Embed Size (px)

Citation preview

Annual Review

2016

Den störunt 15 300 medarbetare. Ö

av IT- och konsultkostnade

skrivningar av tillgångar

kostnaderna sprids över fl

tig och effektiv kostnadsb

lja d r kronor

utde g på 5 50 o o peaktie.

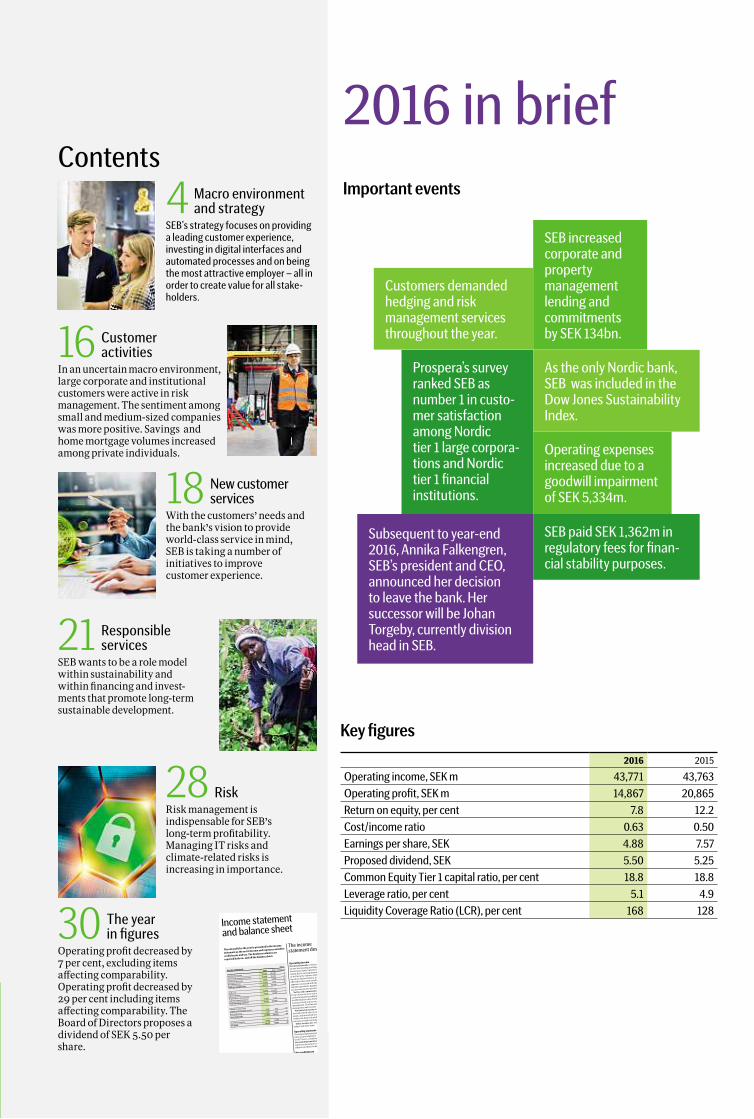

Contents

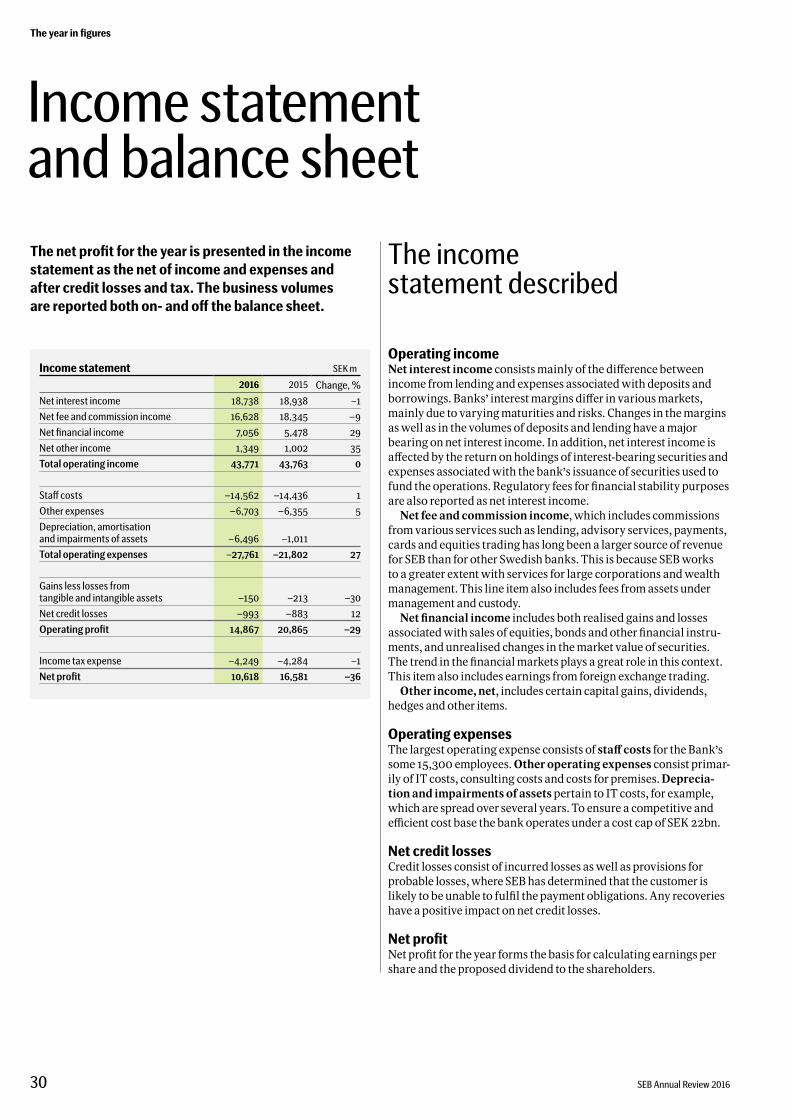

The net profit for theyear is presented in t

he income

statement as the netof income and expen

ses and after

credit losses and tax. The business volum

es are

reported both on- and off the balance she

et.

The incomestatement desc

Operating income

Net interest income consistsmai

income from lending and expens

borrowings. Banks’ interestmarg

mainly due to varyingmaturities

aswell as in the volumes of depo

ing on net interest income. In add

affected by the returnon holding

expenses associatedwith the ba

fund the operations.Regulatory

are also reported as net interest

Net fee and commission inc

from various services suchas, l

cards and equities trading has l

for SEB than for other Swedish

a greater extentwithservices f

management. This lineitem al

management and custody.

Net financial income inclu

associatedwith salesof equiti

ments, and unrealised change

trend in the financialmarkets

item also includes earnings fr

Other income, net, includ

hedges and other items.

Operating expenses

The largest operatingexpen

some 15,300 employees.Ot

ily of IT costs, consulting co

tion and impairments of a

which are spread over sever

efficient cost base thebank

Net credit losses

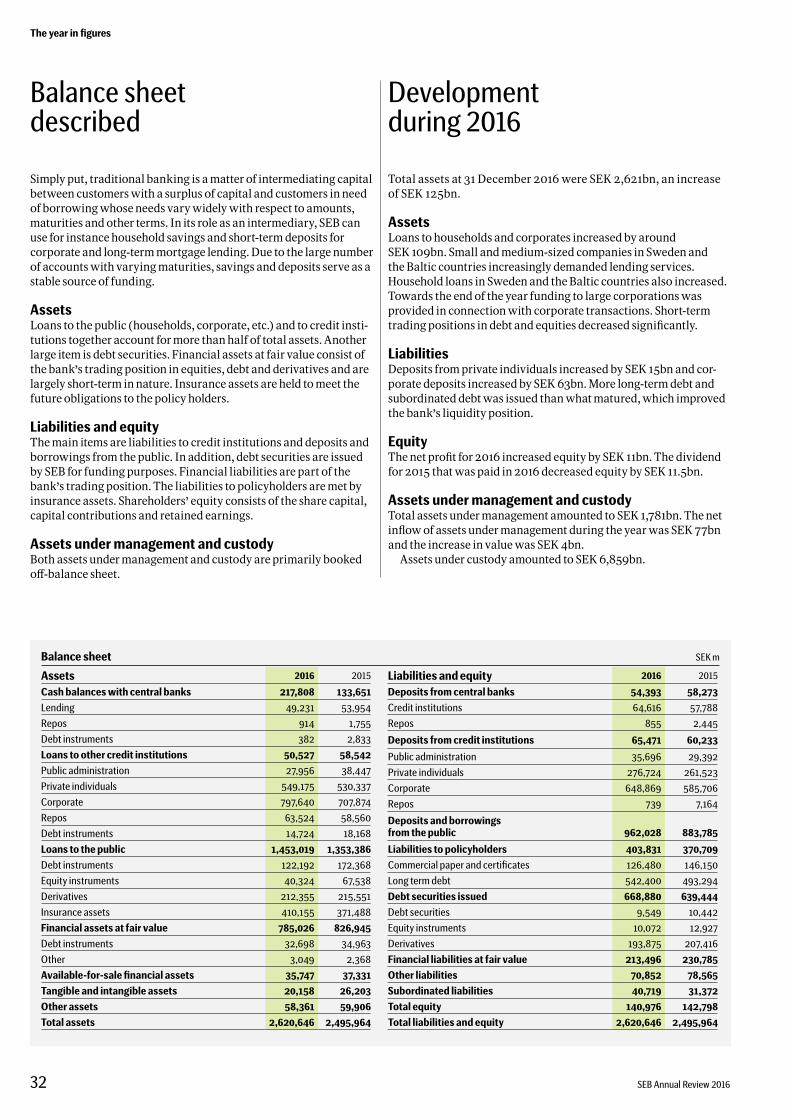

Income statementand balance sheet

Income statementSEKm

2016 2015 Change,%

Net interest income18,738 18,938 -1

Net fee and commission income

16,628 18,345 -9

Net financial income7,056 5,478 29

Net other income1,349 1,002 35

Total operating income43,771 43,763 0

Staff costs–14,562 -14,436 1

Other expenses–6,703 -6,355 5

Depreciation, amortisation

and impairments of assets

–6,496 -1,011

Total operating expenses –27,761 -21,802 27

Gains less losses from

tangible and intangible assets

–150 -213 -30

Net credit losses–993 -883 12

Operating profit14,867 20,865 -29

Income tax expense–4,249 -4,284 -1

Net profit10,618 16,581 -36

2016 in briefImportant events

Customers demandedhedging and riskmanagement servicesthroughout the year.

Prospera’s surveyranked SEB asnumber 1 in custo-mer satisfactionamong Nordictier 1 large corpora-tions and Nordictier 1 financialinstitutions.

As the only Nordic bank,SEB was included in theDow Jones SustainabilityIndex.

SEB increasedcorporate andpropertymanagementlending andcommitmentsby SEK 134bn.

Operating expensesincreased due to agoodwill impairmentof SEK 5,334m.

SEB paid SEK 1,362m inregulatory fees for finan-cial stability purposes.

2016 2015

Operating income, SEKm 43,771 43,763Operating profit, SEKm 14,867 20,865Return on equity, per cent 7.8 12.2Cost/income ratio 0.63 0.50Earnings per share, SEK 4.88 7.57Proposed dividend, SEK 5.50 5.25Common Equity Tier 1 capital ratio, per cent 18.8 18.8Leverage ratio, per cent 5.1 4.9Liquidity Coverage Ratio (LCR), per cent 168 128

Key figures

Subsequent to year-end2016,Annika Falkengren,SEB’s president and CEO,announced her decisionto leave the bank.Hersuccessor will be JohanTorgeby, currently divisionhead in SEB.

4 Macro environmentand strategy

SEB’s strategy focuses on providinga leading customer experience,investing in digital interfaces andautomated processes and on beingthemost attractive employer – all inorder to create value for all stake-holders.

18 Newcustomerservices

With the customers’ needs andthe bank’s vision to provideworld-class service inmind,SEB is taking a number ofinitiatives to improvecustomer experience.

28 RiskRiskmanagement isindispensable for SEB’slong-term profitability.Managing IT risks andclimate-related risks isincreasing in importance.

16 Customeractivities

In an uncertainmacro environment,large corporate and institutionalcustomerswere active in riskmanagement. The sentiment amongsmall andmedium-sized companieswasmore positive. Savings andhomemortgage volumes increasedamong private individuals.

21 Responsibleservices

SEBwants to be a rolemodelwithin sustainability andwithin financing and invest-ments that promote long-termsustainable development.

