Embed Size (px)

Citation preview

A LOOK AT THE FINANCIAL STATEMENTSFINANCIAL STATEMENTS – HOW THEY RELATE TO EACH OTHER AND FINANCIAL STATEMENT ANALYSIS

Edward B. Peacock, CPA

214 356 [email protected]

Topics• Levels of Financial Statements

▫Example Statements (see handouts)▫Government-wide statements▫Fund level statements▫Statistical Section

• Financial Analysis – process of drawing meaning from financial statements▫ Identifying Available Resources

GAAP basis Budgetary basis

General fund Proprietary funds

• Ratio Analysis

Edward B. Peacock, CPA

Edward B. Peacock, CPA

Levels of Financial Statements

•Government-wide financial statements▫Measurement focus – economic resources▫Basis of accounting - accrual basis▫Statement of Net Assets – p11 - reports what

the government owns and owes at the end of the fiscal year Two columns - governmental activities and

business-type activities – side by side comparison

▫Statement of Activities - p12-13 – reports financial results during a fiscal year

Edward B. Peacock, CPA

Levels of Financial Statements

•Fund level financial statements, p14-24▫Governmental funds, p14-15

Modified accrual basis Current assets and current liabilities

Reconciliations of modified accrual to full accrual basis, p16, p19

▫Proprietary funds, W&S, Golf Full accrual basis

Current assets and current liabilities are identified in the fund level SNA, p11, p20

Edward B. Peacock, CPA

Levels of Financial Statements•Statistical Section

▫Typically presents information for the most recent 10 years

▫Usually is not audited▫Contains tables of trends – help you understand

how your gov’t’s finances have changed over time Financial Revenue capacity Debt capacity Demographic and economic information Operating information

Edward B. Peacock, CPA

Identifying Available Resources•Government-wide Statements

▫Restricted versus unrestricted net assets, p11•Fund level statements

▫Governmental funds Fund balance, p14

▫Proprietary funds Unrestricted net assets, p11, p21 Working capital (current assets less current

liabilities) Frequently used in rate analysis

Cash basis, p23

Edward B. Peacock, CPA

Restricted and Unrestricted Net Assets•Capital assets net of related debt, p11

▫Cannot readily be sold and converted into cash

•Restricted net assets▫External restrictions on how resources may

be used•Unrestricted net assets

▫Resources that don’t fall into the first two categories

▫Not necessarily liquid

Edward B. Peacock, CPA

Fund Level Resources•Governmental Funds, p14

▫Nonspendable – not a liquid resource▫Restricted – externally restricted for a specific

purpose Special revenue funds Capital projects funds Debt service funds

▫Committed – appropriated by governing body▫Assigned fund balance – can be unassigned▫Unassigned – can be used as beginning

