Embed Size (px)

Citation preview

AKES Conference on Korea and the World Economy, XI

“New Challenge for the Korea and the World Economy in the Era of

Globalization and Polarization”

A Comparative Analysis of Korea’s Free Trade Agreements by

CGE Models: New Challenges under Globalization

Linyue Li

The Central University of Finance and Economics

June, 2012

Abstract

In this paper, the economic impacts of Korea’s possible Free Trade Agreements

(FTAs) with China, Japan, ASEAN (10)1, the United States and EU (27) are

investigated qualitatively and quantitatively. There are seven possible FTAs for Korea:

Korea – China, Korea – Japan, Korea – China & Japan, Korea – China & Japan &

ASEAN, Korea – ASEAN, Korea – United States, and Korea – EU. To conduct the

assessment, both static and dynamic CGE models with 7 regions, 12 sectors and 5

endowments are employed, assuming that skilled labor, unskilled labor, and capital

are able to be mobile among the regions, and at the same time, land and natural

resource are not mobile among the regions. The major finding is that Korea would

benefit most from a Korea – China & Japan & ASEAN FTA, which is the largest

possible FTA in East Asia. The results of this paper will be meaningful to explore

Korea’s potential FTAs with major economies and contribute to the discussion on

economic integration.

Keywords: Computable General Equilibrium (CGE) model, Free Trade Agreement

(FTA), ASEAN, China P.R., Japan

JEL Classification: F10, F14, F15

Corresponding author, assistant professor, at the department of International Trade and Economics,

the Central University of Finance and Economics, [email protected]

1 ASEAN=Association of Southeast Asian Nations, ASEAN (10) include Brunei Darussalam, Cambodia, Indonesia, Lao PDR, Malaysia, Myanmar, Philippines, Singapore, Thailand, and Viet Nam.

1

I. Introduction

After the global financial crisis, as the interdependence of countries is

growing, the impact of globalization through the increasing integration of trade,

finance, people, and ideas in one global market has been widely discussed, with world

GDP and global trade both in the process of recovering to pre-crisis levels. South

Korea, as one of the few developed countries that were able to avoid a recession

during the global financial crisis, has reached economic growth rate at 6.16% (World

Development Indicator, April 2012) in 2010, which was a sharp recovery from

economic growth rates of 2.3% in 2008 and 0.32% in 20092 when the global financial

crisis hit. Heavily dependent on international trade, South Korea is still one of the

fastest – growing countries in 2000s, with sixth largest exporter and tenth largest

importer in the world in 2010.

Since 1997 - 98 Asian Financial Crisis, Asian economies, especially Korea,

China and Japan has begun to show their continuous interest in regional economic

cooperation, while the fever for regionalism is growing in other parts of the world.

Mutual benefit with strategic cooperation in a far-reaching view is the meaning for

regional cooperation. However, Korea still implemented the trade policy consistent

with the agreements within the multilateral framework of GATT and WTO, until the

late 1990s. In the wake of the Asian Financial Crisis, both external and internal

factors led Korea to realize the importance of adopting an FTA approach with major

economies, such as Japan, ASEAN, the United States, and the European Union (Yoon

et al., 2009).

Starting with the FTA negotiations with Chile in November 1998, Korea

has successfully established FTAs with Chile in 2002, with Singapore in 2005, with

ASEAN in 2005 for goods and services and in 2009 for investment, with the United

States in 2007, with India in 2009, and with EU in 2010, and involved in FTAs with

Canada, Mexico and other countries in the world. Meanwhile, China – Japan – Korea

trilateral summit is making significant progress to promote stronger economic

cooperation and political dialogue annually for the consideration of China – Japan –

Korea FTA, since the first meeting in Manila in November 1999.

2 South Korea’s GDP growth rate in 2008 and 2009 are from World Development Indicator, World Bank,

April 2012.

2

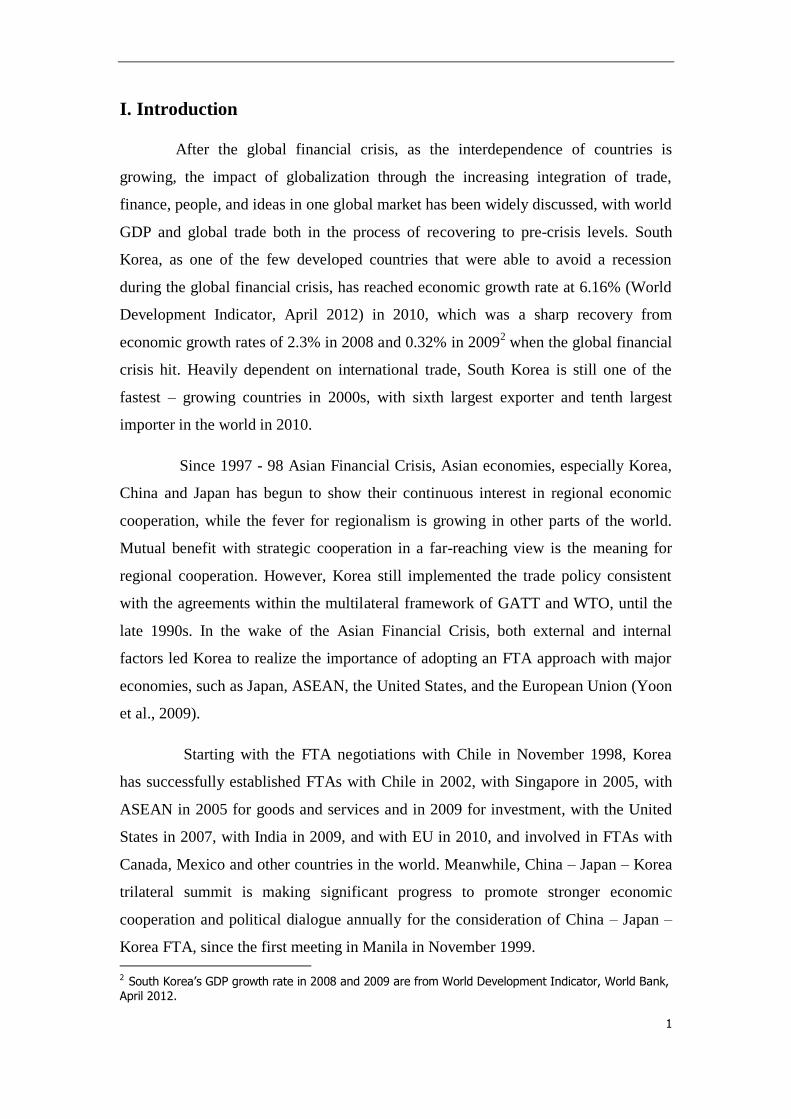

Figure 1: Exports to Korea as the Share of Total Exports among

Ranking Top 7 Economies, 1990 – 2011

Source: IMF, Direction of Trade Statistics (DOTS)