30 The yearin figures

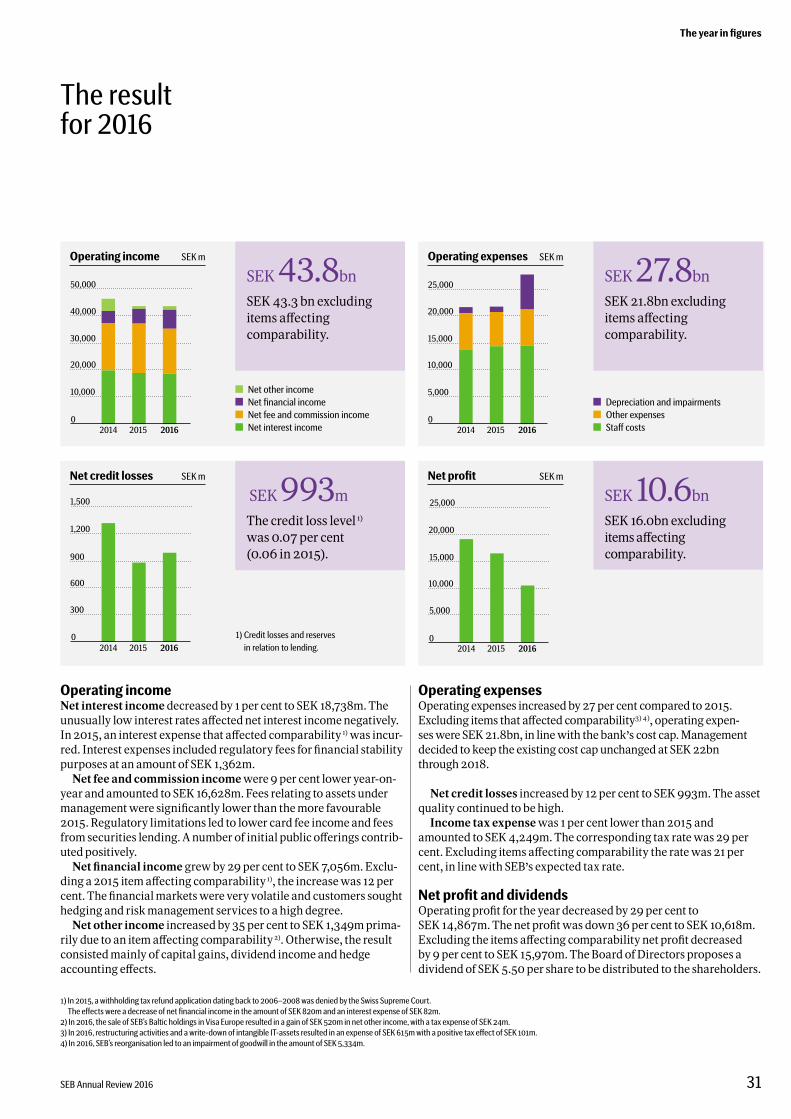

Operating profit decreased by7 per cent, excluding itemsaffecting comparability.Operating profit decreased by29 per cent including itemsaffecting comparability. TheBoard of Directors proposes adividend of SEK5.50 pershare.

Whowe areOur commitment to create value for our customers is basedon a tradition of entrepreneurship, international outlook andlong-term perspective.As a bankwe have an important roleto play in the shift to amore sustainableworld.

Our purposeWe believe that entrepreneurialminds and innovative companies arekey to creating a better world.We arehere to enable them to achieve theiraspirations and succeed throughgood times and bad.

Our visionTo deliver world-class serviceto our customers.

Our strategicpriorities• Leading customer experience• Maintaining resilience

and flexibility• Growing in areas of strength

160years in the service

of enterprise

Our financial targetsOutcome

2016 1)

Outcome2015 1)

Dividend payout ratioat 40 per cent or moreof earnings per share

75% 2) 66%

Common Equity Tier 1capital ratio of around 150basis points overrequirement

18.8% 3) 18.8%

Return on equitycompetitive with peers 11.3% 4) 12.9%

1) Outcome excludes items affecting comparability. See p. 30.2) Outcome incl. items affecting comparability is 113%.

Dividend proposal: SEK 5.50 per share (5.25).3) Regulatory requirement at year-end 2016: 16.9%.4) Outcome incl. items affecting comparability is 7.8%.

1) Excluding items affecting comparability.2) Compound Annual Growth Rate (CAGR).

Operating profitExpensesIncome

20161990 1995 20052000 2010

+5 %2)

+4 %2)

+8 %2)

43

22

20

13

8

3

Ourprofitdevelopment1990–2016 1)

SEK bn

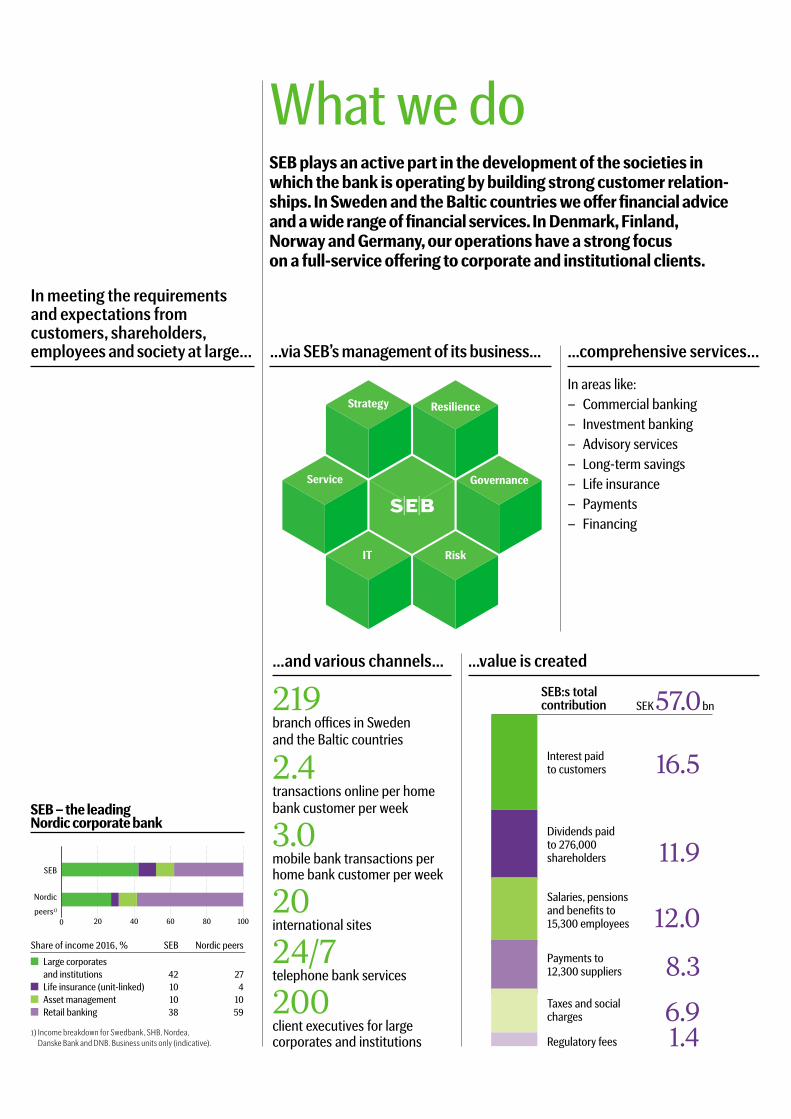

What we doSEBplays an active part in the development of the societies inwhich the bank is operating bybuilding strong customer relation-ships. In Sweden and the Baltic countriesweofferfinancial adviceandawide rangeoffinancial services. InDenmark, Finland,NorwayandGermany,our operations have a strong focuson a full-service offering to corporate and institutional clients.

…comprehensive services...

In areas like:– Commercial banking– Investment banking– Advisory services– Long-term savings– Life insurance– Payments– Financing

…and various channels…

219branch offices in Swedenand the Baltic countries

2.4transactions online per homebank customer per week

3.0mobile bank transactions perhome bank customer per week

20international sites

24/7telephone bank services

200client executives for largecorporates and institutions

…via SEB’smanagement of its business...

Strategy Resilience

Service

IT Risk

Governance

In meeting the requirementsand expectations fromcustomers, shareholders,employees and society at large...

SEB– the leadingNordic corporatebank

0 20 40 60 80 100

Share of income 2016, % SEB Nordic peers

Large corporatesand institutions 42 27Life insurance (unit-linked) 10 4Asset management 10 10Retail banking 38 59

1) Income breakdown for Swedbank, SHB, Nordea,Danske Bank and DNB. Business units only (indicative).

SEB

Nordic

peers1)

…value is created

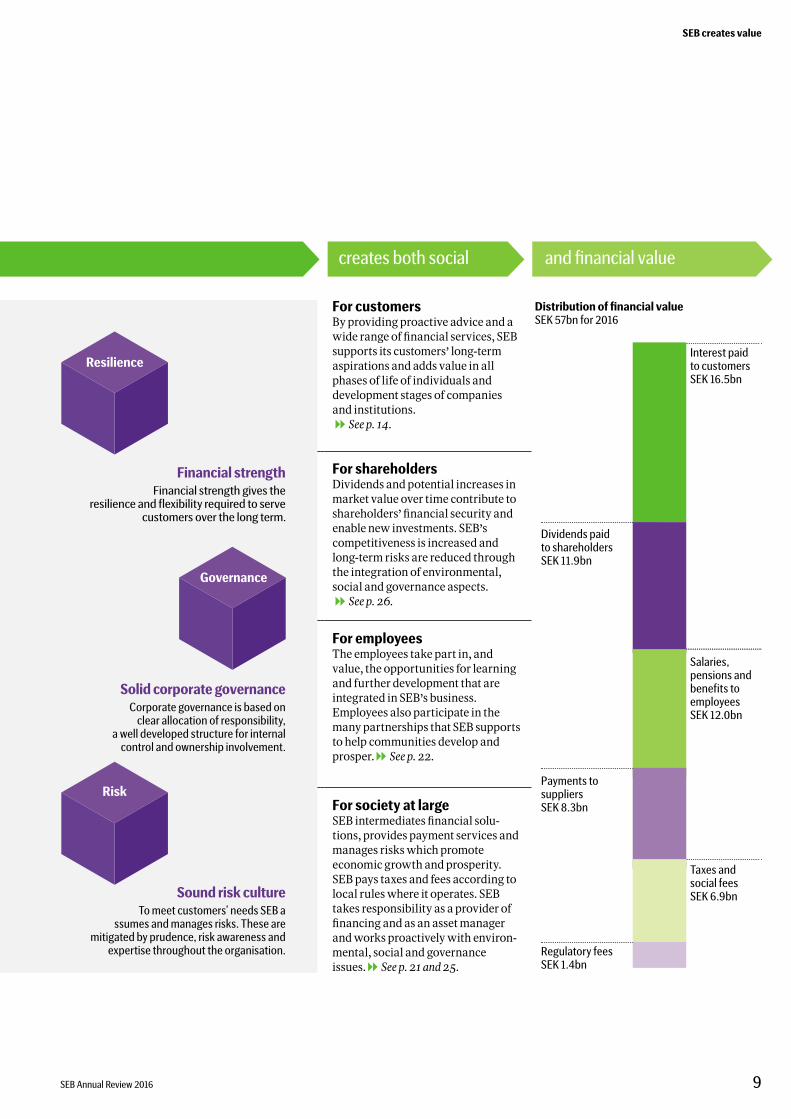

SEB:s totalcontribution SEK57.0bn

Interest paidto customers

Dividends paidto 276,000shareholders

Salaries, pensionsand benefits to15,300 employees

Payments to12,300 suppliers

Taxes and socialcharges

Regulatory fees

16.5

11.9

12.0

8.3

6.91.4

This is SEB

Customers always come first. Our committed andexperienced 15,300 employeeswork as a team to serveour customers.

Whomwe serve

PrivateindividualsSEB has approximately 4 millionprivate individuals among itscustomers in Sweden and the Balticcountries. Of these some 1.4 millionare home bank customers.

Small andmedium-sized companiesIn all, SEB serves approximately400,000 small and medium-sizedcompanies in Sweden and the Balticcountries. Of these, some 267,000are home bank customers.

2,300large corporations

LargecorporationsSEB’s corporate customers in theNordic region are among the largestin their respective industries. InGermany they range from large mid-corporates to large multinationals.

700financial institutions

FinancialinstitutionsSEB’s institutional clients operateboth in the Nordic countries andinternationally.

1.4million home bank customers

267,000home bank customers

In the past year, the shiftingmarket environ-ment continued to impact customer behav-iour. Customers’ demand for advisory andriskmanagement services remained. Asbusiness sentiment grewmore positivetowards the end of the year, event-drivenlarge corporate credit demand rose and SEBparticipated in a number of public equitylistings in theNordic region. However, thelow interest rate environment pushedmanyfinancial institutions tomove further outon the risk curve and into less liquid invest-ments. Both in Sweden and in the Balticcountrieswe supported domesticallyfocused SMEs as they showed a growingwillingness to invest.

The shifting demographic trendswithincreasingly ageing populations increasethe needs for long-term savings. Customersappreciated our holistic savings offering,which nowalso includes traditional lifeinsurance. SEB has taken an industry-leading approach as both private indivi-duals and institutional clients havehigher demands for sustainability-focusedinvestments.

The banking industry, just like all indus-tries, has had to revisit businessmodelsfollowing digitalisation and the rapidlychanging customer behaviours. Thus, 2016

The year 2016marked the start ofa new business plan focused ongrowth and transformation.

