Embed Size (px)

Citation preview

04/18/2304/18/23

Property Claim ServicesProperty Claim Services

The PCS Process for Identifying The PCS Process for Identifying Catastrophes and Estimating Catastrophes and Estimating

the Related Lossesthe Related Losses

ByByGary Kerney, AIC, RPAGary Kerney, AIC, RPAAssistant Vice PresidentAssistant Vice President

PCSPCS

04/18/2304/18/23

IntroductionIntroduction

What is a Catastrophe?What is a Catastrophe?

The PCS process for estimating cat lossesThe PCS process for estimating cat losses

What’s ahead?What’s ahead?

Where and What are the challenges?Where and What are the challenges?

04/18/2304/18/23

What Is a Catastrophe?What Is a Catastrophe?

Catastrophe DefinitionCatastrophe Definition An event causing $25 million or more of An event causing $25 million or more of

insured property damage insured property damage ANDAND affecting a significant number of affecting a significant number of

policyholders and insurerspolicyholders and insurers

04/18/2304/18/23

What Is a Catastrophe?What Is a Catastrophe?

Catastrophe Definition Changes Over Catastrophe Definition Changes Over TimeTime

1949 to December 1982 - $1 million1949 to December 1982 - $1 million

1983 to December 1996 - $5 million1983 to December 1996 - $5 million

Since January 1, 1997 - $25 millionSince January 1, 1997 - $25 million

04/18/2304/18/23

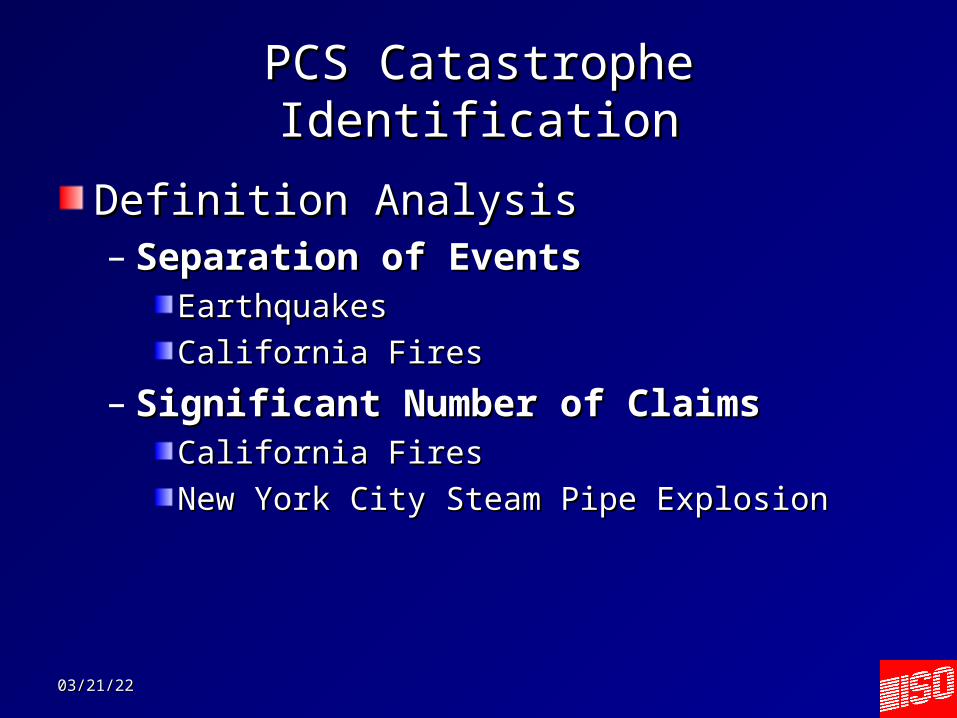

PCS Catastrophe IdentificationPCS Catastrophe Identification

Definition AnalysisDefinition Analysis– Separation of EventsSeparation of Events

EarthquakesEarthquakes

California Fires California Fires

– Significant Number of ClaimsSignificant Number of ClaimsCalifornia FiresCalifornia Fires

