Embed Size (px)

Citation preview

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 1/58

Dr. Denis Schweizer Associate Professor of Finance John Molson School of Business, Concordia UniversityMailing address: 1455 de Maisonneuve Boulevard West, Montreal, Quebec H3G 1M8Office: MB 11.305Phone: +1(514)-848-2424, ext. 2926Fax: +1(514)-848-4500E-mail: [email protected]

5. Asset Allocation

Investment Analysis

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 2/58

Page 2Investment AnalysisDenis Schweizer

Agenda

I. Ambiguity Risk

II. Strategic Asset Allocation with Alternative Investments

III. Application to Hedge Funds

IV. Appendix: Estimation of Ambiguity Aversion

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 3/58

Page 3Investment AnalysisDenis Schweizer

Zeitraum: 12.94-12.04

A n n u a l i s i e r t e R e n d i t e

4%

6%

8%

10%

12%

100% Hedgefonds

100% trad. Portfolio

15% Hedgefonds

4,2 % 4,4 % 4,6 % 4,8 % 5,0 %

14%

Annualisierte Volatilität

10% 5% Hedgefonds

z Ein Investment in diversifizierten Hedgefonds-Strategien bietet die Möglichkeit,

das Risiko-/ Ertragsverhältnis zu verbessern

z Zahlreiche wissenschaftliche Studien belegen vorgenanntes Ergebnis

Trad. Portfolio*

76% Renten

10% Aktien

10% Immobilien

4% Liquidität

7.0%

9.0%

11.0%

13.0%

15.0%

17.0%

0% 2% 4% 6% 8% 10% 12% 14% 16%

volatility

r e t u r n

equity, bonds, without hedgefundsequities, bonds plus hedge funds

8,5%

9,0%

9,5%

10,0%

10,5%

11,0%

11,5%

12,0%

0,0% 2,0% 4,0% 6,0% 8,0% 10,0% 12,0% 14,0% 16,0% 18,0%

Volatilität p.a.

R e n

d i t e p . a .

Rohstoffe: 40%

US-Aktien: 40%

US-Anleihen: 20%

Rohstoffe: 10%

US-Aktien: 10%

US-Anleihen: 80%

US-Anleihe: 100%

US-Aktien: 100%

Is an investmen t in tradit ional investmen ts st i l l reasonable?

Or is the re levant qu estion: “H ow m uch should be invested in w hich Alternative

Investme nt c lass?”

Do Alternative Investments add Value to

traditional Portfolios?

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 4/58

Page 4Investment AnalysisDenis Schweizer

How do portfolio of German institutional investors

look like and why is this the case?*

0,005

0,0055

0,006

0,0065

0,007

0,0075

0,008

0,0085

0,009

0,006 0,011 0,016 0,021 0,026 0,031

E x p

e c t e d R e t u r n p . m .

Standard Deviation p. m.

Empirischer Rand Impliziter Rand investiertes Portfolio

0,005

0,0055

0,006

0,0065

0,007

0,0075

0,008

0,0085

0,006 0,011 0,016 0,021 0,026 0,031

e r w a r t e t e R e n d i t e p . m .

Standardabweichung p. m.

Empirischer Rand

investiertes Portfolio

Results are based on a study by Funke, Johanning und Rudolph (2006). They asked147 German institutional investors for their asset allocation.

*

Summary

• The average invested portfolio is not onthe efficient frontier

• Diversification benefits are lost

• For the given expected return the in

investment weight for……bonds is close to be identical…shares is too high (about 6%)…Alternative Investments is too low

(about 5%)

The reasons for this investment behavior can be found in the Behavioral-Finance-Research and aresummarized under the term „ambiguity risk“

The more familiar an investor is with a certain asset class the less is his „ambiguity risk“

The „ambiguity aversion“ for German institutional investors corresponds with an risk increase of

87%, which means that the implicit monthly standard deviation is 6.38% compared with an empirical

3.41%!

Bonds Stocks Alternative Inv.