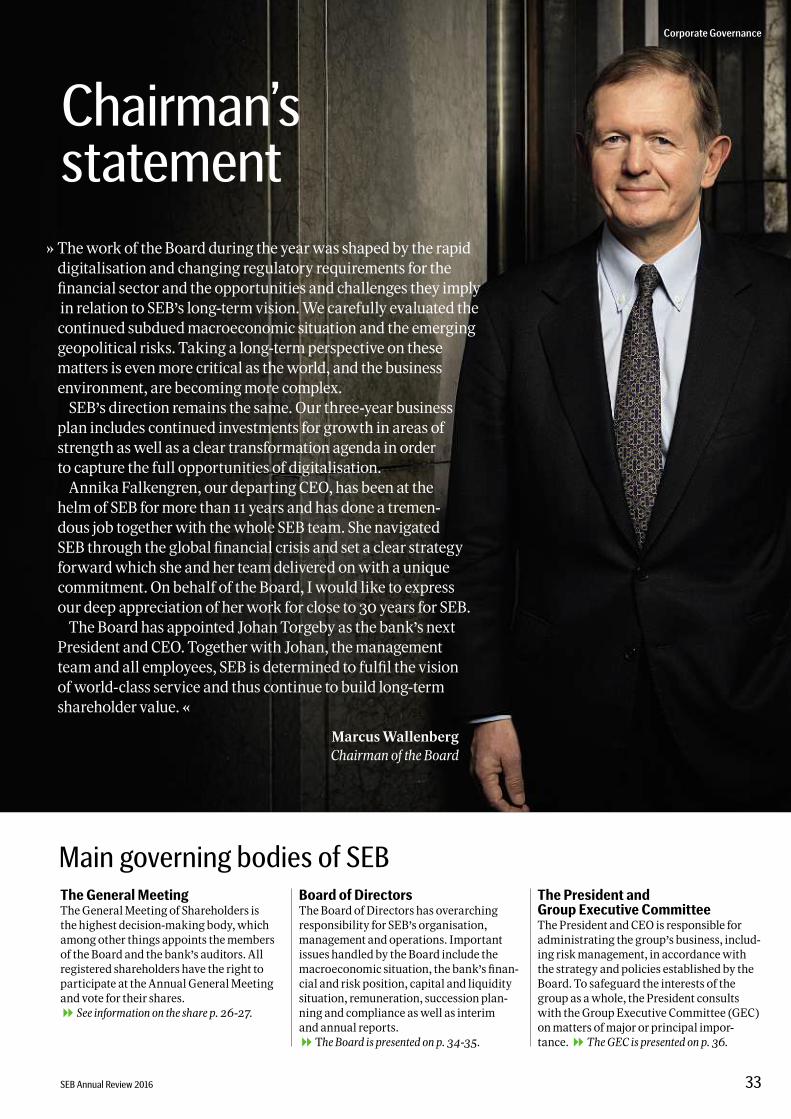

Lookingbackatmy tenure as the chief execu-tive of this fantastic bank, Imust say it hasbeen an era of somany different – and all ofthem exceptional – economic phases. Thefirst yearswere characterised by abundantliquidity, rapid credit growth and distortedrisk-return rewards. By nowwe all knowhow it ended. The deep global financialcrisiswith the acute phase following thecrash of LehmanBrothers in 2008, hadimmense effects not only for the financialsystem, but also for the real economy. Stilltoday, real global growth is not firing on allcylinders, despite years of unconventionalmonetary policywithmassive quantitativeeasing programmes and even negativeinterest rates.

In SEB,we have always been guided bytwo principles:maintaining resilienceand flexibility, and staying close to ourcustomers. Through a strong balance sheetand sufficient liquidity reserves,we cansupport our customers in good times andbad,while continuously developing servicestomake the customer experience evenmoreconvenient.

World-classservice

» Thewhole SEB teamwill, step by step,continue to deliver on our vision. «

marked the beginning of a three-year busi-ness plan for SEB reflecting our belief thatgoing forward customer orientation anddigitalisationwill increase in importance.We are changing ourways ofworkingand have invested in and launched newcustomer interfaces in all segments, aswell as a number of new services includingremote advice.

Iwould like to take this opportunity tothank all employees and customers for theircommitment to and trust in SEB all throughthese years. It has been lots of hardwork,butmost of all it has beenmore than elevenyears of passion for SEB. I know that thewhole great SEB teamwill – step by step –continue to deliver on our vision ofworld-class service.

Stockholm, February 2017

Annika FalkengrenPresident and Chief Executive Officer

President’s statement

MacroenvironmentThreemajor global trends are impacting banks’ operating environment.Customer behaviour and expectations are changingwith the digitaltransformation. Global growth,with lowor negative interest rates andnew regulatory requirements, remains uncertain. Demands on banks totake responsibility for amore sustainableworld are higher.

The global economy remained uncertainfollowing a number of unexpectedeconomic and political events during 2016.However, therewere clear signs of economicturnaround. Initiatives for infrastructureinvestmentswere taken. The increase inUSinterest ratesmay have been a starting pointfor a shift away from the very lowor nega-tive interest rates, eventually leading todiscontinuing the central banks’massivequantitative easing programmes. The

Complexity inthe macro environment

record-high global debt remains to bemanaged for a long time, however.

The referendum in theUnitedKingdomresulting in the favour of Brexit aswell asthe presidential election in theUnitedStates contributed to increased uncertaintyaround international trade and politicalstability. A rapid increase in populist,nationalist and protectionist forceswas alsoseen in 2016 in a number of countries.

Conflicts and uncertainty inmany partsof theworld have resulted inmajorwavesofmigration that are creating tension.

Rapid digitaltransformation

The rapid technical developmentis a new industrial revolutionDigitalisation is leading to new customerbehaviours and newbusinessmodels arerewriting themap for society,many in-dustries and for private individuals – sotoo for the financial sector.

Customers expect accessible and con-venient services. Digitalisation providesample opportunity to create newand easy-to-use niche services for payments, savingsand lending. One example is the highlysuccessfulmobile payment service, Swish,which is owned by the Swedish bank sector.The transformation is putting demands onfaster development, simplified processesand increased automation in the bankingsector andwill, over time, result in substan-tial efficiencymeasures.

Flexible and agile companieswhich lackheavy infrastructure and are not burdenedby the same rules and regulations as banksare entering the financialmarkets. Thesefintech companies also represent an oppor-tunity for the financial sector and there aremany examples of partnerships building ontraditional banks’ infrastructure that leadto innovative and effective solutions for thecustomers.

There is substantial underlying publictrust in traditional universal banks and theyoffer customers comprehensive solutionsand a total viewof their financial situation.Building on this trust, SEB is striving tomeet the increasing expectations of thecustomers.

» The Sw

edish re

po

ratewas n

egative

through

outthe

year an

dwas

–0,5 pe

r cent a

t

year-en

d. «

SEB Annual Review 2016 5

Macro environment

The new financial regulations that continue to be developed are creatinguncertainty about economic development, since no one today hasassessed the total effect of all rules and regulations.

Standardised risk-weights mayincrease lending ratesThe new, standardised risk-weight floor thatis currently being discussed by the BaselCommittee poses a challenge to theNordicbanking system,which is successfully usingindividual risk classifications to assess itscapital needs.

A standardised risk-weight floor accord-ing to theBasel Committee’s recommenda-tion removes the incentive to use sound riskprinciples,where low riskmeans lowerinterest rates for the customer andhigh riskmeans higher interest rates for the customer.Thiswould lead to a dramatic rise in capitalneeds inNordic banks. This, in turn,wouldlead to higher rates for corporate lending,which in turnwould have a direct impact ongrowth in the real economy.

In January 2017 the Basel Committeeannounced that it is postponing the publica-tion of the risk-weight floor rules untilfurther notice. In a longer perspective theuncertainty remains.

Proposed new financial taxIn the opinion of the Swedish governmentbanks are insufficiently taxed becausefinancial services are VAT-exempt. There-fore, a 15 per cent tax onwages and benefitsthat relate to the VAT-exempt financialservices is proposed. In addition, the taxis proposed to be non-tax deductible.

If implemented, the taxwould affect notonly the financial sector but also companiesthat run treasury departments and thefintech sector.

According to calculations provided by theSwedish Bankers’ Association asmany as16,000 jobs in Swedenwould be threatenedif these planswere in fact carried out, sincejobsmay bemoved abroad in order to lowerstaff costs.

The total estimated effect from theproposal under discussion on SEB is aroundSEK700mper year in additional costs.

New regulationscreate uncertainty

The Basel Committee

Stabilising thefinancial sector

Regulatory requirements on banks inSweden are among the strictest in theworld.Recent Swedish regulations are designedto further stabilise the Swedish financialsector and further ensure banks’ contri-bution to society.

Based on experiences frompreviousfinancial crises, national governmentshave established so-called resolution fundswith the purpose to finance potential futuresupport from the government to credit insti-tutions.

Similarly, deposit guarantees provideprotection for retail depositors in case ofbank default.

Financial contributionsIn Sweden, banks contribute to the resolu-tion fund for stability purposes and to thenational deposit guarantee scheme.

In 2016, SEB’s total regulatory feeswereSEK 1.4bn. In 2017,when the full resolutionfee is charged, the bank expects the fees toamount to SEK2.1bn, the absolutemain partofwhich are paid in Sweden.

Risk of unfair competition

Interest on subordinated debt that quali-fies as additional tier 1 capital and tier 2capital is no longer deductible forincome tax purposes. The reason is thatsuch debt is considered to be part ofbanks’ capital base and therefore shouldbe treated as capital for tax purposes.

Since thiswould be a tax on Swedishbanks only there is a risk of unfaircompetition in relation to internationalfinancial institutions.

The additional tax on SEB is estimatedto around SEK360m in 2017 and SEK300m in 2018 and thereafter.

SEB Annual Review 20166

Macro environment

The role of business in the shift to amore sustainable world wasmani-fested for the first time in 2015when the UN 17 global sustainabledevelopment goals were signed andthe global and legally bindingclimate agreement was adopted atthe COP21meeting in Paris.

The business sector contributes to theworkwith the 17 global sustainable developmentgoals that have been set by theUN. Thegoals span awide range, frompoverty eradi-cation to promotion of health, prosperityand economic growth. For each goal thereare specific targets to be achieved over thenext 15 years. To reach these targets, allpartiesmust do their part, governments,business and industry aswell as civil soci-ety. SEBwas one of the 400 companieswhich signed a global petition in support ofthe climate agreement and the bank hasrevised its position on climate changewith a

clear ambition to be involved and contributeto limiting globalwarming towell below2degrees Celsius.

The financial sector has a key role to playin channelling investment capital to infra-structure and fossil-free energy systems. Indoing so companies are not only helping toaddress the climate threat – they also havebetter prospects for sustainable growth andthus better returns.See also SEB’s Sustainability Report 2016.

Most countries are facing significant demo-graphic challenges posed by ageing popula-tions.

The dependency burden for the activelyworking portion of the population is grow-ing,which strains social security systems.There is a growing realisation that individu-als themselves need to take greater respon-sibility for their financial security throughsavings and insurance solutions. In this areathe financial sector canmake a contributionby providing easily accessible advice andlong-term investment services.

Demographicchallenges

Shift to a moresustainable world

Sustainable development goals

Stakeholder dialogue

Financialmarketsareat thecoreofcreatingeconomicandsocial value inamodernsociety.Herebanksplayakeyrole.

SEBmaintains an active dialogue notonlywith customers and employees butalsowith other stakeholders such as share-holders, suppliers, government agencies,legislators and representatives of the localcommunities in placeswhere SEB oper-ates. In this dialogue, SEB has identifiedthe issues that aremost important forstakeholders aswell as for the bank. They

are in agreement and are in linewith thebank’s strategic direction on the base ofriskmanagement, financial strength andresilience.

Mutual issues are:• providing fulfilling customer experience

and good service

• maintaining high standards of businessethics and IT security

• contributing to a society characterisedby innovation and resource efficiency.

Society

EmployeesCustomers

Shareholders

SEB Annual Review 2016 7

Macro environment

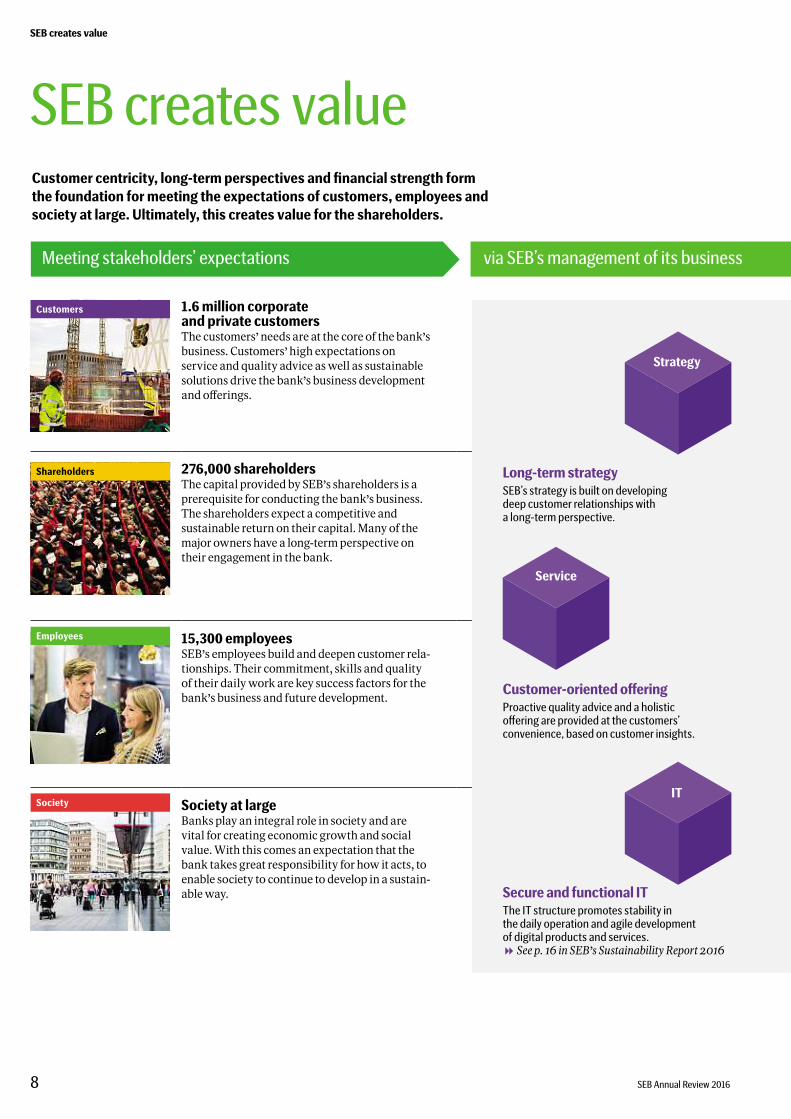

SEB creates value

Meeting stakeholders’ expectations via SEB’s management of its business

Customer centricity, long-term perspectives and financial strength formthe foundation for meeting the expectations of customers, employees andsociety at large. Ultimately, this creates value for the shareholders.