New York City Steam Pipe ExplosionNew York City Steam Pipe Explosion

04/18/2304/18/23

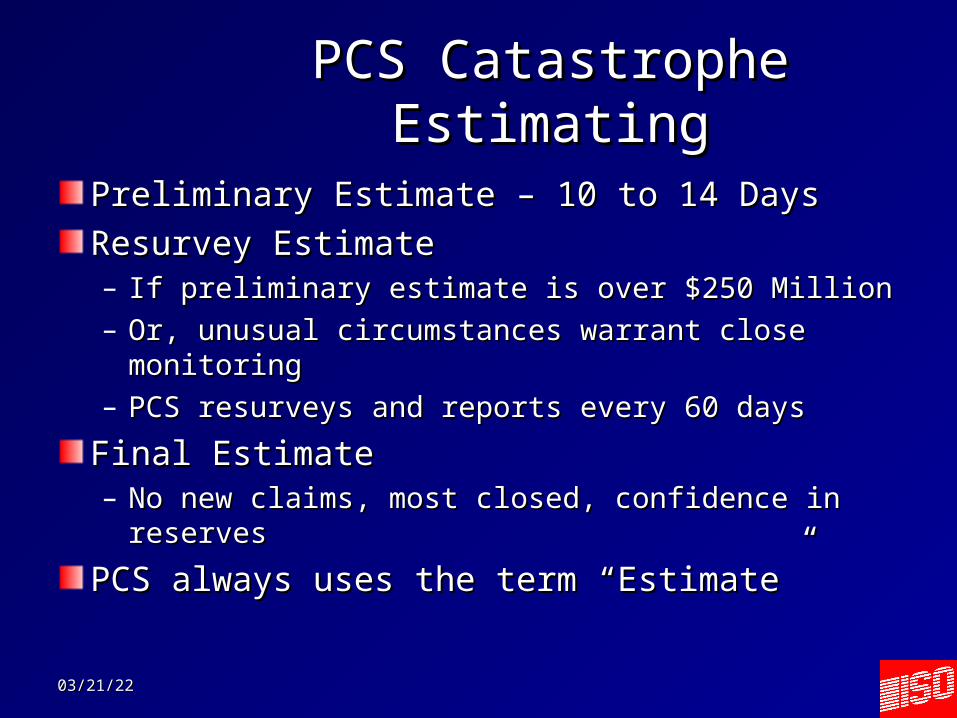

PCS Catastrophe EstimatingPCS Catastrophe Estimating

Preliminary Estimate – 10 to 14 DaysPreliminary Estimate – 10 to 14 Days

Resurvey EstimateResurvey Estimate– If preliminary estimate is over $250 MillionIf preliminary estimate is over $250 Million– Or, unusual circumstances warrant close monitoringOr, unusual circumstances warrant close monitoring– PCS resurveys and reports every 60 daysPCS resurveys and reports every 60 days

Final EstimateFinal Estimate– No new claims, most closed, confidence in reservesNo new claims, most closed, confidence in reserves

PCS always uses the term “Estimate”PCS always uses the term “Estimate”

04/18/2304/18/23

PCS Sources for Loss InformationPCS Sources for Loss Information

Insurer Loss ReportsInsurer Loss Reports

Market Share AnalysisMarket Share Analysis

On-Site Surveys or FlyoversOn-Site Surveys or Flyovers

National Insurance Risk Profile DataNational Insurance Risk Profile Data

ConfidentialityConfidentiality

Estimate CompilationsEstimate Compilations

04/18/2304/18/23

Insured Property Damage by PCS Storm FamilyInsured Property Damage by PCS Storm Family1950 to 20081950 to 2008

Storm FamilyStorm Family Estimated Insured LossEstimated Insured Loss

Hurricane (88)Hurricane (88) $135,556,445,790$135,556,445,790

Wind and Thunderstorm Event (1198)Wind and Thunderstorm Event (1198) $96,725,197,458$96,725,197,458

Winter StormWinter Storm $23,678,656,159$23,678,656,159

Fire - OtherFire - Other $20,050,753,604$20,050,753,604

EarthquakeEarthquake $13,964,150,000$13,964,150,000

Wildland FireWildland Fire $6,467,348,000$6,467,348,000

Tropical StormTropical Storm $3,974,320,000$3,974,320,000

RiotRiot $970,250,000$970,250,000

Water DamageWater Damage $300,000,000$300,000,000

Utility Service DisruptionUtility Service Disruption $180,000,000$180,000,000

Volcanic EruptionVolcanic Eruption $27,000,000$27,000,000

Total Insured Loss (1536)Total Insured Loss (1536) $301,104,121,011$301,104,121,011