resource in the budget

Edward B. Peacock, CPA

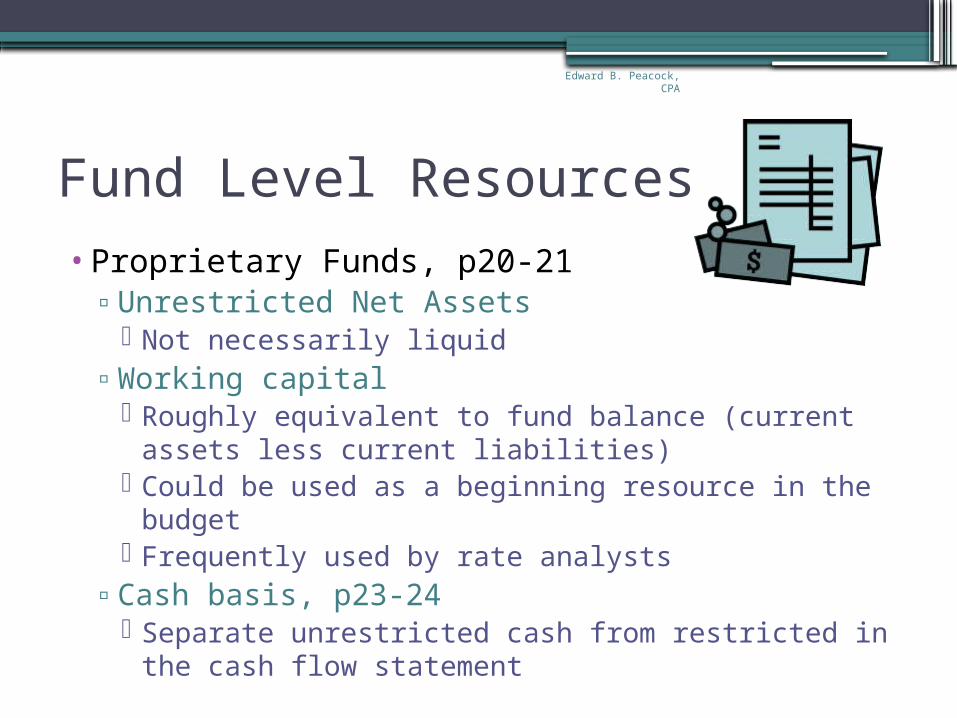

Fund Level Resources•Proprietary Funds, p20-21

▫Unrestricted Net Assets Not necessarily liquid

▫Working capital Roughly equivalent to fund balance (current assets

less current liabilities) Could be used as a beginning resource in the

budget Frequently used by rate analysts

▫Cash basis, p23-24 Separate unrestricted cash from restricted in the

cash flow statement

Edward B. Peacock, CPA

General Fund - Unassigned Fund Balance Measures

2011 2012

Unassigned Fund Balance, p14 $8,938,129 $11,741,652

Total Expenditures and Other Financing Sources and Uses, p17

$46,735,773 $44,836,091

Unassigned Fund Balance as a % of Total Expenditures and Other Financing Sources and Uses

19% 26%

Total Expenditures and Other Financing Sources and Uses (Per Day)

$128,043 $122,839

Unassigned Fund Balance # of Days of Operations

70 81

Edward B. Peacock, CPA

Working Capital - Proprietary Funds

•A short term measure of the funds’ ability to meet the obligations that will come due over the next year

•Current assets less current liabilities•A more stringent approach – compare

only the most liquid assets, generally unrestricted cash and cash equivalents to current liabilities

Edward B. Peacock, CPA

Proprietary Funds – Working Capital

FY 2011 Water and Sewer

FY 2011Golf

FY 2012Water and Sewer

FY 2012Golf

Current Assets, p20

SNA $15,980,106

$94,032 $15,987,055

$81,224

Less: Current Liabilities, p21

SNA $5,060,044 $1,447,670

$5,328,831 $1,401,595

Working Capital

$10,920,062

-$1,353,638

$10,658,224

-$1,320,371

Edward B. Peacock, CPA

Proprietary Funds Expenditures – Budgetary Basis

FY 2011 Water and Sewer

FY 2011Golf

FY 2012Water and Sewer

FY 2012Golf

Operating Expenses, p22

SREV 18,490,100

2,937,825 17,948,243

2,941,753

Less: Depreciation, p22

SREV -2,464,771 -403,024 -2,529,720 -402,428

Add: Transfers, p22 SREV 1,501,990 199,141 1,444,541 232,120

Add: Debt Principal, p23

SCF 1,470,000 285,000 1,540,000 295,000

Add: Interest, p23 SCF 501,768 126,867 274,208 119,525

Total Expenditures 19,499,087

3,145,809 18,677,292

3,185,970

Expenditures per Day 53,422 8,619 51,171 8,729

Edward B. Peacock, CPA

Proprietary Funds – Working Capital Measures

FY 2011 Water and Sewer

FY 2011Golf

FY 2012Water and Sewer

FY 2012Golf

Total Expenditures (Budgetary Basis)

