Embed Size (px)

Citation preview

1 | P a g e

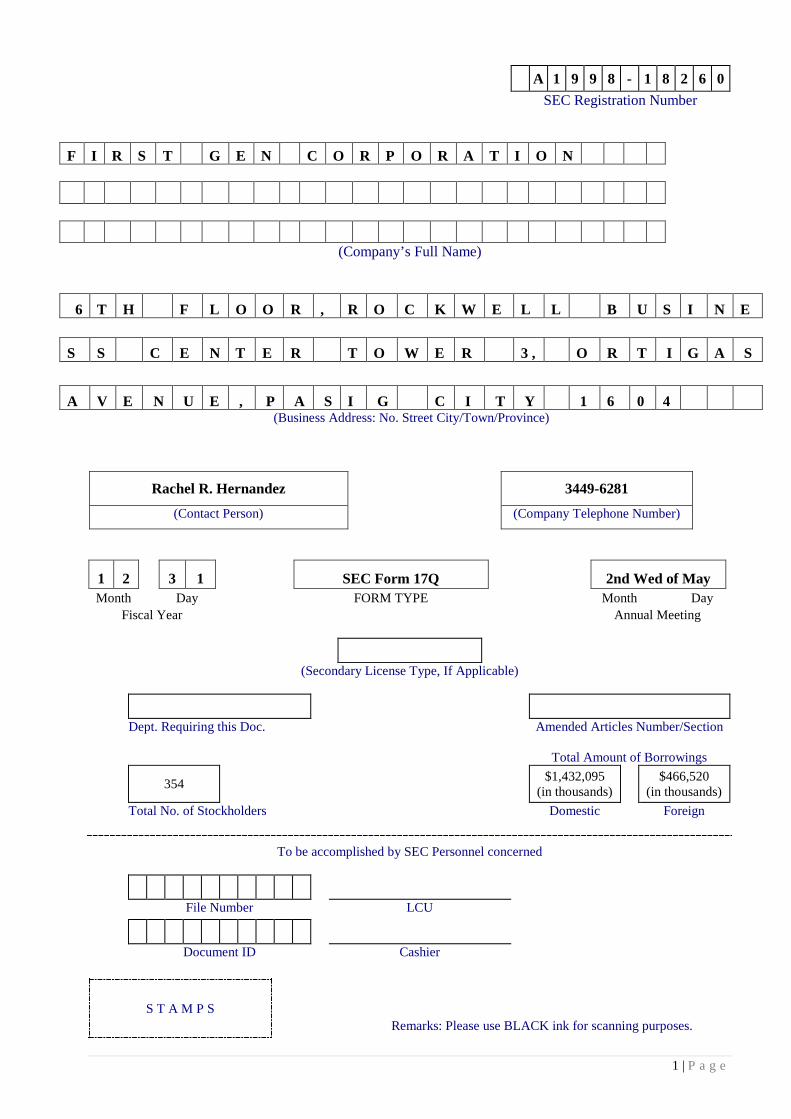

A 1 9 9 8 - 1 8 2 6 0 SEC Registration Number

F I R S T G E N C O R P O R A T I O N

(Company’s Full Name)

6 T H F L O O R , R O C K W E L L B U S I N E

S S C E N T E R T O W E R 3 , O R T I G A S

A V E N U E , P A S I G C I T Y 1 6 0 4 (Business Address: No. Street City/Town/Province)

Rachel R. Hernandez 3449-6281 (Contact Person) (Company Telephone Number)

1 2 3 1 SEC Form 17Q 2nd Wed of May Month Day FORM TYPE Month Day

Fiscal Year Annual Meeting

(Secondary License Type, If Applicable)

Dept. Requiring this Doc. Amended Articles Number/Section

Total Amount of Borrowings

354 $1,432,095 (in thousands)

$466,520 (in thousands)

Total No. of Stockholders Domestic Foreign

To be accomplished by SEC Personnel concerned

File Number LCU

Document ID Cashier

S T A M P S Remarks: Please use BLACK ink for scanning purposes.

1 | P a g e

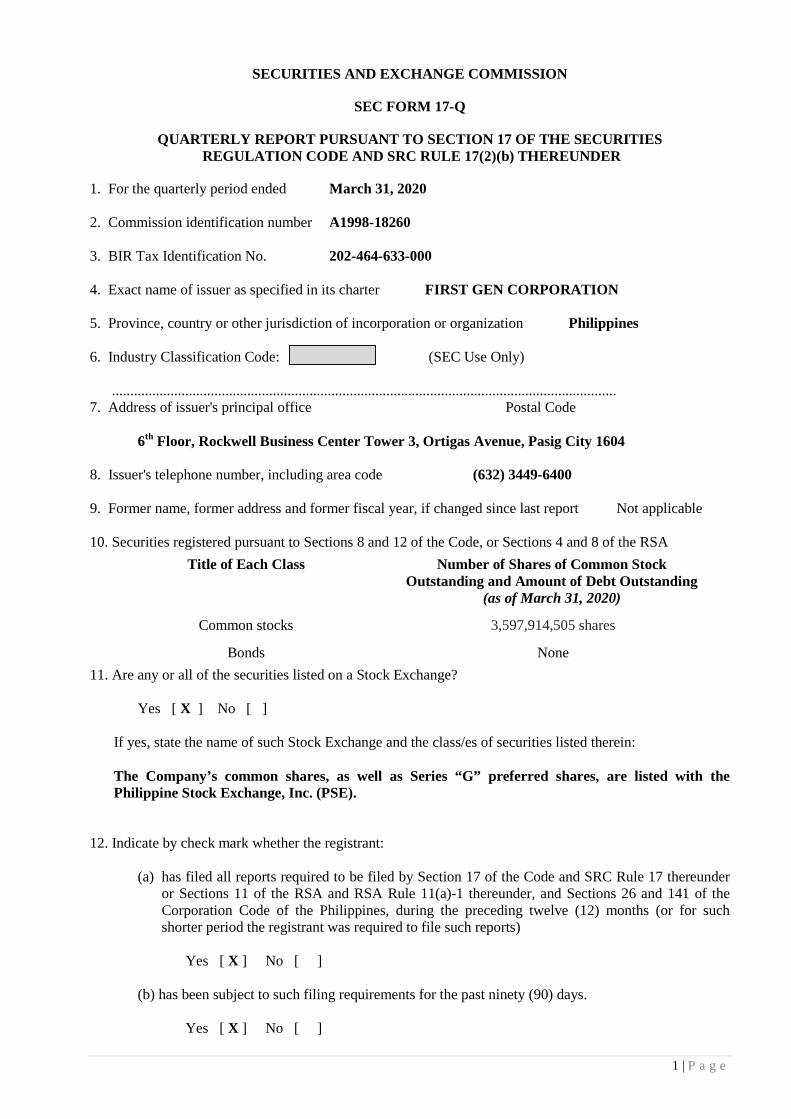

SECURITIES AND EXCHANGE COMMISSION

SEC FORM 17-Q

QUARTERLY REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SRC RULE 17(2)(b) THEREUNDER

1. For the quarterly period ended March 31, 2020 2. Commission identification number A1998-18260 3. BIR Tax Identification No. 202-464-633-000 4. Exact name of issuer as specified in its charter FIRST GEN CORPORATION 5. Province, country or other jurisdiction of incorporation or organization Philippines 6. Industry Classification Code: (SEC Use Only) .......................................................................................................................................... 7. Address of issuer's principal office Postal Code

6th Floor, Rockwell Business Center Tower 3, Ortigas Avenue, Pasig City 1604 8. Issuer's telephone number, including area code (632) 3449-6400 9. Former name, former address and former fiscal year, if changed since last report Not applicable 10. Securities registered pursuant to Sections 8 and 12 of the Code, or Sections 4 and 8 of the RSA

Title of Each Class Number of Shares of Common Stock Outstanding and Amount of Debt Outstanding

(as of March 31, 2020)

Common stocks 3,597,914,505 shares

Bonds None 11. Are any or all of the securities listed on a Stock Exchange? Yes [ X ] No [ ]

If yes, state the name of such Stock Exchange and the class/es of securities listed therein:

The Company’s common shares, as well as Series “G” preferred shares, are listed with the Philippine Stock Exchange, Inc. (PSE).

12. Indicate by check mark whether the registrant:

(a) has filed all reports required to be filed by Section 17 of the Code and SRC Rule 17 thereunder or Sections 11 of the RSA and RSA Rule 11(a)-1 thereunder, and Sections 26 and 141 of the Corporation Code of the Philippines, during the preceding twelve (12) months (or for such shorter period the registrant was required to file such reports)

Yes [ X ] No [ ]

(b) has been subject to such filing requirements for the past ninety (90) days. Yes [ X ] No [ ]

1 | P a g e

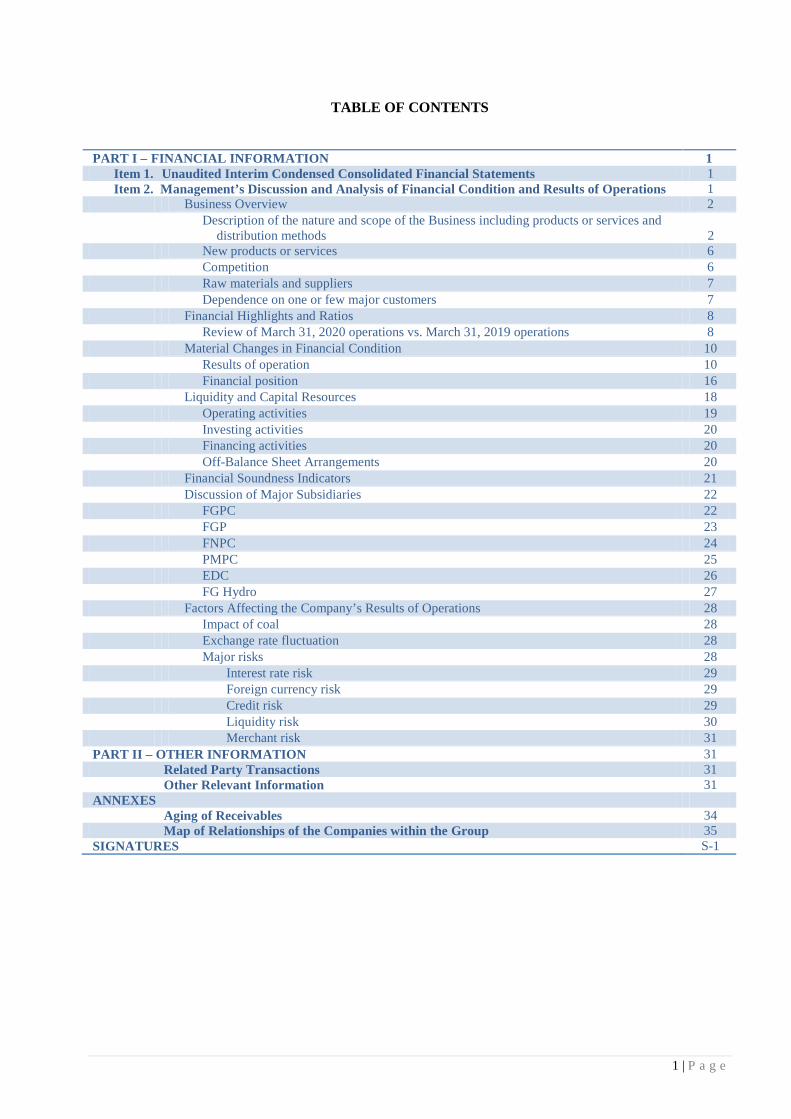

TABLE OF CONTENTS PART I – FINANCIAL INFORMATION 1

Item 1. Unaudited Interim Condensed Consolidated Financial Statements 1 Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations 1

Business Overview 2 Description of the nature and scope of the Business including products or services and

distribution methods

2 New products or services 6 Competition 6 Raw materials and suppliers 7 Dependence on one or few major customers 7 Financial Highlights and Ratios 8 Review of March 31, 2020 operations vs. March 31, 2019 operations 8 Material Changes in Financial Condition 10 Results of operation 10 Financial position 16 Liquidity and Capital Resources 18 Operating activities 19 Investing activities 20 Financing activities 20 Off-Balance Sheet Arrangements 20 Financial Soundness Indicators 21 Discussion of Major Subsidiaries 22 FGPC 22 FGP 23 FNPC 24 PMPC 25 EDC 26 FG Hydro 27 Factors Affecting the Company’s Results of Operations 28 Impact of coal 28 Exchange rate fluctuation 28 Major risks 28 Interest rate risk 29 Foreign currency risk 29 Credit risk 29 Liquidity risk 30 Merchant risk 31 PART II – OTHER INFORMATION 31

Related Party Transactions 31 Other Relevant Information 31

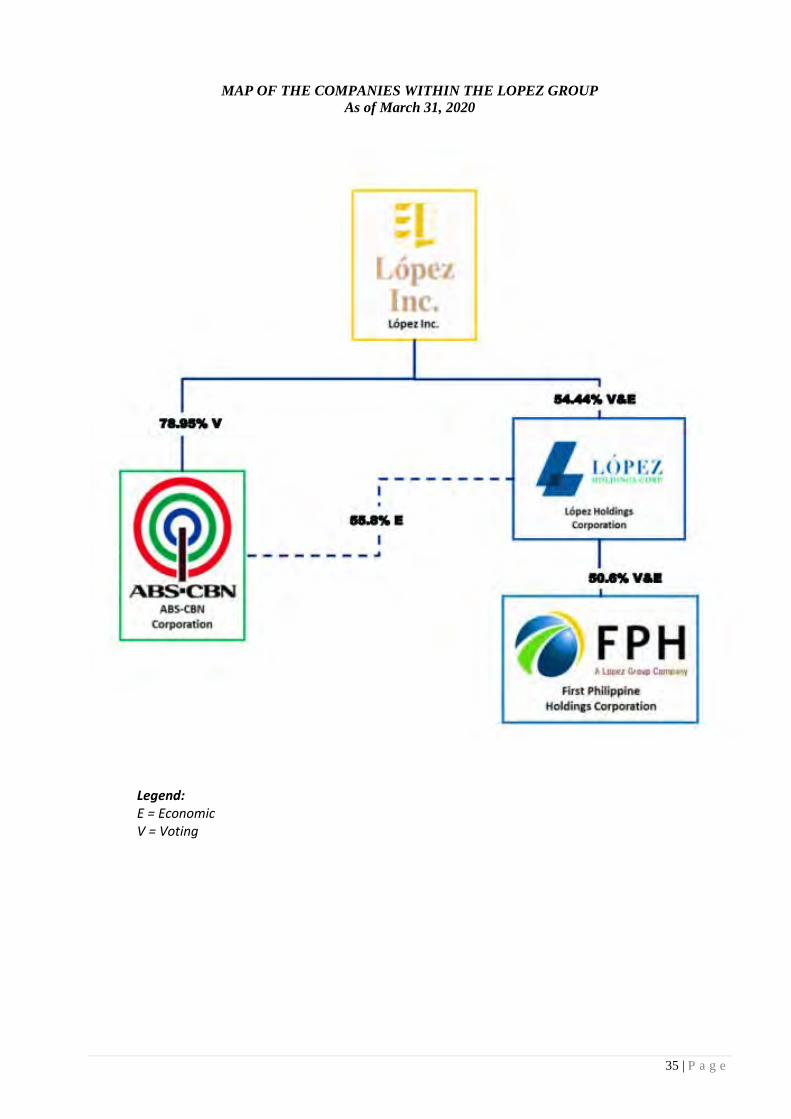

ANNEXES Aging of Receivables 34 Map of Relationships of the Companies within the Group 35

SIGNATURES S-1

1 | P a g e

PART I – FINANCIAL INFORMATION

Item 1. Financial Statements.

Attached to this report as Annex “A” is the Corporation’s unaudited interim condensed consolidated financial statements as of March 31, 2020 (with comparative audited figures as at December 31, 2019) and for the three-month periods ended March 31, 2020 and 2019. The unaudited interim condensed consolidated financial statements for the period ended March 31, 2020 have been prepared in accordance with Philippine Financial Reporting Standards (“PFRS”) specific to Philippine Accounting Standard 34, Interim Financial Reporting, and hence do not include all of the information required in the December 31, 2019 annual audited consolidated financial statements. Item 2. Management's Discussion and Analysis (MD&A) of Financial Condition and Results of Operations. In the following discussion and analysis of our financial condition and results of operations, unless the context indicates or otherwise requires, any references to “we”, “us”, “our”, “Company”, “First Gen Group” means First Gen Corporation and its consolidated subsidiaries and references to “First Gen” pertains to the Parent Company, First Gen Corporation, not including its subsidiaries (please see Note 2 – Summary of Significant Accounting Policies to the accompanying unaudited interim condensed consolidated financial statements for the list of these subsidiaries, including a description of their respective principal business activities and First Gen’s direct and/or indirect equity interest). The following discussion and analysis of the Company’s consolidated financial performance for the period ended March 31, 2020 should be read in conjunction with its unaudited interim condensed consolidated financial statements and the accompanying notes as at March 31, 2020 and the audited consolidated financial statements as at December 31, 2019. The primary objective of this MD&A is to help the readers understand the dynamics of the Company’s business and the key factors underlying its financial results. Hence, our MD&A is comprised of a discussion of its core business, and analysis of the results of operations for each business segment. This section also focuses on key statistics from the unaudited interim condensed consolidated financial statements and pertains to known risks and uncertainties relating to the power industry in the Philippines where we operate up to the stated reporting period. This report also contains information that may constitute "forward-looking statements." Generally, the words "believe," "expect," "intend," "estimate," "anticipate," "plan," "foresee," "will," and similar expressions identify forward-looking statements, which generally are not historical in nature. However, the absence of these words or similar expressions does not mean that a statement is not forward-looking. All statements that address operating performance, events or developments that we expect or anticipate will occur in the future - including statements relating to revenue growth and statements expressing general views about future operating results - are forward-looking statements. Such forward-looking statements are made based on management’s current expectations or beliefs as well as assumptions made by, and information currently available to, management. First Gen does not make express or implied representations or warranties as to the accuracy and completeness of the information contained herein and shall not accept any responsibility or liability (including any third party liability) for any loss or damage, whether or not arising from any error or omission in compiling such information or as a result of any party’s reliance or use of such information. In addition, forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from our Company's historical experience and our present expectations or projections. These risks and uncertainties include, but are not limited to, those described in Risk Factors Affecting the Company’s Results of Operations and elsewhere in this report and in our Annual Report on Form 17-A for the year ended December 31, 2019, and those described from time to time in our future reports filed with the Philippine Securities and Exchange Commission (SEC). The financial information appearing in this report and in the accompanying audited consolidated financial statements is stated in United States dollars. All references to “U.S. dollars,” “US$” or “dollars” are to the lawful currency of the United States; all references to “Philippine pesos,” “Php” or “pesos” are to the lawful currency of the Philippines; and all references to “Euro” or “€” are to the lawful currency of the European Union. Unless otherwise indicated, translations of Philippine peso amounts into U.S. dollars in this report and in the accompanying audited consolidated financial statements were made based on the exchange rate quoted through the Banker’s Association of the Philippines as at March 31, 2020. Additional information about the Company, including annual and quarterly reports, can be found on our corporate website www.firstgen.com.ph.

