Embed Size (px)

Citation preview

SPECIAL COMMENT

RESIDENTIAL MBS

Table of Contents:

SUMMARY 1 WE NOTE KEY DIFFERENCES AMONG MARKETS 1 I. MORTGAGES 4 PRIME TRANSACTION COLLATERAL CHARACTERISTICS 4 THIRD-PARTY CREDIT PROTECTION IS WIDELY USED IN JAPAN, AUSTRALIA AND THE NETHERLANDS 6 PERFORMANCE COMPARISONS 7 II. NOTES 9 RMBS STRUCTURAL FEATURES ARE SIMPLER IN JAPAN, AUSTRALIA AND THE NETHERLANDS 9 AUSTRALIA 10 PAYMENT RISK AND EXTENSION RISK 13 III. SET-OFF AND COUNTERPARTY RISK 13 SET-OFF RISK 13 COUNTERPARTY RISK 16 BACK-UP SERVICER RISK 16 SWAP COUNTERPARTY RISK 17 IV. DOWNGRADE DRIVERS 18 APPENDIX A 19 MOODY’S RELATED RESEARCH 34

Analyst Contacts:

SYDNEY +612.9270.8199

Arthur Karabatsos +612.9270.8160 Vice President - Senior Analyst [email protected]

LONDON +44.20.7772.5454

Jonathan Livingstone +44.20.7772.5520 Vice President - Senior Analyst [email protected]

Annabel Schaafsma +44.20.7772.8761 Associate Managing Director [email protected]

TOKYO +81.3.5408.4100

Hiroyuki Kato +81.3.5408.4261 Vice President - Senior Analyst [email protected]

» contacts continued on the last page

SEPTEMBER 24, 2013

A Comparison of Japanese, Australian, Dutch and UK RMBS and Mortgage Markets

Summary

Following increased interest from investors in Australian, Dutch and UK residential mortgage-backed securities (RMBS), we produced this report to compare and provide insight into these different markets. We have expanded on the report “A Primer: Comparing Japanese, Australian, Dutch and UK RMBS and Mortgage Markets,” which was published in March 2013.

We Note Key Differences Among Markets

» Receivable Characteristics Vary Among Countries: Dutch and UK interest-only (IO) loans expose investors to bullet repayment risk because borrowers pay only the interest portion for the entire life of the loan (30 years). Conversely, Japanese and Australian IO loans do not expose the borrower to bullet repayment risk because they are typically IO for less than five years (in Australia) or one year (in Japan), before fully amortising.

» Lender’s Mortgage Insurance Mitigates Credit Risk in Australian and Dutch RMBS: Most Australian RMBS loans have lenders mortgage insurance (LMI), with the two largest providers being private companies rated Aa3 and A1. In the Netherlands, NHG Guarantee, backed by a Aaa-rated government-sponsored entity, provides LMI to loans that meet certain criteria. Typically, LMI covers up to 30% of the loans in the Dutch mortgage market. Unlike Australian LMI, Dutch LMI coverage amortises on an annuity basis. UK lenders do not use LMI, while lenders in Japan obtain a guarantee, generally from a subsidiary. We do not usually rate the subsidiary.

» Set-Off Risk Is Most Significant in Dutch RMBS: Set-off risk is more significant in Dutch RMBS compared to other markets because the Dutch tax law encourages the use of IO mortgages in combination with repayment vehicles, which are usually savings or insurance policies provided by an insurance company. If the insurer becomes bankrupt, the borrower can set off the value of the policy against the outstanding amount of the mortgage loan (insurance set-off risk). Over time, this risk increases because the value of the policy increases.

» Note Types Also Vary Between Countries: Dutch and UK master trusts issue soft bullets, as opposed to the Australian and Japanese standalone structures, which typically issue straight pass-through notes. However, soft bullets are not immune to prepayment or extension risk because they rely on the continued support of the originator to supply mortgages to the trust. This supply ensures the generation of sufficient principal to redeem the notes on their scheduled maturity dates.

2 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

» Credit Profiles of UK and Dutch Master Trusts Are More Volatile: UK and Dutch master trust portfolios change on a regular basis as the seller adds new loans to the portfolio. The portfolio can lose the benefits of more seasoned borrowers building equity1 in their homes over time. While performance criteria and other tests will mitigate the risk of the new loans decreasing the overall credit quality of the portfolio, it is possible to change individual portfolio characteristics, such as, geographical concentration and the proportion of high loan-to-value (LTV) loans. Typically, lenders do not add new loans to Australian and Japanese portfolios; their static nature leaves them more vulnerable than dynamic portfolios to the performance of any one vintage of loans.

» Operational Risks Are Lower in Australia and Japan: Australian and Japanese RMBS deals have more certainty in terms of Back-Up Servicer (BUS) arrangements because they identify from closing which entity is legally liable to perform the BUS role. Conversely, Dutch and UK transactions typically rely on the credit strength of the servicer to avoid the need for a BUS. For lower or non-rated servicers, however, Dutch and UK RMBS put additional structural features in place, such as (1) pre-appointing a BUS, or requiring the appointment of one following a trigger event; or (2) appointing a facilitator, who uses commercially reasonable efforts to find a replacement servicer on substantially the same terms as the existing servicer.

» We highlight key differences, and compare and contrast mortgage loans, notes, set-off and counterparty risk, and downgrade drivers between the different markets.

» We explain in detail the workings of UK master trusts. The guide compares the four markets based on collateral characteristics and underwriting, LMI, housing, income and population, RMBS performance, and RMBS structural features.

» Exhibit 1 illustrates various credit risk relativities between the different RMBS markets.

1 The more equity a borrower has in their home, the less likely they will default.

3 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

EXHIBIT 1

Credit Risk Relativities Between Different RMBS Markets

High

Medium

Low

Collateral Profile Risk

Japan

Australia

Netherlands

UK

Prepayment Risk

Japan Australia Netherlands

UK

Set-off Risk

Japan

Australia

Netherlands UK

Back-up Servicer Risk

Japan

Australia

Netherlands

UK

Swap Counterparty Risk

Japan

Australia

Netherlands UK

LTV

Japan Australia

Netherlands UK

Mortgage Product Complexity

Japan

Australia

Netherlands

UK

4 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

I. Mortgages

Prime Transaction Collateral Characteristics

Japanese and Dutch transactions are the most conservative.

Japan

Japanese prime RMBS deals are very conservative; their portfolios contain only owner-occupied, full-documentation mortgage loans that are made mostly to full-time employees of medium-sized or large corporations. The lending criteria of the large banks focus less on LTV and more on an applicant’s occupation, income and income sustainability.2 The weighted average LTV (WALTV) of new deals is typically between 80% and 95%, although it is common for borrowers to borrow the full purchase price of a home.

The financial strength or credit quality of an applicant’s employer determines income sustainability. Lenders consider the income stability of permanent employees of medium-sized or large companies to be robust because a combination of Japan’s corporate culture and labour laws makes it difficult to lay off such employees. In addition, Japanese banks often securitise mortgage pools that consist of only fixed-rate mortgages.

Japanese lenders do not rely heavily on recoveries from underlying properties in the event of a default because of the drop in real estate prices in the 1990s and continued house price declines.

Risk-Based Pricing: Lenders generally charge all of their owner-occupied borrowers the same interest rate irrespective of their LTV ratios.

Australia

Australian prime RMBS portfolios consist of a much broader range of loan characteristics than those of the other markets. They can contain owner-occupied and investment3 loans to either full-time employees or self-employed borrowers, full documentation mortgages and low documentation4 loans, and loans with short-term fixed and variable rates.

Similar to the Dutch market, Australian mortgage loans can consist of multiple loan parts. Each loan part can have different characteristics, such as amortisation type and an interest reset period. A prime mortgage generally is one that meets the underwriting criteria for LMI policies, which typically exclude borrowers with an adverse credit history. Almost all loans in Australian RMBS deals are covered by an LMI policy.

Australian investment mortgages are riskier than owner-occupied mortgages and are also a mainstream product provided by prime lenders. About 30% of Australian mortgages are for investment purposes compared with 2% in Japan.

The WALTV of a new deal is typically 60%-65%.

Risked-Based Pricing: Australian mortgages have no risk-based pricing. All borrowers pay the same rate of interest regardless of LTV, loan amount or occupancy type.

The Netherlands

Dutch deals are backed by owner-occupied loans only. These deals have a large proportion of fixed-rate loans (typically between five and 10 years in length), a high proportion of IO loans and high LTVs. The typical WALTV of a new deal is around 90%, based on the property’s foreclosure value.

Dutch mortgage loans can consist of multiple loan parts with different characteristics, such as amortisation types and interest reset periods. Because of the tax deductibility of mortgage interest, a

2 See “Japanese mortgage delinquencies have higher correlation with self employment status than high LTV,” July 2012. 3 Investment mortgages are the Australian equivalent of UK buy-to-let (BTL) mortgages. 4 A mortgage where the lender does not require the applicant to provide full documented proof of income.