04/18/2304/18/23

The PCS Top 10The PCS Top 10All Hurricanes except WTC and NorthridgeAll Hurricanes except WTC and Northridge

YEARYEAR CAT #CAT # STORM FAMILYSTORM FAMILY ESTIMATED ESTIMATED LOSS LOSS

20052005 4949 Hurricane KatrinaHurricane Katrina $41,100,000,000$41,100,000,000

20012001 4848 Fire - OtherFire - Other $18,778,500,000$18,778,500,000

19921992 2727 Hurricane AndrewHurricane Andrew $15,500,000,000$15,500,000,000

19941994 7878 EarthquakeEarthquake $12,500,000,000$12,500,000,000

20082008 6060 Hurricane IkeHurricane Ike $11,500,000,000$11,500,000,000

20052005 5454 Hurricane WilmaHurricane Wilma $10,300,000,000$10,300,000,000

20042004 2626 Hurricane CharleyHurricane Charley $7,475,000,000$7,475,000,000

20042004 3030 Hurricane IvanHurricane Ivan $7,110,000,000$7,110,000,000

20052005 5151 Hurricane RitaHurricane Rita $5,627,200,000$5,627,200,000

20042004 2828 Hurricane FrancesHurricane Frances $4,595,000,000$4,595,000,000

PCS Resurvey EstimatesPCS Resurvey Estimates

04/18/2304/18/23

Survey # 2 3 4 5 6 7 8 9 10 11 Final Est ($bn)1 Katrina (49-05) 10.9% 0.0% 6.5% 0.0% 0.0% 0.2% 0.0% 0.0% 1.0% 0.0% 41.12 Northridge (78-94) 80.0% 22.2% 30.9% 25.0% 15.6% 7.7% 4.5% 6.8% 0.0% 12.53 Wilma (54-05) 38.0% 11.1% 10.2% 0.0% 0.0% 0.0% 0.0% 10.34 Rita (51-05) 6.0% 0.0% 1.4% 5.4% 5.8% 0.0% 0.0% 5.65 Charley (26-04) 0.0% 9.9% 0.0% 0.0% 0.0% 7.56 Frances (28-04) 0.0% 3.7% 0.0% 0.0% 0.0% 4.67 W&T (61-02) 22.1% 50.3% 19.8% 8.8% 0.0% 1.78 WTC (48-01) 0.0% 22.6% 0.0% -7.7% 18.89 Ivan (30-04) 18.3% 0.0% 0.0% 0.0% 7.1

10 Jeanne (29-04) 6.0% 6.3% 0.0% 0.0% 3.711 W&T (38-01) 193.1% 11.8% 0.0% 15.8% 2.212 W&T (88-03) 101.9% 2.4% 0.0% 3.213 Georges (69-98) 15.9% 0.0% 0.0% 314 TS Allison (44-01) 104.9% 0.0% 0.0% 2.515 Floyd (97-99) 35.8% 8.9% 0.0% 216 Isabel (95-03) 44.0% 0.0% 0.0% 1.717 Andrew (27-92) 37.2% 44.9% 15.518 Gustav (58-08) 13.2% 0.0% 2.219 Ike (60-08)* 31.5% 7.9% 11.520 Opal (54-95) 0.0% 2.121 Oakland Hills (87-91) 41.7% 1.722 WS (46-93) 7.7% 1.823 Hugo (18-89) 5.3% 4.2

Avg 35.4% 10.6% 4.3% 4.3% 3.1% 2.0% 1.1% 3.4% 0.5% 0.0% 166.5

04/18/2304/18/23

Catastrophe Loss EstimatingCatastrophe Loss Estimating

PCS figures are not adjusted for inflation –PCS figures are not adjusted for inflation –– Stated in the dollar value of the year of Stated in the dollar value of the year of

occurrence, or in “nominal” dollarsoccurrence, or in “nominal” dollars

Also not adjusted for demographic or other Also not adjusted for demographic or other changes over timechanges over time– Value of comparing Elena (1985) to Katrina Value of comparing Elena (1985) to Katrina

(2005)?(2005)?