2 | P a g e

BUSINESS OVERVIEW

Description of the Nature and Scope of the Business including Products or Services

First Gen Corporation (the Company or First Gen) is engaged in the business of power generation through the following operating companies:

(i) First Gas Power Corporation (FGPC), which operates the 1,000 MW Santa Rita natural gas-firedpower plant;

(ii) FGP Corp. (FGP), which operates the 500 MW San Lorenzo natural gas-fired power plant;(iii) First NatGas Power Corp. (FNPC), which operates the 420 MW San Gabriel natural gas-fired

power flex plant;(iv) Prime Meridian PowerGen Corporation (PMPC), which operates the 97 MW Avion natural gas-

fired power plant;(v) FG Bukidnon Power Corporation (FG Bukidnon), which operates the 1.6 MW FG Bukidnon mini-

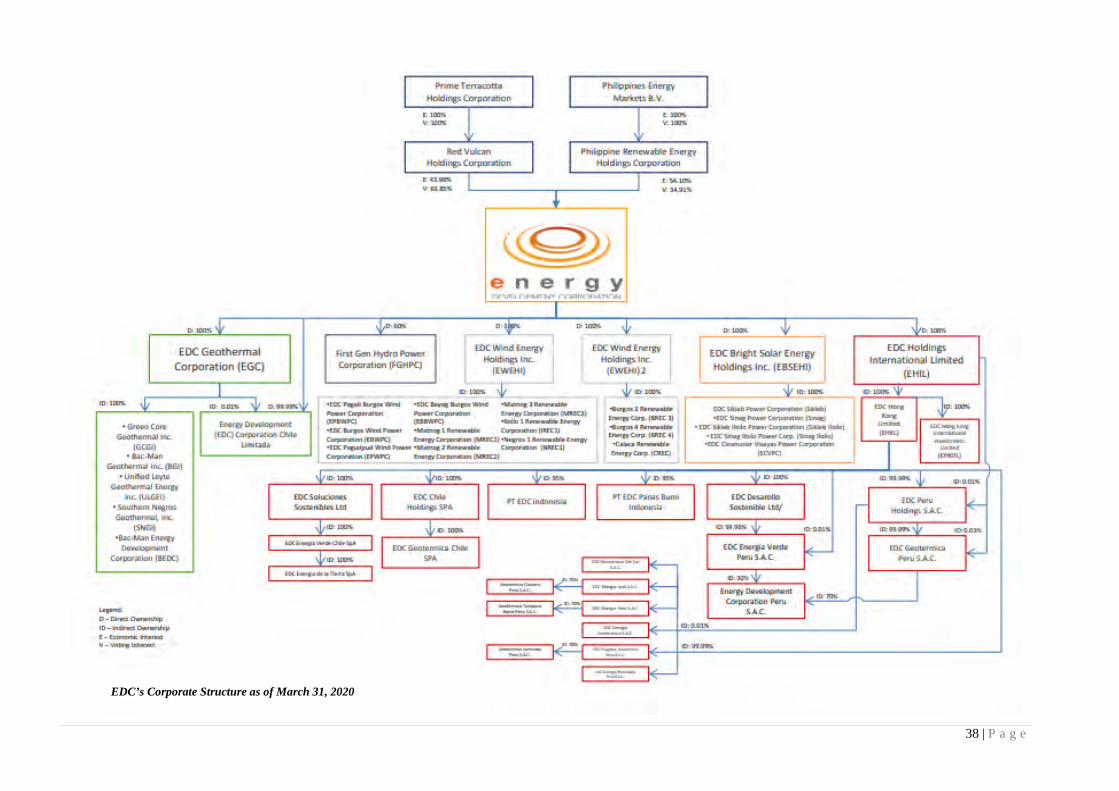

hydroelectric power plant;(vi) Energy Development Corporation (EDC), with an aggregate installed capacity of approximately

1,341.3 MW owns and operates the following plants:o 588.4 MW Unified Leyte geothermal power plantso 172.5 MW Palinpinon geothermal power plantso 140.0 MW Bac-Man geothermal power plantso 123.0 MW Tongonan geothermal power planto 106.0 MW Mindanao geothermal power plantso 49.4 MW Nasulo geothermal power planto 150 MW Burgos Wind Energy projecto 6.82 MW Burgos Solar Energy projecto 5.17 MW Solar Rooftop projects

(vii) First Gen Hydro Power Corporation (FG Hydro), which operates the 132 MW Pantabangan-Masiway hydroelectric power plants.

First Gen’s direct and indirect 45.7% economic interest in EDC is held through the Company, Prime Terracota Holdings Corporation (Prime Terracota), Northern Terracotta Power Corporation (Northern Terracotta), and Red Vulcan Holdings Corporation (Red Vulcan). First Gen has a 40.0% direct economic interest in FG Hydro.

Prior to September 30, 2017, the Company also directly and indirectly owned 1.98 billion common shares in EDC, of which 986.34 million common shares were held through its wholly-owned subsidiary, Northern Terracotta. The 1.98 billion common shares were equivalent to a 10.6% economic interest in EDC. Following the successful tender offer conducted by Philippines Renewable Energy Holdings Corporation (PREHC), which settled on September 29, 2017, to acquire up to 47.5% of EDC’s common shares, First Gen and Northern Terracotta participated and sold 9.0% of their combined 10.6% economic stake in EDC.

After the tender offer in September 2017, the Company’s total economic stake in EDC was 41.6%, of which 40.0% is currently held through Red Vulcan while the remaining 1.6% is held through First Gen directly and Northern Terracotta. Moreover, First Gen held a 61.1% voting interest in EDC post the first tender offer, of which 60.0% was held through Red Vulcan. The Company continued to consolidate EDC given its controlling voting stake in EDC post the September 2017 tender offer.

On August 7, 2018, EDC’s board of directors approved the voluntary delisting of the company from the Philippine Stock Exchange, Inc. (PSE). In relation thereto, the board likewise approved the conduct of a tender offer at P7.25 per share for up to 2,040,006,713 of EDC’s common shares (representing approximately 10.9% of outstanding common shares) held collectively by its stockholders other than Red Vulcan, First Gen, Northern Terracotta, and PREHC. Following the closing of the tender offer on October 22, 2018, a total of 2,009,107,731 common shares (representing 10.7% of outstanding common shares) were tendered, accepted and thereafter purchased by EDC on November 5, 2018. Following the completion of the tender offer, Red Vulcan, First Gen, Northern Terracotta, and PREHC collectively held more than 99.8% of the outstanding listed shares of EDC.

3 | P a g e

On September 19, 2018, EDC filed a petition for its delisting with the PSE, subject to the outcome of the tender offer. On November 21, 2018, PSE’s board of directors approved EDC’s Petition for Voluntary Delisting and authorized the delisting of their common shares from the Official Registry of the PSE, effective on November 29, 2018. On December 5, 2018, EDC’s board of directors approved the issuance of additional 326,250,000 non-preemption common shares to PREHC out of its existing unissued capital stock due to PREHC’s capital infusion. The Company continues to consolidate EDC post-delisting from the PSE, given its controlling stake. As of March 31, 2020, the Company’s total voting and economic interests in EDC are 65.0% and 45.7%, respectively. The following discussion focuses on the results of operations of First Gen and its power generating companies. As of March 31, 2020, First Gen's ownership interests in these operating companies are indirectly held through intermediate holding companies, with the exception of FG Hydro, where First Gen directly holds a 40.0% economic interest as stated above. Since the acquisition of the entire outstanding capital stock of Bluespark Management Limited (Bluespark) (formerly Lisbon Star Management Limited) on May 30, 2012 by Blue Vulcan Holdings Corporation (Blue Vulcan), a wholly-owned subsidiary of First Gen, the Company now beneficially owns 100.0% of First Gas Holdings Corporation (FGHC), FGP, and FNPC, (collectively referred to as the “First Gas Group”) through its intermediate holding companies.

▪ FGHC was incorporated on February 3, 1995 as a holding company for the development of natural gas-

fired power plants and other non-power gas related businesses. The company was 60.0% owned by First Gen and 40.0% owned by Dualcore Holdings Inc. (Dualcore) [formerly BG Consolidated Holdings (Philippines), Inc. (BG)] prior to the acquisition of the non-controlling stake of BG in the natural gas projects in May 2012. As a result of the transaction, First Gen effectively owns 100.0% of FGHC. FGHC wholly-owns FGPC, the project company of the 1,000 MW Santa Rita power plant.

▪ FGPC is the project company of the Santa Rita power plant. The company was incorporated on

November 24, 1994 to develop the 1,000 MW combined-cycle natural gas-fired power plant located in Santa Rita, Batangas City within the First Gen Clean Energy Complex (FGEN Clean Complex). The company started full commercial operations on August 17, 2000. FGPC generates electricity for Meralco under a 25-year Power Purchase Agreement (PPA). In order to fulfill its responsibility to operate and maintain the power plant, FGPC has an existing agreement with Siemens Power Operations, Inc. (SPOI), a 100.0% subsidiary of Siemens AG, to act as the operator under an Operations & Maintenance Agreement (O&M Agreement).

▪ Unified Holdings Corporation (Unified) was incorporated on March 30, 1999 as the holding company of

First Gen’s 60.0% equity share in FGP, the project company of the 500 MW San Lorenzo Power Plant. First Gen owns 100.0% of Unified.

o FGP is the project company of the San Lorenzo power plant. The company was established on July

23, 1997 to develop a 500 MW combined-cycle natural gas-fired power plant in Santa Rita, Batangas City, adjacent to the 1,000 MW Santa Rita power plant inside the FGEN Clean Complex. The company started full commercial operations on October 1, 2002. It is likewise operated by SPOI under a separate O&M Agreement and generates electricity under a separate 25-year PPA with Meralco.

▪ AlliedGen Power Corp. (AGPC) was incorporated and registered with the SEC on February 14, 2005.

AGPC wholly-owns FNPC, the project company of the 420 MW San Gabriel natural gas-fired flex power plant (San Gabriel). AGPC is a wholly-owned subsidiary of First Gen. o FNPC is the project company of San Gabriel. San Gabriel is adjacent to the existing Santa Rita and

San Lorenzo power plants inside the FGEN Clean Complex in Santa Rita, Batangas City. The San

4 | P a g e

Gabriel plant is capable of serving both the base load to mid-merit requirements of the Luzon Grid. San Gabriel went into commercial operations in November 2016 and was a 100.0% merchant plant until end-June 2018. In March 2018, it was awarded a six-year Power Supply Agreement (PSA) by Meralco for 414 MW of San Gabriel’s baseload capacity after undergoing a Competitive Selection Process (CSP). The sale of electricity to Meralco commenced on June 26, 2018 following the grant of a provisional approval for FNPC’s contract with Meralco that was received from the Energy Regulatory Commission (ERC). The PSA will expire on February 23, 2024 and can be extended upon mutual agreement with Meralco.

▪ Prime Meridian PowerGen Corporation (PMPC) was incorporated and registered with the SEC on

August 8, 2011. The company is a wholly-owned subsidiary of First Gen. PMPC is the operating company of the 97 MW Avion open-cycle natural gas-fired power plant (Avion) that is likewise located adjacent to the existing natural gas-fired power plants inside the FGEN Clean Complex. The Avion plant is using General Electric’s LM6000 PC Sprint aero-derivative gas turbines and has the capability to burn natural gas or diesel. The plant went into commercial operations in September 2016. It is currently a 100.0% merchant plant.

▪ First Gen Renewables, Inc. (FGRI), formerly known as First Philippine Energy Corporation, was

established on November 29, 1978. It is tasked to develop prospects in the Renewable Energy (RE) market. On June 17, 2014, the SEC approved the Plan and Articles of Merger between FGRI and Bluespark that was executed on April 29, 2014 following the majority vote of the board of directors and by the vote of the stockholders owning and representing more than two-thirds of the outstanding capital stock of constituent corporations on April 24, 2014. As a result of the merger, FGRI became the surviving corporation and is now 99.1% effectively-owned by Blue Vulcan. FGRI effectively owns a 40.0% voting and economic interest in the Santa Rita and San Lorenzo power plants. Prior to the merger, FGRI was a wholly-owned subsidiary of First Gen. o FG Bukidnon, a wholly-owned subsidiary of FGRI, was incorporated on February 9, 2005. Upon

conveyance of First Gen in October 2005, FG Bukidnon took over the operations and maintenance of the FG Bukidnon Hydroelectric power plant. The run-of-river plant consists of two 800-kW turbine generators that use water from the Agusan River to generate electricity. It is connected to the local distribution grid of the Cagayan Electric Power & Light Company, Inc. (CEPALCO) via the National Grid Corporation of the Philippines (NGCP) line.

▪ Prime Terracota was incorporated on October 17, 2007 as the holding company of Red Vulcan. Red

Vulcan was incorporated on October 5, 2007 as the holding company for First Gen’s 60.0% voting and 40.0% economic stake in EDC.

On November 22, 2007, First Gen, through Red Vulcan, was declared the winning bidder for the Philippine National Oil Company and EDC Retirement Fund’s remaining shares in EDC. Such common shares represent a 40.0% economic interest in EDC, while the combined common and preferred shares represent 60.0% of the voting rights in EDC. EDC is the Philippines’ largest producer of geothermal energy, operating 12 geothermal power plants in the four geothermal service contract areas where it is principally involved in: (i) the production of geothermal steam for sale to subsidiaries; and, (ii) the generation and sale of electricity through EDC-owned geothermal power plants to National Power Corporation (NPC) and various offtakers. o Tongonan, Kananga, Leyte – EDC operates three geothermal steamfield projects in Leyte, which

deliver steam to the 123 MW Tongonan geothermal power plant, and the 588.4 MW Unified Leyte geothermal power plants.

o Southern Negros, Valencia, Negros Oriental – EDC operates two geothermal steamfield projects in Southern Negros, which deliver steam to the 172.5 MW Palinpinon geothermal power plants, and the 49.4 MW Nasulo power plant.

o Bacon-Manito, Albay and Sorsogon – EDC operates two geothermal steamfield projects, which deliver steam to the 140 MW Bacman geothermal power plants.

5 | P a g e

o Mt. Apo, Kidapawan, Cotabato – EDC operates one geothermal steamfield project, which delivers

steam to the 106 MW Mindanao power plants. Likewise, EDC owns the 150 MW Burgos Wind Power Plant (Burgos Wind) and the 6.82 MW Burgos Solar Project (Burgos Solar) both situated in Burgos, Ilocos Norte. As of March 31, 2020, EDC likewise has a 5.17 MW total of solar rooftop projects. As mentioned in the preceding section regarding the equity transactions of EDC in 2018, the Company continues to consolidate EDC after its delisting from the PSE, given its controlling stake. As of March 31, 2020, the Company’s total voting and economic interests in EDC are 65.0% and 45.7%, respectively.

▪ FG Hydro was incorporated on March 13, 2006 as a wholly-owned subsidiary of First Gen. On September 8, 2006, FG Hydro emerged as the winning bidder for the then 100 MW Pantabangan and the 12 MW Masiway Hydroelectric Power Plants (PMHEPP). PMHEPP was transferred to FG Hydro on November 18, 2006, representing the first major generating asset of NPC to be successfully transferred to the private sector. On October 15, 2008, First Gen’s Board of Directors (BOD) approved the sale of 60.0% of FG Hydro to EDC and the divestment was completed in November 2008. As a result of the divestment, First Gen’s direct voting and economic interests in FG Hydro were reduced to 40.0%. Moreover, the completion of the rehabilitation and upgrade project of Pantabangan hydroelectric power plant’s Units 1 and 2 in 2010 increased the power generation capacity of PMHEPP by 20 MW to 132 MW. FG Hydro likewise rehabilitated the Masiway plant to address equipment obsolescence specifically on the excitation, protection and generator systems, as well as the main step-up transformer of Masiway. Following the developments in EDC’s shares in 2017 and 2018, the Company’s effective economic stake in FG Hydro is equivalent to 67.4% as of March 31, 2020.