Average Allocation 80.02% 13.71% 6.28% Optimal Allocation 81.36% 7.74% 10.90%

Empirical Frontier Implicit Frontier Invested Portfolio

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 5/58

Page 5Investment AnalysisDenis Schweizer

Agenda

I. Ambiguity Risk

II. Strategic Asset Allocation with Alternative Investments

III. Application to Hedge Funds

IV. Appendix: Estimation of Ambiguity Aversion

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 6/58

Page 6Investment AnalysisDenis Schweizer

Agenda

II. Strategic Asset Allocation with Alternative Investments

a. Distribution Properties

b. Risk Measures

c. Risk Adjusted Performance Measures

d. Optimization Procedure

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 7/58

Page 7Investment AnalysisDenis Schweizer

The normal distribution is the classical reference

for the measurement of risk and return

x

f(x)

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 8/58

Page 8Investment AnalysisDenis Schweizer

Are the properties of the normal distribution

sufficient to evaluate return distributions?

The normal distribution can be described completely by the parameters µ (expected value)and σ (standard deviation)

The focal point of the distribution is the expected value – this is where the mostobservations are realized

The distribution is symmetric around the expected value

− The skewness is zero

The “width” of the distribution is determined by the standard deviation – the higher thestandard deviation, the flatter the curve of the distribution

− The kurtosis of the normal distribution is three, i.e. the excess kurtosis is zero

− The higher the kurtosis, the more of the realized returns are at the edges of the

distribution Normally distributed returns are frequently assumed in financial economics / portfolio

theory

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 9/58

Page 9Investment AnalysisDenis Schweizer

Are returns normally distributed?

The normal distribution and the “68-95-rule”

H ow large i s the skewness kurtos is and excess-kurtos is of the normal

distr ibut ion?

H ow can w e evalua te if returns a re in fac t norm ally distributed?

x

f(x)

68% 95%

μ +2 σ μ - 2 σ

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 10/58

Page 10Investment AnalysisDenis Schweizer

Typical Shapes of “Normal” Distributions

normal distribution right (positive) skewed distribution

left (negative) skewed distribution leptocurtic (fat teiled) distribution

platykurtic distribution

Return

P r o b a b i l i t y m a s s

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 11/58

Page 11Investment AnalysisDenis Schweizer

Typical hedge fund strategy distributions

-40% -33% -25% -17% -9% -1% 7%

Historical Return

Equity Market Neutral

Frequency

Normal Distribution

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 12/58

Page 12Investment AnalysisDenis Schweizer

The skewness and its influence as the third

moment of the return distribution

FSD=FPSD

FSD=FPSD

FSD>FPSD

FSD<FPSD

FSD>FPSD

Symmetrical Distribution (SD)

Positively Skewed

Distribution (PSD)

Mean

FSD=FPSD

FSD=FPSD

FSD>FPSD

FSD<FPSD

FSD>FPSD

Symmetrical Distribution (SD)

Positively Skewed

Distribution (PSD)

Mean

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 13/58

Page 13Investment AnalysisDenis Schweizer

Risk-averse investors have a preference for right-

skewed distributions

The symmetrical distribution features more returns at the left edge of the distributionthan a positively (right) skewed distribution

At the vertical lines, both distributions have the same number of realizations above andbelow these lines

This implies that between the two vertical lines more returns are realized in the positively(right) skewed distribution

In the positively (right) skewed distribution, more realizations are below the

expected value

− But: extreme losses can be avoided

− Furthermore, the probability of high profits is higher than for a symmetricdistribution that is identical in all other respects

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 14/58

Page 14Investment AnalysisDenis Schweizer

The kurtosis and its influence as fourth moment

of the return distribution

FEK=FNEKFEK=FNEK

FEK>FNEK

FEK<FNEEK

FEK>FNEK

Distribution without

Excess-Kurtosis (NEK)

Distribution with

Excess-Kurtosis (EK) FEK<FNEEK

Mean=Median=Modus

FEK=FNEK

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 15/58

Page 15Investment AnalysisDenis Schweizer

Investors with High Loss Aversion Prefer Return

Distributions without Excess-Kurtosis

Return distributions with positive Excess-Kurtosis (leptokurtic) feature extreme

returns more often than distributions with negative Excess-Kurtosis (platykurtic)

Expected absolute losses as well as probability of profits is higher for leptokurticdistributions