04/18/2304/18/23

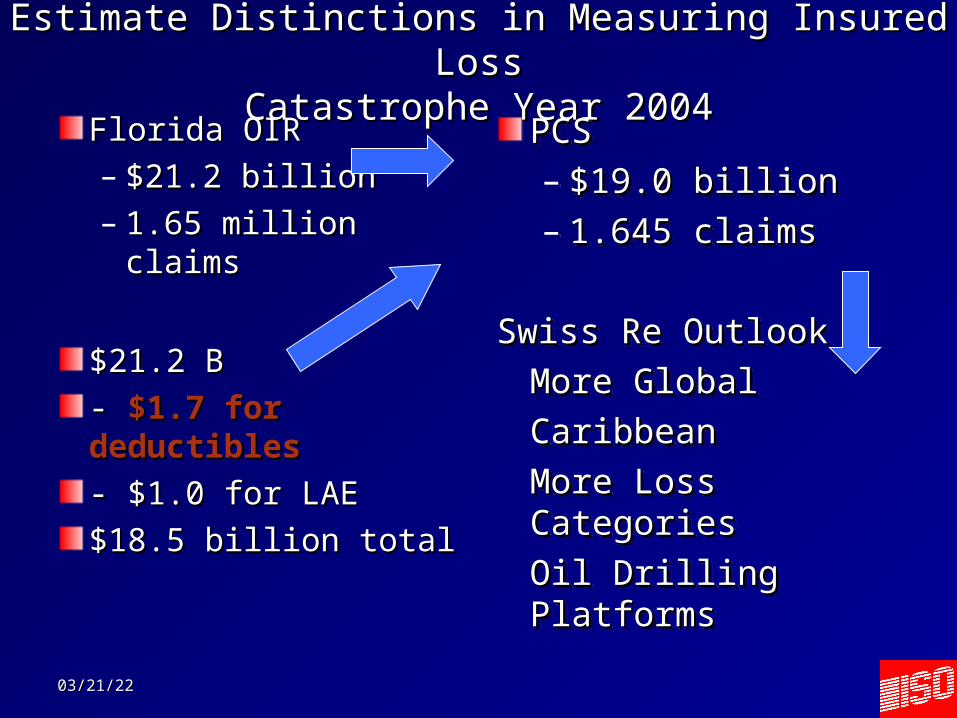

Estimate Distinctions in Measuring Insured LossEstimate Distinctions in Measuring Insured LossCatastrophe Year 2004Catastrophe Year 2004

PCSPCS– $19.0 billion$19.0 billion– 1.645 claims 1.645 claims

Swiss Re OutlookSwiss Re Outlook

More GlobalMore Global

CaribbeanCaribbean

More Loss CategoriesMore Loss Categories

Oil Drilling Oil Drilling PlatformsPlatforms

PCSPCS– $19.0 billion$19.0 billion– 1.645 claims 1.645 claims

Swiss Re OutlookSwiss Re Outlook

More GlobalMore Global

CaribbeanCaribbean

More Loss CategoriesMore Loss Categories

Oil Drilling Oil Drilling PlatformsPlatforms

Florida OIRFlorida OIR– $21.2 billion$21.2 billion– 1.65 million claims1.65 million claims