▪ First Gen Energy Solutions, Inc. (FGES) was incorporated and registered with the SEC on November 24,

2006. As a wholly-owned subsidiary of First Gen, FGES markets and sells electricity generated by First Gen and EDC to address the power requirements of Contestable Customers. In addition, it provides value-added services relevant to its core business. FGES holds a Retail Electricity Supplier (RES) license effective for a period of five years from May 2016 until May 2021. FGES’ RES business has a total contracted demand of 43.9 MW from 7 contestable customers as of March 31, 2020.

Principal Products or Services First Gen and its subsidiaries are primarily involved in the power generation business. It owns power plants which utilize natural gas, geothermal, wind, hydro, and solar power. The electricity generated is primarily sold to Meralco, NPC, electric cooperatives, privately-owned distribution utilities (DUs), large industrial clients, and NGCP, pursuant to long-term PPAs, Power Supply Contracts (PSCs), PSAs, Wholesale Electricity Spot Market (WESM), Ancillary Services Procurement Agreement (ASPA), and the Feed-In-Tariff (FiT). The following is a summary of First Gen’s products/services and their markets as of March 31, 2020:

Company

Principal products/services

Market

Effective Contribution to Consolidated

Revenues* of First Gen

FGPC - Power generation MERALCO US$158.6 million

FGP - Power generation MERALCO US$80.7 million

FNPC - Power generation MERALCO US$46.2 million

PMPC - Power generation WESM US$1.0 million (or P49.5 million)

FG Bukidnon - Power generation CEPALCO US$0.1 million (or P4.0 million)

FG Hydro - Power generation WESM / NGCP/ PSAs with industrial customers

US$13.0 million (or P662.0 million)

6 | P a g e

EDC EDC holds service contracts with the Department of Energy (DOE) corresponding to 15 geothermal contract areas

EDC, through its subsidiary,

EDC Burgos Wind Power Corporation (EBWPC), operates the 150 MW wind project in Burgos, Ilocos Norte. EDC also owns and operates the 6.82 MW Burgos Solar Power Plant.

EDC operates the 5.17 MW

Gaisano Rooftop Solar project located in Iloilo, Leyte, Aklan, and Sorsogon.

NPC (for power generation & steam sales), WESM, NGCP, electric cooperatives and industrial customers pursuant to the PPAs, PSAs and contracts, and Feed-in Tariff (FiT)

US$178.0 million** (or P9,039.5 million)

FGES - Retail energy supply Contestable Customers US$3.9 million (or P196.4 million)

* Pertains to revenues from sale of electricity only ** Pertains to EDC’s consolidated revenues from sale of electricity, excluding FG Hydro

Note: The Philippine Peso balances of PMPC, FG Bukidnon, FG Hydro, EDC, and FGES were translated to U.S. Dollar using the weighted average rate of US$1.00:P50.786 for the period ended March 31, 2020. FGPC, FGP and FNPC’s functional currency is the U.S. Dollar..

New Product / Service First Gen intends to expand into businesses that complement its power generation operations. In particular, the Company expects to play a major role in the development of downstream natural gas transmission and distribution facilities, and other projects using renewable sources of energy. Competition The implementation of the Electric Power Industry Reform Act of 2001 (EPIRA) by the Government paved the way for a more independent and market-driven Philippine power industry. This has allowed for competition not limited by location, and driven by market forces. As such, selling power and, consequently, the dispatch of power plants depend on the ability to offer competitively-priced power to the market. As a group, First Gen has multiple power plants and projects in Luzon, Visayas, and Mindanao. The successful privatization of NPC assets and NPC-IPP contracts in Luzon and Visayas, coupled with the integration of the Luzon and Visayas grids under the WESM, and the initial commercial operations of the RCOA in June 2013, introduced new players and opened competition in the power industry. The Aboitiz group and the San Miguel group are the Company’s closest competitors, while conglomerates, such as the Ayala Group, have entered the industry. The performance of the Philippine economy and the historical high returns of power projects in the country have attracted many potential competitors, including multinational corporations and equipment suppliers, to explore opportunities in the development of electric power generation projects in the Philippines. Accordingly, competition for and from new power projects has increased in line with the economic growth in the Philippines. Moving forward, the First Gen Group continues to face competition both in the development of new power generation facilities and in the acquisition of existing power plants (if there are any). The First Gen Group believes that it will be able to compete because of its track record, competitively-priced portfolio of power generating assets, the reliability of its power plants, its use of clean and renewable fuels, and its expertise and experience in power supply contracting and trading.

7 | P a g e

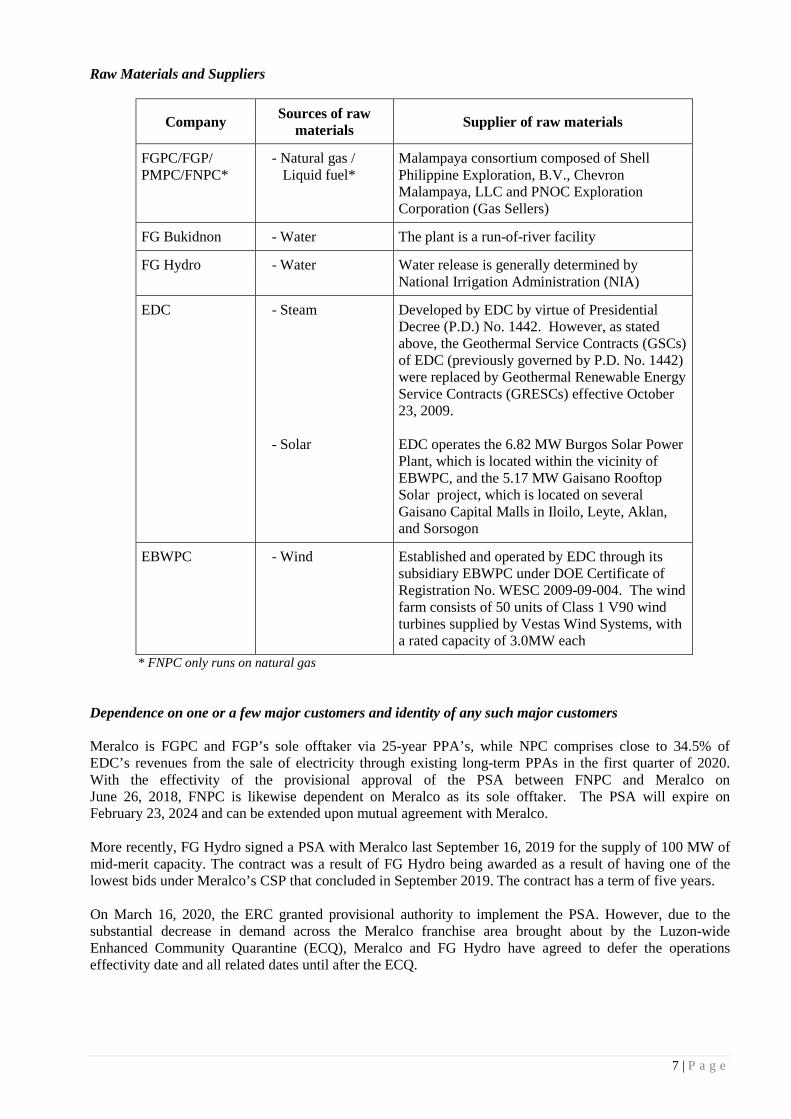

Raw Materials and Suppliers

Company Sources of raw materials Supplier of raw materials

FGPC/FGP/ PMPC/FNPC*

- Natural gas / Liquid fuel*

Malampaya consortium composed of Shell Philippine Exploration, B.V., Chevron Malampaya, LLC and PNOC Exploration Corporation (Gas Sellers)

FG Bukidnon - Water The plant is a run-of-river facility

FG Hydro - Water Water release is generally determined by National Irrigation Administration (NIA)

EDC - Steam - Solar

Developed by EDC by virtue of Presidential Decree (P.D.) No. 1442. However, as stated above, the Geothermal Service Contracts (GSCs) of EDC (previously governed by P.D. No. 1442) were replaced by Geothermal Renewable Energy Service Contracts (GRESCs) effective October 23, 2009. EDC operates the 6.82 MW Burgos Solar Power Plant, which is located within the vicinity of EBWPC, and the 5.17 MW Gaisano Rooftop Solar project, which is located on several Gaisano Capital Malls in Iloilo, Leyte, Aklan, and Sorsogon

EBWPC - Wind Established and operated by EDC through its subsidiary EBWPC under DOE Certificate of Registration No. WESC 2009-09-004. The wind farm consists of 50 units of Class 1 V90 wind turbines supplied by Vestas Wind Systems, with a rated capacity of 3.0MW each

* FNPC only runs on natural gas Dependence on one or a few major customers and identity of any such major customers Meralco is FGPC and FGP’s sole offtaker via 25-year PPA’s, while NPC comprises close to 34.5% of EDC’s revenues from the sale of electricity through existing long-term PPAs in the first quarter of 2020. With the effectivity of the provisional approval of the PSA between FNPC and Meralco on June 26, 2018, FNPC is likewise dependent on Meralco as its sole offtaker. The PSA will expire on February 23, 2024 and can be extended upon mutual agreement with Meralco. More recently, FG Hydro signed a PSA with Meralco last September 16, 2019 for the supply of 100 MW of mid-merit capacity. The contract was a result of FG Hydro being awarded as a result of having one of the lowest bids under Meralco’s CSP that concluded in September 2019. The contract has a term of five years. On March 16, 2020, the ERC granted provisional authority to implement the PSA. However, due to the substantial decrease in demand across the Meralco franchise area brought about by the Luzon-wide Enhanced Community Quarantine (ECQ), Meralco and FG Hydro have agreed to defer the operations effectivity date and all related dates until after the ECQ.

8 | P a g e

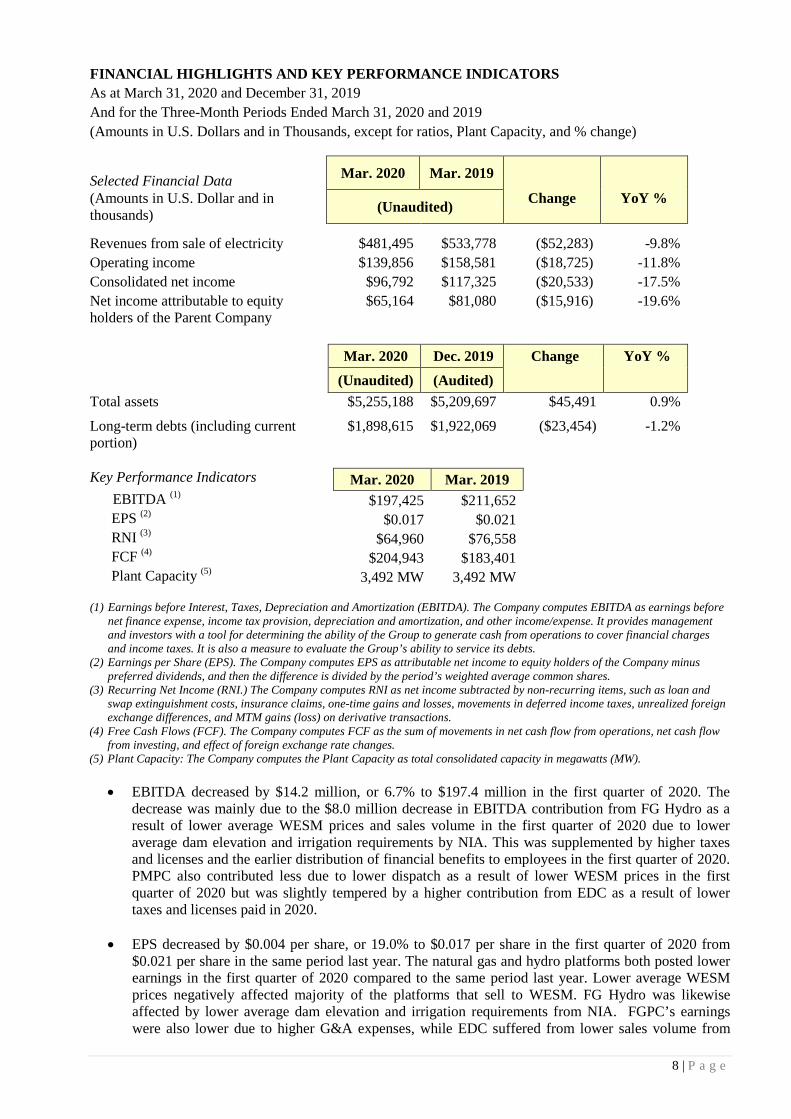

FINANCIAL HIGHLIGHTS AND KEY PERFORMANCE INDICATORS As at March 31, 2020 and December 31, 2019 And for the Three-Month Periods Ended March 31, 2020 and 2019 (Amounts in U.S. Dollars and in Thousands, except for ratios, Plant Capacity, and % change)

Selected Financial Data Mar. 2020 Mar. 2019

Change YoY % (Amounts in U.S. Dollar and in thousands) (Unaudited)

Revenues from sale of electricity $481,495 $533,778 ($52,283) -9.8% Operating income $139,856 $158,581 ($18,725) -11.8% Consolidated net income $96,792 $117,325 ($20,533) -17.5% Net income attributable to equity holders of the Parent Company

$65,164 $81,080 ($15,916) -19.6%

Mar. 2020 Dec. 2019 Change YoY % (Unaudited) (Audited)

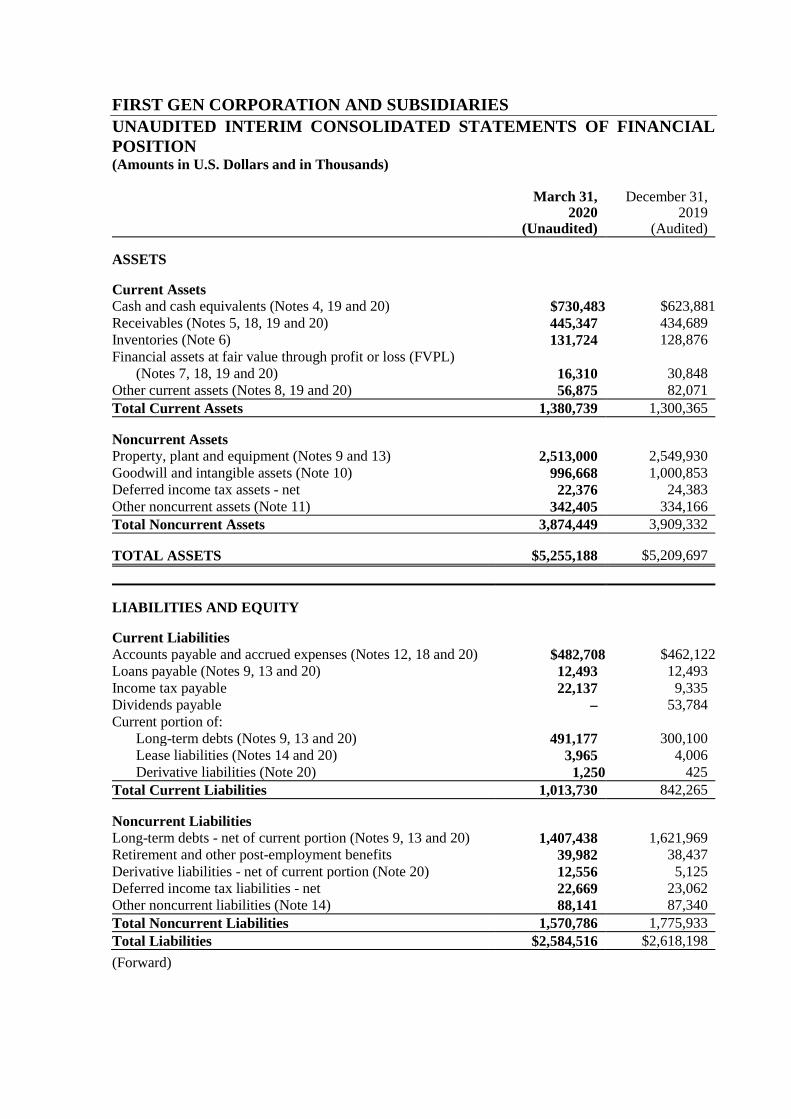

Total assets $5,255,188 $5,209,697 $45,491 0.9%

Long-term debts (including current portion)

$1,898,615 $1,922,069 ($23,454) -1.2%

Key Performance Indicators Mar. 2020 Mar. 2019

EBITDA (1) $197,425 $211,652 EPS (2) $0.017 $0.021 RNI (3) $64,960 $76,558 FCF (4) $204,943 $183,401 Plant Capacity (5) 3,492 MW 3,492 MW

(1) Earnings before Interest, Taxes, Depreciation and Amortization (EBITDA). The Company computes EBITDA as earnings before

net finance expense, income tax provision, depreciation and amortization, and other income/expense. It provides management and investors with a tool for determining the ability of the Group to generate cash from operations to cover financial charges and income taxes. It is also a measure to evaluate the Group’s ability to service its debts.

(2) Earnings per Share (EPS). The Company computes EPS as attributable net income to equity holders of the Company minus preferred dividends, and then the difference is divided by the period’s weighted average common shares.

(3) Recurring Net Income (RNI.) The Company computes RNI as net income subtracted by non-recurring items, such as loan and swap extinguishment costs, insurance claims, one-time gains and losses, movements in deferred income taxes, unrealized foreign exchange differences, and MTM gains (loss) on derivative transactions.

(4) Free Cash Flows (FCF). The Company computes FCF as the sum of movements in net cash flow from operations, net cash flow from investing, and effect of foreign exchange rate changes.

