Embed Size (px)

Citation preview

JANE AMBACHTSHEERAMSTERDAM, 15 JANUARY 2020

CFA Society VBA Netherlands

5 YEARS AFTER COP 21, WHERE ARE WE AND WHAT LIES AHEAD?

marketing communication

1. TAKEAWAYS FROM COP 25

2. WHY WILL THERE BE AN INEVITABLE POLICY RESPONSE?

3. THE INEVITABLE POLICY RESPONSE

4. FROM TOP DOWN TO BOTTOM UP: INTRODUCING EROCI

5. TAKE AWAYS FOR INVESTORS WITH A 3-5 YEAR TIME HORIZON

CONTENTS

15/01/2020 25 years after COP 21, where are we and what lies ahead?

TAKEAWAYS FROM COP 251.

35 years after COP 21, where are we and what lies ahead? 15/01/2020

Takeaways from COP 25

45 years after COP 21, where are we and what lies ahead? 15/01/2020

Source: Google

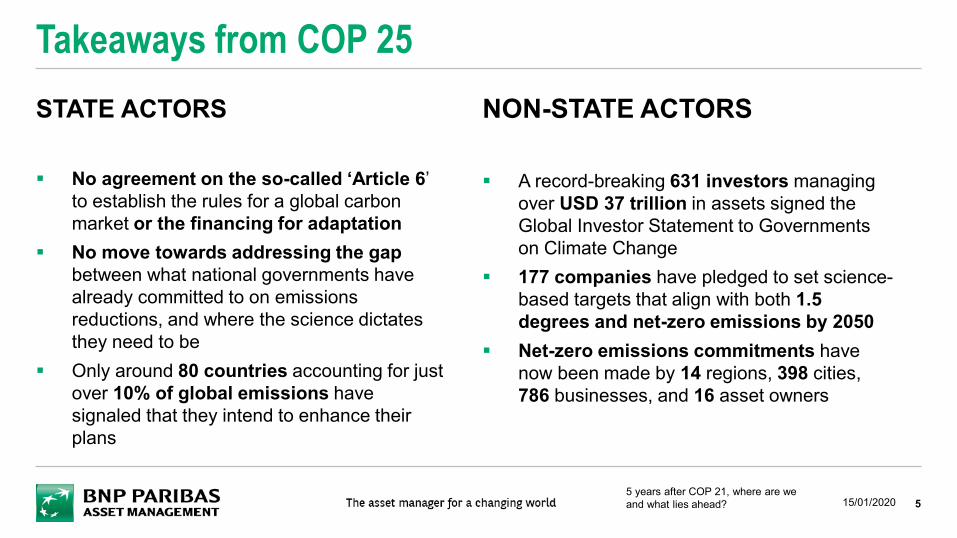

STATE ACTORS

No agreement on the so-called ‘Article 6’ to establish the rules for a global carbon market or the financing for adaptation

No move towards addressing the gap between what national governments have already committed to on emissions reductions, and where the science dictates they need to be

Only around 80 countries accounting for just over 10% of global emissions have signaled that they intend to enhance their plans

Takeaways from COP 25

5

NON-STATE ACTORS

A record-breaking 631 investors managing over USD 37 trillion in assets signed the Global Investor Statement to Governments on Climate Change

177 companies have pledged to set science-based targets that align with both 1.5 degrees and net-zero emissions by 2050

Net-zero emissions commitments have now been made by 14 regions, 398 cities, 786 businesses, and 16 asset owners

5 years after COP 21, where are we and what lies ahead? 15/01/2020

6

Today’s focus is on … A forecast policy response to climate

Developedby

5 years after COP 21, where are we and what lies ahead? 15/01/2020

Trademark, copyright, and other intellectual property rights are and remain the property of their respective owners.

WHY WILL THERE BE AN INEVITABLE POLICY RESPONSE?

2.

75 years after COP 21, where are we and what lies ahead? 15/01/2020

8

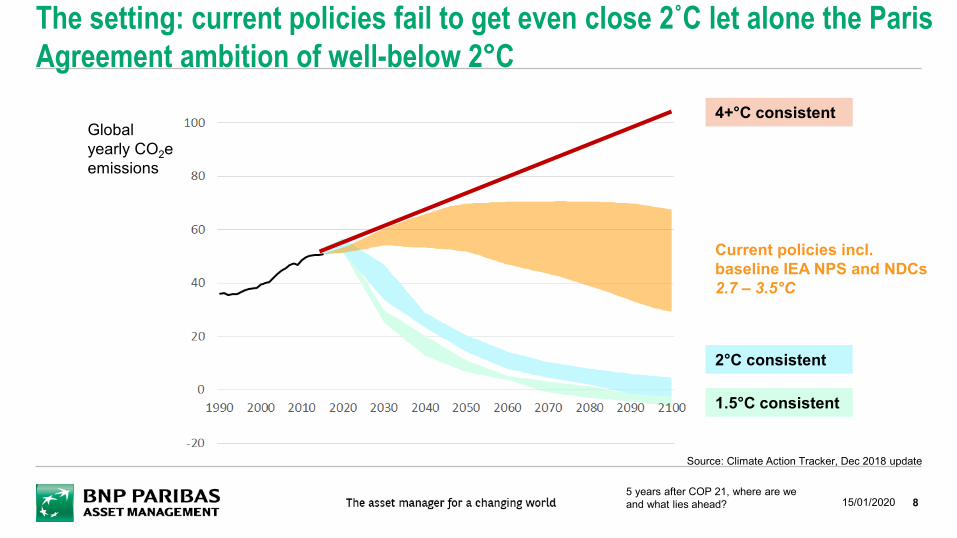

The setting: current policies fail to get even close 2˚C let alone the Paris Agreement ambition of well-below 2°C

Source: Climate Action Tracker, Dec 2018 update

Current policies incl. baseline IEA NPS and NDCs2.7 – 3.5°C

2°C consistent

1.5°C consistent

Global yearly CO2e emissions

4+°C consistent

5 years after COP 21, where are we and what lies ahead? 15/01/2020

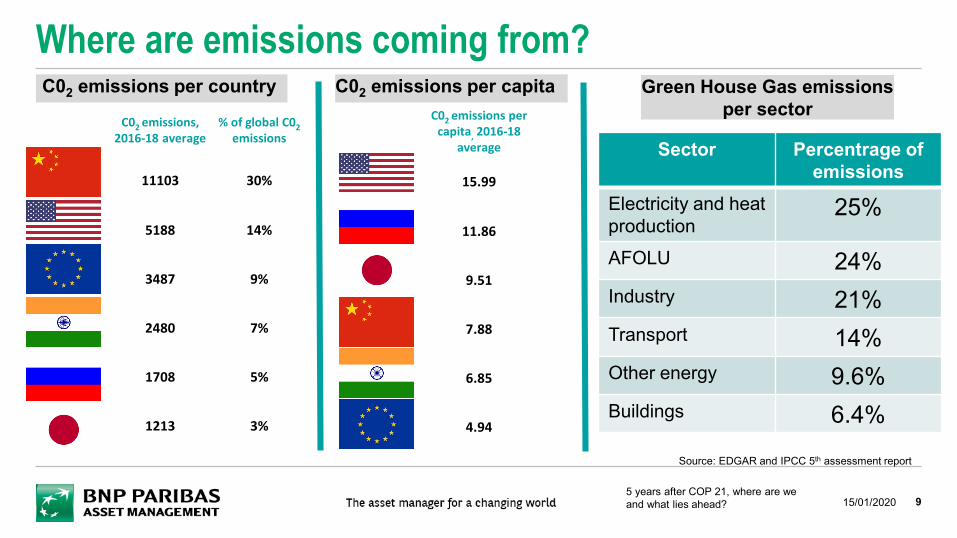

Where are emissions coming from?

