliance on Rule 144A. The Exempt Offer isbeing made in the DIFC pursuant to an exemption from registrationunder the Offered Securities Rules of the DFSA.

International Offering . . . . . . 2,129,527,994 Shares are being offered in the International Offering(i) outside the United States in reliance on Regulation S, includingShares being offered in the Exempt Offer in the DIFC pursuant to anexemption from registration under the Offered Securities Rules of theDFSA, and (ii) within the United States only to QIBs in reliance onRule 144A.

UAE Retail Offer . . . . . . . . . . 307,692,306 Shares are being offered in the UAE to (i) nationals ofthe UAE or other Gulf Cooperation Council (‘‘GCC’’) countries whoare resident in the UAE or another GCC country, (ii) other UAEresidents with a valid residency visa and (iii) corporate entitiesorganised under the laws of the UAE or another GCC country, who,in each case, hold a securities account with one of the brokersparticipating in the UAE Retail Offer, apply for Shares pursuant tothe UAE Retail Offer in the UAE and meet certain otherrequirements (‘‘Eligible Applicants’’). Pursuant to the terms of theUAE Retail Offer, applications under the UAE Retail Offer must besubmitted (together with all supporting documents) by EligibleApplicants in accordance with the terms and conditions governing theUAE Retail Offer no later than 12:00 p.m. (Dubai time) onNovember 15, 2007 (or such later time as we and the lead receivingbank for the UAE Retail Offer may decide).

Sukuk Allocation . . . . . . . . . . 808,079,700 Shares will be allocated to, or on behalf of, theSukukholders in connection with the redemption of the PCFCDevelopment Sukuk in accordance with its terms. See ‘‘Description ofthe PCFC Development FZCO Sukuk’’ for more information.

Shares . . . . . . . . . . . . . . . . . . . Conditional on, and with effect from, DIFX Admission, our sharecapital will consist of 16,600,000,000 ordinary shares, each with anominal value of $0.10, which are fully paid, issued and outstanding.The Shares have the rights described under ‘‘Description of ShareCapital’’.

Offer Price . . . . . . . . . . . . . . . . The Offer Price is $1.30 per Share.

Over-allotment Option . . . . . . . The Selling Shareholder has granted the Stabilisation Manager, onbehalf of the several Underwriters, the Over-allotment Optionpursuant to which the Stabilisation Manager may purchase up to anadditional 462,147,489 Shares at the initial offering price (the ‘‘OfferPrice’’) within 30 days from the Closing Date to cover over-allotments, if any, made in connection with the Global Offering and to

6

www.global-reports.com

cover any short positions resulting from stabilisation transactions. Inaddition, to the extent that the Over-allotment Option is exercised, upto an additional 110,552,511 Shares will be allocated to, or on behalfof, Sukukholders.

Payment and settlement . . . . . . Purchasers will be required to make payment for the Shares on thesettlement date, which is expected to be on or about the Closing Date.If the DIFX Admission does not take place, the Selling Shareholderhas undertaken to the Joint Global Coordinators and theUnderwriters to return promptly the gross proceeds, if any, paid to iton the Closing Date.

Payment for, and delivery of, the Shares is expected to be made on thesettlement date to the accounts of purchasers through the book-entryfacilities of the Central Securities Depositary (the ‘‘CSD’’) operatedby the DIFX. Trading of the Shares will take place through the tradingsystem of the DIFX. Shares may be held either in accounts openedwith the CSD by the holders thereof or through custodian omnibusaccounts and the ownership of the Shares will be evidenced by theholdings in such accounts. Clearing and settlement of trades on theDIFX by brokers or custodians may be performed only throughmembers of the DIFX that are authorised clearing members (the‘‘Clearing Members’’). Each Clearing Member must hold a securitiesaccount with the CSD and a cash account with a designatedsettlement bank for settlement purposes. Similarly, a custodian needsto hold an omnibus account with the CSD and a cash account with asettlement bank for settlement of off-exchange trades. Settlement ofsecurities trading on the DIFX is governed by the DIFX BusinessRules. See ‘‘Clearance and Settlement’’.

Closing Date . . . . . . . . . . . . . . November 26, 2007.