Investors aiming at avoiding high losses do not invest in Asset classes with leptocurticdistributions

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 16/58

Page 16Investment AnalysisDenis Schweizer

Testing for Normal Distribution

The Jarque-Bera Test uses the estimators for skewness and kurtosis of a distribution. Thetest statistic is calculated as follows:

=6 2 +

3 2

4, = ~ 2 2

The test parameter is asymptotically 2 2 -distributed with two degrees of freedom

H0 = data is normally distributed

H1 = data is not normally distributed

The null hypothesis can be rejected at the 5% (1%) confidence level, if the test parameter( JB ) is higher than 5.99 (9.21)

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 17/58

Page 17Investment AnalysisDenis Schweizer

Agenda

II. Strategic Asset Allocation with Alternative Investments

a. Distribution Properties

b. Risk Measures

c. Risk Adjusted Performance Measures

d. Optimization Procedure

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 18/58

Page 18Investment AnalysisDenis Schweizer

Variance

The variance σ 2 is the most frequently used variability measure

In order to calculate the variance, the differences of all returns with their average aresquared, summed up, and divided by the number of observations

2 =

=1

1 1 ̅ 2 + 2 ̅ 2 + ⋯ + ̅ 2

=1

1 ̅ 2

=1

The variance is the average squared deviation from the average!

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 19/58

Page 19Investment AnalysisDenis Schweizer

Standard Deviation

The standard deviation σ is the square root of the variance Advantage: the standard deviation is denominated in the same dimension as the average

(the return) and is therefore easier to interpret.

The variance is denominated in the dimension of return-square.

= =

=1

1 ̅ 2

=1

Annualization: .. = .. ∙

Empirical examples for the standard deviation

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 20/58

Page 20Investment AnalysisDenis Schweizer

Semi-Volatility

When calculating the semi-volatility, only the negative deviations from the average aretaken into account:

=

1

� 2

=1

For being below the average

Annualization is conducted analogously to the standard deviation

.. = .. ∙ 252

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 21/58

Page 21Investment AnalysisDenis Schweizer

Maximum Draw Down

Maximum Draw Down (MaxDD) indicates the highest loss ever realized

0

50

100

150

200

250

300

J a n 9 1

J a n 9 2

J a n 9 3

J a n 9 4

J a n 9 5

J a n 9 6

J a n 9 7

J a n 9 8

J a n 9 9

J a n 0 0

J a n 0 1

J a n 0 2

J a n 0 3

J a n 0 4

J a n 0 5

J a n 0 6

W e r t

Crude oil

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 22/58

Page 22Investment AnalysisDenis Schweizer

Short Fall Risk (Lower Partial Moments)

What is the probability of missing the target (loss)?

How large are the expected losses in the case of losses?

What is the variability of the losses?

=1

∙

=1 = 1,

<

= 0,

= ()

0 =

1 = 2 = ( )

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 23/58

Page 23Investment AnalysisDenis Schweizer

Exercise: LPM and Semi-Volatility

You observe following prices for an asset:

Calculate following risk measures for τ = 0% and τ = 5%:

− (0)

− (1)

− (2)

− Semi-Volatility

Date Price

Jan 1, 2013 $100.00

Feb 1, 2013 $105.00

Mar 1, 2013 $98.00

Apr 1, 2013 $102.30

May 1, 2013 $96.25

Jun 1, 2013 $108.00

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 24/58

Page 25Investment AnalysisDenis Schweizer

Value-at-Risk (VaR)

The Value-at-Risk denotes the loss that will not be exceeded with a probability ( α ) and

within a certain time horizon (t).

Example: A portfolio with a total value of $ 5 million has a VaR of $ 50,000 for an a of99% and a holding period of t=1 day

That means, that with a certainty of 99%, for an invested sum of $ 5 million, there will notoccur a loss larger than $ 50,000 within the next day.

What are the problems associated with using the Value-at-Risk ?

Probability,e.g. 1%

Value distribution for a giventime horizon,e.g. 1 day

Expected Value

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 25/58

Page 26Investment AnalysisDenis Schweizer

Problems with using the VaR

What is the risk and the VaR of a short put?