Figure 2: Imports from Korea as the Share of Total Imports among

Ranking Top 7 Economies, 1990 – 2011

Source: IMF, Direction of Trade Statistics (DOTS)

Figure 1 shows the exports to Korea as the share of total exports among

selected countries which rank top 7 economies from 1990 to 2011, while Figure 2

shows the imports from Korea as the share of total imports among ranking top 7

economies from 1990 to 2011, correspondingly. China P.R., Japan, Indonesia, the

Philippines, and Vietnam appear in both graphs, indicating South Korea’s important

3

trade position as an importer and an exporter to these countries, compared with other

7 ASEAN countries, 3 NAFTA countries and the EU as a whole.

In the first graph, the dramatic increase of Vietnam’s exports to Korea as the

share of Vietnam’s total exports during the first half of 1990s and the peak reached in

1994 illustrates the great effects from the establishment of diplomatic relations

between Vietnam and Korea in 1992. Vietnam’s major exports to Korea include

agriculture, forestry and marine products, while Vietnam’s principal imports from

Korea include petroleum oils and oils, apparel, and automobiles. Abundant human

and natural resources in Vietnam and advanced technologies in Korea make their

economic growth through win-win cooperation.

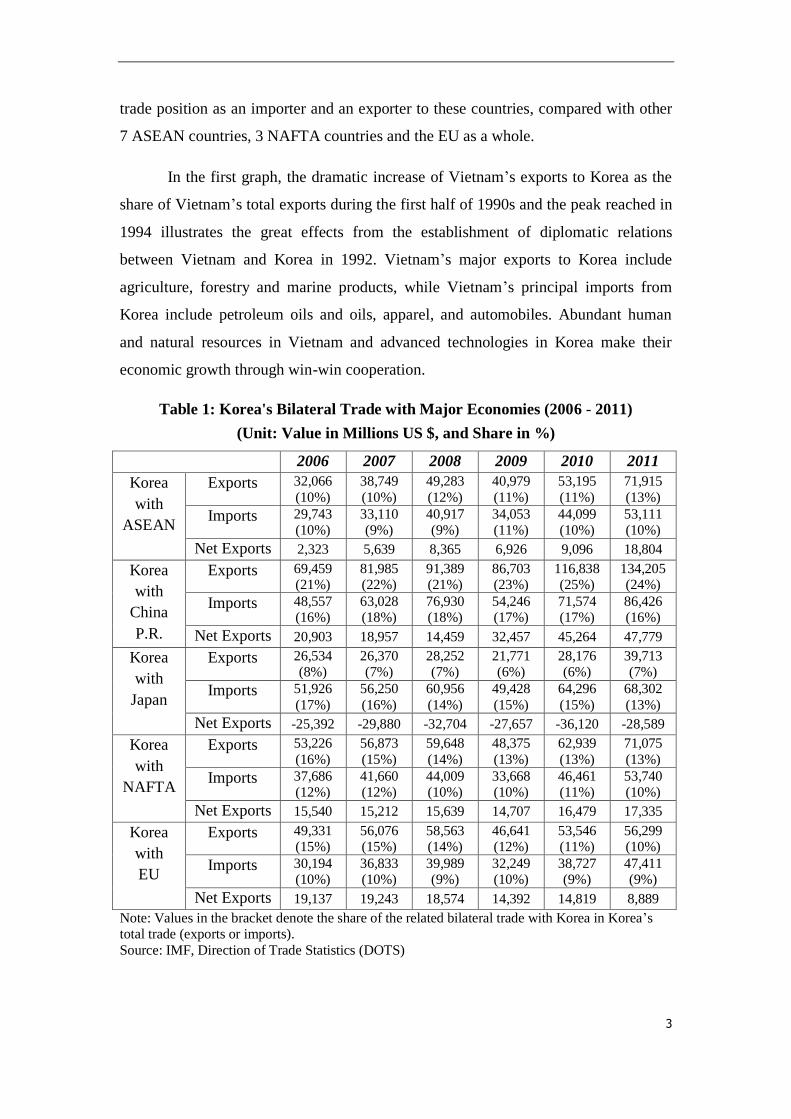

Table 1: Korea's Bilateral Trade with Major Economies (2006 - 2011)

(Unit: Value in Millions US $, and Share in %)

2006 2007 2008 2009 2010 2011

Korea

with

ASEAN

Exports 32,066

(10%)

38,749

(10%)

49,283

(12%)

40,979

(11%)

53,195

(11%)

71,915

(13%)

Imports 29,743 (10%)

33,110 (9%)

40,917 (9%)

34,053 (11%)

44,099 (10%)

53,111 (10%)

Net Exports 2,323 5,639 8,365 6,926 9,096 18,804

Korea

with

China

P.R.

Exports 69,459 (21%)

81,985 (22%)

91,389 (21%)

86,703 (23%)

116,838 (25%)

134,205 (24%)

Imports 48,557 (16%)

63,028 (18%)

76,930 (18%)

54,246 (17%)

71,574 (17%)

86,426 (16%)

Net Exports 20,903 18,957 14,459 32,457 45,264 47,779

Korea

with

Japan

Exports 26,534 (8%)

26,370 (7%)

28,252 (7%)

21,771 (6%)

28,176 (6%)

39,713 (7%)

Imports 51,926

(17%)

56,250

(16%)

60,956

(14%)

49,428

(15%)

64,296

(15%)

68,302

(13%)

Net Exports -25,392 -29,880 -32,704 -27,657 -36,120 -28,589

Korea

with

NAFTA

Exports 53,226

(16%)

56,873

(15%)

59,648

(14%)

48,375

(13%)

62,939

(13%)

71,075

(13%)

Imports 37,686 (12%)

41,660 (12%)

44,009 (10%)

33,668 (10%)

46,461 (11%)

53,740 (10%)

Net Exports 15,540 15,212 15,639 14,707 16,479 17,335

Korea

with

EU

Exports 49,331 (15%)

56,076 (15%)

58,563 (14%)

46,641 (12%)

53,546 (11%)

56,299 (10%)

Imports 30,194 (10%)

36,833 (10%)

39,989 (9%)

32,249 (10%)

38,727 (9%)

47,411 (9%)

Net Exports 19,137 19,243 18,574 14,392 14,819 8,889

Note: Values in the bracket denote the share of the related bilateral trade with Korea in Korea’s total trade (exports or imports).

Source: IMF, Direction of Trade Statistics (DOTS)

4

In the second graph, Brunei’s imports from Korea as the share of Brunei’s

total imports experienced significant increase since 1994, indicating that the trade

position of Korea in Brunei become increasingly important. Brunei’s major imports

from Korea include motor cars, heating and cooking machinery, steel products and

telephone sets, while Brunei’s major exports to Korea include mineral products,

agriculture and fishery products, and steel and metal products. Since 2006, Brunei –

Korea bilateral trade has been in favor of Brunei, with Korea’s trade deficit with

Brunei reaching 1654.3 million US $ in 2008.