Restrictions on purchases andtransfers of Shares . . . . . . . . . The Shares are subject to certain restrictions on their purchase, resale

and transfer. For more information, see ‘‘Subscription and Sale’’ and‘‘Transfer Restrictions’’.

Dividends . . . . . . . . . . . . . . . . . Subject to the considerations and limitations discussed in ‘‘DividendPolicy’’, it is our current dividend policy that not less than 20% of ourprofit for the year attributable to shareholders of the Company (afterseparately disclosable items) will be distributed as dividends. We donot intend to pay a dividend in respect of our pro forma results ofoperations for the year ended December 31, 2006 or the six monthsended June 30, 2007.

Although we can make no guarantee that we will, should we declareany dividends in the future, our Shares sold in the Global Offering,including any of our Shares sold pursuant to the exercise of theOver-allotment Option, if any, will be entitled to any such dividends ifthe relevant record date is on or after the Closing Date or the closingdate of the Over-allotment Option, as applicable.

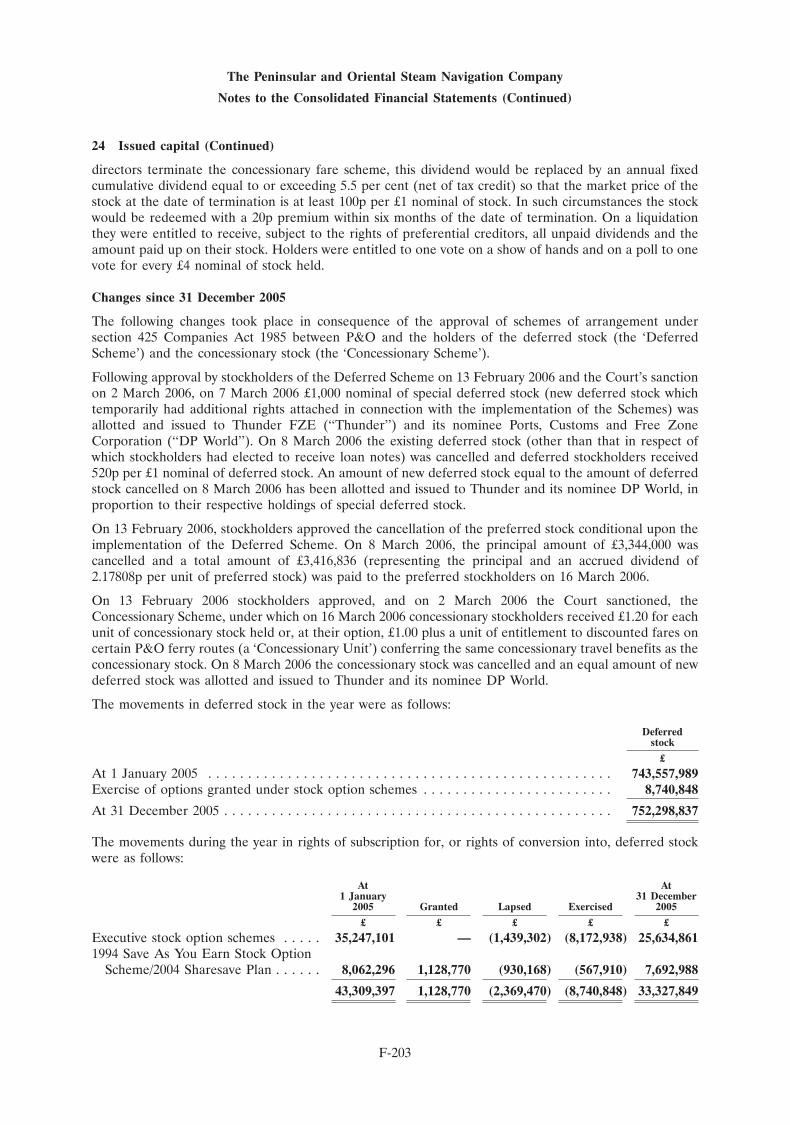

Use of proceeds . . . . . . . . . . . . The net proceeds which will be received by the Selling Shareholderfrom the Global Offering will be approximately $3,109.3 million (orapproximately $3,699.7 million if the Over-allotment Option isexercised in full) (in each case, after deduction of commissions). All ofthe expenses of the Global Offering will be paid by the SellingShareholder.