1.6 million corporateand private customersThe customers’ needs are at the core of the bank’sbusiness. Customers’ high expectations onservice and quality advice aswell as sustainablesolutions drive the bank’s business developmentand offerings.

276,000 shareholdersThe capital provided by SEB’s shareholders is aprerequisite for conducting the bank’s business.The shareholders expect a competitive andsustainable return on their capital.Many of themajor owners have a long-termperspective ontheir engagement in the bank.

15,300 employeesSEB’s employees build and deepen customer rela-tionships. Their commitment, skills and qualityof their dailywork are key success factors for thebank’s business and future development.

Society at largeBanks play an integral role in society and arevital for creating economic growth and socialvalue.With this comes an expectation that thebank takes great responsibility for how it acts, toenable society to continue to develop in a sustain-ableway.

Long-term strategySEB’s strategy is built on developingdeep customer relationships witha long-term perspective.

Customer-oriented offeringProactive quality advice and a holisticoffering are provided at the customers’convenience, based on customer insights.

Secure and functional ITThe IT structure promotes stability inthe daily operation and agile developmentof digital products and services. See p. 16 in SEB’s Sustainability Report 2016

Strategy

IT

Service

Employees

Customers

Society

Shareholders

SEB Annual Review 20168

SEB creates value

and financial valuecreates both social

Distribution of financial valueSEK 57bn for 2016

For customersBy providing proactive advice and awide range of financial services, SEBsupports its customers’ long-termaspirations and adds value in allphases of life of individuals anddevelopment stages of companiesand institutions.See p. 14.

For shareholdersDividends and potential increases inmarket value over time contribute toshareholders’ financial security andenable new investments. SEB’scompetitiveness is increased andlong-term risks are reduced throughthe integration of environmental,social and governance aspects.See p. 26.

For employeesThe employees take part in, andvalue, the opportunities for learningand further development that areintegrated in SEB’s business.Employees also participate in themany partnerships that SEB supportsto help communities develop andprosper.See p. 22.

For society at largeSEB intermediates financial solu-tions, provides payment services andmanages riskswhich promoteeconomic growth and prosperity.SEB pays taxes and fees according tolocal ruleswhere it operates. SEBtakes responsibility as a provider offinancing and as an assetmanagerandworks proactivelywith environ-mental, social and governanceissues.See p. 21 and 25.

Financial strengthFinancial strength gives the

resilience and flexibility required to servecustomers over the long term.

Solid corporate governanceCorporate governance is based onclear allocation of responsibility,

a well developed structure for internalcontrol and ownership involvement.

Sound risk cultureTomeet customers’ needs SEB a

ssumes andmanages risks. These aremitigated by prudence, risk awareness and

expertise throughout the organisation.

Resilience

Risk

Governance

Interest paidto customersSEK 16.5bn

Salaries,pensions andbenefits toemployeesSEK 12.0bn

Taxes andsocial feesSEK 6.9bn

Dividends paidto shareholdersSEK 11.9bn

Payments tosuppliersSEK 8.3bn

Regulatory feesSEK 1.4bn

SEB Annual Review 2016 9

SEB creates value

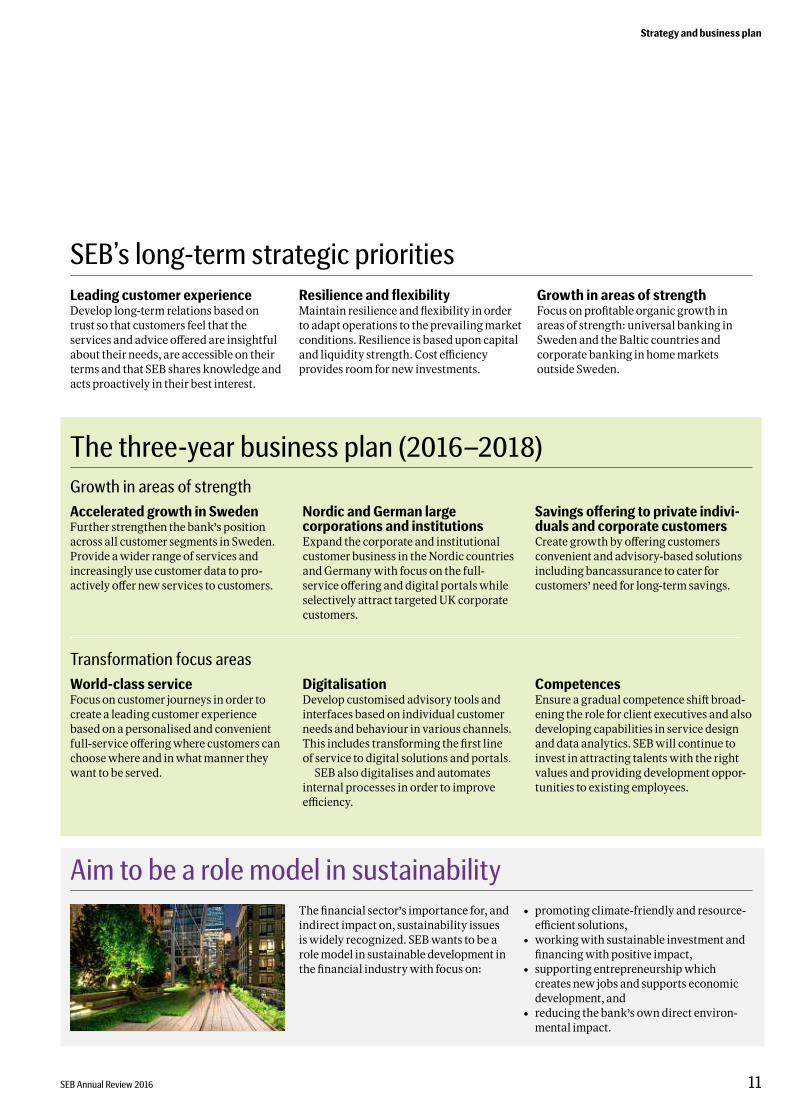

World-classserviceSEB’s long-term vision reflects a future inwhich customer orientation anddigitalisation increase in importance. In this environment, the bank’s ambi-tion is to be the undisputed leading Nordic corporate and institutional bankand the top universal bank in Sweden and the Baltic countries.

Leading customer experienceDevelop long-term relations based ontrust so that customers feel that theservices and advice offered are insightfulabout their needs, are accessible on theirterms and that SEB shares knowledge andacts proactively in their best interest.

Resilience and flexibilityMaintain resilience and flexibility in orderto adapt operations to the prevailingmarketconditions. Resilience is based upon capitaland liquidity strength. Cost efficiencyprovides room for new investments.

The financial sector’s importance for, andindirect impact on, sustainability issuesiswidely recognized. SEBwants to be arolemodel in sustainable development inthe financial industrywith focus on:

Growth in areas of strengthFocus on profitable organic growth inareas of strength: universal banking inSweden and the Baltic countries andcorporate banking in homemarketsoutside Sweden.

• promoting climate-friendly and resource-efficient solutions,

• workingwith sustainable investment andfinancingwith positive impact,

• supporting entrepreneurshipwhichcreates new jobs and supports economicdevelopment, and

• reducing the bank’s owndirect environ-mental impact.

Aim to be a role model in sustainability

SEB’s long-term strategic priorities

The three-year business plan (2016–2018)Growth in areas of strengthAccelerated growth in SwedenFurther strengthen the bank’s positionacross all customer segments in Sweden.Provide awider range of services andincreasingly use customer data to pro-actively offer new services to customers.

Nordic and German largecorporations and institutionsExpand the corporate and institutionalcustomer business in theNordic countriesandGermanywith focus on the full-service offering and digital portalswhileselectively attract targetedUK corporatecustomers.

Savings offering to private indivi-duals and corporate customersCreate growth by offering customersconvenient and advisory-based solutionsincluding bancassurance to cater forcustomers’ need for long-term savings.

Transformation focus areasWorld-class serviceFocus on customer journeys in order tocreate a leading customer experiencebased on a personalised and convenientfull-service offeringwhere customers canchoosewhere and inwhatmanner theywant to be served.

DigitalisationDevelop customised advisory tools andinterfaces based on individual customerneeds and behaviour in various channels.This includes transforming the first lineof service to digital solutions and portals.

SEB also digitalises and automatesinternal processes in order to improveefficiency.

CompetencesEnsure a gradual competence shift broad-ening the role for client executives and alsodeveloping capabilities in service designand data analytics. SEBwill continue toinvest in attracting talentswith the rightvalues and providing development oppor-tunities to existing employees.

SEB Annual Review 2016 11

Strategy and business plan

Dividend payout ratio Per cent

Overall targetsand outcome

2) According to the Net Promoter Score method

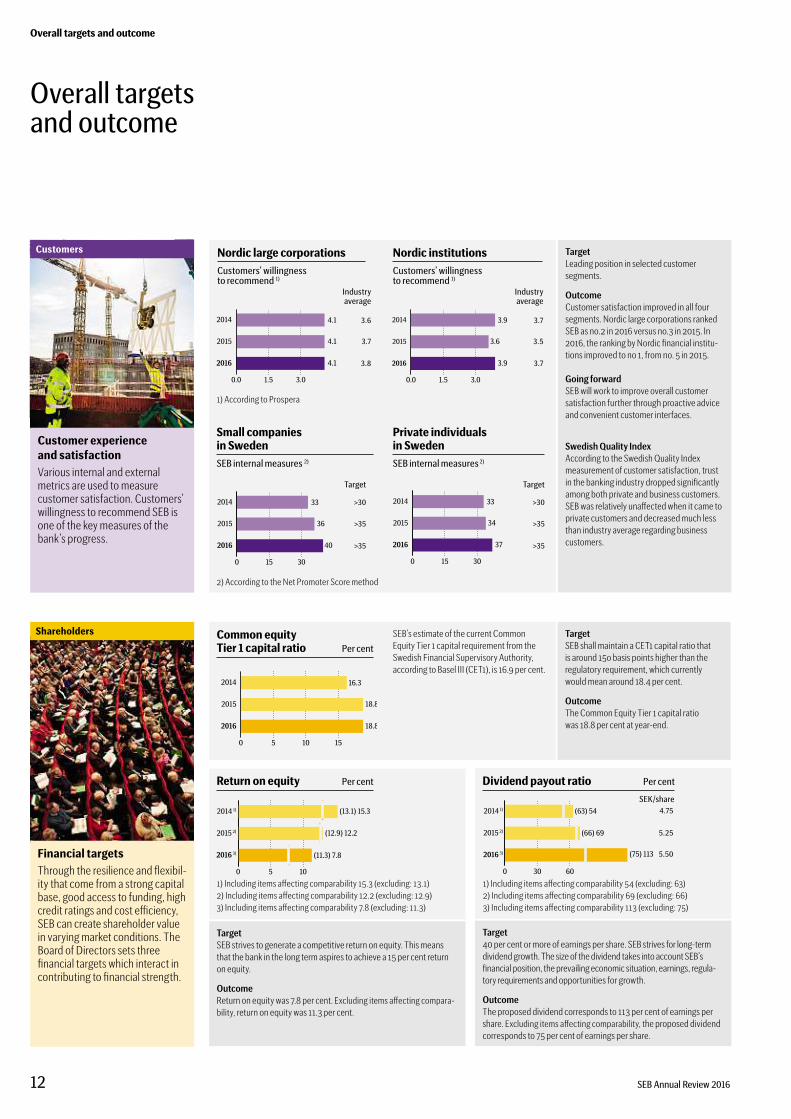

1) According to Prospera

0.0 1.5 3.0

2016

2015

2014 4.1

4.1

4.1

0 15 30

2016

2015

2014 33

36

40

0 5 10 15

2016

2015

2014 16.3

18.8

18.8

0 5 10

2016

3)

2015 2)

2014 1) (13.1) 15.3

(11.3) 7.8

(12.9) 12.2

2016

3)

2015 2)

2014 1)

0 30 60

(75) 113

(66) 69

(63) 54

0.0 1.5 3.0

2016

2015

2014 3.9

3.6

3.9

0 15 30

2016

2015

2014 33

34

37

Customer experienceand satisfactionVarious internal and externalmetrics are used to measurecustomer satisfaction. Customers’willingness to recommend SEB isone of the key measures of thebank’s progress.

Target

Industryaverage

Industryaverage

SEK/share

Target

TargetLeading position in selected customersegments.

OutcomeCustomer satisfaction improved in all foursegments. Nordic large corporations rankedSEB as no.2 in 2016 versus no.3 in 2015. In2016, the ranking by Nordic financial institu-tions improved to no 1, from no. 5 in 2015.

Going forwardSEB will work to improve overall customersatisfaction further through proactive adviceand convenient customer interfaces.