9

Source: EDGAR and IPCC 5th assessment report

C02 emissions, 2016-18 average

% of global C02 emissions

11103 30%

5188 14%

3487 9%

2480 7%

1708 5%

1213 3%

C02 emissions per country C02 emissions per capita C02 emissions per

capita, 2016-18 average

15.99

11.86

9.51

7.88

6.85

4.94

Green House Gas emissionsper sector

Sector Percentrage of emissions

Electricity and heatproduction

25%

AFOLU 24%Industry 21%Transport 14%Other energy 9.6%Buildings 6.4%

5 years after COP 21, where are we and what lies ahead? 15/01/2020

10

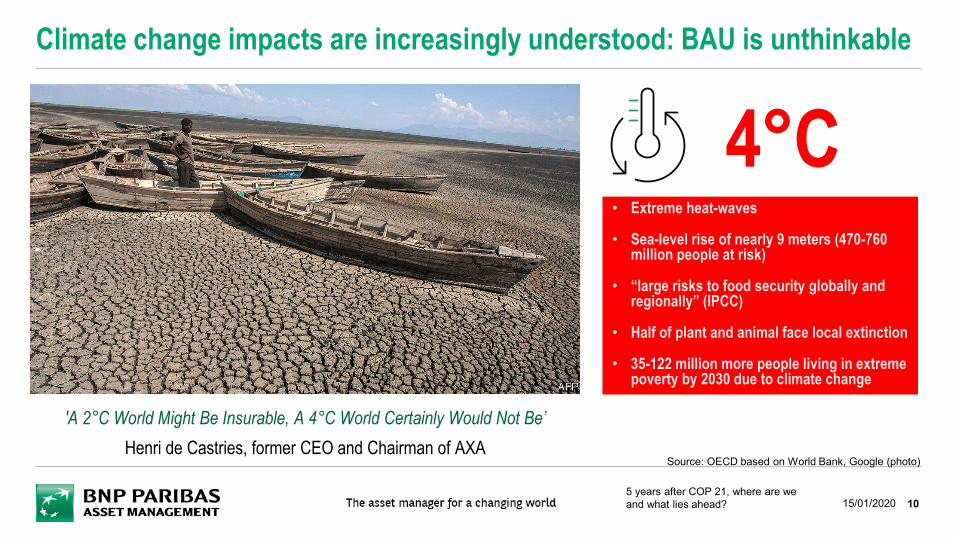

Climate change impacts are increasingly understood: BAU is unthinkable

'A 2°C World Might Be Insurable, A 4°C World Certainly Would Not Be’ Henri de Castries, former CEO and Chairman of AXA

• Extreme heat-waves

• Sea-level rise of nearly 9 meters (470-760 million people at risk)

• “large risks to food security globally and regionally” (IPCC)

• Half of plant and animal face local extinction

• 35-122 million more people living in extreme poverty by 2030 due to climate change

4°C

Source: OECD based on World Bank, Google (photo)

5 years after COP 21, where are we and what lies ahead? 15/01/2020

11

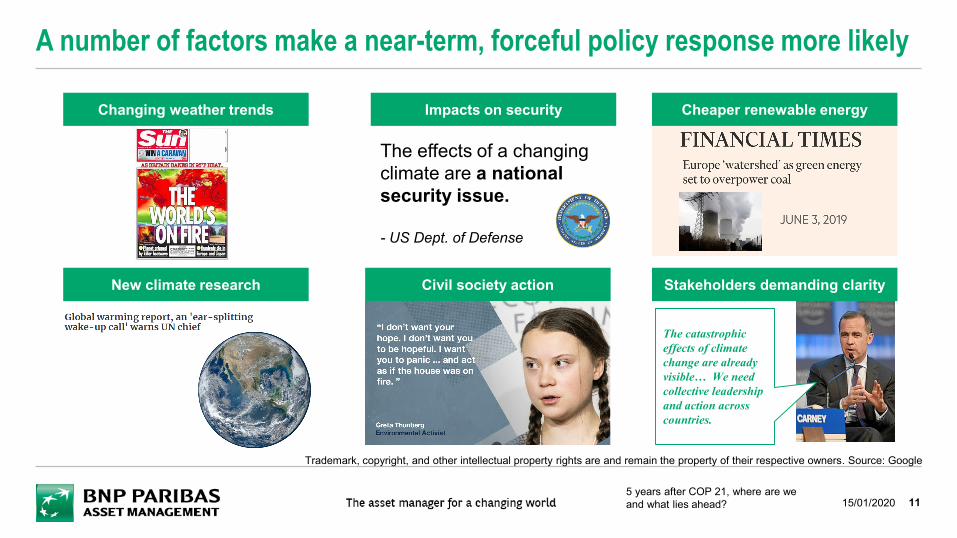

A number of factors make a near-term, forceful policy response more likely

The catastrophic effects of climate change are already visible… We need collective leadership and action across countries.

Changing weather trends

New climate research

Impacts on security Cheaper renewable energy

Stakeholders demanding clarity Civil society action

The effects of a changing climate are a national security issue.

- US Dept. of Defense

5 years after COP 21, where are we and what lies ahead? 15/01/2020

Trademark, copyright, and other intellectual property rights are and remain the property of their respective owners. Source: Google

THE INEVITABLE POLICY RESPONSE 3.