S t +1 Bt =S t −VaR(95%)t stock

Value-at-Risk for a normally distributed underlying

Probability

p=5 %

∆S

Profit-and-loss profile of ashort put at maturityduration = holding period

Strike Price

VaR(95%) underlying(10 days holding period)

∆S =0S t =current price of the underlying

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 26/58

Page 27Investment AnalysisDenis Schweizer

-15,0% -10,0% -5,0% 0,0% 5,0% 10,0% 15,0%

Historical Data

Fitted Distribution

Max Loss CVaR VaR

F r e q u e

n c y

Probabilityα=0.01

Return-15.0% -10.0% -5.0% 0.0% 5.0% 10.0% 15.0%

Conditional Value at Risk

The volatility measures the

symmetric scattering of the expectedreturns around the average

For asymmetrical returndistributions the volatility does notmeasure the risk adequately

VaR as a risk measure cuts thereturn distribution at the alpha-quantile and disregards all lossesbeyond that threshold –theoretically, total default risks canbe neglected by this risk measure

CVaR indicates the average expectedloss beyond the VaR and thereforedoes not only account for themagnitude, but also the probabilityof extreme risks

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 27/58

Page 28Investment AnalysisDenis Schweizer

Agenda

II. Strategic Asset Allocation with Alternative Investments

a. Distribution Properties

b. Risk Measures

c. Risk Adjusted Performance Measures

d. Optimization Procedure

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 28/58

Page 29Investment AnalysisDenis Schweizer

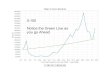

Sharpe Ratio

TheSharpe Ratio

measures the excess return of a portfolio over the risk free rate per riskunit (volatility)

= =

Volatility

Performance

Risk Free Rate

(MoneyMarket)

Portfolio

α

SR m easures the s lope

Th e high er the s lopte the

highe the sha rpe rat io

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 29/58

Page 30Investment AnalysisDenis Schweizer

Sortino Ratio

The Sortino Ratio measures the excess return of a portfolio over the risk free rate per riskunit (LPMtau (2))

= = 2

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 30/58

Page 31Investment AnalysisDenis Schweizer

Sterling Ratio and Reverse Calmar Ratio

The Sterling Ratio measures the excess return of a portfolio over the risk free rate perrisk unit measured by Maximum Drawdown (MaxDD)

=

=

What is the average time period an investor has to wait (measured in years) until the loss iscaught up – Reverse Calmar Ratio?

= �(. )

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 31/58

Page 32Investment AnalysisDenis Schweizer 32

Return on Value-at-Risk

The Return on Value-at-Risk measures the excess return of a portfolio over the risk free

rate per risk unit measured by Value-at-Risk (in absolute terms) for a givenα

-Quantile andtime period

() = ()

© Denis Schweizer

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 32/58

Page 33Investment AnalysisDenis Schweizer

Autocorrelation

Abnormality(?):

High Sharpe Ratios for Hedge Fund indices (market inefficiencies?)

Returns of Hedge Funds are in general not normally distributed

Negative skewness and high kurtosis, especially when the Sharpe Ratio is high

High autocorrelation (AC) of first order for the returns

High autocorrelation yields to an underestimation of the volatility ( Smoothing ) and

therefore the Sharpe Ratio is overestimated

⇒ Reasons are e.g. illiquid trading strategies for which a daily appraisal is not possible

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 33/58

Page 34Investment AnalysisDenis Schweizer

Basic De-Smoothing of Autocorrelation

De-Smoothing of the returns – first order AC (Brooks / Kat 2002, Geltner 1993):

= ∗

−1

∗

1

− = unobservable , true return in t

− ∗ = observable Return in t

− = Autocorrelation

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 34/58

Page 35Investment AnalysisDenis Schweizer

Advanced De-Smoothing Techniques

New method introduces by Getmansky, Lo und Makarov (2004, JFE) which isappropriate for Alternative Investments

Returns of Alternative Investments often show high levels of autocorrelation because ofappraisal smoothing, stale pricing, illiquidity, etc.