SwedishQuality IndexAccording to the Swedish Quality Indexmeasurement of customer satisfaction, trustin the banking industry dropped significantlyamong both private and business customers.SEB was relatively unaffected when it came toprivate customers and decreased much lessthan industry average regarding businesscustomers.

SEB’s estimate of the current CommonEquity Tier 1 capital requirement from theSwedish Financial Supervisory Authority,according to Basel III (CET1), is 16.9 per cent.

1) Including items affecting comparability 15.3 (excluding: 13.1)2) Including items affecting comparability 12.2 (excluding: 12.9)3) Including items affecting comparability 7.8 (excluding: 11.3)

1) Including items affecting comparability 54 (excluding: 63)2) Including items affecting comparability 69 (excluding: 66)3) Including items affecting comparability 113 (excluding: 75)

Customers Nordic large corporationsCustomers’ willingnessto recommend 1)

Small companiesin SwedenSEB internal measures 2)

Return on equity Per cent

Common equityTier 1 capital ratio Per cent

Nordic institutionsCustomers’ willingnessto recommend 1)

Private individualsin SwedenSEB internal measures 2)

Shareholders

Financial targetsThrough the resilience and flexibil-ity that come from a strong capitalbase, good access to funding, highcredit ratings and cost efficiency,SEB can create shareholder valuein varying market conditions. TheBoard of Directors sets threefinancial targets which interact incontributing to financial strength.

>30

3.73.6

>30

5.25

4.75

5.50

>35

>35

3.5

3.7

3.7

3.8

>35

>35

TargetSEB shall maintain a CET1 capital ratio thatis around 15o basis points higher than theregulatory requirement, which currentlywould mean around 18.4 per cent.

OutcomeThe Common Equity Tier 1 capital ratiowas 18.8 per cent at year-end.

Target40 per cent or more of earnings per share. SEB strives for long-termdividend growth. The size of the dividend takes into account SEB’sfinancial position, the prevailing economic situation, earnings, regula-tory requirements and opportunities for growth.

OutcomeThe proposed dividend corresponds to 113 per cent of earnings pershare. Excluding items affecting comparability, the proposed dividendcorresponds to 75 per cent of earnings per share.

TargetSEB strives to generate a competitive return on equity. This meansthat the bank in the long term aspires to achieve a 15 per cent returnon equity.

OutcomeReturn on equity was 7.8 per cent. Excluding items affecting compara-bility, return on equity was 11.3 per cent.

SEB Annual Review 201612

Overall targets and outcome

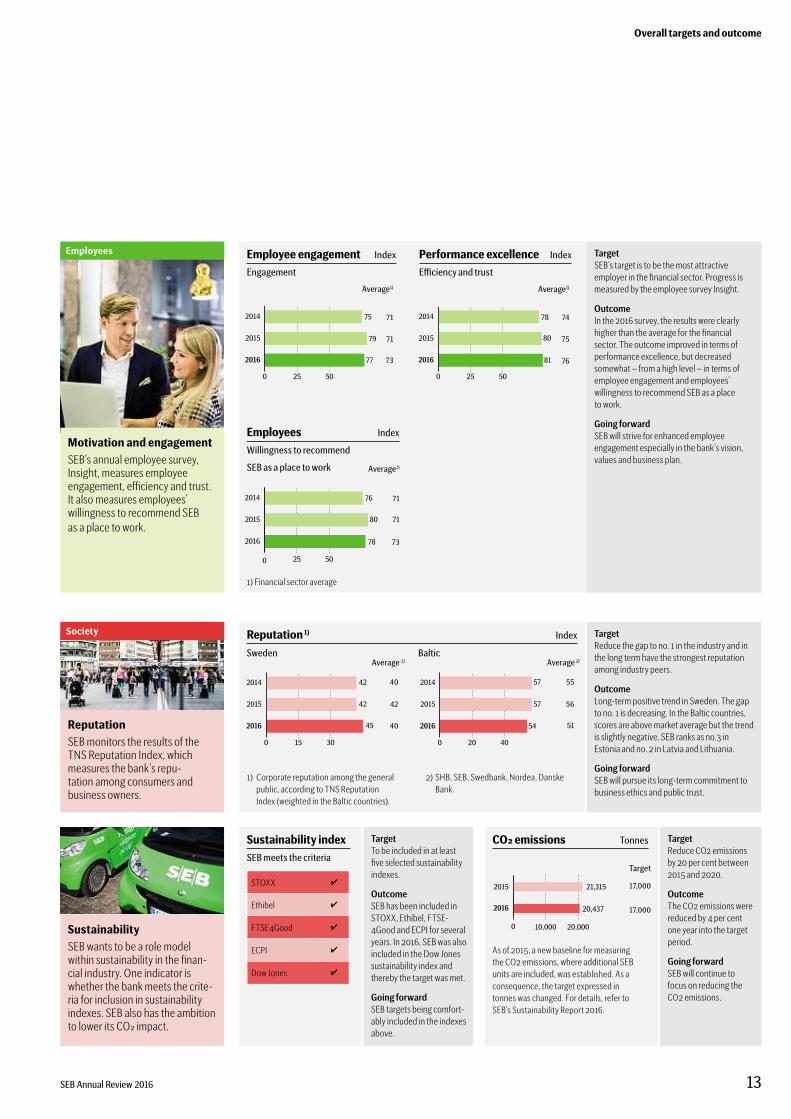

ReputationSEB monitors the results of theTNS Reputation Index, whichmeasures the bank’s repu-tation among consumers andbusiness owners.

Motivation and engagementSEB’s annual employee survey,Insight, measures employeeengagement, efficiency and trust.It also measures employees’willingness to recommend SEBas a place to work.

TargetSEB’s target is to be the most attractiveemployer in the financial sector. Progress ismeasured by the employee survey Insight.

OutcomeIn the 2016 survey, the results were clearlyhigher than the average for the financialsector. The outcome improved in terms ofperformance excellence, but decreasedsomewhat – from a high level – in terms ofemployee engagement and employees’willingness to recommend SEB as a placeto work.

Going forwardSEB will strive for enhanced employeeengagement especially in the bank’s vision,values and business plan.

Employees

Society

SustainabilitySEB wants to be a role modelwithin sustainability in the finan-cial industry. One indicator iswhether the bank meets the crite-ria for inclusion in sustainabilityindexes. SEB also has the ambitionto lower its CO2 impact.

Sustainability indexSEBmeets the criteria

0 15 30

2016

2015

2014

42

42

45

0 20 40

2016

2015

2014

57

57

54

0 10,000 20,000

2016

2015 21,315

20,437

Reputation 1) Index

CO2 emissions Tonnes

2) SHB, SEB, Swedbank, Nordea, DanskeBank.

1) Corporate reputation among the generalpublic, according to TNS ReputationIndex (weighted in the Baltic countries).

1) Financial sector average

As of 2015, a new baseline for measuringthe CO2 emissions, where additional SEBunits are included, was established. As aconsequence, the target expressed intonnes was changed. For details, refer toSEB’s Sustainability Report 2016.

STOXX

Ethibel

FTSE4Good

ECPI

Dow Jones

Employee engagement Index

Engagement

Average1)

0 25 50

2016

2015

2014 75

79

77

71

71

73

Performance excellence Index

Efficiency and trust

0 25 50

2016

2015

2014 78

80

81

Average1)

75

74

76

Sweden Baltic

Employees Index

Willingness to recommend

SEB as a place towork

0 25 50

2016

2015

2014 76

80

78

71

40 55

71

42 56

73

40 51

Average1)

Average 2) Average 2)

Target

17,000

17,000

TargetTo be included in at leastfive selected sustainabilityindexes.

OutcomeSEB has been included inSTOXX, Ethibel, FTSE-4Good and ECPI for severalyears. In 2016, SEB was alsoincluded in the Dow Jonessustainability index andthereby the target was met.

Going forwardSEB targets being comfort-ably included in the indexesabove.

TargetReduce CO2 emissionsby 20 per cent between2015 and 2020.

OutcomeThe CO2 emissions werereduced by 4 per centone year into the targetperiod.

Going forwardSEB will continue tofocus on reducing theCO2 emissions.

TargetReduce the gap to no. 1 in the industry and inthe long term have the strongest reputationamong industry peers.

OutcomeLong-term positive trend in Sweden. The gapto no. 1 is decreasing. In the Baltic countries,scores are above market average but the trendis slightly negative. SEB ranks as no.3 inEstonia and no. 2 in Latvia and Lithuania.

Going forwardSEB will pursue its long-term commitment tobusiness ethics and public trust.

SEB Annual Review 2016 13

Overall targets and outcome

Customers andcustomer servicesIn a rapidly changing world, innovation and transformationare key for SEB — new services, solutions andmeeting placesare developed in close cooperation with customers in orderto offer world-class service.

Large corporations Financial institutionsSEB serves some 2,300 large corporations in awide range ofindustries and inmost caseswith an international focus. In theNordic countries these corporations are among the largest in theirrespective industries, while inGermany and theUnitedKingdomthe customers range from the largemid-corp segment tomulti-national corporations.

SEB serves some 700financial institutions, consisting of pensionand assetmanagers, hedge funds, insurance companies andother banks, active in theNordic countries and internationally.

Strategy• Aim tomake SEB a preferred partner by offering a comprehen-

sive range of financial services and advice for all aspects of acompany’s operations, using the bank’s broad expertise anddepth of industry knowledge.

• Expand businesswith the existing customer base in theNordiccountries andGermany, building on long-termpersonal rela-tionships.

• Focus on convenient digital customer portals and processefficiency in addition to cost and capital efficiency.

• Grow thenumber of corporate customers in theUnitedKingdom.

Strategy• Meet the financial institutions’ needs by a specialised customer

key account organisationwhere the bank’s offerings arecombinedwith a depth of expertise in the operations of theinstitutional clients.

• Focus on convenient digital client portals and process effi-ciency in addition to cost and capital efficiency.

• Offer a comprehensive range of services to customers in theNordic countries andGermany and offerNordic productsglobally.

Small andmedium-sized companies Private individualsSEB serves some400,000 small andmedium-sized companies inSweden and the Baltic countries. Of these 168,000 are home bankcustomers in Sweden and 99,000 in the Baltic countries. There areapproximately 500mid-corp and public sector customers inSweden,manywith international operations. The public sectorincludes government agencies, state-owned companies andmunicipalities.

In all, SEB has approximately fourmillion private customers inSweden and the Baltic countries. Of these 485,000 are homebank customers in Sweden and 904,000 in the Baltic countries.For private customerswith sizeable capital and a need formorequalified advice, SEB offers a comprehensive range of privatebanking services. SEB has approximately 25,000 private bank-ing customers.

Strategy• Develop SEB’s offering based on the bank’s strong position

among large corporations in theNordic region. Offer small andmedium- sized companies convenient services and proactiveadvice, based on a deep insight of their entire situation, includ-ing the needs of both the employees and the owners.

• Serve smaller businesseswith the help of packaged services andincreased accessibility through digital interfaces.

Strategy• Meet customers’ full needs for financial advice and services

during all phases of life.• Strive tomake it easy for customers tomanage their personal

finances and plan for the future. Proactivity and accessibilityare key in providing convenient services.

• Provide options for long-term savings since ageing popula-tions are putting pressure on the publicwelfare systemwhichmeans that individuals need to take greater responsibility fortheir financial security.

Customersegments

TeoOttolaKonecranes

Readmore on p. 17.

Anders ParrowReadmore on p. 20.

Katre KõvaskSüdameapteek

Readmore on p. 19.

Meet ourcustomers

SEB Annual Review 2016 15

Customer segments

Tentative, but more activity towards the end of the yearIn the beginning of the year, characterisedbymacroeconomic uncertainty, largecorporate customerswere cautious. Therewas higher demand for lending towardsthe end of the year, driven by a number ofcorporate events. In addition, SEB played aninstrumental role as adviser and arranger infor instance the listing of Arcus inNorwayandDNA in Finland. Private equity inves-torswere increasingly active. Customers

requested advisory and riskmanagementservices in the volatilemarket environmentthroughout the year. In theUnitedKing-dom, new customers chose SEB for itsNordic relationship bank profile.

Customer satisfactionSEBwas ranked no. 1 among tier 1 largecorporations in theNordic region inProspera’s customer satisfaction survey.

Large corporations

Activity driven by low interest rates and volatile marketsUncertainty regarding the impact of bank-ing regulations aswell the direction ofcentral bank policies characterised a goodpart of 2016. Activity among financial insti-tutionswas generally lowbut increasedtowards the end of the year. In times ofmarket turbulence, especially around theBrexit referendumand the presidential elec-tion in theUnited States,marketswere vola-tile and riskmanagement activity high. Thelow interest rate environment prompted

many financial institutions to take onmorerisk by investing in less liquid assets.

Institutional investors grew increasinglyinterested in sustainability focused invest-ments.

Customer satisfactionSEBwas ranked no. 1 by tier 1 financial insti-tutions in theNordic region in Prospera’scustomer satisfaction survey.

Financial institutions

Positive development in both Sweden and the Baltic countriesSwedish small andmedium-sized compa-nieswere less affected by the global uncer-tainty. The anticipated investments in in-frastructure in Sweden created a positivemomentum. Around 9,000 new companieschose to become home bank customers inSEB. Their need for financing and savingsservices grew and SEB’s digital serviceswere increasingly utilised.

Digital servicesThebusiness banking app, the internetbank, the Swish app for payment services forcompanies and e-invoice are all examples ofdigital initiatives thatwere appreciated bythe small andmedium-sized customers.