125 years after COP 21, where are we and what lies ahead? 15/01/2020

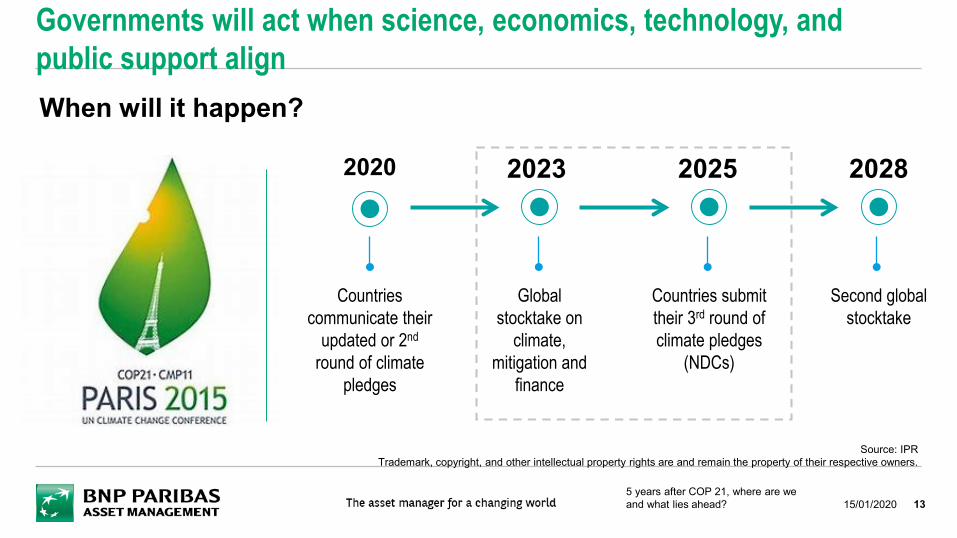

Governments will act when science, economics, technology, and public support align

13

When will it happen?

2020

Countries communicate their

updated or 2nd

round of climate pledges

2025

Countries submit their 3rd round of climate pledges

(NDCs)

2023

Global stocktake on

climate, mitigation and

finance

2028

Second global stocktake

Source: IPRTrademark, copyright, and other intellectual property rights are and remain the property of their respective owners.

5 years after COP 21, where are we and what lies ahead? 15/01/2020

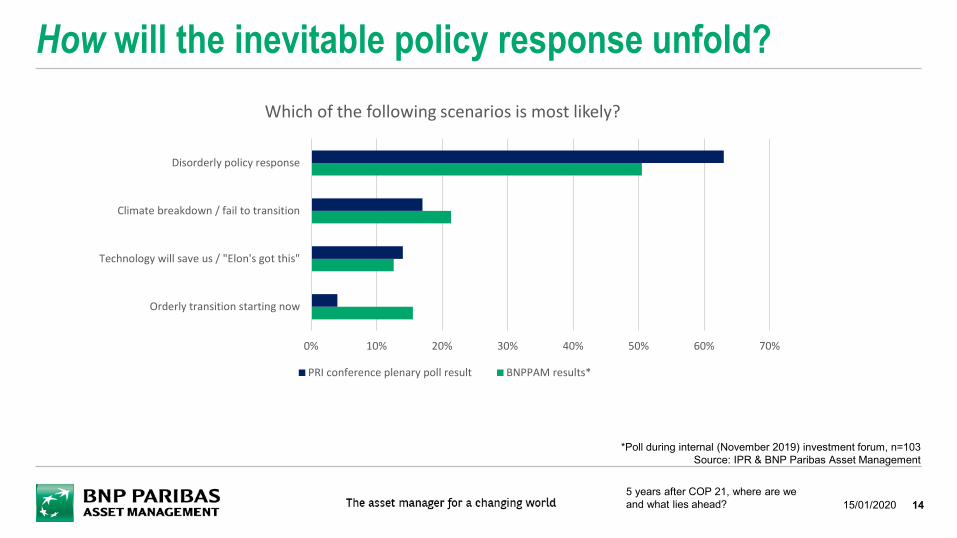

How will the inevitable policy response unfold?

14

0% 10% 20% 30% 40% 50% 60% 70%

Orderly transition starting now

Technology will save us / "Elon's got this"

Climate breakdown / fail to transition

Disorderly policy response

Which of the following scenarios is most likely?

PRI conference plenary poll result BNPPAM results*

*Poll during internal (November 2019) investment forum, n=103Source: IPR & BNP Paribas Asset Management

5 years after COP 21, where are we and what lies ahead? 15/01/2020

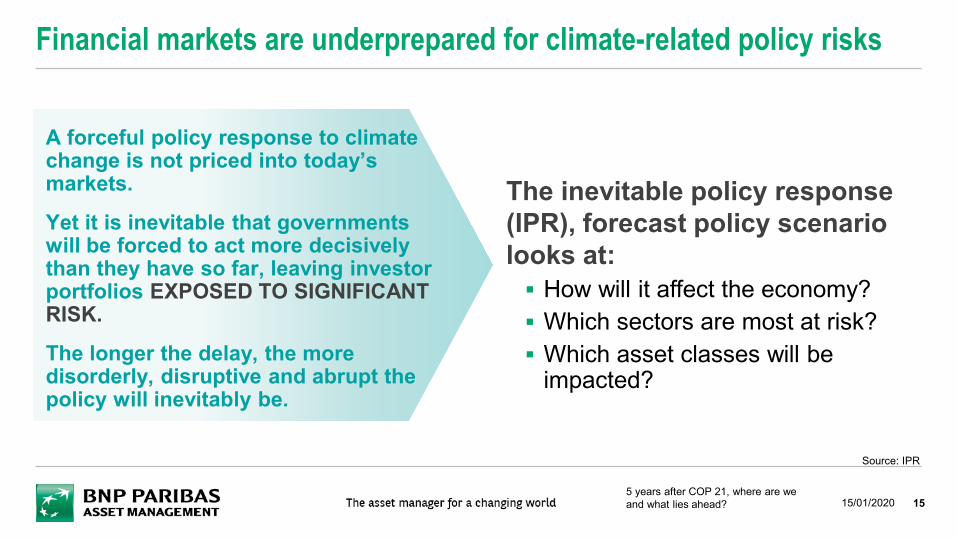

The inevitable policy response (IPR), forecast policy scenario looks at: How will it affect the economy? Which sectors are most at risk? Which asset classes will be

impacted?

Financial markets are underprepared for climate-related policy risks

15

A forceful policy response to climate change is not priced into today’s markets.

Yet it is inevitable that governments will be forced to act more decisively than they have so far, leaving investor portfolios EXPOSED TO SIGNIFICANT RISK.

The longer the delay, the more disorderly, disruptive and abrupt the policy will inevitably be.

Source: IPR

5 years after COP 21, where are we and what lies ahead? 15/01/2020

16

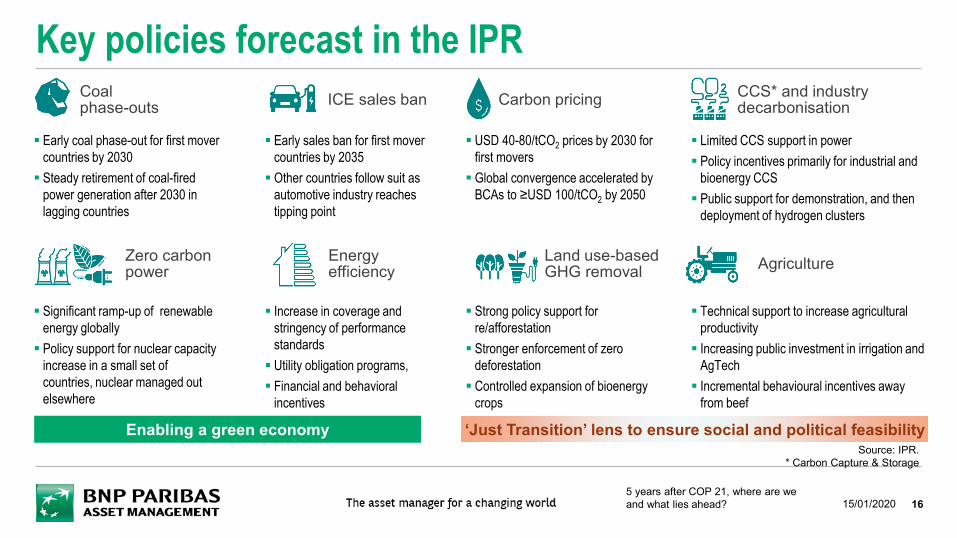

Key policies forecast in the IPR Coalphase-outs ICE sales ban Carbon pricing CCS* and industry