19,499,087

3,145,809 18,677,292

3,185,970

Expenditures per Day

53,422 8,619 51,171 8,729

Working Capital 10,920,062

-1,353,638

10,658,224

-1,320,371

Working Capital as % of Total Expenditures

56% -43% 57% -41%

Number of Days Working Capital

204 -157 208 -151

Edward B. Peacock, CPA

Proprietary Funds – Unrestricted Cash

2012 W&S 2012 GOLF

Current assets: Cash and cash equivalents

SNA

$13,299,600

$0

Noncurrent assets:Restricted cash and investments

SNA

$11,844,580

$220,320

Cash and cash equivalents, ending

SCF $25,144,180

$220,320

Edward B. Peacock, CPA

Ratio Analysis•The act of converting the numbers in the FS into

a form which specific decisions can be based•Are created by dividing one number into another•Financial story is not told with a single ratio, but

with an accumulation of ratios and other information

• If presented ratio information, be careful to ask how it was calculated

•Always specify the components of the ratios used in your analyses

Edward B. Peacock, CPA

Ratio Analysis

•To give meaningful financial ratios, always place your ratios in context, i.e.,▫Compare to PY – improving, declining,

holding steady?▫Compare to other similar governments –

higher, lower, roughly the same?▫Is there a commonly accepted benchmark?

Edward B. Peacock, CPA

Types of Ratios• Common-Size Ratios

▫$ Dollar Change▫% Percentage Change

• Short Term Focus – Liquidity▫Current Ratio▫Quick Ratio

• Long Term Focus – Solvency▫Debt to Assets Ratio▫Debt to Net Assets▫Coverage Ratios

Interest Coverage Debt Service Coverage

Edward B. Peacock, CPA

Common-Size Ratios

•Serve two valuable purposes▫Provide quick overview of finances▫How they’ve changed since prior year▫Can be applied to any kind of FS