(5) Plant Capacity: The Company computes the Plant Capacity as total consolidated capacity in megawatts (MW). • EBITDA decreased by $14.2 million, or 6.7% to $197.4 million in the first quarter of 2020. The

decrease was mainly due to the $8.0 million decrease in EBITDA contribution from FG Hydro as a result of lower average WESM prices and sales volume in the first quarter of 2020 due to lower average dam elevation and irrigation requirements by NIA. This was supplemented by higher taxes and licenses and the earlier distribution of financial benefits to employees in the first quarter of 2020. PMPC also contributed less due to lower dispatch as a result of lower WESM prices in the first quarter of 2020 but was slightly tempered by a higher contribution from EDC as a result of lower taxes and licenses paid in 2020.

• EPS decreased by $0.004 per share, or 19.0% to $0.017 per share in the first quarter of 2020 from

$0.021 per share in the same period last year. The natural gas and hydro platforms both posted lower earnings in the first quarter of 2020 compared to the same period last year. Lower average WESM prices negatively affected majority of the platforms that sell to WESM. FG Hydro was likewise affected by lower average dam elevation and irrigation requirements from NIA. FGPC’s earnings were also lower due to higher G&A expenses, while EDC suffered from lower sales volume from

9 | P a g e

their geothermal plants in 2020. In addition, FNPC had lower capacity fees billed to Meralco due to its scheduled maintenance outage, which coincided with the end of its PSA Contract year 2 in January 2020, and higher G&A expenses for the period.

• RNI decreased by $11.6 million, or 15.1% to $65.0 million in the first quarter of 2020 from $76.6 million in the same period last year. This was primarily attributable to FG Hydro due to the aforementioned reasons in the first quarter of 2020. In addition, FGPC contributed lower RNI primarily due to lower operating income for the period as a result of early release of staff benefits and payment of taxes and licenses. Furthermore, FNPC contributed lower RNI due to lower capacity fees billed to Meralco due to its scheduled maintenance outage which coincided with the end of its PSA Contract year 2 in January 2020. In addition, PMPC’s RNI contribution was less due to lower WESM prices and dispatch.

• FCF increased by $21.5 million, or 11.7% to $204.9 million in the first quarter of 2020 from $183.4 million in the same period last year. This was primarily due to net redemptions of financial assets at FVPL, lower short-term investments and DSRA funding booked this period, augmented by lower additions to property, plant, & equipment for EDC, PMPC, and FNPC, which spent for various plant improvements in 2019. The increase was partially offset by lower EBITDA from FG Hydro and the natural gas assets.

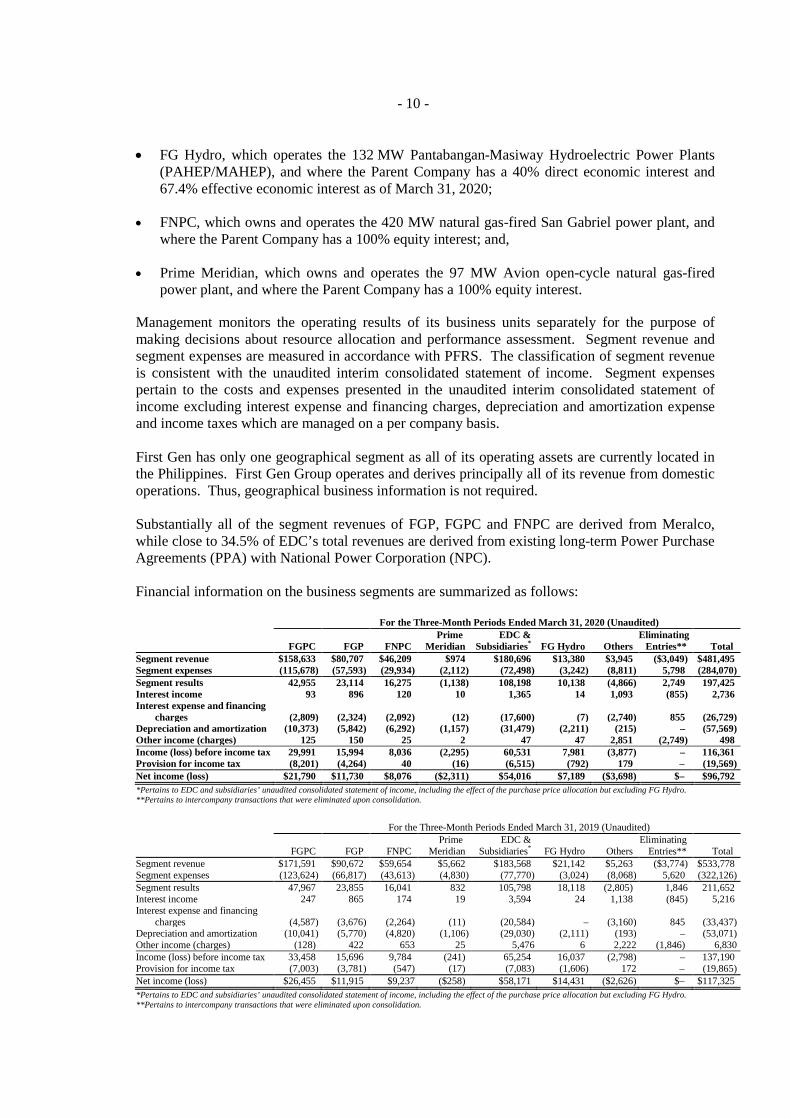

Review of March 31, 2020 operations vs. March 31, 2019 operations The First Gen Group generated a consolidated net income of $96.8 million in the first quarter of 2020, a $20.5 million or 17.5% decrease from $117.3 million posted in the same period last year. Consolidated revenues from the sale of electricity reached $481.5 million in the first quarter of 2020, $52.3 million or 9.8% lower than the $533.8 million posted in the same period last year due to lower revenues from the natural gas platform, FG Hydro, and EDC as a result of the aforementioned reasons. Net Income Attributable to Equity Holders of the Parent Company Net income attributable to the equity holders of the Parent Company decreased by $15.9 million, or 19.6% to $65.2 million in the first quarter of 2020, compared to $81.1 million recognized in the same period last year. The decrease in attributable net income was mainly due to the lower contributions of the following subsidiaries:

• FG Hydro’s net income contribution decreased by $4.9 million, or 50.2% to $4.8 million in the first quarter of 2020 compared to $9.7 million in the same period last year. The decrease was driven by lower average WESM selling price at P2.93/kWh in the first quarter of 2020 compared to P4.94/kWh in the same period last year, which was accompanied by lower generation of 194 GWh during the period compared to 217 GWh for the same period in 2019, on account of lower dam elevation and irrigation requirements of NIA. This was partially offset by higher revenues from ancillary services in the first quarter of 2020 compared to the same period last year.

• FGPC’s net income contribution decreased by $4.7 million, or 17.6% to $21.8 million in the first quarter of 2020 from $26.5 million in the same period last year. This was a result of higher staff costs and taxes and licenses. This was partially offset by lower interest expenses as a result of a decrease in LIBOR rates, a reversal from a foreign exchange loss in 2019 to a foreign exchange gain in 2020.

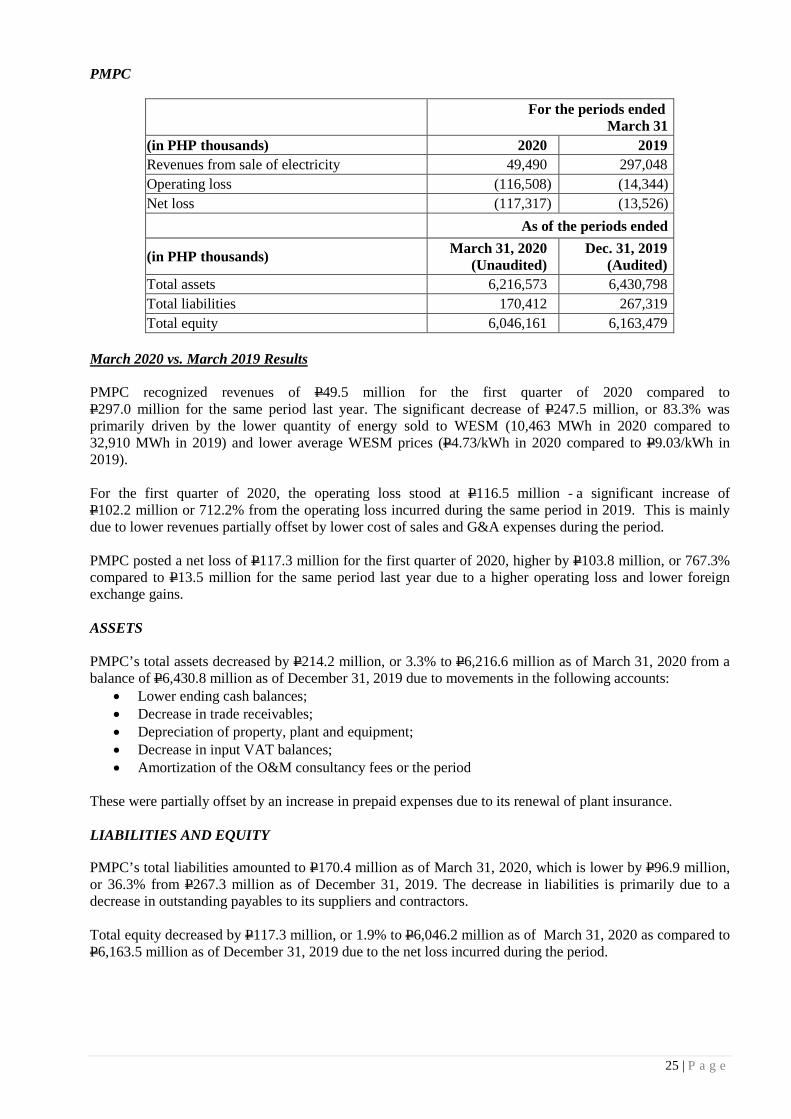

• PMPC’s net loss contribution increased by $2.0 million to a $2.2 million loss in the first quarter of 2020 from a $0.2 million loss in the same period last year. This was a result of lower average WESM prices of P4.73/kWh in the first quarter of 2020 from P9.03/kWh in the same period last year. This resulted from lower dispatch at 4.9% for the first quarter of 2020 compared to 15.7% in the same period in 2019 but was partially offset by lower fuel prices and the absence of maintenance works performed in the same period last year.

• EDC’s net income contribution (ex-hydro) only slightly decreased by $1.9 million, or 6.7% to $25.8 million in the first quarter of 2020 from $27.7 million in the same period last year. This was mainly due to lower sales volume from Unified Leyte, Palinpinon, and Mindanao. The ULGEI, Nasulo, and

10 | P a g e

Tongonan plants also suffered from lower average selling prices in 2020. Net income was further reduced by lower insurance claim proceeds received in 2020 compared to the same period last year. The above decreases were partially offset by lower interest expenses due to a partial redemption of EDC’s $211.0 million Bond amounting to $29.9 million in February 2019 and the full repayment of EDC’s term loans with various banks totaling to P3.7 billion in 2019.

• FNPC’s net income contribution decreased by $1.2 million, or 11.6% to $8.8 million in the first quarter of 2020 from $10.0 million in the same period last year largely driven by San Gabriel’s lower capacity fees billed to Meralco due to its scheduled maintenance outage, which coincided with the end of its PSA Contract year 2 in January 2020, and higher G&A expenses for the period. These were partially offset by the absence of replacement power purchases during its extended maintenance outage in the first quarter of 2019.

FIRST GEN MATERIAL CHANGES IN FINANCIAL CONDITION (March 31, 2020 vs. March 31, 2019)

CONSOLIDATED STATEMENTS OF INCOME

Horizontal and Vertical Analyses of Material Changes for the periods ended March 31, 2020 and 2019

HORIZONTAL ANALYSIS

2020 2019 2020 vs. 2019 2020 vs. 2019 2020 2019

Revenues from sale of electricity $481,495 $533,778 ($52,283) -9.8% 100.0% 100.0%TOTAL REVENUES 481,495 533,778 (52,283) -9.8% 100.0% 100.0%

OPERATING EXPENSESCosts of sale of electricity (295,105) (331,704) 36,599 -11.0% -61.3% -62.1%General and administrative expenses (46,534) (43,493) (3,041) 7.0% -9.7% -8.1%

Sub-total (341,639) (375,197) 33,558 -8.9% -71.0% -70.3%

FINANCIAL INCOME (EXPENSE)Interest income 2,736 5,216 (2,480) -47.5% 0.6% 1.0%Interest expense and financing charges (26,729) (33,437) 6,708 -20.1% -5.6% -6.3%

Sub-total (23,993) (28,221) 4,228 -15.0% -5.0% -5.3%

OTHER INCOME (CHARGES)Mark-to-market gain on derivatives – net 313 78 235 301.3% 0.1% 0.0%Mark-to-market gain on financial assets at FVPL – net 44 610 (566) -92.8% 0.0% 0.1%Proceeds from insurance claims 19 7,061 (7,042) -99.7% 0.0% 1.3%Foreign exchange gains (losses) – net (97) 1,459 (1,556) -106.6% 0.0% 0.3%Loss on extinguishment of long-term debts - (1,764) 1,764 -100.0% 0.0% -0.3%Others – net 219 (614) 833 135.7% 0.0% -0.1%

Sub-total 498 6,830 (6,332) -92.7% 0.1% 1.3%

INCOME BEFORE INCOME TAX 116,361 137,190 (20,829) -15.2% 24.2% 25.7%Provision for (benefit from) income tax:

Current 17,840 21,095 (3,255) -15.4% 3.7% 4.0%Deferred 1,729 (1,230) 2,959 240.6% 0.4% -0.2%

19,569 19,865 (296) -1.5% 4.1% 3.7%NET INCOME $96,792 $117,325 ($20,533) -17.5% 20.1% 22.0%

Net income attributable to:Equity holders of the Parent Company $65,164 $81,080 ($15,916) -19.6% 13.5% 15.2%Non-controlling Interests $31,628 $36,245 ($4,617) -12.7% 6.6% 6.8%

VERTICAL ANALYSIS

11 | P a g e

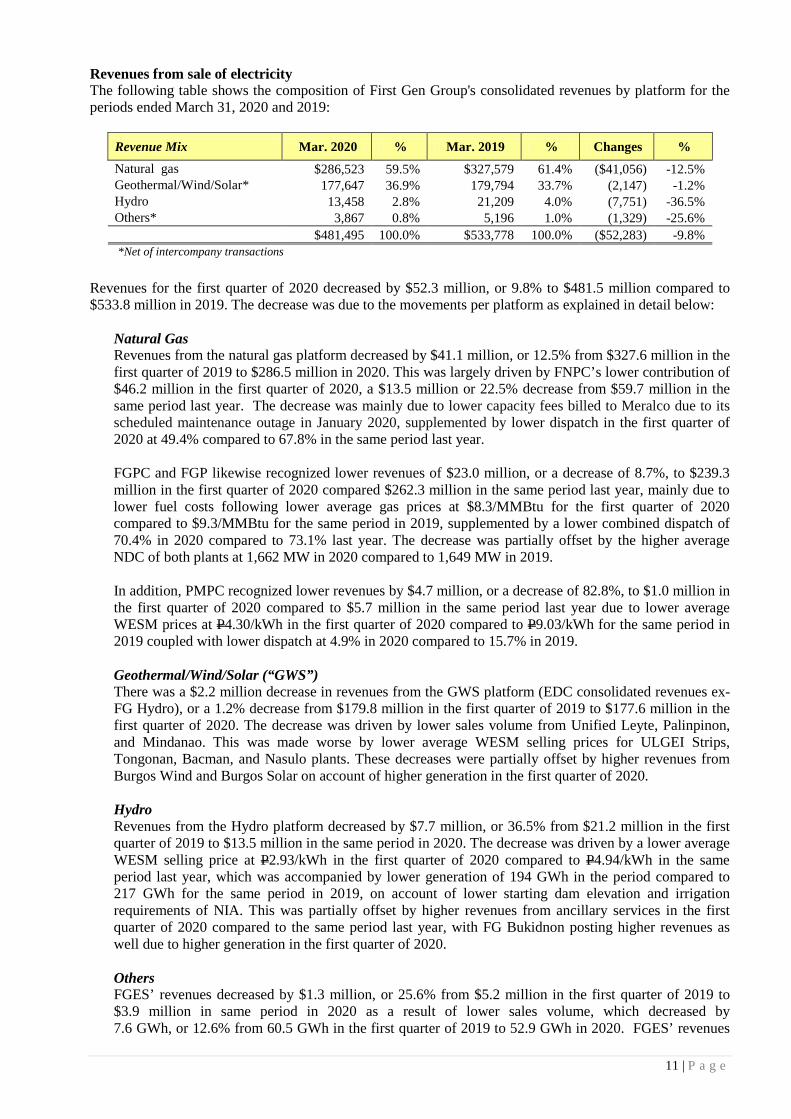

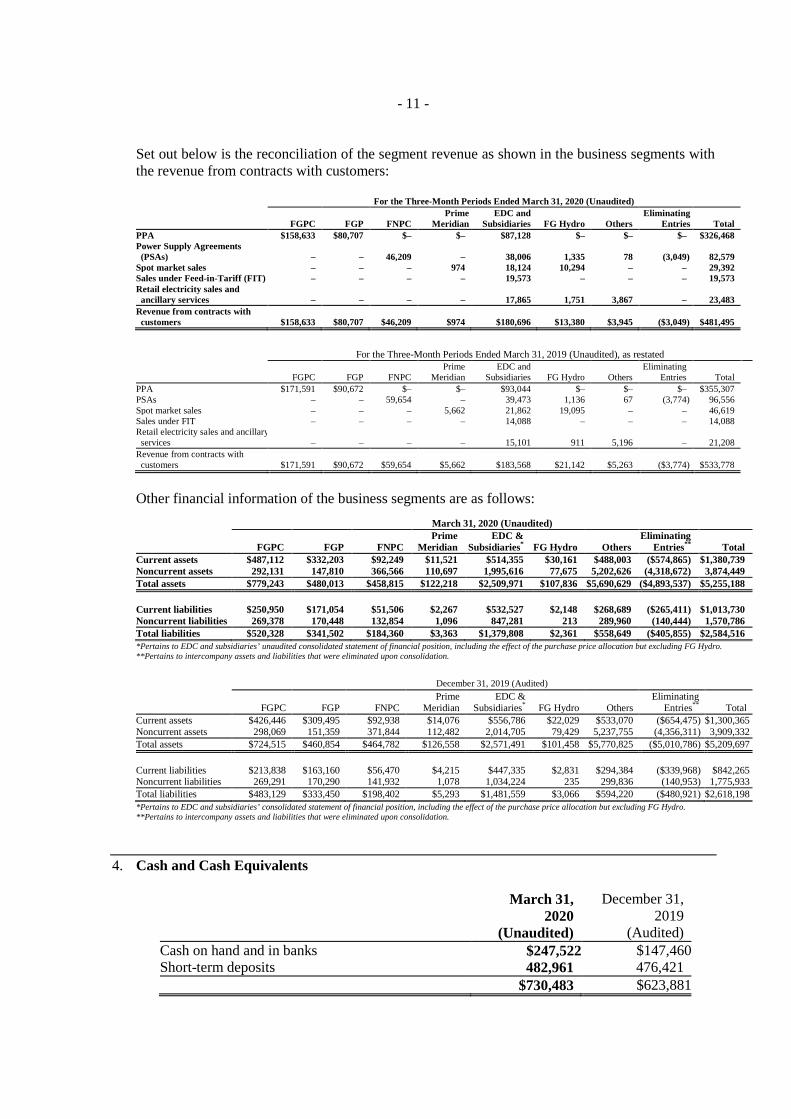

Revenues from sale of electricity The following table shows the composition of First Gen Group's consolidated revenues by platform for the periods ended March 31, 2020 and 2019:

Revenue Mix Mar. 2020 % Mar. 2019 % Changes % Natural gas $286,523 59.5% $327,579 61.4% ($41,056) -12.5% Geothermal/Wind/Solar* 177,647 36.9% 179,794 33.7% (2,147) -1.2% Hydro 13,458 2.8% 21,209 4.0% (7,751) -36.5% Others* 3,867 0.8% 5,196 1.0% (1,329) -25.6%

$481,495 100.0% $533,778 100.0% ($52,283) -9.8% *Net of intercompany transactions

Revenues for the first quarter of 2020 decreased by $52.3 million, or 9.8% to $481.5 million compared to $533.8 million in 2019. The decrease was due to the movements per platform as explained in detail below:

Natural Gas Revenues from the natural gas platform decreased by $41.1 million, or 12.5% from $327.6 million in the first quarter of 2019 to $286.5 million in 2020. This was largely driven by FNPC’s lower contribution of $46.2 million in the first quarter of 2020, a $13.5 million or 22.5% decrease from $59.7 million in the same period last year. The decrease was mainly due to lower capacity fees billed to Meralco due to its scheduled maintenance outage in January 2020, supplemented by lower dispatch in the first quarter of 2020 at 49.4% compared to 67.8% in the same period last year. FGPC and FGP likewise recognized lower revenues of $23.0 million, or a decrease of 8.7%, to $239.3 million in the first quarter of 2020 compared $262.3 million in the same period last year, mainly due to lower fuel costs following lower average gas prices at $8.3/MMBtu for the first quarter of 2020 compared to $9.3/MMBtu for the same period in 2019, supplemented by a lower combined dispatch of 70.4% in 2020 compared to 73.1% last year. The decrease was partially offset by the higher average NDC of both plants at 1,662 MW in 2020 compared to 1,649 MW in 2019. In addition, PMPC recognized lower revenues by $4.7 million, or a decrease of 82.8%, to $1.0 million in the first quarter of 2020 compared to $5.7 million in the same period last year due to lower average WESM prices at P4.30/kWh in the first quarter of 2020 compared to P9.03/kWh for the same period in 2019 coupled with lower dispatch at 4.9% in 2020 compared to 15.7% in 2019.

Geothermal/Wind/Solar (“GWS”) There was a $2.2 million decrease in revenues from the GWS platform (EDC consolidated revenues ex-FG Hydro), or a 1.2% decrease from $179.8 million in the first quarter of 2019 to $177.6 million in the first quarter of 2020. The decrease was driven by lower sales volume from Unified Leyte, Palinpinon, and Mindanao. This was made worse by lower average WESM selling prices for ULGEI Strips, Tongonan, Bacman, and Nasulo plants. These decreases were partially offset by higher revenues from Burgos Wind and Burgos Solar on account of higher generation in the first quarter of 2020.

Hydro Revenues from the Hydro platform decreased by $7.7 million, or 36.5% from $21.2 million in the first quarter of 2019 to $13.5 million in the same period in 2020. The decrease was driven by a lower average WESM selling price at P2.93/kWh in the first quarter of 2020 compared to P4.94/kWh in the same period last year, which was accompanied by lower generation of 194 GWh in the period compared to 217 GWh for the same period in 2019, on account of lower starting dam elevation and irrigation requirements of NIA. This was partially offset by higher revenues from ancillary services in the first quarter of 2020 compared to the same period last year, with FG Bukidnon posting higher revenues as well due to higher generation in the first quarter of 2020.

Others FGES’ revenues decreased by $1.3 million, or 25.6% from $5.2 million in the first quarter of 2019 to $3.9 million in same period in 2020 as a result of lower sales volume, which decreased by 7.6 GWh, or 12.6% from 60.5 GWh in the first quarter of 2019 to 52.9 GWh in 2020. FGES’ revenues

12 | P a g e

are from supply charges and power sold to contestable customers, which are sourced from electricity generated by EDC and FG Hydro. FGES had 7 contracted customers by end-March 2020 compared to 12 customers by end-March 2019. The number of customers decreased due to contracts which expired and some customers that were renewed under an affiliate – BacMan Geothermal Inc. (BGI) RES.

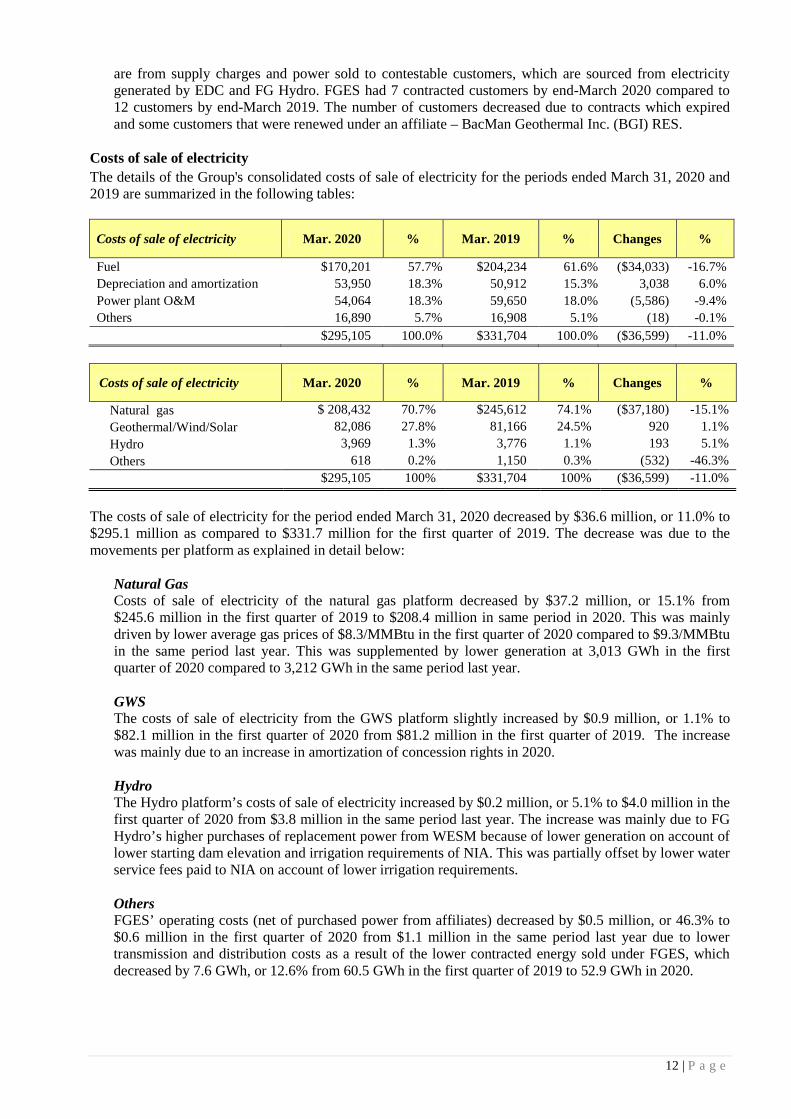

Costs of sale of electricity The details of the Group's consolidated costs of sale of electricity for the periods ended March 31, 2020 and 2019 are summarized in the following tables:

Costs of sale of electricity Mar. 2020 % Mar. 2019 % Changes %

Fuel $170,201 57.7% $204,234 61.6% ($34,033) -16.7% Depreciation and amortization 53,950 18.3% 50,912 15.3% 3,038 6.0% Power plant O&M 54,064 18.3% 59,650 18.0% (5,586) -9.4% Others 16,890 5.7% 16,908 5.1% (18) -0.1%

$295,105 100.0% $331,704 100.0% ($36,599) -11.0%

Costs of sale of electricity Mar. 2020 % Mar. 2019 % Changes %

Natural gas $ 208,432 70.7% $245,612 74.1% ($37,180) -15.1% Geothermal/Wind/Solar 82,086 27.8% 81,166 24.5% 920 1.1% Hydro 3,969 1.3% 3,776 1.1% 193 5.1% Others 618 0.2% 1,150 0.3% (532) -46.3%

$295,105 100% $331,704 100% ($36,599) -11.0%

The costs of sale of electricity for the period ended March 31, 2020 decreased by $36.6 million, or 11.0% to $295.1 million as compared to $331.7 million for the first quarter of 2019. The decrease was due to the movements per platform as explained in detail below:

Natural Gas Costs of sale of electricity of the natural gas platform decreased by $37.2 million, or 15.1% from $245.6 million in the first quarter of 2019 to $208.4 million in same period in 2020. This was mainly driven by lower average gas prices of $8.3/MMBtu in the first quarter of 2020 compared to $9.3/MMBtu in the same period last year. This was supplemented by lower generation at 3,013 GWh in the first quarter of 2020 compared to 3,212 GWh in the same period last year.

GWS The costs of sale of electricity from the GWS platform slightly increased by $0.9 million, or 1.1% to $82.1 million in the first quarter of 2020 from $81.2 million in the first quarter of 2019. The increase was mainly due to an increase in amortization of concession rights in 2020.

Hydro The Hydro platform’s costs of sale of electricity increased by $0.2 million, or 5.1% to $4.0 million in the first quarter of 2020 from $3.8 million in the same period last year. The increase was mainly due to FG Hydro’s higher purchases of replacement power from WESM because of lower generation on account of lower starting dam elevation and irrigation requirements of NIA. This was partially offset by lower water service fees paid to NIA on account of lower irrigation requirements. Others FGES’ operating costs (net of purchased power from affiliates) decreased by $0.5 million, or 46.3% to $0.6 million in the first quarter of 2020 from $1.1 million in the same period last year due to lower transmission and distribution costs as a result of the lower contracted energy sold under FGES, which decreased by 7.6 GWh, or 12.6% from 60.5 GWh in the first quarter of 2019 to 52.9 GWh in 2020.

13 | P a g e

G&A Expenses G&A expenses increased by $3.0 million, or 7.0% to $46.5 million in the first quarter of 2020 from $43.5 million in the same period last year. The increase is primarily due to higher staff costs related to financial assistance gratuity to employees in light of the COVID-19 health crisis. This was supplemented by EDC’s increased amortization of right-of-use of assets from the adoption of PFRS 16, Leases, as well as the Group’s donations for COVID-19 relief. This was partially offset by a decrease in EDC’s taxes and licenses and lower professional fees. Interest expense and financing charges Interest expense and financing charges decreased by $6.7 million, or 20.1% to $26.7 million in the first quarter of 2020 from $33.4 million in the same period last year. The decrease was primarily due to the Company’s lower outstanding debt due to several aforementioned loan prepayments. This was supplemented by the lower outstanding debt balances of FGPC, FGP, the Parent, and FNPC as a result of regular principal repayments. Foreign exchange gains (losses) – net The First Gen Group recognized foreign exchange losses amounting to $0.1 million in the first quarter of 2020, a $1.6 million or 106.6% decrease from a $1.5 million gain in the same period last year. The reversal primarily relates to EDC’s foreign exchange losses on transactions denominated in the Chilean Peso. This movement was supplemented by lower foreign exchange gains from FNPC, FGP, and the Parent due to the depreciation of the Philippine Peso against the U.S. Dollar in the first quarter of 2020. MTM gain (loss) on derivatives and MTM gain (loss) on financial assets at FVPL For the first quarter of 2020, the net MTM gain on derivatives and financial assets at FVPL stood at $0.4 million, a decrease of $0.3 million from the $0.7 million net gain booked in the first quarter of 2019. The decrease was mainly due to a $0.5 million decline in the MTM gains from EDC's financial assets at FVPL compared to 2019, partially offset by an increase of $0.2 million in the MTM derivative gains compared to 2019. Other Income / Charges – net Other income stood at $0.2 million in the first quarter of 2020, a $4.5 million or 93.6% decrease from $4.7 million booked in the first quarter of 2019. This decrease in other income was mainly due to EDC’s lower insurance claim proceeds, slightly offset by the absence of a one-time debt extinguishment cost of $1.8 million following the partial redemption of its $211.0 million bond in February 2019. Provision for Income Tax The provision for income tax decreased by $0.3 million, or 1.5% to $19.6 million for the first quarter of 2020 from $19.9 million in the same period last year. The decrease was primarily to a result of EDC, FG Hydro, and FGPC’s lower taxable income in the first quarter of 2020 compared to the same period last year. This was offset by the reversal of the benefit from deferred income tax recognized in 2019 to a provision for deferred income tax in 2020 as a result of depreciation of the Philippine Peso against the U.S. Dollar during the period. Net Income The First Gen Group generated a consolidated net income of $96.8 million in the first quarter of 2020, $20.5 million or 17.5% lower than the $117.3 million in the first quarter of 2019. The decrease in net income was mainly due to the lower contributions of the following subsidiaries:

• FG Hydro’s net income contribution decreased by $7.2 million, or 50.2% to $7.2 million in the first quarter of 2020 compared to $14.4 million in the same period last year. The decrease was driven by lower average WESM selling price at P2.93/kWh in the first quarter of 2020 compared to P4.94/kWh in the same period last year, which was accompanied by lower generation of 194 GWh in the period compared to 217 GWh for the same period in 2019, on account of lower dam elevation and irrigation requirements of NIA. This was partially offset by higher revenues from ancillary services in the first quarter of 2020 compared to the same period last year.

• FGPC’s net income contribution decreased by $4.7 million, or 17.6% to $21.8 million in the first quarter of 2020 from $26.5 million in the same period last year. This was a result of higher staff

14 | P a g e

costs and taxes and licenses. This was partially offset by lower interest expenses as a result of a decrease in LIBOR rates and the reversal from a foreign exchange loss in 2019 to a foreign exchange gain in 2020.

• EDC’s net income contribution (ex-hydro) decreased by $4.2 million, or 7.2% to $54.0 million in the first quarter of 2020 from $58.2 million in the same period last year. This was mainly due to lower sales volume from Unified Leyte, Palinpinon, and Mindanao. The ULGEI, Nasulo, and Tongonan plants also suffered from lower average contracted and WESM selling prices in 2020. Net income was further reduced by lower insurance claim proceeds received in 2020 compared to the same period last year. The above decreases were partially offset by lower interest expenses due to a partial redemption of EDC’s $211.0 million Bond amounting to $29.9 million in February 2019 and the full repayment of EDC’s term loans with various banks totaling to P3.7 billion in 2019.

• PMPC’s net loss contribution increased by $2.0 million to a $2.2 million loss in the first quarter of 2020 from a $0.2 million loss in the same period last year. This was a result of lower average WESM prices of P4.73/kWh in the first quarter of 2020 from P9.03/kWh in the same period last year. This resulted from lower dispatch at 4.9% for the first quarter of 2020 compared to 15.7% in the same period in 2019 but was partially offset by lower fuel prices and the absence of maintenance works performed in the same period last year.

• FNPC’s net income contribution decreased by $1.2 million, or 11.6% to $8.8 million in the first

quarter of 2020 from $10.0 million in the same period last year largely driven by San Gabriel’s lower capacity fees billed to Meralco due to its scheduled maintenance outage in January 2020 and incurred higher G&A expenses for the period. These were partially offset by the absence of replacement power purchases during its extended maintenance outage in the first quarter of 2019.

Net Income Attributable to Equity Holders of the Parent Company Net income attributable to the equity holders of the Parent Company decreased by $15.9 million, or 19.6% to $65.2 million in the first quarter of 2020, compared to $81.1 million recognized in the same period last year. The decrease in attributable net income was mainly due to the lower contributions of the following subsidiaries:

• The Company’s wholly owned subsidiaries for its natural gas platform; namely, FGPC, FNPC, and PMPC recognized lower income in the first quarter of 2020 compared to the same period in 2019, as discussed above.