Active Baltic customersDevelopmentwas also positive in the Balticcountries,where companies have beenadept at countering the effects of theRussian sanctions. Customerweremorepositive and their financing needs increasedin all three countries.

Small and medium-sized companies

In the uncertain environment, bothlarge corporate customers andinstitutions maintained a wait-and-see approach, but the need for riskmanagement services was high.Small andmedium-sized companieswere more positive. On the privateside, customers increasingly useddigital services for their financialneeds.

Customeractivities in 2016

SEB Annual Review 201616

Customer activities

Digital services and greater need for long-term savingsWith the changing demographics, privateindividuals’ awareness of long-term savingsand risk insurance solutions increased.Customers took advantage of SEB’simproved offer in the long-term savingsarea,with unit-linked and traditional lifeinsurance options and also appreciated thepossibility to use digital pension analysisservices.

The stockmarket’s performancewasreflected in customers’ behaviours. Towardsthe end of the year customers increasinglychose to invest in equity and allocationfunds.

Private individuals increased their digitalpresence andmobile interactionswere fourtimes as high as the internet banking inter-actions in Sweden.

Household mortgagesHouseholds in Sweden continued to investin newhomes in a real estatemarketwherethe housing shortage and low interest ratessignificantly pushed up prices.

The new strict amortisation requirementsthatwere implemented in Sweden in 2016had a limited effect on SEB’s customerssince the bank has had similar internal rulesin place for some time.

Baltic regionIn the Baltic countries, thereweremoder-ately positive economic signs driven byprivate consumption and activity increasedamong private customers. Their demand forboth loans and savings products increased.

Youngsters appreciated SEB’s educationalseminars on personal finance.

Private individuals Support to entrepreneurs in allphases from start-up to growth

In SEB, supporting entrepreneurshipand newbusiness start-ups goeswithoutsaying. In Sweden, SEBhas establishedcollaborations along the entire entrepre-neur spectrum, fromnewtoestablishedcompanies See p. 25.

SEBoperates the Innovation Forum–ameeting placewhere promisingcutting-edge companieswith ties toeducational and research institutionshave anopportunity to gain access topotential investors among SEB’s custom-ers. The event is highly appreciated andhas led to concrete investments for abouthalf of the participants.

In theBaltic countries, SEBarrangesseminarswhere corporate customers getinformation and anopportunity to inter-act,with the aim tohelp eachotherrealise their growth ambitions throughthe power of innovation.

» SEB actswith agility, littlebureaucracy and has aproactive approach. «

Meet one of our largecorporate customers

Finland’s Konecranes, a world-leadingmanu-facturer in the lifting business, servescustomers inmanufacturing and processindustries, shipyards, ports and terminals.

In January, the company finalised theacquisition of Terex’s material handling andport solutions segment, a deal which in onestroke nearly doubled revenue, comple-mented the product offering and expandedthe installed base of cranes significantly. SEBplayed a key role in developing the financingsolution.

“SEB has been a strategic partner since ourinception in themid-1990s. We have a longand extensive relationship characterised bymutual trust. SEB’s contacts are easy to dealwith, they act with agility and little bureau-cracy and have a proactive approach”, saysTeo Ottola, Chief Financial Officer.

TeoOttolaCFO Konecranes

SEB Annual Review 2016 17

Customer activities

With customer needs in focus andwith the bank’s vision to provideworld-class service, SEB is takinga number of initiatives to improvecustomer experience.

During 2016, SEB capitalised on the poten-tial of digital technology and developedand launched new services aimed at allcustomer segments.

Thiswork is being conducted at a fastpace,withmany small deliveries that aredeveloped in close collaborationwithcustomers. Some solutions are developedby SEB,while others rely on partnershipswith other service providers.

Customer satisfaction pilotToput the customer experience front andcentre, SEB is having sevenbranchofficestestwhat happens if the operations are solelyevaluated on customer satisfactionwithoutmonitoring financial key ratios. The pilot isshowingpromising results and the staff isfindingnewways to provide the best possi-ble customer service.

New customerservices

Virtual trainee incustomer service

The virtual trainee Aida has begunworking at SEB’s customer service. For awhile now she has been answering ques-tions, assisting customerswith simplebankingmatters and she has learnt tospeak Swedish. Her “recruitment” isone ofmany tests SEB is doing todevelop the customer experience andoffermore efficient banking serviceswith the help of artificial intelligence.

Aida is at the cutting edge of techno-logy. In contrast to so-called chatbots,Aida can learn to understand, conducta dialogue and perform tasks just like ahuman.

SEB is the first bank in Europe to usethis type of artificial intelligence in itscustomer service operations.

World-class custodyfunctionality

In 2016, SEB’s first customers gainedaccess to the bank’s newglobal custodyaccount services platform that has beendeveloped in partnershipwith the inves-tor services company BrownBrothersHarriman (BBH). The newplatformoffers improved solutions formanagingcustomers’mutual funds, collateral,corporate events, cashmanagement,currency trading andmore.

SEB handles the customer relation-ship and interface,while BBHprovidesthe technical platform and takes re-sponsibility for certain administrativeprocesses. Through this partnershipSEB gains access to cutting-edge tech-nologywhile retaining responsibilityfor the customer relationship.

The bank forentrepreneurs

Through the 2017 launch of Greenhouse,a broader service offering, SEBwill takethe next step toward being a strongerbusiness partner for growth companies.

The newoffering is based on in-depthinterviewswith high-growth enterprisesabout challenges and problems in theirday-to-day operations. Tomeet theirneeds, SEB offers its entire pallet ofexpertise – frommergers and acquisi-tions (M&A) to investment banking andcorporate and family law. In cooperationwith external partners SEB also offersservices relating to staffing and contrac-tualmatters aswell as auditing, legalcounsel, consulting and advisers.

In theBaltic countries SEB is conduct-ing joint innovation initiativeswithcustomers. This strengthens thepartner-shipswith entrepreneurs.

SEB Annual Review 201618

New customer services

The branch office evolvesThe personal relationwith customers isimportant and SEBwill always have branchoffices. However, in aworldwhere bankingtransactions are increasingly digital, whatwill the future branch office look like andwhat serviceswill be provided? Part of theanswer can be found at a new type of branchoffice located in Stockholm, aswell as at theinnovation centres for small andmedium-sized companies that SEB has established inthe Baltic countries.

Initiatives like these are away of develop-ingmeeting places in close cooperationwith customers.With the help of customerfeedback, SEB strives to design new typesof open and invitingmeeting places.

First in pensions market withdigital advisory meetingsSEBwas the first player in the Swedishoccupational pensionsmarket to offercustomers a fully digital advisorymeeting.The process is initiatedwith customerscompleting aweb-based formwith theinformation needed to conduct an analysisof their current status. During theweb-based advisorymeeting, where the twoparties share screens, customers can seehow the outcomewould be affected byvarious decisions and can set goals fortheir financial security. The customerscan then sign their choices digitally.

This digitalised process allows SEB tooffer personal advice remotely nomatterwhere the customer is located. This hasincreased the bank’s accessibilitywhilestreamlining its advisorywork.

New convenient interfacefor large corporate customersSEB has upgraded its cashmanagementfunctionality so that customers get a betterviewof not only their total cash balances –in SEB and other banks– but also of theirmost advanced global liquidity solutions.Accessibility has been improved so thatcustomers canmonitor and act on theiraccounts also viamobile devices.

» I appreciate SEB’ opennessto entrepreneurship andinnovation. «

Meet one of our medium-sizedcorporate customers

With seven new pharmacies, sales growingnearly three times faster than themarket andalmost doubled earnings (EBITDA), KatreKõvask, CEO of the Estonian pharmacy chainSüdameapteek, can look back on a good year.

An open, flexible and close relationshipwith the company’s financial partner SEB is animportant part of the continued expansion.

“Bank relations is about building a partner-ship, working together and pulling in thesame direction. It is based on both partiesbeing open and transparent. I appreciate theopenness to promote entrepreneurship andinnovation that the bank stands for”, shesays.

Katre KõvaskCEO Südameapteek

SEB Annual Review 2016 19

New customer services

Digital processes improve customerexperience and free up resourcesTo gain the full potential of the technologi-cal development and, based on a customerperspective, create new, automated flows, itis often necessary to rethink processes fromscratch. SEB has identified a number of keyprocesses inwhich the entire chain fromcustomer transaction to IT system is beingredesigned.

Customers buying a home is one example.SEB has launched its first, concrete step inthis area in the formof a newdigital func-tion that helps customers determinewhichhome they can afford. Another example isthe annual credit reviews of corporate busi-ness inwhich the potential savingsmay beas high as three to fourman-weeks ofworkper year per customer.

Investing in innovative solutionsSEB invests in high-tech companieswithinnovative solutions that could be relevantfor the bank and its customers.

In 2016 SEB invested in the fintechcompanyTink,which has developed an app

that helps users get a better overviewoftheir income and expenses. Its functionalityis being integrated into SEB’smobile app.SEB also invested in Coinify, a companywith a platform for blockchain payments,and in the companyNow Interact, whichuses artificial intelligence andmachinelearning to predict customer behaviour.Another example is Leasify, a companywitha digital solution for leasing arrangementsaimed at companies.

The potential of blockchainBlockchain technology,whichwasoriginally developed for the Bitcoincryptocurrency, is believed to havemajorpotential in streamlining payment flowsby removing the need for intermediaries.SEB is participating in several blockchaininitiatives. In addition to its investmentin Coinify, the bank isworkingwith thefintech companyRipple to use its block-chain solution for payments.

Innovationbenefits customers

Promoting internal innovation

SEB encourages a culture for change andinnovation. One such initiative is SEB’sInnovation Lab,where employees pres-ent their ideas live to a jury consistingof seniormanagers. If approved, theemployee can develop and prototypethe idea during a set period of time.

Several ideas have already come tofruition, such as SEB’s virtual openhouses,which are offered in colla-borationwith the realtor Husman&Hagberg. Another example is a signifi-cantly streamlined process forwelcom-ing new customers using digital tools.

»A bank that I cantrust is a great asset. «

Meet one of our private customers

The love of boats and birds has been a themethroughout his life. A few years ago his deci-sion – at 89 years of age – to buy a new sail-boat, specially designed for solo trips, caughtmedia attention. 54 years ago, the same boatinterest made Anders Parrow a customer ofSEB and he has been faithful to the bank eversince.

Anders likes to visit the bank andmeetwith his adviser, but also appreciates theinternet bank and themobile bank app.“I can’t imagine banking without them”,he says. Anders regularly takes part ofSEB’s market analysis as input to his port-folio management.

Anders Parrow

20

Benefits of innovation

The financial sector has a largeindirect influence on the long-termsustainable development. Stake-holders have high expectations inthis area and SEB has raised itsambition and aims to be a rolemodel within sustainability.

Green financingThe climate challenge requiresmajor invest-ments in energy supply, the transport sectorand sustainable urban development. SEBcontributes by assisting customerswithfinancing of green investments in infra-structure and renewable energy, includinghydro power,wind power and solar energy.

SEB participated in the creation of theworld’s first green bond,whichwas issuedby theWorld Bank in 2008. Since then, theglobalmarket for green bonds has gainedmomentumand grown sharply. In 2016,green bondswere issued to a value of almostUSD95 billion – capital that has thus beenchannelled to quality assured green proj-ects. SEBwas the fourth largest arranger/underwriter globally, with amarket shareof 4.4 per cent of this volume.

SEB applies policies that limit lending tocompanies in sectors such as fossil fuels,

mining andmetals. SEB does not providenewfinancing of coalmining and coalpowerplants. The bank’s sector policies andposition statements form a valuable base indialogueswith corporate customers andhelp increase awareness about sustainabil-ity aspects in various decisions.

Responsible investmentsCustomers increasingly expect that SEBwillmanage their assets in a responsiblemanner. For a number of years the bank hasmade a concerted effort to take sustainabil-ity into account in all investment processes,based on the conviction that this leads tobetter investments and higher returns forcustomers. At year-end SEBmanaged assetsat a total of SEK584billion (517) in accor-dancewith the Principles of ResponsibleInvestments (PRI).

SEB excludes investments in particularsectors and areas, such as controversialweapons and nuclear arms, aswell as incompanies that derivemore than 20per cent

of their sales from coal production. On theother hand, SEB is alsoworking to a greaterextentwith positive selectionwhere portfo-liomanagers prioritise companies thatworkaccording to sustainable principles.

In 2016 SEB entered into a newpartner-shipwithHermes InvestmentManagement,creating an opportunity to increase thenumber of sustainability dialogueswithcompanies outside theNordic region.

Measurement of the carbon footprint offunds has been expanded and now includesmost of the bank’s equity funds.

Dow Jones sustainability indexSEB has high ambitions in its sustainabilitywork and aims to be a rolemodel in thefinancial industry in this area. A sign thatthe efforts are paying offwas that in 2016SEBmet the strict criteria for inclusion andwas – as the only bank in theNordic coun-tries – accepted as part of theDow Jonessustainability index.

Customers expectresponsible services

Microfinancing

SEBwas the first bank in Sweden tolaunchmicrofinance funds directed atinstitutional investors. The aim is to offeran attractive investment opportunitywitha distinct social character. The fund assetscreate a ripple effectwhen borrowersinvest or use other business services. Thisway jobs are created leading to growth indeveloping countries.

The bank’s fourmicrofinance fundshave a combined value ofmore thanSEK4billion,which reachesmore than17million entrepreneurs in developingcountries viamicrofinance institutions.