From the perspective of Korea, Table 1 represents Korea’s bilateral trade

with ASEAN, China P.R., Japan, NAFTA, and EU, as the share of Korea’s total trade.

For the annual share in percentage, China P.R. takes up around a quarter of Korea’s

total exports, along with NAFTA at 14% on average, EU at about 13%, ASEAN at

about 11.2% and Japan at about 7%. The rank of Korea’s bilateral imports with

trading partners is China at 17% on average, Japan at 15% on average, NAFTA at

about 10.83%, ASEAN at about 9.83% and EU at 9.5% on average. The proportions

for these five trading partners are relatively stable during the period from 2006 to

2011, which include 2007 – 2009 the global financial crisis. Therefore, it is natural

and meaningful to discuss the possibility of adopting an FTA with each of them or the

combination of these major trading partners.

Under this background, the paper will focus on Korea’s Free Trade

Agreements (FTAs) to do a comparative analysis through computable general

equilibrium (CGE) models. The purpose of this study is to explore optimal FTAs for

the Korea and the world economy, considering new challenges under globalization

and polarization. At the same time, the research on Korea’s FTAs will contribute to

the discussion on economic integration.

The structure of this paper is organized as the follows. Section II briefly

reviews the major findings and contributions in the existing literature. Section III

describes the empirical framework in qualitative analysis and quantitative analysis. In

section IV, the results from quantitative approach through CGE model are presented

for comparative analysis in different dimensions. Section V concludes the paper and

indicates future research direction, followed by the reference.

5

II. Literature Review

A number of studies usually used a computable general equilibrium (CGE)

model with the database of the Global Trade Analysis Project (GTAP) to quantify the

economic impact of FTAs. Generally speaking, there are two types of CGE models:

static CGE model and dynamic or capital accumulation CGE model. The static model

evaluates the immediate impact of the removal of trade barriers, in the short run,

while the dynamic model incorporates medium – and long – term efficiency gains

from capital accumulation and resource re-allocation. In general, empirical studies

using dynamic CGE model often find a bigger aggregate GDP and bigger welfare

gains among member countries from an FTA, because a dynamic model incorporates

the impact of trade on growth through accumulated investment and shows higher

gains compared to the static model3. The advantage of standardized CGE model is to

derive a lot of valuable results at a relatively small expense with little effort (Yoon et

al., 2009).

CGE model is widely used to quantitatively assess changes in national

output, industry production and welfare resulting from a policy change or some

economic shock, especially for the trade policy studies. To analyze the effects of

changes in trade policy, such as regional trade agreements and multilateral trade

liberalization negotiations, CGE model has been extensively used to do analysis. For

example, Hertel et al. (2001) used the CGE model to analyze the economic impacts of

an FTA between Singapore and Japan. Tongzon (2001) investigated the influence of

China’s entry into WTO on the other East Asian countries.

To examine and quantify the effects of a trilateral FTA for Northeast Asia,

Ko (2000), Lee, J.W. (2002), Abe (2003), Park (2004), Lee et al. (2005), and Yoon et

al. (2009) all applied a CGE model to assess the economic impacts of the FTA.

However, due to different underlying assumptions and specifications, such as the

version of the Global Trade Analysis Project (GTAP) database, the type of CGE

model and the scenarios used to assess the effects of trade liberalization, the literature

on FTAs has produced varying results on the value of estimated economic impacts.

3 Please see ADB working paper “The PRC’s Free Trade Agreements with ASEAN, Japan, and the Republic of Korea: A Comparative Analysis” by Gemma Estrada, Donghyun Park, Innwon Park, and

Soonchan Park, January, 2012.

6

In the literature to study Korea’s FTA with China and Japan, Yoon et al.

(2009) made contribution to compare the macroeconomic and sector effects of

bilateral agreements or a trilateral FTA among China, Korea and Japan. Based on

their results, from the perspective of Korea, Korea’s FTA with China is most

beneficial for Korea, while China’s FTA with Korea and Japan will generate most

beneficial results for China, considering four possible FTA scenarios among China,

Japan, and Korea (Yoon et al., 2007 and 2009).

As China’s role in East Asia’s recovery from the recent global financial

crisis highlighted China’s growing role as an engine of growth not only for Asia, but

also for the world, there are many potential gains from entering into FTAs with China,

for the countries who collectively from a large and fast-growing market. Therefore,

Korea’s three possible FTAs with China: Korea – China FTA, Korea – China & Japan

FTA and Korea – China & Japan & ASEAN FTA will be focused on. The discussion

on the results of Korea – China & Japan FTA is meaningful for China – Korea –

Japan trilateral cooperation and the East Asian community, after the trilateral summit

held in Seoul, 2012. However, previous literatures on this study rarely do

comparisons of Korea’s existing and potential FTAs with China, Japan, ASEAN,

NAFTA and EU through both static CGE model and dynamic CGE model. The

inspiration of writing this paper is to fill this gap with updated database (GTAP

database 7), CGE model and latest information about status of Korea’s FTA (See

Table 2). The contribution of this paper is to highlight the existing and potential

impacts of Korea’s FTAs with China, Japan, ASEAN, NAFTA, and EU.

In addition, different from most of the previous studies, this paper will do a

comparative analysis mainly in two different dimensions. For the first dimension, the

welfare and output effects from trade for Korea’s 7 possible FTAs will be compared

through either static CGE model or dynamic CGE model. For the second dimension,

the results from static CGE model and dynamic CGE model will be compared for

each possible FTA. In the process of comparative analysis, quantitative and

qualitative analysis will be combined to do explanation. New challenges in the era of

globalization and polarization, such as changing global economy, the dynamic cost of

polarization against the potential dynamic benefits, fragile recovery from recession,

business cycle transmission through trade channel and the transmission of negative

7

effects from EU crisis will be considered in the discussion on the possibility to realize

the optimal FTAs which are likely to be mutually beneficial for both Korea and

Korea’s trading partner, further promoting the cooperation for Korea and the world

economy.