decarbonisation

Zero carbon power

Energy efficiency

Land use-based GHG removal Agriculture

Early sales ban for first mover countries by 2035 Other countries follow suit as

automotive industry reaches tipping point

Early coal phase-out for first mover countries by 2030 Steady retirement of coal-fired

power generation after 2030 in lagging countries

USD 40-80/tCO2 prices by 2030 for first movers Global convergence accelerated by

BCAs to ≥USD 100/tCO2 by 2050

Limited CCS support in power Policy incentives primarily for industrial and

bioenergy CCS Public support for demonstration, and then

deployment of hydrogen clusters

Increase in coverage and stringency of performance standards Utility obligation programs, Financial and behavioral

incentives

Significant ramp-up of renewable energy globally Policy support for nuclear capacity

increase in a small set of countries, nuclear managed out elsewhere

Technical support to increase agricultural productivity Increasing public investment in irrigation and

AgTech Incremental behavioural incentives away

from beef

Strong policy support for re/afforestation Stronger enforcement of zero

deforestation Controlled expansion of bioenergy

crops

Enabling a green economy ‘Just Transition’ lens to ensure social and political feasibilitySource: IPR.

* Carbon Capture & Storage

5 years after COP 21, where are we and what lies ahead? 15/01/2020

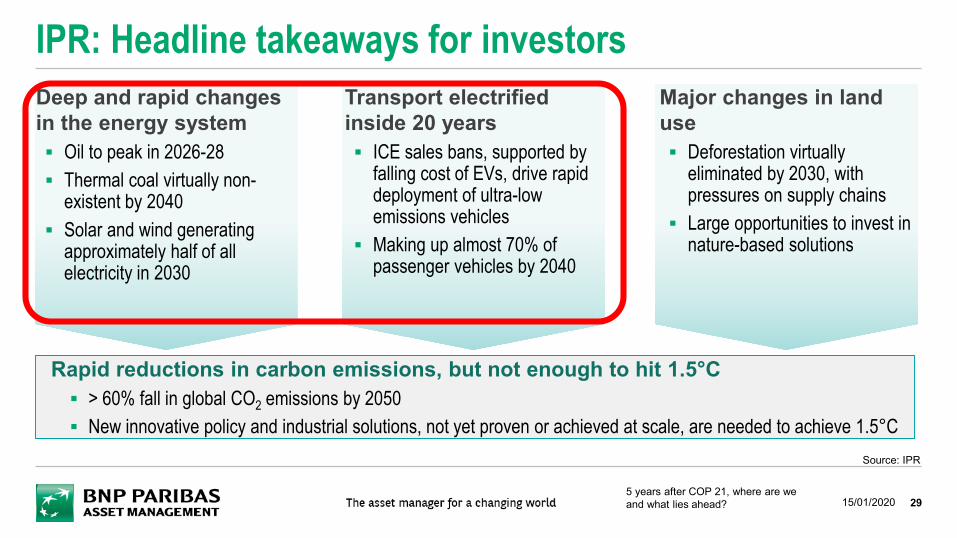

17

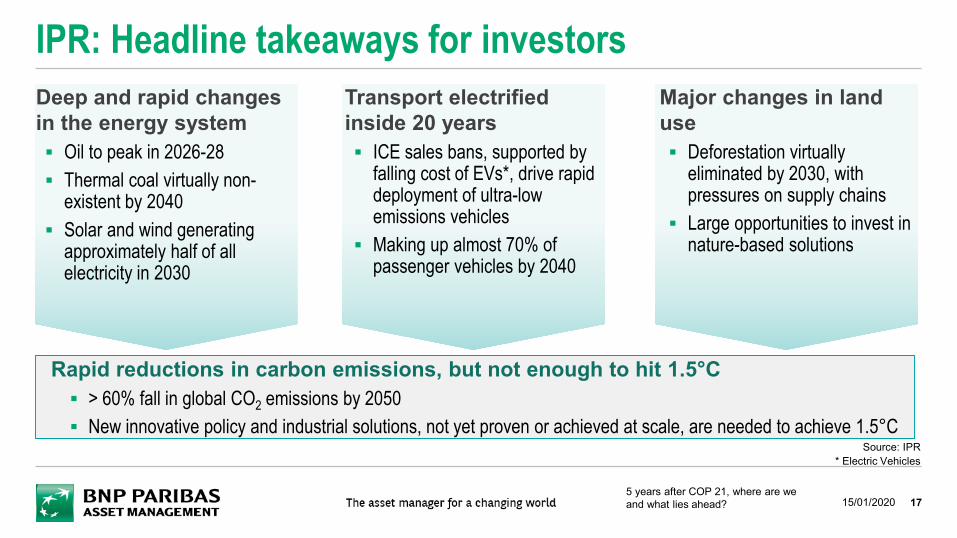

IPR: Headline takeaways for investorsDeep and rapid changesin the energy system Oil to peak in 2026-28 Thermal coal virtually non-

existent by 2040 Solar and wind generating

approximately half of all electricity in 2030

Transport electrified inside 20 years ICE sales bans, supported by

falling cost of EVs*, drive rapid deployment of ultra-low emissions vehicles

Making up almost 70% of passenger vehicles by 2040

Major changes in land use Deforestation virtually

eliminated by 2030, with pressures on supply chains

Large opportunities to invest in nature-based solutions

Rapid reductions in carbon emissions, but not enough to hit 1.5°C > 60% fall in global CO2 emissions by 2050 New innovative policy and industrial solutions, not yet proven or achieved at scale, are needed to achieve 1.5°C