5 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

typical loan consists of a pure IO loan part with no repayment terms for its principal portion and one or more IO loan parts which benefit from indirect amortisation through the accumulation of principal in separate repayment vehicles.

By removing tax deductibility for IO loans, the new tax deductibility rules explained below positively affect new RMBS transactions since non-amortising mortgage products directly affect loss given default. Borrowers’ willingness to pay mortgage instalments will increase with the rising equity levels, and back-ended mortgage defaults will decrease because of reduced balloon payments at maturity.

Revised regulations5 will likely reduce the levels of both IO loans and LTVs. The Dutch Code of Conduct unifies lenders’ underwriting practices because it is very prescriptive on a number of underwriting criteria, such as maximum LTV and affordability testing. Affordability testing incorporates standard inputs for living expenses, acceptable income and interest rate stresses.

Risked-Based Pricing: While there is generally no risk-based pricing, loans with a National Mortgage Guarantee (NHG)6 receive an interest rate reduction of 0.40 to 0.50 percentage points.

UK

A significant proportion of UK prime RMBS use a master trust structure containing owner-occupied, full documentation or fast-track7 mortgages to either full-time employed or self-employed borrowers. The proportion of non-prime collateral in master trusts has declined since the credit crunch.

The proportion of IO loans will decrease in UK pools. In October 2012, the Mortgage Market Review (MMR) published a set of new rules, including regulations on IO lending, effective from April 2014. 8 In anticipation of the new framework, lenders have already changed their underwriting procedures. With some lenders withdrawing from the IO segment entirely and others beginning to add greater amounts of more recent vintages, which have higher levels of repayment loans, the proportion of IO loans in master trusts is decreasing.

The MMR includes a requirement for lenders to perform an affordability assessment to ensure a credible repayment strategy. The new rules are not, however, prescriptive with lenders able to take into account individual circumstances, such as allowing the sale of the mortgaged property where such a course of action is a credible strategy.

From April 2014, the MMR will also introduce minimum standards to assess affordability against interest rate increases. The new stressed affordability assessment considers market expectations for interest rates over the next five years, subject to a minimum stress of 1% in flat-rate scenarios. Lenders will be required to take into account consumers’ ability to manage their expenditures once they take on a mortgage.

WALTV is typically around 60%-65%.

Risk-Based Pricing: The use of risk-based pricing by lenders is widespread and determined by LTV as well as other risk characteristics, such as whether the loan is backed by an investment property. Currently, high LTV borrowers are paying around 2 percentage points more than those with LTVs that are less than 75%.

5 See “Dutch RMBS: New Coalition’s Proposed Agreement Reduces Leverage While Affordability Remains Largely Unaffected,” November 2012. 6 LMI backed by a government sponsored entity. 7 Fast track loans are those originated without full income checking, but which are not marketed as having limited income checks. 8 See “Moody’s: New FSA MMR rules will benefit UK prime RMBS in the long term,” November 2012.

6 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

Third-Party Credit Protection Is Widely Used in Japan, Australia and the Netherlands

In Japan, all loans are covered by a guarantee typically provided by the lender’s subsidiary to mitigate credit risk. Both Australian and the Dutch deals use LMI, but the type of provider and coverage differs.

In Australia, most RMBS loans have LMI provided by private companies covering the full amount of outstanding principal. In the Dutch mortgage market, about 30% of the loans are covered by LMI provided by a government entity. The coverage amortises on an annual basis. UK lenders do not use any third-party protection.

Japan Obtains Subsidiary Guarantees for All Loans

Private-sector financial institutions obtain a guarantee, generally from a subsidiary, for all loans they originate. If a borrower defaults, the issuer benefits from the guarantor’s payment of outstanding principal and accrued interest.

While we do not usually rate guarantors, we do rate their parent banks (Aa-Baa) in many instances.

While the issuer benefits from the guarantee, the structure of many deals is such that the subordination provided by the unrated junior note is sufficient for the senior notes to obtain a Aaa (sf) rating without any benefit from the guarantee.

Australia – LMI

An LMI policy covers the lender if -- upon default of a borrower -- there is unpaid principal or interest after applying the sales proceeds of the homes. LMI is effective for the duration of mortgages and covers the lender for 100% of the outstanding principal amount, accrued interest, and reasonable expenses involved in enforcing the mortgage, as well as for marketing and selling the property.

Impact of LMI on RMBS notes is decreasing:9 The credit quality of the notes reflects the credit quality of the underlying mortgages and consideration of the credit quality of the LMI provider.

» For the senior notes, consideration of the credit quality of the LMI provider means that the notes can achieve a Aaa (sf) rating with less subordination provided by the mezzanine and junior notes, than without LMI.

» Since the 2008-09 global financial crisis, the structures of most senior notes do not give benefit to the credit quality of the LMI provider, and hence their Aaa (sf) credit qualities are independent of the LMI provider. This is done to prevent exposing the senior note’s rating to the volatility in the mortgage insurer’s rating.

» Mezzanine notes, which we typically rate at Aaa (sf) or Aa1 (sf), rely on the LMI provider for their credit quality because LMI provides the first level of credit support.

» The credit qualities and ratings of junior notes are highly reliant on the credit quality of the mortgage insurer because such notes are directly exposed to losses not covered by LMI. Collateral losses not covered by LMI will translate into losses on the junior notes.

» Rating downgrades have been almost entirely restricted to junior notes owing to the downgrades of mortgage insurers, rather than to the poor performance of mortgages.

9 See “Approach for Incorporating Lender’s Mortgage Insurance in Australian RMBS,” October 2012.

7 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

The Netherlands – National Mortgage Guarantee (NHG) guarantee

The Nationale Hypotheek Garantie (NHG) guarantee may cover Dutch loans, compensating the lender after the end of the foreclosure process for a defaulted borrower. However, the NHG guarantee amortises on a 30-year annuity repayment basis and, therefore, typically does not match the actual amortisation profile of the mortgage loan. This mismatch creates a coverage gap over time and leads to credit risk for IO loan parts. However, the risk is mitigated as most defaults occur in the first few years after origination.

Exhibit 2 illustrates how the LMI coverage gap increases over time with IO loans because the LMI coverage amortises on an annual basis, while the loan amount remains unchanged.

EXHIBIT 2

Dutch LMI Coverage

* A borrower’s IO loan can only be based on a LTV of 50%. The remainder will amortise. SOURCE: Moody’s Investors Service

The borrower pays the tax-deductible NHG fee in a single up-front payment at origination.

Impact of NHG guarantee on RMBS notes:10 We factor the NHG guarantee into our ratings by taking it into account in our assessment of the credit quality of the pool; it incorporates (1) the rating of Stichting Waarborgfonds Eigen Woningen (WEW) (Aaa); (2) the amortisation mismatch between the guarantee and underlying mortgage loan; and (3) the rescission rate. As a result, the credit enhancement for NHG loans is lower than that of non-guaranteed mortgages