$21.2 B$21.2 B

- - $1.7 for $1.7 for deductiblesdeductibles

- $1.0 for LAE- $1.0 for LAE

$18.5 billion total$18.5 billion total

04/18/2304/18/23

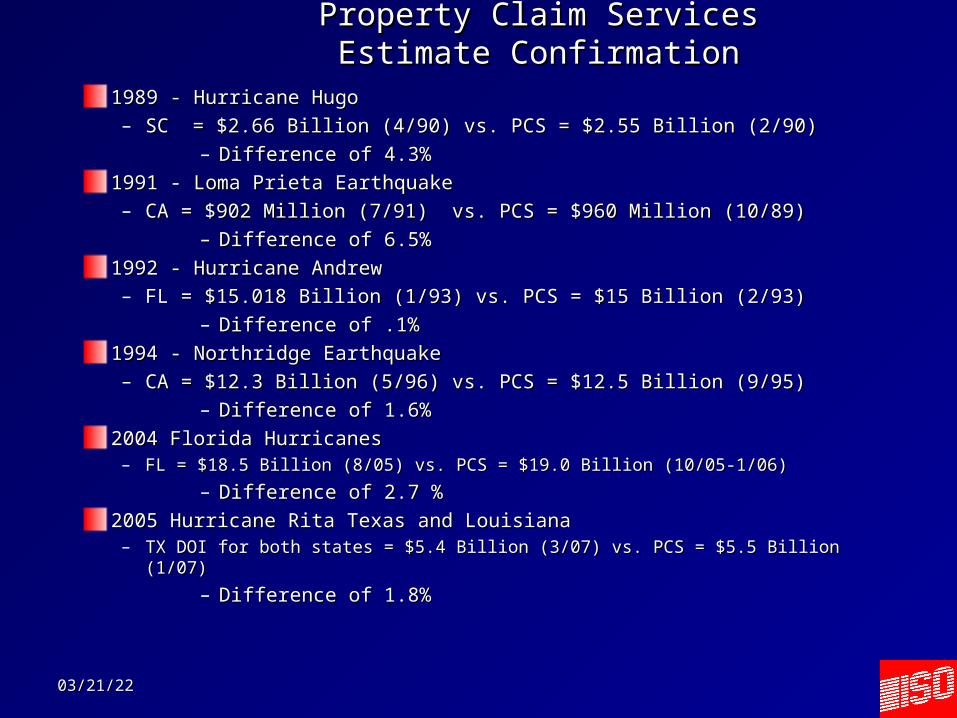

Property Claim ServicesProperty Claim ServicesEstimate ConfirmationEstimate Confirmation

1989 - Hurricane Hugo1989 - Hurricane Hugo– SC = $2.66 Billion (4/90) vs. PCS = $2.55 Billion (2/90)SC = $2.66 Billion (4/90) vs. PCS = $2.55 Billion (2/90)

– Difference of 4.3%Difference of 4.3%

1991 - Loma Prieta Earthquake1991 - Loma Prieta Earthquake– CA = $902 Million (7/91) vs. PCS = $960 Million (10/89)CA = $902 Million (7/91) vs. PCS = $960 Million (10/89)

– Difference of 6.5%Difference of 6.5%

1992 - Hurricane Andrew1992 - Hurricane Andrew– FL = $15.018 Billion (1/93) vs. PCS = $15 Billion (2/93)FL = $15.018 Billion (1/93) vs. PCS = $15 Billion (2/93)

– Difference of .1%Difference of .1%

1994 - Northridge Earthquake1994 - Northridge Earthquake– CA = $12.3 Billion (5/96) vs. PCS = $12.5 Billion (9/95)CA = $12.3 Billion (5/96) vs. PCS = $12.5 Billion (9/95)

– Difference of 1.6%Difference of 1.6%

2004 Florida Hurricanes2004 Florida Hurricanes– FL = $18.5 Billion (8/05) vs. PCS = $19.0 Billion (10/05-1/06)FL = $18.5 Billion (8/05) vs. PCS = $19.0 Billion (10/05-1/06)

– Difference of 2.7 %Difference of 2.7 %

2005 Hurricane Rita Texas and Louisiana2005 Hurricane Rita Texas and Louisiana– TX DOI for both states = $5.4 Billion (3/07) vs. PCS = $5.5 Billion (1/07)TX DOI for both states = $5.4 Billion (3/07) vs. PCS = $5.5 Billion (1/07)

