Embed Size (px)

Citation preview

2014 HIS Vendor ReviewPart 4: Small Hospital Vendors

© 2015 by H.I.S. Professionals, LLC, all rights reserved.

By Vince Ciotti, PrincipalHIS Professionals, LLC

CPSI Medhost Healthland NextGen

Small Hospital Vendors• Our revenue review ends with vendors targeting:

– Small hospitals of under 100 beds, including Critical Access Hospitals (CAH) of <25 beds

– Before you dismiss this “tiny” market, realize there are over 1,300 CAH hospitals in the US,

– Plus another ≈1,000 from 25 to 100 beds, so this “small” market has a large footprint!

• This episode covers the 4 big small vendors:

- In the bottom of the pack in revenue

- But with huge client bases

- Origins, acquisitions, & mergers

- Recent revenue growth/decline

- Candid assessment of future prospects

© 2015 by H.I.S. Professionals, LLC, all rights reserved.

• Computer Programming & Systems, Inc. – was founded in 1979 and has been on our HIS vendor revenue charts for decades:

• A rather impressive revenue HIS-tory considering their target market is hospitals with under 100 beds who have small IT budgets…

© 2015 by H.I.S. Professionals, LLC, all rights reserved.

• They have a total of about 650 clients, most of which are CAH or under 100 beds, with only a few larger community hospitals:

CPSI Client Base

© 2015 by H.I.S. Professionals, LLC, all rights reserved.

(this page left blank intentionally)

CPSI’s Many Product Lines

• Compared to the bewildering array of products from giants like McKesson, Siemens, Allscripts, GE, Meditech, etc., CPSI is easy:

CPSI Products & Prospects

- It’s the “CPSI System,” period.

- Saving them a ton of money on marketing staff, brochures, ppt slides, proposals, contracts, etc.

• Other “quirks” include having never bought anything, ever!

– They self-developed every single application & module inhouse, and their product breadth is amazingly wide & deep:

• Not only every clinical & financial app, but all ancillaries, and even their own Time & Attendance system and PACS!

• So we’re pretty bullish on them remaining on top of the small vendor market for quite some time, especially if small hospitals are getting over their post-MU blues and going to market again.

© 2015 by H.I.S. Professionals, LLC, all rights reserved.

• At HIMSS in April, 2015, CPSI shocked the small hospital crowd when they renamed themselves as Evident, LLC.

• Evident-ly they feared their old moniker of “Computer Programming & Systems, Inc.” sounded a little archaic…

2015 Flash!

• They also re-named their HIS from “CPSI System” to “Thrive,” which is what they hope to do in the mid-size hospital market of 100 to 300 beds. Easier to announce that goal than to attain it…

– They kept the name “TruBridge” for their RCM outsourcing business, so now we’ll see if the marketing mavens on Wall Street who sell such “branding” techniques pay off…

© 2015 by H.I.S. Professionals, LLC, all rights reserved.

• Founded as Health Management Systems in 1984, HMS was acquired by VC firm Primus in 2007, who formed HealthTechHoldings as their parent company, then merged them with EDIS leader MedHost in 2010. Confused? So am I, but at least now no one mixes them up with the other “HMS” vendor in NYC…

- HMS grew rapidly by selling to the many hospital chains also based near Nashville, like Community Health Systems, with 200 hospitals in 29 states.

• Their forte for these chains is an ERP designed to pool cash payments from many hospitals into one central bank, while centralizing AP, purchasing & materials as well - tricky stuff!

- MedHost was a long-term leader in EDIS systems, and with a slick interface to HMS, they pose a nice solution to how EDs are the source of most admissions.

© 2015 by H.I.S. Professionals, LLC, all rights reserved.

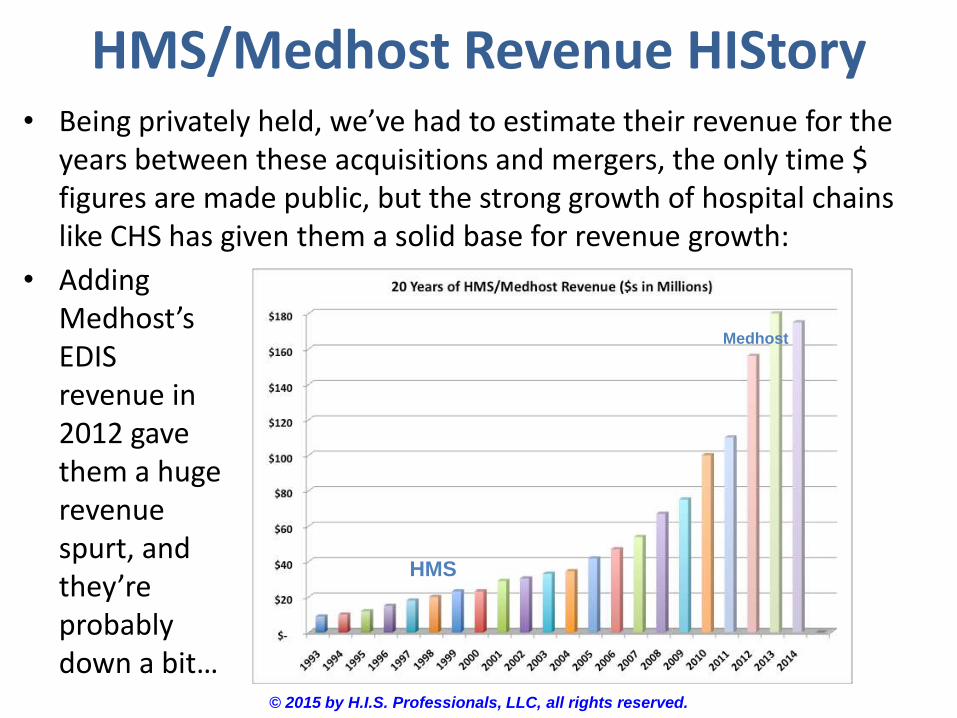

• Being privately held, we’ve had to estimate their revenue for the years between these acquisitions and mergers, the only time $ figures are made public, but the strong growth of hospital chains like CHS has given them a solid base for revenue growth:

• Adding Medhost’sEDIS revenue in 2012 gave them a huge revenue spurt, and they’re probably down a bit…

HMS/Medhost Revenue HIStory

HMS

Medhost

© 2015 by H.I.S. Professionals, LLC, all rights reserved.

• Their HIS client base is skewed toward the smaller & mid-sized hospitals that proprietary chains like CHS tend to acquire; in addition, they have ≈370 EDIS hospital clients of all bed sizes.

Medhost HIS Client Base

© 2015 by H.I.S. Professionals, LLC, all rights reserved.

• Founded as Dairyland in 1981 in Minn, Healthland grew rapidly in their specialty market among small hospitals in the Midwest. Re-named Dairyland Health Systems (DHS), they were acquired in 2007 by Francisco Partners (who also bought QuadraMed).

- Healthland’s original HIS was such a “classic” they named it that, to distinguish it from several other HIS vendors & systems they’ve acquired over the years:

• “Centriq” – Healthland’s latest “go forward” system they are trying to convert their large client base of ≈500 small hospitals (most under 50 beds) over to; so far, about half have moved…

- Advanced Professional Software (APS) out of Waco, TX, in 2008, a financial vendor acquired mainly for its 140 clients.

- American Health Network (AHN), whose modern “Claris” system helped lead Healthland into developing its modern HIS:

© 2015 by H.I.S. Professionals, LLC, all rights reserved.

• Being privately held like HMS, we’ve had to estimate Healthland’s revenue for the years between these acquisitions, the only time $ figures are made public, but the addition of APS and AHN’s systems and clients should have given them growth:

• Their revenue suffered post-Y2K like almost every other HIS vendors did, and they probably slowed post MU…

Healthland Revenue HIStory

Y2K

MU

© 2015 by H.I.S. Professionals, LLC, all rights reserved.

• NextGen is the smallest player in the small-sized hospital market in number of hospitals, but they have the largest revenue ($445M) due to the huge physician practice revenue from ≈40K MD clients.

- NextGen’s parent firm QSI (Quality Systems Inc) was formed many decades ago, and they are a giant in the physician practice market, commonly known as “ambulatory” (as if hospitals didn’t have a lot of outpatients who walk in for tests…)

• QSI recently acquired the “free” interface engine formerly known as Mirth, so you may see their name pop up in IE bids...

• NextGen got into the hospital field by acquiring two HIS vendors:

- Opus– a solid EHR piloted by hospital chain Universal Health Systems (UHS).

- Sphere – Florian Weiland’s rock-solid financial systems, both RCM & ERP.

• At HIMSS in April, 2015, a NextGen rep surprised us by stating they would no longer be selling the Opus/Sphere “solution” to community hospitals, but just CAH sites.

• They’ll keep supporting it for the ≈80 current clients on Opus & Sphere, but new prospects will be CAH only…

2nd 2015 HIMSS Shocker…

• Sad news for the 25-100 bed hospitals who hoped that a giant firm like NextGen would pour the financial investment needed to build a truly integrated hospital & physician practice system.

© 2015 by H.I.S. Professionals, LLC, all rights reserved.

• Interesting trend how many leading physician practice vendors are buying their way into the hospital HIS market like NextGen:

– Allscripts – this MD giant with ≈50K physician practices on its PM and EHR systems acquired Eclipsys in 2010 to enter the large hospital market through its strong RCM & EHR systems.

– Athenahealth just acquired RazorInsights, a very small HIS vendor (≈$2M in annual revenue) with only ≈30 clients, mostly CAH, based in GA. Athenahealth is a major player in the physician practice market with about 60K providers.

• I guess these moves make them feel they can compete with Epic by playing in both markets, but what a difference to have a fully integrated system for hospitals & physician practices like Epic pioneered (and Meditech & Paragon are now starting to build), versus buying an HIS and building an interface to its foreign DB and OS, like these 3 physician practice vendors have done…

Latest Big Entrant into Small Market

Recap• So there it is, the 2014 revenue figures for the 12 leading HIS

vendors, separated into their three target market niches:

– Large hospitals >300 beds, AMCs & IDNs, who buy:

• Cerner, Epic, Allscripts and GE

– Mid-sized community hospitals from 1-300 beds, who buy:

• Meditech, McKesson’s Paragon, NTT Data & QuadraMed– Small hospitals under 100 beds, who generally buy from:

• CPSI (“Evident”), Medhost, Healthland and Next(“Last?”)Gen

• The only question I couldn’t answer is why so many have blue as the color of their logo – is it a sign of recent market activity?

• I’m sure I missed a few things more, so if you have any questions (like how much I got for my 1969 Honda CB750 on eBay), contact:

- 505.466.4958