Performance Comparisons

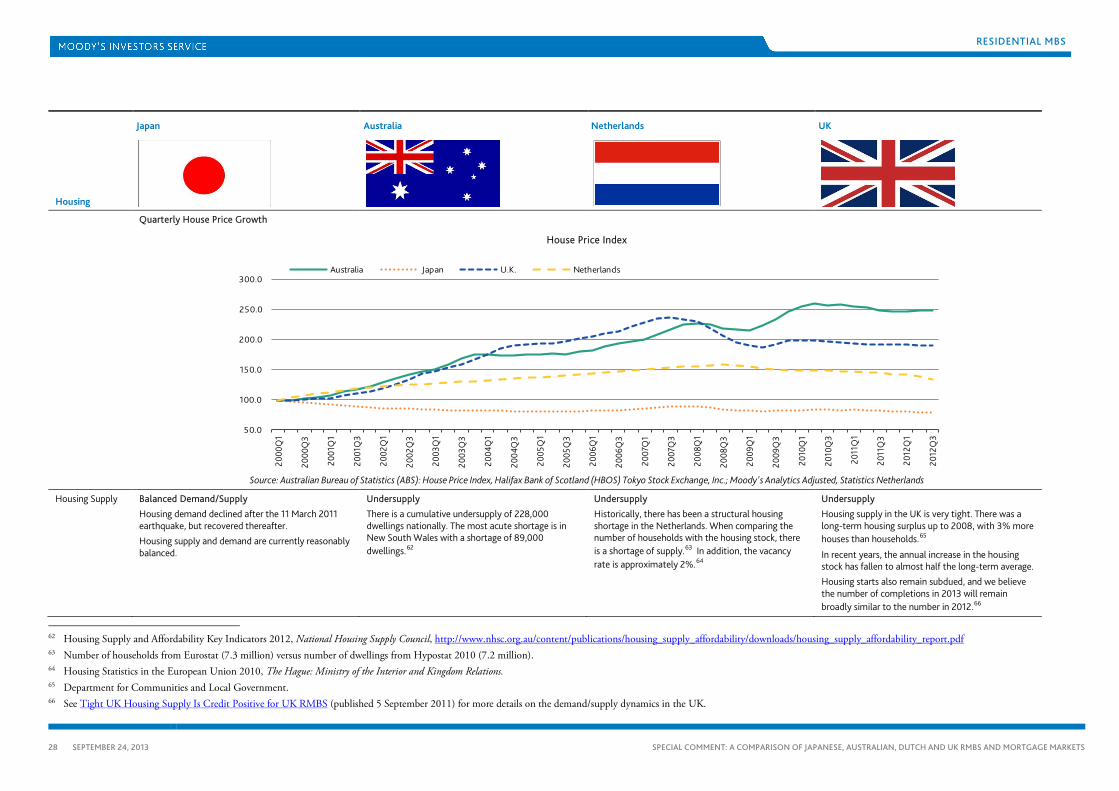

Exhibit 3 charts the 60-days plus delinquencies of the Japanese, Australian, Dutch and UK markets. Even when accounting for buy-backs, Japan shows the lowest delinquencies. The UK has the highest delinquencies. Australia and the Netherlands have about the same level of delinquencies.

10 See “Moody’s Updated Approach to NHG Mortgages in Rating Dutch RMBS”, 17 March 2009

Time

Euro

s

Loan Balance - Interest Only Loan*

Dutch LMI coverage amortises on an annual basis

LMI Coverage Gap

8 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

EXHIBIT 3

Japanese, Australian, Dutch, and UK RMBS Delinquencies

Source: Moody’s Investors Service’s Global Structured Finance Collateral Performance Review (4 December 2012); Moody’s Investors Service’s UK Prime RMBS Indices (19 October 2012)

We usually compare mortgage performance between jurisdictions on a same-seasoning basis with static portfolios. However, UK and Dutch master trusts are revolving, making like-for-like comparisons less straightforward.

In Japan, buy-back requirements, coupled with the moratorium law, also keep mortgage performance artificially low. Many Japanese RMBS deals require sellers to buy back at par all modified mortgages.

Modified mortgages include11 those with temporarily suspended principal repayments (typically for up to one year) or extended mortgage terms, which reduce the repayment burden on the borrower.

The number of buy-backs has increased dramatically with the introduction of the moratorium law in December 2009, which encourages lenders to modify a mortgage when asked by a financially troubled borrower. The law expired in March 2013 but lenders continue to modify mortgages, because the governmental agency supervising financial institutions, Japan Financial Services Agency requested that they continue to do so.

11 Modified mortgages do not include only “the mortgages modified for financially troubled obligors,” but also include the mortgages modified for obligors with good

credit (for example, by lowering interest rates) so that they do not refinance their mortgages with other banks.

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

Jan-

04

Apr-

04

Jul-0

4

Oct

-04

Jan-

05

Apr-

05

Jul-0

5

Oct

-05

Jan-

06

Apr-

06

Jul-0

6

Oct

-06

Jan-

07

Apr-

07

Jul-0

7

Oct

-07

Jan-

08

Apr-

08

Jul-0

8

Oct

-08

Jan-

09

Apr-

09

Jul-0

9

Oct

-09

Jan-

10

Apr-

10

Jul-1

0

Oct

-10

Jan-

11

Apr-

11

Jul-1

1

Oct

-11

Jan-

12

Apr-

12

Jul-1

2

% o

f Out

stan

ding

Bal

ance

Japan Repurchase Rate Japan Conforming RMBS 60 plus delinquencies

Australian Prime RMBS 60 plus delinquencies Dutch RMBS 60 plus delinquencies

UK Prime RMBS 60 plus delinquencies

9 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

II. Notes

RMBS Structural Features Are Simpler in Japan, Australia and the Netherlands

Japanese, Australian and Dutch RMBS deals use relatively simple standalone structures that issue pass-through notes, meaning that payments received from the underlying mortgages pass straight through to investors. The structures have a single static portfolio of mortgages backing each new issuance of notes. The issuers typically redeem notes in a sequential order.

Prime UK deals are generally master trusts with dynamic pools, which means that new loans can continually be added, subject to performance triggers. Master trusts allow for the programmatic issuance of notes similar to medium-term note programmes, allowing for quicker execution, in addition to reduced documentation and costs. Master trusts generally contain controlled amortisation, and soft bullet and pass-through notes. One Dutch originator uses master trust structures that are a hybrid between the UK master trust and the standalone structures. Dutch master trusts also have single dynamic portfolios supporting many issuances but, unlike the UK, do not have seller shares.

Standalone Structures – Japan, Australia and the Netherlands

Although Japan, Australia and the Netherlands all use simple standalone structures, differences exist in the typical number of tranches and principal and interest payment structures.

Japan

Japanese deals typically have one or two Aaa (sf)-rated senior notes and one unrated junior note. If there are two senior notes, the principal payment can be either pro-rata or sequential between them, as illustrated in Exhibit 4. In pro-rata deals, one of the senior notes receives a fixed interest rate and the other receives a floating interest rate.

The junior note receives no interest and is always unrated, and is held by the originator. A junior note receives surplus income (excess spread). In many cases, following the seller’s default, the senior notes receive the excess spread.

10 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

EXHIBIT 4

Waterfall and Loss Allocation - Japan

Source: Moody’s Investors Service

Australia

Australian deals typically issue two or three different classes of notes. Exhibit 5 illustrates a typical three-note issuance. Initially, the collection flows through the principal sequentially; after which the deal switches to paying the principal pro rata upon specific events, such as delinquencies remaining below a certain level, and a doubling of the relative size of the subordinate notes relative to the mezzanine and junior notes since closing.

EXHIBIT 5

Waterfall and Loss Allocation - Australia

Source Moody’s Investors Service

Senior Aaa(sf)Floating RateWAL ≈ 7 yrs

Senior Aaa(sf) Fixed RateWAL ≈ 7 yrs

Unrated Junior NoteUnrated Junior Note

Senior Aaa(sf)Fixed RateWAL ≈ 2 yrs

Senior Aaa(sf)Fixed RateWAL ≈ 10 yrs

Excess Spread

Mortgage Guarantee (if any)

Sequential Pay (Principal & Interest)

Pro Rata(Principal)

Loss

Allo

catio

nPrin

cipa

l & In

tere

st

Excess Spread

Mortgage Guarantee (if any)

Lenders Mortgage Insurance

Senior Aaa(sf)Floating Rate

Mezzanine Aa2(sf) –Aa1(sf)Floating Rate

Junior Aa3(sf) – A1(sf)Floating Rate

Excess Spread

Loss

Allo

catio

n

Sequ

entia

l or P

ro R

ata

Prin

cipa

l

Sequ

entia

l Inte

rest

11 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

Some Australian deals12 have used a variety of techniques – such as, remarketing of notes and repurchasing agreements -- to create soft bullets without the use of date-based calls.

The Netherlands

Exhibit 6 illustrates a typical Dutch standalone structure, which means that it incorporates the elements common to most Dutch RMBS transactions. The typical structure includes a number of classes of notes and commonly contains two Class A subclasses: Class A1 and Class A2. Class A1 and Class A2 receive the principal sequentially with interest paid pro rata, and then all other classes in order of priority sequentially. In general, the Class A notes receive a floating interest rate and the junior notes receive either a fixed or floating interest rate.

EXHIBIT 6

Waterfall and Loss Allocation – the Netherlands

Source: Moody’s Investors Service

Master Trusts – the Netherlands and UK

Why master trusts?: The term “master trust” refers to a structure that allows ongoing issuance, similar to a medium-term note programme, enabling the issuer to quickly issue a large volume of notes. One of the main benefits of a master trust is its ability to manage principal payments to investors via bullet and scheduled amortisation notes. The presence of these note types -- in combination with a seller share and deal triggers -- reduces prepayment risk.

Master trusts reduce issuance costs and increase the speed of execution because the issuer uses the same underlying documents, mortgages and structure for each issuance. Additionally, the structural features in master trusts allow subordinated notes to have earlier expected maturity dates than the corresponding senior notes.

In the UK, master trusts are the largest part of the RMBS market, accounting for 80.6% of all outstanding issuances and with most large lenders using them. To date, only one Dutch lender,

12 Torrens, 2010-3; Medallion, 2011-1; Swan, 2010-2; Interstar, 2006-2G; NAB, 2011-1.

12 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

ABN AMRO,13 has adopted a master trust. As such, master trusts in the Netherlands only represent 25% of the total outstanding issuances.14

The Netherlands

Typical Dutch master trusts are hybrids between the UK master trust structures and single standalone Australian/Japanese deals. While Dutch master trusts have a single dynamic portfolio supporting many issuances, they do not have the concept of a seller share.15

As with UK master trust structures, the typical Dutch master trust has a two-tier special purpose vehicle (SPV) structure, an asset purchaser and an issuer. The seller disposes of a portfolio of mortgage loans to the asset purchasers. The latter funds the purchase through an intercompany loan from the issuer. The master issuer can issue new notes in the future, which the same pool of assets will back.