SEB’s position statementsand sector policies

Readmore about SEB’s policies atsebgroup.com/about-seb/who-we-are

SEB reports its sustainability work inaccordance with GRIG4. For furtherinformation, see sebgroup.com

SEB Annual Review 2016 21

Responsible services

For the second year in a row, 3,000 employees gathered in Stockholm to be involved and inspired by theinitiatives taken to reach SEB’s long-term vision. Themeeting was broadcast to local events in 20 countries.

In a changing world, SEB is impacted by the rapid pace oftechnological development, evolving customer behaviours,and expectations on future employees. The bank’s role insociety is becoming increasingly important forSEB’s attraction as an employer.

SEB’semployees

Employee statistics2016 2015 2014

Number ofemployees, average 16,260 16,599 16,742

Sweden 8,222 8,320 8,352

Other Nordic countries 1,369 1,404 1,411

Baltic countries 5,125 5,118 5,100

Number of employeesat year-end 16,087 16,432 16,767

Average number offull-time equivalents 15,279 15,605 15,714

Employeeturnover,% 10.7 9.0 8,9

Sick leave,%(in Sweden) 3.0 2.8 2.4

Femalemanagers,% 46 44 43

Insight

Employeeengagement 77 79 75

Performanceexcellence 81 80 78

Committed employeeswith a servicemindset, who collaborate andwhowant to develop new competences,is a key success factor.

SEB’s Insight employee survey for 2016confirms that there is strong support forthe bank’s vision and strong commitmentamong employees to participate andchange. Employee engagement scoresremained high in 2016 – clearly higher thanfor peer companies – as did the scores forperformance excellence,which increasedfor the fourth consecutive year.

Focus of improvementmeasures is tomore clearly take the customer-first perspec-tive, further improve internal collaboration,and to simplify processes.

Activities in order to develop these areashave includedworkshops focusing on clari-fying the connection between employees’own values and the bank’s. Employees havegained opportunities to reflect on, andformulate, their own values, and thereafteralign them to the bank’s joint values.

Managing changeand newways of workingThe employees’ and the organisation’s abil-ity to collaborate andmanage change arecrucial for the future. In SEB this is done inan environment characterised by involve-ment and innovation.

Asanexample, SEB isdevelopingnewwaysofworking built on an iterative approach inthe design of services. Thismeans cross-functional teamsmapping customer jour-neys, based on customer needs and feedbackloops, before prototypes of new solutionsare launched to the customers. The newagileways ofworking are aimed at drawingfull benefit of digitalisation and providingan even better customer experience.

The agileways ofworking have also beenadopted in SEB’s IT operations. Develop-ment and deliveries are being conducted insmall steps rather than in large projects overa longer period of time.

In 2016, individually adapted agile train-ing courseswere held formore than 2,000employees, a strategic initiative to createfavourable conditions to quickly andsuccessfully adaptways ofworking tothe changing needs.

Planning for future competencesThe digital transformation drives the needto plan for future competences in the longterm. SEB isworking throughout the bankto analyse and identify needs based onselected parameters. Competence needs areincluded as an integral part of the businessplanning.

Areas inwhich needs are clearly risinginclude digital design, data analysis and IT.The bank has broadened its recruitment tosearch for these skills via new channels andarenas, not only among individualswith abackground in finance and business admin-istration. Employees’ roleswill be expandedin order to be able tomeet customer needsfor comprehensive service. Inmany casesthis requires employees towork in newways.

LeadershipSEB has a long tradition of identifyingand developing leaders at an early stage.Constant changes in the business environ-ment are putting ever-growing demands onmanagers,whomust inspire, serve as rolemodels and establish conditions so thatemployees and teams can develop thebusiness in the bestway possible.

During the year, Grow2Leadwas devel-oped, a digital portal for employees inter-ested in a future role as a leader. The portalprovides inspiration and developmentopportunities, and can help employeesdecide if amanager role is a suitable careerpath.

For existingmanagers, the bank has globalprogrammes that offer opportunities todevelop their leadership qualities both asindividuals and as teammembers.

A controversial taxFor the financial sector in Sweden, a 15 percent tax based on grosswages is beingconsidered for implementation in 2018.The total estimated financial effect on SEBof the proposal under discussion is aroundSEK700mper year. According to a reportfrom the Swedish Bankers’ Association, asmany as 16,000 jobswould be threatenedif these planswere in fact carried out.

SEB Annual Review 2016 23

SEB’s employees

»My goal is to build high-performing teams that deliverstellar results. This requires satisfied andmotivatedemployees. There is thus no conflict between employeesatisfaction and results – they are symbiotic.

I want my leadership to be characterised by simplicity,clarity and communication. At the same time, I want tobe transparent and sharemy insights on the total picture.In doing so, most decisions will be natural for employees. «

Anders Lundström,manager within asset advisory services,was named Leader of the Year (“Årets ledartröja”) by theFinancial Sector Union in SEB.

Anders Lundström–Leader of the year 2016

health index based on questions in theInsight employee survey. This is the firstglobal tool formeasuringwork environ-ment and health at both the divisional andcountry levels.

In 2017, SEB’s newofficeswill be inaugu-rated at Arenastaden outside Stockholm,where 4,500 employeeswill be gathered. Indesigning theworkplace, strong focuswasput on enabling a positivework environ-mentwithmodern and functionalworkspaces, large common areas, project roomsand quiet areas, an extensive fitness facility,and healthy food in own restaurants.

Learning opportunitiesAt SEB, continuous learning is a vitalprerequisite for the ability to adapt to newcircumstances. The bank offers awidearray of training courses and, via a portal,employees can get an overviewof the entireoffering – including training that is specificfor SEB aswell as training offered by exter-nal providers – includingmethods andeffective tools to facilitate learning. In all,more than 600 courses are offered.

Increasing diversitySEB is convinced that diversity and inclu-sion among its people help the bank achievegreater success over time.

All employees are to be offered equalopportunities to develop individually,regardless of their gender, ethnicity, age,sexual orientation or faith. SEB strives toachieve an even gender balance at everylevelwithin the organisation and toincrease the share of employeeswith aninternational background.

The bank isworking actively, both interms of structures and processes and inspecific initiatives, to increase the numberofwomen in higher operative positions andin senior leader roles.

In 2016, 46 per cent (44) of SEB’smanag-erswerewomen. Among senior executivesthis sharewas 31 per cent (27).

Health andwork environmentEnsuring employee longevity is becomingincreasingly important in pacewith anageing population and the possibility of ahigher retirement age. SEB isworking longterm and preventively to offer a safe andsoundworkplace in an effort to ensureemployeewell-being and a soundwork/lifebalance.

The focus of the bank’swork environ-ment initiatives is on stress, workloads andrisk identification. In Sweden, in 2016, thebank increased its support tomanagerswithemployees on sick leave. They are offeredtelephone support fromnurses at companyhealth services and rehabilitation special-istswho are experienced in assessing suit-able paths for a rapid recovery and return towork. In Sweden, the SEB sick-leaveremains low, at 3 per cent, comparedwithother industries and the financial sector.

During 2016, SEB introduced a global

Customers firstWe put our customers’ needsfirst, always seeking tounderstand how to deliverreal value.

CollaborationWe achieve moreworking together.

SEB’scorevalues

CommitmentWe are personally dedi-cated to the success ofour customers and areaccountable for our actions.

SimplicityWe strive to simplify whatis complex.

SEB Annual Review 201624

SEB’s employees

SEB’s core values

SEB’s core values serve as the foundation for the bank’sways ofworking and culture,and in combinationwith the bank’s vision – to deliverworld-class service to our custom-ers – they serve tomotivate and inspire employees,managers and the organisation as awhole. These values are described in SEB’s Code of Conduct, which provides guidanceon ethicalmatters for all employees.Read the Code of Conduct at sebgroup.com

SEB plays an active role in thecommunities in which the bankoperates by promoting entrepre-neurship and enterprise as wellas supporting young people.

SEB shares the conviction that business andindustry have a key role to play inmeetingthe global sustainable development goalsthatwere adopted by theUN’s 193memberstates in 2015. Themost important contri-butions come from the bank’s core busi-nesses,where green financing, sustainableinvestment and combating financial crimeare included. But SEB is also activelyinvolved in communitymatters through itsmany partnerships for entrepreneurshipand youth initiatives.

Volunteers raising young people’sknowledge of economicsSEB partnerswith organisations thatworkto include youths in social development byraising their knowledge of personal finance.In the three Baltic countries, for the past fewyears SEB has been participating in nation-wide campaigns to increase financial liter-acy among young people. In 2016 volun-teers fromSEB visitedmore than 230schools in an effort to give children funda-mental skills in personal finance andeconomic planning.

In Sweden, too, the bank isworking activelyto increase understanding of economicsamong young people.Within the frame-work of SEB’s partnershipwithMentorSweden, teams of employees participate inthe professionalmentor programme,consisting of a series of threeworkshops atwhich the bank gives young people adviceon day-to-day finances, explains businessnorms and provides advice on how to applyfor jobs. In 2016 eight such programmeswere carried out at schools in Sweden’smajormetropolitan areas. Volunteers fromSEB also serve as coaches and jurymembersin theDreamChallenge initiative,whereyoung people get help on formulating aplan for their dream careers.

Summer camp forfuture entrepreneursSEBworkswith organisations that are dedi-cated to spurring interest and inspirationamong youths aswell as newly arrivedimmigrants in entrepreneurship and enter-prise. These include Junior Achievement,PrinceDaniel’s Fellowship, SIMENext,Enterprise Agency and the InternationalEntrepreneur Association in Sweden.

In 2016 the bank became involved in anewly started summer camp for teenagedaspiring entrepreneurs. In cooperationwithSIMENext, some 20 youthswere offeredspots at the camp for oneweek of intensedrilling in digital entrepreneurship.

Social entrepreneursgain insight into doing businessIn 2016, a partnershipwas startedwithInkludera Invest, an umbrella organisationfor social entrepreneurs. The commondenominator for these is that theyworkwithout a profitmotive to create a betterworld. However, they can still benefitgreatly from tools such as business plans,budgets, and earnings analyses to developtheir operations.

Togetherwith Inkludera Invest, SEBarranged a basic course in business admin-istration and invited social entrepreneursto share insights around the conditionsfor doing business.

Investing incommunities

SEB supports entrepreneurs– from business concept tothriving companies

Rolemodels

Incubationand growth

Start-ups

Businessconcept

Inspiration

• Junior Achievement • Prins Daniels Fellowship • SIME Next

• Venture Cup • Business Challenge

• NyföretagarCentrum (Enterprise Agencies) • Interna-tional Enterpreneur Association in Sweden

• Sting • Connect • SUP46 • SEB Innovation Forum• YEoS •Minc • G-Lab21 • BASE10 • Inkludera Invest

• Entrepreneur of the year • Guldklubban

SEB Annual Review 2016 25

Investing in communities

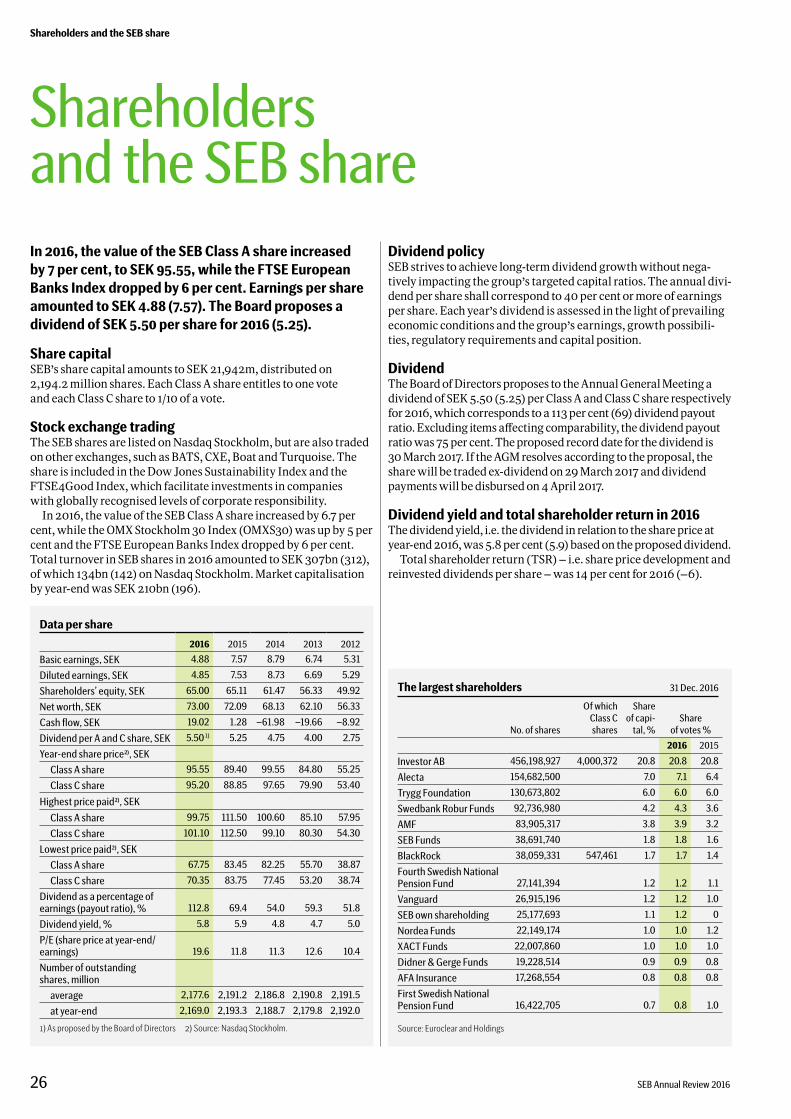

In 2016, the value of the SEB Class A share increasedby 7 per cent, to SEK 95.55, while the FTSE EuropeanBanks Index dropped by 6 per cent. Earnings per shareamounted to SEK 4.88 (7.57). The Board proposes adividend of SEK 5.50 per share for 2016 (5.25).