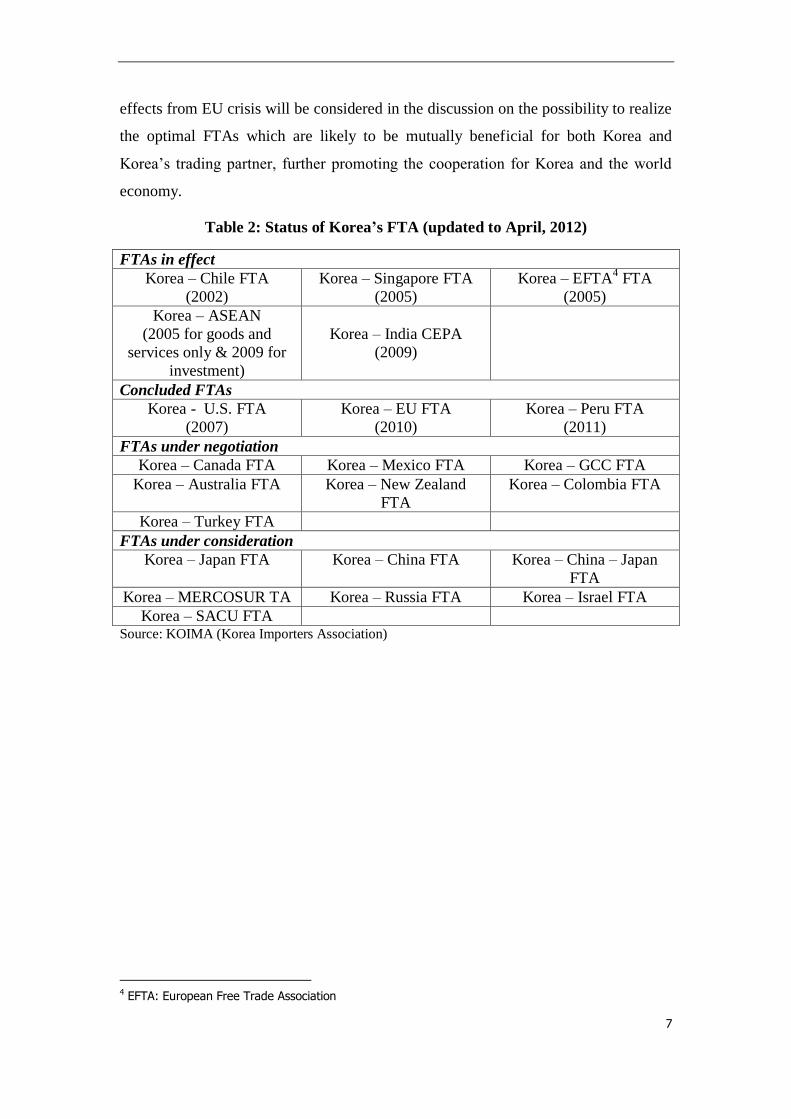

Table 2: Status of Korea’s FTA (updated to April, 2012)

FTAs in effect

Korea – Chile FTA

(2002)

Korea – Singapore FTA

(2005)

Korea – EFTA4 FTA

(2005)

Korea – ASEAN

(2005 for goods and

services only & 2009 for

investment)

Korea – India CEPA

(2009)

Concluded FTAs

Korea - U.S. FTA

(2007)

Korea – EU FTA

(2010)

Korea – Peru FTA

(2011)

FTAs under negotiation

Korea – Canada FTA Korea – Mexico FTA Korea – GCC FTA

Korea – Australia FTA Korea – New Zealand

FTA

Korea – Colombia FTA

Korea – Turkey FTA

FTAs under consideration

Korea – Japan FTA Korea – China FTA Korea – China – Japan

FTA

Korea – MERCOSUR TA Korea – Russia FTA Korea – Israel FTA

Korea – SACU FTA Source: KOIMA (Korea Importers Association)

4 EFTA: European Free Trade Association

8

III. Empirical Framework

Empirical framework consists of qualitative approach and quantitative

approach, since qualitative analysis and quantitative analysis could complement each

other to probe deeply into the potential impacts of Korea’s different FTAs. Qualitative

analysis which starts with the comparison of static factors could lay a foundation for

further quantitative analysis.

In terms of qualitative approach, economic index, such as GDP, GDP-PPP,

population, total trade volume and geographical distance with Korea, are applied as

important indicators to do qualitative analysis, comparatively. Since previous studies

have shown that the potential gains from an FTA tend to increase with membership

size and the size of the free trade area, on the one hand; On the other hand, countries

or economies with close geographical proximity tend to engage in trade with each

other, especially those linked by efficient transport systems.

Table 3 represents a comparison of the sizes of Korea’s actual and

potential trading partners for FTAs, in terms of GDP in current US dollars, GDP

based on purchase power parity (GDP – PPP), population, land area and total trade

volume. To compare Korea’s existing and potential FTAs qualitatively, the sum of

sizes for member countries in FTAs will be calculated. For example, Korea – China

FTA is 1014.48+5926.61=6941.09 for GDP in current billion US $,

1422.31+10169.5=11591.81 for GDP – PPP in current billion US $,

48.88+1338.30=1387.18 for population in million people. Through simple calculation

and comparison, the size of Korea’s FTAs could be ranked as follows. For GDP in

current US $, Korea – NAFTA FTA (KNAFTA)>Korea – EU FTA (KEU)>Korea

– ASEAN & China & Japan FTA (KCJ+ASEAN)>Korea – China & Japan FTA

(KCJ)>Korea – China FTA (KC)>Korea – Japan FTA (KJ) >Korea – ASEAN

FTA (KASEAN); For GDP – PPP, KNAFTA>KEU>KCJ+ASEAN>KC>KCJ>

KJ>KASEAN; For population, KCJ+ASEAN>KCJ>KC>KASEAN>KEU>

KNAFTA>KJ; For land area, KNAFTA>KCJ+ASEAN>KC>KCJ>KASEAN>

KEU>KJ; For total trade volume, KEU>KCJ+ASEAN>KNAFTA>KCJ>KC>

9

KASEAN>KJ. Therefore, Korea – ASEAN & China & Japan FTA and Korea –

NAFTA FTA have relative comparative advantage in sizes, and Korea – Japan FTA

has relative comparative disadvantage in term of sizes. In terms of geographical

proximity with Korea, negative effects are involved as the geographical distance with

Korea increases. The rank in terms of geographical proximity is KCJ>KC>KJ>

KASEAN>KCJ+ASEAN>KEU>KNAFTA, indicating that Korea – NAFTA FTA

has relative comparative disadvantage and Korea – China & Japan has relative

comparative advantage in terms of geographical proximity. In addition, development

levels among member countries of an actual or potential FTA matter for successful

integration. To some extent, the development levels could be measured by annual

GDP growth rate. In terms of annual GDP growth rate, Korea is close to ASEAN

(average) and Japan. Based on the above three aspects of the indicators,

comprehensive results for qualitative analysis implies that Korea – ASEAN & China

& Japan FTA, Korea – China FTA and Korea – China & Japan FTA could generate

larger output effects and welfare effects, compared with other combination of Korea’s

FTAs. The results from the qualitative approach are expected to be consistent with the

results from the quantitative approach.