The transaction structure incorporates some credit enhancement features (for example, subordination among classes of notes) at the issuer level and other features (such as excess spread) at the asset purchaser level.

Structures issue soft bullet notes as well as pass-through notes. The issuer can redeem a soft bullet note at the scheduled maturity date through (1) the issuance of new notes; (2) the (partial) repurchase of the pool by the originators; or (3) the (partial) sale of the pool to a third party. Unlike UK master trusts, there is no accumulation period within the structure to repay the soft bullet notes on their scheduled maturity date.

UK

Master trusts are the most common structure in UK RMBS, accounting for 80.6% of all UK Prime RMBS issuances. Smaller lenders generally securitise buy-to-let (BTL) mortgages and non-prime mortgages, using distinct standalone SPVs, often with closed-end pools similar to Australian, Dutch and Japanese RMBS. UK master trust structures have a single portfolio of mortgages supporting multiple issuances, and differ in three key ways from deals in Australia, the Netherlands and Japan.

First, the mortgage portfolio in UK master trusts is dynamic and can change on a monthly basis owing to the seller adding new mortgages to the portfolio. Unlike static portfolios, dynamic portfolios may lose the benefits of seasoning16 and increasing borrower equity.17

However, the diversification of loans in dynamic portfolios is often greater, and therefore less vulnerable to the performance of any one vintage. Additionally, the Moody’s Portfolio Variation18 or LTV tests mitigate the risks of dynamic portfolios as they only permit assets to be added, should the credit risk remain within pre-determined limits.19

Second, UK master trusts have a more complicated system of rules governing payment waterfalls. Cash flow allocations depend on a number of different factors, which change over time, including delinquency and repayment rates, Principal Deficiency Ledger (PDL) levels, the seller share, trust size and servicer insolvency.

Finally, we can see a variety of different notes; bullet, scheduled amortisation and pass-through. The deals incorporate structural features that allow timely payment of bullet notes. These features

13 The five ABN AMRO master trusts are Beluga Master Issuer BV, Dolphin Master Issuer BV, Fishbowl Master Issuer BV, Goldfish Master Issuer B.V. and

Oceanarium Master Issuer BV. 14 Source: Moody’s Dutch Prime and NHG RMBS Indices, 2013 Q2 15 In UK MT structures the sellers retain an interest in the pool of mortgages sold to the MT, known as the “seller share.” 16 Seasoning refers to the number of months since the borrower first took out the mortgage. The longer a mortgage performs, the less likely it is to go delinquent. We

view seasoning positively when determining the credit risk of a mortgage. 17 The more equity a borrower has in their home the less likely they will be to default. 18 The MPV Test is an asset scoring model similar to the UK MILAN model as Moody’s assigns a default frequency and severity following default for each loan based

upon its LTV and then adjusts for adverse characteristics. The MPV Test is calibrated at closing and so when it is run following close at a pool addition date the MPV Test value is a relative indicator of the trust credit quality.

19 See “Substitution Criteria in EMEA RMBS Revolving Deals”, September 2009.

13 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

include cash accumulation periods and the use of the reserve fund. A large seller share and trust size can assist in making timely principal payments because more principal receipts, and not just receipts based on the size of funding share, will be accumulated prior to the scheduled due date.

Payment Risk and Extension Risk

Prepayment Risk

Australian, Dutch and Japanese RMBS are pass-through structures,20 with principal payments from mortgages passing directly to investors in order to gradually repay the notes. The maturity profile of the notes is uncertain. Dutch RMBS structures typically include date based calls,21 which in combination with the high concentration of IOs in the pools, provide investors with more certainty on the note maturity profile. However, in Australian and Japanese RMBS structures, investors are exposed to significant prepayment risk because borrowers can pay off their mortgage early, or make unscheduled payments.

In the UK and Dutch master trusts, the issuance of bullet notes,22 controlled amortisation notes or scheduled amortisation notes mitigates prepayment risk. Other than for hard bullet notes, the payment of these notes to schedule is still normally contingent on the continued support of the originator adding mortgages to the trust, so as to maintain the trust size and the seller share (in the UK), thereby generating sufficient principal to redeem notes on their scheduled dates.

Extension Risk

Soft bullets controlled amortisation or scheduled amortisation notes issued by master trusts can suffer from extension risk23 when the note is not redeemed on the expected maturity date. UK master trusts have structural features that accumulate the principal prior to the expected payment date. However, low principal payment rates -- as recently experienced due to the slower housing market and tighter credit conditions – would mean that there may not be timely payment in the absence of sponsor support.

Dutch master trust structures do not incorporate accumulation features so investors are more reliant on the seller to re-issue new notes, or repurchase a portion of the mortgage pool to enable the issuer to redeem the notes on the expected maturity date.

Extension risks often occur owing to reasons unrelated to asset performance, such as when a non-asset trigger is breached. Such non-asset triggers include servicer interruption, or the addition of an insufficient value of new mortgages to replace repaid mortgages, leading to the trust size or seller share falling below minimum levels.

III. Set-Off and Counterparty Risk

Set-Off Risk

Set-off risk occurs when a borrower has the right to reduce the amount of money owed by the same amount that the lender owes. In RMBS deals, deposit set-off risk potentially arises where a borrower holds both a mortgage and deposit account with the same lender.

20 Some Australian issuers have eradicated prepayment risk by employing bespoke structuring methods to structure a soft bullet note. 21 Date based calls allow the issuer to call the notes after an appointed date. 22 A soft bullet is a note similar to a corporate bond (hard bullet), because to redeem the note, all the principal repayments to investors are viewed as single payments.

However, it is called a soft bullet because the issuer does not guarantee the final bullet payment on the expected maturity date. That said, issuers have paid the majority of these securitisations on time. Failure to redeem the soft bullet on the expected maturity date will result in an increase in the note’s rate of interest. We do not consider this to be an event of default.

23 See “UK RMBS Master Trusts: Extension Risk Remains Significant due to Low Principal Payment Rates”, May 2012.

14 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

Deposit set-off can then occur on the insolvency of the lender when the borrower seeks to reduce the amount they owe on their mortgage by the amount the lender owes under their deposit accounts. However, the degree of risk and the nature of the mitigants vary by jurisdictions. In the Netherlands, the issue of deposit set-off often does not arise because of the lack of mutuality. In Japan and the UK, structural features mitigate the risk with cash reserves and minimum seller shares, respectively, providing protection. In Australia, set-off waivers, triggers to break mutuality and deposit insurance sufficiently mitigate deposit set-off risk.

Japan – Deposit Set-Off Risk

In Japan, many originators/issuers of RMBS are deposit-taking banks. Therefore, a mortgage borrower can set off their mortgages -- equal to their deposits held with the bank -- following the bank’s default. In Japanese RMBS deals, however, deposit insurance, cash reserves and additional credit enhancement mitigate deposit set-off risk.

Deposit insurance: In principle, the Deposit Insurance Corporation of Japan (DICJ)24 insures bank deposits up to a maximum of JPY10 million25 ($100,000) plus accrued interest. After a bank defaults, borrowers with deposits of less than JPY10 million have no incentive to set off because deposit insurance fully covers their deposits. However, borrowers with deposits higher than JPY10 million may set off their mortgages against the uncovered portion of their deposits; the total amount of deposits minus JPY10 million.

At the individual RMBS deal level, the following mitigants exist to offset deposit set-off risk:

» Cash reserve from closing: From the deal’s closing, the servicer monitors the amount of borrowers’ deposits. The servicer calculates the maximum set-off exposure to deposits exceeding JPY10 million. The deal sponsor will place that amount of cash into a reserve account to mitigate deposit set-off risk.

» Cash reserve after credit breach: Some RMBS deals that do not monitor the level of borrowers’ deposits from closing have bank rating triggers that, if breached, require the establishment of a cash reserve as described above. A bank would breach its rating trigger if its short-term rating were to become, for example, Prime-2 or less.

Australia – Deposit Set-Off Risk

Deposit set-off risk is an issue in Australian RMBS deals because the main issuers of RMBS are authorised deposit-taking institutions (ADIs),26 which also hold deposits from the mortgage borrower. The waiver of set-off and the breaking of mutuality enable ADIs, with their RMBS deals, to proceed without requiring any additional support and sufficiently mitigates deposit set-off risk.

Waiver of set-off: Mortgage loan documents contain clauses where the borrower contractually waives the right of set-off.