The observable return is the weighted sum of the past returns

− 0 = Θ0 ∙ + ⋯ + Θ ∙ −

− Θ 0,1 and = 0, … ,

− 1 = Θ0 + ⋯ + Θ

Therefore:− 0 =

− 0 = 2 ∙ 2 ≤ 2 with 2=Θ02+,…, Θ2

Advanced De-Smoothing Techniques

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 35/58

Page 36Investment AnalysisDenis Schweizer

Advanced De-Smoothing Techniques

(continued)

For solving the problem Getmansky, Lo und Makarov (2004) suggest a de-smoothing ofthe returns:

− 1. step: Estimation of the parameters Θ0 + ⋯ + Θ with MaximumLikelihood (MLE)

− 2. step: Calculation of the true returns and volatilities

Example:

− 0 = 0.25 ∙ + 0.25 ∙ −1 + 0.25 ∙ −2 + 0.25 ∙ −3

−

2=

4

∙0.252 = 0

.25

Therefore, the true (de-smoothed) variance is four times higher then the observed variance

Descriptive Statistics for the Different HF

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 36/58

Page 37Investment AnalysisDenis Schweizer

Descriptive Statistics for the Different HF

Strategies with and without Autocorrelation

Without Autocorrelation

Convertible

Arbitrage Distressed

Emerging

Markets

Equity Market

Neutral Event Driven

Fixed Income

Arbitrage Global Macro L/S Equity

Mean p.m. 0,31% 0,67% 0,50% 0,51% 0,50% 0,09% 0,91% 0,72%

Standard Diviation

p.m. 3,98% 3,84% 8,55% 3,73% 2,66% 3,55% 5,48% 6,24%

Skewness -3,45 -2,63 -1,14 -8,84 -0,92 -4,15 -0,50 -0,32

Excess Kurtosis 18,14 15,94 5,08 97,83 5,42 25,48 4,42 3,19

arque-Bera 2370,74 1772,01 194,97 62186,87 206,12 4518,47 129,18 66,64

P-Value 0,00% 0,00% 0,00% 0,00% 0,00% 0,00% 0,00% 0,00%

With Autocorrelation Convertible

Arbitrage Distressed

Emerging

Markets

Equity Market

Neutral Event Driven

Fixed Income

Arbitrage Global Macro L/S Equity

Mean p.m. 0,45% 0,80% 0,68% 0,51% 0,54% 0,24% 1,02% 0,82% Standard Diviation

p.m. 2,08% 1,97% 4,31% 3,45% 1,31% 1,84% 2,87% 3,09%

Skewness -3,59 -2,73 -1,29 -11,29 -1,05 -4,50 -0,28 0,05

Excess Kurtosis 18,74 14,01 6,61 134,79 4,68 27,26 3,71 3,41

arque-Bera 2534,27 1423,88 316,87 117522,78 165,71 5185,03 88,65 73,17

P-Value 0,00% 0,00% 0,00% 0,00% 0,00% 0,00% 0,00% 0,00%

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 37/58

Page 38Investment AnalysisDenis Schweizer

Agenda

II. Strategic Asset Allocation with Alternative Investments

a. Distribution Properties

b. Risk Measures

c. Risk Adjusted Performance Measures

d. Optimization Procedure

Validity and Applicability of Modern Portfolio

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 38/58

Page 39Investment AnalysisDenis Schweizer

Validity and Applicability of Modern Portfolio

Theory (MPT) Depends on Strict Assumptions

Assumptions of Markowitz’ portfolio selection (1952)

Perfect and complete capital market

Risk averse investors

Investments by the µ-σ-princpile

Time horizon is 1 period n linear independent and risk-bearing securities

Number of risk-bearing securities is 2 (or more)

Securities have finite variances and expected values

Normative recommendations

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 39/58

Page 40Investment AnalysisDenis Schweizer

Optimization Problem

The multiple-assets-portfolio has to be optimized by using different risk measures(volatility, semi-variance, conditional value at risk (5%) and maximum drawdown and fordifferent commodity benchmarks

The goal of the analysis is to answer the question if commodities are useful componentsfor portfolios under various levels of risk appetite and different expectations towards thefuture return of multiple-assets-portfolios?

Subject to constraint

for , , , , .