– Difference of 1.8%Difference of 1.8%

04/18/2304/18/23

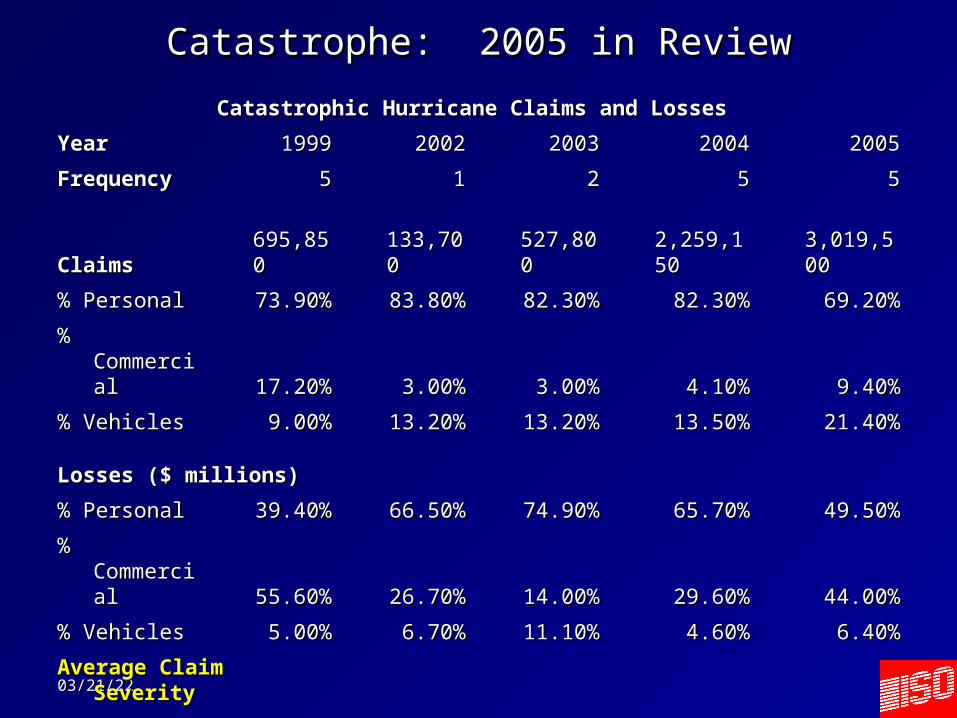

Catastrophe: 2005 in ReviewCatastrophe: 2005 in Review

Catastrophic Hurricane Claims and LossesCatastrophic Hurricane Claims and Losses

YearYear 19991999 20022002 20032003 20042004 20052005

FrequencyFrequency 55 11 22 55 55

ClaimsClaims 695,850695,850 133,700133,700 527,800527,800 2,259,1502,259,150 3,019,5003,019,500

% Personal% Personal 73.90%73.90% 83.80%83.80% 82.30%82.30% 82.30%82.30% 69.20%69.20%

% Commercial% Commercial 17.20%17.20% 3.00%3.00% 3.00%3.00% 4.10%4.10% 9.40%9.40%

% Vehicles% Vehicles 9.00%9.00% 13.20%13.20% 13.20%13.20% 13.50%13.50% 21.40%21.40%

Losses ($ millions)Losses ($ millions)

% Personal% Personal 39.40%39.40% 66.50%66.50% 74.90%74.90% 65.70%65.70% 49.50%49.50%

% Commercial% Commercial 55.60%55.60% 26.70%26.70% 14.00%14.00% 29.60%29.60% 44.00%44.00%

% Vehicles% Vehicles 5.00%5.00% 6.70%6.70% 11.10%11.10% 4.60%4.60% 6.40%6.40%

Average Claim SeverityAverage Claim Severity

PersonalPersonal $1,773 $1,773 $2,554 $2,554 $3,061 $3,061 $9,049 $9,049 $11,860 $11,860

CommercialCommercial $10,769 $10,769 $28,750 $28,750 $11,376 $11,376 $22,337 $22,337 $77,592 $77,592

VehiclesVehicles $1,856 $1,856 $1,638 $1,638 $2,755 $2,755 $3,626 $3,626 $4,988 $4,988

04/18/2304/18/23

Catastrophe Loss and ClaimsCatastrophe Loss and Claims

All Catastrophes 2004All Catastrophes 2004 $27.5 B$27.5 B 3.4 million3.4 millionHurricane Claims 2004Hurricane Claims 2004 $22.9 B$22.9 B 2.3 million 2.3 million

All Catastrophes 2005All Catastrophes 2005 $61.5 B$61.5 B 4.4 million4.4 millionHurricane Claims 2005Hurricane Claims 2005 $57.5 B$57.5 B 3.4 million 3.4 million

