Embed Size (px)

Citation preview

7-1

Chapter Seven

Event Budgeting

7-2

Chapter learning objectives

7.1 Understand the nature and purpose of a budget in an event management context

7.2 Identify the various types of budget that may be used for events

7.3 Identify and explain all aspects of the event budgeting process

7.4 Explain how to use and interpret breakeven analysis

7-3

Chapter learning objectives

7.5 Identify and explain the key considerations associated with developing an income strategy

7.6 Understand the importance of cash flow considerations and how they should be addressed

7.7 Explain key aspects of costing and estimating in the development of an event budget

7.8 Understand the key steps in managing an event budget.

7-4

Units of Competency and Elements

SITXFIN402 Manage finances within a budget1.Allocate budget resources

2.Monitor financial activities against budget

3.Identify and evaluate options for improved budget performance

4.Complete financial and statistical reports

SITXFIN501 Prepare and monitor budgets1.Prepare budget information

2.Prepare budget

3.Finalise budget

4.Monitor and review budget

Introduction

• Personal budgets include an estimate of our incomes and expenses.

• Business budgets are more complex.

• They express the business objectives of the organisation in dollar terms.

• Event budgets are event plans in dollar terms.

• Financial considerations must be planned for in minute detail to ensure positive outcomes.

7-5

The nature and purpose of an event budget

• The ability to predict and monitor event costs is a critical aspect of event management.

– Rapidly escalating costs can signal disaster for event finances and cash flows.

– As well as reducing overall financial performance, cost blow outs can lead to significant cash flow problems.

• Due to the uneven nature of cash inflows and outflows, the potential for cash flow problems is ever present.

7-6

The nature and purpose of an event budget

• The ability to event revenue is also critical

– Sluggishness or poor performance in terms of ticket sales, sponsorship or other revenue raising activities can signal major financial and cash flow problems.

• The event budget is a simple and effective planning and control tool.

• When used effectively, it helps the event manager to predict event finances and cash flows, and then keep them on track.

7-7

The nature and purpose of an event budget

• Event budgets are effective planning and control tool.

• The purpose of an event budget is to:

– predict and monitor event costs and revenues

– provide financial objectives for evaluating performance

– facilitate awareness of cost reduction opportunities

– create awareness of financial position for stakeholders

– create a control system

– facilitate planning for future events.

7-8

Types of budgets

• There may be the need for separate budgets for one event.

• Line-item budget

– Estimation of every cost and revenue item

– Level of detail may be outlined by stakeholders.

• Program budget

– Created for a specific program or element

– Separating this budget from the main budget allows financial aspects of the program to be considered alone.

7-9

The budgeting process

• Environmental factors

– Forecast of revenue sources such as ticket sales

– Consider effects on revenue streams:

• Economic climate

• Trends for event type

• Market research

• Revenue from previous events

• Change from previous events

– Forecast of expenditure needs to undertake the same forecasting.

7-10

The budgeting process

• Levels of uncertainty

– When developing a budget, considerations that relate to uncertainties about future revenue may at times, be disturbing

– It may, for example, be necessary to broaden the revenue base in order to address current levels of uncertainty

– A greater awareness of areas of uncertainty or vulnerability in terms of revenue generation is one of the key benefits of budgeting.

7-11

The budgeting process

• Addressing uncertainty

– When considerable uncertainty exists, alternative budgets representing different scenarios may be developed.

• These different scenarios are simply different views of what may be expected in the future.

• Ticket sales may be very high or somewhat depressed.

• Expenditures may be kept well under control or may, for various reasons, be greater than initially expected.

– Three budgets may be developed representing a most likely scenario, a pessimistic scenario and an optimistic scenario.

7-12

The budgeting process

• Levels of detail

– The level of detail required and categorisation of various revenues and expenditures is an important concern in the construction of event budgets

– The number of different revenue and expenditure categories should be determined primarily by the need to control or influence them

– The needs of stakeholders must be taken into account when determining levels of detail.

7-13

The budgeting process

• Budget objectives

– To change or not to change?

– Budgets are mechanisms to ensure sound decision making

– Stakeholders need to be considered before change is made.

• Ongoing communication with stakeholders

– Continuous communication reduces the likelihood of major problems down the track

– Awareness amongst stakeholders of key financial outcomes represents an important benefit or by-product of the budgeting process.

7-14

The budgeting process

• Budget review

– Regular monitoring of the budget is recommended

– If expenses are above expected levels, measures must be taken to control costs

– The ability to recognise variances and take corrective action at the appropriate time represents one of the key benefits of budgeting.

7-15

The budgeting process

• Future budgets

– Easier to develop realistic budgets with experience

– Financial discipline with budgets increases over time

– Event budgeting process is summarised here:

• Analysis of environmental factors

• Assessment of levels of uncertainty

• Forecasts and categorisation of revenues and expenditures

• Budget drafting and assessment against objectives

• Distribution of budget to stakeholders

• Negotiation and finalisation of budget

• Regular review of budget

• Collection of information for future budgets.