Source: IPR* Electric Vehicles

5 years after COP 21, where are we and what lies ahead? 15/01/2020

18

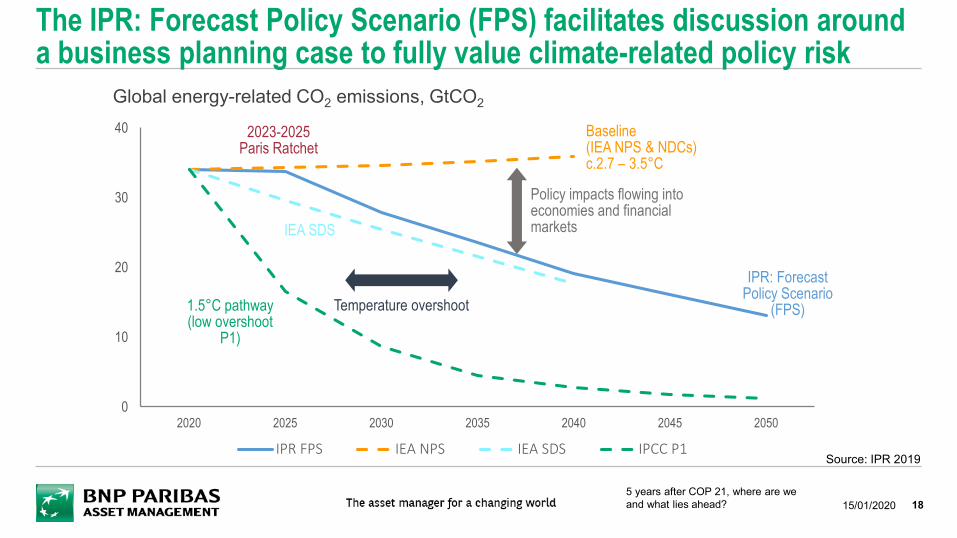

The IPR: Forecast Policy Scenario (FPS) facilitates discussion around a business planning case to fully value climate-related policy risk

0

10

20

30

40

2020 2025 2030 2035 2040 2045 2050

IPR FPS IEA NPS IEA SDS IPCC P1

2023-2025Paris Ratchet

Baseline(IEA NPS & NDCs)c.2.7 – 3.5°C

Policy impacts flowing into economies and financial markets

IPR: Forecast Policy Scenario

(FPS)Temperature overshoot1.5°C pathway (low overshoot

P1)

IEA SDS

Global energy-related CO2 emissions, GtCO2

Source: IPR 2019

5 years after COP 21, where are we and what lies ahead? 15/01/2020

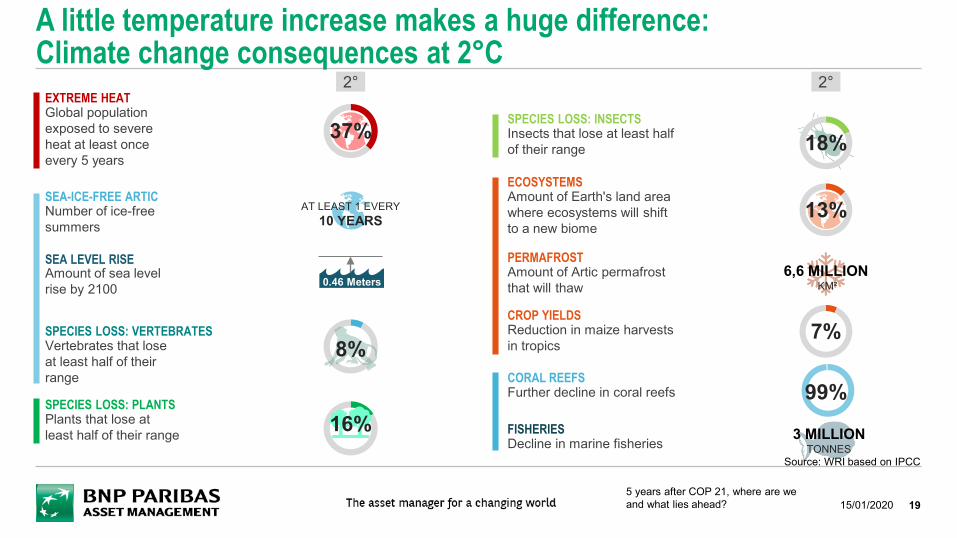

A little temperature increase makes a huge difference:Climate change consequences at 2°C

EXTREME HEATGlobal population exposed to severe heat at least once every 5 years

SEA-ICE-FREE ARTICNumber of ice-free summers

SEA LEVEL RISEAmount of sea level rise by 2100

SPECIES LOSS: VERTEBRATESVertebrates that lose at least half of their range

SPECIES LOSS: PLANTSPlants that lose at least half of their range

SPECIES LOSS: INSECTSInsects that lose at least half of their range

ECOSYSTEMSAmount of Earth's land area where ecosystems will shift to a new biome

PERMAFROSTAmount of Artic permafrost that will thaw

CROP YIELDSReduction in maize harvests in tropics

CORAL REEFSFurther decline in coral reefs

FISHERIESDecline in marine fisheries

2°

0.46 Meters

37%

AT LEAST 1 EVERY10 YEARS

8%

16%

18%

13%

99%

3 MILLIONTONNES

6,6 MILLIONKM²

7%

2°

Source: WRI based on IPCC

195 years after COP 21, where are we and what lies ahead? 15/01/2020

20

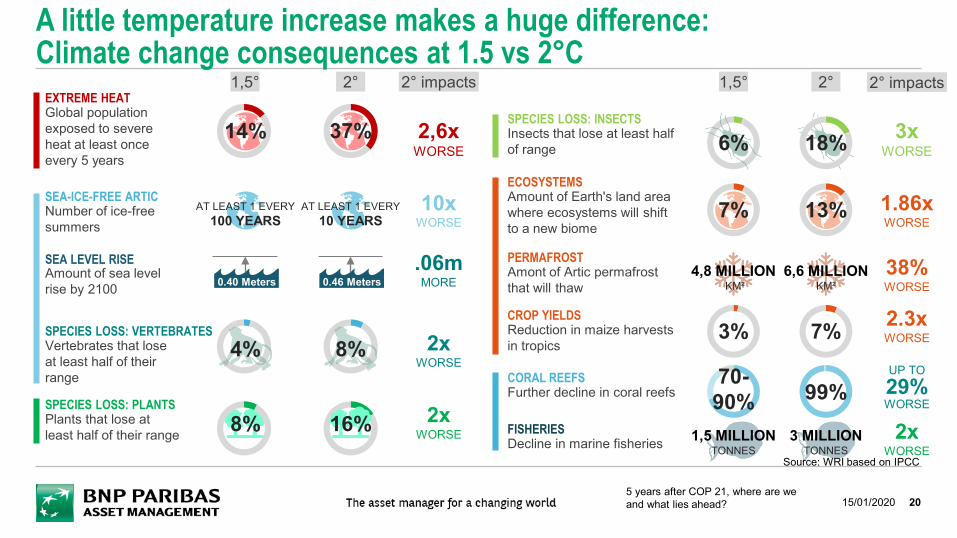

A little temperature increase makes a huge difference:Climate change consequences at 1.5 vs 2°C