Share capitalSEB’s share capital amounts to SEK21,942m, distributed on2,194.2million shares. Each Class A share entitles to one voteand each Class C share to 1/10 of a vote.

Stock exchange tradingThe SEB shares are listed onNasdaq Stockholm, but are also tradedon other exchanges, such as BATS, CXE, Boat and Turquoise. Theshare is included in theDow Jones Sustainability Index and theFTSE4Good Index,which facilitate investments in companieswith globally recognised levels of corporate responsibility.

In 2016, the value of the SEBClass A share increased by 6.7 percent, while theOMXStockholm30 Index (OMXS30)was up by 5 percent and the FTSEEuropean Banks Index dropped by 6 per cent.Total turnover in SEB shares in 2016 amounted to SEK 307bn (312),ofwhich 134bn (142) onNasdaq Stockholm.Market capitalisationby year-endwas SEK210bn (196).

Dividend policySEB strives to achieve long-termdividend growthwithout nega-tively impacting the group’s targeted capital ratios. The annual divi-dend per share shall correspond to 40 per cent ormore of earningsper share. Each year’s dividend is assessed in the light of prevailingeconomic conditions and the group’s earnings, growth possibili-ties, regulatory requirements and capital position.

DividendTheBoardofDirectors proposes to theAnnualGeneralMeeting adividendof SEK5.50 (5.25) perClassAandClass C share respectivelyfor 2016,which corresponds to a 113 per cent (69) dividendpayoutratio. Excluding items affecting comparability, the dividendpayoutratiowas 75per cent. Theproposed recorddate for the dividend is30March2017. If theAGMresolves according to the proposal, thesharewill be traded ex-dividendon29March2017 anddividendpaymentswill be disbursedon4April 2017.

Dividend yield and total shareholder return in 2016Thedividendyield, i.e. thedividend in relation to the shareprice atyear-end2016,was5.8per cent (5.9) basedon theproposeddividend.

Total shareholder return (TSR) – i.e. share price development andreinvested dividends per share –was 14 per cent for 2016 (–6).

Shareholdersand the SEB share

The largest shareholders 31 Dec. 2016

No. of shares

Of whichClass Cshares

Shareof capi-tal,%

Shareof votes%

2016 2015

Investor AB 456,198,927 4,000,372 20.8 20.8 20.8

Alecta 154,682,500 7.0 7.1 6.4

Trygg Foundation 130,673,802 6.0 6.0 6.0

Swedbank Robur Funds 92,736,980 4.2 4.3 3.6

AMF 83,905,317 3.8 3.9 3.2

SEB Funds 38,691,740 1.8 1.8 1.6

BlackRock 38,059,331 547,461 1.7 1.7 1.4

Fourth Swedish NationalPension Fund 27,141,394 1.2 1.2 1.1

Vanguard 26,915,196 1.2 1.2 1.0

SEB own shareholding 25,177,693 1.1 1.2 0

Nordea Funds 22,149,174 1.0 1.0 1.2

XACT Funds 22,007,860 1.0 1.0 1.0

Didner & Gerge Funds 19,228,514 0.9 0.9 0.8

AFA Insurance 17,268,554 0.8 0.8 0.8

First Swedish NationalPension Fund 16,422,705 0.7 0.8 1.0

Source: Euroclear and Holdings

Data per share

2016 2015 2014 2013 2012

Basic earnings, SEK 4.88 7.57 8.79 6.74 5.31

Diluted earnings, SEK 4.85 7.53 8.73 6.69 5.29

Shareholders’ equity, SEK 65.00 65.11 61.47 56.33 49.92

Net worth, SEK 73.00 72.09 68.13 62.10 56.33

Cash flow, SEK 19.02 1.28 –61.98 –19.66 –8.92

Dividend per A and C share, SEK 5.50 1) 5.25 4.75 4.00 2.75

Year-end share price2), SEK

Class A share 95.55 89.40 99.55 84.80 55.25

Class C share 95.20 88.85 97.65 79.90 53.40

Highest price paid2), SEK

Class A share 99.75 111.50 100.60 85.10 57.95

Class C share 101.10 112.50 99.10 80.30 54.30

Lowest price paid2), SEK

Class A share 67.75 83.45 82.25 55.70 38.87

Class C share 70.35 83.75 77.45 53.20 38.74

Dividend as a percentage ofearnings (payout ratio),% 112.8 69.4 54.0 59.3 51.8

Dividend yield,% 5.8 5.9 4.8 4.7 5.0

P/E (share price at year-end/earnings) 19.6 11.8 11.3 12.6 10.4

Number of outstandingshares, million

average 2,177.6 2,191.2 2,186.8 2,190.8 2,191.5

at year-end 2,169.0 2,193.3 2,188.7 2,179.8 2,192.0

1) As proposed by the Board of Directors 2) Source: Nasdaq Stockholm.

SEB Annual Review 201626

Shareholders and the SEB share

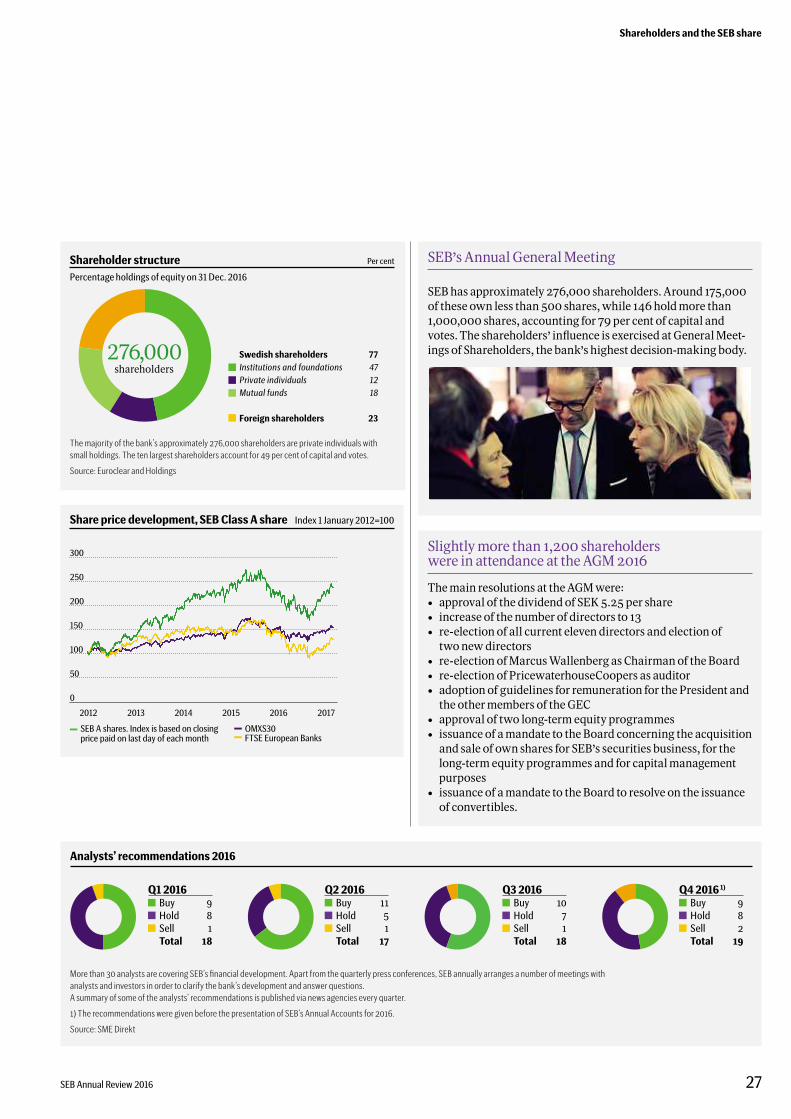

SEB’s Annual GeneralMeeting

SEB has approximately 276,000 shareholders. Around 175,000of these own less than 500 shares, while 146 holdmore than1,000,000 shares, accounting for 79 per cent of capital andvotes. The shareholders’ influence is exercised at GeneralMeet-ings of Shareholders, the bank’s highest decision-making body.

Slightlymore than 1,200 shareholderswere in attendance at the AGM2016

Themain resolutions at the AGMwere:• approval of the dividend of SEK5.25 per share• increase of the number of directors to 13• re-election of all current eleven directors and election of

two newdirectors• re-election ofMarcusWallenberg as Chairman of the Board• re-election of PricewaterhouseCoopers as auditor• adoption of guidelines for remuneration for the President and

the othermembers of theGEC• approval of two long-term equity programmes• issuance of amandate to the Board concerning the acquisition

and sale of own shares for SEB’s securities business, for thelong-term equity programmes and for capitalmanagementpurposes

• issuance of amandate to the Board to resolve on the issuanceof convertibles.

Analysts’ recommendations 2016

More than 30 analysts are covering SEB’s financial development. Apart from the quarterly press conferences, SEB annually arranges a number of meetings withanalysts and investors in order to clarify the bank’s development and answer questions.A summary of some of the analysts’ recommendations is published via news agencies every quarter.

1) The recommendations were given before the presentation of SEB’s Annual Accounts for 2016.

Source: SME Direkt

Q2 2016Buy 11Hold 5Sell 1Total 17

Q4 2016 1)

Buy 9Hold 8Sell 2Total 19

Q1 2016Buy 9Hold 8Sell 1Total 18

Q3 2016Buy 10Hold 7Sell 1Total 18

Shareholder structure Per cent

Percentage holdings of equity on 31 Dec. 2016

Swedish shareholders 77

Institutions and foundations 47Private individuals 12Mutual funds 18

Foreign shareholders 23

276,000shareholders

The majority of the bank’s approximately 276,000 shareholders are private individuals withsmall holdings. The ten largest shareholders account for 49 per cent of capital and votes.

Source: Euroclear and Holdings

Share price development, SEB Class A share Index 1 January 2012=100

OMXS30SEB A shares. Index is based on closing

price paid on last day of each month FTSE European Banks

2012 2013 2014 2015 2016 2017

0

50

100

250

200

150

300

SEB Annual Review 2016 27

Shareholders and the SEB share

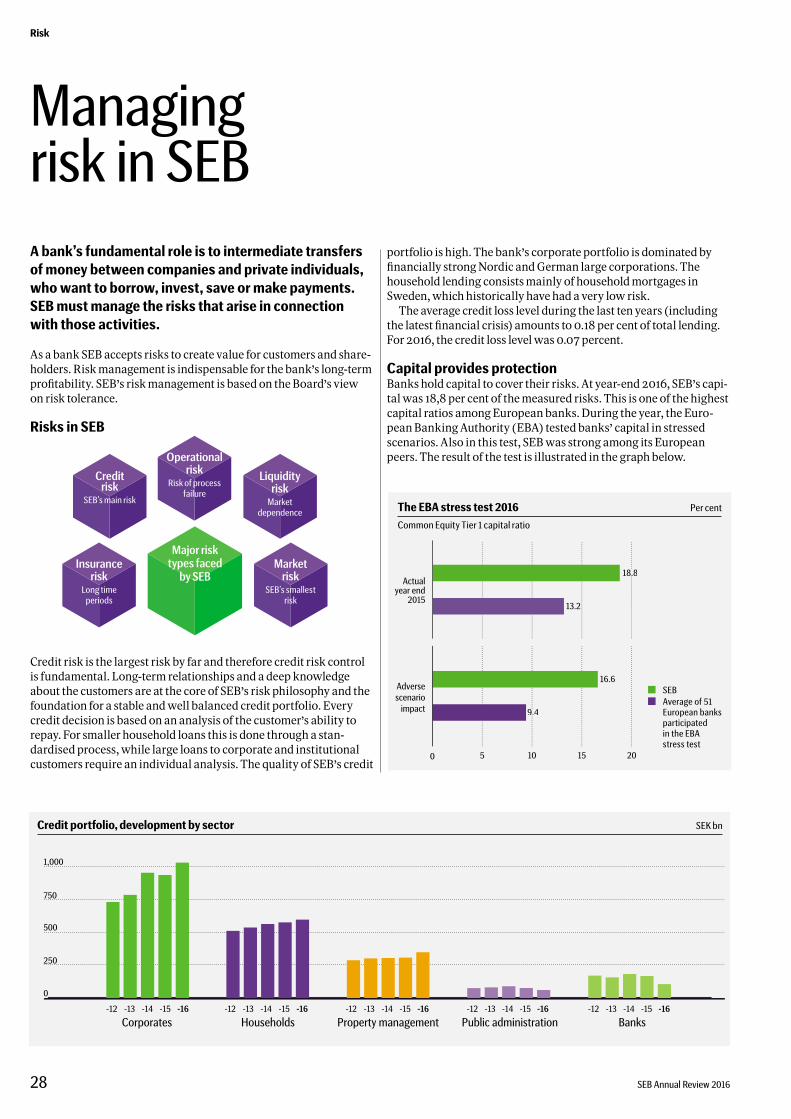

A bank’s fundamental role is to intermediate transfersof money between companies and private individuals,whowant to borrow, invest, save or make payments.SEBmust manage the risks that arise in connectionwith those activities.