information Percentage change – shows magnitude of

change Percentage distribution – shows portion of

the total represented by individual elements

Edward B. Peacock, CPA

Dollar Amount and Percentage Change

2011 2012 $ Change % Change

Capital Assets

SNA

254,274,206

250,588,786

-3,685,420

-1.45%

Receivables

SNA

15,865,895 17,326,709 1,460,814 9.21%

Edward B. Peacock, CPA

Percentage Distribution2011 2012

Capital Assets

SNA

254,274,206, 63.53%

250,588,786, 61.16%

Receivables

SNA

15,865,895, 3.96% 17,326,709, 4.23%

Edward B. Peacock, CPA

Liquidity Ratios

•Concerned with the ability to pay immediate obligations

•Current ratio▫Current assets / current liabilities

•Quick ratio▫Cash and cash equivalents / current

liabilities

Edward B. Peacock, CPA

Current and Quick RatiosFY 2011 Water and Sewer

FY 2011Golf

FY 2012Water and Sewer

FY 2012Golf

Current Assets

SNA

15,980,106 94,032 15,987,055 81,224

Cash and Investments

SNA

13,036,960 0 13,299,600 0

Current Liabilities

SNA

5,060,044 1,447,670 5,328,831 1,401,595

CURRENT RATIO

3.16 .06 3.00 .06

QUICK RATIO

2.58 0.00 2.50 0.00

Edward B. Peacock, CPA

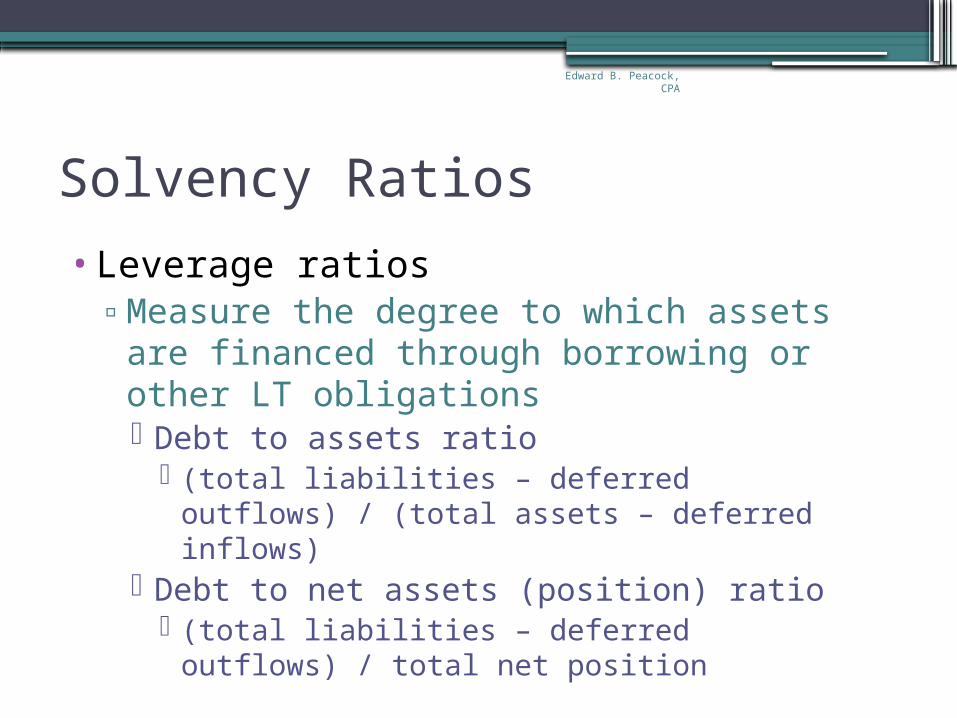

Solvency Ratios

•Leverage ratios▫Measure the degree to which assets are

financed through borrowing or other LT obligations Debt to assets ratio

(total liabilities – deferred outflows) / (total assets – deferred inflows)

Debt to net assets (position) ratio (total liabilities – deferred outflows) / total net