EXTREME HEATGlobal population exposed to severe heat at least once every 5 years

SEA-ICE-FREE ARTICNumber of ice-free summers

SEA LEVEL RISEAmount of sea level rise by 2100

SPECIES LOSS: VERTEBRATESVertebrates that lose at least half of their range

SPECIES LOSS: PLANTSPlants that lose at least half of their range

SPECIES LOSS: INSECTSInsects that lose at least half of range

ECOSYSTEMSAmount of Earth's land area where ecosystems will shift to a new biome

PERMAFROSTAmont of Artic permafrost that will thaw

CROP YIELDSReduction in maize harvests in tropics

CORAL REEFSFurther decline in coral reefs

FISHERIESDecline in marine fisheries

0.40 Meters

14%

AT LEAST 1 EVERY100 YEARS

4%

8%

6%

7%

70-90%

1,5 MILLIONTONNES

4,8 MILLIONKM²

1,5° 2°

0.46 Meters

37%

AT LEAST 1 EVERY10 YEARS

8%

16%

18%

13%

99%

3 MILLIONTONNES

6,6 MILLIONKM²

3% 7%

2,6xWORSE

10xWORSE

.06mMORE

2xWORSE

2xWORSE

2° impacts 1,5° 2°

3xWORSE

1.86xWORSE

UP TO29%WORSE

2xWORSE

2° impacts

38%WORSE

2.3xWORSE

Source: WRI based on IPCC

5 years after COP 21, where are we and what lies ahead? 15/01/2020

21

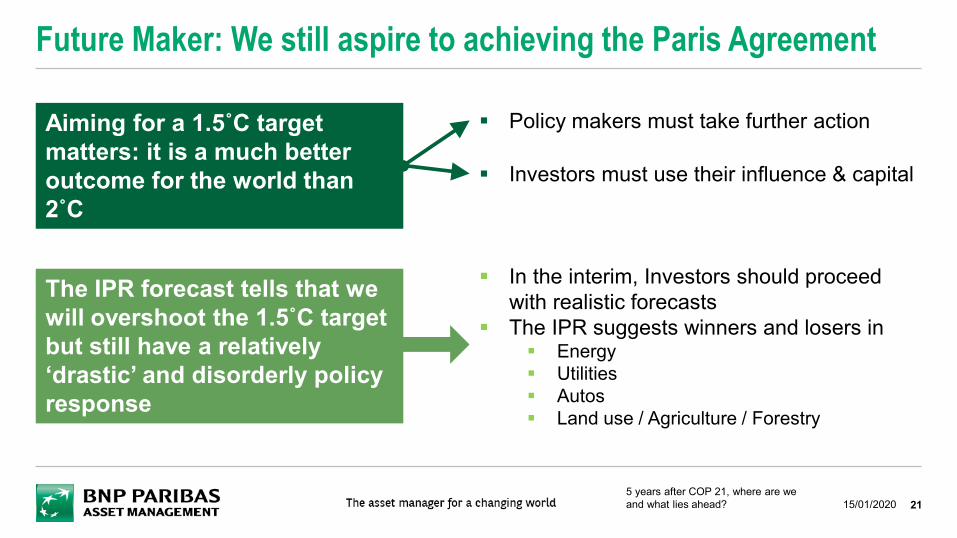

Future Maker: We still aspire to achieving the Paris Agreement

The IPR forecast tells that we will overshoot the 1.5˚C target but still have a relatively ‘drastic’ and disorderly policy response

Aiming for a 1.5˚C target matters: it is a much better outcome for the world than 2˚C

Policy makers must take further action

Investors must use their influence & capital

In the interim, Investors should proceed with realistic forecasts

The IPR suggests winners and losers in Energy Utilities Autos Land use / Agriculture / Forestry

5 years after COP 21, where are we and what lies ahead? 15/01/2020

FROM TOP DOWN TO BOTTOM UP: INTRODUCING EROCI

4.

225 years after COP 21, where are we and what lies ahead? 15/01/2020

23

A number of factors make a near-term, forceful policy response more likely

The catastrophic effects of climate change are already visible… We need collective leadership and action across countries.

Changing weather trends

New climate research

Impacts on security Cheaper renewable energy

Stakeholders demanding clarity Civil society action

The effects of a changing climate are a national security issue.

- US Dept. of Defense

5 years after COP 21, where are we and what lies ahead? 15/01/2020

Trademark, copyright, and other intellectual property rights are and remain the property of their respective owners. Source: Google

Oil needs a long-term breakeven price of USD 10-USD 20/bbl to remain competitive in mobility. Renewables offer a higher Energy Return on Capital Invested

(EROCI) when used to power cars and light-duty vehicles Wind and solar-energy + battery electric vehicles will produce 6x-7x

more useful energy than oil at USD 60/bbl The economics of renewables are impossible for oil to compete with

over the cycle Short-run marginal cost of zero; clean; easy to transport Could replace up to 40% of global oil demand The oil industry should consider the fate of the European utilities over

the last decade & the risk of stranded assets

EROCI: a new concept for analyzing the economics of energy

245 years after COP 21, where are we and what lies ahead? 15/01/2020

25

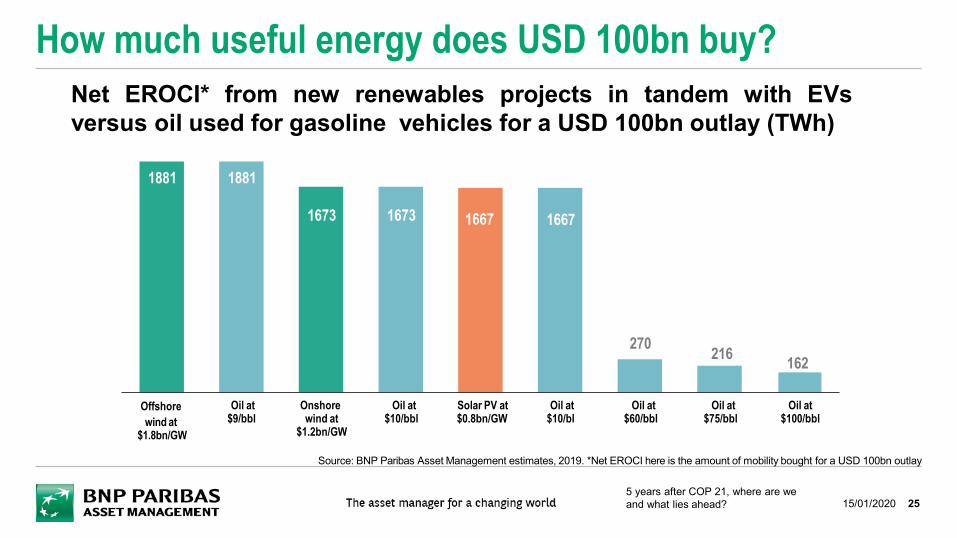

How much useful energy does USD 100bn buy?