Breaking mutuality: Australian RMBS deals have triggers to break mutuality under certain circumstances. These events include originator insolvency, a decline below a certain credit quality, (typically below a Baa3 rating), or failure to transfer money to the trust within a predefined time. When such events occur, the trustee will perfect its equitable interest in the mortgages, such that the trustee transfers the legal title27 of the loans from the lender to the trustee, and hence breaks mutuality.

Deposit insurance: In November 2008, the Australian government created a deposit insurance scheme called the Australian Government Guarantee Scheme for Large Deposits and Wholesale

24 The DICJ (est. 1 July 1971) is the administrative organ of Japan’s deposit insurance system under the Deposit Insurance Law. The current share of the Japanese

government stands at around 95% of total capital. The DICJ’s supervising authorities are the Ministry of Finance and the Financial Services Agency. 25 The DICJ website [http://www.dic.go.jp/english/index.html]. 26 The Australian government authorises ADIs to take deposits under the Banking Act 1959. These institutions include banks, building societies and credit unions. 27 The trustee of the SPV holds an irrevocable title perfection power of attorney which enables it to perfect the title quickly.

15 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

Funding.28 Under the scheme, the government guarantees deposit balances of up to and including AUD250,000 per customer, per institution. However, borrowers with deposits exceeding AUD250,000 may still set off their mortgages against the uncovered portion of their deposits (the total amount of a deposit minus AUD250,000).

The Netherlands – Deposit and Insurance Set-Off Risk

As in the UK and other jurisdictions in Europe, the Netherlands has a Deposit Guarantee Scheme (DGS) in place to protect individuals from losing their savings if a deposit-taking institution becomes insolvent. The compensation limit under the DGS is €100,000 and all natural persons as well as certain small legal entities are eligible for compensation. Each compensation payment is based on the claimant’s gross claim, with no deduction with respect to liabilities owned by the depositor.29

Since the seller does not notify borrowers of the sale of the mortgage loans to the issuer, where the lender and the deposit-taking institution are the same legal entity, deposit set-off risk may be an issue for the RMBS deal for any deposit amounts exceeding the DGS limit. We incorporate this deposit set-off risk into our cash flow modelling of the deal.

However, very few Dutch deals have deposit set-off risk because the lender often originates mortgages out of a mortgage bank or entity that is separately incorporated from the deposit-taking institution.

Insurance policy set-off risk: Because the value of the repayment vehicle starts at zero and accumulates up to the loan amount (in full or in part) over 30 years, insurance policy set-off risk in Dutch RMBS deals increases over time. The recent change in tax deductibility rules – which requires all new mortgages to have annuity repayment structures -- will phase out IO loans twinned with insurance products, ultimately reducing insurance policy set-off risk in RMBS deals.

Where the borrower accumulates funds in a bank savings product, a sub-participation agreement (whereby policy provider passes funds on to the originator as if it were an annuity repayment) typically mitigates set-off risk in RMBS structures.

UK – Deposit and Other Set-Off Risk30

The minimum seller share incorporates a component to mitigate deposit set-off risk by taking into account the level of deposits from the originator. To de-link this risk from the rating of the originator, following the breach of a rating trigger, the amount is sometimes recalculated.

Under English law, obligors are able to set off deposits held with an insolvent originator against payments that they owe under securitised receivables. However, an issuer’s exposure to set-off is substantially reduced where obligors can claim compensation under the Financial Services Compensation Scheme (FSCS). This is because an obligor will not assert set-off in respect of deposits for which they have received a compensation payment.

Where the FSCS does not fully compensate an obligor -- for instance, where their deposits exceed the £85,000 FSCS limit -- then they may set off the uncompensated portion of their deposits against the master trust.

Other set-off risk: If an originator becomes insolvent, a borrower may not be able to draw down on the flexible features on their mortgage loan and may attempt to set off the extra cost of accessing funds. To mitigate against this risk, the minimum seller share generally includes an amount equal to 24% of the flexible draw capacity.

28 Australian government website, http://www.guaranteescheme.gov.au/ 29 Initially the Dutch Central Bank’s guidance was to determine the payout under the DGS after setting off any claims the deposit-taking institution had on the

borrower. This guidance has recently changed and we are proposing to change our methodology accordingly in line with other European jurisdictions. See http://www.moodys.com/viewresearchdoc.aspx?docid=PBS_SF265743

30 See “Moody’s Approach to Quantifying Set-off Risk for Securitisation and Covered Bonds Transactions Originated by UK Deposit-Taking Institutions,” May 2012.

16 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

Counterparty Risk

The two major areas of counterparty risk that we compared between the regions are back-up servicer (BUS) risk and swap counterparty risk.

Back-Up Servicer Risk

Compared to Australian and Japanese deals, Dutch and UK deals are more vulnerable to BUS risk following a servicer disruption as they do not have the responsibility of servicing or facilitating a transfer.

Japan

In Japan, the asset trustee is primarily responsible for servicing in accordance with Japan’s Trust Law. Under the deal agreements, the asset trustee delegates the servicing to the servicer. If the servicer needs replacing, then the asset trustee is obligated to service the mortgage portfolio, or look for a substitute servicer. Many Japanese RMBS issued by regional banks have a BUS at closing, though many RMBS issued by the major banks, and those rated in Aa (sf) range, do not.

Australia

Australian deals require the issuing trustee in all deals to perform the BUS function, even for highly rated major banks. Although the trustees act in the capacity of a “cold” back-up and have the option to outsource the servicing to a third party, they are proactive in terms of gaining an understanding of the client’s operations as well as a preliminary understanding of the logistics of stepping into the BUS role.

Increasingly in Australian deals, we are witnessing “warm” BUS arrangements, whereby the trustee conducts a more thorough operational review, identifying key people, bank accounts and service providers, as well as developing a plan by which they can swiftly transfer the BUS role in a distressed scenario. While warm back-up clients tend to be unrated non-banks, a few are rated banks.

The Netherlands

Standard Dutch deals do not identify a BUS at closing. Upon the default of the servicer, the issuer and trustee must facilitate servicer replacement, using their best efforts. When a servicer’s rating does not exceed, or is not equal to A3, the deal typically incorporates BUS replacement triggers and BUS facilitator arrangements.

In a number of deals, a third-party servicer (Stater Nederland N.V. or Quion Groep B.V.) participates in the deal at closing, wherein the servicer sub-contracts out certain services to this third party.

UK

UK RMBS master trust deals are similar to standard Dutch deals in that they do not identify a BUS at closing. Instead, the master trust deals rely on the credit strength of the servicer. The trustees have a legal responsibility to ensure continued servicing of the mortgages.

Some UK RMBS deals also appoint a BUS facilitator at closing, or upon the servicer being rated below A3. The BUS facilitator’s role is to find a replacement servicer, if the need arises, using reasonable efforts.31 In the UK, there is a third-party servicing market with a strong history of transfers.

31 See “The Role of Back-up Servicer Facilitators in European ABS and RMBS Explained,” 20 March 2012.

17 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

Swap Counterparty Risk

Compared to Japanese deals, Australian, Dutch and UK deals have greater counterparty risk because of the presence of entities to hedge swap risks.

Japan

Japanese deals typically have no swap counterparties because (1) interest rate risk does not affect these deals (the deals receive a fixed rate of interest from the mortgages and pay out a lower fixed interest rate to the RMBS notes); or (2) sufficient over-collateralisation to cover negative carry mitigates any potential interest rate risk.

Japanese deals also only issue notes in their domestic currency, thereby removing the need for foreign exchange swap counterparties.

Australia

In Australia, unlike many other mortgage markets charging floating interest rates, the lender does not tie the rate to an index, such as the London Interbank Offered Rate (LIBOR). Instead, the lender sets the floating rate at their sole discretion, and which is referred to as a Discretionary Variable Rate (DVR). This exposes the deal to basis risk because the DVR could be set at a rate lower than that paid to the notes.

To mitigate this basis risk, most RMBS deals carry a basis swap32 to hedge any rate mismatches between the DVR charged on the mortgages and the floating-rate obligations on the notes. If the swap terminates, the lender must set the DVR at a sufficient level to ensure that the deal can pay all the expenses of the deal, including the interest on the notes, when due. We refer to this level as the threshold rate. The lender typically adds an additional 0.20-0.25 percentage points to the threshold rate as a buffer for any enforceable expenses.

The Netherlands

Dutch swaps are valuable to the deal for two reasons. Firstly, they mitigate the interest rate mismatch between the long-term fixed rate received from the underlying mortgages and the floating interest rate due under the notes. Secondly, the swaps typically include a net excess spread, whereby the issuer deducts costs (net of senior expenses and note costs) as well as a guaranteed excess spread (for example, 50 basis points) from the payment made to the swap counterparty, thus providing another level of credit enhancement to the issuer.