In terms of quantitative analysis, computable general equilibrium (CGE)

model in both static and dynamic forms will be applied to assess the effects of future

policy changes. The CGE analysis developed by Purdue University through global

trade analysis project can capture the outcomes of complicated interactions among

diverse economic activities by incorporating all economic activities into the

theoretical model. This paper utilizes GTAP database version 7, which uses 2004 as

the reference year, including 87 regions and 57 sectors. The databases derived from

individual country input-output tables, consists of regional input – output data,

macroeconomic data, bilateral trade flows, trade protection and energy data. For the

simulation for Korea’s different FTAs, the GTAPAgg6p5 is used to aggregate the

date into 7 regions, 12 sectors (See Table 4), and 5 endowments, assuming that skilled

labor, unskilled labor, and capital are able to be mobile among the regions, and at the

same time, land and natural resource are not mobile among the regions.

10

Table 3: Comparison of Economic Index in 2010

GDP

annual

growth

(%)

GDP

(current

billion

US $)

GDP-

PPP

(billion

$)

Populatio

n, total

(million)

Land

area (sq.

thousand

km)

Trade

volume

(billion

US $)

Geographic

al distance

with

Korea

(km) (%) (%) (%) (%) (%)

Brunei

Darussalam -1.77

14.50 20.20 0.40 5.27 11.39 3819

(0.02) (0.03) (0.01) (0.004) (0.03)

Cambodia 5.96 11.24 31.02 14.14 176.52 14.77

3629 (0.02) (0.04) (0.21) (0.14) (0.04)

Indonesia 6.10 706.56 1037.50 239.87 1811.57 328.38

5278 (1.12) (1.35) (3.48) (1.40) (0.89)

Lao PDR 8.45 7.30 15.82 6.20 230.80 4.58

3208 (0.01) (0.02) (0.09) (0.18) (0.01)

Malaysia 7.19 237.80 418.37 28.40 328.55 421.21

4609 (0.38) (0.55) (0.41) (0.25) (1.14)

Myanmar 10.42 84.03 93.54 47.96 653.52 13.37

3688 (0.13) (0.12) (0.70) (0.50) (0.04)

Philippines 7.63 199.59 370.18 93.26 298.17 138.24

2614 (0.32) (0.48) (1.35) (0.23) (0.37)

Singapore 14.47 208.77 294.12 5.08 0.70 878.98

4667 (0.33) (0.38) (0.07) (0.001) (2.38)

Thailand 7.81 318.52 591.26 69.12 510.89 434.69

3719 (0.50) (0.77) (1.00) (0.39) (1.18)

Vietnam 6.78 106.43 278.62 86.93 310.07 166.91

2744 (0.17) (0.36) (1.26) (0.24) (0.45)

ASEAN 7.31

(aver.)

1894.7 3150.6 591.4 4326.1 2412.5 3810

(aver.) (3.00) (4.11) (8.58) (3.34) (6.53)

China 10.40 5926.61 10169.5 1338.30 9327.48 3273.18

962 (9.37) (13.26) (19.41) (7.19) (8.86)

Japan 4.00 5458.84 4299.29 127.45 364.50 1668.21

1153 (8.63) (5.61) (1.85) (0.28) (4.52)

Korea, Rep. 6.16 1014.48 1422.31 48.88 97.10 1063.34

0 (1.60) (1.85) (0.71) (0.07) (2.88)

CJK 6.85

(aver.)

12399.9 15891.1 1514.6 9789.1 6004.7 705

(aver.) (19.60) (20.72) (21.97) (7.55) (16.25)

Canada 3.21 1577.04 1332.63 34.13 9093.51 955.47

13653.29 (2.49) (1.74) (0.49) (7.01) (2.59)

Mexico 5.52 1035.87 1651.88 113.42 1943.95 640.87

12071 (1.64) (2.15) (1.65) (1.50) (1.73)

United

States 3.00

14586.7 14586.7 309.35 9147.42 4175.18 7866.71

(23.06) (19.02) (4.49) (7.05) (11.30)

NAFTA 3.91

(aver.)

17199.6 17571.2 456.9 20184.9 5771.5 11197

(aver.) (27.19) (22.91) (6.63) (15.56) (15.62)

European

Union

2.11

(aver.)

16241.1 15939.8 502.13 4181.73 13033.7 8273

(aver.) (25.67) (20.78) (7.28) (3.22) (35.28)

Note: Numbers in the brackets denote the share of related variables in the world total. For the rows of ASEAN, CJK, NAFTA and European Union, GDP, GDP-PPP, Population, Land, and Trade

Volume calculate the aggregate of the member countries, and GDP growth and geographical distance with Korea calculate the average of the member countries. Source: World Development Indicator Online (accessed April 2012)

11

Table 4: Model Aggregations

Economies (number of countries)

<7 Regions>

Sectors

<12 Sectors>

Republic of Korea

China P.R.

Japan

EU (27): Austria, Belgium, Bulgaria,

Cyprus, the Czech Republic,

Denmark, Estonia, Finland,

France, Germany, Greece,

Hungary, Ireland, Italy, Latvia,

Lithuania, Luxembourg, Malta,

the Netherlands, Poland,

Portugal, Romania, Slovakia,

Slovenia, Spain, Sweden, and

the United Kingdom

ASEAN (10): Brunei Darussalam,

Cambodia, Indonesia, Lao

PDR, Malaysia, Myanmar,

Philippines, Singapore,

Thailand, and Viet Nam

NAFTA (3): Canada, Mexico, and the

United States

Rest of the World

Agriculture, Forestry, and Fishery (AFF)

Mining (MIN)

Textile products (TEX)

Pulp, paper and wooden products (PPW)

Chemical and petroleum products (CPP)

Iron and metal (IM)

Motor vehicles and transport equipment

(MTE)

Electronic equipment (EE)

Machinery and equipment (ME)

Manufactures (MAU)

Electricity, gas, and water (EGW)

Other Services (OSV)

Note: In the column of sectors, the letter combinations in the brackets denote the short form of the

related sector.