1881 1881

1673 1673 1667 1667

270 216 162

Offshorewind at

$1.8bn/GW

Oil at$9/bbl

Onshore wind at

$1.2bn/GW

Oil at$10/bbl

Solar PV at$0.8bn/GW

Oil at$10/bl

Oil at$60/bbl

Oil at$75/bbl

Oil at$100/bbl

Net EROCI* from new renewables projects in tandem with EVsversus oil used for gasoline vehicles for a USD 100bn outlay (TWh)

Source: BNP Paribas Asset Management estimates, 2019. *Net EROCI here is the amount of mobility bought for a USD 100bn outlay

5 years after COP 21, where are we and what lies ahead? 15/01/2020

26

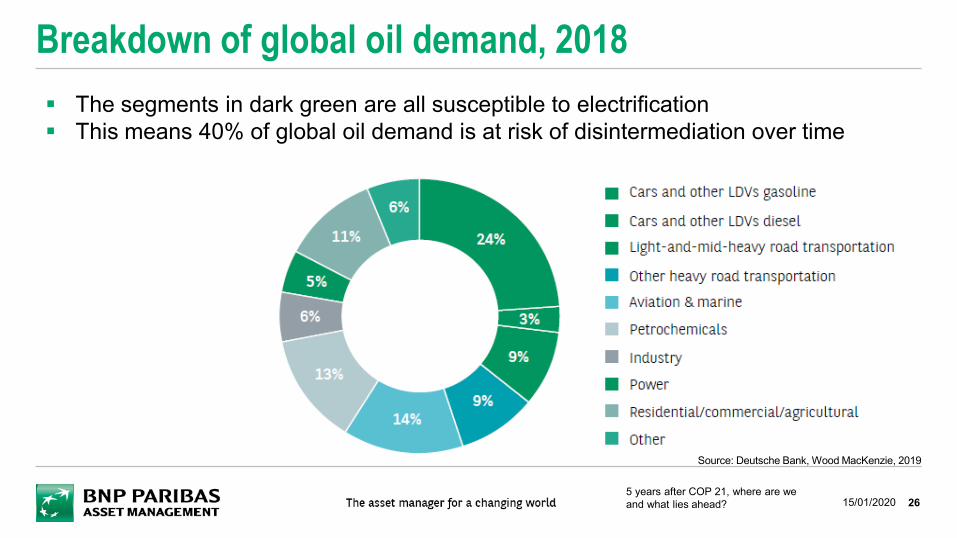

Breakdown of global oil demand, 2018 The segments in dark green are all susceptible to electrification This means 40% of global oil demand is at risk of disintermediation over time

Source: Deutsche Bank, Wood MacKenzie, 2019

5 years after COP 21, where are we and what lies ahead? 15/01/2020

27

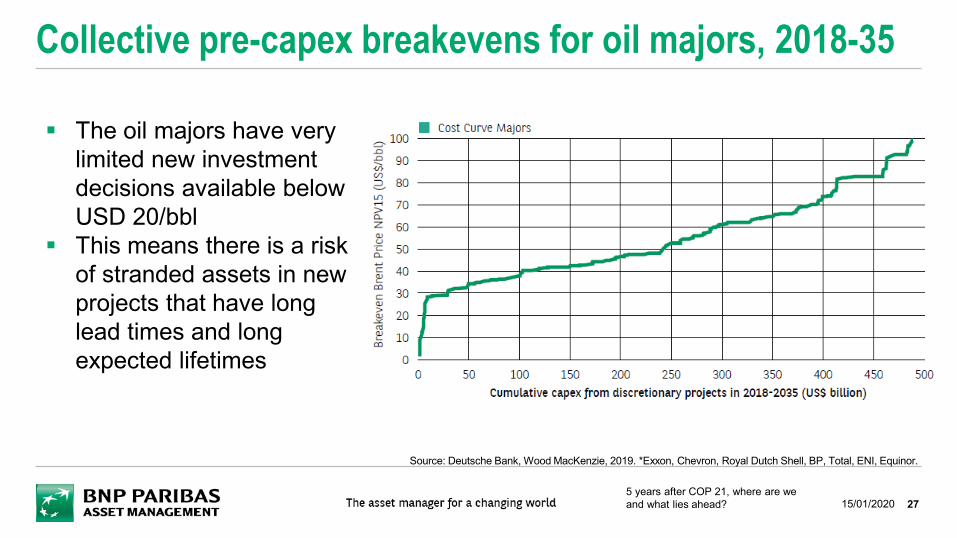

Collective pre-capex breakevens for oil majors, 2018-35

The oil majors have very limited new investment decisions available below USD 20/bbl

This means there is a risk of stranded assets in new projects that have long lead times and long expected lifetimes

Source: Deutsche Bank, Wood MacKenzie, 2019. *Exxon, Chevron, Royal Dutch Shell, BP, Total, ENI, Equinor.

5 years after COP 21, where are we and what lies ahead? 15/01/2020

CONCLUSION5.

285 years after COP 21, where are we and what lies ahead? 15/01/2020

29

IPR: Headline takeaways for investorsDeep and rapid changesin the energy system Oil to peak in 2026-28 Thermal coal virtually non-

existent by 2040 Solar and wind generating

approximately half of all electricity in 2030

Transport electrified inside 20 years ICE sales bans, supported by

falling cost of EVs, drive rapid deployment of ultra-low emissions vehicles

Making up almost 70% of passenger vehicles by 2040

Major changes in land use Deforestation virtually

eliminated by 2030, with pressures on supply chains

Large opportunities to invest in nature-based solutions

Rapid reductions in carbon emissions, but not enough to hit 1.5°C > 60% fall in global CO2 emissions by 2050 New innovative policy and industrial solutions, not yet proven or achieved at scale, are needed to achieve 1.5°C