Furthermore, in the case of Dutch master trusts,33 swaps also provide liquidity support to the deal. In this type of structure, the swap counterparty will always make its payments to the issuer under the agreement. However, if interest payments from the underlying mortgages are not received from a servicer, the issuer is not obligated to make its payment to the swap counterparty. This less standard feature makes Dutch master trust swaps more difficult to transfer to a third party, if needed.

UK

UK RMBS master trusts contain basis rate swaps at the funding level and foreign exchange swaps at the issuer level.

At the funding level, the swaps convert the revenue received from the trust -- which is a mixture of fixed, BBR-linked and SVR-linked rates -- to LIBOR plus a margin.

At the issuer level, the relevant swap counterparty exchanges non-GBP note amounts from GBP

into the relevant note currency.

33 ABN Amro is the only bank providing RMBS master trusts in the Netherlands.

18 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

IV. Downgrade Drivers

Generally, a shared downgrade driver in Japan, Australia and the Netherlands has been due to how we assess the benefits of a third-party guarantee and LMI. In Australia, downgrades were largely restricted to the junior notes and some mezzanine notes, while in Japan and the Netherlands, many senior notes -- that were rated Aaa (sf) -- have been downgraded.

Japan

Japanese RMBS have recorded some downgrades, mostly due to the downgrades of third parties, such as mortgage guarantors. For example, we have downgraded some RMBS deals guaranteed by Japan Housing Finance Agency (JHF); to Aa2 from Aaa in 2009, and again to Aa3 in 2011.

We only downgraded four deals in 2011 because of poor collateral performance. The RMBS sector in Japan remains stable, reflecting the good performance of collateral mortgage pools.

Australia

In Australia, we have never downgraded a prime or non-conforming deal as a result of poor performance of the underlying mortgages. Most of our downgrades have affected junior notes in prime deals because of mortgage insurer downgrades, or the increased probability that a particular LMI may deny or reduce a claim.34

The Netherlands

Dutch RMBS deals have performed strongly since they first debuted in 1999. This performance is in line with our expectations because the Dutch market has traditionally showed lower delinquency rates than its European peers and continues to do so. We have never downgraded Aaa (sf) notes because of mortgage performance. However, we have downgraded some junior notes as a result of underperformance.

In the past, we downgraded Aaa (sf) Dutch RMBS notes as a result of (1) a change in 2009 in how we assess the benefit of the NHG guarantee;35 and (2) an originator bankruptcy36 in May 2011. This bankruptcy resulted in due care claims, which argued that the originator had (1) originated loans with excessively high LTVs and/or debt to income ratios; and/or (2) sold unnecessary or inappropriately priced insurance products. The bankruptcy trustee compensated borrowers through set-off against their outstanding loan balances.

UK

Over the past 14 years, we have not downgraded any UK RMBS master trust notes. In 2010, however, we downgraded the Whinstone and Whinstone 2 synthetic deals (which reference the Granite Master Trust reserve funds) because their subordinated positions exposed them to higher delinquency levels and low LIBOR rates. We have a stable outlook for UK prime RMBS over the next 12-18 months, and expect the outstanding notes of UK RMBS master trusts to show resilience to any moderate deviation from this outlook.

We released a request for comment in July 2012 in which we requested market feedback on potential changes to our rating implementation guidance for assessing linkage to swap counterparties. If the revised rating implementation guidance is implemented as proposed, the ratings on certain notes may be negatively affected; following a counterparty default, any shortfall may be fully borne by the affected note, as opposed to being shared across all the notes of a given class.37

34 See “Approach for Evaluating Lender’s Mortgage Insurance in Australian RMBS,” 19 October 2012. 35 See “Moody’s Updated Approach to NHG Mortgages in Rating Dutch RMBS,” 17 March 2009. 36 See “Moody’s Downgrades Dutch ABS/RMBS Chapel and Monastery Originated by DSB,” 31 May 2011. 37 See "Approach to Assessing Linkage to Swap Counterparties in Structured Finance Cashflow Transactions: Request for Comment," 2 July 2012 and “Structural

Differences Can Raise UK RMBS Master Trust Exposure to FX Swap Counterparties,” 18 October 2012.

19 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

Appendix A

UK Master Trusts

We have included this appendix to explain UK RMBS master trust structures as they are more complex than the standalone RMBS seen in other markets.

Dynamic master trusts: UK RMBS master trusts differ from standalone securitisation structures as notes issued at different times share the same mortgage pool.

The seller is able to add new mortgages to the trust and may do so in order to issue new notes, or to maintain the minimum trust size, or minimum seller share.

Trust beneficiaries: The mortgage trustee acquires mortgages38 from the seller and, without segregating them in any way (for example, by date of sale), holds them for the benefit of the funding companies and seller. The issuer has exposure to the mortgages via the intercompany loan. The issuer uses the interest and principal received by a funding company -- as a result of its share in the trust -- to service the intercompany loan and, in turn, to pay the interest and principal due on the notes.

The seller of the mortgages retains an interest in the portfolio as it is a beneficiary to the trust via the seller share.

The seller and the funding companies are separate beneficiaries to the mortgages in proportion to the size of their shares and do not have any rights or obligations to each other.

EXHIBIT 7

Typical RMBS Structure – UK

38 Trust property also includes capitalised interest, rights under insurance properties, and cash held due to payments by borrowers.

Seller Trust

Property

Series 1

Class A Class B Class C

Transfer of loans

Funding

Issuer

Seller share

Funding Share

Servicer

Contribution

Principal and interest on intercompany loan

Subscription proceeds

Series 2

Class A Class B Class C

Principal and interest on the notes Principal and interest

on intercompany loan

Note issue proceeds

Basis rate hedging and reserve fund

FX hedging

20 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

Fluctuation of shares in the trust property: The Funding 1 share, Funding 2 share (if applicable) and the seller share of the trust property will fluctuate, depending on a number of factors, including:

» the allocation of principal receipts on the mortgages to funding companies and the seller

» losses arising on the mortgages

» the assignment of any new mortgages

» the acquisition by funding companies of part of the seller share due to a new issuance

» underpayments, payment holidays or flexible drawings by borrowers on their mortgages

EXHIBIT 8

Trust Structure

Cash flow and loss allocation: The cash manager allocates revenue receipts between the beneficiaries in proportion to their shares. However, the cash manager allocates the principal to funding, as opposed to the seller, if there are note repayment or accumulation requirements. In addition, if there is a non-asset trigger breach -- due to, for example, seller insolvency, or minimum seller share or trust size not being met -- then all notes will become due and payable. In this situation, the seller will not receive any cash until there is either an asset trigger breach (that is, there is a balance on the Class A PDL), or the funding share has been repaid. If an asset trigger breach occurs, the cash manager allocates the principal receipts pro rata between funding and the seller.

The cash manager allocates the losses on the sale of repossessed properties between the seller and funding on a pro-rata basis at the time the trust realises the losses. In the case where the seller share pays down in advance of the funding share because notes are not due and payable, then the cash manager will allocate more losses to funding. If, however, the issued notes are short-dated or become so, as a result of the trust breaching a non-asset trigger, then funding will pay down in priority to the seller, meaning that the seller will in effect act as credit enhancement to the deal.

Waterfalls and Loss Allocation

The cash manager allocates funds at three levels:

1. At the trust level, to distribute principal and interest between the seller and funding

2. At the funding level, to distribute interest and principal to the different tranches of intercompany loans

3. At the issuer level, to make interest and principal payments on the notes

At the trust level, the cash manager always allocates revenue receipts pro rata between the seller and funding

Class A

Class B

Class C

Mortgage

Portfolio

Seller Share (GBP30)

Funding Share (GBP70)

(GBP100)

21 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

At the trust level, the cash manager allocates principal receipts as follows:

» If there is no trigger breach: the cash manager first allocates principal receipts to funding, if notes are either within a cash accumulation period, or due and payable. The cash manager allocates any excess to the seller

» If there is a non-asset trigger event breach, but no asset trigger breach: the cash manager allocates all principal receipts to funding

» If there is an asset trigger breach: The cash manager allocates principal receipts pro rata between funding and the seller

At the funding level, the cash manager, on behalf of funding, uses revenue receipts to pay senior fees, and then pay the debt-servicing costs, and clear the PDLs in order of note class. The interest payable on any unrated Z notes issued ranks below the reserve fund.39

At the funding level, the cash manger, on behalf of funding, uses principal receipts to repay different tranches of intercompany loans, taking into account any activated deferral triggers (for example, the level of arrears, reserve fund draws, low payment rates, or notes being past their step-up date).

If a note is in an accumulation period, but not yet due, cash may remain trapped at the funding level for payment at a later period.

At the issuer level, the cash manager, on behalf of the issuer, uses the revenue and principal amounts deployed to make payments on the funding intercompany mortgage tranches to make the required note payments.