7-16

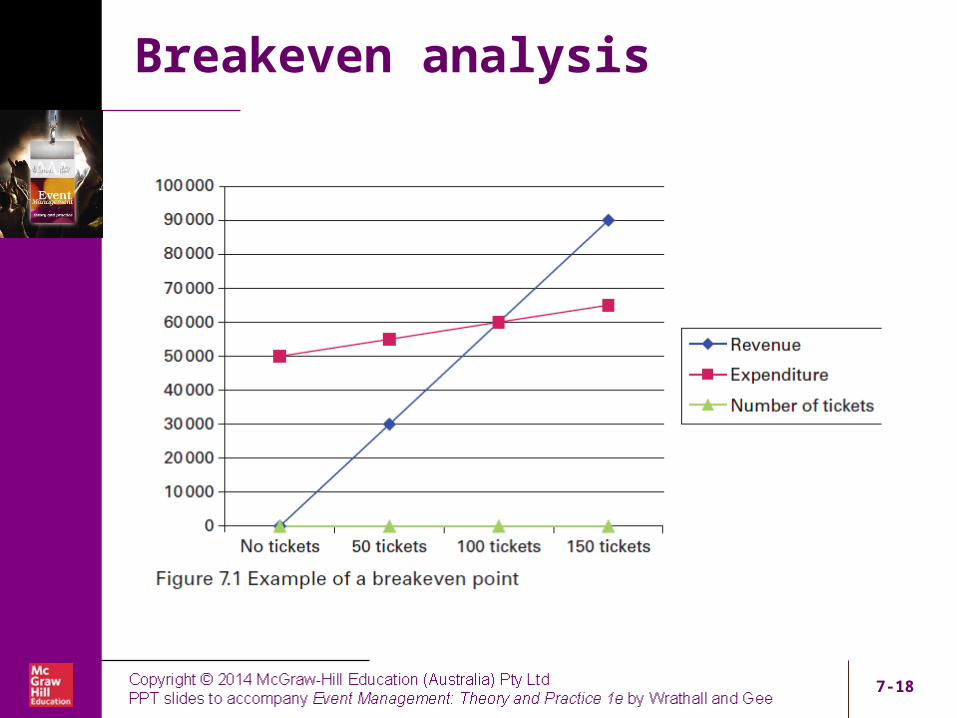

Breakeven analysis

• Budgets can be developed in terms of revenue or breakeven points.

• Breakeven point is where all costs are covered by revenue. Additional revenue = profit.

• Calculating breakeven points require knowledge of:

– Fixed costs

• Same cost no matter how many tickets are sold

• Example: cost of a guest speaker or salaries for event staff

– Variable costs

• Costs that change dependant on how many tickets are sold

• Example: food and beverage.

7-17

Breakeven analysis

7-18

Income strategy

• Income varies dependant on the income strategy.

• Sponsorship

– Level of sponsorship reliant on stakeholder views

– Very important to some event types.

• Grants

– From local, state and federal government bodies.

• Licensing of product sales

– Can generate extensive income

– Events managers need to make agreements with manufacturers or distributors for a share of profits.

7-19

Income strategy

• Ticket sales

– Before event or at the gate

– Higher price = greater revenue per ticket

– Lower price = greater number of tickets sold

– Price people will pay

– Venue capacity

– Other revenue sources

– Logistic issues.

• Other sources of income

– Rental for stalls, sale of programs, parking fees, food and beverage sales.

7-20

Cash flow considerations

• Related to pattern of income and expenditure.

• To avoid cash flow problems:

– develop a cash flow timing chart

– delay expenditure as long as possible

– gain information about supplier terms

– maintain close control over expenditure

– design income strategies to bring forward revenue streams.

7-21

Review of the budget

• Things do not always go to plan!

• Unanticipated expenses, budget blowouts, etc. usually result in an unfavourable change.

• Budgets are the ‘best attempt’ at anticipating financial movements for an event.

• Constant reviews of the budget increase the likelihood of issues being detected.

• Control measures and corrective actions can then be implemented to reduce loss.

7-22

Information for the development of future budgets

• Forecasts may be inaccurate due to lack of information.

• Past experience is useful, but new and unanticipated factors must be considered.

• Three approaches to anticipating costs:

– Top-down

– Bottom-up

– Parametric.

7-23

Managing an event budget

• The effective management of an event budget involves:

– Constantly monitoring the budget to identify variances in expenditure or revenue

– If actual expenditure exceeds budget expenditure, corrective action is required to:

• reduce costs, or

• increase revenue to offset cost increases, or

• A combination of both

– Where expenditure problems have occurred, greater levels of detail may be required in the future to more closely monitor the situation and identify areas of concern.

7-24

Managing an event budget

– If actual revenue falls short of budget revenue, corrective action is required to:

• Increase revenues

• Reduce costs to offset revenue losses

• A combination of both

– Where revenue problems have occurred, alternative sources of revenue may need to be identified.

– Based on past experience, event budgets must be constantly reviewed to ensure they are realistic.

7-25

Chapter summary

• Budgets are one of the most fundamental planning and control tools for event managers.

• Effective budget management allows for planning of finances.

• Cash flow issues can be avoided.

• Allows for revenues and expenditures to be monitored and controlled.

• Budgeting relies upon examination of environmental factors, levels of uncertainty, forecasts and categorisation of revenue and expenditure.

7-26

Chapter summary

• Managing a budget involves constantly monitoring expenditure and revenue, taking corrective action as required, and reviewing budgets to ensure that they remain realistic.

7-27