position

Edward B. Peacock, CPA

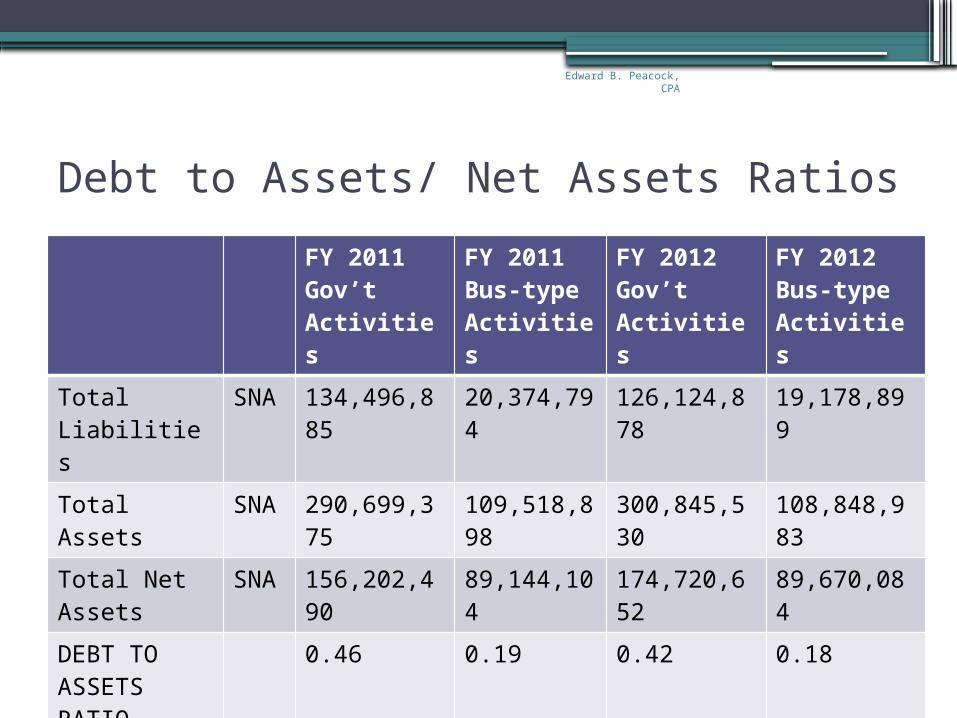

Debt to Assets/ Net Assets RatiosFY 2011 Gov’t Activities

FY 2011 Bus-type Activities

FY 2012Gov’t Activities

FY 2012Bus-type Activities

Total Liabilities

SNA

134,496,885

20,374,794

126,124,878

19,178,899

Total Assets SNA

290,699,375

109,518,898

300,845,530

108,848,983

Total Net Assets

SNA

156,202,490

89,144,104

174,720,652

89,670,084

DEBT TO ASSETS RATIO

0.46 0.19 0.42 0.18

DEBT TO NET ASSETS RATIO

0.86 0.23 0.72 0.21

Edward B. Peacock, CPA

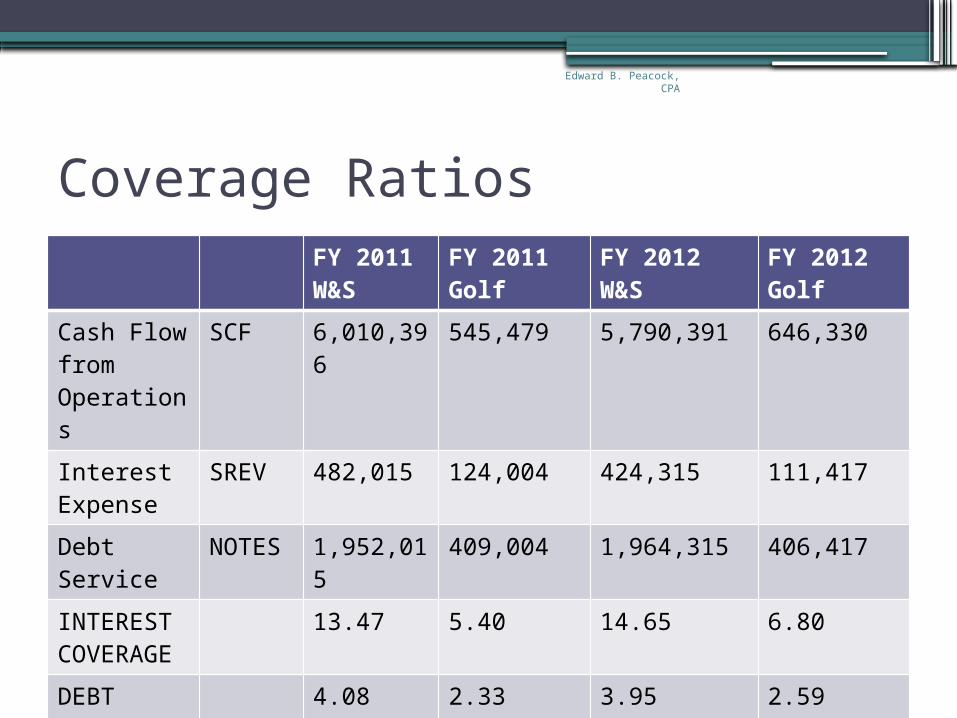

Coverage Ratios

•Compare available resources with resource needs▫Interest coverage

Cash flow from operations + interest expense / interest expense

▫Debt service coverage Cash flow from operations + debt service /

debt service

Edward B. Peacock, CPA

Coverage RatiosFY 2011 W&S

FY 2011Golf

FY 2012W&S

FY 2012Golf

Cash Flow from Operations

SCF 6,010,396

545,479 5,790,391 646,330

Interest Expense

SREV 482,015 124,004 424,315 111,417

Debt Service

NOTES

1,952,015

409,004 1,964,315 406,417

INTEREST COVERAGE

13.47 5.40 14.65 6.80

DEBT SERVICE COVERAGE

4.08 2.33 3.95 2.59

Edward B. Peacock, CPA

Summary AnalysisGeneral Fund W&S Golf

2011 2012 2011 2012 2011 2012

FB, WC %

19% 26% 56% 57% -43% -41%

# Days 70 81 204 208 -157 -151

Current Ratio

3.16 3.00 .06 .06

Quick Ratio

2.58 2.50 0 0

Interest Coverage

13.47 14.65 5.4 6.8

Debt Svc Coverage

4.08 3.95 2.33 2.59

Questions?

Eddie Peacock

Edward B. Peacock, CPA214 356 [email protected]://www.EBPeacockCPA.com

Edward B. Peacock, CPA