If the tranches are non-GBP denominated, the cash manager, on behalf of the issuer, makes payments to swap counterparties instead. The cash manager, on behalf of the issuer, will then use the money received from the relevant swap counterparties to pay the noteholders.

Capitalist versus socialist structures: In a capitalist trust, not all the notes of the same class will share the same PDL, whereas in a socialist trust, all the notes of the same class will share a PDL. A trust may be capitalist as it has more than one funding vehicle, or because it has one funding vehicle with different issuers each having separate PDLs. In a capitalist structure, therefore, notes from a given class in one part of the structure may have more enhancement than the same class in another. In a socialist structure, however, and at a given time, notes from the same class will have the same levels of subordination.

In a socialist trust, different notes from the same class could still experience different losses owing to the presence of time subordination.

Similarly, it is also possible that the cash manager, on behalf of the issuer, can repay a more subordinate note from one series before a more senior note from a note with a later maturity. If performance deteriorates, triggers and payment tests protect the senior notes.

For trusts with more than one funding vehicle, the cash manager allocates revenue proportionally between the funding vehicles. However, for trusts with separate PDLs within one funding company, the cash manager allocates revenue on a pro-rata basis, taking into account the intercompany mortgage balance less the PDL. In case of a shortfall, the cash manager also allocates losses and principal on a pro-rata basis.

39 Funding usually holds the reserve fund on behalf of the issuer. This action is in line with the PDL’s position,

which is also at the funding level. The cash is in a GIC (guaranteed investment contract), in line with our criteria which requires it to be held at a P-1 rated institution.

22 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

EXHIBIT 9

Capitalist Master Trust Structure

The cash manager allocates losses on a pro-rata basis between tranches of the same class that share the same PDL, regardless of when the issuer issued them. Furthermore, notes sharing the same PDL will share credit enhancement features, such as excess spread, reserve fund and subordination.

The cash manager records losses against a PDL for the amount of the loss realised following the sale of the property backing the mortgage. A principal deficiency sub-ledger corresponds to each class of notes.

EXHIBIT 9

Programme Origination Type

Aire Valley Bradford & Bingley Socialist

Arkle Lloyds Socialist

Fosse Alliance & Leicester / Santander UK Socialist

Gracechurch Barclays Socialist

Granite Northern Rock Asset Management Capitalist

Holmes Abbey / Santander UK Socialist

Lanark Clydesdale Bank Socialist

Langton Santander UK Capitalist

Lannraig Clydesdale Bank Socialist

Permanent Bank of Scotland Socialist

Silverstone Nationwide Socialist

Role of the seller share: The seller does not issue a note. Instead, the seller simply owns part of the trust (the seller share).

The seller share covers risks unrelated to mortgage performance (such as, set-off risk relating to both deposits and the loss of flexible amounts following originator insolvency). Additionally, the mortgage trustee can set off any losses arising from the seller’s failure to meet its obligations in terms of representations and warranties from the seller share.

SPV - Series 1(2009)

Class A

Class B

Class C

SPV - Series 2(2010)

Class A

Class B

Class C

SPV - Series 3(2011)

Class A

Class B

Class C

SPV (Issuer)

Principal & Interest.

Excess funds

Reserve Account

Excess Spread

Reserve Account

Excess Spread

Reserve Account

Excess Spread

23 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

An additional benefit of the seller share is that it allows the trust to accumulate funds faster, therefore reducing the extension risk for bullet and scheduled amortisation notes.

The minimum seller share ranges from 5% to15%, depending on the level of flexible mortgages and the set-off risk from retail deposits in the trust. This percentage compares with an average seller share of 30% in UK RMBS.

However, the presence of a large seller share will reduce the amount of unencumbered assets; as such, it will be set after taking into account the overall funding strategy.

RESIDENTIAL MBS

24 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

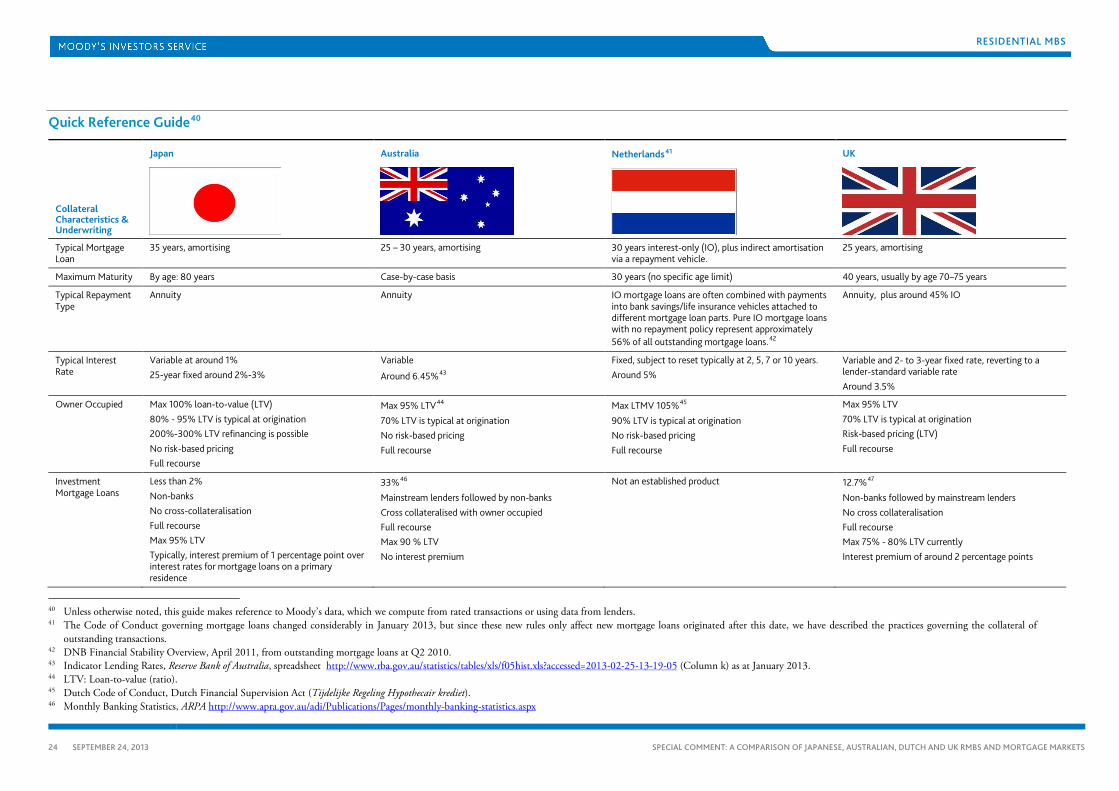

Quick Reference Guide40

Collateral Characteristics & Underwriting

Japan

Australia

Netherlands41

UK

Typical Mortgage Loan

35 years, amortising 25 – 30 years, amortising 30 years interest-only (IO), plus indirect amortisation via a repayment vehicle.

25 years, amortising

Maximum Maturity By age: 80 years Case-by-case basis 30 years (no specific age limit) 40 years, usually by age 70–75 years

Typical Repayment Type

Annuity Annuity IO mortgage loans are often combined with payments into bank savings/life insurance vehicles attached to different mortgage loan parts. Pure IO mortgage loans with no repayment policy represent approximately 56% of all outstanding mortgage loans.42

Annuity, plus around 45% IO

Typical Interest Rate

Variable at around 1% 25-year fixed around 2%-3%

Variable

Around 6.45%43

Fixed, subject to reset typically at 2, 5, 7 or 10 years. Around 5%

Variable and 2- to 3-year fixed rate, reverting to a lender-standard variable rate Around 3.5%

Owner Occupied Max 100% loan-to-value (LTV) 80% - 95% LTV is typical at origination 200%-300% LTV refinancing is possible No risk-based pricing Full recourse

Max 95% LTV44

70% LTV is typical at origination No risk-based pricing Full recourse

Max LTMV 105%45

90% LTV is typical at origination No risk-based pricing Full recourse

Max 95% LTV 70% LTV is typical at origination Risk-based pricing (LTV) Full recourse

Investment Mortgage Loans

Less than 2% Non-banks No cross-collateralisation Full recourse Max 95% LTV Typically, interest premium of 1 percentage point over interest rates for mortgage loans on a primary residence

33%46 Mainstream lenders followed by non-banks Cross collateralised with owner occupied Full recourse Max 90 % LTV No interest premium

Not an established product 12.7%47

Non-banks followed by mainstream lenders No cross collateralisation Full recourse Max 75% - 80% LTV currently Interest premium of around 2 percentage points

