Embed Size (px)

Citation preview

A Presentation to Entrepreneurial CA Luncheon

November 25th, 2008

Financial Market Seizure. • Securitization market: This market is CLOSED

• 85% of mortgages were funded through the securitization market in the better part of this decade. The seizure of this market has also severely impacted liquidity in credit card markets, student loans, corporate finance amongst others

• Next problem area is basic bank ‘on balance sheet’ lending. • First time EVER you’re going to see an overall contraction in the mortgage

lending in the United States

The Ring of Fire:

• Self Reinforcing (downward) Spiral: rating agencies, and their downgrades of various securities, various corporate debts that (then) require additional capital for the banks to post, which triggers more downgrades etc.

Next to Go: • A major corporate failure will (probably) trigger a seizure in the

Credit Default Swap market

• Many state and local governments in the US participated in the mortgage market, and now their feeling the pinch = about 12% of US GDP.

• Credit cards, two trillion dollars in liquidity is being taken away from consumers – this is literally going to be ripped out of their wallets. (credit card lines will be reduced by this amount)

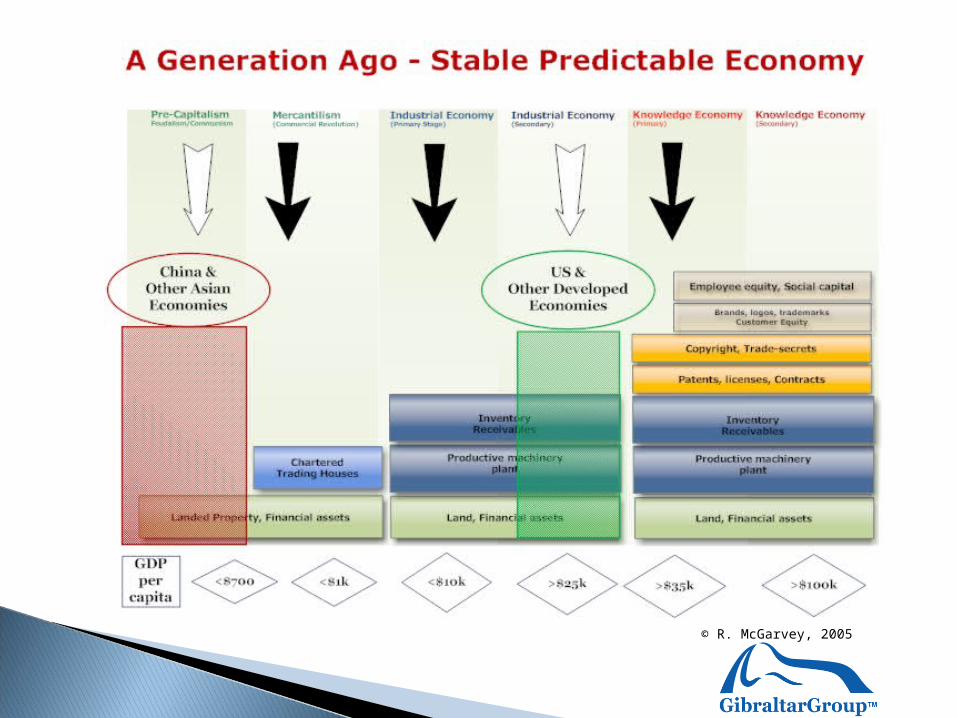

New Engines of Growth in the global economy

Source: Brookings Institute

Declining Industry◦ Between 1995 and 2005 the world’s 20 largest economies lost

approximately 25 million industrial jobs.

Continued Growth◦ Nevertheless, despite the shrinking of their industrial work

forces, the output in these countries as a measure of GDP increased by over 50%.

Intangibles Dominate◦ Today, in the United States and other Western economies in

particular, market services have displaced industrial production as the primary engine of growth; studies suggest that ‘intangible’ assets are now contributing over three-quarters of U.S. GDP.

© R. McGarvey, 2005

IASB: “an asset is a resource that is controlled by the enterprise as a result of past events (for example, purchase or self-creation) and from which future economic benefits (inflows of cash or other assets) are expected.”

Role of Assets #1, Source of Earnings◦ An asset Traditional or Non-traditional must be a causal

agent for earnings or their equivalent.

Role of Assets #2, Repository of Accumulated Value◦ Asset quality is a critical factor in its ability to store and

maintain value (degree of asset permeability)

© R. McGarvey, 2007

© R. McGarvey, 2005

© R. McGarvey, 2005

Stage 1: New Assets Start Generating New Wealth Spice Merchants in Venice, New Ford Assembly Lines

Stage 2: Management Rush to Earnings The engines of growth are embraced EAGERLY

Stage 3: Over Stretch Over commitment by business – unidentified risks Monetary Over Stretch – Expanding money/credit supply Fiscal Over Stretch – consumers/business/governments

Stage 4: Bubbles Burst: Stock Market Correct The Sky is Falling etc.

Stage 5: Recession Reform of institutions and behavior Focus on ‘Preservation’ of capital

Stage 6: Rebirth New legal, securities regulations, GAAP, etc – Have our Cake and

Eat it Too.

Prepare for less tax oriented more asset management practices

Prediction: within 20 years INCOME TAX will be gone, replaced by a combination of:

Consumption taxes (GST, VAT etc.) Government/industry , royalty –like revenue streams.

Role of Accountants #1, Identifying, Evaluating and Measuring Corporate Value

A solid traditional accounting role returns. Strengthening Balance Sheets (i.e. Management Statements )

rather than minimizing them for Tax Purposes. Role of Accountants #2, Bridge to Finance

Banks et al are going to need support if they are to adequately capitalize the new economy, accountants have a VITAL role to play

Customer Equity: A Corporate Asset?