12

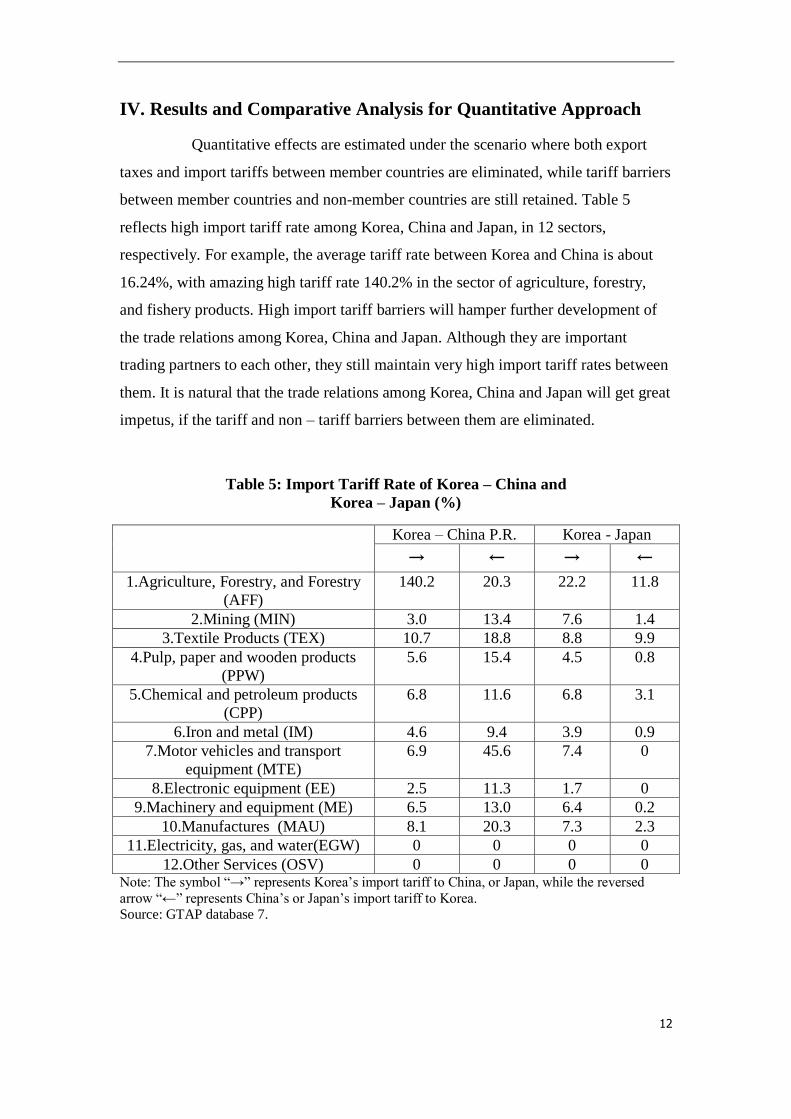

IV. Results and Comparative Analysis for Quantitative Approach

Quantitative effects are estimated under the scenario where both export

taxes and import tariffs between member countries are eliminated, while tariff barriers

between member countries and non-member countries are still retained. Table 5

reflects high import tariff rate among Korea, China and Japan, in 12 sectors,

respectively. For example, the average tariff rate between Korea and China is about

16.24%, with amazing high tariff rate 140.2% in the sector of agriculture, forestry,

and fishery products. High import tariff barriers will hamper further development of

the trade relations among Korea, China and Japan. Although they are important

trading partners to each other, they still maintain very high import tariff rates between

them. It is natural that the trade relations among Korea, China and Japan will get great

impetus, if the tariff and non – tariff barriers between them are eliminated.

Table 5: Import Tariff Rate of Korea – China and

Korea – Japan (%)

Korea – China P.R. Korea - Japan

→ ← → ←

1.Agriculture, Forestry, and Forestry

(AFF)

140.2 20.3 22.2 11.8

2.Mining (MIN) 3.0 13.4 7.6 1.4

3.Textile Products (TEX) 10.7 18.8 8.8 9.9

4.Pulp, paper and wooden products

(PPW)

5.6 15.4 4.5 0.8

5.Chemical and petroleum products

(CPP)

6.8 11.6 6.8 3.1

6.Iron and metal (IM) 4.6 9.4 3.9 0.9

7.Motor vehicles and transport

equipment (MTE)

6.9 45.6 7.4 0

8.Electronic equipment (EE) 2.5 11.3 1.7 0

9.Machinery and equipment (ME) 6.5 13.0 6.4 0.2

10.Manufactures (MAU) 8.1 20.3 7.3 2.3

11.Electricity, gas, and water(EGW) 0 0 0 0

12.Other Services (OSV) 0 0 0 0 Note: The symbol “→” represents Korea’s import tariff to China, or Japan, while the reversed

arrow “←” represents China’s or Japan’s import tariff to Korea. Source: GTAP database 7.