All Catastrophes 2006All Catastrophes 2006 $ 9.0 B$ 9.0 B 2.3 million2.3 millionHurricane Claims 2006Hurricane Claims 2006 0 0 0 0

All Catastrophes 2007All Catastrophes 2007 $ 6.7 B$ 6.7 B 1.2 million 1.2 millionHurricane ClaimsHurricane Claims 0 0 0 0

All Catastrophes 2008All Catastrophes 2008 $26.0 B$26.0 B 4.0 million4.0 millionHurricane Claims 2008Hurricane Claims 2008 $14.1 B$14.1 B 1.7 million1.7 million

04/18/2304/18/23

What’s AheadWhat’s AheadIn a recent report for the Organisation for Economic Co-In a recent report for the Organisation for Economic Co-operation and Development, researchers noted:operation and Development, researchers noted:– The first estimate of exposure to coastal flooding and high winds The first estimate of exposure to coastal flooding and high winds

finds 60% of worldwide exposure in 10 cities (ranked in order):finds 60% of worldwide exposure in 10 cities (ranked in order):MiamiMiami

Greater New YorkGreater New York

New OrleansNew Orleans

Osaka-KobeOsaka-Kobe

TokyoTokyo

AmsterdamAmsterdam

RotterdamRotterdam

NagoyaNagoya

Tampa-St. PeteTampa-St. Pete

Virginia BeachVirginia Beach

04/18/2304/18/23

What’s AheadWhat’s Ahead

How bad might it become?How bad might it become?– Remodel the 1938 hurricaneRemodel the 1938 hurricane– Infrastructure damageInfrastructure damage– Weather concernsWeather concerns– Time to repairTime to repair– Demand from other catastrophesDemand from other catastrophes

Expanded Catastrophe InformationExpanded Catastrophe Information

Loss TypeLoss Type– Workers CompWorkers Comp– Offshore and Related PropertyOffshore and Related Property– Madoff – D&O, E&O, Upscale HO TheftMadoff – D&O, E&O, Upscale HO Theft

Loss TerritoryLoss Territory– Europe (PERILS)Europe (PERILS)– JapanJapan– CaribbeanCaribbean– CanadaCanada– AustraliaAustralia

04/18/2304/18/23

04/18/2304/18/23

The Expanding Impact of The Expanding Impact of CatastrophesCatastrophes

Demand Surge – Demand Surge – – Basic Principle, Florida Contractors, LA & MS contractors, WilmaBasic Principle, Florida Contractors, LA & MS contractors, Wilma

Adjuster “Burnout”Adjuster “Burnout”– Fight the NeighborFight the Neighbor– Talking to the WallTalking to the Wall

Rebuilding ProcessRebuilding Process– Land useLand use– Building codesBuilding codes– Employee NeedsEmployee Needs– Availability of insuranceAvailability of insurance

04/18/2304/18/23

The Expanding Impact of CatastrophesThe Expanding Impact of Catastrophes

New Lines of Insurance AffectedNew Lines of Insurance Affected– World Trade Center AttackWorld Trade Center Attack

Life, Health, Workers CompLife, Health, Workers Comp

Use of PCS catastrophe serial numberUse of PCS catastrophe serial number

– Hurricane KatrinaHurricane KatrinaLife and Health Benefits InsuranceLife and Health Benefits Insurance

Mortgage InsuranceMortgage Insurance

– PandemicPandemicTXDOI Survey for Business ContinuityTXDOI Survey for Business Continuity

04/18/2304/18/23

Other Repercussions and IssuesOther Repercussions and Issues

There are other, major consequences that follow from mega-catastrophes:

Class action lawsuits spurred in part by a lack of appropriate coverage for perils that end up being uninsured.

Finding sympathetic juries for trials of those accused of perpetrating insurance fraud.

The debt incurred by the National Flood Insurance Program and other public entities, such as wind pools, requires taxpayers to assume a long term debt to support recovery efforts.

The political furor that results from either personal loss experience or from the perception of utter breakdown in response and recovery efforts.

A change in the way insurers manage risk and exposure that often includes increased premiums or higher deductibles or non-renewed policies.