= ; 0 < ≤

1 + ⋯ + = 1 ∀ = 1, . . ,

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 40/58

Page 41Investment AnalysisDenis Schweizer

Agenda

I. Ambiguity Risk

II. Strategic Asset Allocation with Alternative Investments

III. Application to Hedge Funds

IV. Appendix: Estimation of Ambiguity Aversion

Descriptive Statistic for the Different Hedge

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 41/58

Page 42Investment AnalysisDenis Schweizer

Descriptive Statistic for the Different Hedge

Fund Strategies with AC

With

AutocorrelationConvertible

Arbitrage Distressed

Emerging

Markets

Equity

Market

Neutral

Event

Driven

Fixed

Income

Arbitrage

Global

Macro

L/S

Equity

Mean p.m. 0.45% 0.80% 0.68% 0.51% 0.54% 0.24% 1.02% 0.82%

Standard

Diviation p.m. 2.08% 1.97% 4.31% 3.45% 1.31% 1.84% 2.87% 3.09%

Skewness -3.59 -2.73 -1.29 -11.29 -1.05 -4.50 -0.28 0.05

Excess Kurtosis 18.74 14.01 6.61 134.79 4.68 27.26 3.71 3.41

Jarque-Bera 2,534.27 1,423.88 316.87 117,522.78 165.71 5,185.03 88.65 73.17

P-Value 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 42/58

Page 43Investment AnalysisDenis Schweizer

Autocorrelation Structure

Lag 1 Lag 2 Lag 3 Lag 4 Lag 5 Lag 6 Lag 7 Lag 8 Lag 9 Lag 10

Convertible

Arbitrage AC 0.557 0.270 0.180 0.141 -0.004 0.175 0.302 0.180 0.126 0.175

Distressed AC 0.388 0.281 0.155 0.119 0.072 0.005 -0.088 0.029 -0.014 -0.025

Emerging

Markets AC 0.281 0.081 0.110 0.033 0.016 -0.011 0.119 0.047 0.008 -0.018

Equity MarketNeutral

AC 0.074 0.257 0.157 0.105 0.051 -0.008 0.091 0.153 -0.001 0.024

Event Driven AC 0.336 -0.011 -0.102 -0.068 0.199 0.091 -0.024 -0.080 -0.036 0.097

Fixed Income

Arbitrage AC 0.503 0.134 0.070 0.059 -0.095 -0.015 0.283 0.221 0.093 0.094

Global Macro AC 0.159 0.072 0.108 -0.106 0.103 0.078 -0.126 0.150 -0.112 0.030

L/S Equity AC 0.202 0.104 -0.017 -0.088 -0.191 0.178 0.121 0.123 0.116 0.039

Numbers in „bold“ mean that the is a s ignificant autocorrelation for the respective lag (95%-level)

Descriptive Statistic for the Different Hedge

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 43/58

Page 44Investment AnalysisDenis Schweizer

p g

Fund Strategies without AC

Without Autocorrelation

Convertible

Arbitrage Distressed

Emerging

Markets

Equity

MarketNeutral

Event

Driven

Fixed

Income

Arbitrage

GlobalMacro

L/S Equity

Mean p.m. 0.45% 0.80% 0.68% 0.51% 0.54% 0.24% 1.02% 0.82%

StandardDiviation p.m. 3.98% 3.84% 8.55% 3.73% 2.66% 3.55% 5.48% 6.24%

Skewness -3.45 -2.63 -1.14 -8.84 -0.92 -4.15 -0.50 -0.32

Excess Kurtosis 18.14 15.94 5.08 97.83 5.42 25.48 4.42 3.19

Jarque-Bera 2,370.74 1,772.01 194.97 62,186.87 206.12 4,518.47 129.18 66.64

P-Value 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

With

AutocorrelationConvertible

Arbitrage Distressed

Emerging

Markets

Equity

Market

Neutral

EventDriven

Fixed

Income

Arbitrage

GlobalMacro

L/S Equity

Mean p.m. 0.45% 0.80% 0.68% 0.51% 0.54% 0.24% 1.02% 0.82%

Standard

Diviation p.m. 2.08% 1.97% 4.31% 3.45% 1.31% 1.84% 2.87% 3.09%

Skewness -3.59 -2.73 -1.29 -11.29 -1.05 -4.50 -0.28 0.05

Excess Kurtosis 18.74 14.01 6.61 134.79 4.68 27.26 3.71 3.41

Jarque-Bera 2,534.27 1,423.88 316.87 117,522.78 165.71 5,185.03 88.65 73.17

P-Value 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

-Optimization and -Efficiency Line

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 44/58

Page 45Investment AnalysisDenis Schweizer

Use the Excel file to play around with weight restrictions. What is the impact on the efficient frontier