13

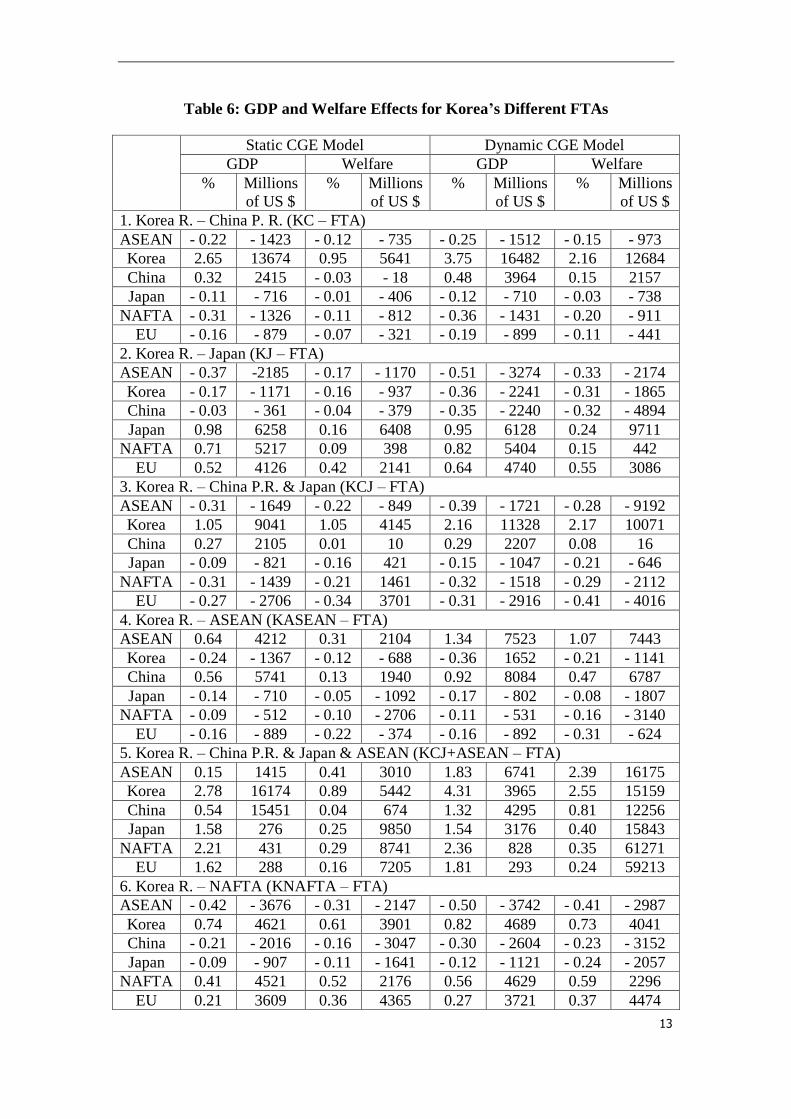

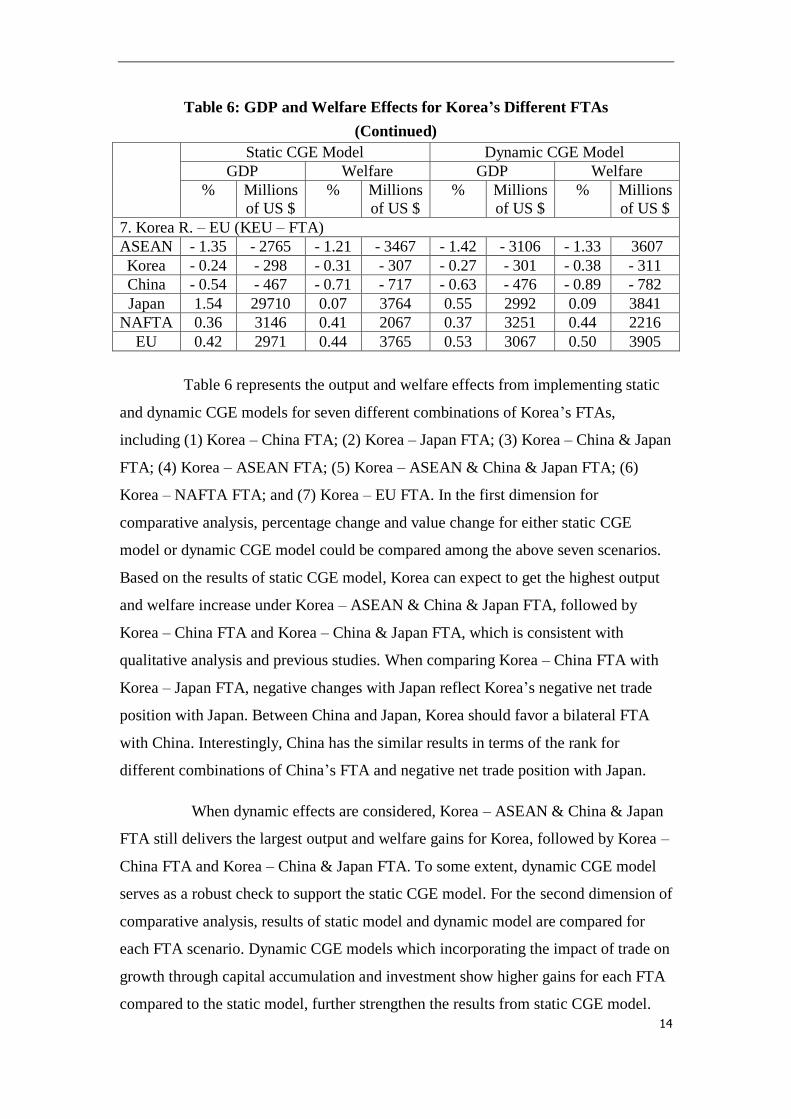

Table 6: GDP and Welfare Effects for Korea’s Different FTAs

Static CGE Model Dynamic CGE Model

GDP Welfare GDP Welfare

% Millions

of US $

% Millions

of US $

% Millions

of US $

% Millions

of US $

1. Korea R. – China P. R. (KC – FTA)

ASEAN - 0.22 - 1423 - 0.12 - 735 - 0.25 - 1512 - 0.15 - 973

Korea 2.65 13674 0.95 5641 3.75 16482 2.16 12684

China 0.32 2415 - 0.03 - 18 0.48 3964 0.15 2157

Japan - 0.11 - 716 - 0.01 - 406 - 0.12 - 710 - 0.03 - 738

NAFTA - 0.31 - 1326 - 0.11 - 812 - 0.36 - 1431 - 0.20 - 911

EU - 0.16 - 879 - 0.07 - 321 - 0.19 - 899 - 0.11 - 441

2. Korea R. – Japan (KJ – FTA)

ASEAN - 0.37 -2185 - 0.17 - 1170 - 0.51 - 3274 - 0.33 - 2174

Korea - 0.17 - 1171 - 0.16 - 937 - 0.36 - 2241 - 0.31 - 1865

China - 0.03 - 361 - 0.04 - 379 - 0.35 - 2240 - 0.32 - 4894

Japan 0.98 6258 0.16 6408 0.95 6128 0.24 9711

NAFTA 0.71 5217 0.09 398 0.82 5404 0.15 442

EU 0.52 4126 0.42 2141 0.64 4740 0.55 3086

3. Korea R. – China P.R. & Japan (KCJ – FTA)

ASEAN - 0.31 - 1649 - 0.22 - 849 - 0.39 - 1721 - 0.28 - 9192

Korea 1.05 9041 1.05 4145 2.16 11328 2.17 10071

China 0.27 2105 0.01 10 0.29 2207 0.08 16

Japan - 0.09 - 821 - 0.16 421 - 0.15 - 1047 - 0.21 - 646

NAFTA - 0.31 - 1439 - 0.21 1461 - 0.32 - 1518 - 0.29 - 2112

EU - 0.27 - 2706 - 0.34 3701 - 0.31 - 2916 - 0.41 - 4016

4. Korea R. – ASEAN (KASEAN – FTA)

ASEAN 0.64 4212 0.31 2104 1.34 7523 1.07 7443

Korea - 0.24 - 1367 - 0.12 - 688 - 0.36 1652 - 0.21 - 1141

China 0.56 5741 0.13 1940 0.92 8084 0.47 6787

Japan - 0.14 - 710 - 0.05 - 1092 - 0.17 - 802 - 0.08 - 1807

NAFTA - 0.09 - 512 - 0.10 - 2706 - 0.11 - 531 - 0.16 - 3140

EU - 0.16 - 889 - 0.22 - 374 - 0.16 - 892 - 0.31 - 624

5. Korea R. – China P.R. & Japan & ASEAN (KCJ+ASEAN – FTA)

ASEAN 0.15 1415 0.41 3010 1.83 6741 2.39 16175

Korea 2.78 16174 0.89 5442 4.31 3965 2.55 15159

China 0.54 15451 0.04 674 1.32 4295 0.81 12256

Japan 1.58 276 0.25 9850 1.54 3176 0.40 15843

NAFTA 2.21 431 0.29 8741 2.36 828 0.35 61271

EU 1.62 288 0.16 7205 1.81 293 0.24 59213

6. Korea R. – NAFTA (KNAFTA – FTA)

ASEAN - 0.42 - 3676 - 0.31 - 2147 - 0.50 - 3742 - 0.41 - 2987

Korea 0.74 4621 0.61 3901 0.82 4689 0.73 4041

China - 0.21 - 2016 - 0.16 - 3047 - 0.30 - 2604 - 0.23 - 3152

Japan - 0.09 - 907 - 0.11 - 1641 - 0.12 - 1121 - 0.24 - 2057

NAFTA 0.41 4521 0.52 2176 0.56 4629 0.59 2296

EU 0.21 3609 0.36 4365 0.27 3721 0.37 4474

14

Table 6: GDP and Welfare Effects for Korea’s Different FTAs

(Continued)