Source: IPR

5 years after COP 21, where are we and what lies ahead? 15/01/2020

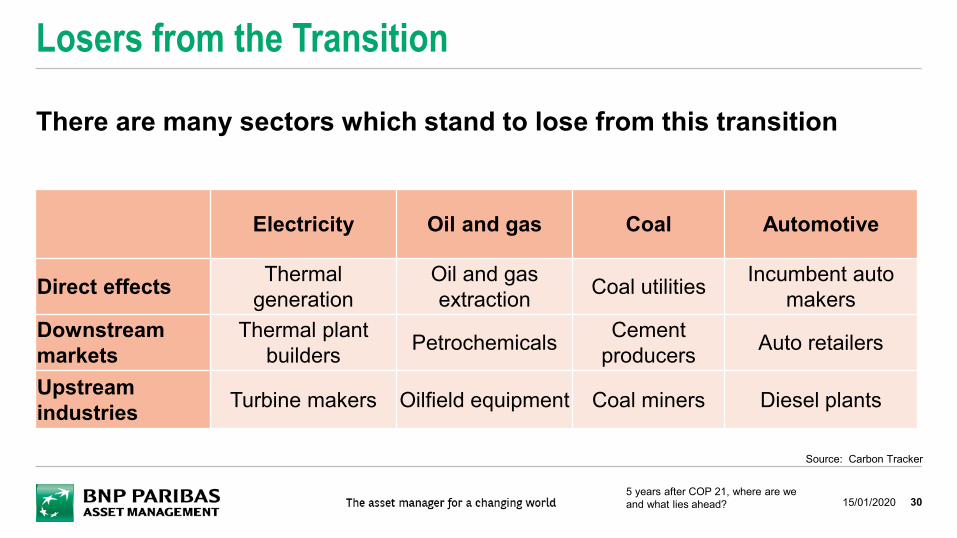

Losers from the Transition

30

There are many sectors which stand to lose from this transition

Electricity Oil and gas Coal Automotive

Direct effects Thermal generation

Oil and gas extraction Coal utilities Incumbent auto

makersDownstream markets

Thermal plant builders Petrochemicals Cement

producers Auto retailers

Upstream industries Turbine makers Oilfield equipment Coal miners Diesel plants

Source: Carbon Tracker

5 years after COP 21, where are we and what lies ahead? 15/01/2020

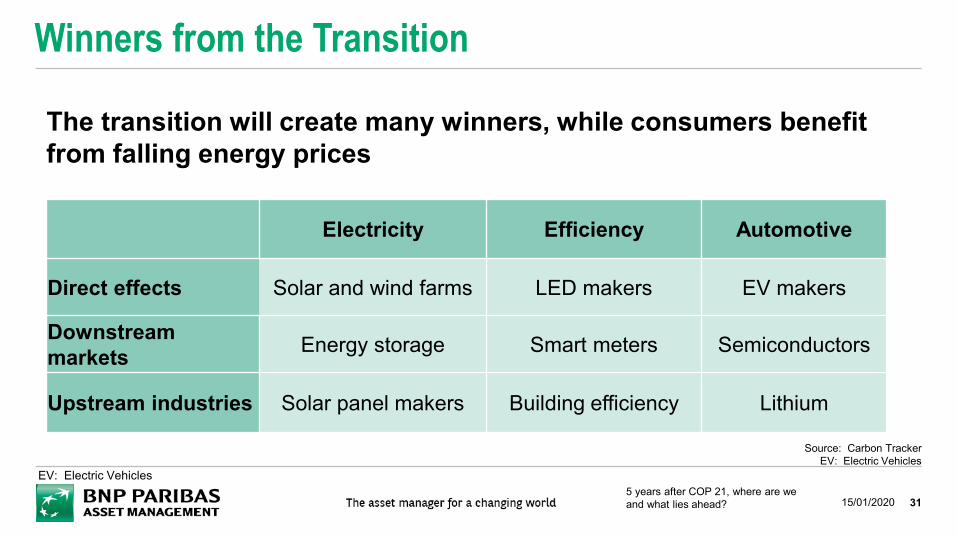

Winners from the Transition

31

The transition will create many winners, while consumers benefit from falling energy prices

Electricity Efficiency Automotive

Direct effects Solar and wind farms LED makers EV makers

Downstream markets Energy storage Smart meters Semiconductors

Upstream industries Solar panel makers Building efficiency Lithium

Source: Carbon TrackerEV: Electric Vehicles

EV: Electric Vehicles5 years after COP 21, where are we and what lies ahead? 15/01/2020

32

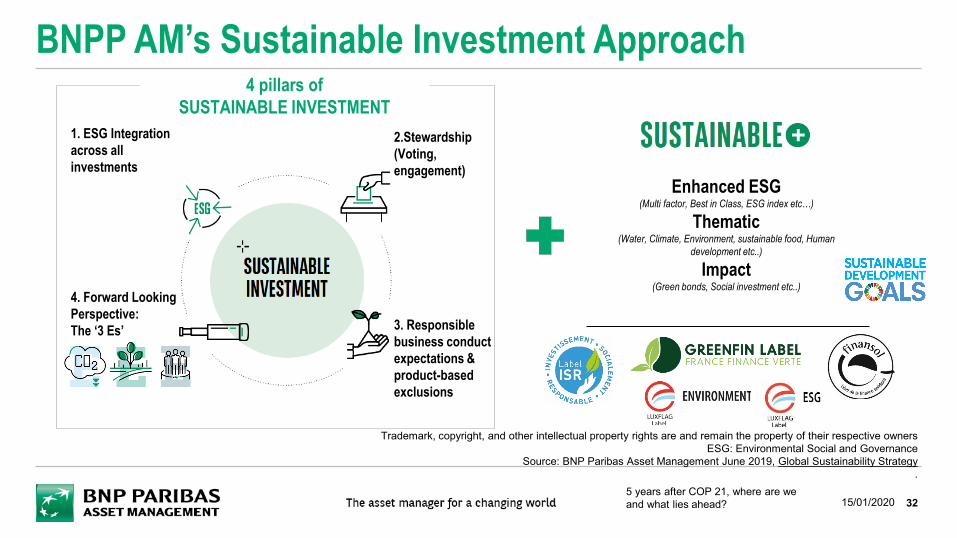

BNPP AM’s Sustainable Investment Approach

1. ESG Integration across all investments

2.Stewardship(Voting, engagement)

4. Forward Looking Perspective: The ‘3 Es’ 3. Responsible

business conduct expectations & product-based exclusions

4 pillars of SUSTAINABLE INVESTMENT

Enhanced ESG(Multi factor, Best in Class, ESG index etc…)

Thematic(Water, Climate, Environment, sustainable food, Human

development etc..)

Impact(Green bonds, Social investment etc..)

Trademark, copyright, and other intellectual property rights are and remain the property of their respective ownersESG: Environmental Social and Governance

Source: BNP Paribas Asset Management June 2019, Global Sustainability Strategy.

5 years after COP 21, where are we and what lies ahead? 15/01/2020

BNP PARIBAS ASSET MANAGEMENT France, “the investment management company,” is a simplified joint stock company with its registered office at 1 boulevard Haussmann 75009 Paris, France, RCS Paris 319 378 832, registered with the “Autorité des marchés financiers” under number GP 96002. This material is issued and has been prepared by the investment management company.This material is produced for information purposes only and does not constitute:1. an offer to buy nor a solicitation to sell, nor shall it form the basis of or be relied upon in connection with any contract or commitment whatsoever or2. investment advice.Opinions included in this material constitute the judgement of the investment management company at the time specified and may be subject to change without notice. The investment management company is not obliged to update or alter the information or opinions contained within this material. Investors should consult their own legal and tax advisors in respect of legal, accounting, domicile and tax advice prior to investing in the financial instrument(s) in order to make an independent determination of the suitability and consequences of an investment therein, if permitted. Please note that different types of investments, if contained within this material, involve varying degrees of risk and there can be no assurance that any specific investment may either be suitable, appropriate or profitable for an investor’s investment portfolio.Given the economic and market risks, there can be no assurance that the financial instrument(s) will achieve its/their investment objectives. Returns may be affected by, amongst other things, investment strategies or objectives of the financial instrument(s) and material market and economic conditions, including interest rates, market terms and general market conditions. The different strategies applied to the financial instruments may have a significant effect on the results portrayed in this material.All information referred to in the present document is available on www.bnpparibas-am.com

Disclaimer

335 years after COP 21, where are we and what lies ahead? 15/01/2020

BNP PARIBAS ASSET MANAGEMENTHerengracht 5951017 CE [email protected]: +31 20 527 5223