for different sets of restrictions? What are the „important“ HF strategies? Why does the portfolio for

the minimum variance portfolio look different from the maximum return portfolio? What is the

impact of the financial crisis? (Hint: The „green“ cells can be changed)

Convertible Arbitrage

Distressed

Emerging Markets

Equity Market Neutral

Risk Arbitrage(Event Driven)

Fixed Income Arbitrage

Global Macro

L/S Equity

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

14,0%

0,0% 2,0% 4,0% 6,0% 8,0% 10,0% 12,0% 14,0% 16,0% 18,0% 20,0%

R e t u r n p . a .

Volatility

Mean-Variance-Optimal without AC Mean-Variance-Optimal with AC

Convertible Arbitrage Distressed

Emerging Markets Equity Market Neutral

Risk Arbitrage (Event Driven) Fixed Income Arbitrage

Global Macro L/S Equity

p y

for Funds of Hedge Funds

C a u t i o n : C a p e d o e s n o t e n a b l e u s e r s

t o f l y .

—

m

n

c

o

um

w

n

n

a

b

FoHF Portfolio Optimizer.xlsm

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 45/58

Page 46Investment AnalysisDenis Schweizer

Agenda

I. Ambiguity Risk

II. Strategic Asset Allocation with Alternative Investments

III. Application to Hedge Funds

IV. Appendix: Estimation of Ambiguity Aversion

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 46/58

Page 47Investment AnalysisDenis Schweizer

Research Paper

Do Institutional Investors Care About the

Ambiguity of Their Assets? – Evidence From

Portfolio Holdings in Alternative Investments

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 47/58

Page 48Investment AnalysisDenis Schweizer

Motivation

One of the major contributions of the capital asset pricing theory (CAPM) is an easily-

applicable optimal portfolio strategy – market Portfolio and risk-free asset.

Admittedly, in practice researchers have documented several deviations from the CAPMportfolio strategy like

− disposition effect (see e.g. Odean(1998), Grinblatt/Keloharju (2001) andFeng/Seasholes (2005)),

− home bias effect (see e.g. Lewis (1995, 1999) and French/Poterba (1991)),

− loss aversion bias (see e.g. Kahneman/Tversky (1979)),

− status quo bias (see e.g. Samuelson/Zeckhauser (1998)),

− etc.

Besides behavioral biases, there is a further important reason for why investors might notfollow the optimal portfolio strategy according to the CAPM:

→ When investors do not perfectly know the risk- and return-characteristics of all riskyassets

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 48/58

Page 49Investment AnalysisDenis Schweizer

Motivation – Risk and Ambiguity

There are two urns:

− Urn A contains 50% red balls and 50% black balls

− Urn B contains red and black balls

(unknown distribution)

Now a gamble: You can win EUR 100 if a red ball is drawn.

Which urn do you choose for the gamble, A or B?

Now the same gamble, with the same urns, but now you can win EUR 100 if a black ball isdrawn.

Again: Which urn do you choose for this gamble, A or B?

A B

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 49/58

Page 50Investment AnalysisDenis Schweizer

ambiguity: state of

uncertainty withunknown probabilities

for possible outcomes

risk: state of

uncertainty withknown probabilities for

possible outcomes

Motivation – Ellsberg-Paradox

Common observation: people choose urn A for both gambles

But: If you choose urn A in the first place, you implicitly assume that urn B contains moreblack balls than red balls

… which makes urn B the optimal choice in the second gamble so called Ellsberg

paradox

Possible explanation: difference between risk and ambiguity

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 50/58

Page 51Investment Analysis

Denis Schweizer

Research Questions

In the real world (institutional and private) investors do not know for sure the true retrun-and risk-characteristics of all risky assets.