40 Unless otherwise noted, this guide makes reference to Moody’s data, which we compute from rated transactions or using data from lenders. 41 The Code of Conduct governing mortgage loans changed considerably in January 2013, but since these new rules only affect new mortgage loans originated after this date, we have described the practices governing the collateral of

outstanding transactions. 42 DNB Financial Stability Overview, April 2011, from outstanding mortgage loans at Q2 2010. 43 Indicator Lending Rates, Reserve Bank of Australia, spreadsheet http://www.rba.gov.au/statistics/tables/xls/f05hist.xls?accessed=2013-02-25-13-19-05 (Column k) as at January 2013. 44 LTV: Loan-to-value (ratio). 45 Dutch Code of Conduct, Dutch Financial Supervision Act (Tijdelijke Regeling Hypothecair krediet). 46 Monthly Banking Statistics, ARPA http://www.apra.gov.au/adi/Publications/Pages/monthly-banking-statistics.aspx

RESIDENTIAL MBS

25 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

Collateral Characteristics & Underwriting

Japan

Australia

Netherlands

UK

Redraws No Common feature

Not subject to updated credit checks Not common Less common than before credit crunch

Available subject to passing updated credit checks

Foreclosure Time (from first missed payment)

6-18 months after default 9-12 months 6-12 months 12 months

Serviceability Measure

Debt-to-income ratio less than 35% to 45% Net service ratio (NSR) >1 NSR = (Net Income – Living Expenses) / Total Outgoings

4x-5x income multiple 25%-35% debt to income

Income multiples <4 Debt-to-income thresholds depending on lender and credit scorecard

Interest Rate Stress Around 4% Standard variable rate: +1.5-2 percentage points 5.0% 48 Around 6% -7%

Credit Bureau Information

Positive and negative information retained Only negative information retained Positive and negative information retained Positive and negative information retained

Key Lending Regulations

Money-Lending Business Control and Regulation Law, 2009

National Consumer Credit Protection (NCCP) 1996 National Instituut voor Budgetvoorlichting (NIBUD): Code of Conduct for lenders, Stichting Autoriteit Financiële Markten (AFM)

Mortgages and Home Finance: Conduct of Business Sourcebook (MCOB), FSA 2007

Market Share of New Lending

Three Mega Banks (around 19%)

Mega Banks Market Share49 Bank of Tokyo-Mitsubishi UFJ (Aa3) 7.2% Sumitomo Mitsui Banking (Aa3) 6.3% Mizuho Bank (A1) 5.7% (Market share of outstanding mortgage amounts) Some US securities firms exited around 2008

Big 4 (around 85%)

Lender Market Share50 CBA (Aa2) 27.4% WBC (Aa2) 25.7% NAB (Aa2) 16.8% ANZ (Aa2) 15.3%.

Top 3 (around 80%)

Lender Market Share51

Rabobank Nederland (Aa2) 33% ABN AMRO Bank N.V. (A2) 25% ING Bank N.V. (A2) 22%

Top 6 (80.7%)

Lender Market Share52 Lloyds Banking Group (A3) 19.9% Santander (A2) 16.8% Barclays (A2) 12.1% Nationwide BS(A2) 12.1% Royal Bank of Scotland (A3, RUR53) 10.4% HSBC Bank (Aa3) 9.4%

Broker Originations 0% About 40%54 About 40%55 50%

47 FSA Q2 2012. 48 Dutch Banking Association, www.nvb.nl 49 Bank Financial Statements, Japan Housing Finance Agency. 50 Monthly Banking Statistics, APRA, issued 31 January 2013. 51 See Moody’s Banking System Outlook - The Netherlands, 11 December 2012 52 Market share as at 2011. 53 RUR: ratings under review.

RESIDENTIAL MBS

26 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

Lenders’ Mortgage Insurance (LMI), Guarantor and National Mortgage Guarantee (NHG)

Japan

Australia

Netherlands

UK

LMI or Guarantor Guarantees widely used LMI widely used NHG guarantee widely used

NHG origination is approximately 23%56 of the total debt

No significant use of LMI

Premium Based on mortgage amounts outstanding Monthly instalments or upfront lump sum

Based on LTV and mortgage amount Upfront lump sum

Borrower pays 0.85%57 of total mortgage upfront to the guarantor

N/A

Providers Bank subsidiary Typically not rated by any rating agencies

Two independent mono-lines Rated (A2) and (A3), respectively

One government entity Homeownership Guarantee Fund (known as Stichting Waarborgfonds Eigen Woningen (WEW) Rated (Aaa)

N/A

Possibility of Claim Reductions

No Yes Yes. However, provisions in the deal documentation require the seller to repurchase loans, if NHG criteria are not met.

N/A

Credit Implications We consider the mortgage guarantee in our rating analysis. However, the structure of many deals provides sufficient unrated junior note subordination for the senior notes to obtain Aaa (sf)-rated credit quality without any benefit from the guarantee.

Senior notes require less subordination to obtain a Aaa (sf) rating. If the deal has structured credit protection, in addition to non-retainable excess spread, the rating of the junior note will correspond to the Insurance Financial Strength (IFSR) of the lowest-rated mortgage insurer in the deal. Otherwise, we are likely to rate the junior note between Ba1 (sf) and B3 (sf), depending on collateral quality and the mortgage insurer’s likely claim reductions.58

Less subordination Our analysis incorporates (1) the mismatch between the annuity amortisation of the guarantee and the actual amortisation of the loan; and (2) the rescission rate (in case there is no full payout by Stichting Waarborgfonds Eigen Woningen (WEW)).

N/A

54 Broker loans accounted for 42% of total mortgage loans originated during the first quarter of 2012. See Mortgage Brokers Continue to Grow – Lifting Market Share and Volume, Mortgage & Finance Association of Australia, 16 May

2012 http://www.mfaa.com.au/default.asp?artid=2848 55 AFM Consumentenmonitor, June 2012. 56 Approximation ultimo 2012, based on total NHG loans (EUR154.1 billion) and total mortgage debt (EUR672.3 billion) (sources: NHG, CBS). 57 As per January 2013 (source: NHG). 58 See Approach for Evaluating Lender’s Mortgage Insurance in Australian RMBS, 19 October 2012.

RESIDENTIAL MBS

27 SEPTEMBER 24, 2013 SPECIAL COMMENT: A COMPARISON OF JAPANESE, AUSTRALIAN, DUTCH AND UK RMBS AND MORTGAGE MARKETS

RESIDENTIAL MBS

Housing

Japan

Australia

Netherlands

UK

House Prices Declining Prices

Residential land prices in Japan rose dramatically in the late 1980s (during the bubble era), before plunging in the early 1990s. Prices have since declined consistently over a prolonged period.

The current index level is the same as in the early 1980s.

Lenders originated the majority of residential mortgage loans backing Japanese RMBS after 2000, when land prices had fallen to low levels after peaking in 1990.

Steady Prices

House prices remain steady, with the current housing shortage supporting prices.

Low unemployment and interest rate cuts by the Reserve Bank of Australia will also support prices.

The recent slowdown in prices and the lower borrowing costs have improved affordability (RP-Data Rismark’s house price-to-income ratio is at its lowest level since March 2003).

Declining Prices

House prices in the Netherlands have been on a downward trend since mid-2008. However we expect them to stabalise over the next 12 months.

According to the Nederlandse Vereniging van Makelaars (NVM) index, the current peak-to-trough decline is approximately 22%.59

Stabilising

UK house prices have started to increase after being flat for the past couple of years. We are expecting to see further increases over the next 12 to 18 months.

While weak demand will weigh on property prices, tight supply will prevent any sustained fall in prices.

Demand will remain weak as households face a number of pressures, including continued job insecurity, squeezed finances and tight credit conditions.

Housing Bubbles 1990

Land prices rose dramatically during the “bubble economy” of the late 1980s. When the bubble burst, prices plunged and have continued to decline to the present.

Current prices are at the same level as in the early 1980s.

The value of a new home declines sharply right after the first purchase, as buyers prefer to buy brand new properties rather than second-hand ones.

2003-04

Australia’s housing market boom (2001–04) ended three years before the global credit crisis, giving the market time to adjust.

Australian policymakers made a deliberate effort to deflate the housing boom through monetary policy tightening, which resulted in a soft landing.

When the 2007 crisis hit, house prices held up well because policymakers lowered interest rates.

2007

House prices in the Netherlands grew strongly in the 1995-2007 period, as economic conditions and debt availability improved.

Since the start of the financial crisis, house prices have declined by approximately 22%.60

2007

House prices grew strongly in the 2000–2007 period, reflecting strong economic conditions and easy access to credit, with prices rising by an average of 12.3% on an annualised basis.61

Prices fell by around 20% between Q3 2007 and Q1 2009, but have since recovered slightly, rising by an average 2.0% annually since the trough in Q1 2009, as a result of tight supply and low interest rates.

59 Nederlandse Vereniging voor Makelaars (NVM), Q2 2013. 60 NVM. 61 As computed by Moody’s from the Lloyds Banking Group and Nationwide house prices indices.

RESIDENTIAL MBS