Static CGE Model Dynamic CGE Model

GDP Welfare GDP Welfare

% Millions

of US $

% Millions

of US $

% Millions

of US $

% Millions

of US $

7. Korea R. – EU (KEU – FTA)

ASEAN - 1.35 - 2765 - 1.21 - 3467 - 1.42 - 3106 - 1.33 3607

Korea - 0.24 - 298 - 0.31 - 307 - 0.27 - 301 - 0.38 - 311

China - 0.54 - 467 - 0.71 - 717 - 0.63 - 476 - 0.89 - 782

Japan 1.54 29710 0.07 3764 0.55 2992 0.09 3841

NAFTA 0.36 3146 0.41 2067 0.37 3251 0.44 2216

EU 0.42 2971 0.44 3765 0.53 3067 0.50 3905

Table 6 represents the output and welfare effects from implementing static

and dynamic CGE models for seven different combinations of Korea’s FTAs,

including (1) Korea – China FTA; (2) Korea – Japan FTA; (3) Korea – China & Japan

FTA; (4) Korea – ASEAN FTA; (5) Korea – ASEAN & China & Japan FTA; (6)

Korea – NAFTA FTA; and (7) Korea – EU FTA. In the first dimension for

comparative analysis, percentage change and value change for either static CGE

model or dynamic CGE model could be compared among the above seven scenarios.

Based on the results of static CGE model, Korea can expect to get the highest output

and welfare increase under Korea – ASEAN & China & Japan FTA, followed by

Korea – China FTA and Korea – China & Japan FTA, which is consistent with

qualitative analysis and previous studies. When comparing Korea – China FTA with

Korea – Japan FTA, negative changes with Japan reflect Korea’s negative net trade

position with Japan. Between China and Japan, Korea should favor a bilateral FTA

with China. Interestingly, China has the similar results in terms of the rank for

different combinations of China’s FTA and negative net trade position with Japan.

When dynamic effects are considered, Korea – ASEAN & China & Japan

FTA still delivers the largest output and welfare gains for Korea, followed by Korea –

China FTA and Korea – China & Japan FTA. To some extent, dynamic CGE model

serves as a robust check to support the static CGE model. For the second dimension of

comparative analysis, results of static model and dynamic model are compared for

each FTA scenario. Dynamic CGE models which incorporating the impact of trade on

growth through capital accumulation and investment show higher gains for each FTA

compared to the static model, further strengthen the results from static CGE model.

15

V. Conclusion and Policy Implication

Under the background of globalization and polarization, challenges and

opportunities coexist for the growing trend of regionalism in recent international

economic environment. Most of the FTAs in the world tend to start with neighboring

countries which are close to each other in terms of income and development level,

history and geography, for example, ASEAN, NAFTA and EU, and then spread to

adjacent regions and areas through contagion effects.

The objective of this paper is to compare and assess Korea’s 7 possible

FTAs involving major economies in the world: China P. R., Korea, Japan, ASEAN,

NAFTA and EU, qualitatively and quantitatively. According to the results of

comparative analysis in two different dimensions, Korea would benefit most from a

Korea – China & Japan & ASEAN FTA, which is the largest possible FTA in East

Asia. This major finding is consistent with previous CGE model studies that have

found that broader FTAs generate higher output and welfare gains for member

countries. From the perspective of Korea, strengthening trade links with the East

Asian neighbors, especially with China, through FTAs offers the opportunities to

enhance Korea’s economic and political position in the Asian region. Korea, China

P.R., Japan, and ASEAN can leverage their common market to reduce their heavy

dependence on exports to the United States and European Union, which would also

contribute to the discussion of decoupling hypothesis and the solution for the problem

of current global account imbalances.

In the path to reach region – wide Korea – China & Japan & ASEAN FTA,

since the process is usually gradual and complex, Korea can keep bilateral FTA as

medium – term trade strategy and pursue region – wide FTA as a long – term trade

strategy. To realize an ideal FTA, political dialogue is also necessary to promote

optimal economic results for each member in an FTA.

Future research direction for this research could disaggregate

macroeconomic effects into different sectors or industry levels to do comparison and

do assessment from the perspective of different trading partners to figure out an

optimal FTA solution for Korea and the global economy.

16

Reference

Abe, K. (2003), “Economic Effects of a Possible FTA among China, Japan and

Korea”, in Y. S. Kim and C. K. Lee (Eds.), Northeast Asian Economic

Integration: Prospects for a Northeast Asian FTA, Korea Institute for

International Economic Policy, Conference Proceedings 03-05.

Estrada, G., D. Y. Park, I. W. Park, and S. C. Park (2012), “The PRC’s Free Trade

Agreements with ASEAN, Japan, and the Republic of Korea: A Comparative

Analysis”, Asian Development Bank Working Paper Series on Regional

Economic Integration, No. 92

Hertel, T.W., T. L. Walmsley, and K. Itakura (2001), “Dynamic Effects of the New

Age Free Trade Agreement between Japan and Singapore”, GTAP working

paper

Ko, J.W. (2000), “Analysis of Economic Effects of a Free Trade Agreement among

Korea, China, and Japan”, International Area Studies Review, Vol. 4, No. 2,

pp. 177-209.

Lee, C. J. et al. (2005), “Rationale for a China-Japan-Korea FTA and Its Impact on

the Korean Economy”, Korea Institute for International Economic Policy,

NRCS Joint Research Series on FTA Issues 05-04.

Lee, J. W. (2002), “Economic Impacts in Northeast Asia: The Perspective of a China-

Japan-Korea FTA”, Journal of Korea Trade, Vol. 6, No. 2, pp. 155-188.

Park, I. W. (2004), “A CGE Analysis of a Korea-China-Japan Free Trade Area”,

Economic Papers, Vol. 6, No. 2, pp. 151-186.

Tongzon, J. L. (2001), “China’s Membership in the World Trade Organization (WTO)

and the Exports of the Developing Economies of East Asia: A Computable

General Equilibrium Approach”, Applied Economics, Vol. 33, pp. 1943-1959.

Yoon, Y. M., and T. D. Yeo (2007), “Trade Structures and Relations among China,

Japan, and Korea”, Journal of the Korean Economy, Vol. 8, No. 1, pp. 1-24.

Yoon, Y. M,. C. Gong, and T. D. Yeo (2009), “A CGE Analysis of Free Trade

Agreement among China, Japan and Korea”, Journal of Korea Trade, Vol. 12,

No. 1, February 2009, 45-64