− Especially for some asset classes such as hedge funds and private equity because

no availibilty of a long history of asset prices,

the investment focus of the managers might considerably change over time,

intransparancy of the portfolio holdings,

etc.

Therefore, two research questions arise:

− Are empirical portfolio holdings of institutional investors effected by ambiguityaversion?

− Which asset classes do exhibit a high ambiguity and which do not?

Relation Between Ambiguity and Optimal

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 51/58

Page 52Investment Analysis

Denis Schweizer

g

Portfolio Allocation

Optimal Portfolios With and Without Ambiguity – illustrative example

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 52/58

Page 53Investment Analysis

Denis Schweizer

Model Framework Used for Calibration Exercise

We use the closed-form solutions provided by Uppal/Wang (2003):

αi represents the asset specific ambiguity parameter

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 53/58

Page 54Investment Analysis

Denis Schweizer

Description of Data Sample

Detailed portfolio holdings of 119 institutional investors

Proxy Indices for the asset classes are:

− Stocks: MSCI Europe -- Total Return index

− Bonds: JPM Europe Government Bond -- Total Return index

−

Real Estate: FTSE NAREIT All REITs -- Total Return index

− Private Equity : CepreX - equally weighted index of the US Growth/Small Buyout andUS Venture Capital single fund indices

− Hedge Funds: HFRX Global Hedge Fund Index

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 54/58

Page 55Investment Analysis

Denis Schweizer

Descriptive Statistics of Return Distributions

• We adjust the returns of the CepreX indices for management fees• We use the Getmansky/Lo/Makarov (2004) approach to unsmooth the private equity time series for significant

autocorrelation up to lag 12.

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 55/58

Page 56Investment Analysis

Denis Schweizer

Calibration Exercise

Implied Ambiguity Parameter Values

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 56/58

Page 57Investment Analysis

Denis Schweizer

Robustness Check

Implied Ambiguity for Different Expected Returns of Alternative Investments

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 57/58

Page 58Investment Analysis

Denis Schweizer

Conclusion

Using the formal model introduced by Uppal/Wang (2003) we can implicitly determinethe ambiguity of the assets in the portfolios of institutional investors.

We find that institutional investors do care for ambiguity because they accept aportfolio Sharpe ratio which is strongly below the maximum Sharpe ratio withoutambiguity.

In terms of the asset specific ambiguity, we can show that equity and bond portfolioshave a relatively low ambiguity in contrast to alternative investments

Among the alternative investments hedge funds exhibit a large ambiguity, even muchhigher than that of private equity investments; however, real estate investments ratherhave a relatively moderate ambiguity.

These qualitative results are robust with regard to the used parameters for the expectedreturns of the asset classes.

8/10/2019 5. Asset Allocation

http://slidepdf.com/reader/full/5-asset-allocation 58/58

References

Feng, L., and Seasholes, M., 2005, “Do Investor Sophistication and Trading Experience Eliminate

Behavioral Biases in Finance Markets?," Review of Finance, 9, 305-51.

French, K. R., and Poterba, J. M., 1991, “Investor Diversification and International Equity Markets," American Economic Review, 81, 222-226.

Grinblatt, M., and Keloharju, M., 2001, “What Makes Investors Trade?," Journal of Finance, 56, 589-616.

Kahneman, D., and Tversky, A., 1979, “Prospect Theory: An Analysis of Decision under Risk,"

Econometrica, 47, 263-291.

Lewis, K. K., 1995, „Puzzles in International Financial Markets," In: Grossman, G. M., and Rogoff, K.

(Eds.), Handbook Of International Economics, Vol. III, North-Holland, Amsterdam.

Lewis, K. K., 1999, “Trying to Explain Home Bias in Equities and Consumption," Journal of Economic

Literature, 37, 571-608.

Odean, T., 1998, “Are Investors Reluctant to Realize Their Losses?," Journal of Finance, 53, 1775-1798.

Samuelson, W., and Zeckhauser, R., 1988, „Status Quo Bias in Decision Making," Journal of Risk and

Uncertainty, 1, 7-59.