• EDC’s contribution to net income attributable to the Parent Company decreased by $1.9 million, or

6.7% to $25.8 million in the first quarter of 2020 from $27.7 million in the same period last year, as discussed above.

• FG Hydro’s contribution to net income attributable to the Parent Company decreased by

$4.9 million, or 50.2% to $4.8 million in the first quarter of 2020 compared to $9.7 million in the same period last year, as discussed above.

15 | P a g e

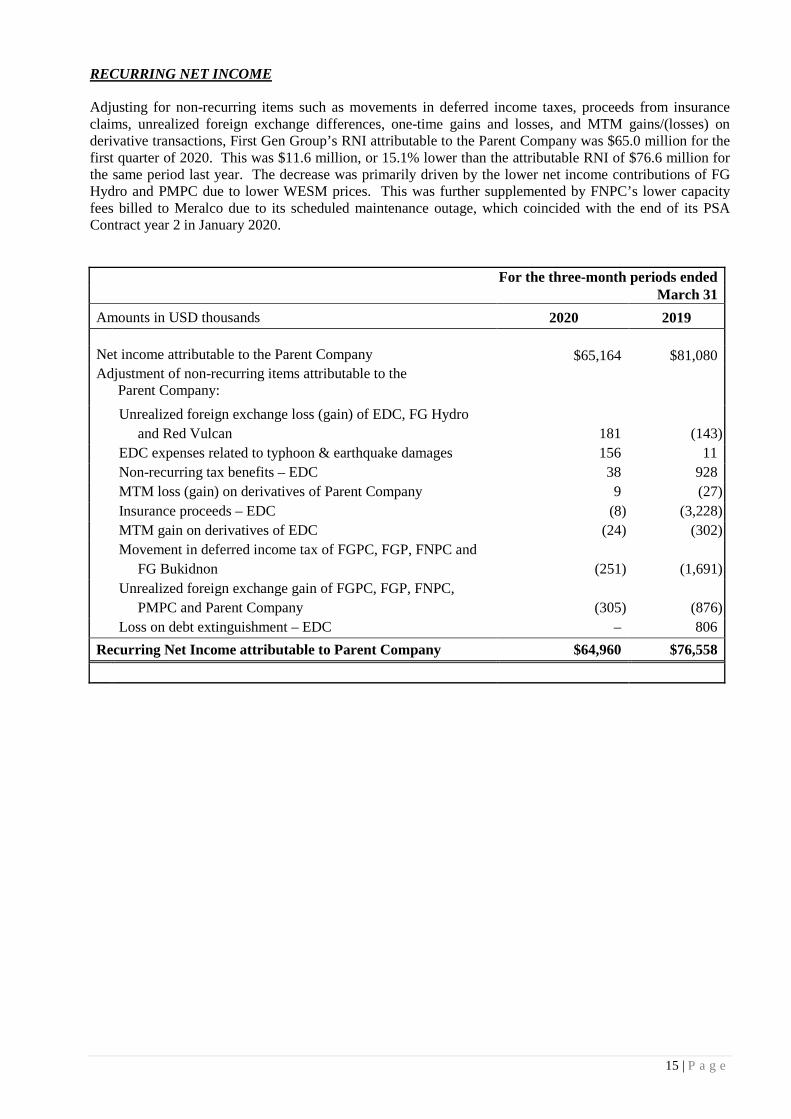

RECURRING NET INCOME Adjusting for non-recurring items such as movements in deferred income taxes, proceeds from insurance claims, unrealized foreign exchange differences, one-time gains and losses, and MTM gains/(losses) on derivative transactions, First Gen Group’s RNI attributable to the Parent Company was $65.0 million for the first quarter of 2020. This was $11.6 million, or 15.1% lower than the attributable RNI of $76.6 million for the same period last year. The decrease was primarily driven by the lower net income contributions of FG Hydro and PMPC due to lower WESM prices. This was further supplemented by FNPC’s lower capacity fees billed to Meralco due to its scheduled maintenance outage, which coincided with the end of its PSA Contract year 2 in January 2020.

For the three-month periods ended March 31

Amounts in USD thousands 2020 2019 Net income attributable to the Parent Company $65,164 $81,080 Adjustment of non-recurring items attributable to the

Parent Company:

Unrealized foreign exchange loss (gain) of EDC, FG Hydro and Red Vulcan

181

(143)

EDC expenses related to typhoon & earthquake damages 156 11 Non-recurring tax benefits – EDC 38 928 MTM loss (gain) on derivatives of Parent Company 9 (27) Insurance proceeds – EDC (8) (3,228) MTM gain on derivatives of EDC (24) (302)

Movement in deferred income tax of FGPC, FGP, FNPC and

FG Bukidnon

(251)

(1,691)

Unrealized foreign exchange gain of FGPC, FGP, FNPC, PMPC and Parent Company

(305)

(876)

Loss on debt extinguishment – EDC – 806

Recurring Net Income attributable to Parent Company $64,960 $76,558

16 | P a g e

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION

Horizontal and Vertical Analyses of Material Changes as of March 31, 2020 and December 31, 2019

Cash and cash equivalents Cash and cash equivalents increased by $106.6 million, or 17.1% to $730.5 million as of March 31, 2020 from $623.9 million as of December 31, 2019 mainly due to higher cash generated from operating activities, redemptions of financial assets at FVPL during the period and lower debt and interest payments. This was partially offset by a payment of preferred dividends in January and payment of dividends to EDC’s minority shareholders.

March 31, 2020 Dec. 31, 2019 HORIZONTAL ANALYSIS VERTICAL ANALYSIS

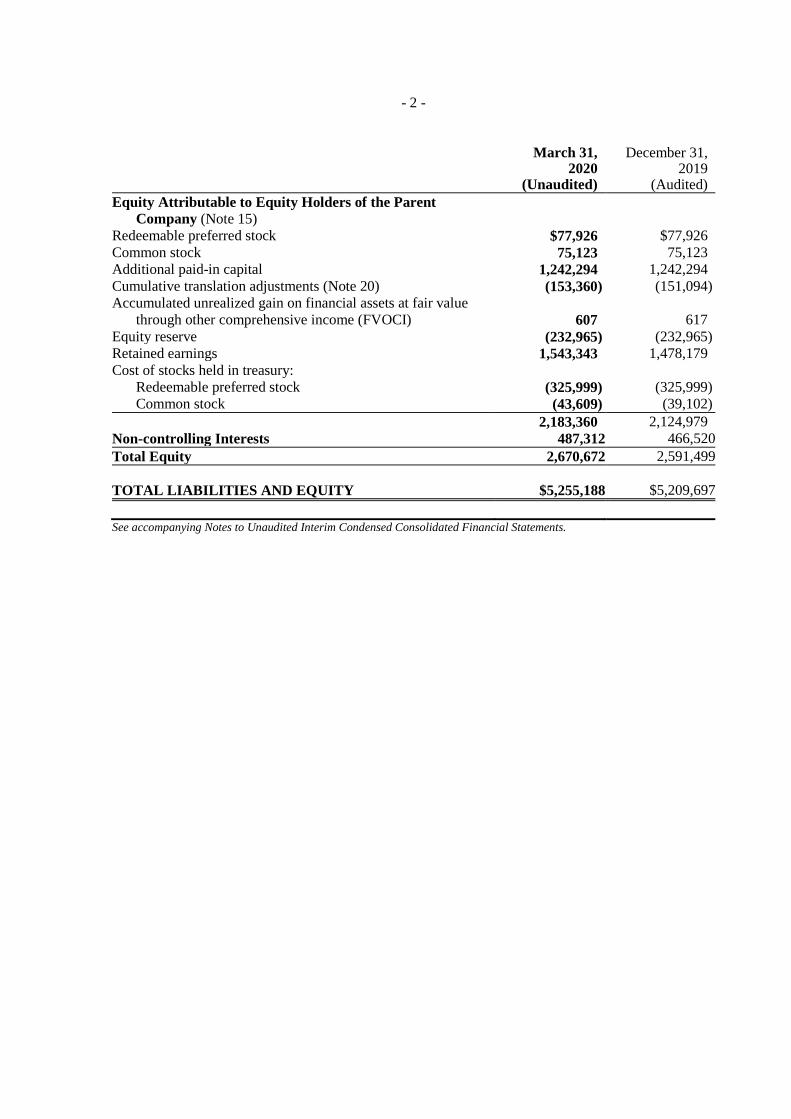

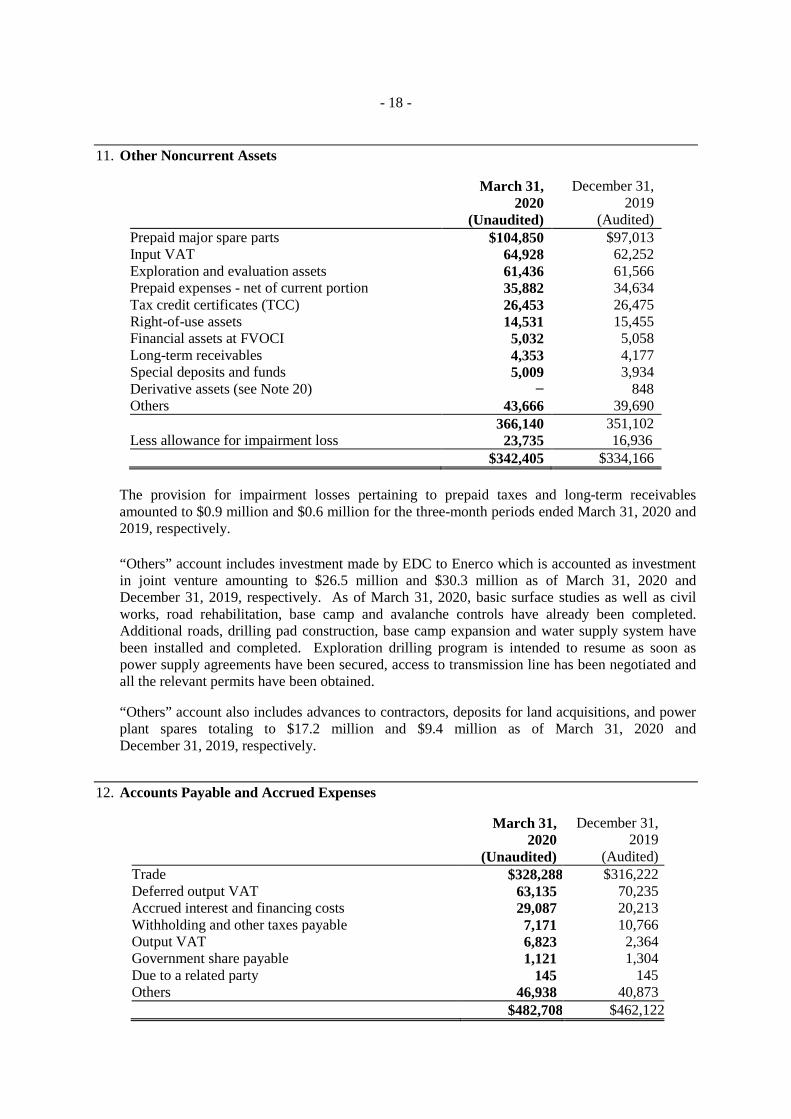

(Amounts in US$ and in Thousands) (Unaudited) (Audited) 2020 vs. 2019 2020 vs. 2019 March 31, 2020 Dec. 31, 2019ASSETSCurrent AssetsCash and cash equivalents $730,483 $623,881 $106,602 17.1% 13.9% 12.0%Receivables 445,347 434,689 10,658 2.5% 8.5% 8.3%Inventories 131,724 128,876 2,848 2.2% 2.5% 2.5%Financial assets at fair value through profit or loss (FVPL) 16,310 30,848 (14,538) -47.1% 0.3% 0.6%Other current assets 56,875 82,071 (25,196) -30.7% 1.1% 1.6%Total Current Assets 1,380,739 1,300,365 80,374 6.2% 26.3% 25.0%Noncurrent AssetsProperty, plant and equipment – net 2,513,000 2,549,930 (36,930) -1.4% 47.8% 48.9%Goodwill and intangible assets 996,668 1,000,853 (4,185) -0.4% 19.0% 19.2%Deferred income tax assets – net 22,376 24,383 (2,007) -8.2% 0.4% 0.5%Other noncurrent assets 342,405 334,166 8,239 2.5% 6.5% 6.4%Total Noncurrent Assets 3,874,449 3,909,332 (34,883) -0.9% 73.7% 75.0%TOTAL ASSETS $5,255,188 $5,209,697 $45,491 0.9% 100.0% 100.0%

LIABILITIES AND EQUITYCurrent LiabilitiesAccounts payable and accrued expenses $482,708 $462,122 $20,586 4.5% 9.2% 8.9%Income tax payable 22,137 9,335 12,802 137.1% 0.4% 0.2%Loans payable 12,493 12,493 - 0.0% 0.2% 0.2%Dividends payable - 53,784 (53,784) -100.0% 0.0% 1.0%Current portion of:

Long-term debts 491,177 300,100 191,077 63.7% 9.3% 5.8%Lease liabilities 3,965 4,006 (41) -1.0% 0.1% 0.1%Derivative liabilities 1,250 425 825 194.1% 0.0% 0.0%

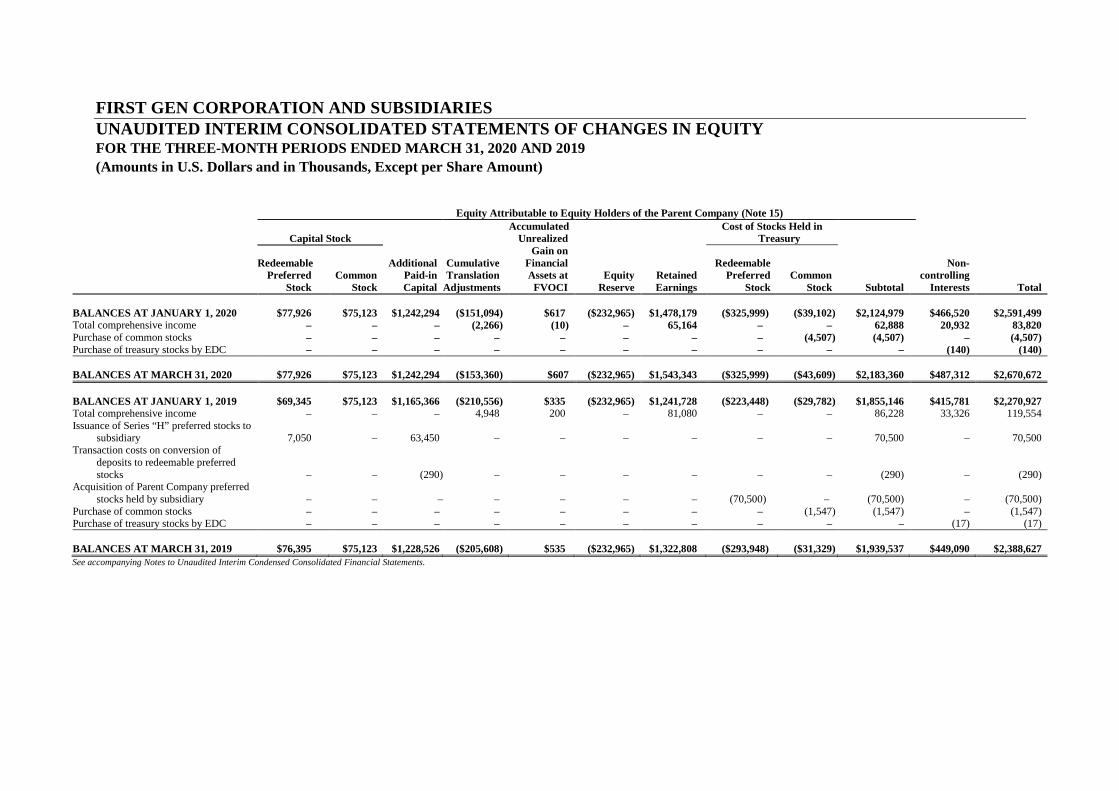

Total Current Liabilities 1,013,730 842,265 171,465 20.4% 19.3% 16.2%Noncurrent Liabilities Long-term debts – net of current portion 1,407,438 1,621,969 (214,531) -13.2% 26.8% 31.1%Retirement and other post-employment benefits 39,982 38,437 1,545 4.0% 0.8% 0.7%Derivative liabilities – net of current portion 12,556 5,125 7,431 145.0% 0.2% 0.1%Deferred income tax liabilities – net 22,669 23,062 (393) -1.7% 0.4% 0.4%Other noncurrent liabilities 88,141 87,340 801 0.9% 1.7% 1.7%Total Noncurrent Liabilities 1,570,786 1,775,933 (205,147) -11.6% 29.9% 34.1%Total Liabilities 2,584,516 2,618,198 (33,682) -1.3% 49.2% 50.3%Equity Attributable to Equity Holders of the Parent CompanyRedeemable preferred stock 77,926 77,926 0 0.0% 1.5% 1.5%Common stock 75,123 75,123 0 0.0% 1.4% 1.4%Additional paid-in capital 1,242,294 1,242,294 0 0.0% 23.6% 23.8%Cumulative translation adjustments (153,360) (151,094) (2,266) 1.5% -2.9% -2.9%Accumulated unrealized gain on financial assets at fair value through other comprehensive income (FVOCI) 607 617 (10) -1.6% 0.0% 0.0%Equity reserve (232,965) (232,965) 0 0.0% -4.4% -4.5%Retained earnings 1,543,343 1,478,179 65,164 4.4% 29.4% 28.4%Cost of stocks held in treasury: 0.0%

Redeemable preferred stock (325,999) (325,999) 0 0.0% -6.2% -6.3%Common stock (43,609) (39,102) (4,507) 11.5% -0.8% -0.8%

Sub-total 2,183,360 2,124,979 58,381 2.7% 41.5% 40.8%Non-controlling Interests 487,312 466,520 20,792 4.5% 9.3% 9.0%Total Equity 2,670,672 2,591,499 79,173 3.1% 50.8% 49.7%TOTAL LIABILITIES AND EQUITY $5,255,188 $5,209,697 $45,491 0.9% 100.0% 100.0%

17 | P a g e

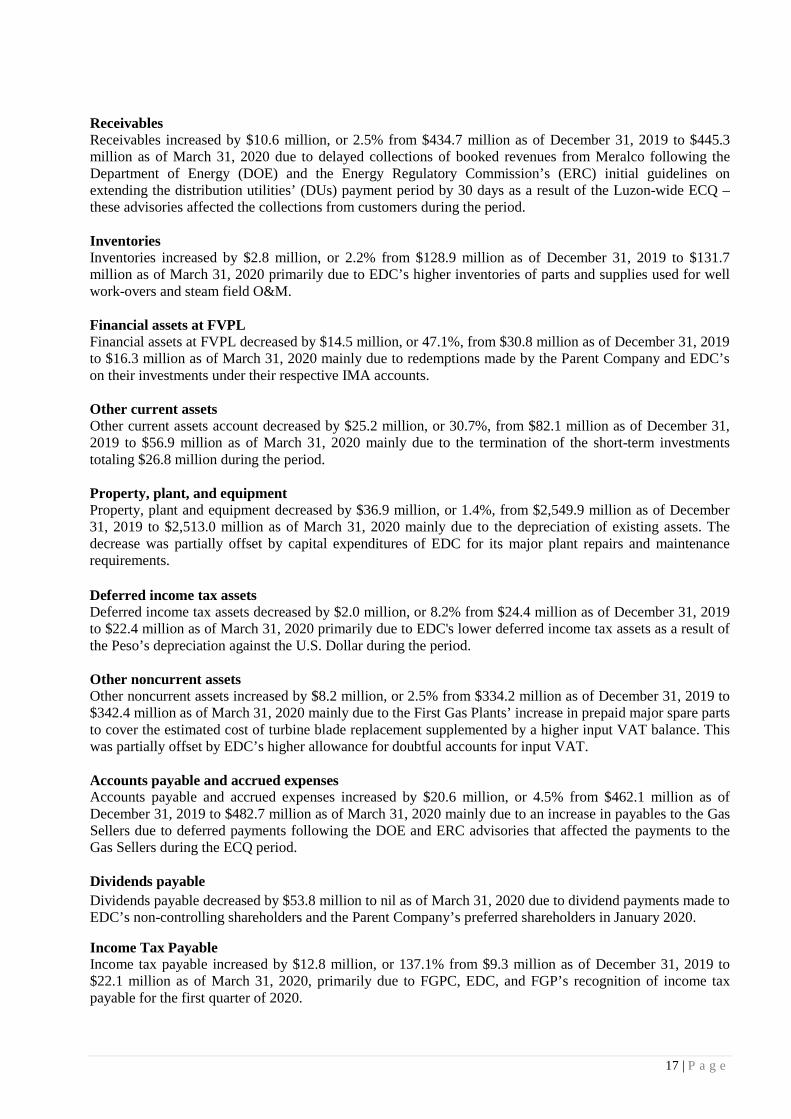

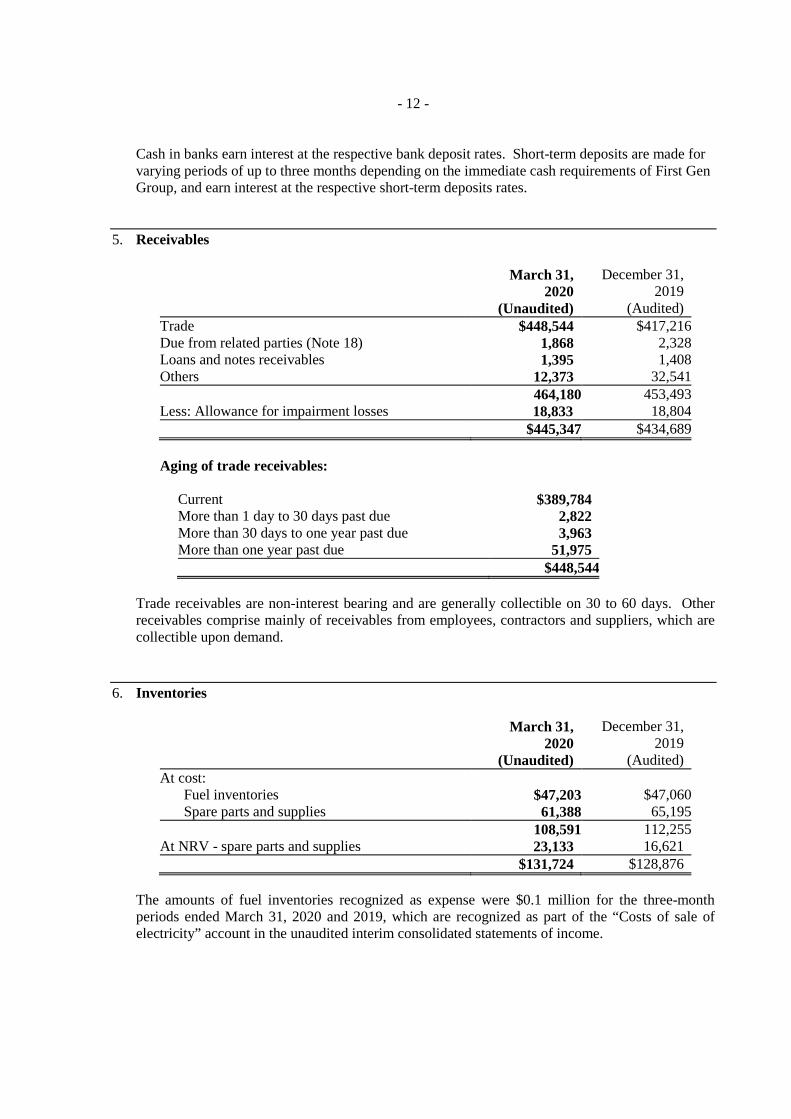

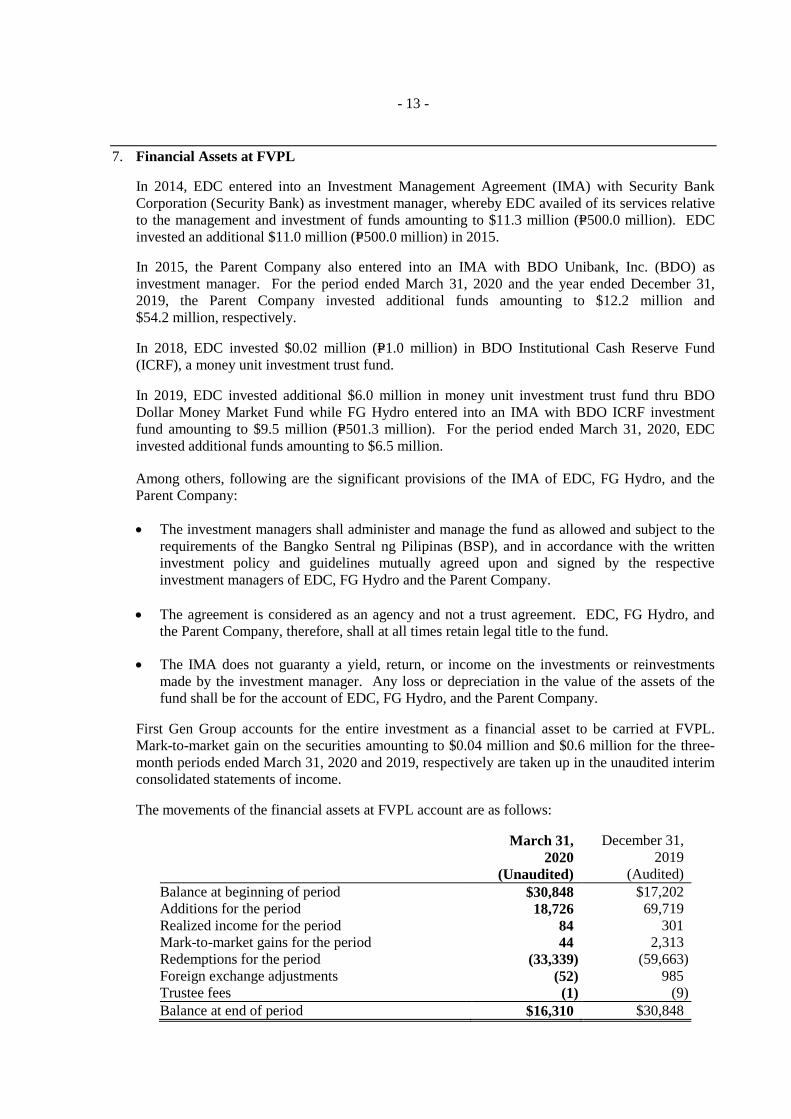

Receivables Receivables increased by $10.6 million, or 2.5% from $434.7 million as of December 31, 2019 to $445.3 million as of March 31, 2020 due to delayed collections of booked revenues from Meralco following the Department of Energy (DOE) and the Energy Regulatory Commission’s (ERC) initial guidelines on extending the distribution utilities’ (DUs) payment period by 30 days as a result of the Luzon-wide ECQ – these advisories affected the collections from customers during the period. Inventories Inventories increased by $2.8 million, or 2.2% from $128.9 million as of December 31, 2019 to $131.7 million as of March 31, 2020 primarily due to EDC’s higher inventories of parts and supplies used for well work-overs and steam field O&M. Financial assets at FVPL Financial assets at FVPL decreased by $14.5 million, or 47.1%, from $30.8 million as of December 31, 2019 to $16.3 million as of March 31, 2020 mainly due to redemptions made by the Parent Company and EDC’s on their investments under their respective IMA accounts. Other current assets Other current assets account decreased by $25.2 million, or 30.7%, from $82.1 million as of December 31, 2019 to $56.9 million as of March 31, 2020 mainly due to the termination of the short-term investments totaling $26.8 million during the period. Property, plant, and equipment Property, plant and equipment decreased by $36.9 million, or 1.4%, from $2,549.9 million as of December 31, 2019 to $2,513.0 million as of March 31, 2020 mainly due to the depreciation of existing assets. The decrease was partially offset by capital expenditures of EDC for its major plant repairs and maintenance requirements. Deferred income tax assets Deferred income tax assets decreased by $2.0 million, or 8.2% from $24.4 million as of December 31, 2019 to $22.4 million as of March 31, 2020 primarily due to EDC's lower deferred income tax assets as a result of the Peso’s depreciation against the U.S. Dollar during the period. Other noncurrent assets Other noncurrent assets increased by $8.2 million, or 2.5% from $334.2 million as of December 31, 2019 to $342.4 million as of March 31, 2020 mainly due to the First Gas Plants’ increase in prepaid major spare parts to cover the estimated cost of turbine blade replacement supplemented by a higher input VAT balance. This was partially offset by EDC’s higher allowance for doubtful accounts for input VAT. Accounts payable and accrued expenses Accounts payable and accrued expenses increased by $20.6 million, or 4.5% from $462.1 million as of December 31, 2019 to $482.7 million as of March 31, 2020 mainly due to an increase in payables to the Gas Sellers due to deferred payments following the DOE and ERC advisories that affected the payments to the Gas Sellers during the ECQ period. Dividends payable Dividends payable decreased by $53.8 million to nil as of March 31, 2020 due to dividend payments made to EDC’s non-controlling shareholders and the Parent Company’s preferred shareholders in January 2020.

Income Tax Payable Income tax payable increased by $12.8 million, or 137.1% from $9.3 million as of December 31, 2019 to $22.1 million as of March 31, 2020, primarily due to FGPC, EDC, and FGP’s recognition of income tax payable for the first quarter of 2020.

18 | P a g e

Long-term debt – current portion The current portion of long-term debt increased by $191.1 million, or 63.7%, from $300.1 million as of December 31, 2019 to $491.2 million as of March 31, 2020 mainly due to the reclassification of EDC’s $181.1 million Note from the noncurrent portion of long-term debt partially offset by the scheduled loan payments of EDC and FNPC. Derivative liabilities –current portion The current portion of derivative liabilities increased by $0.8 million, or 194.1%, from $0.4 million as of December 31, 2019 to $1.2 million as of March 31, 2020 due to the unfavorable MTM valuation adjustment of EDC‘s derivative assets which are used to hedge against possible foreign exchange losses and interest rate risks resulting in a net liability position. Long-term debt – net of current portion Long-term debt decreased by $214.5 million, or 13.2%, from $1,622.0 million as of December 31, 2019 to $1,407.5 million as of March 31, 2020 mainly due to the reclassification of EDC’s $181.1 million Note from to the current portion of long-term debt as mentioned above. Retirement and other post-employment benefits This account increased by $1.6 million, or 4.0%, from $38.4 million as of December 31, 2019 to $40.0 million as of March 31, 2020 mainly due to the recognition of retirement expense provisions during the period. Derivative liabilities – net of current portion Derivative liabilities increased by $7.4 million from $5.1 million as of December 31, 2019 to $12.5 million as of March 31, 2020 mainly due to the unfavorable MTM valuation adjustment of EDC’s derivative assets which hedge against possible foreign exchange and interest rate risks resulting to a net liability position. Retained earnings Retained earnings increased by $65.2 million, or 4.4%, from $1,478.1 million as of December 31, 2019 to $1,543.3 million as of March 31, 2020. The increase was due to the First Gen Group’s attributable earnings to the Parent Company of $65.2 million for the first quarter of 2020. LIQUIDITY AND CAPITAL RESOURCES

We rely largely on operating cash flows, borrowings, and capital-raising to provide our liquidity requirements. Due to our significant operating cash flows as well as our financial assets, access to capital markets, available lines of credit, and revolving credit agreements, we believe that we have, and will maintain, the ability to meet our liquidity needs for the foreseeable future, which include:

• the working capital requirements of our operations; • investments in our business; • dividend payments; • share repurchases; • paying down outstanding debt; • contributions to our retirement plans and other post-employment benefits; and • business development activities.

The near-term outlook for our business remains sound, and we expect to generate sufficient cash flows from operations and financing activities, which will give us significant flexibility to meet our financial commitments. We normally use debt financing to lower our overall cost of capital and increase our return on stockholders' equity. We have a history of borrowing funds domestically and internationally, and continue to have the ability to borrow funds at reasonable interest rates.

19 | P a g e

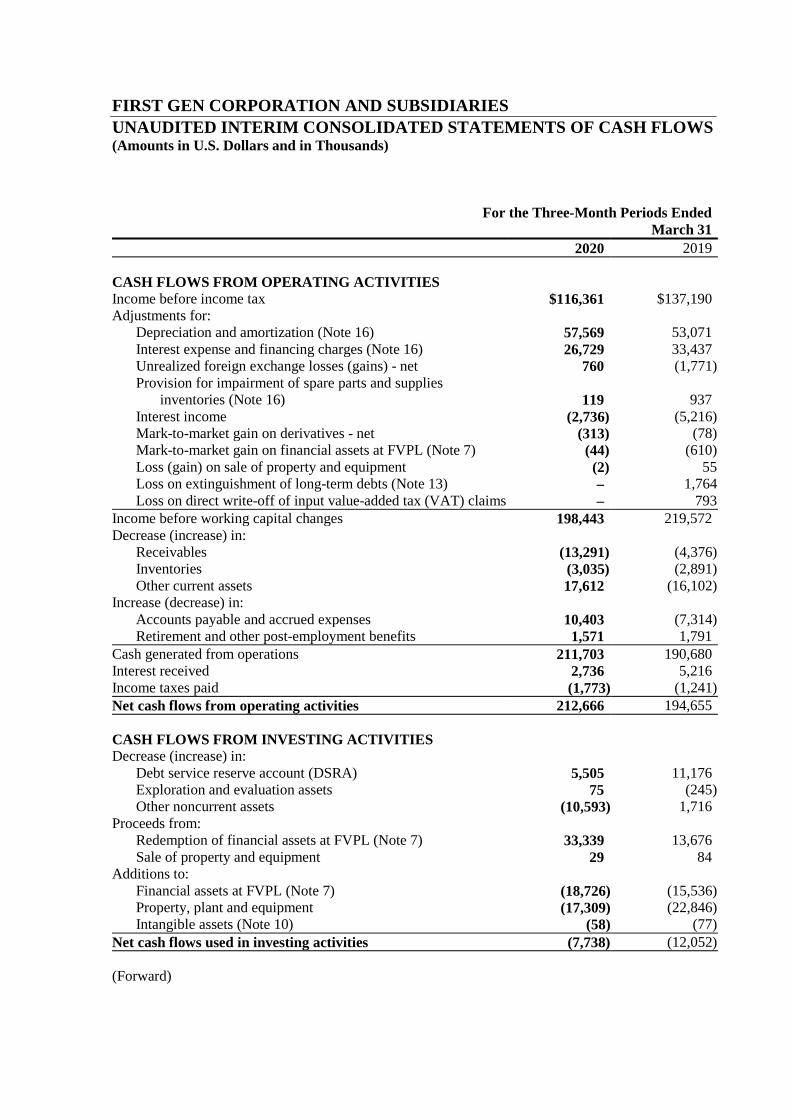

The following table shows our consolidated cash flows for the periods ended March 31, 2020 and 2019, and provides certain relevant measures of our liquidity and capital resources as of March 31, 2020 and December 31, 2019:

(in Thousand U.S. Dollars except for For the periods ended March 31 financial ratios and % change 2020 2019 Change YoY % Consolidated Cash Flows Net cash flows from operating activities $212,666 $194,655 $18,011 9.3% Net cash flows used in investing activities (7,738) (12,052) 4,314 -35.8% Net cash flows used in financing activities (98,341) (118,906) 20,565 -17.3% Total Capital Expenditures1 $17,292 $23,168 ($5,876) -25.4% Effect of foreign exchange rate changes in cash & cash equivalents $15 $798 ($783) -98.1%

1 Total capital expenditures include additions to property, plant and equipment, exploration and evaluation assets, intangible assets, and

capitalized borrowing costs for the year regardless of whether payment was made or not.

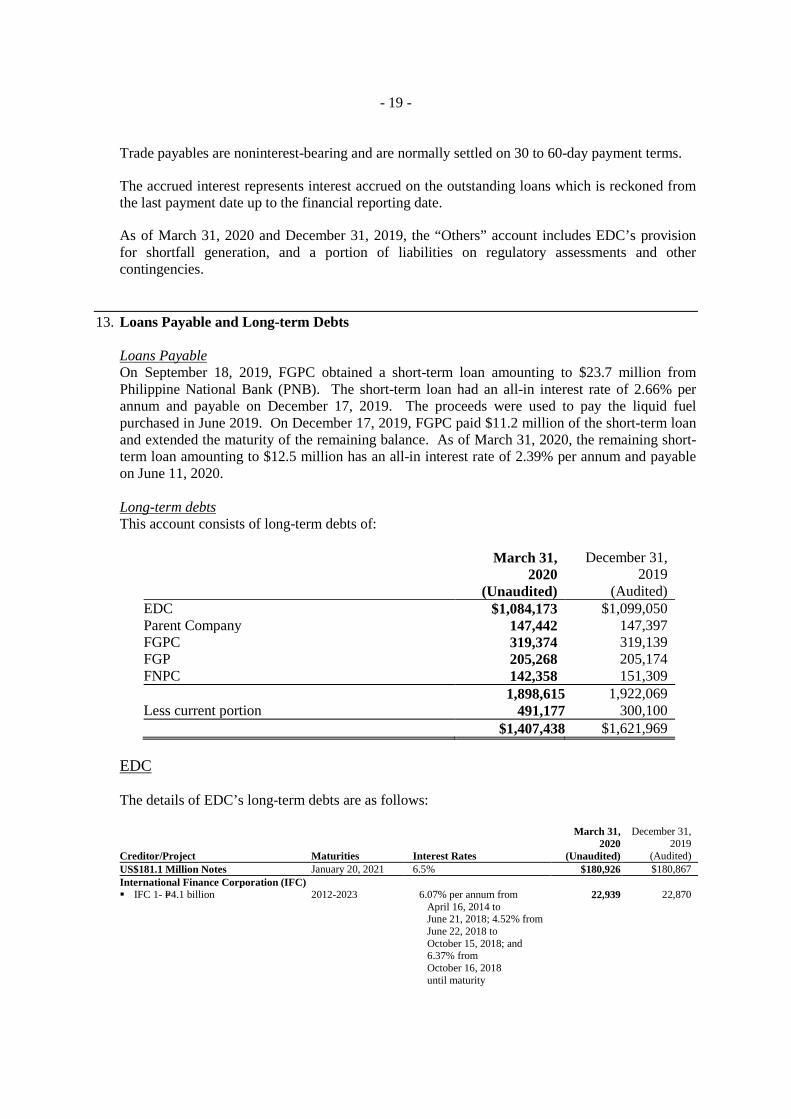

Capitalization March 2020 Dec. 2019 Change YoY % Interest-bearing debts:

Loans payable $12,493 $12,493 $0 0.0% Current portion 491,177 300,100 191,077 63.7% Noncurrent portion 1,407,438 1,621,969 (214,531) -13.2%

Total interest-bearing long-term debt 1,911,108 1,934,562 (23,454) -1.2% Total equity attributable to equity holders of the Parent Company 2,183,360 2,124,979 58,381 2.7% $4,094,468 $4,059,541 $34,927 0.9% Other Selected Financial Data March 2020 Dec. 2019 Total assets $5,255,188 $5,209,697 Cash and cash equivalents $730,483 $623,881 Financial assets at FVPL 16,310 30,848

$746,793 $654,729

The First Gen Group's total consolidated assets as of March 31, 2020 amounted to $5.3 billion, which is slightly higher by $45.5 million or 0.9%, compared to $5.2 billion as of December 31, 2019. Consolidated cash and cash equivalents and financial assets at FVPL amounted to $746.8 million as of March 31, 2020, $92.1 million or 14.1% higher compared to $654.7 million as of December 31, 2019. Principal sources of cash and cash equivalents in the first quarter of 2020 were cash generated from operations, which were partially offset by the scheduled and voluntary principal and interest payments on First Gen Group’s existing loans, payments of dividends to preferred stockholders, capital expenditures, and the buyback of common stocks. Cash Flows from Operating Activities Net cash flows from operating activities increased by $18.0 million, or 9.3% to $212.7 million in the first quarter of 2020 from $194.7 million in the same period last year. This was primarily due to the absence of short-term investments and DSRA funding booked as current assets this year, both of which reduced cash flows from operating activities last year. This was partially offset by lower EBITDA from FG Hydro, FGPC, FNPC, PMPC, and FGP.

20 | P a g e

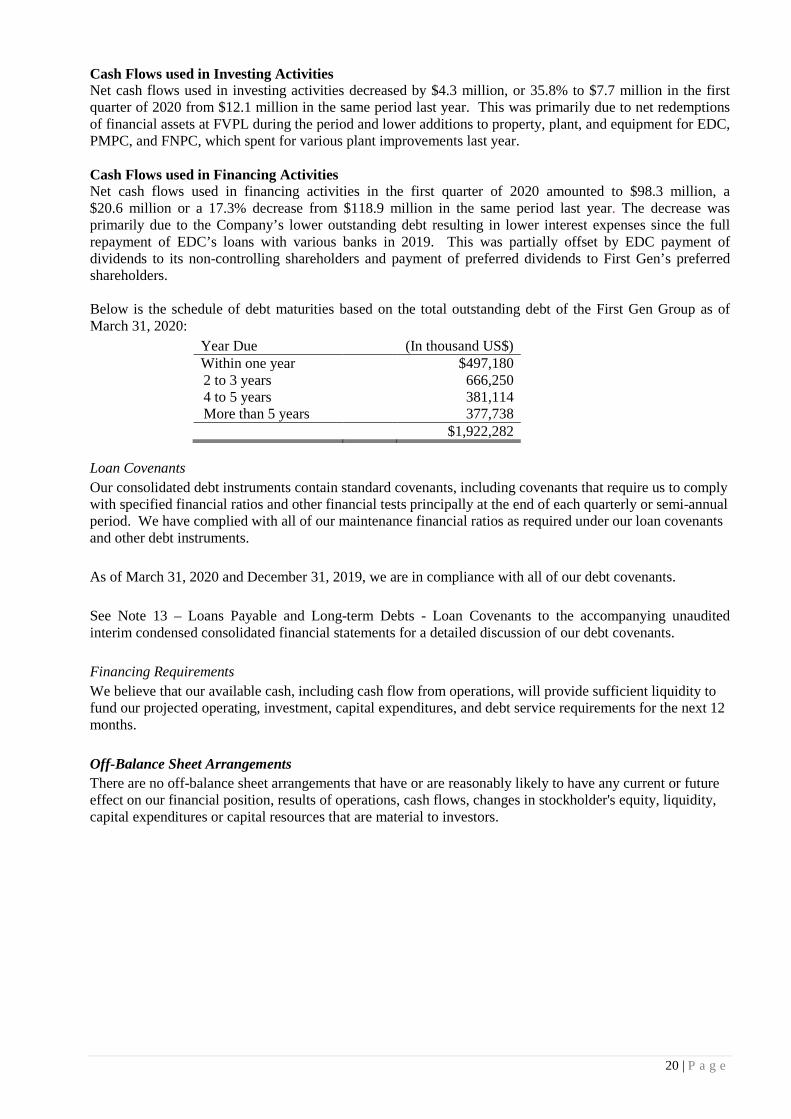

Cash Flows used in Investing Activities Net cash flows used in investing activities decreased by $4.3 million, or 35.8% to $7.7 million in the first quarter of 2020 from $12.1 million in the same period last year. This was primarily due to net redemptions of financial assets at FVPL during the period and lower additions to property, plant, and equipment for EDC, PMPC, and FNPC, which spent for various plant improvements last year. Cash Flows used in Financing Activities Net cash flows used in financing activities in the first quarter of 2020 amounted to $98.3 million, a $20.6 million or a 17.3% decrease from $118.9 million in the same period last year. The decrease was primarily due to the Company’s lower outstanding debt resulting in lower interest expenses since the full repayment of EDC’s loans with various banks in 2019. This was partially offset by EDC payment of dividends to its non-controlling shareholders and payment of preferred dividends to First Gen’s preferred shareholders. Below is the schedule of debt maturities based on the total outstanding debt of the First Gen Group as of March 31, 2020:

Year Due (In thousand US$) Within one year $497,180 2 to 3 years 666,250 4 to 5 years 381,114 More than 5 years 377,738 $1,922,282

Loan Covenants Our consolidated debt instruments contain standard covenants, including covenants that require us to comply with specified financial ratios and other financial tests principally at the end of each quarterly or semi-annual period. We have complied with all of our maintenance financial ratios as required under our loan covenants and other debt instruments. As of March 31, 2020 and December 31, 2019, we are in compliance with all of our debt covenants. See Note 13 – Loans Payable and Long-term Debts - Loan Covenants to the accompanying unaudited interim condensed consolidated financial statements for a detailed discussion of our debt covenants. Financing Requirements We believe that our available cash, including cash flow from operations, will provide sufficient liquidity to fund our projected operating, investment, capital expenditures, and debt service requirements for the next 12 months. Off-Balance Sheet Arrangements There are no off-balance sheet arrangements that have or are reasonably likely to have any current or future effect on our financial position, results of operations, cash flows, changes in stockholder's equity, liquidity, capital expenditures or capital resources that are material to investors.

21 | P a g e

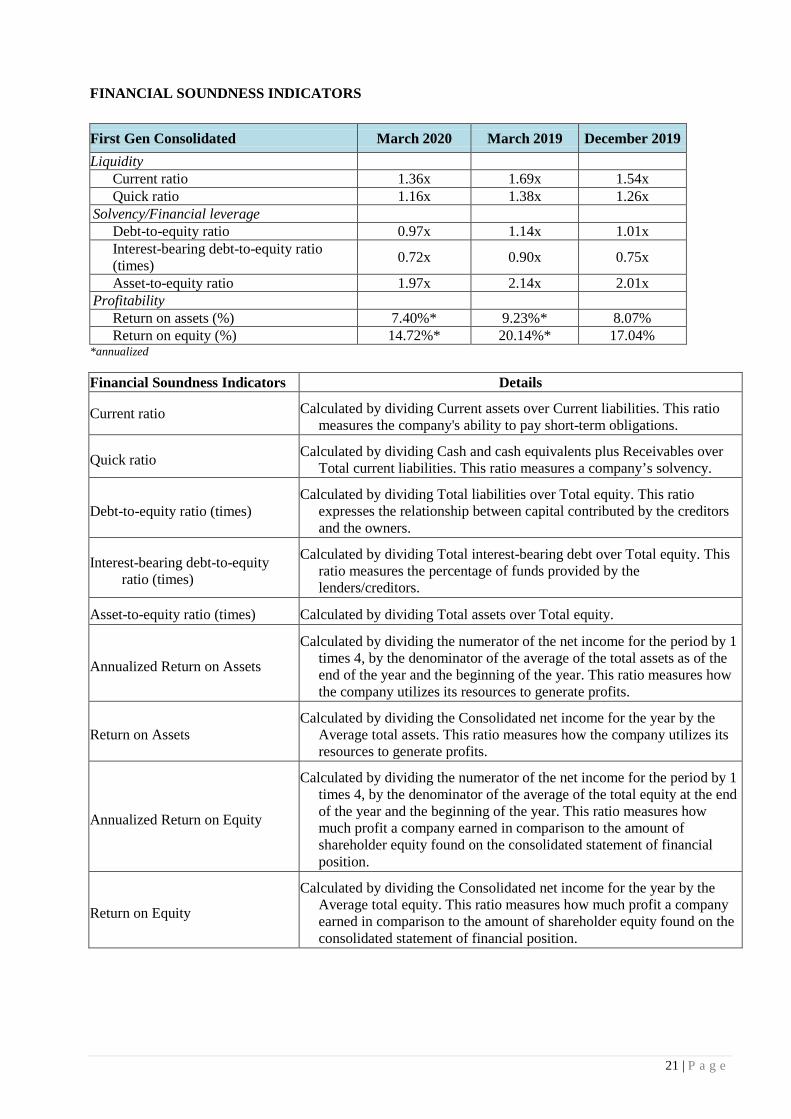

FINANCIAL SOUNDNESS INDICATORS

First Gen Consolidated March 2020 March 2019 December 2019 Liquidity

Current ratio 1.36x 1.69x 1.54x Quick ratio 1.16x 1.38x 1.26x

Solvency/Financial leverage Debt-to-equity ratio 0.97x 1.14x 1.01x Interest-bearing debt-to-equity ratio (times) 0.72x 0.90x 0.75x

Asset-to-equity ratio 1.97x 2.14x 2.01x Profitability

Return on assets (%) 7.40%* 9.23%* 8.07% Return on equity (%) 14.72%* 20.14%* 17.04%

*annualized Financial Soundness Indicators Details

Current ratio Calculated by dividing Current assets over Current liabilities. This ratio measures the company's ability to pay short-term obligations.

Quick ratio Calculated by dividing Cash and cash equivalents plus Receivables over Total current liabilities. This ratio measures a company’s solvency.

Debt-to-equity ratio (times) Calculated by dividing Total liabilities over Total equity. This ratio

expresses the relationship between capital contributed by the creditors and the owners.

Interest-bearing debt-to-equity ratio (times)

Calculated by dividing Total interest-bearing debt over Total equity. This ratio measures the percentage of funds provided by the lenders/creditors.

Asset-to-equity ratio (times) Calculated by dividing Total assets over Total equity.

Annualized Return on Assets

Calculated by dividing the numerator of the net income for the period by 1 times 4, by the denominator of the average of the total assets as of the end of the year and the beginning of the year. This ratio measures how the company utilizes its resources to generate profits.

Return on Assets Calculated by dividing the Consolidated net income for the year by the

Average total assets. This ratio measures how the company utilizes its resources to generate profits.

Annualized Return on Equity

Calculated by dividing the numerator of the net income for the period by 1 times 4, by the denominator of the average of the total equity at the end of the year and the beginning of the year. This ratio measures how much profit a company earned in comparison to the amount of shareholder equity found on the consolidated statement of financial position.

Return on Equity

Calculated by dividing the Consolidated net income for the year by the Average total equity. This ratio measures how much profit a company earned in comparison to the amount of shareholder equity found on the consolidated statement of financial position.

22 | P a g e

DISCUSSIONS OF MAJOR SUBSIDIARIES

FGPC

For the periods ended March 31 (Unaudited)

(in USD thousands) 2020 2019 Revenues from sale of electricity 158,633 171,591 Operating income 32,582 37,927 Net income 21,790 26,456 As of the periods ended

(in USD thousands) March 31, 2020 (Unaudited)

Dec. 31, 2019 (Audited)

Total Assets 779,243 724,515 Debt - net of debt issuance costs 331,867 331,632 Other Liabilities 188,461 151,304 Total Equity 258,915 241,579

March 2020 vs. March 2019 Results FGPC’s revenues decreased by $13.0 million, or 7.6% to $158.6 million in the first quarter of 2020 from $171.6 million in the same period in 2019. The decrease in revenues was primarily attributable to lower fuel revenues from natural gas consumption and lower average gas prices ($8.3/MMBtu in 2020 from $9.30/MMBtu in 2019) coupled with Sta. Rita’s lower average plant dispatch (69.8% in 2020 compared to 71.5% in 2019). However, the decrease was partially offset by Sta. Rita’s slightly higher average NDC (1,095 MW in 2020 compared to 1,091 MW in 2019). Operating income decreased by $5.3 million, or 14.1% to $32.6 million in the first quarter of 2020 primarily due to higher G&A expenses, compared to $37.9 million in the same period last year. FGPC posted a net income of $21.8 million in the first quarter of 2020, lower by $4.7 million or 17.6% from the $26.5 million of income generated in the same period in 2019. The decrease in net income was mainly due to lower operating income and lower benefit from deferred income tax. ASSETS FGPC’s total assets as of March 31, 2020 stood at $779.2 million, an increase of $54.7 million, or 7.6% higher than the balance of $724.5 million as of December 31, 2019 due to the movement in the following accounts:

• Higher ending cash balances from operations; • Higher level of trade and other receivables; and • Increase in prepaid major spare parts pending the installation of new turbine blades in the plant.

These were partially offset by:

• Depreciation and amortization of property, plant and equipment; and • Lower financial assets at Fair Value through Other Comprehensive Income (FVOCI) due to

unfavorable movements in their MTM valuation. LIABILITIES AND EQUITY FGPC’s total liabilities amounted to $520.3 million as of March 31, 2020, higher by $37.4 million or 7.7% from $482.9 million as of December 31, 2019. The increase in liabilities is primarily due to the recognition of additional income tax payable for the first quarter of 2020, interest accrual on long-term debts, and increase in outstanding accounts payable to suppliers.

23 | P a g e